The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss interest rates, corporate profits, valuations and more stock news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Newsletter Trades – Numerous Transactions Across 4 Portfolios

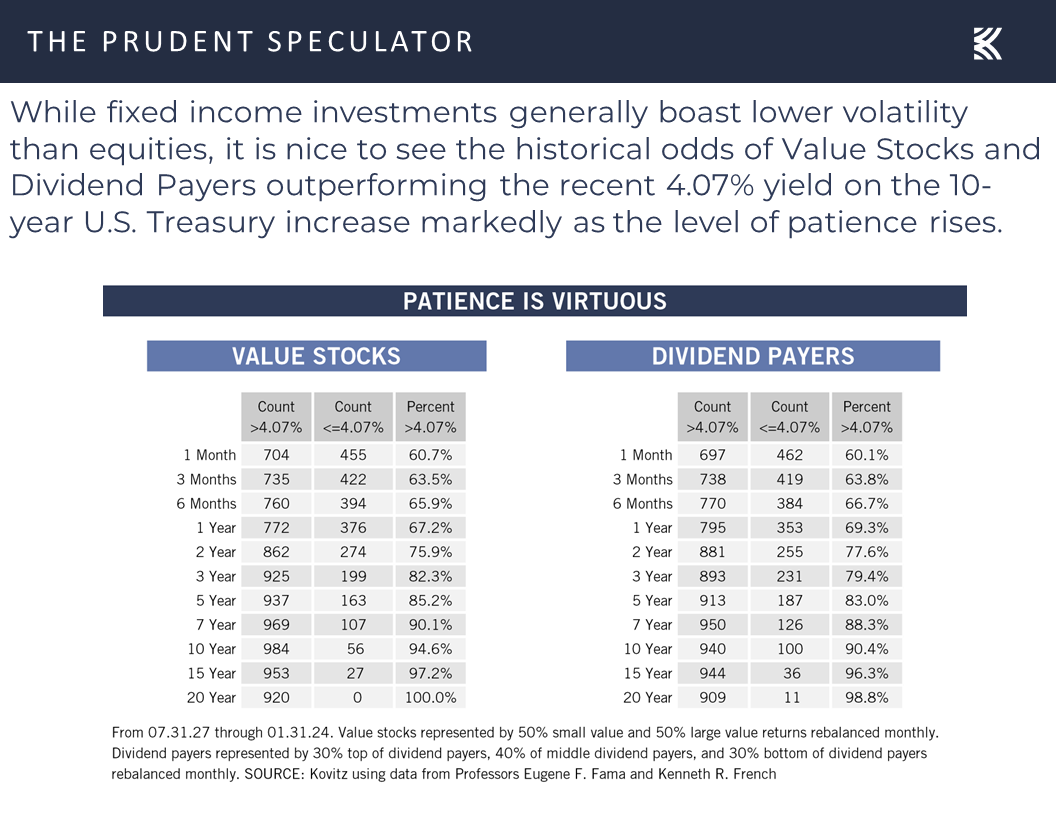

Interest Rates – Yields Fall; Fed on Track to Cut Rates in the Not-Too Distant Future

Econ News – Mixed Numbers but Modest GDP Growth in ’24 Still Likely

Corporate Profits – Solid Growth this Year and Next the Forecast

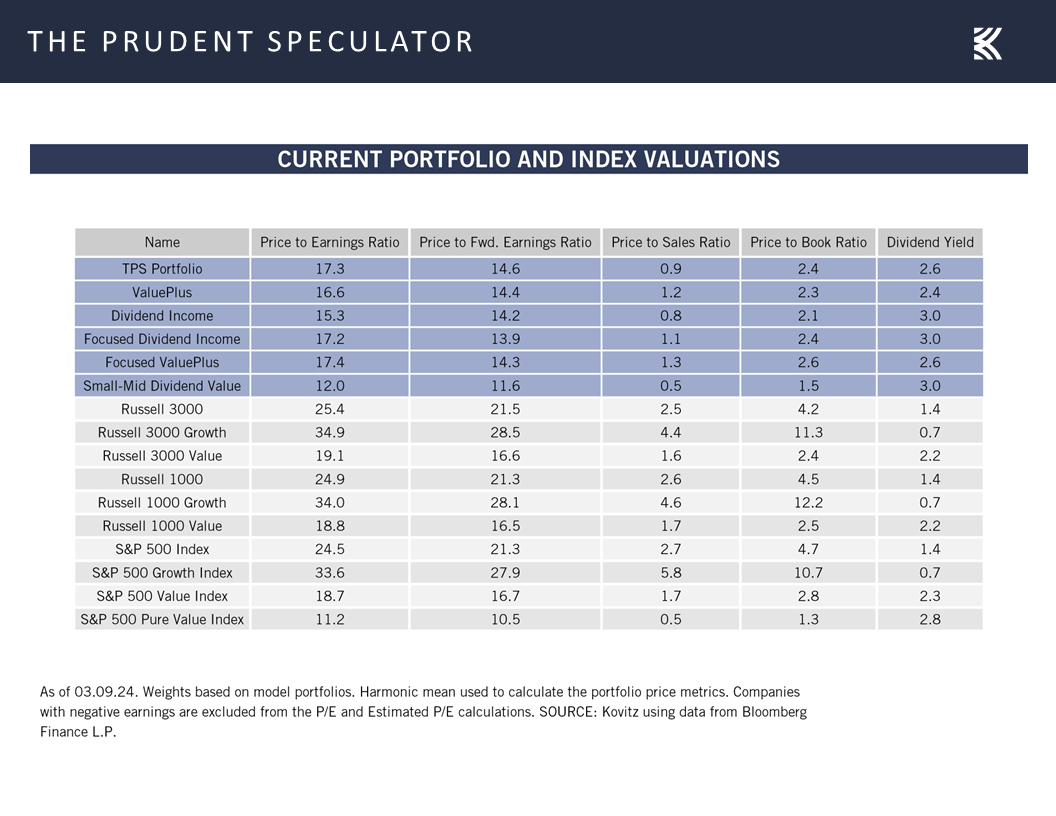

Valuations – Value Stocks Attractively Priced

Sentiment – Lots of Optimism

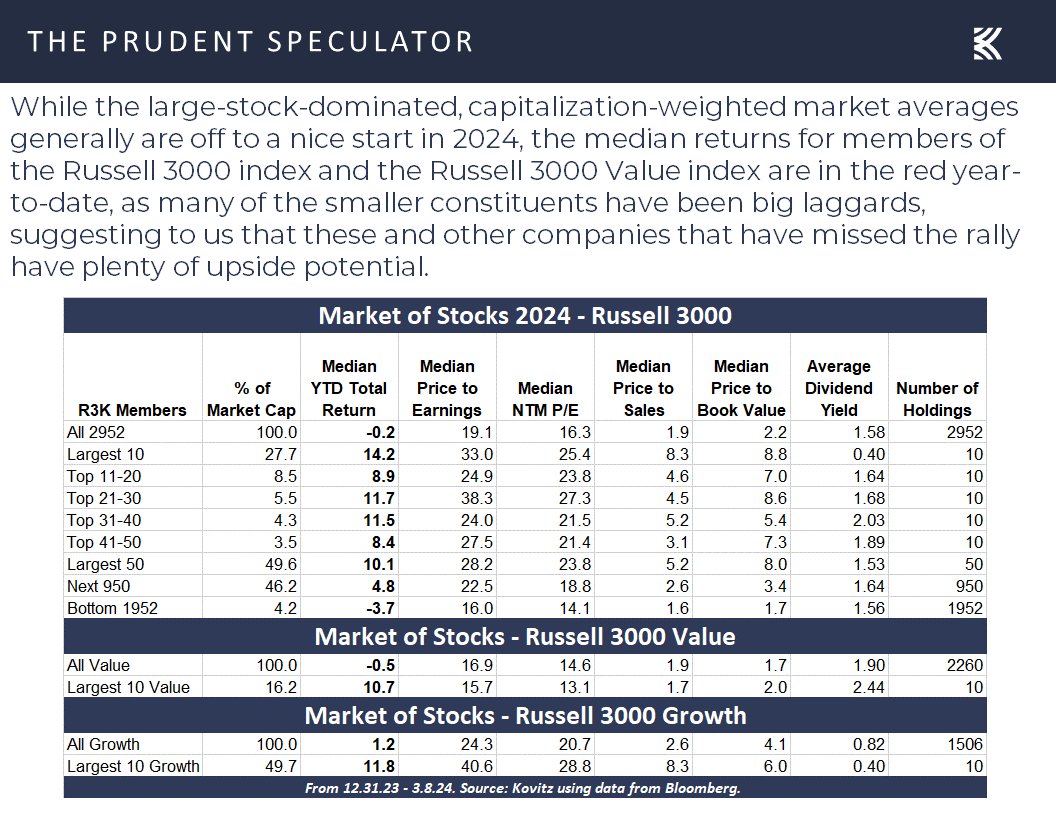

Market of Stocks – Median Stock Still Down on the Year

Stock News – Updates on nine stocks across six different sectors

Interest Rates – Yields Fall; Fed on Track to Cut Rates in the Not-Too Distant Future

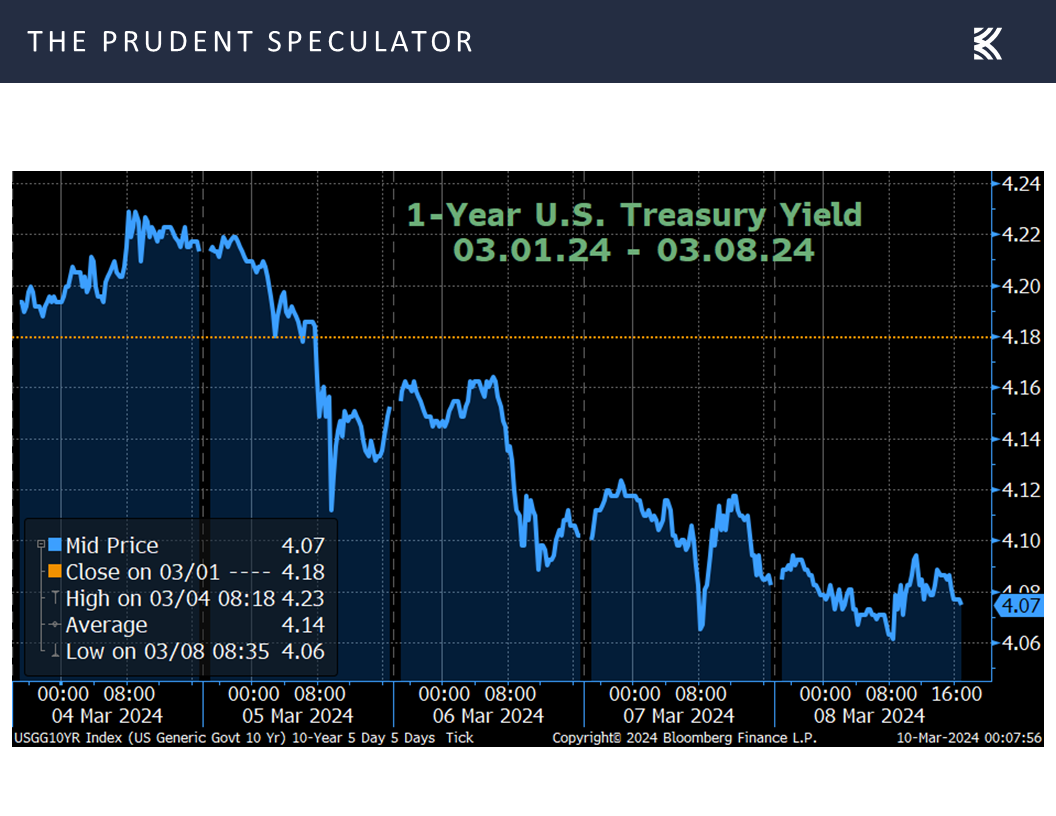

With the yield on the benchmark 10-Year U.S. Treasury dipping to 4.07%, down from 4.18% the week prior,

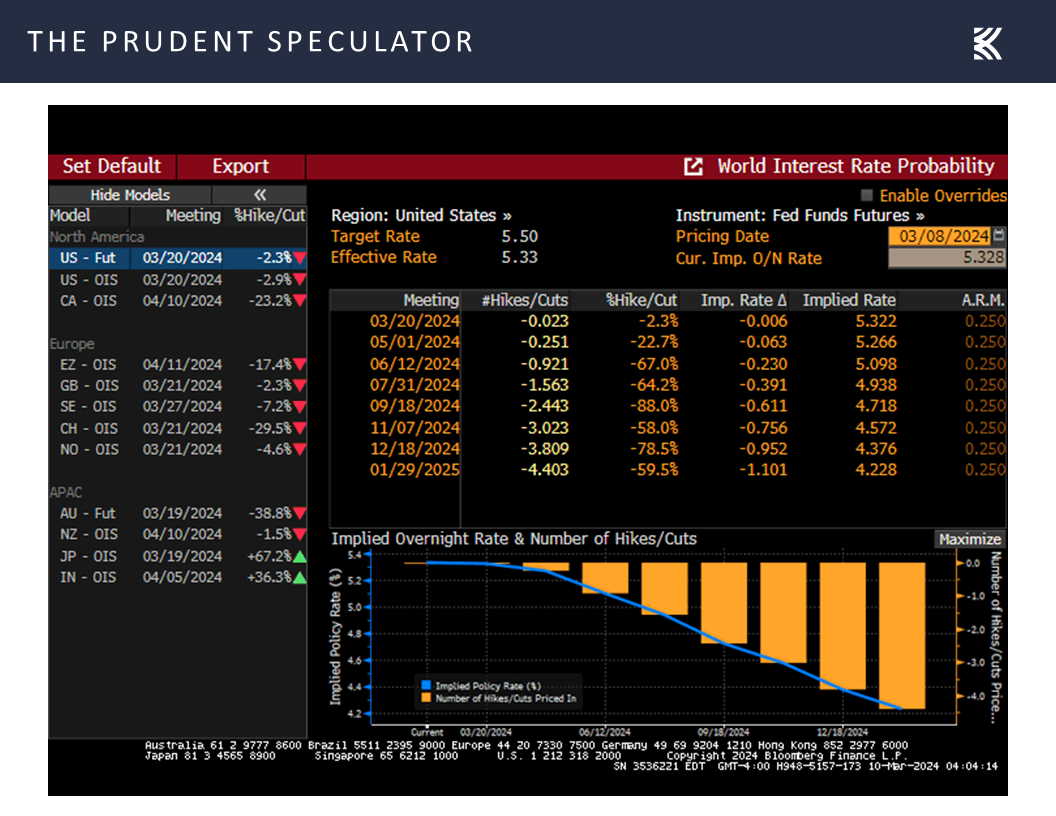

it would seem that bond traders took a glass-half-full view of Jerome H. Powell’s trip to Capitol Hill last week, as the betting on the year-end Fed Funds rate targeted 4.38%, down from 4.42% at the end of the preceding week.

it would seem that bond traders took a glass-half-full view of Jerome H. Powell’s trip to Capitol Hill last week, as the betting on the year-end Fed Funds rate targeted 4.38%, down from 4.42% at the end of the preceding week.

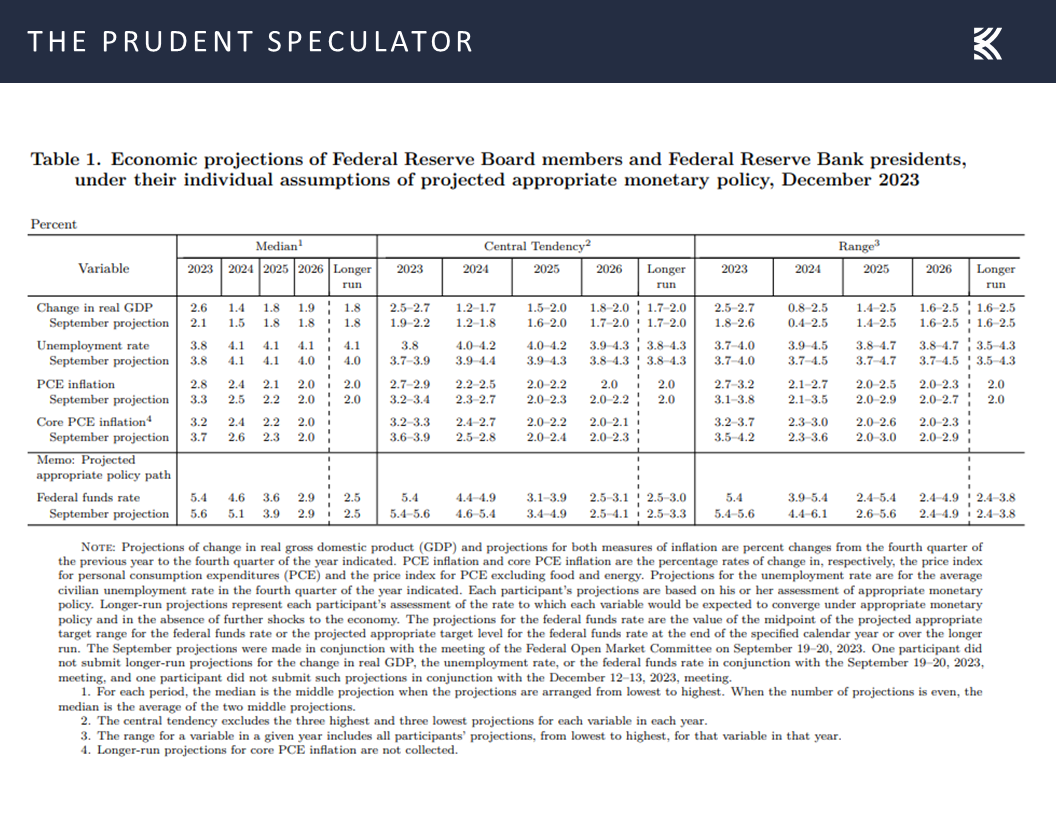

On the subject of potential interest rate cuts, the Fed Chair told the House Financial Services Committee, “We want to see a little bit more data so that we can become confident. We’re not looking for better inflation readings than we’ve had. We’re just looking for more of them.” Of course, most are of the mind that rates will be coming down. The question is the timing and frequency of the reductions as the last Fed projections (now nearly three months old) suggested a 4.6% year-end Fed Funds rate.

Econ News – Mixed Numbers but Modest GDP Growth in ’24 Still Likely

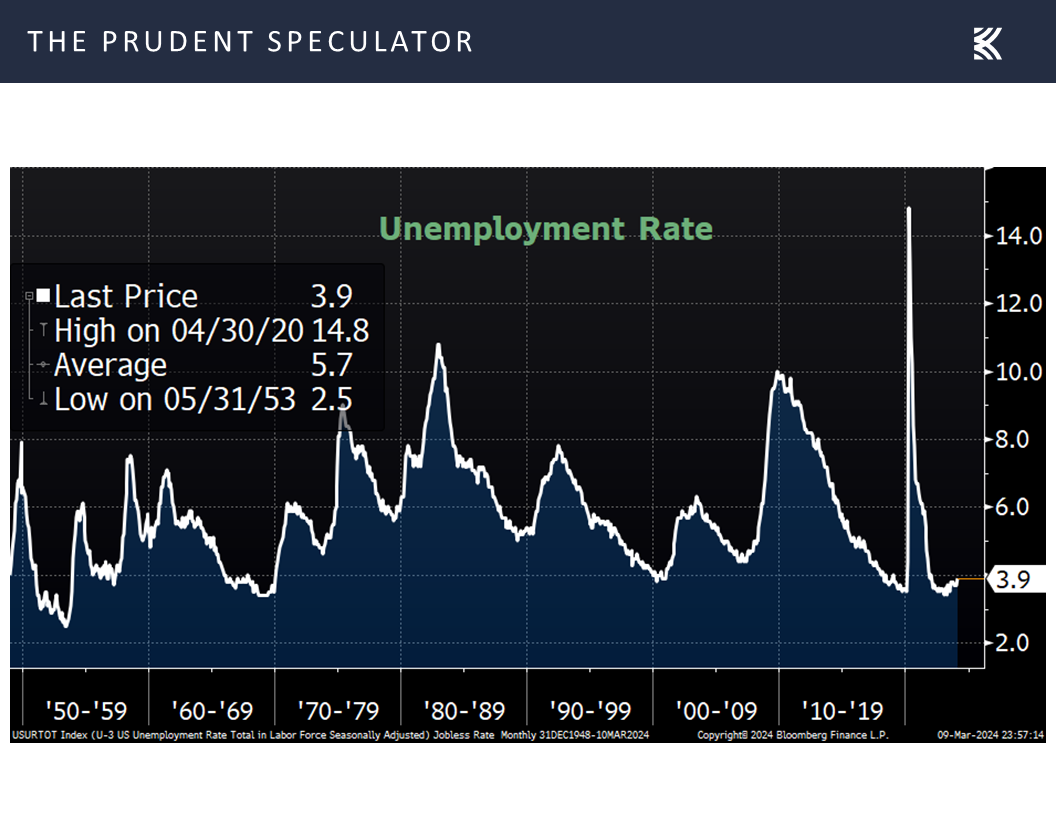

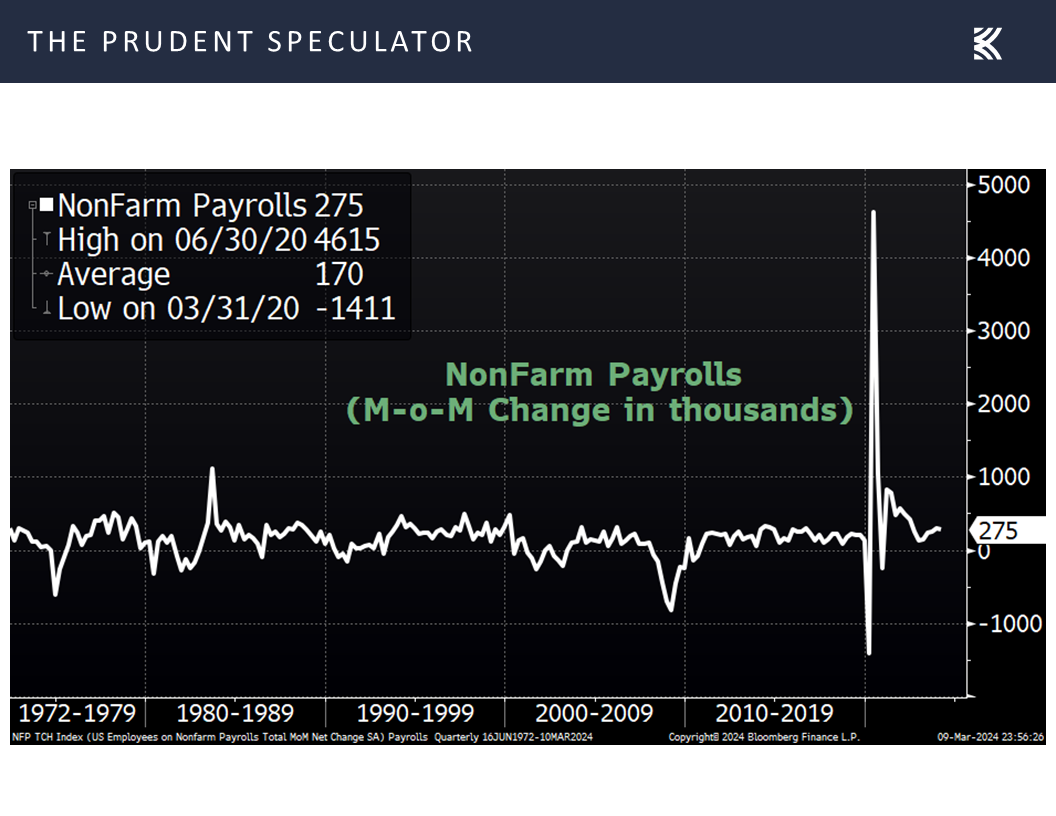

Those Fed forecasts also called for a 4.1% unemployment rate and last week’s big labor numbers for February saw a higher-than-expected jobless figure of 3.9%,

…even as the tally of new payrolls exceeded expectations of 200,000 with an increase of 275,000.

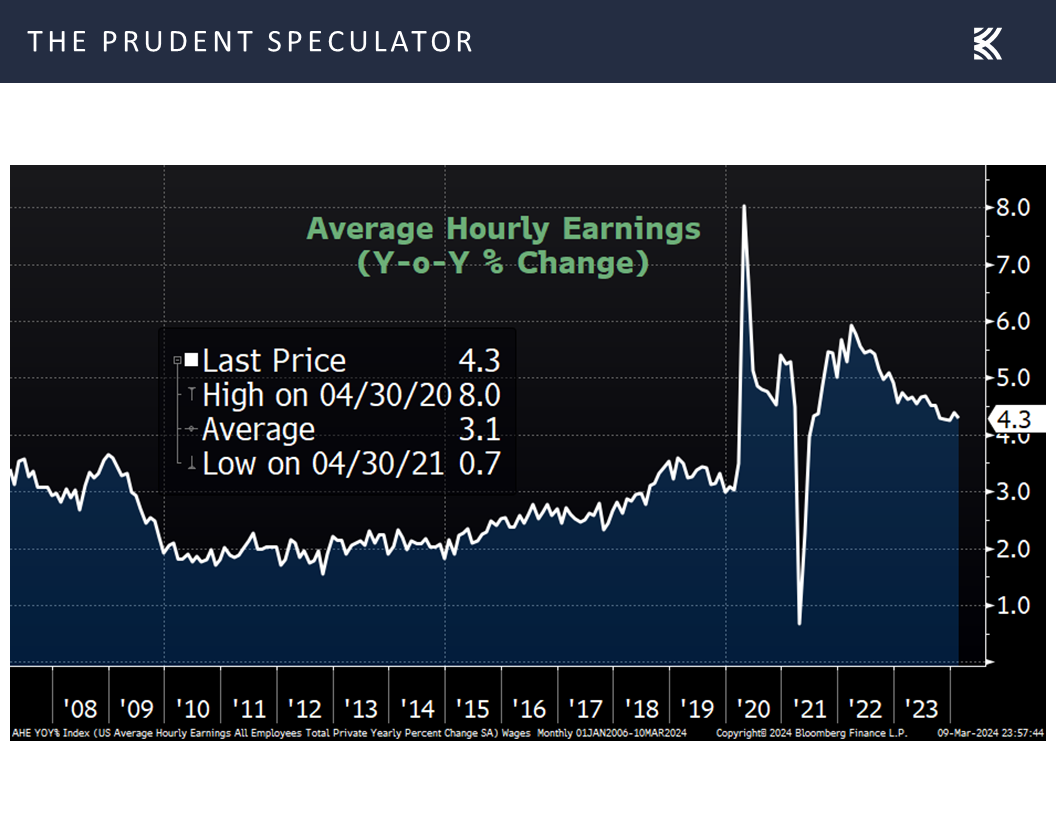

Wage growth on a year-over-year basis of 4.3% was in line with expectations and was down from 4.5% in January, supporting the argument that inflation data continues to head in the right direction.

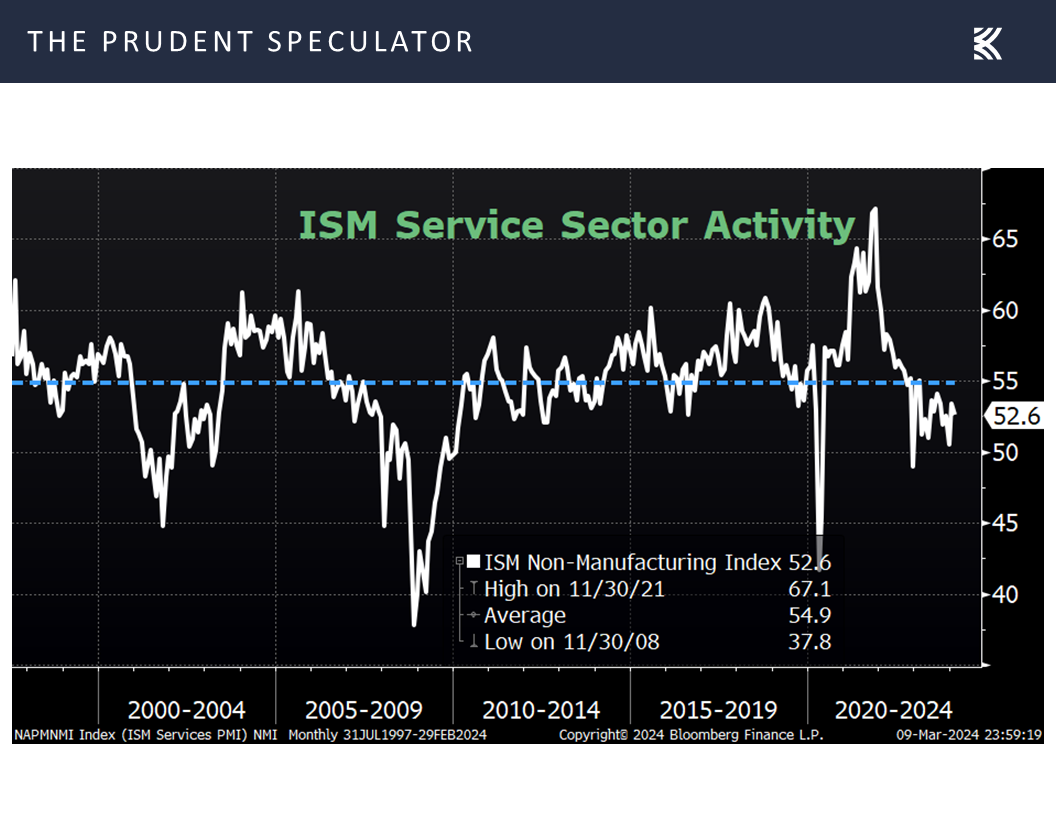

On the GDP side of the economic equation, the estimates from the Fed for 1.4% real (inflation-adjusted) growth this year remains reasonable. After all, the important Institute for Supply Management reading on the health of the services sector for February came in at 52.6, down from 53.4 in January and below estimates of 53.0. The keeper of the non-manufacturing gauge explained, “A Services PMI® above 49 percent, over time, generally indicates an expansion of the overall economy. Therefore, the February Services PMI® indicates the overall economy is growing for the 14th consecutive month after one month of contraction in December 2022. The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for February (52.6 percent) corresponds to a 1.2-percent increase in real gross domestic product (GDP) on an annualized basis.”

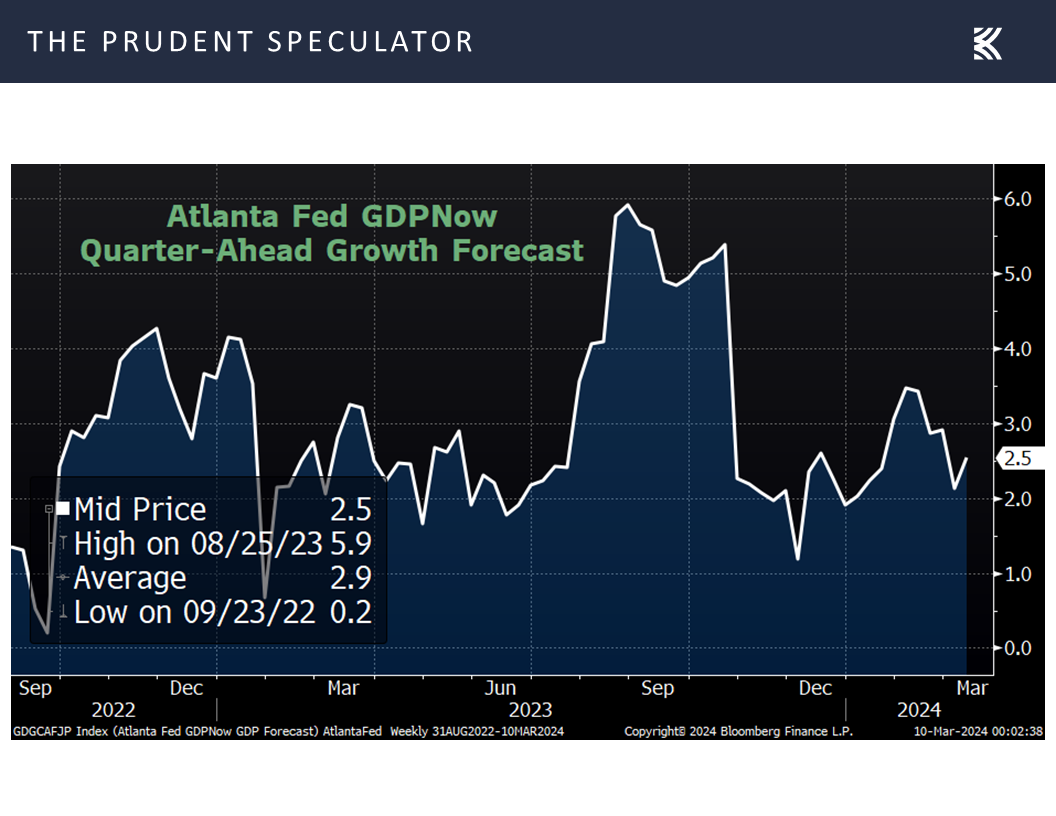

No doubt, given that the latest projection for Q1 real GDP growth from the Atlanta Fed stood at 2.5%,

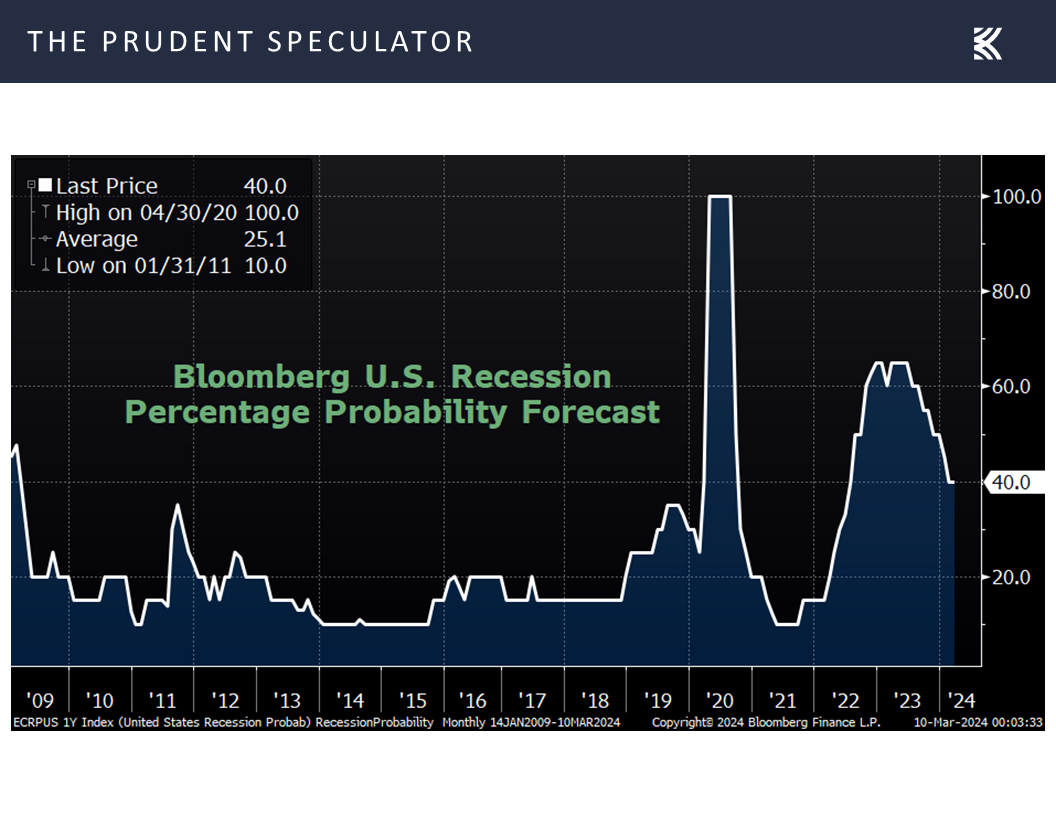

…the thinking is that the economy will expand moderately as we move through the year, and the consensus is that a recession will not take place as evidenced by Bloomberg’s current tabulation of the odds of contraction this year standing at 40%.

Corporate Profits – Solid Growth this Year and Next the Forecast

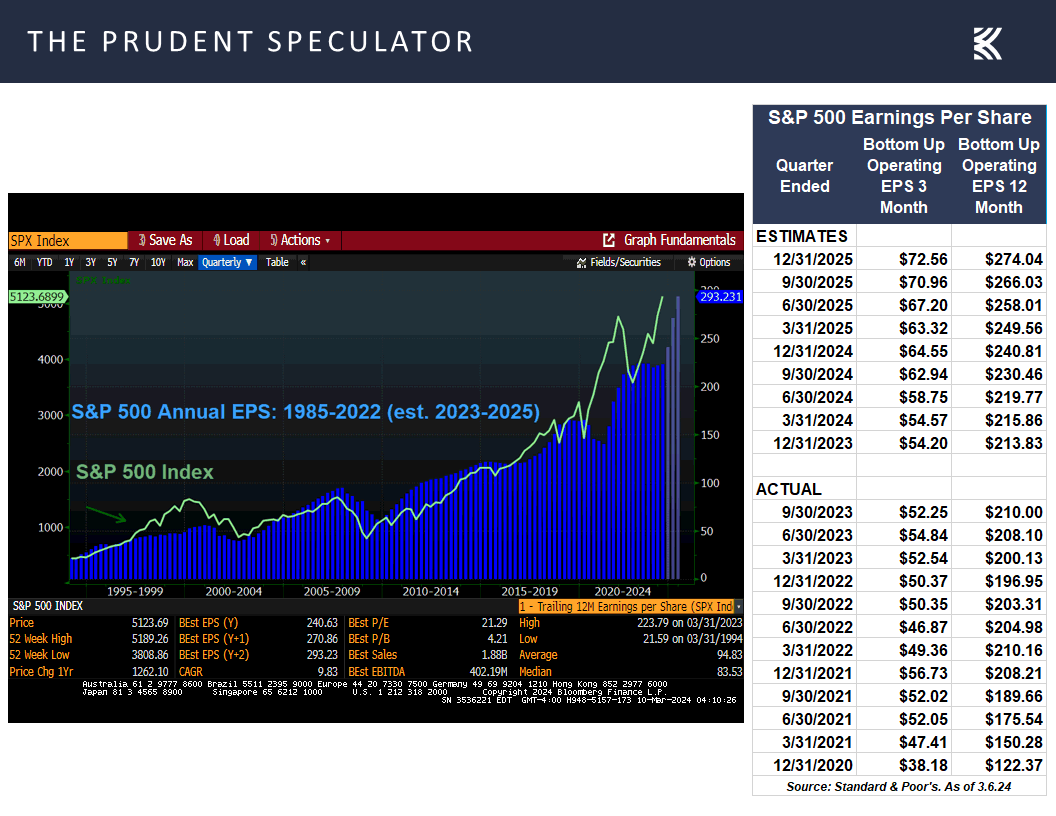

Certainly, there is no recession on the horizon on the corporate profit front, at least according to current EPS projections from Standard & Poor’s for 2024 and 2025

Valuations – Value Stocks Attractively Priced

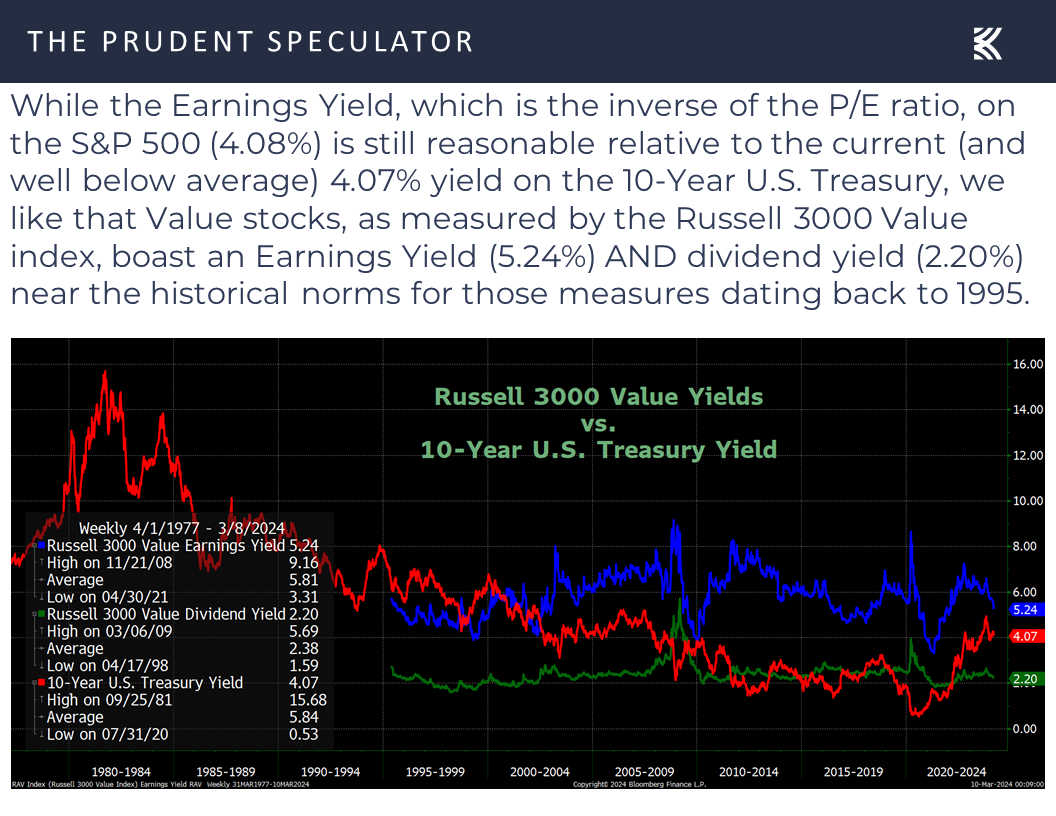

which we think bolsters the earnings/dividend yields valuation argument for reasonably priced stocks like those that we have long championed,

as well as the relative P/E ratio argument.

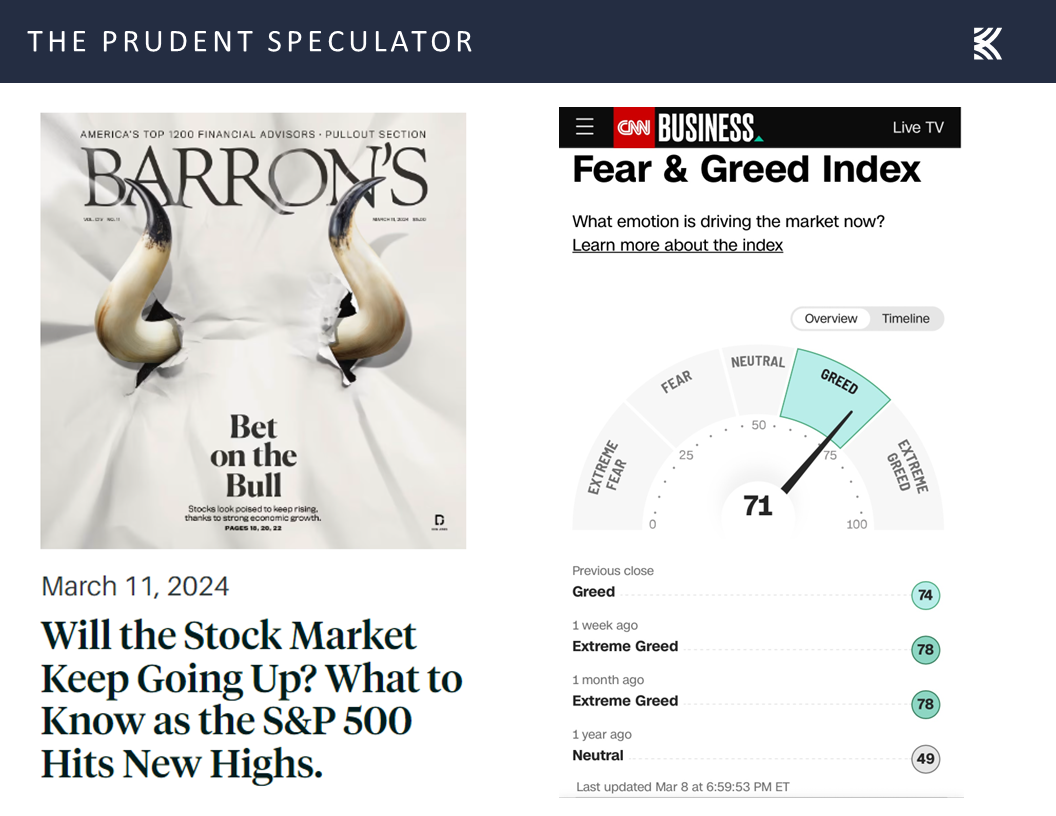

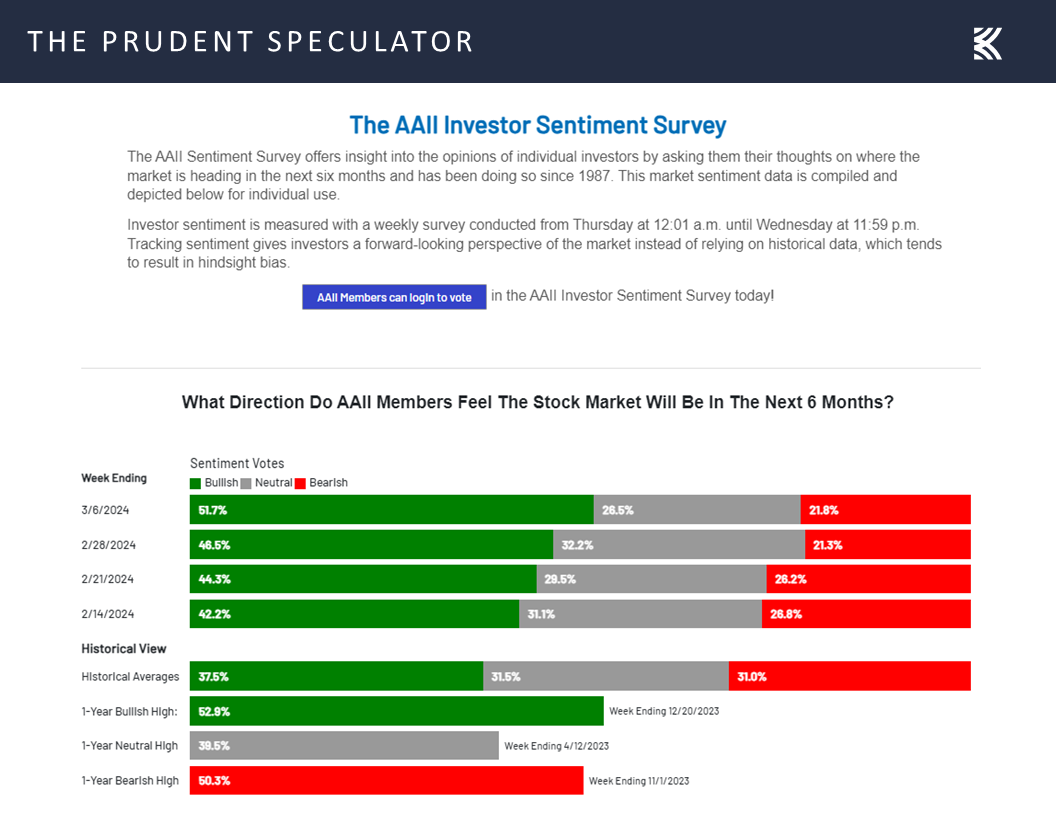

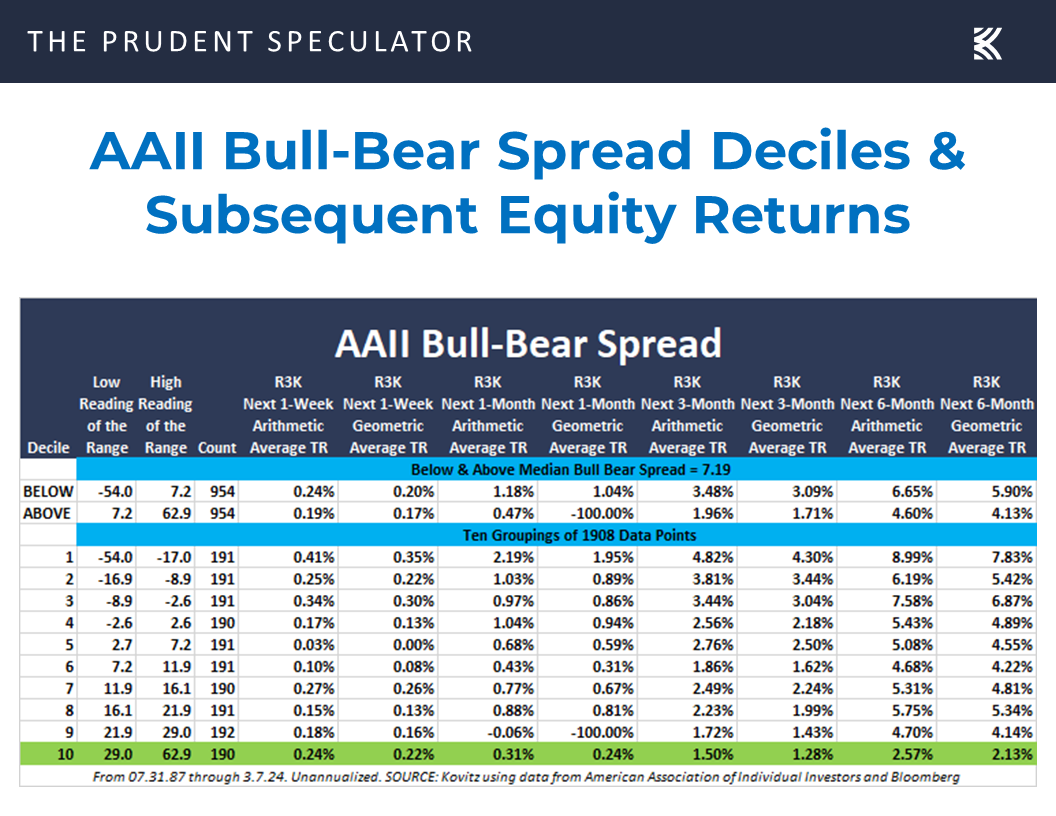

Sentiment – Lots of Optimism

True, some have become concerned that there is too much optimism for stocks, be it this weekend’s bullish Barron’s cover story, the CNN Fear & Greed index,

or the latest weekly AAII Investor Sentiment survey,

but 37 years of market history supports sticking with stocks no matter the mood of Main Street.

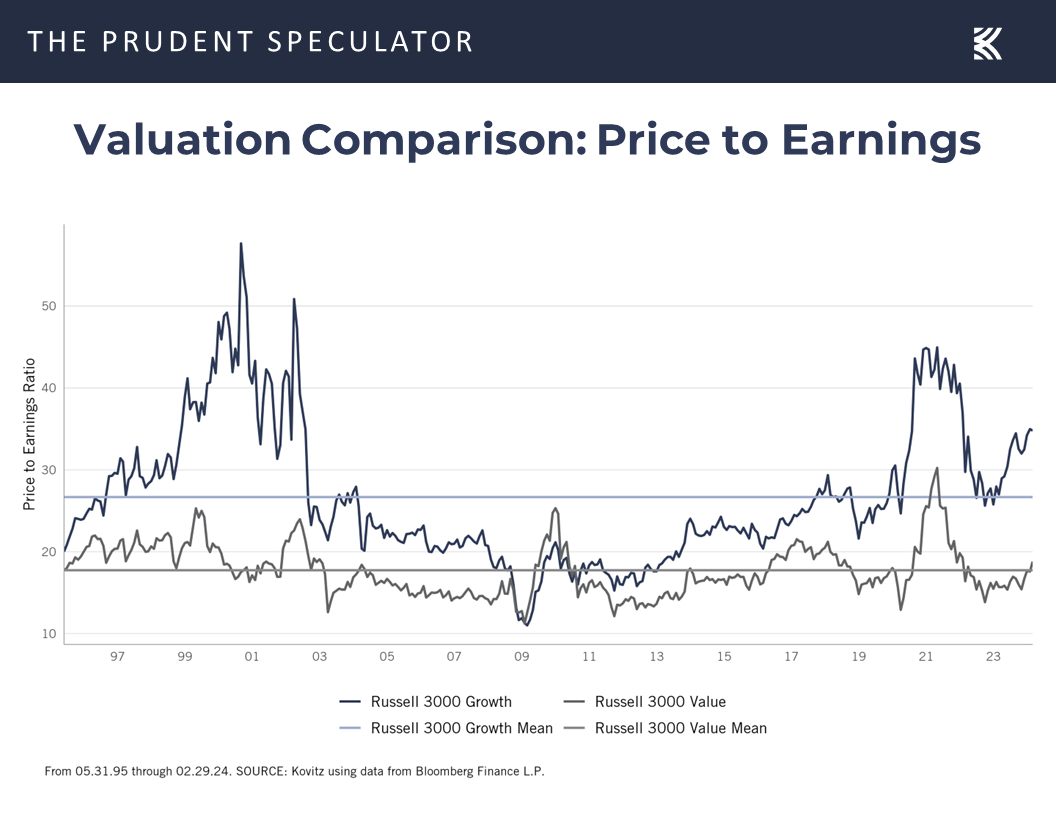

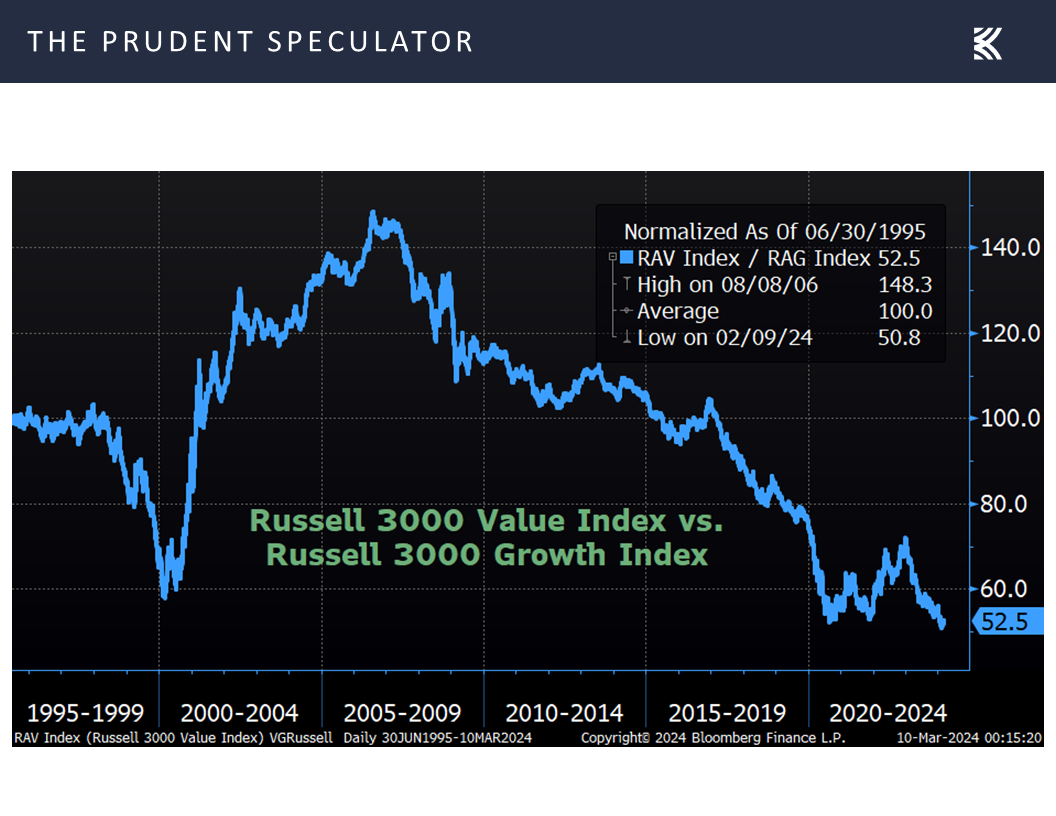

This is especially true today, in our view, as despite a solid five days of outperformance for Value stocks last week, the Russell 3000 Value index remains near its lowest relative value ever versus the Russell 3000 Growth index,

Market of Stocks – Median Stock Still Down on the Year

while the median stock this year is still in the red.

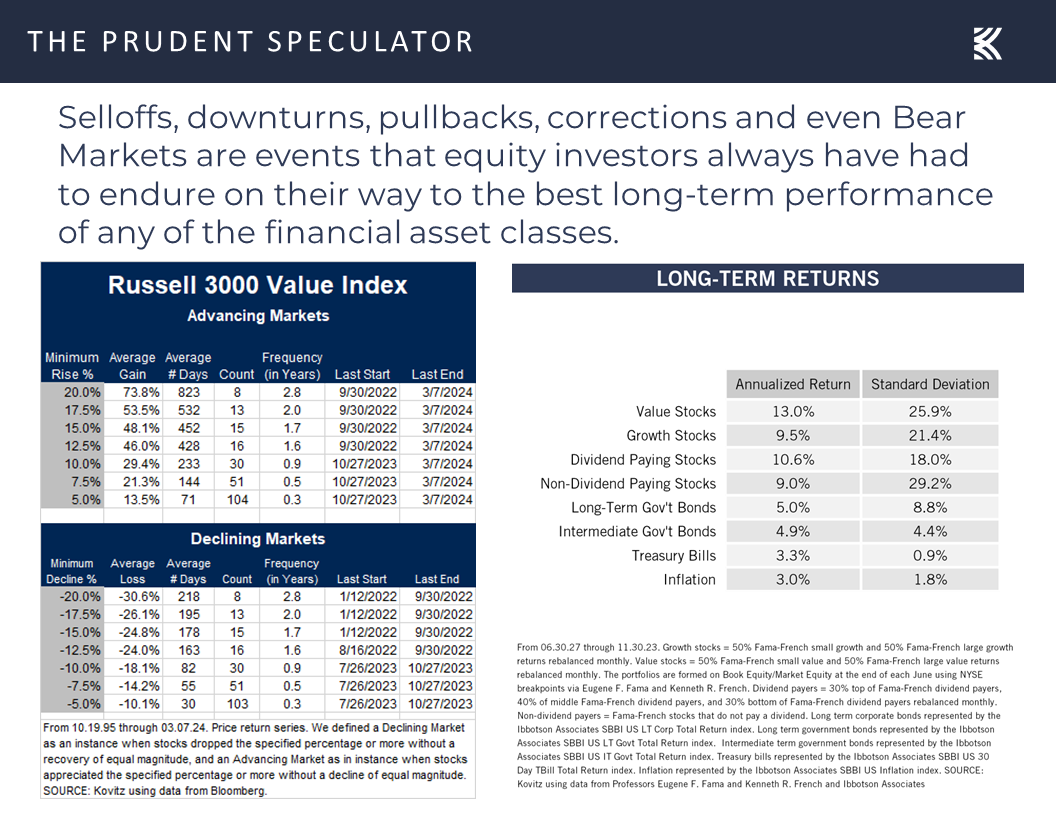

We always are braced for downside volatility as ups and downs are what investors must accept in order to achieve terrific long-term returns from equities,

but we sleep well at night with our risk mitigation efforts that include buying and patiently harvesting inexpensively priced stocks,

but we sleep well at night with our risk mitigation efforts that include buying and patiently harvesting inexpensively priced stocks,

and maintaining a long-term time horizon.

Stock News – Updates on nine stocks across six different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Interest Rates, Corporate Profits, Valuations and more Stock News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss interest rates, corporate profits, valuations and more stock news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Newsletter Trades – Numerous Transactions Across 4 Portfolios

Interest Rates – Yields Fall; Fed on Track to Cut Rates in the Not-Too Distant Future

Econ News – Mixed Numbers but Modest GDP Growth in ’24 Still Likely

Corporate Profits – Solid Growth this Year and Next the Forecast

Valuations – Value Stocks Attractively Priced

Sentiment – Lots of Optimism

Market of Stocks – Median Stock Still Down on the Year

Stock News – Updates on nine stocks across six different sectors

Interest Rates – Yields Fall; Fed on Track to Cut Rates in the Not-Too Distant Future

With the yield on the benchmark 10-Year U.S. Treasury dipping to 4.07%, down from 4.18% the week prior,

On the subject of potential interest rate cuts, the Fed Chair told the House Financial Services Committee, “We want to see a little bit more data so that we can become confident. We’re not looking for better inflation readings than we’ve had. We’re just looking for more of them.” Of course, most are of the mind that rates will be coming down. The question is the timing and frequency of the reductions as the last Fed projections (now nearly three months old) suggested a 4.6% year-end Fed Funds rate.

Econ News – Mixed Numbers but Modest GDP Growth in ’24 Still Likely

Those Fed forecasts also called for a 4.1% unemployment rate and last week’s big labor numbers for February saw a higher-than-expected jobless figure of 3.9%,

…even as the tally of new payrolls exceeded expectations of 200,000 with an increase of 275,000.

Wage growth on a year-over-year basis of 4.3% was in line with expectations and was down from 4.5% in January, supporting the argument that inflation data continues to head in the right direction.

On the GDP side of the economic equation, the estimates from the Fed for 1.4% real (inflation-adjusted) growth this year remains reasonable. After all, the important Institute for Supply Management reading on the health of the services sector for February came in at 52.6, down from 53.4 in January and below estimates of 53.0. The keeper of the non-manufacturing gauge explained, “A Services PMI® above 49 percent, over time, generally indicates an expansion of the overall economy. Therefore, the February Services PMI® indicates the overall economy is growing for the 14th consecutive month after one month of contraction in December 2022. The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for February (52.6 percent) corresponds to a 1.2-percent increase in real gross domestic product (GDP) on an annualized basis.”

No doubt, given that the latest projection for Q1 real GDP growth from the Atlanta Fed stood at 2.5%,

…the thinking is that the economy will expand moderately as we move through the year, and the consensus is that a recession will not take place as evidenced by Bloomberg’s current tabulation of the odds of contraction this year standing at 40%.

Corporate Profits – Solid Growth this Year and Next the Forecast

Certainly, there is no recession on the horizon on the corporate profit front, at least according to current EPS projections from Standard & Poor’s for 2024 and 2025

Valuations – Value Stocks Attractively Priced

which we think bolsters the earnings/dividend yields valuation argument for reasonably priced stocks like those that we have long championed,

as well as the relative P/E ratio argument.

Sentiment – Lots of Optimism

True, some have become concerned that there is too much optimism for stocks, be it this weekend’s bullish Barron’s cover story, the CNN Fear & Greed index,

or the latest weekly AAII Investor Sentiment survey,

but 37 years of market history supports sticking with stocks no matter the mood of Main Street.

This is especially true today, in our view, as despite a solid five days of outperformance for Value stocks last week, the Russell 3000 Value index remains near its lowest relative value ever versus the Russell 3000 Growth index,

Market of Stocks – Median Stock Still Down on the Year

while the median stock this year is still in the red.

We always are braced for downside volatility as ups and downs are what investors must accept in order to achieve terrific long-term returns from equities,

and maintaining a long-term time horizon.

Stock News – Updates on nine stocks across six different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.