The Prudent Speculator, a value-oriented investment newsletter we’ve published continuously since March 1977, has been guided–through thick and thin–by three core tenets: patience, selection and diversification. We believe selection (improving the odds of success) and diversification (risk reduction) are useful, and we extoll their virtues frequently in our Newsletter and Insights, as well as in the weekly Market Commentary. However, we must admit it’s possible, and likely probable, to retire a millionaire simply by observing the first tenet, patience.

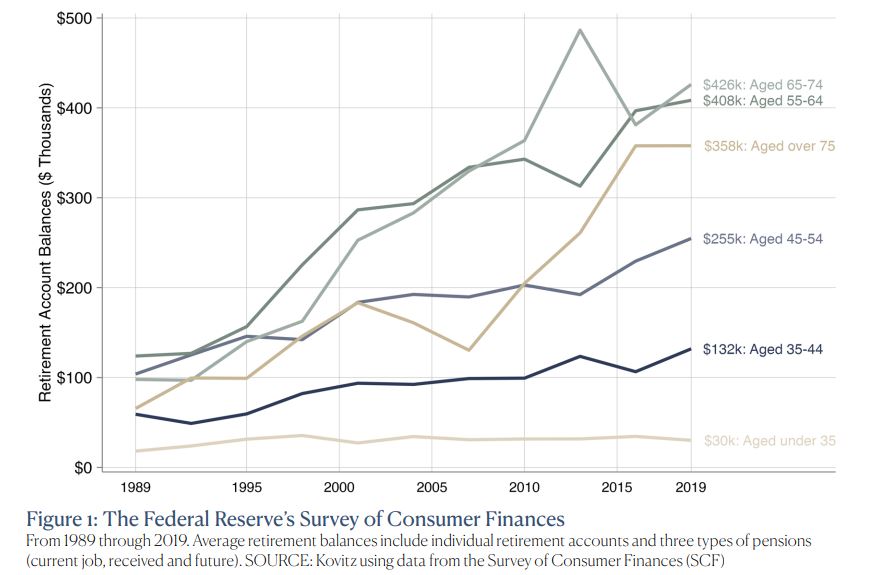

The bad news first. The Fed’s Survey of Consumer Finances shows the mean retirement account size in 2019 was $255,000, having steadily grown from $76,000 in 1989. Figure 1 shows those in the 55-74 range have accumulated over $400,000, and the 75+ cohort reports a mean balance closer to $358,000. While the drop in balances for the 75+ crowd makes sense because people are expected to draw down their accounts in retirement, it is worrying that those under 35 years old have saved a paltry $30,170. Even though the figure indicates the average American has built a sizeable nest egg for retirement, the figures are for the Census-reported 49.6% of American families with a retirement account at all. More than half do not have retirement savings!

Disconcerting Trends

Financial outcomes for the 55+ crowd are largely set at this point, even as perks like catch-up contributions and larger salaries remain useful tools to make a late effort to stockpile investable assets. Beginning as early as 62 years old, Social Security benefits kick in, providing 49% of total retirement income for eligible individuals according to the Social Security Administration. The Administration notes other significant sources of retirement-aged income include annuities/pensions (16%) and earnings (24%), the latter reflecting continued participation in the workforce by Social Security recipients. Defined benefit pensions have become rarities–the count has dropped from 175,000 in 1986 to 47,000 in 2020–and there are perpetual worries Social Security may ‘dry up’, leaving U.S. workers evermore reliant on their own retirement preparations.

Start Now

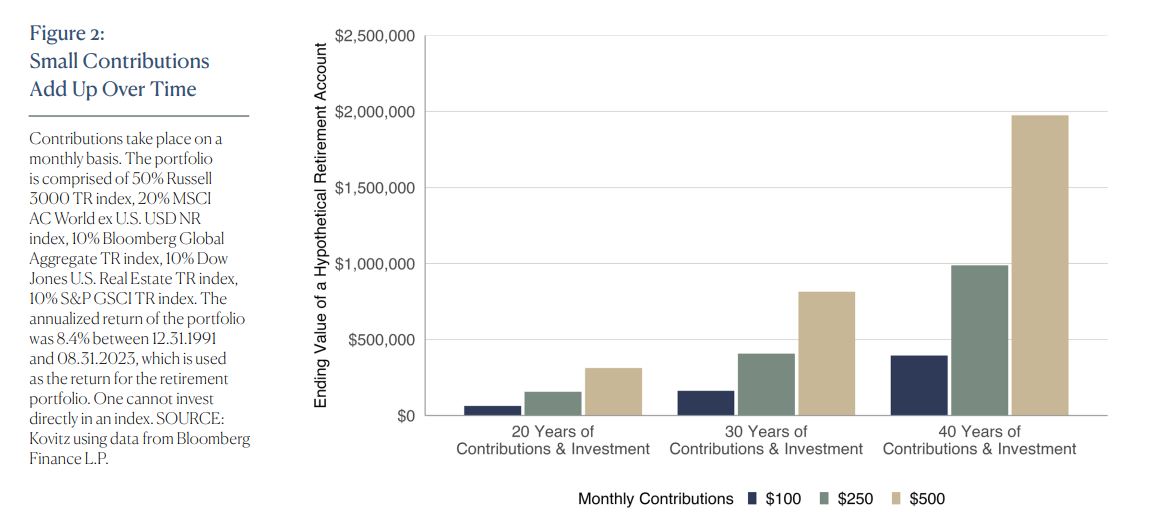

The good news is with patience and persistence, individuals can retire comfortably, even if the thought of accumulating a million dollars in addition to life obligations may seem like too much to ask at this point. With near-term spending needs rising rapidly, we can appreciate why folks would wonder why it’s even worth saving for the future at all when those funds could be spent now. For illustrative purposes in Figure 2, we constructed a diversified portfolio comprised of a blend of 50% U.S. stocks, 20% non-U.S. stocks, 10% bonds and 10% commodities. Between December 1991 and August 2023, the average annualized return of the portfolio is 8.4%. We believe this annualized return serves as a useful benchmark for planning purposes, though we note long-term average returns for portfolios built on specific factors including those for Value or Dividend-Payers (which we favor in our investment processes) have hovered around 13% and 11% per annum, respectively, since 1927.

The results are compelling. Figure 2 shows massive differences between end values for several levels of monthly saving over the study’s time frame and demonstrates that one doesn’t need to put away thousands of dollars per month to end up retiring with a million dollars or more. In fact, squirreling away $250 per month over 40 years is sufficient to accumulate $1 million, while $100 per month results in a final tally around $400,000. Put another way, recurring contributions of $100 per month for 40 years achieves roughly the same outcome as contributions of $250 for 30 years. In fact, 40 years of $100 contributions easily exceeds the final value of $500 per month saved for 20 years. It is those extra early years that allow the $100 to converge to similar ending values.

A Shift Employers to Employees

Believe it or not, employers are a great source of ‘free’ money, and we do not mean taking a long lunch. Data from Willis Towers Watson (WTW) shows that 100% of Fortune 500 companies offer some type of retirement plan. Retirement plans have shifted in recent years, moving from plans in which the employer bears the retirement income risk to those in which the employee bears the risk. In 1998, WTW reported 49% of Fortune 500 employers offered a defined benefit (DB) plan, which specifies with a formula (usually based on salary and years of service) how much an employee is entitled to receive in retirement. In the event that investment returns are subpar, the employer would be on the hook to contribute additional money to fund the distributions. In 2019, the year of the latest WTW study, just 3% of Fortune 500 employers offered a DB plan, opting instead for hybrid or defined contribution (DC) plans. In a defined contribution plan, the company deposits a certain amount (often matched by the employee), and future investment returns become the responsibility of the employee. While DC plans come with plenty of support to guide self-management of retirement funds, subpar investment returns leading up to and after retirement become the problem of the employee. This can lead to lower-than-expected retirement distributions.

Your Employer Wants To Give You Free Money

Surprisingly, the employer matching can be significant. The $100 per month that we charted in Figure 2 could easily turn out to be a low estimate of saving efforts. But first, a quick primer on the several types of retirement plans. Simple individual retirement accounts (IRA) and 401(k) plans are frequently available for employees of for-profit businesses, while 403(b) and 457(b) plans are offered to tax-exempt and government workers, respectively. They all function in a similar manner, in that both an employer and employee can contribute earnings to the plan, provided certain (reasonable) qualifications are met. There are contribution maximums, which tend to rise year-to-year based on inflation.

Employers have leeway in terms of their employee retirement plan contributions. Some opt to deposit a flat 3% of an employee’s salary irrespective of the employee’s contributions. Indeed.com quotes the median salary for an early saver (20-24 years old) near $35,000. Nota bene: a median is the middle value, meaning one employee makes above $35,000 and another below. A 3% company match would translate to a contribution of $1,050 per year or $88 per month. Workers 35 years and older have median salaries above $50,000, penciling out to monthly employer contributions of $125 or more.

In some situations, employers will match employee contributions up to a certain portion of their salary. In a scenario where an employer matches up to 3%, an early saver making $35,000 would save $176 per month if matched dollar-for-dollar ($88 employee contribution and $88 employer contribution) or $132 per month if matched fifty cents-per-dollar ($88 employee contribution and $44 employer contribution). We must make another admission. In more than 45 years of stock investing, we’ve never come across an investment that was guaranteed to double its money. Of course, after the money hits your retirement account (instead of your brokerage or bank account), we do like the prospects for a broadly diversified portfolio of Value stocks!

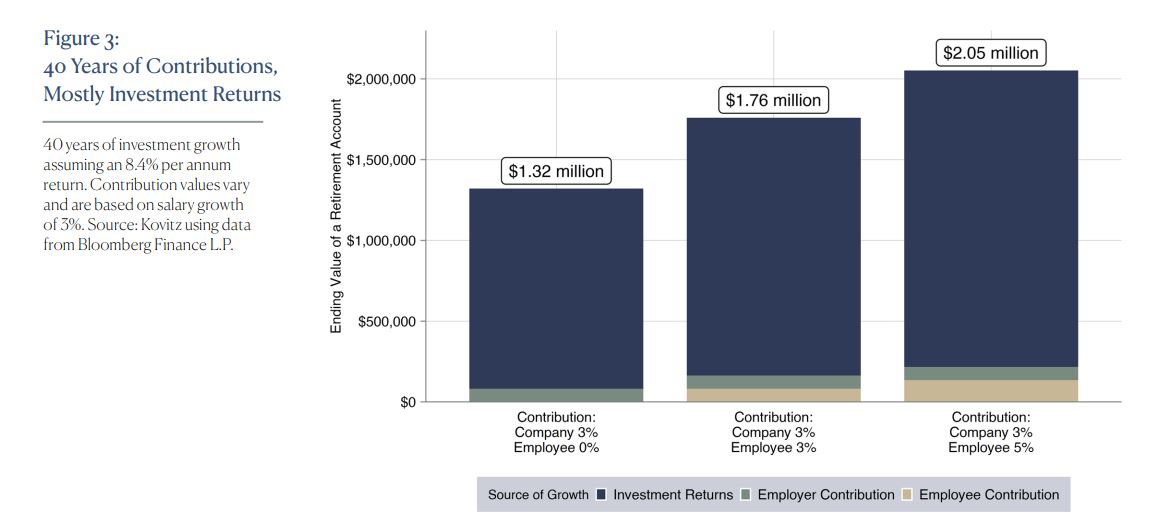

Important to this discussion, too, is that contributions are not taxed until they are eventually withdrawn and employers in many situations opt to make additional contributions via profit sharing. In Figure 3, we chart varying contribution rates for a hypothetical 401k plan for a 25-year-old until they are 65. For matching and contribution purposes, the initial salary starts at $35,000, grows at a rate of 3.0% (which is in line with average inflation rates since 1927) and we use 8.4% for investment returns.

In Figure 3, an employer contributed 3% in each series and the employee’s contribution varied between 0% and 5%. Total employer contribution was $82,000 in all cases, while the total employee contribution varied between $0 and $136,000. Even though the investment growth does the majority of the heavy lifting, an employee’s contribution has meaningful impact on the account’s value just before retirement at 65 years old, adding an extra $730,000 for “just” $136,000 of contributions.

Participation Encouraged

Employee Retirement Income Security Act (ERISA) rules state that employees who work 1,000 hours or more in a rolling year are eligible to participate in a retirement plan. Unfortunately, retirement benefits are not applied uniformly, or even required. Consistent with the 49.6% participation rate from the U.S. Census, payroll services company ADP wrote in its Retirement Savings Trends report that 50.1% of employers offer retirement benefits. The report offered some interesting, if discouraging, details. Just one third of companies with 20 or fewer employees offer retirement benefits, compared with 98% of companies with more than 5,000 employees. For those that offered plans, the 41.1% of employees in the 20-to-24 age group contributed 4.6% of their income. Those in the 55+ group saw 65.6% participation with 8.5% of income set aside in a retirement account.

Happily, the SECURE 2.0 Act of 2022 improves American retirement prospects. Included in the Act are requirements for automatic enrollment in retirement plans, automatic contribution escalators, increased catch-up contributions, expanded eligibility and provisions for emergency savings accounts. Although employees can opt out from many of the (what we think are) improvements, opt-out policies dramatically improve participation rates because people often make little effort to change the status quo. Fidelity, a brokerage firm and custodian, reported that 91% of employees with automatic retirement savings plan enrollments did not end up opting out, indicating that a status quo bias could be ‘gamed’ to help employees save more.

For The Price A Grande Latte

How does a young worker making a modest salary start saving for retirement without their employer’s help? Surely, it’s a bridge too far to expect a young worker to suddenly start saving $1,000+ per month. However, there are opportunities for small contributions to add up over time. For example, foregoing a $5 beverage one per week and investing those dollars each month would add $72,210 to one’s retirement nest egg after 40 years. Simply recognizing that little changes over long periods of time may turn into meaningful results can be enough to turn the tide.

The Early Bird Gets The Worm Then Some

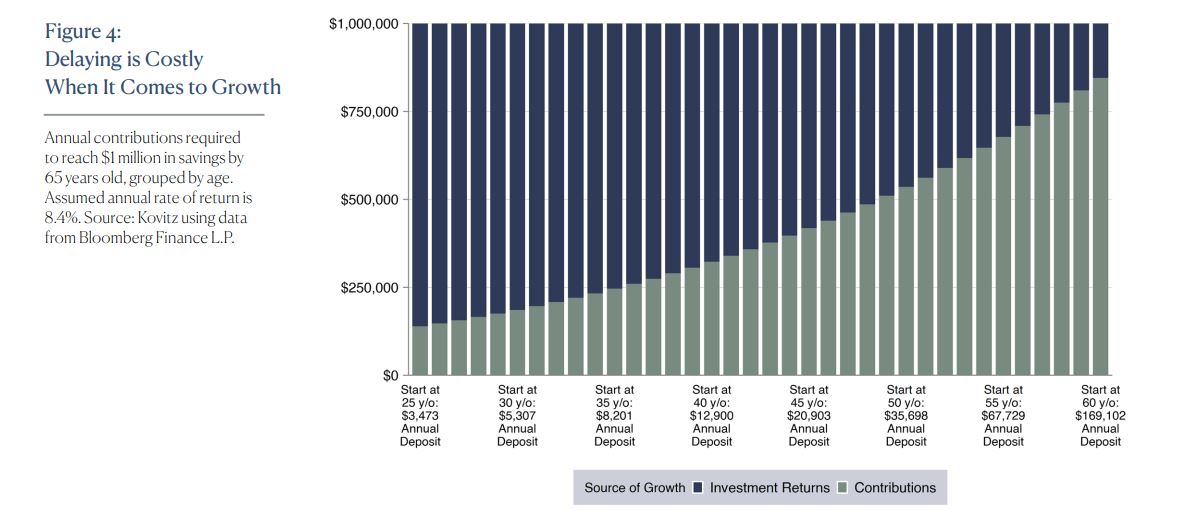

Even though retirement saving in an ideal world is a joint effort from the employee and employer, that’s not always the case. In situations where the burden of retirement saving rests squarely on an employee’s shoulders, Figure 4 shows early contributions have a giant impact when it comes to easing pressure on annual savings needs. Excluding tailwinds like wage growth, a 25-year-old ‘only’ needs to contribute $3,467 per year to reach the $1 million mark by the time they are 65, whereas someone starting at 55 years old would have to put away nearly $68,000 per year. Investment returns account for a whopping $861,000 of $1,000,000 for a 25-year-old, compared with investment returns accounting for $323,000 for a 55 year-old saver.

‘Cash’ And ‘Bonds’ Are Four-Letter Words

We think it’s worth noting that we added cash and bonds to our blended portfolio because we understand they can enhance an investor’s overall allocation in ways a strictly-equity portfolio usually cannot. However, young investors should consider the negative impact of cash and bonds in portfolios relative to equity returns, specifically in situations where invested funds are not needed within a short period of time.

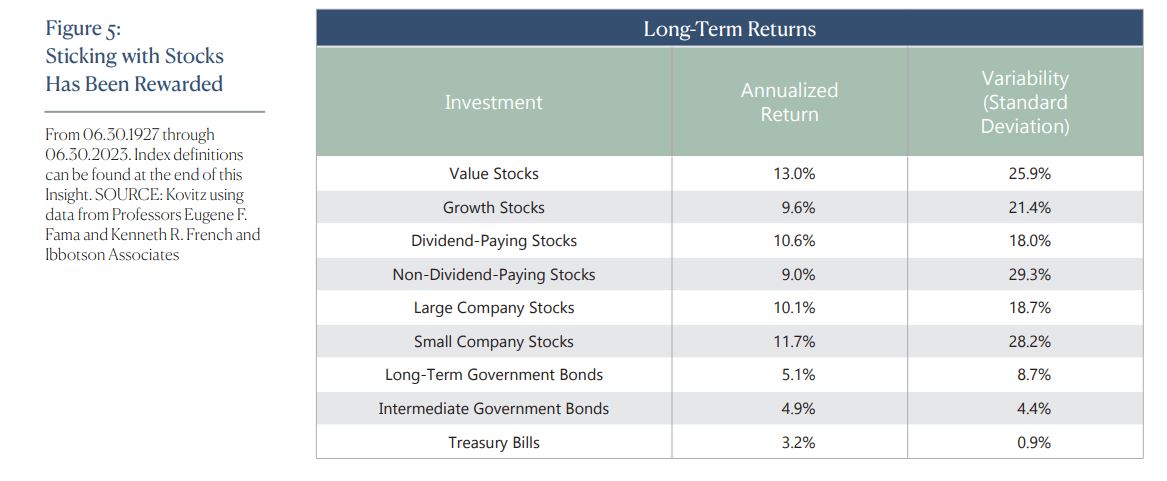

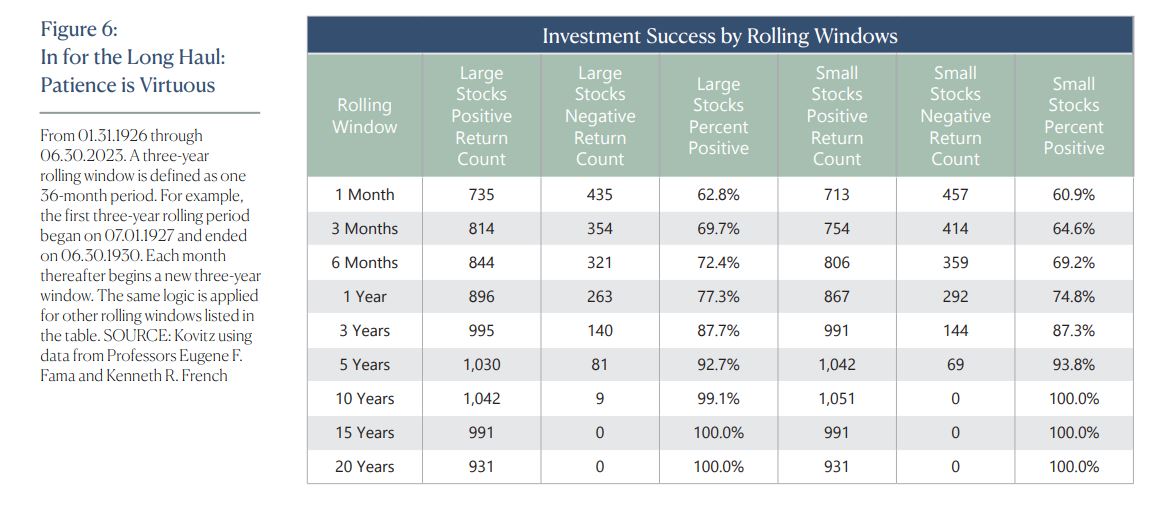

In general, cash and bonds serve as stores of value. As part of an overall investment allocation, holding cash and bonds is intended to buffer the return of the overall portfolio from oscillations in stock prices, such that one can meet upcoming cash needs. However, young investors shouldn’t have near-term cash needs for their retirement accounts and reductions in exposure to cash and bonds have historically improved returns. Figure 6 shows the odds of positive returns hit 100% around the 12 year mark, meaning that investing for 12 years at any point since 1926 would have earned a positive return, with Figure 5 showing Large- and Small-Company stocks return north of 10% on average. While the table below offers the Large/Small Company series, the story is similar if we substitute in the Value/Growth or Dividend/No-Dividend series.

Delay Not

In the 2003 book, Damn Right! Behind the Scenes with Berkshire Hathaway Billionaire Charlie Munger, author Janet Lowe wrote, “[Charlie] Munger has said that accumulating the first $100,000 from a standing start, with no seed money, is the most difficult part of building wealth. Making the first million was the next big hurdle. To do that, a person must consistently underspend his income. Getting wealthy, he explains, is like rolling a snowball. It helps to start on the top of a long hill—start early and try to roll that snowball for a very long time.” We think that message is correct and important, especially for young investors planning for the future.

Of course, there are many factors that determine systematic retirement contribution amounts, even as we always believe the right amount is “as much as possible.” For some, that will be $1,000 or more per month, and for others it might be $25 or $50. The key in the early years is not necessarily to contribute the right dollar amount or pick the right stock, it’s to save and invest early, allowing the “miracle of compounding” to do its job. As a bonus, early savers will be familiar with the ebbs and flows of their investments, having accumulated years of experience by the time they hit their prime earning years.

Of course, it can be helpful to have professional guidance rather than going it alone. We offer our clients and their families a wide variety of investment options paired with an experienced team of Wealth Advisors, which allows allocation decisions to be tailored for individual situations, taking into account factors like time horizon, risk-taking ability and personal goals.

For more than four decades, we have collaborated with our clients in their investment decision-making process as they pursue their long-term financial goals. We are committed to keeping your goals, concerns and attitude about investing at the heart of your plan. If you’re ready to experience our personalized investment approach and exceptional client service, contact Jason R. Clark, CFA at 949.424.1013 or jclark@kovitz.com.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.