The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Economic Outlook, Federal Reserve, Earnings, Valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Week in Review – May Off to a Good Start

Fed Meeting – Rates Unchanged

Historical Evidence – Higher Fed Funds Rate & Rising Interest Rates Not Negatives for Stocks, On Average

Econ Outlook – Powell & OECD Upbeat

Earnings – Solid Growth Estimated in ’24 & ’25

Econ Stats – Not too Hot, Not too Cold

Volatility – Ups and Downs But Long-Term Trend is Up

Valuations – Inexpensive Metrics for TPS Portfolio

Sentiment – Bull-Bear Spread Back to Normal

Stock News – Updates on JNJ, PHG, VWAPY, MMM, GLW, LEG, CVS, PFE, NYCB, QCOM, BHE, WRK, MRNA, AMGN, FDP & AAPL

Week in Review – May Off to a Good Start

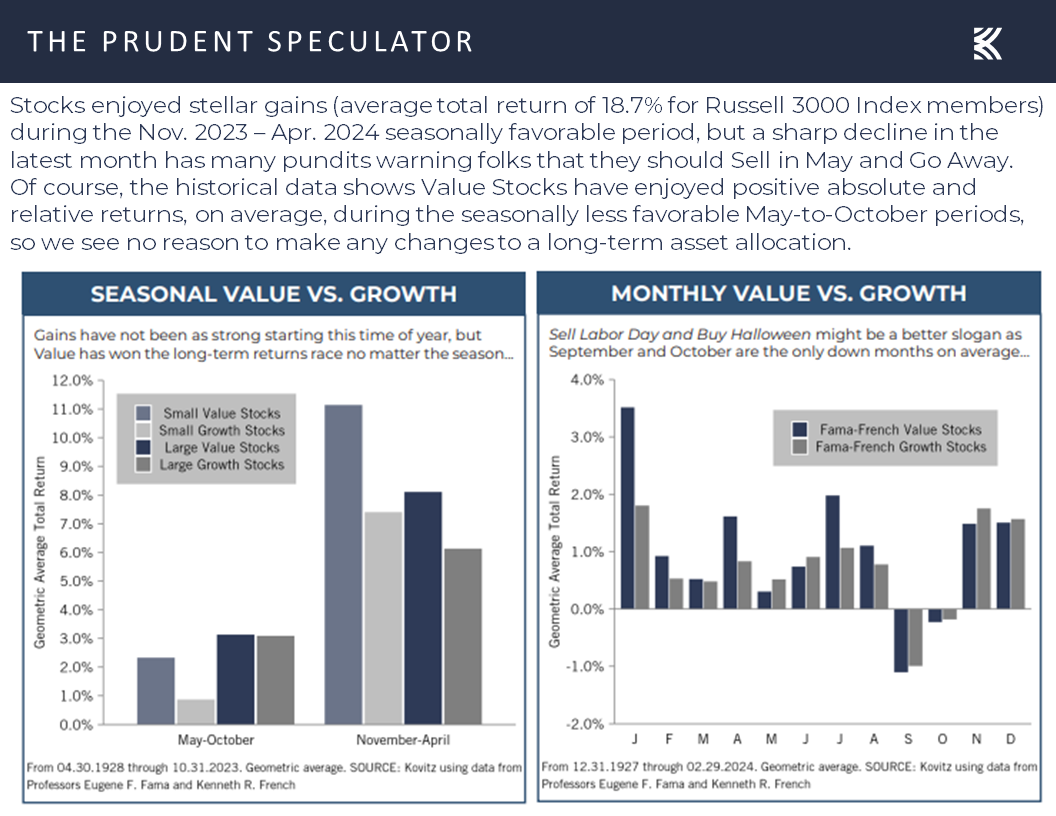

The seasonally less favorable (but not unfavorable, on average) May – October period,

Fed Meeting – Rates Unchanged

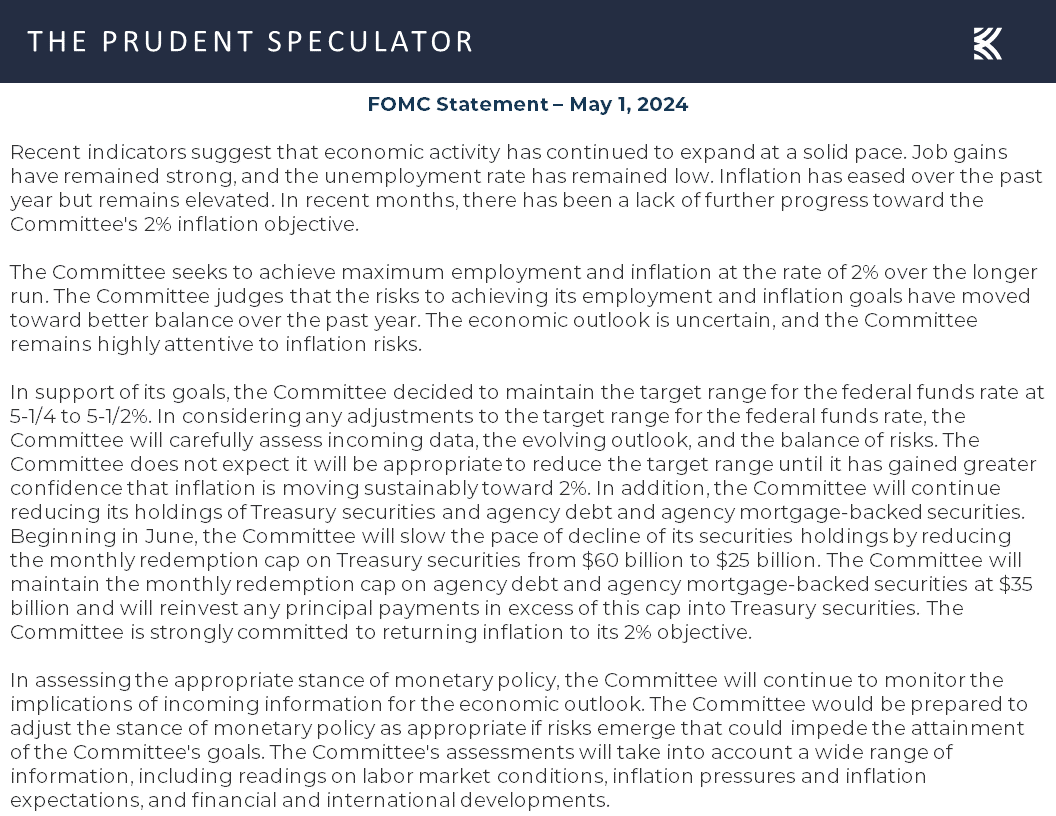

started on a high note, following the announcement on May 1 that the Federal Reserve would leave its target for the Fed Funds rate unchanged at a range of 5.25% to 5.50%,

and Jerome H. Powell’s response in his Press Conference that same day to the query: “I wonder, obviously Michelle Bowman has been saying that there is a risk that rates may need to increase further, although it’s not her baseline outlook, I wonder if you see that as a risk as well, and if so, what change in conditions would merit considering raising rates at this point?”

The Fed Chair replied, “So I think it’s unlikely that the next policy rate move will be a hike. I’d say it’s unlikely. You know, our policy focus is really what I just mentioned, which is how long to keep policy restrictive. You ask what would it take, I think we’d need to see persuasive evidence that our policy stance is not sufficiently restrictive to bring inflation sustainably down to 2 percent over time. That’s not what we think we’re seeing, as I mentioned, but something like that is what it would take. We’d look at the totality of the data and answer that question that would include inflation, inflation expectations, and all the other data too.”

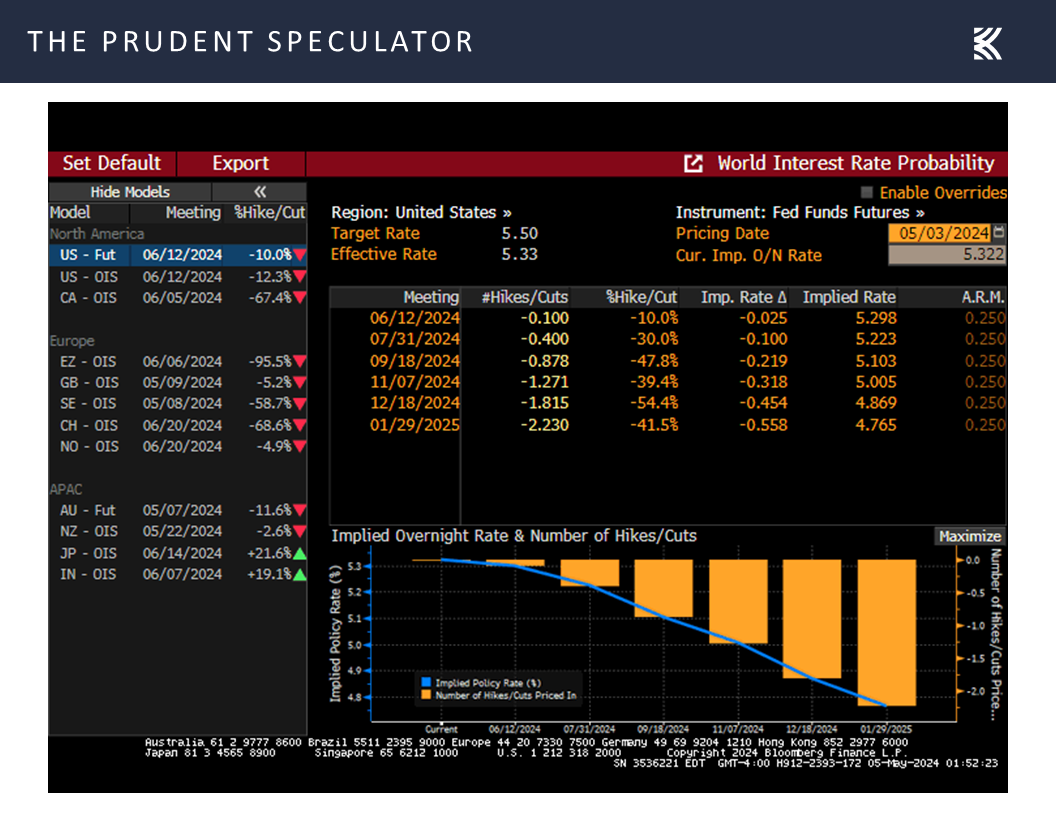

Given that some traders were worried that a rate hike could be on the table, the more dovish comments led to a sizable drop in the year-end betting in the Fed Funds futures market to a rate of 4.87% from 4.99% the week prior,

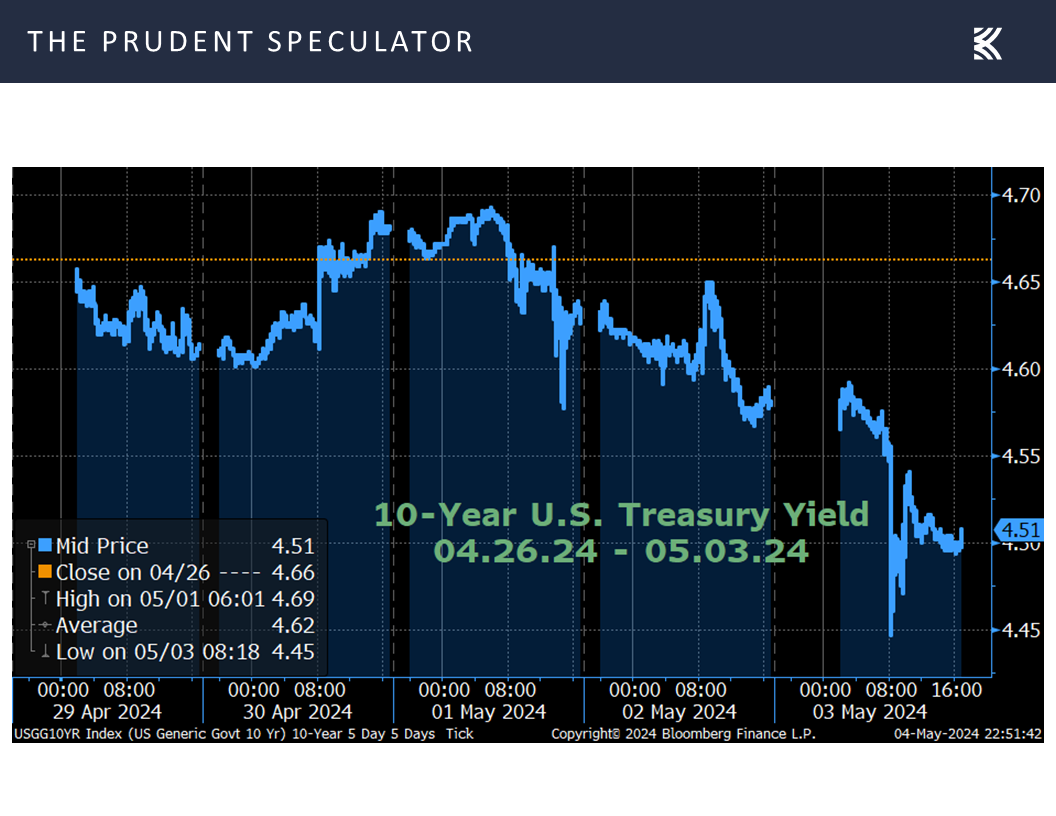

and contributed to a rally in government bonds with the yield on the 10-Year U.S. Treasury dropping from nearly 4.7% pre-Fed to near 4.5% by week’s end.

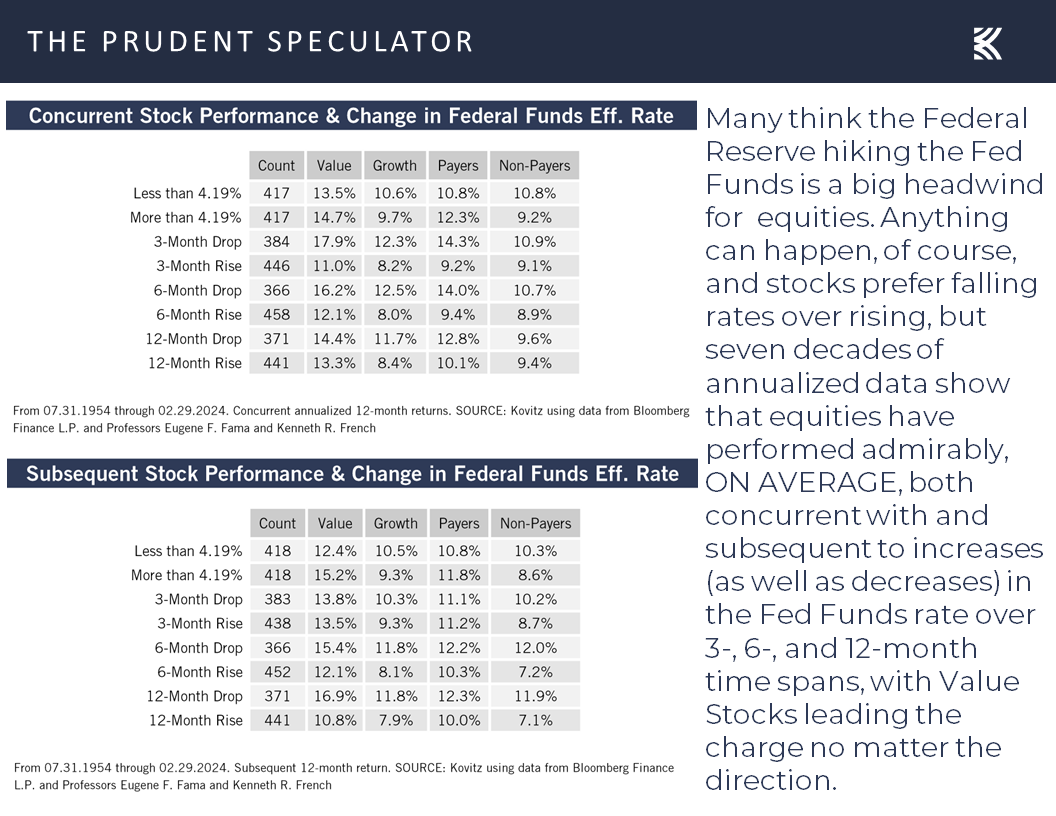

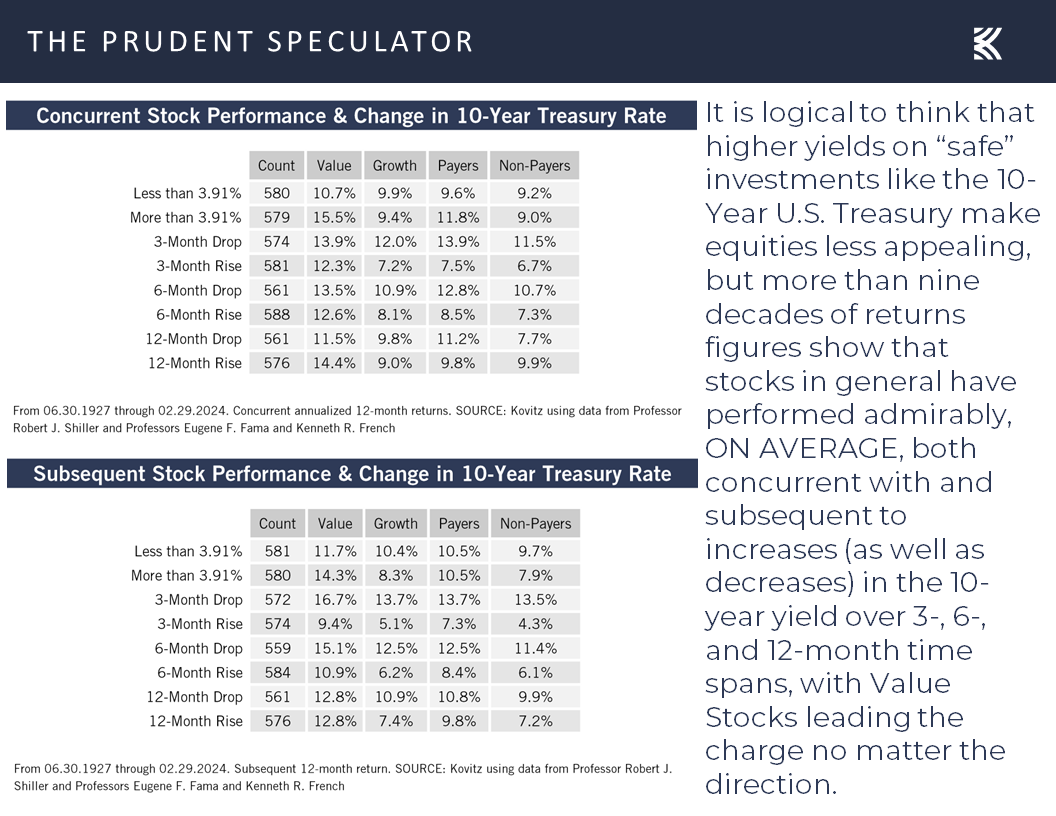

Historical Evidence – Higher Fed Funds Rate & Rising Interest Rates Not Negatives for Stocks, On Average

Of course, history shows that investors should stick with stocks, especially Value, whether the Fed Funds rate is high or low or whether it is rising or falling,

with the same also the case for the 10-Year Treasury yield,

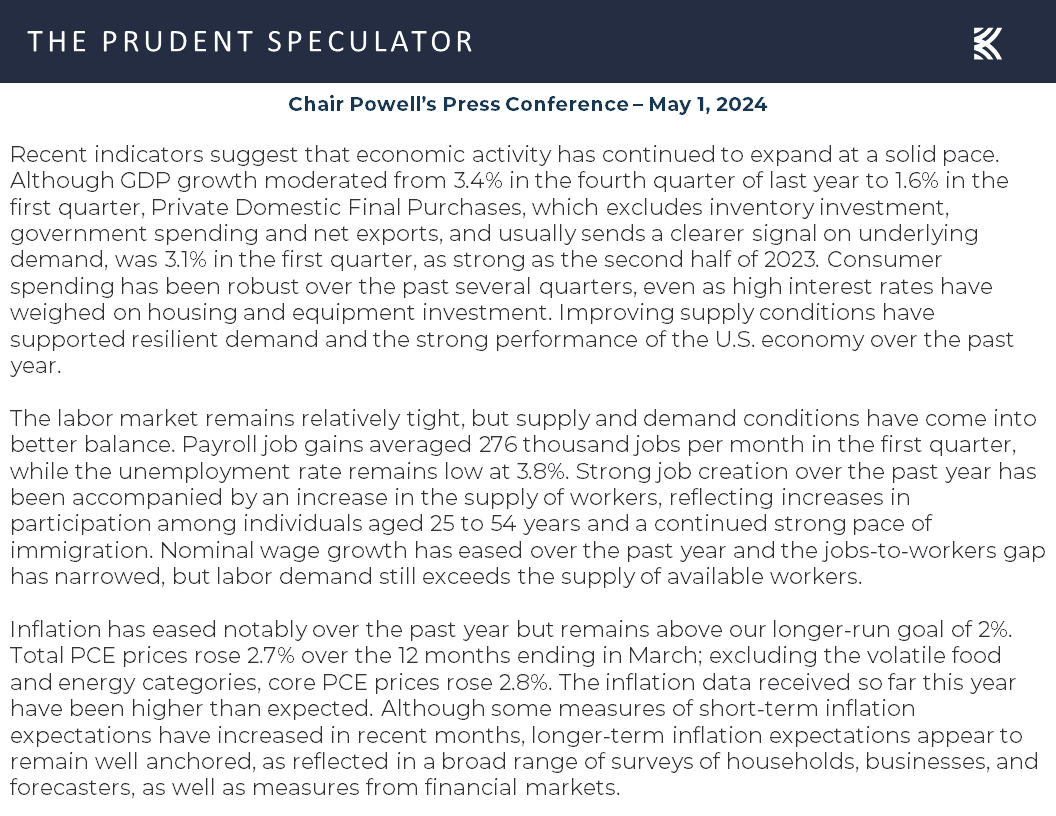

Econ Outlook – Powell & OECD Upbeat

but traders evidently were pleased that Chair Powell in his prepared Press Conference remarks was relatively upbeat on the health of the U.S. economy,

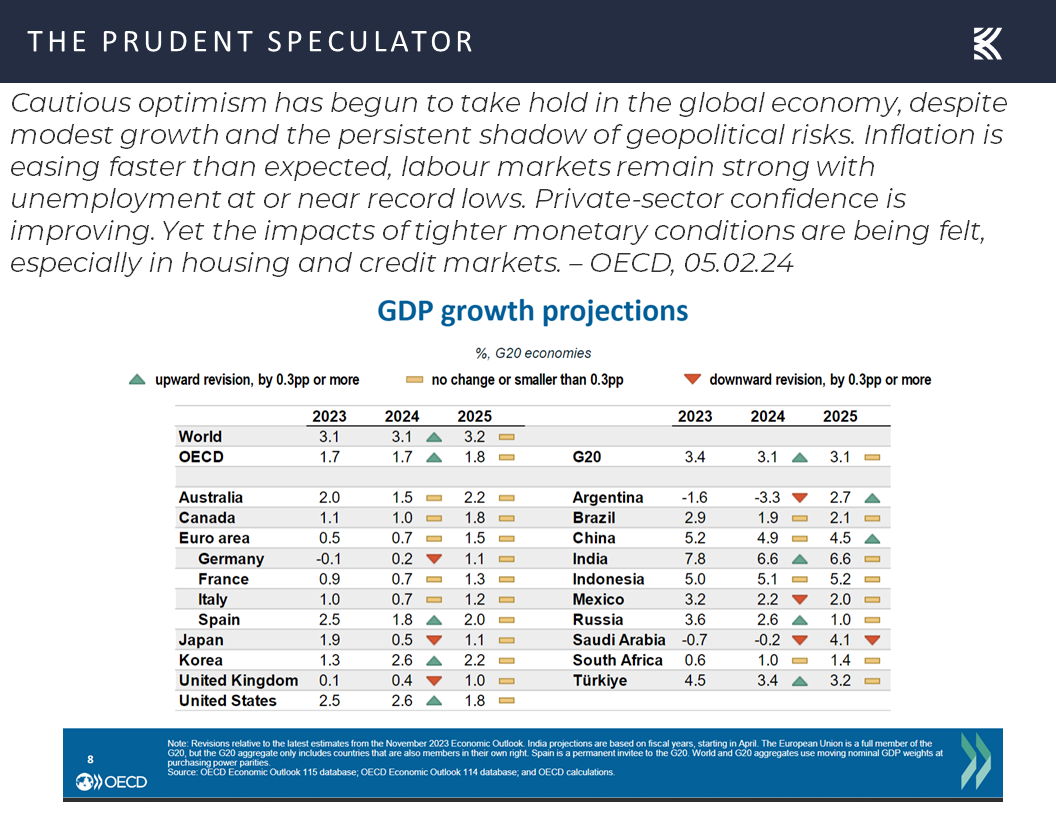

…while the Organisation for Economic Co-operation and Development was cautiously optimistic on May 2 in its outlook for domestic and global GDP growth.

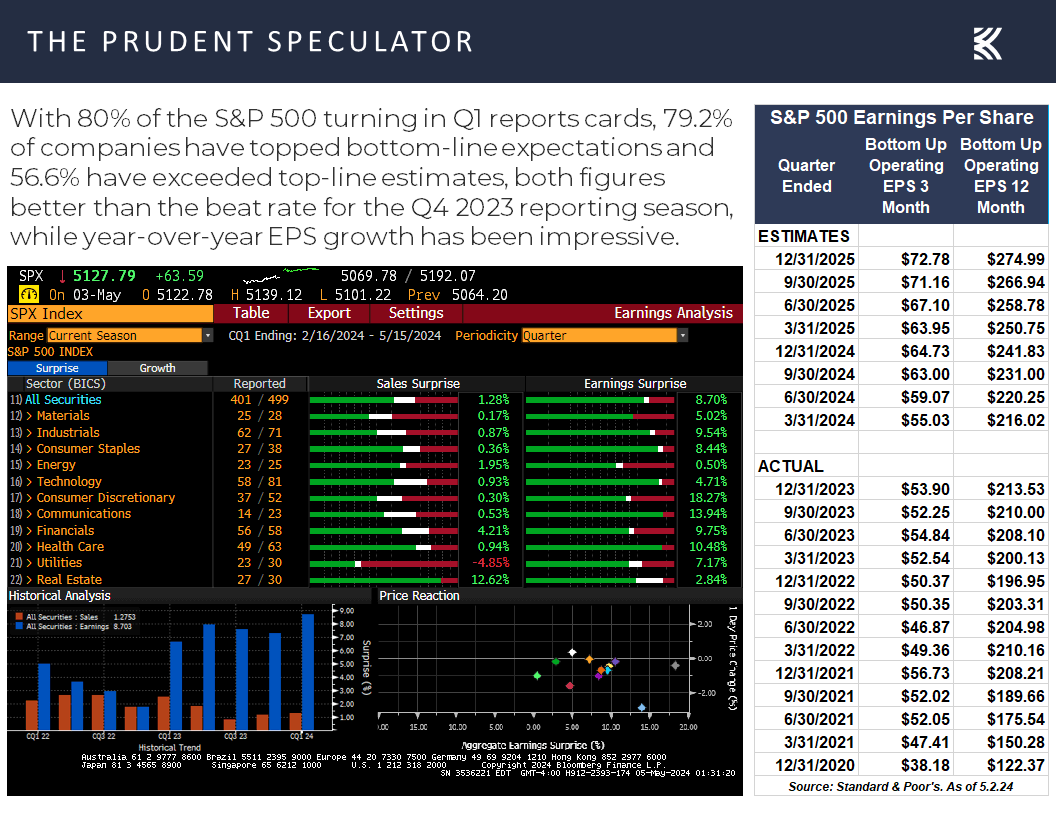

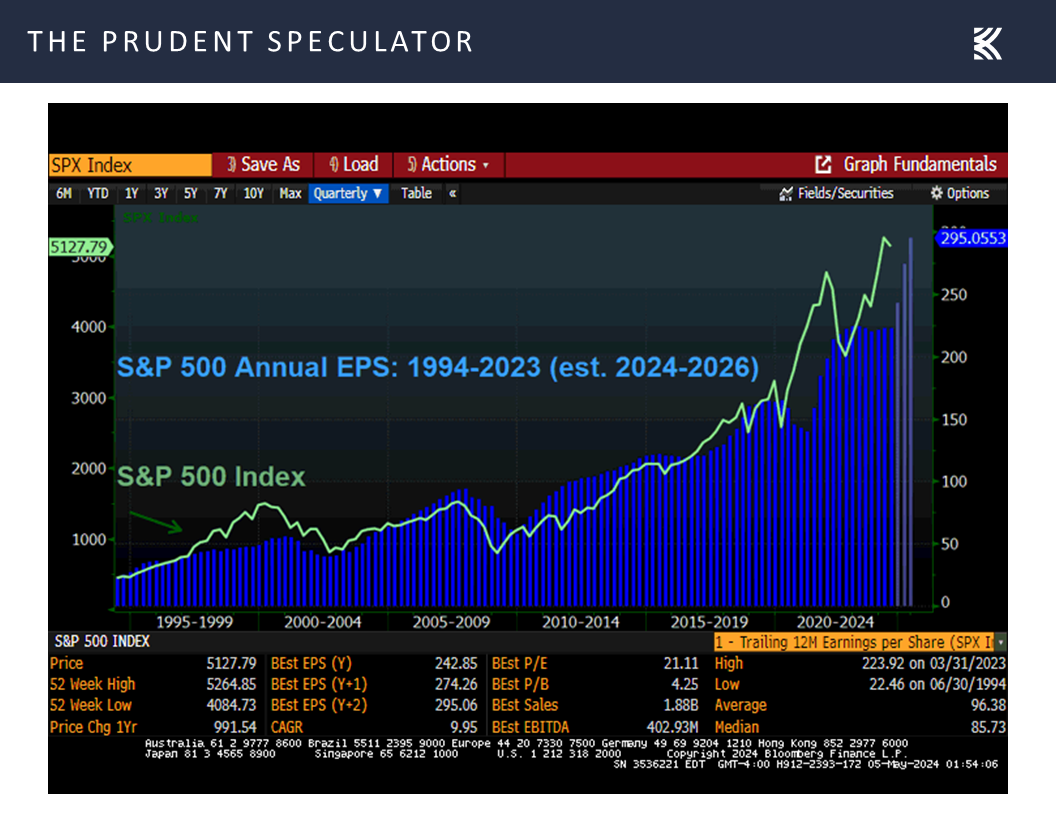

Earnings – Solid Growth Estimated in ’24 & ’25

No doubt, a solid economic backdrop is a positive for corporate profits and estimates for EPS growth this year and next presently are robust. True analysts are often overly rosy in their projections, but Q1 earnings reports have beat expectations at a better-than-79% clip,

and history shows that stock prices generally follow profits higher.

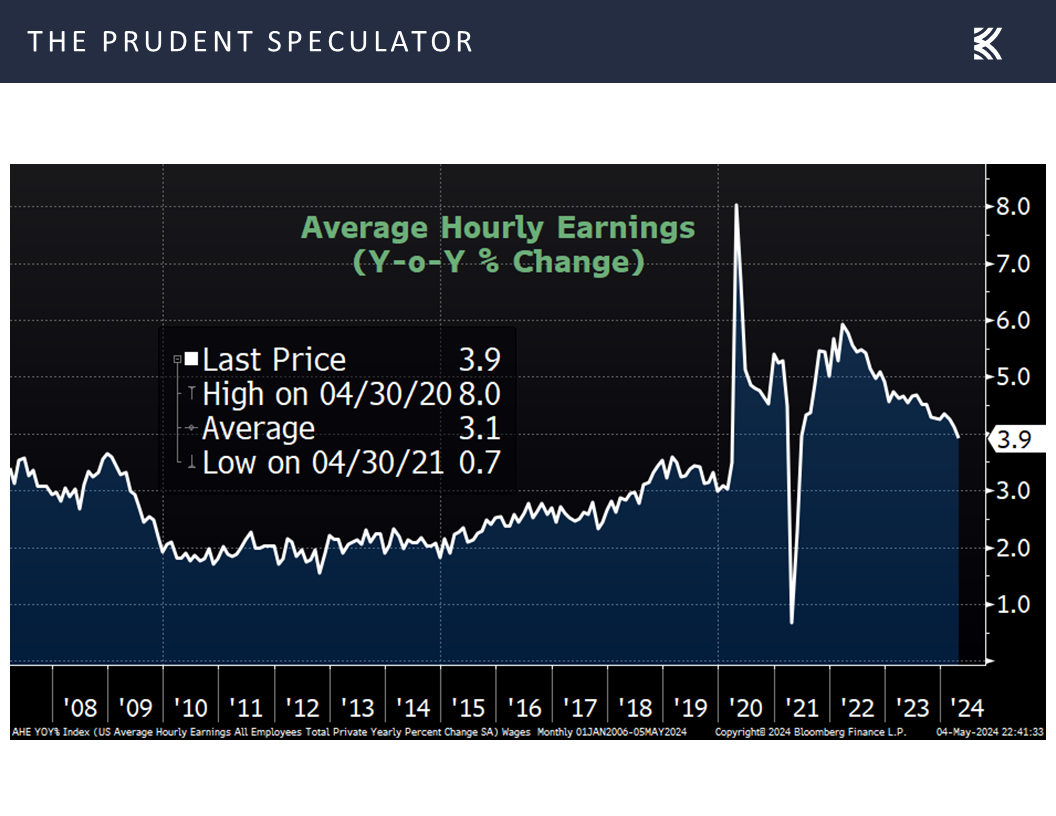

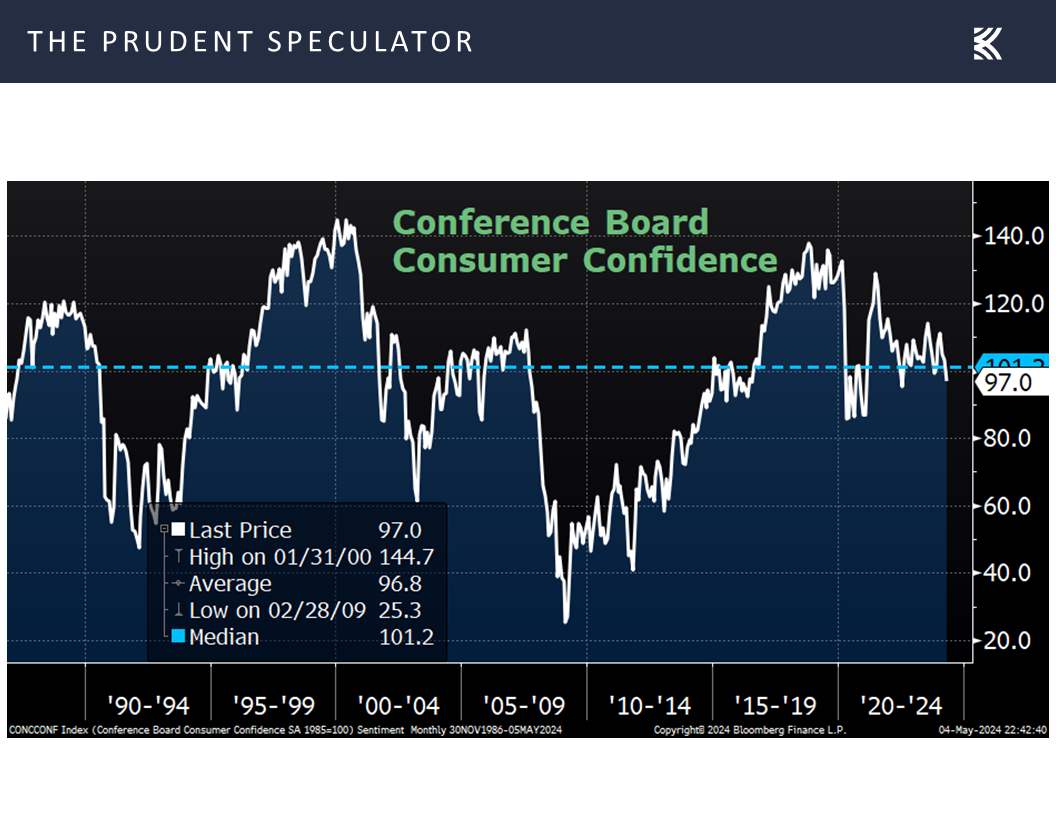

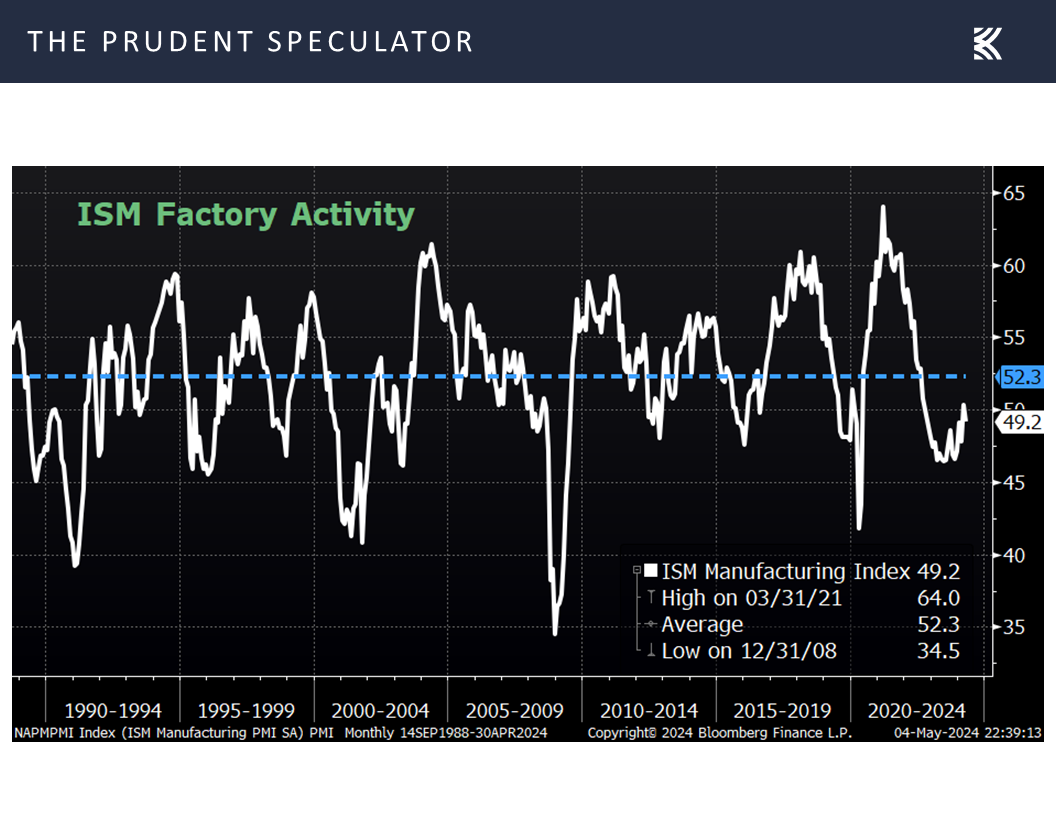

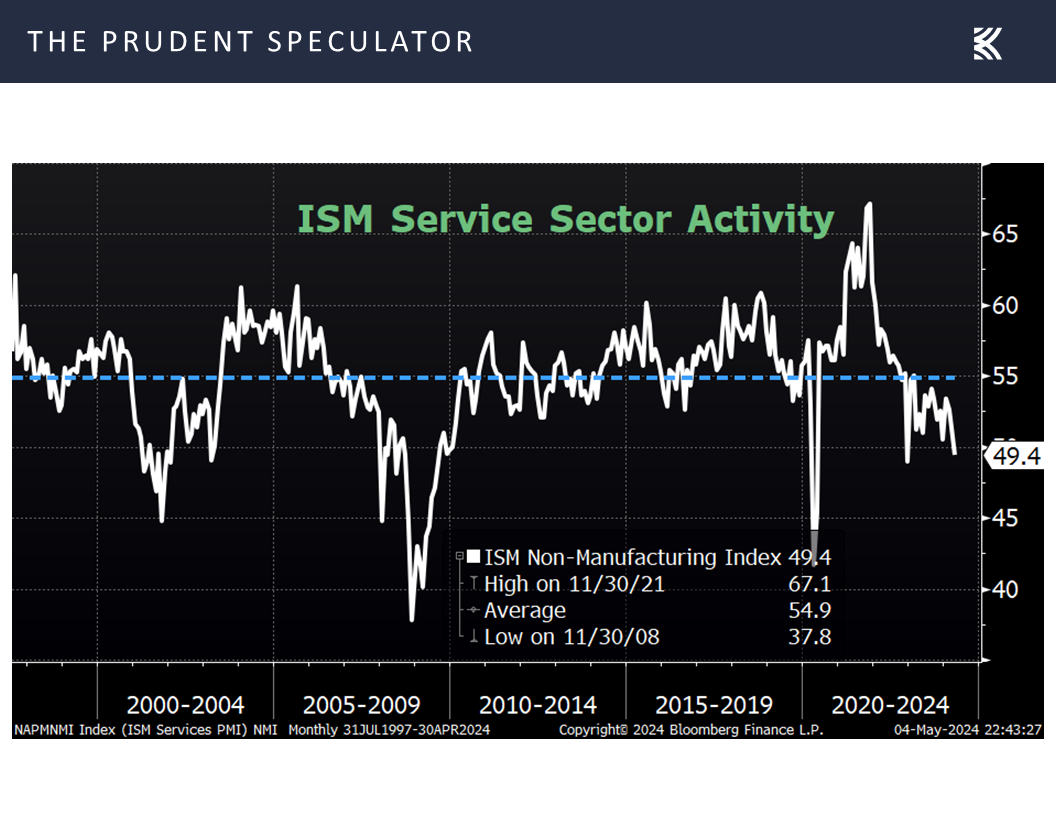

Econ Stats – Not too Hot, Not too Cold

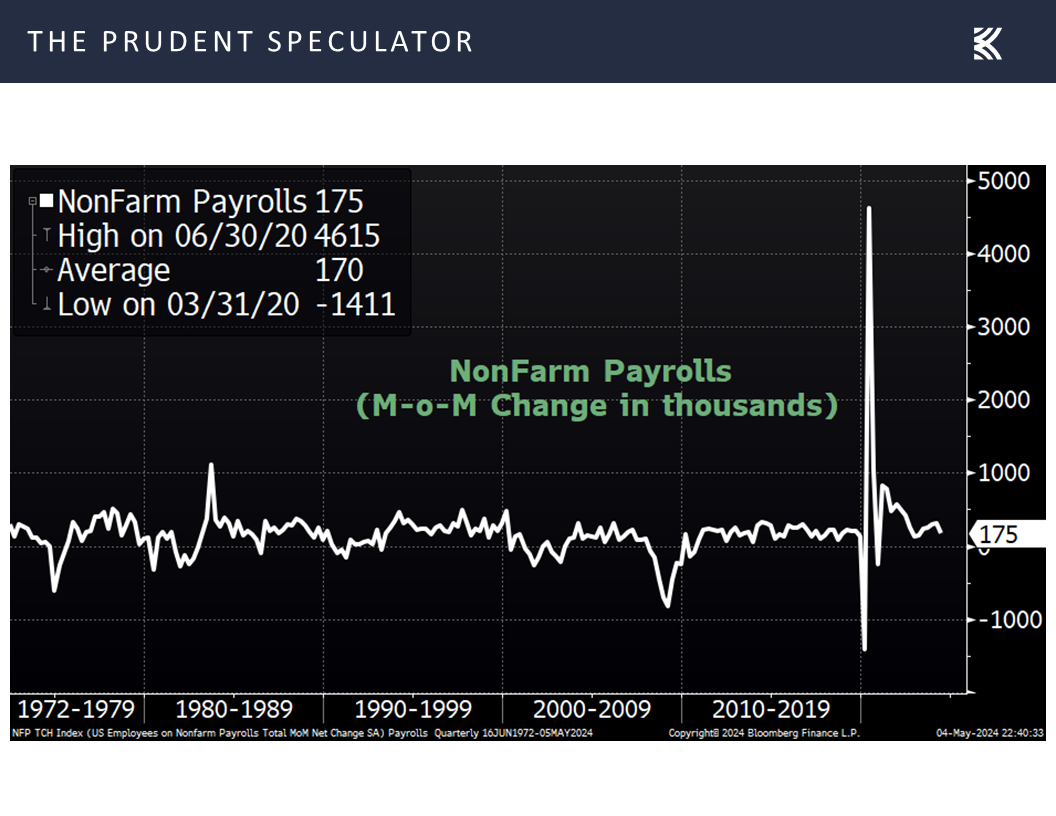

To be sure, it is a delicate dance these days between those who would prefer a strong economy and those who would like Federal reserve rate cuts, so not-too-cold and not-too-hot statistics are generally greeted with enthusiasm, as was the case in response to Friday’s big jobs report. The Labor Department saw a still healthy, but weaker-than-expected, 175,000 new payrolls created,

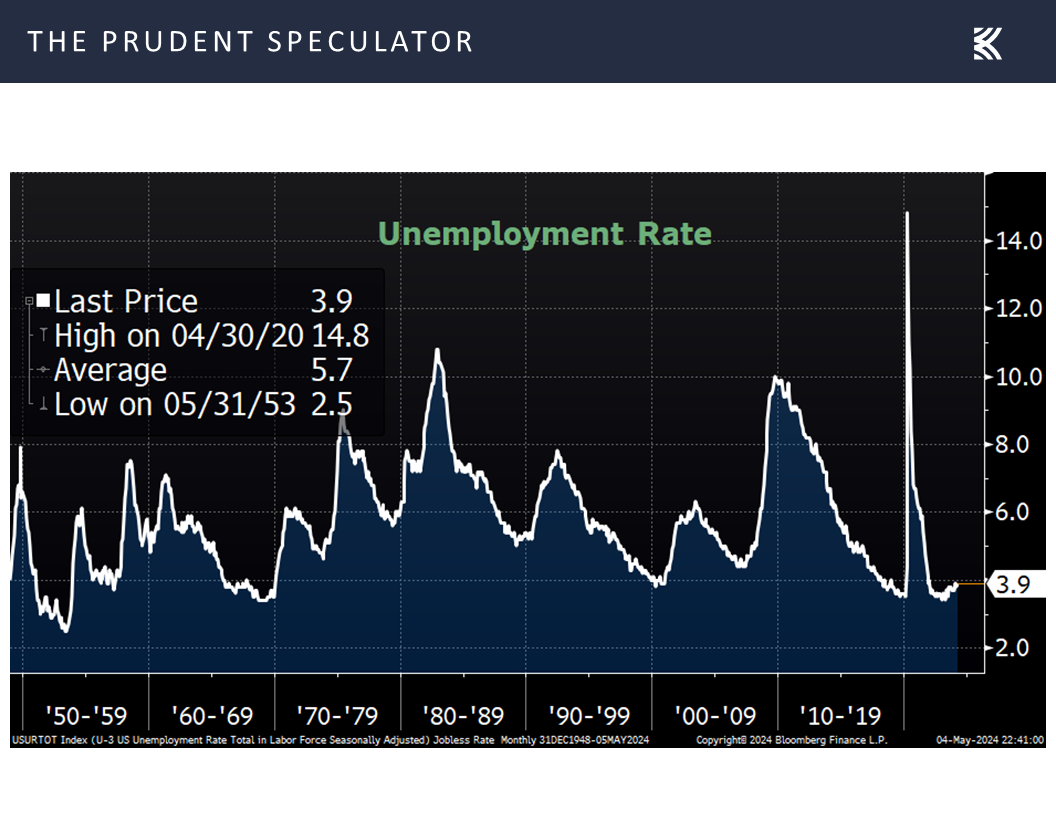

while the unemployment rate ticked up to 3.9%,

and growth in average hourly earnings slowed to 3.9%, down from 4.1% in March, helping temper fears of higher inflation.

Yes, other economic data points came in weaker than expected, like the Conference Board’s Consumer Confidence Index for April (97.0 vs. 104.0 est.),

the Institute for Supply Management’s (ISM) measure of activity in the factory sector in April dropping to 49.2 (50.0 est.),

and the ISM Service Sector Non-Manufacturing Index coming in at 49.4 for April, compared to the consensus forecast of 52.0.

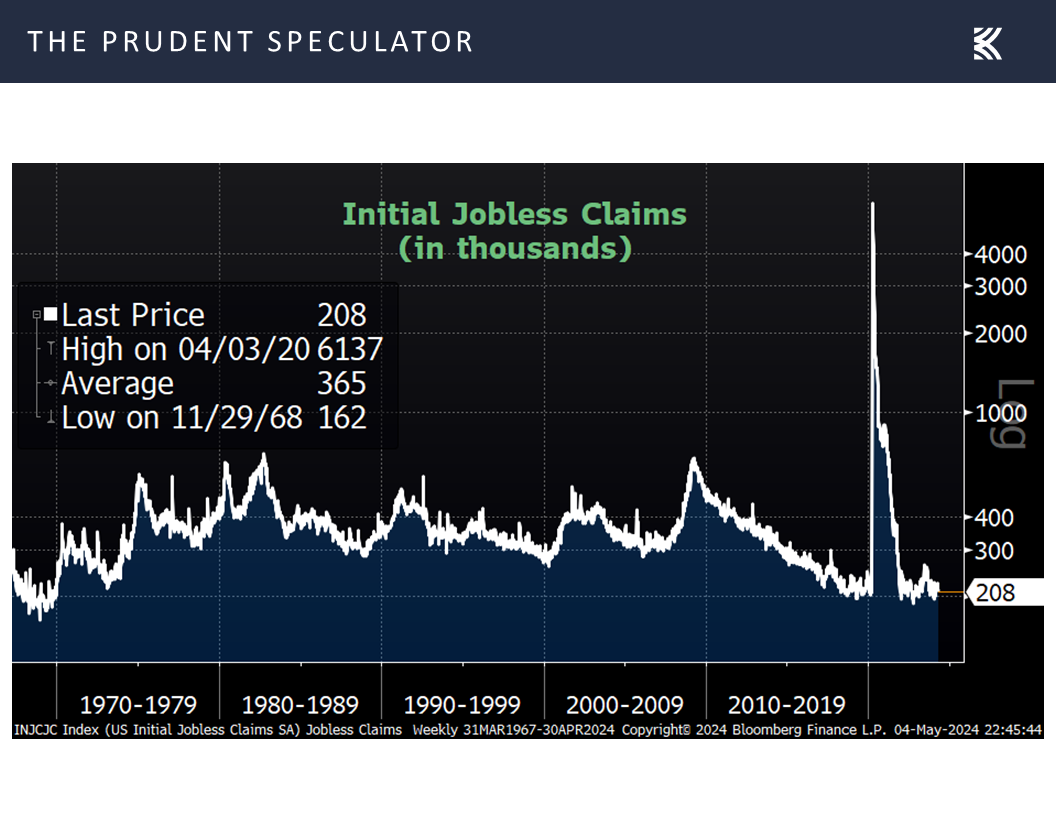

However, first-time filings for unemployment benefits in the latest week dipped to a very low 208,000,

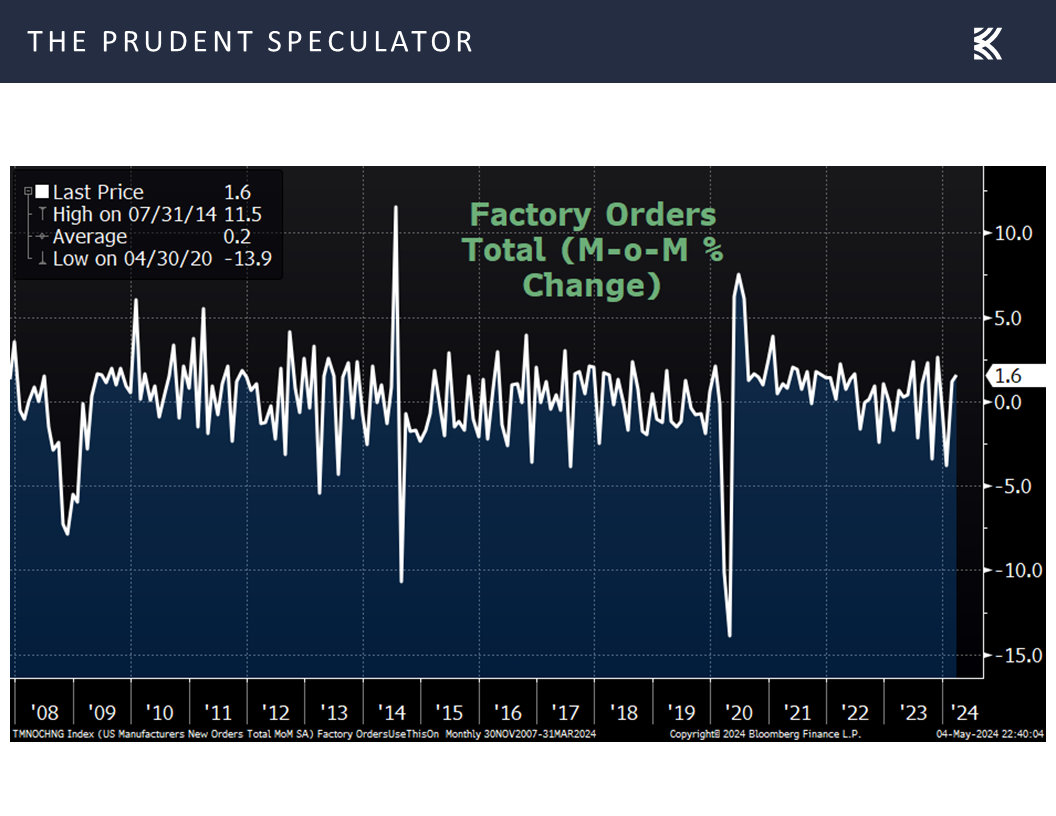

and factory orders for March rose by a better-than-average 1.6%,

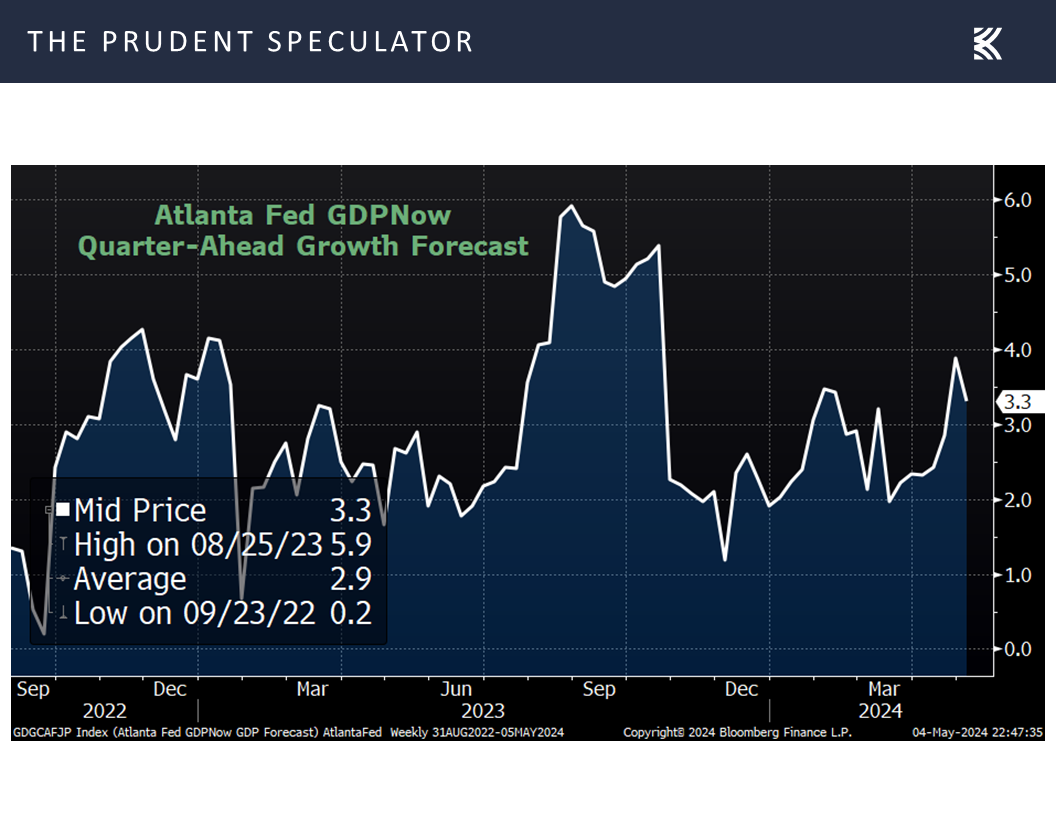

while the latest Atlanta Fed projection for real (inflation-adjusted) Q2 U.S. GDP Growth stood at a rich 3.3%,

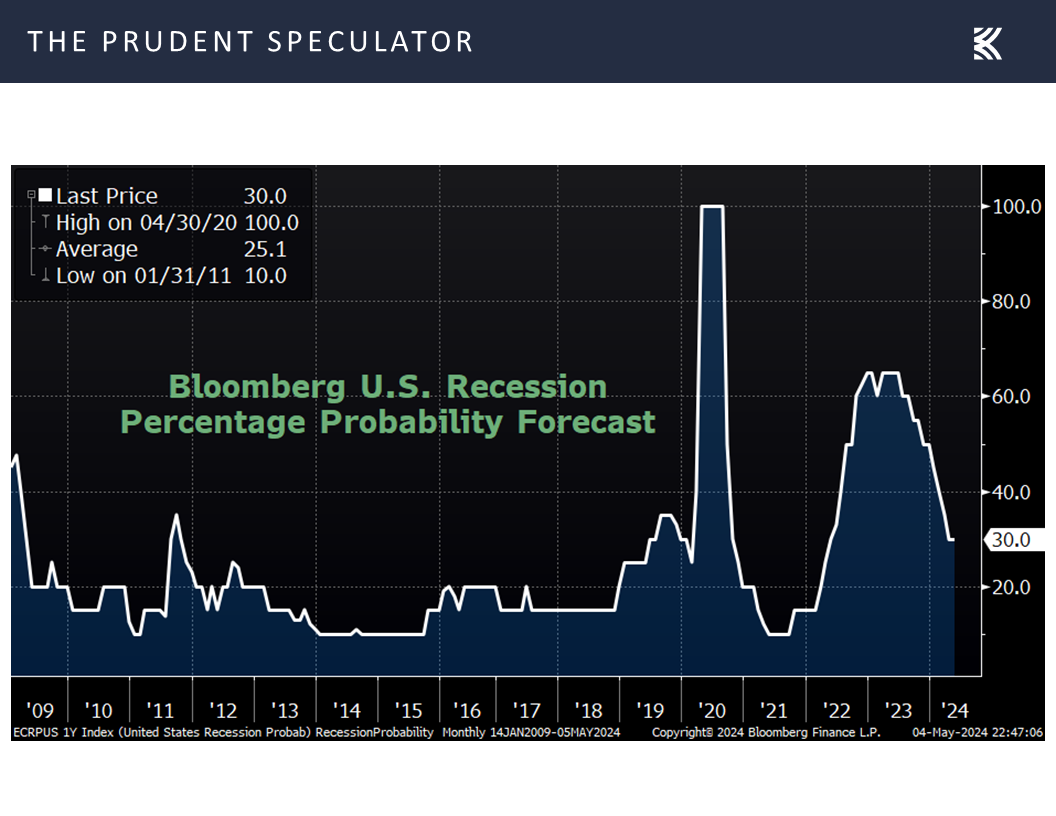

and the odds of recession in the next 12 months, as tabulated by Bloomberg, remained at a relatively low 30%.

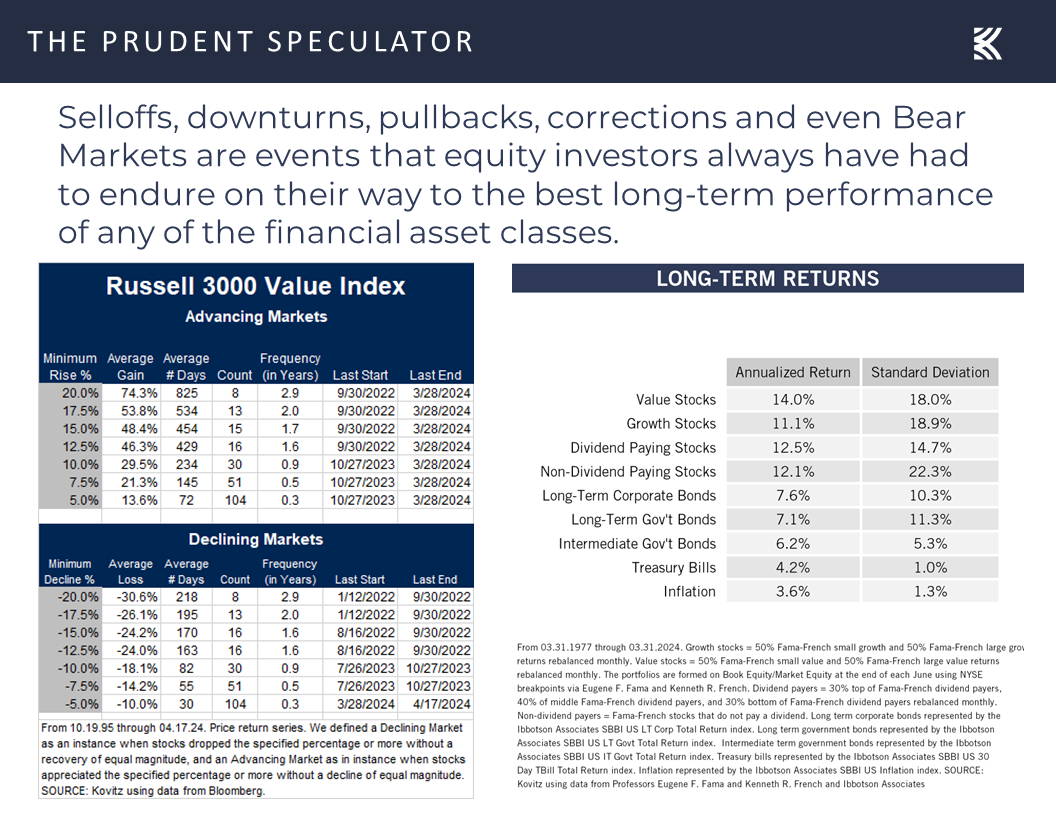

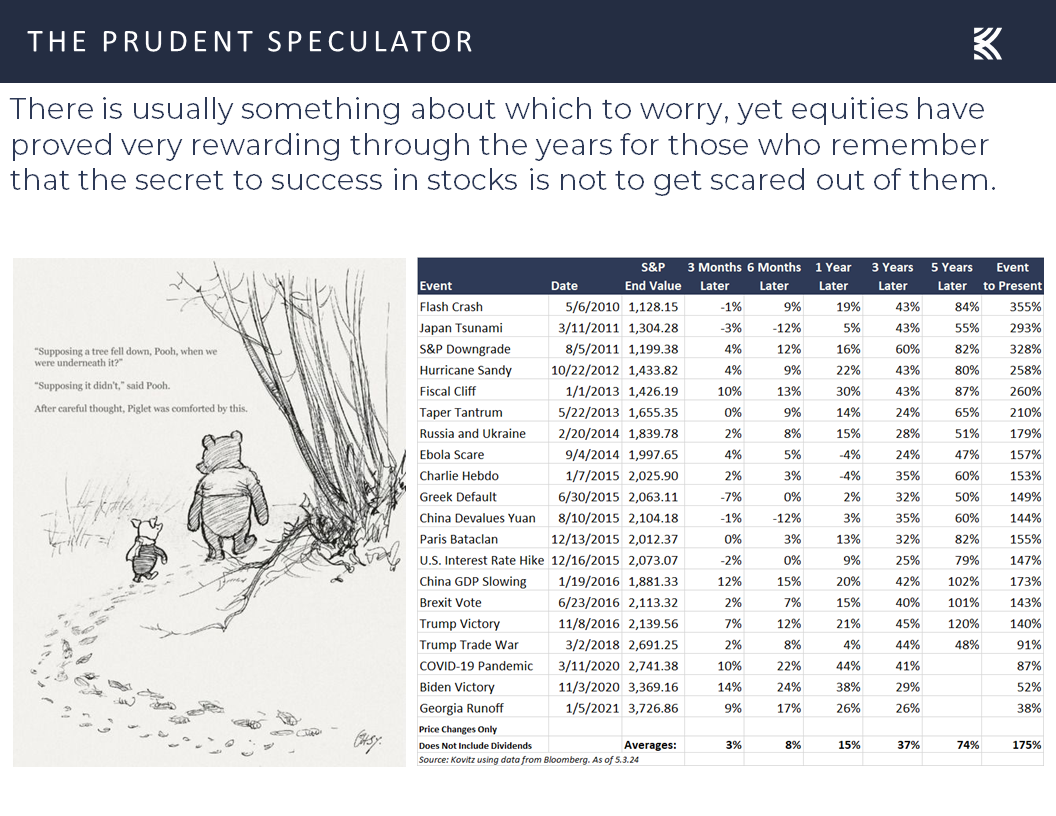

Volatility – Ups and Downs But Long-Term Trend is Up

We always are braced for downside volatility as selloffs, corrections and even Bear Markets are part of the investment equation, but we remain confident that equities will continue to provide handsome rewards,

to those who remember that time in the market trumps market timing.

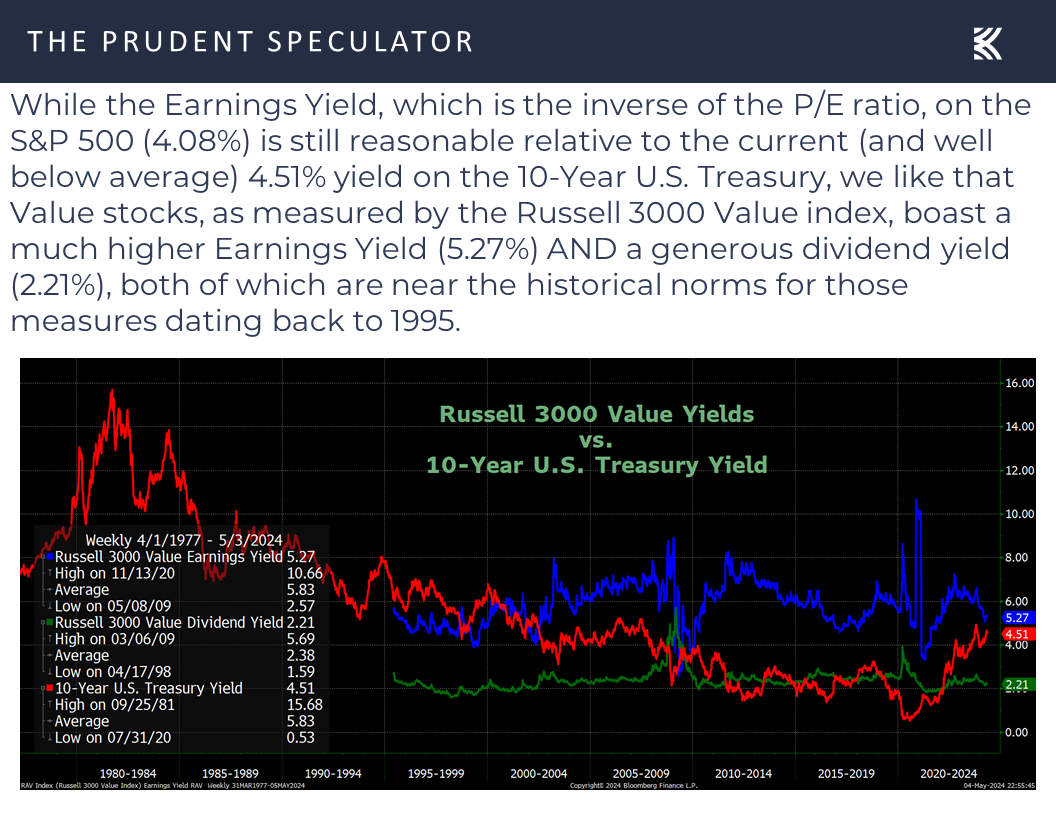

Further, we remain of the opinion that Value stocks in general are reasonably priced,

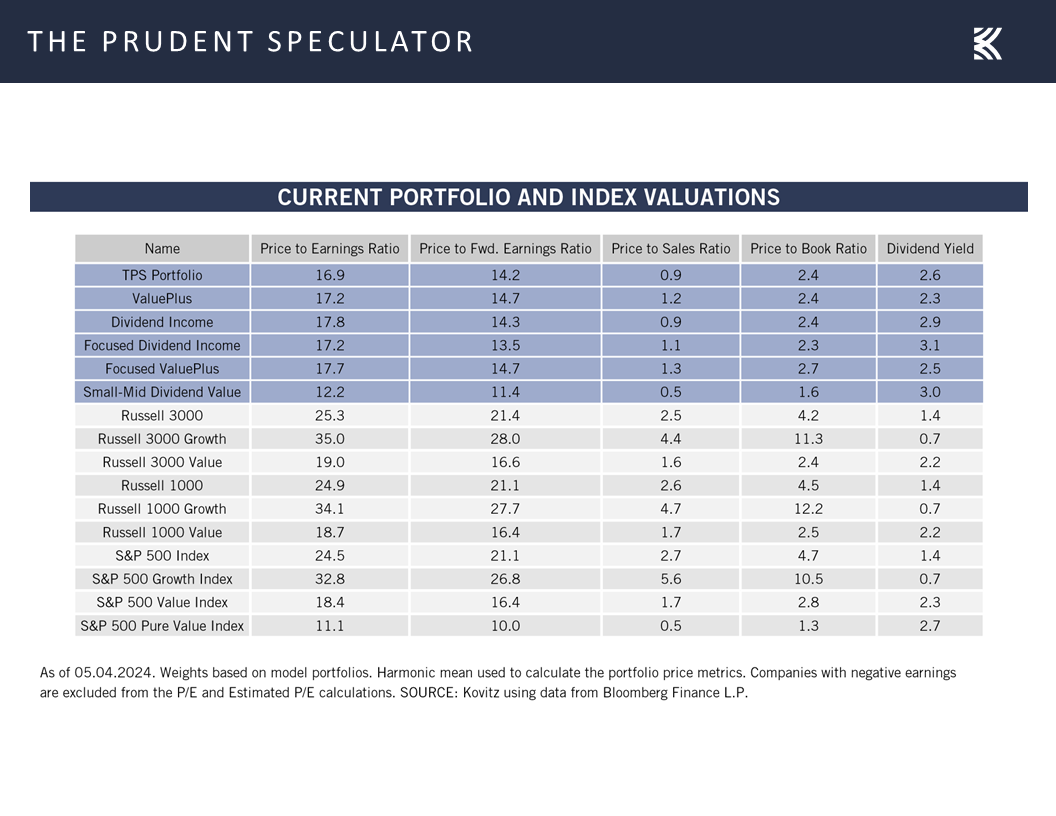

Valuations – Inexpensive Metrics for TPS Portfolio

while we continue to sleep well at night with the even more attractive valuation metrics associated with our broadly diversified portfolios of what we believe are undervalued stocks.

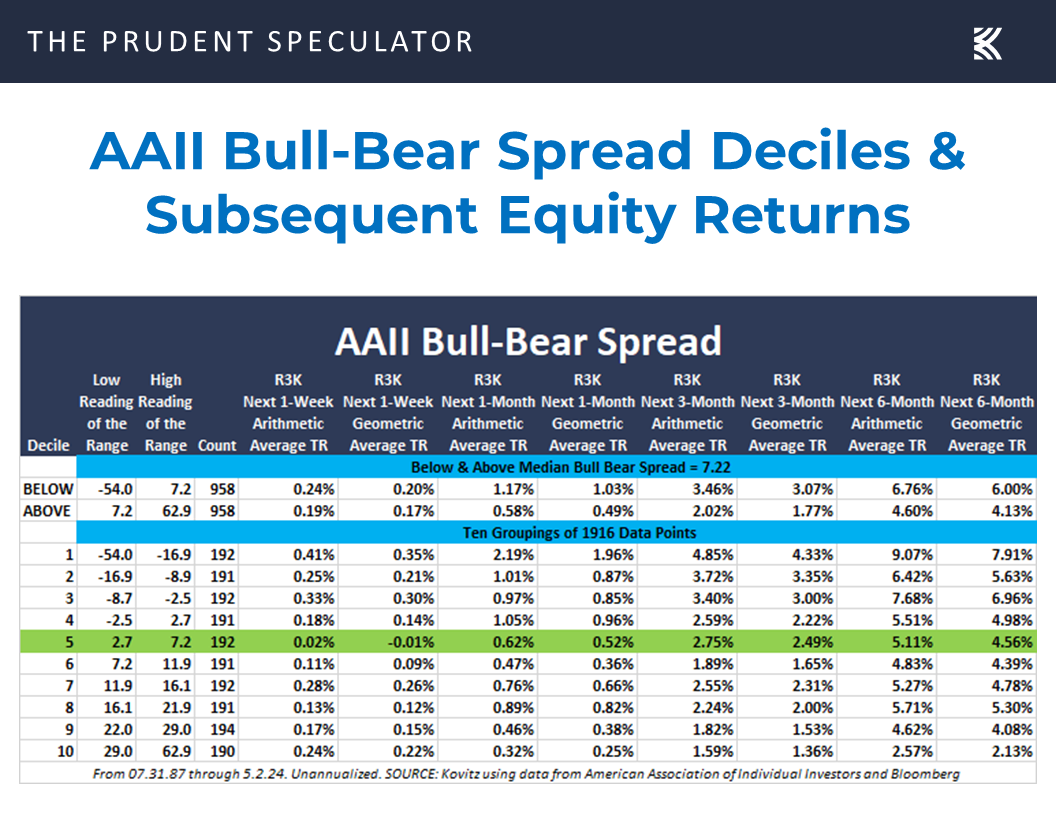

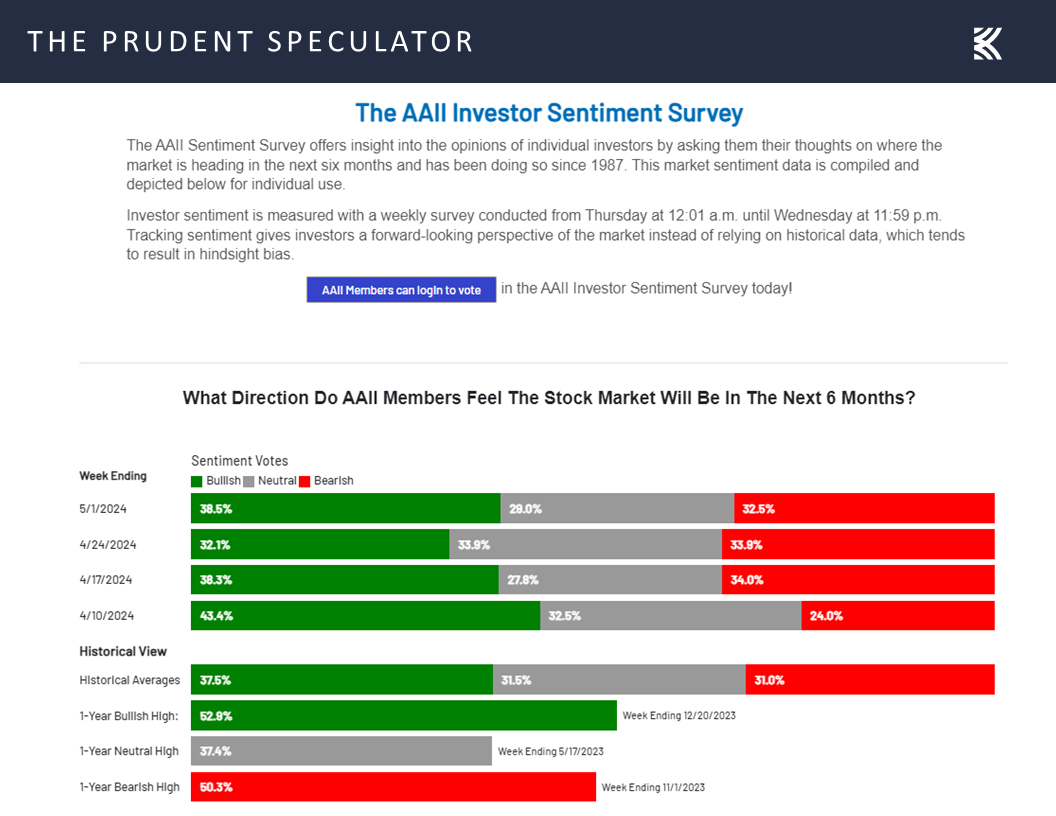

Sentiment – Bull-Bear Spread Back to Normal

Though optimism on Main Street is not reason to sell stocks, based on an extensive analysis of the American Association of Individual Investors Bull-Bear Spread and subsequent equity market returns,

we don’t mind that the latest read on the AAII gauge shows figures in line with the historical norms for this contrarian sentiment measure.

Stock News – Updates on seventeen stocks across eleven different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Federal Reserve, Economic Outlook, Earnings, Valuations and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Economic Outlook, Federal Reserve, Earnings, Valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Week in Review – May Off to a Good Start

Fed Meeting – Rates Unchanged

Historical Evidence – Higher Fed Funds Rate & Rising Interest Rates Not Negatives for Stocks, On Average

Econ Outlook – Powell & OECD Upbeat

Earnings – Solid Growth Estimated in ’24 & ’25

Econ Stats – Not too Hot, Not too Cold

Volatility – Ups and Downs But Long-Term Trend is Up

Valuations – Inexpensive Metrics for TPS Portfolio

Sentiment – Bull-Bear Spread Back to Normal

Stock News – Updates on JNJ, PHG, VWAPY, MMM, GLW, LEG, CVS, PFE, NYCB, QCOM, BHE, WRK, MRNA, AMGN, FDP & AAPL

Week in Review – May Off to a Good Start

The seasonally less favorable (but not unfavorable, on average) May – October period,

Fed Meeting – Rates Unchanged

started on a high note, following the announcement on May 1 that the Federal Reserve would leave its target for the Fed Funds rate unchanged at a range of 5.25% to 5.50%,

and Jerome H. Powell’s response in his Press Conference that same day to the query: “I wonder, obviously Michelle Bowman has been saying that there is a risk that rates may need to increase further, although it’s not her baseline outlook, I wonder if you see that as a risk as well, and if so, what change in conditions would merit considering raising rates at this point?”

The Fed Chair replied, “So I think it’s unlikely that the next policy rate move will be a hike. I’d say it’s unlikely. You know, our policy focus is really what I just mentioned, which is how long to keep policy restrictive. You ask what would it take, I think we’d need to see persuasive evidence that our policy stance is not sufficiently restrictive to bring inflation sustainably down to 2 percent over time. That’s not what we think we’re seeing, as I mentioned, but something like that is what it would take. We’d look at the totality of the data and answer that question that would include inflation, inflation expectations, and all the other data too.”

Given that some traders were worried that a rate hike could be on the table, the more dovish comments led to a sizable drop in the year-end betting in the Fed Funds futures market to a rate of 4.87% from 4.99% the week prior,

and contributed to a rally in government bonds with the yield on the 10-Year U.S. Treasury dropping from nearly 4.7% pre-Fed to near 4.5% by week’s end.

Historical Evidence – Higher Fed Funds Rate & Rising Interest Rates Not Negatives for Stocks, On Average

Of course, history shows that investors should stick with stocks, especially Value, whether the Fed Funds rate is high or low or whether it is rising or falling,

with the same also the case for the 10-Year Treasury yield,

Econ Outlook – Powell & OECD Upbeat

but traders evidently were pleased that Chair Powell in his prepared Press Conference remarks was relatively upbeat on the health of the U.S. economy,

…while the Organisation for Economic Co-operation and Development was cautiously optimistic on May 2 in its outlook for domestic and global GDP growth.

Earnings – Solid Growth Estimated in ’24 & ’25

No doubt, a solid economic backdrop is a positive for corporate profits and estimates for EPS growth this year and next presently are robust. True analysts are often overly rosy in their projections, but Q1 earnings reports have beat expectations at a better-than-79% clip,

and history shows that stock prices generally follow profits higher.

Econ Stats – Not too Hot, Not too Cold

To be sure, it is a delicate dance these days between those who would prefer a strong economy and those who would like Federal reserve rate cuts, so not-too-cold and not-too-hot statistics are generally greeted with enthusiasm, as was the case in response to Friday’s big jobs report. The Labor Department saw a still healthy, but weaker-than-expected, 175,000 new payrolls created,

while the unemployment rate ticked up to 3.9%,

and growth in average hourly earnings slowed to 3.9%, down from 4.1% in March, helping temper fears of higher inflation.

Yes, other economic data points came in weaker than expected, like the Conference Board’s Consumer Confidence Index for April (97.0 vs. 104.0 est.),

the Institute for Supply Management’s (ISM) measure of activity in the factory sector in April dropping to 49.2 (50.0 est.),

and the ISM Service Sector Non-Manufacturing Index coming in at 49.4 for April, compared to the consensus forecast of 52.0.

However, first-time filings for unemployment benefits in the latest week dipped to a very low 208,000,

and factory orders for March rose by a better-than-average 1.6%,

while the latest Atlanta Fed projection for real (inflation-adjusted) Q2 U.S. GDP Growth stood at a rich 3.3%,

and the odds of recession in the next 12 months, as tabulated by Bloomberg, remained at a relatively low 30%.

Volatility – Ups and Downs But Long-Term Trend is Up

We always are braced for downside volatility as selloffs, corrections and even Bear Markets are part of the investment equation, but we remain confident that equities will continue to provide handsome rewards,

to those who remember that time in the market trumps market timing.

Further, we remain of the opinion that Value stocks in general are reasonably priced,

Valuations – Inexpensive Metrics for TPS Portfolio

while we continue to sleep well at night with the even more attractive valuation metrics associated with our broadly diversified portfolios of what we believe are undervalued stocks.

Sentiment – Bull-Bear Spread Back to Normal

Though optimism on Main Street is not reason to sell stocks, based on an extensive analysis of the American Association of Individual Investors Bull-Bear Spread and subsequent equity market returns,

we don’t mind that the latest read on the AAII gauge shows figures in line with the historical norms for this contrarian sentiment measure.

Stock News – Updates on seventeen stocks across eleven different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.