John D. Rockefeller purportedly said, “Do you know the only thing that gives me pleasure? It’s to see my dividends coming in.” We hope he found more to enjoy in life, but there is something to be said about the tangibility of income generated from one’s investments. Whether it is real estate, bonds or stocks, one can worry a little less about the fluctuations in the value of the underlying assets when there is regular cash flow coming in.

And, when it comes to equities, we note that a third of the total return for Large-Capitalization stocks over the past 95 years has come from dividend income. Payouts are relatively modest these days, with the S&P 500 yielding 1.6%, but for the period 1926-2021, the income return worked out to 3.9% per year as part of the 10.5% annualized total return.

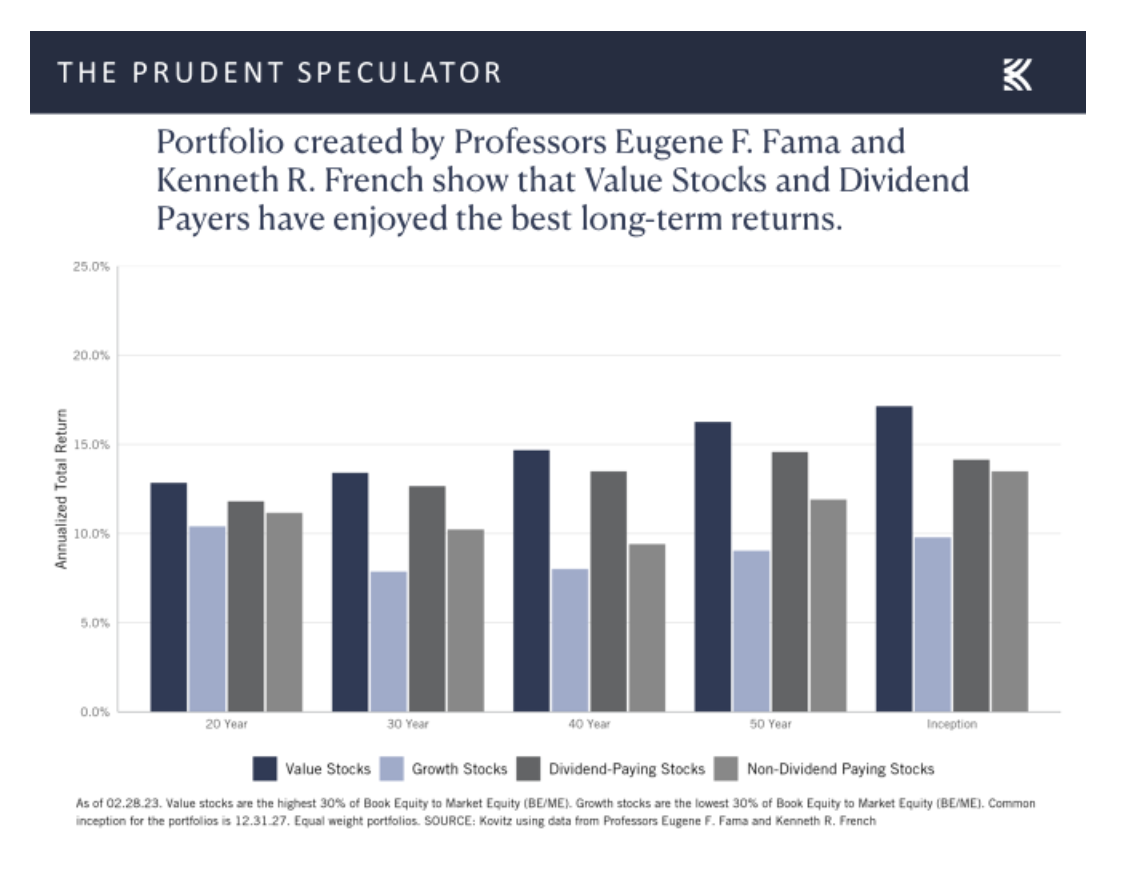

True, the return from capital appreciation has dwarfed the return from dividends, but history shows that Dividend-Paying stocks have enjoyed better long-term returns than Non-Dividend Payers over the past 20, 30, 40, 50 and 95 years.

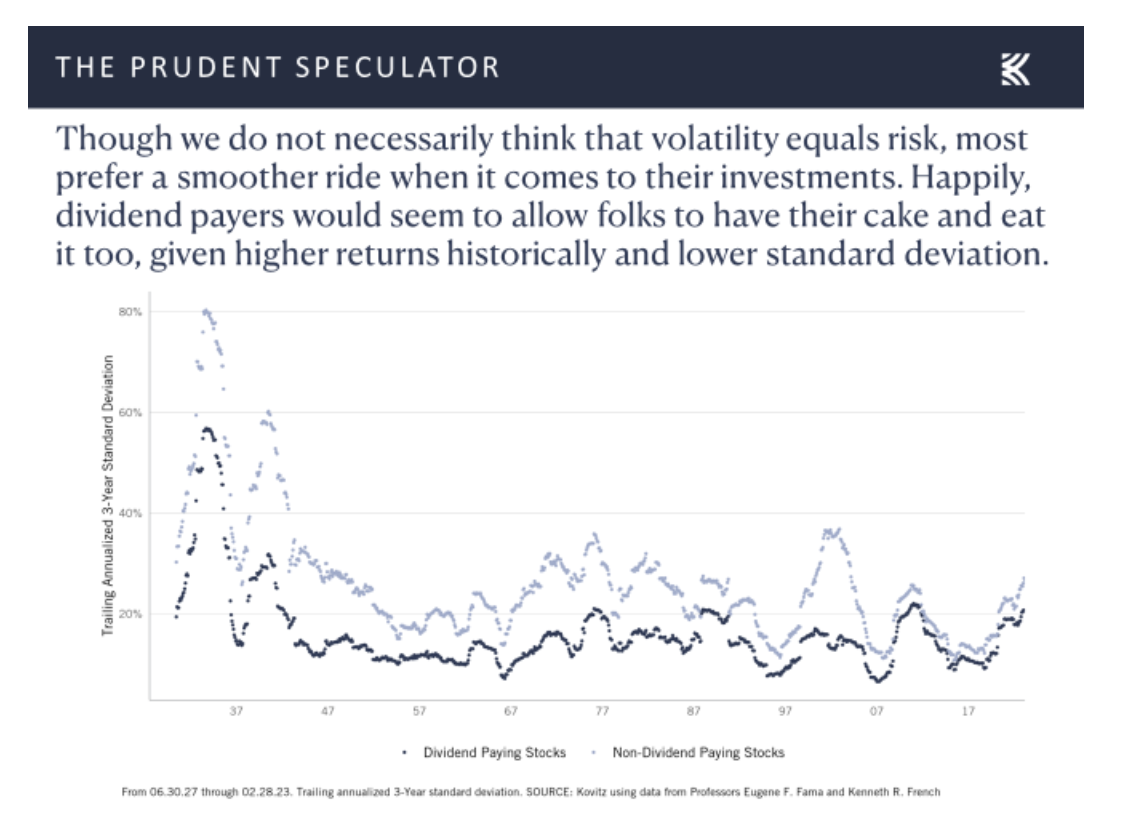

Even better, that outperformance has come with lower volatility as the standard deviation of returns has been lower for Dividend Payers. Not quite the Holy Grail, but higher returns and lower risk is what Wall Street is always targeting!

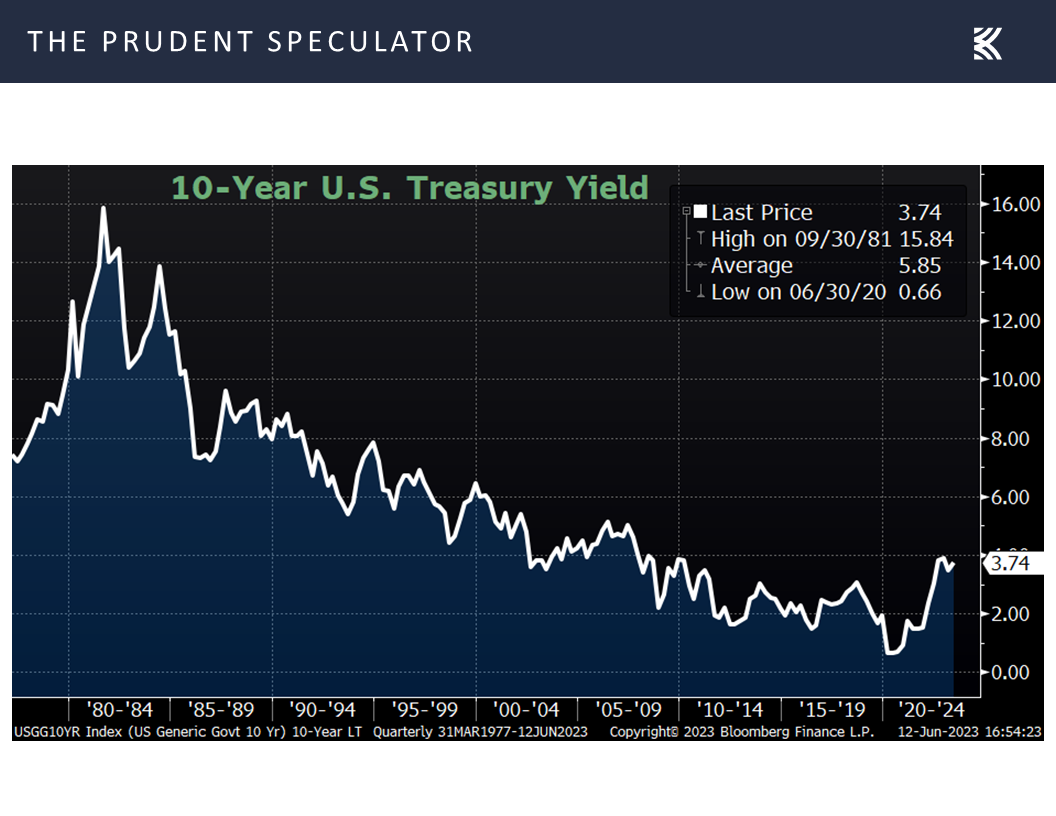

Some will argue that dividends are not very appealing these days, given that interest rates have risen, but the current yield on the benchmark 10-Year U.S. Treasury is today well below its 5.85% average since we launched The Prudent Speculator newsletter in March 1977, some 46 years ago.

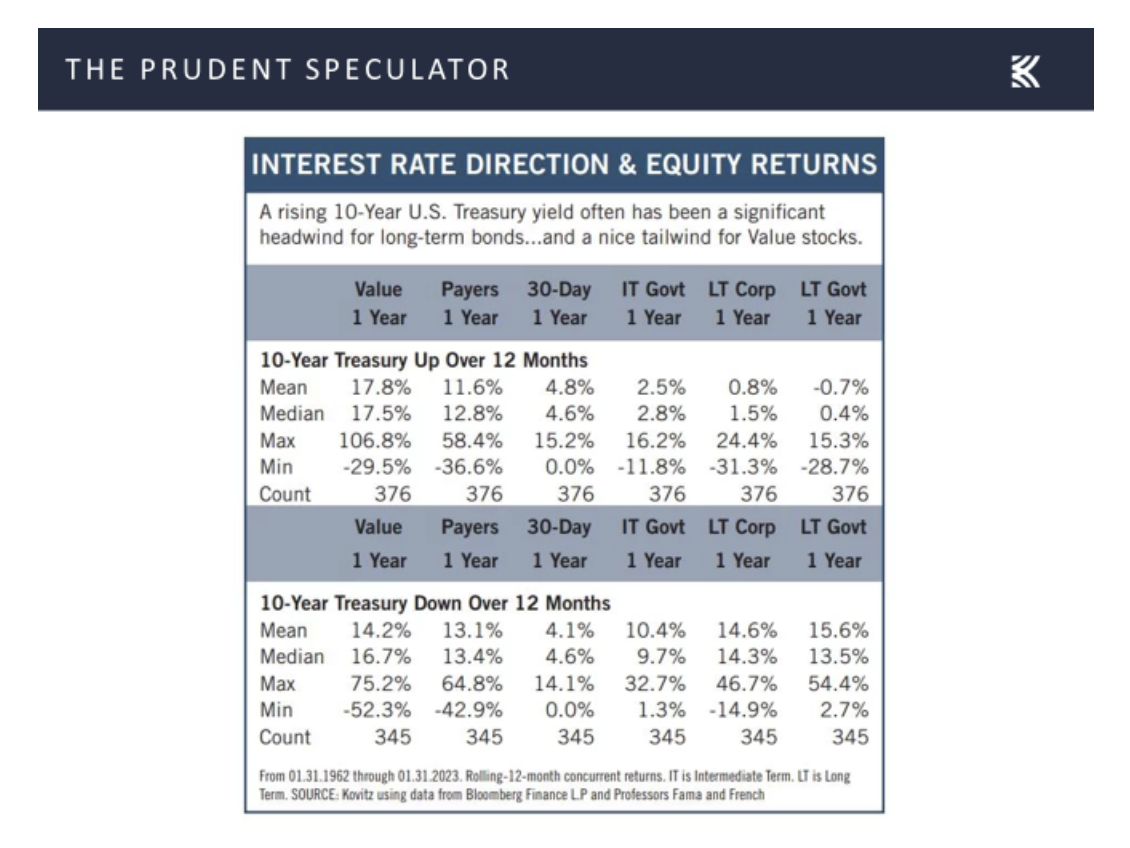

We also realize that some think rising interest rates are bad for equity returns, but history, on average, vehemently argues otherwise. In fact, that only conclusion that can be drawn is that a higher 10-Year Treasury yield over a 12-month span is bad for…long-term government bonds.

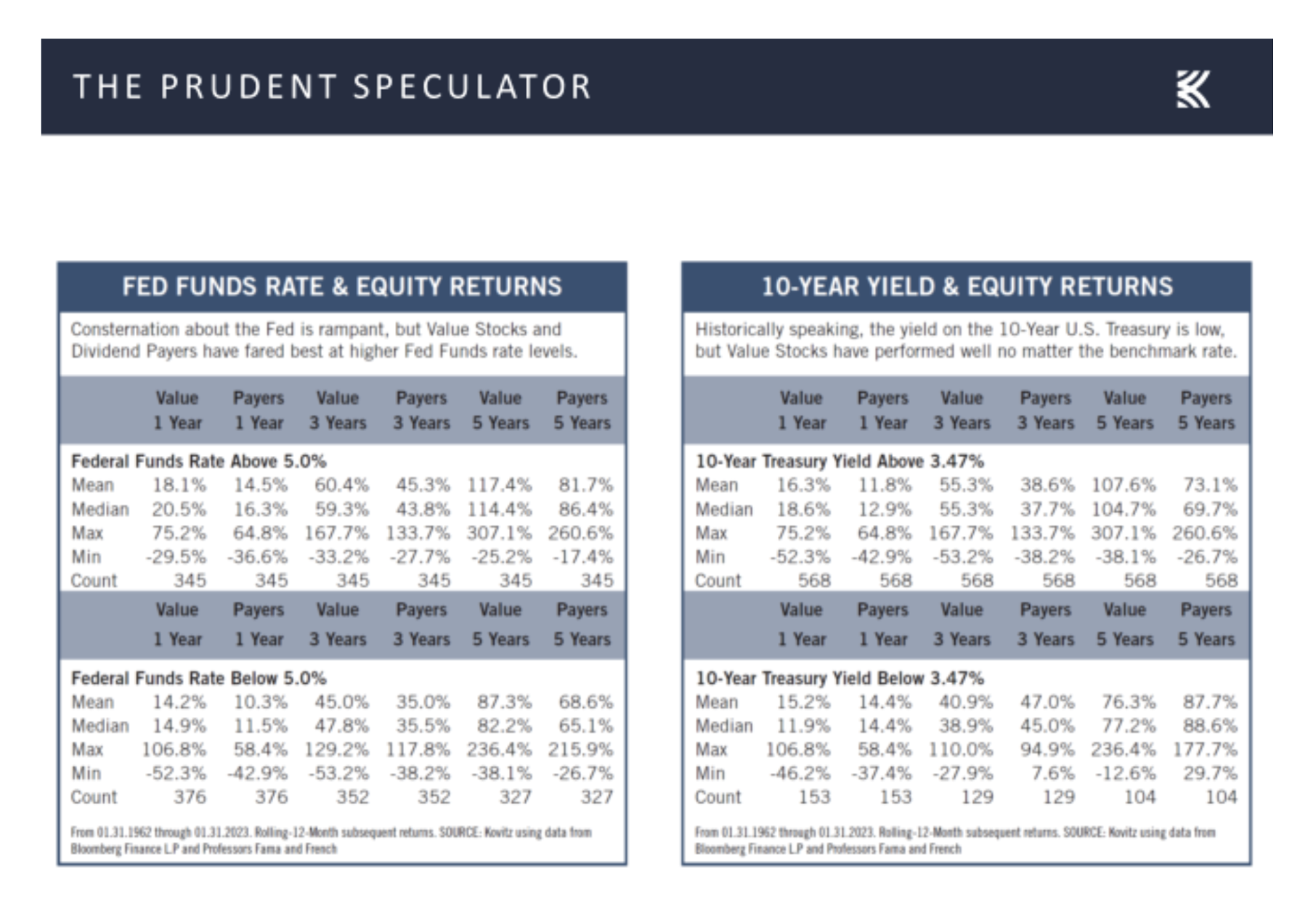

Further, Dividend Payers (and Value Stocks) have performed very well, again on average, when the Federal Funds Rate and the 10-Year Treasury Yield are elevated.

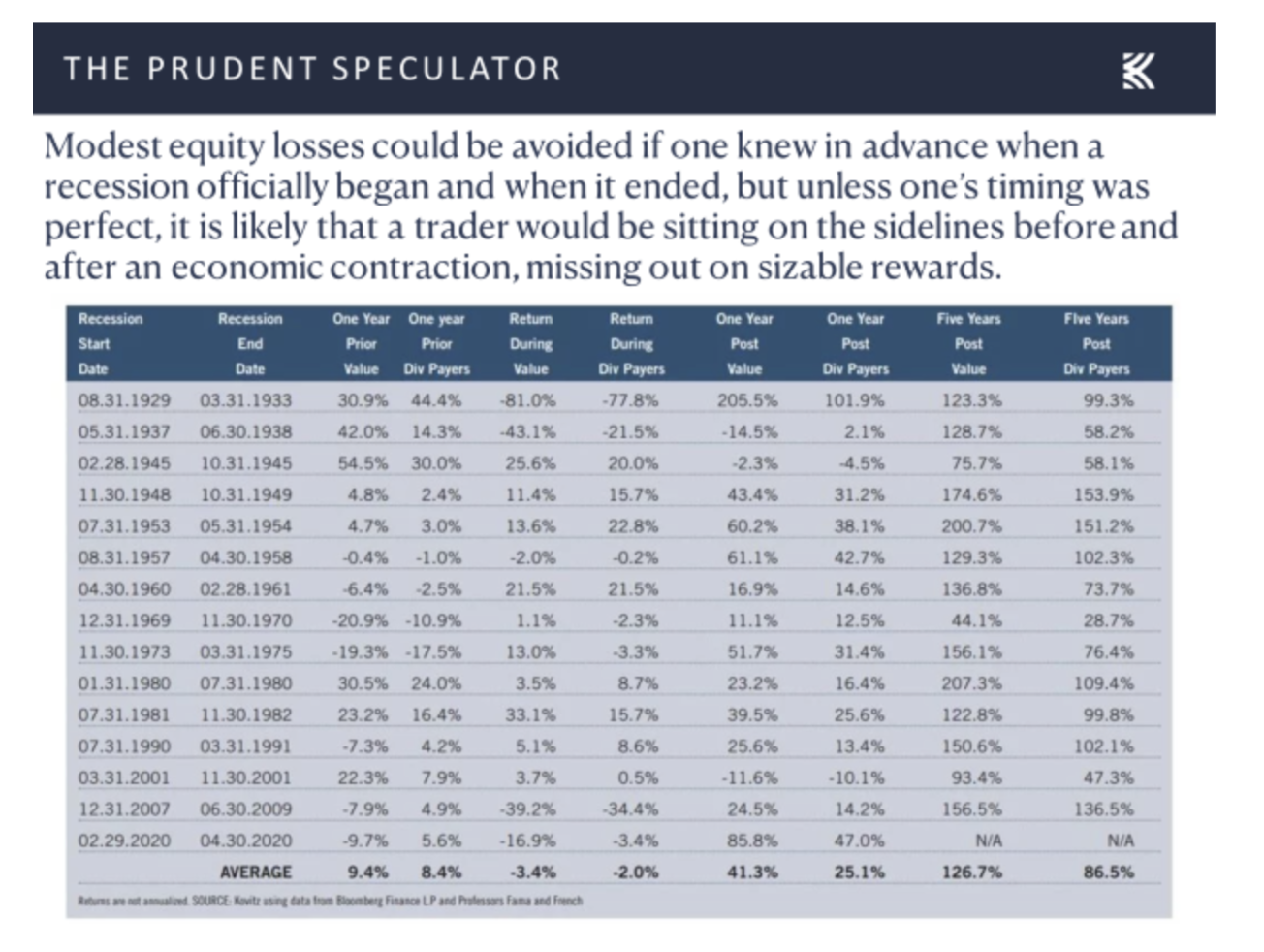

And many are worried about a recession’s impact on stocks, but the data going back more than nine decades suggests that sizable gains, on average, for dividend payers have occurred pre- and post-recession, while the odds of successfully exiting when a recession begins and reentering when the contraction ends are incredibly slim. After all, even economists can’t agree until well after the fact when those dates actually happened.

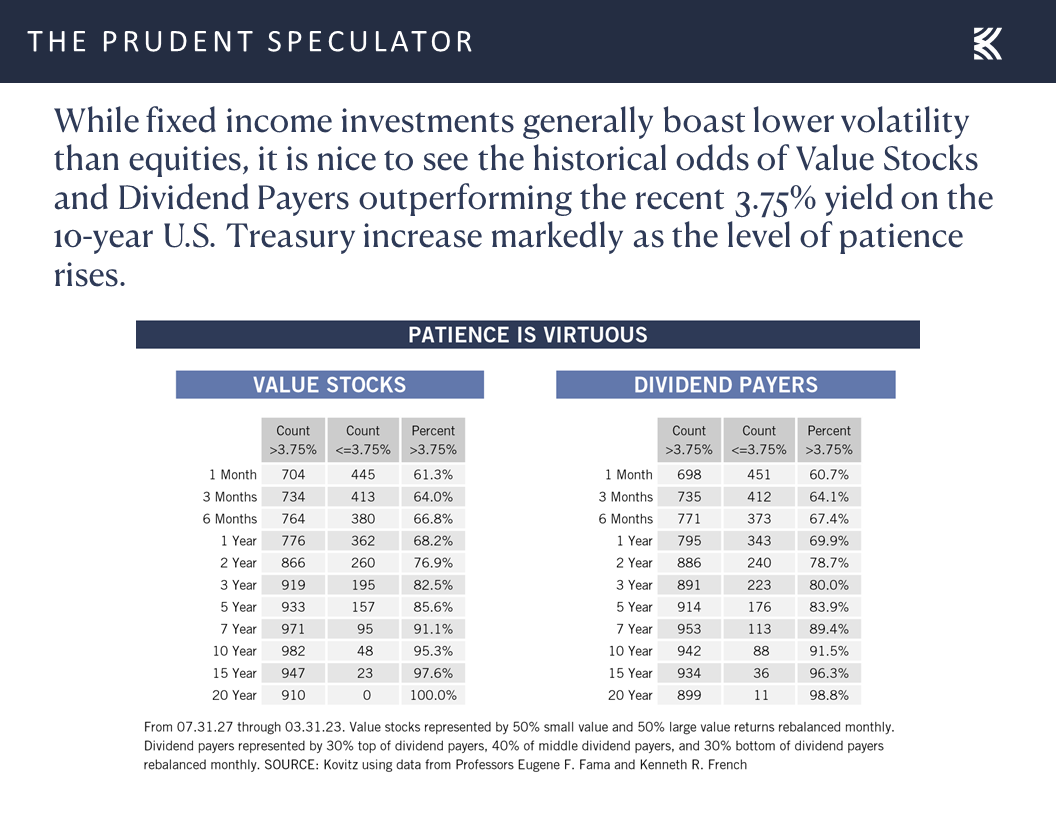

In addition, if history can be a guide, the weight of the evidence suggests that those with a longer-term time horizon have strong odds of achieving a better annualized rate of return with Dividend-Paying stocks than they would with a 3.75% Treasury yield. Hold for 3 months and the chance of Dividend success is 64.1%, but hold for 1 year and it rises to 69.9%, while a 5-year hold brings the probability to 83.9%. And for those who think a 3.75%-yielding U.S. Treasury is the way to go for the next decade, consider that Dividend Payers have exceeded that return in 91.5% of the historical periods dating back to 1927.

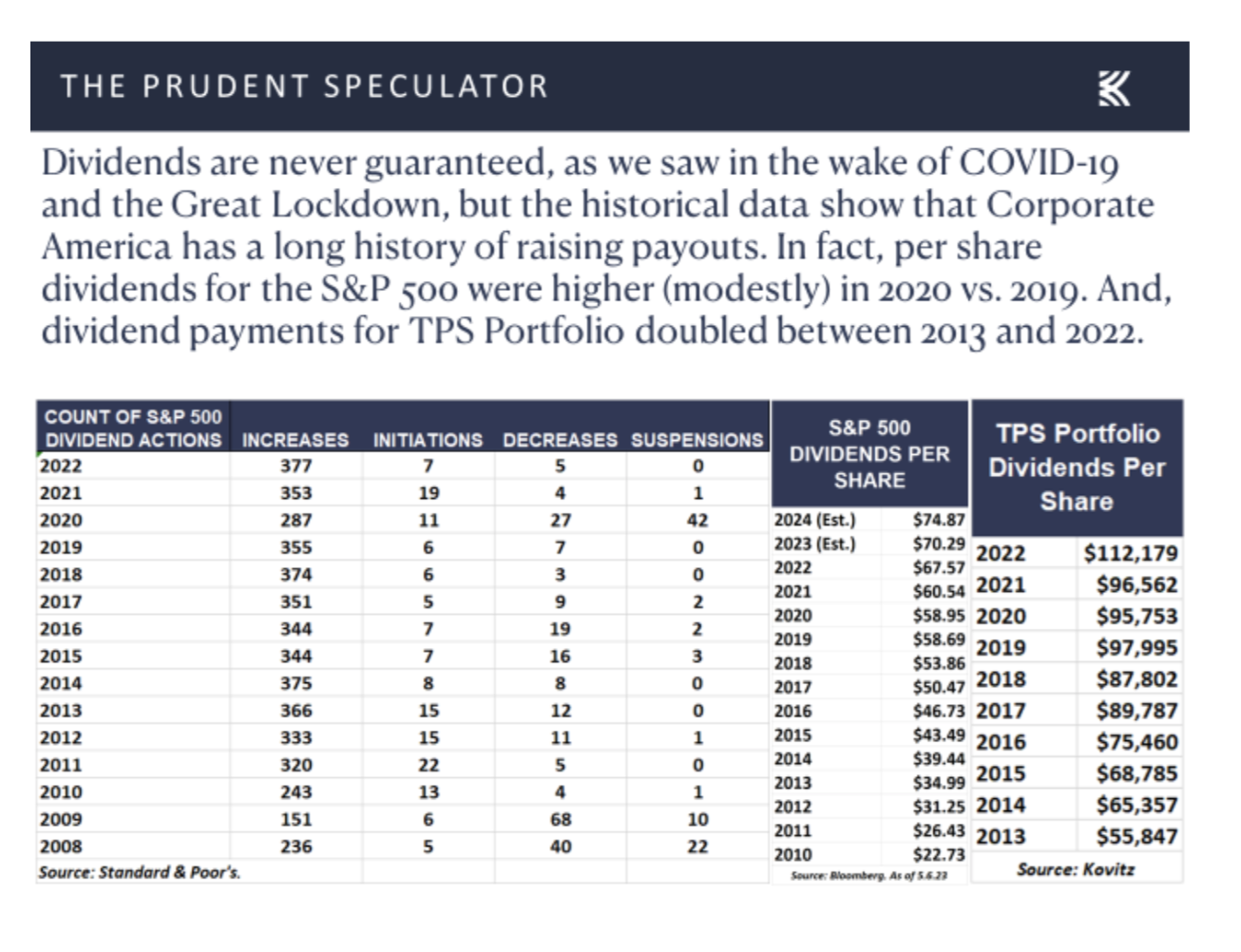

Another very important consideration often overlooked is that as corporate profits rise over time,

companies generally boost their dividends over time. In fact, the total dividend payout for our real-money newsletter portfolio, TPS Portfolio, has more than doubled over the last 10 years.

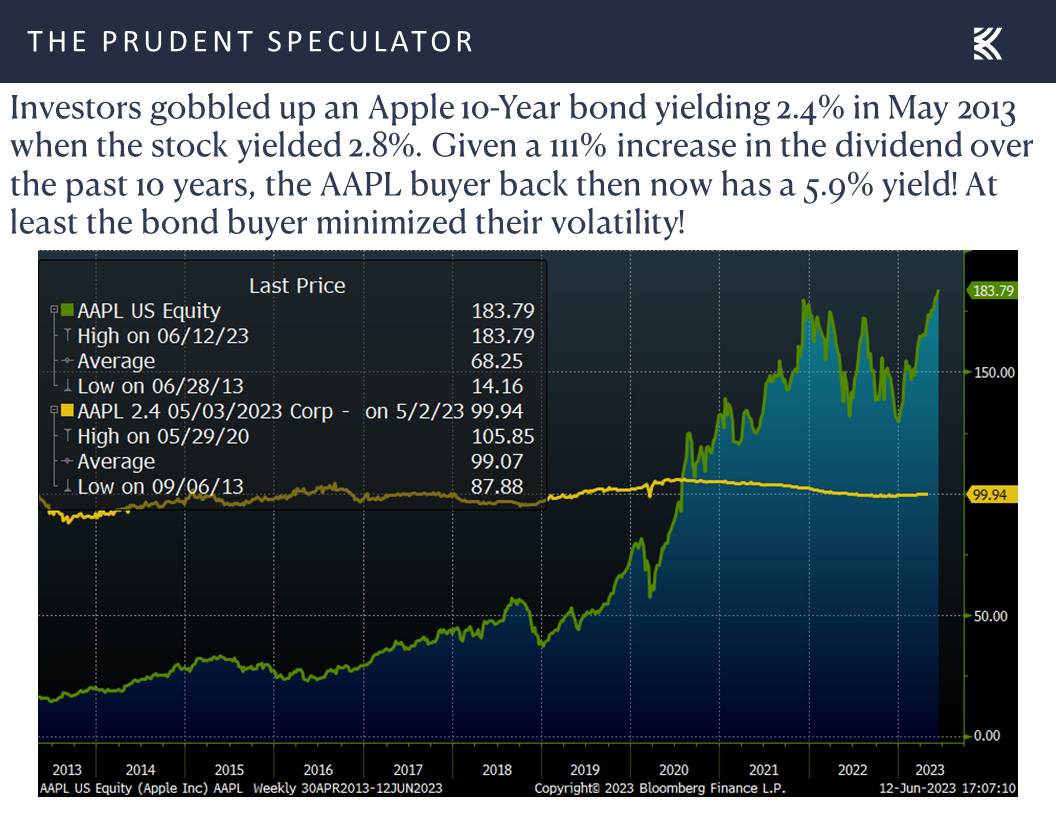

Further illustrating the point is consumer electronics titan Apple (AAPL). Few would consider Apple much of a dividend stock, given a current yield of around 0.5%, but those who bought the stock when it was yielding 2.8% back in 2013 are now receiving a yield on that investment of 5.9%, given all of the dividend hikes in the years since.

Finally, we offer the reminder that it is a market of stocks and not a stock market, and those willing to step away from the indexes can build a broadly diversified portfolio of what we believe to be undervalued stocks with a generous dividend yield of more than 3%, like we have in TPS Portfolio.

And speaking of TPS Portfolio, here are a dozen inexpensively priced stocks that we own, each of which boasts a dividend yield of more than 2.6%, a history of boosting the payout and a stock price that has recently retreated, adding to the long-term total return potential over the next decade.