The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss growth, stock news, interest rates, valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week In Review – Plenty of Volatility; Modest Gains for Value

Miracle of Compounding – Small Gains Add Up Over Time

Econ Stats – More Good News than Bad

Interest Rates – 10-Year Yield and Odds of a Hike in the Fed Funds Rate Rise

Inflation – Longer-Term Expectations Retreat; CPI & PPI Modestly Above Projections

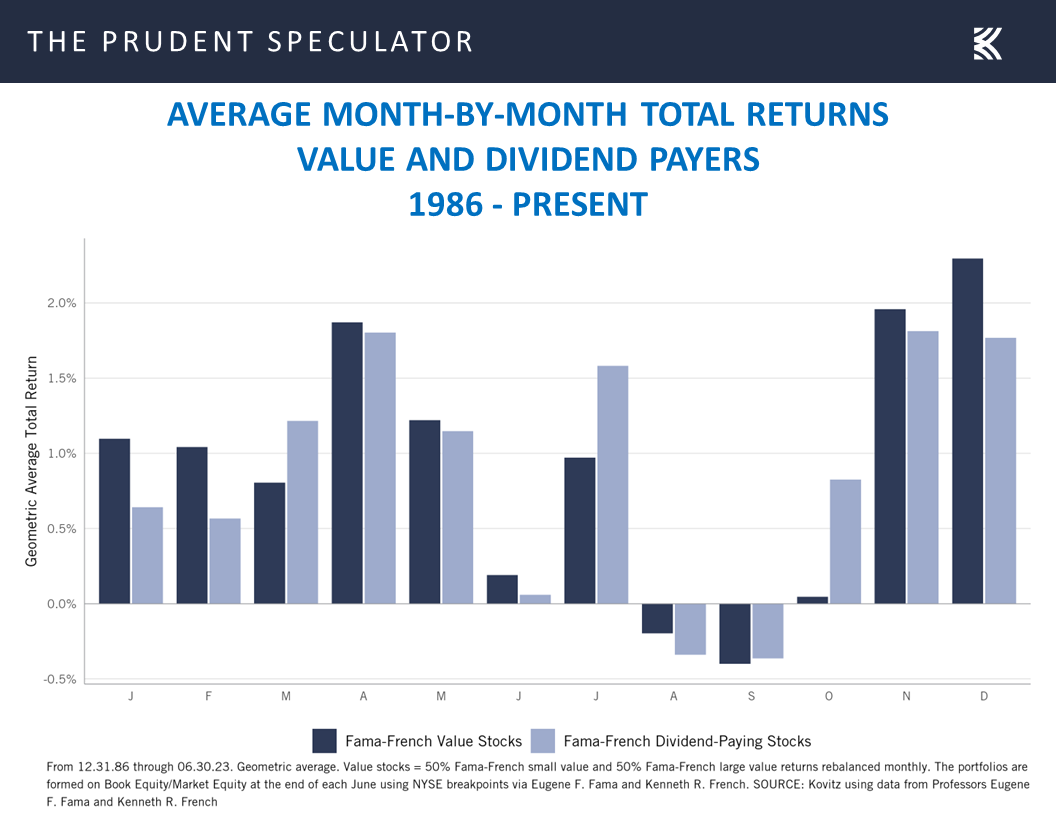

Valuations – Liking the Metrics Associated with our Portfolios

Growth – Stock Prices, GDP and Corporate Profits Have Increased Over Time

Stock News – Updates on fifteen stocks across

Week In Review – Plenty of Volatility; Modest Gains for Value

As all eyes are on this week’s FOMC Meeting September 19-20, the major market averages ended the most-recent five trading days on a down note, continuing a less-than-grand stretch for stocks during the seasonally less favorable time of year.

Miracle of Compounding – Small Gains Add Up Over Time

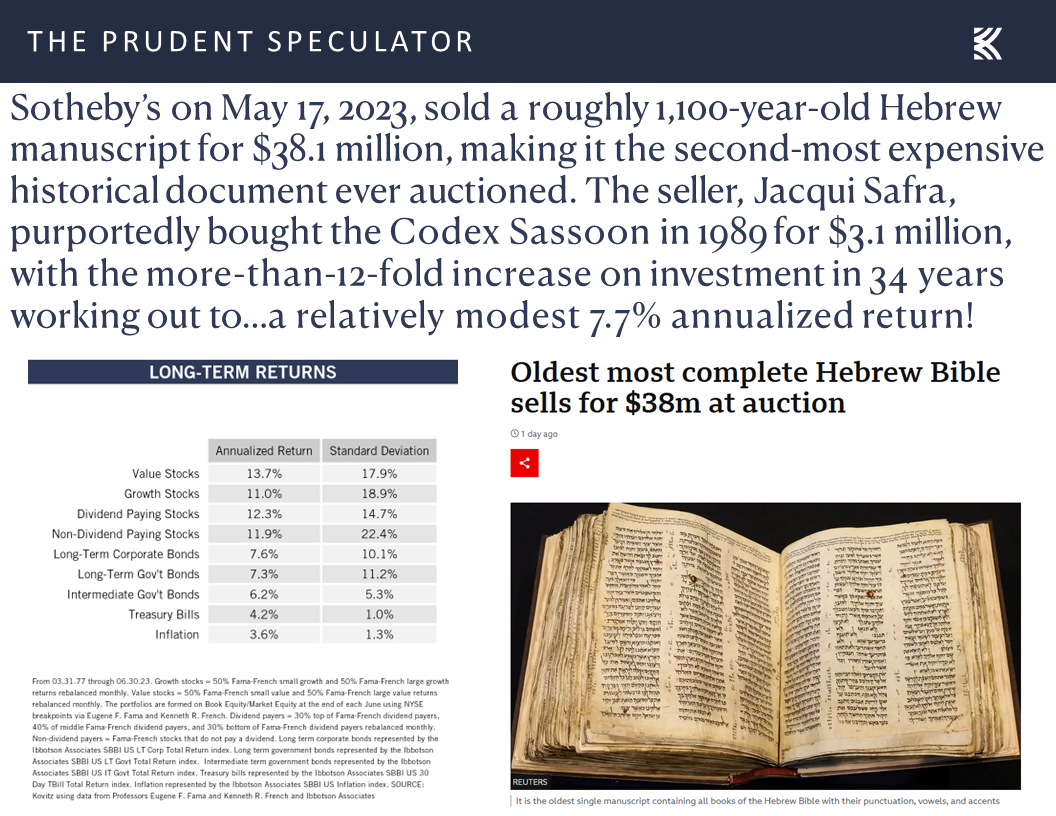

Happily, the Value indexes managed gains last week. Of course, the 0.37% uptick in the Russell 2000 Value index and the 0.46% advance for the Russell 3000 Value index don’t sound that great, but those returns annualize to 21.17% and 26.95%, respectively. To be sure, average yearly equity returns historically have not come close to those figures, but substantial wealth can accrue over time even with relatively modest gains. Time and patience can lead to the Miracle of Compounding.

Econ Stats – More Good News than Bad

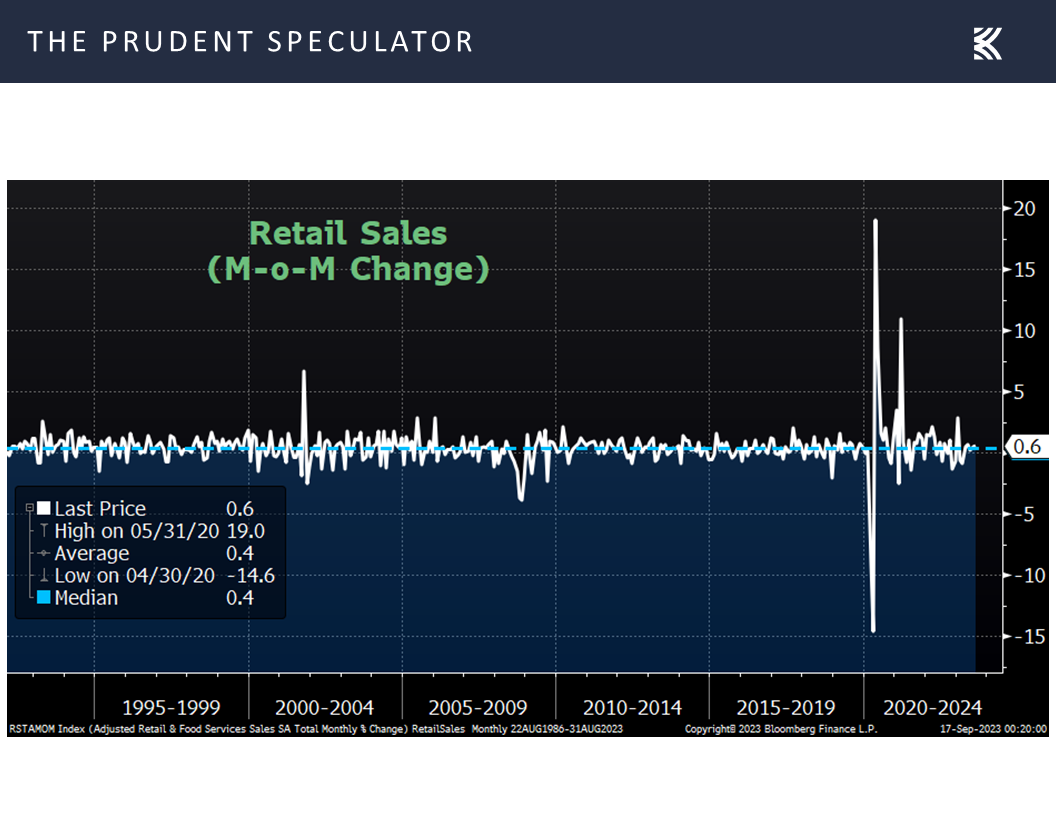

We would argue that the renewed interest in Value was due to the release of relatively upbeat economic data last week as retail sales rose 0.6% in August, well above expectations for a 0.1% increase. True, much of the gain was due to higher prices at the pump, but sales excluding autos and gas climbed 0.2%, topping forecasts of a -0.1% dip.

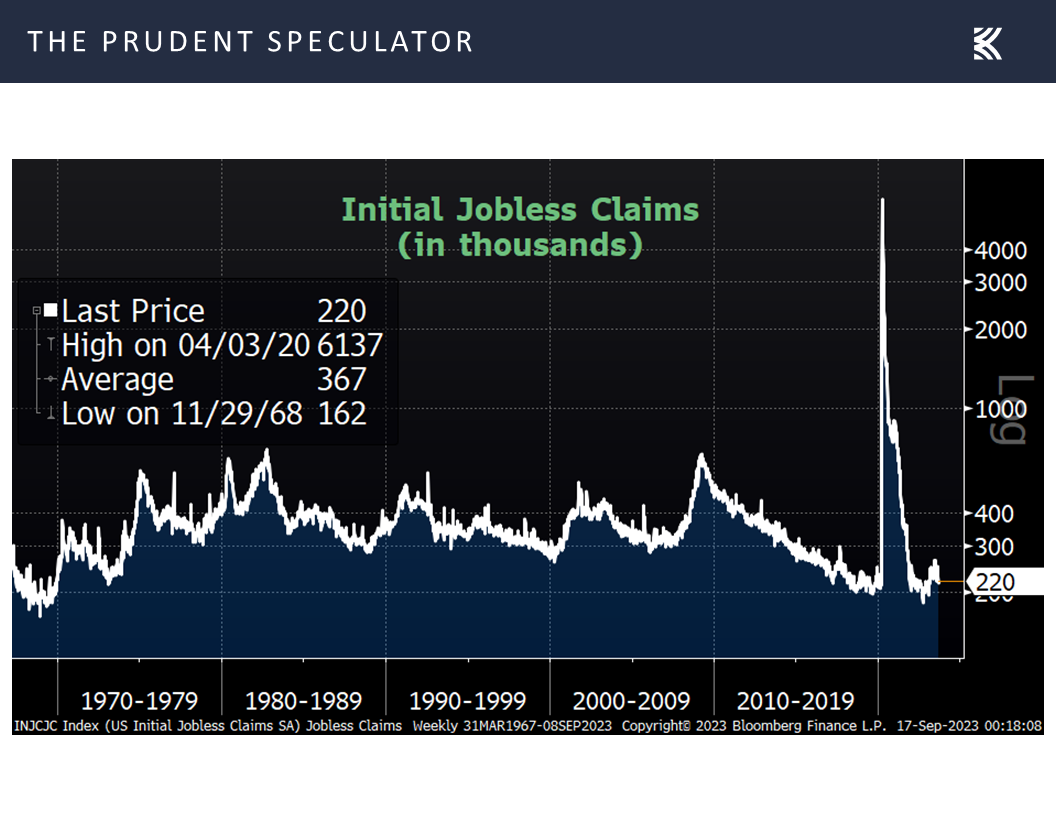

The consumer remains in relatively good shape, with the labor market also continuing to see healthy numbers, as first-time filings for unemployment benefits om the latest week came in at 220,000, below projections of 225,000. The near-record-low jobless figures are even more impressive when considering that the workforce has expanded over the years.

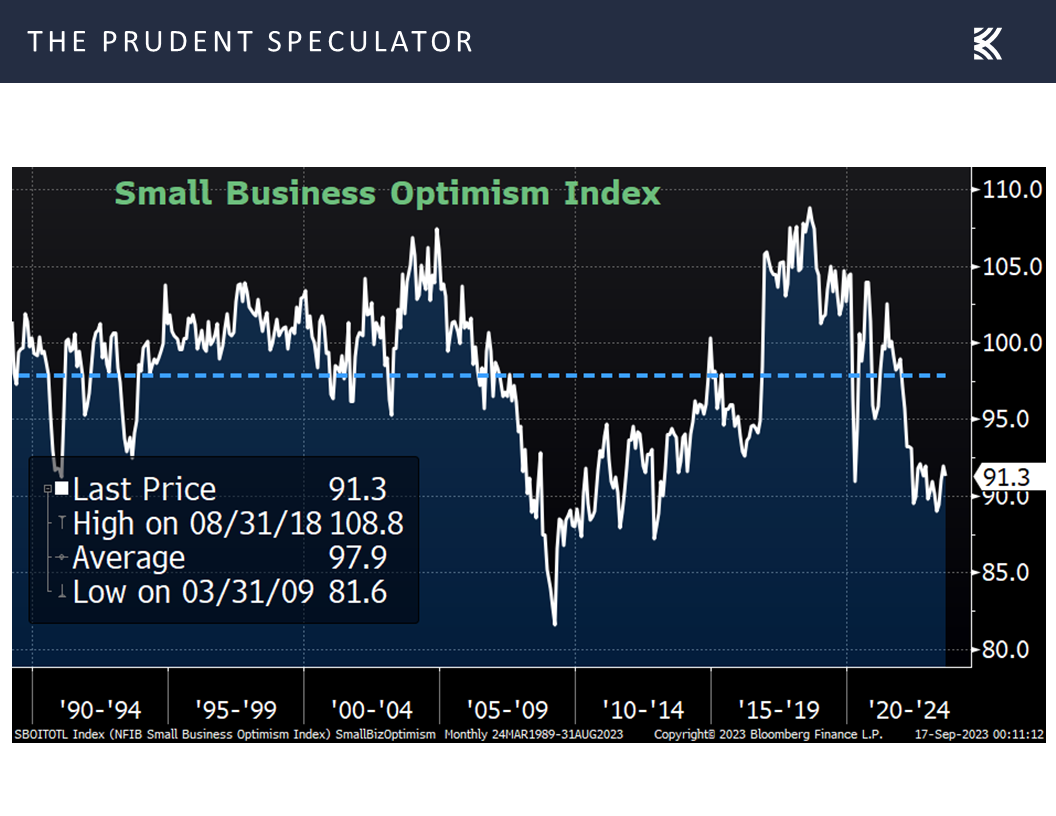

Interestingly, the mood on Main Street is less than rosy, as both the NFIB Small Business Optimism gauge for August,

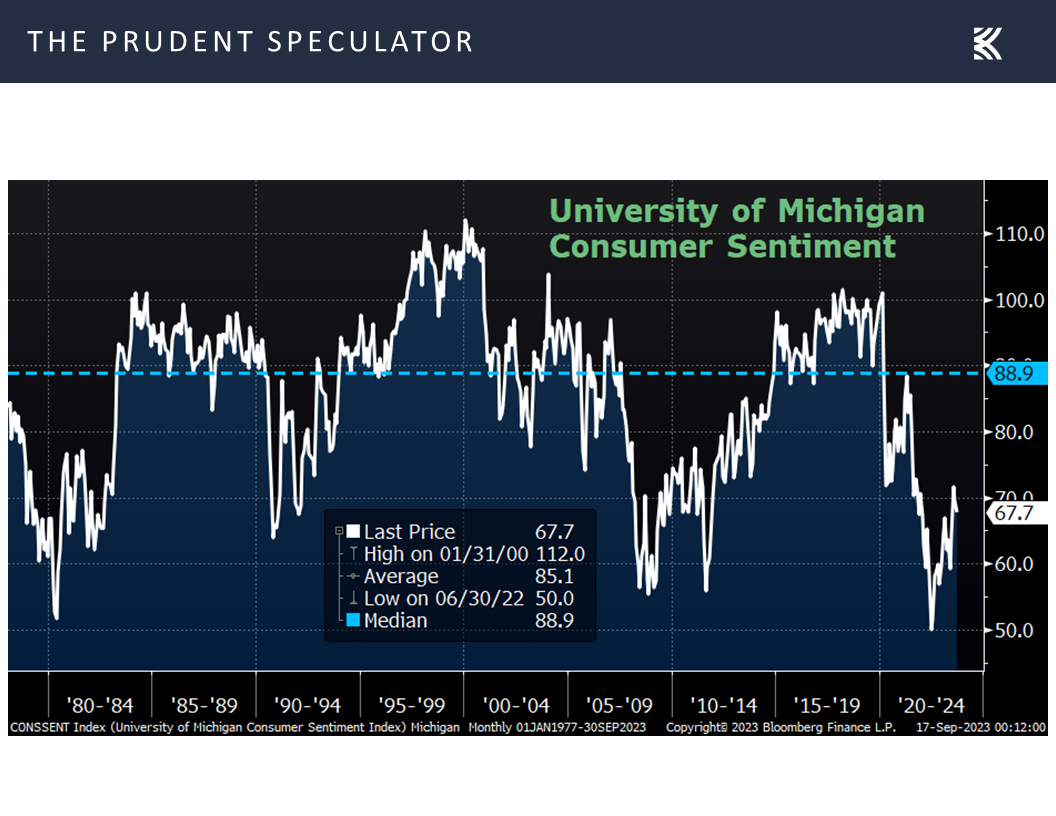

and the Univ. of Michigan’s preliminary measure of Consumer Sentiment for September trailed expectations, with each currently residing well below average,

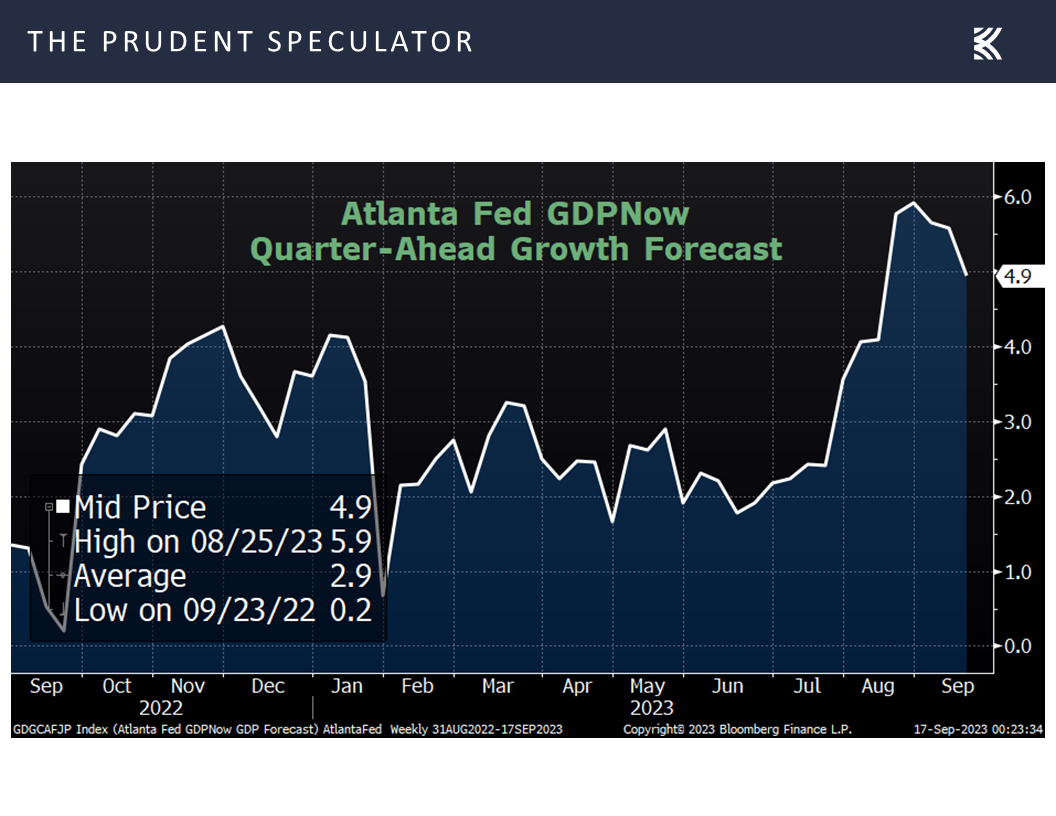

even as the latest estimate for Q3 real (inflation-adjusted) U.S. GDP growth from the Atlanta Fed stood at an impressive 4.9%.

With the August reading on Industrial Production and the September Empire Manufacturing PMI both topping estimates,

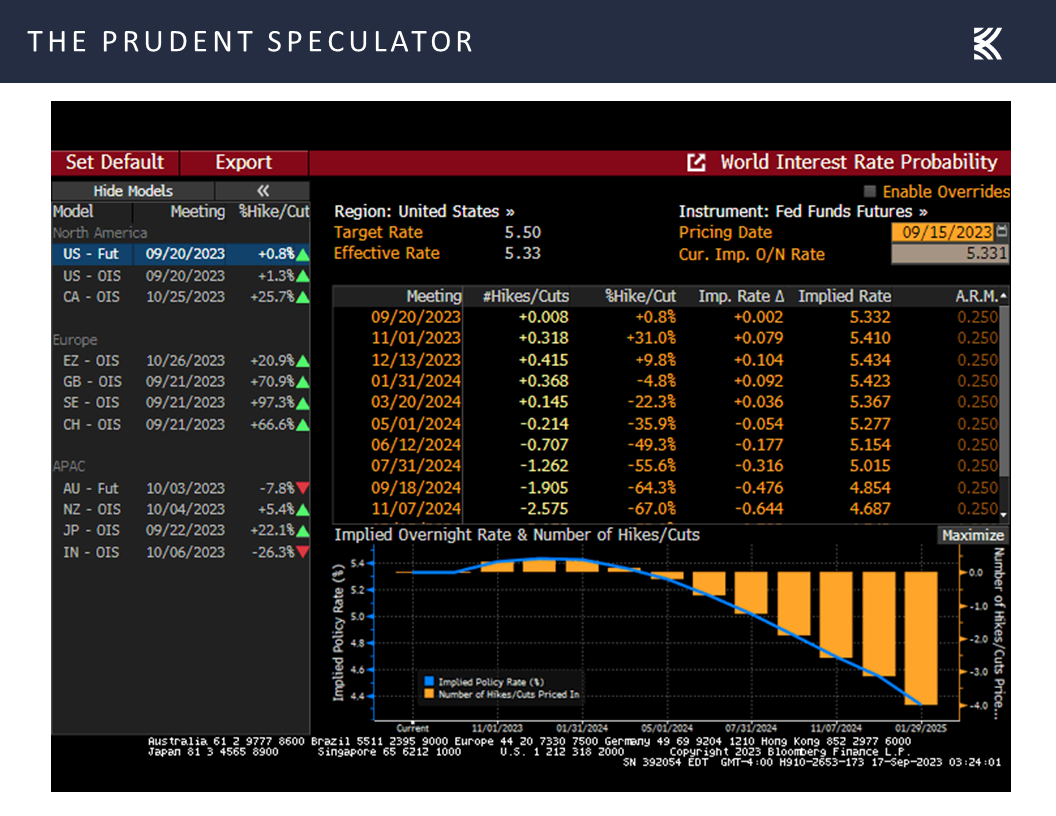

Interest Rates – 10-Year Yield and Odds of a Hike in the Fed Funds Rate Rise

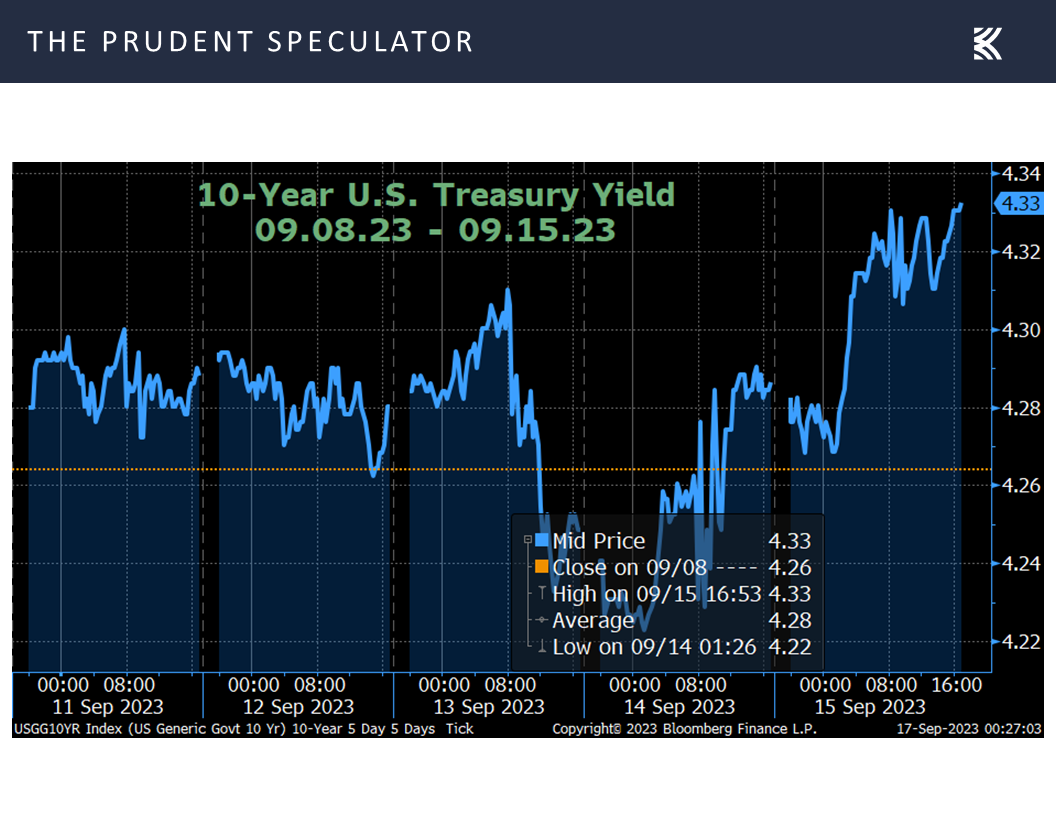

interest rates ticked up last week as the yield on the benchmark 10-year U.S. Treasury rose from 4.26% to 4.33%,

and the chances of a less accommodative Federal Reserve decreased, per the Fed Funds futures market.

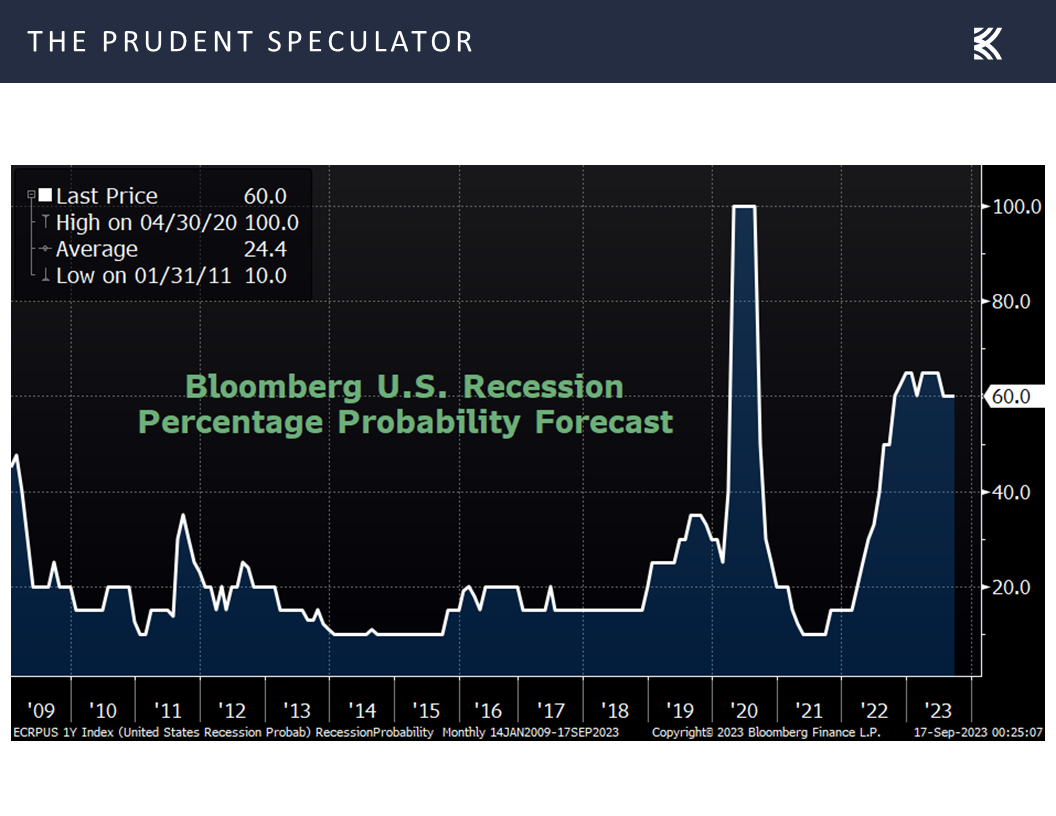

Of course, the chart above shows that Fed rate cuts are expected in 2024, as the risk of recession remains elevated,

Inflation – Longer-Term Expectations Retreat; CPI & PPI Modestly Above Projections

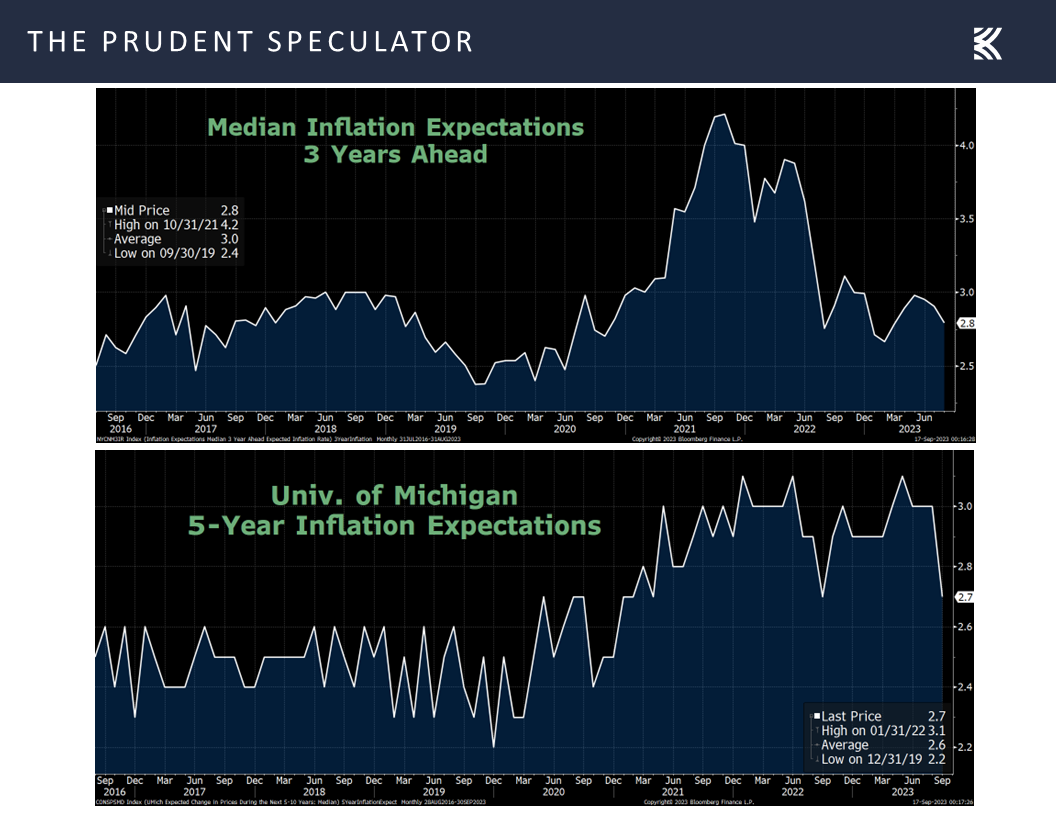

and inflation expectations both intermediate-term and long-term remain well contained.

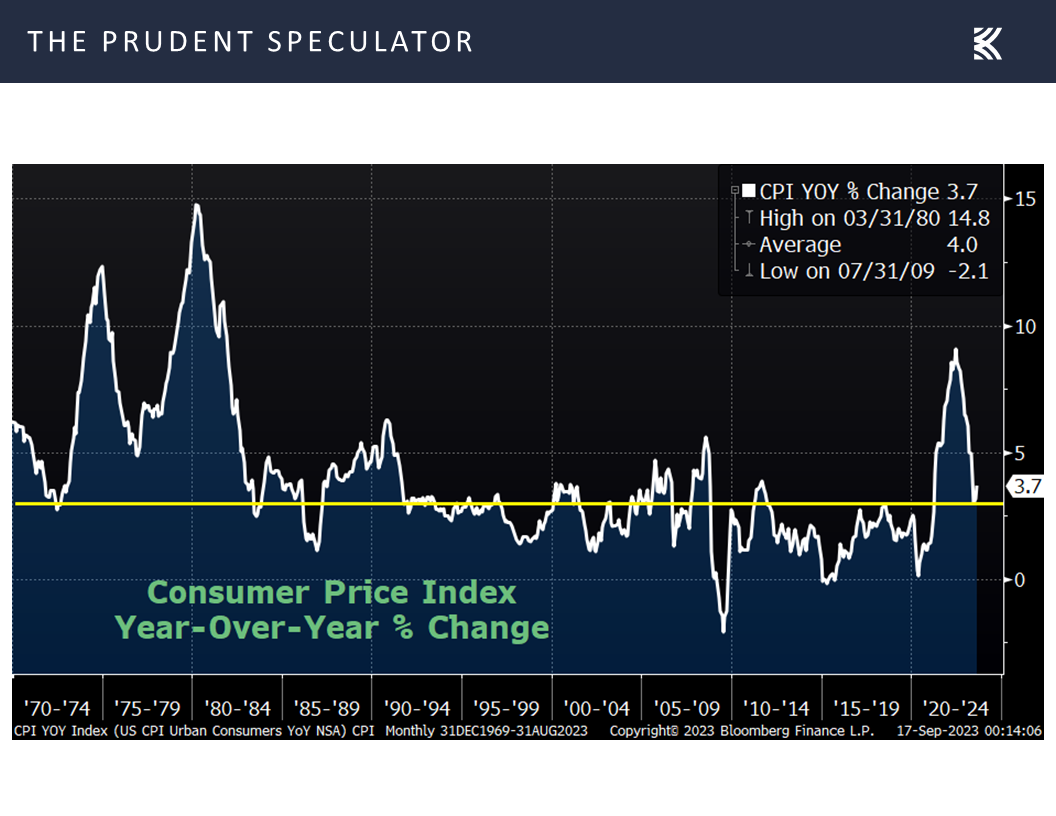

And speaking of inflation, the current data continue to remain a bit too hot for the Fed’s liking, with the Consumer Price Index (CPI) for August rising a slightly higher than forecast 3.7%,

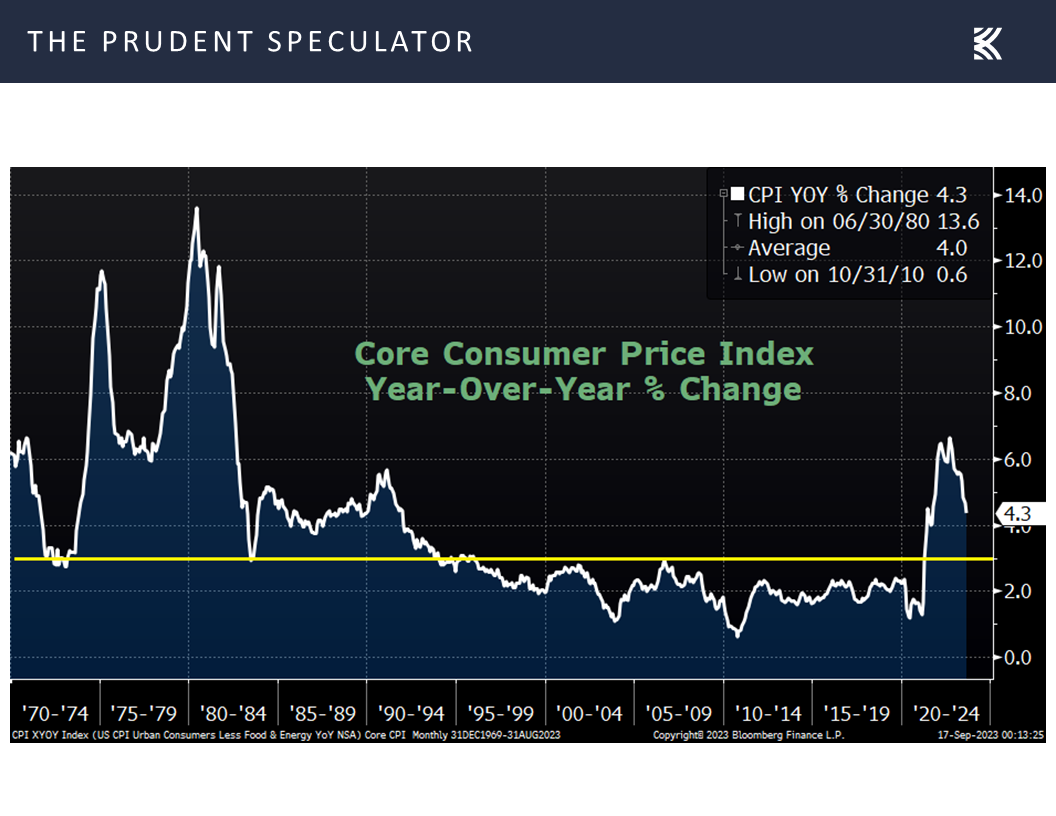

even as the Core-CPI rate (excludes volatile food and energy prices) rose an as-expected 4.3%,

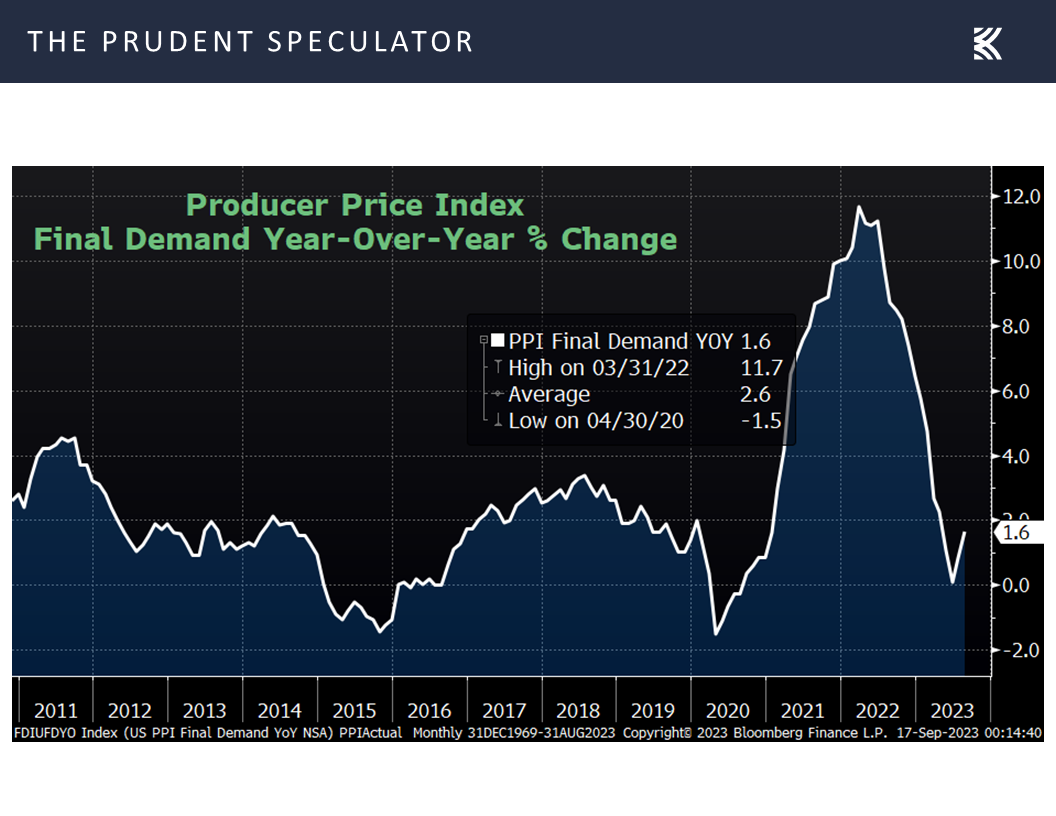

and pricing pressures at the wholesale level (Producer Price Index) continued to trend below the historical norm.

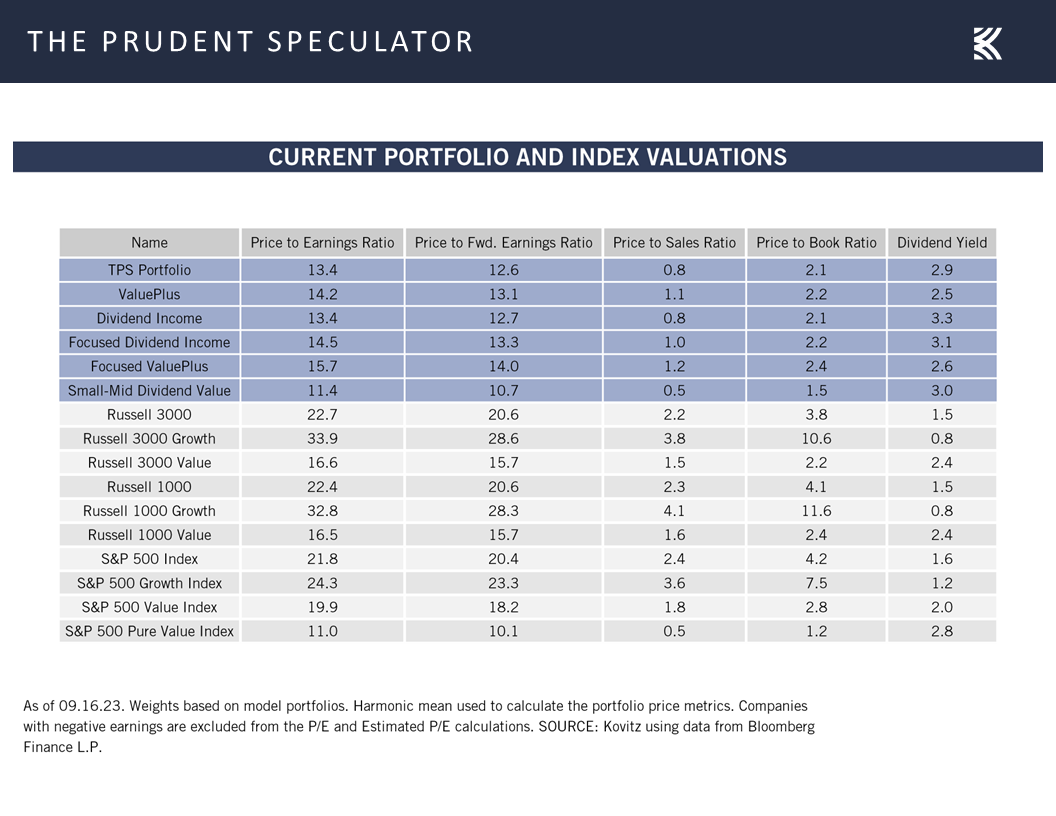

Valuations – Liking the Metrics Associated with our Portfolios

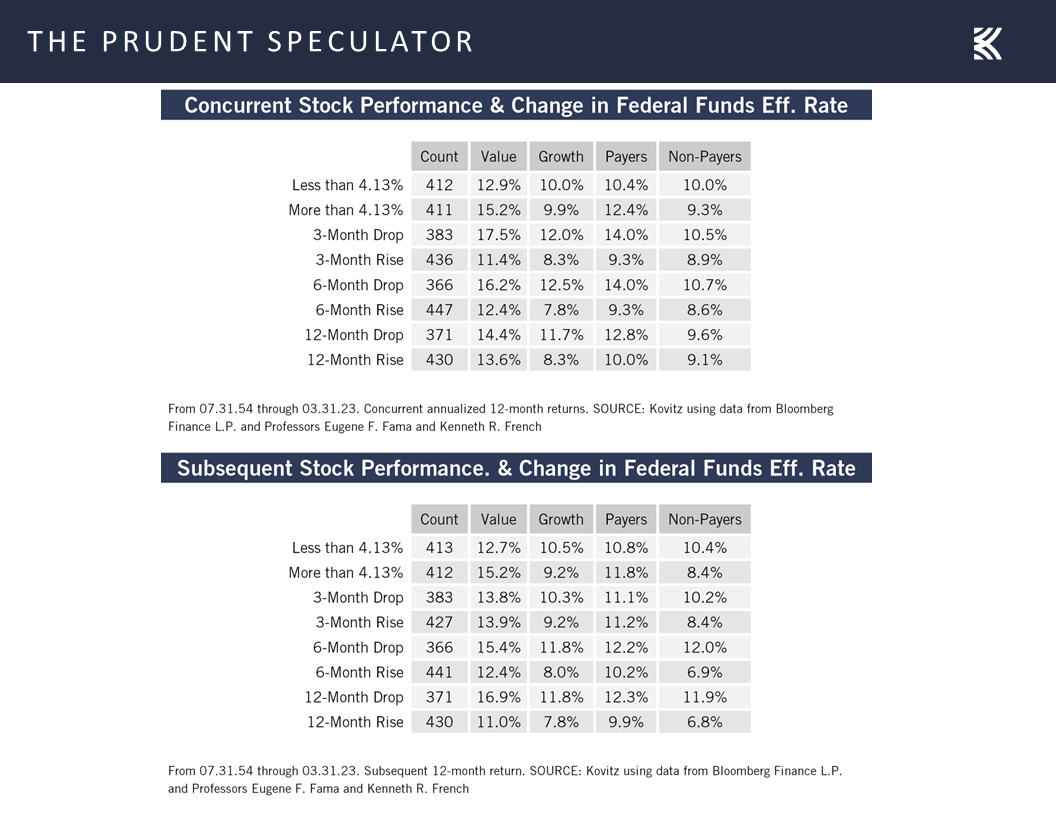

Obviously, Jerome H. Powell & Co. will be front and center this week as the decision on monetary policy will be announced on Wednesday, but we offer the reminder that whether the Fed is raising or lowering interest rates, stocks have performed fine, on average. This goes for performance both concurrent with and subsequent to changes in the Fed Funds rate.

So, we continue to stay the course with our broadly diversified portfolios of what we believe are undervalued stocks, though we are always braced for downside volatility.

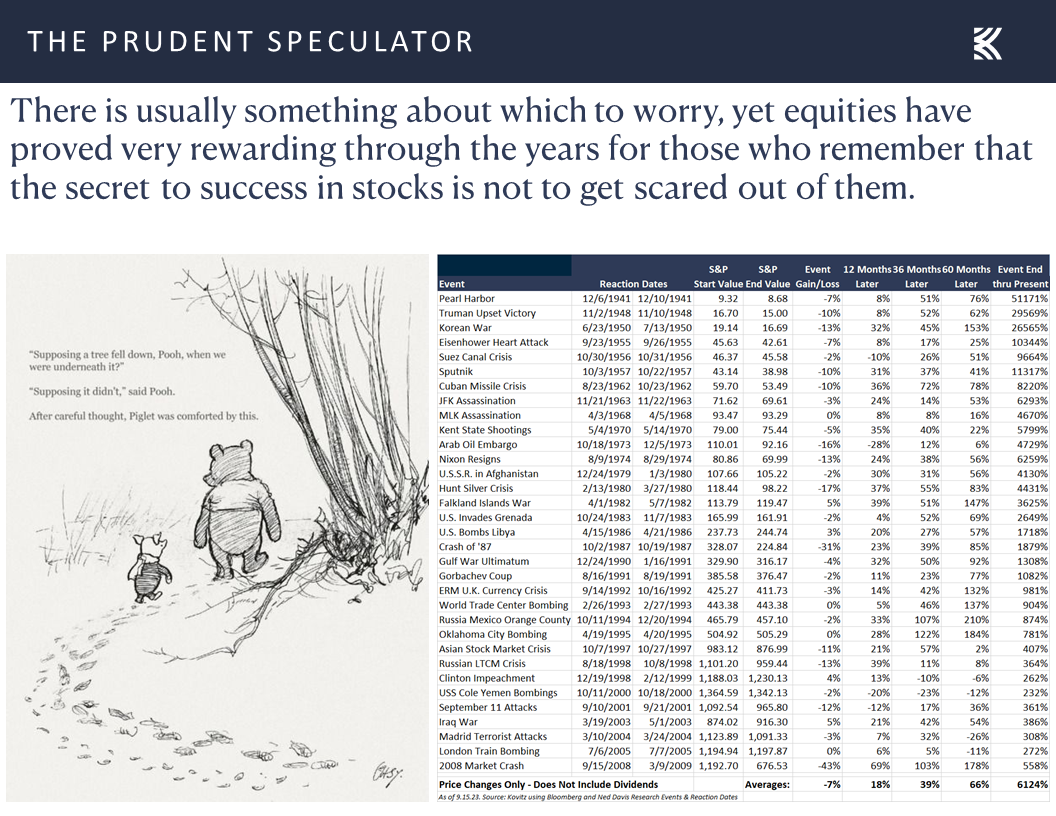

Market history is filled with plenty of disconcerting events, yet those who remember that the secret to success in stocks is not to get scared out of them have been handsomely rewarded in the fullness of time,

Growth – Stock Prices, GDP and Corporate Profits Have Increased Over Time

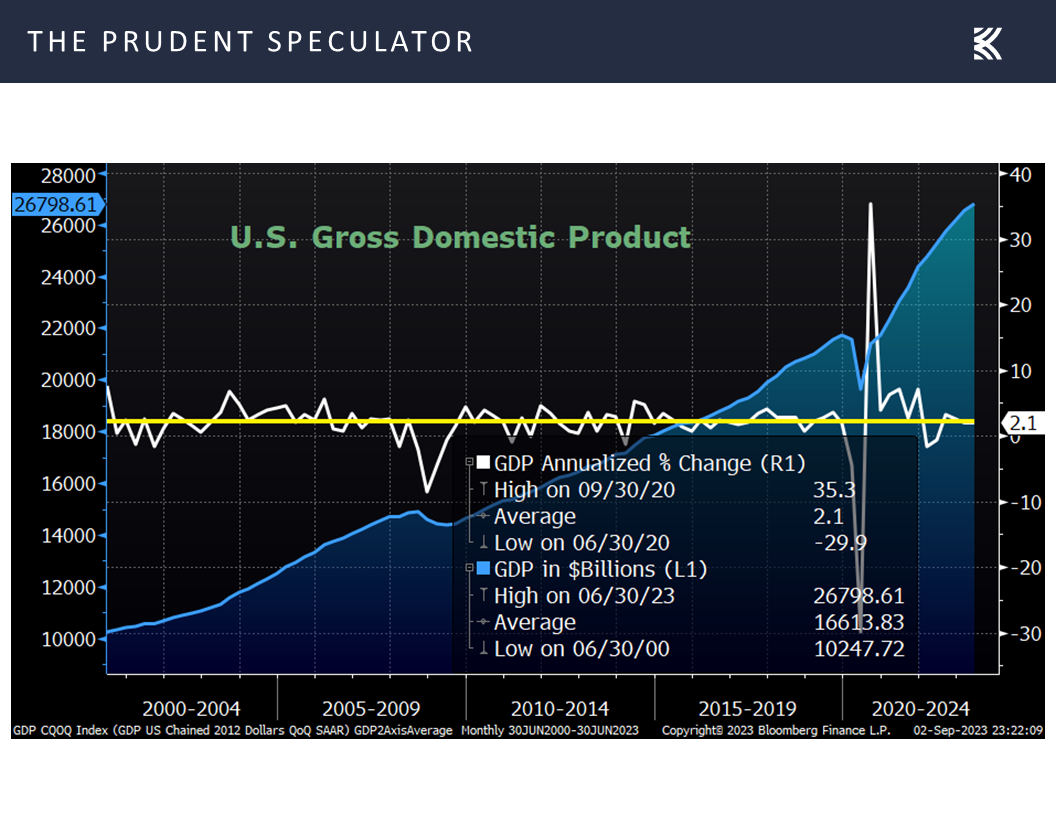

as prices have appreciated as GDP has expanded,

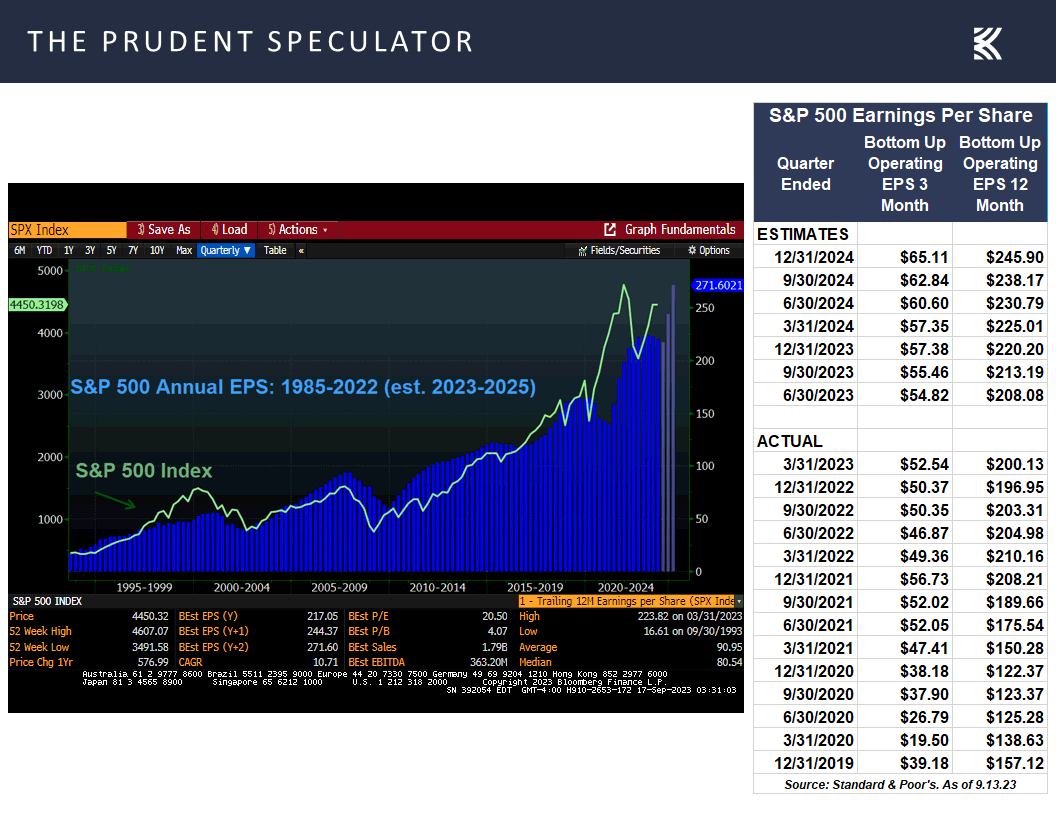

and corporate profits have grown.

Stock News – Updates on eight stocks across ten different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Growth, Stock News, Interest Rates, Valuations and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss growth, stock news, interest rates, valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week In Review – Plenty of Volatility; Modest Gains for Value

Miracle of Compounding – Small Gains Add Up Over Time

Econ Stats – More Good News than Bad

Interest Rates – 10-Year Yield and Odds of a Hike in the Fed Funds Rate Rise

Inflation – Longer-Term Expectations Retreat; CPI & PPI Modestly Above Projections

Valuations – Liking the Metrics Associated with our Portfolios

Growth – Stock Prices, GDP and Corporate Profits Have Increased Over Time

Stock News – Updates on fifteen stocks across

Week In Review – Plenty of Volatility; Modest Gains for Value

As all eyes are on this week’s FOMC Meeting September 19-20, the major market averages ended the most-recent five trading days on a down note, continuing a less-than-grand stretch for stocks during the seasonally less favorable time of year.

Miracle of Compounding – Small Gains Add Up Over Time

Happily, the Value indexes managed gains last week. Of course, the 0.37% uptick in the Russell 2000 Value index and the 0.46% advance for the Russell 3000 Value index don’t sound that great, but those returns annualize to 21.17% and 26.95%, respectively. To be sure, average yearly equity returns historically have not come close to those figures, but substantial wealth can accrue over time even with relatively modest gains. Time and patience can lead to the Miracle of Compounding.

Econ Stats – More Good News than Bad

We would argue that the renewed interest in Value was due to the release of relatively upbeat economic data last week as retail sales rose 0.6% in August, well above expectations for a 0.1% increase. True, much of the gain was due to higher prices at the pump, but sales excluding autos and gas climbed 0.2%, topping forecasts of a -0.1% dip.

The consumer remains in relatively good shape, with the labor market also continuing to see healthy numbers, as first-time filings for unemployment benefits om the latest week came in at 220,000, below projections of 225,000. The near-record-low jobless figures are even more impressive when considering that the workforce has expanded over the years.

Interestingly, the mood on Main Street is less than rosy, as both the NFIB Small Business Optimism gauge for August,

and the Univ. of Michigan’s preliminary measure of Consumer Sentiment for September trailed expectations, with each currently residing well below average,

even as the latest estimate for Q3 real (inflation-adjusted) U.S. GDP growth from the Atlanta Fed stood at an impressive 4.9%.

With the August reading on Industrial Production and the September Empire Manufacturing PMI both topping estimates,

Interest Rates – 10-Year Yield and Odds of a Hike in the Fed Funds Rate Rise

interest rates ticked up last week as the yield on the benchmark 10-year U.S. Treasury rose from 4.26% to 4.33%,

and the chances of a less accommodative Federal Reserve decreased, per the Fed Funds futures market.

Of course, the chart above shows that Fed rate cuts are expected in 2024, as the risk of recession remains elevated,

Inflation – Longer-Term Expectations Retreat; CPI & PPI Modestly Above Projections

and inflation expectations both intermediate-term and long-term remain well contained.

And speaking of inflation, the current data continue to remain a bit too hot for the Fed’s liking, with the Consumer Price Index (CPI) for August rising a slightly higher than forecast 3.7%,

even as the Core-CPI rate (excludes volatile food and energy prices) rose an as-expected 4.3%,

and pricing pressures at the wholesale level (Producer Price Index) continued to trend below the historical norm.

Valuations – Liking the Metrics Associated with our Portfolios

Obviously, Jerome H. Powell & Co. will be front and center this week as the decision on monetary policy will be announced on Wednesday, but we offer the reminder that whether the Fed is raising or lowering interest rates, stocks have performed fine, on average. This goes for performance both concurrent with and subsequent to changes in the Fed Funds rate.

So, we continue to stay the course with our broadly diversified portfolios of what we believe are undervalued stocks, though we are always braced for downside volatility.

Market history is filled with plenty of disconcerting events, yet those who remember that the secret to success in stocks is not to get scared out of them have been handsomely rewarded in the fullness of time,

Growth – Stock Prices, GDP and Corporate Profits Have Increased Over Time

as prices have appreciated as GDP has expanded,

and corporate profits have grown.

Stock News – Updates on eight stocks across ten different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.