The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Economic News, Volatility, Jeremy Siegel, and more Stock News. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

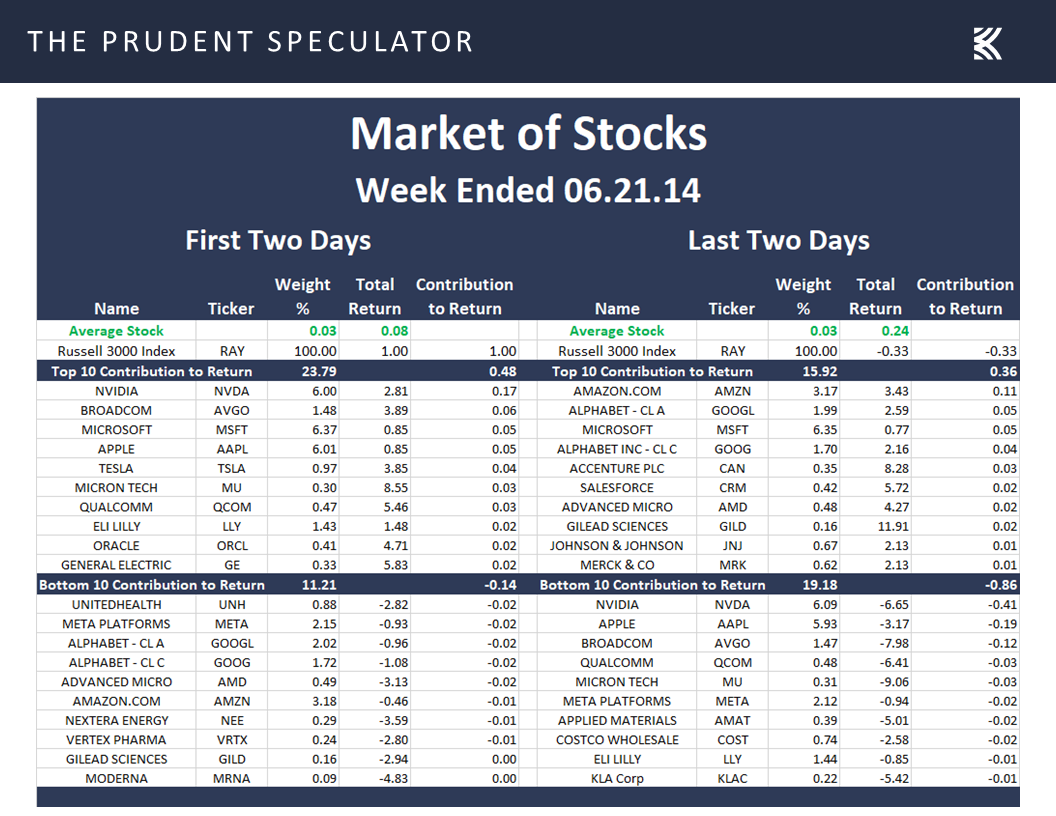

Market Breadth – A Handful of Mega Caps Up but Most Stocks Down Last Week; Average Stock Down on the Year

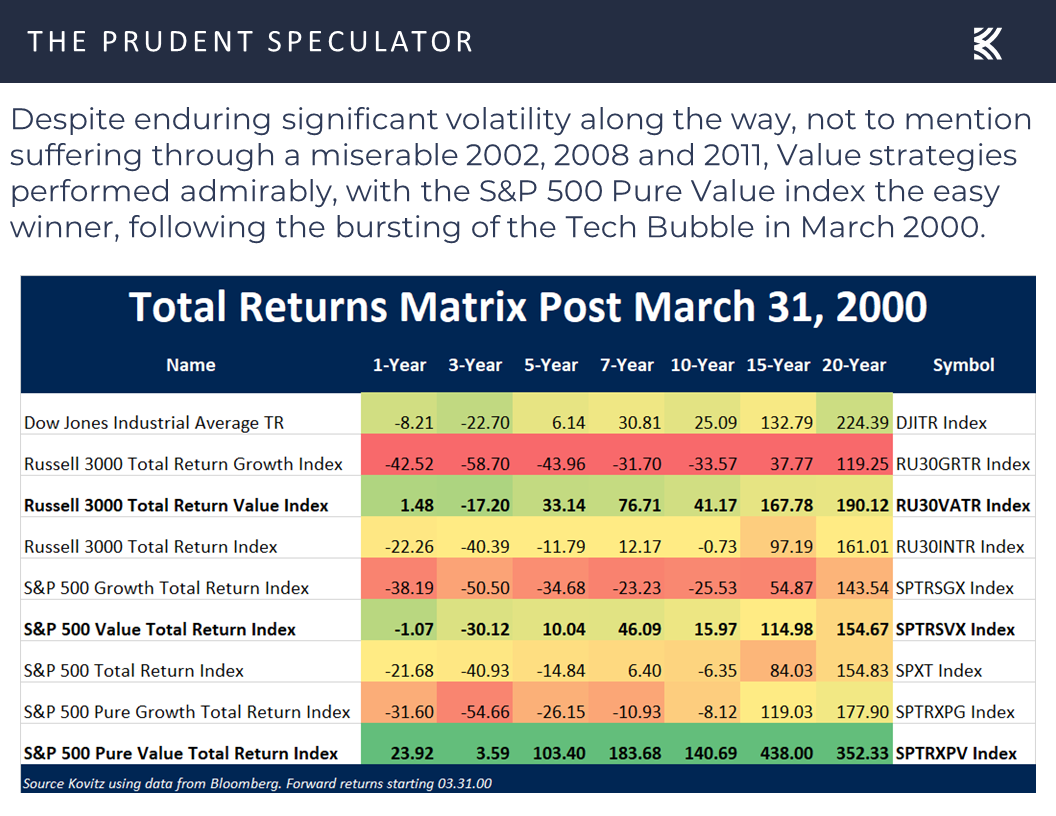

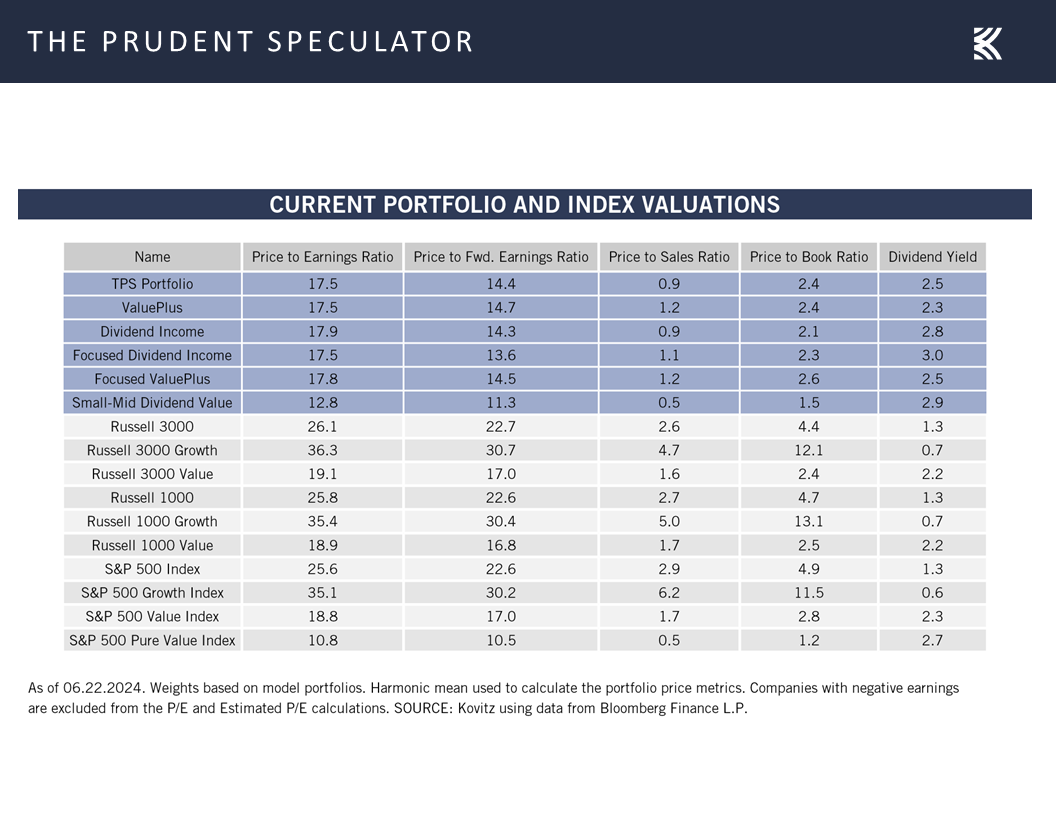

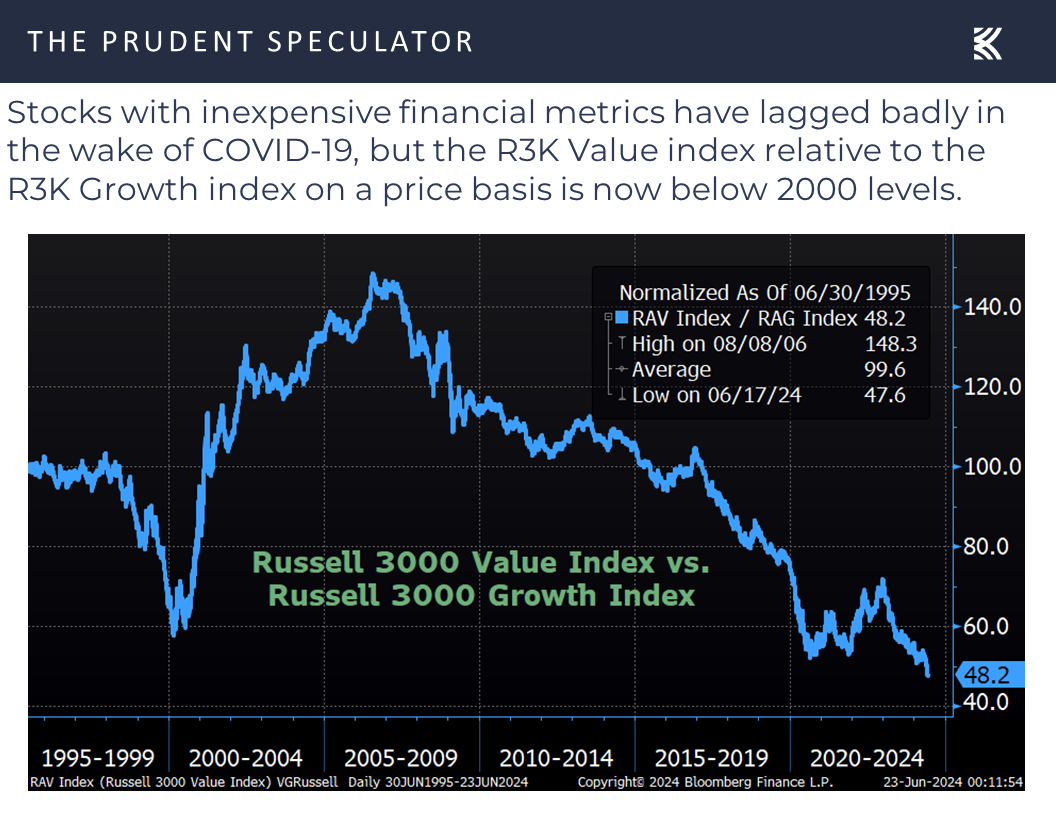

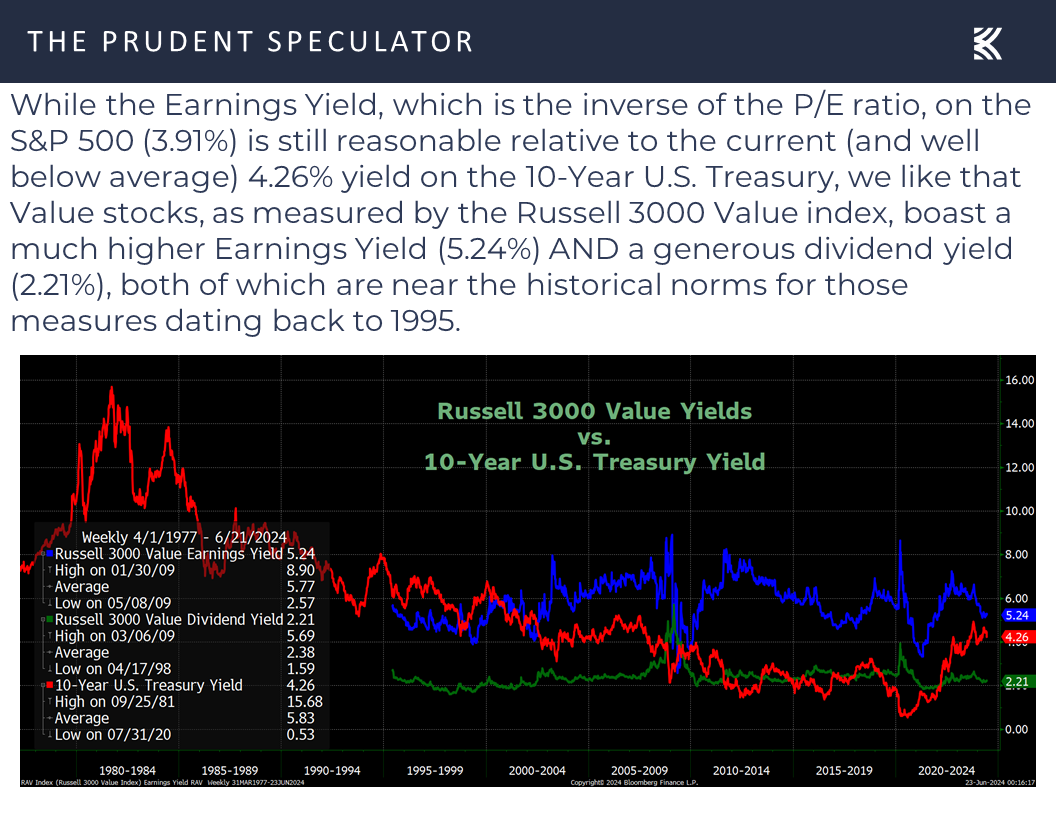

Value – Tech Bubble History Lesson; R3K Value Index Very Inexpensive Relative to R3K Growth

Inflation – Lower-than-Expected CPI & PPI

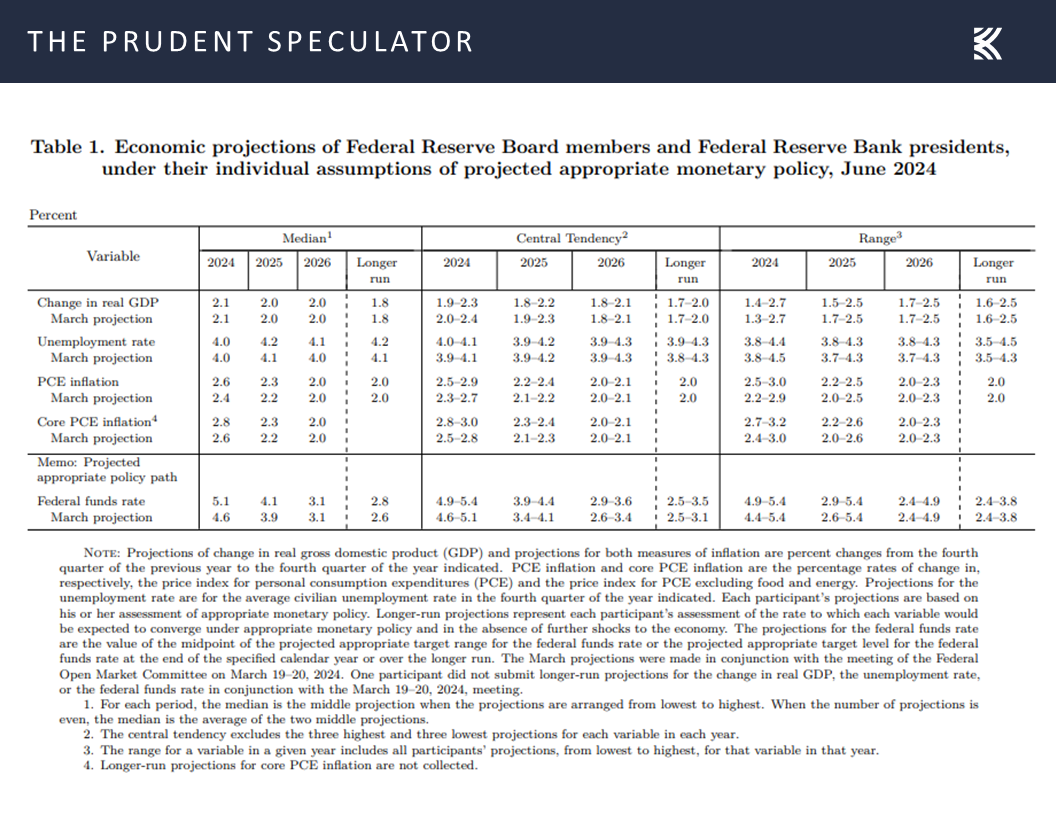

Fed Econ Projections – 1 Rate Cut This Year; 4 Cuts Next Year

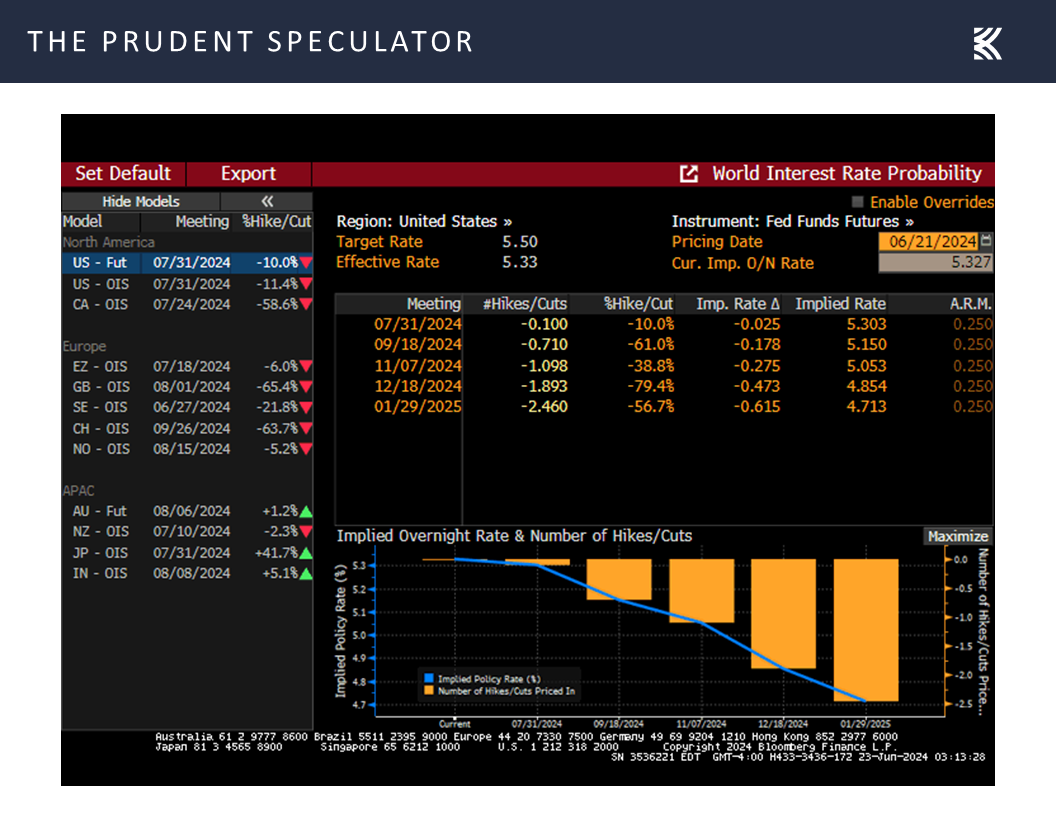

Interest Rates – Lower 10-Year Yield & Lower Expected Year-End Fed Funds Rate vs. the Prior Week

Econ News – Mixed Data; Fed & World Bank Each Projecting Decent U.S. Growth for ’24 and ’25

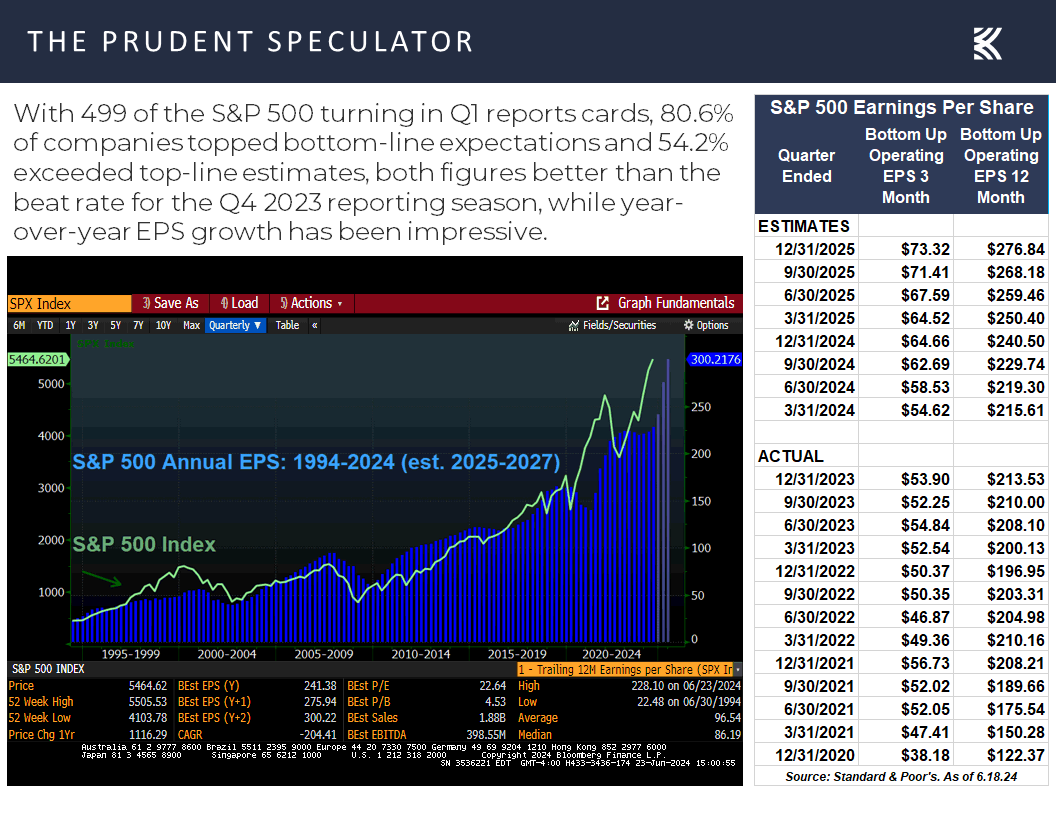

Earnings – Solid Growth Estimated in ’24 & ’25

Volatility – Scary Headlines & Plenty of Gyrations Along the Way but Long-Term Trend is Up

Stock News – Updates on AAPL, ORCL, AVGO, GM & ZBH

Market Breadth – A Handful of Mega Caps Up but Most Stocks Down Last Week; Average Stock Down on the Year

It was another fascinating week for equities with the Juneteenth demarcation line offering yet another reminder that it is a market of stocks and not simply a stock market. After all, the capitalization-weighted Russell 3000 index (R3K) performed very well (gaining 1.00%) over the first two days of the week, yet the average stock advanced only 0.08%. It was a complete reversal over the second two days of the week with the R3K dropping 0.33% and the average stock climbing 0.24%.

Value – Tech Bubble History Lesson; R3K Value Index Very Inexpensive Relative to R3K Growth

Interestingly, several of the big (from a contribution to return standpoint) early-week winners (generally A.I.-related), were the late-week losers…and vice versa, providing more evidence that a rising/retreating tide doesn’t lift/sink all boats. Such was the case following the bursting of the Dot.com Bubble when many of the high-flying Tech (Growth) stocks cratered and residents of the Value camp dramatically outperformed.

Of course, no two market environments are ever the same, and today’s stellar A.I. performers are business that drive substantial profits to the bottom line (and we own several), unlike many of the red-ink-laden Dot.com companies a quarter century ago, but we continue to sleep very well at night with the inexpensive valuation metrics (including our A.I. holdings) for our broadly diversified portfolios.

This is especially true given that the divergence in returns between the Growth and Value indexes that, despite the latter beating the former last week, is now at a greater extreme than in early-2000,

and considering the reasonable multiple of earnings relative to the historical mean for the Russell 3000 Value index,

with the earnings yield (inverse of the P/E ratio) also confirming that Value stocks are not overly expensive, unlike Growth stocks, versus where they have traded since 1995.

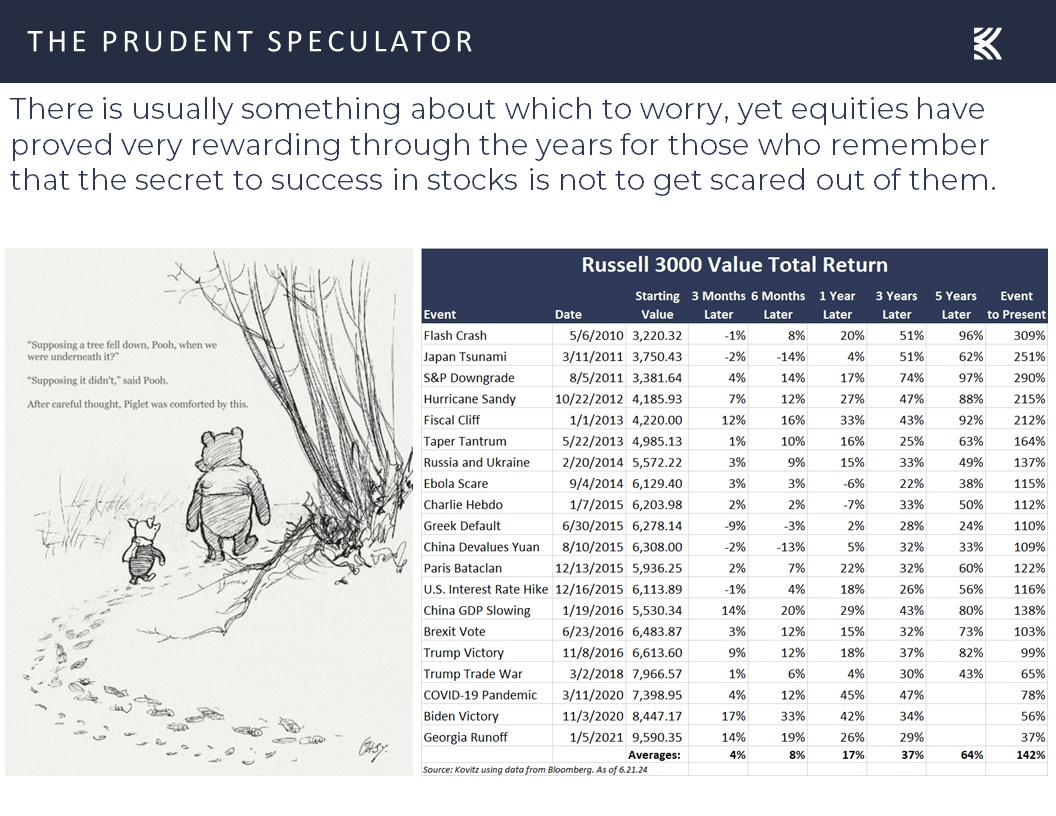

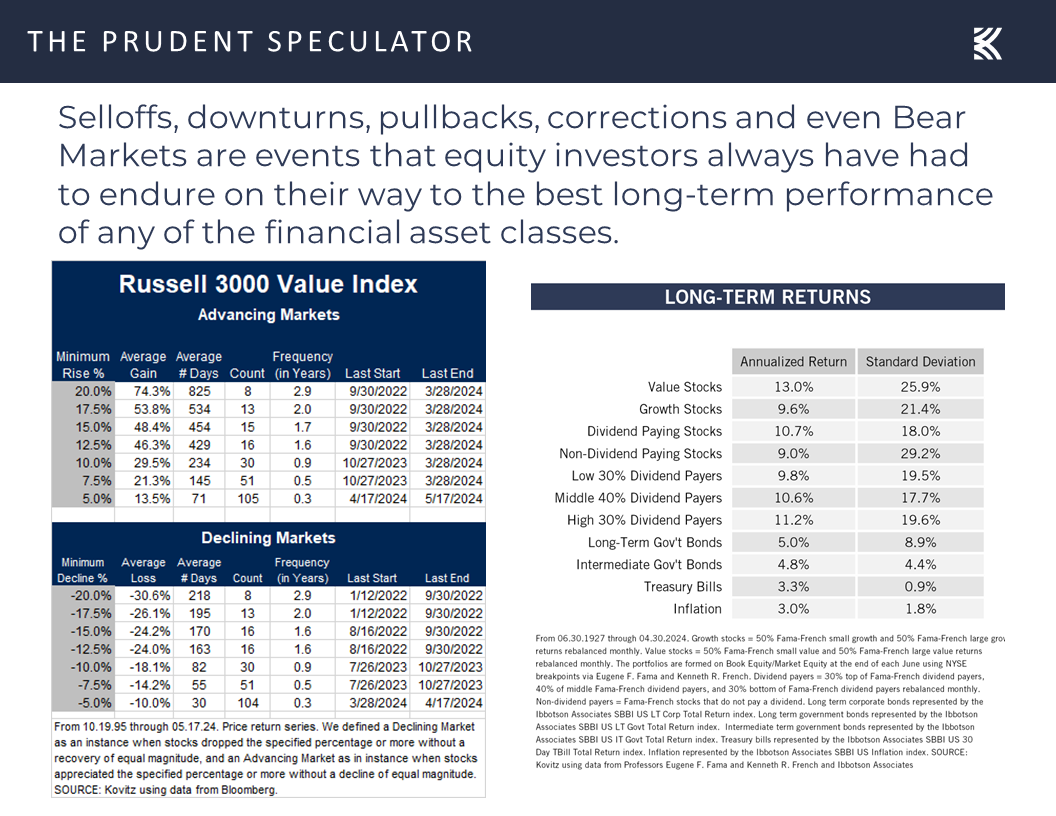

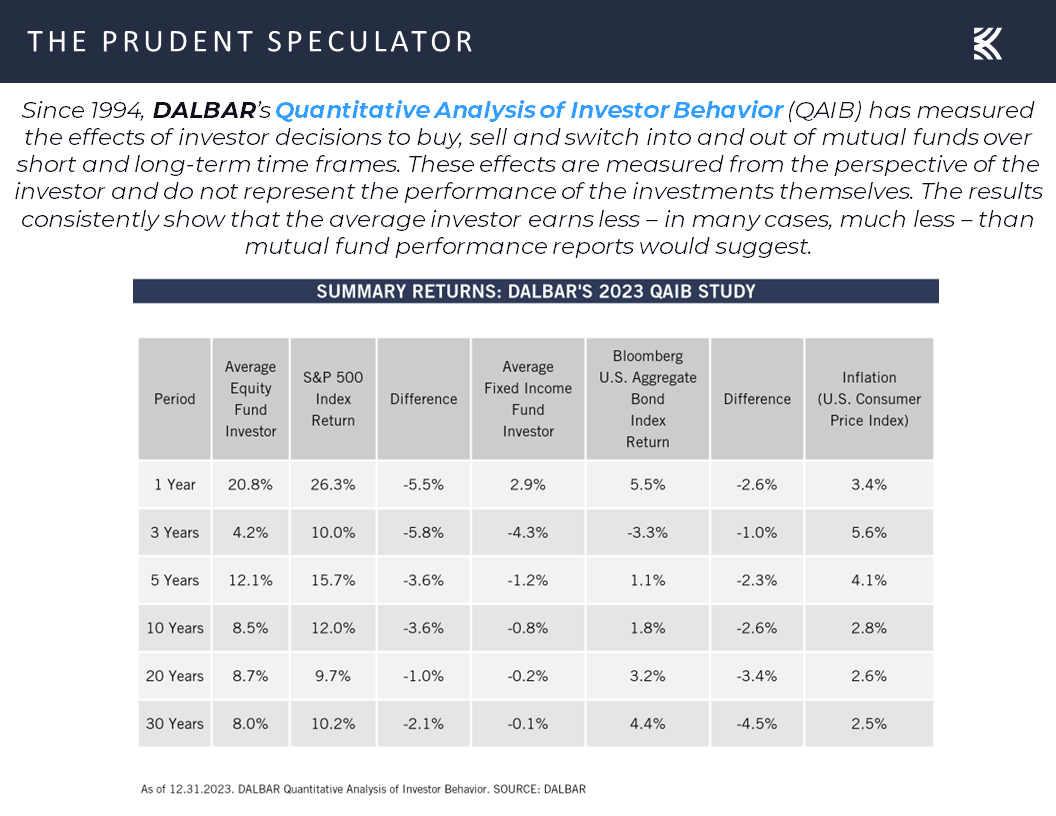

Volatility – Scary Headlines & Plenty of Gyrations Along the Way but Long-Term Trend is Up

That does not mean that it is up, up and away for the kind of stocks we favor, as there will always be disconcerting headlines with which we must contend,

not to mention bouts of sometimes frightening volatility, but the rewards for long-term-oriented investors have been terrific,

assuming they remember that the secret to success in stocks is not to get scared out of them. Indeed, as data from DALBAR in the table below show, time in the market has proven to trump market timing.

Long-Term Catalysts – EPS & GDP Have Grown Over Time

Of course, there is valid rationale for stocks providing handsome returns over time as corporate profits have grown,

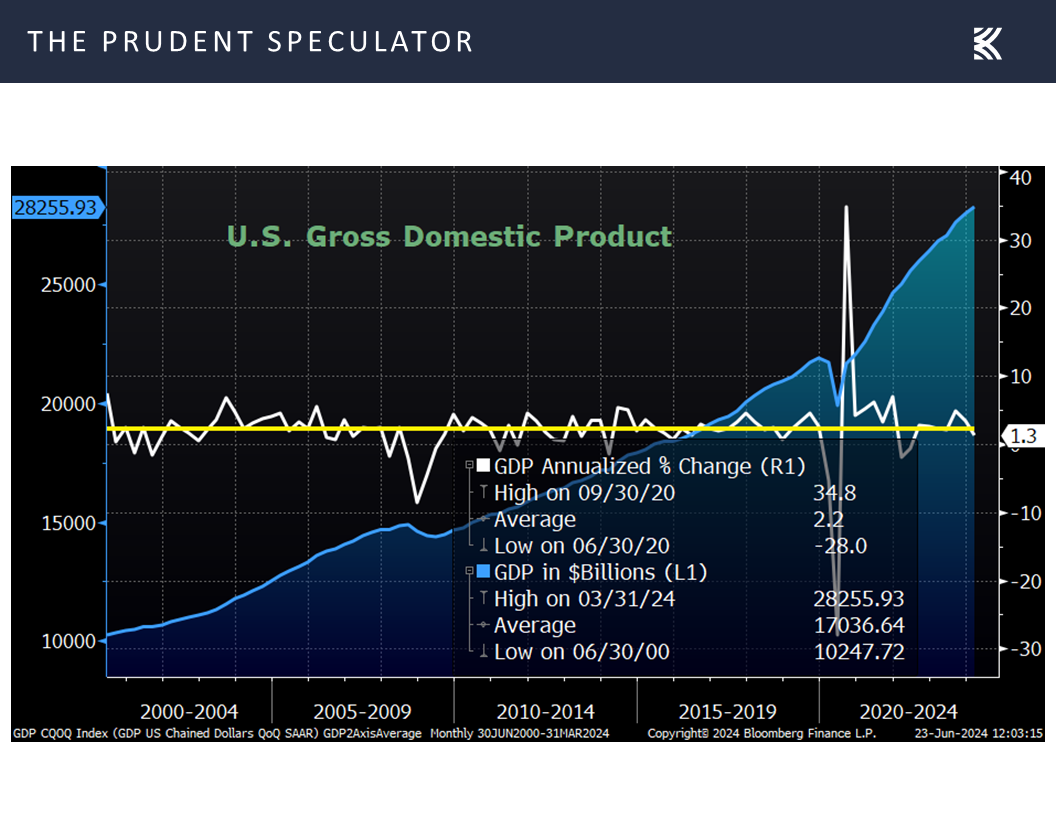

as the U.S. economy has grown.

Econ News – Mixed Data; Growth Still Projected for ’24, ’25 and ’26

The question, then, is the outlook for growth going forward. The Federal Reserve, for its part, projects OK real (inflation-adjusted) GDP expansion in the 2% range for each of 2024, 2025 & 2026,

with a likely series of cuts in the Fed Funds rate helping to support the economy.

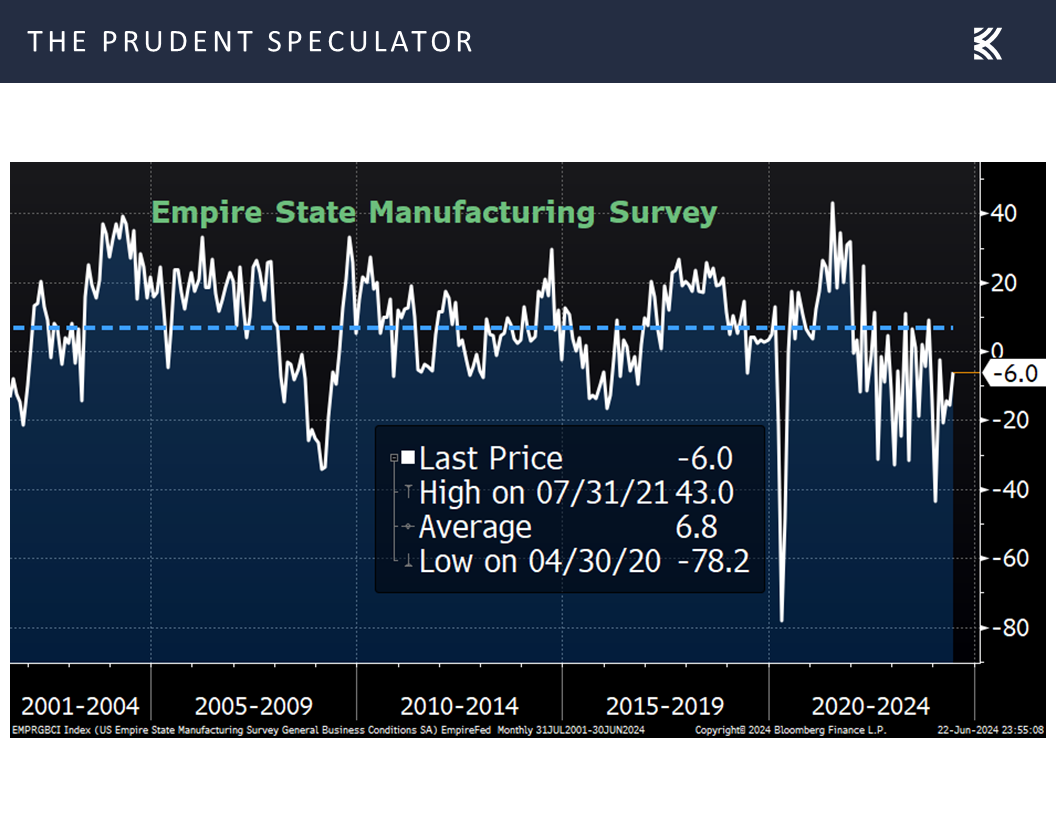

No doubt, there is plenty of disagreement about when those rate reductions may begin, and last week’s mixed economic numbers did not swing the pendulum much in either direction. For example, the Empire Manufacturing Index came in at -6.0 for June, but this gauge on the health of the factory sector in the New York area was better than estimated and an improvement from the -15.6 reading in May.

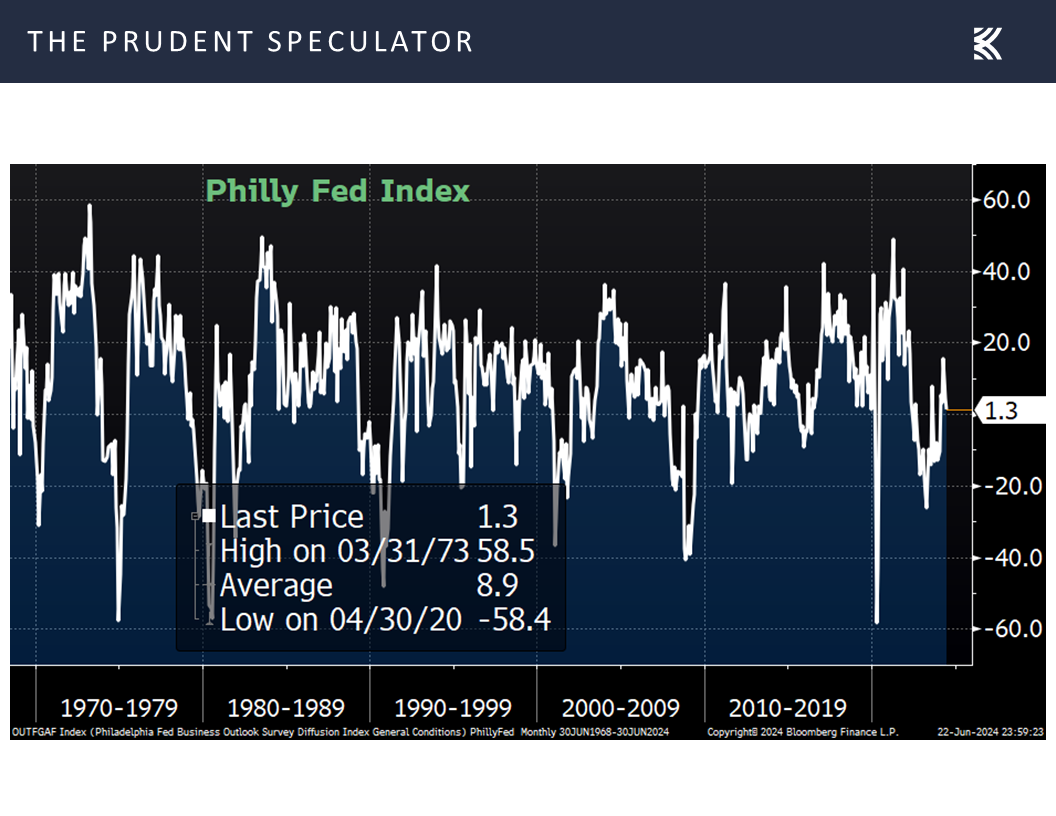

On the other hand, the Philadelphia Fed measure of East-Coast business output for June fell to 1.3, below projections and down from 4.5 in May.

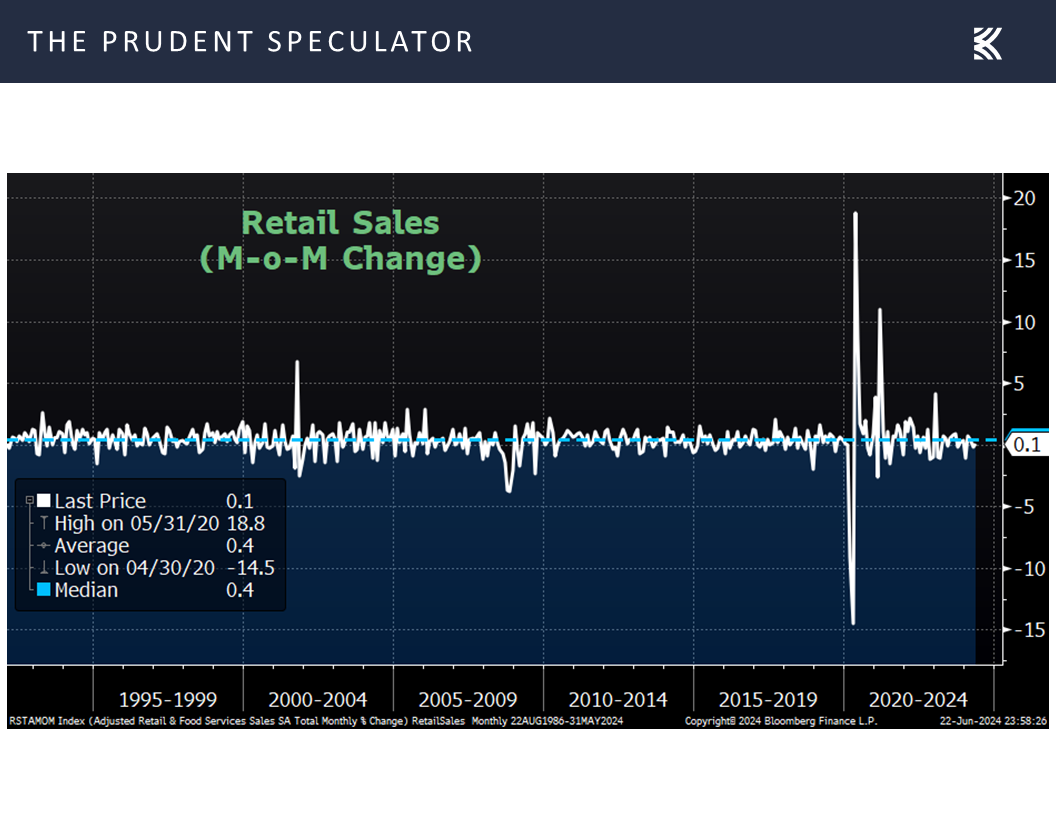

The latest figures on retail sales also trailed estimates, advancing 0.1% in May, below forecasts calling for a 0.3% increase,

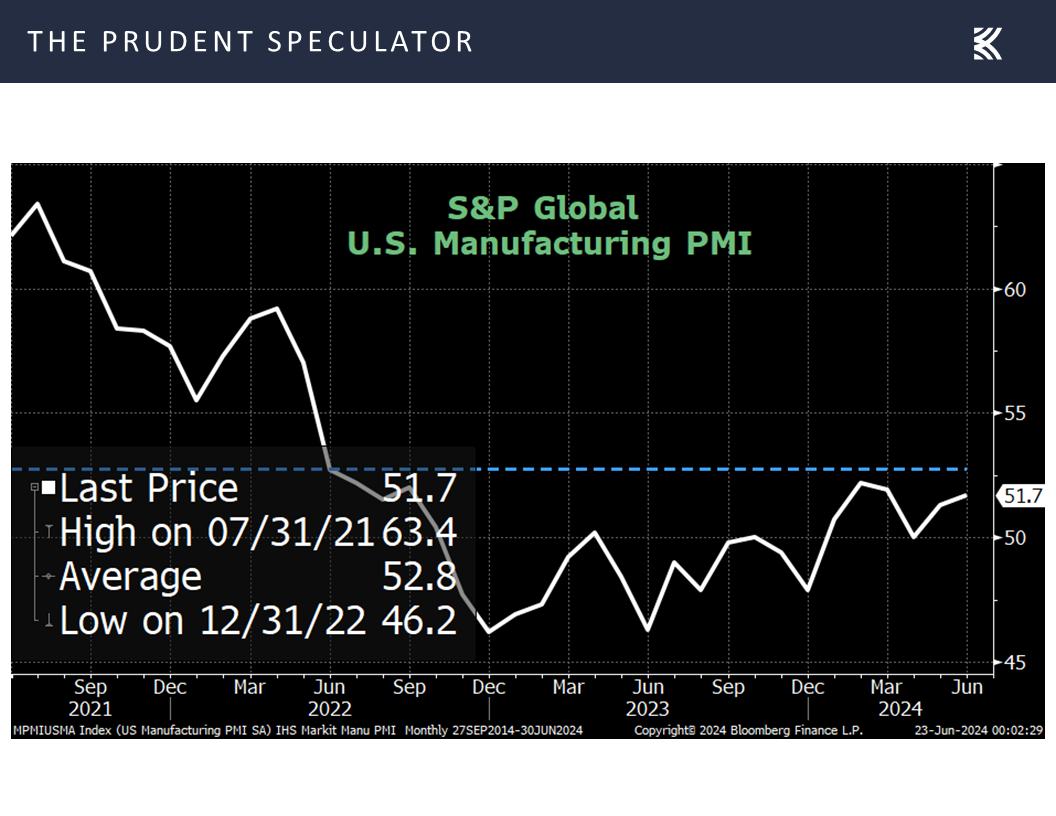

but tallies from S&P Global for both U.S. Manufacturing,

but tallies from S&P Global for both U.S. Manufacturing,

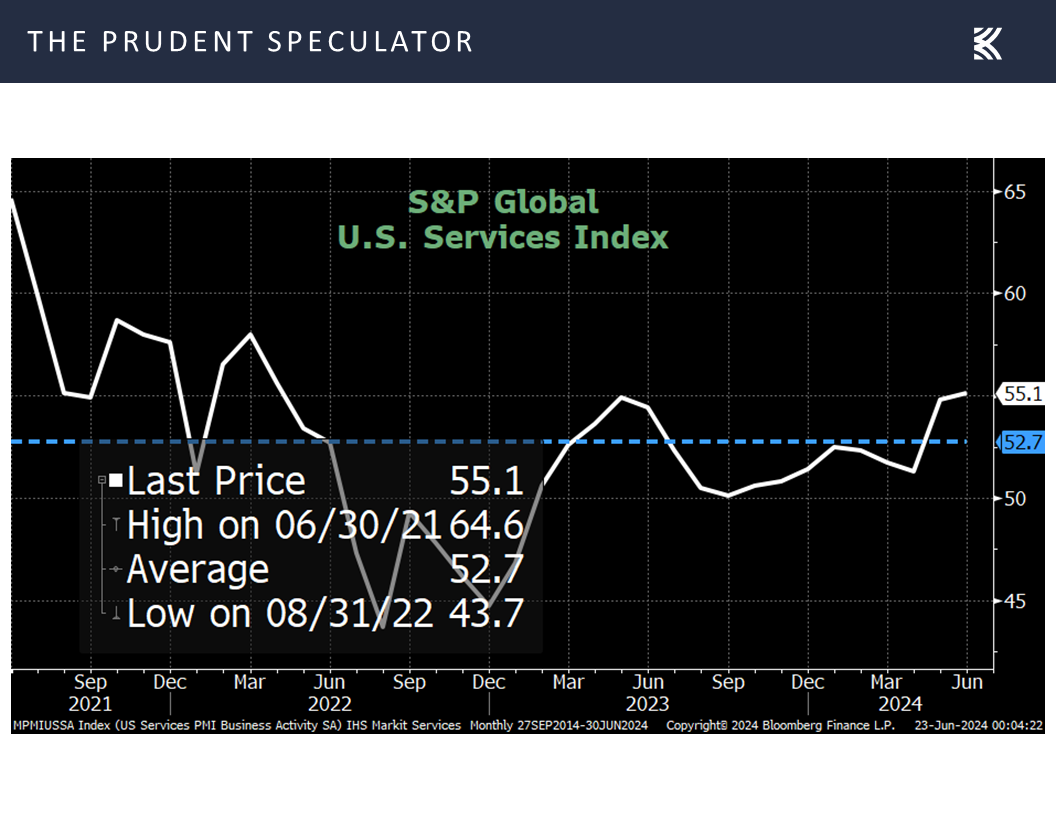

and the even-more-important U.S. services sector each topped estimates for June and improved from May’s respective readings.

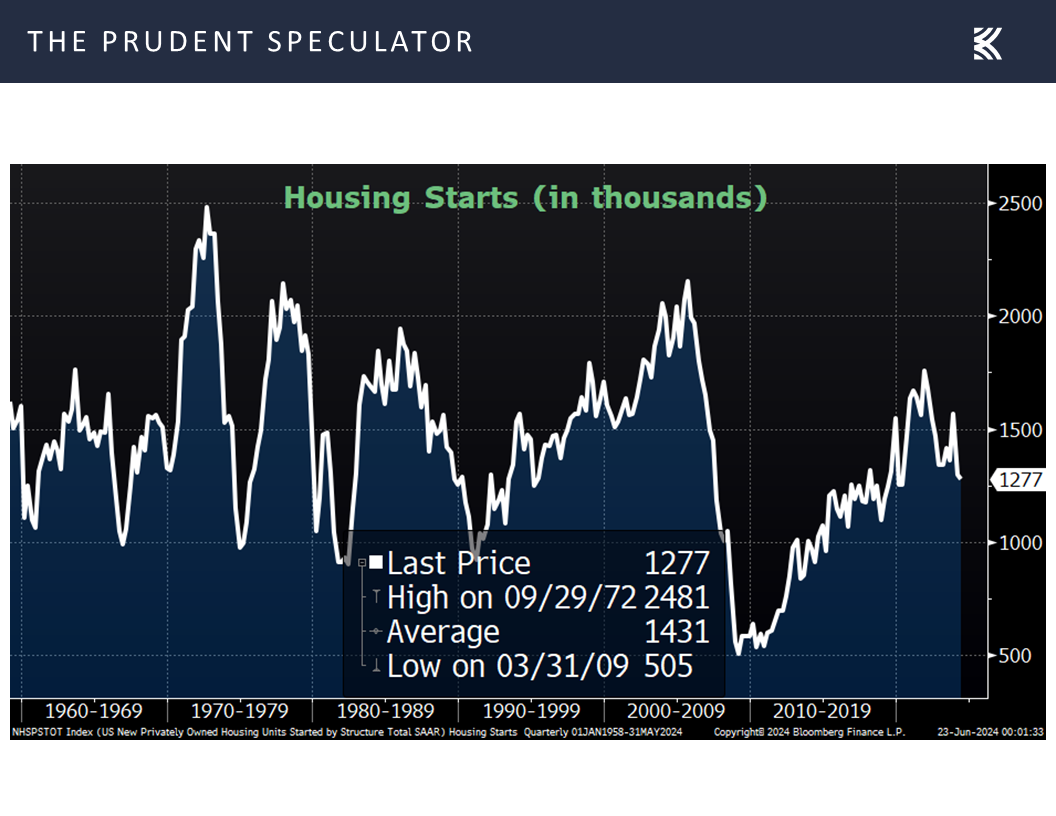

True, housing data was not exactly robust, be it housing starts in May,

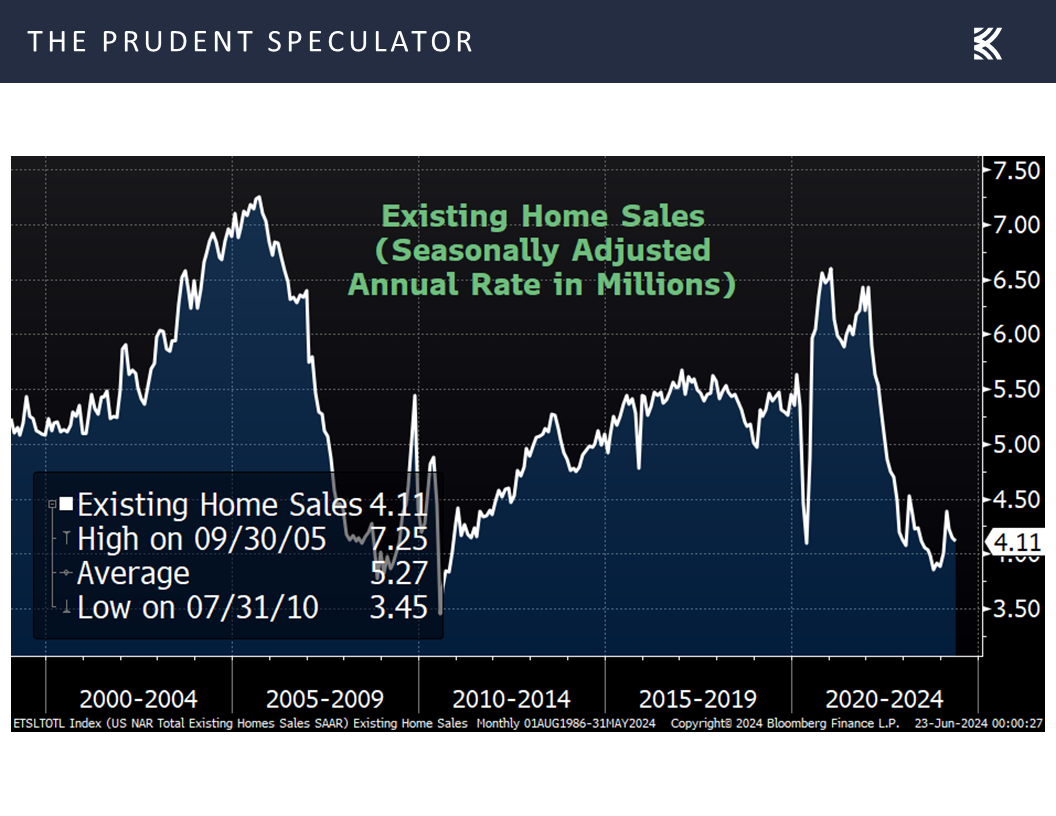

or existing home sales, also for May,

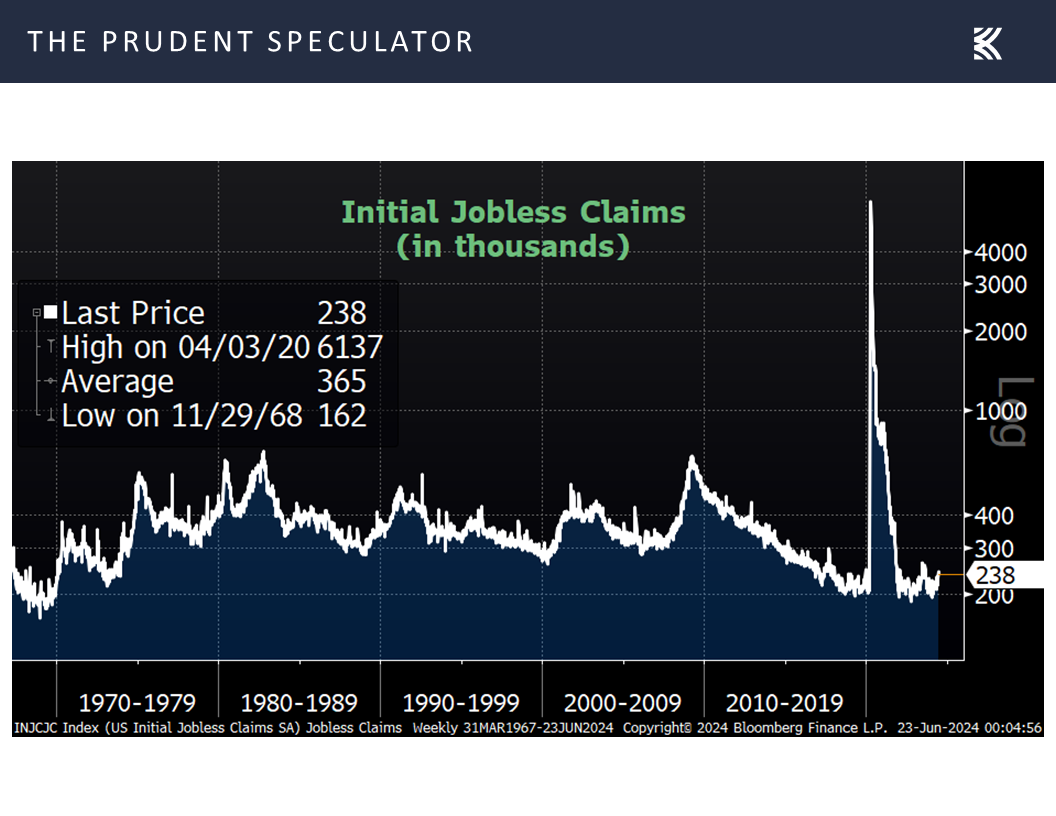

but the labor market remains healthy, with near-multi-generational lows in first time filings for unemployment benefits,

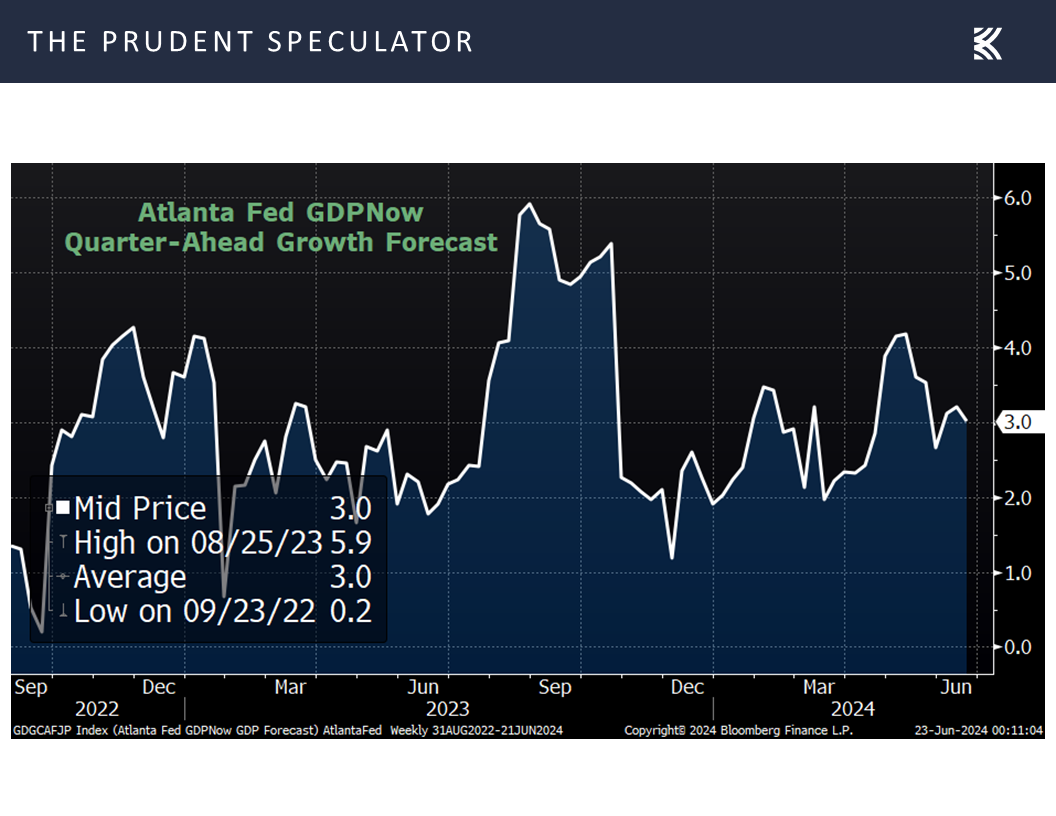

and the Atlanta Fed’s current forecast for real GDP growth this quarter resides at a robust 3.0%.

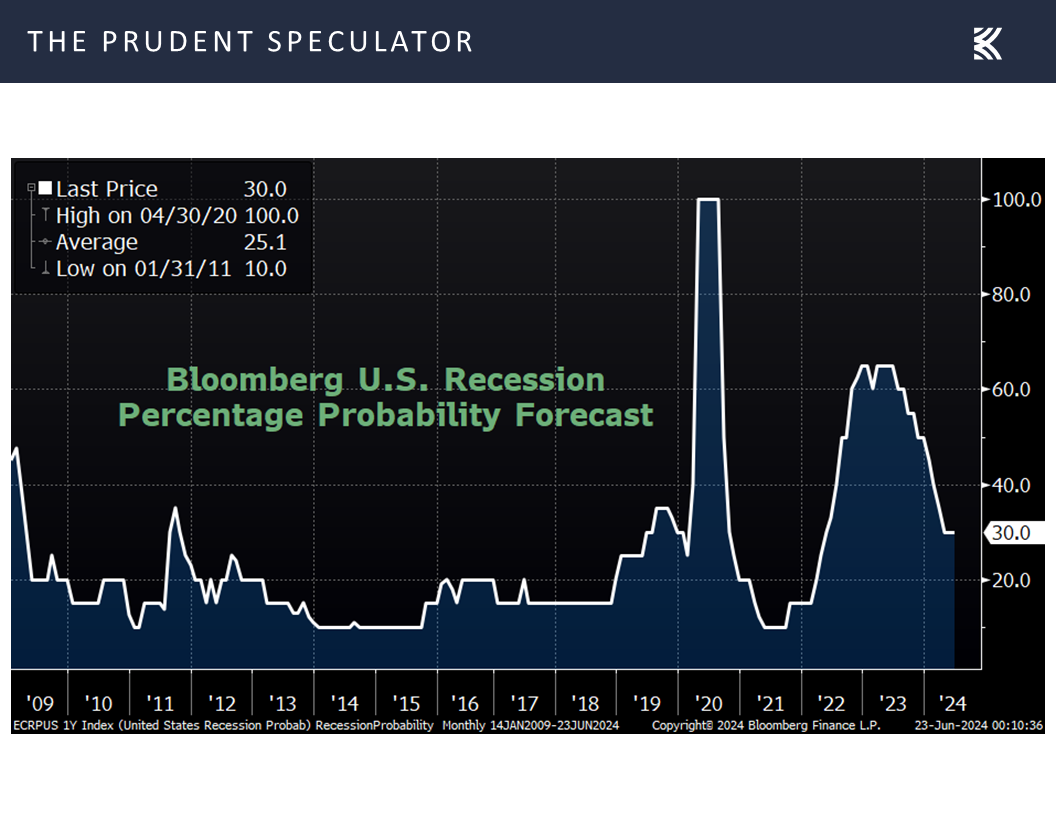

We might add that the odds of recession in the next 12 months, as tabulated by data provider Bloomberg, remain at a relatively low 30%,

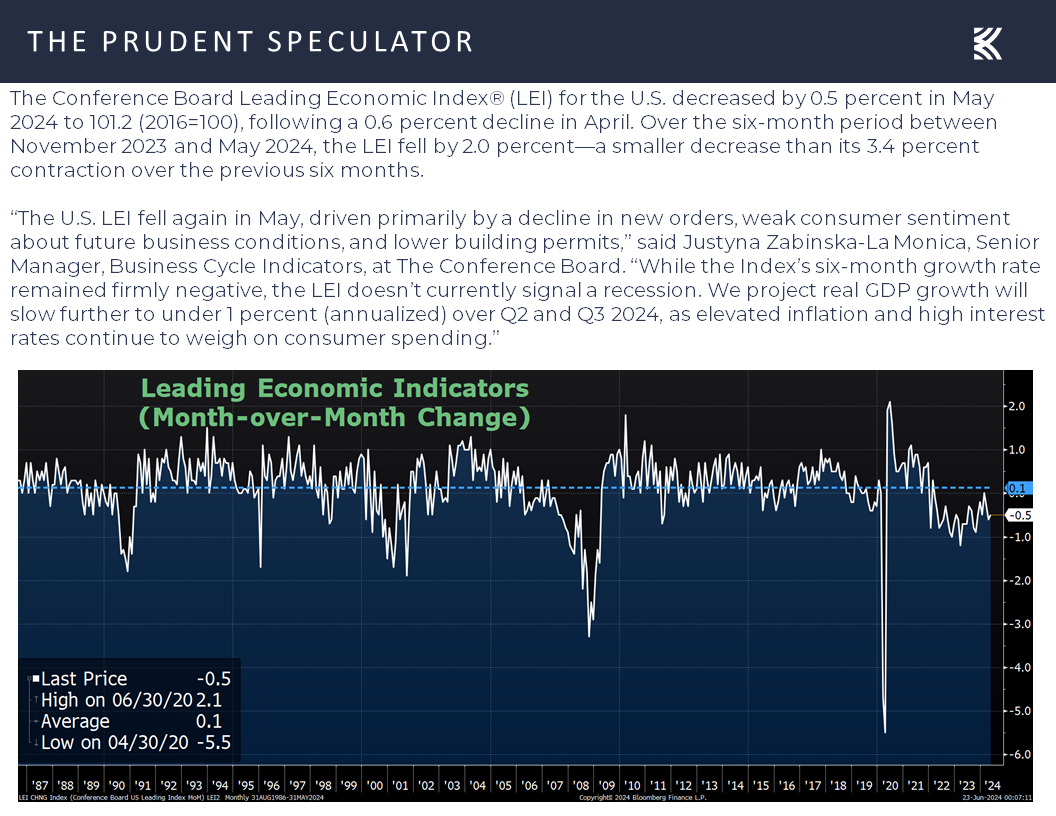

while even the keepers of the pessimistic Leading Economic Index do NOT think the 0.5% decline in May signals an economic contraction.

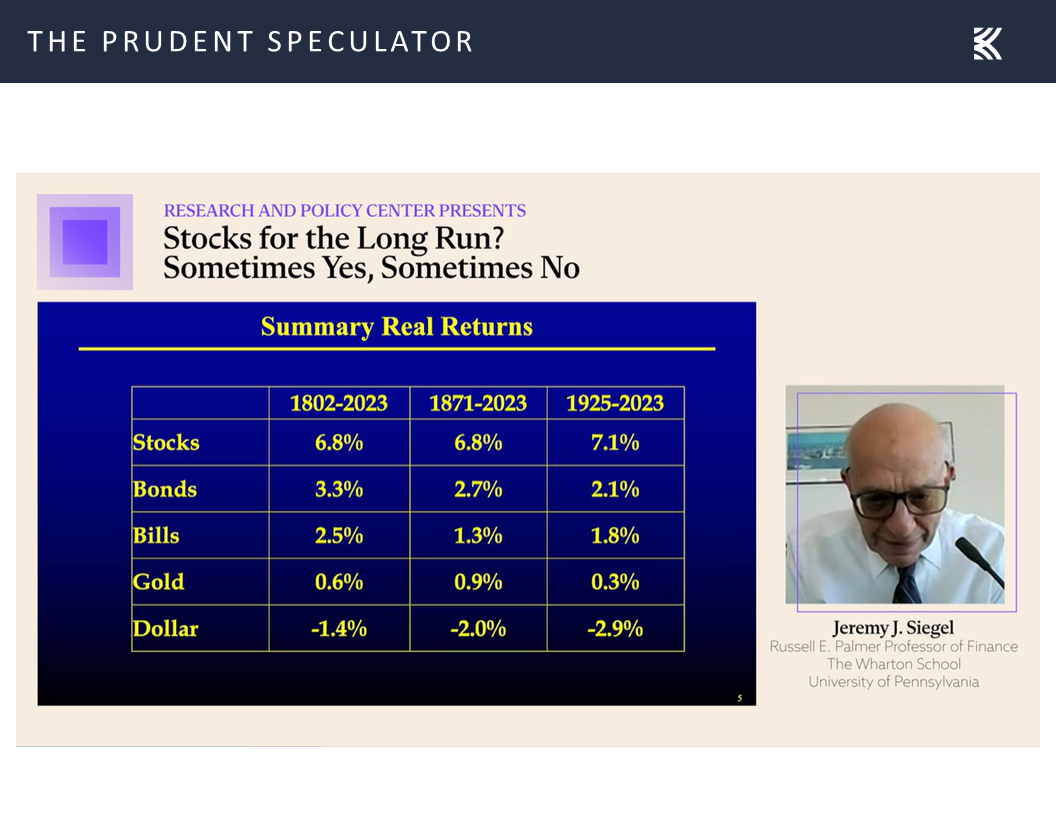

Jeremy Siegel – Stocks for the Long Run: 7% Average Annualized Real (Inflation-Adjusted) Returns

To be sure, anything can happen with stock prices going forward and we must always be braced for downside movements, but we see no reason to argue with Jeremy Siegel’s conclusion that equities are the place to be for those with a long-term time horizon, especially on a real (inflation-adjusted) basis.

Stock News – Updates on three stocks across three different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Economic Data, Volatility, Jeremy Siegel and more Stock News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Economic News, Volatility, Jeremy Siegel, and more Stock News. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Market Breadth – A Handful of Mega Caps Up but Most Stocks Down Last Week; Average Stock Down on the Year

Value – Tech Bubble History Lesson; R3K Value Index Very Inexpensive Relative to R3K Growth

Inflation – Lower-than-Expected CPI & PPI

Fed Econ Projections – 1 Rate Cut This Year; 4 Cuts Next Year

Interest Rates – Lower 10-Year Yield & Lower Expected Year-End Fed Funds Rate vs. the Prior Week

Econ News – Mixed Data; Fed & World Bank Each Projecting Decent U.S. Growth for ’24 and ’25

Earnings – Solid Growth Estimated in ’24 & ’25

Volatility – Scary Headlines & Plenty of Gyrations Along the Way but Long-Term Trend is Up

Stock News – Updates on AAPL, ORCL, AVGO, GM & ZBH

Market Breadth – A Handful of Mega Caps Up but Most Stocks Down Last Week; Average Stock Down on the Year

It was another fascinating week for equities with the Juneteenth demarcation line offering yet another reminder that it is a market of stocks and not simply a stock market. After all, the capitalization-weighted Russell 3000 index (R3K) performed very well (gaining 1.00%) over the first two days of the week, yet the average stock advanced only 0.08%. It was a complete reversal over the second two days of the week with the R3K dropping 0.33% and the average stock climbing 0.24%.

Value – Tech Bubble History Lesson; R3K Value Index Very Inexpensive Relative to R3K Growth

Interestingly, several of the big (from a contribution to return standpoint) early-week winners (generally A.I.-related), were the late-week losers…and vice versa, providing more evidence that a rising/retreating tide doesn’t lift/sink all boats. Such was the case following the bursting of the Dot.com Bubble when many of the high-flying Tech (Growth) stocks cratered and residents of the Value camp dramatically outperformed.

Of course, no two market environments are ever the same, and today’s stellar A.I. performers are business that drive substantial profits to the bottom line (and we own several), unlike many of the red-ink-laden Dot.com companies a quarter century ago, but we continue to sleep very well at night with the inexpensive valuation metrics (including our A.I. holdings) for our broadly diversified portfolios.

This is especially true given that the divergence in returns between the Growth and Value indexes that, despite the latter beating the former last week, is now at a greater extreme than in early-2000,

and considering the reasonable multiple of earnings relative to the historical mean for the Russell 3000 Value index,

with the earnings yield (inverse of the P/E ratio) also confirming that Value stocks are not overly expensive, unlike Growth stocks, versus where they have traded since 1995.

Volatility – Scary Headlines & Plenty of Gyrations Along the Way but Long-Term Trend is Up

That does not mean that it is up, up and away for the kind of stocks we favor, as there will always be disconcerting headlines with which we must contend,

not to mention bouts of sometimes frightening volatility, but the rewards for long-term-oriented investors have been terrific,

assuming they remember that the secret to success in stocks is not to get scared out of them. Indeed, as data from DALBAR in the table below show, time in the market has proven to trump market timing.

Long-Term Catalysts – EPS & GDP Have Grown Over Time

Of course, there is valid rationale for stocks providing handsome returns over time as corporate profits have grown,

as the U.S. economy has grown.

Econ News – Mixed Data; Growth Still Projected for ’24, ’25 and ’26

The question, then, is the outlook for growth going forward. The Federal Reserve, for its part, projects OK real (inflation-adjusted) GDP expansion in the 2% range for each of 2024, 2025 & 2026,

with a likely series of cuts in the Fed Funds rate helping to support the economy.

No doubt, there is plenty of disagreement about when those rate reductions may begin, and last week’s mixed economic numbers did not swing the pendulum much in either direction. For example, the Empire Manufacturing Index came in at -6.0 for June, but this gauge on the health of the factory sector in the New York area was better than estimated and an improvement from the -15.6 reading in May.

On the other hand, the Philadelphia Fed measure of East-Coast business output for June fell to 1.3, below projections and down from 4.5 in May.

The latest figures on retail sales also trailed estimates, advancing 0.1% in May, below forecasts calling for a 0.3% increase,

and the even-more-important U.S. services sector each topped estimates for June and improved from May’s respective readings.

True, housing data was not exactly robust, be it housing starts in May,

or existing home sales, also for May,

but the labor market remains healthy, with near-multi-generational lows in first time filings for unemployment benefits,

and the Atlanta Fed’s current forecast for real GDP growth this quarter resides at a robust 3.0%.

We might add that the odds of recession in the next 12 months, as tabulated by data provider Bloomberg, remain at a relatively low 30%,

while even the keepers of the pessimistic Leading Economic Index do NOT think the 0.5% decline in May signals an economic contraction.

Jeremy Siegel – Stocks for the Long Run: 7% Average Annualized Real (Inflation-Adjusted) Returns

To be sure, anything can happen with stock prices going forward and we must always be braced for downside movements, but we see no reason to argue with Jeremy Siegel’s conclusion that equities are the place to be for those with a long-term time horizon, especially on a real (inflation-adjusted) basis.

Stock News – Updates on three stocks across three different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.