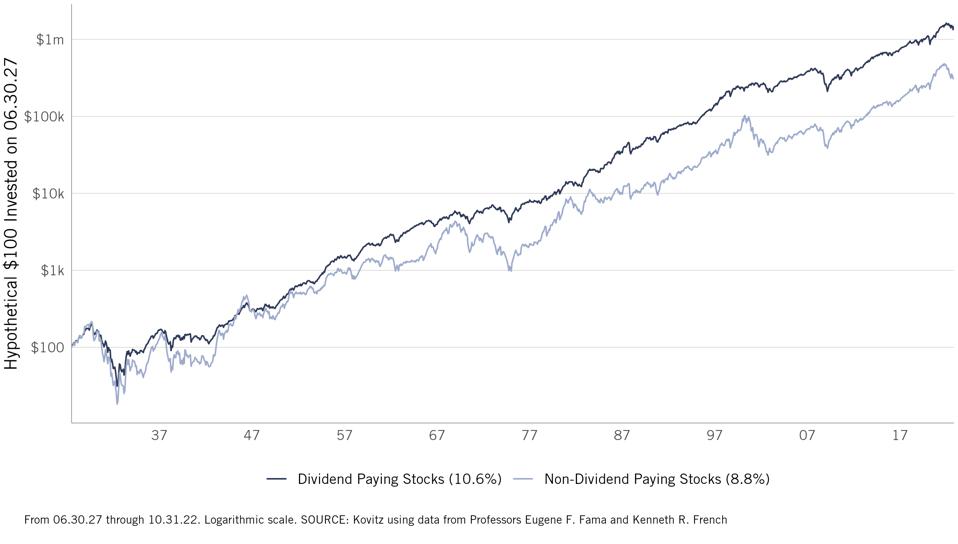

Oil titan John D. Rockefeller once quipped, “Do you know the only thing that gives me pleasure? It’s to see my dividends coming in.” While paying a dividend is not a hard criterion for every stock included in the portfolios my team and I manage at The Prudent Speculator, I continue to find significant appeal in dividend-paying equities.

The rise in yields from fixed income investments have made these instruments far more interesting than they have been in years. Of course, this is offset by the threat of eroding purchasing power from sustained inflation.

While dividends are never guaranteed, Corporate America’s history of rising payouts suggest this slice of the equity market can help investors dampen the impacts from inflation. In addition, the income investors receive in periods of market turbulence should help folks worry less about price fluctuations.

While neither stocks nor bonds have been immune from volatility in the current year, and as we mentioned in our most recent post: Investing In A Higher Interest Rate Environment, students of market history likely understand that about the only conclusion we can draw about rising interest rates is that they are a headwind for bonds.

DIVIDEND HIKERS

Notably, the S&P 500 Dividend Aristocrats Index (which includes the stocks of companies that have paid and increased their annual dividends for at least 50 consecutive years) has been a leading performer in the current year, down 5.5% on a total return basis as of December 21, (vs. -17.3% for the broader index).

One Aristocrat, Abbott Laboratories (ABT) is off by more than 20% year-to-date, as the boom from COVID testing is expected to drastically slow next year and recalls of baby formula have weighed on the nutrition segment.

The stock’s slide makes the current P/E multiple of 19 a very reasonable price, given that the historical average is above 30. Further, the company boasts a diversified revenue stream that should protect the current dividend payout with multiple avenues for growth, particularly within Medical Devices and the Alinity division.

Abbott’s success in COVID-19 testing made it a major cog in the fight against the virus. The effort more than doubled the cash on its balance sheet compared to before the pandemic, which increases the likelihood of tuck-in M&A activity given management’s propensity for deals in the not-too-distant past.

Finally, earlier this month, Abbott raised the dividend by 8.5%, pushing the yield up to 1.8%.

BIG PHARMA

Also ripe for the picking are two pharmaceutical behemoths that aren’t considered Aristocrats today, but may be well on their way as both have increased their dividends in the past month.

Pfizer’s (PFE) partnership with BioNTech is well-known, having generated more than $60 billion from its COVID vaccine over the past two years, but analysts project that figure to drop to below $10 billion by 2030. Nevertheless, the company recently said that it estimates a $15 billion sales opportunity for its mRNA franchise (which includes flu, combination flu/COVID and other experimental vaccine candidates) out to 2030.

Back in November, management had raised the lower end of its full-year 2022 revenue forecast to $99.5 billion, up from $98 billion. The boost incorporates a bump to its full-year COVID vaccine revenue estimate by $2 billion to $34 billion after Q3 sales came in almost $2 billion over the average analyst projection, and about $22 billion of Paxlovid sales (the firm’s COVID pill). The expectation for adjusted EPS also moved higher, rising to a range of $6.40 to $6.50, up from a range of $6.30 to $6.45.

For its part, Merck & Co. (MRK) has found major winners Keytruda, Lagevrio, Gardasil and Januvia on pace to each gross well over $3 billion in 2022 (the first two clearing that hurdle in a single quarter). These achievements and a deep pipeline with room to add to existing franchises present a compelling opportunity for growth at a very reasonable valuation.

Results released last week from a mid-stage clinical study of Keytruda combined with an experimental personalized mRNA cancer vaccine could mean its own mRNA partnership is around the corner. The personalized cancer concoction was created by Moderna (MRNA), which demonstrated a statistically significant and clinically meaningful improvement in primary endpoint of recurrence-free survival from melanoma (and reduced the risk of recurrence or death by 44%) versus Keytruda alone (which already reduced the risk of death or recurrence by 43% vs. placebo in testing).

The two companies plan to initiate a Phase 3 study in melanoma patients in 2023, which will need to confirm the findings from Phase 2, while potential exists that a similar combination (which incorporates patient tissue samples) could achieve additional oncological indications beyond skin cancer.

Merck boasts a history of returning cash to shareholders, a diversified revenue stream and solid free-cash-flow generation.

Both Pfizer and Merck are available for forward P/E multiples below that of the S&P 500 with dividend yields of 3.3% and 2.6%, respectively.

Learn More:

We frequently publish investment-oriented content on our Blog and reach thousands of subscribers through our weekly Market Commentary and monthly Newsletter. Please click here for subscription information.

For more details about our wealth management and asset management services, kindly fill out this Contact Us form and we’ll reach out to you shortly.