The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the AAII Sentiment, Valuations, Interest Rates and more. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Trading Week – Scary Season Rally Continues

Interest Rates – Yields have Jumped; Stocks Haven’t Minded Historically, on Average

Headlines – Stocks Always Have Overcome Disconcerting News in the Fullness of Time

Volatility – Ups and Downs but Long-Term Trend Has Been Up

Profits – Favorable EPS Outlook

Econ Outlook – Mixed Stats, but Solid GDP Growth the Forecast

Valuations – Liking our Metrics

Sentiment – AAII Bullishness Retreats; Bearishness Jumps

Stock News –

Interest Rates – Yields have Jumped; Stocks Haven’t Minded Historically, on Average

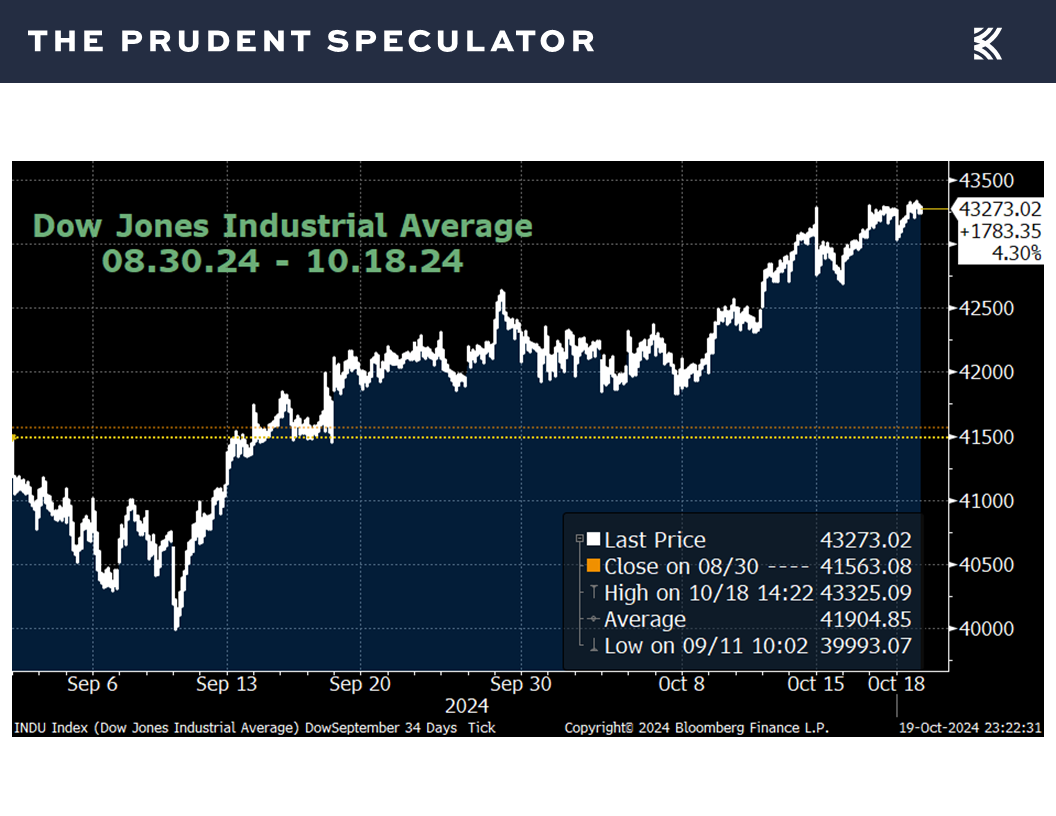

There are still nine trading days to go, but just as we said last week, the historically seasonally weaker September-October time span this time around has provided support for our long-held assertion that time in the market trumps market timing. Bucking the propensity for red ink, on average, since the launch of The Prudent Speculator in 1977,

the equity markets managed to again gain ground last week, adding to the handsome advance since the start of the often spooky two-month period.

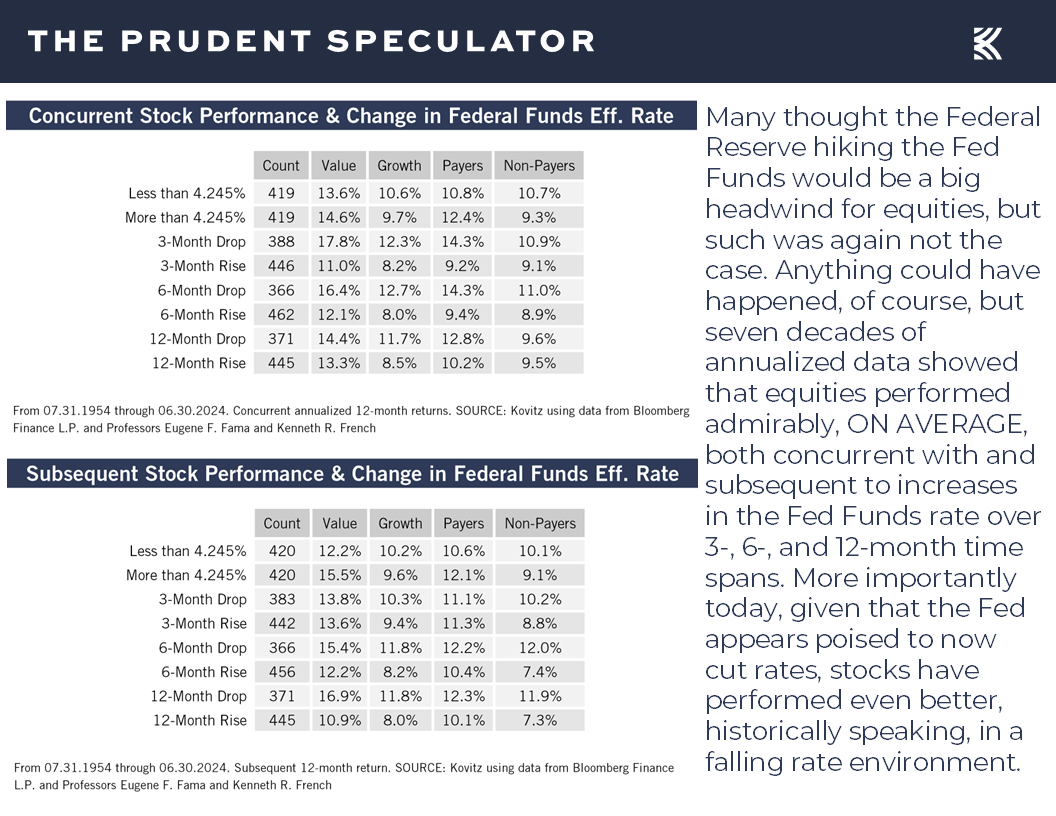

All the gains of late have come since the Federal Reserve cut its target for the Fed Funds rate on September 18, which would seem to make sense, given the evidence since 1954 that shows that stocks perform better when the nation’s central bank is easing monetary policy.

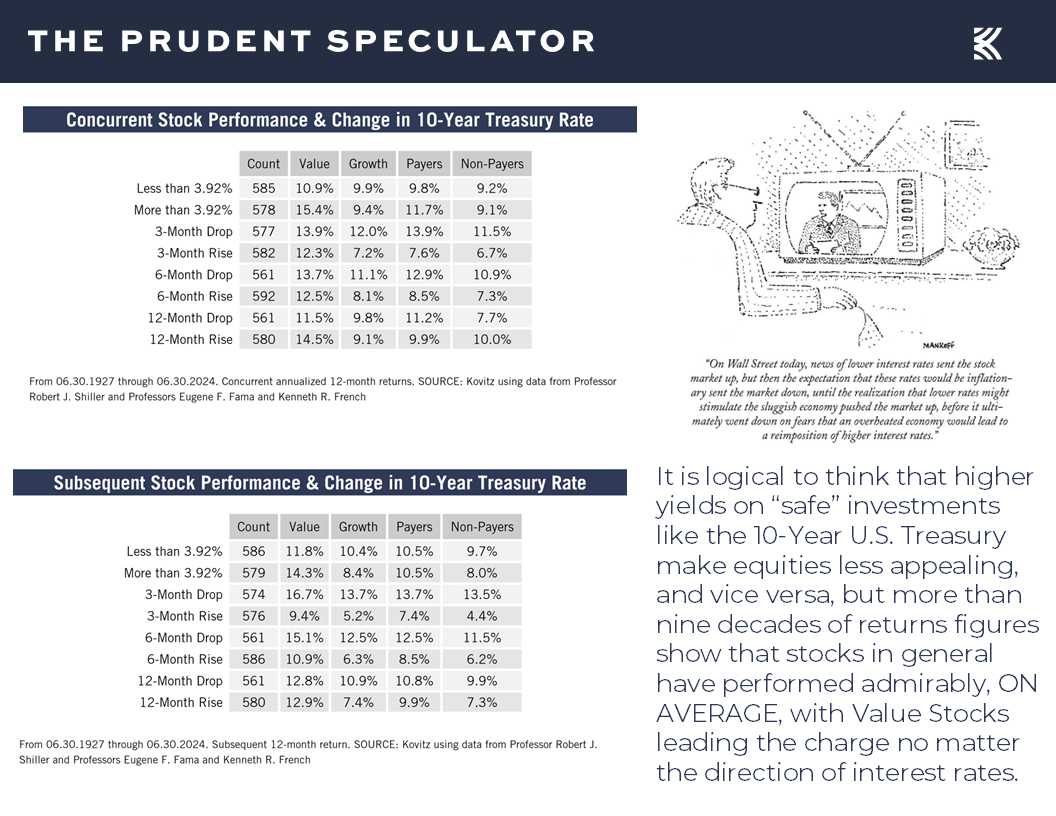

However, longer-term interest rates actually have jumped since the Fed reduced short-term rates, with the yield on the 10-Year U.S. Treasury climbing from 3.65% on September 17 to 4.08% today.

Of course, history also shows that, on average, stocks perform fine whether the yield on the benchmark government bond is rising or falling,

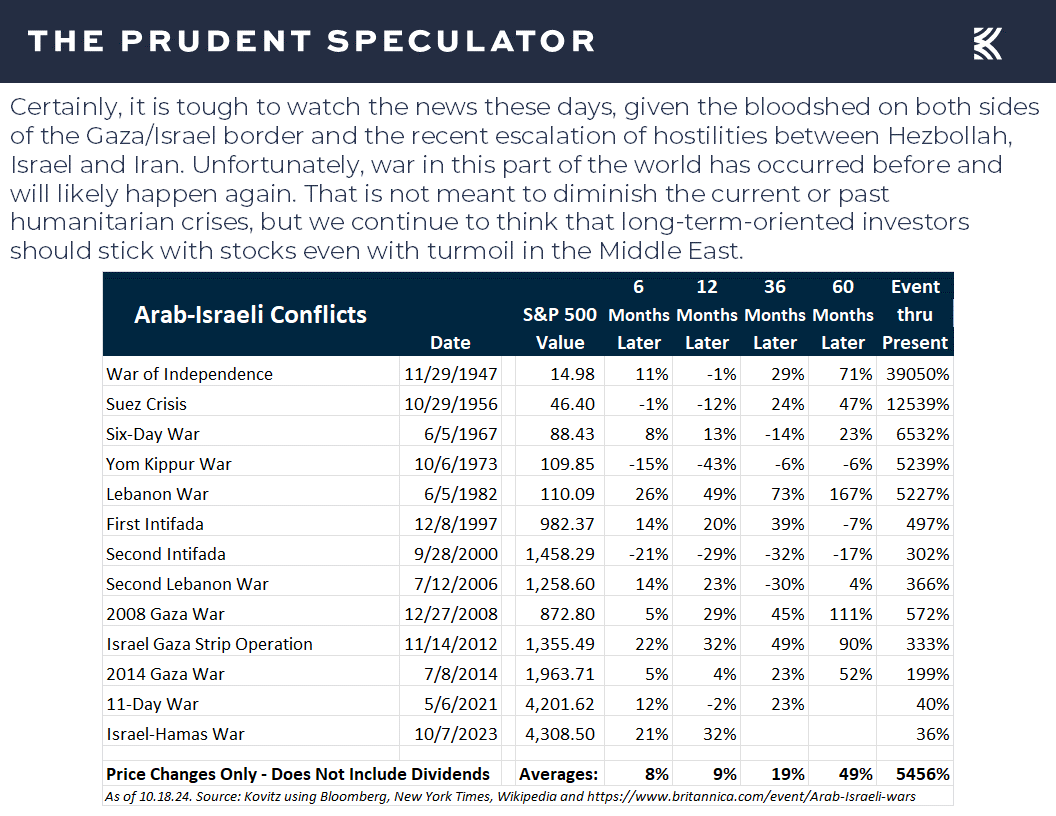

Headlines – Stocks Always Have Overcome Disconcerting News in the Fullness of Time

as also has been the case when Arab-Israeli conflicts have occurred,

and following many other disconcerting events.

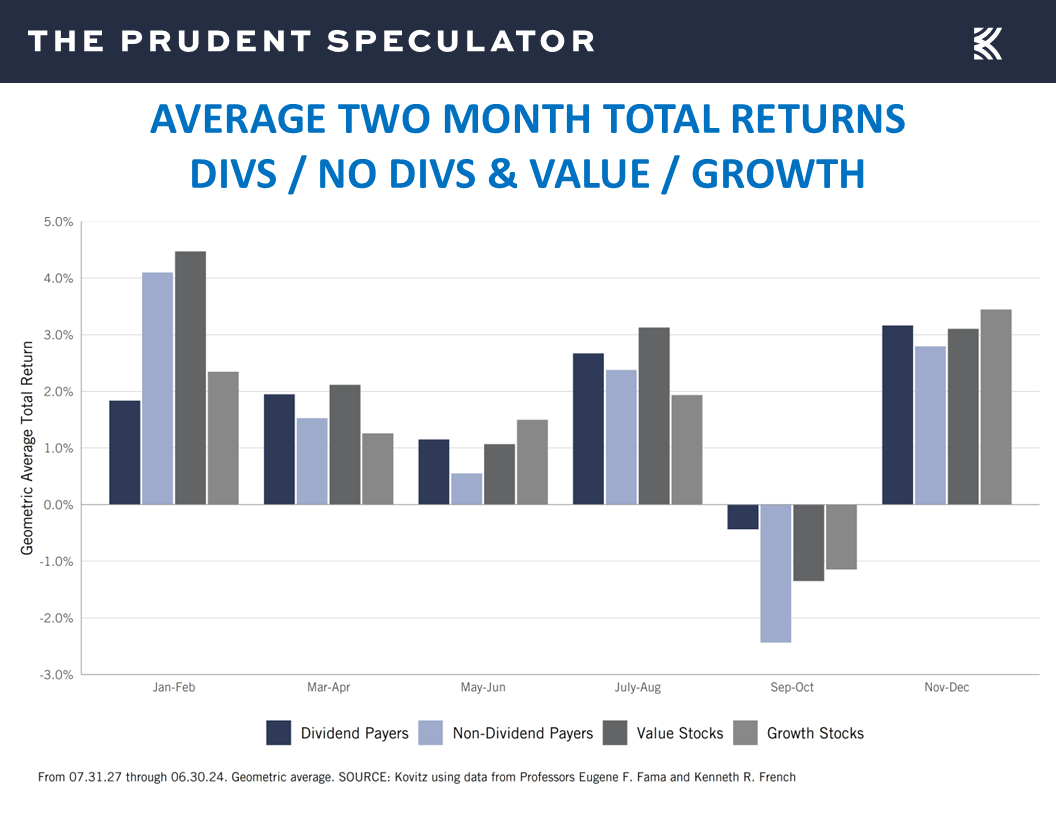

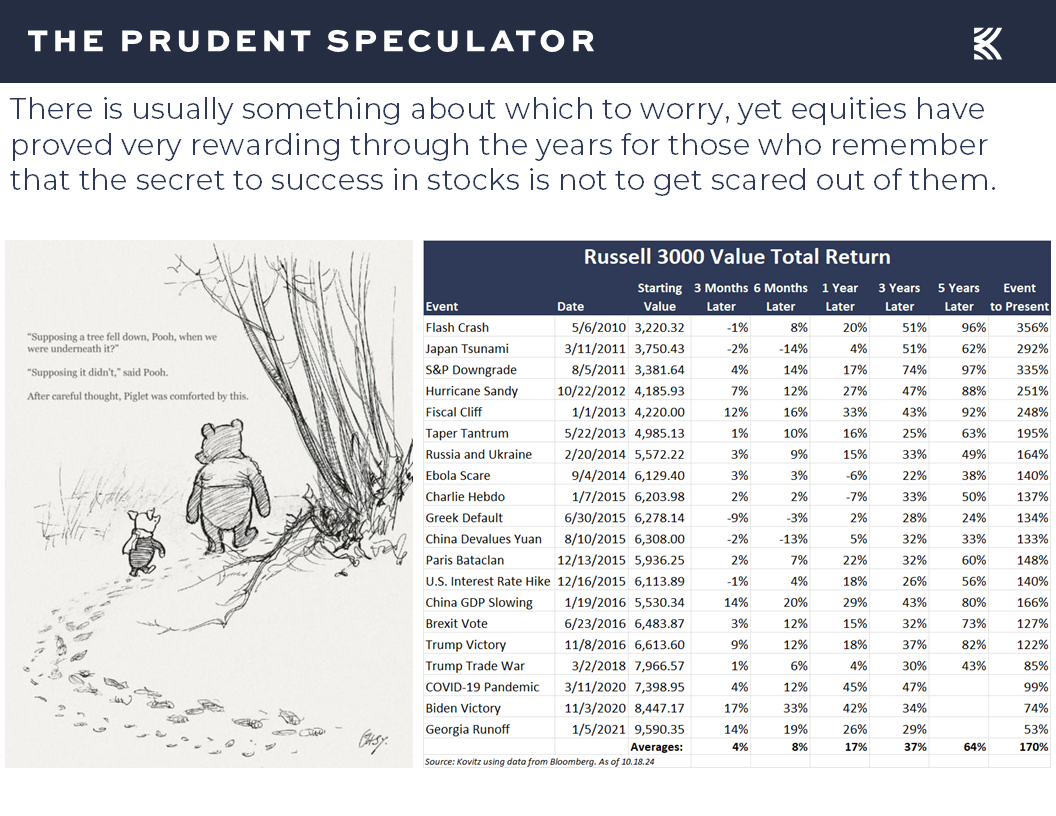

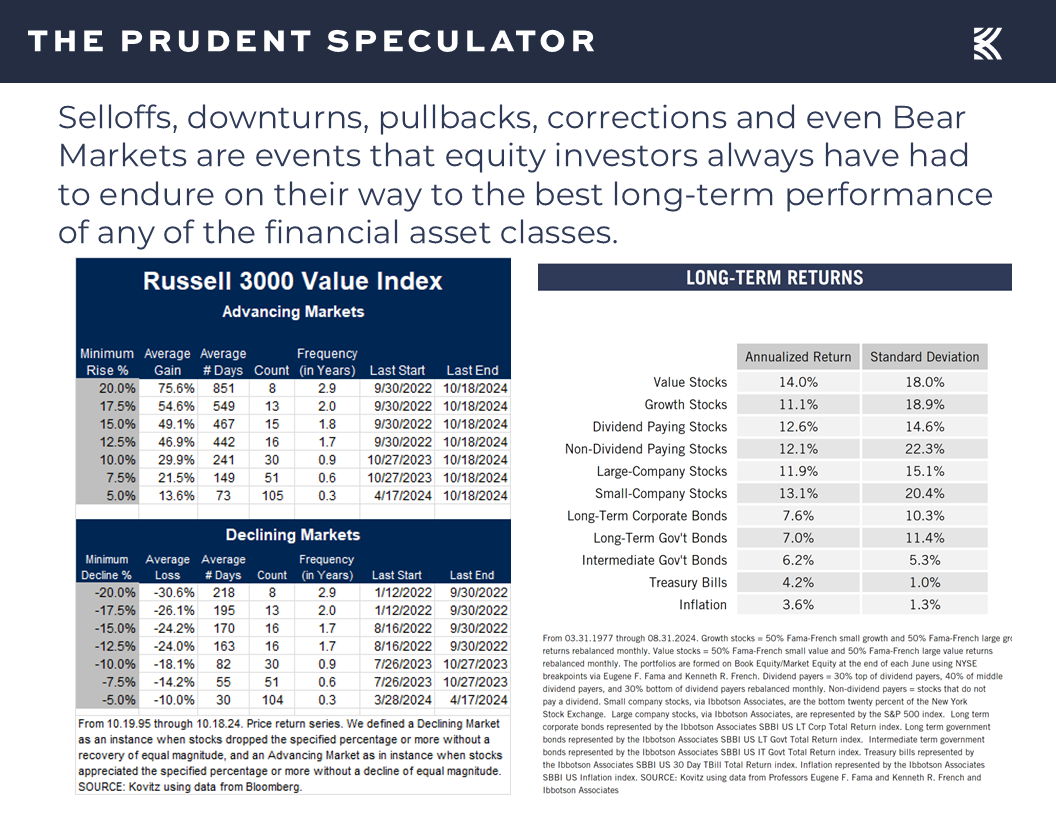

Volatility – Ups and Downs but Long-Term Trend Has Been Up

That is not to say that equities will rise no matter what, and there have been numerous worrisome downturns through the years, including a whopping 30 drops of 10% or more just since 1995, but over the long haul, stocks have proved rewarding for those who stick with them through thick and thin,

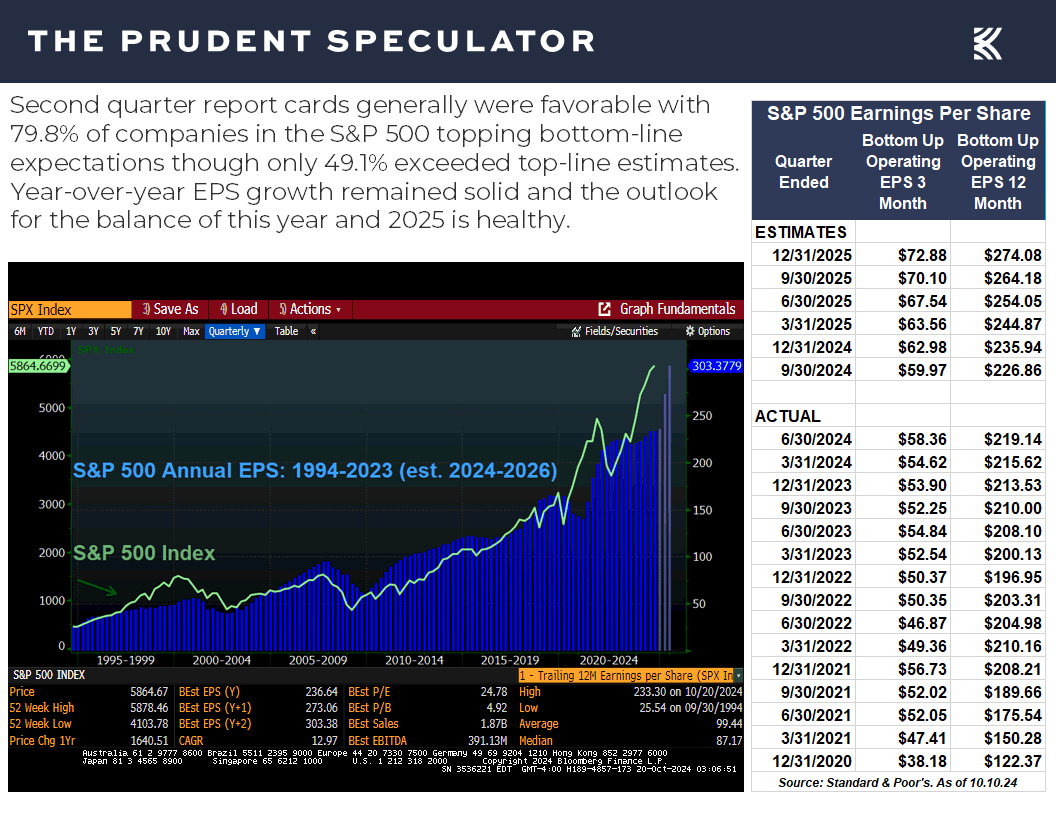

Profits – Favorable EPS Outlook

as corporations have become more valuable, given that their profits have grown over time, with earnings per share projected to expand nicely over the remainder of this year and in 2025.

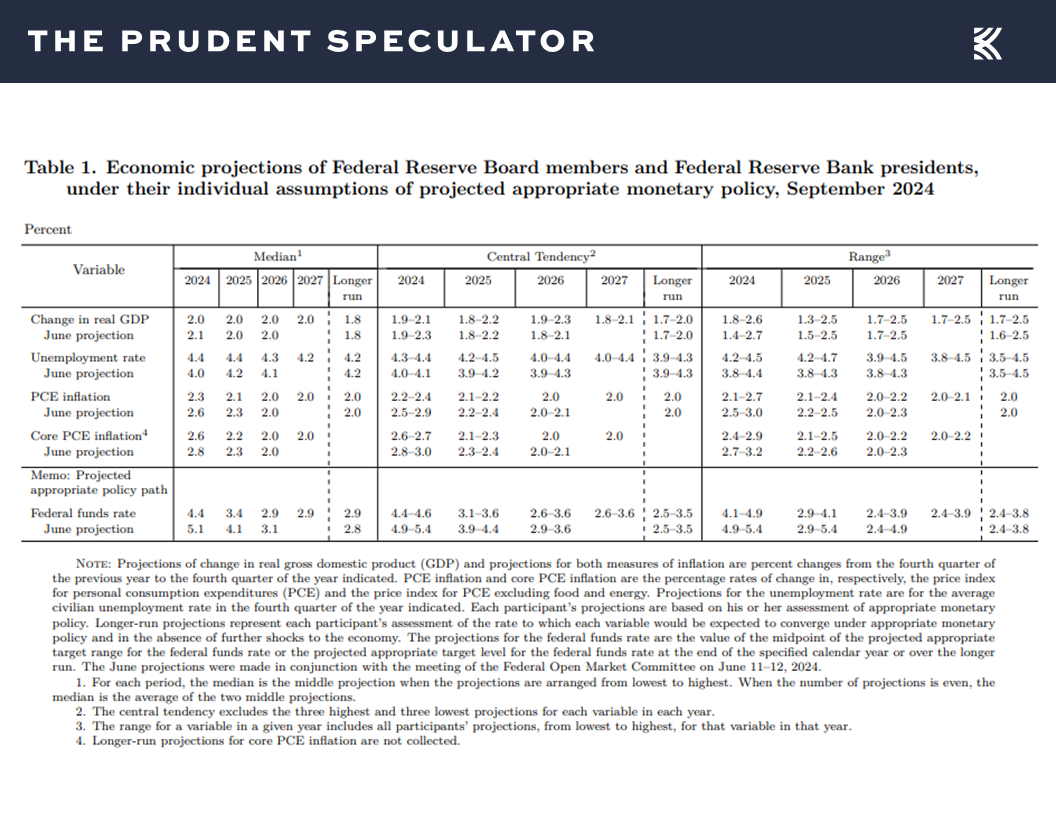

No doubt, the strength of the economy is key to the growth of top and bottom lines for Corporate America, and statistics out last week continued to support the projections provided last month by Jerome H. Powell & Co. that call for inflation to move closer to the Fed’s long-run goal of 2.0% and real (inflation-adjusted) U.S. GDP growth to remain in the 2.0% range.

Econ Outlook – Mixed Stats, but Solid GDP Growth the Forecast

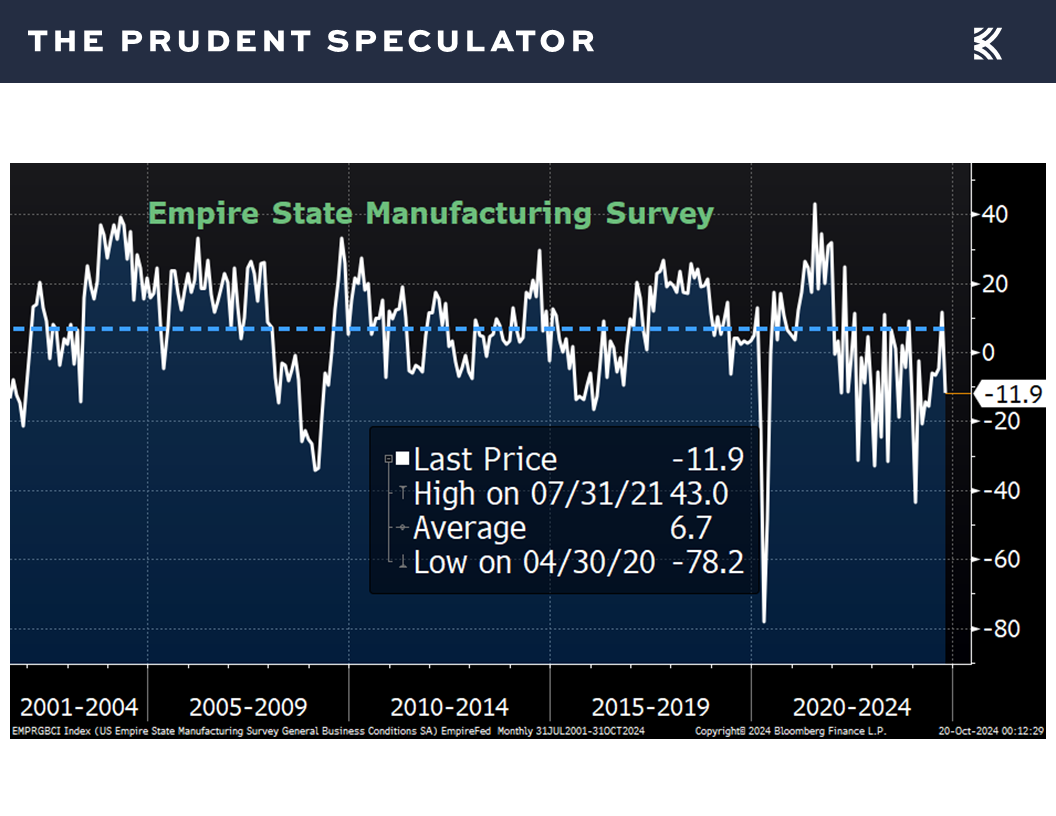

To be sure, some of the economic numbers were weaker-than-expected last week, as the Empire Manufacturing gauge of factory activity in the New York area dropped to -11.9 for October, well below estimates of 3.6,

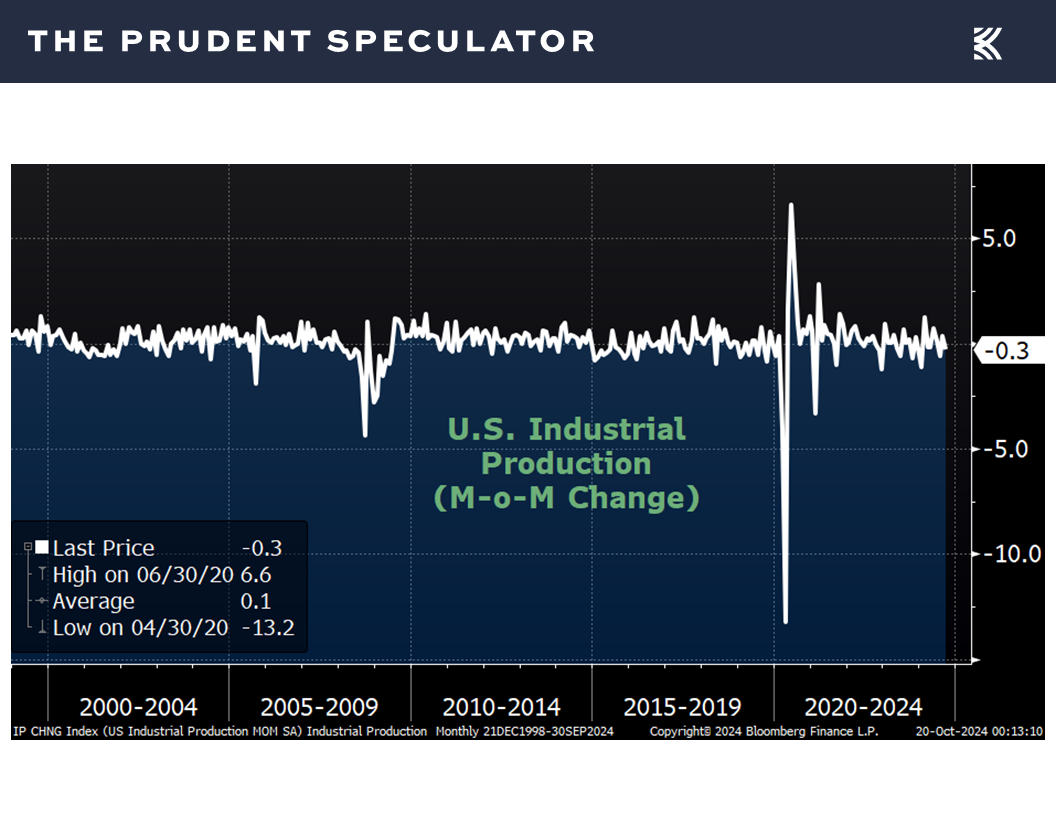

and industrial production in September retreated by a worse-than-forecast 0.3%, down from a revised increase of 0.3% in August.

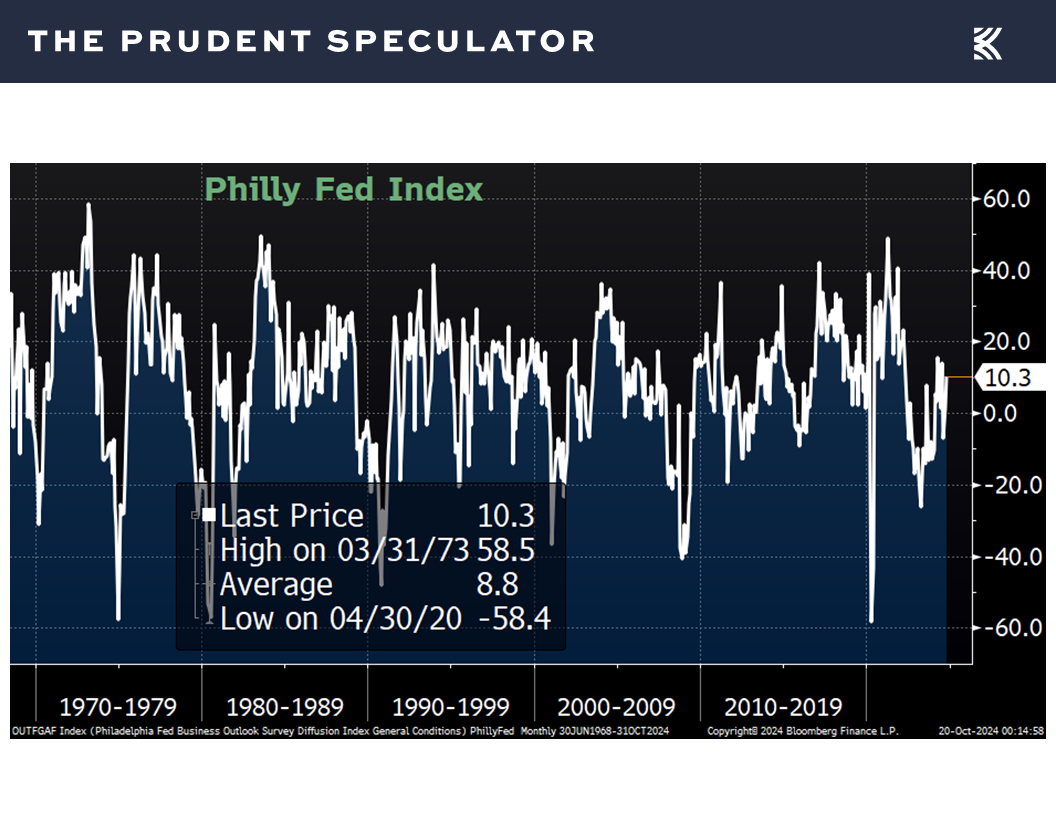

On the other hand, manufacturing activity in the Philadelphia area this month improved to a reading of 10.3, nicely higher than the 3.0 estimate and up from 1.7 in August,

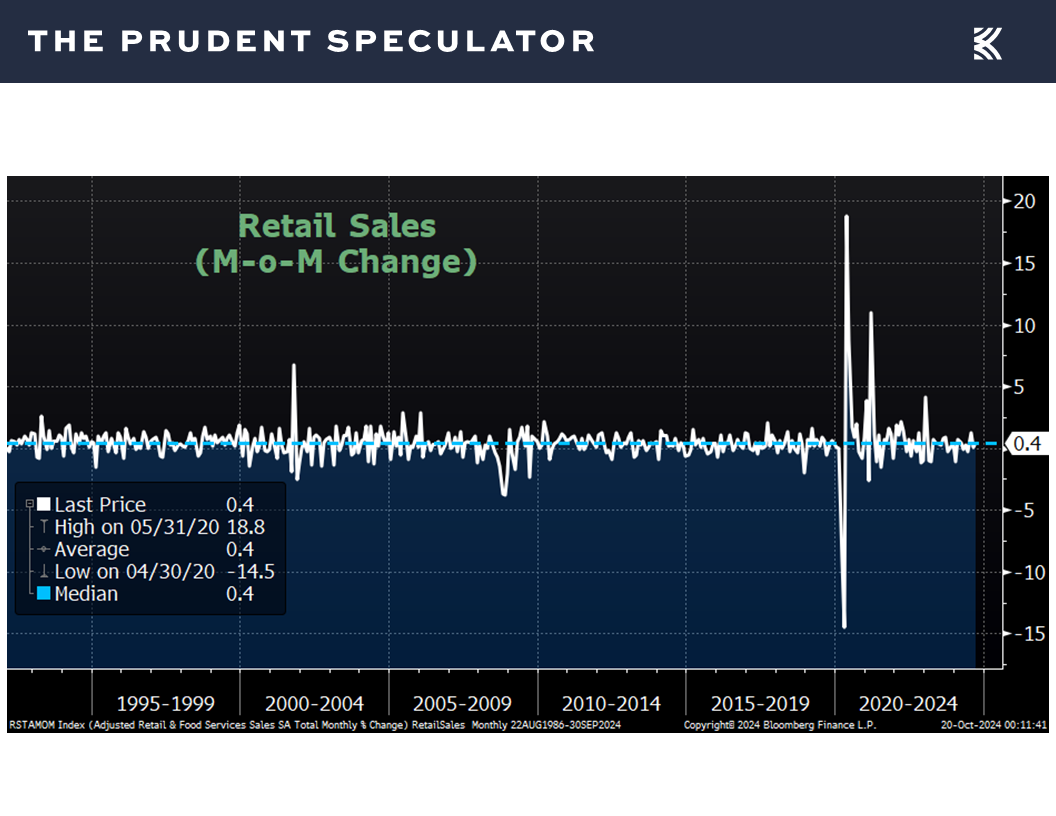

retail sales for September rose a better-than-expected 0.4%,

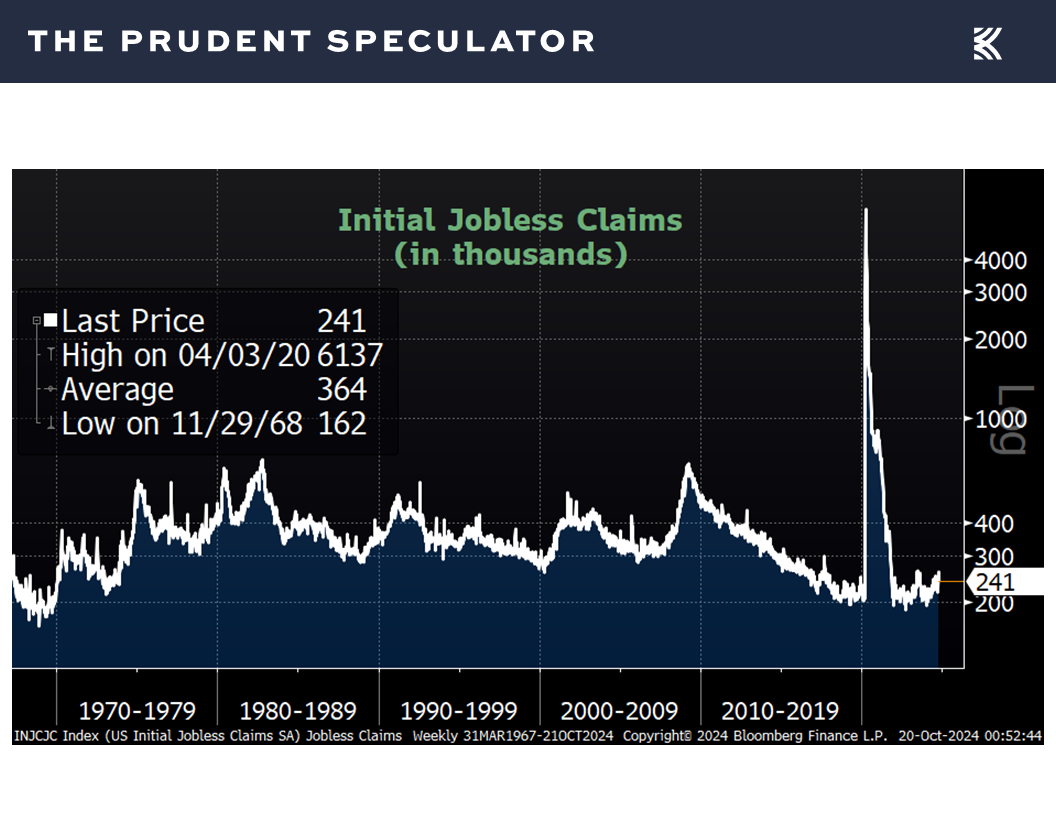

and first-time filings for unemployment benefits dropped to 241,000 in the latest week, down from a revised 260,000 the week prior,

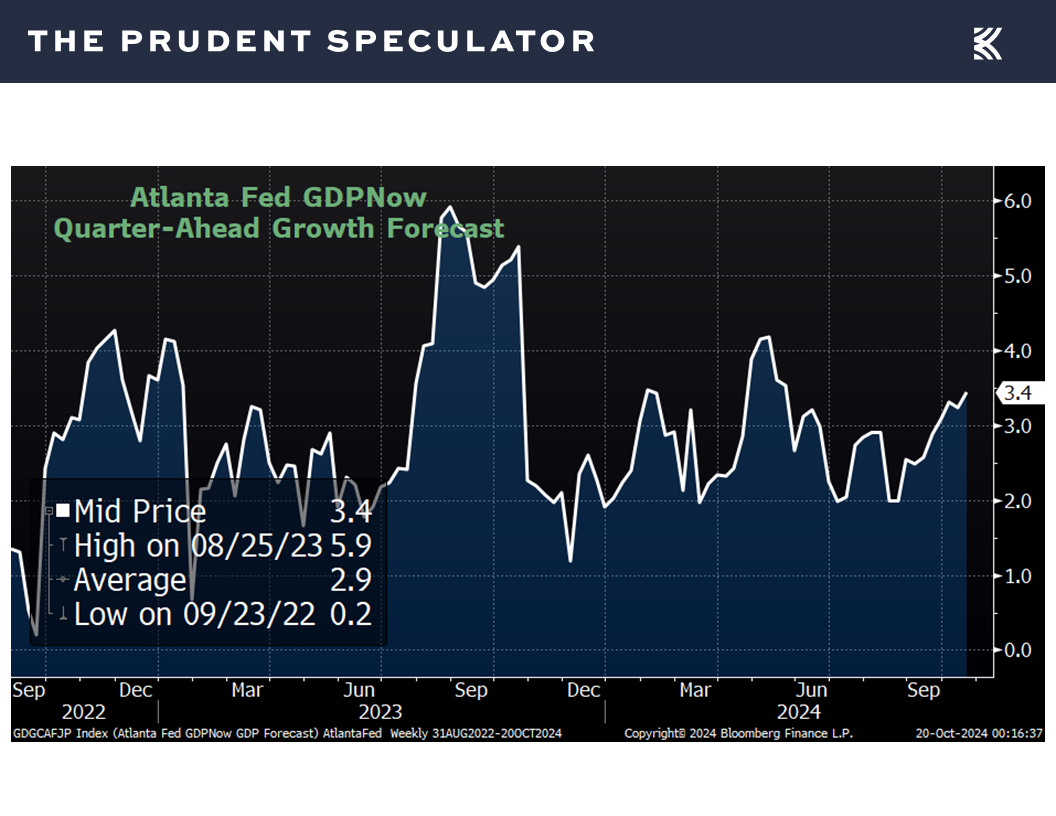

with the latest forecast from the Atlanta Fed for Q3 GDP growth rising last week to 3.4%, up from 3.2% the week prior.

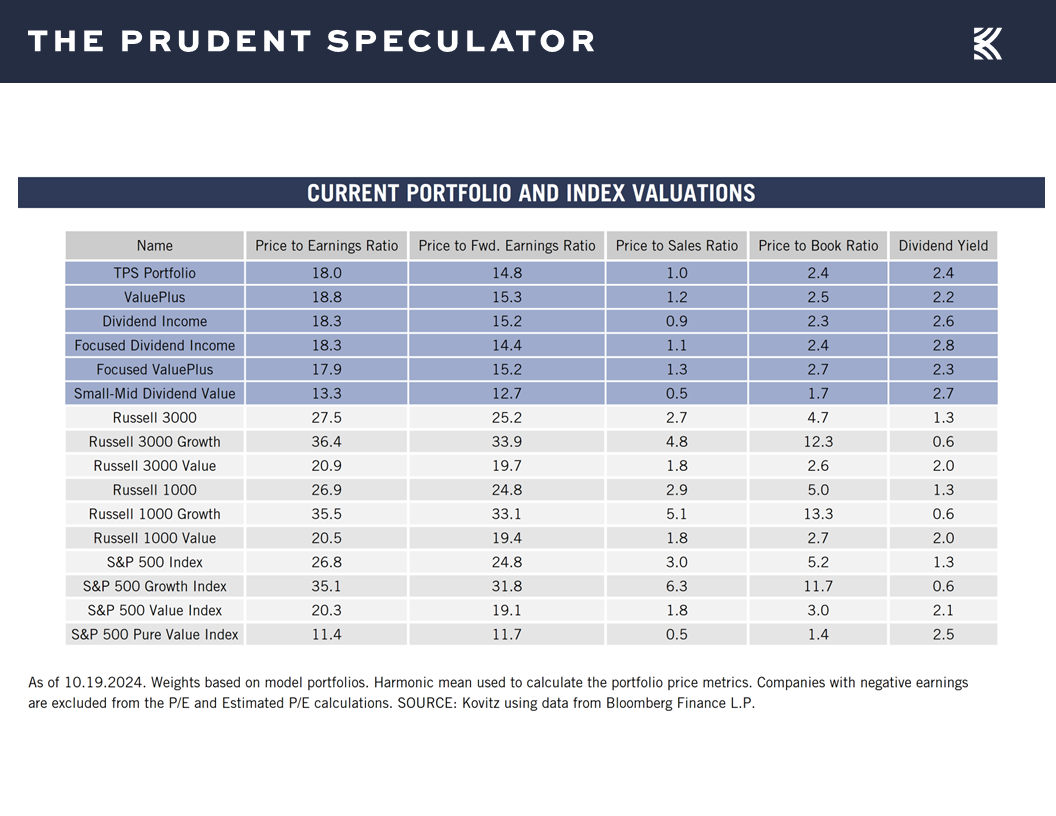

Valuations – Liking our Metrics

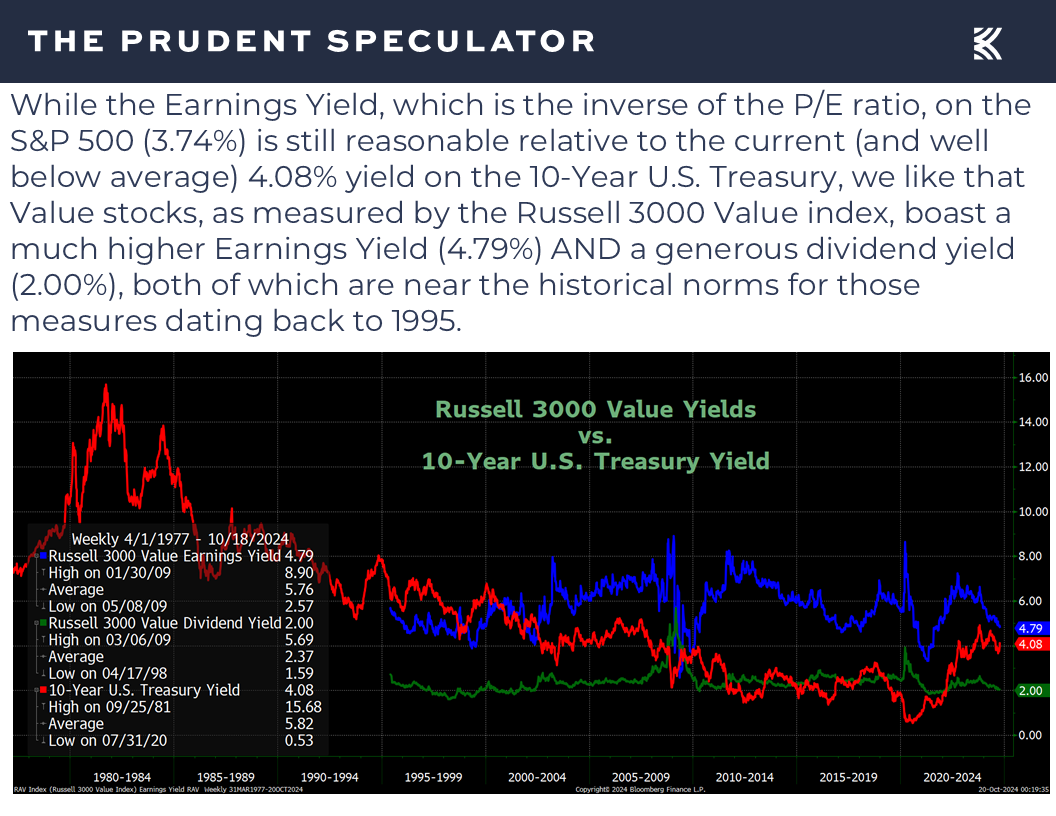

So, while we are always braced for market pullbacks and we have a little extra cash in our managed accounts these days, we continue to think that Value stocks in general are reasonably priced,

and we especially like the valuation metrics associated with our broadly diversified portfolios of what we believe are undervalued stocks.

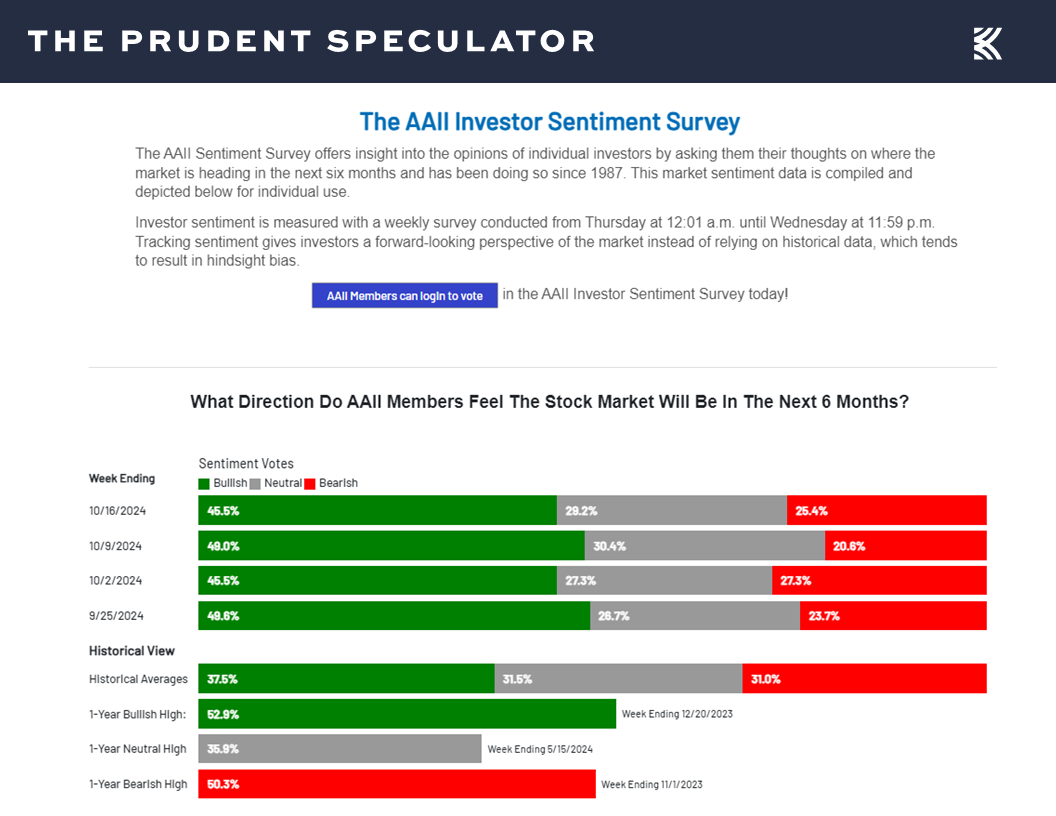

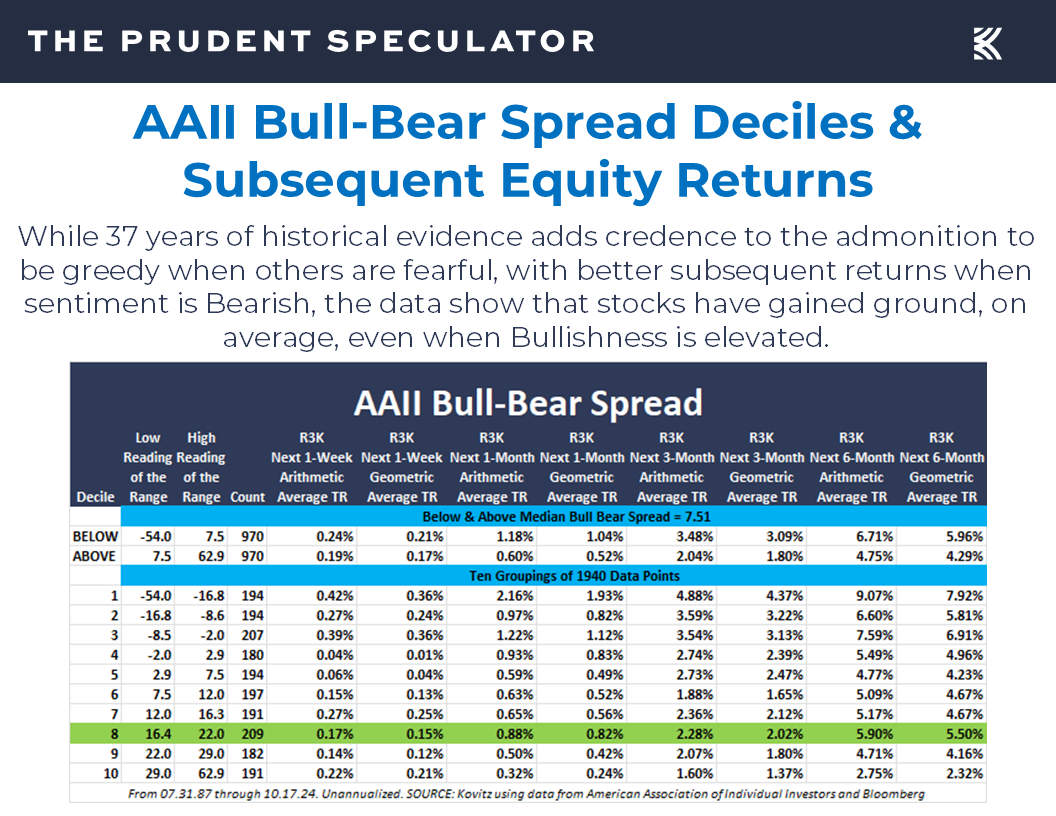

Sentiment – AAII Bullishness Retreats; Bearishness Jumps

And, we weren’t unhappy to see optimism retreat and pessimism rise on Main Street last week as tabulated in the weekly Bull-Bear Sentiment Survey from the American Association of Individual Investors,

though this supposedly contrarian measure argues for maintaining equity positions and not being fearful even when folks are greedy!

Stock News – Updates on nineteen stocks across seven different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

AAII Sentiment, Valuations, Interest Rates and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the AAII Sentiment, Valuations, Interest Rates and more. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Trading Week – Scary Season Rally Continues

Interest Rates – Yields have Jumped; Stocks Haven’t Minded Historically, on Average

Headlines – Stocks Always Have Overcome Disconcerting News in the Fullness of Time

Volatility – Ups and Downs but Long-Term Trend Has Been Up

Profits – Favorable EPS Outlook

Econ Outlook – Mixed Stats, but Solid GDP Growth the Forecast

Valuations – Liking our Metrics

Sentiment – AAII Bullishness Retreats; Bearishness Jumps

Stock News –

Interest Rates – Yields have Jumped; Stocks Haven’t Minded Historically, on Average

There are still nine trading days to go, but just as we said last week, the historically seasonally weaker September-October time span this time around has provided support for our long-held assertion that time in the market trumps market timing. Bucking the propensity for red ink, on average, since the launch of The Prudent Speculator in 1977,

the equity markets managed to again gain ground last week, adding to the handsome advance since the start of the often spooky two-month period.

All the gains of late have come since the Federal Reserve cut its target for the Fed Funds rate on September 18, which would seem to make sense, given the evidence since 1954 that shows that stocks perform better when the nation’s central bank is easing monetary policy.

However, longer-term interest rates actually have jumped since the Fed reduced short-term rates, with the yield on the 10-Year U.S. Treasury climbing from 3.65% on September 17 to 4.08% today.

Of course, history also shows that, on average, stocks perform fine whether the yield on the benchmark government bond is rising or falling,

Headlines – Stocks Always Have Overcome Disconcerting News in the Fullness of Time

as also has been the case when Arab-Israeli conflicts have occurred,

and following many other disconcerting events.

Volatility – Ups and Downs but Long-Term Trend Has Been Up

That is not to say that equities will rise no matter what, and there have been numerous worrisome downturns through the years, including a whopping 30 drops of 10% or more just since 1995, but over the long haul, stocks have proved rewarding for those who stick with them through thick and thin,

Profits – Favorable EPS Outlook

as corporations have become more valuable, given that their profits have grown over time, with earnings per share projected to expand nicely over the remainder of this year and in 2025.

No doubt, the strength of the economy is key to the growth of top and bottom lines for Corporate America, and statistics out last week continued to support the projections provided last month by Jerome H. Powell & Co. that call for inflation to move closer to the Fed’s long-run goal of 2.0% and real (inflation-adjusted) U.S. GDP growth to remain in the 2.0% range.

Econ Outlook – Mixed Stats, but Solid GDP Growth the Forecast

To be sure, some of the economic numbers were weaker-than-expected last week, as the Empire Manufacturing gauge of factory activity in the New York area dropped to -11.9 for October, well below estimates of 3.6,

and industrial production in September retreated by a worse-than-forecast 0.3%, down from a revised increase of 0.3% in August.

On the other hand, manufacturing activity in the Philadelphia area this month improved to a reading of 10.3, nicely higher than the 3.0 estimate and up from 1.7 in August,

retail sales for September rose a better-than-expected 0.4%,

and first-time filings for unemployment benefits dropped to 241,000 in the latest week, down from a revised 260,000 the week prior,

with the latest forecast from the Atlanta Fed for Q3 GDP growth rising last week to 3.4%, up from 3.2% the week prior.

Valuations – Liking our Metrics

So, while we are always braced for market pullbacks and we have a little extra cash in our managed accounts these days, we continue to think that Value stocks in general are reasonably priced,

and we especially like the valuation metrics associated with our broadly diversified portfolios of what we believe are undervalued stocks.

Sentiment – AAII Bullishness Retreats; Bearishness Jumps

And, we weren’t unhappy to see optimism retreat and pessimism rise on Main Street last week as tabulated in the weekly Bull-Bear Sentiment Survey from the American Association of Individual Investors,

though this supposedly contrarian measure argues for maintaining equity positions and not being fearful even when folks are greedy!

Stock News – Updates on nineteen stocks across seven different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.