The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss econ data, physics, fed minutes and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Thanksgiving – Al Frank Perspective

Physics – Economic Growth, Profit Growth, Dividend Growth Drive Stock Prices

Fed Minutes – Nothing New vs. FOMC Statement and Powell Remarks on Nov. 1

Econ Data – Mixed Bag; Recession Probability Declines; Q4 GDP Growth Estimate Rises

Reasons for Optimism – Valuations & Calendar

Stock News – Updates on six stocks across three different sectors

Thanksgiving – Al Frank Perspective

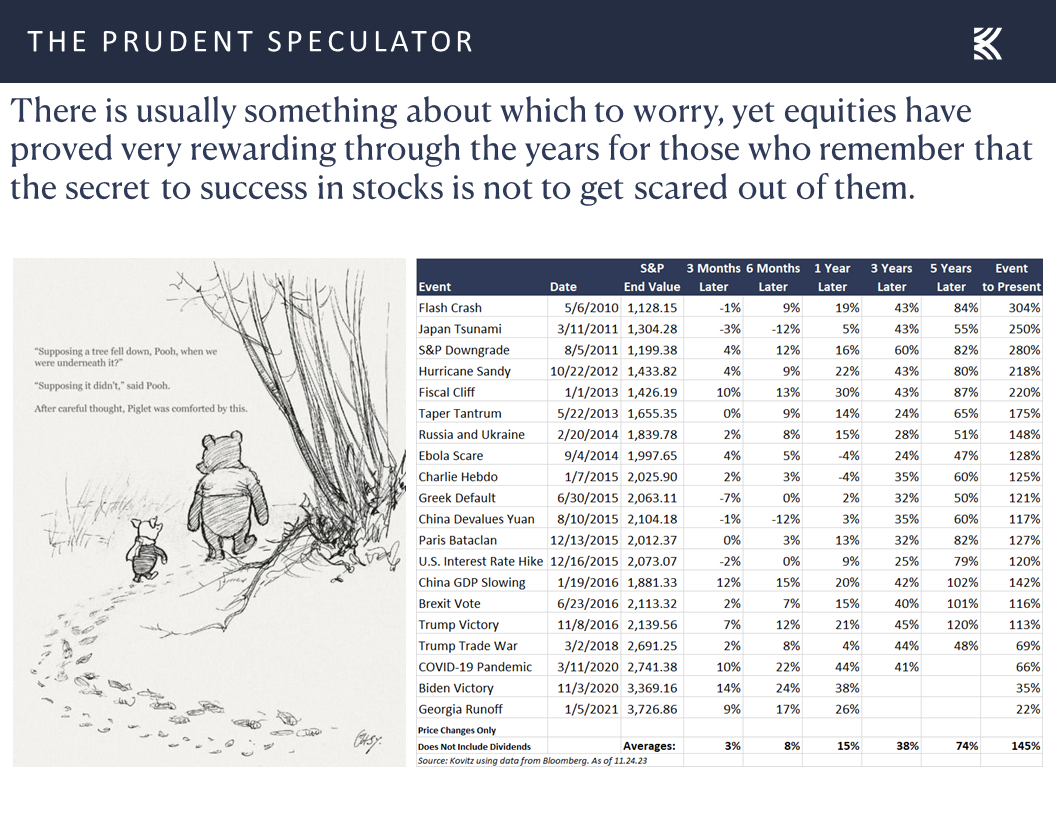

We hope everyone had a wonderful Thanksgiving. There is always much for which to be grateful this time of year, and we like to reflect on words of wisdom from our founder Al Frank:

How relatively well off most of us are and how much we have to be thankful for, not just one day a year but most of the time. Sure, there are pains, traumas, sicknesses—physical, mental and spiritual—unfairnesses and outrages that overwhelm our sense of well being. Still, usually we have a choice of considering life as a tough chore with suffering relief or pleasure, or accepting life as a wonderful gift with marvelous if modest possibilities interspersed with occasional stumbles and hard times.

No doubt, the trials and tribulations of the financial markets pale in comparison to disconcerting global and domestic headlines, but Al passed away more than 21 years ago, yet his words remain very germane for those who choose to invest in stocks. Indeed, despite many bricks in the proverbial Wall of Worry, equities have overcome frightening event after frightening event,

to post terrific long-term returns,

with even those who forget that the only problem with market timing is getting the timing right still having a positive experience, on average.

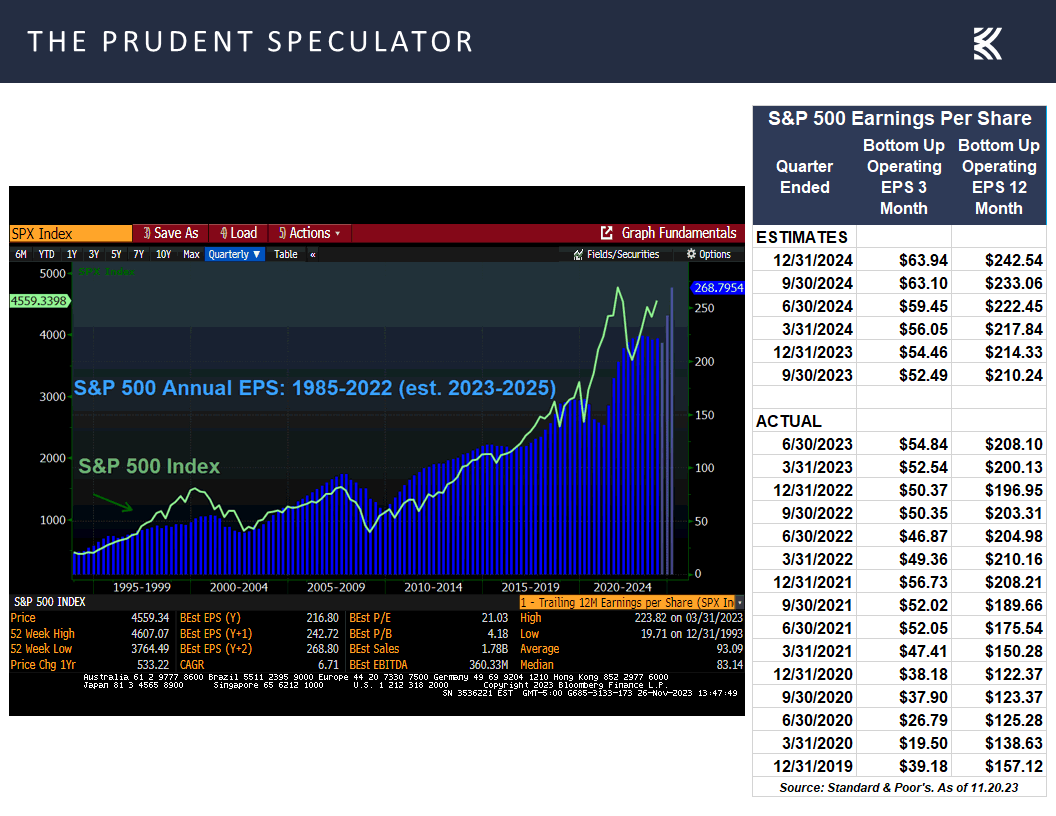

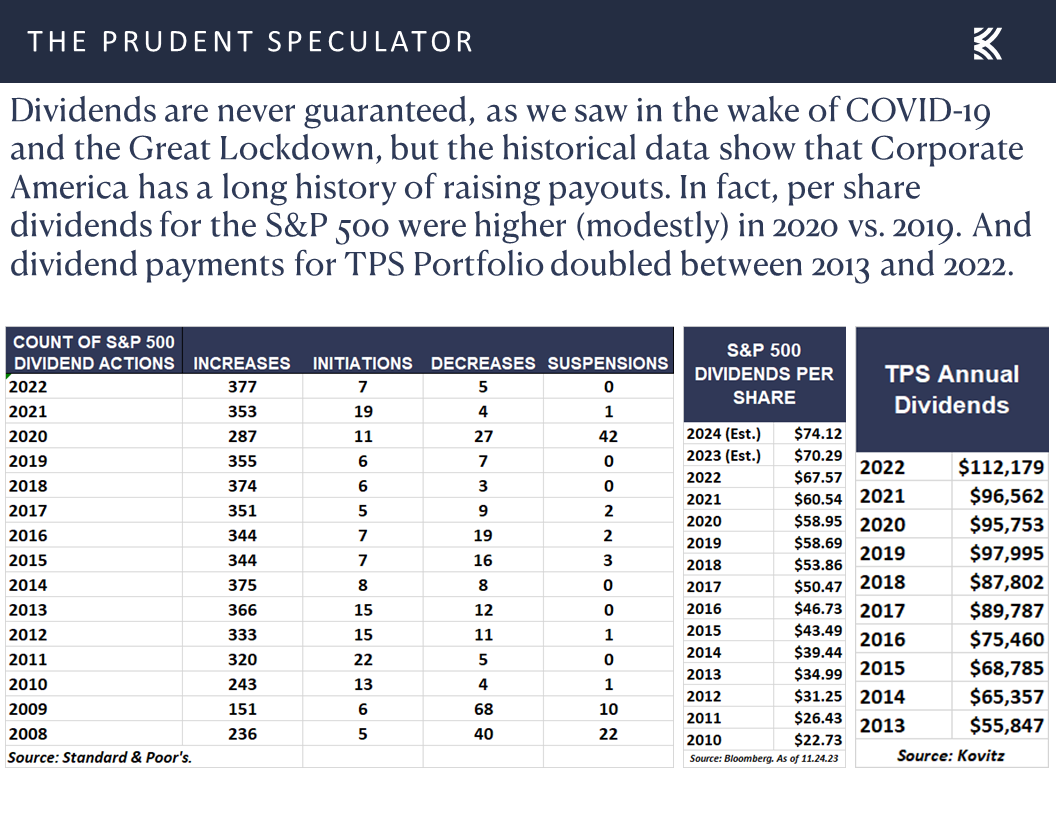

Physics – Economic Growth, Profit Growth, Dividend Growth Drive Stock Prices

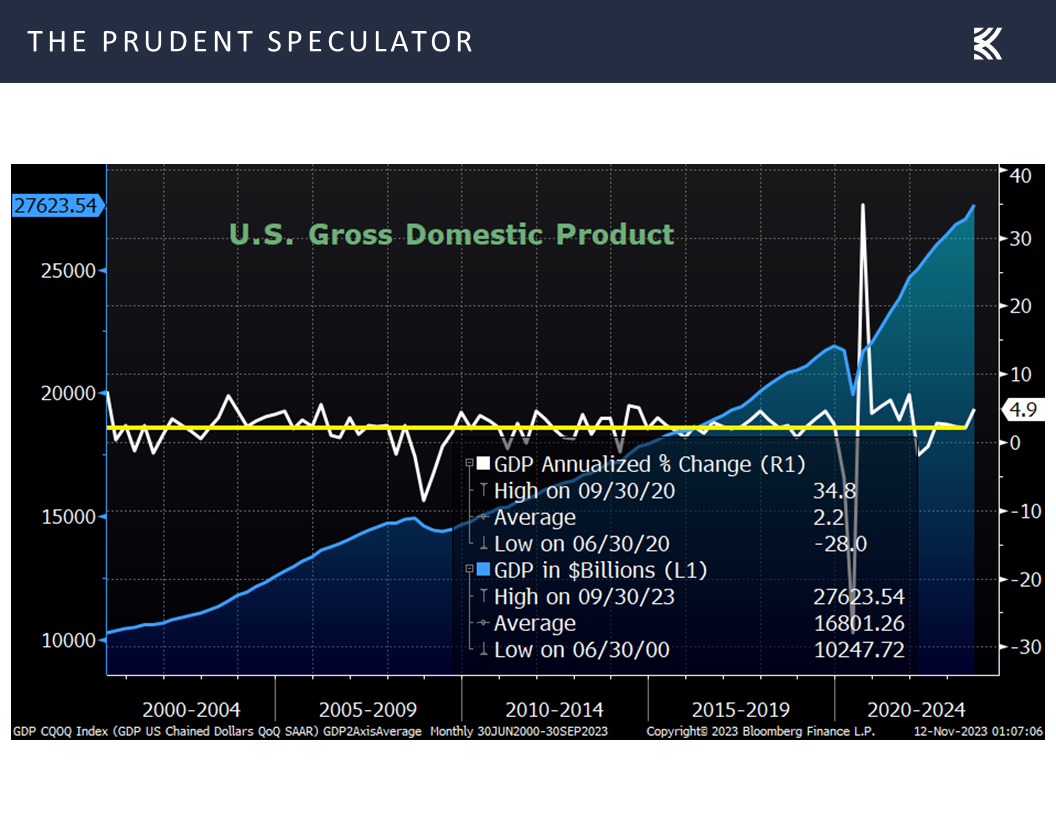

It isn’t luck or hocus pocus that has elevated stock prices through the years. No, equities have appreciated in value over time because the U.S. economy has grown mightily on both a real (inflation-adjusted) and a nominal (actual dollars) basis,

which has propelled corporate profits (tabulated in nominal dollars),

and dividend payouts (nominal dollars) markedly higher.

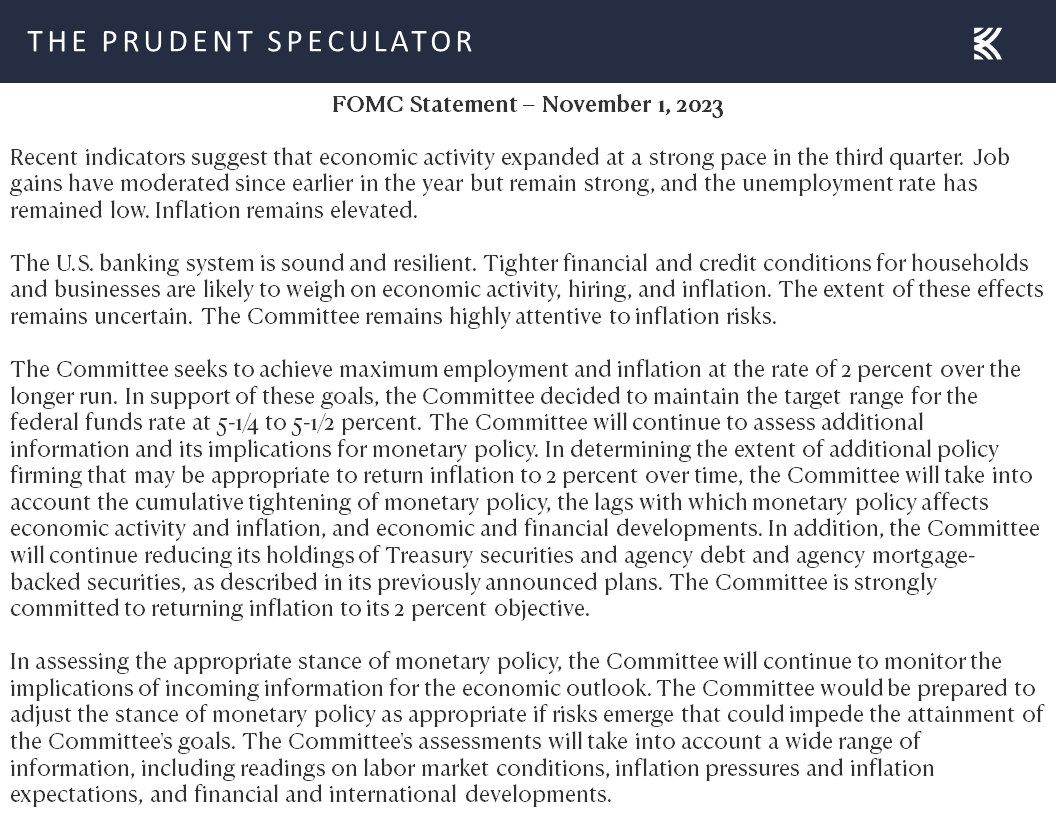

Fed Minutes – Nothing New vs. FOMC Statement and Powell Remarks on Nov. 1

Of course, the evidence presented above does not stop short-term-oriented traders from pushing stock prices higher and lower. Such was the case again during the Holiday-shortened trading week just ended, with the major market averages posting modest gains for three of the four days.

Obviously, we are happy to see the seasonally favorable time of year thus far live up to its historical probabilities,

but we are often puzzled by the rationale behind the daily market gyrations, given that stocks retreated in price on Tuesday arguably due to the release of the minutes of the Oct. 31 – Nov. 1 FOMC Meeting.

The revelations included, “All participants agreed that the committee was in agreement to proceed carefully,” and, “Participants expected that the data arriving in coming months would help clarify the extent to which the disinflation process was continuing, aggregate demand was moderating in the face of tighter financial and credit conditions, and labor markets were reaching a better balance between demand and supply.”

Not surprisingly, those comments essentially echoed the Fed Statement on Nov. 1,

as well as remarks Fed Chair Jerome H. Powell made at his Press Conference that same day: “Given how far we have come, along with the uncertainties and risks we face, the Committee is proceeding carefully. We will make decisions about the extent of additional policy firming and how long policy will remain restrictive based on the totality of the incoming data, the evolving outlook, and the balance of risks.”

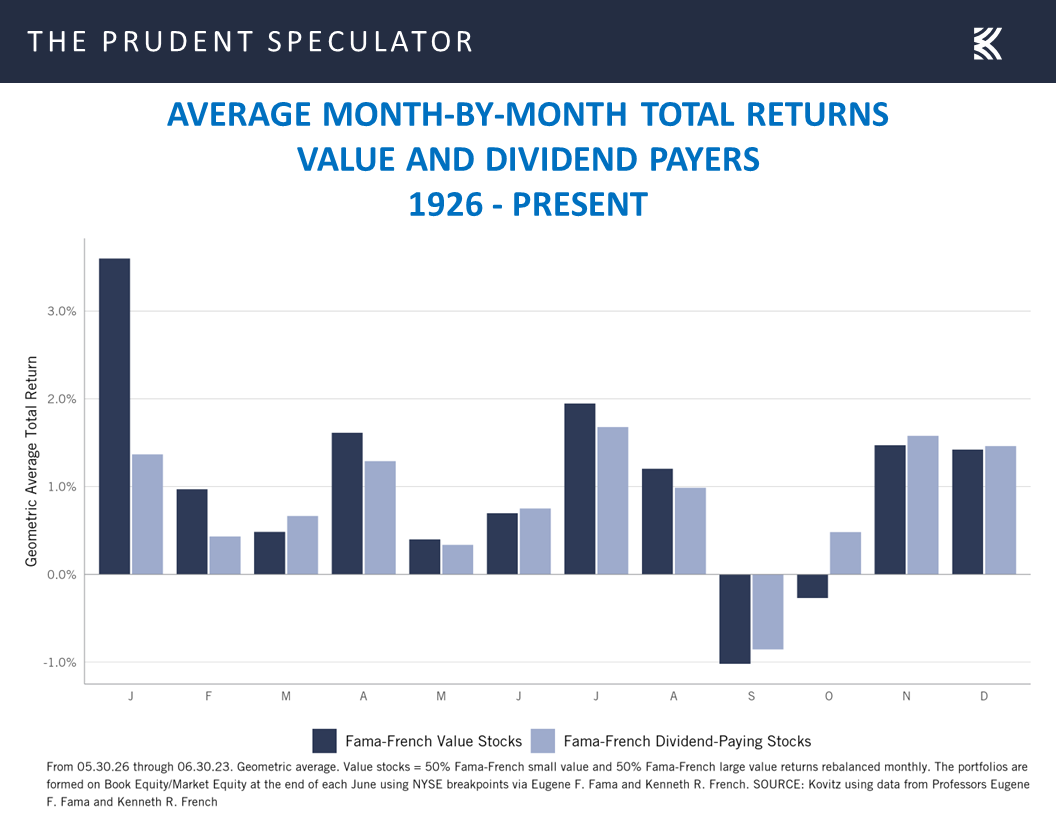

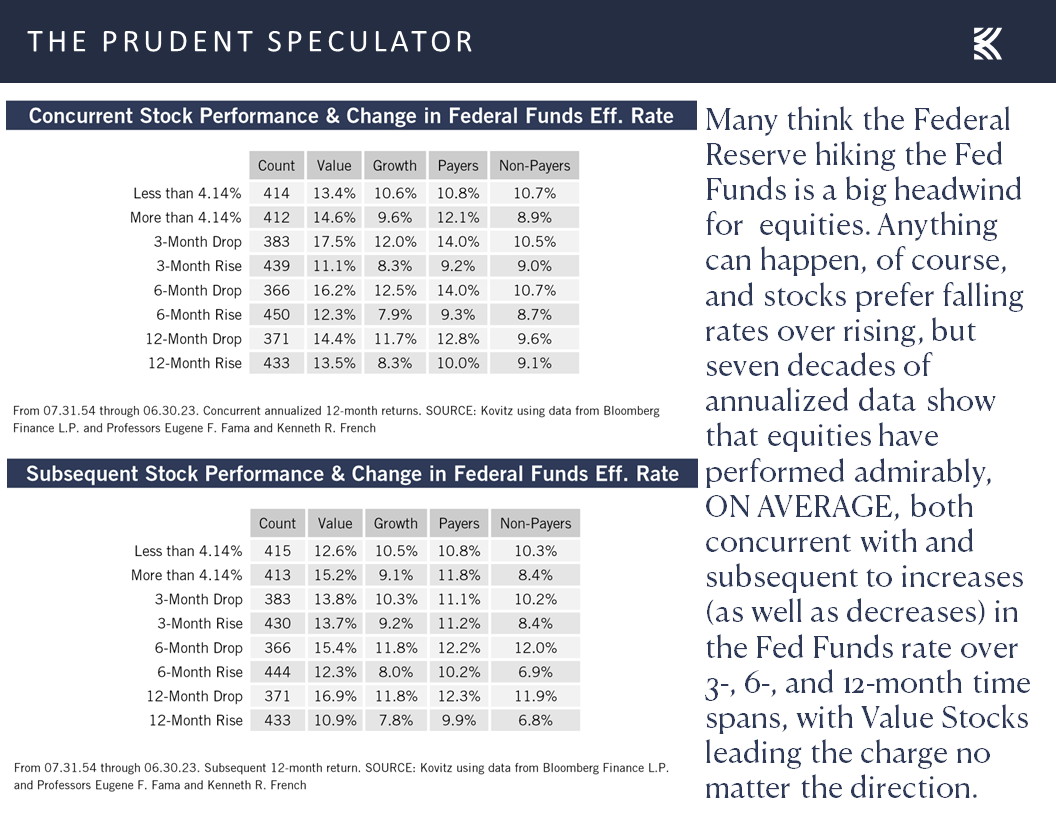

We understand that many market participants hang on every utterance from Federal Reserve officials, but, contrary to popular theory, we note that history shows that whether the Fed is raising or lowering the Fed Funds rate, stocks have performed fine, with Value and Dividend Payers, believe it or not, actually preferring a higher rate based on both average concurrent and subsequent performance figures.

Econ Data – Mixed Bag; Recession Probability Declines; Q4 GDP Growth Estimate Rises

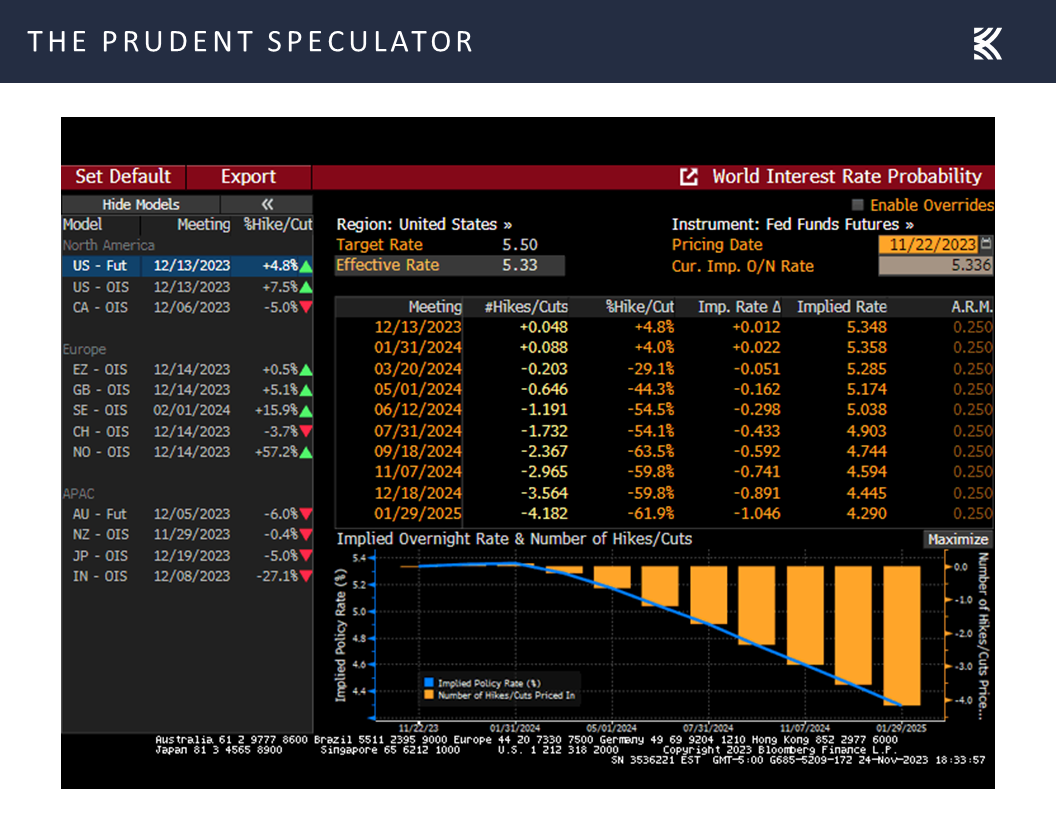

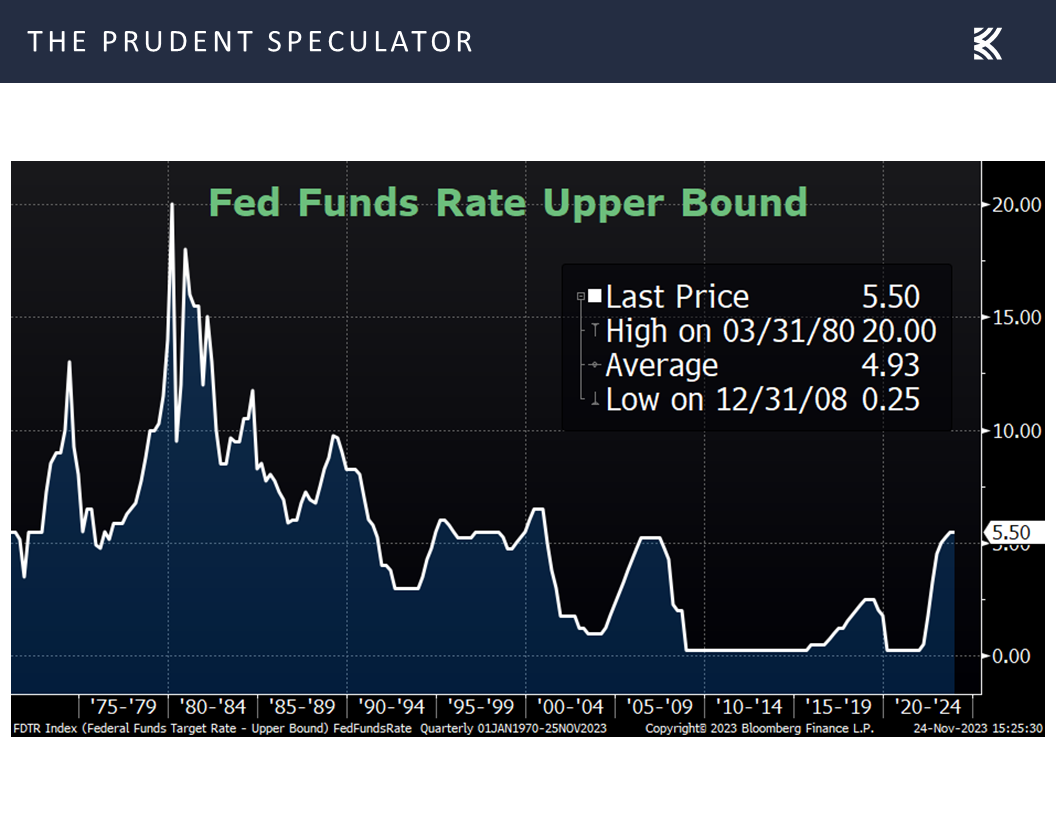

To be sure, the Fed will remain data dependent in its decision to tighten or loosen monetary policy going forward, but those who wager on such things are betting that the Fed Funds rate will be cut by more than 75 basis points (0.75%) next year, ending 2024 below 4.5%,

which would then put the benchmark central-bank lending rate below the historical norm dating back to 1970,

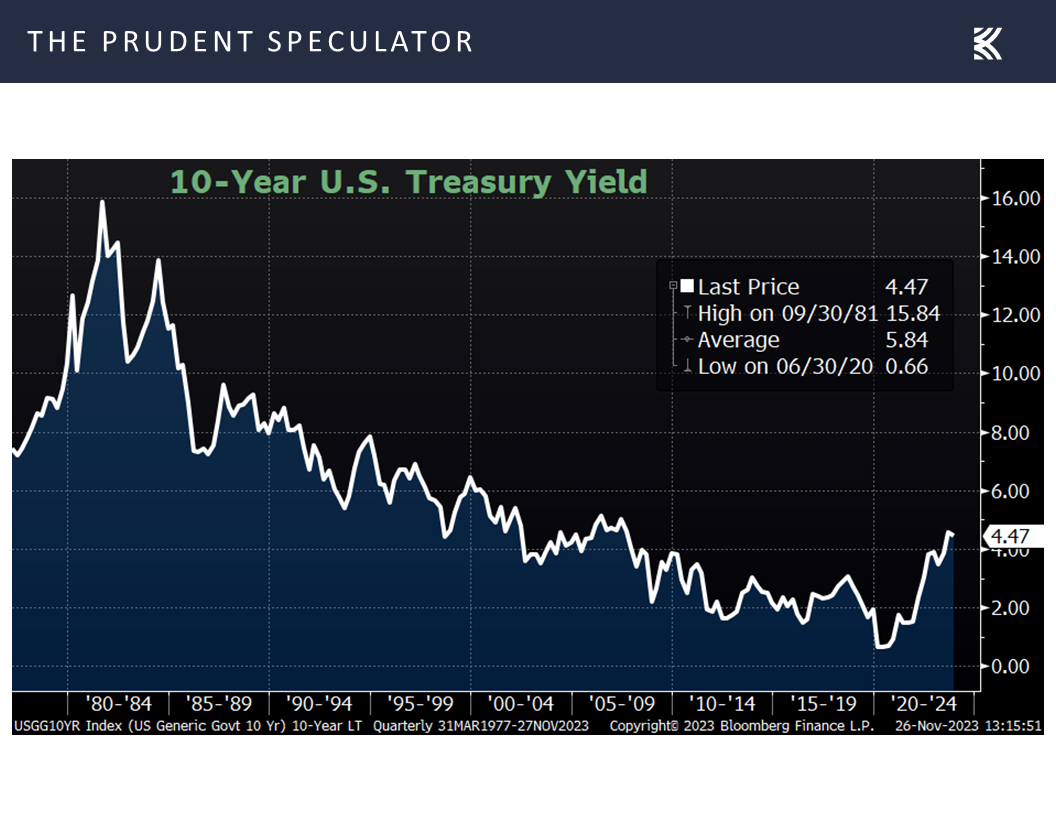

and in line with the current yield on the 10-year U.S. Treasury, which is still well below its average since the launch of The Prudent Speculator in March 1977.

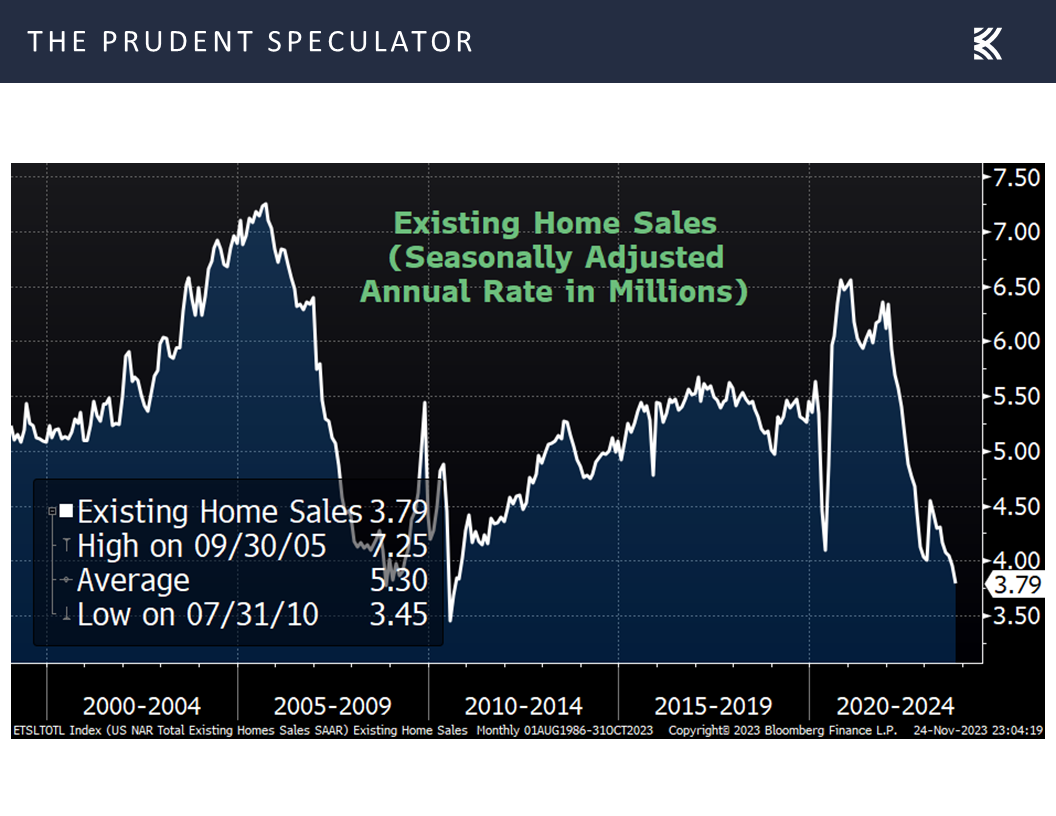

And speaking of the latest data, economic numbers out last week were mixed. On the one hand, sales of existing homes in October dropped to a seasonally adjusted annual rate of 3.79 million,

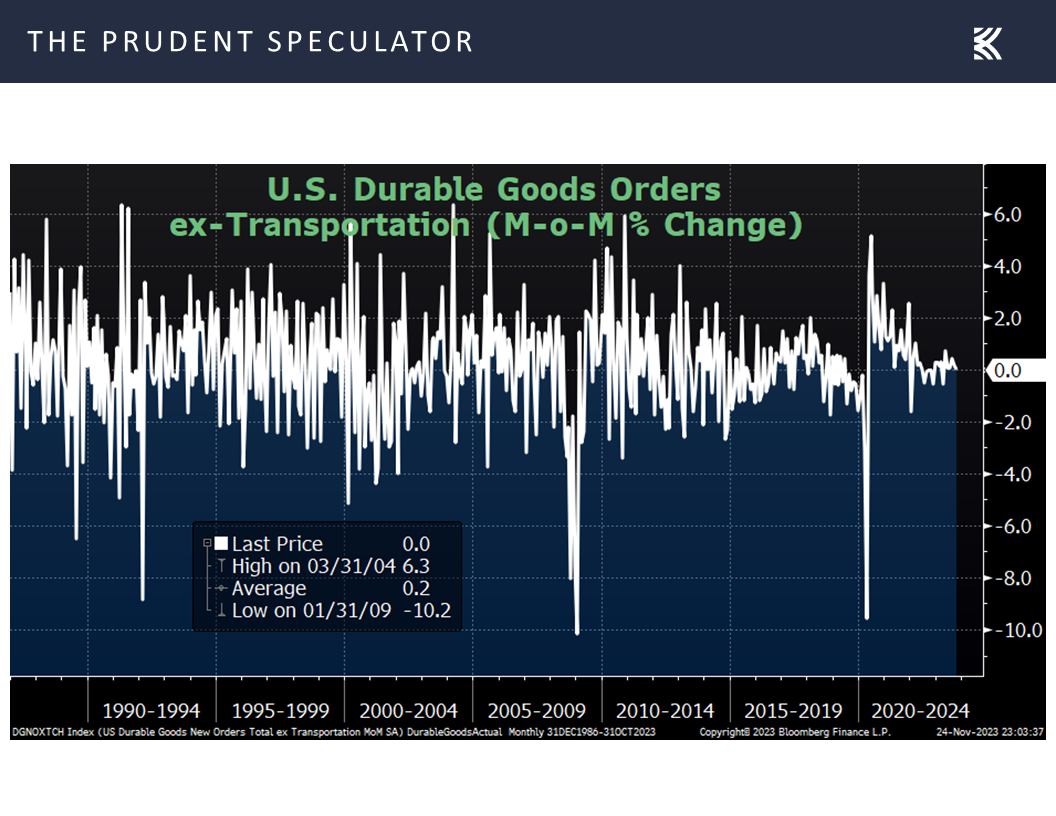

and orders for durable goods, excluding the volatile transportation sector, held steady last month, with each of these tallies coming in below expectations.

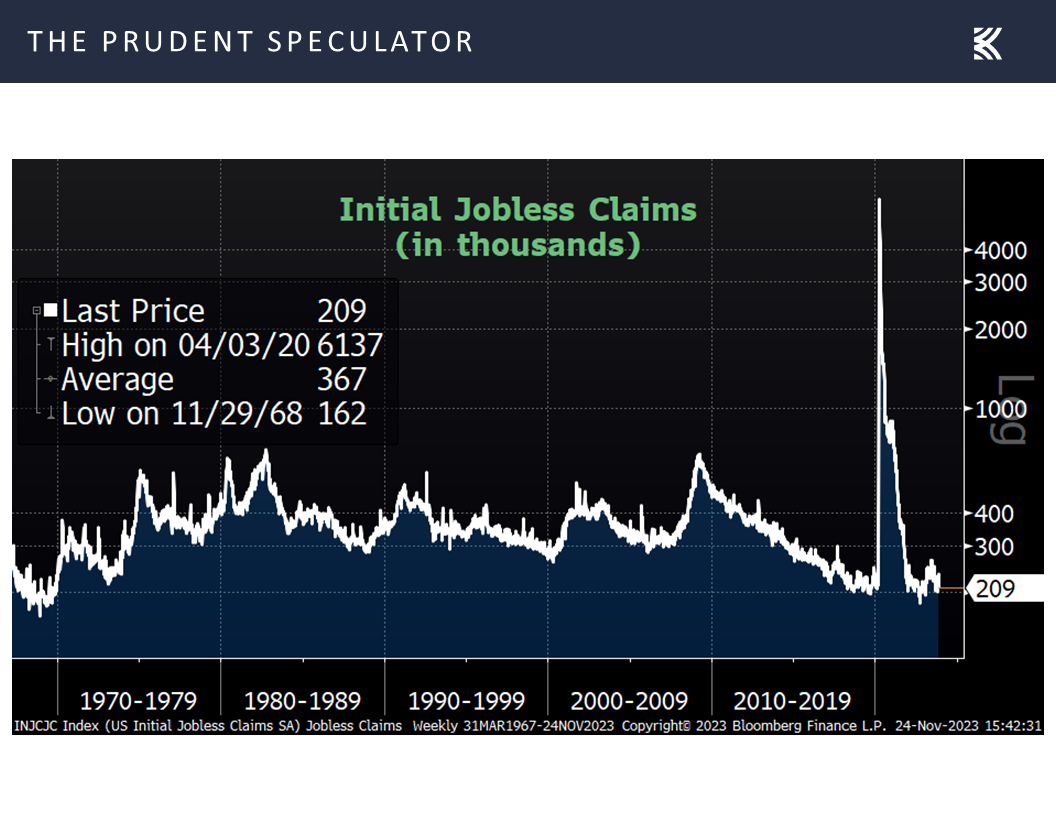

On the other hand, first-time filings for unemployment benefits dipped to 209,000, better than the 227,000 estimate,

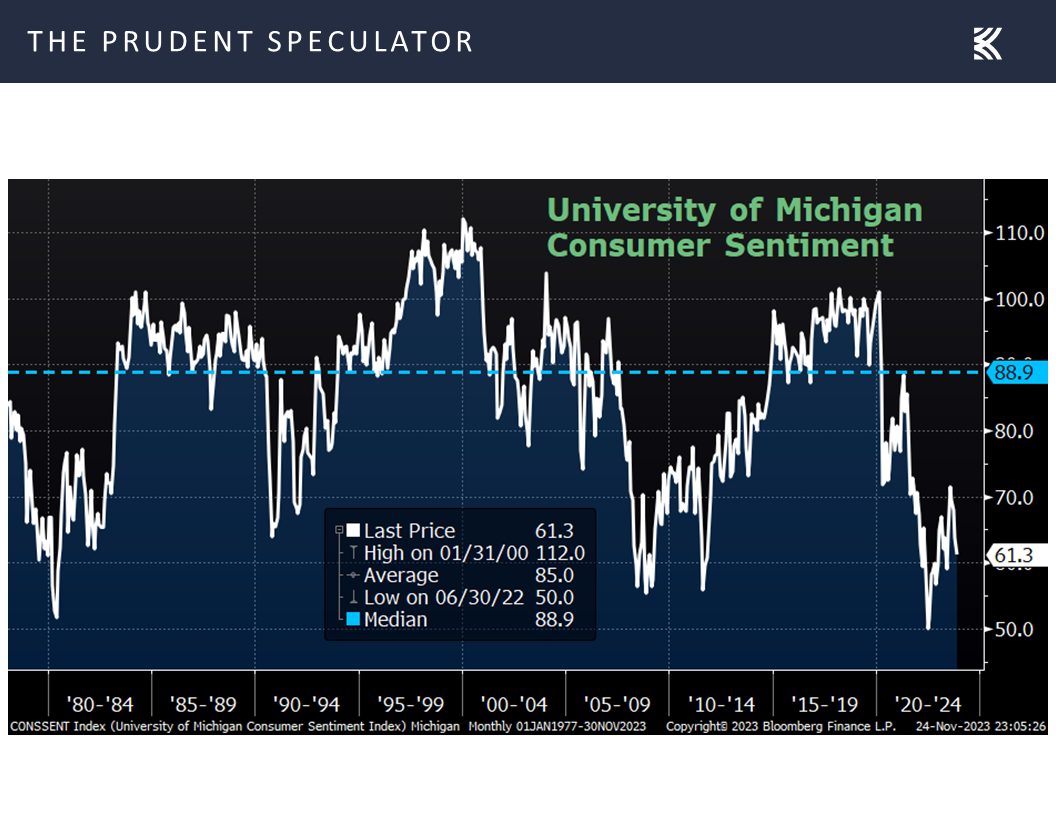

and the early read on consumer sentiment for November from the Univ. of Michigan modestly exceeded projections, although the figure was far below the historical norm.

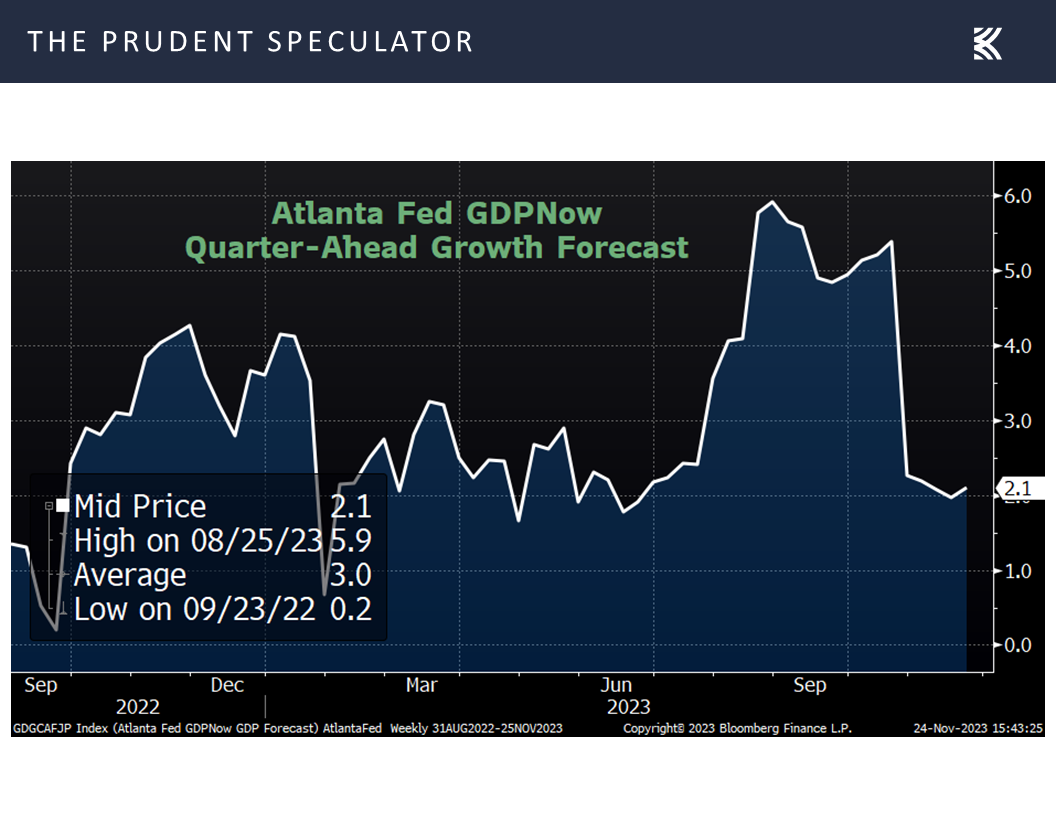

Taken together, the latest economic statistics caused forecasters to bump up their projection slightly for Q4 real GDP growth to 2.1%,

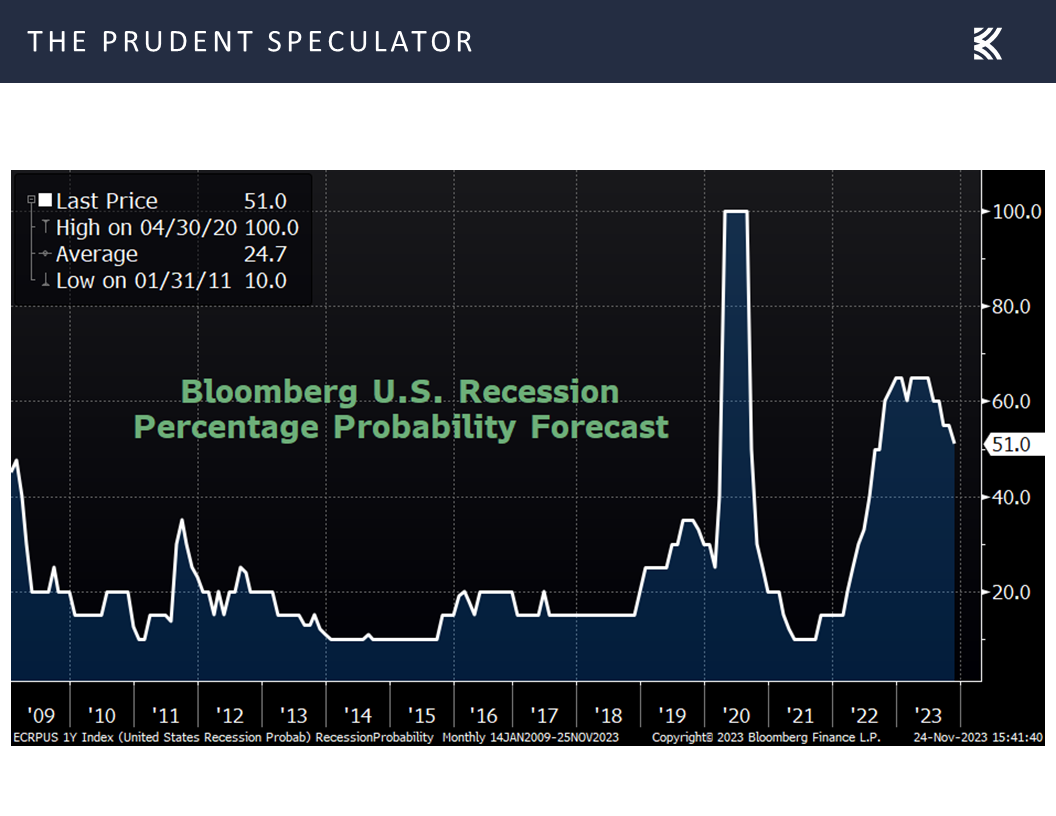

and to lower the odds of recession in the next 12 months to 51%, down from the 55% level at which the Bloomberg gauge had resided for quite some time,

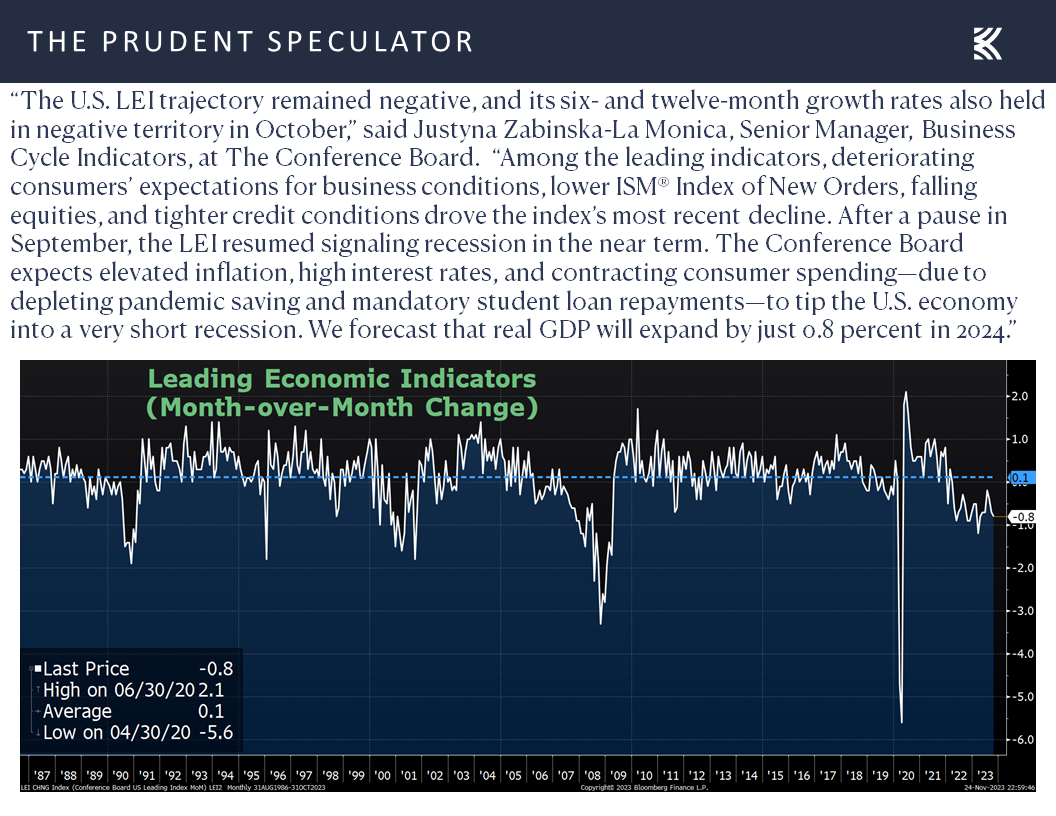

even as the widely watched Leading Economic Index for October continued to suggest a “very short” recession is in the cards next year despite a guesstimate of 0.8% real GDP growth from The Conference Board for all of 2024.

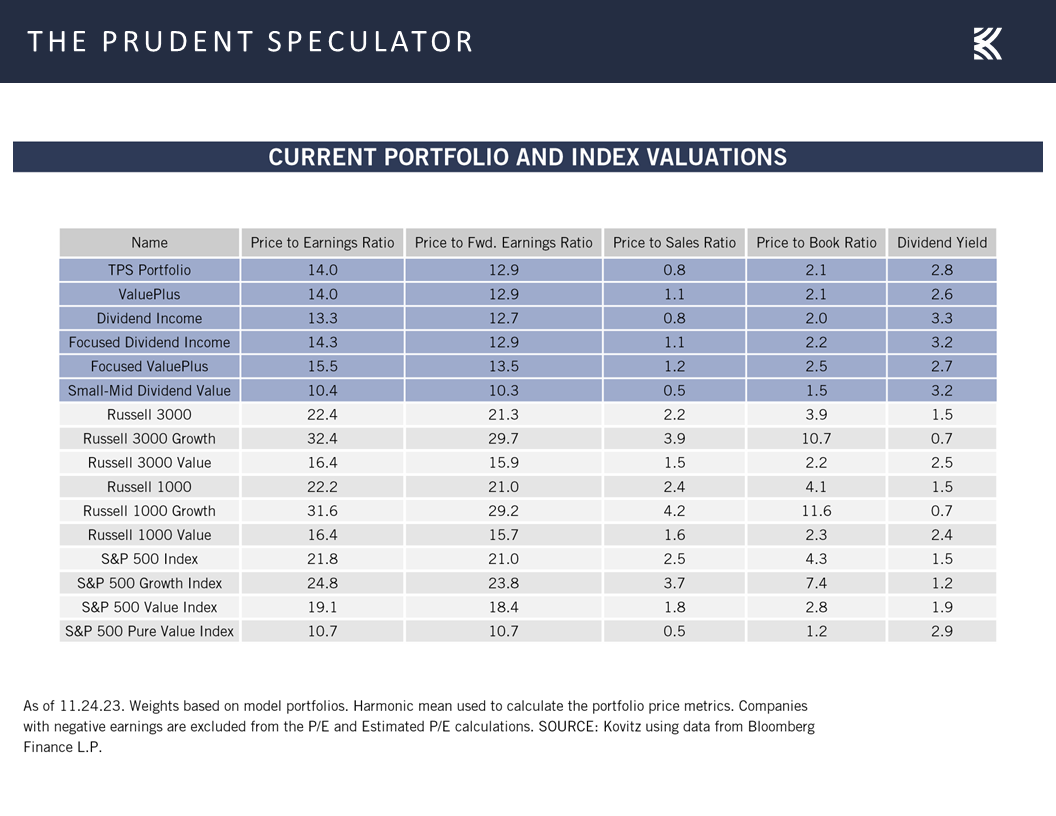

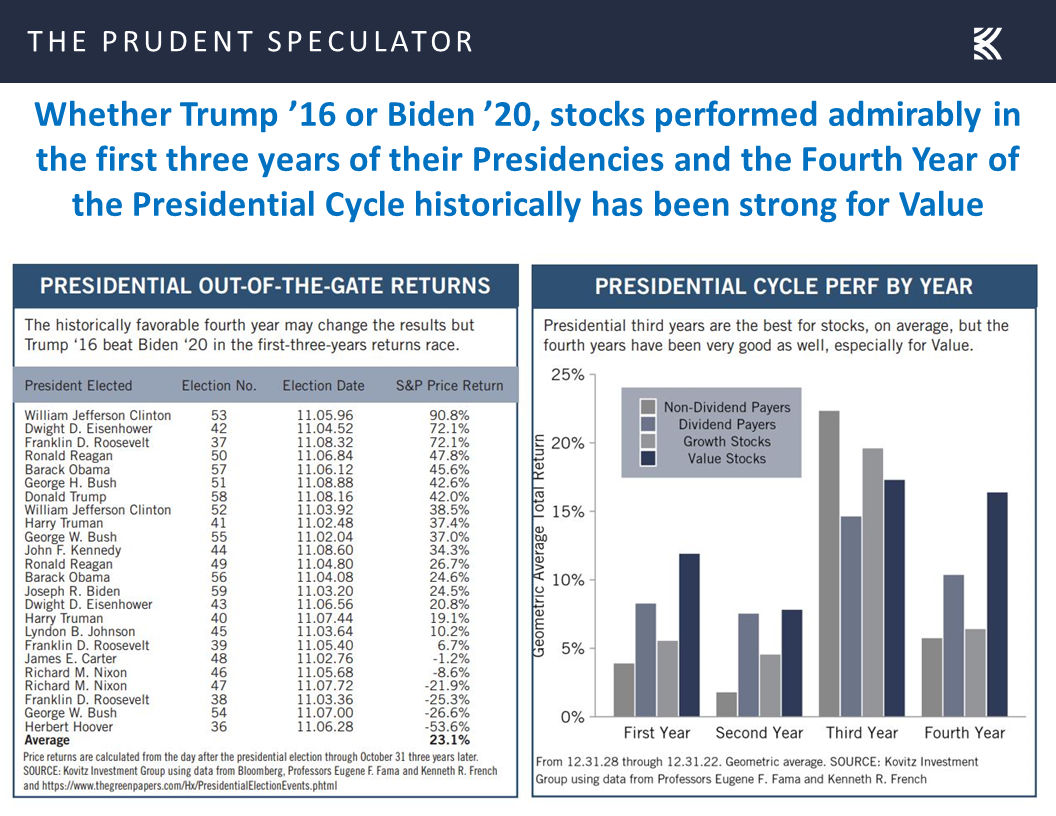

Reasons for Optimism – Valuations & Calendar

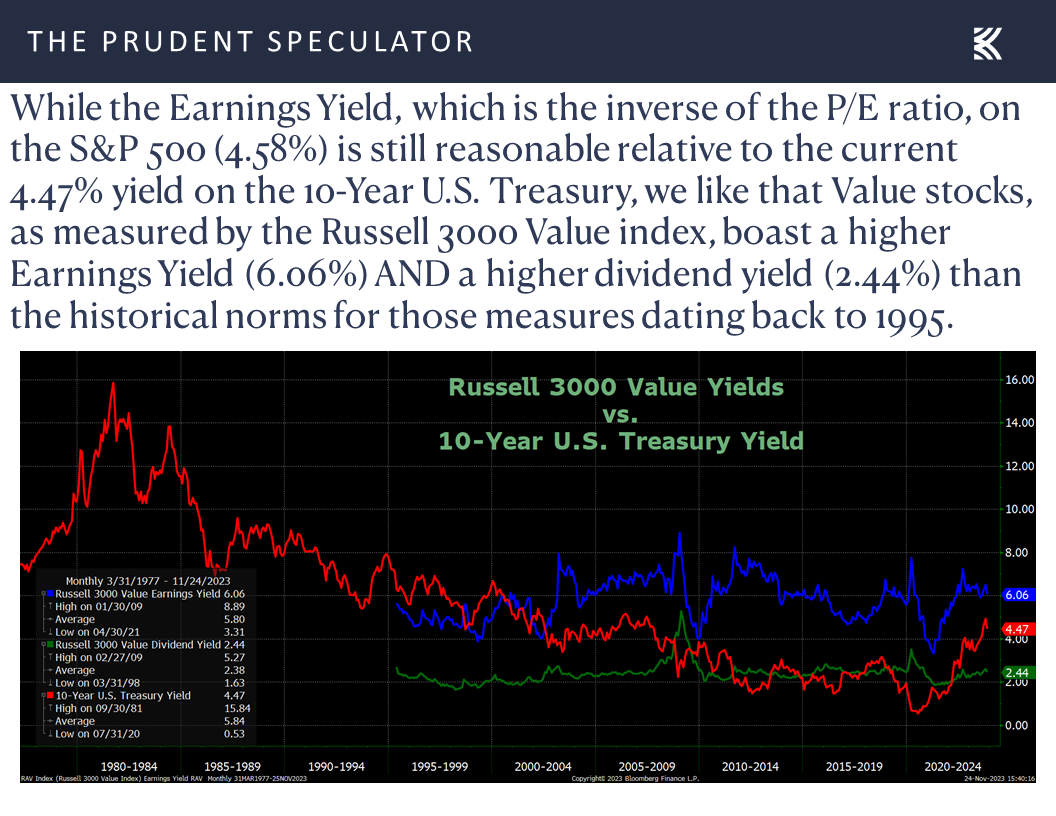

Though we remain braced for downside volatility, and the equity futures are pointing to a lower opening when trading resumes today, we see no reason to alter our optimistic long-term view, especially given that the kind of stocks we have long favored remain reasonably priced,

with the metrics even more attractive on our broadly diversified portfolios of what we believe to be undervalued stocks,

and the calendar in the seasonally favorable part (Third and Fourth Years) of the Presidential Cycle.

Stock News – Updates on six stocks across three different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Econ Data, Physics, Fed Minutes and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss econ data, physics, fed minutes and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Thanksgiving – Al Frank Perspective

Physics – Economic Growth, Profit Growth, Dividend Growth Drive Stock Prices

Fed Minutes – Nothing New vs. FOMC Statement and Powell Remarks on Nov. 1

Econ Data – Mixed Bag; Recession Probability Declines; Q4 GDP Growth Estimate Rises

Reasons for Optimism – Valuations & Calendar

Stock News – Updates on six stocks across three different sectors

Thanksgiving – Al Frank Perspective

We hope everyone had a wonderful Thanksgiving. There is always much for which to be grateful this time of year, and we like to reflect on words of wisdom from our founder Al Frank:

How relatively well off most of us are and how much we have to be thankful for, not just one day a year but most of the time. Sure, there are pains, traumas, sicknesses—physical, mental and spiritual—unfairnesses and outrages that overwhelm our sense of well being. Still, usually we have a choice of considering life as a tough chore with suffering relief or pleasure, or accepting life as a wonderful gift with marvelous if modest possibilities interspersed with occasional stumbles and hard times.

No doubt, the trials and tribulations of the financial markets pale in comparison to disconcerting global and domestic headlines, but Al passed away more than 21 years ago, yet his words remain very germane for those who choose to invest in stocks. Indeed, despite many bricks in the proverbial Wall of Worry, equities have overcome frightening event after frightening event,

to post terrific long-term returns,

with even those who forget that the only problem with market timing is getting the timing right still having a positive experience, on average.

Physics – Economic Growth, Profit Growth, Dividend Growth Drive Stock Prices

It isn’t luck or hocus pocus that has elevated stock prices through the years. No, equities have appreciated in value over time because the U.S. economy has grown mightily on both a real (inflation-adjusted) and a nominal (actual dollars) basis,

which has propelled corporate profits (tabulated in nominal dollars),

and dividend payouts (nominal dollars) markedly higher.

Fed Minutes – Nothing New vs. FOMC Statement and Powell Remarks on Nov. 1

Of course, the evidence presented above does not stop short-term-oriented traders from pushing stock prices higher and lower. Such was the case again during the Holiday-shortened trading week just ended, with the major market averages posting modest gains for three of the four days.

Obviously, we are happy to see the seasonally favorable time of year thus far live up to its historical probabilities,

but we are often puzzled by the rationale behind the daily market gyrations, given that stocks retreated in price on Tuesday arguably due to the release of the minutes of the Oct. 31 – Nov. 1 FOMC Meeting.

The revelations included, “All participants agreed that the committee was in agreement to proceed carefully,” and, “Participants expected that the data arriving in coming months would help clarify the extent to which the disinflation process was continuing, aggregate demand was moderating in the face of tighter financial and credit conditions, and labor markets were reaching a better balance between demand and supply.”

Not surprisingly, those comments essentially echoed the Fed Statement on Nov. 1,

as well as remarks Fed Chair Jerome H. Powell made at his Press Conference that same day: “Given how far we have come, along with the uncertainties and risks we face, the Committee is proceeding carefully. We will make decisions about the extent of additional policy firming and how long policy will remain restrictive based on the totality of the incoming data, the evolving outlook, and the balance of risks.”

We understand that many market participants hang on every utterance from Federal Reserve officials, but, contrary to popular theory, we note that history shows that whether the Fed is raising or lowering the Fed Funds rate, stocks have performed fine, with Value and Dividend Payers, believe it or not, actually preferring a higher rate based on both average concurrent and subsequent performance figures.

Econ Data – Mixed Bag; Recession Probability Declines; Q4 GDP Growth Estimate Rises

To be sure, the Fed will remain data dependent in its decision to tighten or loosen monetary policy going forward, but those who wager on such things are betting that the Fed Funds rate will be cut by more than 75 basis points (0.75%) next year, ending 2024 below 4.5%,

which would then put the benchmark central-bank lending rate below the historical norm dating back to 1970,

and in line with the current yield on the 10-year U.S. Treasury, which is still well below its average since the launch of The Prudent Speculator in March 1977.

And speaking of the latest data, economic numbers out last week were mixed. On the one hand, sales of existing homes in October dropped to a seasonally adjusted annual rate of 3.79 million,

and orders for durable goods, excluding the volatile transportation sector, held steady last month, with each of these tallies coming in below expectations.

On the other hand, first-time filings for unemployment benefits dipped to 209,000, better than the 227,000 estimate,

and the early read on consumer sentiment for November from the Univ. of Michigan modestly exceeded projections, although the figure was far below the historical norm.

Taken together, the latest economic statistics caused forecasters to bump up their projection slightly for Q4 real GDP growth to 2.1%,

and to lower the odds of recession in the next 12 months to 51%, down from the 55% level at which the Bloomberg gauge had resided for quite some time,

even as the widely watched Leading Economic Index for October continued to suggest a “very short” recession is in the cards next year despite a guesstimate of 0.8% real GDP growth from The Conference Board for all of 2024.

Reasons for Optimism – Valuations & Calendar

Though we remain braced for downside volatility, and the equity futures are pointing to a lower opening when trading resumes today, we see no reason to alter our optimistic long-term view, especially given that the kind of stocks we have long favored remain reasonably priced,

with the metrics even more attractive on our broadly diversified portfolios of what we believe to be undervalued stocks,

and the calendar in the seasonally favorable part (Third and Fourth Years) of the Presidential Cycle.

Stock News – Updates on six stocks across three different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.