The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s Market Commentary, we discuss AAII Sentiment, Tariffs, Earnings, Interest Rates and More. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 10 Buys for 4 Portfolios

Week – S&P Recaptures 6000

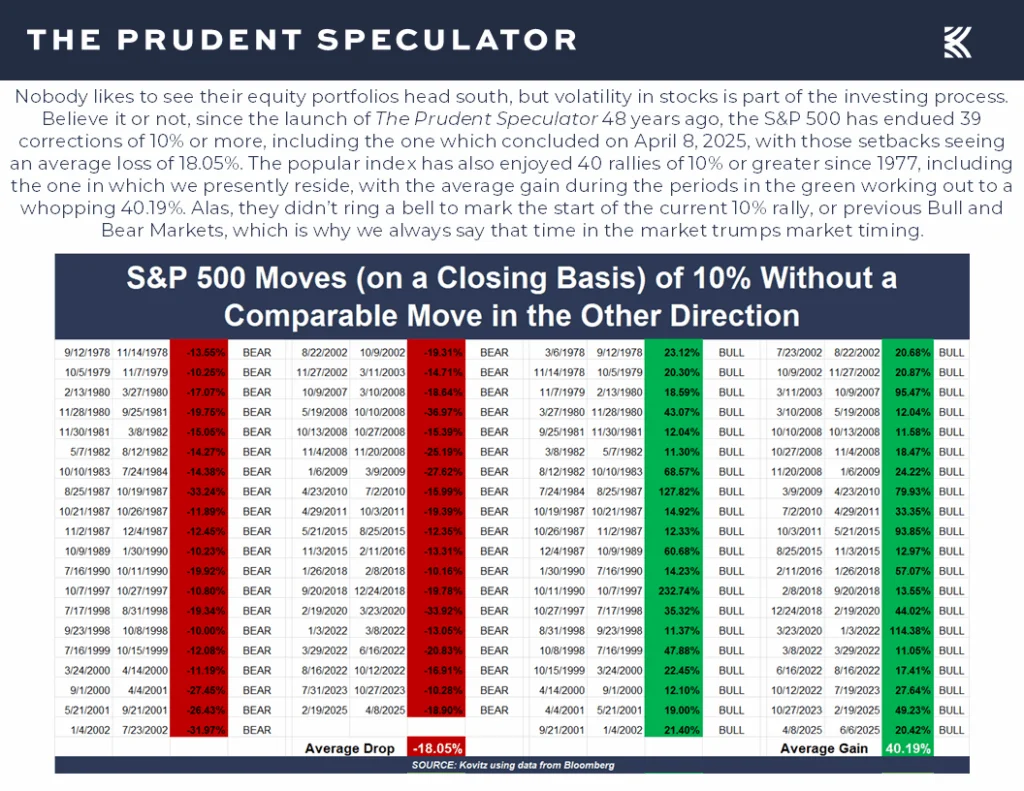

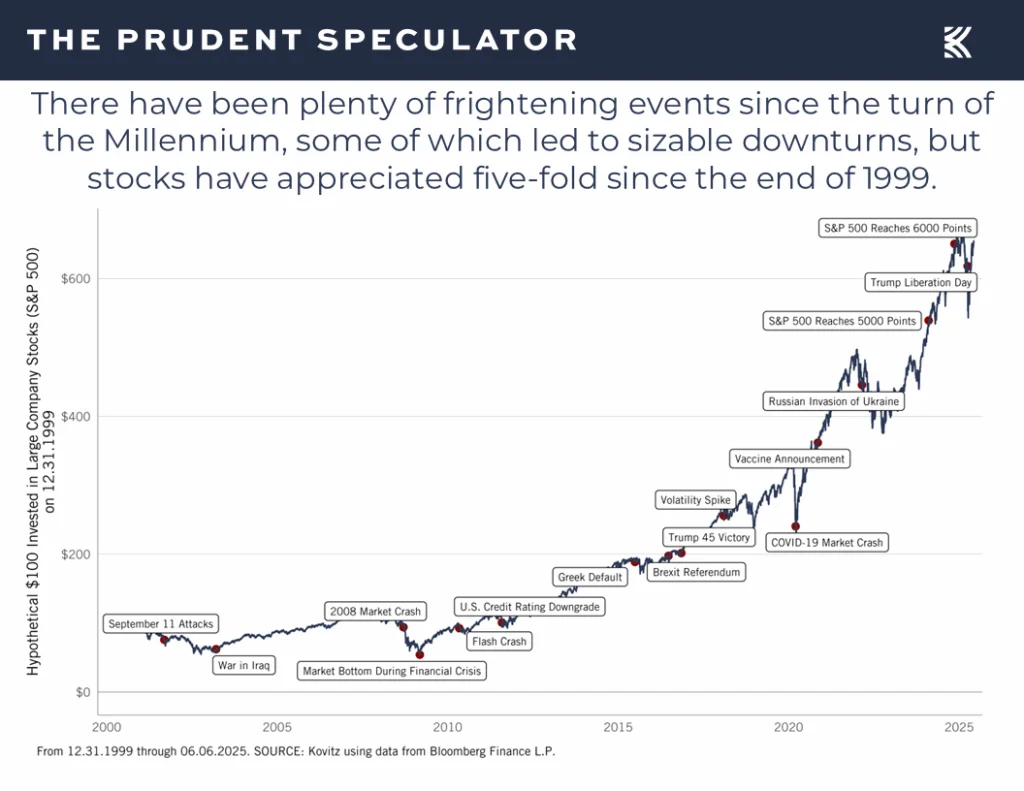

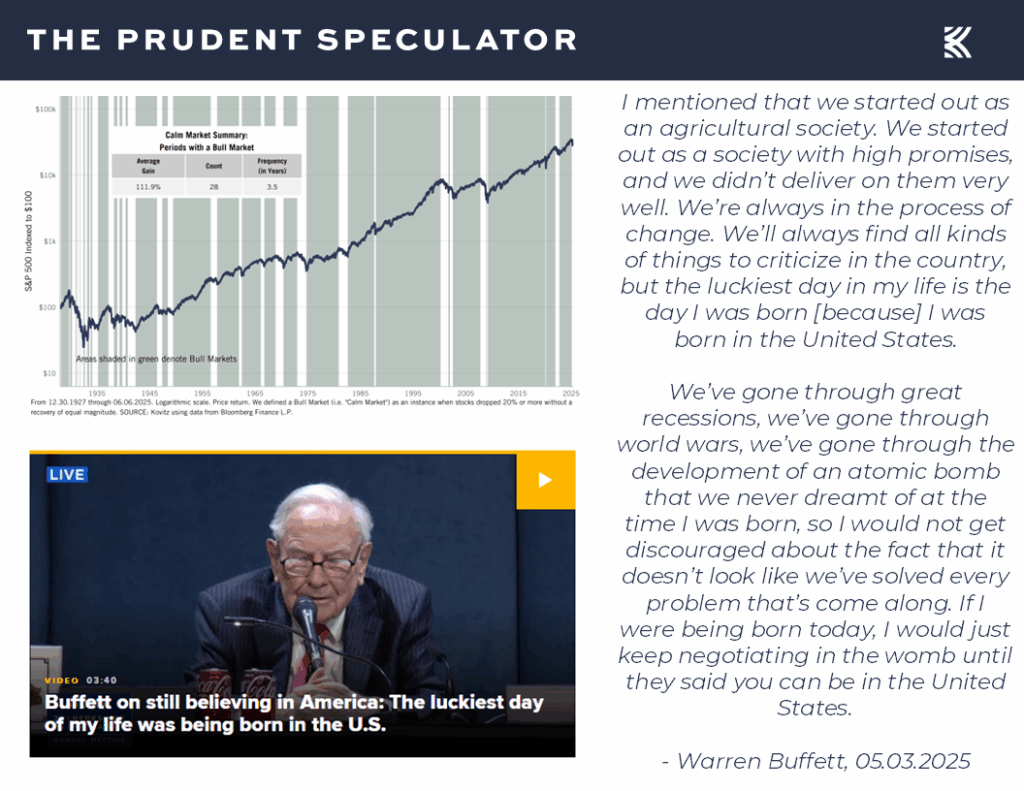

Wall of Worry – Always Something to Fret About, but Long-Term Trend has been Higher

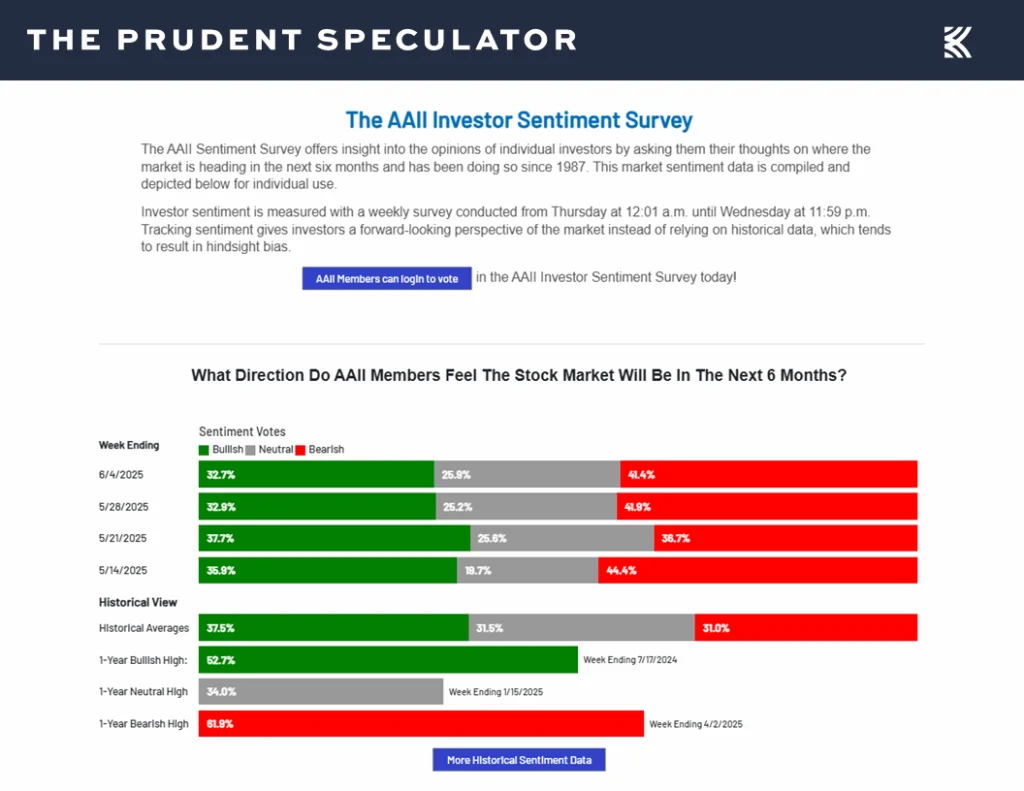

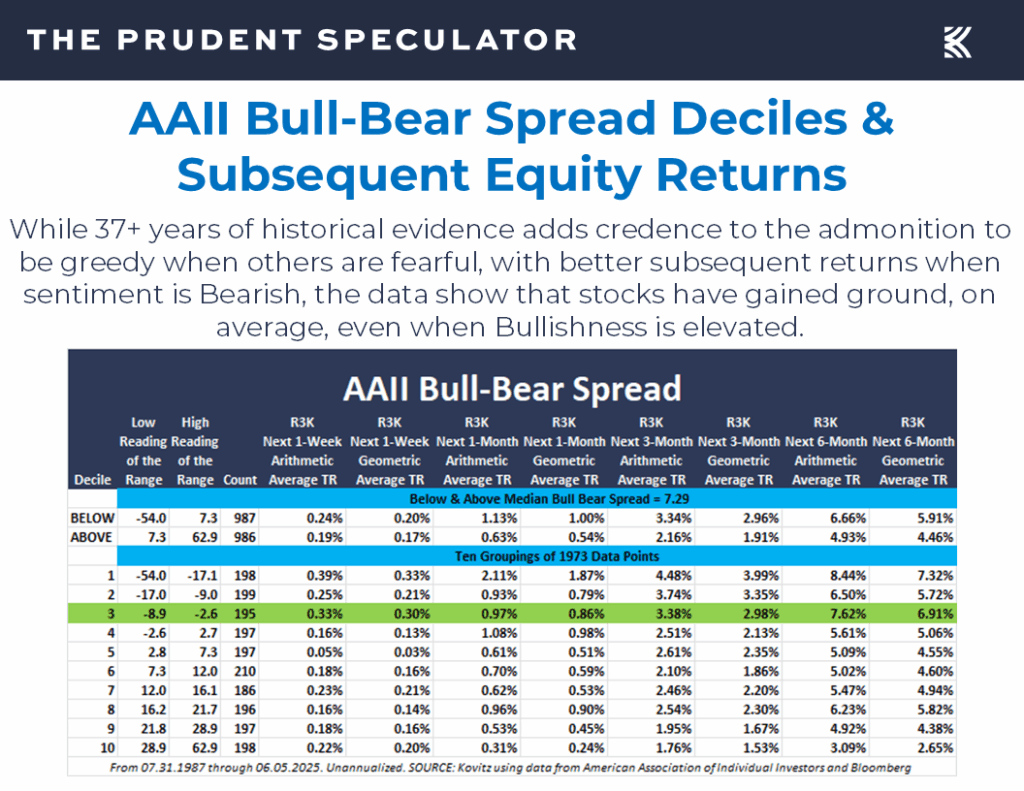

Sentiment – More Bears than Bulls – Contrarian Buy Signal

Tariffs – Stocks Have Moved Higher Throughout History Despite Duties

Econ News – Mixed Numbers but Growth Still the Forecast

EPS – Corporate Profit Growth in 2025 and 2026 Still the Expectation

Recessions – History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

Interest Rates – Long-Term Government Bond Yields Climb, but Stocks Historically Don’t Mind Rising Rates

Valuations – Attractive Metrics on our Portfolios

Stock News – Comments on four stocks across four different sectors

Week – S&P Recaptures 6000

Despite a nasty falling out between the world’s richest man and the world’s most powerful man, equities again gained ground last week, with the recovery from the April 8 lows for the S&P 500 eclipsing the 20% mark

and providing another reminder that stocks have long climbed a wall or worry,

Wall of Worry – Always Something to Fret About, but Long-Term Trend has been Higher

as the long-term trend in prices has been higher, with the S&P 500 reclaiming the psychologically important 6000 level as of Friday’s close.

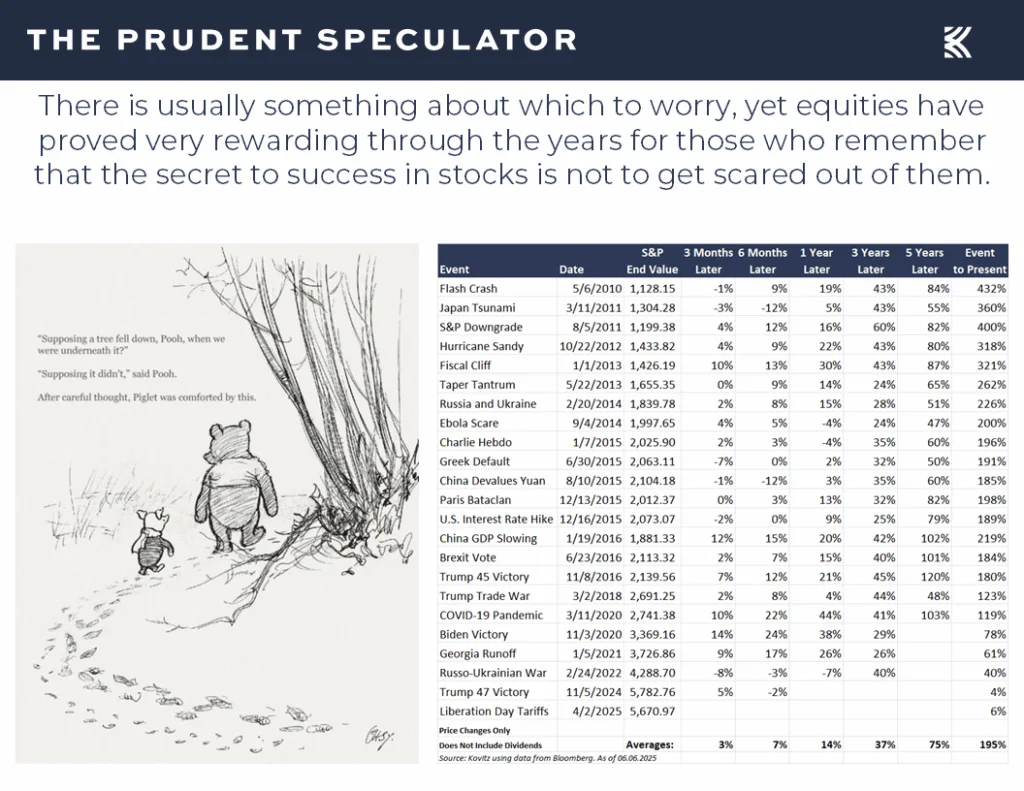

To be sure, there remains plenty to worry about…as is always the case,

Sentiment – More Bears than Bulls – Contrarian Buy Signal

and some have argued that this is one of the most hated V-shaped rebounds in history, as evidenced by folks on Main Street continuing to remain pessimistic on the prospects for stocks over the next six months,

though, happily, the AAII Bull-Bear Sentiment gauge has long been a contrarian indicator, validating the admonition to be greedy when others are fearful.

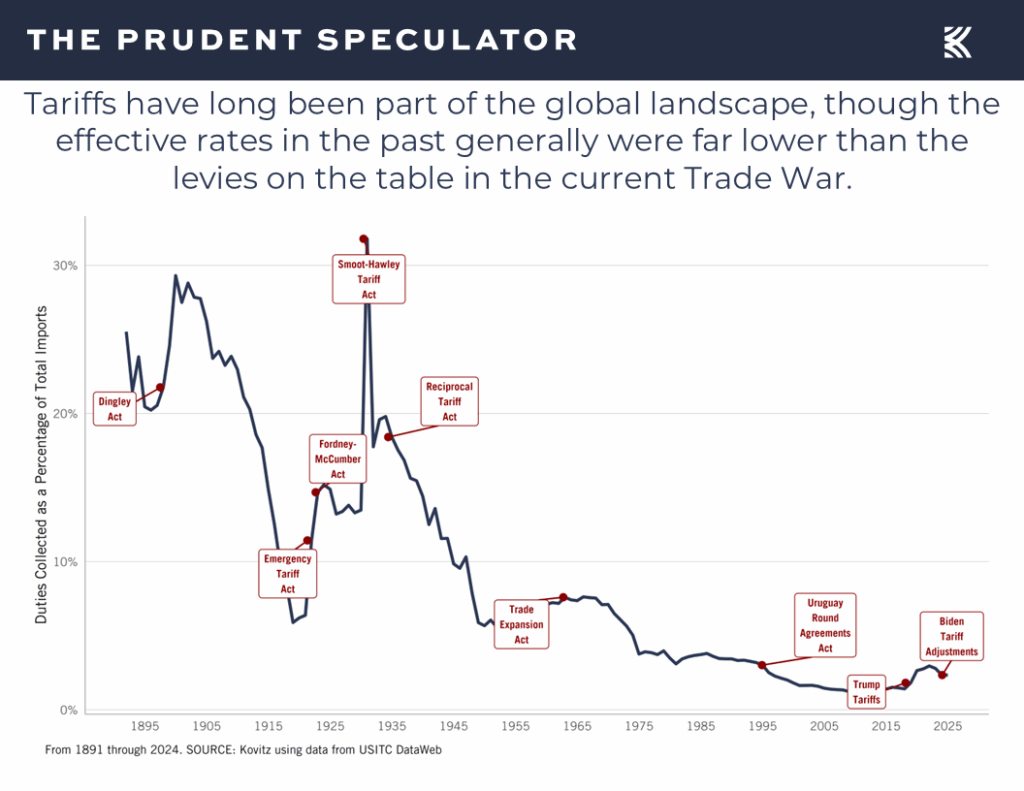

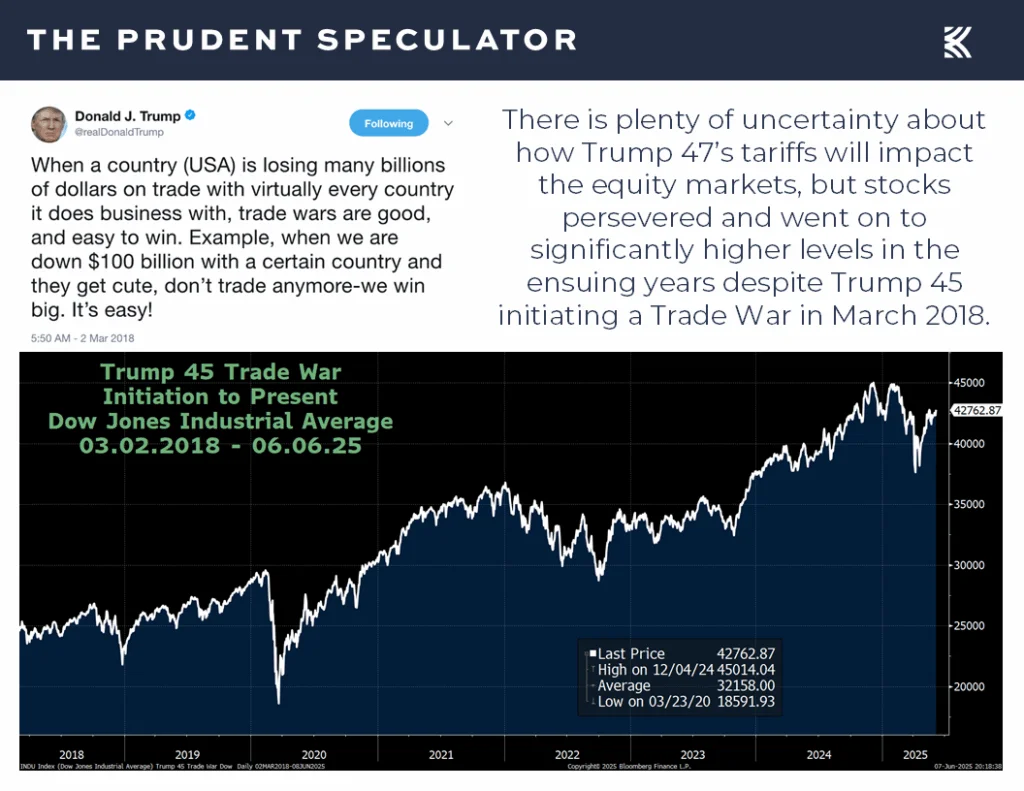

Tariffs – Stocks Have Moved Higher Throughout History Despite Duties

None of this is meant to suggest that concerns are unfounded and we respect that there have been numerous trips south along the path to long-term investment gains,

However, we continue to remember the advice of Vannevar Bush, who said, “Fear cannot be banished, but it can be calm and without panic; it can be mitigated by reason and evaluation.” After all, tariffs have long been part of the investment equation,

including in the first Trump Presidency, when the Dow was at 25000 at the start of the Trade War in March 2018.

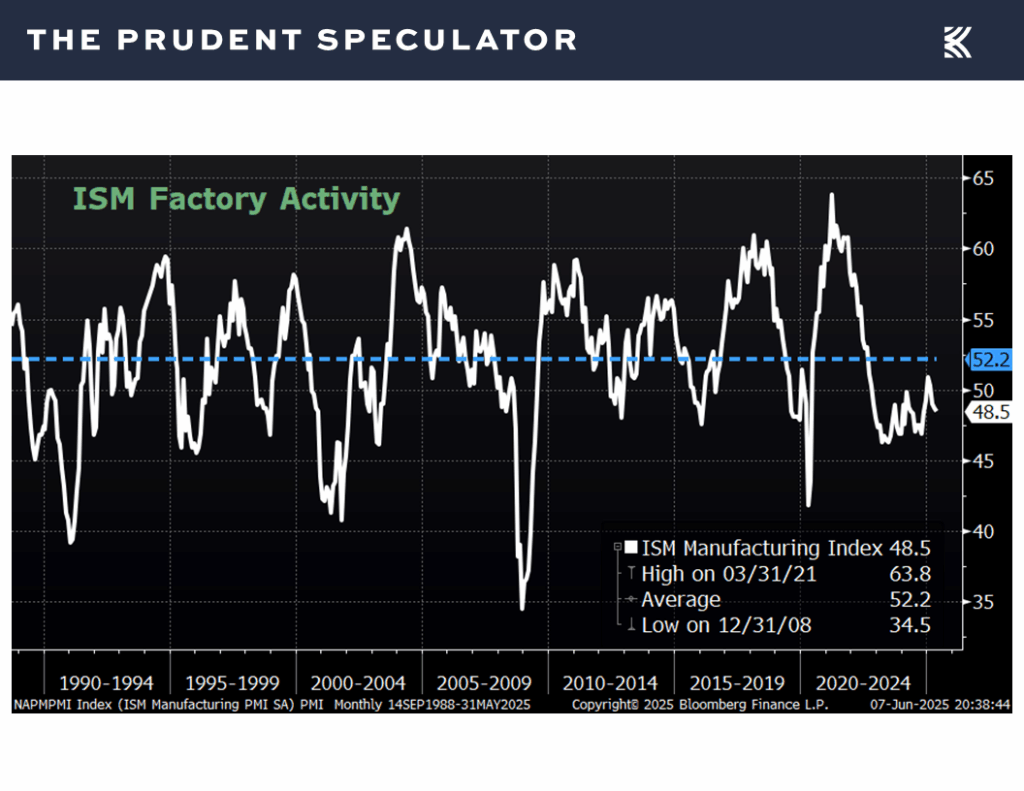

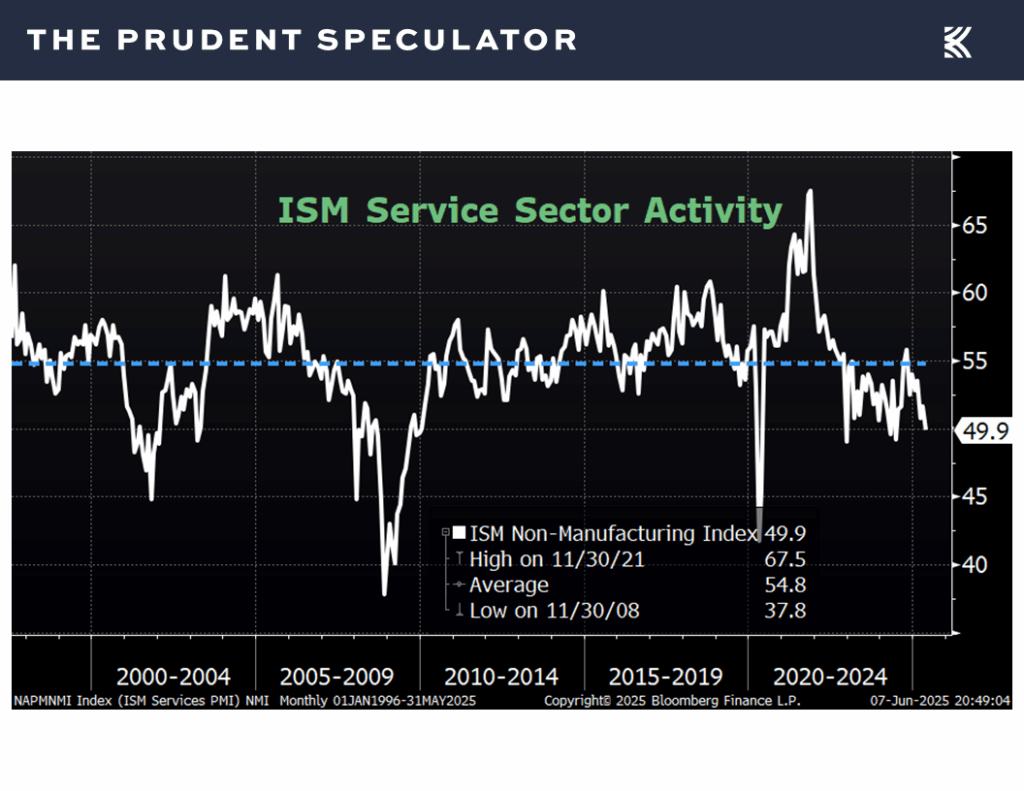

Econ News – Mixed Numbers but Growth Still the Forecast

Obviously, the impact of tariffs on the economy is a major wildcard, and we realize that last week an important figure on the health of the factory sector came in below expectations as the May ISM Manufacturing index (PMI) pulled back to 48.5, versus the consensus estimate of 49.5 and the April reading of 48.7,

and it was a similar story on the outlook for the services sector as the ISM Non-Manufacturing index (NMI) for May skidded to 49.8, down from 51.6 the month prior and forecasts of 52.0.

Of course, while 50 is the dividing line between expansion and contraction in the ISM data, raising the possibility of recession in the overall economy, it is important to understand that ISM states the following:

The past relationship between the Manufacturing PMI® and the overall economy indicates that the May reading (48.5 percent) corresponds to a change of plus-1.7 percent in real gross domestic product (GDP) on an annualized basis.

The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for May (49.9 percent) corresponds to a 0.4-percentage point increase in real gross domestic product (GDP) on an annualized basis.

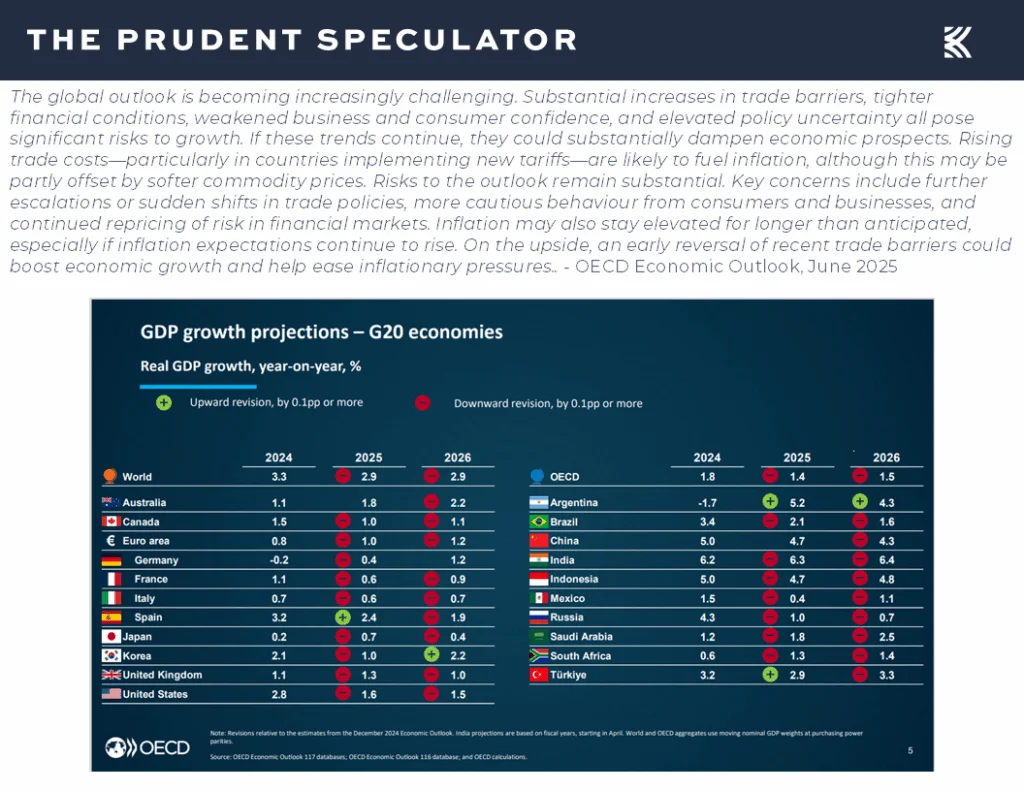

True, those GDP numbers are not exactly robust, and we also learned last week that the Organisation for Economic Co-operation and Development downgraded its outlook for the global and U.S. economies,

EPS – Corporate Profit Growth in 2025 and 2026 Still the Expectation

but real (inflation-adjusted) growth of 1.6% this year would not a recession make, and should still provide a favorable backdrop for corporate profit growth,

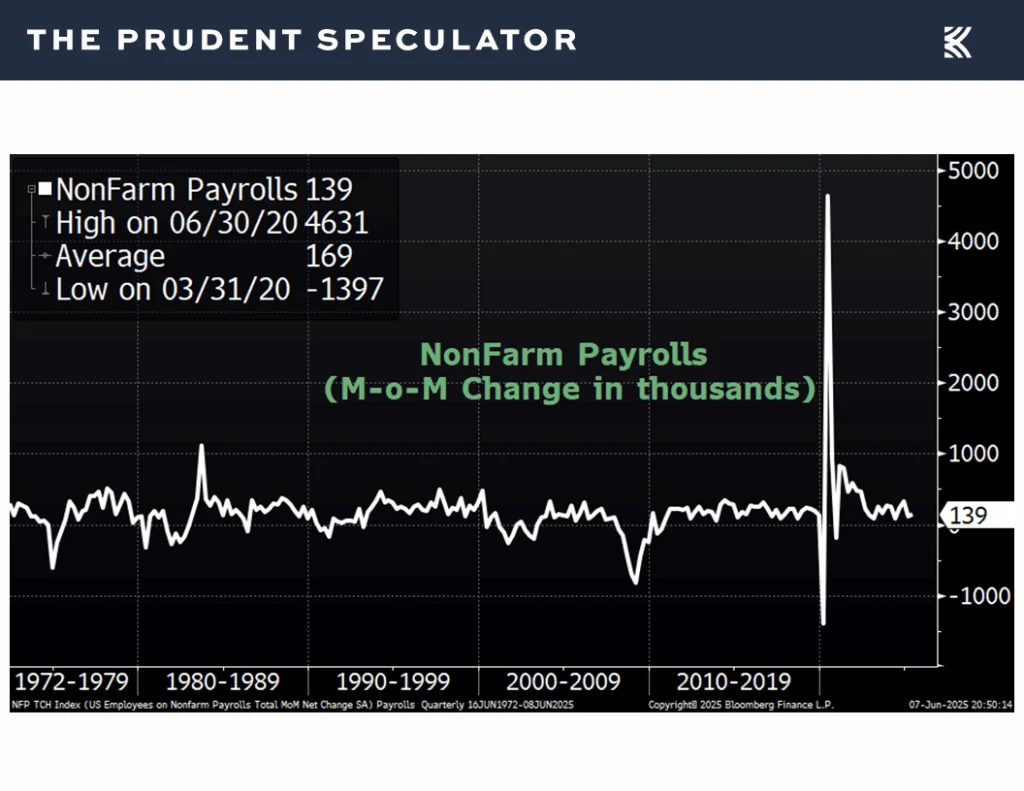

while the all-important domestic jobs number increase for May of 139,000 reported on Friday was better than projected.

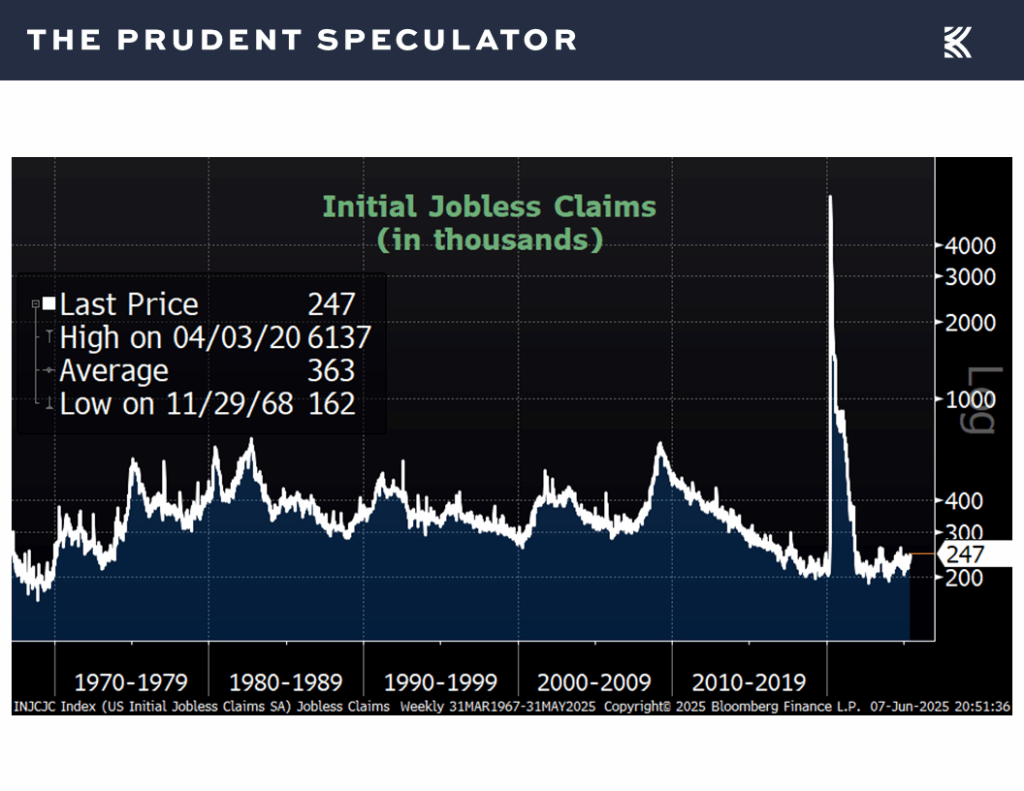

Yes, initial filings for jobless benefits have ticked higher in recent weeks,

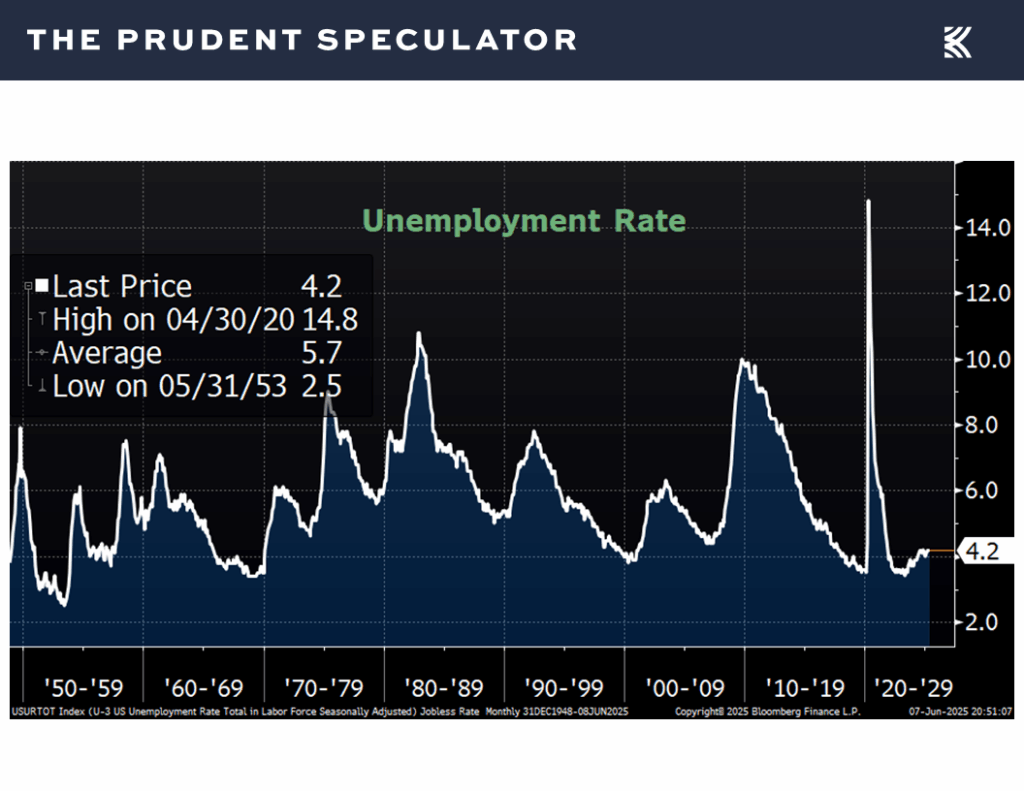

but the unemployment rate for May held steady at 4.2%,

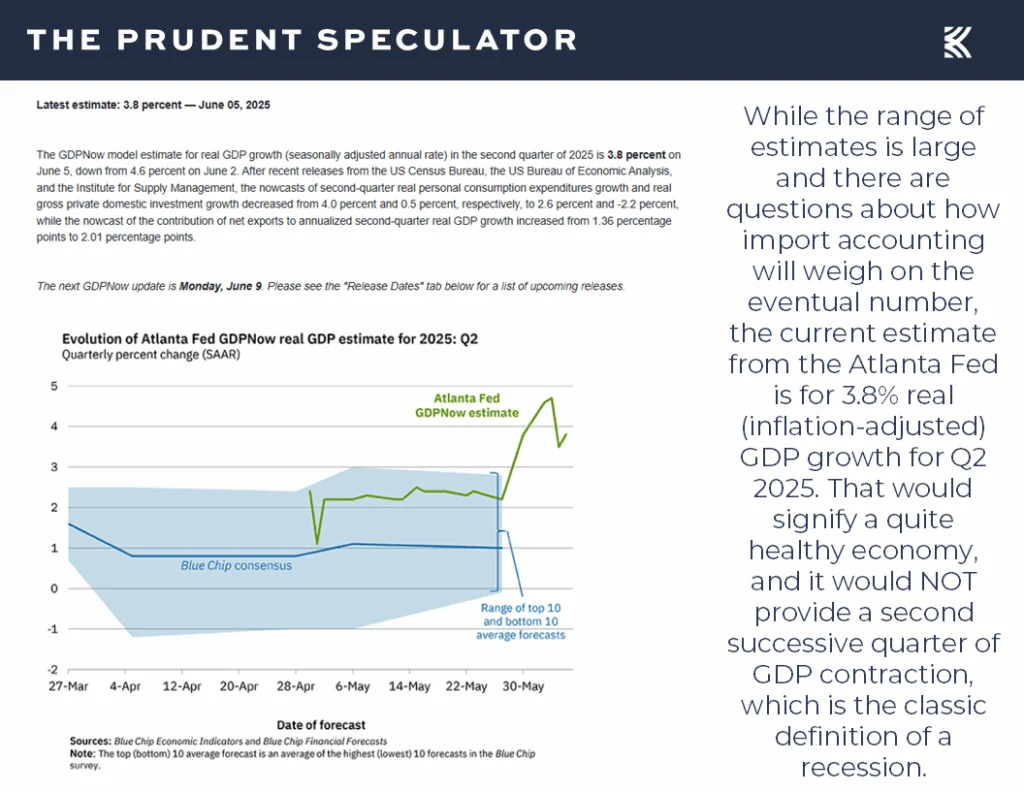

and the latest estimate from the Atlanta Fed for Q2 real GDP growth stood at a very solid 3.8%.

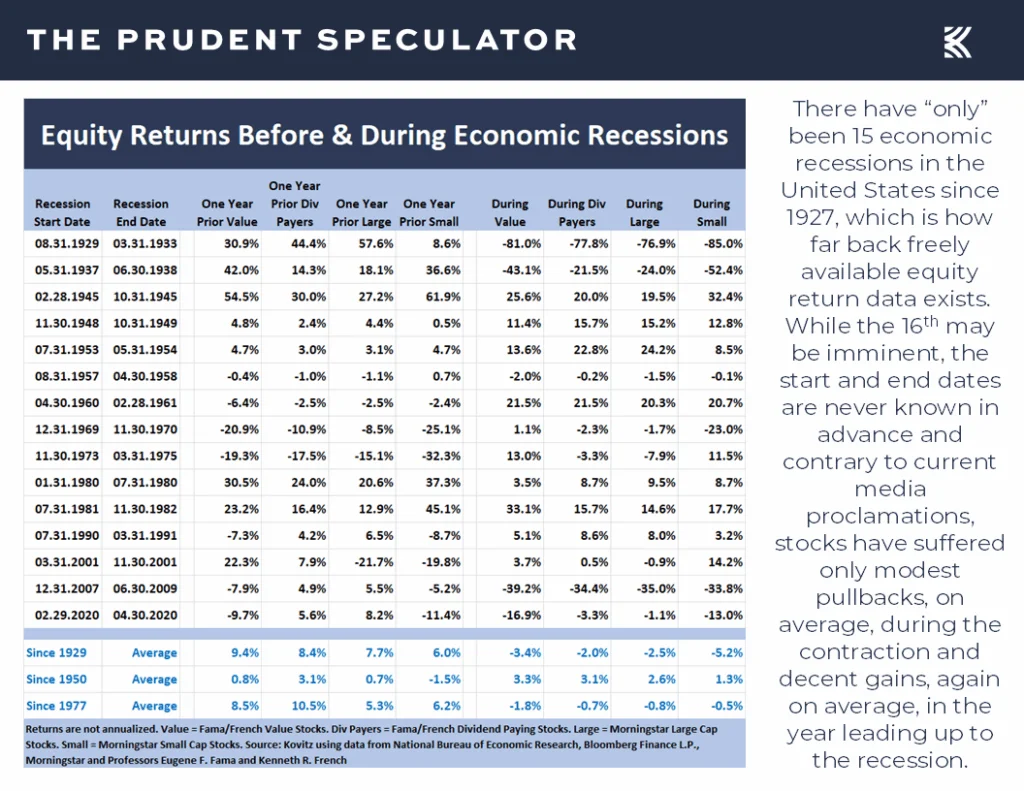

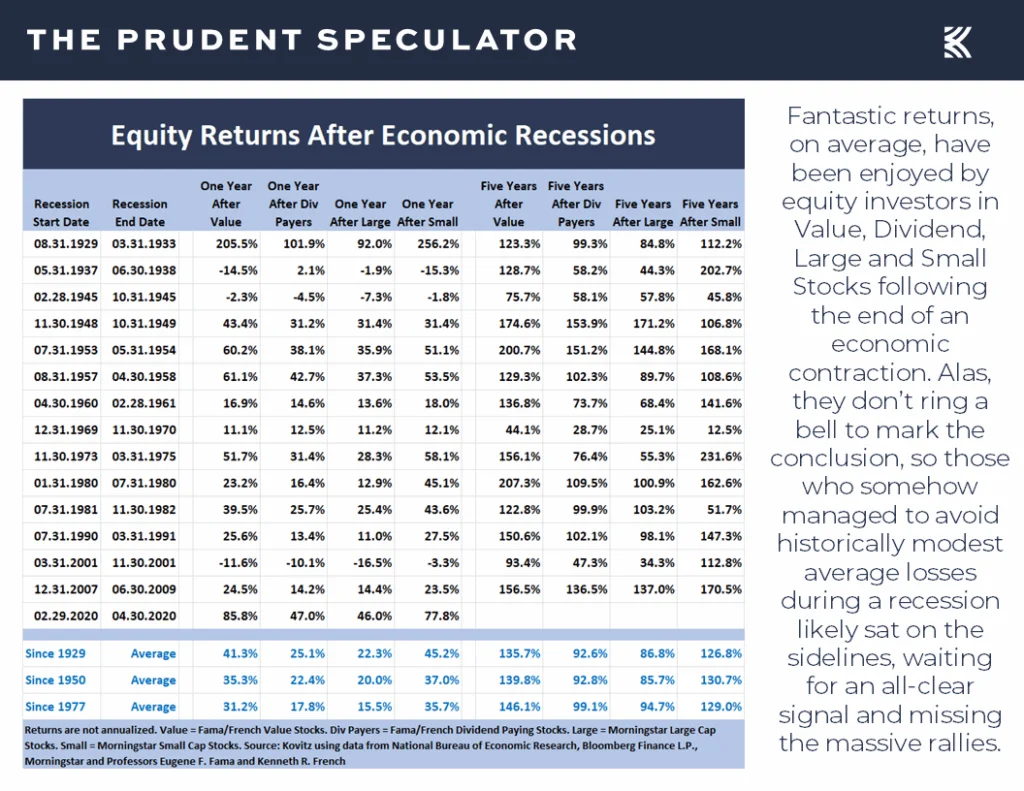

Recessions – History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

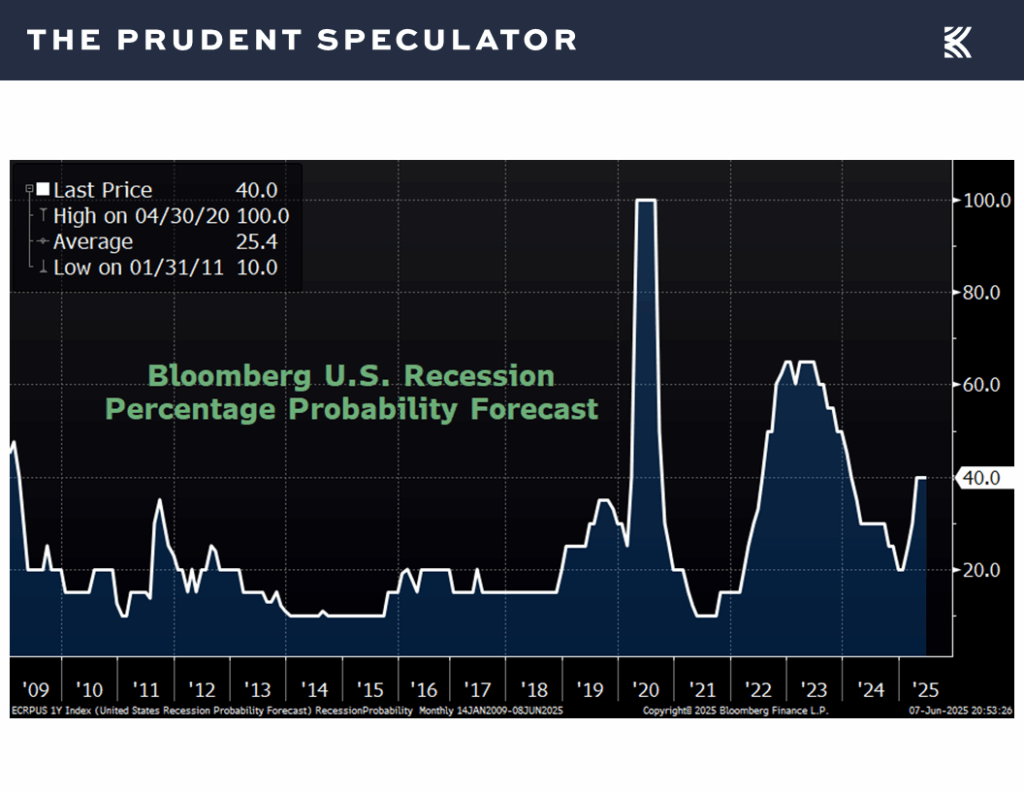

Anything can happen as we move forward, and the current odds of an economic contraction in the next 12 months, as tabulated by Bloomberg reside at 40%,

but economic forecasting has long been fraught with peril (it is virtually impossible to know in advance when a downturn begins and ends) and long-term-oriented investors should take comfort in what the historical evidence shows about equity returns before and during recessions,

and especially in the year after!

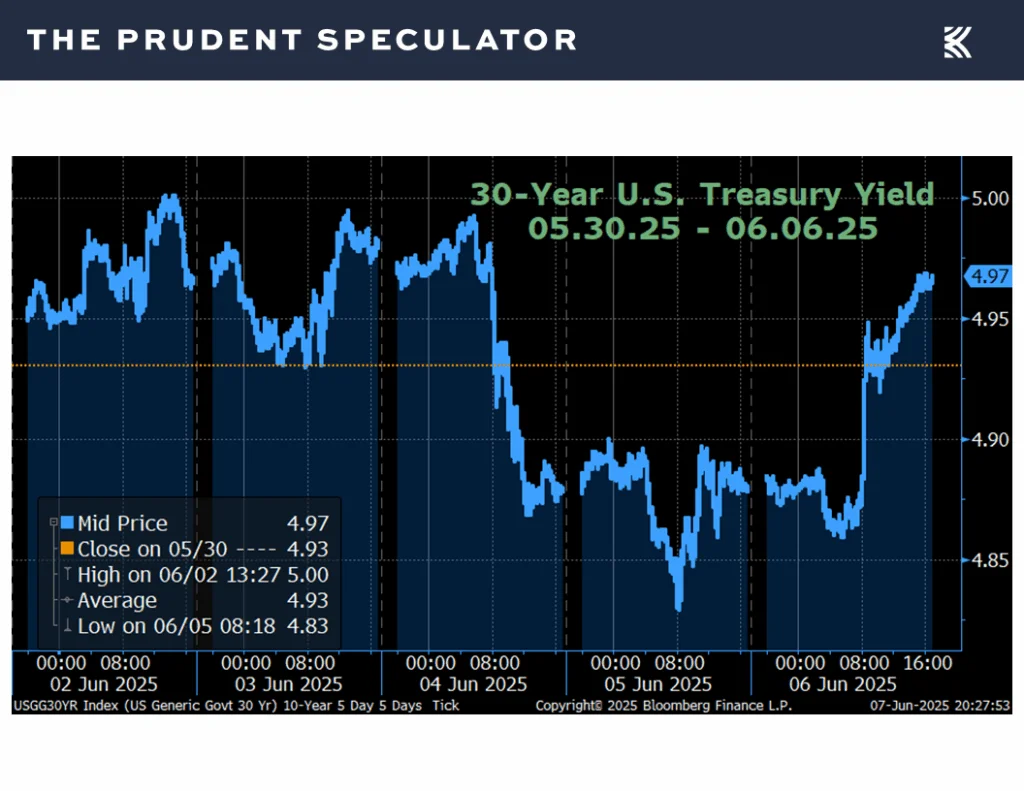

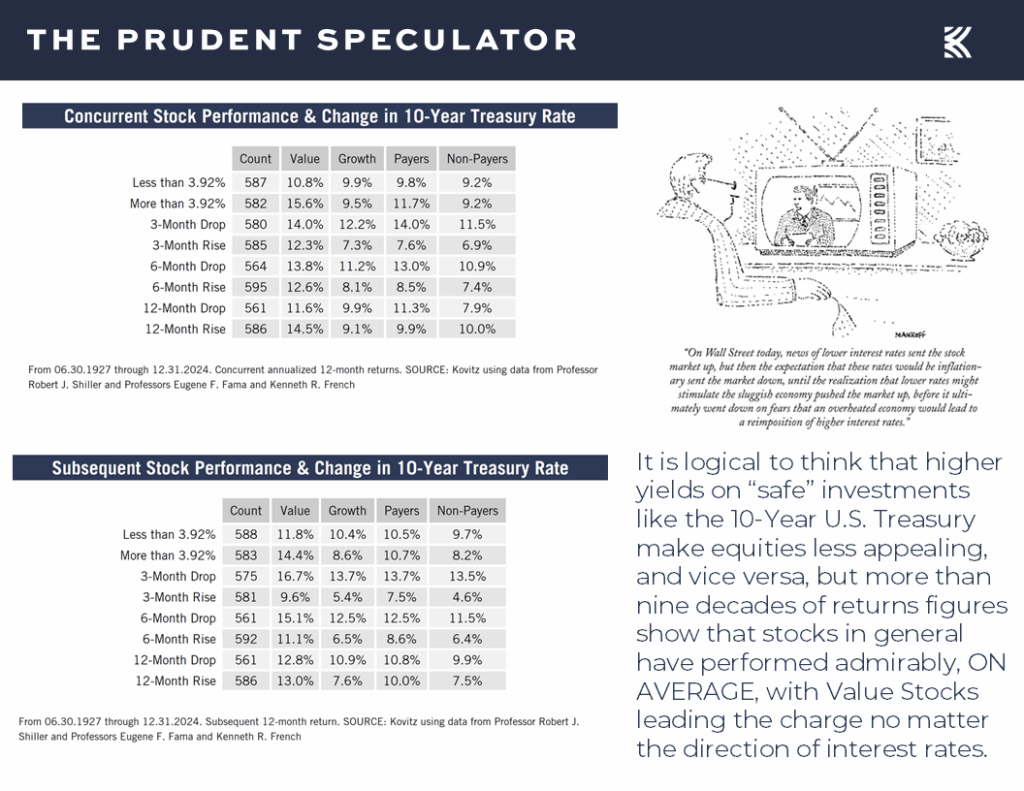

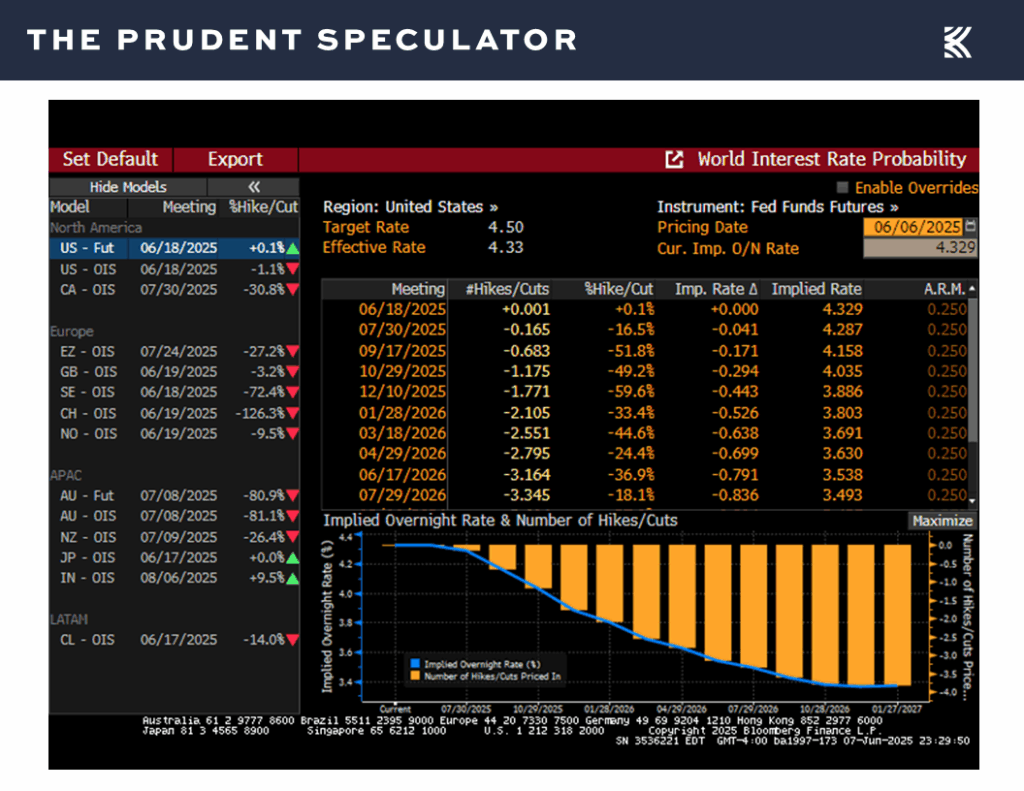

Interest Rates – Long-Term Government Bond Yields Climb, but Stocks Historically Don’t Mind Rising Rates

We also understand that recent increases in interest rates have caused consternation, but we point out that stocks rallied last week despite a rise in the 30-Year U.S. Treasury yield from 4.93% to 4.97%,

and nearly a century of data shows that equities, especially those of the Value variety, have performed fine whether long-term government bond yields are rising or falling,

while betting in the Fed Funds futures market continues to call for Jerome H. Powell & Co. to lower rates as much as three times over the next 12 months.

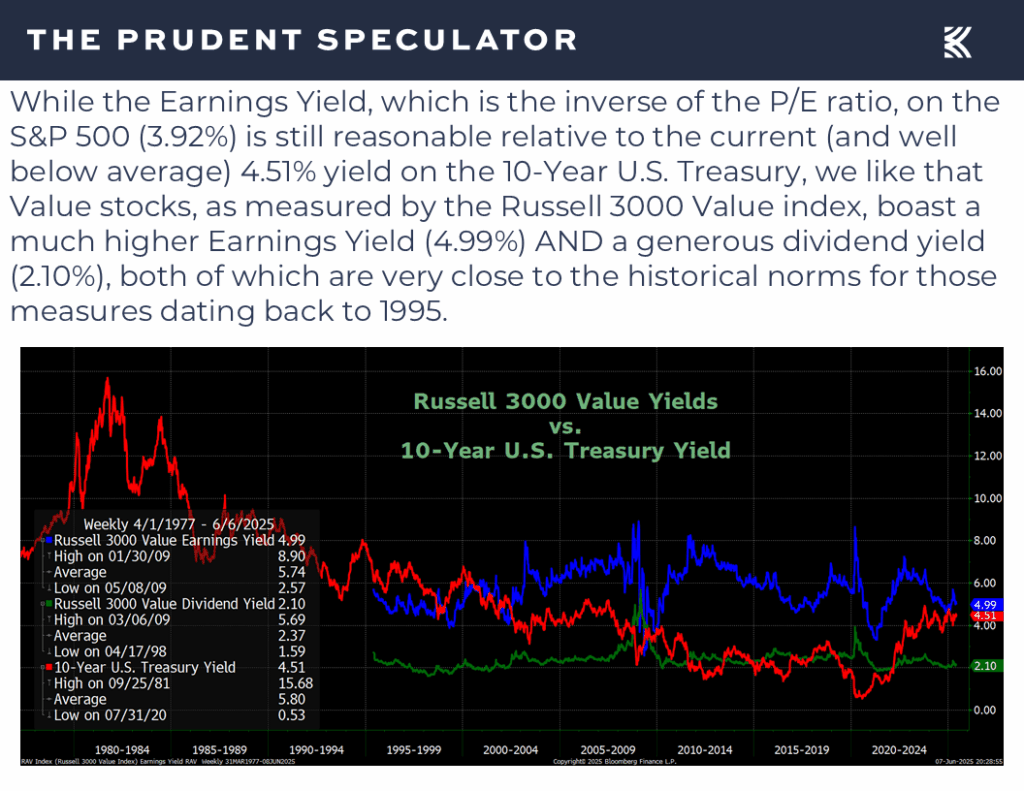

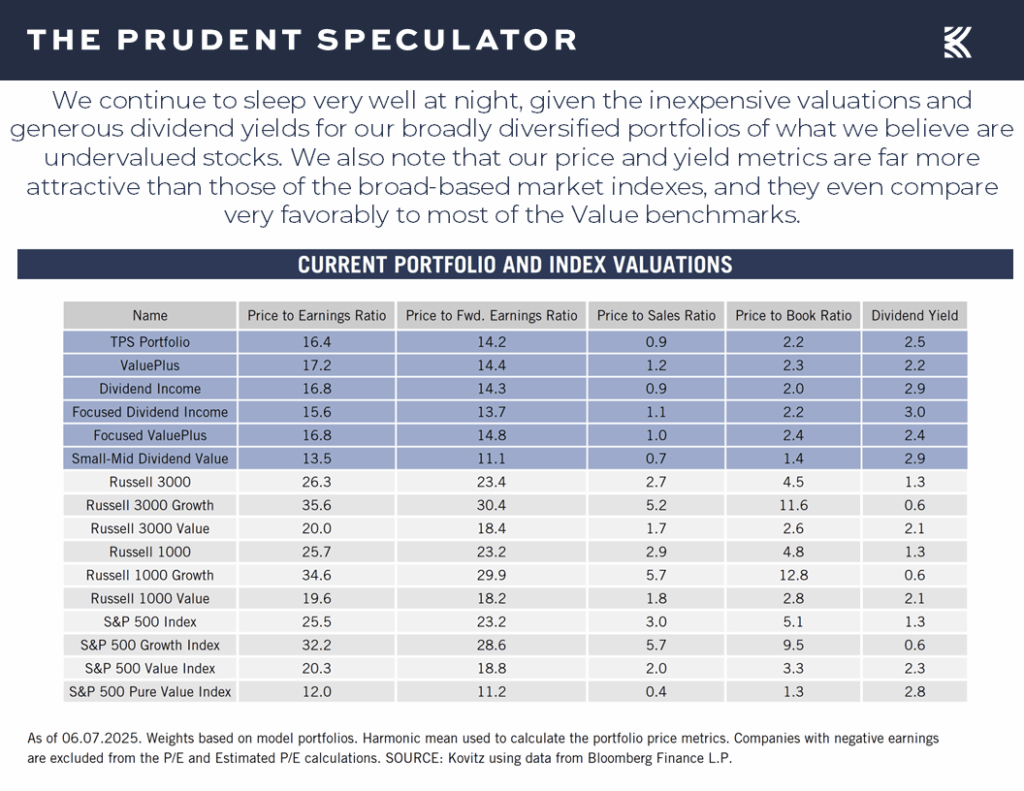

Valuations – Attractive Metrics on our Portfolios

And we think that the current level of interest rates is reasonable from an earnings and dividend yield perspective for inexpensively priced stocks in general,

and our broadly diversified portfolios of what we believe are undervalued stocks in particular.

Stock News – Updates on four stocks across four different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

AAII Sentiment, Tariffs, Earnings, Interest Rates and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s Market Commentary, we discuss AAII Sentiment, Tariffs, Earnings, Interest Rates and More. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 10 Buys for 4 Portfolios

Week – S&P Recaptures 6000

Wall of Worry – Always Something to Fret About, but Long-Term Trend has been Higher

Sentiment – More Bears than Bulls – Contrarian Buy Signal

Tariffs – Stocks Have Moved Higher Throughout History Despite Duties

Econ News – Mixed Numbers but Growth Still the Forecast

EPS – Corporate Profit Growth in 2025 and 2026 Still the Expectation

Recessions – History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

Interest Rates – Long-Term Government Bond Yields Climb, but Stocks Historically Don’t Mind Rising Rates

Valuations – Attractive Metrics on our Portfolios

Stock News – Comments on four stocks across four different sectors

Week – S&P Recaptures 6000

Despite a nasty falling out between the world’s richest man and the world’s most powerful man, equities again gained ground last week, with the recovery from the April 8 lows for the S&P 500 eclipsing the 20% mark

and providing another reminder that stocks have long climbed a wall or worry,

Wall of Worry – Always Something to Fret About, but Long-Term Trend has been Higher

as the long-term trend in prices has been higher, with the S&P 500 reclaiming the psychologically important 6000 level as of Friday’s close.

To be sure, there remains plenty to worry about…as is always the case,

Sentiment – More Bears than Bulls – Contrarian Buy Signal

and some have argued that this is one of the most hated V-shaped rebounds in history, as evidenced by folks on Main Street continuing to remain pessimistic on the prospects for stocks over the next six months,

though, happily, the AAII Bull-Bear Sentiment gauge has long been a contrarian indicator, validating the admonition to be greedy when others are fearful.

Tariffs – Stocks Have Moved Higher Throughout History Despite Duties

None of this is meant to suggest that concerns are unfounded and we respect that there have been numerous trips south along the path to long-term investment gains,

However, we continue to remember the advice of Vannevar Bush, who said, “Fear cannot be banished, but it can be calm and without panic; it can be mitigated by reason and evaluation.” After all, tariffs have long been part of the investment equation,

including in the first Trump Presidency, when the Dow was at 25000 at the start of the Trade War in March 2018.

Econ News – Mixed Numbers but Growth Still the Forecast

Obviously, the impact of tariffs on the economy is a major wildcard, and we realize that last week an important figure on the health of the factory sector came in below expectations as the May ISM Manufacturing index (PMI) pulled back to 48.5, versus the consensus estimate of 49.5 and the April reading of 48.7,

and it was a similar story on the outlook for the services sector as the ISM Non-Manufacturing index (NMI) for May skidded to 49.8, down from 51.6 the month prior and forecasts of 52.0.

Of course, while 50 is the dividing line between expansion and contraction in the ISM data, raising the possibility of recession in the overall economy, it is important to understand that ISM states the following:

The past relationship between the Manufacturing PMI® and the overall economy indicates that the May reading (48.5 percent) corresponds to a change of plus-1.7 percent in real gross domestic product (GDP) on an annualized basis.

The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for May (49.9 percent) corresponds to a 0.4-percentage point increase in real gross domestic product (GDP) on an annualized basis.

True, those GDP numbers are not exactly robust, and we also learned last week that the Organisation for Economic Co-operation and Development downgraded its outlook for the global and U.S. economies,

EPS – Corporate Profit Growth in 2025 and 2026 Still the Expectation

but real (inflation-adjusted) growth of 1.6% this year would not a recession make, and should still provide a favorable backdrop for corporate profit growth,

while the all-important domestic jobs number increase for May of 139,000 reported on Friday was better than projected.

Yes, initial filings for jobless benefits have ticked higher in recent weeks,

but the unemployment rate for May held steady at 4.2%,

and the latest estimate from the Atlanta Fed for Q2 real GDP growth stood at a very solid 3.8%.

Recessions – History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

Anything can happen as we move forward, and the current odds of an economic contraction in the next 12 months, as tabulated by Bloomberg reside at 40%,

but economic forecasting has long been fraught with peril (it is virtually impossible to know in advance when a downturn begins and ends) and long-term-oriented investors should take comfort in what the historical evidence shows about equity returns before and during recessions,

and especially in the year after!

Interest Rates – Long-Term Government Bond Yields Climb, but Stocks Historically Don’t Mind Rising Rates

We also understand that recent increases in interest rates have caused consternation, but we point out that stocks rallied last week despite a rise in the 30-Year U.S. Treasury yield from 4.93% to 4.97%,

and nearly a century of data shows that equities, especially those of the Value variety, have performed fine whether long-term government bond yields are rising or falling,

while betting in the Fed Funds futures market continues to call for Jerome H. Powell & Co. to lower rates as much as three times over the next 12 months.

Valuations – Attractive Metrics on our Portfolios

And we think that the current level of interest rates is reasonable from an earnings and dividend yield perspective for inexpensively priced stocks in general,

and our broadly diversified portfolios of what we believe are undervalued stocks in particular.

Stock News – Updates on four stocks across four different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.