The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss earnings, Jerome H. Powell, the AAII Sentiment, a recession and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Sentiment – Stocks Fall Just as Folks Pile In

Volatility – Plenty of Disconcerting Events but Long-Term Trend in Equities is Higher

Jerome H. Powell – Fed Chair on Capitol Hill

Inflation – Prior Fed Fight Went Very Well for Value & Dividend Payers

Econ Stats – Stronger-than-Expected Housing Numbers and LEI Contracts but Q2 GDP Growth Outlook Improves

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

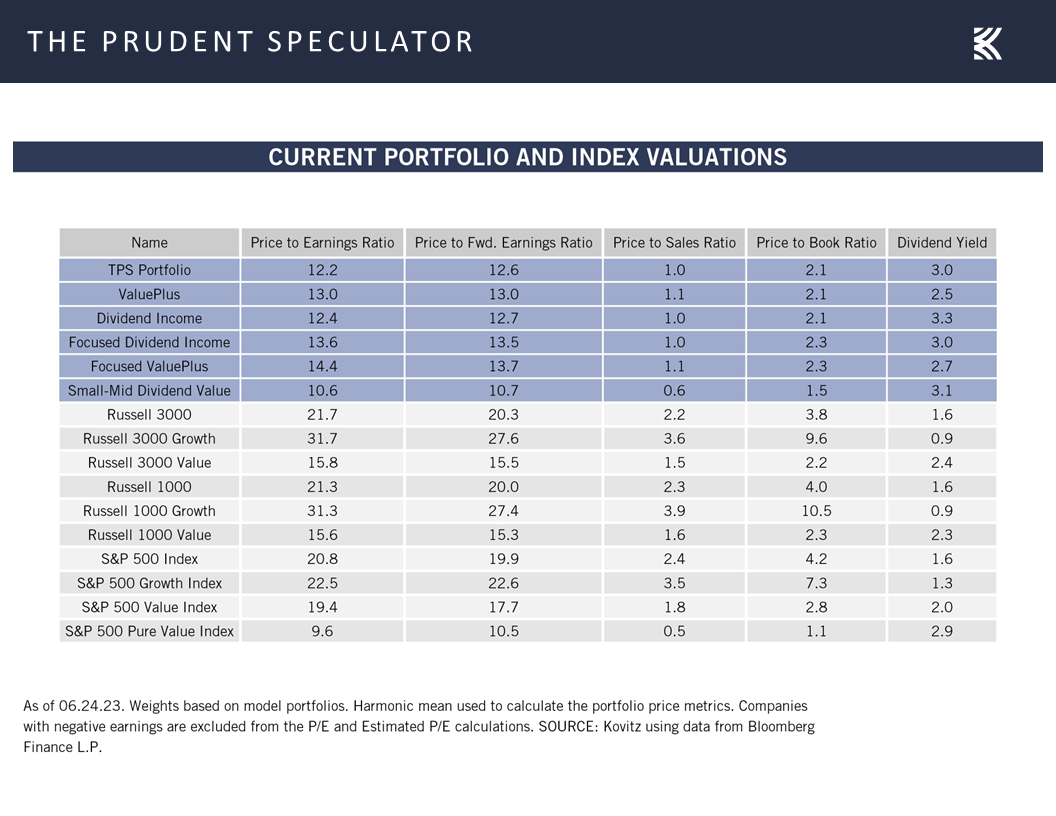

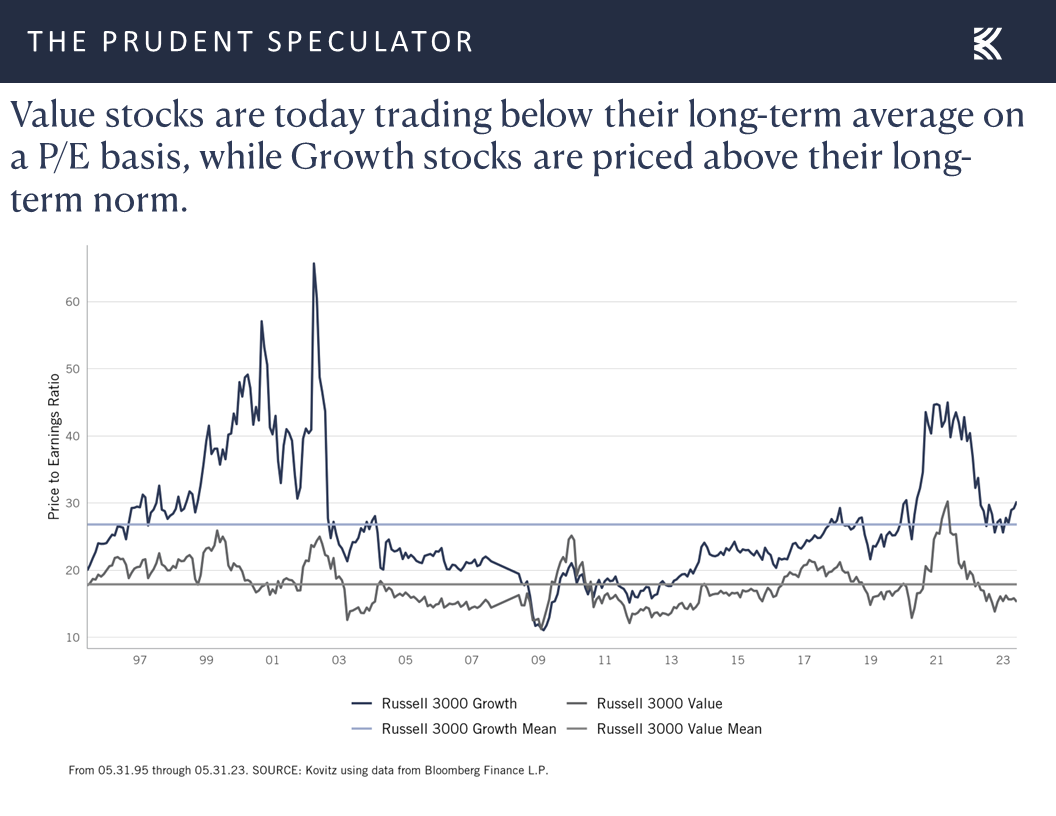

Valuations – Stocks, Especially Value, Remain Reasonably Priced

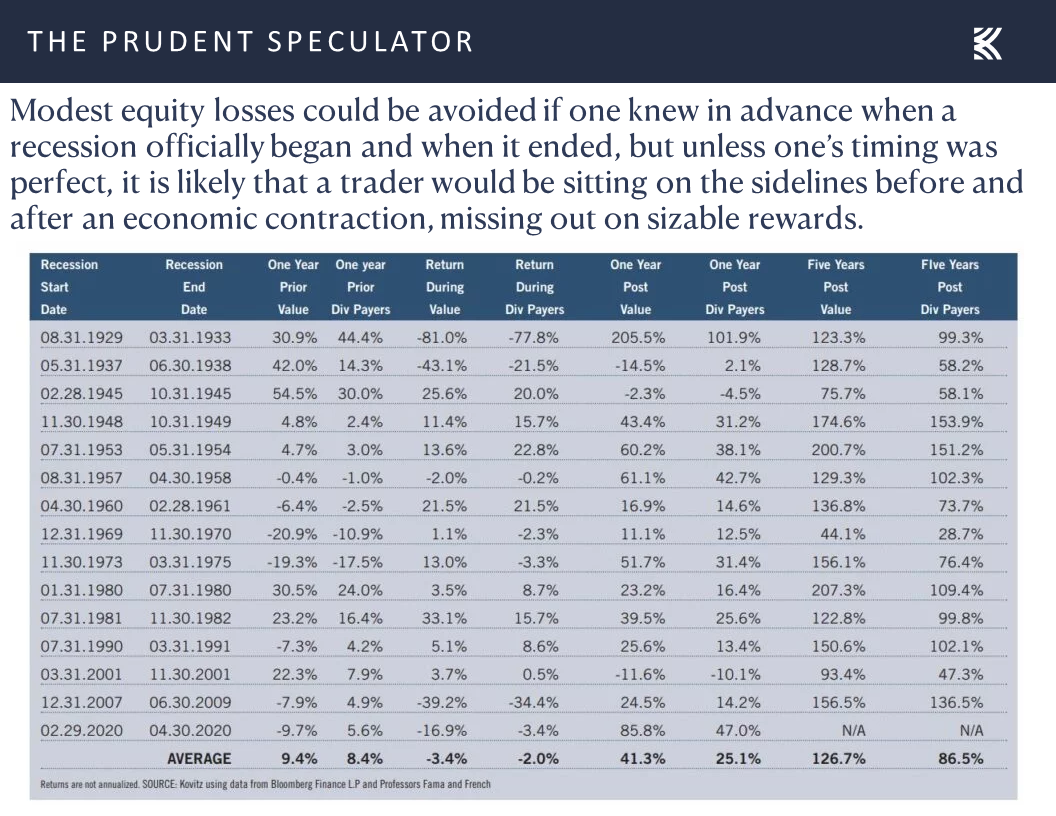

Recessions – No Reason for Long-Term-Oriented Investors to Fear a Contraction

Stock News – Updates on FDX, WKC & CIVI

Sentiment – Stocks Fall Just as Folks Pile In

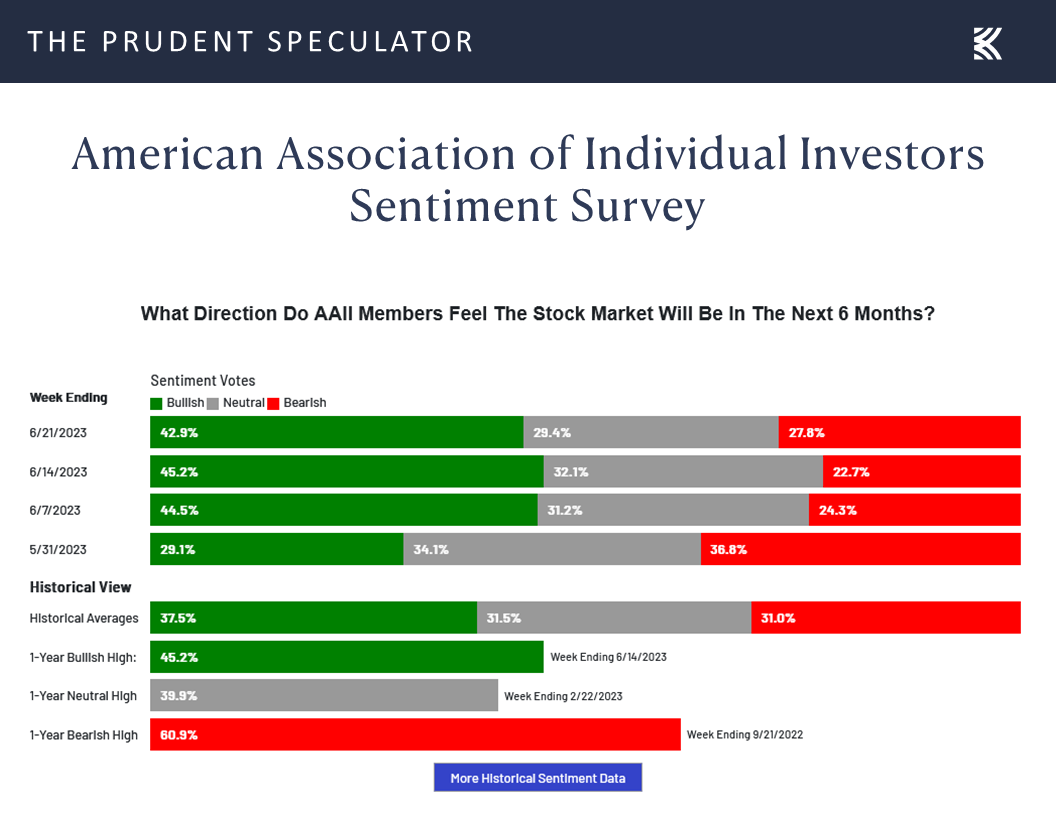

The four-trading-day period just ended provided another reminder of why the only problem with market timing is getting the timing right. After all, stocks suffered their worst week since March, right after the American Association of Individual Investors (AAII) Bull-Bear Spread hit its most optimistic level in 19 months the week prior.

To be sure, it isn’t as if one should abandon stocks when Bullishness is high as subsequent equity returns, on average, have still been positive, but we were not unhappy to see the Bull-Bear Spread contract last week to 15.1 points from 22.5 the week before.

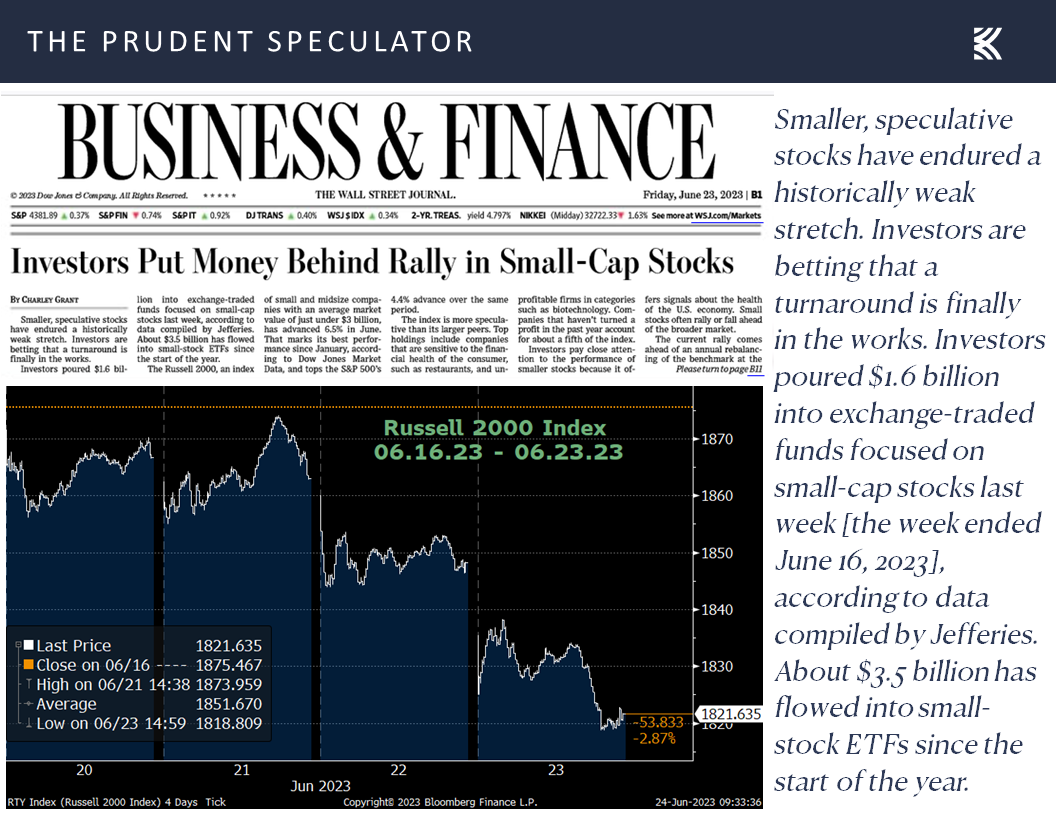

Of course, the AAII Sentiment Survey merely tabulates whether folks are Bullish or Bearish on stocks for the next six months and we note that people may say one thing and do something else with their money. This time around, however, it would seem that the optimists were talking the talk and walking the walk, as evidenced by The Wall Street Journal running a piece on Friday proclaiming, “Investors Put Money Behind Rally In Small Cap-Stocks,” and highlighting the big flows into smaller stocks the week prior…right before the Russell 2000 suffered a big setback over the past four trading sessions.

Volatility – Plenty of Disconcerting Events but Long-Term Trend in Equities is Higher

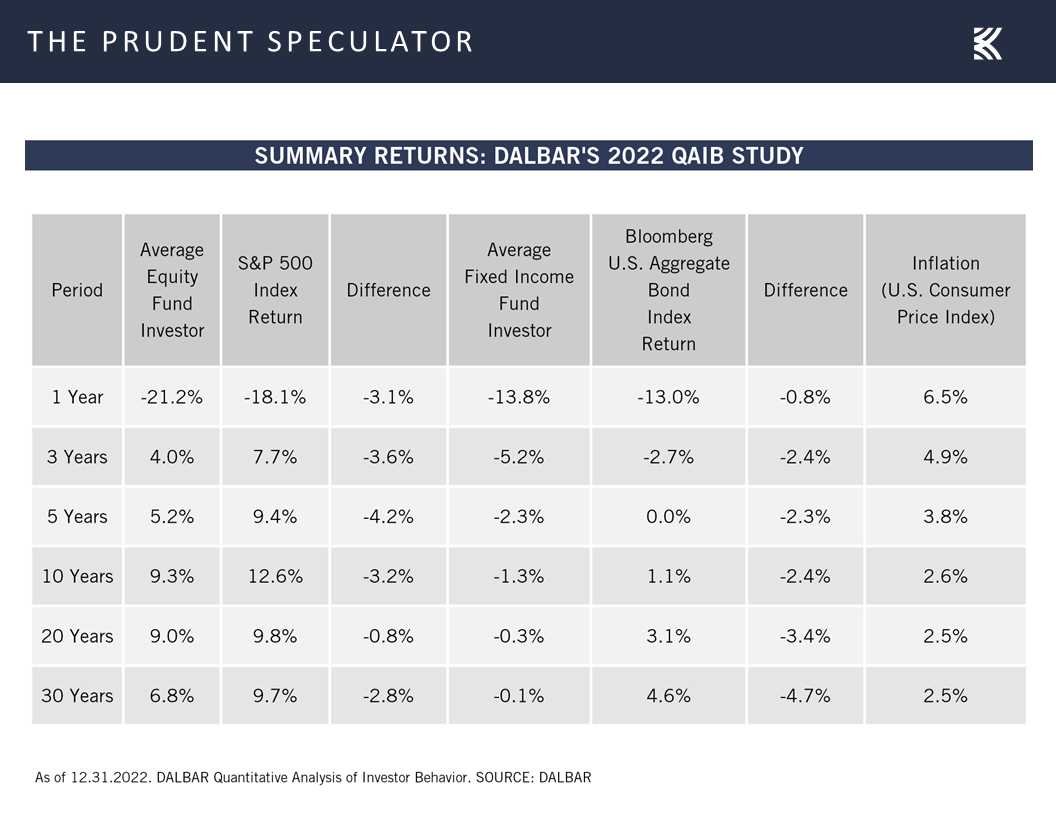

It isn’t the first and it won’t be the last instance that investors zigged when it might have been better to have zagged, but it does provide more evidence that far too many folks shoot themselves in the foot with ill-timed moves into and out of stocks. As we frequently cite, numbers on investor returns from data research firm DALBAR show that whether it comes to equity or fixed income funds, market timing can be hazardous to one’s wealth.

Believe it or not, over the past 30 years, investors in stock funds have cost themselves mightily with lousy timing decisions, while bond fund investors have fared even worse. Incredibly, the investor return in equity funds trailed the return of the S&P 500 by 280-basis-point per annum over the last three decades, while the average fixed-income investor saw a 470-basis-point difference from the bond benchmark, which pushed returns into the red for the entire period. That’s correct, per DALBAR, the average investor in bond funds lost money for the 30 years ending 2022.

Jerome H. Powell – Fed Chair on Capitol Hill

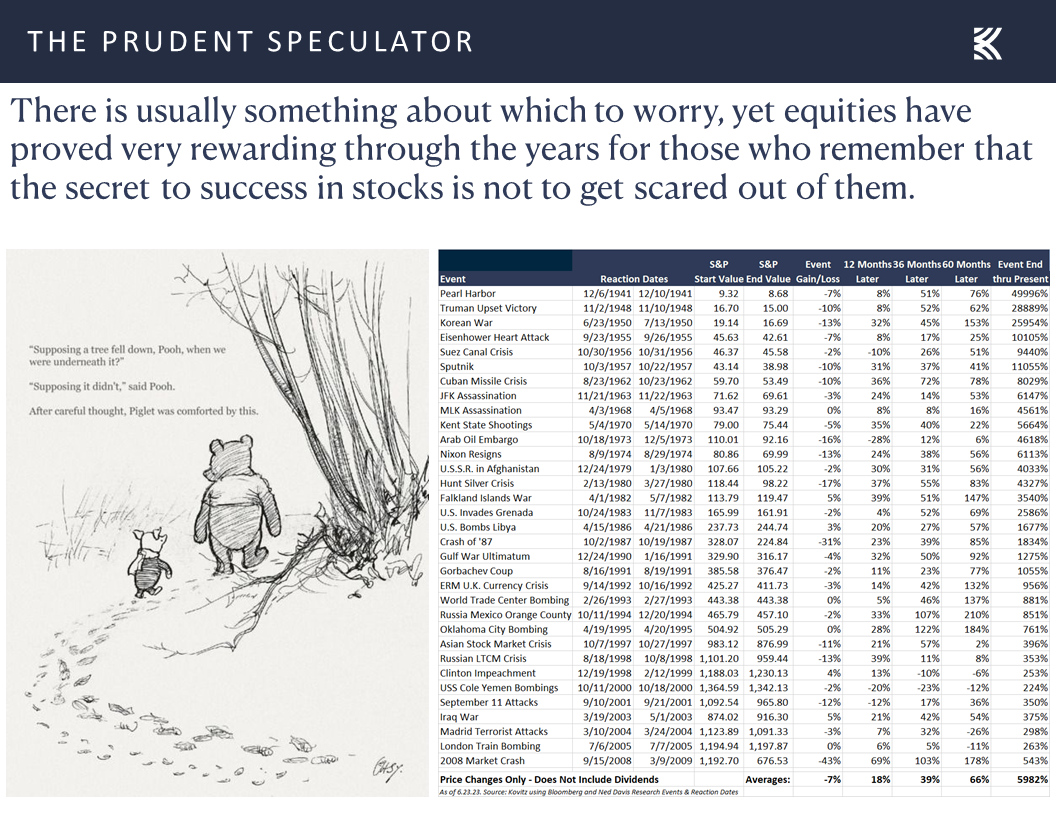

While the direction of stocks over the long term has been higher, despite plenty of disconcerting events along the way,

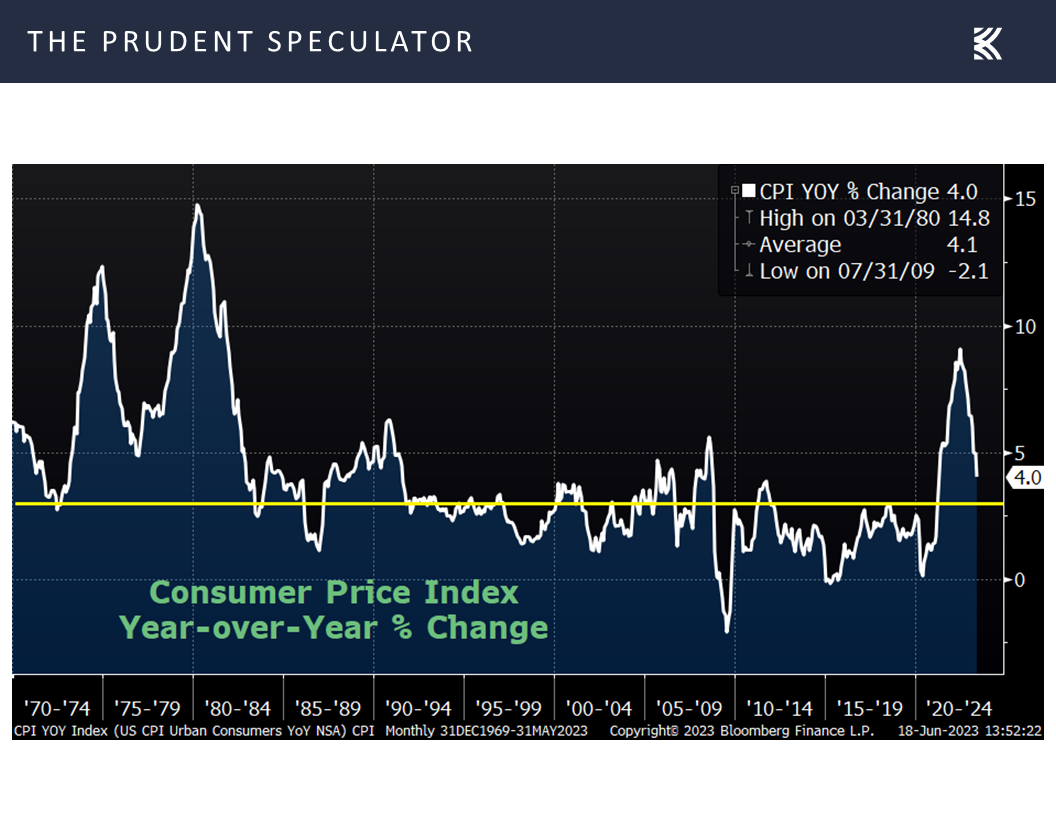

we respect that many are worried that inflation remains well above the Federal Reserve’s 2.0% target,

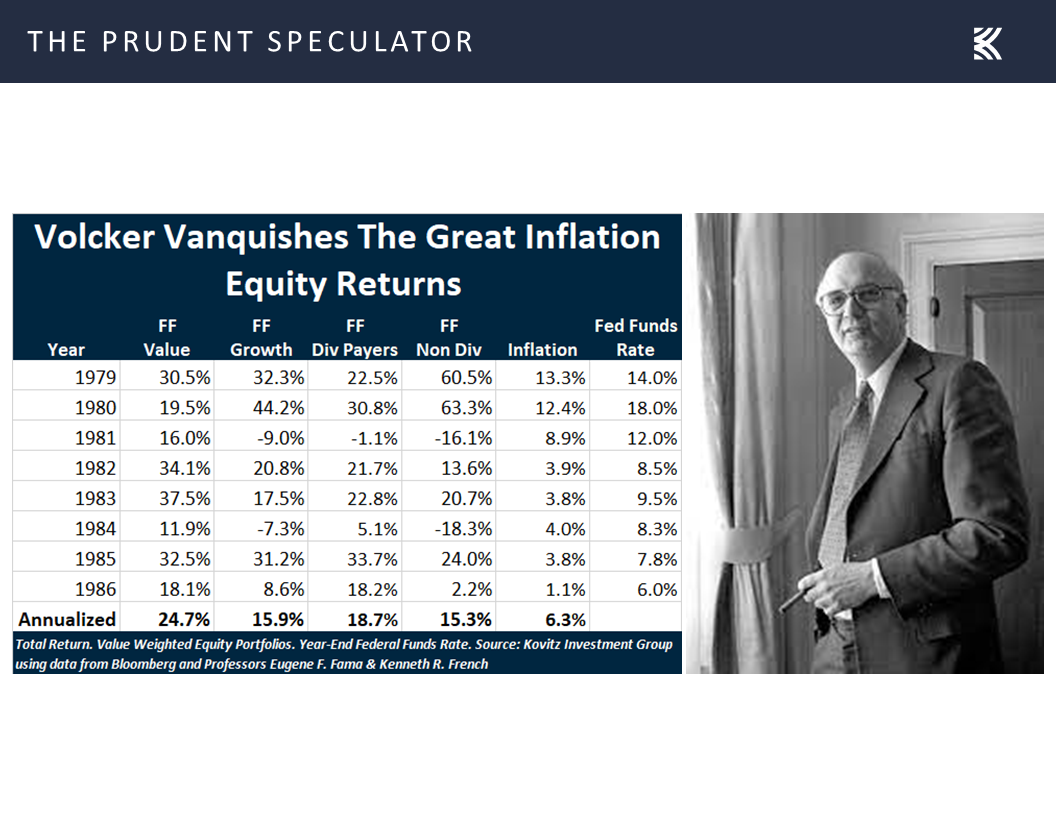

even as the last big Federal Reserve fight with inflation at the end of the 1970s turned out spectacularly well for Value Stocks and Dividend Payers, despite the Volcker Fed arguably causing two recessions along the way.

Inflation – Prior Fed Fight Went Very Well for Value & Dividend Payers

There is no guarantee that the past is prologue and Jerome H. Powell testified on Capitol Hill last week, “Inflation pressures continue to run high, and the process of getting inflation back down to 2% has a long way to go.”

There is no guarantee that the past is prologue and Jerome H. Powell testified on Capitol Hill last week, “Inflation pressures continue to run high, and the process of getting inflation back down to 2% has a long way to go.”

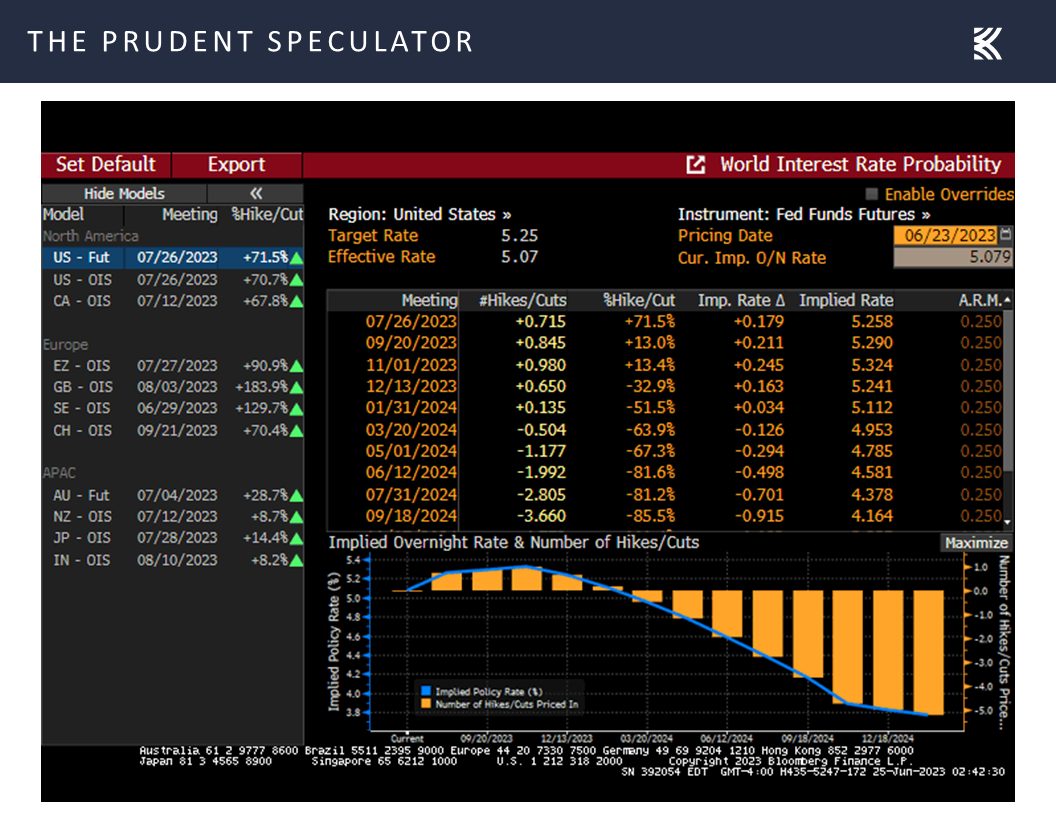

The Fed Chair went on to state, “Nearly all FOMC participants expect that it will be appropriate to raise interest rates somewhat further by the end of the year,” which caused a slight increase in the expected rates in the Fed Funds futures market. Of course, the current year-end level suggested by the futures of 5.24%, while up from 5.21% a week ago,

is still below the FOMC’s projection of 5.6%.

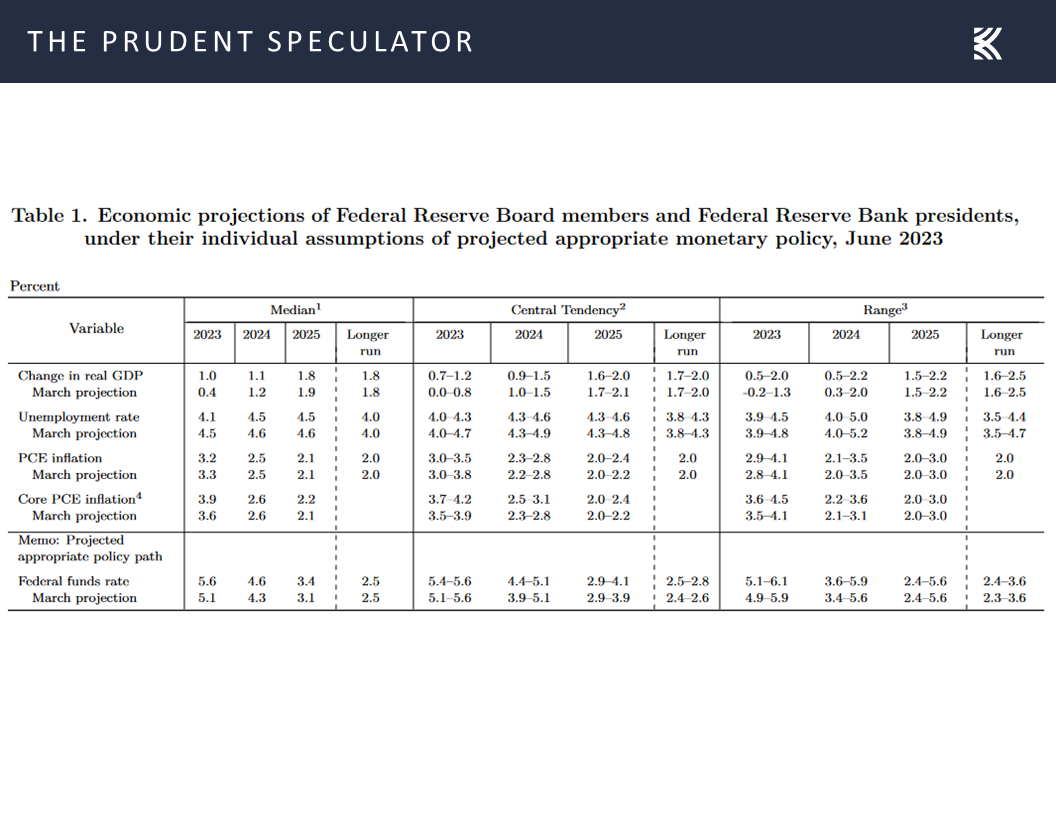

Those projections from the FOMC also show that the U.S. economy will avoid recession and will see modest real (inflation-adjusted) growth of 1.0% this year, with Chair Powell’s Current Economic Situation and Outlook in his prepared Capitol Hill remarks supporting that view.

The U.S. economy slowed significantly last year, and recent indicators suggest that economic activity has continued to expand at a modest pace. Although growth in consumer spending has picked up this year, activity in the housing sector remains weak, largely reflecting higher mortgage rates. Higher interest rates and slower output growth also appear to be weighing on business fixed investment.

The labor market remains very tight. Over the first five months of the year, job gains averaged a robust 314,000 jobs per month. The unemployment rate moved up but remained low in May, at 3.7 percent. There are some signs that supply and demand in the labor market are coming into better balance. The labor force participation rate has moved up in recent months, particularly for individuals aged 25 to 54. Nominal wage growth has shown some signs of easing, and job vacancies have declined so far this year. While the jobs-to-workers gap has narrowed, labor demand still substantially exceeds the supply of available workers.

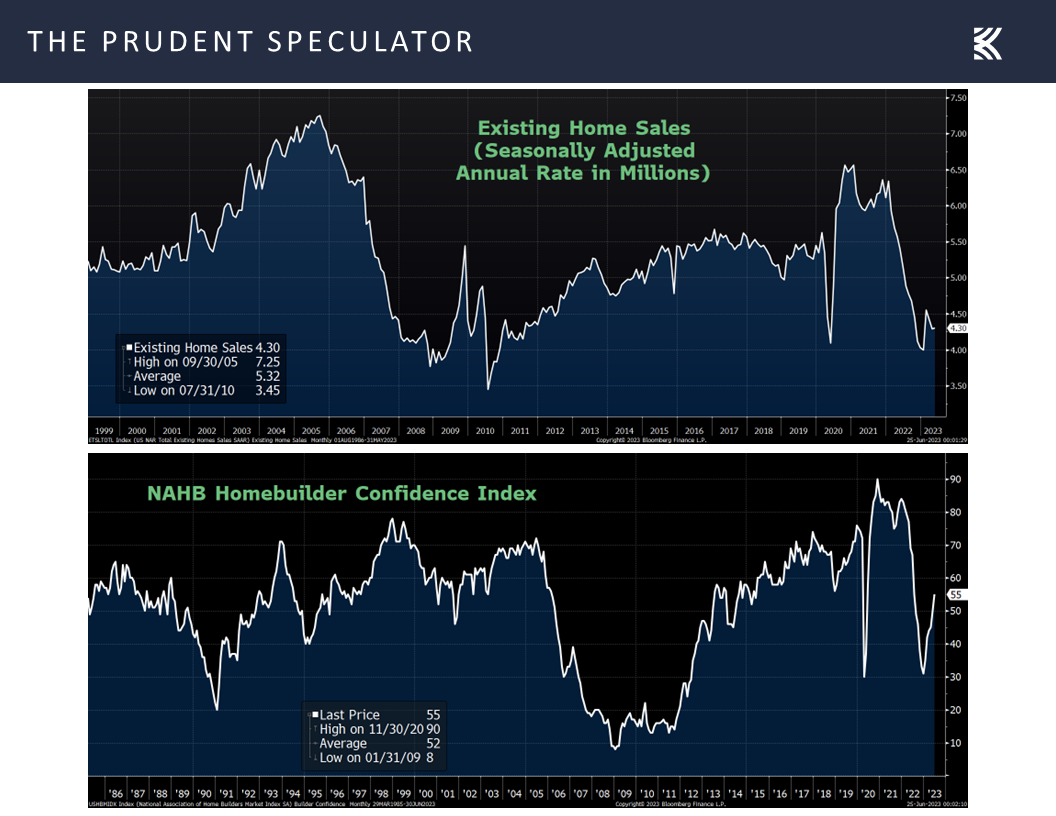

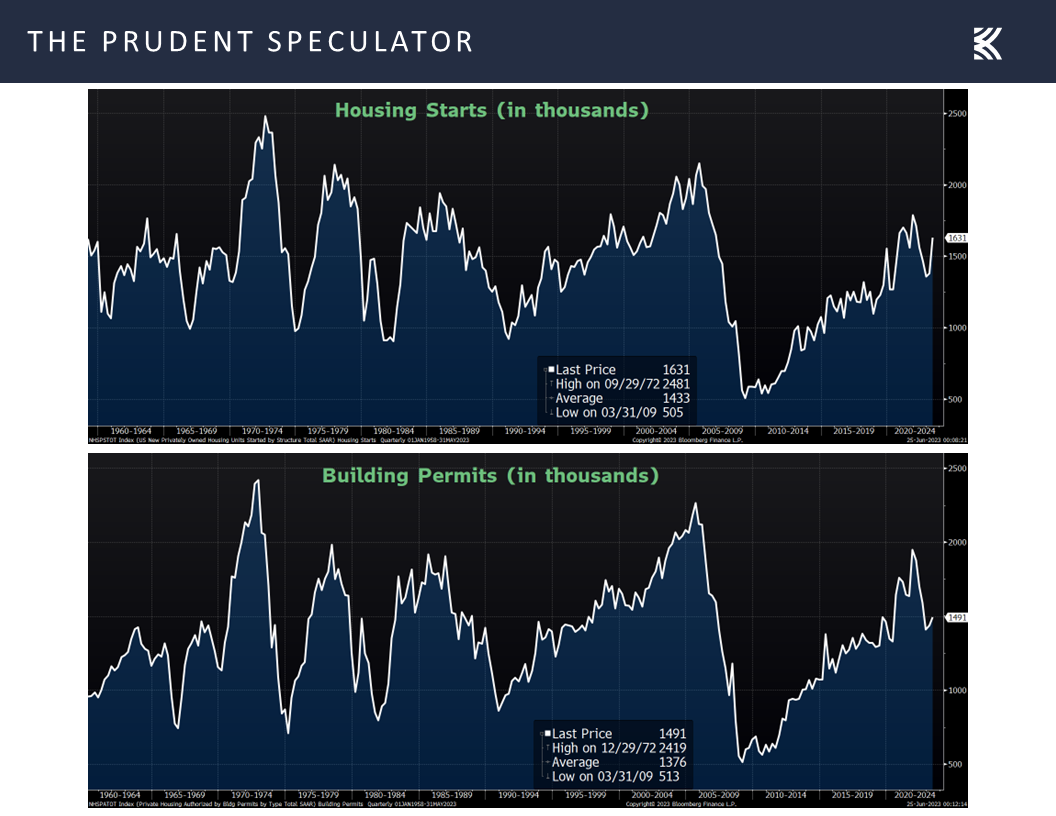

Interestingly, the numbers out last week on the state of housing seemed more upbeat than Mr. Powell’s assessment, given better-than-expected data on existing home sales for May and homebuilder sentiment for June, despite higher mortgage rates.

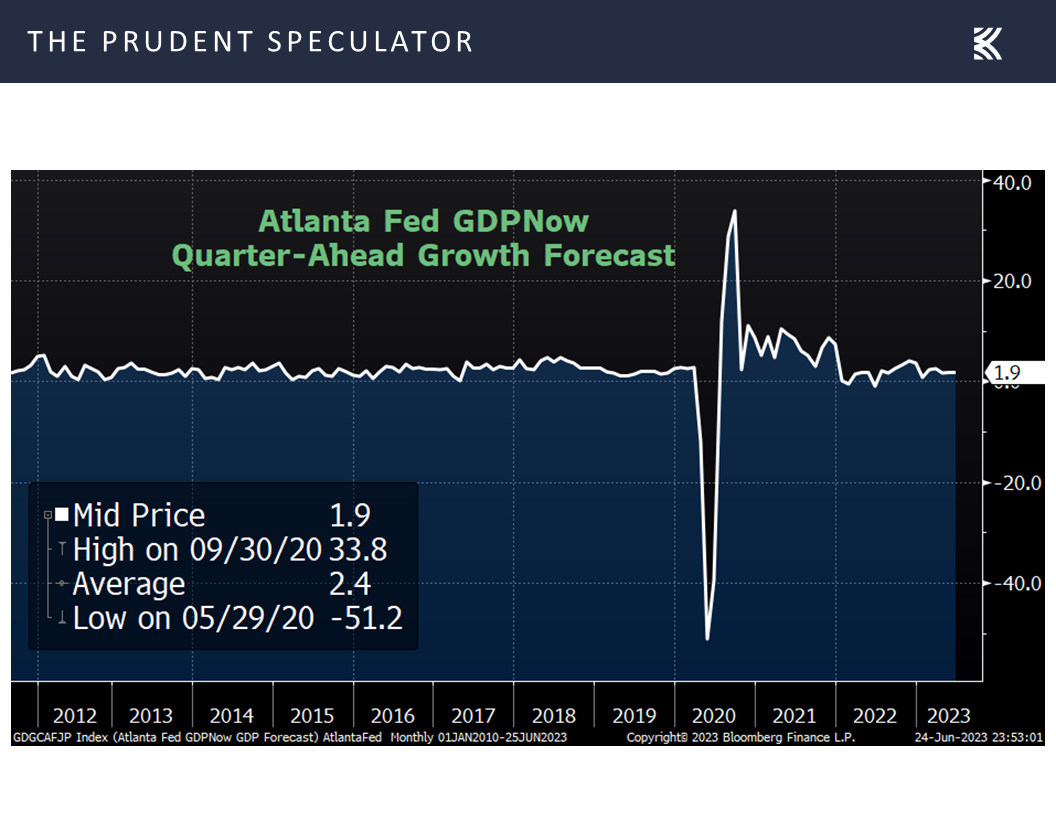

Econ Stats – Stronger-than-Expected Housing Numbers and LEI Contracts but Q2 GDP Growth Outlook Improves

Builders seemed to be putting their money where their more optimistic mouths were, given much-stronger-than-forecast figures on May housing starts and building permits.

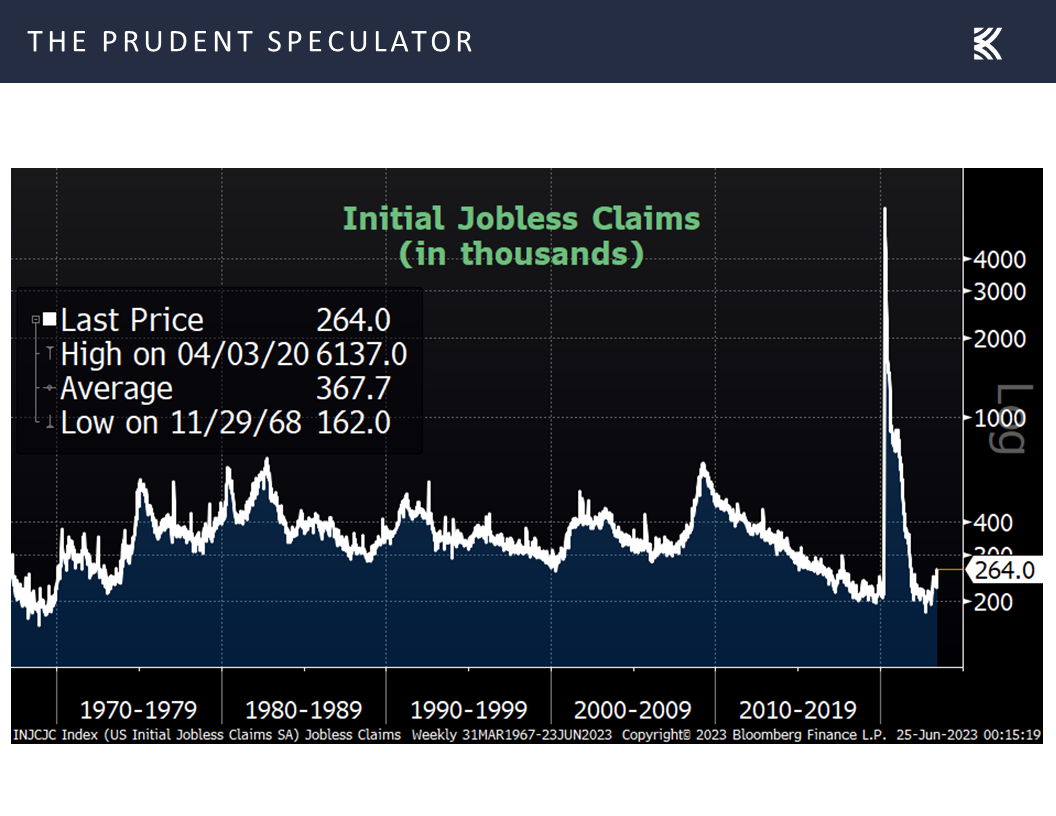

True, first-time filings for unemployment benefits ticked up in the latest week,

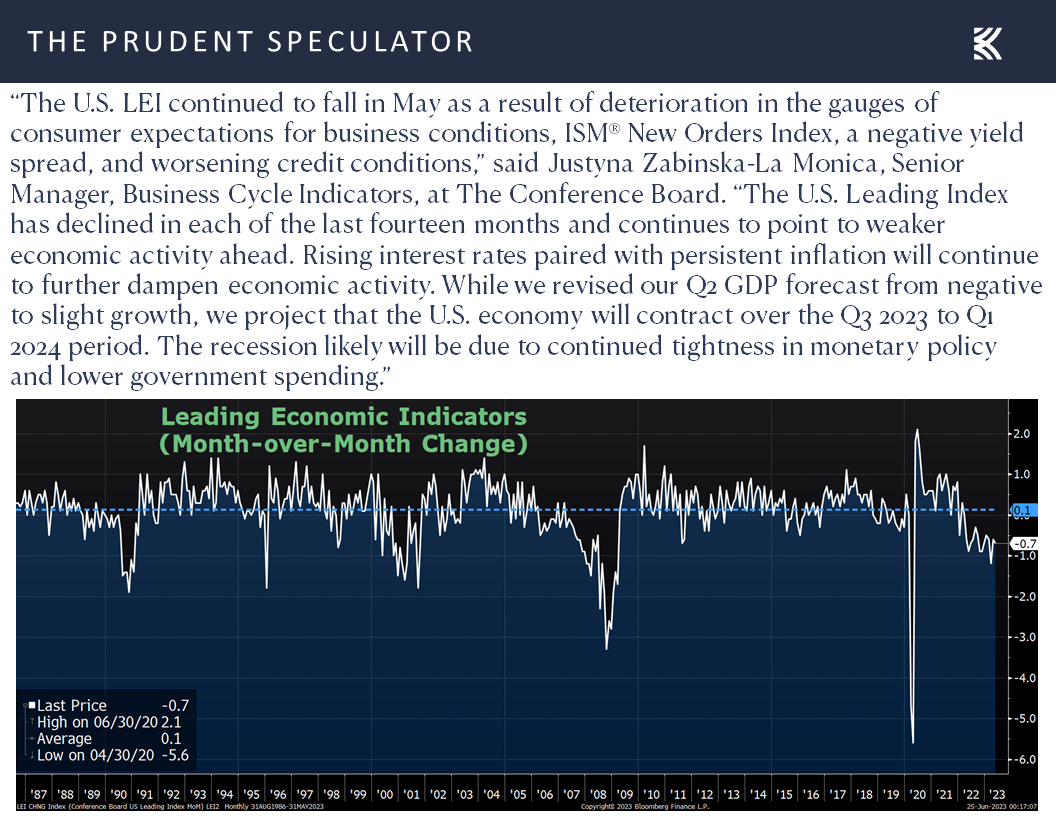

and the forward-looking Leading Economic Index from the Conference Board fell by 0.7% in May, while the keeper of that gauge continues to think a recession is on the way,

but the latest projection from the Atlanta Fed for Q2 real economic growth moved up a tad to 1.9% last week from 1.8% the week prior.

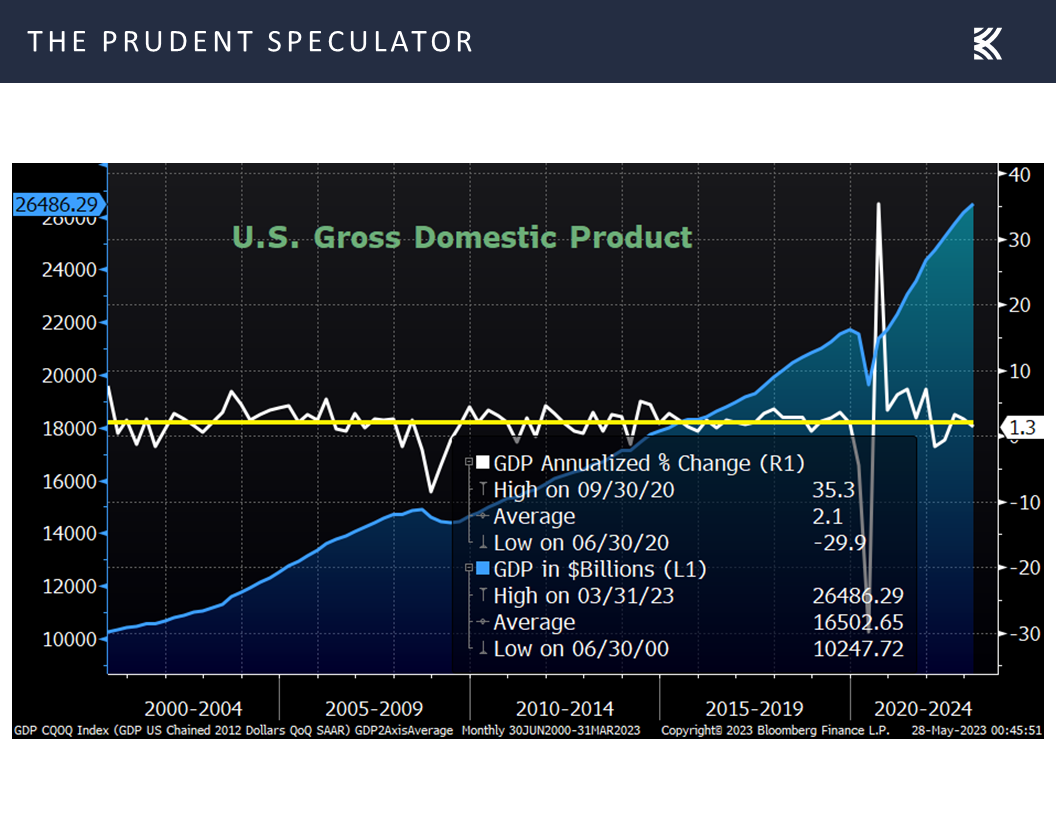

Time will tell whether we manage to avoid an inflation-adjusted economic contraction, but we have seen virtually no estimates that call for a drop in nominal U.S. GDP,

which we think should continue to provide a favorable backdrop for corporate profits, which are measured in nominal dollars,

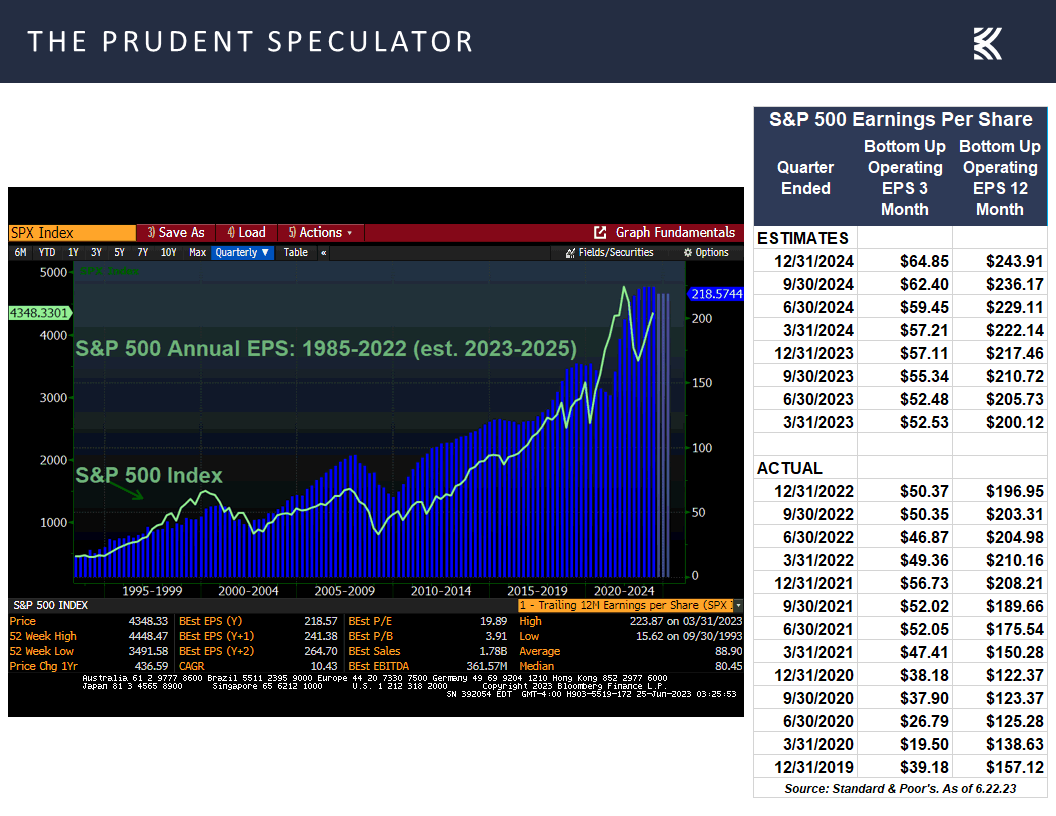

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

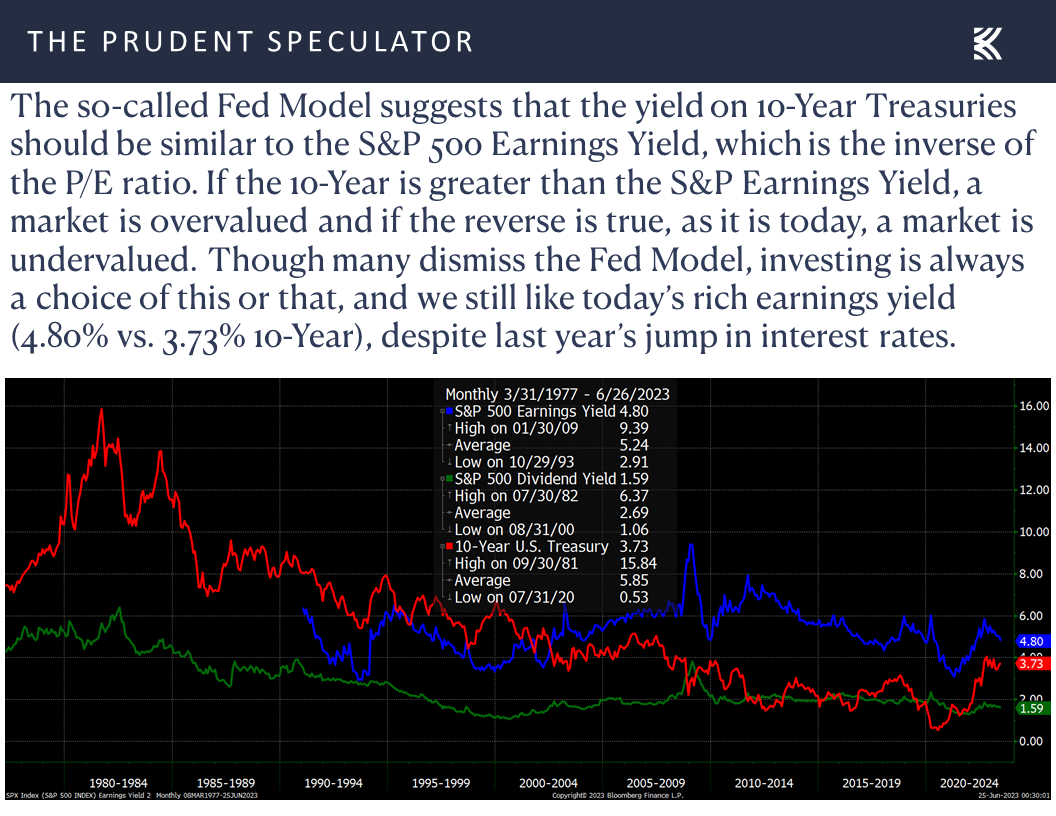

and should support the argument that stocks, which are also priced in nominal dollars, are still reasonably priced vis-à-vis long-term interest rates.

Valuations – Stocks, Especially Value, Remain Reasonably Priced

More importantly, we continue to like the dividend yields and valuation metrics associated with our broadly diversified portfolios of what we believe to be undervalued stocks,

while we note that Value, unlike Growth, is still trading below its historical norm on an earnings basis since the inception of the Russell style indexes in 1995.

Recessions – No Reason for Long-Term-Oriented Investors to Fear a Contraction

Finally, given our long-term time horizon, we might argue that we would like to see a recession, as historically modest average declines during the contraction for Value Stocks and Dividend Payers have been followed by a massive rebound, on average, over the ensuing 12-months and five years after the economic downturn has ended.

Stock News – Updates on three stocks across three different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Recession, Earnings, Jerome. H Powell, AAII Sentiment and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss earnings, Jerome H. Powell, the AAII Sentiment, a recession and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Sentiment – Stocks Fall Just as Folks Pile In

Volatility – Plenty of Disconcerting Events but Long-Term Trend in Equities is Higher

Jerome H. Powell – Fed Chair on Capitol Hill

Inflation – Prior Fed Fight Went Very Well for Value & Dividend Payers

Econ Stats – Stronger-than-Expected Housing Numbers and LEI Contracts but Q2 GDP Growth Outlook Improves

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

Valuations – Stocks, Especially Value, Remain Reasonably Priced

Recessions – No Reason for Long-Term-Oriented Investors to Fear a Contraction

Stock News – Updates on FDX, WKC & CIVI

Sentiment – Stocks Fall Just as Folks Pile In

The four-trading-day period just ended provided another reminder of why the only problem with market timing is getting the timing right. After all, stocks suffered their worst week since March, right after the American Association of Individual Investors (AAII) Bull-Bear Spread hit its most optimistic level in 19 months the week prior.

To be sure, it isn’t as if one should abandon stocks when Bullishness is high as subsequent equity returns, on average, have still been positive, but we were not unhappy to see the Bull-Bear Spread contract last week to 15.1 points from 22.5 the week before.

Of course, the AAII Sentiment Survey merely tabulates whether folks are Bullish or Bearish on stocks for the next six months and we note that people may say one thing and do something else with their money. This time around, however, it would seem that the optimists were talking the talk and walking the walk, as evidenced by The Wall Street Journal running a piece on Friday proclaiming, “Investors Put Money Behind Rally In Small Cap-Stocks,” and highlighting the big flows into smaller stocks the week prior…right before the Russell 2000 suffered a big setback over the past four trading sessions.

Volatility – Plenty of Disconcerting Events but Long-Term Trend in Equities is Higher

It isn’t the first and it won’t be the last instance that investors zigged when it might have been better to have zagged, but it does provide more evidence that far too many folks shoot themselves in the foot with ill-timed moves into and out of stocks. As we frequently cite, numbers on investor returns from data research firm DALBAR show that whether it comes to equity or fixed income funds, market timing can be hazardous to one’s wealth.

Believe it or not, over the past 30 years, investors in stock funds have cost themselves mightily with lousy timing decisions, while bond fund investors have fared even worse. Incredibly, the investor return in equity funds trailed the return of the S&P 500 by 280-basis-point per annum over the last three decades, while the average fixed-income investor saw a 470-basis-point difference from the bond benchmark, which pushed returns into the red for the entire period. That’s correct, per DALBAR, the average investor in bond funds lost money for the 30 years ending 2022.

Jerome H. Powell – Fed Chair on Capitol Hill

While the direction of stocks over the long term has been higher, despite plenty of disconcerting events along the way,

we respect that many are worried that inflation remains well above the Federal Reserve’s 2.0% target,

even as the last big Federal Reserve fight with inflation at the end of the 1970s turned out spectacularly well for Value Stocks and Dividend Payers, despite the Volcker Fed arguably causing two recessions along the way.

Inflation – Prior Fed Fight Went Very Well for Value & Dividend Payers

The Fed Chair went on to state, “Nearly all FOMC participants expect that it will be appropriate to raise interest rates somewhat further by the end of the year,” which caused a slight increase in the expected rates in the Fed Funds futures market. Of course, the current year-end level suggested by the futures of 5.24%, while up from 5.21% a week ago,

is still below the FOMC’s projection of 5.6%.

Those projections from the FOMC also show that the U.S. economy will avoid recession and will see modest real (inflation-adjusted) growth of 1.0% this year, with Chair Powell’s Current Economic Situation and Outlook in his prepared Capitol Hill remarks supporting that view.

The U.S. economy slowed significantly last year, and recent indicators suggest that economic activity has continued to expand at a modest pace. Although growth in consumer spending has picked up this year, activity in the housing sector remains weak, largely reflecting higher mortgage rates. Higher interest rates and slower output growth also appear to be weighing on business fixed investment.

The labor market remains very tight. Over the first five months of the year, job gains averaged a robust 314,000 jobs per month. The unemployment rate moved up but remained low in May, at 3.7 percent. There are some signs that supply and demand in the labor market are coming into better balance. The labor force participation rate has moved up in recent months, particularly for individuals aged 25 to 54. Nominal wage growth has shown some signs of easing, and job vacancies have declined so far this year. While the jobs-to-workers gap has narrowed, labor demand still substantially exceeds the supply of available workers.

Interestingly, the numbers out last week on the state of housing seemed more upbeat than Mr. Powell’s assessment, given better-than-expected data on existing home sales for May and homebuilder sentiment for June, despite higher mortgage rates.

Econ Stats – Stronger-than-Expected Housing Numbers and LEI Contracts but Q2 GDP Growth Outlook Improves

Builders seemed to be putting their money where their more optimistic mouths were, given much-stronger-than-forecast figures on May housing starts and building permits.

True, first-time filings for unemployment benefits ticked up in the latest week,

and the forward-looking Leading Economic Index from the Conference Board fell by 0.7% in May, while the keeper of that gauge continues to think a recession is on the way,

but the latest projection from the Atlanta Fed for Q2 real economic growth moved up a tad to 1.9% last week from 1.8% the week prior.

Time will tell whether we manage to avoid an inflation-adjusted economic contraction, but we have seen virtually no estimates that call for a drop in nominal U.S. GDP,

which we think should continue to provide a favorable backdrop for corporate profits, which are measured in nominal dollars,

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

and should support the argument that stocks, which are also priced in nominal dollars, are still reasonably priced vis-à-vis long-term interest rates.

Valuations – Stocks, Especially Value, Remain Reasonably Priced

More importantly, we continue to like the dividend yields and valuation metrics associated with our broadly diversified portfolios of what we believe to be undervalued stocks,

while we note that Value, unlike Growth, is still trading below its historical norm on an earnings basis since the inception of the Russell style indexes in 1995.

Recessions – No Reason for Long-Term-Oriented Investors to Fear a Contraction

Finally, given our long-term time horizon, we might argue that we would like to see a recession, as historically modest average declines during the contraction for Value Stocks and Dividend Payers have been followed by a massive rebound, on average, over the ensuing 12-months and five years after the economic downturn has ended.

Stock News – Updates on three stocks across three different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.