Inflation, rising interest rates and economic worries were top of mind heading into 2023, causing many folks to remain on the market’s sidelines. The efforts to kneecap inflation by the Federal Reserve seem to have worked, suggesting that a fabled “Soft Landing” has moved from improbable to possible. As pricing pressures receded, the Fed slowed the pace of rate hikes, with the Fed Funds rate eventually reaching 5.5% in July and holding steady since.

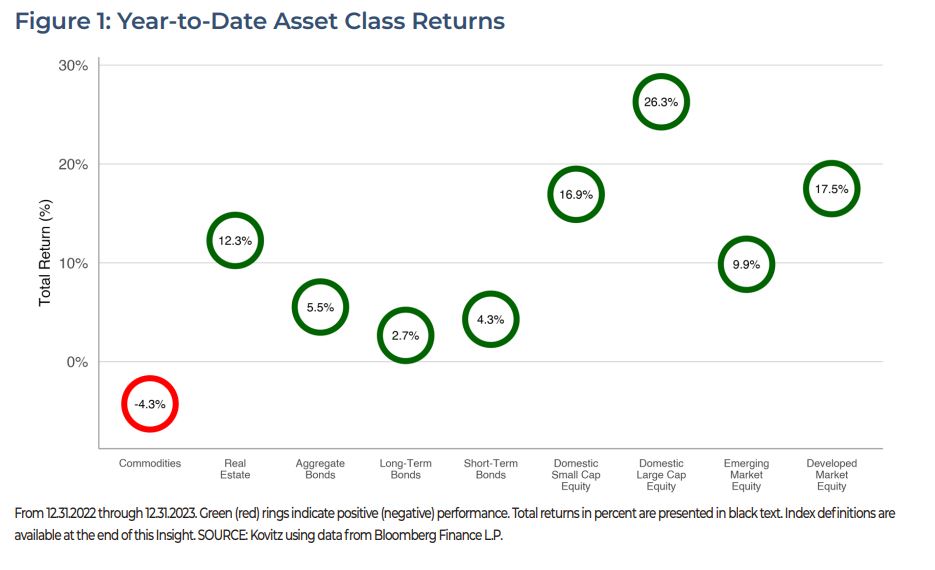

Unfortunately for those parked in cash, the worries had a real cost as equity markets turned in a solid year. The S&P 500 rose 26.3% including dividends, while Small Company stocks rose 16.9%. Global returns were also respectable. After a drubbing in 2022, bonds posted modest gains, while public real estate’s double-digit tally was more than double the long-term average.

Of course, it was not all smooth sailing in 2023. There were two 10% corrections, while the average stock was mired in the red for much of the year before rallying post-Halloween and the sizable returns of the cap-weighted market indexes were driven by huge gains in just a handful of mega-cap names. However, we again saw that the secret to investment success in stocks is not to get scared out of them.

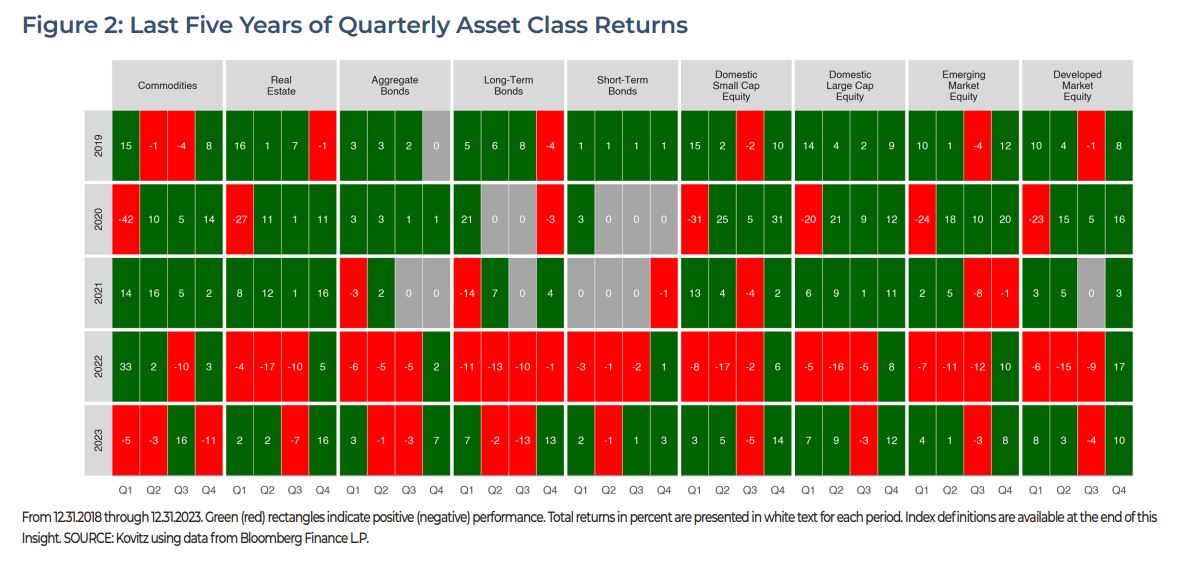

Quarterly Returns Fluctuate

The worries that plagued portfolios in 2021 and 2022 have started to fade away, and the rally in Q4 offered another reminder that it’s hard to get market timing right. There are plenty of reasons to be optimistic about long-term investment return potential and the overall trajectory of the economy, but we have noticed the reasons to buy stocks aren’t trumpeted as loudly as the reasons to sell them.

Factor Performance

Value stocks struggled to keep up with Growth stocks in 2023, a reversal from Value’s large outperformance in 2022, evening out the two-year performance derby for the pair. Quality and Size also were factors that turned in a solid year, while High-Yield, Minimum Volatility and Momentum factors saw subdued returns. Having managed Value-oriented portfolios since 1977 with success, we think investors who make factor-based investments are better suited to longer holding periods.

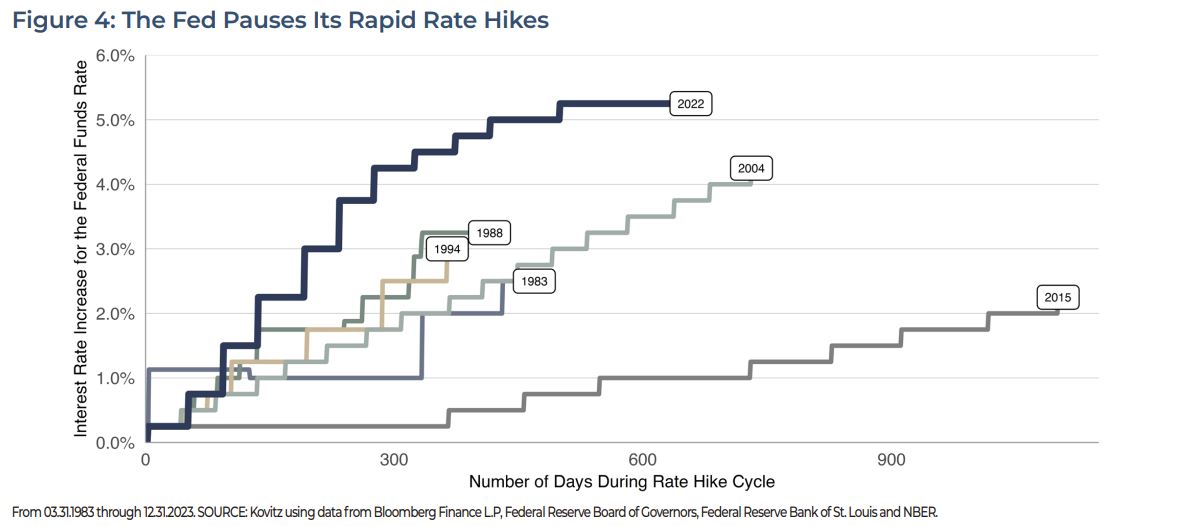

Well, That Escalated Quickly

In comparison to rate-hike cycles since 1983, the Federal Reserve moved at breakneck speed in 2022/2023. While 2015’s cycle took more than a thousand calendar days, the latest hike cycle rose 5.25% in just 16 months. With the hikes largely doing the trick in the Federal Reserve’s eyes, rates have plateaued since July and the FOMC’s “dot plot” predicts (for whatever that is worth) a pullback in rates beginning in 2024, eventually reaching a long-term target around 2.5%.

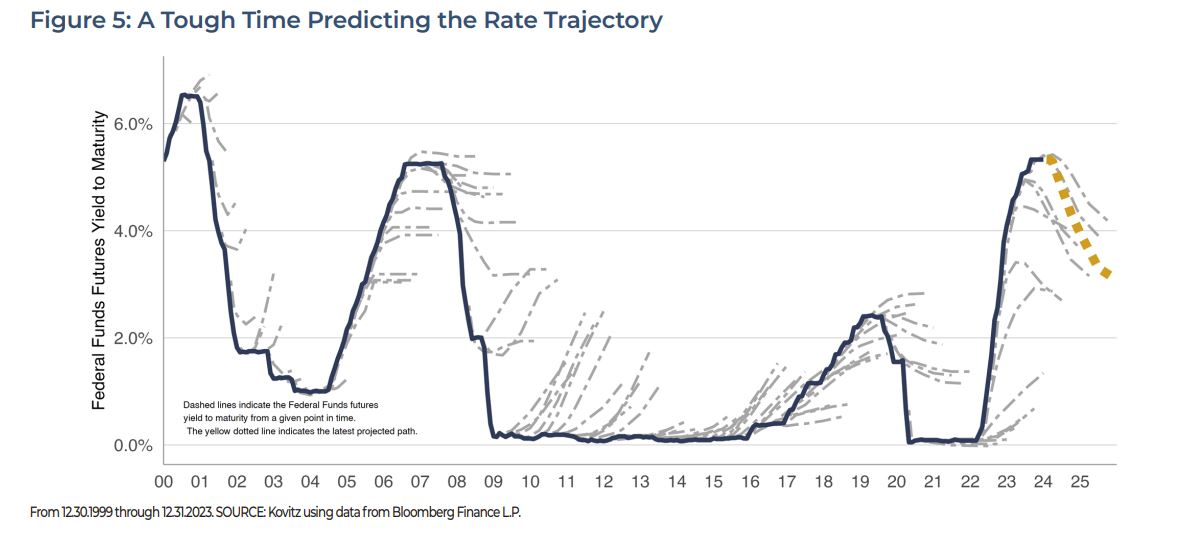

It’s Hard To Predict The Future

We amended the word predicts in quotes above because it’s difficult to predict the future, especially so when it comes to interest rates. In Figure 5, we plot the Federal Funds Rate and point-in-time futures trajectories. While a significant rate retreat may happen over the next few years, there were only a handful of instances the futures markets accurately predicted the path of rates. Importantly, there is real money in the futures market, meaning it’s not a willy-nilly poll of a handful of folks.

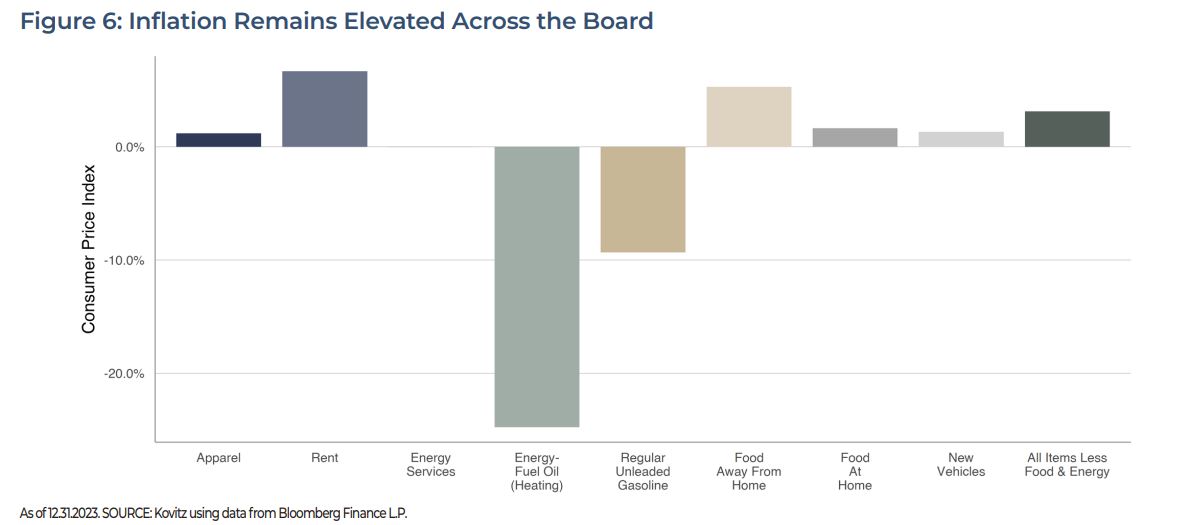

Living Has Become Slightly Less Expensive

Inflation, inflation, inflation. From the dinner table to the car lot, the rising cost of living dominated conversation for nearly two years. Although slower-moving components like rent have continued to climb, energy and fuel prices have made substantial retreats, while the pace of price hikes for apparel, new auto and food prices has dramatically slowed. We suspect the relief is welcomed.

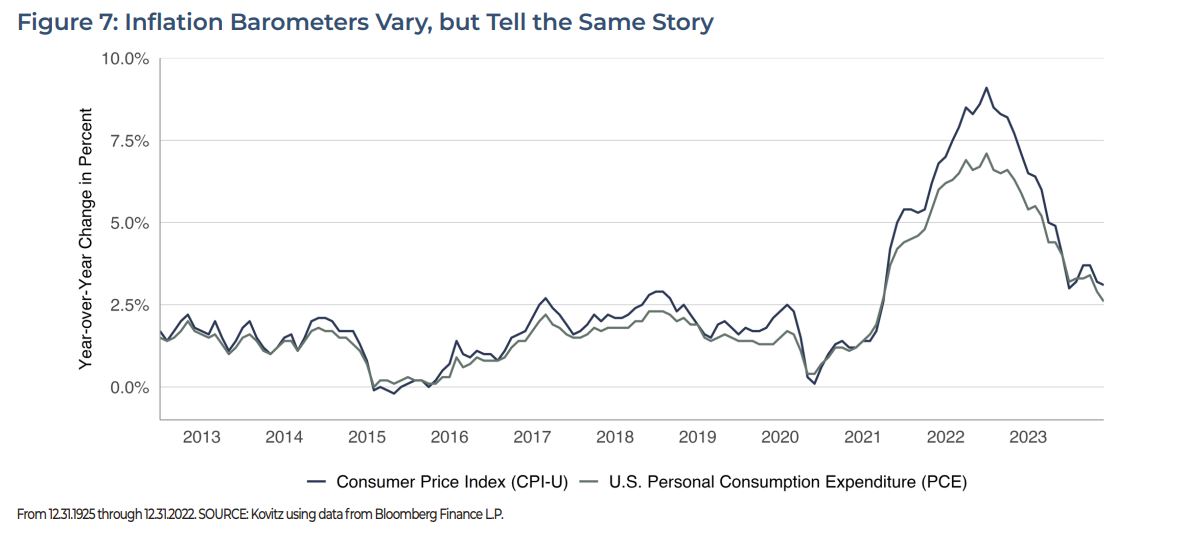

Inflation, But Different

The Consumer Price Index (CPI-U) and U.S. Personal Consumption Expenditure Index (PCE) are commonly used to measure inflation. Both track a basket of goods, but vary in formula, weight, scope and other factors. CPI-U uses household data, while PCE uses business data. CPI only considers out-of-pocket spending, and PCE includes indirect expenditures. Methodology differences frequently result in different inflation figures. We monitor both but prefer to use PCE, as does the Federal Reserve.

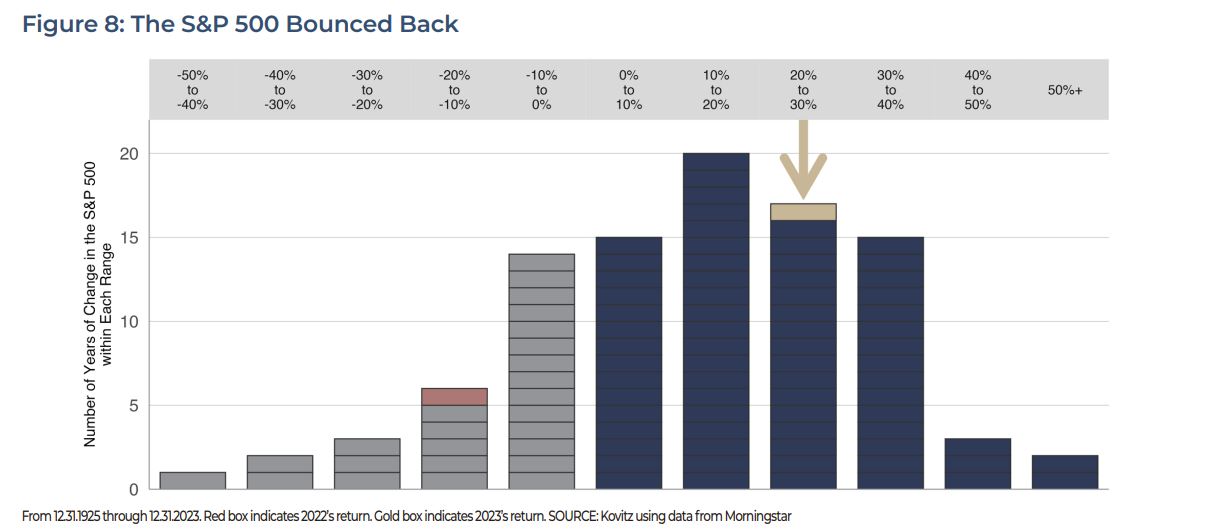

You Are Here: Equities

Stock returns made a strong resurgence last year (following a dismal 2022) and offered another reminder that the hardest part of market timing is getting the timing right. As the year’s return shows, the recession that was loudly predicted to arrive in 2023 did not in fact arrive, and the Bloomberg Recession Probability index fell from a high of 68% in January 2023 to 50% at the end of December.

You Are Here: Bonds

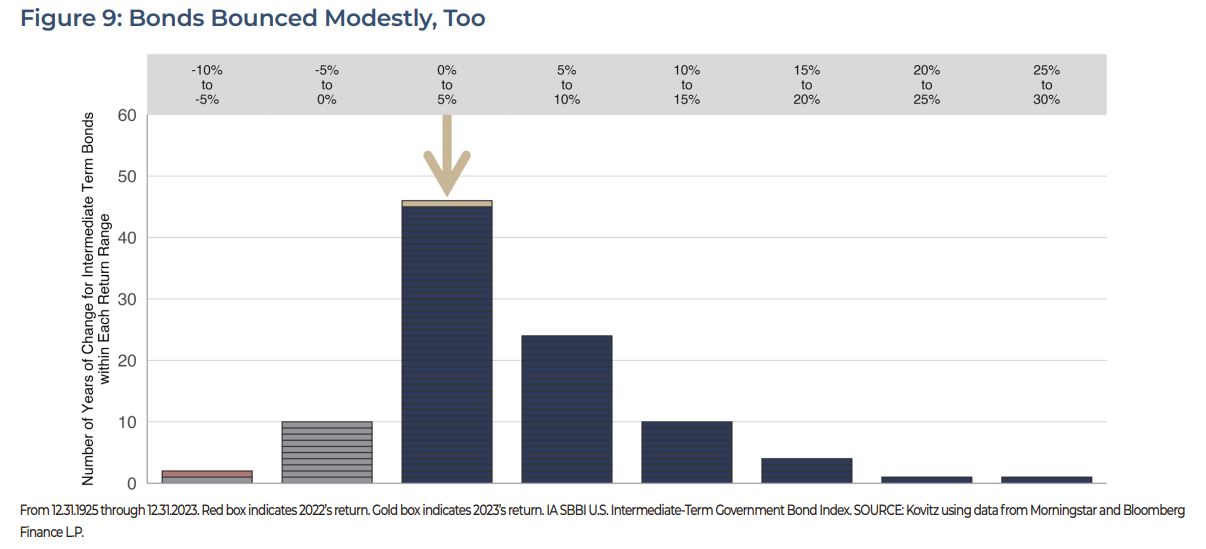

On the bond side of the investment world, a series of swift rate hikes by the Federal Reserve sent bond prices plunging in 2022 (red box), with the mathematical certainty that rising interest rates send bond prices falling on full display. Figure 9 shows there was a modest recovery by intermediate-term bonds (average maturity around 5 years), and certainly no records were set by the barely positive performance figures.

Avoiding What, Exactly?

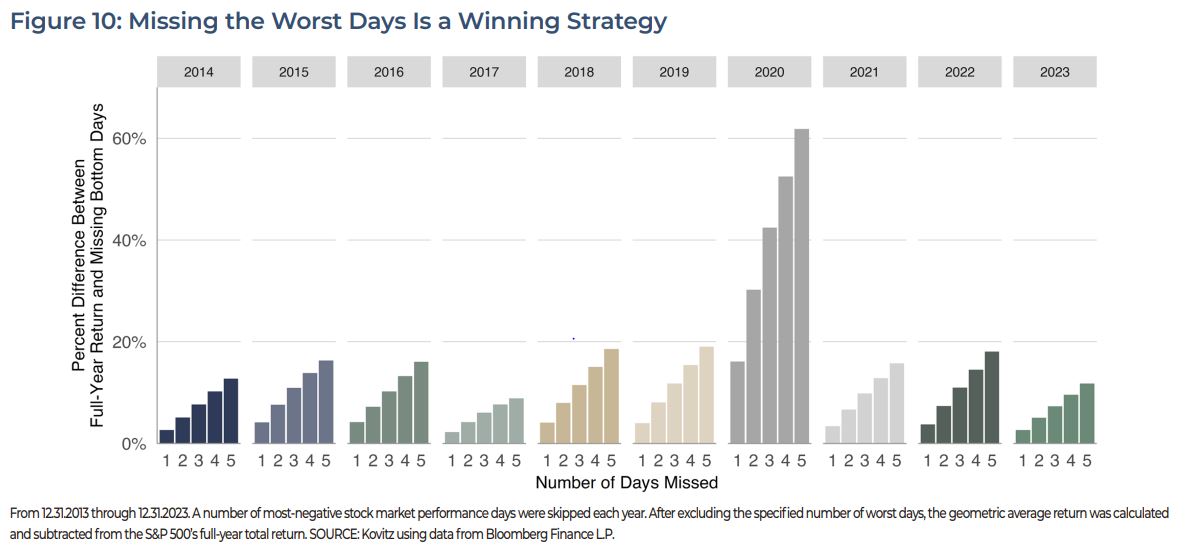

The art of portfolio building usually includes some downside aversion. Most often, this is accomplished by making allocations to different asset classes and is the ‘first line of defense’ for the rainy days that inevitably come. What would happen if we missed those sharply negative days completely? Figure 10 shows it would be a lucrative strategy. Including the wild ride that was 2020, the average annual performance improvement from missing the bottom five days is 19.9% over the last decade.

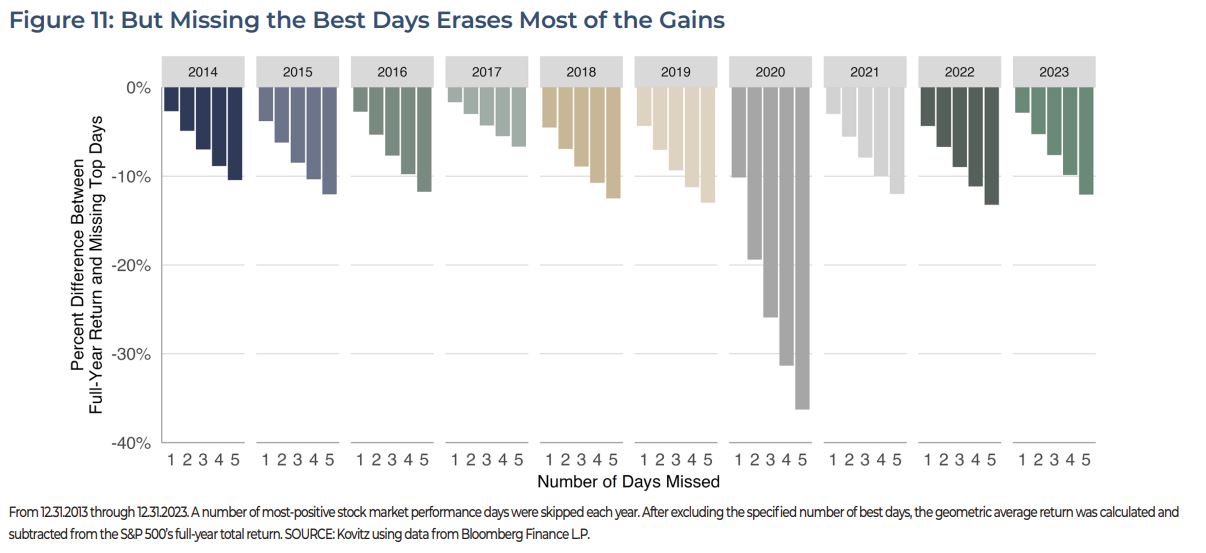

With volatile up-and-down days often occurring in clumps, the strategy would almost certainly miss the five best days, too. Figure 11 shows the impact, averaging an annual 14.0% reduction in returns over the past ten years. The strategy’s 6% gap narrows further when we consider that a 14.0% loss (by not experiencing the up days) and a 19.9% gain (by skipping the down days) ends up adding just 3.1% to the 12.0% S&P 500 annualized return. There are taxes and transaction costs to consider, too, lest we forget to include the cost of the crystal ball algorithm to perfectly time the top and bottom days each year.

Aggregate Valuations Are Volatile

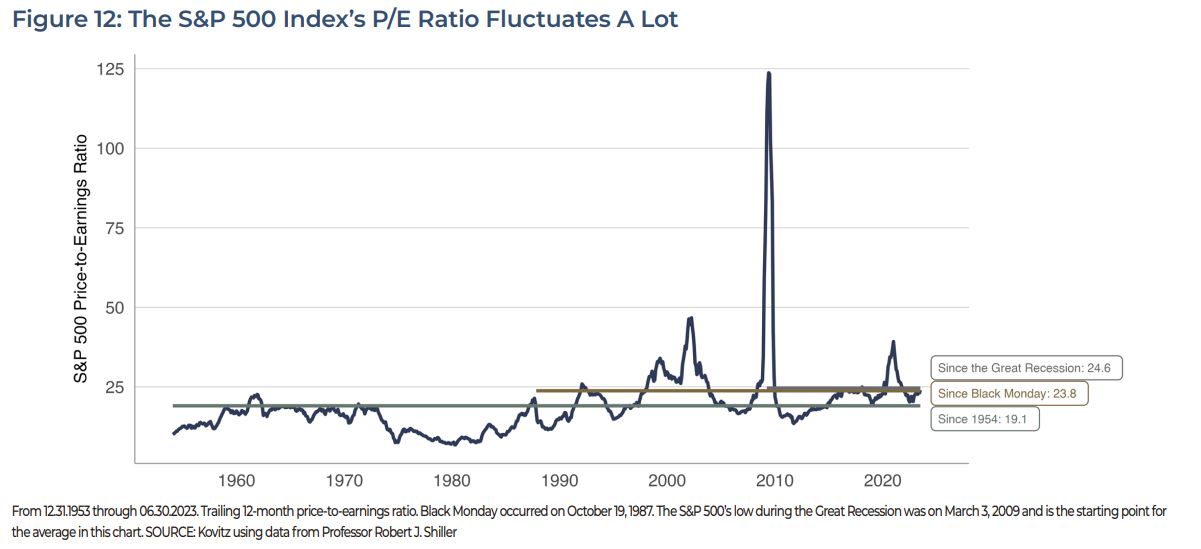

Since 1954, the long-term price-to-earnings ratio average for the S&P 500 has hovered around 19 times (green line), while the ratio’s recent averages have been quite a bit higher (Black Monday in 1987 in gold and the low point during Great Recession in grey). The swings in the series can be distilled into two factors: (1) the S&P 500’s price level (numerator), which is currently around 4800 and (2) the S&P 500’s trailing earnings per share (denominator).

Multiples Can Change Too

Investors love to see growth in earnings (or at least growth in earnings projections), even though it’s possible for the S&P 500 price to climb without actually experiencing underlying earnings growth. Below, we chart the current S&P 500 P/E multiple (in navy), with earnings multiples between 14 times and 24 times in the background. As Figures 12 and 13 show, the multiple fluctuates over time, and the current P/E ratio of 22x has risen from 19 since the end of 2022 and is not historically extreme.

S&P 500 Index Excluding The Top Stocks

Recent gains have been propelled by a handful of stocks. Over the last five years, just five stocks (Apple, Microsoft, Nvidia, Amazon and Meta Platforms) have accounted for 35% of the S&P 500’s 107% rise. The Top 10 stocks have driven nearly half of the returns. Large weights and somewhat expensive valuations thanks to soaring prices that have not been entirely backed by earnings growth resulted in an aggregate index that appears substantially more expensive than the mean stock.

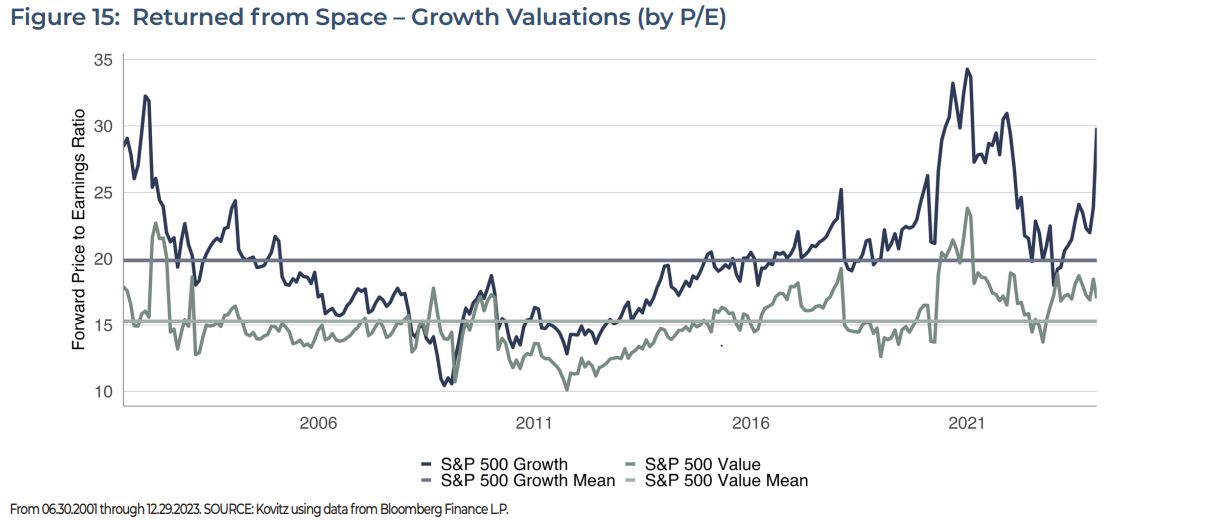

Value Stocks Remain Attractive

One of the most common valuation metrics, the P/E ratio, measures the price an investor pays for a unit of earnings. While Value (stocks with lower P/E ratios, per the S&P 500 Value index), has seen its ratio rise above longer-term averages, Growth (stocks with higher P/E ratios, per the S&P 500 Growth index) is much further above its historical norm. We think this discrepancy elevates the attractiveness of Value on a relative basis.

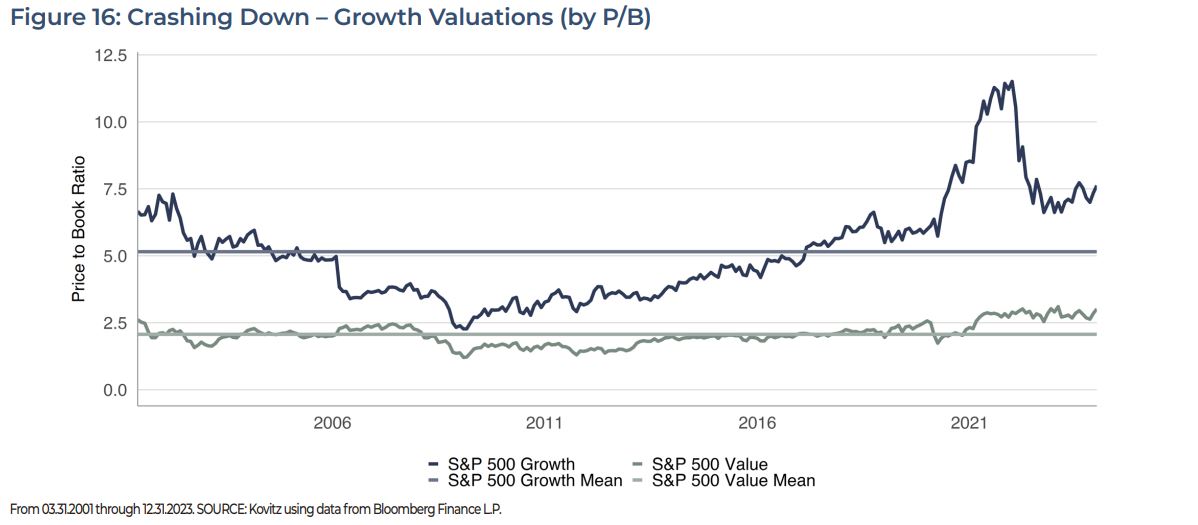

P/E Isn’t The Only Measure

Another measure frequently used in an academic classification of Value and Growth stocks is the Price-to-Book (P/B) ratio. It measures the difference between a company’s market value (i.e. market capitalization) and book value (assets less liabilities). As measured by the P/B ratio, the valuation gap is larger than usual these days, after narrowing in 2022 and modestly expanding again in 2023.

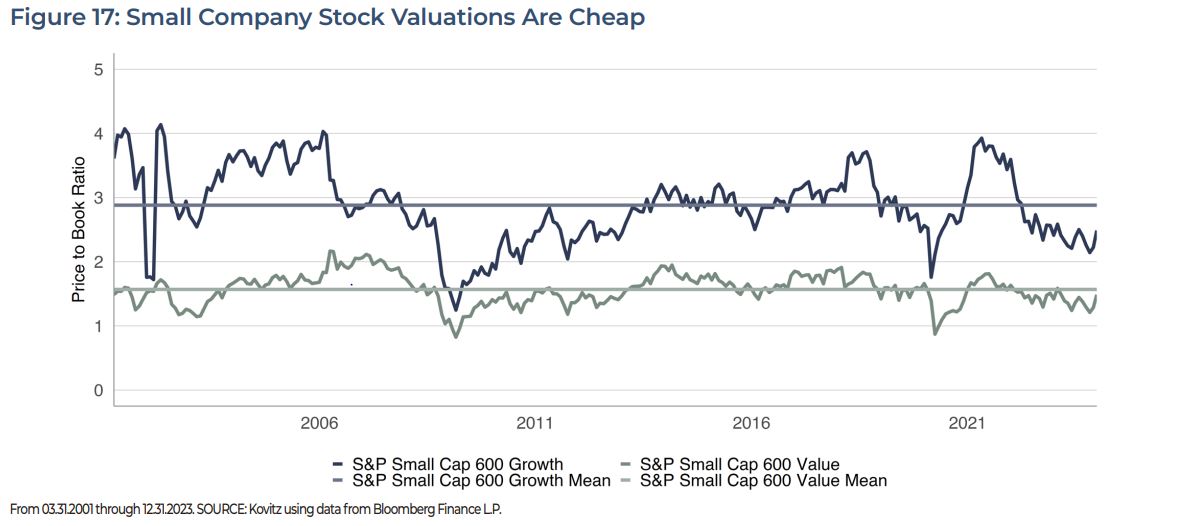

Small Caps

Whether located on the Value or Growth end of the spectrum, Small-Caps presently trade at significant discounts to their historical average multiples. When compared against the Large-Cap S&P 500 values in Figure 16, the relative inexpensiveness of Small Company stocks is even more pronounced. The differences in valuations are in part due to the Tech-heavy rally in 2023, which pushed the S&P 500 index 26% higher, while the average stock’s return was about half that figure.

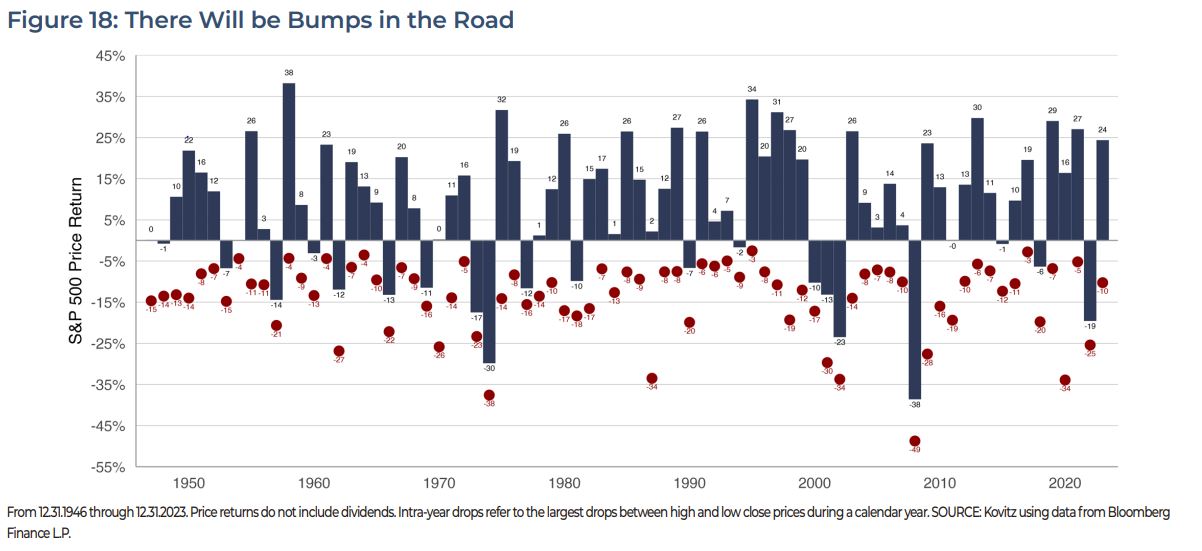

Equity Markets Go Up (And Sometimes Down)

One of the best illustrations showing annual stock market gyrations is offered below. The red dots mark the low point each year (peak to trough) and the navy bar is the final price return for that year. In no year did the S&P 500 finish at its low point, and we suspect those that bailed out of equities in 2020 after the bottom fell out in March are doing some major face-palming. Last year, the S&P 500 dropped as much as 10%, yet ended the year up 24% (excluding dividends!).

The Rally May Continue

In our 2024 Stock Market Outlook, we discussed seven investment themes for the upcoming year and offered a friendly reminder that we are buying our undervalued stocks for their three-to-five-year or longer potential, with the intention of holding them through a business cycle or two. The 18 preceding charts endeavor to add color to what we wrote in the Outlook by presenting historical context for tidbits that might be presented as points to worry about in the future. And of course, those remarks are usually offered with minimal context and oodles of chutzpah, largely because that sells well on TV or in the newspaper. We must live with such prognostications, even as they do not help folks stay on the path to success.

We do not mean to suggest that the ride in down the stock market road will be free of wacky gyrations, stress or worries. Indeed the year is off to quite a start, with the first few days of trading lively. Yet, we think those with long-term time horizons stand to benefit from their patience and persistence, having always been rewarded in the fullness of time. Unsurprisingly, the kind folks in our Compliance department will want us to caution that past performance is not indicative of future results and there are no assurances the next century will be like the last, but we see no reason to temper our enthusiasm for our broadly diversified portfolios of undervalued stocks. When inevitable market drops do occur or we become less certain about our convictions, we remind ourselves of this quote from Warren Buffett’s 2020 letter, “In its brief 232 years of existence, however, there has been no incubator for unleashing human potential like America. Despite some severe interruptions, our country’s economic progress has been breathtaking.”

Partner With Us

For more than 46 years, we have collaborated with our clients in their investment decision making process as they pursue their long-term financial goals. We are committed to keeping your goals, concerns and attitude about investing at the heart of your plan. If you’re ready to experience our personalized investment approach and exceptional client service, contact Jason R. Clark, CFA at 949.424.1013 or jclark@kovitz.com.