Every month, The Prudent Speculator produces a newsletter that includes a market summary, helpful charts and graphs, recent equity market news, economic outlook and specific stock investment strategies focused on value stock investing. This month, our Graphic Detail offers our annual review of Valuation Factor returns, while we again add stocks to our four newsletter portfolios. We also include a preview of our current Recommended Stock List and Portfolio Builder section with ten highlighted stocks. Note that the entire list is available to our community of loyal subscribers only.

Editor’s Note: Dow Jones, Market Timing, Interest Rates

The first two days of April offered yet another reminder that selloffs, downturns, pullbacks, corrections and even Bear Markets are always part of the investment equation, but March was a terrific month. After all, the breadth of the market advance expanded markedly with the S&P 500 Equal Weighted index outperforming the capitalization-weighted S&P 500 and the Russell 3000 Value index (R3KV) outpacing its Growth counterpart by a sizable margin.

Those indexes ended Q1 with handsome year-to-date gains that pushed all the major equity market averages further into Bull Market territory since the October lows, and left the Dow Jones Industrial Average within shouting distance of the psychologically important 40,000 mark. As April marks 22 years since Al Frank’s passing, we thought it timely to turn to our founder for perspective written back in 1998 with the Dow near 9,000.

I have often quoted Mae West’s famous assertion, “Too much of a good thing is wonderful!” I think I understand some of the basic reasons for the large-cap-stock market to be at historically higher levels. Without going into great detail, the principal basis for today’s Bull Market is the realization by a great many that equities historically generally outperform most other forms of investments. This condition provides a constant stream of capital for buying stocks, which is frequently augmented by new and old investors joining in the bullish enthusiasm.

I’m very concerned about the mania in Internet stocks and the seeming inability of rational investors to bid up the relatively very undervalued small-and midcap stocks. We are getting closer to a substantial correction, but whether that begins tomorrow or three months from now, I would not care to guess. As I pay my substantial capital gains taxes on stocks that have for the most part advanced higher since I sold them, I feel rather good about clearing out some of my more fully valued portfolio and replacing those shares with more undervalued shares. I look forward to continuing this process of creating capital gains (and tax liabilities) and letting the market fend for itself.

Al was more or less spot on as a substantial correction did occur in 1998, Internet stocks eventually received their comeuppance when the Tech Bubble burst in 2000, it proved wise to swap more richly valued stocks for more undervalued names AND equities continued to outperform most other investments in the fullness of time.

Clearly, there can be no assurance that past is prologue, but as was the case more than a quarter-century ago, we remain very confident that time in the market will trump market timing, even as we concede that 10% corrections occur on average every 11 months and we could argue that there is a mania in A.I. stocks these days while so-called Meme stocks continue to see wild price swings.

Many are of the mind that the “market” is overvalued, but we offer the reminder that we are invested in individual stocks, with the forward P/E ratio for TPS Portfolio of 15 far less than the 22 for the S&P 500 and even below the 17 for the R3KV. What’s more, the dividend yield for TPS is 2.5%, versus 1.4% for the S&P and 2.1% for the R3KV.

True, interest rates have ticked higher of late, but the current yield of 4.36% on the 10-Year U.S. Treasury compares favorably to the 5.82% long-term average since the launch of The Prudent Speculator 47 years ago. And, Federal Reserve Chair Jerome H. Powell reminded on March 20, “We believe that our policy rate is likely at its peak for this tightening cycle and that, if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year.”

With Mr. Powell adding, “Inflation has eased substantially while the labor market has remained strong, and that is very good news,” we maintain our belief that patiently investing in a broadly diversified portfolio of undervalued stocks will continue to be a good thing!

“Do not spoil what you have by desiring what you have not.” — Epicurus

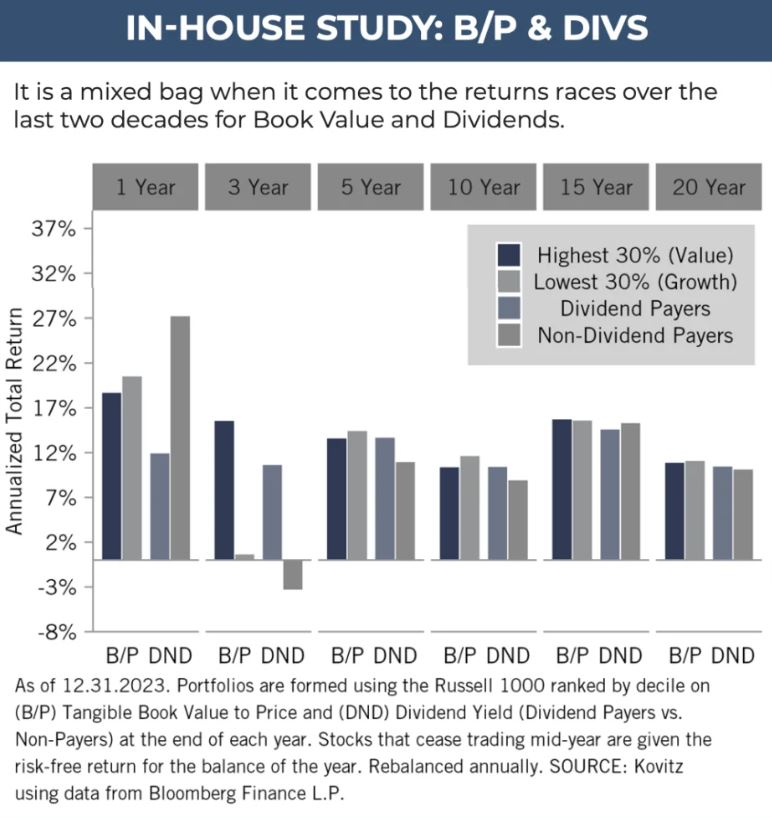

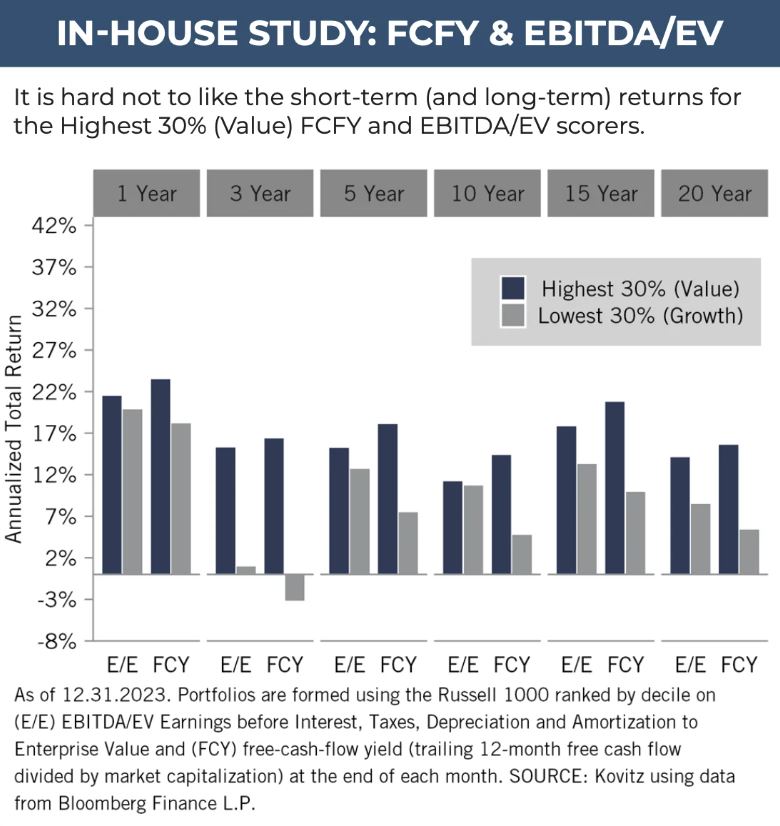

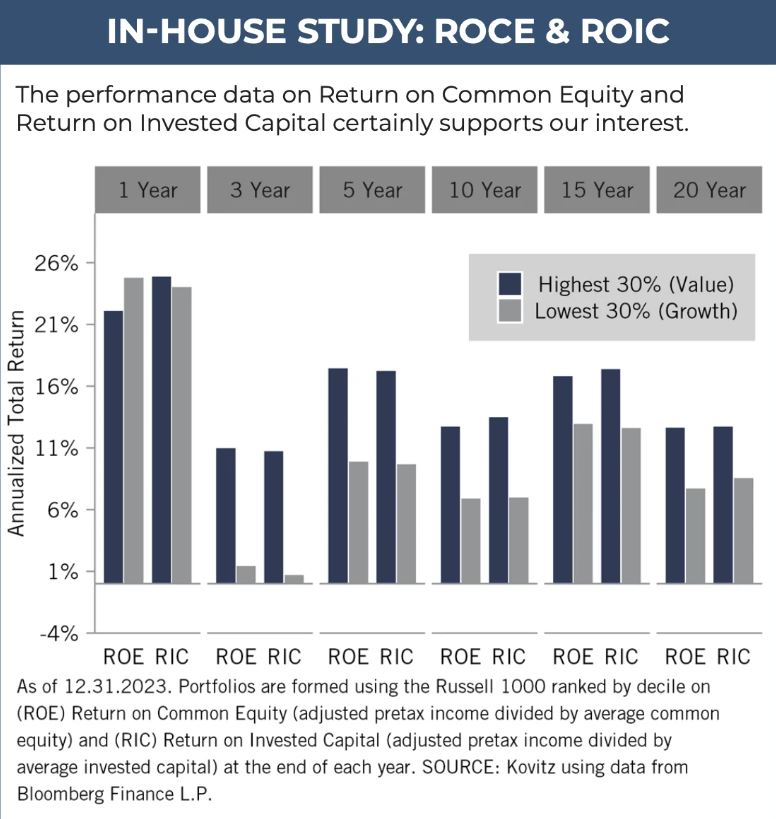

Graphic Detail: Valuation Factors Revisited: Historical Evidence

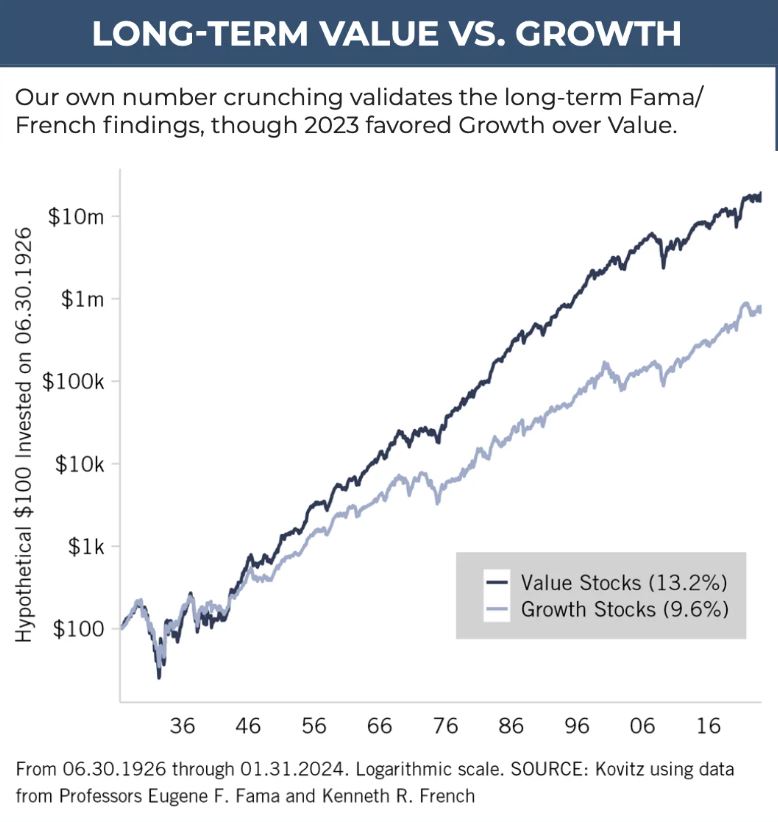

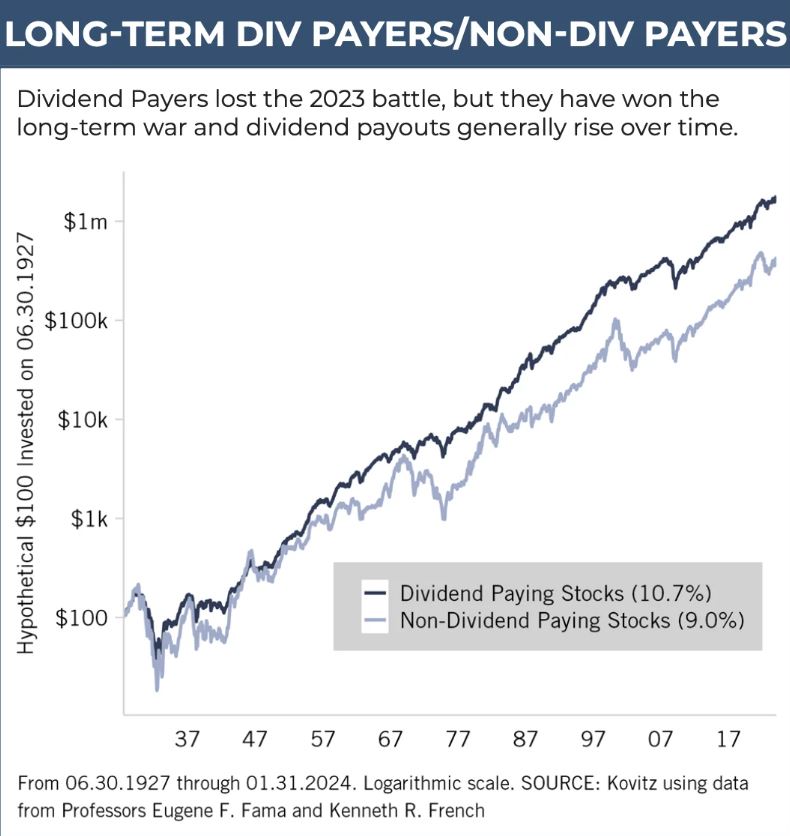

Value stocks, per data from June 1927 through January 2024 compiled by Professors Eugene F. Fama and Kenneth R. French, have topped the long-term performance scorecard versus Growth by a score of 13.2% to 9.6% per annum. And, via a separate data series, the duo has calculated that Dividend-Paying stocks have outperformed Non-Dividend Payers by a per-year tally of 10.7% to 9.0% over the same nine-plus decades. Those return gaps are large, especially when one considers the impact of compounding over multi-year periods. It is little wonder, then, given our multi-year time horizon, that we remain loyal to our four-plus-decade-old strategy of buying and harvesting portfolios of what we believe to be undervalued stocks, most often of dividend-paying companies.

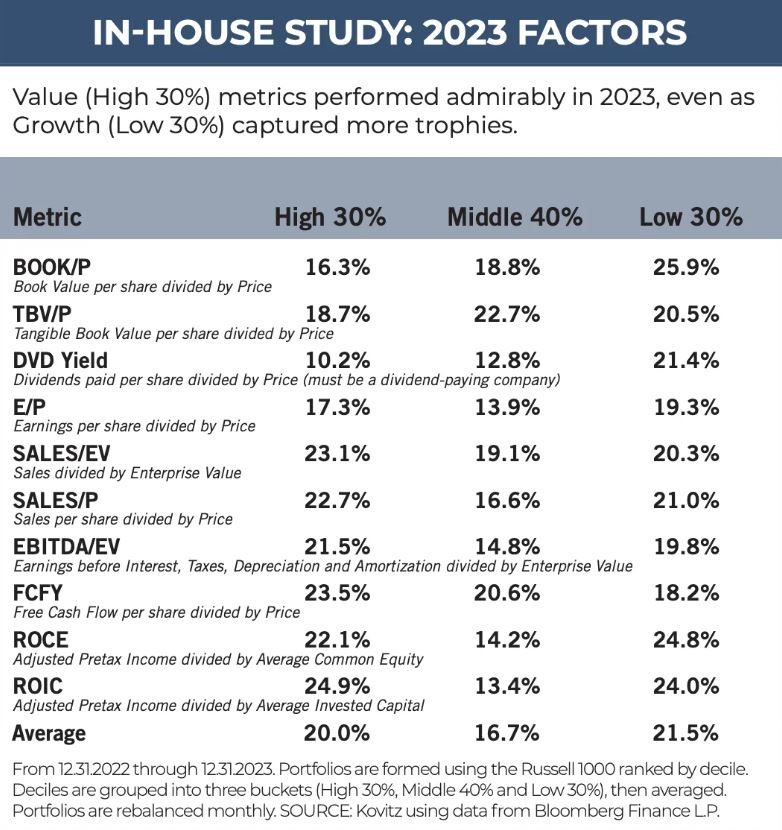

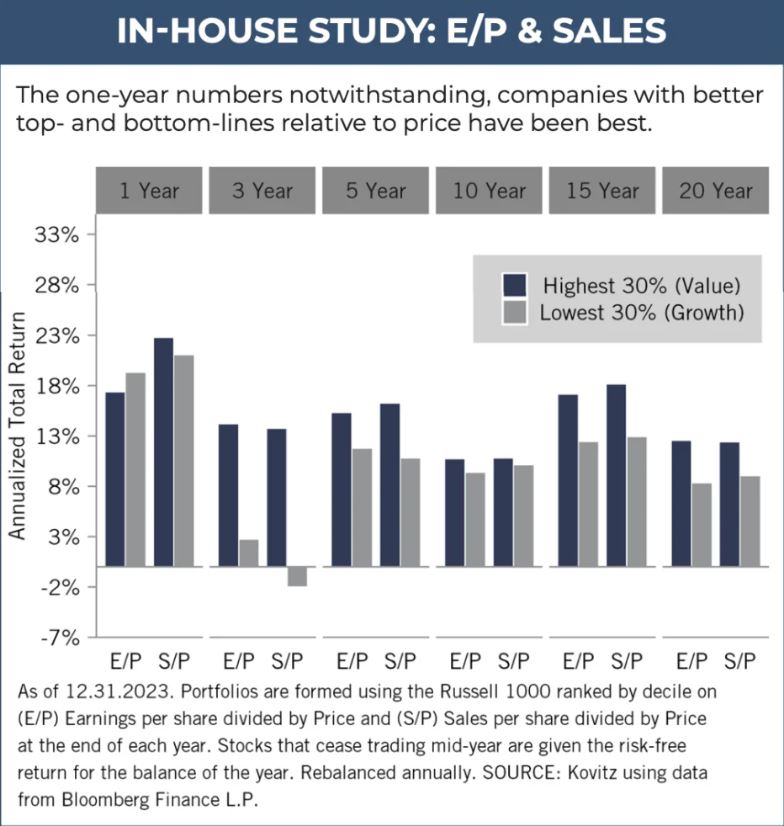

While we think that folks would naturally gravitate toward inexpensive stocks, given that most seek bargains in their everyday lives, 2023 was a year in which double-digit percentage returns were available pretty much across the board. True, the average stock in the broad-based Russell 3000 index returned only 13.8% last year, as SmallCaps generally were also-rans in the performance derby, but just about any way they were sliced and diced in our annual factor-based review of the Large-Cap Russell 1000 index for 2023, stocks had terrific average returns.

Of course, we concede that stocks with higher dividend yields bucked their historical propensity for outperformance, while more expensively priced stocks generally won the returns race, but we offer the reminder that we are not constrained by academic definitions of Value and Growth. Indeed, we hardly think that the traditional price-to-book-value distinction that has long been the academic dividing line tells a complete story, so we are constantly evaluating additional metrics, many of which are displayed in the accompanying charts. As we cast our lines for new investment ideas, our objective is to always be fishing in a pond stocked with companies that exhibit characteristics of those that have proven over time to be better long-term performers.

That in mind, we crunch plenty of our own numbers so that we can validate the historical evidence and determine if other valuation factors are worthy of inclusion in our work. Our initial screens are only one step in our investment process, but we continue to think that Free-Cash-Flow Yield, EBITDA/Enterprise Value, Return on Common Equity and Return on Invested Capital are measures that add value to our quantitative analytics.

Recommended Stock List

In this space, we list all of the stocks we own across our multi-cap-value managed account strategies and in our four newsletter portfolios. See the last page for pertinent information on our flagship TPS strategy, which has been in existence since the launch of The Prudent Speculator in March 1977.

Readers are likely aware that TPS has long been monitored by The Hulbert Financial Digest (“Hulbert”). As industry watchdog Mark Hulbert states, “Hulbert was founded in 1980 with the goal of tracking investment advisory newsletters. Ever since it has been the premiere source of objective and independent performance ratings for the industry.” For info on the newsletters tracked by Hulbert, visit: http://hulbertratings.com/since-inception/.

Keeping in mind that all stocks are rated as “Buys” until such time as we issue an official Sales Alert, we believe that all of the companies in the tables on these pages trade for significant discounts to our determination of long-term fair value and/or offer favorable risk/reward profiles. Note that, while we always seek substantial capital gains, we require lower appreciation potential for stocks that we deem to have more stable earnings streams, more diversified businesses and stronger balance sheets. The natural corollary is that riskier companies must offer far greater upside to warrant a recommendation. Further, as total return is how performance is ultimately judged, we explicitly factor dividend payments into our analytical work.

While we always like to state that we like all of our children equally, meaning that we would be fine in purchasing any of the 100+ stocks, we remind subscribers that we very much advocate broad portfolio diversification with TPS Portfolio holding more than eighty of these companies. Of course, we respect that some folks may prefer a more concentrated portfolio, however our minimum comfort level in terms of number of overall holdings in a broadly diversified portfolio is at least thirty!

TPS rankings and performance are derived from hypothetical transactions “entered” by Hulbert based on recommendations provided within TPS, and according to Hulbert’s own procedures, irrespective of specific prices shown within TPS, where applicable. Such performance does not reflect the actual experience of any TPS subscriber. Hulbert applies a hypothetical commission to all “transactions” based on an average rate that is charged by the largest discount brokers in the U.S., and which rate is solely determined by Hulbert. Hulbert’s performance calculations do not incorporate the effects of taxes, fees, or other expenses. TPS pays an annual fee to be monitored and ranked by Hulbert. With respect to “since inception” performance, Hulbert has compared TPS to 19 other newsletters across 62 strategies (as of the date of this publication). Past performance is not an indication of future results. For additional information about Hulbert’s methodology, visit: http://hulbertratings.com/methodology/.

Portfolio Builder

Each month in this column, we highlight 10 stocks with which readers might populate their portfolios: American Tower (AMT), Fresh Del Monte (DVN), Alphabet (GOOG) and seven others.