Our first Special Report on the upcoming election, Market Insights for the 2024 Presidential Election, offered a 35,000-foot view of presidencies, congress and stock market history reaching back nearly a century. The broad conclusion was that stock markets rise (with interceding setbacks) irrespective of the resident in White House, makeup of congress or any other political angle. While the message of sticking with stocks as part of a long-term-oriented investment plan long has been the right advice, we realize that Wall Street pundits’ constant promotion of immediate portfolio action may capture more interest, even as their takes often vacillate based on the latest polls and candidate comments.

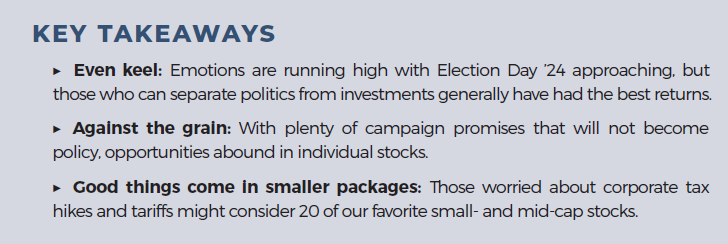

Figure 1 shows betting odds for a race that is still too close to call. With a month to go before the polls close, we offer the reminder that the major equity averages are trading near all-time highs, illustrating that markets have managed to move higher over the long term whether a D or an R occupies the Oval Office and/or controls Congress. Of course, individual stocks could be impacted by a President Trump or President Harris administration, so in this report, we highlight specific companies worthy of consideration for those with a multi-year time horizon.

PAST PERFORMANCE

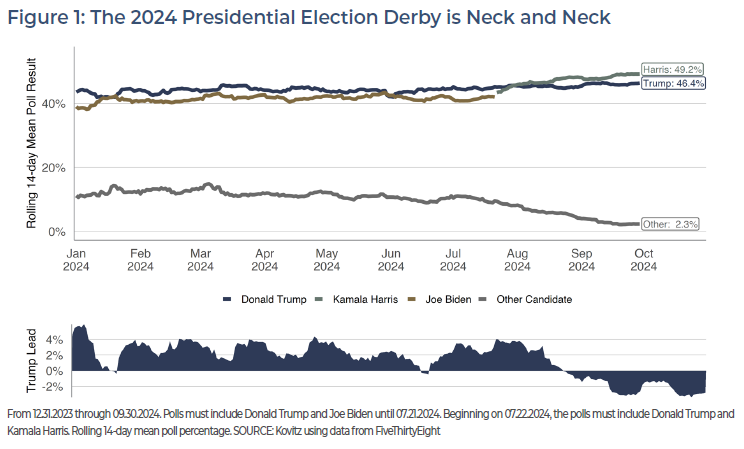

Warren Buffett said, “If past history was all there was to the game, the richest people would be librarians,” but we think it valuable to examine how investors fared with Donald Trump and Joe Biden (and Kamala Harris) in the White House, especially with talking heads on financial TV proclaiming that various stocks or sectors will crash or soar depending on who wins in November. Believe it or not, as shown in Figure 2, equities in general performed very well under both administrations!

Represented by the S&P 500 index, large- and mega-capitalization stocks returned an average of 14% (Trump) and 16% (Biden) per annum, compared with an average annualized total return of 11% since 1989. Small-company returns, represented by the Russell 2000 index, were close to 10% for both presidents, a figure that’s just over 1% better than the since-1989 average.

At a more granular level, most sector returns are fairly close in proximity and in most cases meet or exceed their respective longer-term averages. True, we caution that the track record is short in this analysis and there are a litany of externalities in play that impacted returns, but it is fascinating to see such a massive difference in Energy sector performance.

Indeed, Biden’s 39% return was 5,460 basis points better than what was registered under the Trump’s administration! The COVID-19 pandemic naturally played a part in the dreadful energy returns, but that didn’t explain all of the underperformance. Between Election Day 2016 and the all-time high before the pandemic on February 19, 2020, the Energy sector index had posted an annualized drop of 3%, which would narrow the spread to 42%, or 4,200 basis points.

Of course, conventional wisdom would have argued that the Energy stock return gap would have favored Trump. After all, on November 17, 2016, Time Magazine proclaimed, “It really is a new day for U.S. energy policy. The President-elect has pledged to roll back environmental regulations, invest in new pipelines and allow drilling on public lands–and he can make many of the changes unilaterally once in office.” And on August 5, 2021, NBC News exclaimed, “President Joe Biden took the wheel of a plug-in Jeep Wrangler to tout electric vehicles on Thursday after signing an executive order setting a national goal for zero-emissions vehicles to make up half of new cars and trucks sold by 2030.”

Looking at other sectors, we have long been overweight Information Technology relative to Value benchmarks, so we are pleased that IT did very well no matter the Commander in Chief, and we continue to be very comfortable with our exposure to many well-known names, including a couple of heavyweights that officially fall into the Communication Services sector. Despite occasionally tough talk on the regulatory front from both sides of the political aisle, we think Tech will fare well, propelled by cloud spending and the push to develop Artificial Intelligence (A.I.), both significant technologies that are in their early innings.

We have long liked companies like consumer electronics king Apple (AAPL) and Internet media giant Alphabet (GOOG), and, more recently, social media titan Meta Platforms (META), who are each scaling up their A.I. offerings with plans to generate additional revenue. We believe smaller-company names like IT solutions provider Hewlett Packard Enterprise (HPE), optical and photonic products concern Lumentum (LITE) and data center REIT Digital Realty (DLR) also stand to benefit from widespread A.I. adoption. We also like semiconductor capital equipment makers Lam Research (LRCX) and Kulicke & Soffa (KLIC), as well as volatile chipmaker Micron Tech (MU), which just posted better-than-expected EPS and raised guidance, as “picks-and-shovels” beneficiaries of the A.I. gold rush. Each of these stocks is trading for reasonable or inexpensive valuation metrics, especially given the growth potential over the next three-to-five years.

Finally, we note that Real Estate is a relatively new addition to the S&P sector lineup, launching in September 2016. While overall returns were not much different under the Trump and Biden administrations, we think the recent shift to the easing of monetary policy by the Federal Reserve bodes well for this interest rate sensitive market segment. We like medical office and laboratory property REIT Alexandria Real Estate (ARE), health care REIT Healthpeak Properties (DOC) and open-air, grocery anchored shopping center REIT Kimco Realty (KIM).

mixing politics and investing

Before getting into other stocks we favor, we offer a couple of caveats. No doubt, it’s tempting to want to use political statements from “our” candidates (or those on the “other” side) as catalysts that necessitate action in a stock portfolio. After all, some would argue that you can zig or you can zag, but if you just stand there, you’re going to get run over. Feeding into the urge to trade, politicians also tend to offer commentary that is not found in SEC filings, analyst notes or management guidance: it’s exciting, emotional and–importantly–always certain…unless it changes!

In this report, we’ll look at a handful of current policy comments from former President Donald Trump and Vice President Kamala Harris. We do our best to separate policies from emotion and evaluate the candidates’ platforms and policy-oriented comments in an even-handed manner, especially as history shows that campaign promises often fail to come to fruition, stock prices do not always follow the script and traders have already cast many votes for perceived winners and losers.

MEA CULPA

By way of example, we think it interesting to discuss GEO Group (GEO), a private operator of prisons. Long-time readers will recognize this name, which we sold on August 18, 2016. In our Sales Alert, we wrote, “What had been shaping up as a nice relative performance day for our portfolios took a major turn for the worse when a memorandum from Deputy Attorney General Sally Q. Yates of the U.S. Department of Justice became public today. The memo announced that the federal government will begin to phase out all of its business with privately operated prisons effective immediately. The shocking news sent shares of prison REIT GEO Group plunging as much as 50% in very heavy trading.”

GEO management said later that day, “While the company was disappointed by today’s DOJ announcement, the impact of this decision on GEO is not imminent. As acknowledged in the announcement, the Bureau of Prisons (BOP) will continue, on a case-by-case basis, to determine whether to extend contracts at the end of their contract period. Notwithstanding today’s announcement, GEO will continue to work with the BOP, as well as all of our government partners, in order to ensure safe and secure operations at all of our facilities.”

And we closed the Sales Alert with, “The shares managed to continue their late-day bounce in the after-hours, even as Presidential front-runner Hillary Clinton tweeted, ‘Glad to see that the Justice Department is ending the use of private prisons. This is the right step forward.’ Time will tell whether we made the right decision in bailing out amidst the panic selling, but we have seen in the last year or so REIT prices devastated when dividends are slashed (hard to see how the payout is not cut), while we believe that it will be very tough for state and international governments to ignore Washington’s official proclamation that the private prison business essentially is not viable.”

The kick in the shin hurt, but the tipping point at the time was that Hillary Clinton was leading the race for the White House, an eventuality that arguably would put GEO out of business or at least impair the company’s ability to make money. Mrs. Clinton did not win the contest and then-President Donald Trump did not force GEO to close shop. The stock, which we sold for $17.05, closed as high as $33 three months after Trump’s inauguration and we licked our wounds.

Counter to what many might have expected, GEO actually fared quite poorly during the Trump Administration, losing 39% without dividends or 10% with dividends from Election Day 2016 to Election Day 2020. Fiddling with the dates does make a sizable difference. Inauguration Day 2017 to Inauguration Day 2021 saw a price return of -67% and a total return of -52%.

We bring up GEO Group because we aren’t completely immune to falling for the very traps that our humble publication so frequently warns about, despite employing a quantitative framework, long-term Target Prices and decades of experience. Who knows when we would have sold GEO had we not in August 2016, but GEO’s subsequent performance record hasn’t been very good. Still, it’s something to keep top of mind as we progress through this election cycle, having to weather the constant barrage of information that can easily knock an investor off the path to long-term investment success.

HEALTH CARE REFORM IN THE 1990’s

“Political” trades don’t all work out poorly, though. In 1993, just-elected President Bill Clinton announced that First Lady Hillary Clinton would head the President’s Task Force on Health Care Reform. Introduced to Congress later that year, HR 3600, proposed prescription insurance reform, price controls for drugs and guaranteed health care for every citizen.

In August 1993, we wrote in TPS Edition #322 that pharma giant Merck (MRK) should have had a stellar 1993, but instead “Merck’s ‘93 ails can be traced directly to the White House and in particular, the market’s concerns about the soon-to-be revealed Hillary Rodham Clinton health care reform agenda which is expected to contain some form of drug industry price controls and perhaps the elimination of tax breaks…Price increases have been virtually non-existent in 1993 and the company has even submitted its own price-control proposal to the White House, tying increases to the Consumer Price Index…Although it is near certain that MRK will no longer be able to grow its earnings at the 25% annualized clip of the past five years, we think long- term investors should seize this opportunity to add one of America’s strongest companies to their portfolios. Because MRK now trades for fourteen times earnings and twelve times cash flow and yields over three percent, numbers not seen in years, we advise its purchase.”

We officially bought MRK on July 30, 1993, for $30.63 and closed the position five years later on June 1, 1998, for an average sale price of $132.25, a 332% gain without dividends. Each year between 1994 and 1998, Merck ended up growing EPS between 13.5% and 27.3%, while HR 3600 died in 1994 after meeting stiff opposition from all sides. The Clinton’s pivoted to pass the Children’s Health Insurance Program (CHIP) in 1997, which met far less opposition and was generally viewed as a success. Extensions of the CHIP legislation were signed by President Obama in 2009 and President Trump in 2018.

THE 2024 RACE

Overall, it’s important to point out that we very much like the current positioning of stocks, industries and sectors in our portfolios. The three-to-five-year Target Prices we publish show plenty of available total return potential for our holdings and we believe broad diversification functions well to ensure the portfolios aren’t overly exposed to any single company. Equally important, we have not made broad adjustments to the portfolios on account of potential political outcomes. We rely on an appropriate asset allocation to mitigate overall client risk and generally believe short-term equity trading is a great way to interrupt long-term capital appreciation.

That’s not to say this election won’t have consequences for our portfolios. It will. We simply don’t know what they will be because we don’t know who is going to win, nor do we know the makeup of congress. Even if we had an election crystal ball and knew there would be a Democratic or Republican sweep, it still would not necessarily change the composition of our portfolios. We need only look back to 2020 and West Virginia Sen. Joe Manchin, a self-described centrist, moderate, conservative Democrat for proof that “control” of congress does not a rubber stamp provide.

Frankly, it is impossible to know which of a candidate’s promises will end up turning into real policy and which will end up dying on the campaign shelf. Further, we do not know how investors would react as the “right” candidate won the 2020 election for GEO Group, and after the early enthusiasm faded, so did the returns. The “wrong” candidate won in 1992 when it came to pharmaceutical pricing, but the legislation stalled, and Merck had a stellar five-year run.

All of that backstory in mind, we look at a selection of campaign-related highlights from the Harris and Trump camps and point out some things to consider as investors look to make updates (or not!) to their own portfolios. Critically, candidate statements are constantly evolving, so the only thing we can say with certainty is that handicapping the odds of various campaign policies crossing the chasm to reality is extraordinarily difficult.

KAMALA HARRIS’S PLATFORM

Bringing down the costs of health care is a key stated priority for the Harris campaign. Her website lists goals of lowering health care premiums, reducing out-of-pocket costs, cancelling billions of dollars in medical debt and capping prices on insulin. While Health Care stocks have had a good year on average, Big Pharma companies like Bristol Myers (BMY) and Pfizer (PFE) have trailed the S&P 500 index, while pharmacy and health care provider CVS Health (CVS) has taken a beating, which has us thinking long-term opportunities are available in all three as bad news that may or may nor materialize is already “in” the share prices. On the positive side, drugmakers Sanofi (SNY) and Amgen (AMGN) have risen 16% and 12% to date, respectively, and the dynamics that have propelled them higher, we believe, remain intact. If price controls don’t work out as outlined in Harris’s plan, we think Health Care could see a healthy move up, as was the case in the 1990’s, while each of the aforementioned companies pays a generous dividend that is well covered by a sizable bottom line. More importantly, given our long-term thinking beyond the next presidency, we continue to believe changing U.S. demographics, including an aging population, remains a major catalyst in support of Health Care stocks.

Harris’s platform includes broad housing support, making rent more affordable and home ownership more attainable. With up to $25,000 in first-time homebuyer support and the recent drop in interest rates making mortgages feel less expensive, we think the likes of appliance maker Whirlpool (WHR) and home improvement retailer Lowe’s (LOW) could see demand growth. We also like homebuilder D.R. Horton (DHI) and furniture seller Ethan Allan (ETD), holdings in our Small-Mid Dividend Value strategy (more about our SMID approach later).

A national ban on price gouging certainly garnered a lot of media attention in August after Harris said she would pursue the policy. The idea is that grocery bills are too high and corporate greed is to blame. There is nothing concrete as to what steps would be taken to lower prices without amping demand and endangering supply, but it’s not like food providers and grocers have massive margins. Protein producer Tyson Foods (TSN) and fruit grower Fresh Del Monte (FDP) sport modest margins in the 2% to 4% range, while grocery chain Kroger’s (KR) profit margin was a measly 1.4% in the latest quarter. All three, we think, now trade in the bargain aisle, making them great stocks to consider for those willing to look beyond the campaign headlines.

The Department of Justice and Attorneys General around the country have been busy lately, busting up purported monopolies, blocking transactions and looking into antitrust violations. One could argue that recent enforcement activity has been too heavy, with clothes and accessories marketer Tapestry’s (TPR) battle to acquire luxury fashion concern Capri Holdings an example.

We can see why the U.S. wanted to intervene on Nippon Steel’s $14.1 billion takeover of United States Steel, but the free market could be freer than it is and sometimes the Justice Department simply gets it wrong. We aren’t sure what a Trump or Harris Administration would bring in terms of a DoJ that has been inconsistent on antitrust enforcement over the last few decades. Would they re-review the dead jetBlue-Spirit deal after letting Alaska and Hawaiian Airlines merge? Would Apple (AAPL) or Qualcomm (QCOM) be allowed to buy Intel (INTC)? Alas, only with the benefit of hindsight will we know about enforcement, so we expect mergers to continue to face scrutiny no matter the president, even as we know that dealmaking will always be present on Wall Street.

“Green Tech” or climate-friendly policies have had mixed impacts and receive equally mixed reviews. The Harris platform claims that victory will help folks lower their household energy costs and creates millions of new jobs. We suspect that might be true on some level, especially as other countries are charging ahead with cleaner technology investments, whether the U.S. joins the party or not. We continue to like engineering and manufacturing firm Siemens AG (SIEGY), carmaker Volkswagen AG (VWAGY) and engine manufacturer Cummins (CMI) for their work on a cleaner future. Although the U.S. could not curtail any impact of climate change on its own, pricing has firmed (a positive) for insurers like Allstate (ALL) and Allianz SE (ALIZY) as worries about the frequency, intensity and losses related to natural disasters have risen.

DONALD TRUMP’S PLATFORM

A go-to tool during his presidency, Former President Trump has made tariffs (or the threat thereof) a key part of the push to accomplish his campaign goals in the event he wins back the Oval Office. He has long toyed with the idea of implementing across-the-board tariffs on imports and his more recent comments have indicated he wants a 10% to 20% duty on wide baskets of goods, with an extra levy on Chinese goods for a total tariff reaching 60% and a four-year phaseout of imports of Chinese-made essential goods. He believes this will boost U.S.-based manufacturing.

Some individual companies may uniquely experience potentially harmful treatment. At an event on September 23, Trump said, “As you know, [ag equipment maker John Deere (DE)] announced a few days ago that they’re going to move a lot of their manufacturing business to Mexico. I’m just notifying John Deere right now, if you do that, we’re putting a 200% tariff on everything you want to sell into the United States.” Sounds ominous, until one remembers that manufacturing stocks like DE, construction and mining equipment titan Caterpillar (CAT) and electrical power equipment maker Eaton (ETN) all enjoyed market-beating returns during the prior Trump years.

Trump has said that high tariffs would be used to fund tax bill reductions elsewhere, making it difficult to estimate the overall impact to our stocks and a person’s wealth in general. Over the years, we have noticed that politicians are quicker to add taxes or invent new accounting methods, rather than cut spending, so our knee-jerk reaction is that we could see temporary adverse impacts for some stocks given the lack of reaction time. Should there be some upheaval, we contend it would be to the benefit of long-term equity buyers. Over longer periods of time, it is possible that companies can relocate to the U.S. to benefit from more favorable supply chain, production and taxation dynamics. However, as we have seen with Intel (INTC), moving work home can be a lot more arduous than it would appear, even as the undervalued chip company is attracting plenty of Wall Street attention, while benefitting from DC efforts to incentivize domestic semiconductor production.

Another key point in the Trump platform is to “make America the dominant energy producer in the world, by far!“ This policy is hardly surprising, given that it was a feature of his first presidency. U.S. crude oil production has steadily marched higher in recent years. Using data from the Energy Information Administration (EIA), Trump’s first year (2017) had 9.4 million barrels per day of crude production. Production reached 12.3 million in 2019 and 12.9 million in 2023. Despite the lagging returns from 2016-2020 for Energy stocks, we think integrated giants like Chevron (CVX) and Exxon Mobil (XOM) can benefit from more U.S. energy production, as can others throughout the chain like global producer EOG Resources (EOG), U.S.-centric E&P outfit Devon Energy (DVN) and refiner HF Sinclair (DINO). We also note that the push to EVs will be decades in the making and more than half of U.S. oil production is not used to power motor vehicles.

Nuclear power has the lowest carbon footprint of all electricity sources, uses the smallest section of land and needs few materials, yet the generation technology has one of the worst reputations around the world. Images of Chernobyl, Three Mile Island and Fukushima are almost impossible to overcome in any discussion for nuclear’s future. As some countries have opted to turn off their reactors, others are bringing them online. Construction of more than 100 reactors are planned worldwide, and a reactor #4 was commissioned at the Vogtle Generating Plant in Georgia in April, the country’s newest. Whether either candidate embraces nuclear energy is unknown at this point, but the tide may be turning.

Microsoft (MSFT) recently announced plans to buy 20 year’s worth of power from Constellation Energy’s Unit 1 of the Three Mile Island plant to power its A.I. data centers. Pinnacle West (PNW) operates three reactors, each with 1,300 megawatts of capacity, at the Palo Verde Generating Station outside Phoenix, Arizona. As Europe found out after the war in Ukraine started, the value of stable energy sources is high and both candidates could return to the newest versions of nuclear power to power the U.S. well into the future, even as it will be a long time before fossil fuels go the way of the dinosaur.

Finally, the Trump platform includes, “Strengthen and modernize our military, making it, without question, the strongest and most powerful in the world,” while the former President also asserts that he will quickly end the Russo-Ukrainian War. Meanwhile, the Harris campaign maintains the position that the U.S. “will stand strong with Ukraine and our NATO allies.” Whether the U.S. simply flexes its military muscle or continues to ship weapons eastbound, we would think that defense contractors like General Dynamics (GD) and Lockheed Martin (LMT) stand to benefit. With the Middle East also a seeming powder keg, it is hard to envision anything but increases in the Pentagon’s budget the next four years.

TAX POLICY IN FOCUS IN 2025 and BEYOND

Perhaps the most important issue on the mind of investors is taxes. Shortly after President Joe Biden bowed out of the race, Vice President Harris came out with an endorsement of a tax on unrealized gains on wealth exceeding $100 million. Opposition was fierce and implementation of the rules would have been tremendously complicated. Apparently sensing the policy would have been dead on arrival, Harris scaled things back.

Her subsequent proposal was to raise the net investment income tax (NIIT) from 3.8% to 5.0% for those with modified adjusted incomes in excess of $400,000. As a comparison, current law imposes the NIIT on single filers earning $200,000 or more and married couples earning $250,000 or more. The combined rate for top earners would be 33%.

Former President Trump has indicated that he plans to make personal tax changes in the 2017 Tax Cuts and Jobs Act (TCJA) permanent. Additionally, he wrote in September on his Truth Social platform that he will “get SALT back,” a reference to the $10,000 cap on state and local taxes imposed by the TCJA. On Trump’s campaign website, the platform does not mention personal taxes, except for “large tax cuts for workers and no tax on tips,” and otherwise offers little detail.

In addition to the potential personal income tax changes, Harris has proposed an increase of the corporate tax rate from 21% to 28%. Additionally, she is proposing a share buyback tax hike from 1% to 4%. Trump has not yet formally proposed corporate tax policy plans, but he has indicated that he would consider extending the TCJA, reducing the corporate tax rate by 1% to 20% and/or trimming corporate income tax rates for U.S. producers to 15%.

Although both tax regimes could have definite impacts on corporate profits for our newsletter recommendations, it’s unlikely that the impact would be felt uniformly. Of course, the bean counters will always endeavor to find loopholes, workarounds and creative solutions to mitigate Corporate America’s tax bill. Such has been the case since 1909, the first year Uncle Sam imposed a separate corporate income tax as few businesses pay the maximum corporate income tax rate, given deductions, exemptions, credits and other legal factors.

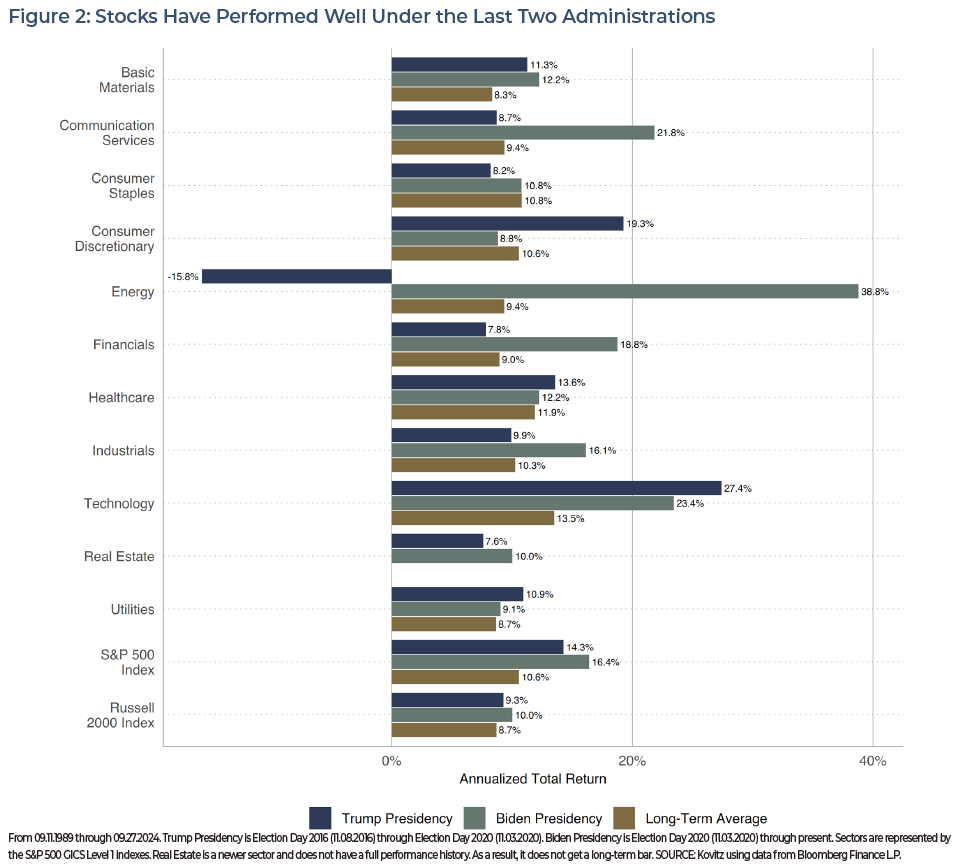

Illustrating the difficulty and complexity of modifications in the tax code, in 2021, the Organisation for Economic Co-Operation and Development (OECD) and more than 130 member jurisdictions agreed to an outline for new tax rules that placed the minimum effective corporate tax rate at 15%. The OECD stated. “The global minimum tax, which is based on the Global Anti-Base Erosion (GloBE) Model Rules, ensures that large multinational enterprises pay a minimum level of tax on their income in each jurisdiction where they operate, thereby reducing the incentive for profit shifting and placing a floor under tax competition, bringing an end to the race to the bottom on corporate tax rates.” Three years later, said tax is not fully implemented around the world and effective tax rates are all over the map as evidenced by the current and average rates reported by the largest U.S. companies.

Figure 3 details the current effective tax rate as well as the 5- and 10-year average effective rates tallied on both an annual and quarterly basis (there are variances from year to year and quarter to quarter) for the largest members of the S&P 500, with numbers pulled from data provider Bloomberg Finance. We note that the biggest companies, including the so-called Magnificent 7 currently pay low effective tax rates, which is a big reason that Goldman Sachs recently estimated the Harris tax hike would shave 5% off after-tax profits for the S&P 500. We aren’t so sure that would be the case, but we might argue that companies that are already high current taxpayers could be more attractive going forward on relative basis.

SMALL & MID CAPS

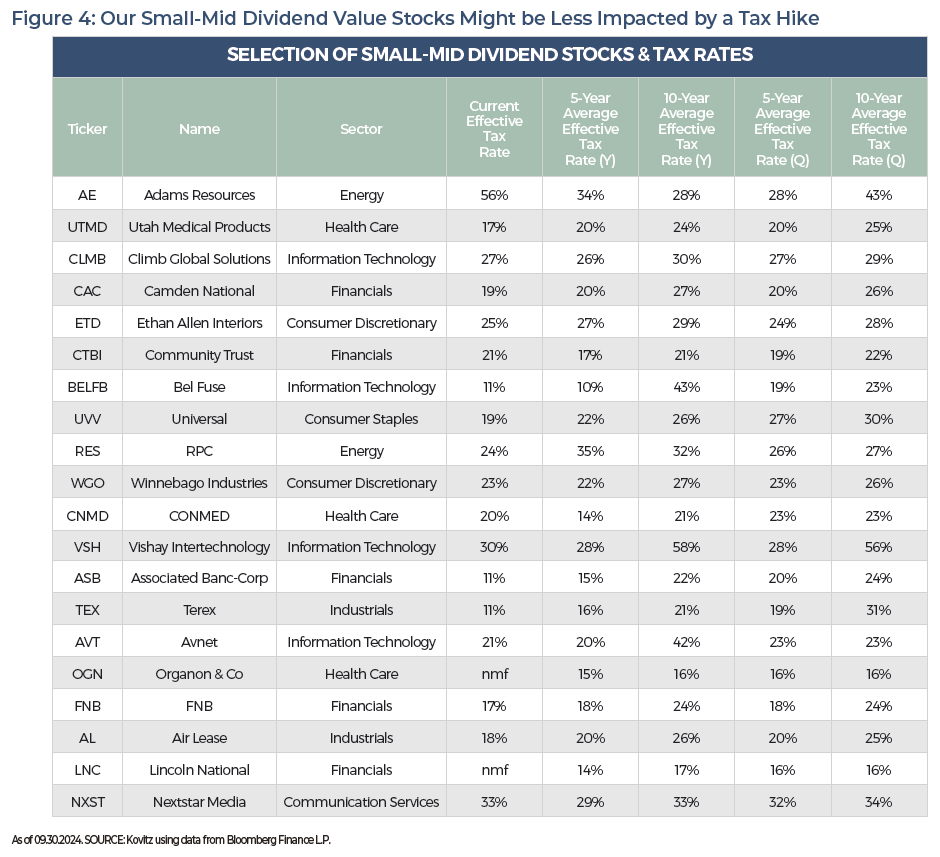

Those worried about the impact a corporate tax increase would have on stocks might consider moving down the market capitalization spectrum. Eleven years ago, we launched our Small-Mid Dividend (SMID) Value managed account strategy that seeks long-term capital appreciation via investments in companies with market capitalizations below $20 billion, including micro-, small- and mid-cap stocks. As with our other income-oriented strategies, the portfolio primarily consists of dividend-paying stocks that are undervalued and/or out-of-favor for their long-term appreciation potential.

In Figure 4, we detail 20 of the names held in the SMID strategy, where the forward P/E ratio on the portfolio is in the 12 range and the dividend yield is 2.8%. More importantly for this tax-related discussion, the average effective current tax rate for our SMID 20 is 22%, compared to 18% for the largest S&P 500 members, while the 5-year average annual effective rate is 21% compared to 17%. True, it would be better to pay less in taxes all things considered, but those companies that are already paying a higher rate would arguably suffer less than those with a low rate, should a Harris tax hike be pushed through, while SMID stocks generally are more focused on the U.S., with potentially less risk from potential Trump tariffs.

HIGHER TAXES ARE GOOD FOR STOCKS?

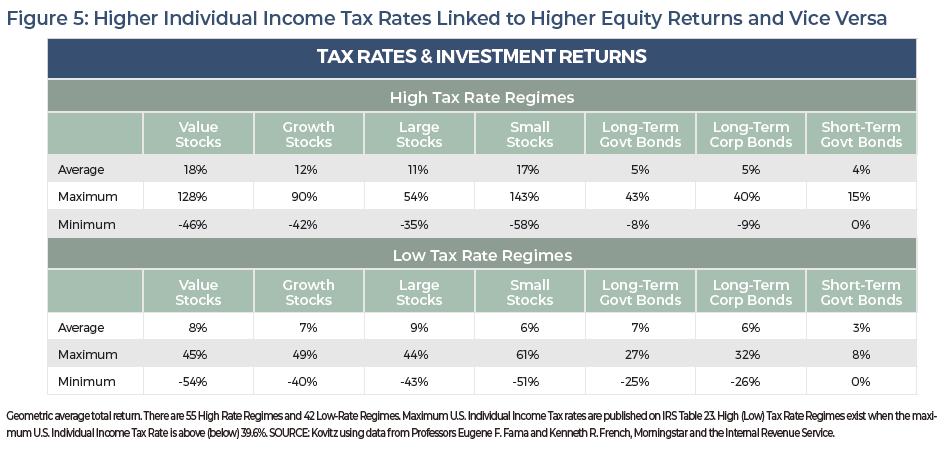

When it comes to taxes, this election is no different than those in the past as numerous stories portend gloom and doom for equities if taxes are raised and unicorns and rainbows should taxes be reduced. On the surface, the logic would appear sound. Who wouldn’t be in a better mood if they kept more of what they earned, and wouldn’t an investor have less incentive to participate in the capital markets if their overall tax bill was higher? Well, we analyzed the returns for individual high-tax regimes (above 39.6% top rate) and low-tax regimes (39.6% and below) over the last 97 years and determined that stocks perform fine on both counts, BUT they have performed better on average when taxes are…drumroll, please…HIGH!

TIME TO HEAD TO THE POLLS

The upcoming election is consequential for many reasons, but we once again feel obligated to warn against making major portfolio moves solely due to the potential person residing at 1600 Pennsylvania Avenue. We have crunched the numbers and trading in and out of stocks based on the resident of the Oval Office would have left an investor on the sidelines for long periods of time. To calculate the damage, we zeroed out returns for the “other” party and ran returns for the Large Company Stocks (S&P 500 index) series. An investor who refused to own stocks during a Republican presidency would have earned an annualized total return of 7.4% and an investor who refused to own stocks during a Democratic presidency would have earned an annualized 2.5%. Both figures fall massively short of the total return for the entire period of 10.1% for the permanently invested index. Plus, the analysis doesn’t include tax consequences from selling appreciated positions, which almost certainly would have further harmed returns.

We freely acknowledge that both candidates have proposed policies that would be good for our stocks. Also, both candidates have proposed policies that would be bad for our stocks. During election seasons, investors are often their own worst enemies considering progress towards their long-term financial goals. We offer a cautious reminder that what is repeated on the campaign trail doesn’t always make it through Capitol Hill and end up as policy.

As voters head to the polls in November, The Prudent Speculator will be riding through its 12th presidential election since 1977. In each case, the stakes were high and the sun came up for the world (and for our stocks) the following day. As is our custom, we simply remain partial to our approach of buying undervalued stocks and patiently holding them for the long term, trimming and harvesting the winners and pruning the losers along the way. It makes for peaceful slumber!