The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Nvidia, Interest Rates, Valuations, and Earnings. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Trades – 9 Buys Across 4 Portfolios

Market of Stocks – Averages Up Last Week; Most Stocks Down

Nvidia – Other Less-Expensive Ways to Participate in A.I. Enthusiasm

Interest Rates – Yields Decline in Latest Week

Econ Data – Mixed Numbers; Q2 GDP Outlook Improves

Earnings – Solid Growth Estimated in ’24 & ’25

Valuations – Inexpensive Multiples for Value Stocks

Sentiment – AAII More Bearish

Volatility – Plenty of Gyrations but Long-Term Trend is Up

Stock News – Updates on the Energy sector and two additional stocks

Market of Stocks – Averages Up Last Week; Most Stocks Down

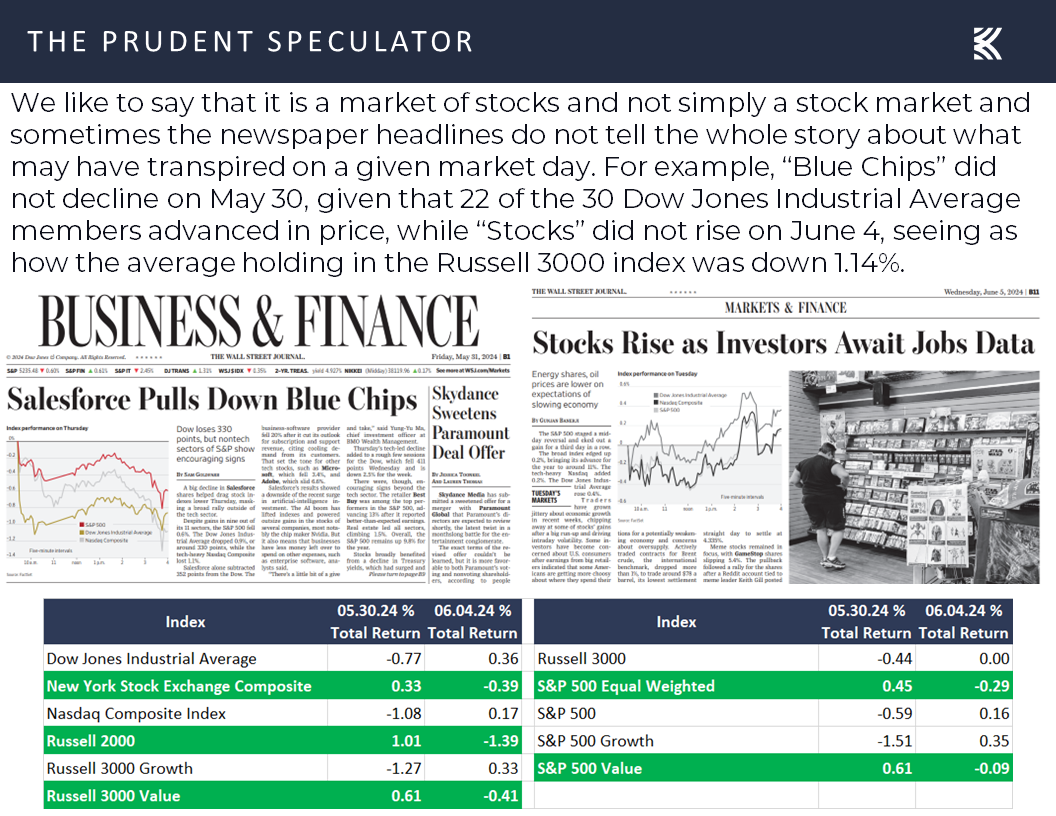

Given that the average stock in the S&P 500 fell 0.70% and the Russell 2000 SmallCap Index skidded 2.07%, the first week of June provided little cheer, even as stories in the financial press might suggest otherwise. It is a market of stocks and not simply a stock market, so we always counsel to look beyond the headlines as sometimes (as was the case for articles in the May 31 and June 5 Wall Street Journal) they can be very misleading in terms of what is happening to a broadly diversified portfolio of inexpensively priced stocks.

Nvidia – Other Less-Expensive Ways to Participate in A.I. Enthusiasm

No doubt, the broad-based indexes are heavily influenced by stocks like high-priced Salesforce in the price-weighted Dow Jones Industrial Average or a titan like Nvidia in the capitalization-weighted S&P 500. And speaking of Nvidia, the investor darling accounts for more than a third (436 basis points) of the S&P’s return this year, given its 4.67% average weight in the index and its 144% total return.

With its market capitalization topping $3 trillion last week, it is not surprising that folks would want to know our current thinking on the rocket ship that has been Nvidia. While we have owned the A.I. superstar in the past with success, we do not presently hold the stock. Clearly, with the benefit of 20-20 hindsight, we wish we still had a position, but the valuation metrics have long been too rich for our taste.

Our investment process, which is valuation-driven and has been evolving since we first turned on the lights at The Prudent Speculator in March 1977, relies on the underlying idea that we should be buying stocks when they are on sale and trading at a significant discount to our determination of fair value. That is, we want to buy stocks that are (temporarily) out-of-favor or underappreciated, as in our view they offer several ways to benefit. These can include a market reassessment upward towards the historical norm for valuation metrics like sales and earnings and/or growth in those metrics. In simplistic terms, the P/E ratio could ratchet back up or the E part of the equation could increase with the P then also climbing.

This disciplined approach has afforded us the opportunity to buy other stellar Wall Street performers like Apple (AAPL – $196.89), which accounts for 15 basis points of the S&P 500’s 2024 return; Microsoft (MSFT – $423.85), 93 basis points; Alphabet (GOOG – $175.95), 43 basis points; and Meta Platforms (META – $492.96), 79 basis points; at what have turned out to be favorable prices, so we are comfortable in remaining patient for market volatility to afford us an inexpensive entry point. Such could one day again be the case with Nvidia. After all, the company, despite its massive market capitalization, still has plenty of growth potential, as the top- and bottom-line is likely to continue to move markedly higher for the foreseeable future.

Of course, we have plenty of exposure to companies that can benefit from the same dynamics that have propelled Nvidia to the stratosphere: Broadcom (AVGO – $1406.64) with its cutting-edge A.I. networking and connectivity solutions; Qualcomm (QCOM – $206.62) with its Snapdragon mobile processors and Adreno GPUs; Micron (MU – $130.94) and its purpose-built memory and storage solutions that support A.I. applications; Digital Realty (DLR – $146.35) and its data center real estate, Intel and its data center chips; Microsoft and its monetization of A.I. technology; et cetera.

In most cases, too, our Tech stocks also pay a dividend and/or buy back shares, whereas Nvidia’s current $0.10 per share quarterly dividend (one cent per share post the imminent 10-for-1 split) doesn’t go very far to help folks looking for their portfolios to generate income.

Interest Rates – Yields Decline in Latest Week

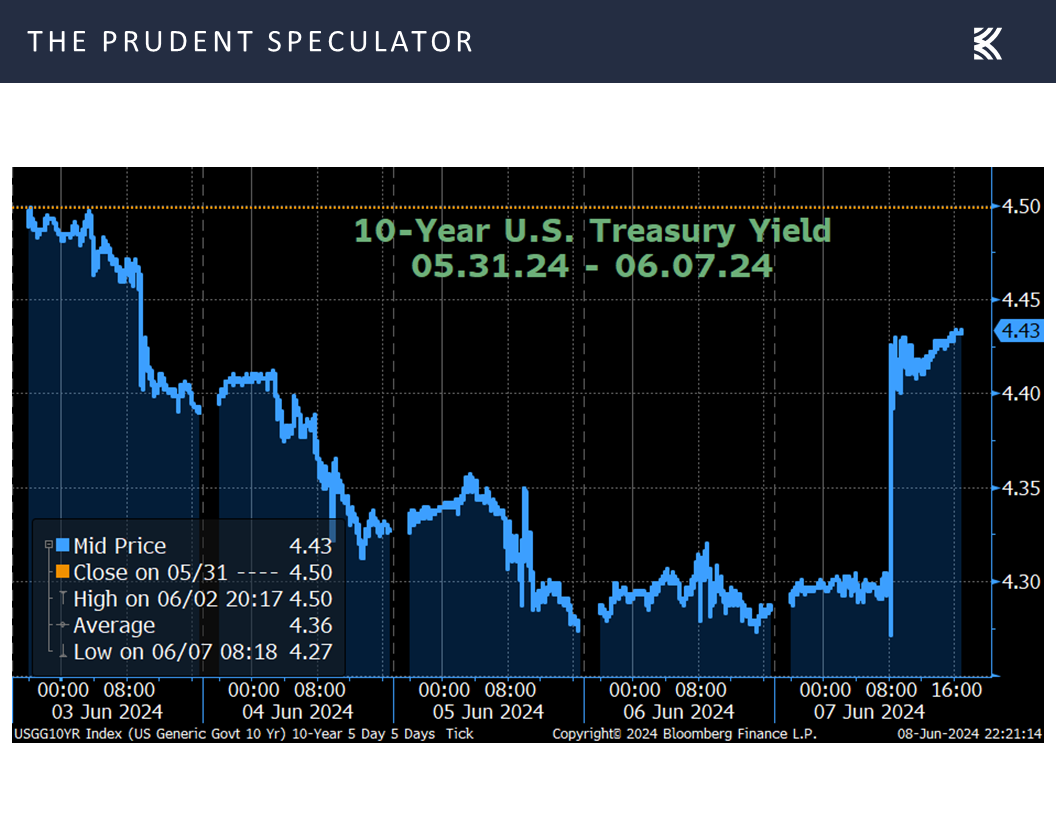

We might have thought that it would have been a favorable week for the proverbial soldiers and not just the generals, given that the yield on the benchmark U.S. government bond declined to 4.43% from 4.50% at the end of the week prior,

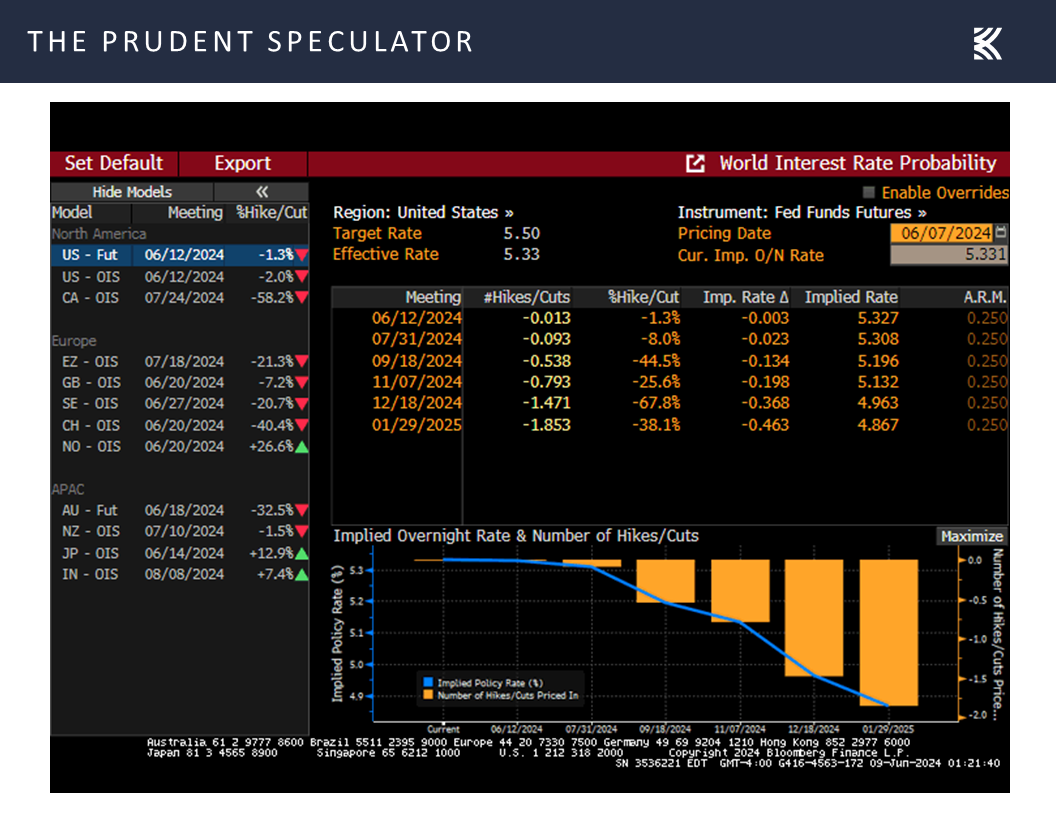

and the betting on the effective level for the year-end Fed Funds rate held steady at 4.963%, compared to 4.965% on May 31.

Econ Data – Mixed Numbers; Q2 GDP Outlook Improves

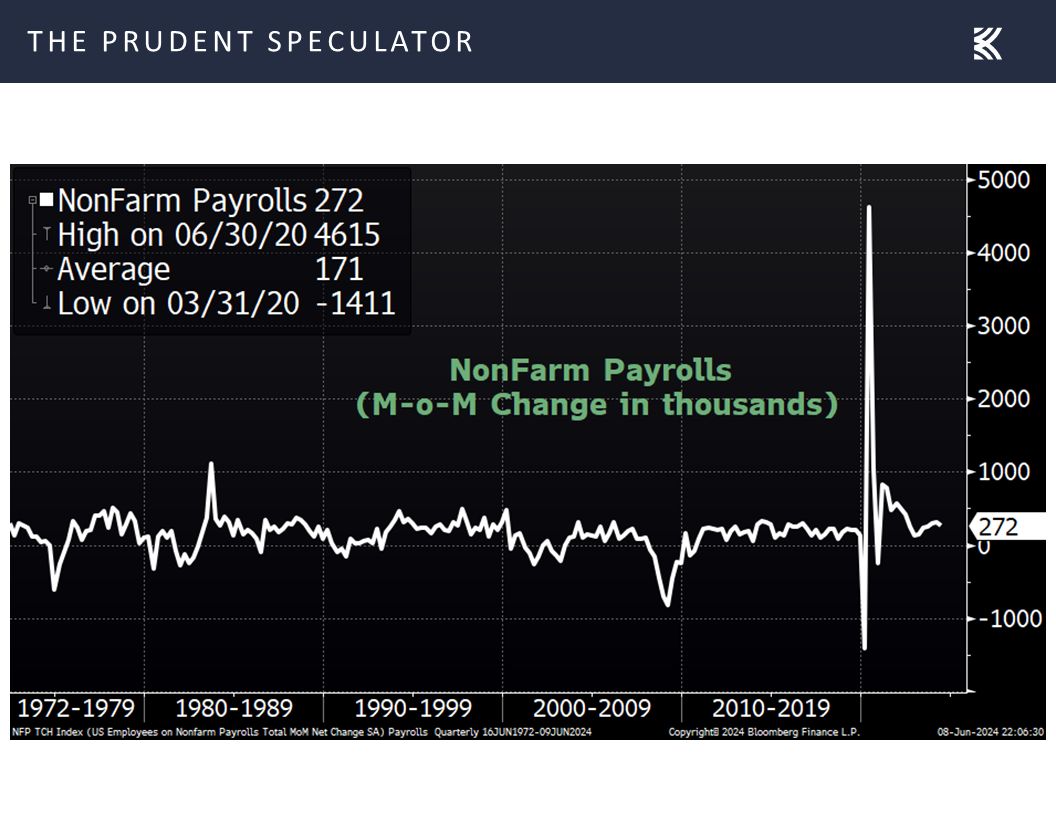

The economic data out last week was mixed as the important jobs report saw far more payrolls (272,000) created than expected in May,

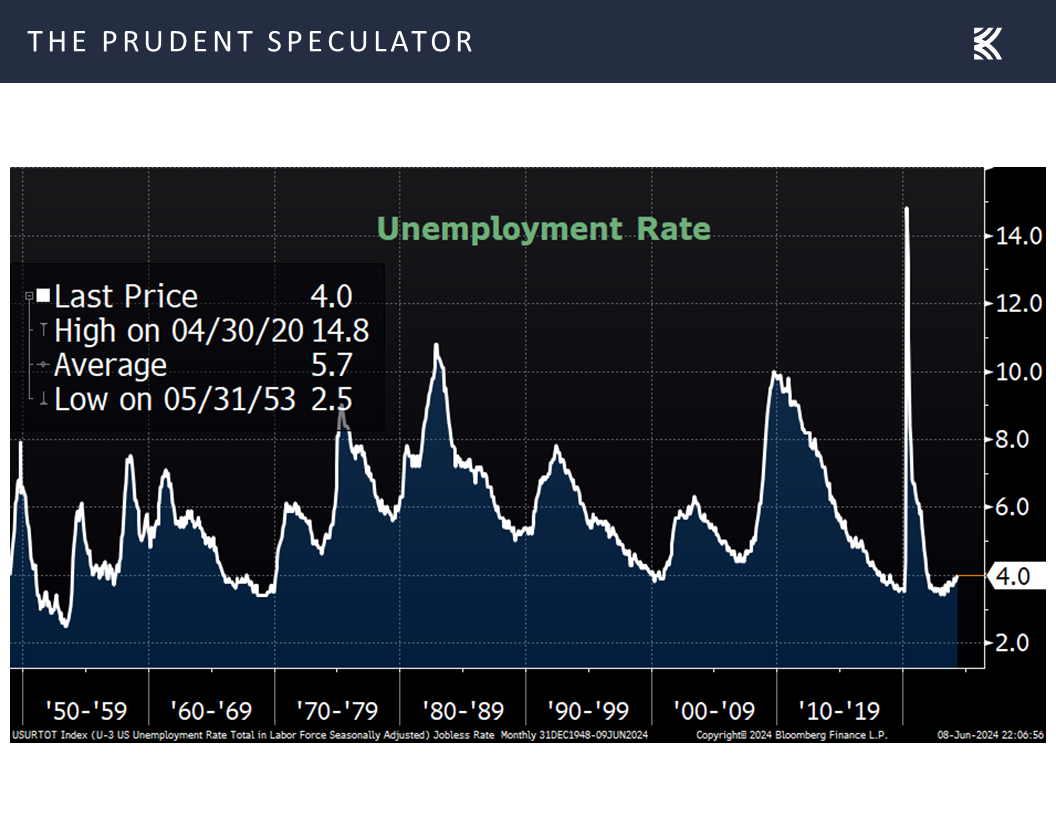

but the jobless rate ticked up to 4.0%, the highest level since November 2021,

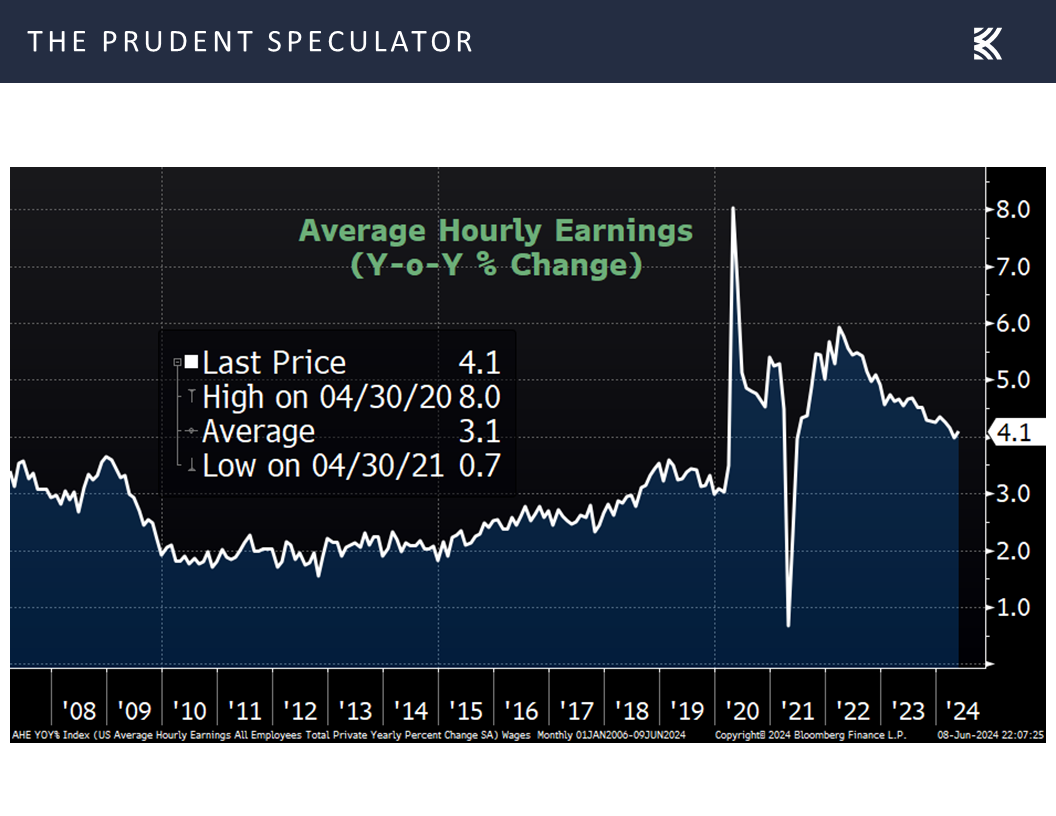

and average hourly earnings rose by a higher-than-estimated 4.1% on a year-over-year basis.

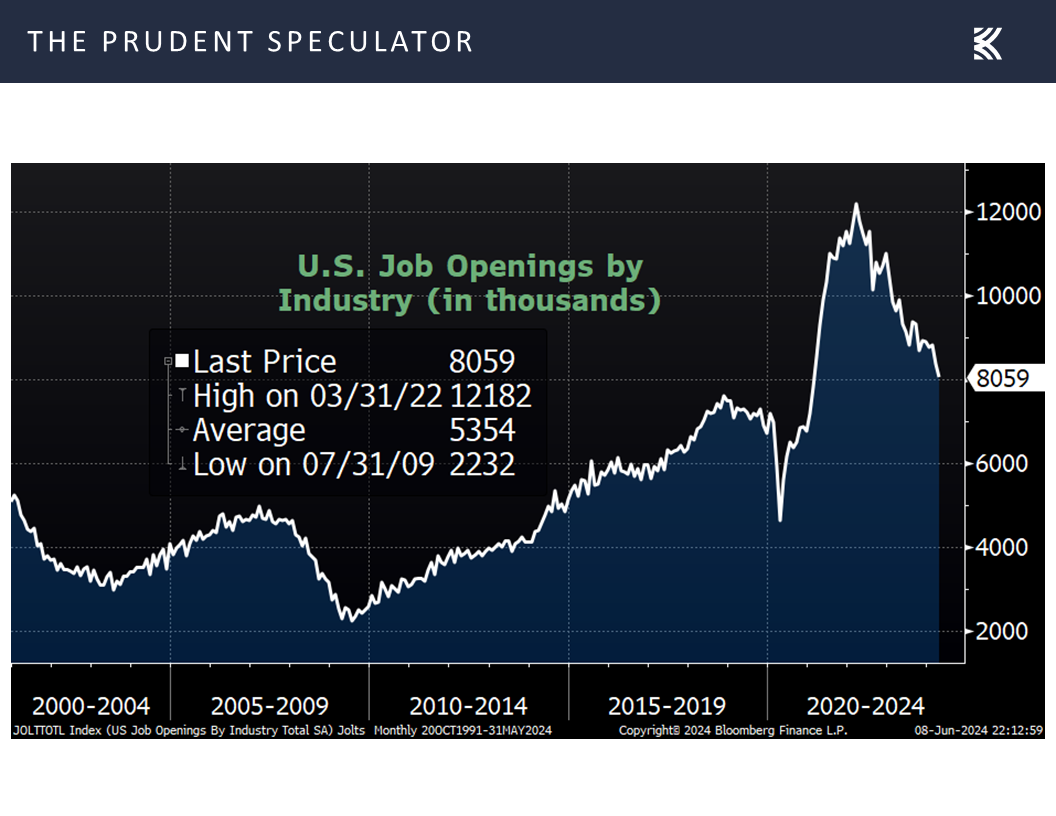

Also arguing that all may not be as rosy as it seems in the labor market, the number of job openings in April fell to 8.06 million, down from a revised 8.35 million in March and below the 8.35 million forecast,

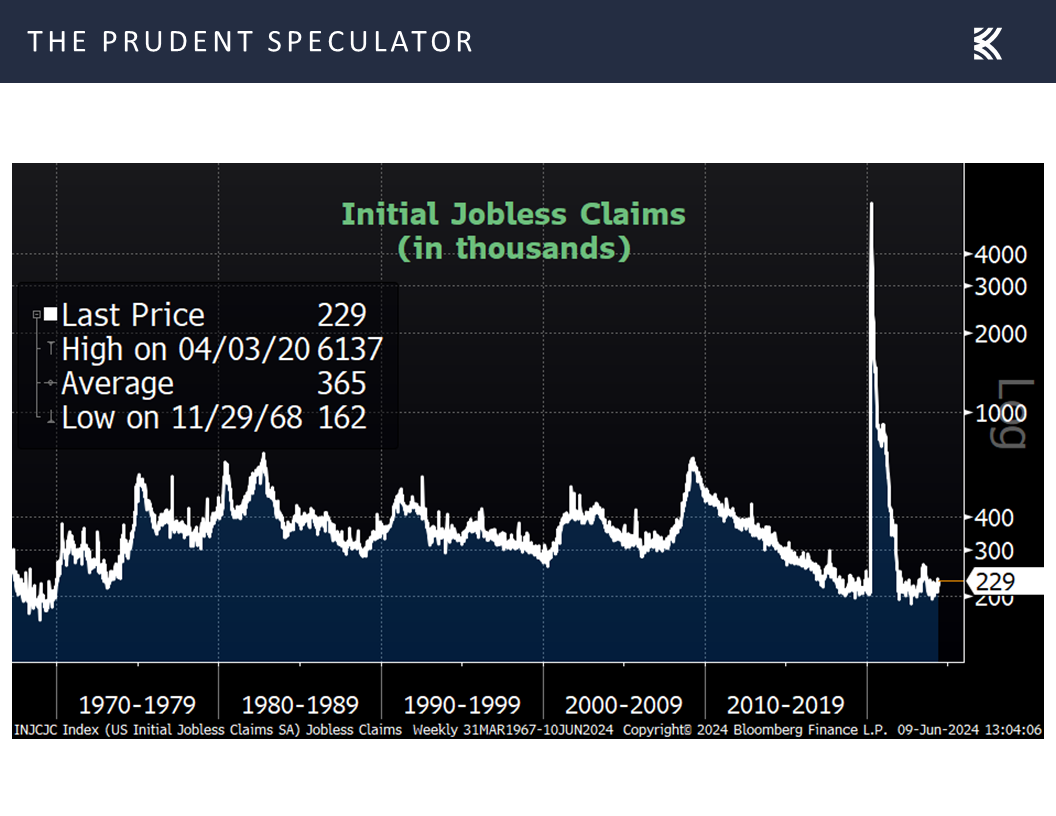

while first-time filings for unemployment benefits in the latest week increased to 229,000, compared to projections of 220,000 and a revised tally of 221,000 the previous week.

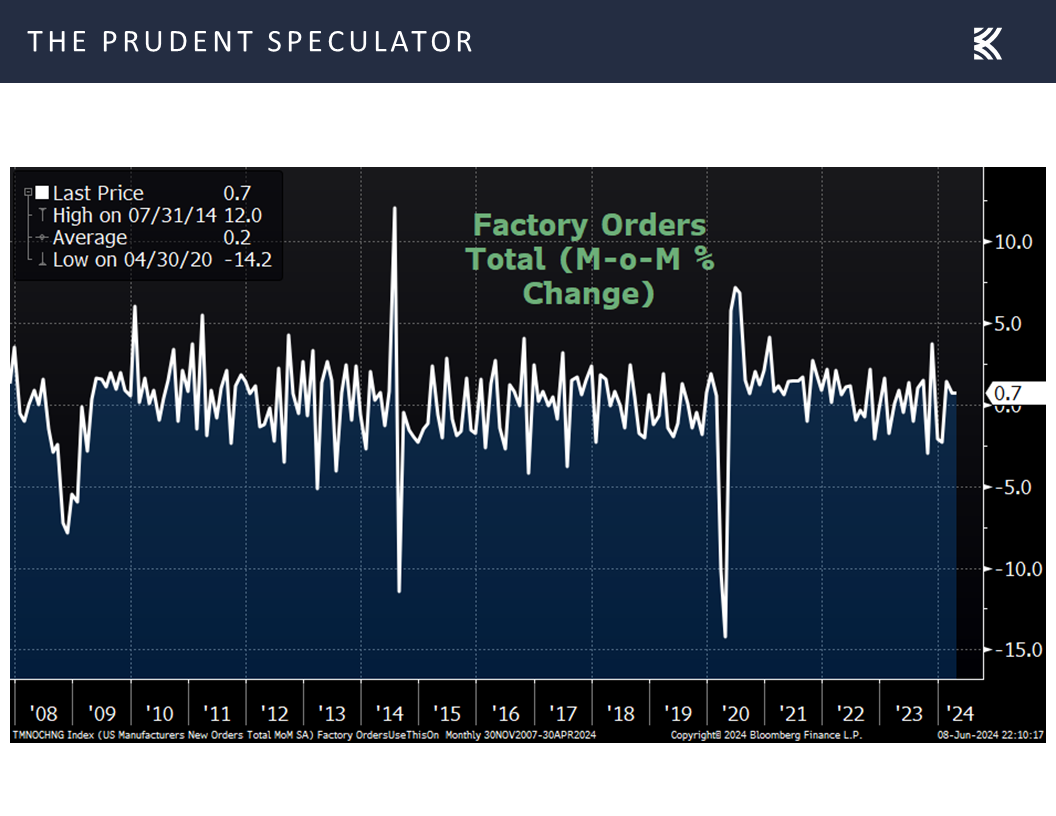

On the other hand, factory orders excluding the volatile transportation sector advanced 0.7% in April, above the 0.5% increase that was expected,

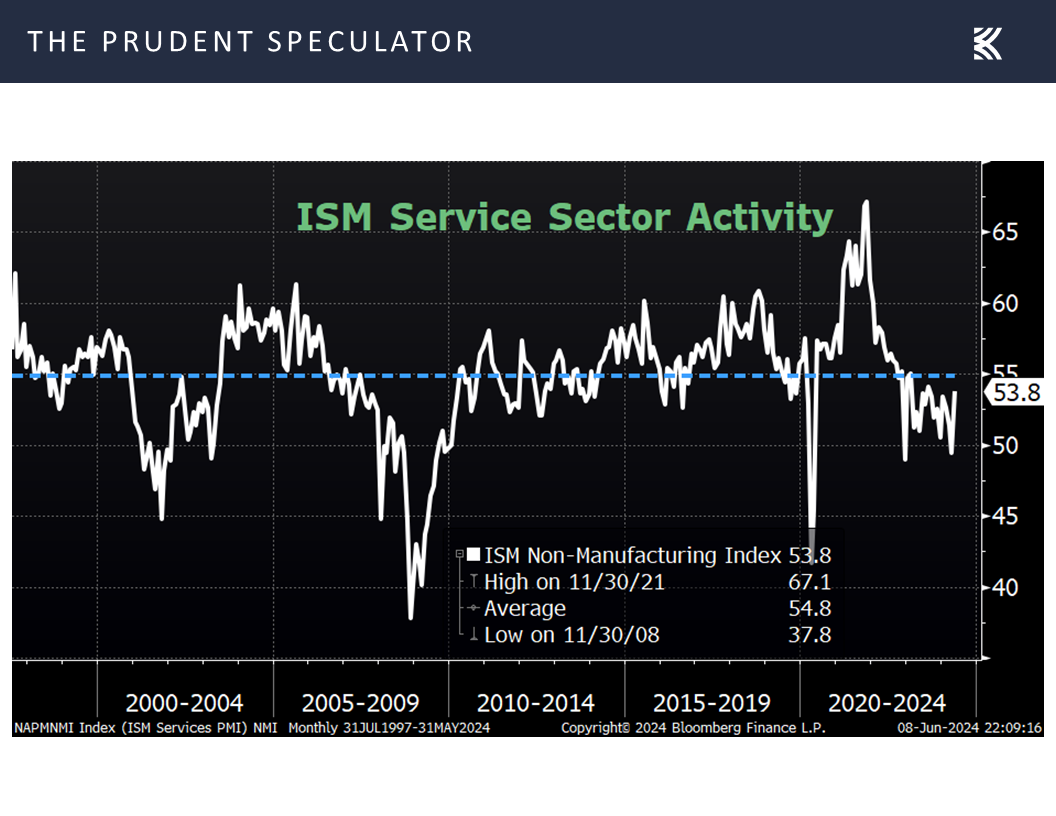

and the report on business for the important Services Sector (Non-Manufacturing Index) in May from the Institute for Supply Management (ISM) jumped to 53.8, well above estimates 51.0.

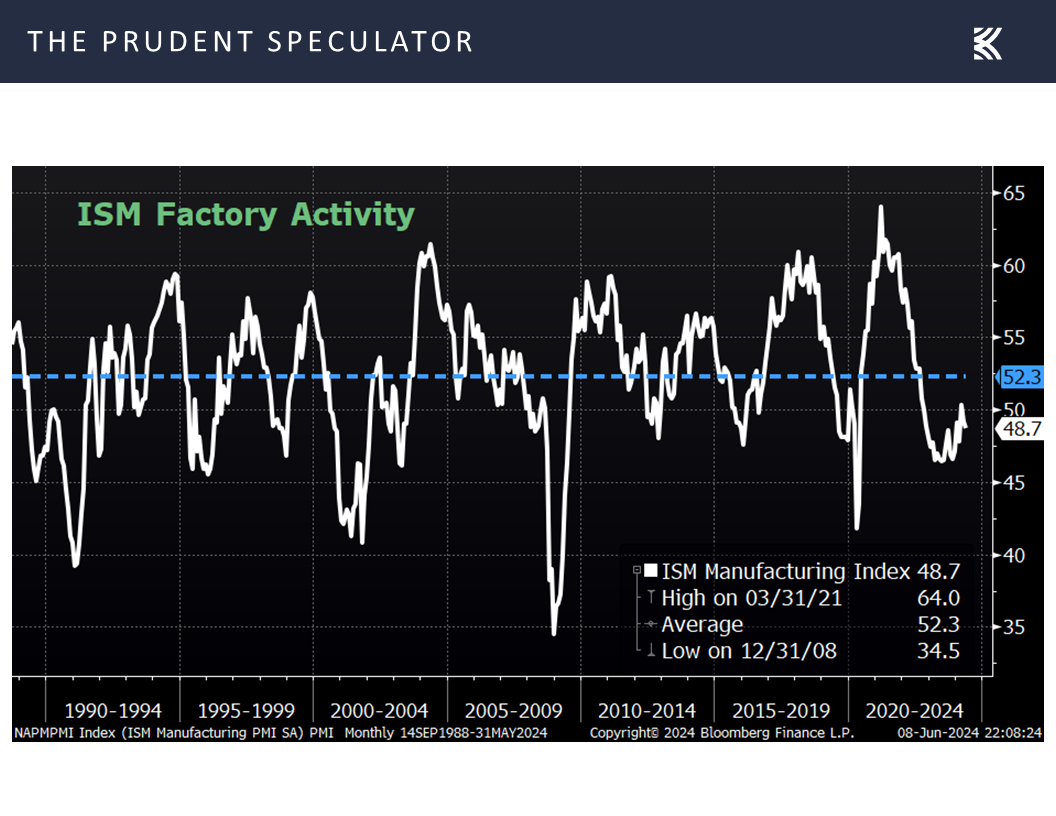

True, the ISM Manufacturing Index for May came in below forecasts at 48.7,

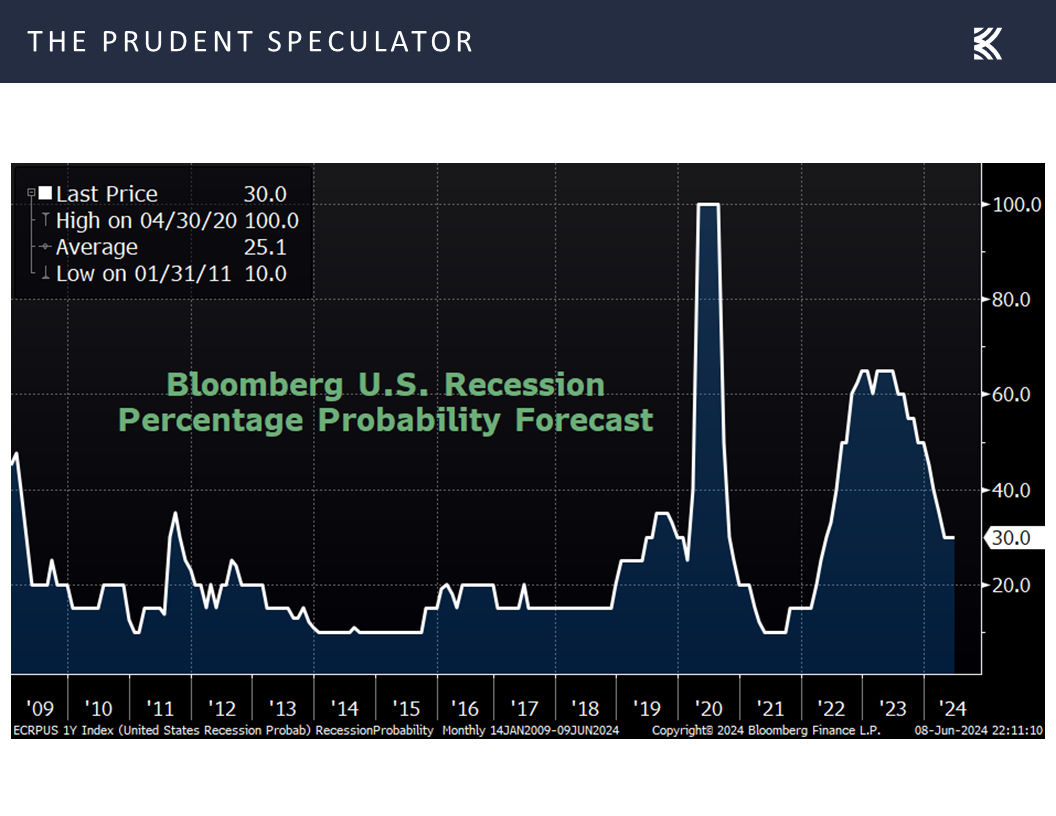

but the odds of recession in the next 12 months, as tabulated by Bloomberg, remained at 30%,

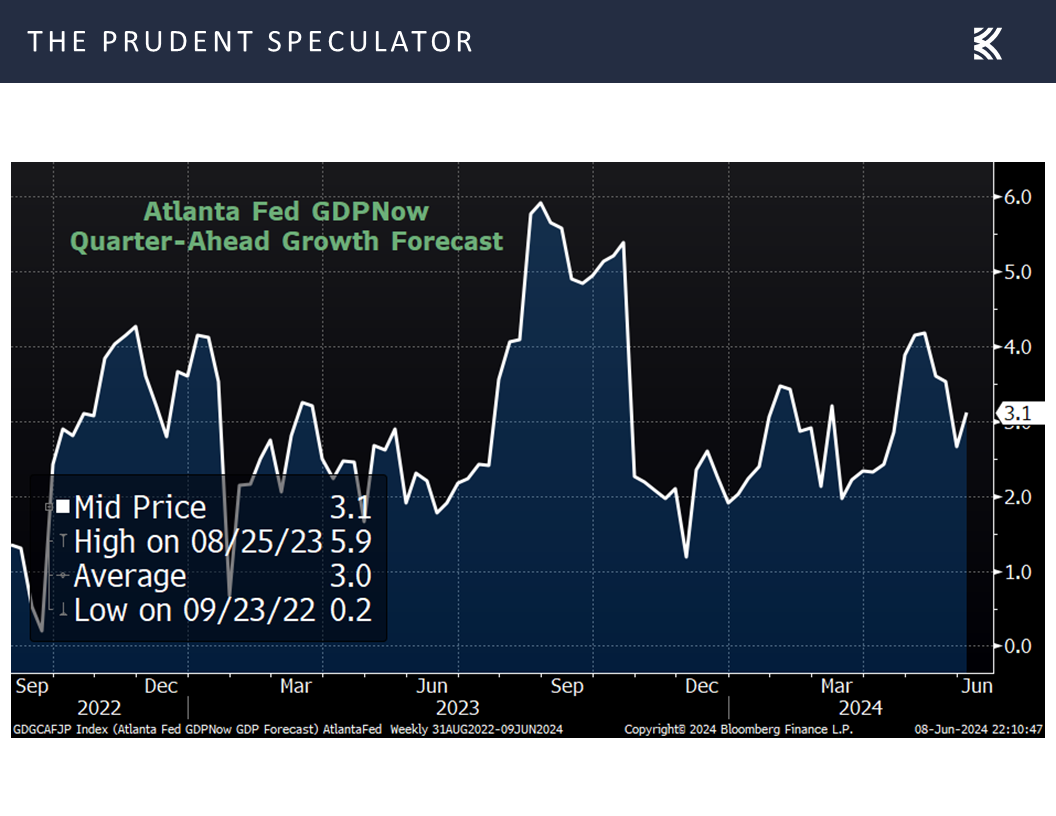

the latest estimate for Q2 real (inflation-adjusted) GDP growth from the Atlanta Fed rebounded to a very good 3.1%,

Earnings – Solid Growth Estimated in ’24 & ’25

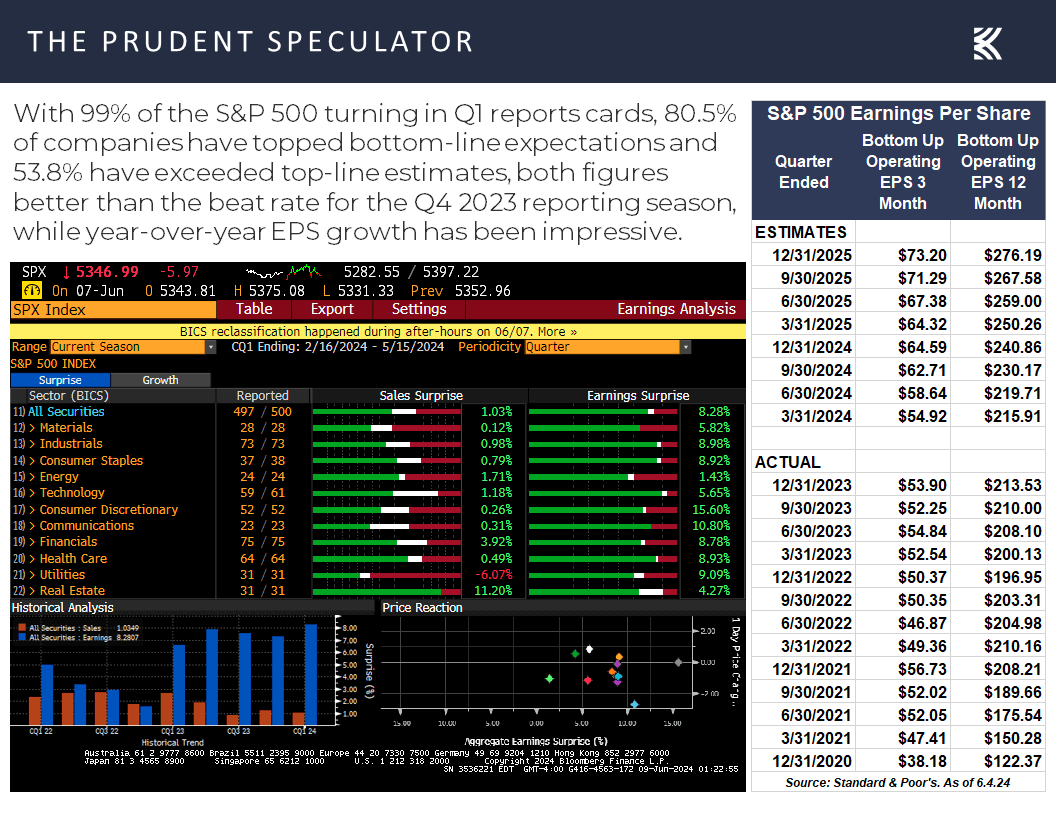

and Standard & Poor’s nudged up its outlook for corporate profit growth this year and next.

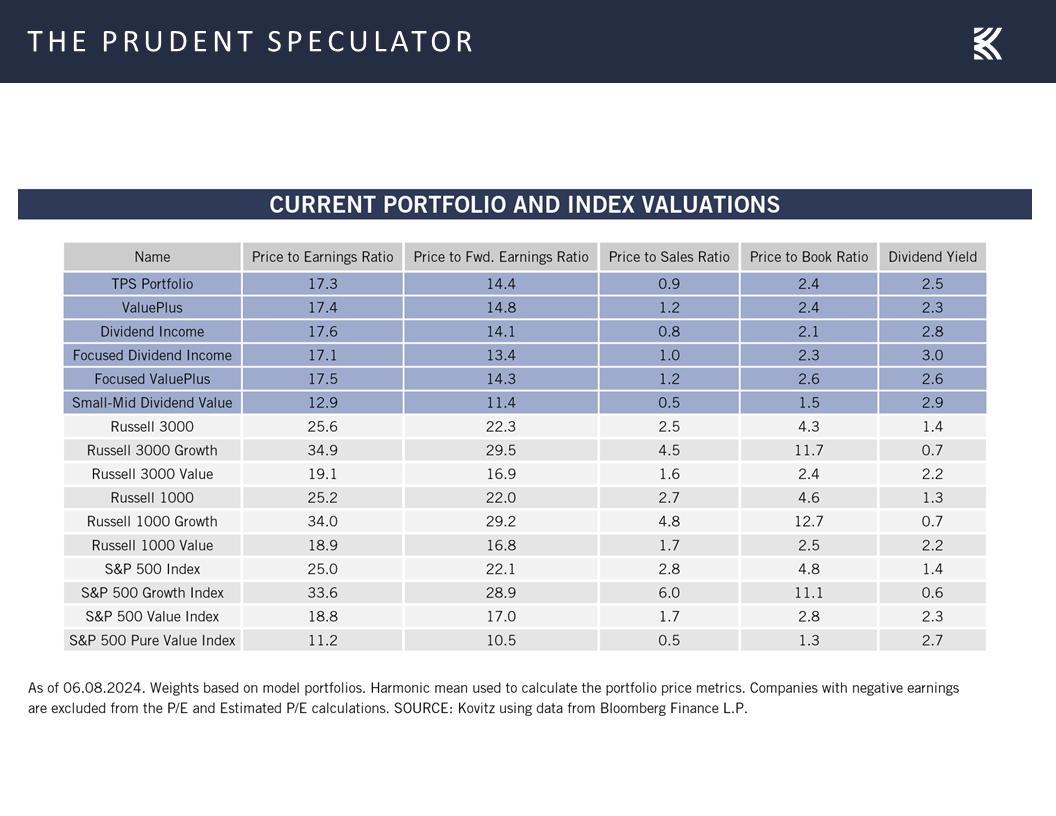

Valuations – Inexpensive Multiples for Value Stocks

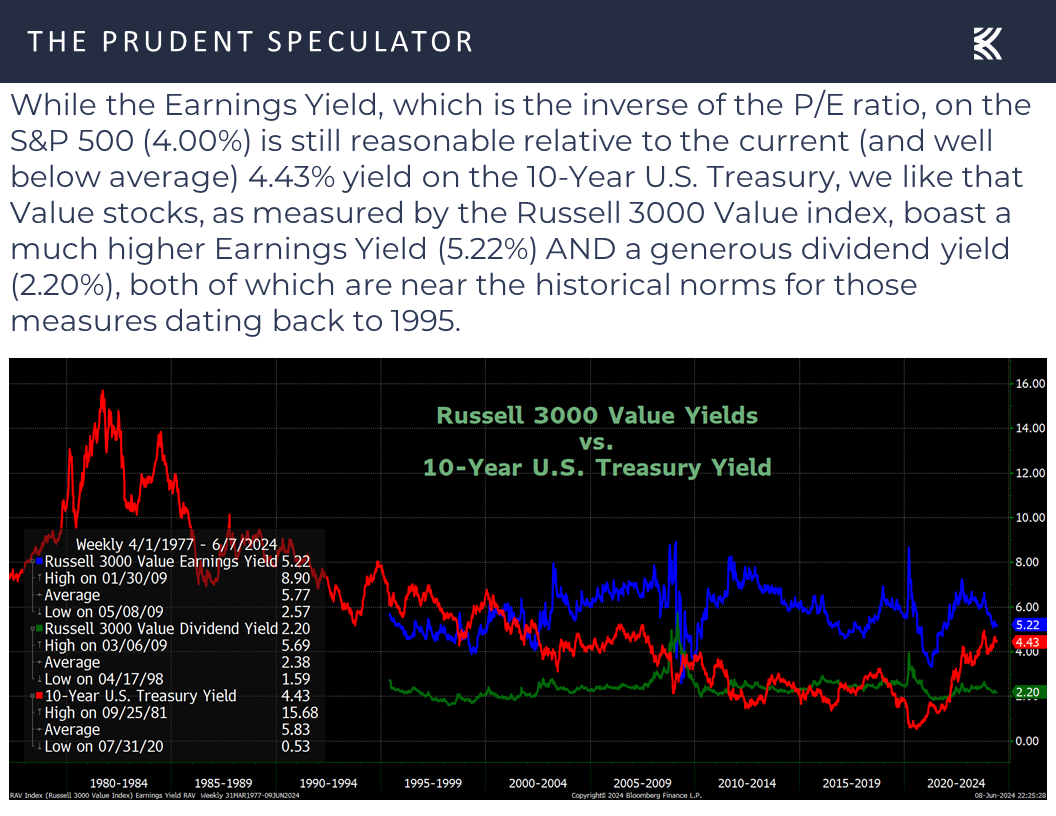

Given that improving earnings, stronger GDP growth and lower interest rates should make stocks more attractive, all else equal,

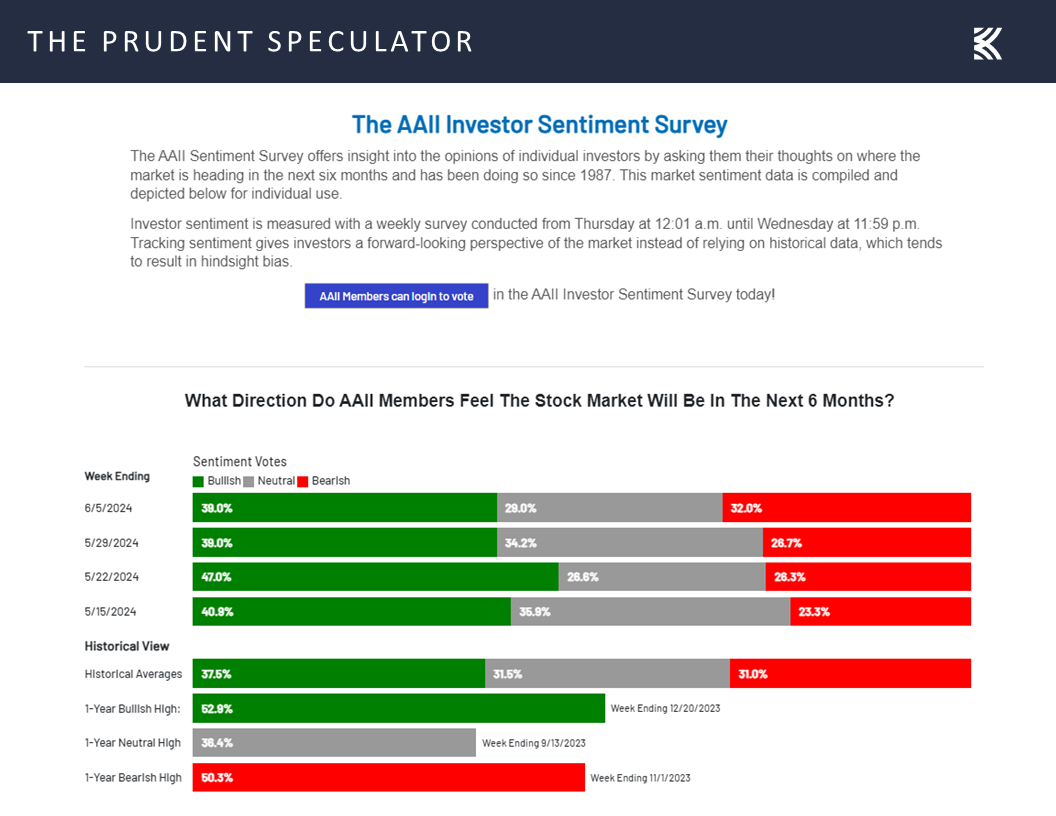

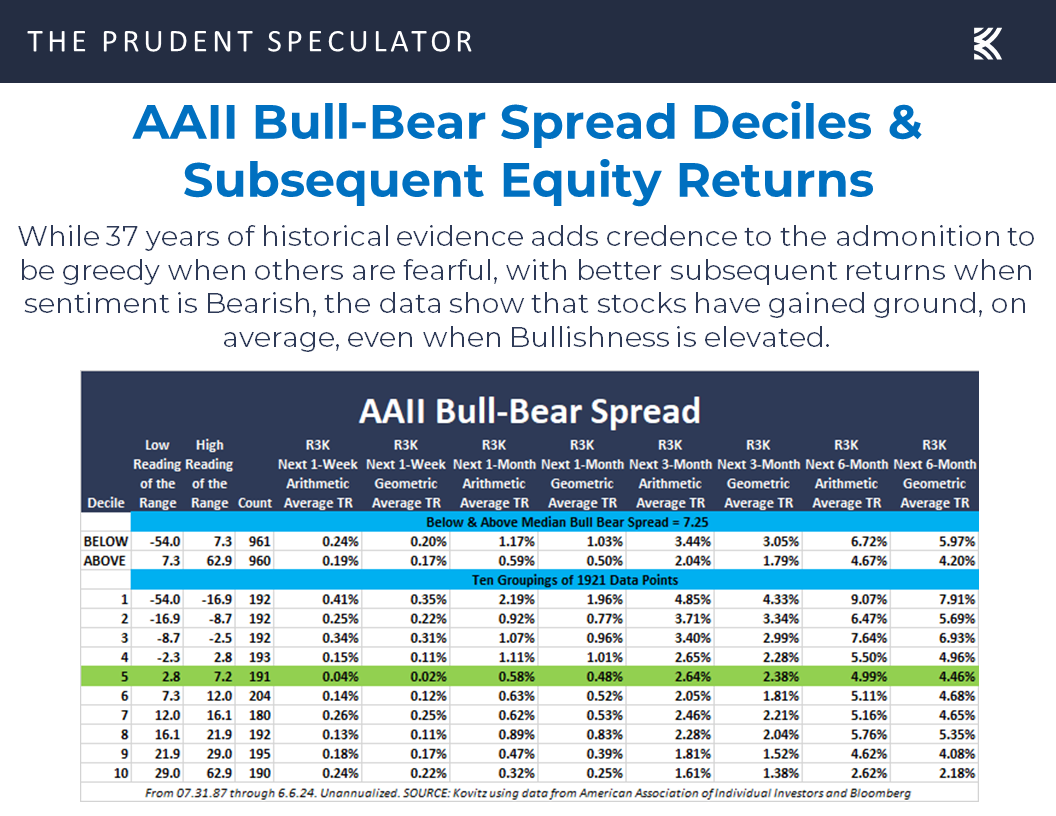

Sentiment – AAII More Bearish

we see no reason to alter our bullish enthusiasm, especially with the folks on Main Street becoming more Bearish last week as there was a rise in pessimists in the weekly Sentiment Survey from the American Association of Individual Investors (AAII)

Of course, the empirical data show that one should stick with stocks no matter what the AAII Bull-Bear gauge is registering,

especially as the evidence is overwhelming that the only problem with market timing is getting the timing right.

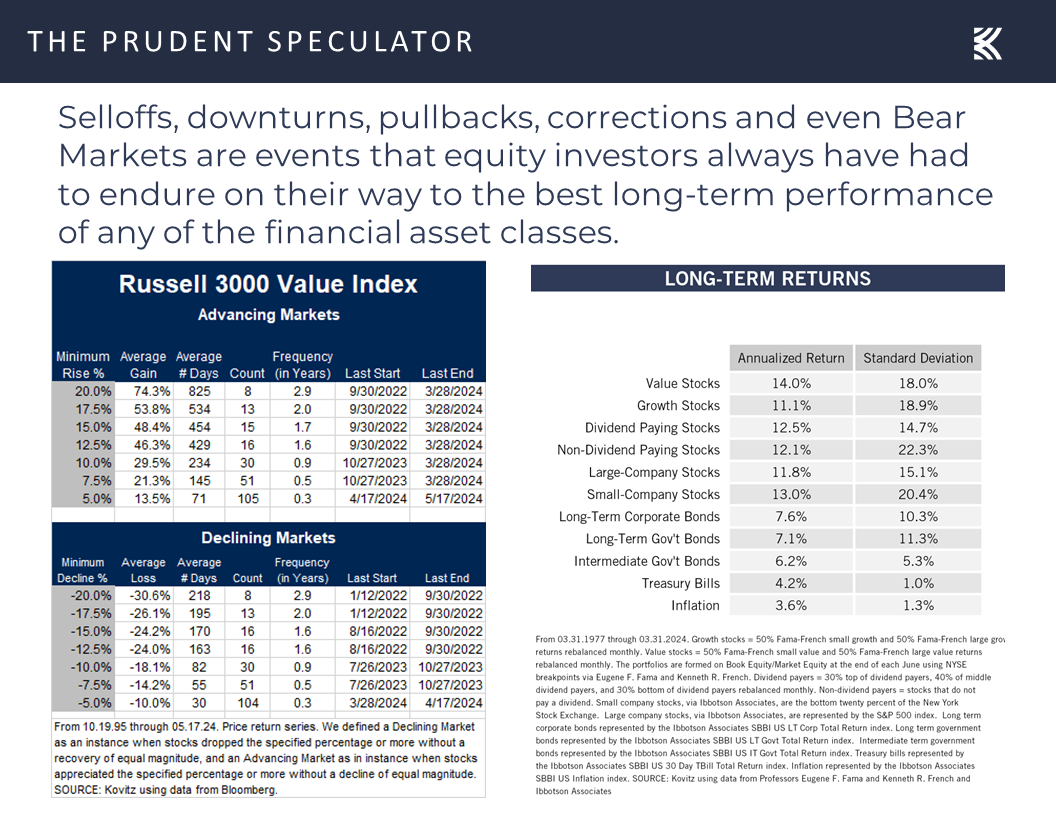

Volatility – Plenty of Gyrations but Long-Term Trend is Up

Yes, we must endure scary headlines along the way,

not to mention sometimes-disconcerting volatility, but equities always have proved very rewarding in the fullness of time.

Stock News – Updates on eight stocks across five different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Nvidia, Interest Rates, Valuations and Earnings

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Nvidia, Interest Rates, Valuations, and Earnings. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Trades – 9 Buys Across 4 Portfolios

Market of Stocks – Averages Up Last Week; Most Stocks Down

Nvidia – Other Less-Expensive Ways to Participate in A.I. Enthusiasm

Interest Rates – Yields Decline in Latest Week

Econ Data – Mixed Numbers; Q2 GDP Outlook Improves

Earnings – Solid Growth Estimated in ’24 & ’25

Valuations – Inexpensive Multiples for Value Stocks

Sentiment – AAII More Bearish

Volatility – Plenty of Gyrations but Long-Term Trend is Up

Stock News – Updates on the Energy sector and two additional stocks

Market of Stocks – Averages Up Last Week; Most Stocks Down

Given that the average stock in the S&P 500 fell 0.70% and the Russell 2000 SmallCap Index skidded 2.07%, the first week of June provided little cheer, even as stories in the financial press might suggest otherwise. It is a market of stocks and not simply a stock market, so we always counsel to look beyond the headlines as sometimes (as was the case for articles in the May 31 and June 5 Wall Street Journal) they can be very misleading in terms of what is happening to a broadly diversified portfolio of inexpensively priced stocks.

Nvidia – Other Less-Expensive Ways to Participate in A.I. Enthusiasm

No doubt, the broad-based indexes are heavily influenced by stocks like high-priced Salesforce in the price-weighted Dow Jones Industrial Average or a titan like Nvidia in the capitalization-weighted S&P 500. And speaking of Nvidia, the investor darling accounts for more than a third (436 basis points) of the S&P’s return this year, given its 4.67% average weight in the index and its 144% total return.

With its market capitalization topping $3 trillion last week, it is not surprising that folks would want to know our current thinking on the rocket ship that has been Nvidia. While we have owned the A.I. superstar in the past with success, we do not presently hold the stock. Clearly, with the benefit of 20-20 hindsight, we wish we still had a position, but the valuation metrics have long been too rich for our taste.

Our investment process, which is valuation-driven and has been evolving since we first turned on the lights at The Prudent Speculator in March 1977, relies on the underlying idea that we should be buying stocks when they are on sale and trading at a significant discount to our determination of fair value. That is, we want to buy stocks that are (temporarily) out-of-favor or underappreciated, as in our view they offer several ways to benefit. These can include a market reassessment upward towards the historical norm for valuation metrics like sales and earnings and/or growth in those metrics. In simplistic terms, the P/E ratio could ratchet back up or the E part of the equation could increase with the P then also climbing.

This disciplined approach has afforded us the opportunity to buy other stellar Wall Street performers like Apple (AAPL – $196.89), which accounts for 15 basis points of the S&P 500’s 2024 return; Microsoft (MSFT – $423.85), 93 basis points; Alphabet (GOOG – $175.95), 43 basis points; and Meta Platforms (META – $492.96), 79 basis points; at what have turned out to be favorable prices, so we are comfortable in remaining patient for market volatility to afford us an inexpensive entry point. Such could one day again be the case with Nvidia. After all, the company, despite its massive market capitalization, still has plenty of growth potential, as the top- and bottom-line is likely to continue to move markedly higher for the foreseeable future.

Of course, we have plenty of exposure to companies that can benefit from the same dynamics that have propelled Nvidia to the stratosphere: Broadcom (AVGO – $1406.64) with its cutting-edge A.I. networking and connectivity solutions; Qualcomm (QCOM – $206.62) with its Snapdragon mobile processors and Adreno GPUs; Micron (MU – $130.94) and its purpose-built memory and storage solutions that support A.I. applications; Digital Realty (DLR – $146.35) and its data center real estate, Intel and its data center chips; Microsoft and its monetization of A.I. technology; et cetera.

In most cases, too, our Tech stocks also pay a dividend and/or buy back shares, whereas Nvidia’s current $0.10 per share quarterly dividend (one cent per share post the imminent 10-for-1 split) doesn’t go very far to help folks looking for their portfolios to generate income.

Interest Rates – Yields Decline in Latest Week

We might have thought that it would have been a favorable week for the proverbial soldiers and not just the generals, given that the yield on the benchmark U.S. government bond declined to 4.43% from 4.50% at the end of the week prior,

and the betting on the effective level for the year-end Fed Funds rate held steady at 4.963%, compared to 4.965% on May 31.

Econ Data – Mixed Numbers; Q2 GDP Outlook Improves

The economic data out last week was mixed as the important jobs report saw far more payrolls (272,000) created than expected in May,

but the jobless rate ticked up to 4.0%, the highest level since November 2021,

and average hourly earnings rose by a higher-than-estimated 4.1% on a year-over-year basis.

Also arguing that all may not be as rosy as it seems in the labor market, the number of job openings in April fell to 8.06 million, down from a revised 8.35 million in March and below the 8.35 million forecast,

while first-time filings for unemployment benefits in the latest week increased to 229,000, compared to projections of 220,000 and a revised tally of 221,000 the previous week.

On the other hand, factory orders excluding the volatile transportation sector advanced 0.7% in April, above the 0.5% increase that was expected,

and the report on business for the important Services Sector (Non-Manufacturing Index) in May from the Institute for Supply Management (ISM) jumped to 53.8, well above estimates 51.0.

True, the ISM Manufacturing Index for May came in below forecasts at 48.7,

but the odds of recession in the next 12 months, as tabulated by Bloomberg, remained at 30%,

the latest estimate for Q2 real (inflation-adjusted) GDP growth from the Atlanta Fed rebounded to a very good 3.1%,

Earnings – Solid Growth Estimated in ’24 & ’25

and Standard & Poor’s nudged up its outlook for corporate profit growth this year and next.

Valuations – Inexpensive Multiples for Value Stocks

Given that improving earnings, stronger GDP growth and lower interest rates should make stocks more attractive, all else equal,

Sentiment – AAII More Bearish

we see no reason to alter our bullish enthusiasm, especially with the folks on Main Street becoming more Bearish last week as there was a rise in pessimists in the weekly Sentiment Survey from the American Association of Individual Investors (AAII)

Of course, the empirical data show that one should stick with stocks no matter what the AAII Bull-Bear gauge is registering,

especially as the evidence is overwhelming that the only problem with market timing is getting the timing right.

Volatility – Plenty of Gyrations but Long-Term Trend is Up

Yes, we must endure scary headlines along the way,

not to mention sometimes-disconcerting volatility, but equities always have proved very rewarding in the fullness of time.

Stock News – Updates on eight stocks across five different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.