The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s Market Commentary, we discuss Moody’s, Recessions, Historical Perspective and more Stock News. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Portfolio Trades – Trimmed NRG in TPS Portfolio

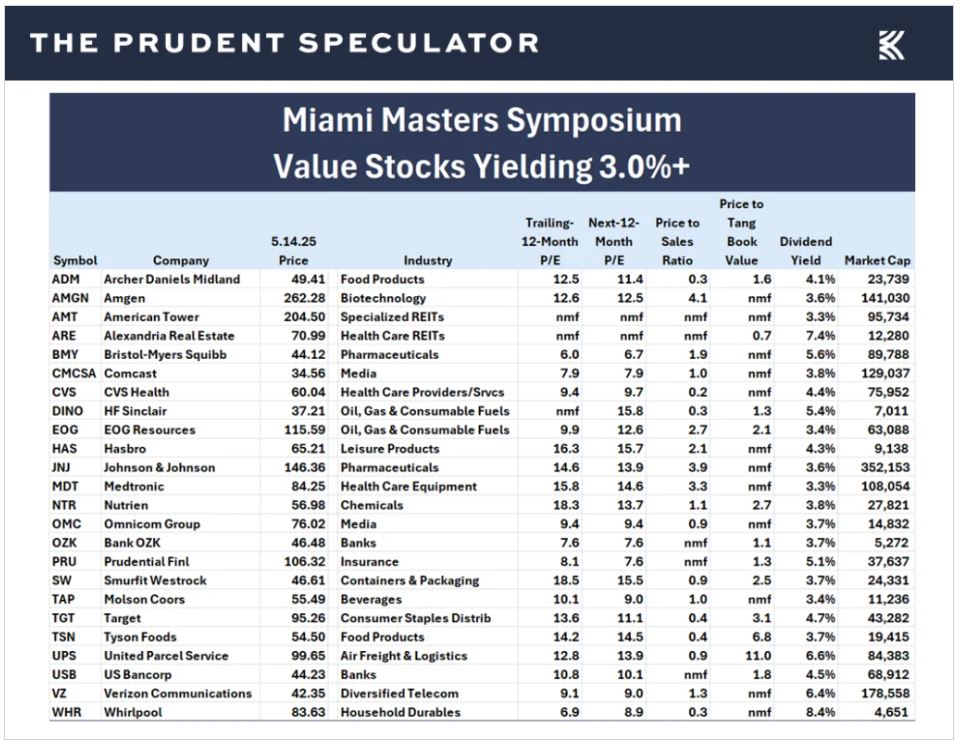

Miami Masters Symposium – 24 Undervalued, 3%+ Yielders

Short-Term Predictions – Yet Another Example of Why the Only Problem with Market Timing is Getting the Timing Right

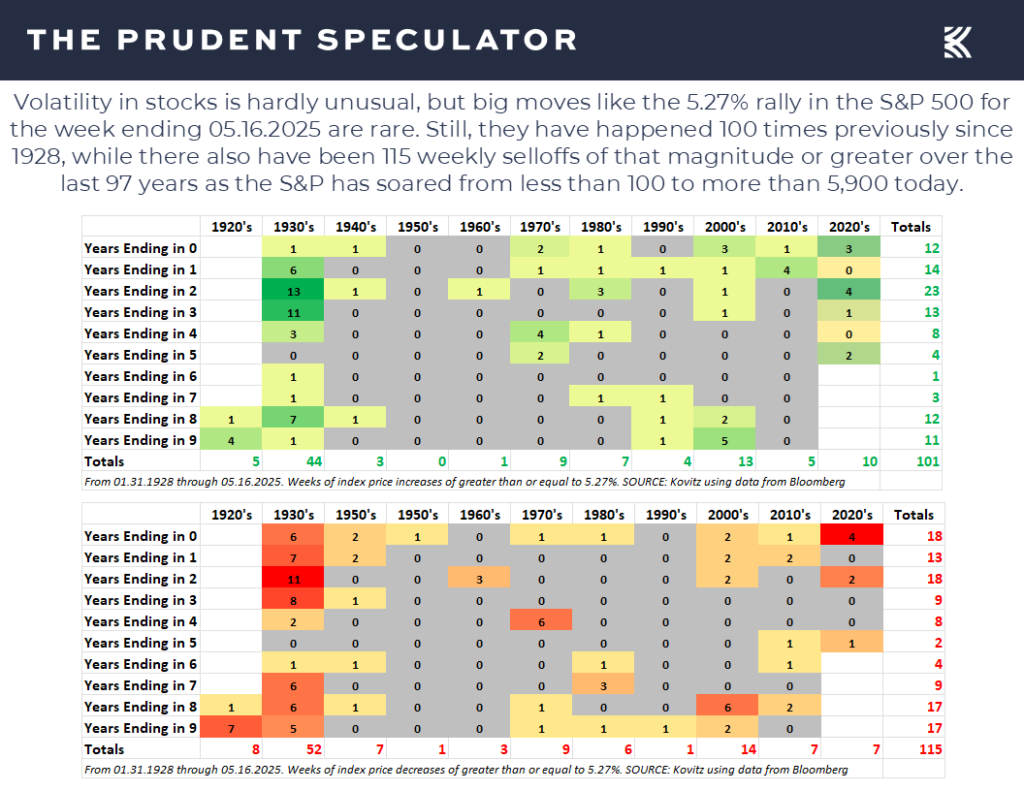

Volatility – 101st Best Week of the Last Century

Historical Perspective – Plenty of Scary Events, but Long-Term Trend is Up

Econ News – Mixed Numbers but Growth Still the Forecast

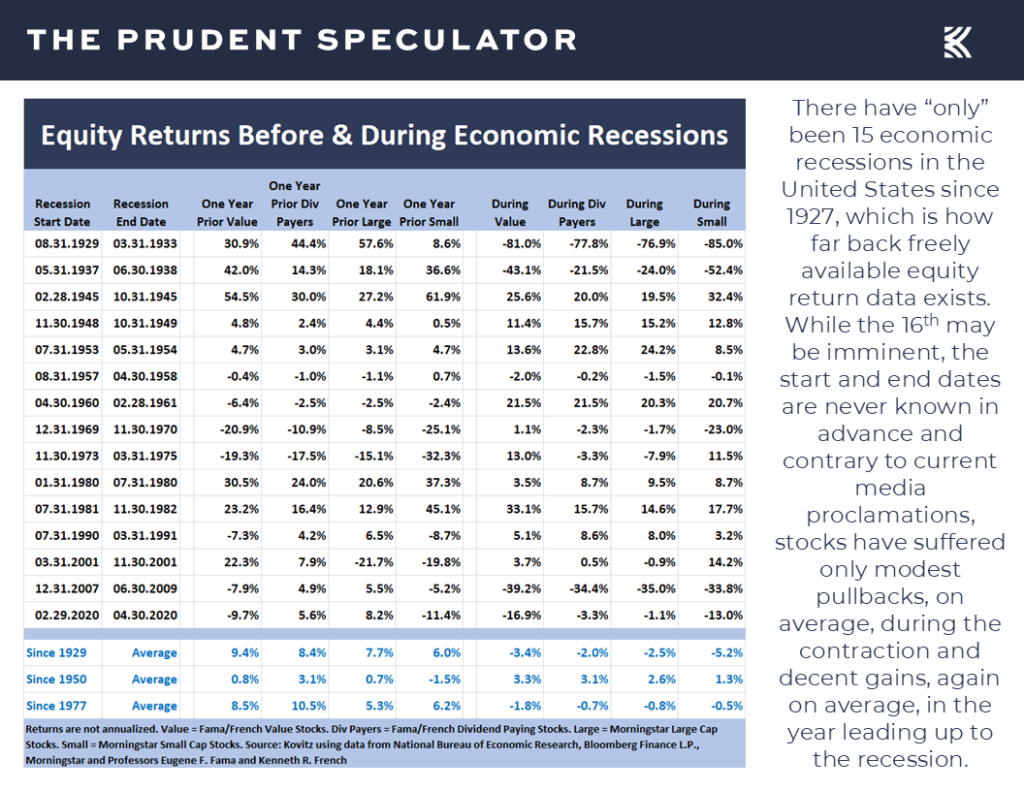

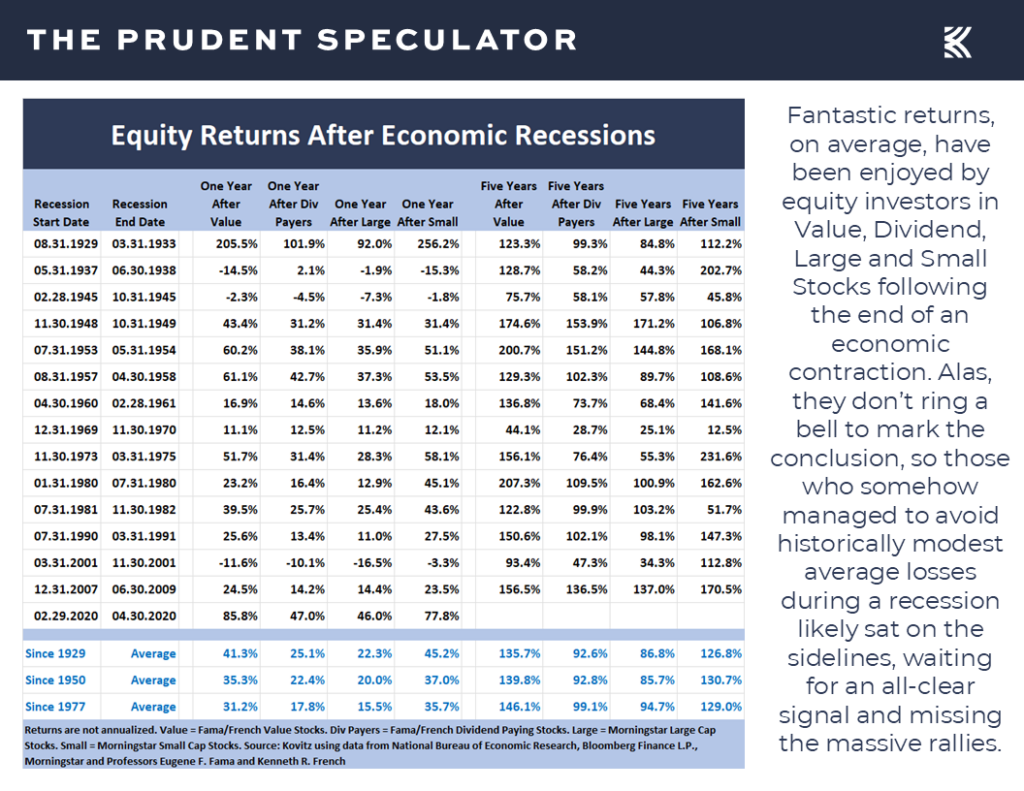

Recessions – Risk Has Jumped, But History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

Inflation – Lower-than-Expected CPI & PPI

Valuations – Attractive Metrics on our Portfolios

Moody’s Downgrades U.S. Credit Rating – History Lesson: S&P & Fitch

Stock News – Comments on CAH, ELV, CVS, AEO, HMC, CSCO, ALIZY, SIEGY & WMT

Miami Masters Symposium – 24 Undervalued, 3%+ Yielders

Your editor spoke at the Miami Masters Symposium on Friday, with the Sleeping Better at Night: The Value of Dividends presentation offering 24 undervalued stocks with yields of at least 3%.

Short-Term Predictions – Yet Another Example of Why the Only Problem with Market Timing is Getting the Timing Right

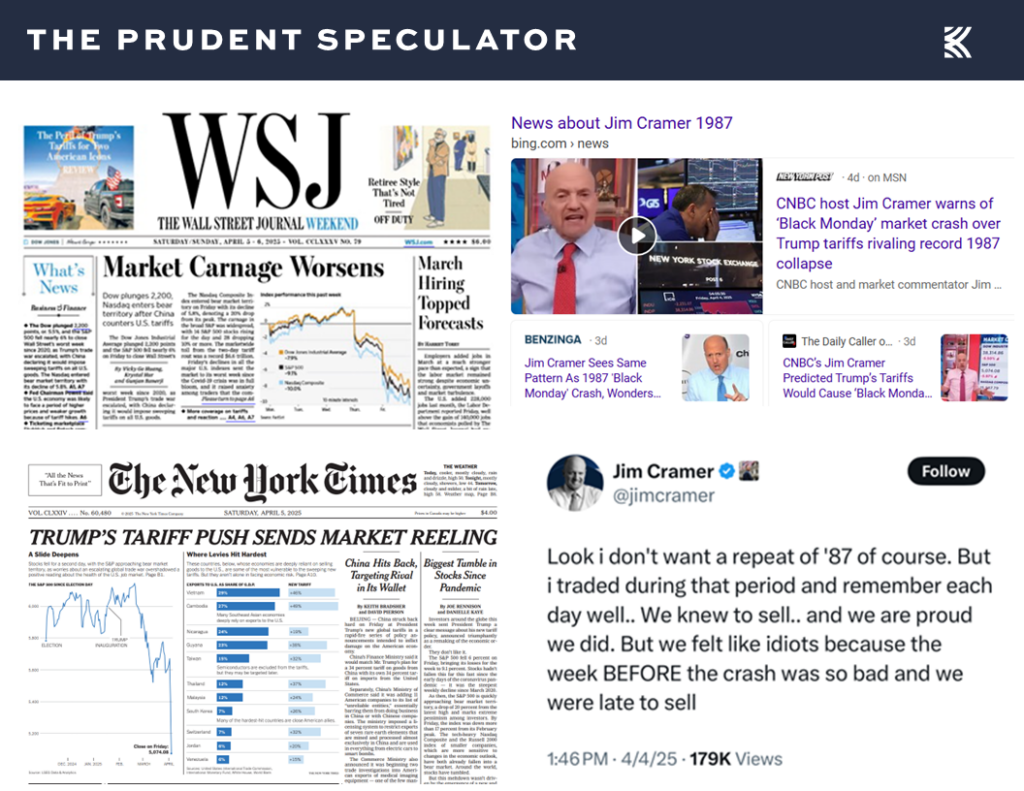

This event was again interesting in that there were a bevy of speakers who seemed very good at touting their successful investment calls, including evidently staying the course six weeks ago when stocks were cratering and CNBC was heralding a new Bear Market.

No doubt, many did keep the faith, but we find that some market pundits are guilty of revisionist history as they learn the hard way that the only problem with market timing is getting the timing right. While not a speaker at the Miami confab, The Wall Street Journal’s Streetwise columnist, who in his defense is charged with making shorter-term market calls, provided a good illustration why the physicist Neils Bohr said, “Prediction is very difficult, especially if it is about the future.”

Volatility – 101st Best Week of the Last Century

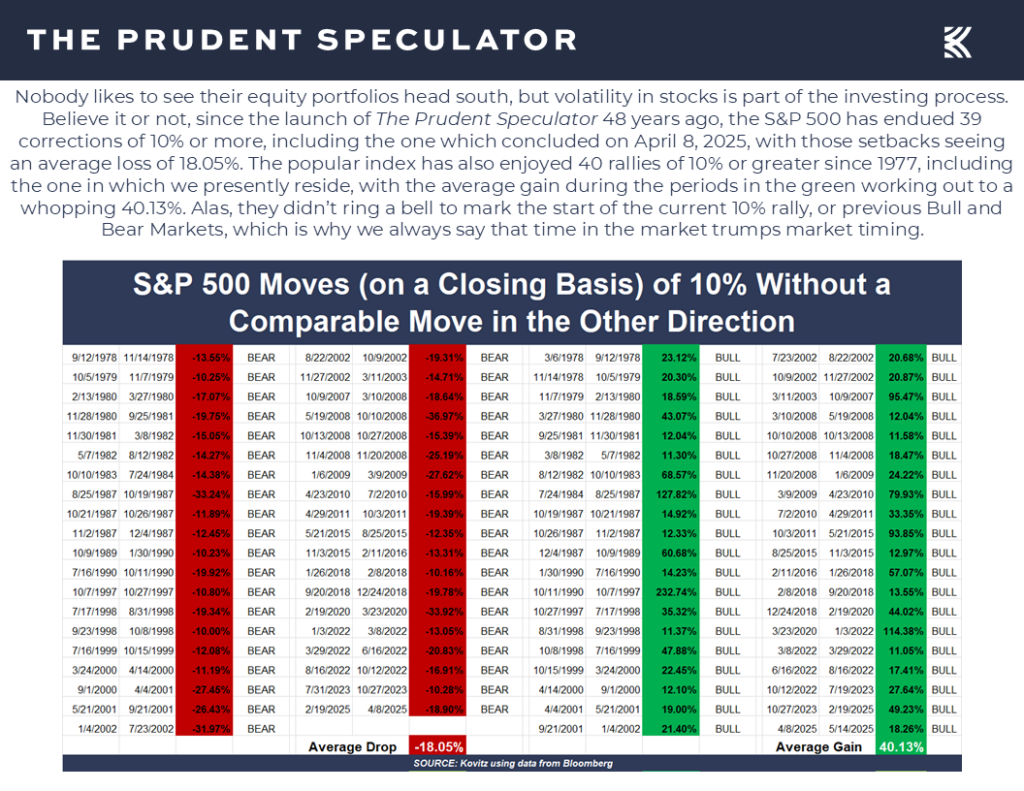

After all, despite writing on April 13, “The damage from Trump’s trade war is far greater than the losses in stocks, bonds and the dollar seen so far,” the take a week ago was that it was clear that stocks had fallen too far when they bottomed on April 8 AND that they were up too much on May 10. The column appeared just in time for the equity markets to soar over the next five days, with the S&P 500’s advance of 5.27% last week the 101st best weekly gain over the last 97+ years.

To be sure, more progress on the global trade front, this time with China, positively altered the investment landscape, but equities have proved rewarding no matter what has transpired for the last century,

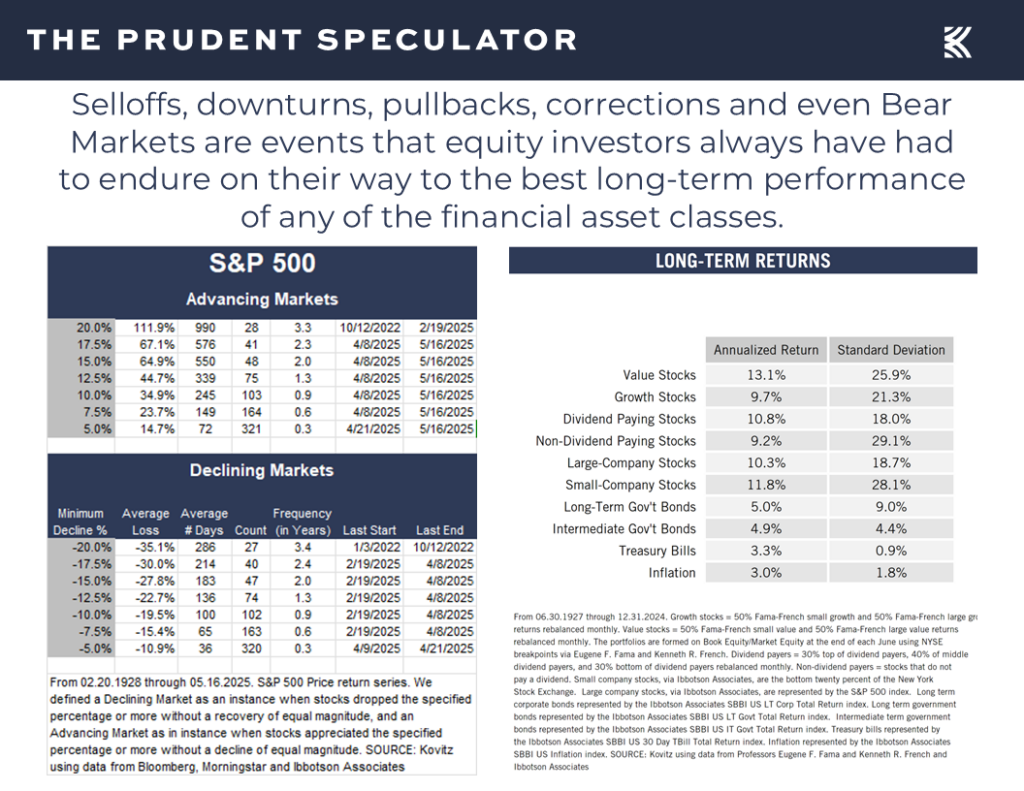

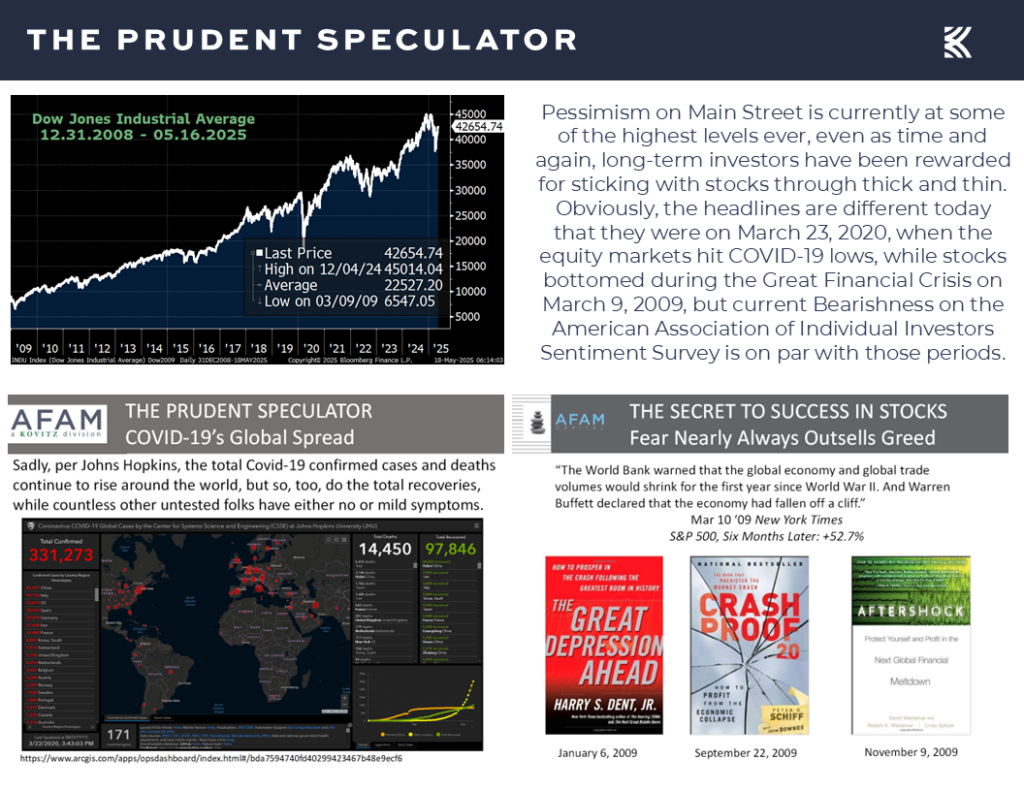

Historical Perspective – Plenty of Scary Events, but Long-Term Trend is Up

with all prior disconcerting events overcome in the fullness of time,

so much so that despite plenty of selloffs along the way, the long-term returns on stocks have been in the 9% to 13% per annum range,

with rallies, including the 40th advance of 10% or more without a decline of comparable magnitude in which we presently reside happening long before any sort of all-clear signal is sounded.

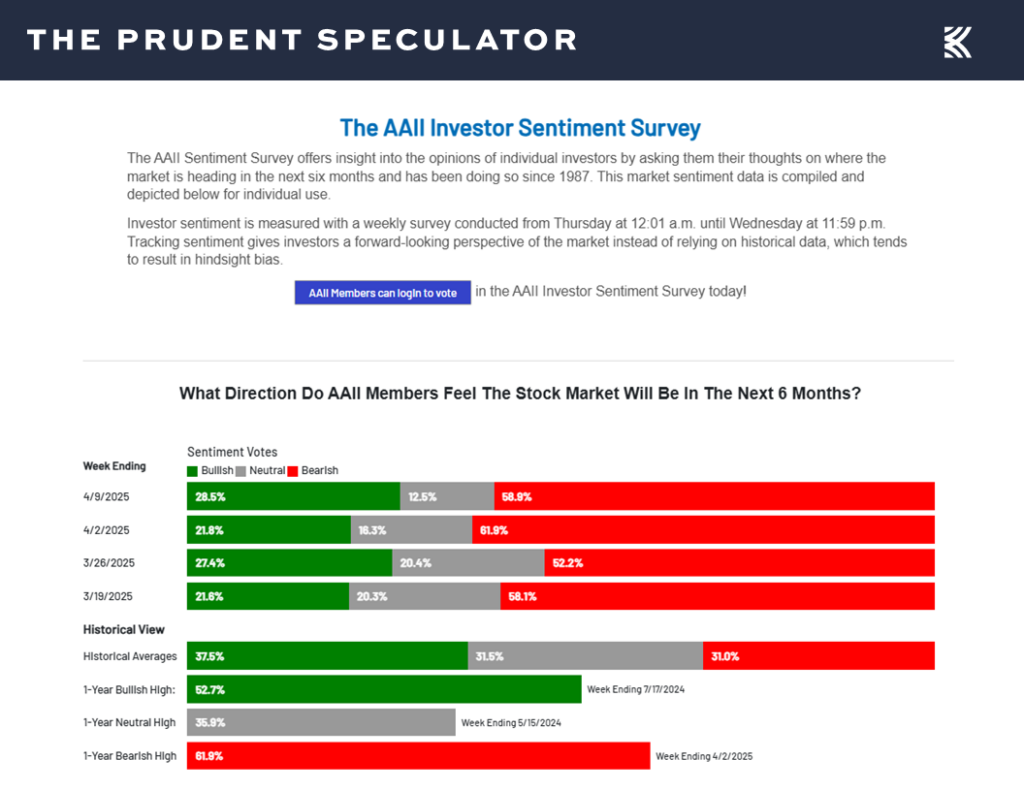

As we have long said, they don’t ring a bell to mark times to enter and exit the equity market. Indeed, those who bailed on stocks during the March/April plunge, when fear levels for investment professionals,

and those on Main Street,

were on par with what was seen during the Great Financial Crisis and during the COVID-19 Pandemic are likely to still sitting on the sidelines.

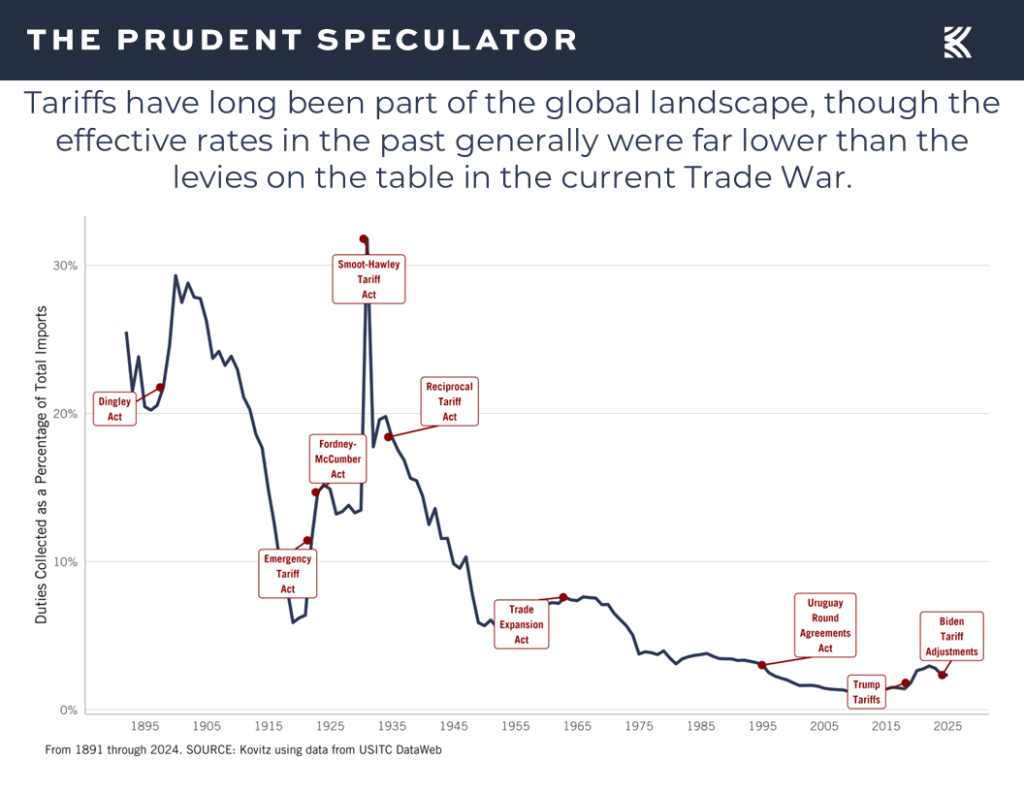

No doubt, tariff uncertainty is still off the charts, even as levies have always been part of the investment backdrop,

Econ News – Mixed Numbers but Growth Still the Forecast

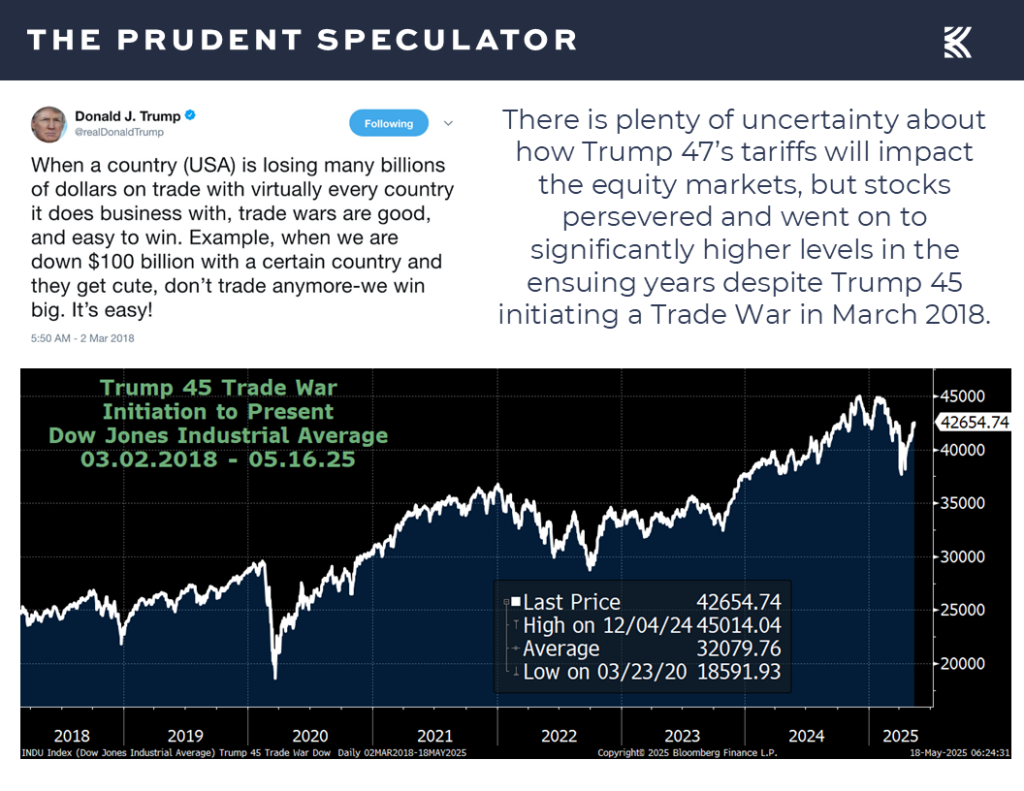

and Trump 45 launched a Trade War with China in March 2018, yet stock prices today are far higher today than they were then,

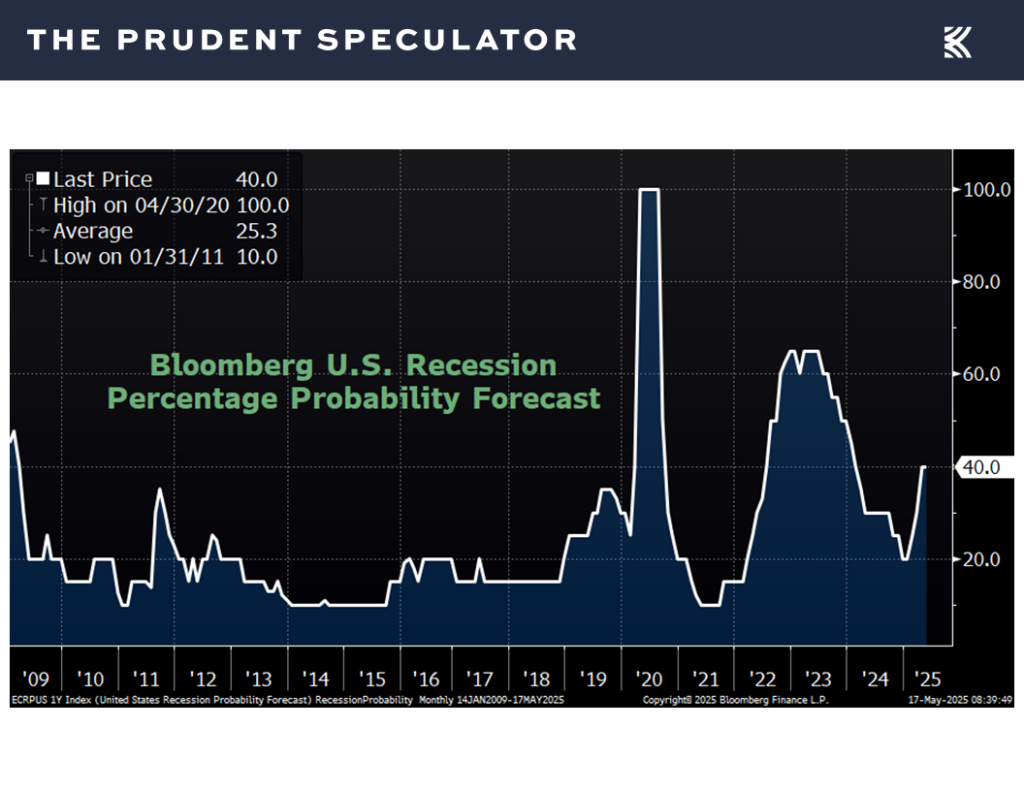

so those worried about a recession don’t exactly have a ton of comfort today, given that the odds of an economic contraction, as tabulated by Bloomberg, remain elevated.

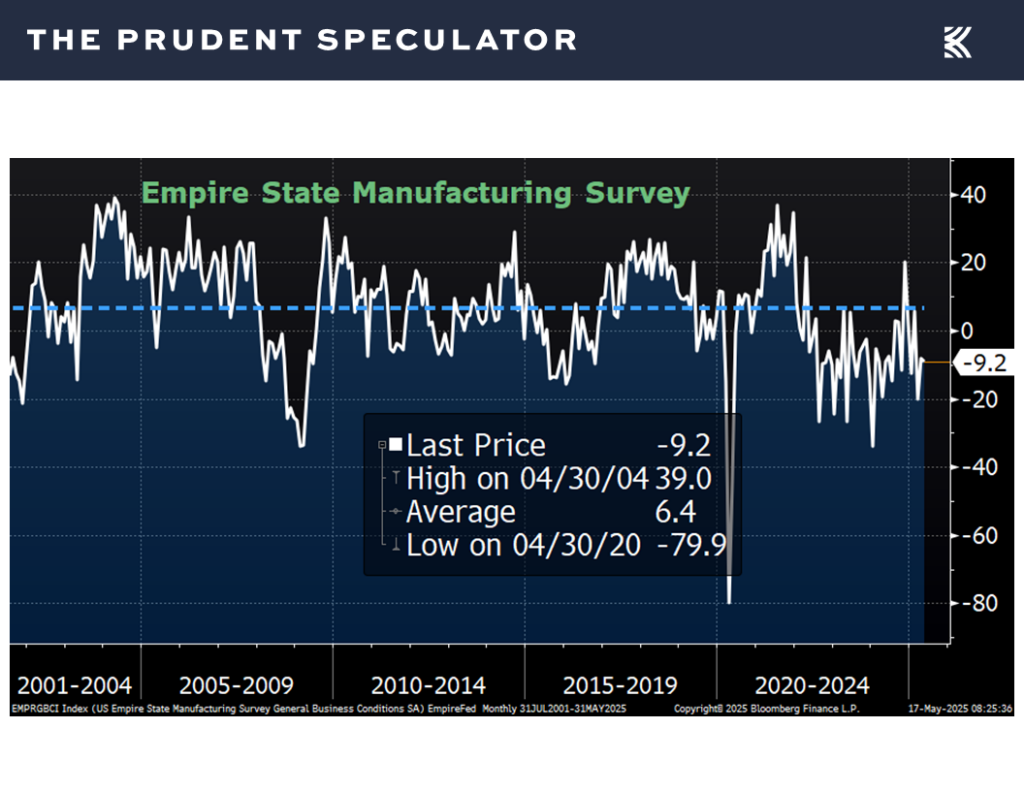

The economic data out last week was not grand with negative readings for May on factory activity in the New York region,

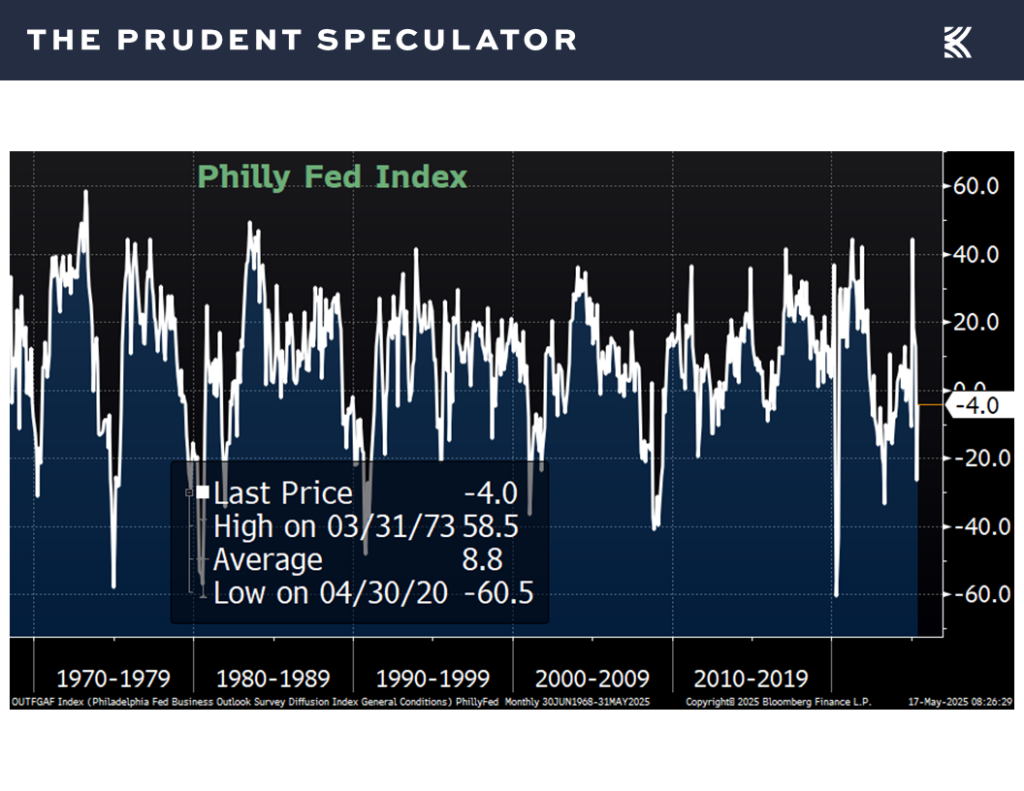

and in the Philadelphia region,

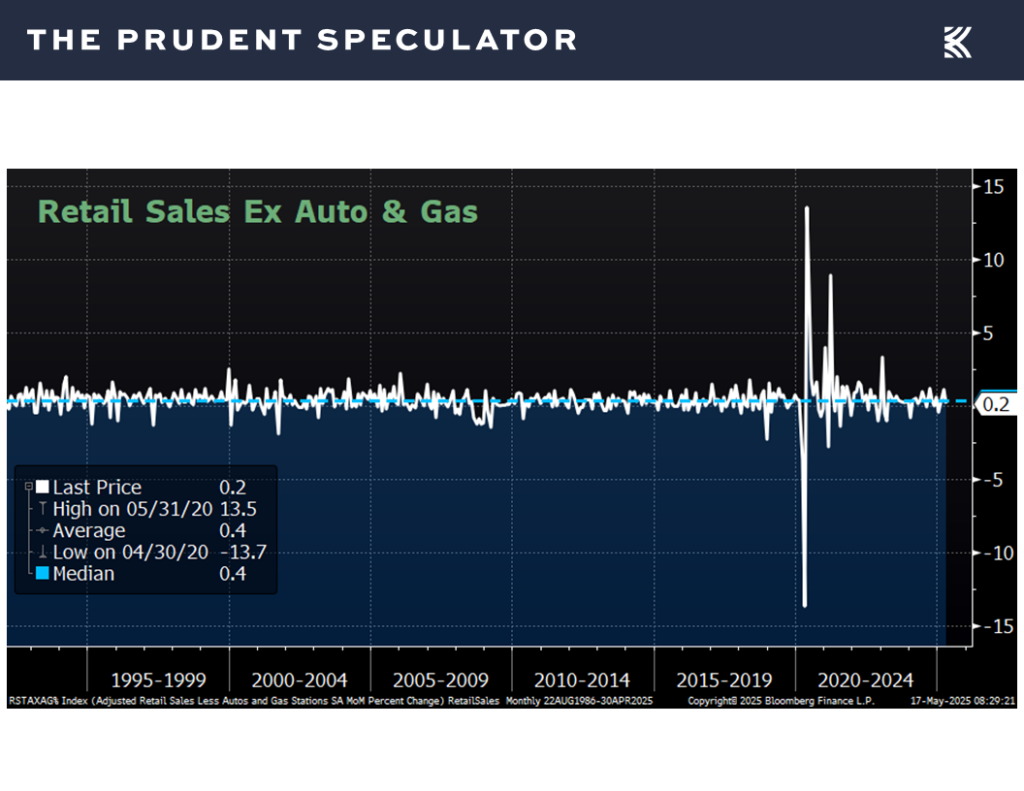

while both retail sales,

and housing starts for April came in below expectations.

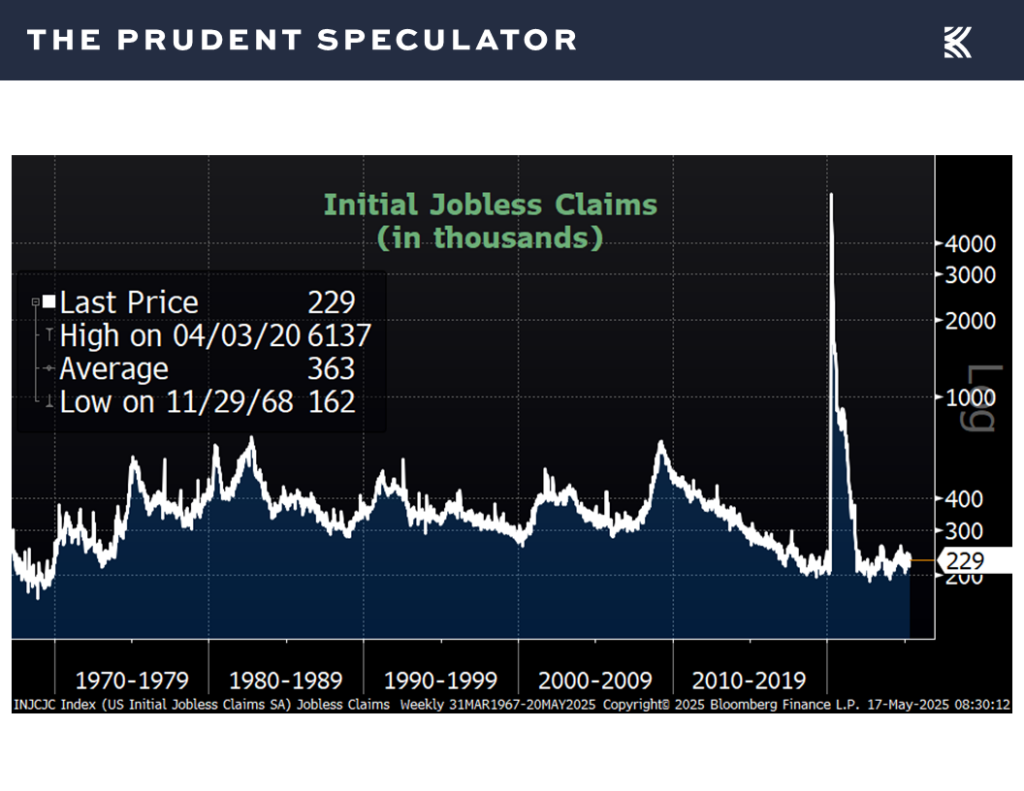

Of course, the labor market continues to show healthy numbers with first-time filings for unemployment benefits remaining near multi-generational lows,

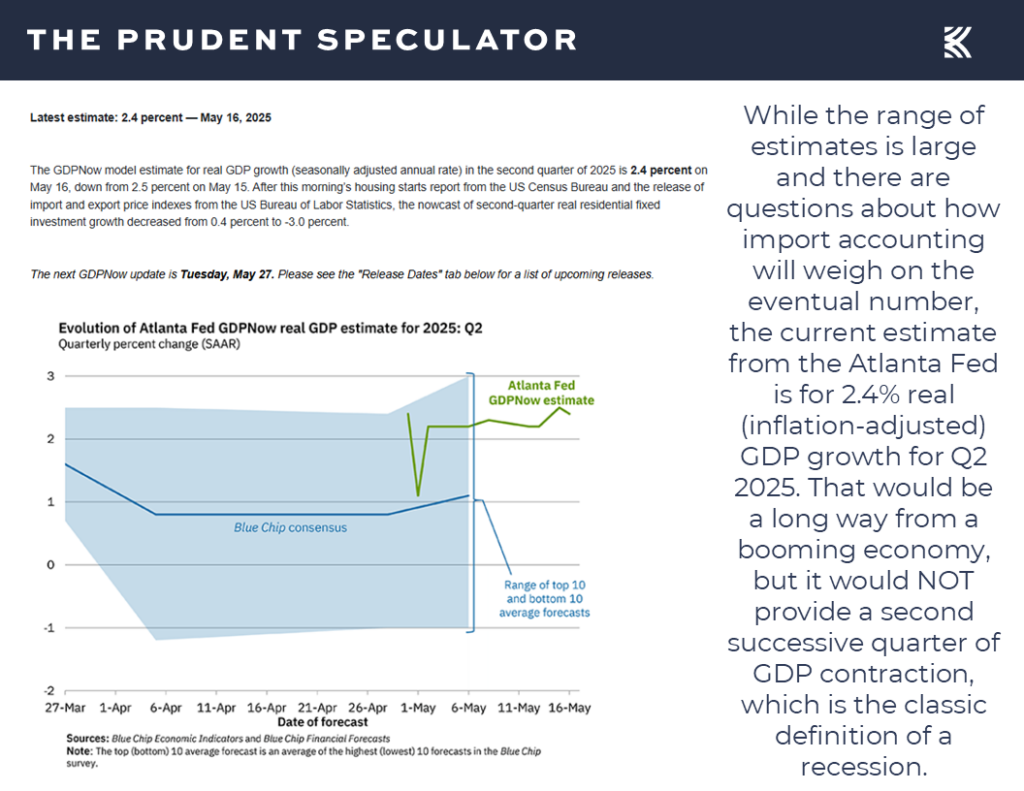

while the latest estimate from the Atlanta Fed for Q2 real (inflation-adjusted) U.S. GDP growth stood at +2.4%.

Recessions – Risk Has Jumped, But History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

Anything can happen as we move forward, and we can’t rule out a recession, but we continue to take comfort in what the historical evidence shows about equity performance, on average, in the year leading up to and during prior economic contractions,

and, more importantly, the year following the end of those recessions!

Inflation – Lower-than-Expected CPI & PPI

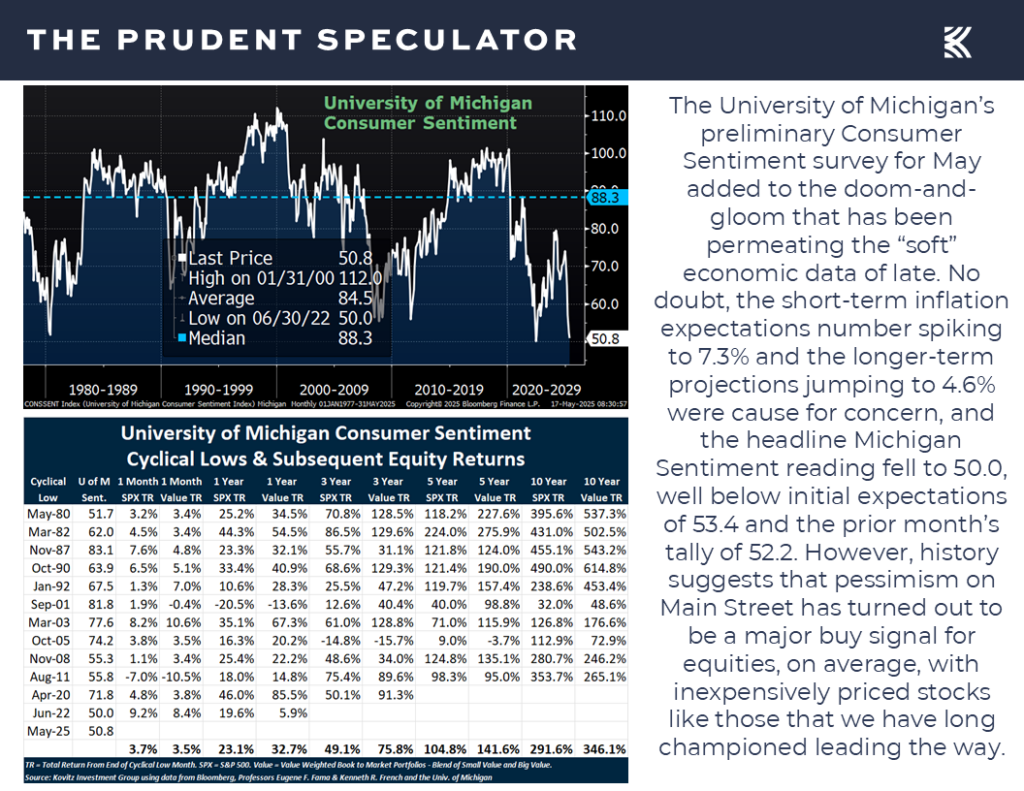

Further, we can’t help but be excited from a contrarian perspective that Consumer Sentiment, as calculated by the Univ. of Michigan, fell to a new cyclical low on Friday, given that this index strongly reinforces the Wall Street adage to be greedy when others are fearful.

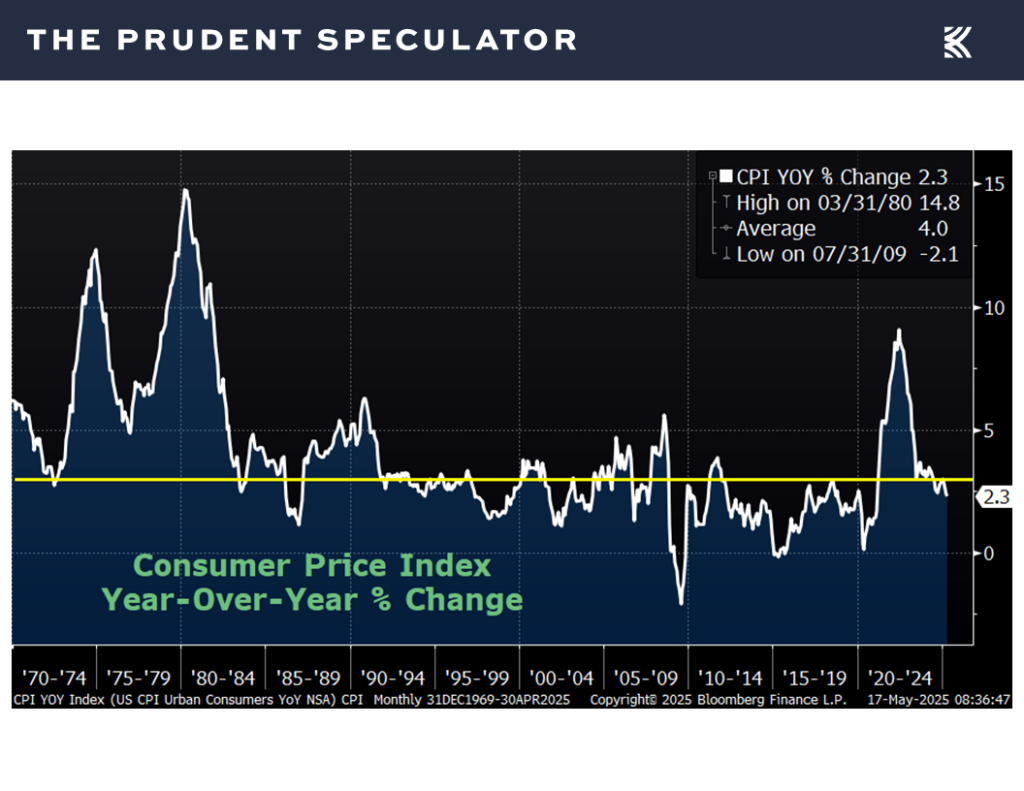

We also note that inflation figures for April came in lower than projected as the Consumer Price Index (CPI) increased 2.3% (est. 2.4%) on a year-over-year basis,

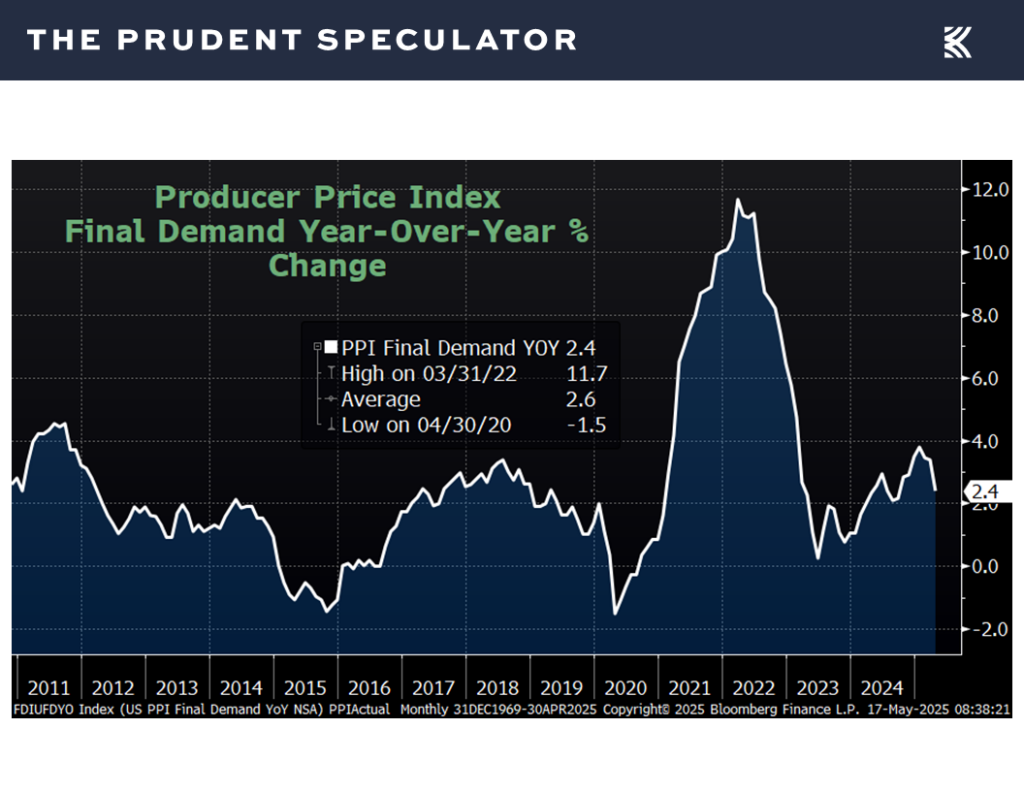

and the Producer Price Index (PPI) climbed 2.4% (est. 2.5%).

Valuations – Attractive Metrics on our Portfolios

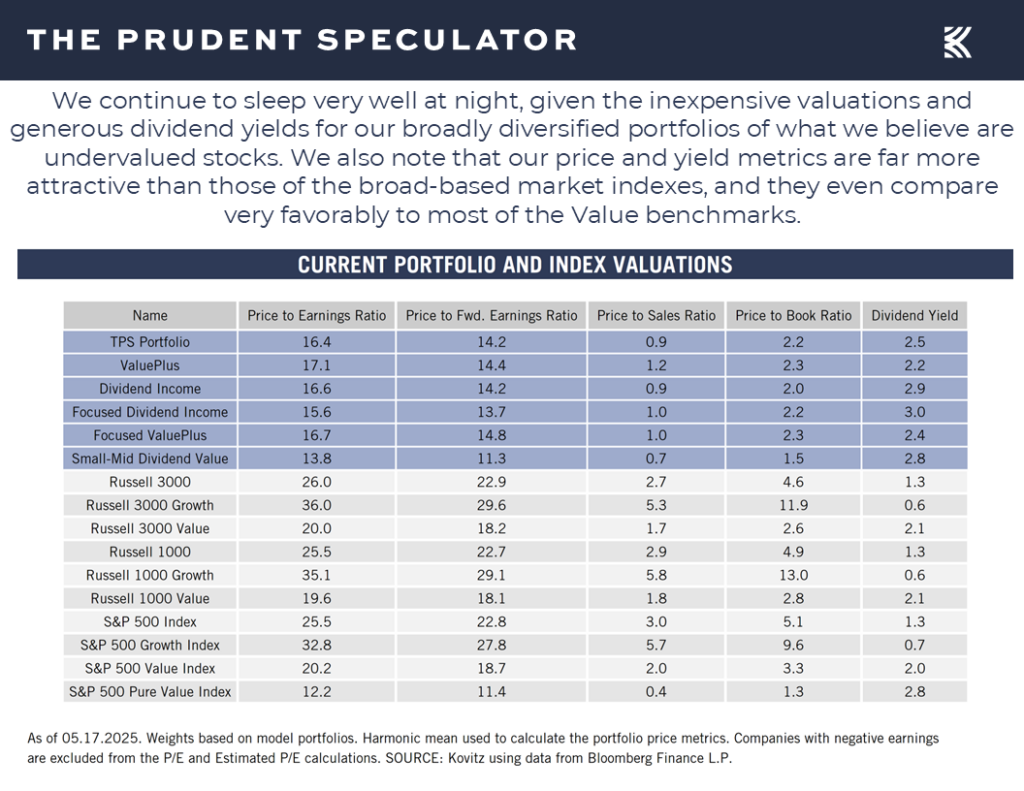

So, while we are always braced for downside volatility, we continue to sleep well at night given the reasonable valuation metrics and generous dividend yields of our broadly diversified portfolios of what we believe are undervalued stocks.

Moody’s Downgrades U.S. Credit Rating – History Lesson: S&P & Fitch

And speaking of downside volatility, the equity futures are suggesting a good-sized pullback will happen when trading resumes this week on news that Moody’s joined Standard & Poor’s and Fitch Ratings in downgrading U.S. debt.

Moody’s said…

Successive U.S. administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs. We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration.

Over the next decade, we expect larger deficits as entitlement spending rises while government revenue remains broadly flat. In turn, persistent, large fiscal deficits will drive the government’s debt and interest burden higher. The U.S.’ fiscal performance is likely to deteriorate relative to its own past and compared to other highly rated sovereigns.

That does sound disconcerting, with many thinking U.S. borrowing costs will rise, but Moody’s added, “The U.S. retains exceptional credit strengths such as the size, resilience and dynamism of its economy and the role of the U.S. dollar as global reserve currency. In addition, while recent months have been characterized by a degree of policy uncertainty, we expect that the U.S. will continue its long history of very effective monetary policy led by an independent Federal Reserve.”

Further, we can look at what we wrote back in August 2023, following the Fitch downgrade,

Not surprisingly, given that the move came a dozen years after Standard & Poor’s did the same thing, following arguably the most acrimonious debt-ceiling squabble in Washington history, most were quick to dismiss the Fitch move.

None other than Warren Buffett proclaimed, “There are some things people shouldn’t worry about. This is one.” The Oracle of Omaha added, “Berkshire bought $10 billion in U.S. Treasurys last Monday. We bought $10 billion in Treasurys this Monday. And the only question for next Monday is whether we will buy $10 billion in 3-month or 6-month T-bills.”

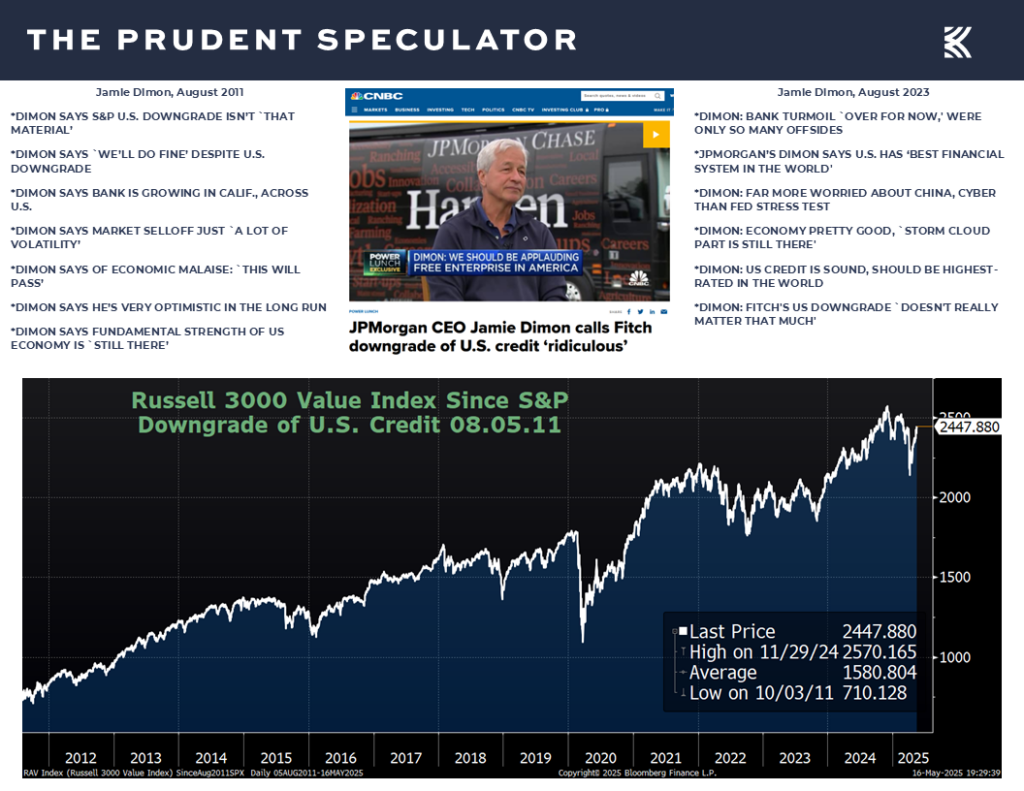

And Jamie Dimon was equally dismissive, with his comments on the right in the chart below. As students of market history, we also offer the JPMorgan Chase CEO’s remarks following the S&P downgrade of Uncle Sam’s credit back in 2011…along with a chart showing that the impact of that event was little more than a blip on the long-term uptrend of the Russell 3000 Value index.

None of this means that the massive U.S. debt burden is not an issue. It very much is, but the big issue from the credit rating agencies was in 2011 when S&P made its move, and stock prices quickly overcame that bombshell and are dramatically higher today!

Stock News – Comments on nine stocks across five different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Moody’s, Recessions, Historical Perspective and more Stock News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s Market Commentary, we discuss Moody’s, Recessions, Historical Perspective and more Stock News. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Portfolio Trades – Trimmed NRG in TPS Portfolio

Miami Masters Symposium – 24 Undervalued, 3%+ Yielders

Short-Term Predictions – Yet Another Example of Why the Only Problem with Market Timing is Getting the Timing Right

Volatility – 101st Best Week of the Last Century

Historical Perspective – Plenty of Scary Events, but Long-Term Trend is Up

Econ News – Mixed Numbers but Growth Still the Forecast

Recessions – Risk Has Jumped, But History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

Inflation – Lower-than-Expected CPI & PPI

Valuations – Attractive Metrics on our Portfolios

Moody’s Downgrades U.S. Credit Rating – History Lesson: S&P & Fitch

Stock News – Comments on CAH, ELV, CVS, AEO, HMC, CSCO, ALIZY, SIEGY & WMT

Miami Masters Symposium – 24 Undervalued, 3%+ Yielders

Your editor spoke at the Miami Masters Symposium on Friday, with the Sleeping Better at Night: The Value of Dividends presentation offering 24 undervalued stocks with yields of at least 3%.

Short-Term Predictions – Yet Another Example of Why the Only Problem with Market Timing is Getting the Timing Right

This event was again interesting in that there were a bevy of speakers who seemed very good at touting their successful investment calls, including evidently staying the course six weeks ago when stocks were cratering and CNBC was heralding a new Bear Market.

No doubt, many did keep the faith, but we find that some market pundits are guilty of revisionist history as they learn the hard way that the only problem with market timing is getting the timing right. While not a speaker at the Miami confab, The Wall Street Journal’s Streetwise columnist, who in his defense is charged with making shorter-term market calls, provided a good illustration why the physicist Neils Bohr said, “Prediction is very difficult, especially if it is about the future.”

Volatility – 101st Best Week of the Last Century

After all, despite writing on April 13, “The damage from Trump’s trade war is far greater than the losses in stocks, bonds and the dollar seen so far,” the take a week ago was that it was clear that stocks had fallen too far when they bottomed on April 8 AND that they were up too much on May 10. The column appeared just in time for the equity markets to soar over the next five days, with the S&P 500’s advance of 5.27% last week the 101st best weekly gain over the last 97+ years.

To be sure, more progress on the global trade front, this time with China, positively altered the investment landscape, but equities have proved rewarding no matter what has transpired for the last century,

Historical Perspective – Plenty of Scary Events, but Long-Term Trend is Up

with all prior disconcerting events overcome in the fullness of time,

so much so that despite plenty of selloffs along the way, the long-term returns on stocks have been in the 9% to 13% per annum range,

with rallies, including the 40th advance of 10% or more without a decline of comparable magnitude in which we presently reside happening long before any sort of all-clear signal is sounded.

As we have long said, they don’t ring a bell to mark times to enter and exit the equity market. Indeed, those who bailed on stocks during the March/April plunge, when fear levels for investment professionals,

and those on Main Street,

were on par with what was seen during the Great Financial Crisis and during the COVID-19 Pandemic are likely to still sitting on the sidelines.

No doubt, tariff uncertainty is still off the charts, even as levies have always been part of the investment backdrop,

Econ News – Mixed Numbers but Growth Still the Forecast

and Trump 45 launched a Trade War with China in March 2018, yet stock prices today are far higher today than they were then,

so those worried about a recession don’t exactly have a ton of comfort today, given that the odds of an economic contraction, as tabulated by Bloomberg, remain elevated.

The economic data out last week was not grand with negative readings for May on factory activity in the New York region,

and in the Philadelphia region,

while both retail sales,

and housing starts for April came in below expectations.

Of course, the labor market continues to show healthy numbers with first-time filings for unemployment benefits remaining near multi-generational lows,

while the latest estimate from the Atlanta Fed for Q2 real (inflation-adjusted) U.S. GDP growth stood at +2.4%.

Recessions – Risk Has Jumped, But History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

Anything can happen as we move forward, and we can’t rule out a recession, but we continue to take comfort in what the historical evidence shows about equity performance, on average, in the year leading up to and during prior economic contractions,

and, more importantly, the year following the end of those recessions!

Inflation – Lower-than-Expected CPI & PPI

Further, we can’t help but be excited from a contrarian perspective that Consumer Sentiment, as calculated by the Univ. of Michigan, fell to a new cyclical low on Friday, given that this index strongly reinforces the Wall Street adage to be greedy when others are fearful.

We also note that inflation figures for April came in lower than projected as the Consumer Price Index (CPI) increased 2.3% (est. 2.4%) on a year-over-year basis,

and the Producer Price Index (PPI) climbed 2.4% (est. 2.5%).

Valuations – Attractive Metrics on our Portfolios

So, while we are always braced for downside volatility, we continue to sleep well at night given the reasonable valuation metrics and generous dividend yields of our broadly diversified portfolios of what we believe are undervalued stocks.

Moody’s Downgrades U.S. Credit Rating – History Lesson: S&P & Fitch

And speaking of downside volatility, the equity futures are suggesting a good-sized pullback will happen when trading resumes this week on news that Moody’s joined Standard & Poor’s and Fitch Ratings in downgrading U.S. debt.

Moody’s said…

Successive U.S. administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs. We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration.

Over the next decade, we expect larger deficits as entitlement spending rises while government revenue remains broadly flat. In turn, persistent, large fiscal deficits will drive the government’s debt and interest burden higher. The U.S.’ fiscal performance is likely to deteriorate relative to its own past and compared to other highly rated sovereigns.

That does sound disconcerting, with many thinking U.S. borrowing costs will rise, but Moody’s added, “The U.S. retains exceptional credit strengths such as the size, resilience and dynamism of its economy and the role of the U.S. dollar as global reserve currency. In addition, while recent months have been characterized by a degree of policy uncertainty, we expect that the U.S. will continue its long history of very effective monetary policy led by an independent Federal Reserve.”

Further, we can look at what we wrote back in August 2023, following the Fitch downgrade,

Not surprisingly, given that the move came a dozen years after Standard & Poor’s did the same thing, following arguably the most acrimonious debt-ceiling squabble in Washington history, most were quick to dismiss the Fitch move.

None other than Warren Buffett proclaimed, “There are some things people shouldn’t worry about. This is one.” The Oracle of Omaha added, “Berkshire bought $10 billion in U.S. Treasurys last Monday. We bought $10 billion in Treasurys this Monday. And the only question for next Monday is whether we will buy $10 billion in 3-month or 6-month T-bills.”

And Jamie Dimon was equally dismissive, with his comments on the right in the chart below. As students of market history, we also offer the JPMorgan Chase CEO’s remarks following the S&P downgrade of Uncle Sam’s credit back in 2011…along with a chart showing that the impact of that event was little more than a blip on the long-term uptrend of the Russell 3000 Value index.

None of this means that the massive U.S. debt burden is not an issue. It very much is, but the big issue from the credit rating agencies was in 2011 when S&P made its move, and stock prices quickly overcame that bombshell and are dramatically higher today!

Stock News – Comments on nine stocks across five different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.