The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Election Perspective, Seasonally Favorable Period, Economic Outlook and More. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Election Webinar – Replay Available: https://www.youtube.com/watch?v=-YYZf7h_rAg

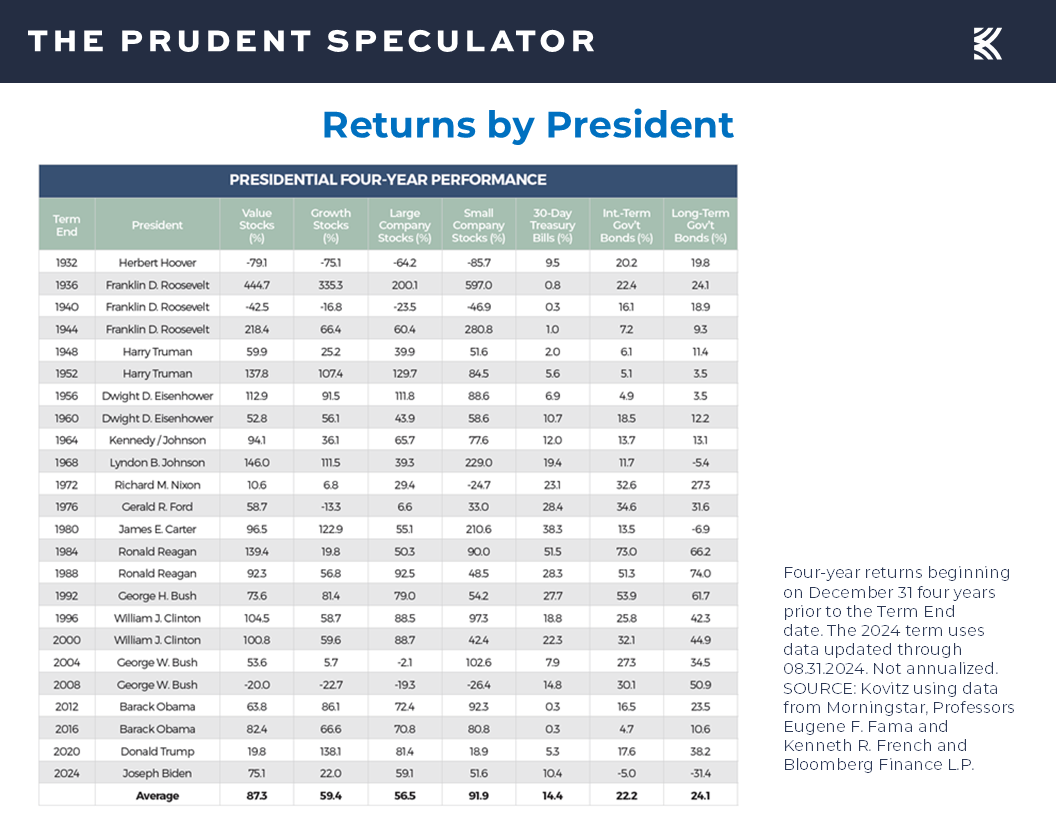

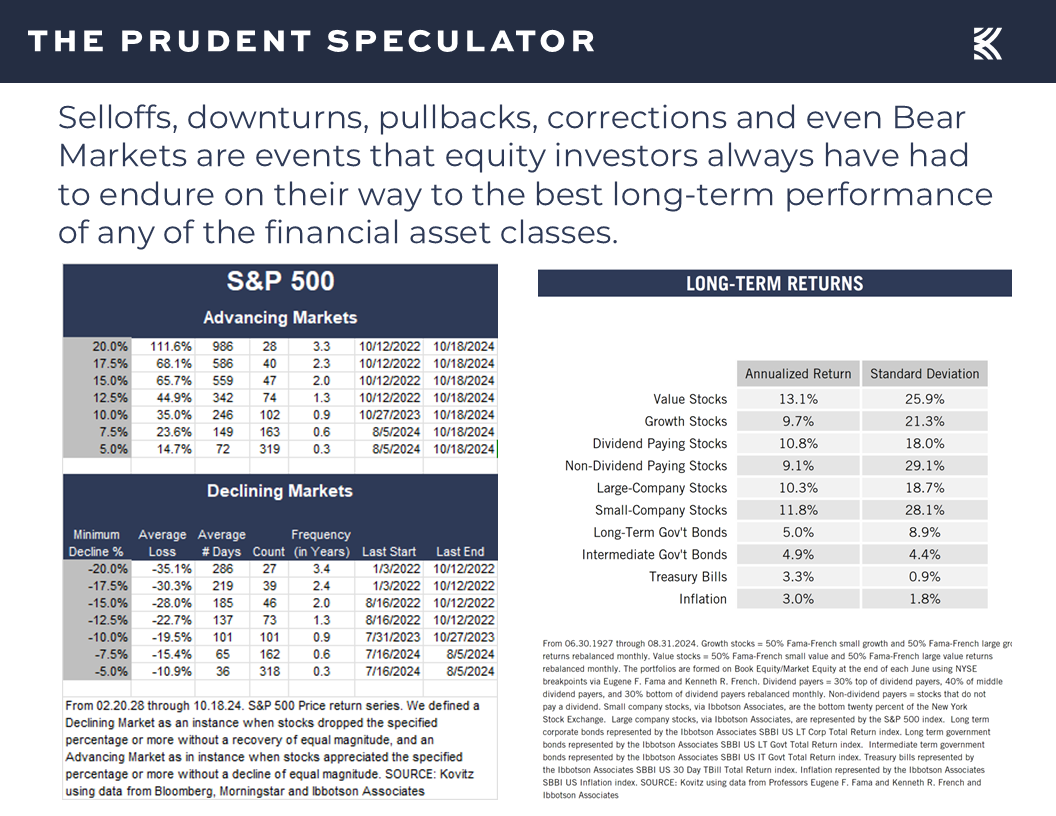

Election Perspective – Historic Equity Returns

Calendar – Seasonally Favorable Period Has Begun

Inflation – PCE Continues to Head in Right Direction

Econ Outlook – Mixed Stats, but Solid GDP Growth the Forecast

Interest Rates – Yields have Jumped; Stocks Haven’t Minded Historically, on Average

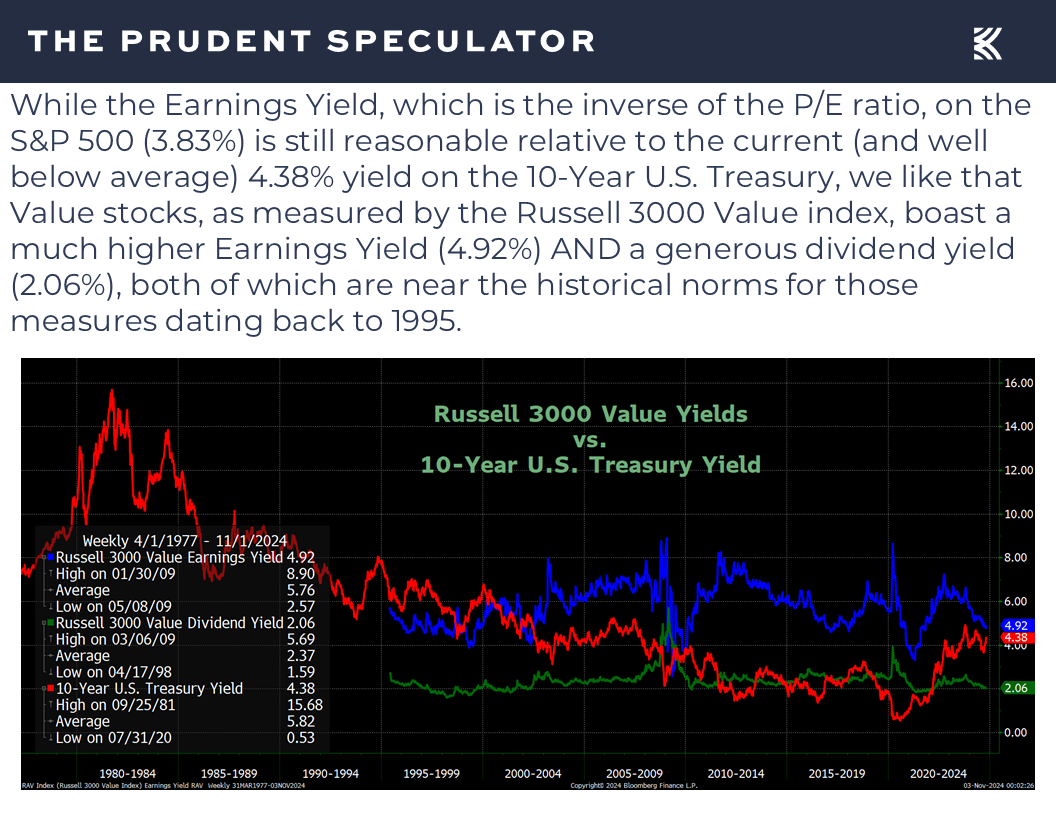

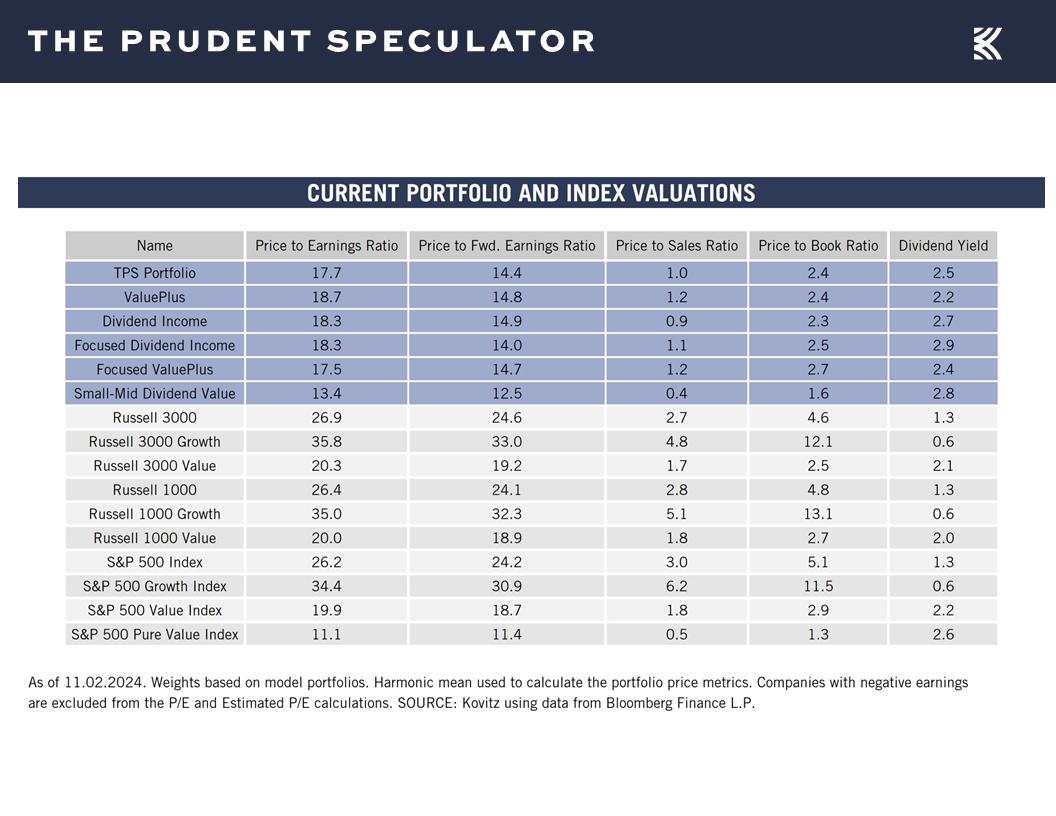

Valuations – Value Stocks Reasonably Priced

Profits – Favorable EPS Outlook

Stock News – Updates on PHG, WM, AMT, PYPL, GLW, GOOG, ZBH, SW, GEN, MSFT, META, FDP, DINO, IP & AAPL

We would like to thank all who tuned in live to our Election Webinar. For those not able to see the event this past Wednesday, a replay is available here:

Election Perspective – Historic Equity Returns

No doubt, there is plenty on the minds of traders and investors alike these days, especially with Election Day 2024 imminent, so we offer the reminder that stocks have performed fine, on average, no matter who occupies the White House,

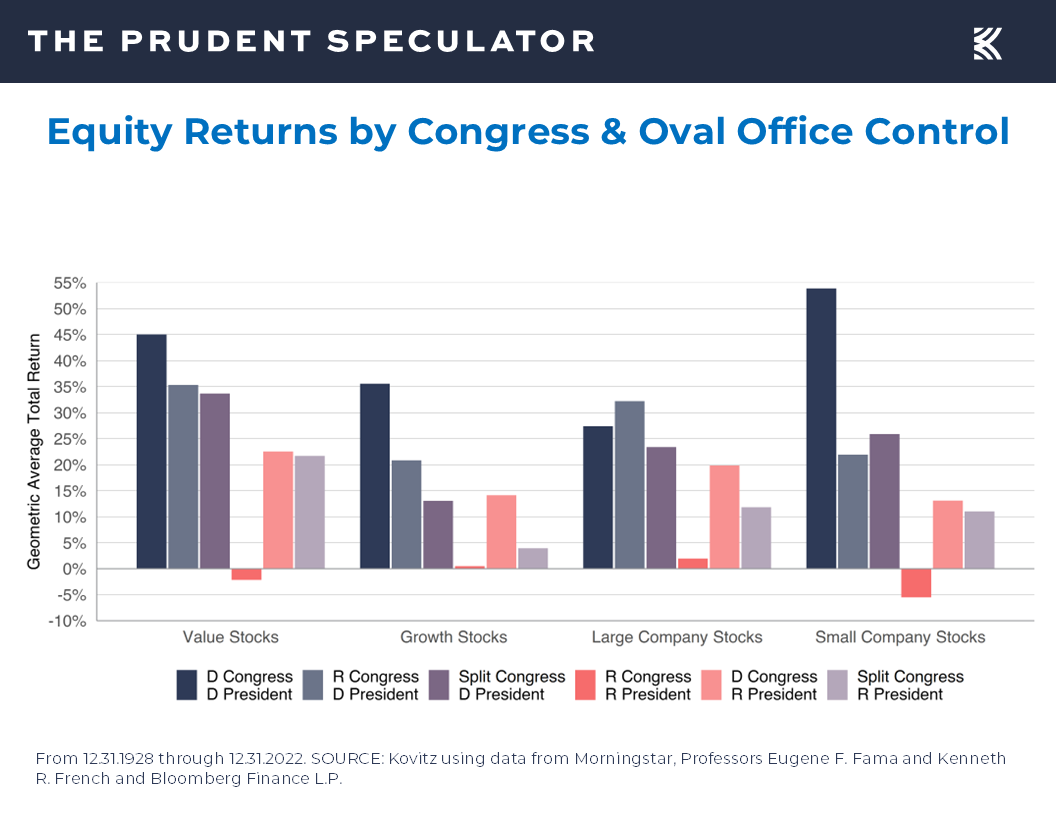

while conventional wisdom that one political party is better than the other for equities has NOT been supported, on average, by nine-decades of returns data. True, the number of data points is small, so one should be careful about drawing concrete conclusions, but it is fascinating that stocks have preferred Democrats in Washington to Republicans,

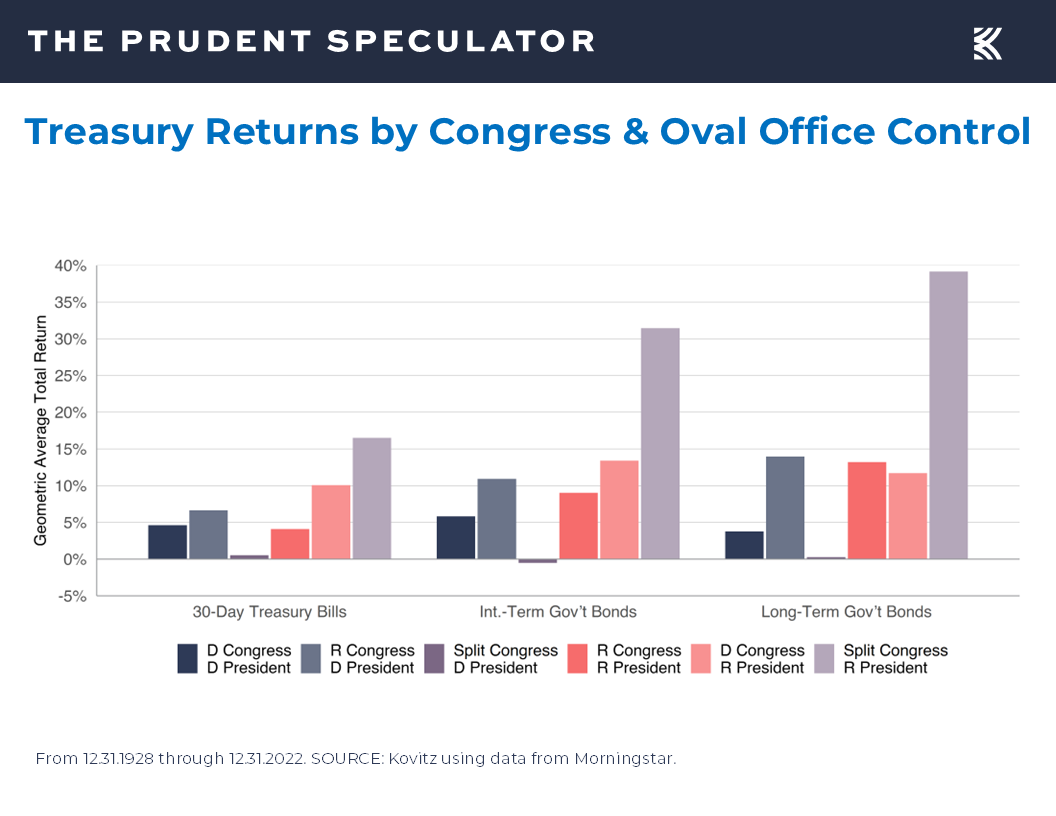

with the reverse true for government bonds.

Obviously, there are numerous factors beyond the resident of 1600 Pennsylvania Avene that have impacted stock prices through the years. Looking at the Presidential terms that ended with red ink for equities, in 1932, the U.S. was in the midst of the Great Depression. Roosevelt’s second term included World War II, while George W.’s first term included the terrorist attacks on September 11 and the second term included the Great Financial Crisis.

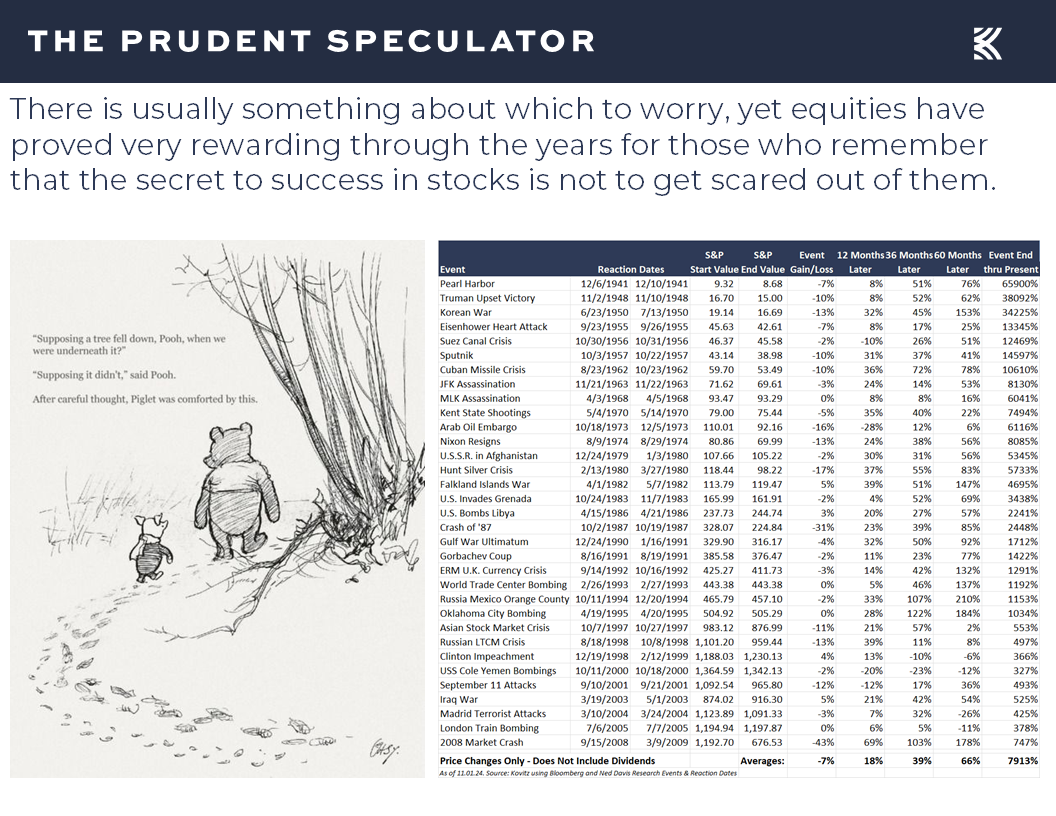

Of course, stocks managed to overcome those turbulent periods and numerous other disconcerting headlines, providing terrific long-term rewards for those that remember that time in the market trumps market timing,

as downside volatility has always given way to upside rallies of even greater magnitude, so much so that returns have ranged from 9.1% (non-dividend payers) to 13.1% (Value) per annum since 1927.

Calendar – Seasonally Favorable Period Has Begun

While stocks closed out the historically weak month of October on a sour note,

we would argue that nothing we saw last week on the economic front dissuades us from feeling enthusiastic about the prospects for equities as we head into the seasonally favorable November through April time span.

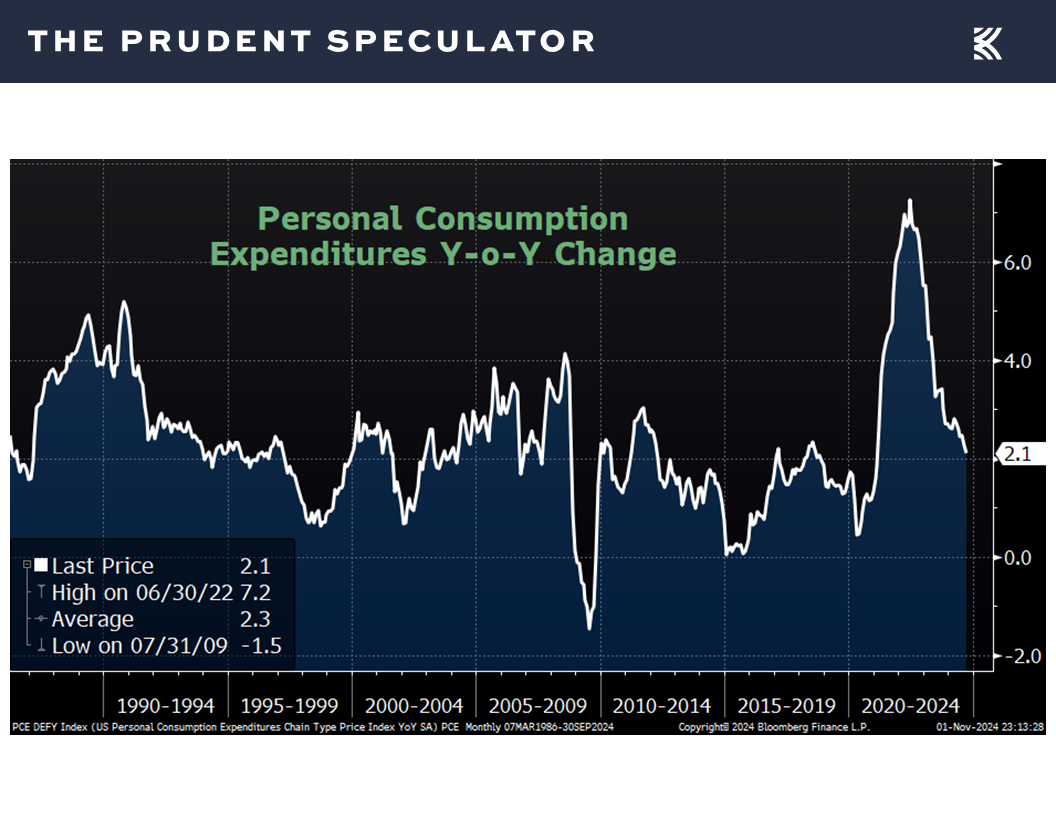

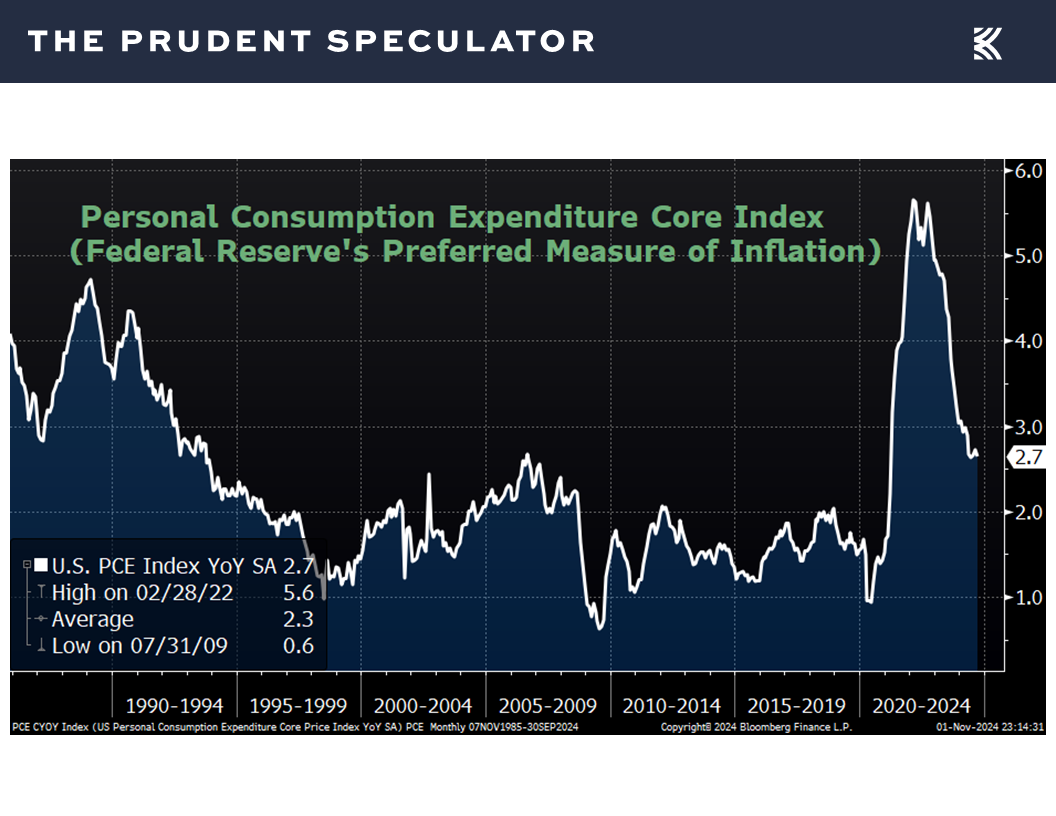

Inflation – PCE Continues to Head in Right Direction

Indeed, prices at the consumer level edged down a tick in September as the personal consumption expenditure (PCE) index declined to an increase of 2.1% on a year-over-year basis versus 2.2% in August.

The Federal Reserve’s preferred gauge, the Core PCE, which excludes volatile food and energy prices, held steady at a 2.7% increase last month,

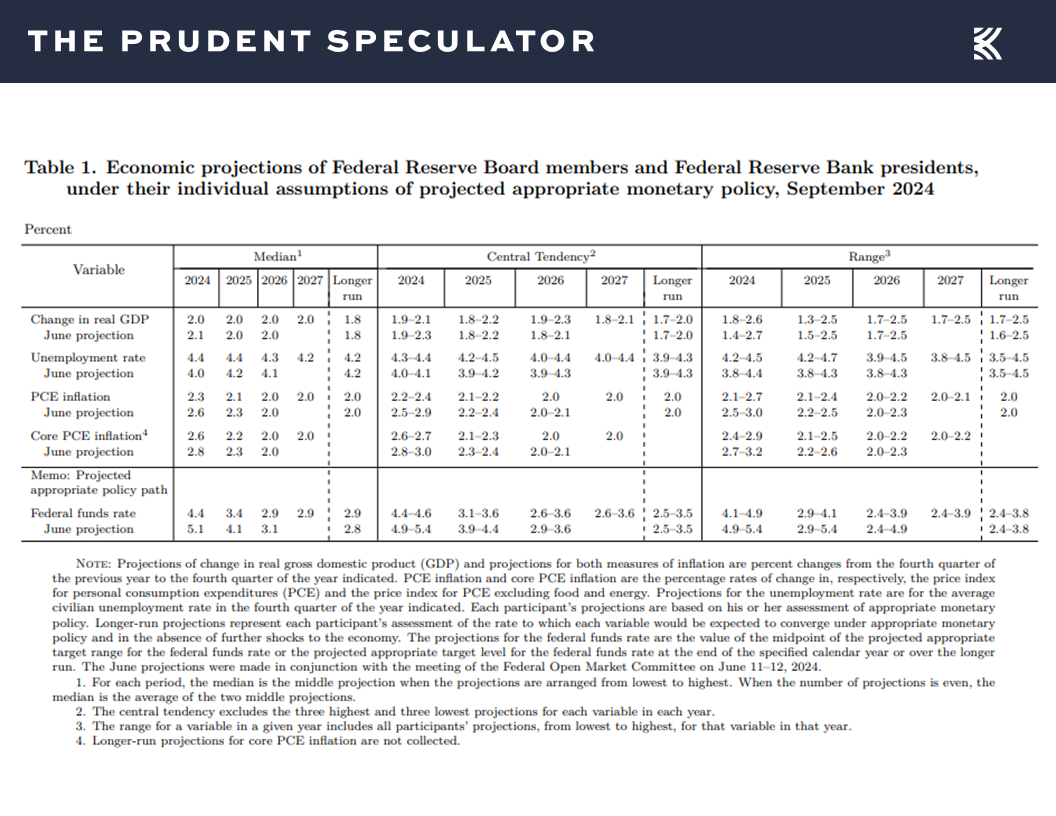

but inflation continues to trend in the right direction and has moved closer to the year-end projections offered in September by Federal Reserve Board members and Federal Reserve Bank presidents.

Econ Outlook – Mixed Stats, but Solid GDP Growth the Forecast

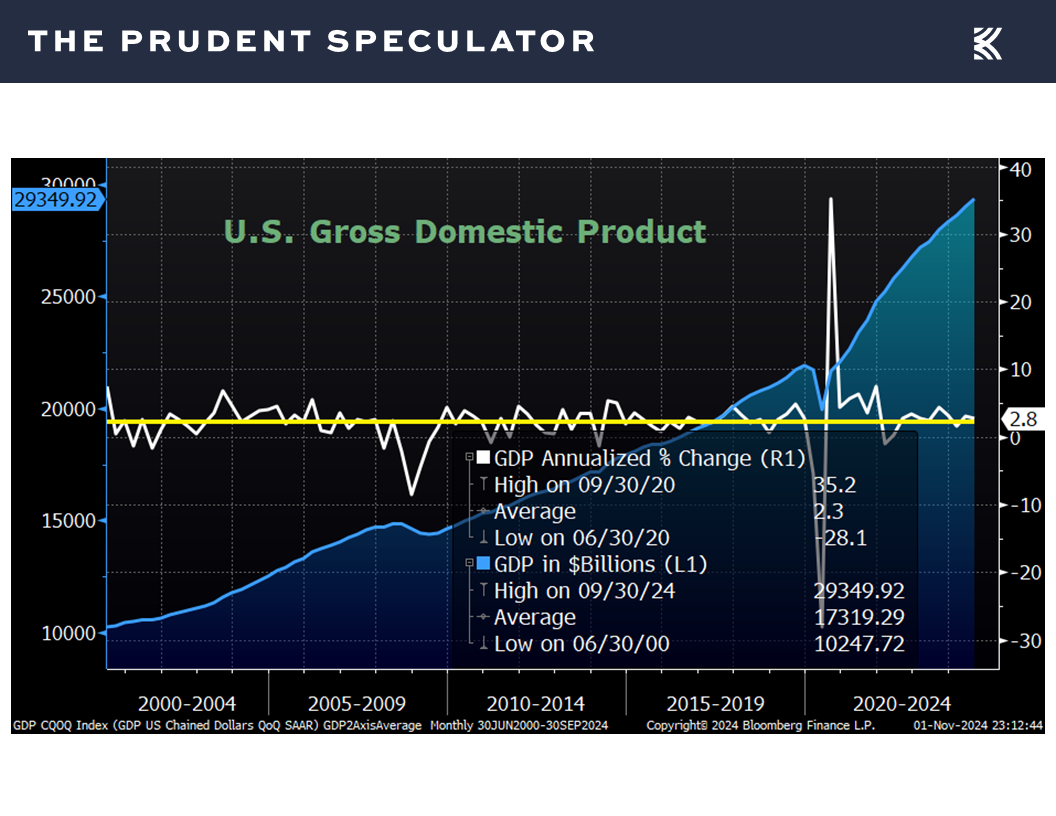

Those forecasts also called for real (inflation-adjusted) U.S. GDP growth of 2.0% this year, a figure that might prove conservative after the first estimate of Q3 GDP growth came in at 2.8% last week,

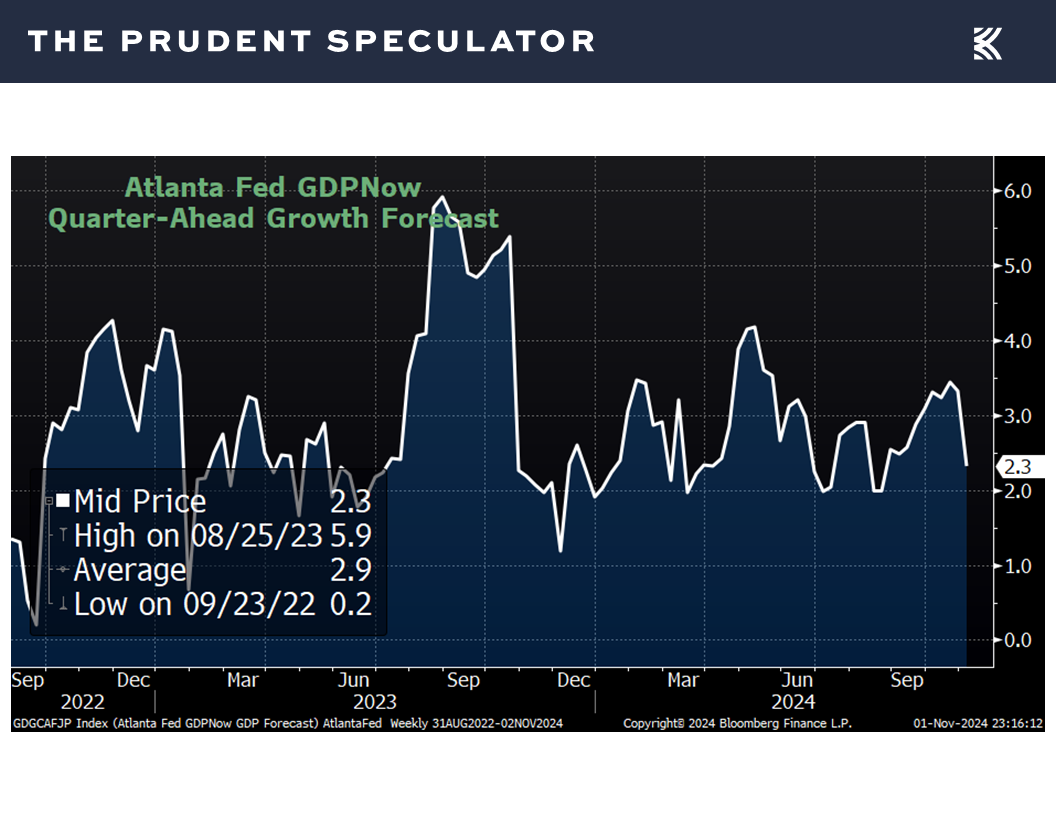

while the initial guess for Q4 GDP growth from the Atlanta Fed stood at 2.3%,

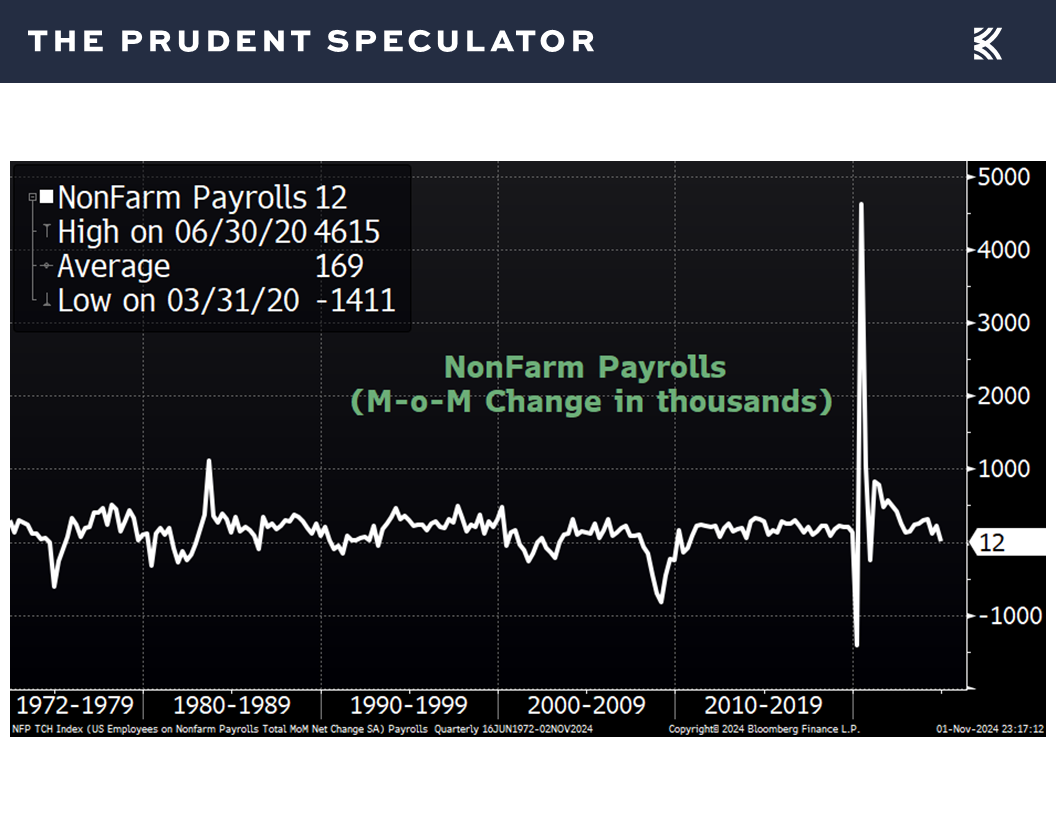

even after nonfarm payrolls rose by only 12,000 in October, well below expectations of growth of 100,000 and the revised tally of 223,000 in September.

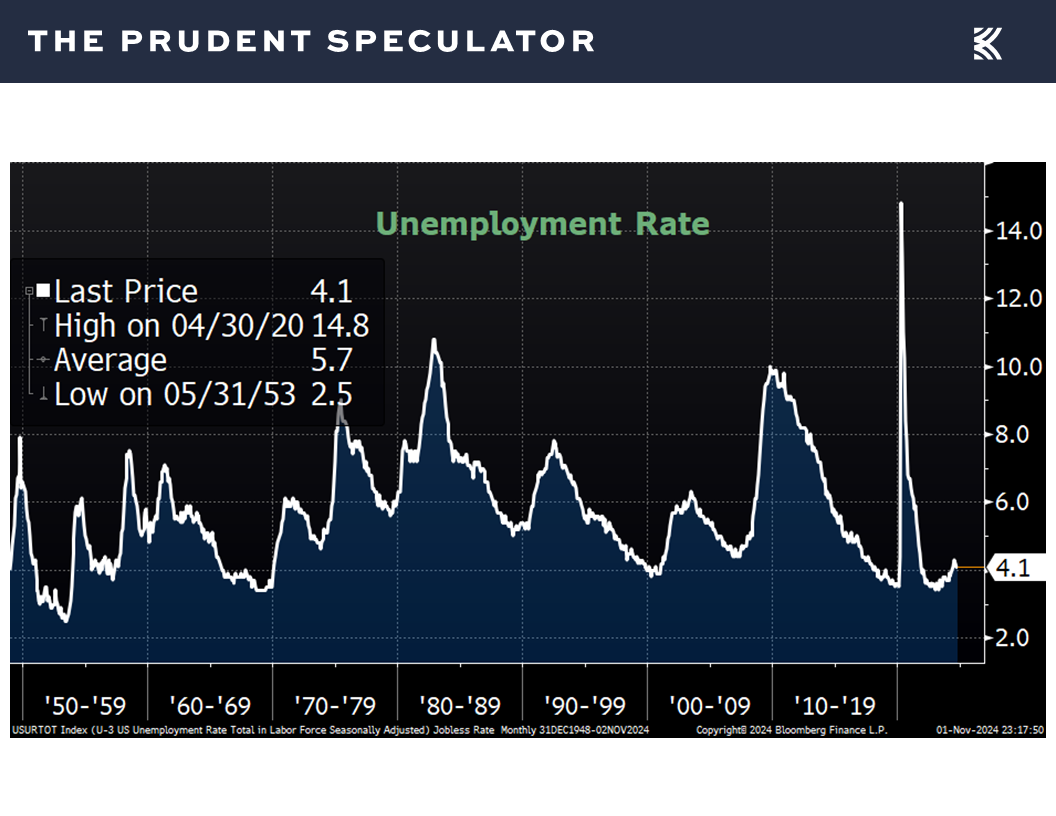

To be sure, Hurricane’s Helene and Milton has a significant impact on the jobs numbers, and the unemployment rate for October was unchanged at 4.1%,

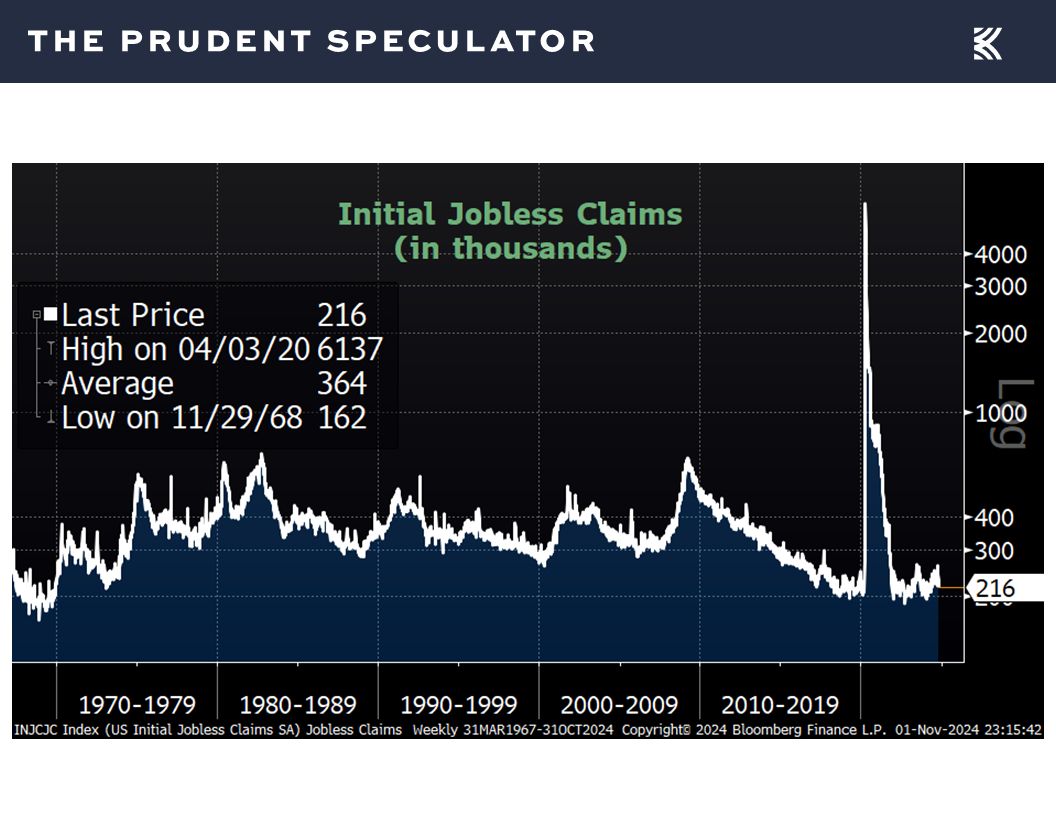

while a more up-to-date reading on the labor market, weekly claims for first-time jobless benefits, saw a drop to a very low 216,000, compared to a revised 228,000 the week prior.

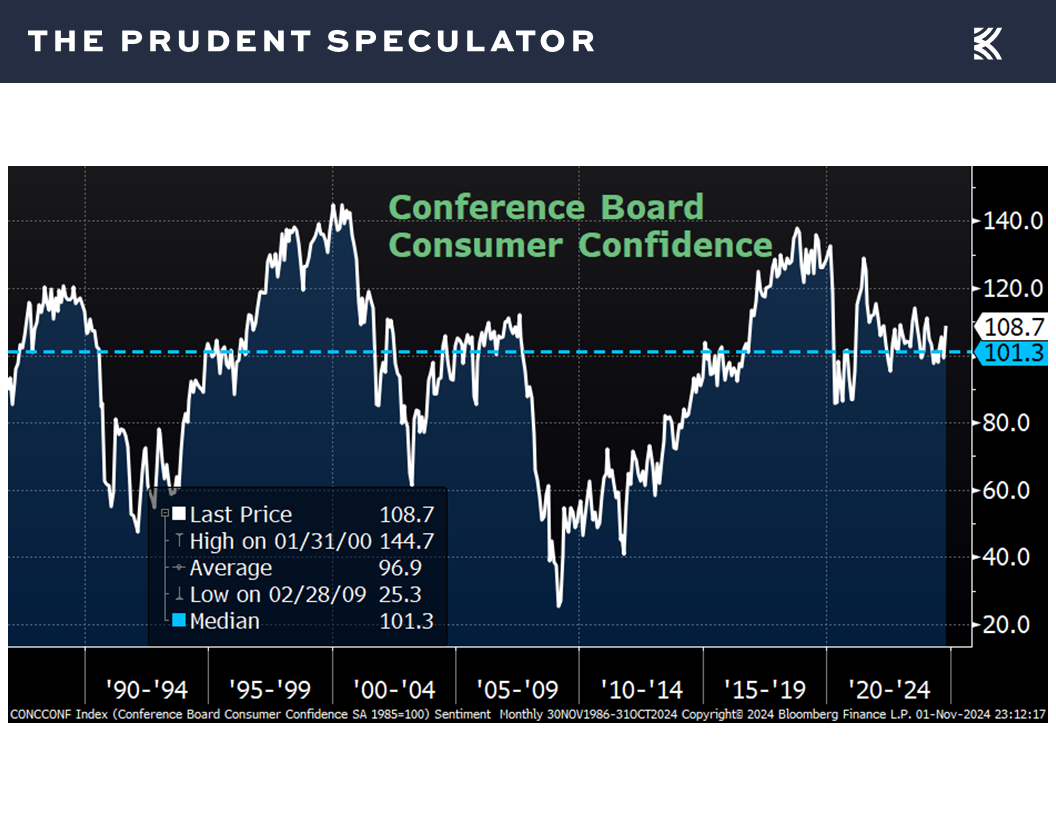

We also learned that consumer confidence, per the Conference Board, jumped to 108.7 last month, well above forecasts of 99.5 and the revised figure of 99.2 for September.

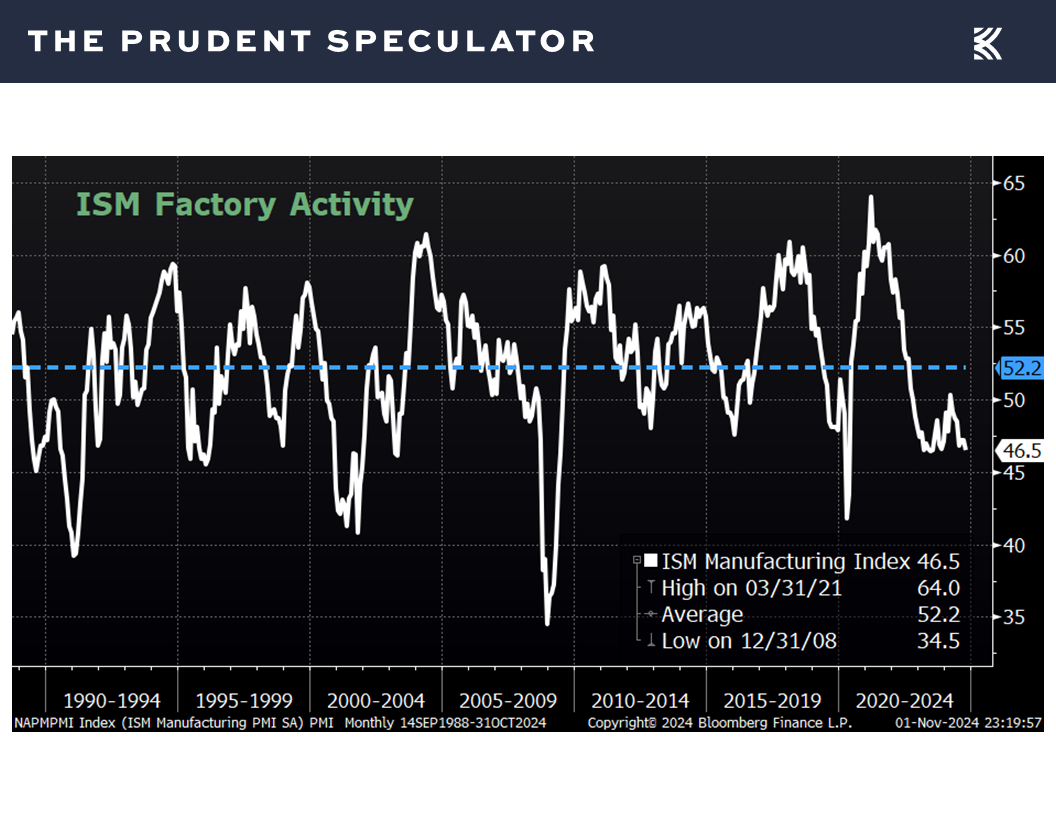

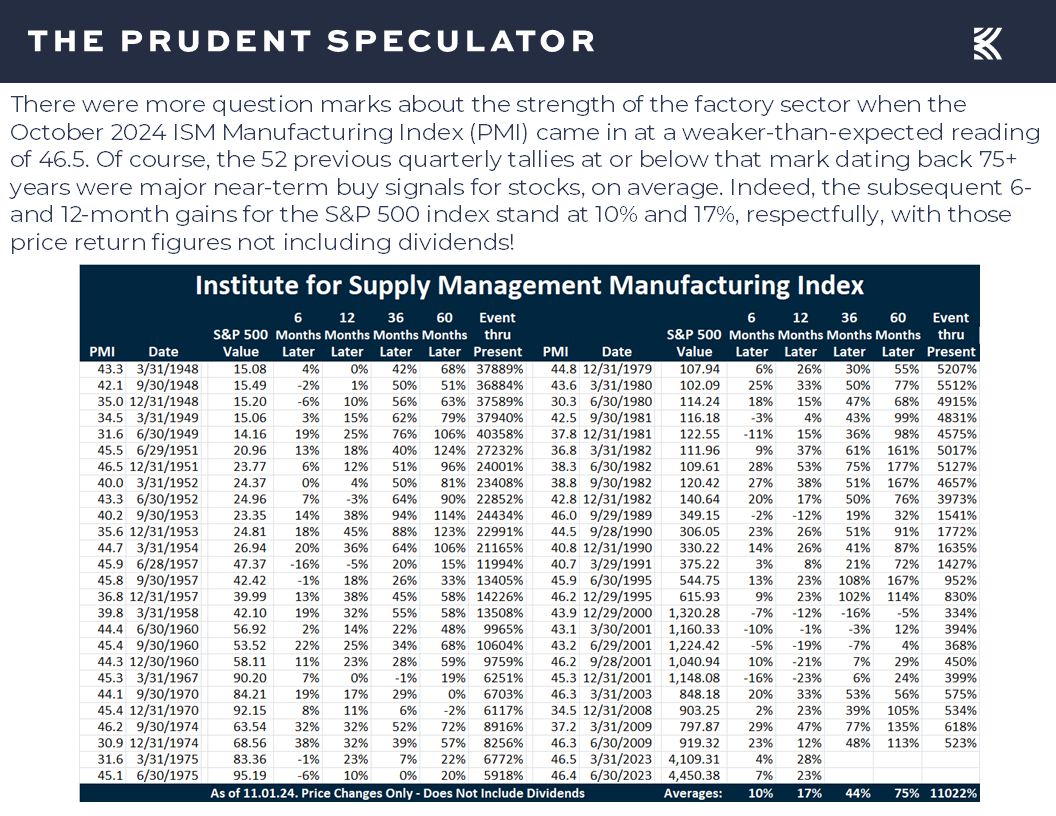

On the negative side of the economic equation, the Institute for Supply Management’s (ISM) gauge of manufacturing activity dipped to 46.5 in October, below the consensus estimate of 47.6 and last month’s reading of 47.2.

For context, we note that ISM states, “The past relationship between the Manufacturing PMI® and the overall economy indicates that the October reading (46.5 percent) corresponds to a change of plus-1.1 percent in real gross domestic product (GDP) on an annualized basis,” while low numbers on this metric, on average, historically have proved to be strong equity market buy signals.

Interest Rates – Yields have Jumped; Stocks Haven’t Minded Historically, on Average

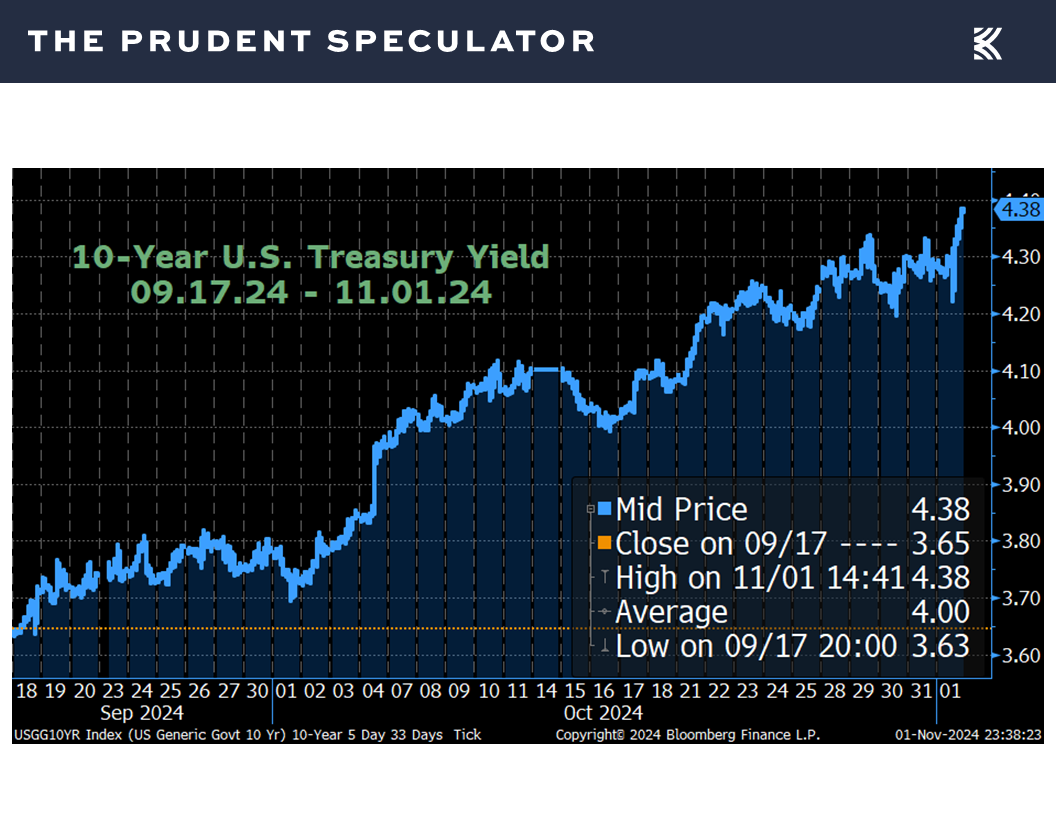

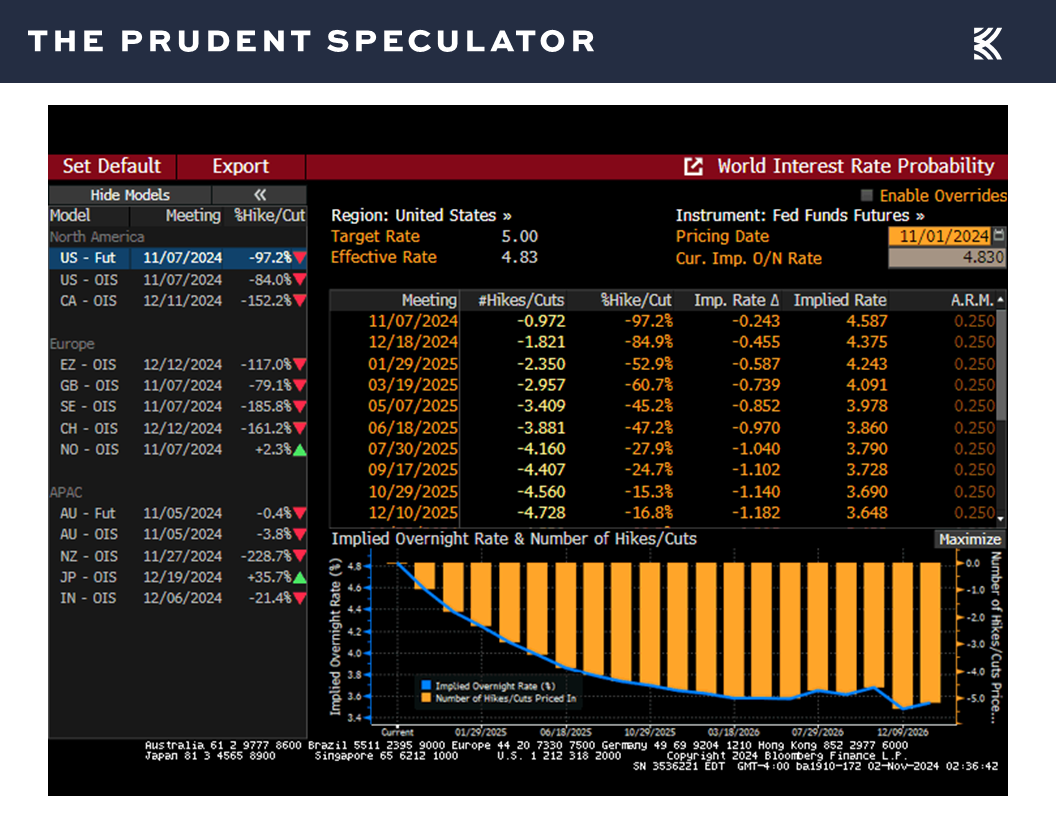

We respect that long-term interest rates jumped anew last week, continuing the significant increase since the Federal Reserve in mid-September cut is target for the Fed Funds rate to 5.0% from 5.5%,

as the betting on additional Fed rate cuts saw the year-end 2025 figure rise to 3.65% at the end of last week, up from 3.52% at the end of the week prior,

Valuations – Value Stocks Reasonably Priced

but valuations for inexpensively priced companies like those that we have long championed remain attractive,

and we continue to like the metrics on our broadly diversified portfolios of what we believe are undervalued stocks even more,

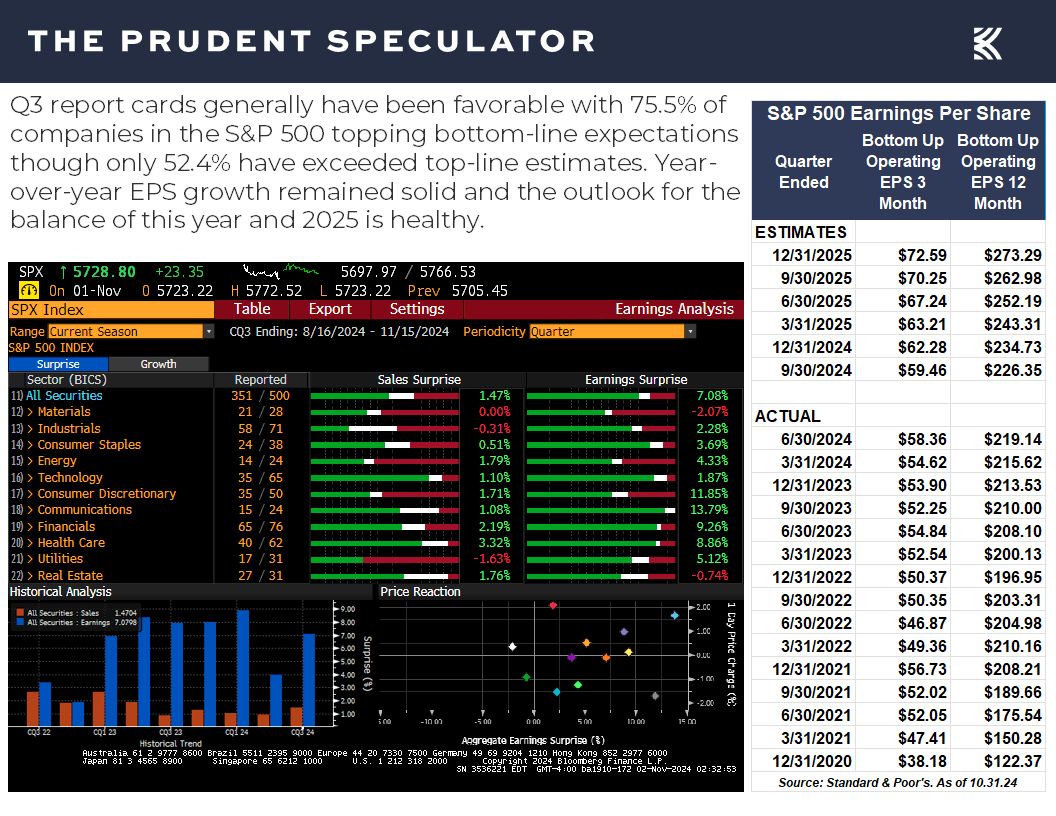

Profits – Favorable EPS Outlook

especially as we think corporate profits in Q4 and in 2025 are likely to continue to show solid growth.

Stock News – Updates on sixteen stocks across eleven different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Election Perspective, Economic Outlook, Interest Rates and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Election Perspective, Seasonally Favorable Period, Economic Outlook and More. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Election Webinar – Replay Available: https://www.youtube.com/watch?v=-YYZf7h_rAg

Election Perspective – Historic Equity Returns

Calendar – Seasonally Favorable Period Has Begun

Inflation – PCE Continues to Head in Right Direction

Econ Outlook – Mixed Stats, but Solid GDP Growth the Forecast

Interest Rates – Yields have Jumped; Stocks Haven’t Minded Historically, on Average

Valuations – Value Stocks Reasonably Priced

Profits – Favorable EPS Outlook

Stock News – Updates on PHG, WM, AMT, PYPL, GLW, GOOG, ZBH, SW, GEN, MSFT, META, FDP, DINO, IP & AAPL

Election Webinar – Replay Available: https://www.youtube.com/watch?v=-YYZf7h_rAg

We would like to thank all who tuned in live to our Election Webinar. For those not able to see the event this past Wednesday, a replay is available here:

Election Perspective – Historic Equity Returns

No doubt, there is plenty on the minds of traders and investors alike these days, especially with Election Day 2024 imminent, so we offer the reminder that stocks have performed fine, on average, no matter who occupies the White House,

while conventional wisdom that one political party is better than the other for equities has NOT been supported, on average, by nine-decades of returns data. True, the number of data points is small, so one should be careful about drawing concrete conclusions, but it is fascinating that stocks have preferred Democrats in Washington to Republicans,

with the reverse true for government bonds.

Obviously, there are numerous factors beyond the resident of 1600 Pennsylvania Avene that have impacted stock prices through the years. Looking at the Presidential terms that ended with red ink for equities, in 1932, the U.S. was in the midst of the Great Depression. Roosevelt’s second term included World War II, while George W.’s first term included the terrorist attacks on September 11 and the second term included the Great Financial Crisis.

Of course, stocks managed to overcome those turbulent periods and numerous other disconcerting headlines, providing terrific long-term rewards for those that remember that time in the market trumps market timing,

as downside volatility has always given way to upside rallies of even greater magnitude, so much so that returns have ranged from 9.1% (non-dividend payers) to 13.1% (Value) per annum since 1927.

Calendar – Seasonally Favorable Period Has Begun

While stocks closed out the historically weak month of October on a sour note,

we would argue that nothing we saw last week on the economic front dissuades us from feeling enthusiastic about the prospects for equities as we head into the seasonally favorable November through April time span.

Inflation – PCE Continues to Head in Right Direction

Indeed, prices at the consumer level edged down a tick in September as the personal consumption expenditure (PCE) index declined to an increase of 2.1% on a year-over-year basis versus 2.2% in August.

The Federal Reserve’s preferred gauge, the Core PCE, which excludes volatile food and energy prices, held steady at a 2.7% increase last month,

but inflation continues to trend in the right direction and has moved closer to the year-end projections offered in September by Federal Reserve Board members and Federal Reserve Bank presidents.

Econ Outlook – Mixed Stats, but Solid GDP Growth the Forecast

Those forecasts also called for real (inflation-adjusted) U.S. GDP growth of 2.0% this year, a figure that might prove conservative after the first estimate of Q3 GDP growth came in at 2.8% last week,

while the initial guess for Q4 GDP growth from the Atlanta Fed stood at 2.3%,

even after nonfarm payrolls rose by only 12,000 in October, well below expectations of growth of 100,000 and the revised tally of 223,000 in September.

To be sure, Hurricane’s Helene and Milton has a significant impact on the jobs numbers, and the unemployment rate for October was unchanged at 4.1%,

while a more up-to-date reading on the labor market, weekly claims for first-time jobless benefits, saw a drop to a very low 216,000, compared to a revised 228,000 the week prior.

We also learned that consumer confidence, per the Conference Board, jumped to 108.7 last month, well above forecasts of 99.5 and the revised figure of 99.2 for September.

On the negative side of the economic equation, the Institute for Supply Management’s (ISM) gauge of manufacturing activity dipped to 46.5 in October, below the consensus estimate of 47.6 and last month’s reading of 47.2.

For context, we note that ISM states, “The past relationship between the Manufacturing PMI® and the overall economy indicates that the October reading (46.5 percent) corresponds to a change of plus-1.1 percent in real gross domestic product (GDP) on an annualized basis,” while low numbers on this metric, on average, historically have proved to be strong equity market buy signals.

Interest Rates – Yields have Jumped; Stocks Haven’t Minded Historically, on Average

We respect that long-term interest rates jumped anew last week, continuing the significant increase since the Federal Reserve in mid-September cut is target for the Fed Funds rate to 5.0% from 5.5%,

as the betting on additional Fed rate cuts saw the year-end 2025 figure rise to 3.65% at the end of last week, up from 3.52% at the end of the week prior,

Valuations – Value Stocks Reasonably Priced

but valuations for inexpensively priced companies like those that we have long championed remain attractive,

and we continue to like the metrics on our broadly diversified portfolios of what we believe are undervalued stocks even more,

Profits – Favorable EPS Outlook

especially as we think corporate profits in Q4 and in 2025 are likely to continue to show solid growth.

Stock News – Updates on sixteen stocks across eleven different sectors

About the Author

Phil Edwards

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.