The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss contrarian sentiments, interest rates, valuations and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week In Review – Sizable Setback; August a Tough Month, on Average, Since 1986

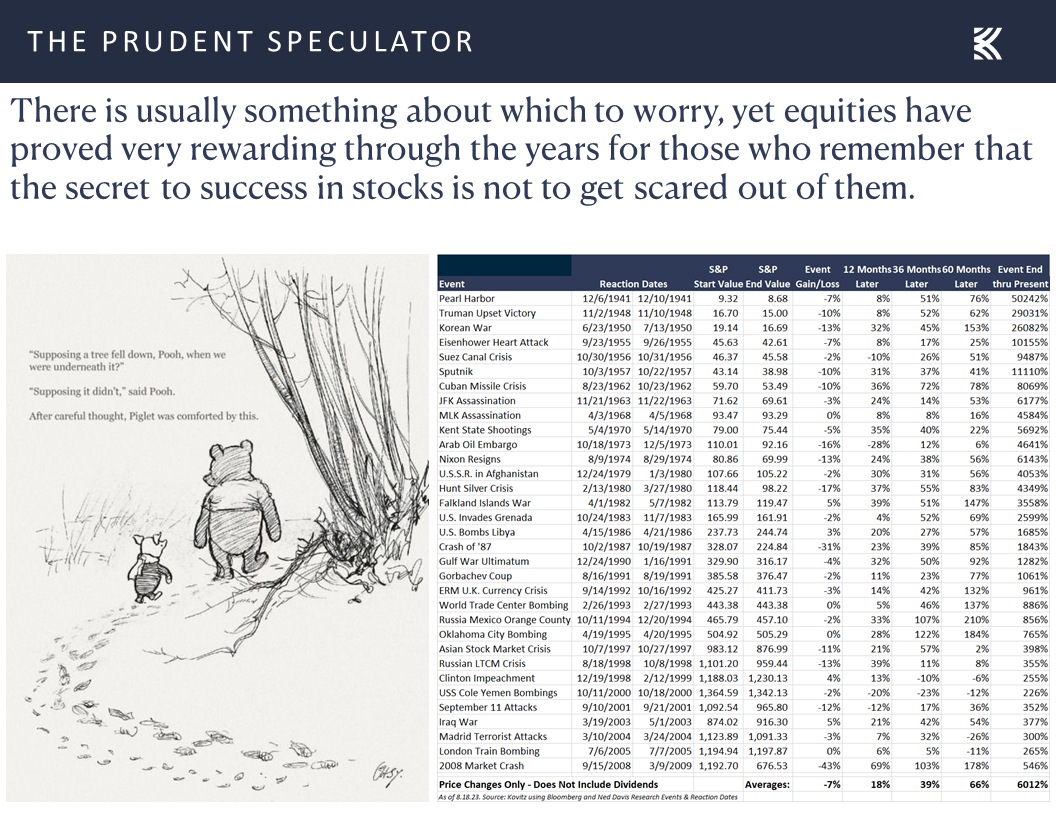

Patience – Lots to Worry About Along the Way, But Over Time Equities Have Proved Rewarding

Partnering With Great Corporations – Companies Become More Valuable as Economy, Profits and Dividends Grow Over Time

Econ News – Generally Favorable Numbers; Q3 GDP Outlook Improves

Interest Rates – History Lesson on Rising Rates and Equity Returns

Valuations – Inexpensive Multiples for our Stocks

Contrarian Sentiment – AAII Becomes Much Less Bullish

Stock News – Updates on nine stocks across four different sectors

Week In Review – Sizable Setback; August a Tough Month, on Average, Since 1986

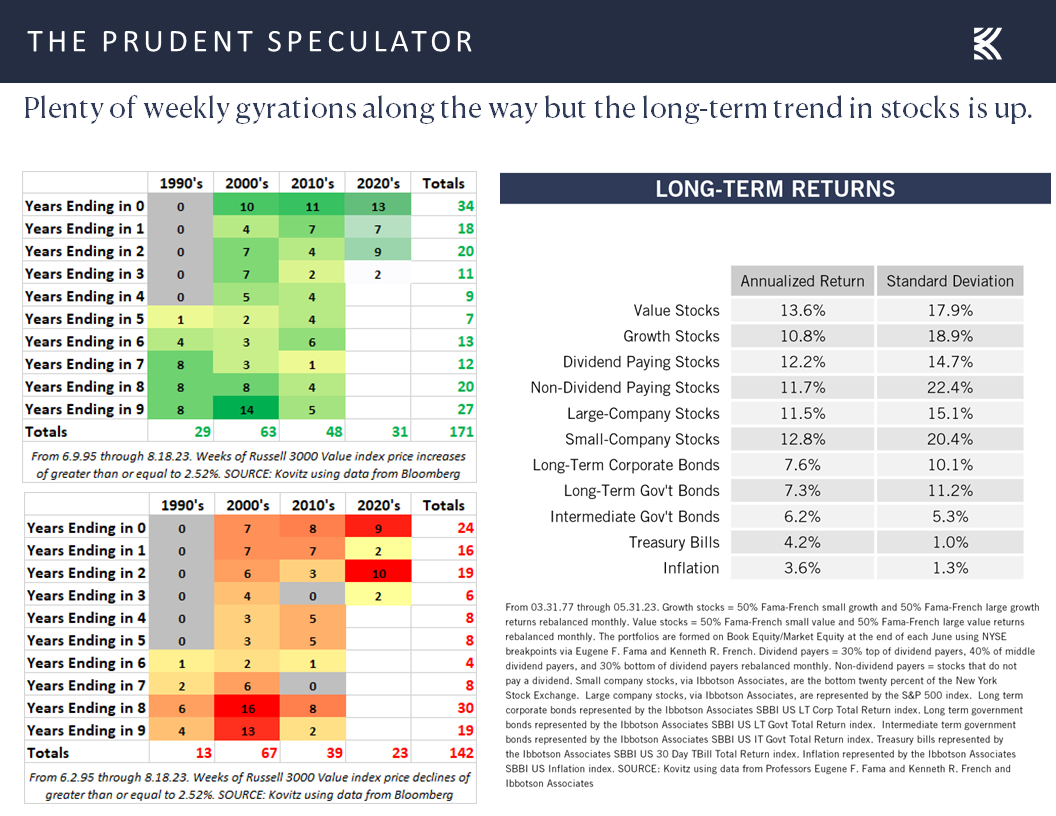

It was a lousy week for equities, with the major market averages pulling back 2% or more and the Russell 3000 Value index (R3KV) turning in the 142nd worst week in its 28-year history, skidding 2.52% on a price basis. Obviously, we never want to downplay moves to the downside, but weekly losses with the magnitude of last week’s or even greater have occurred five times per year on average. Happily, gains of comparable or larger scale have taken place with greater frequency, so much so that Value stocks have managed to post terrific returns of 13.6% per annum dating back to the inception of The Prudent Speculator in March 1977.

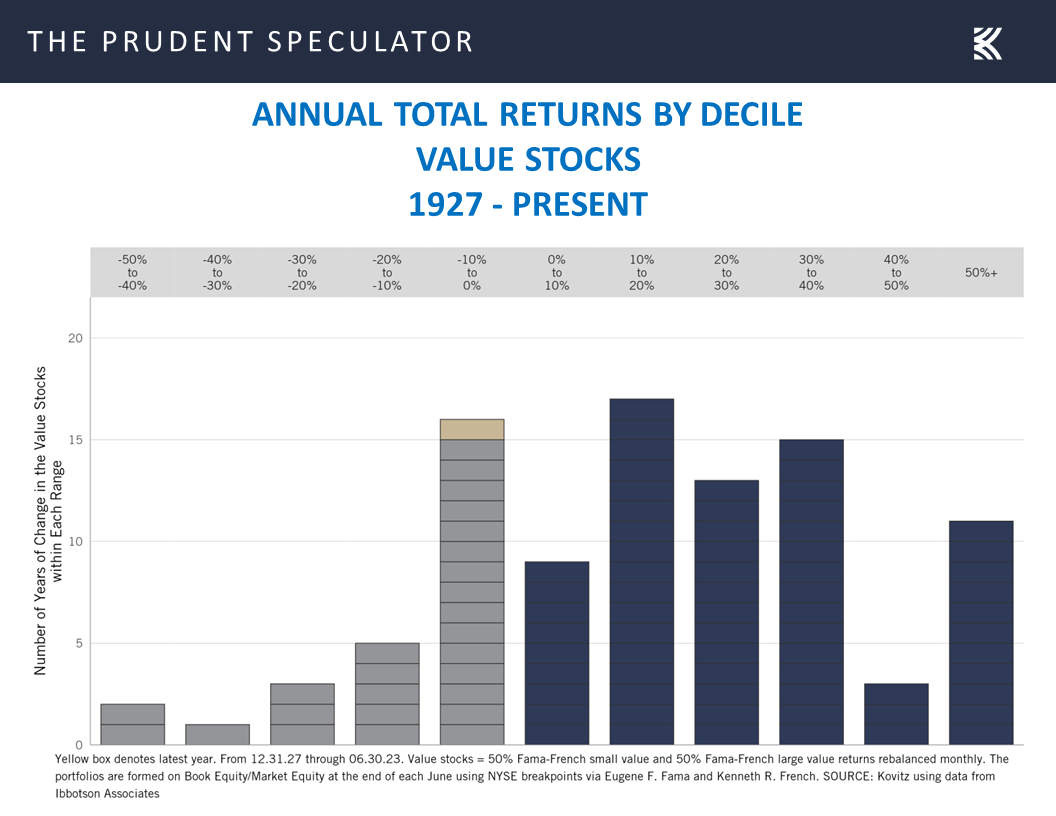

Patience – Lots to Worry About Along the Way, But Over Time Equities Have Proved Rewarding

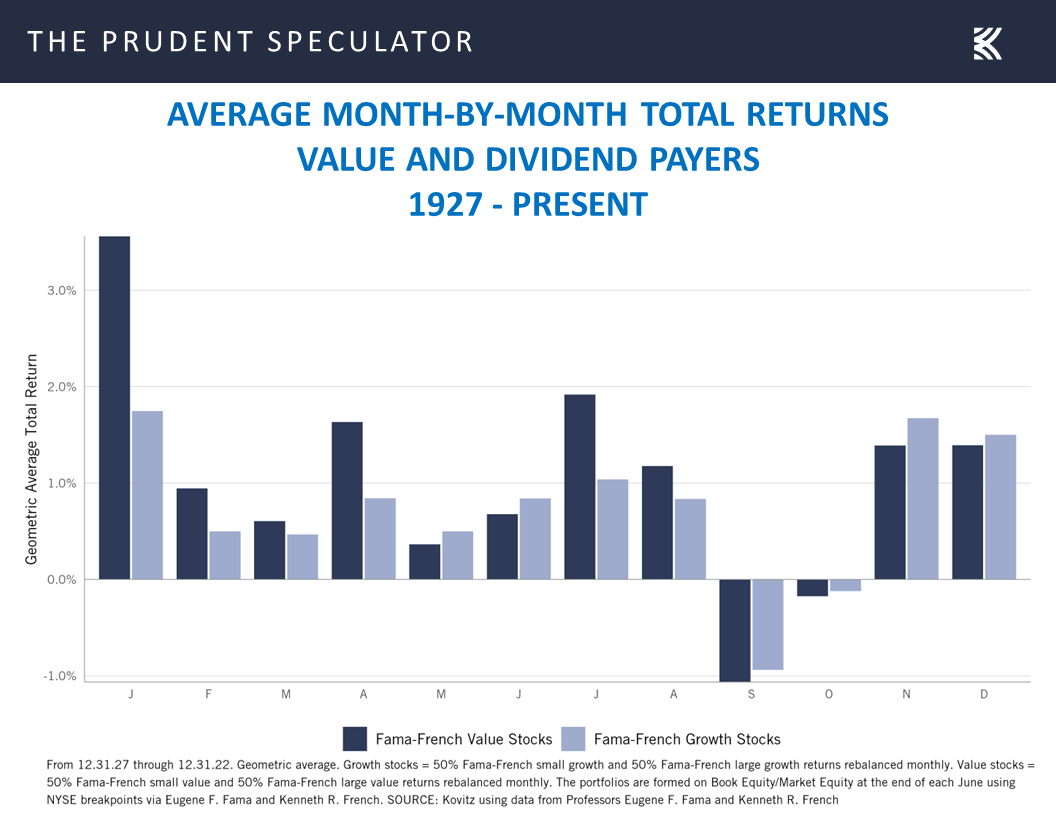

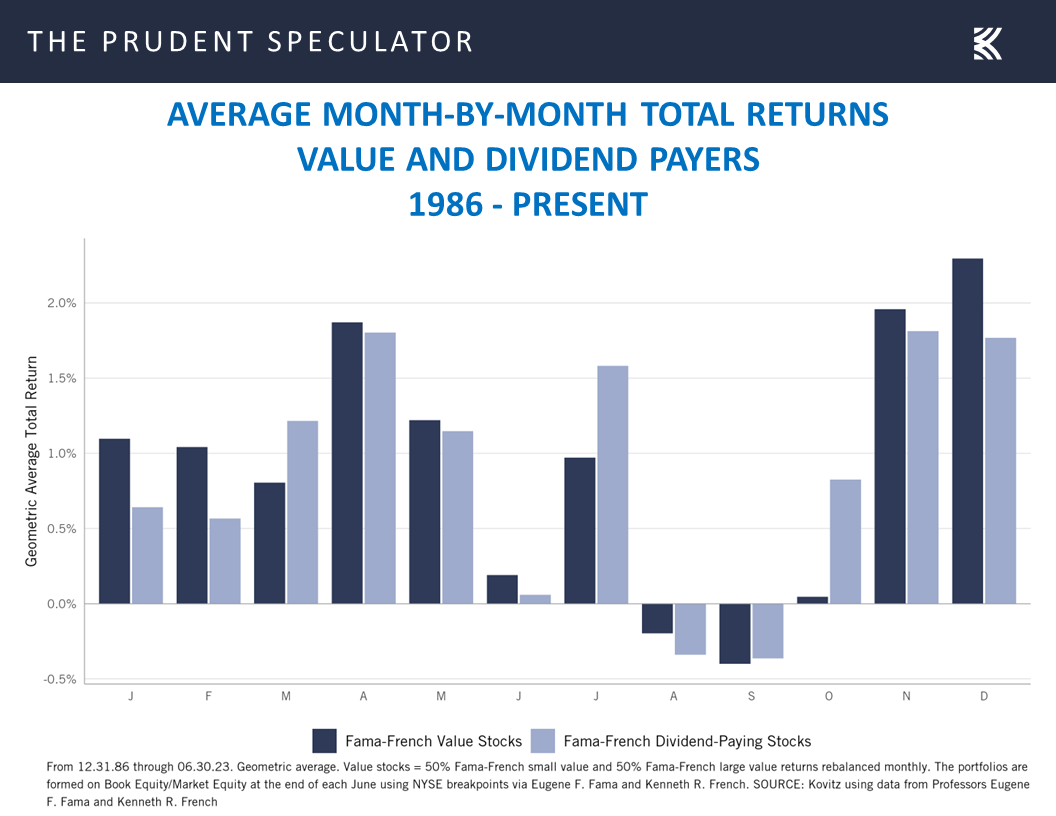

Interestingly, though August has been a fine performer, on average, for Value Stocks and Dividend Payers going all the way back to 1927,

the month has been in the red, again on average, for both since your Editor came to learn at the foot of the great Al Frank in early-1987.

Partnering With Great Corporations – Companies Become More Valuable as Economy, Profits and Dividends Grow Over Time

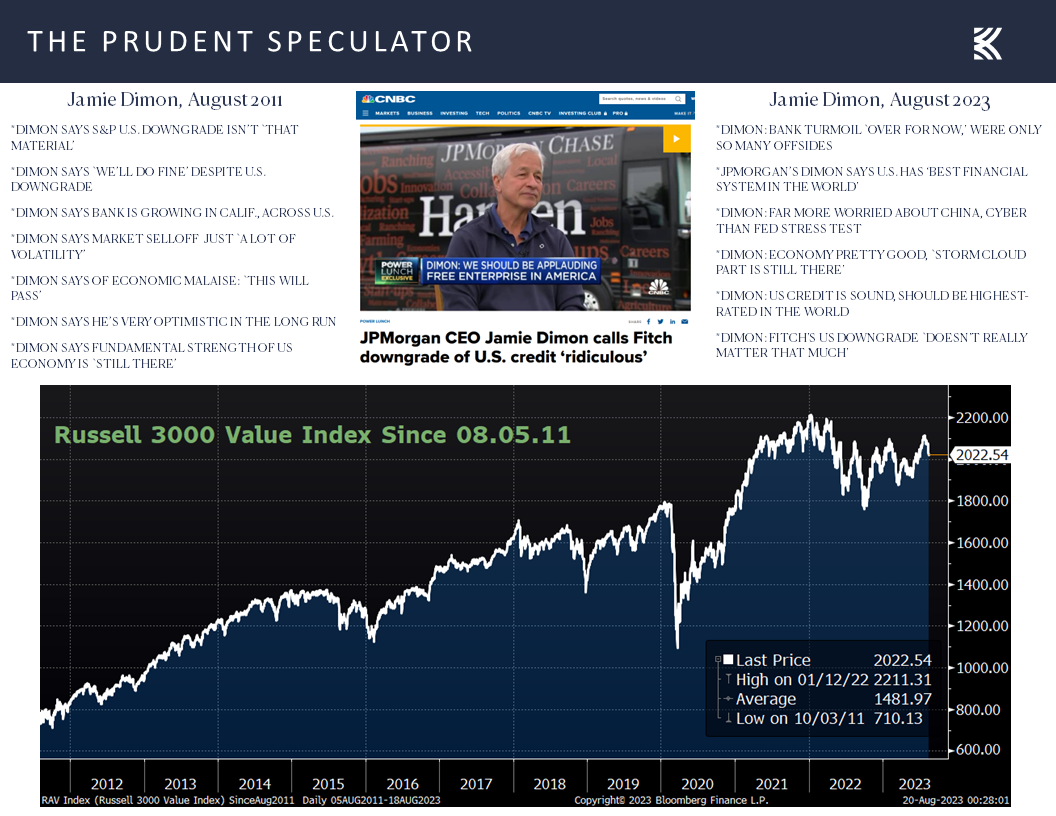

While volatility is hardly unusual, many will point to the downgrade of the U.S. credit rating by Fitch Ratings on August 1 as the catalyst for the current decline, even as JPMorgan Chase (JPM – $148.97) CEO Jamie Dimon was quick to dismiss the move, saying that it doesn’t really matter that much.

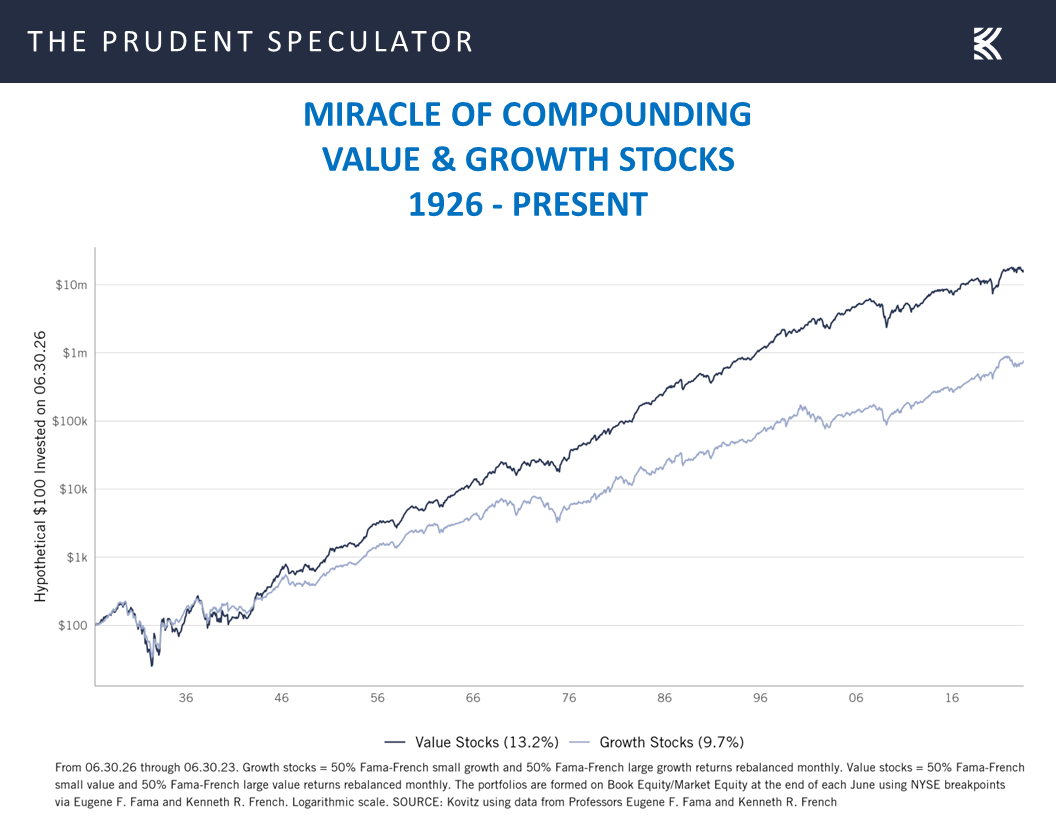

Those comments echoed his response to a similar downgrade from Standard & Poor’s on August 5, 2011. Back then, Mr. Dimon argued that decision wasn’t that material, even as the R3KV index plunged 7.4% in the wake of the S&P downgrade. Of course, that dip is hardly visible on the chart below.

The R3KV is off 4.2% this time around and we note that the S&P-Downgrade losses in 2011 were recouped less than a month later, with the incident not even showing any red ink when measured with a three-month-or-longer ruler. History is merely a guide and not the gospel, but equities have been overcoming disconcerting events since the dawn of stock trading.

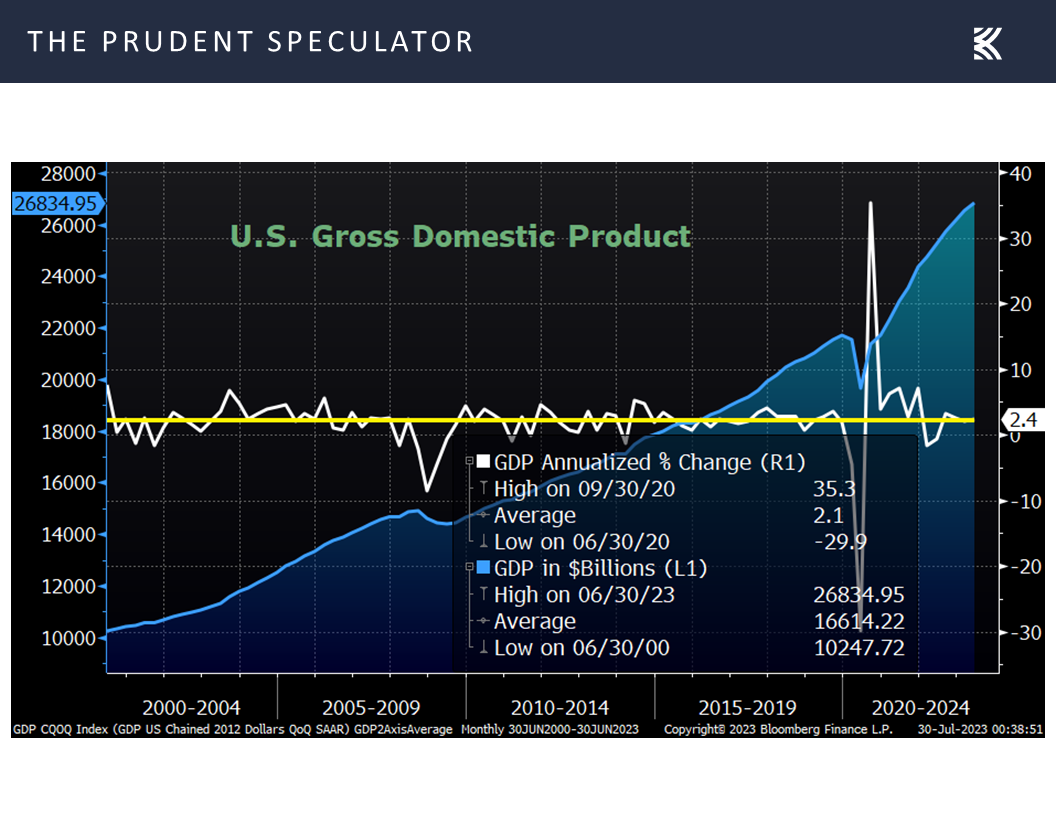

To be sure, anything can happen in the near-term, but Al Frank taught us, “We think of ourselves as partners in great corporations, growing in wealth as they prevail, rather than traders of pieces of paper.” Given that the economy grows over time,

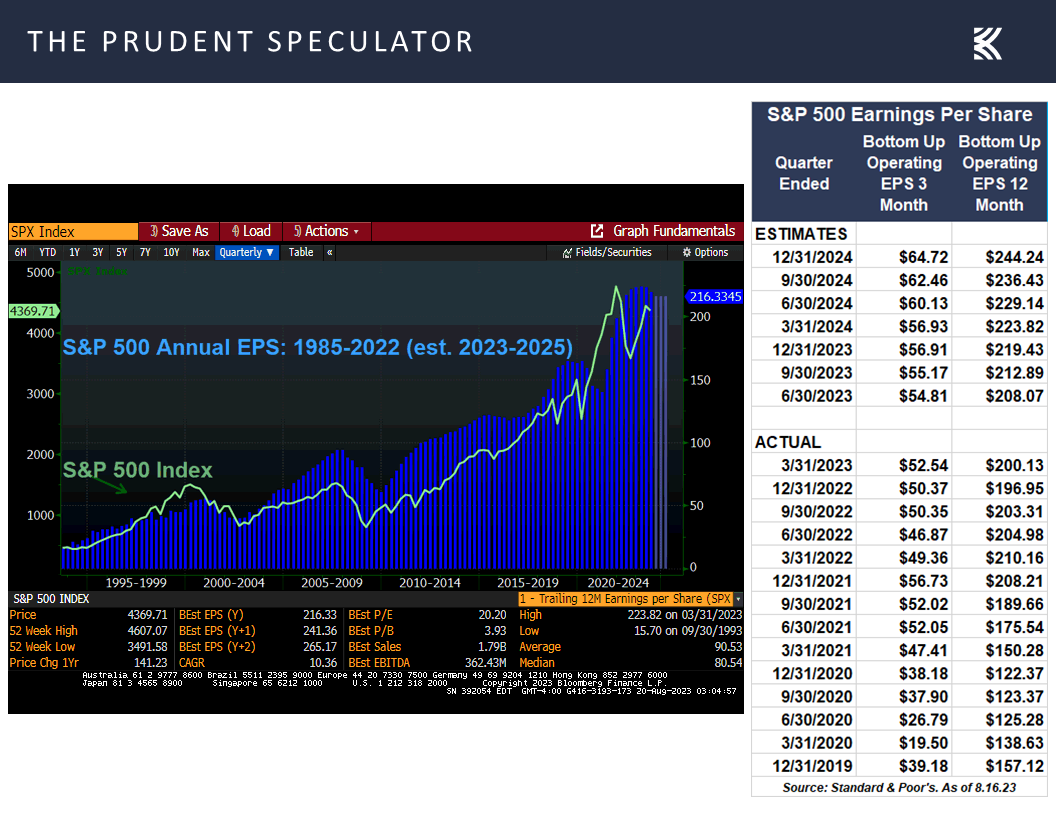

as do corporate profits,

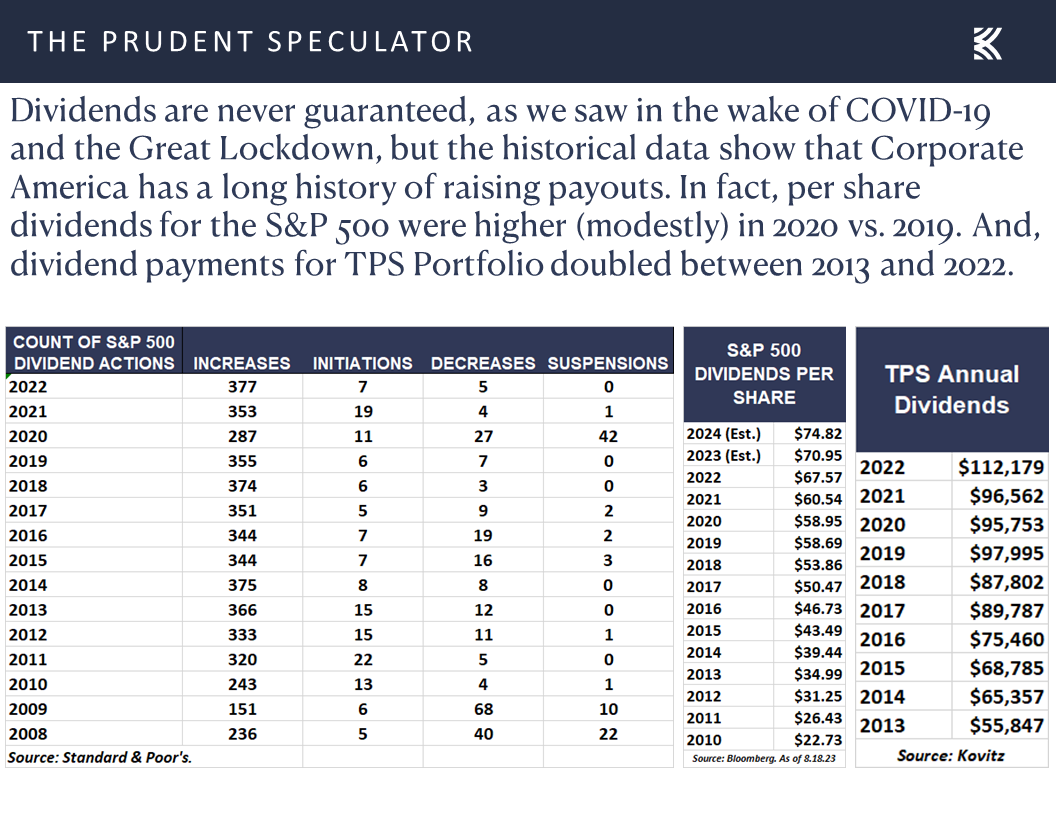

and dividend payouts,

it shouldn’t be a grand surprise that stocks have turned in far more good years than bad,

and that substantial wealth has accrued to those who remember that time in the market trumps market timing.

Econ News – Generally Favorable Numbers; Q3 GDP Outlook Improves

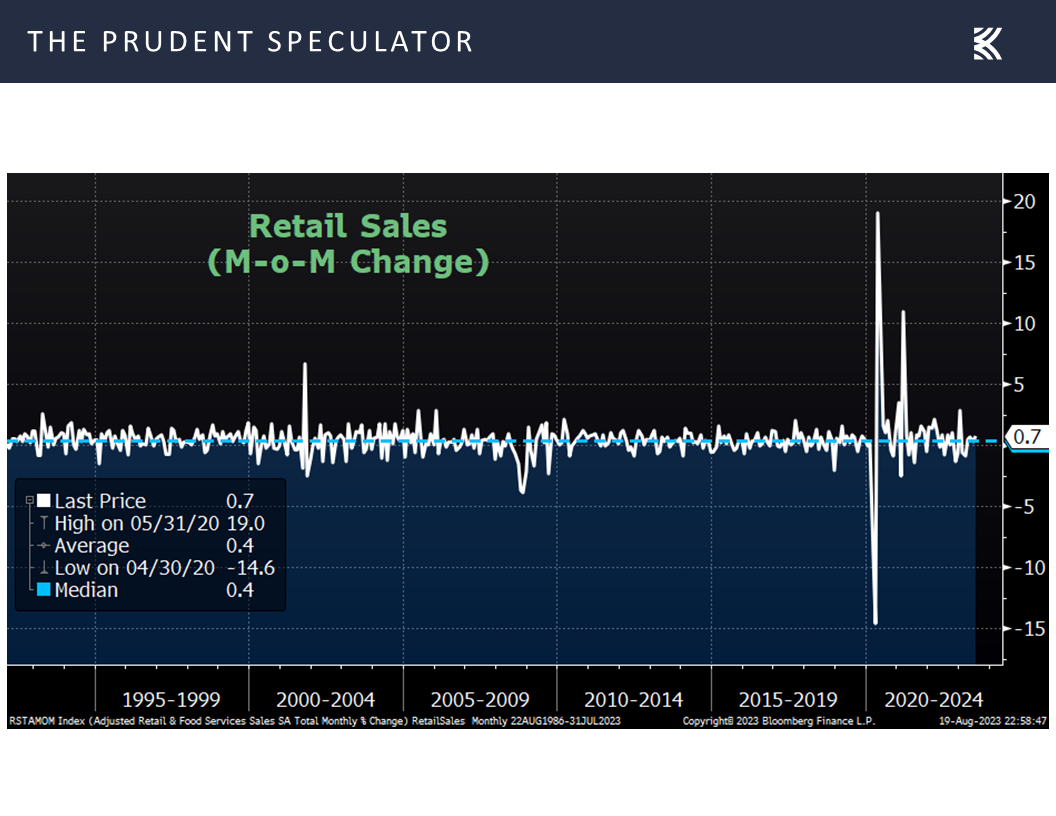

And speaking of the economy, the numbers out last week generally were favorable, as retail sales rose 0.7% in July, the largest increase in six months and better than expectations,

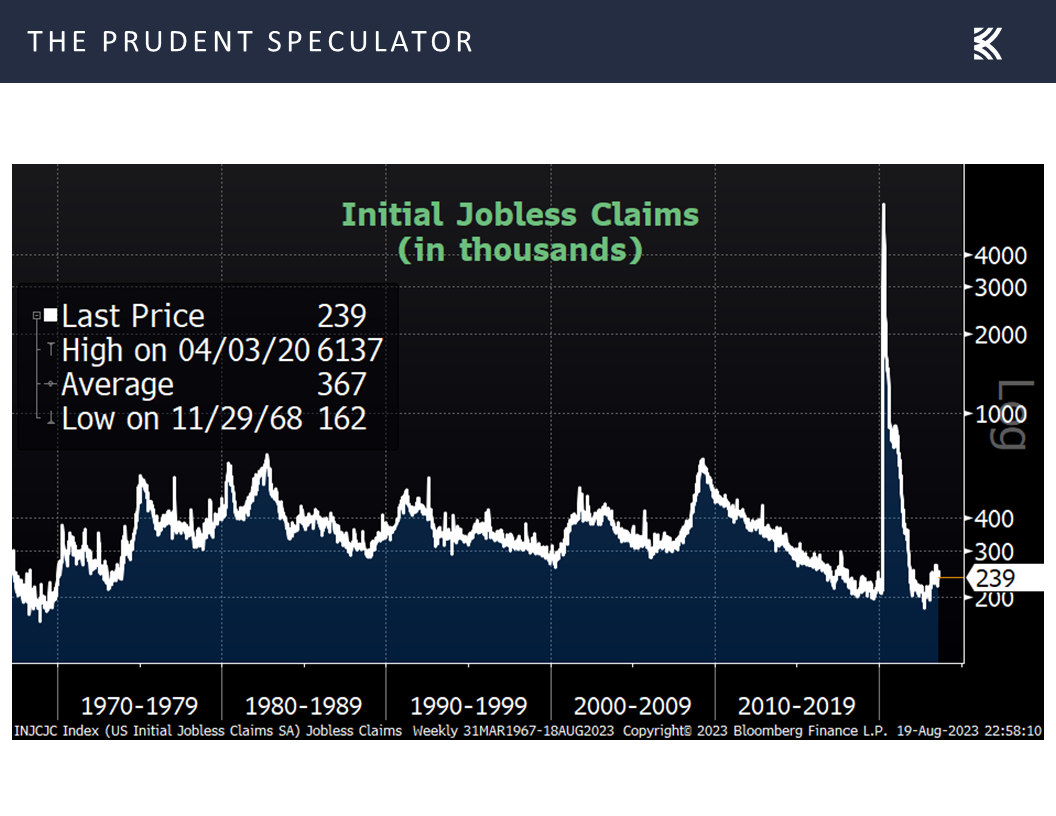

while first-time filings for unemployment benefits dipped to a historically very low 239,000, down from 250,000 the week prior, confirming the exceptional strength of the labor market.

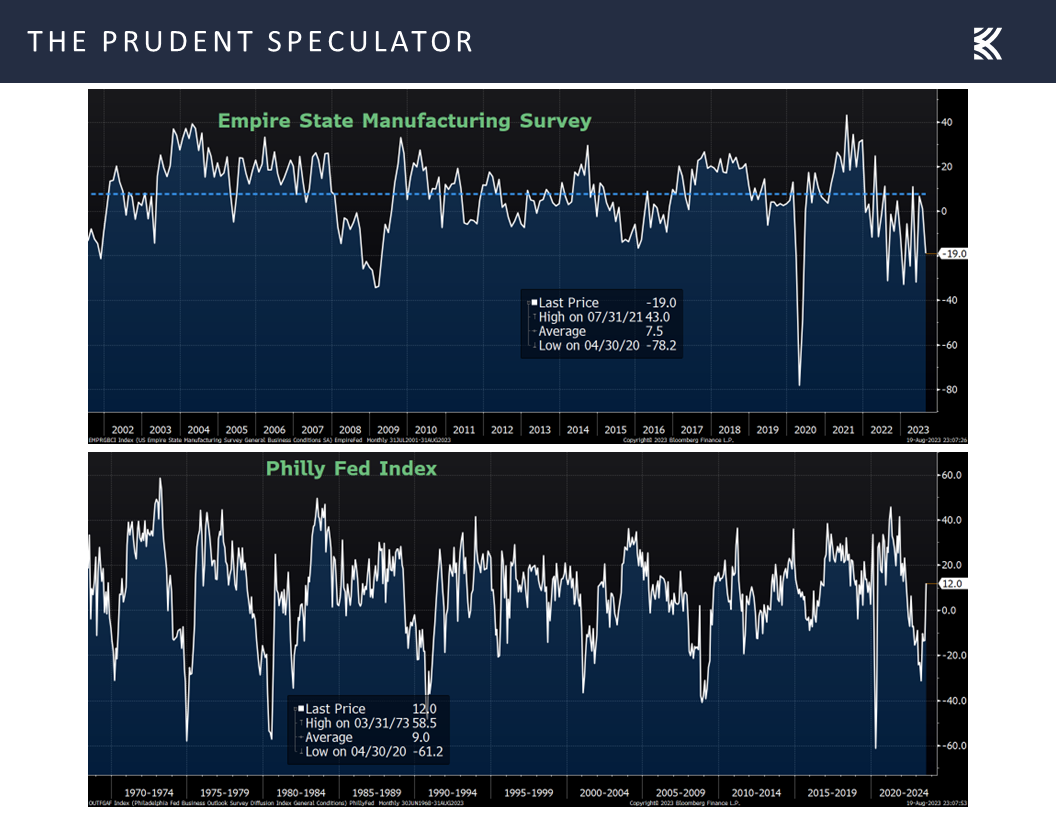

To be sure, there were mixed numbers on the health of the manufacturing sector on the East Coast, with the Empire State PMI trailing estimates by a wide margin, but the Philadelphia Fed PMI came in well above forecasts.

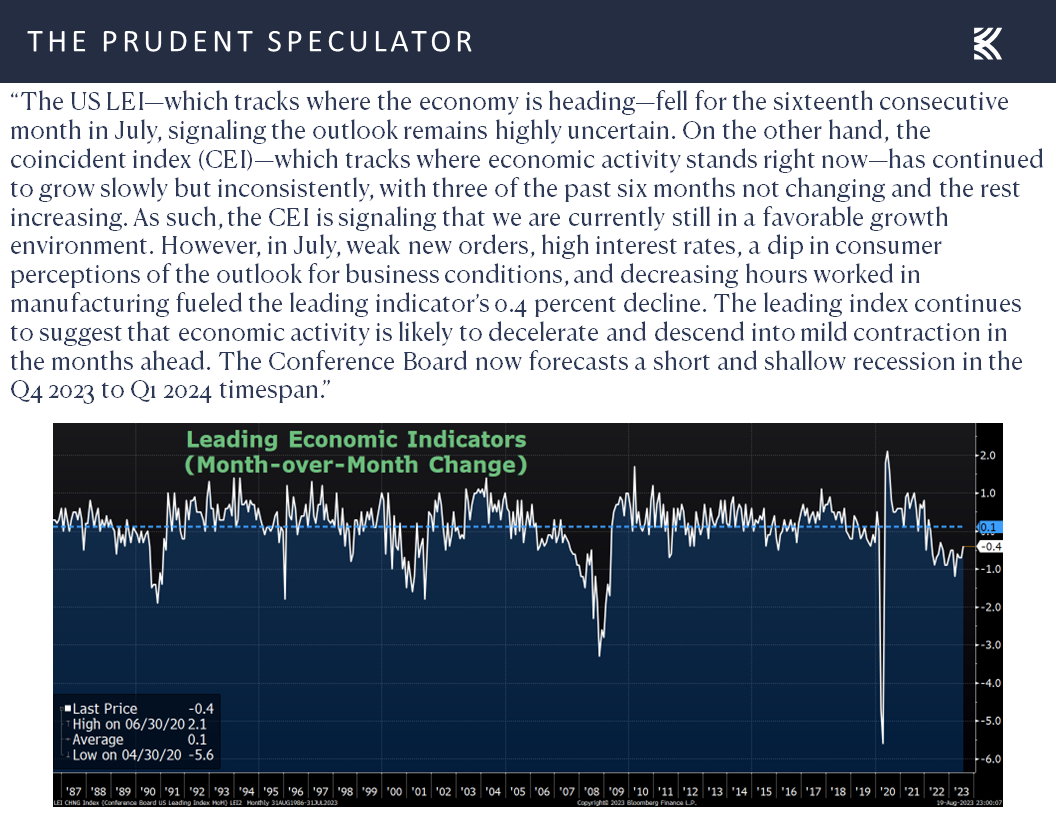

The important forward-looking Leading Economic Indicators (LEI) for July turned out to be in line with projections, but the -0.4% reading was an improvement from the -0.7% figure posted in June. And perhaps more interesting, the Conference Board, the keeper of the LEI gauge, tempered its economic contraction call to a “short and shallow recession in the Q4 2023 to Q1 2024 timespan,” from the color offered the month prior. Last month, the Conference Board argued, “We forecast that the U.S. economy is likely to be in recession from Q3 2023 to Q1 2024. Elevated prices, tighter monetary policy, harder-to-get credit, and reduced government spending are poised to dampen economic growth further.”

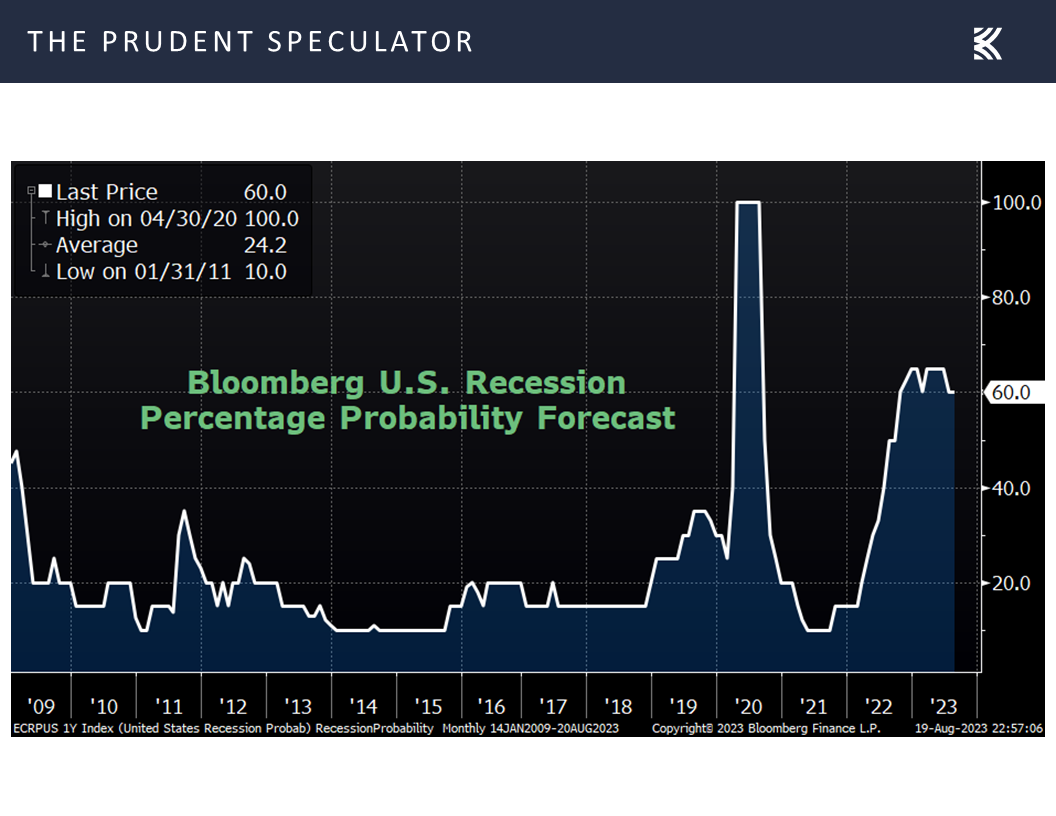

Still, a pessimistic view on the prospects for economic growth seemingly remains the consensus call,

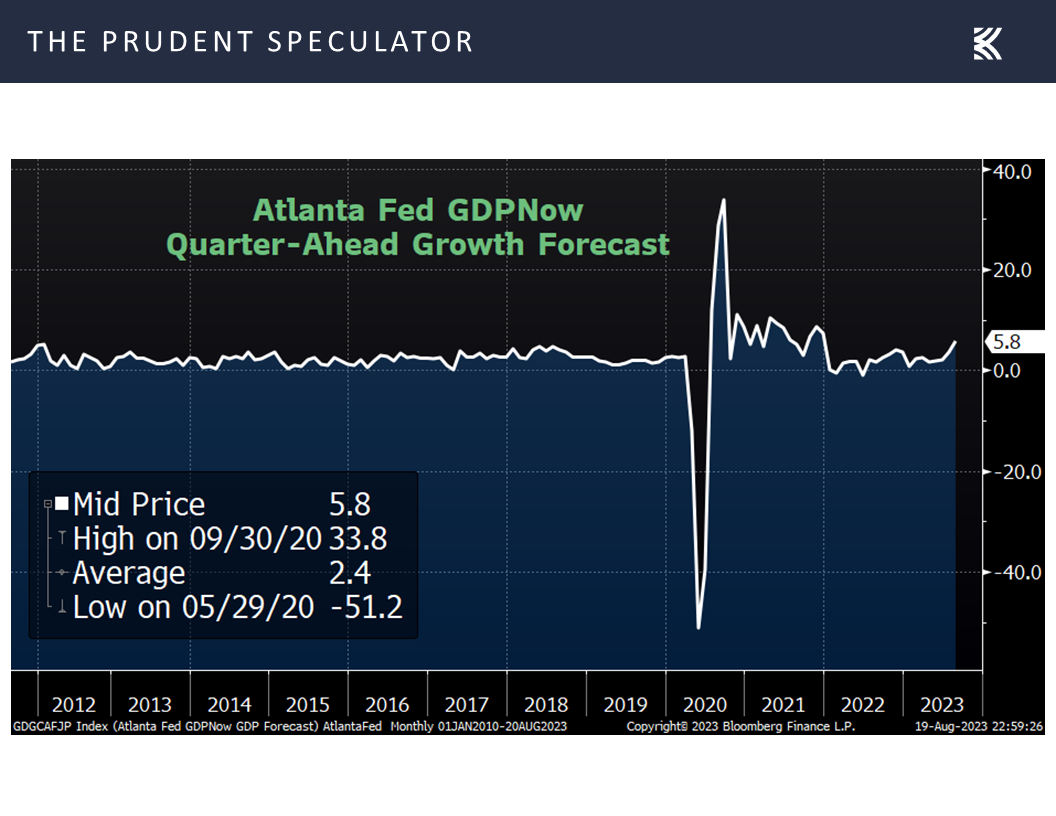

even as the latest estimate for Q3 real (inflation-adjusted) U.S. GDP growth jumped to a whopping 5.8% last week, per calculations from the Atlanta Fed.

Is it any wonder that John Kenneth Galbraith stated, “The only function of economic forecasting is to make astrology look respectable?”

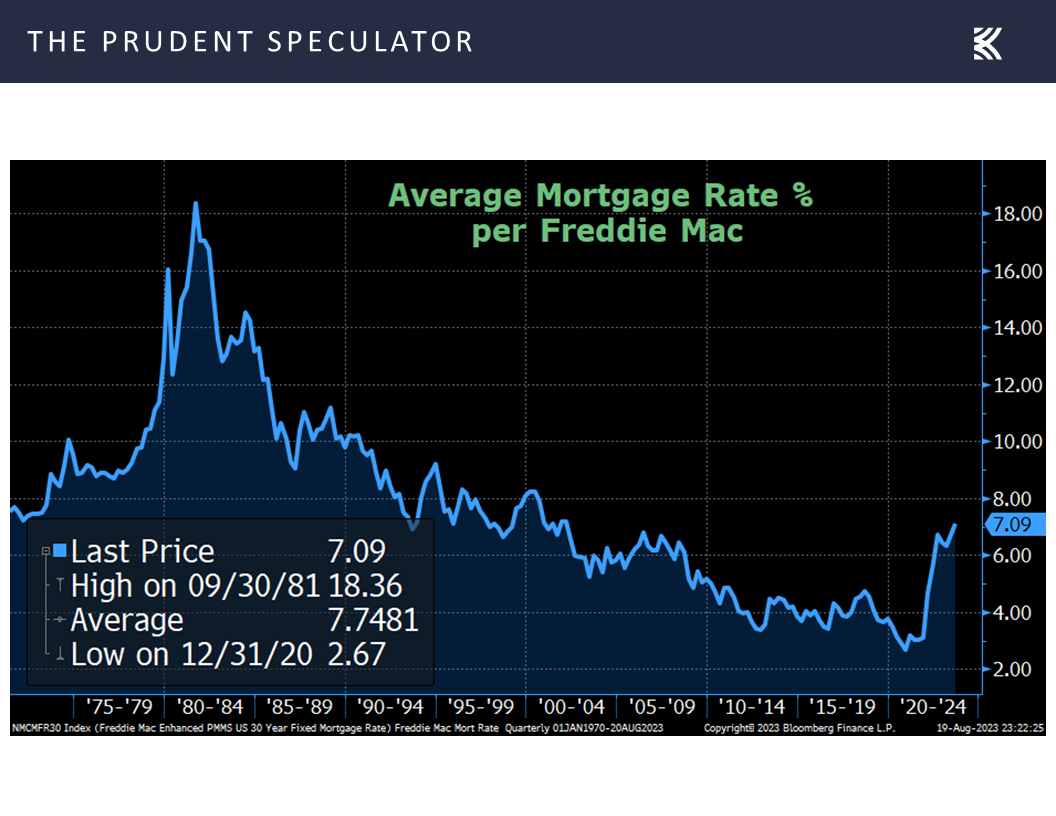

Interest Rates – History Lesson on Rising Rates and Equity Returns

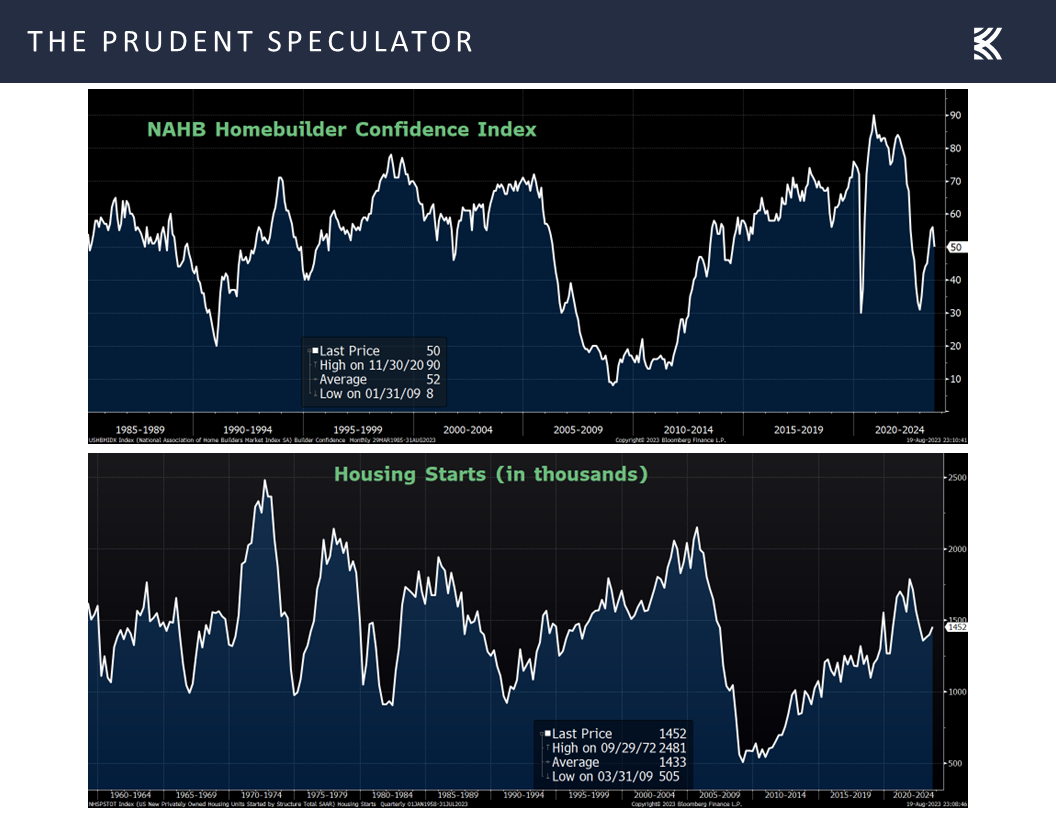

Clearly, the economy faces headwinds as mortgage rates are now at their highest level in more than two decades, but borrowing costs for home buyers are still below the historic average dating back to 1970,

and homebuilder confidence has held up better than many might have expected, with housing starts ticking up in July.

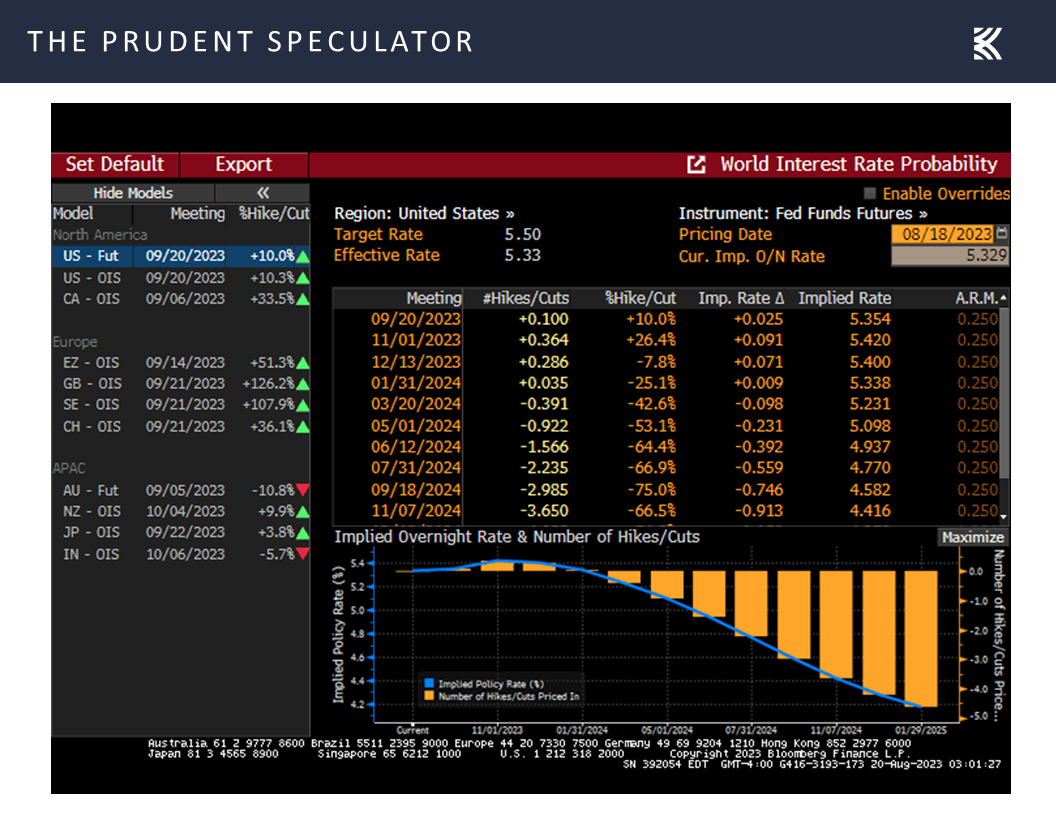

Interestingly, the worry for some market participants is that the economy might be too strong for the Federal Reserve’s taste, as expectations for cuts in the Federal Funds rate next year were reined in a bit last week,…

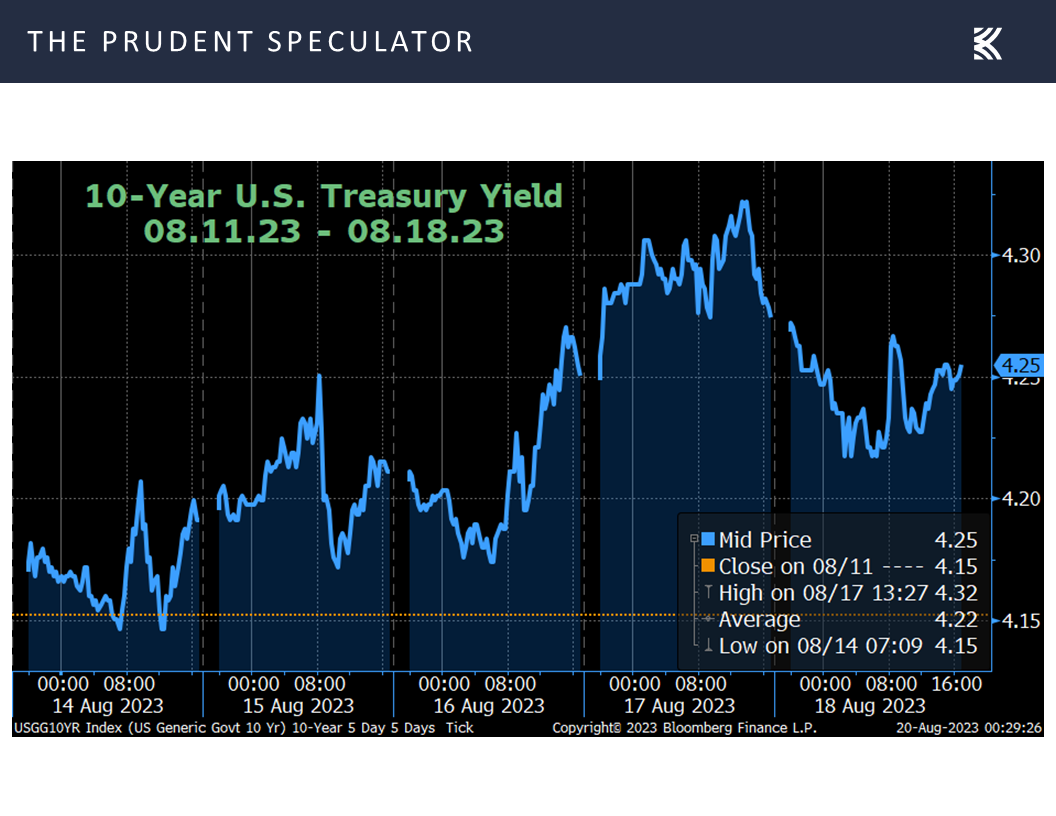

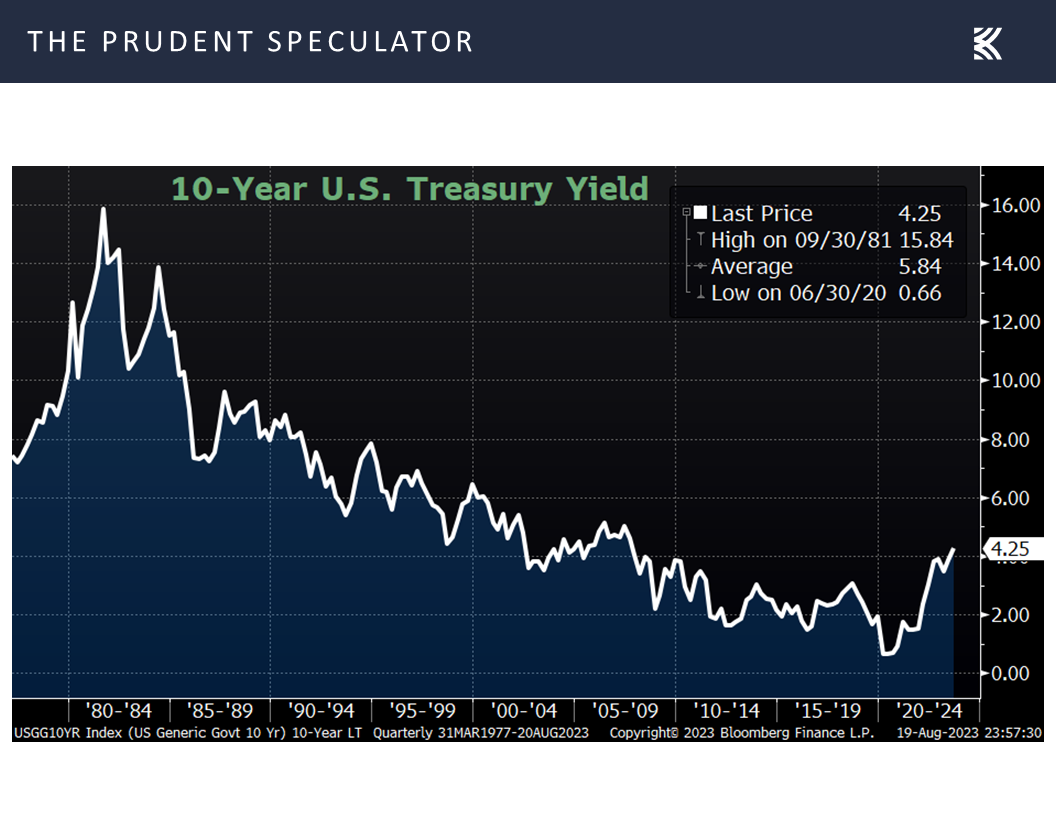

and the yield on the benchmark 10-Year U.S. Treasury closed Friday at 4.25%, after hitting 4.32% on Thursday, the latter tally the highest since 2007.

Not surprisingly, the rise in interest rates and the dip in stocks brought out the usual talking heads offering statements like, “When investors start demanding higher yields on longer-term bonds to compensate for the risk of inflation, that is correlated with lower risk-asset prices.” Such a view sounds logical in theory, but in practice, one doesn’t have to look too hard to find evidence to the contrary.

After all, the yield on the 10-Year was 3.88% at the start of 2023, yet stocks have enjoyed a solid year thus far, though we should add that the current level of 4.25% is still well below the long-term average of 5.84%.

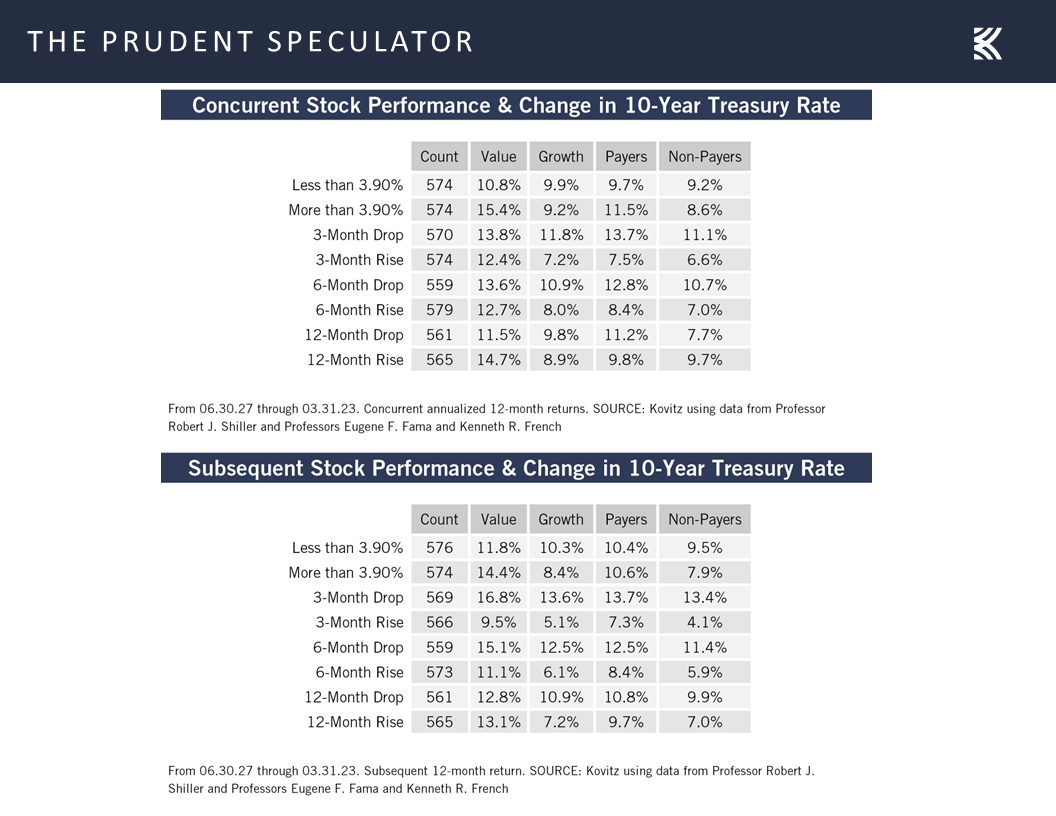

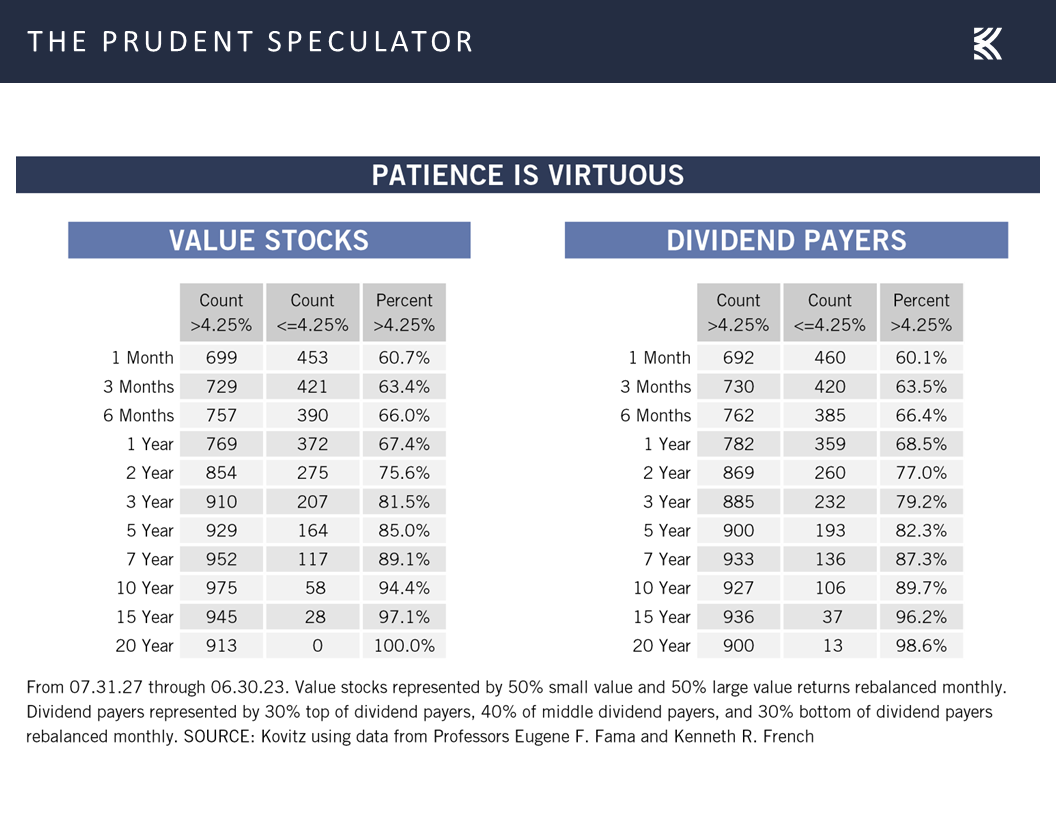

Believe it or not, and further debunking the “rising-rates-lead-to-lower-stock-prices” assertion, history shows that Value Stocks and Dividend Payers have each done better, on average, when the yield on the 10-Year Treasury is above the long-term median than when it is below. True, equities arguably prefer to see rates falling, in terms of the concurrent and subsequent performance shown above, but the data is overwhelming, on average, that those with a long-term (or even intermediate-term) time horizon should not fret about a rising 10-Year Treasury yield.

That does not mean that stocks won’t move south in the near-term, but we like the historical odds that the longer one holds Value Stocks and Dividend Payers, the greater the chance of better returns than what a 10-Year Treasury buyer will receive today.

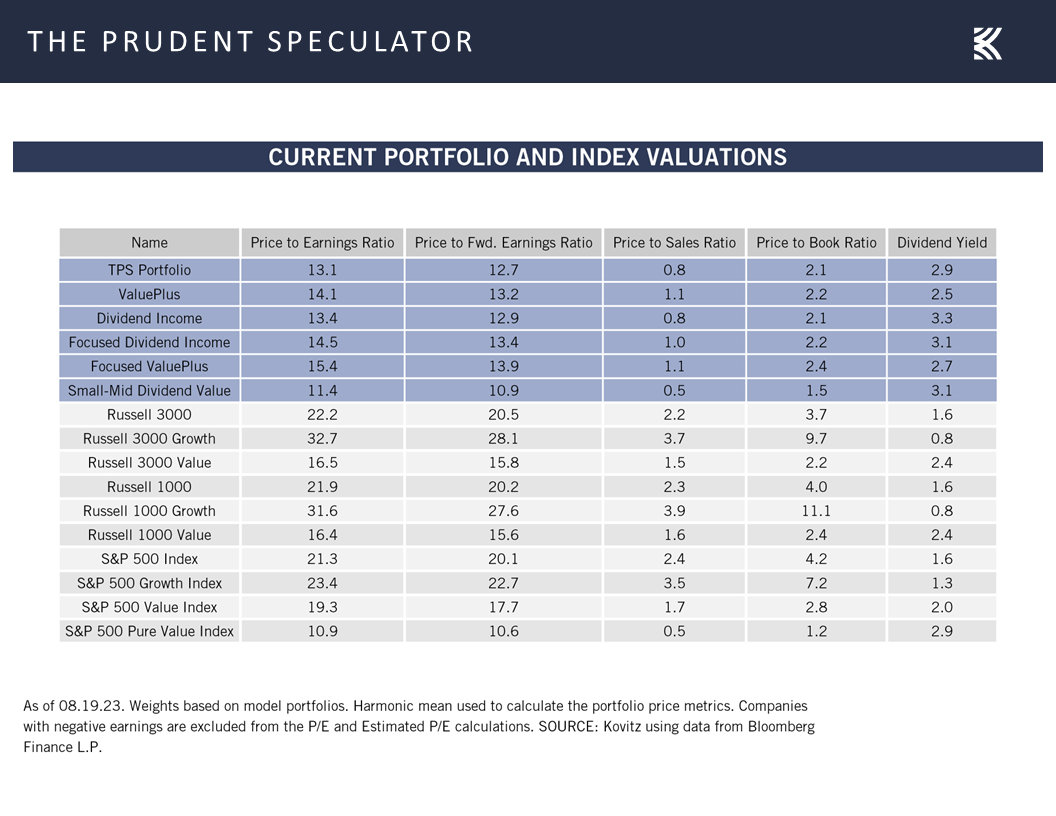

Valuations – Inexpensive Multiples for our Stocks

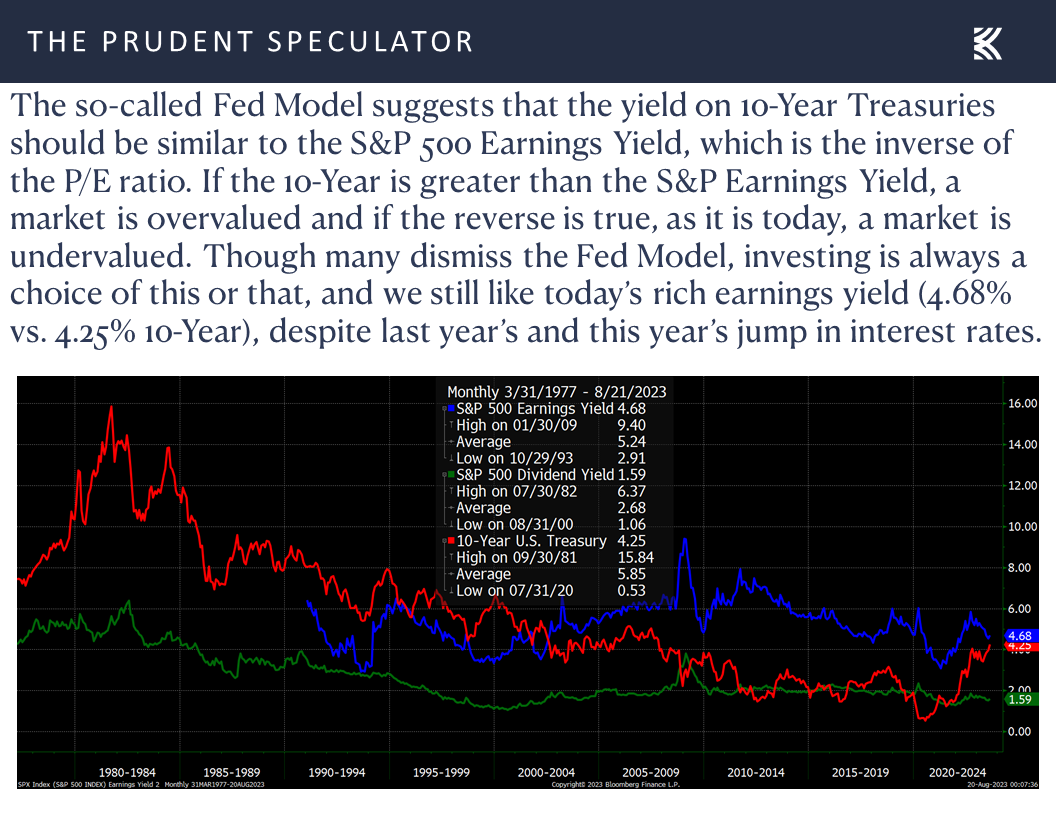

As always, we remain braced for additional downside market activity, but we continue to think that stocks in general are reasonably priced,

and that our broadly diversified portfolios of what we believe to be undervalued stocks are inexpensively priced,

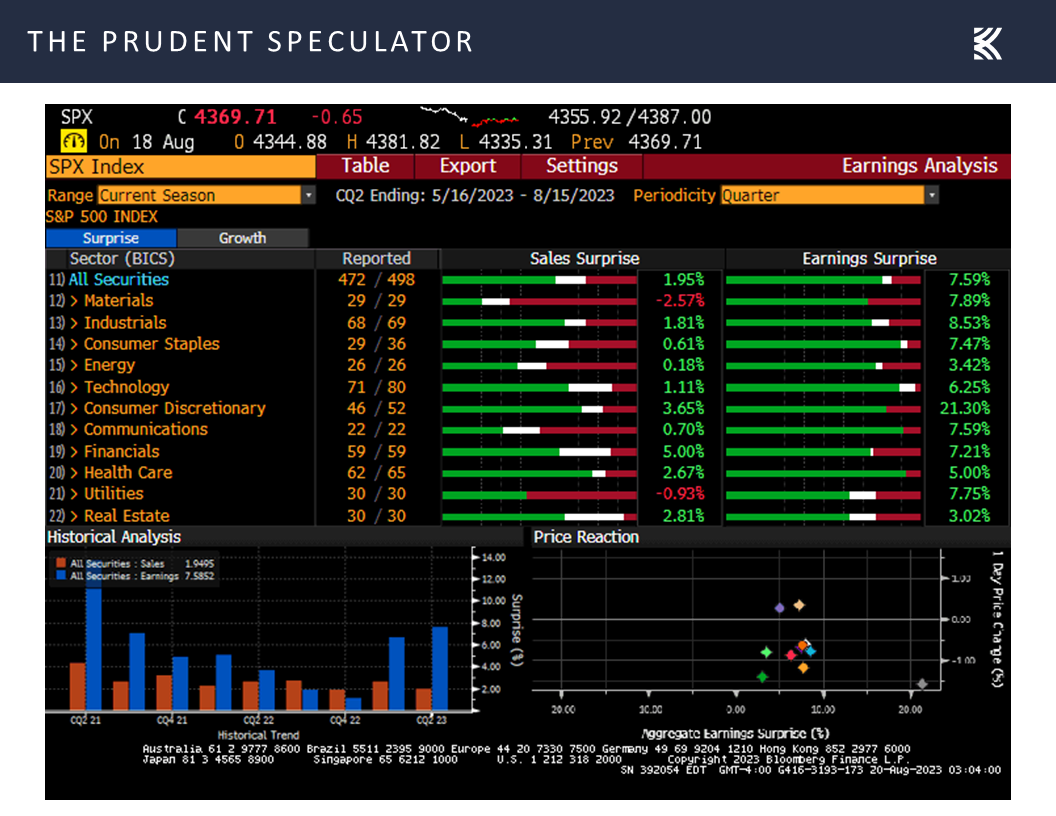

especially as Q2 earnings reporting season continued the trend of results trumping subdued expectations. In fact, 80.0% of S&P 500 constituents topped second quarter EPS projections, a much better “beat” rate than is usually the case.

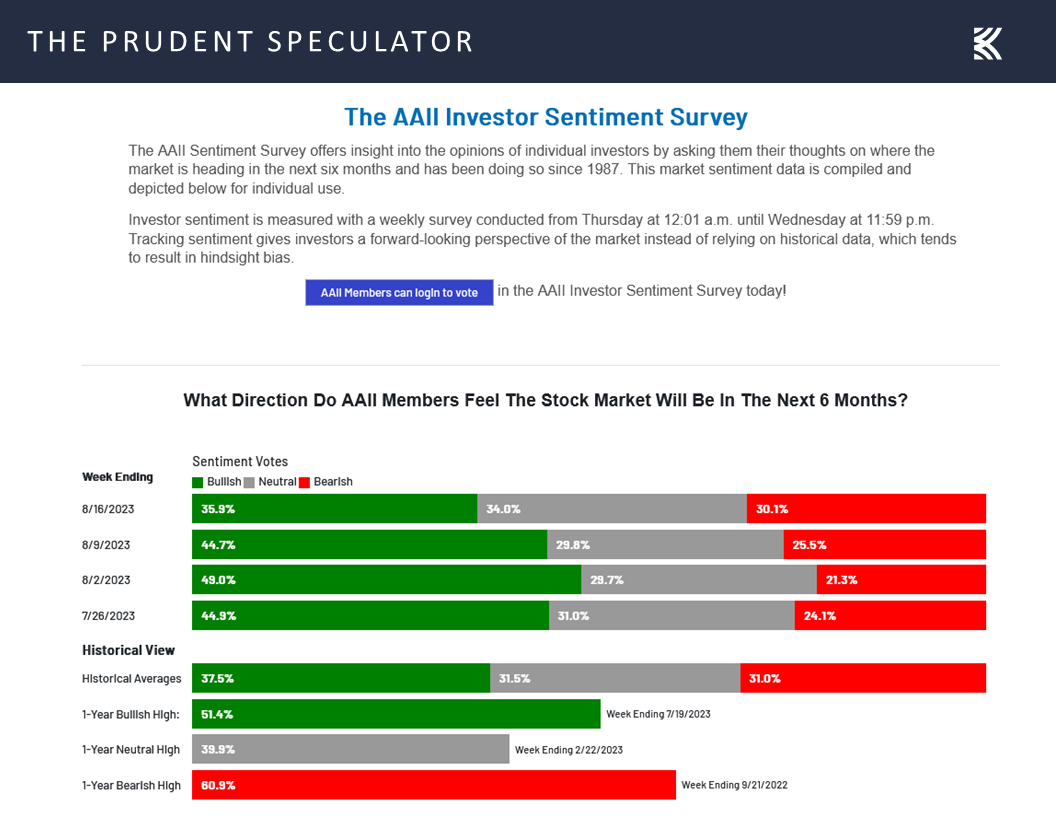

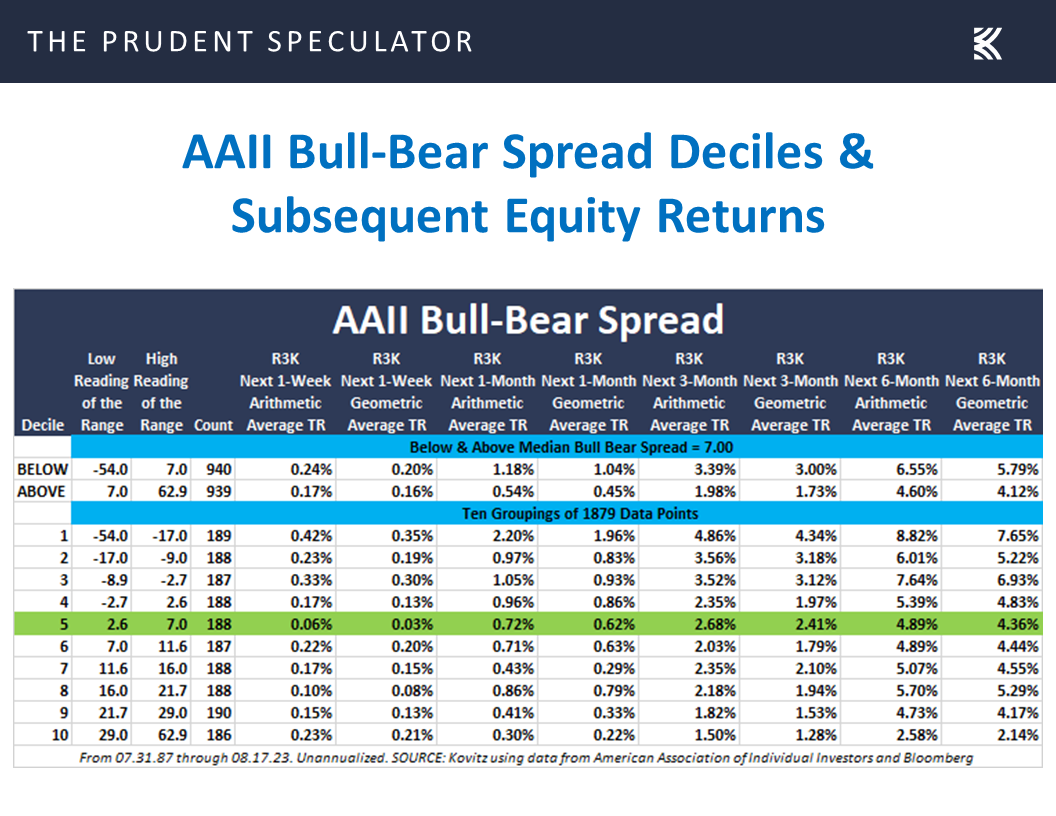

Contrarian Sentiment – AAII Becomes Much Less Bullish

We’ll close this missive by again offering the reminder that the only problem with market timing is getting the timing right. Indeed, the number of Bulls in the latest American Association of Individual Investors (AAII) sentiment survey dropped to 35.9% a figure below the long-term average, yet it was just two weeks ago that Bulls dwarfed Bears by more than a two-to-one margin.

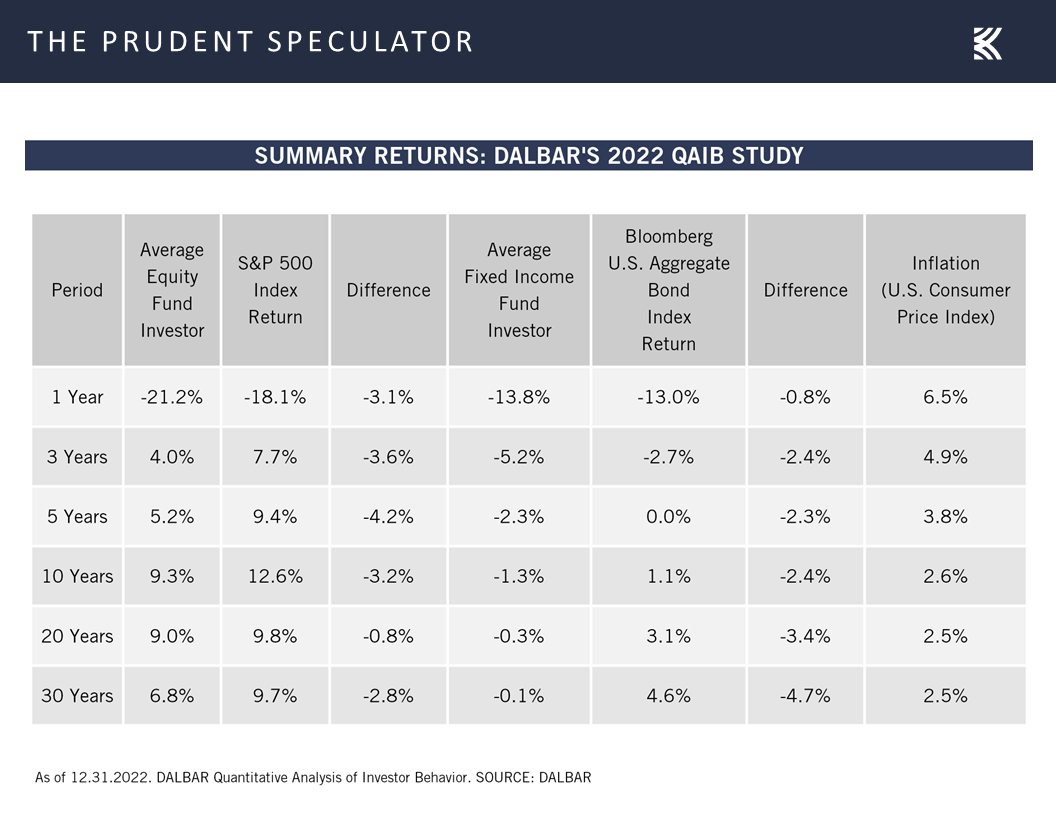

Sadly, such behavior of liking stocks more at higher prices and less at lower prices has been going on for decades, with equity fund investors, per data provider DALBAR, proving to be awful in their timing decisions.

Warren Buffett states, “Be greedy when others are fearful, and fearful when others are greedy,” but the evidence we have compiled on the AAII Bull-Bear Spread suggests that the first half of his statement is the most valuable, so we can’t say we are unhappy to see the latest increase in pessimism on Main Street.

Stock News – Updates on nine stocks across five different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Contrarian Sentiment, Interest Rates, Valuations and more Economic News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss contrarian sentiments, interest rates, valuations and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week In Review – Sizable Setback; August a Tough Month, on Average, Since 1986

Patience – Lots to Worry About Along the Way, But Over Time Equities Have Proved Rewarding

Partnering With Great Corporations – Companies Become More Valuable as Economy, Profits and Dividends Grow Over Time

Econ News – Generally Favorable Numbers; Q3 GDP Outlook Improves

Interest Rates – History Lesson on Rising Rates and Equity Returns

Valuations – Inexpensive Multiples for our Stocks

Contrarian Sentiment – AAII Becomes Much Less Bullish

Stock News – Updates on nine stocks across four different sectors

Week In Review – Sizable Setback; August a Tough Month, on Average, Since 1986

It was a lousy week for equities, with the major market averages pulling back 2% or more and the Russell 3000 Value index (R3KV) turning in the 142nd worst week in its 28-year history, skidding 2.52% on a price basis. Obviously, we never want to downplay moves to the downside, but weekly losses with the magnitude of last week’s or even greater have occurred five times per year on average. Happily, gains of comparable or larger scale have taken place with greater frequency, so much so that Value stocks have managed to post terrific returns of 13.6% per annum dating back to the inception of The Prudent Speculator in March 1977.

Patience – Lots to Worry About Along the Way, But Over Time Equities Have Proved Rewarding

Interestingly, though August has been a fine performer, on average, for Value Stocks and Dividend Payers going all the way back to 1927,

the month has been in the red, again on average, for both since your Editor came to learn at the foot of the great Al Frank in early-1987.

Partnering With Great Corporations – Companies Become More Valuable as Economy, Profits and Dividends Grow Over Time

While volatility is hardly unusual, many will point to the downgrade of the U.S. credit rating by Fitch Ratings on August 1 as the catalyst for the current decline, even as JPMorgan Chase (JPM – $148.97) CEO Jamie Dimon was quick to dismiss the move, saying that it doesn’t really matter that much.

Those comments echoed his response to a similar downgrade from Standard & Poor’s on August 5, 2011. Back then, Mr. Dimon argued that decision wasn’t that material, even as the R3KV index plunged 7.4% in the wake of the S&P downgrade. Of course, that dip is hardly visible on the chart below.

The R3KV is off 4.2% this time around and we note that the S&P-Downgrade losses in 2011 were recouped less than a month later, with the incident not even showing any red ink when measured with a three-month-or-longer ruler. History is merely a guide and not the gospel, but equities have been overcoming disconcerting events since the dawn of stock trading.

To be sure, anything can happen in the near-term, but Al Frank taught us, “We think of ourselves as partners in great corporations, growing in wealth as they prevail, rather than traders of pieces of paper.” Given that the economy grows over time,

as do corporate profits,

and dividend payouts,

it shouldn’t be a grand surprise that stocks have turned in far more good years than bad,

and that substantial wealth has accrued to those who remember that time in the market trumps market timing.

Econ News – Generally Favorable Numbers; Q3 GDP Outlook Improves

And speaking of the economy, the numbers out last week generally were favorable, as retail sales rose 0.7% in July, the largest increase in six months and better than expectations,

while first-time filings for unemployment benefits dipped to a historically very low 239,000, down from 250,000 the week prior, confirming the exceptional strength of the labor market.

To be sure, there were mixed numbers on the health of the manufacturing sector on the East Coast, with the Empire State PMI trailing estimates by a wide margin, but the Philadelphia Fed PMI came in well above forecasts.

The important forward-looking Leading Economic Indicators (LEI) for July turned out to be in line with projections, but the -0.4% reading was an improvement from the -0.7% figure posted in June. And perhaps more interesting, the Conference Board, the keeper of the LEI gauge, tempered its economic contraction call to a “short and shallow recession in the Q4 2023 to Q1 2024 timespan,” from the color offered the month prior. Last month, the Conference Board argued, “We forecast that the U.S. economy is likely to be in recession from Q3 2023 to Q1 2024. Elevated prices, tighter monetary policy, harder-to-get credit, and reduced government spending are poised to dampen economic growth further.”

Still, a pessimistic view on the prospects for economic growth seemingly remains the consensus call,

even as the latest estimate for Q3 real (inflation-adjusted) U.S. GDP growth jumped to a whopping 5.8% last week, per calculations from the Atlanta Fed.

Is it any wonder that John Kenneth Galbraith stated, “The only function of economic forecasting is to make astrology look respectable?”

Interest Rates – History Lesson on Rising Rates and Equity Returns

Clearly, the economy faces headwinds as mortgage rates are now at their highest level in more than two decades, but borrowing costs for home buyers are still below the historic average dating back to 1970,

and homebuilder confidence has held up better than many might have expected, with housing starts ticking up in July.

Interestingly, the worry for some market participants is that the economy might be too strong for the Federal Reserve’s taste, as expectations for cuts in the Federal Funds rate next year were reined in a bit last week,…

and the yield on the benchmark 10-Year U.S. Treasury closed Friday at 4.25%, after hitting 4.32% on Thursday, the latter tally the highest since 2007.

Not surprisingly, the rise in interest rates and the dip in stocks brought out the usual talking heads offering statements like, “When investors start demanding higher yields on longer-term bonds to compensate for the risk of inflation, that is correlated with lower risk-asset prices.” Such a view sounds logical in theory, but in practice, one doesn’t have to look too hard to find evidence to the contrary.

After all, the yield on the 10-Year was 3.88% at the start of 2023, yet stocks have enjoyed a solid year thus far, though we should add that the current level of 4.25% is still well below the long-term average of 5.84%.

Believe it or not, and further debunking the “rising-rates-lead-to-lower-stock-prices” assertion, history shows that Value Stocks and Dividend Payers have each done better, on average, when the yield on the 10-Year Treasury is above the long-term median than when it is below. True, equities arguably prefer to see rates falling, in terms of the concurrent and subsequent performance shown above, but the data is overwhelming, on average, that those with a long-term (or even intermediate-term) time horizon should not fret about a rising 10-Year Treasury yield.

That does not mean that stocks won’t move south in the near-term, but we like the historical odds that the longer one holds Value Stocks and Dividend Payers, the greater the chance of better returns than what a 10-Year Treasury buyer will receive today.

Valuations – Inexpensive Multiples for our Stocks

As always, we remain braced for additional downside market activity, but we continue to think that stocks in general are reasonably priced,

and that our broadly diversified portfolios of what we believe to be undervalued stocks are inexpensively priced,

especially as Q2 earnings reporting season continued the trend of results trumping subdued expectations. In fact, 80.0% of S&P 500 constituents topped second quarter EPS projections, a much better “beat” rate than is usually the case.

Contrarian Sentiment – AAII Becomes Much Less Bullish

We’ll close this missive by again offering the reminder that the only problem with market timing is getting the timing right. Indeed, the number of Bulls in the latest American Association of Individual Investors (AAII) sentiment survey dropped to 35.9% a figure below the long-term average, yet it was just two weeks ago that Bulls dwarfed Bears by more than a two-to-one margin.

Sadly, such behavior of liking stocks more at higher prices and less at lower prices has been going on for decades, with equity fund investors, per data provider DALBAR, proving to be awful in their timing decisions.

Warren Buffett states, “Be greedy when others are fearful, and fearful when others are greedy,” but the evidence we have compiled on the AAII Bull-Bear Spread suggests that the first half of his statement is the most valuable, so we can’t say we are unhappy to see the latest increase in pessimism on Main Street.

Stock News – Updates on nine stocks across five different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.