The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Corporate Profits, Interest Rates, Rally Extends and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

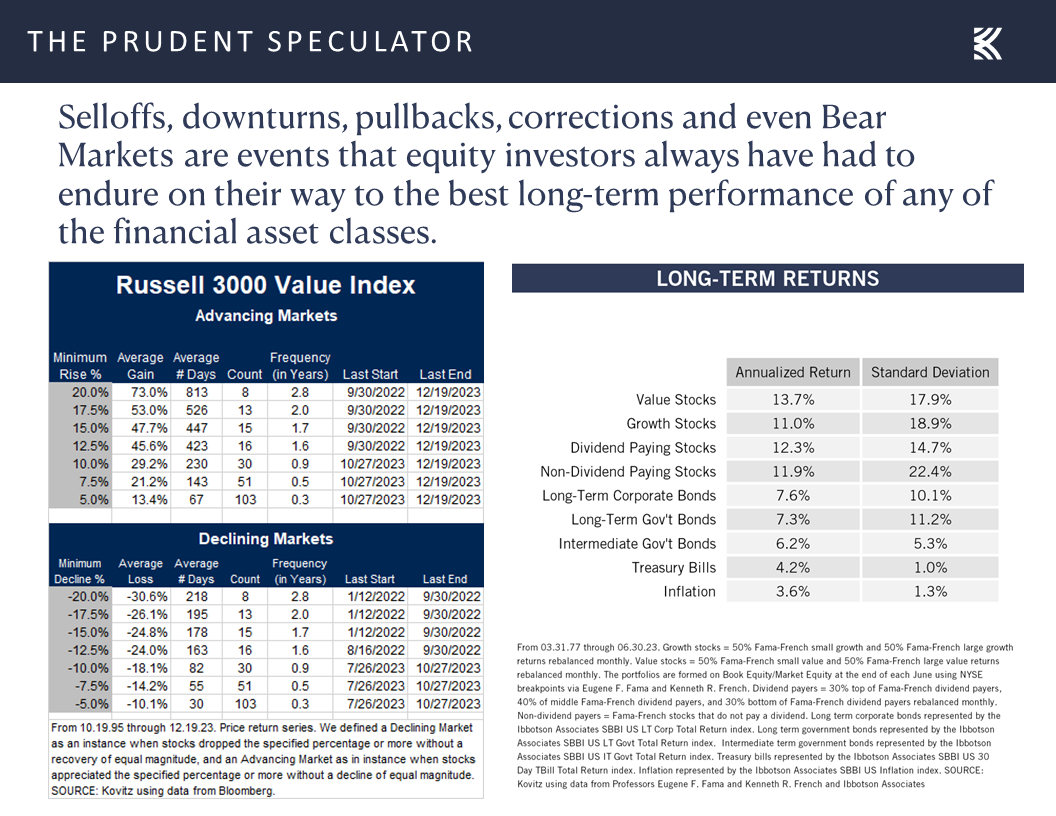

Rally Extends – Big Drop on Wednesday, But Weekly Gain

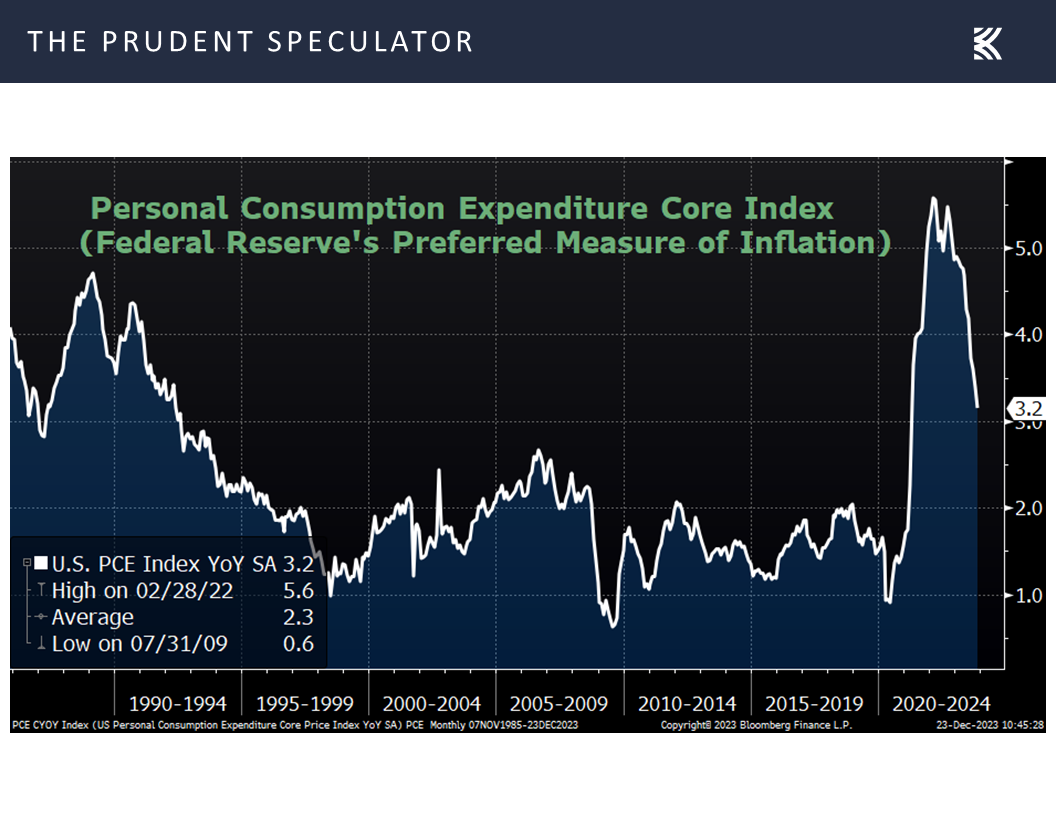

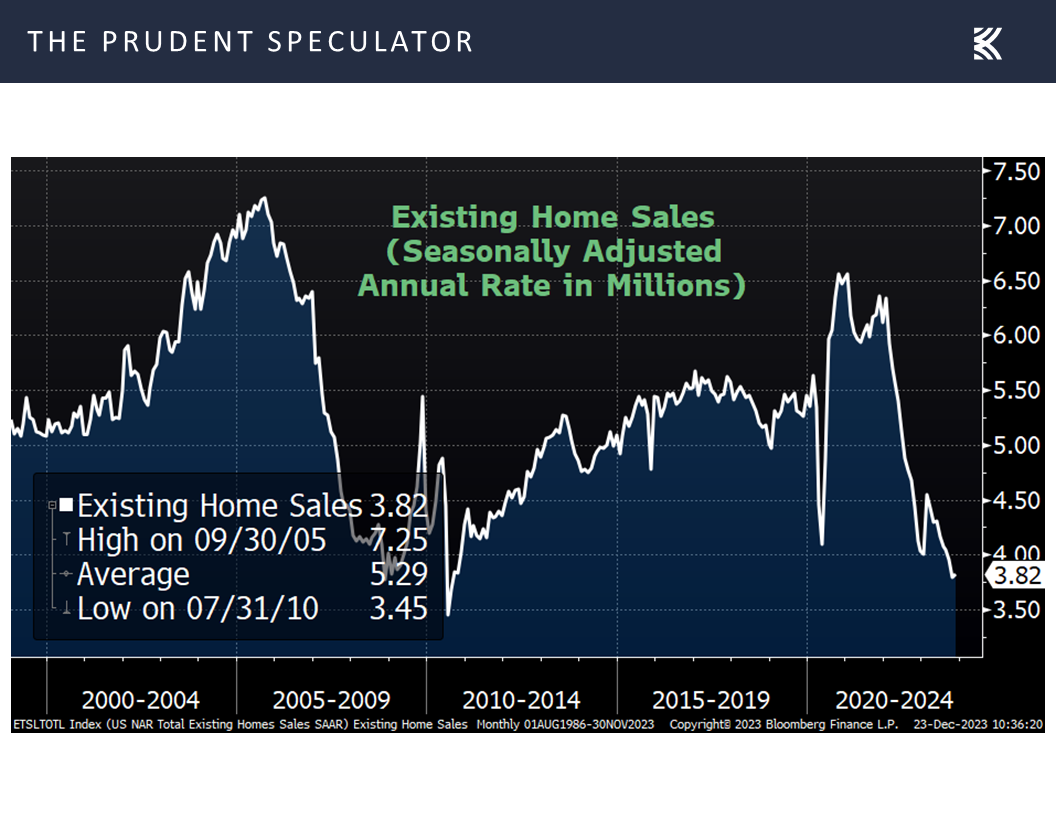

Econ News – Inflation Declines; Housing and Consumer Confidence Better Than Expected

Corporate Profits – EPS Expected to Grow in ’24

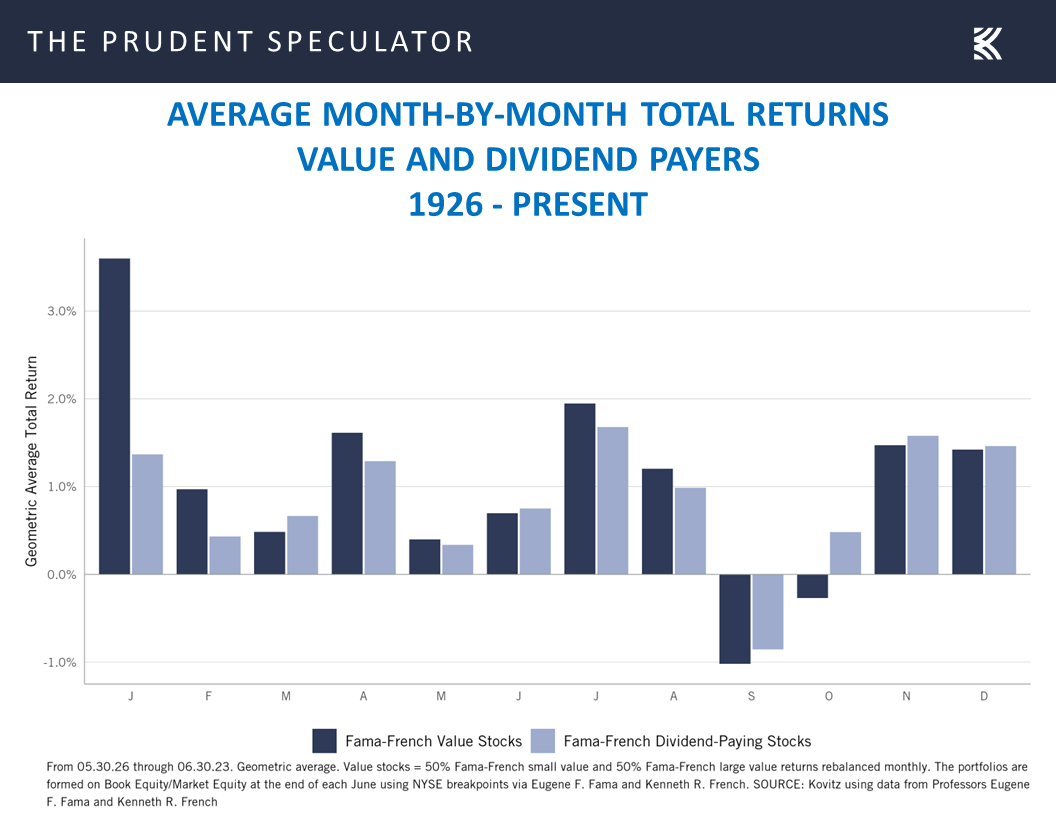

Interest Rates – Supportive of Equities; Especially Value

Sentiment – AAII Bulls Running High

Stock News – Updates on eight stocks across six sectors

Rally Extends – Big Drop on Wednesday, But Weekly Gain

While Wednesday’s big 470+ point plunge in the Dow Jones Industrial Average and 1.69% skid in the Russell 3000 Value index provided a vivid reminder that downside volatility is always something investors must put up with along the way toward achieving handsome long-term returns,

the major market averages for the full week managed to gain ground, continuing the sizable advance since the October 27 lows, with the seasonally favorable November – April time span continuing its torrid start.

Econ News – Inflation Declines; Housing and Consumer Confidence Better Than Expected

The data out last week did nothing to dispel the notion that inflation is coming down as the Federal Reserve’s preferred gauge, the Core Personal Consumption Expenditure Index, rose just 0.1% in November and 3.2% on a year-over-year basis.

Further, the numbers continued to show that the U.S. economy is holding up well, with better-than-expected news on existing home sales,

and groundbreaking for new homes.

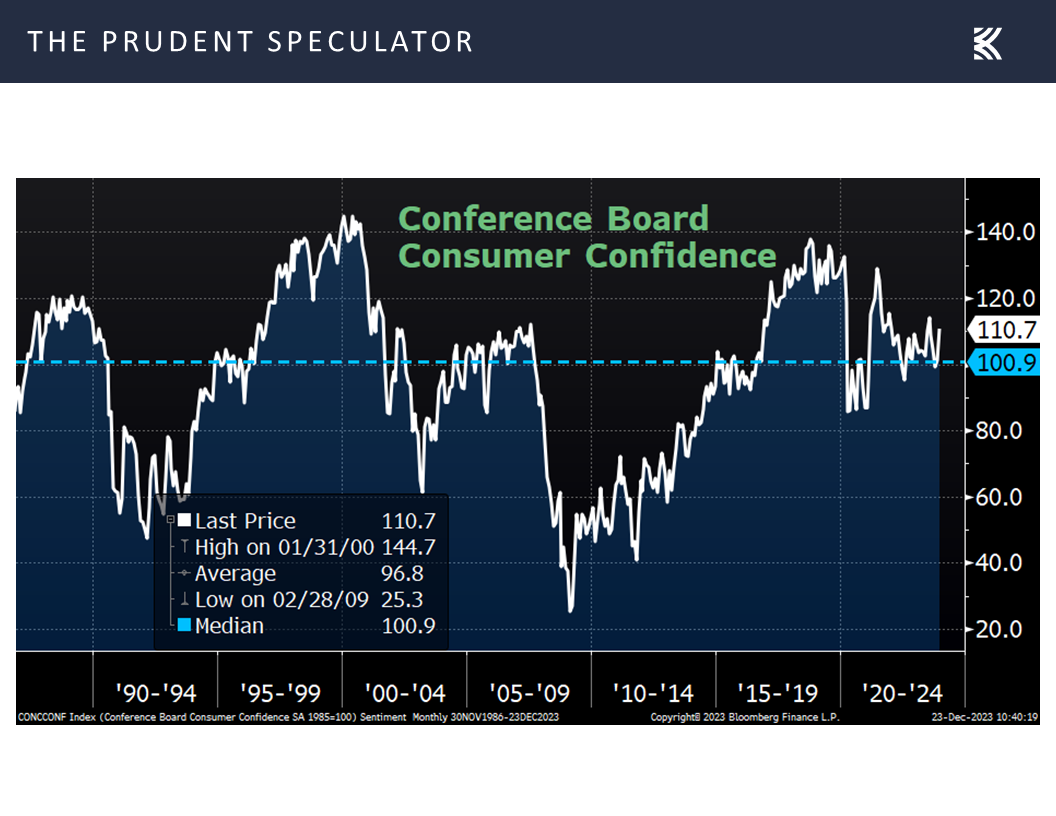

Consumer Confidence, per the Conference Board, also topped forecasts,

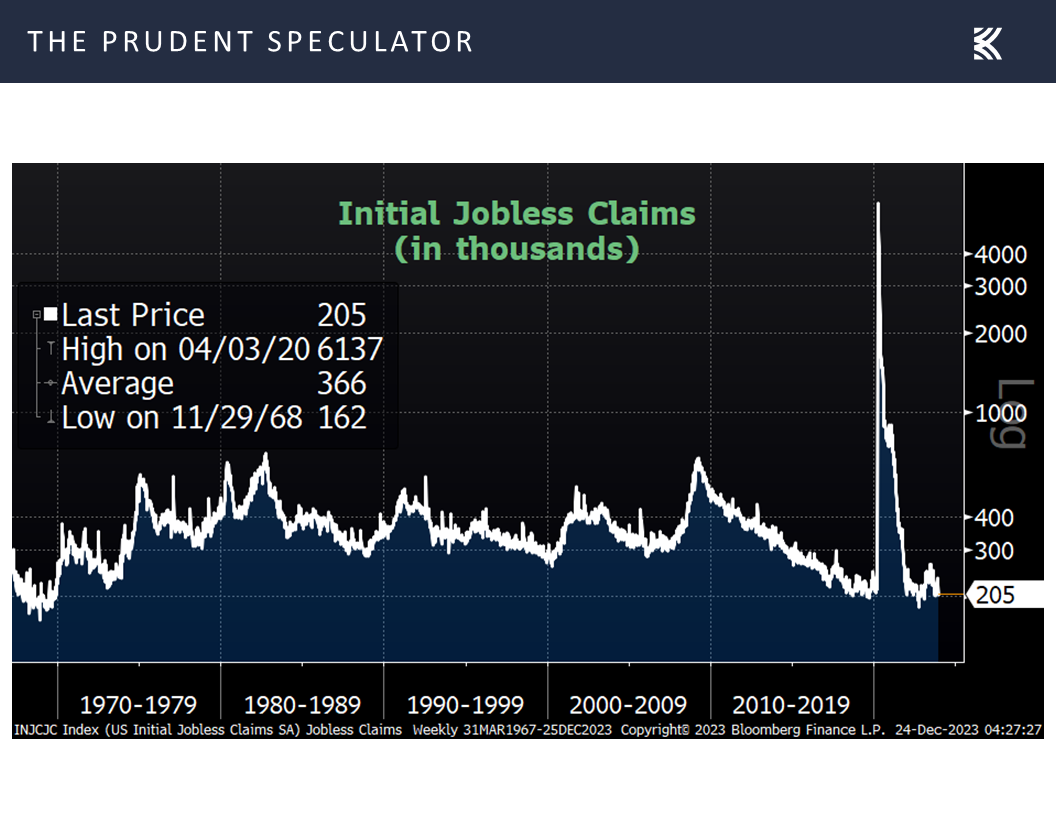

and first-time filings for unemployment benefits remained near multi-generational lows.

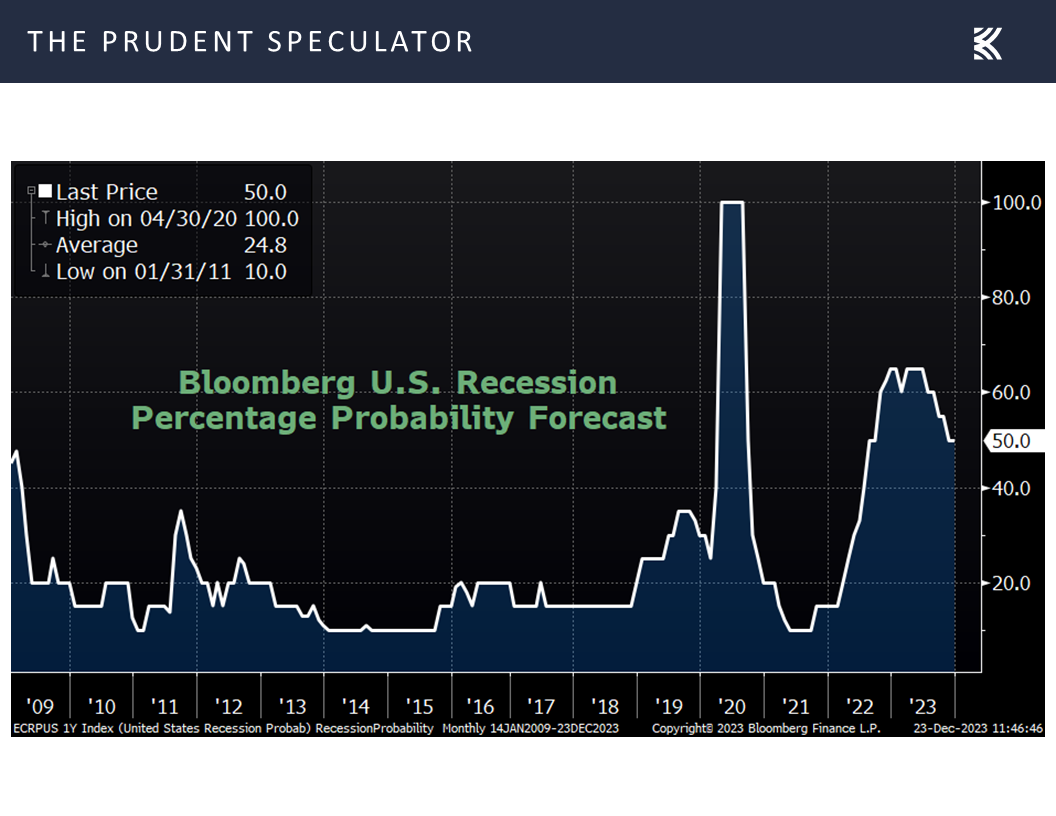

True, the odds of recession in the next 12 months, as calculated by Bloomberg, continue to reside at 50%,

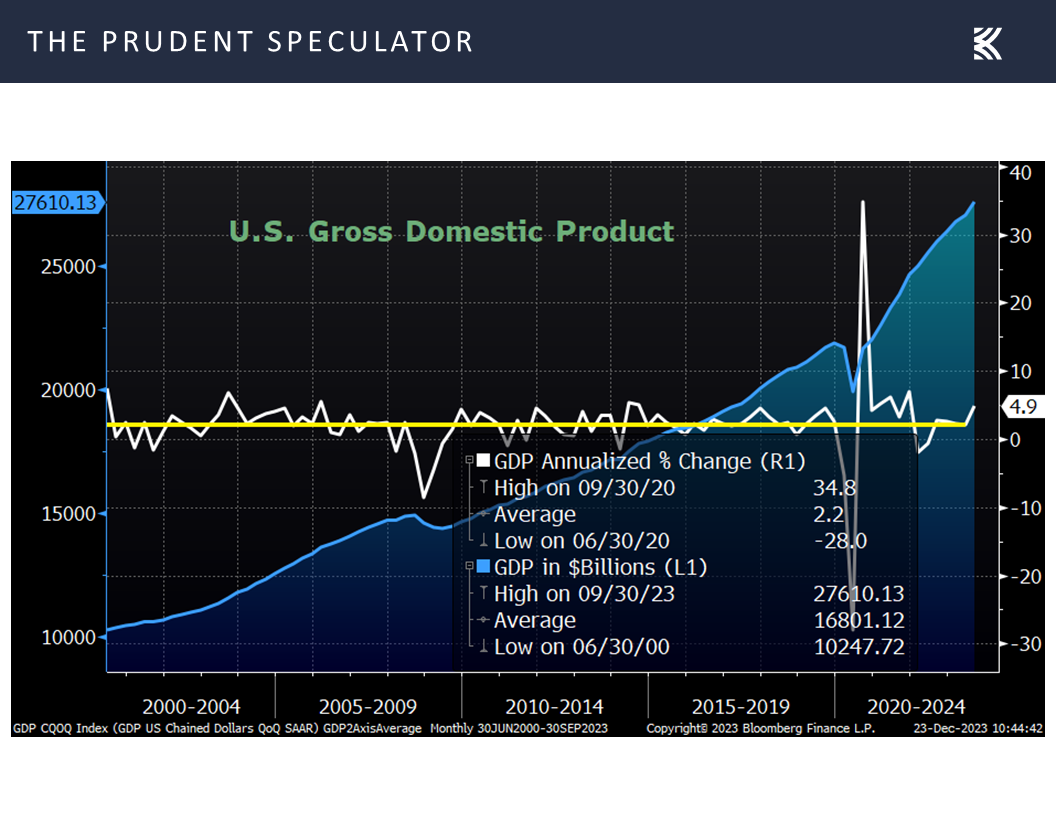

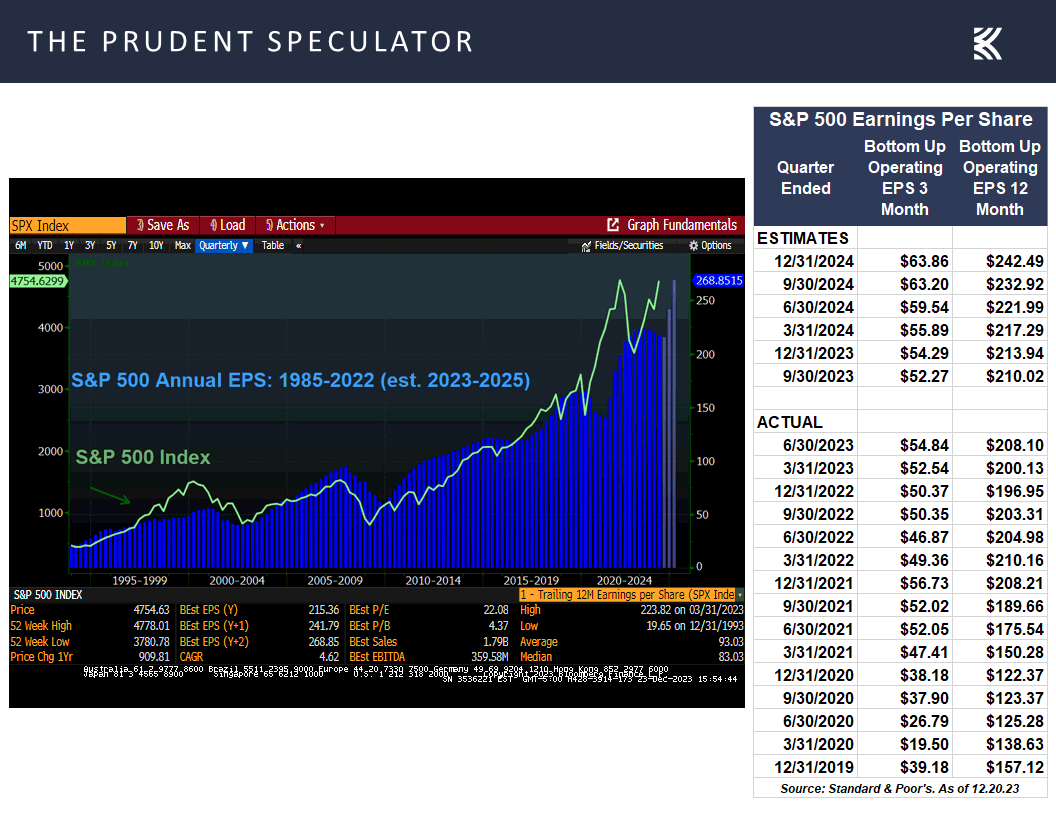

but Q3 real (inflation-adjusted) GDP jumped 4.9%,

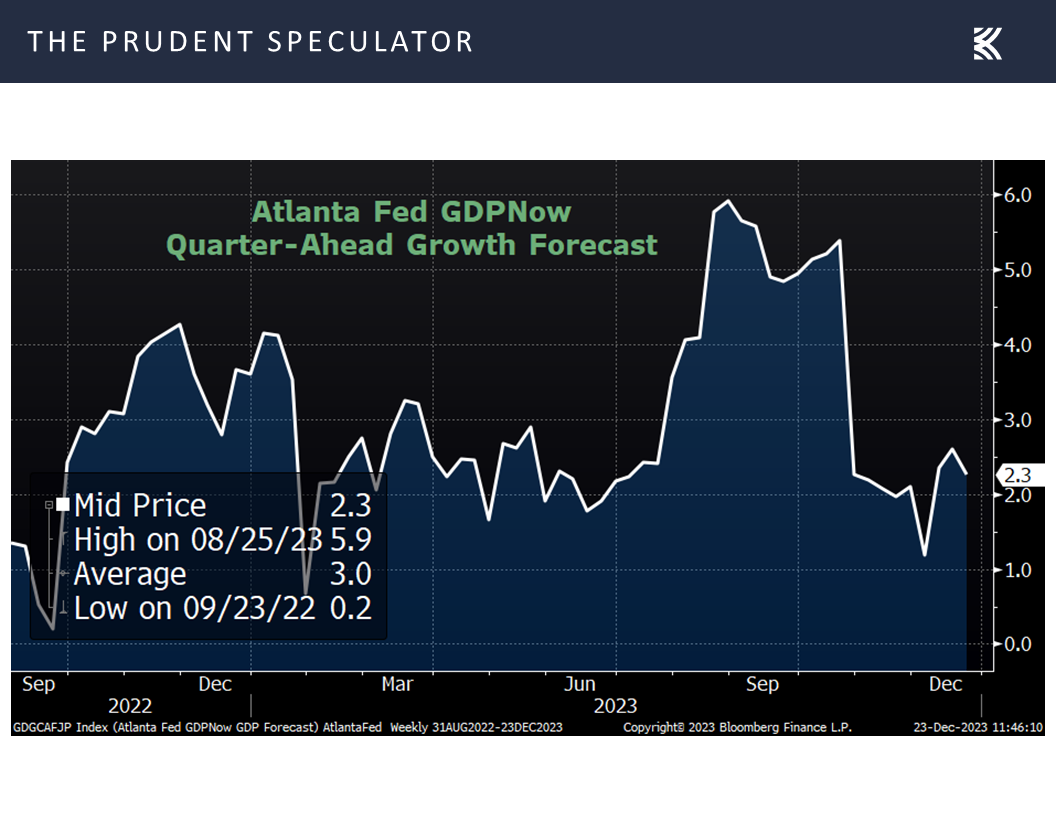

and the latest projection for Q4 real GDP growth from the Atlanta Fed stood at a solid 2.3%

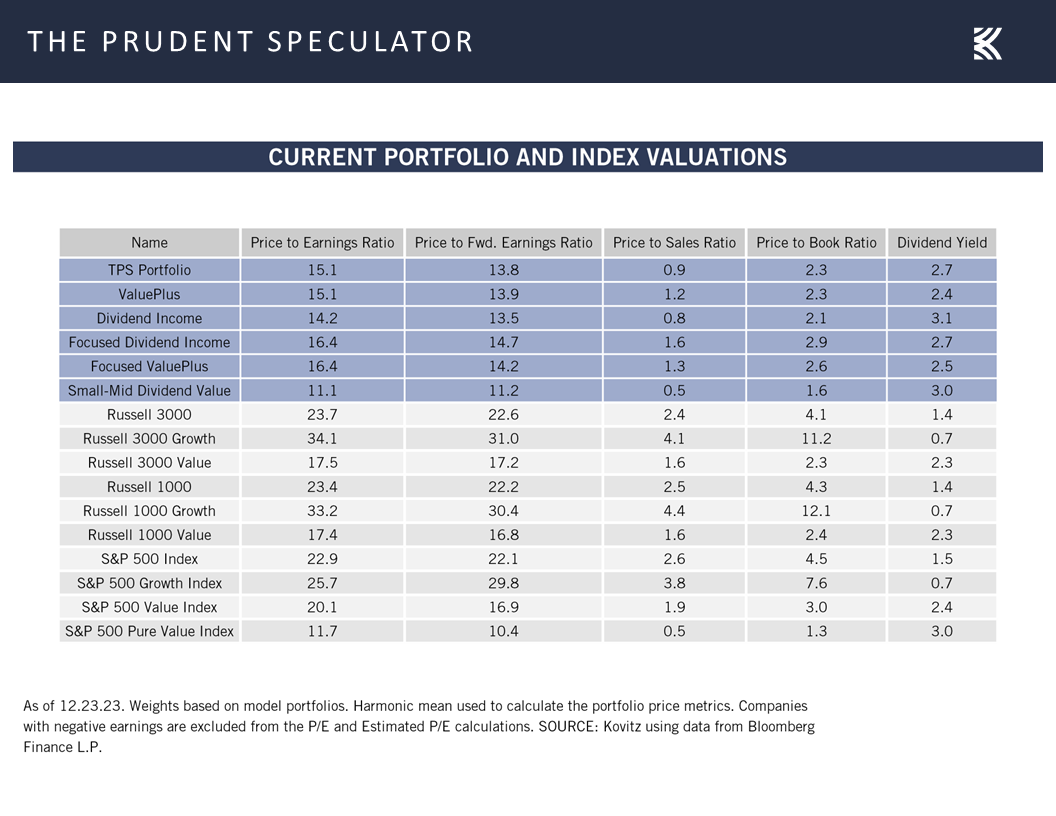

Corporate Profits – EPS Expected to Grow in ’24

which supports a favorable outlook for the health of corporate profits.

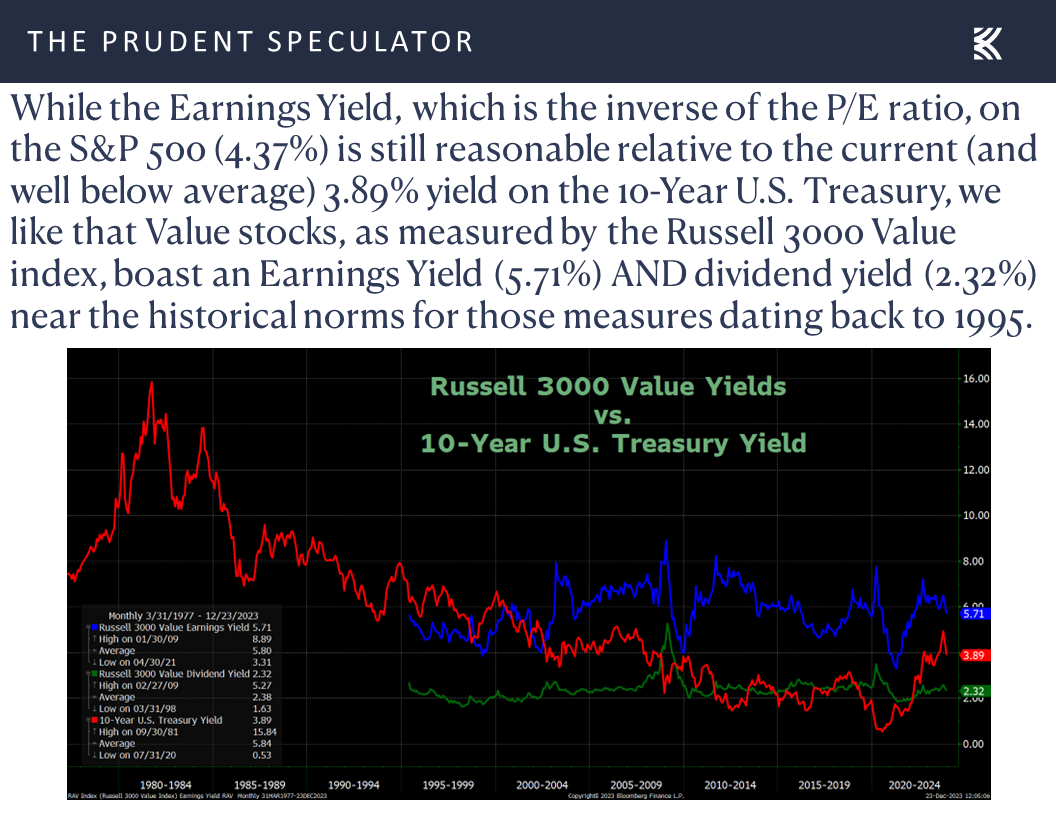

Interest Rates – Supportive of Equities; Especially Value

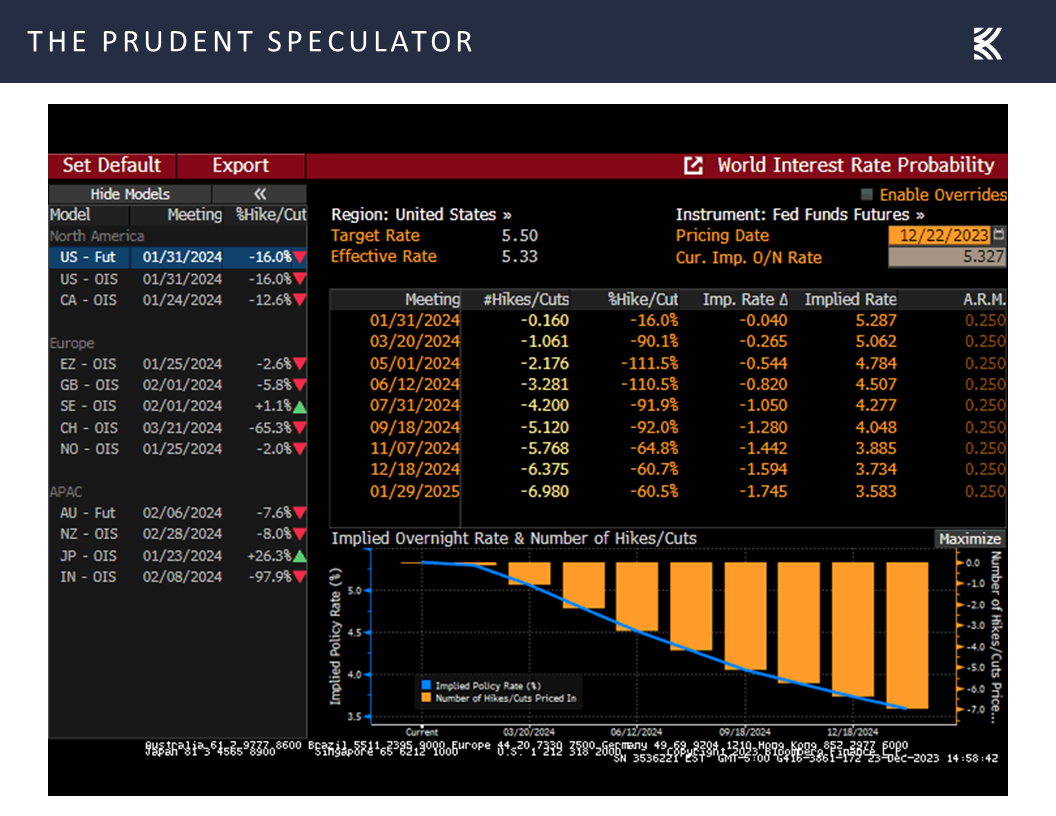

Bets are increasing that the Federal Reserve will engage in a series of interest rate cuts in 2024,

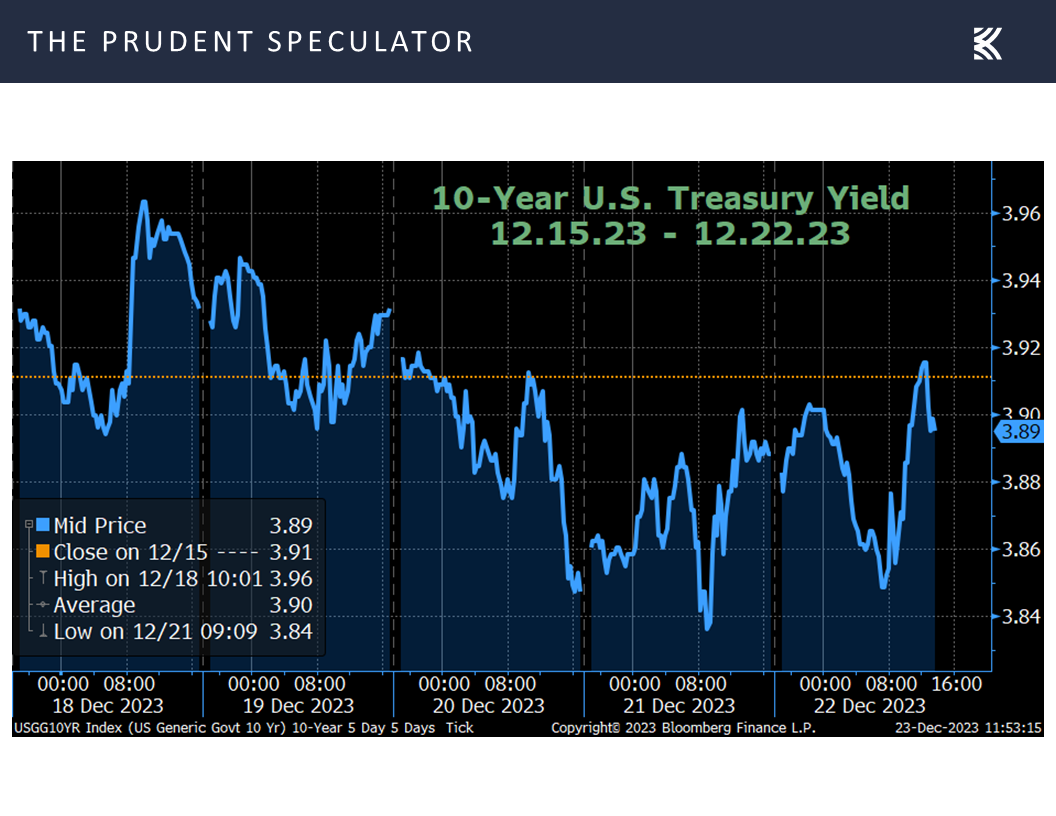

and the yield on the 10-Year U.S. Treasury edged lower last week,

with the drop in the risk-free rate over the last few months adding to the valuation appeal of equites in general,

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular.

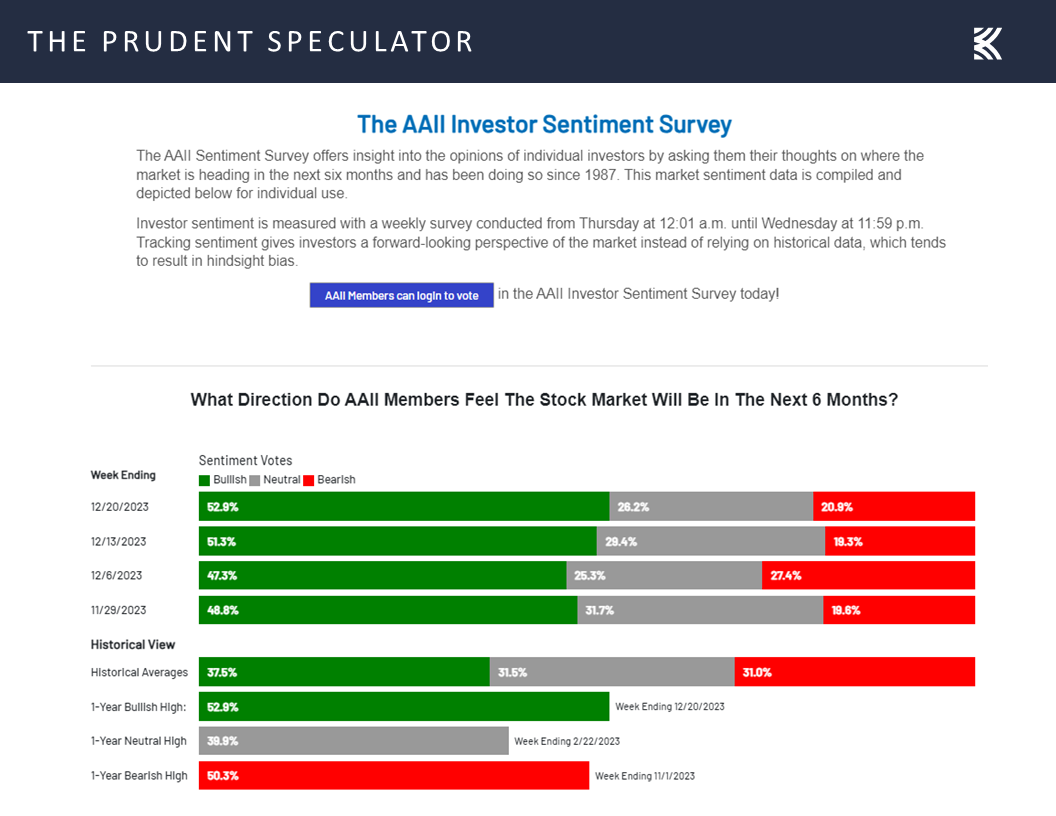

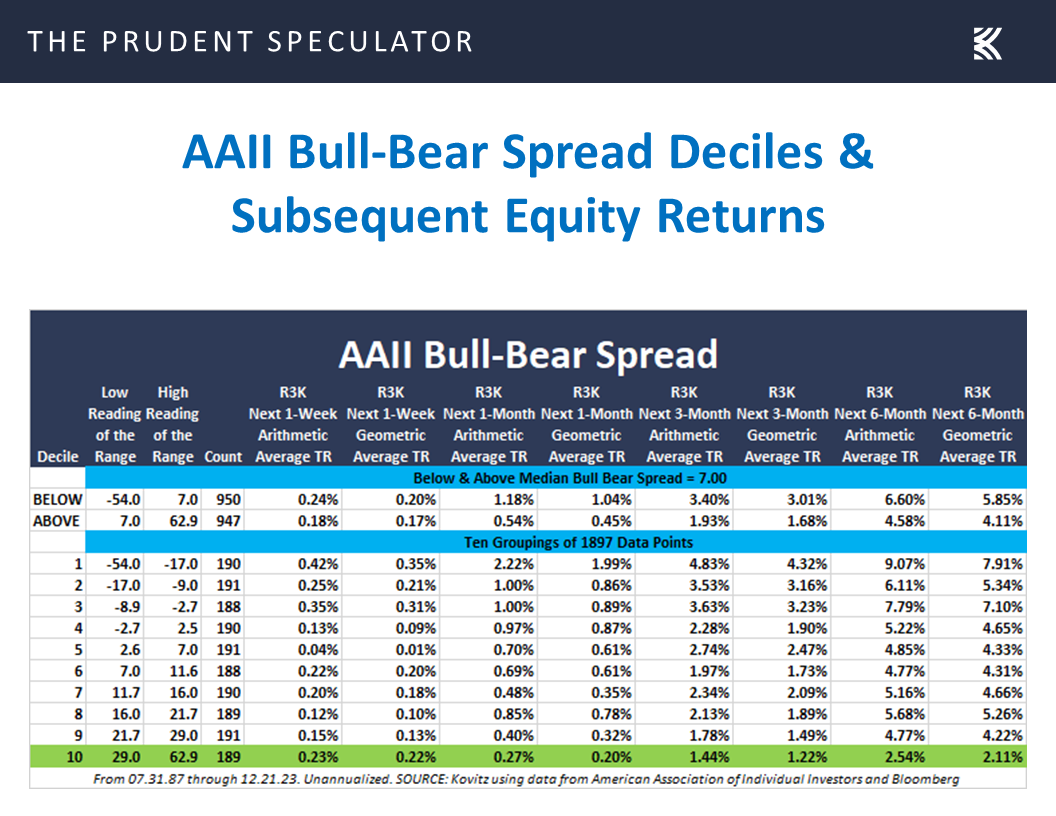

Sentiment – AAII Bulls Running High

Of course, we realize that there is plenty of Wall Street optimism on Main Street as the latest Sentiment Survey from the American Association of Individual Investors (AAII) continued to show a wealth of Bulls and a dearth of Bears.

Nevertheless, the historical evidence argues for sticking with stocks even if folks are enthused about them,

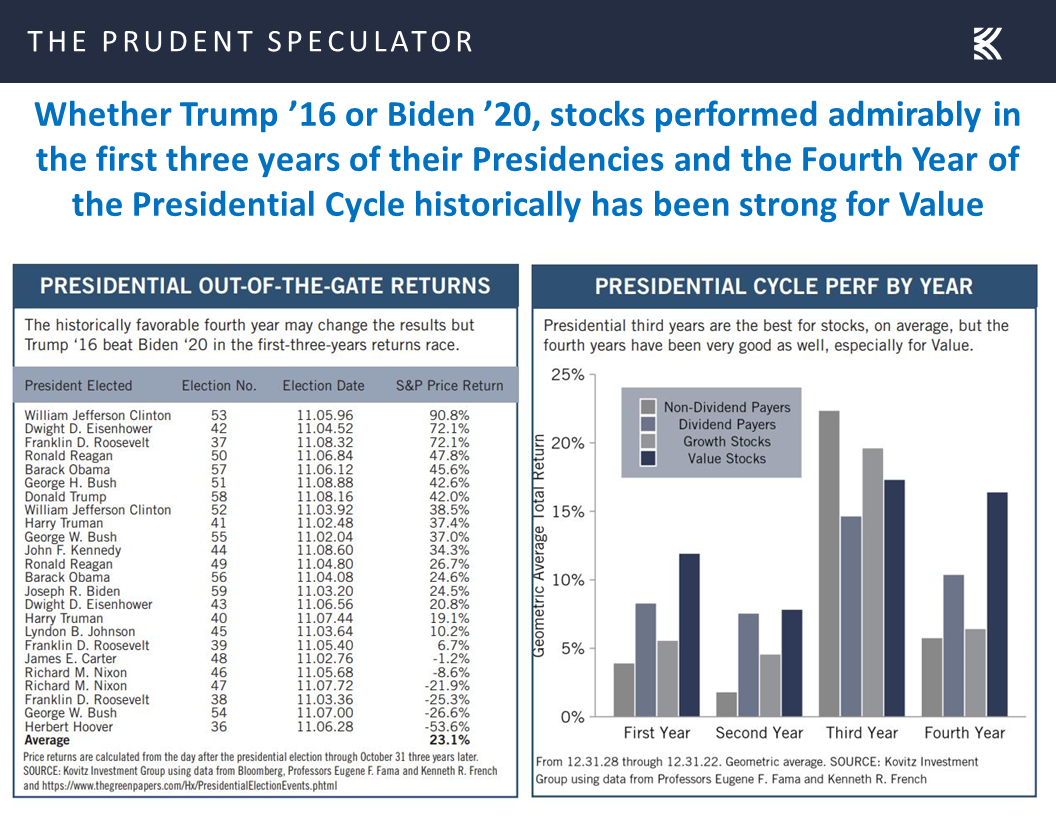

while we like that the calendar is about to turn to the historically positive fourth year of the Presidential Cycle.

Stock News – Updates on eight stocks across six different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Corporate Profits, Interest Rates, Rally Extends and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Corporate Profits, Interest Rates, Rally Extends and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Rally Extends – Big Drop on Wednesday, But Weekly Gain

Econ News – Inflation Declines; Housing and Consumer Confidence Better Than Expected

Corporate Profits – EPS Expected to Grow in ’24

Interest Rates – Supportive of Equities; Especially Value

Sentiment – AAII Bulls Running High

Stock News – Updates on eight stocks across six sectors

Rally Extends – Big Drop on Wednesday, But Weekly Gain

While Wednesday’s big 470+ point plunge in the Dow Jones Industrial Average and 1.69% skid in the Russell 3000 Value index provided a vivid reminder that downside volatility is always something investors must put up with along the way toward achieving handsome long-term returns,

the major market averages for the full week managed to gain ground, continuing the sizable advance since the October 27 lows, with the seasonally favorable November – April time span continuing its torrid start.

Econ News – Inflation Declines; Housing and Consumer Confidence Better Than Expected

The data out last week did nothing to dispel the notion that inflation is coming down as the Federal Reserve’s preferred gauge, the Core Personal Consumption Expenditure Index, rose just 0.1% in November and 3.2% on a year-over-year basis.

Further, the numbers continued to show that the U.S. economy is holding up well, with better-than-expected news on existing home sales,

and groundbreaking for new homes.

Consumer Confidence, per the Conference Board, also topped forecasts,

and first-time filings for unemployment benefits remained near multi-generational lows.

True, the odds of recession in the next 12 months, as calculated by Bloomberg, continue to reside at 50%,

but Q3 real (inflation-adjusted) GDP jumped 4.9%,

and the latest projection for Q4 real GDP growth from the Atlanta Fed stood at a solid 2.3%

Corporate Profits – EPS Expected to Grow in ’24

which supports a favorable outlook for the health of corporate profits.

Interest Rates – Supportive of Equities; Especially Value

Bets are increasing that the Federal Reserve will engage in a series of interest rate cuts in 2024,

and the yield on the 10-Year U.S. Treasury edged lower last week,

with the drop in the risk-free rate over the last few months adding to the valuation appeal of equites in general,

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular.

Sentiment – AAII Bulls Running High

Of course, we realize that there is plenty of Wall Street optimism on Main Street as the latest Sentiment Survey from the American Association of Individual Investors (AAII) continued to show a wealth of Bulls and a dearth of Bears.

Nevertheless, the historical evidence argues for sticking with stocks even if folks are enthused about them,

while we like that the calendar is about to turn to the historically positive fourth year of the Presidential Cycle.

Stock News – Updates on eight stocks across six different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.