The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss volatility, inflation, valuations, the AAII Sentiment and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Volatility – Ups & Downs are Normal; Stocks Have Persevered Through Plenty of Disconcerting Events

Econ Update – Better-than-Expected Numbers

Inflation – PCE In Line with Forecasts; Fed Likely on Hold

Valuations – Stocks, Especially Value, Reasonably Priced

Sentiment – AAII Becomes Much More Bearish

Stock News – Updates on nineteen stocks across eleven different sectors

Volatility – Ups & Downs are Normal; Stocks Have Persevered Through Plenty of Disconcerting Events

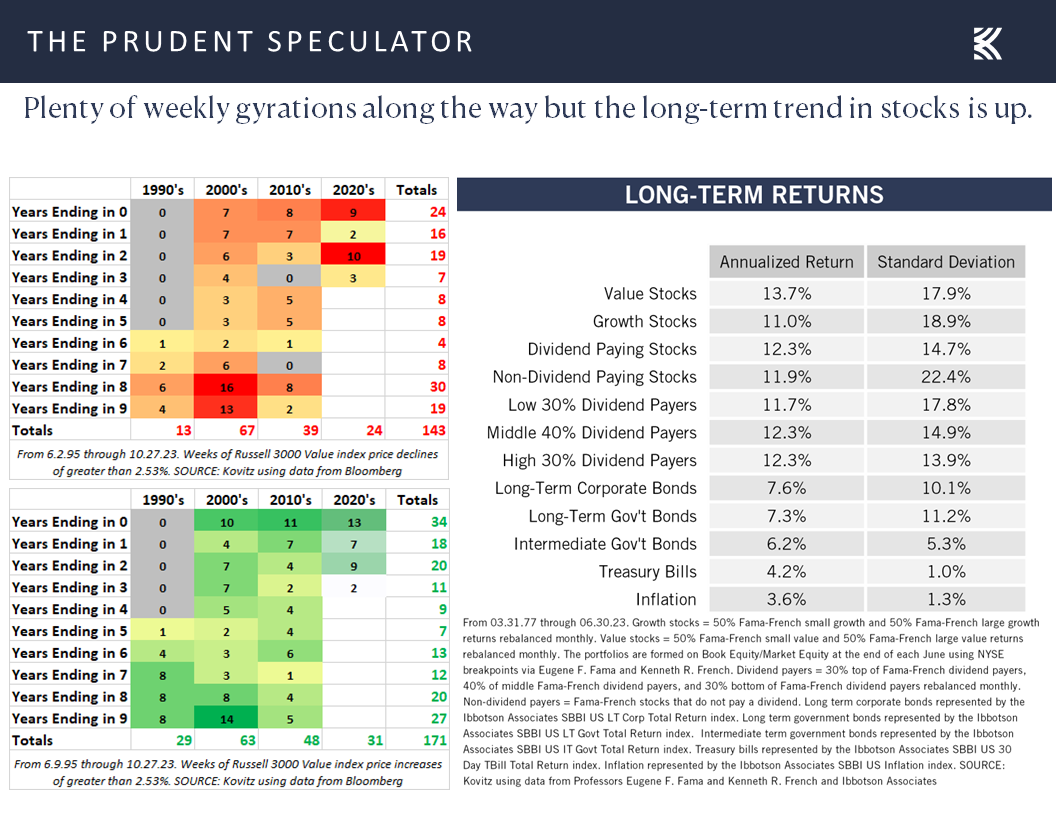

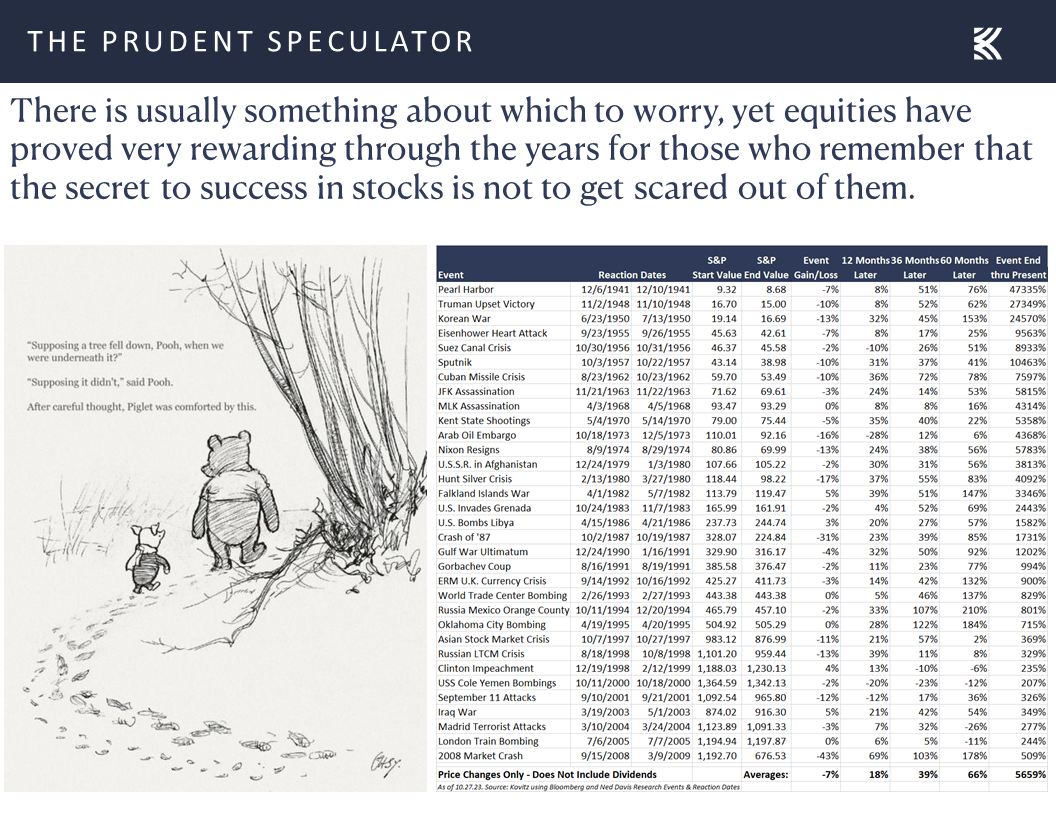

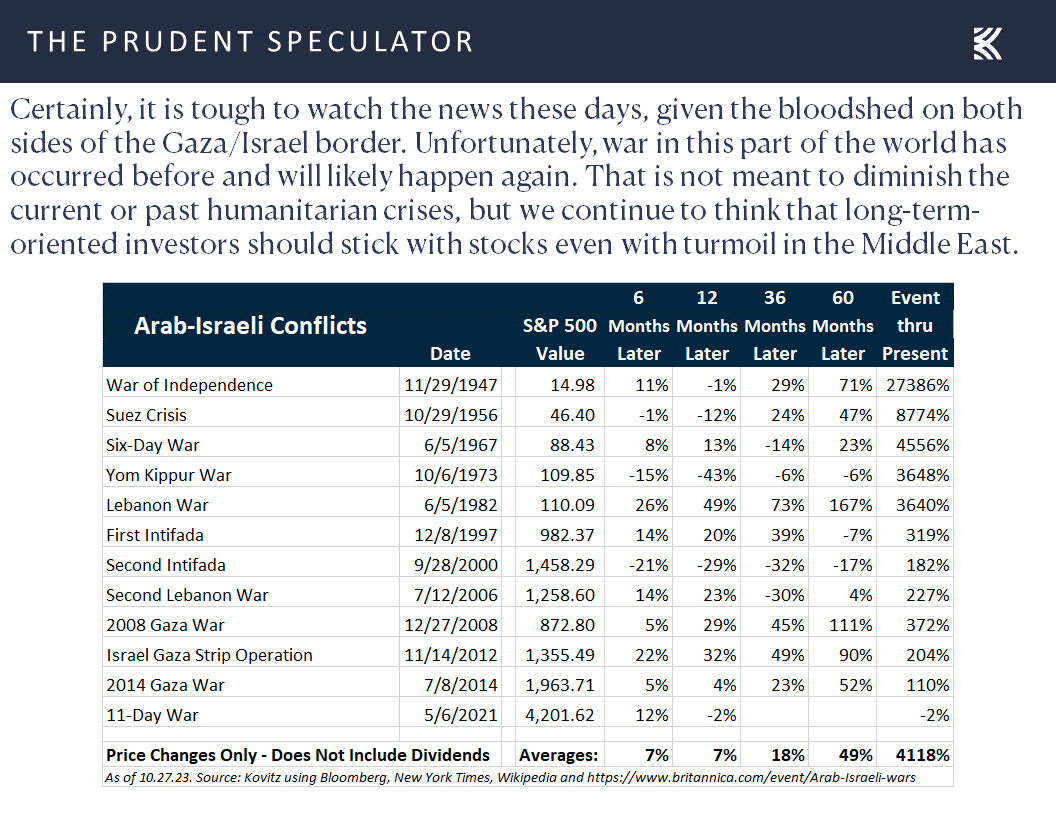

With a mass murderer on the loose in Maine and an escalation of Israel’s operations in Gaza, it was difficult for traders last week to focus on anything but those disconcerting headlines. Alas, equities suffered another sizable decline, with the Russell 3000 Value index losing nearly 2.54% on a price basis, the 143rd worst week over the last 28 years.

Obviously, given that Value stocks have enjoyed terrific returns of 13.7% per annum since the launch of The Prudent Speculator in 1977, with Dividend Payers seeing an average annualized return of 12.3%, there have been plenty of positive weeks as well,

with uncertainty seemingly always something with which investors must contend.

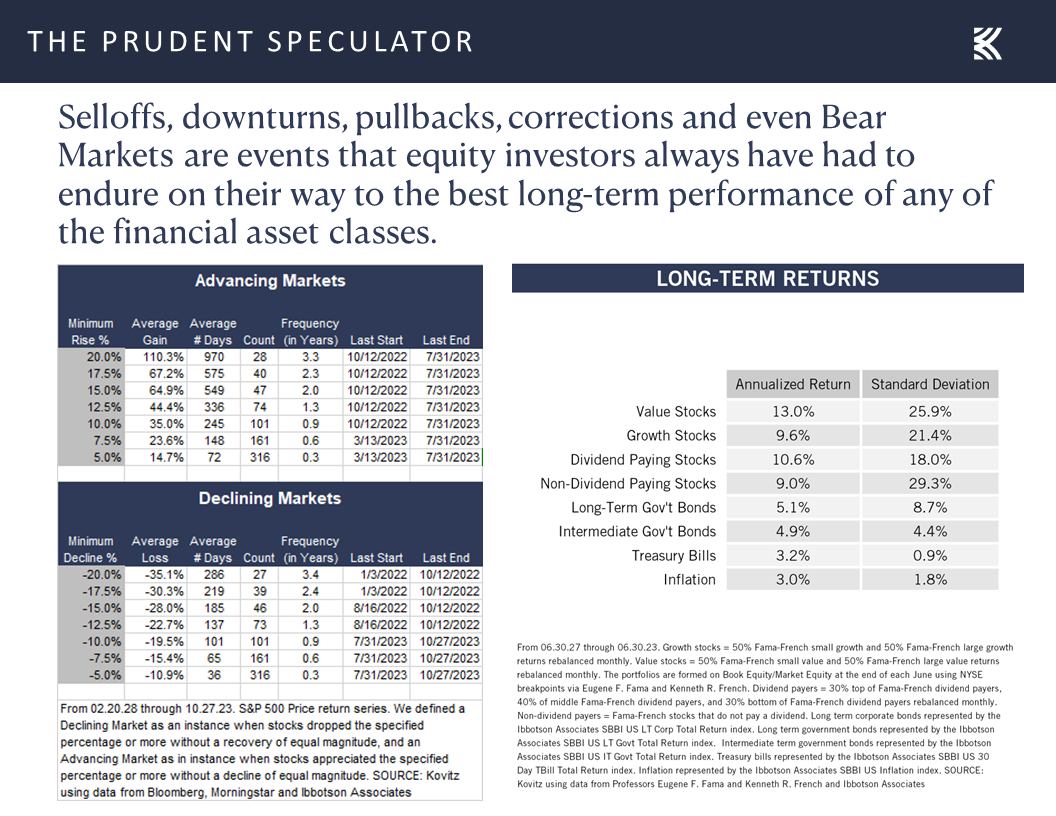

To be sure, volatility will always be part of the investment equation, and the tech-centric S&P 500 index is now suffered a 10% decline from the summer highs, something that has happened 101 times going back to 1926. So-called corrections have taken place every 11 months or so, on average, despite the stellar long-term returns on average for stocks over those nine-plus decades,

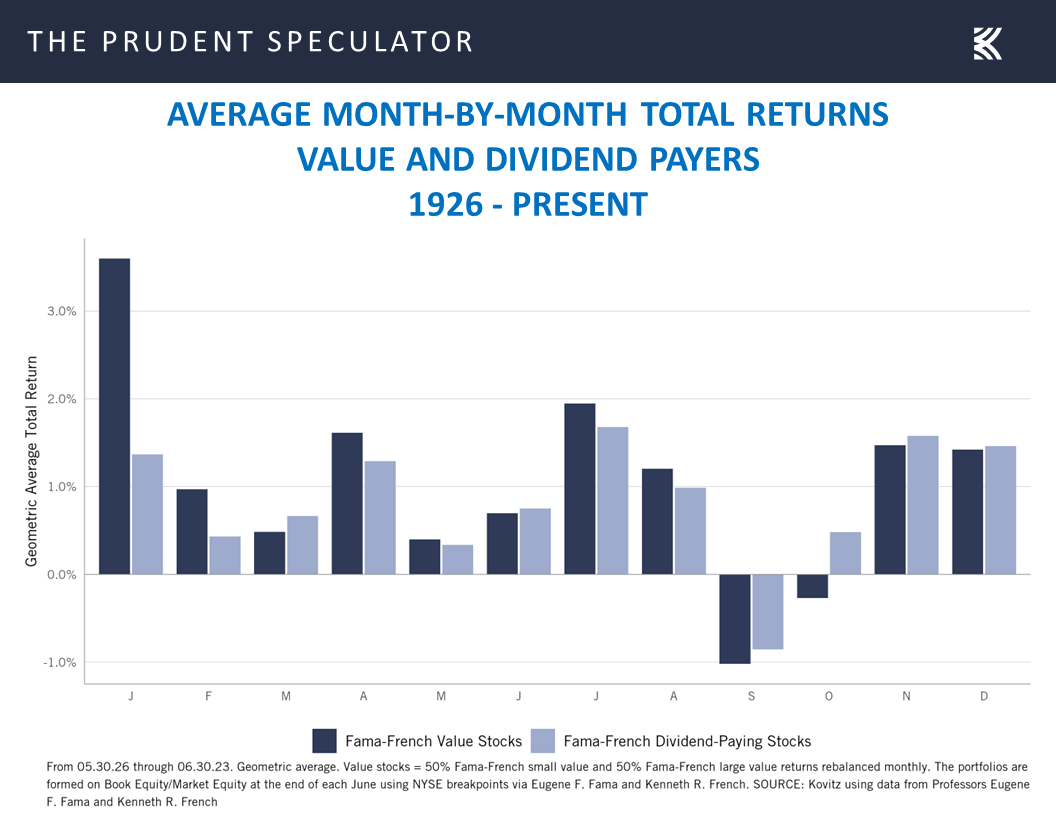

while history shows that September and October are the only two months of the year where Value stocks have suffered losses, on average.

Econ Update – Better-than-Expected Numbers

Of course, anything can happen as we go forward, and we suspect developments in the Middle East will have a sizable impact on the near-term direction stocks traverse,

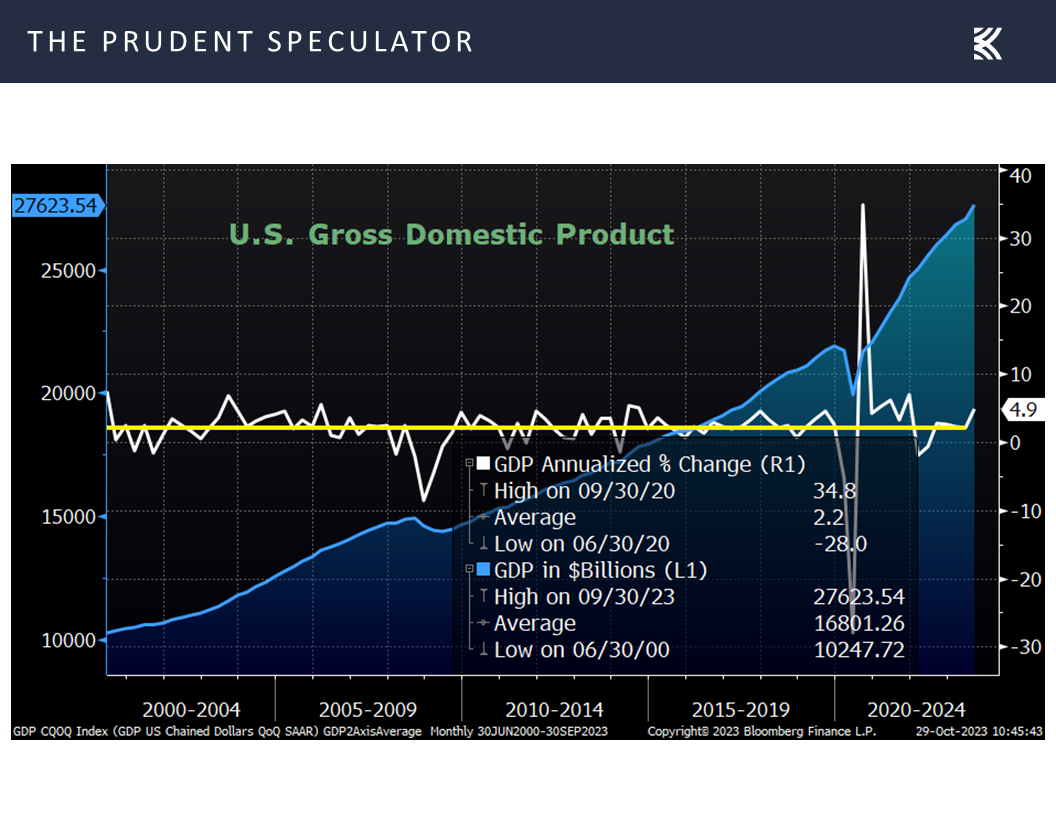

but we are now only two trading days from the start of the seasonally favorable six month of the year, while the economic news out last week might have led to a sizable equity rally under more normal geopolitical conditions. After all, Q3 U.S. GDP growth came in better than expected at a 4.9% real (inflation-adjusted) rate,

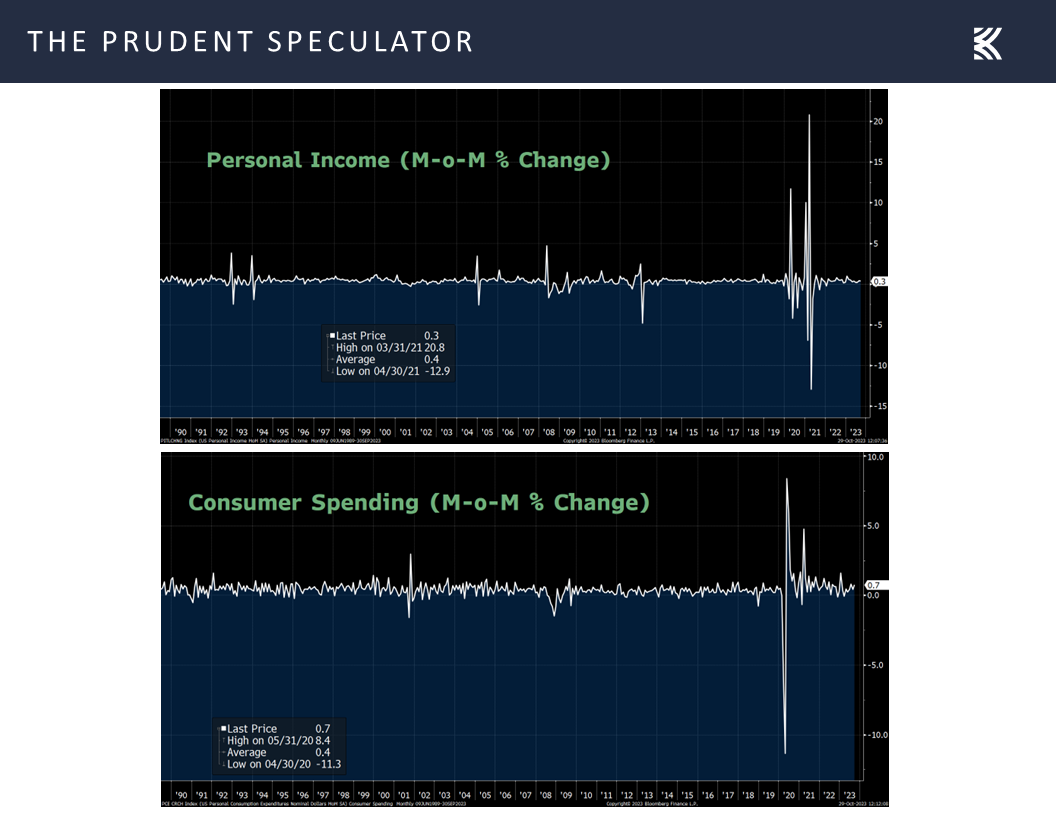

as consumer spending remained robust, while personal incomes grew modestly.

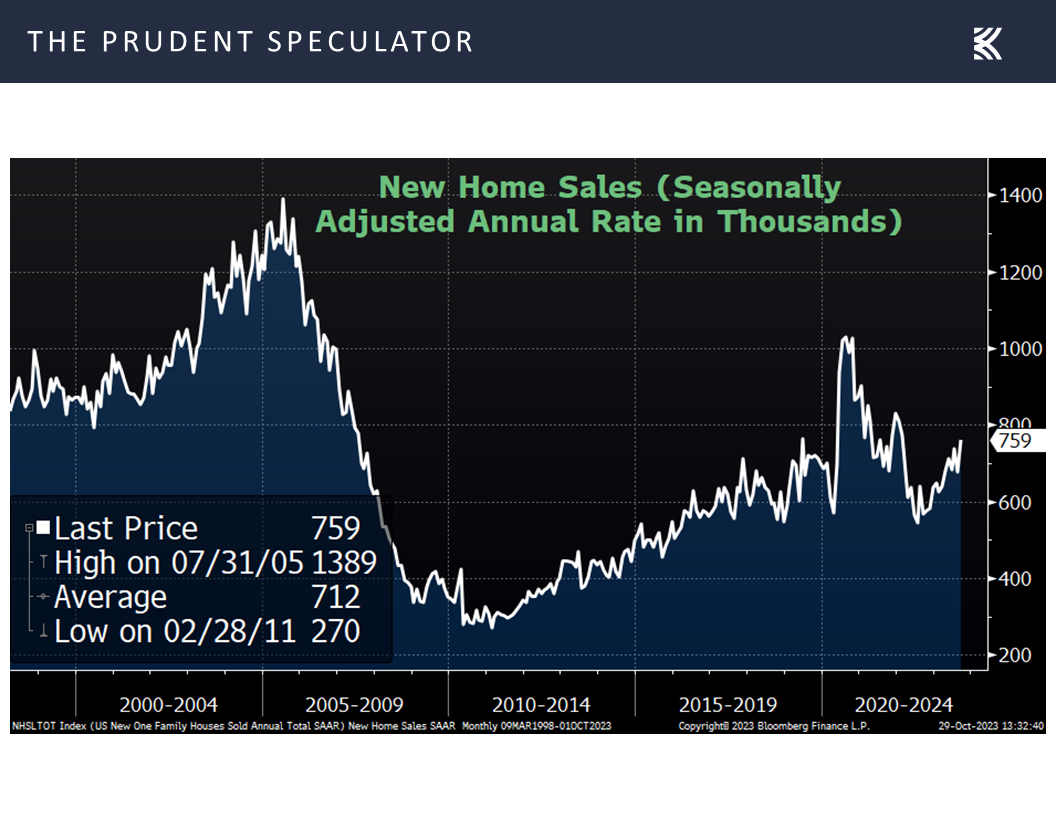

The housing market also held up better than most might have thought in September, with both new home sales,

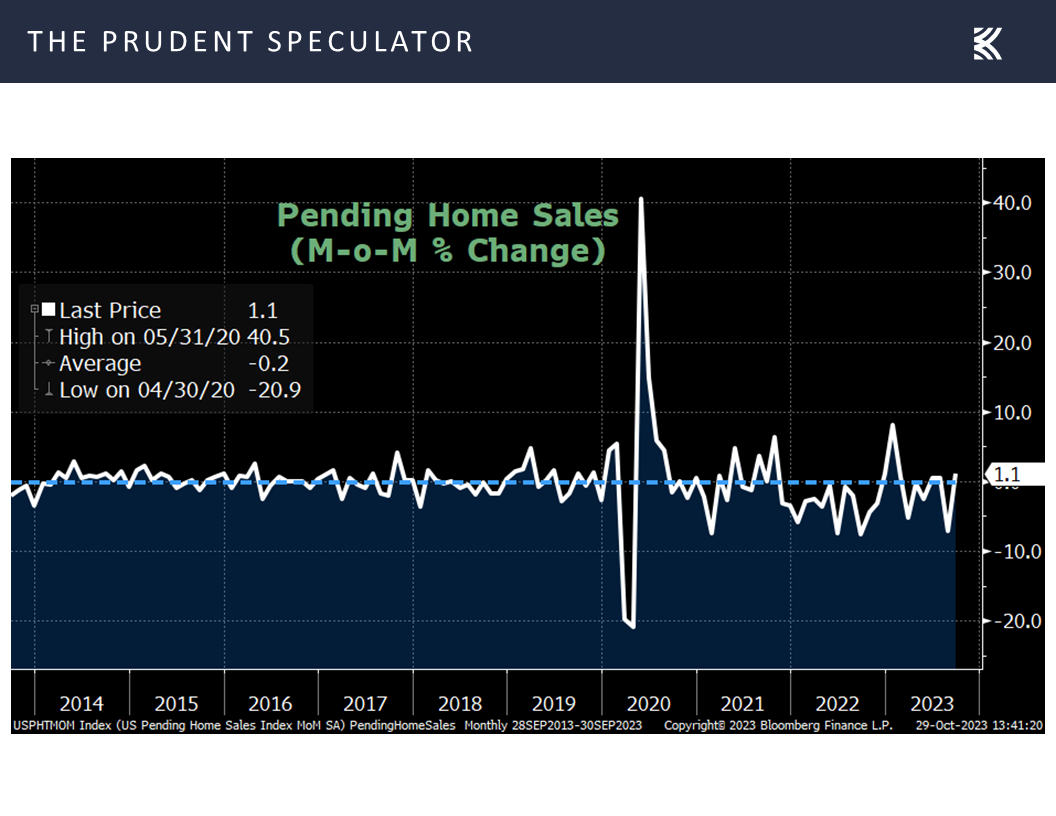

and pending sales of existing homes topping much-more-pessimistic estimates.

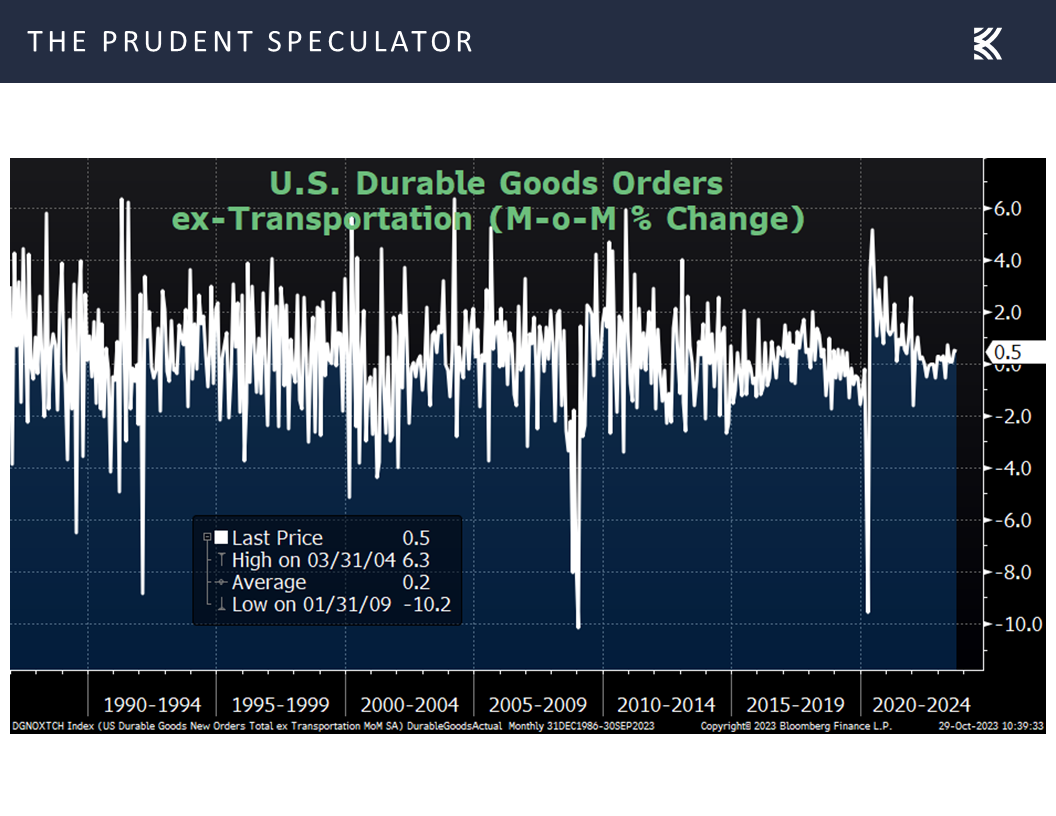

Looking ahead, orders for durable goods exceeded expectations in September, with a 0.5% advance excluding the volatile transportation sector,

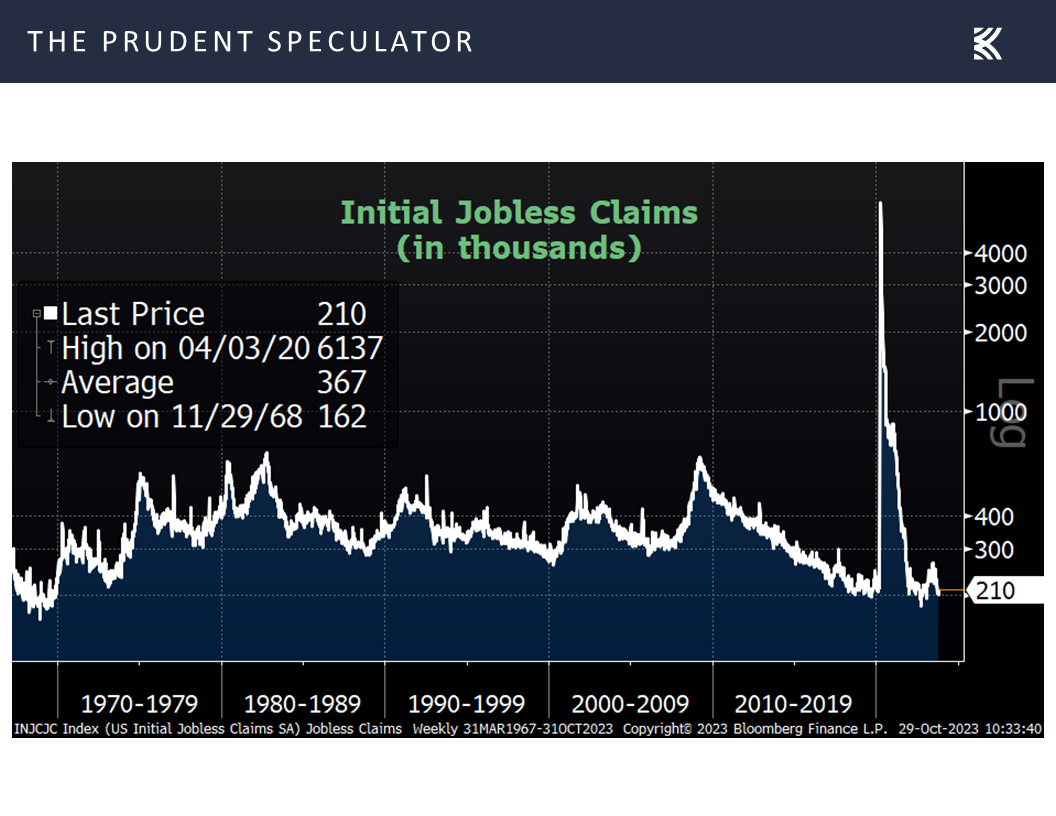

first-time filings for unemployment benefits continued to rest near multi-generational lows,

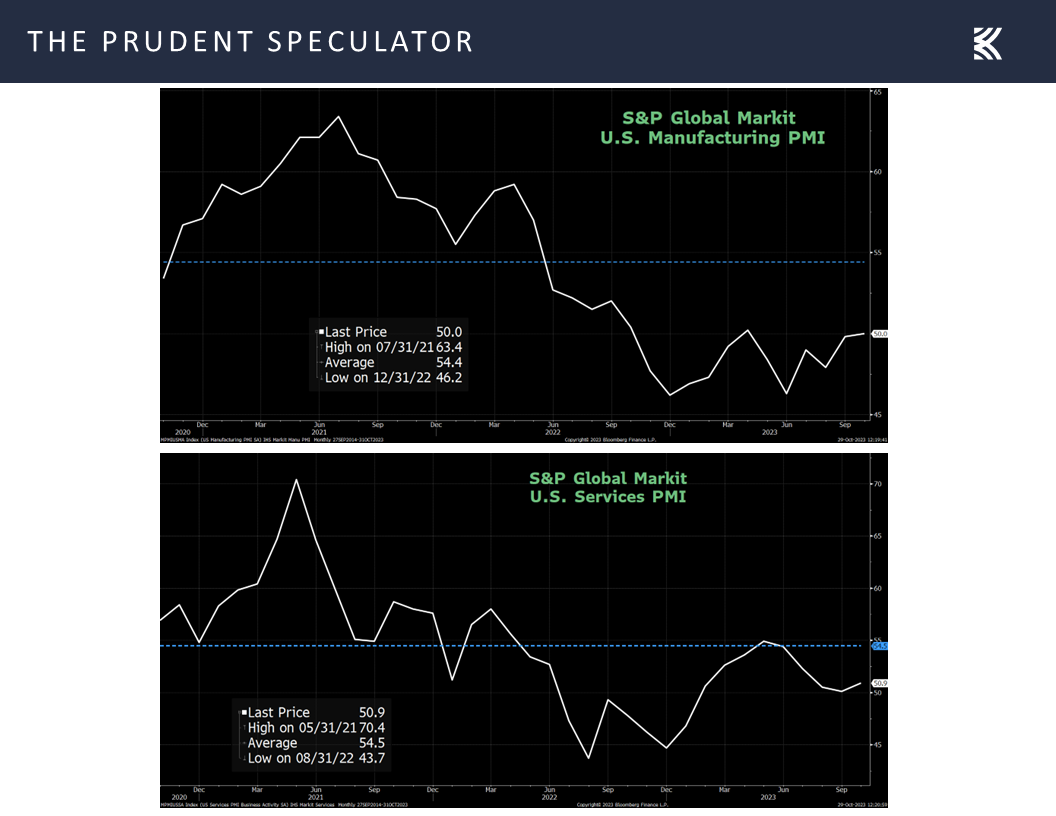

and the October factory and service sector PMI’s as calculated by Standard & Poor’s beat forecasts, with Chris Williamson, chief business economist at S&P Global Market Intelligence, stating, “Hopes of a soft landing for the U.S. economy will be encouraged by the improved situation seen in October.”

The initial estimate for Q4 real GDP growth from the Atlanta Fed came in at a solid 2.3%,

The initial estimate for Q4 real GDP growth from the Atlanta Fed came in at a solid 2.3%,

and the probability calculation for a recession in the next 12 months as tabulated by Bloomberg continued to reside at an elevated 55%.

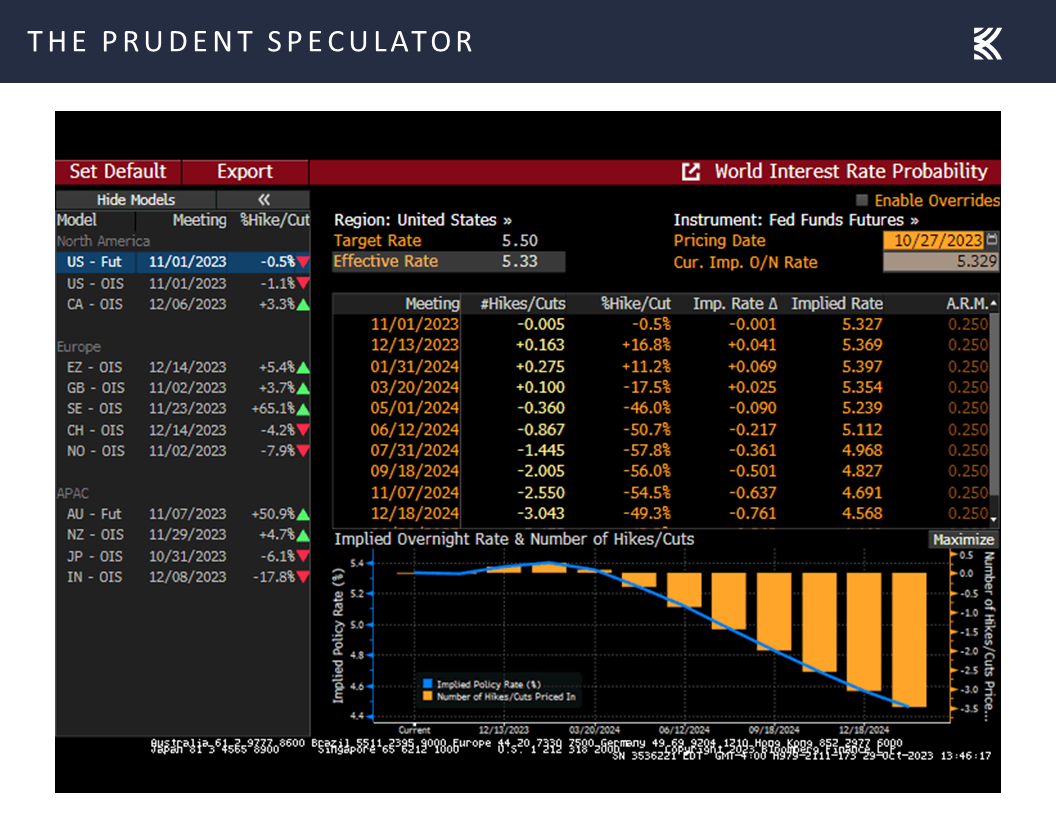

Inflation – PCE In Line with Forecasts; Fed Likely on Hold

Turing to the inflation outlook, the Federal Reserve’s preferred price measure, the core personal consumption expenditure index rose 3.7% in September, in line with expectations.

True, there was some concern that near-term consumer inflation expectations have moved higher this month, but longer-term estimates remained reasonably well-anchored,

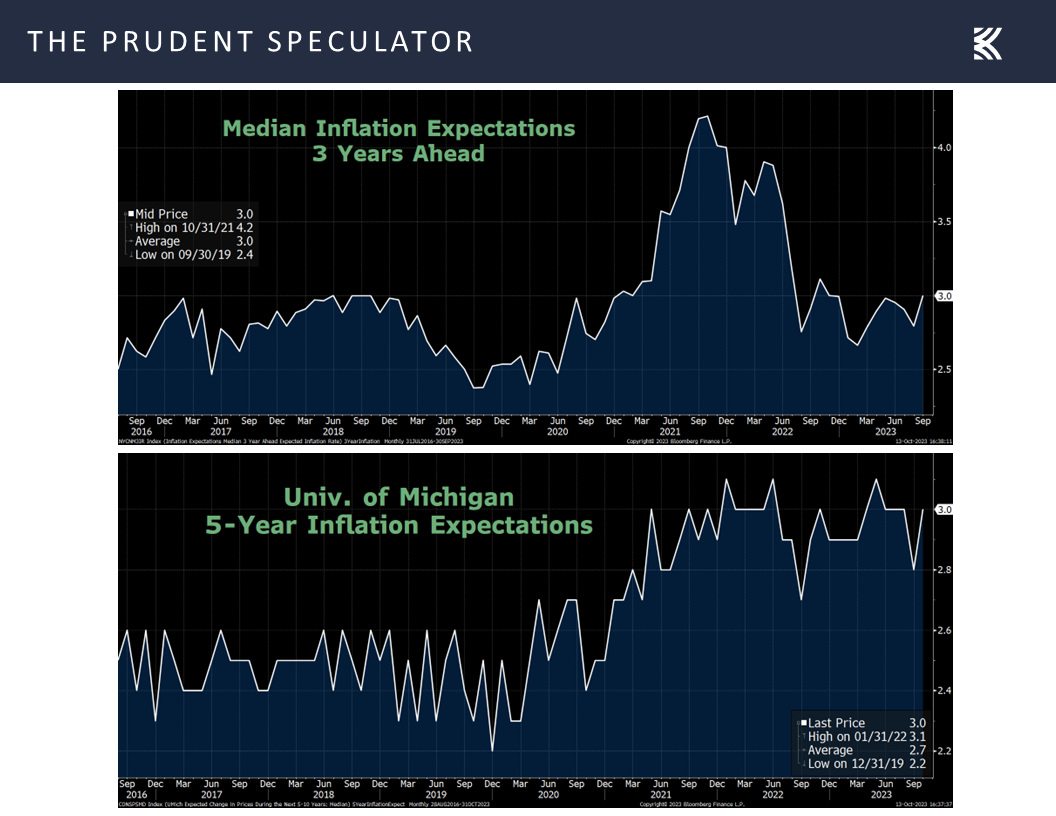

True, there was some concern that near-term consumer inflation expectations have moved higher this month, but longer-term estimates remained reasonably well-anchored,

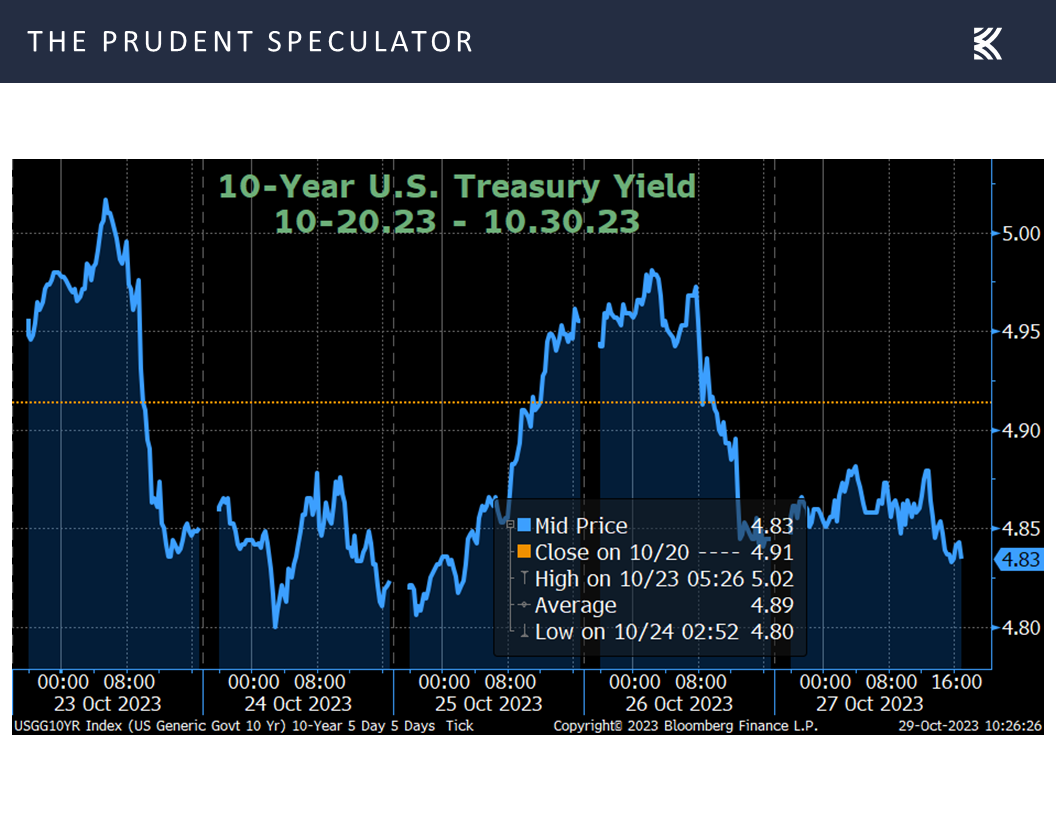

while the benchmark 10-Year U.S. Treasury yield fell from 4.91% to 4.83%.

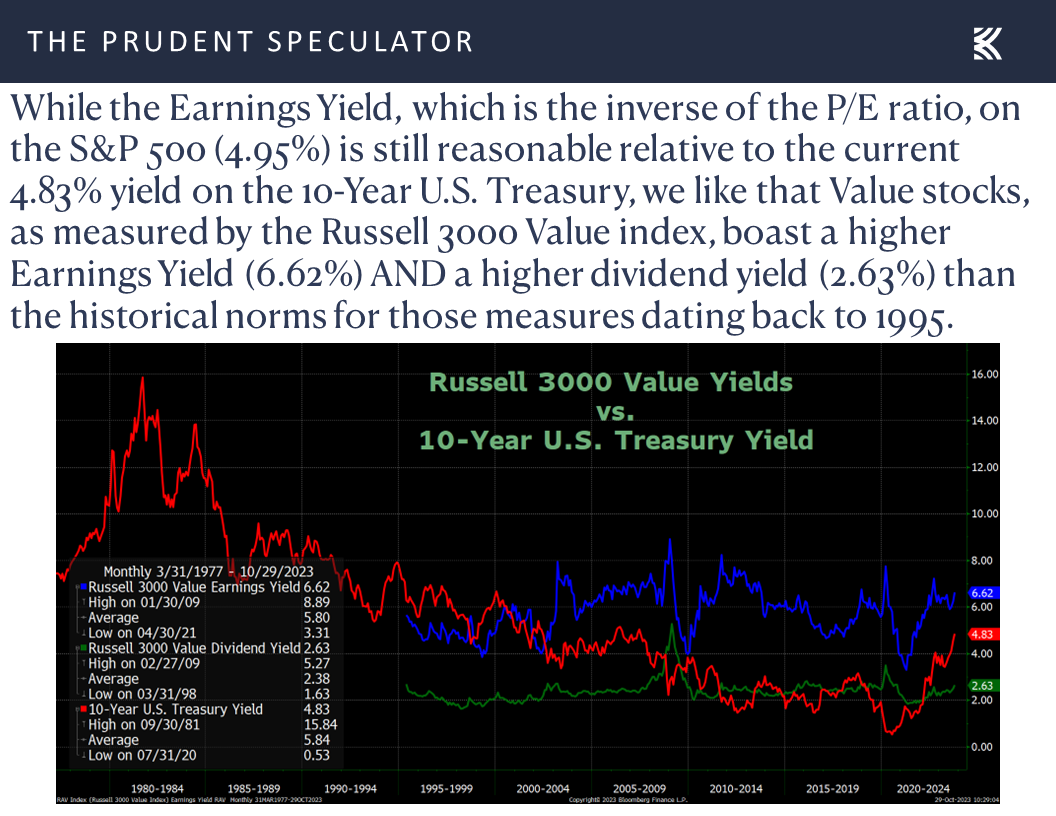

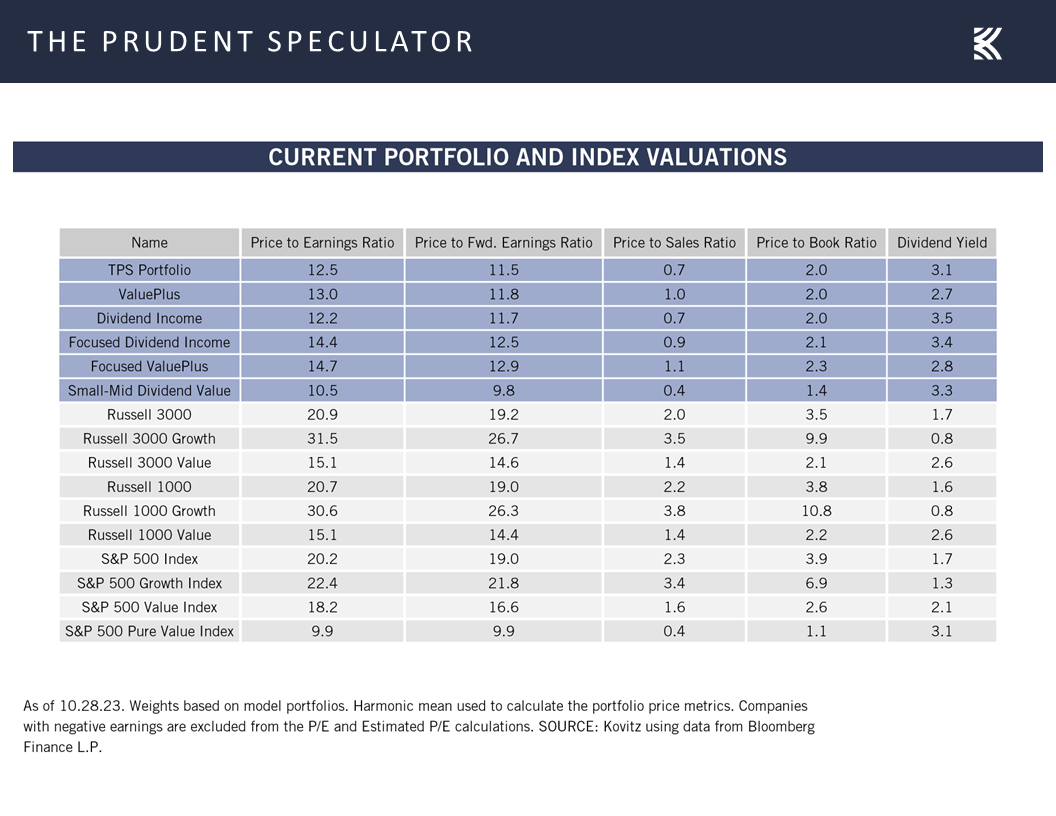

Valuations – Stocks, Especially Value, Reasonably Priced

As we constantly state, we are braced for additional equity market downside, but we see no reason to alter our long-term enthusiasm for equities, especially given the reasonable valuations for Value stocks in general,

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular.

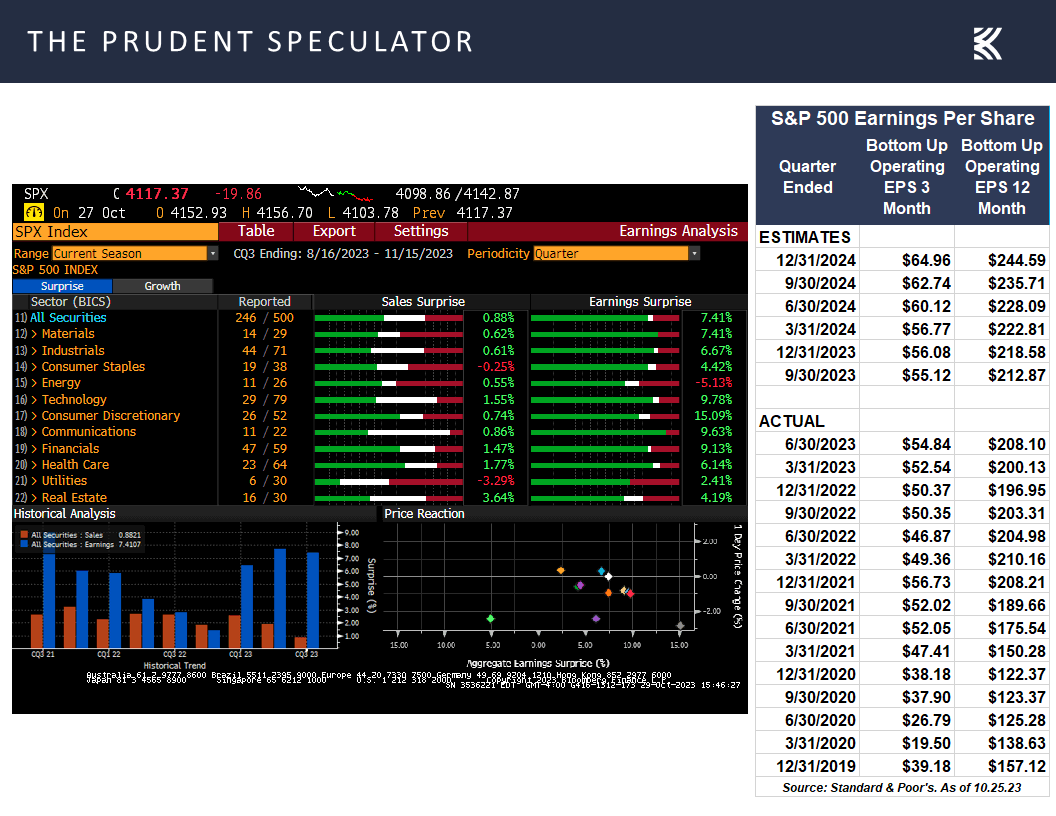

There have been negative reactions to more than few quarterly reports from Corporate America of late, but we think the Earnings component of the P/E equation is poised for continued growth,

Sentiment – AAII Becomes Much More Bearish

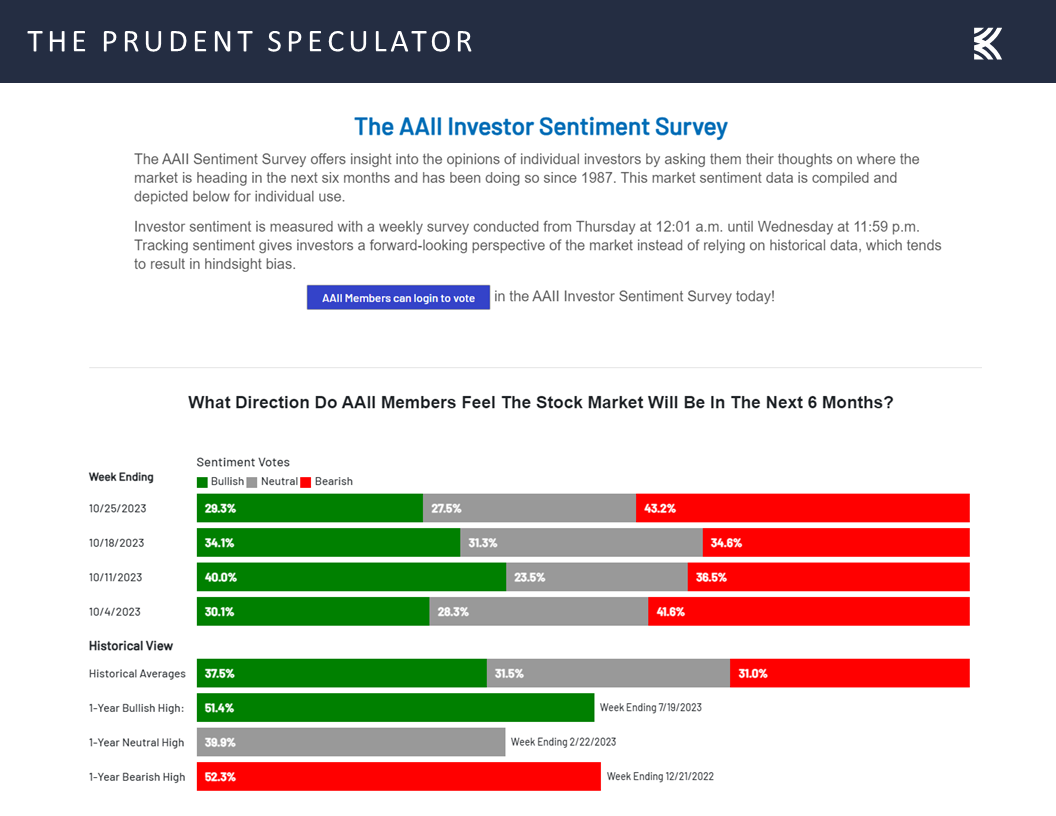

while we are not unhappy, given our contrarian nature, that folks on Main Street have again become pessimistic, with the latest Sentiment Survey from the American Association of Individual Investors (AAII) seeing a 4.8-point drop in the Bulls and an 8.6-point rise in the Bears.

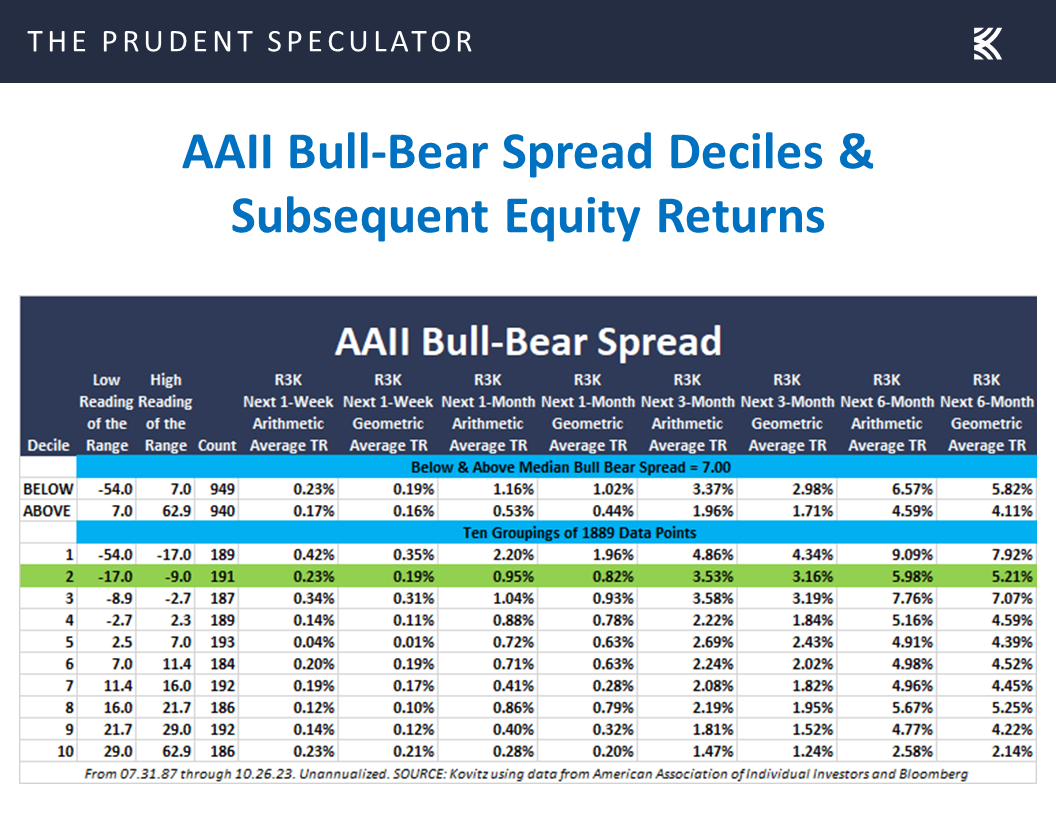

There are never any assurances that past performance is indicative of future performance, but there is a historical reason that AAII is widely viewed as a contra-indicator. We aren’t quite to the most-Bearish-Sentiment-best-forward-returns decile, but the second decile in which we now reside has been a place we have liked to dwell in years gone by, on average!

Stock News – Updates on nineteen stocks across eleven different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Volatility, Inflation, Valuations, AAII Sentiment and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss volatility, inflation, valuations, the AAII Sentiment and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Volatility – Ups & Downs are Normal; Stocks Have Persevered Through Plenty of Disconcerting Events

Econ Update – Better-than-Expected Numbers

Inflation – PCE In Line with Forecasts; Fed Likely on Hold

Valuations – Stocks, Especially Value, Reasonably Priced

Sentiment – AAII Becomes Much More Bearish

Stock News – Updates on nineteen stocks across eleven different sectors

Volatility – Ups & Downs are Normal; Stocks Have Persevered Through Plenty of Disconcerting Events

With a mass murderer on the loose in Maine and an escalation of Israel’s operations in Gaza, it was difficult for traders last week to focus on anything but those disconcerting headlines. Alas, equities suffered another sizable decline, with the Russell 3000 Value index losing nearly 2.54% on a price basis, the 143rd worst week over the last 28 years.

Obviously, given that Value stocks have enjoyed terrific returns of 13.7% per annum since the launch of The Prudent Speculator in 1977, with Dividend Payers seeing an average annualized return of 12.3%, there have been plenty of positive weeks as well,

with uncertainty seemingly always something with which investors must contend.

To be sure, volatility will always be part of the investment equation, and the tech-centric S&P 500 index is now suffered a 10% decline from the summer highs, something that has happened 101 times going back to 1926. So-called corrections have taken place every 11 months or so, on average, despite the stellar long-term returns on average for stocks over those nine-plus decades,

while history shows that September and October are the only two months of the year where Value stocks have suffered losses, on average.

Econ Update – Better-than-Expected Numbers

Of course, anything can happen as we go forward, and we suspect developments in the Middle East will have a sizable impact on the near-term direction stocks traverse,

but we are now only two trading days from the start of the seasonally favorable six month of the year, while the economic news out last week might have led to a sizable equity rally under more normal geopolitical conditions. After all, Q3 U.S. GDP growth came in better than expected at a 4.9% real (inflation-adjusted) rate,

as consumer spending remained robust, while personal incomes grew modestly.

The housing market also held up better than most might have thought in September, with both new home sales,

and pending sales of existing homes topping much-more-pessimistic estimates.

Looking ahead, orders for durable goods exceeded expectations in September, with a 0.5% advance excluding the volatile transportation sector,

first-time filings for unemployment benefits continued to rest near multi-generational lows,

and the October factory and service sector PMI’s as calculated by Standard & Poor’s beat forecasts, with Chris Williamson, chief business economist at S&P Global Market Intelligence, stating, “Hopes of a soft landing for the U.S. economy will be encouraged by the improved situation seen in October.”

The initial estimate for Q4 real GDP growth from the Atlanta Fed came in at a solid 2.3%,

The initial estimate for Q4 real GDP growth from the Atlanta Fed came in at a solid 2.3%,

and the probability calculation for a recession in the next 12 months as tabulated by Bloomberg continued to reside at an elevated 55%.

Inflation – PCE In Line with Forecasts; Fed Likely on Hold

Turing to the inflation outlook, the Federal Reserve’s preferred price measure, the core personal consumption expenditure index rose 3.7% in September, in line with expectations.

True, there was some concern that near-term consumer inflation expectations have moved higher this month, but longer-term estimates remained reasonably well-anchored,

True, there was some concern that near-term consumer inflation expectations have moved higher this month, but longer-term estimates remained reasonably well-anchored,

while the benchmark 10-Year U.S. Treasury yield fell from 4.91% to 4.83%.

Valuations – Stocks, Especially Value, Reasonably Priced

As we constantly state, we are braced for additional equity market downside, but we see no reason to alter our long-term enthusiasm for equities, especially given the reasonable valuations for Value stocks in general,

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular.

There have been negative reactions to more than few quarterly reports from Corporate America of late, but we think the Earnings component of the P/E equation is poised for continued growth,

Sentiment – AAII Becomes Much More Bearish

while we are not unhappy, given our contrarian nature, that folks on Main Street have again become pessimistic, with the latest Sentiment Survey from the American Association of Individual Investors (AAII) seeing a 4.8-point drop in the Bulls and an 8.6-point rise in the Bears.

There are never any assurances that past performance is indicative of future performance, but there is a historical reason that AAII is widely viewed as a contra-indicator. We aren’t quite to the most-Bearish-Sentiment-best-forward-returns decile, but the second decile in which we now reside has been a place we have liked to dwell in years gone by, on average!

Stock News – Updates on nineteen stocks across eleven different sectors

About the Author

Phil Edwards

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.