The Prudent Speculator Monthly Newsletter Issue #675 – January 2023

- Editor’s Note

- Graphic Detail

- Recommended Stock List

- Portfolio Builder

- Databank

- Disclosures

“Only when the tide goes out do you discover who has been swimming naked.” — Warren Buffett

Happy New Year! With stocks suffering a sizable decline in December, we suspect that few are sorry to see the calendar turn to 2023. After all, the broad-based S&P 500 and Russell 3000 equity indexes each retreated more than 5.7% last month, capping a terrible year in which the former ended with a total return of negative 18.1% and the latter minus 19.2%.

There were few places to hide in 2022 as the MSCI Emerging Market and Developed Market equity indexes posted respective losses on a total return basis of 17.7% and 19.9%, while even supposedly safer fixed income instruments stumbled badly. Believe it or not, the Bloomberg Barclays Global and U.S. Aggregate Bond indexes skidded 16.2% and 13.0%, respectively, on a total return basis.

Of course, all those dollops of red ink were not nearly as bad as the massive wallops inflicted on formerly high-flying meme stocks, SPACs, profitless companies and richly valued names, which endured plunges on par with the bursting of the Tech Bubble back in 2000. The New York Times proclaimed, “2022 Was the Year the Music Stopped on Wall Street.” Indeed, a spike in inflation led to a series of rate hikes from a newly hawkish Federal Reserve, despite many not-so-grand economic numbers, forcing a major reassessment of equity valuations.

Not surprisingly, the renewed emphasis on financial fundamentals favored reasonably priced stocks by a wide margin last year, with double-digit percentage return gaps between Growth and Value indexes, even as the latter simply lost less than the former. There are no awards for the declines on Value last year, but we were glad to see that inexpensive stocks held up far better, which is in keeping with the historical evidence when inflation is high, when the Fed is tightening, when interest rates are moving up and when the economy is not robust.

We had our share of winners last year, but many of our stocks were caught in the overall downtrend. As such, we are now up to 11 negative performance years (1981, 1984, 1987, 1990, 1994, 2002, 2008, 2011, 2015, 2018 & 2022) out of the 46 since the launch of The Prudent Speculator in 1977.

Happily, there have been 35 positive years in our history, with the gains in those green periods dwarfing the losses in the lean years. Certainly, it would be nice to somehow have sidestepped the corrections and Bear Markets along the way, but there is far too much evidence that confirms that the only problem with market timing is getting the timing right. Illustrating the point, Bloomberg noted that going into 2022, Wall Street strategists were predicting another good year, with an S&P 500 target near 4950. The index finished the year at 3840

On the flip side, and keeping in mind that it is good to be greedy when others are fearful, there is little enthusiasm for stocks today. The current consensus prognostication from those same strategists is 4078, the 6% estimated gain for 2023 well below the usual upside target. Folks on Main Street are even less enchanted with the outlook as the latest Sentiment Survey from AAII showed a score of 26.5% to 47.6% in favor of the Bears, versus the usual seven-point Bull advantage.

We respect that stocks face headwinds as we head into 2023, with the Federal Reserve estimating real U.S. GDP growth of 0.5%, unemployment of 4.6%, core PCE inflation of 3.5% and a Fed Funds rate of 5.1%. However, given that the average stock ended 2022 in a Bear Market, we think a far more dismal set of economic numbers has been priced into many stocks. Further, we believe higher nominal GDP growth this year, along with generally healthy consumer balance sheets, will support modest corporate profit growth, while we do not think market interest rates will move significantly higher. Warren Buffett states that a pin lies in wait for every bubble, and some balloons are still likely to burst, but plenty of air has been let out of equities while we remain very comfortable with the NTM P/E ratio of 12 and dividend yield of 2.9% for TPS Portfolio.

Featured Graphs, Charts and Visuals

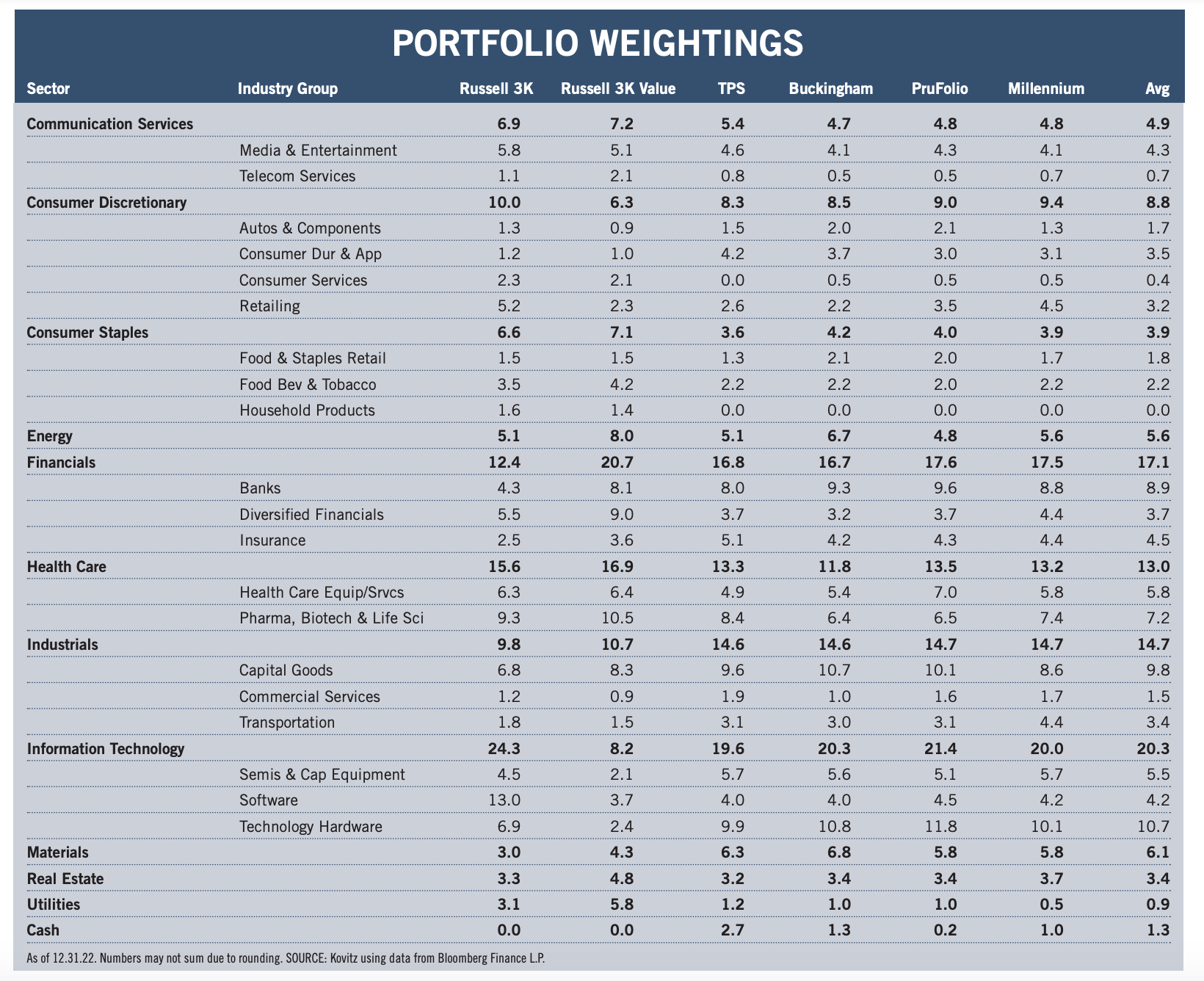

Sector and Industry Group Weightings

Time again to compare the current sector and industry group weightings of our four newsletter portfolios to those of the broad-based Russell 3000 and Russell 3000 Value indexes, noting that our valuation metrics more closely resemble those of Value-oriented gauges. While we very much remain bottom-up stock pickers focused on the merits of individual companies, we also keep an eye on the composition of the indexes in order to ensure that we are comfortable in the over- or under-weighting of a particular sector or industry group. As such, we are able to better focus our subjective reviews on the output of the objective new-idea generation screens that we run every day on areas in which we might desire additional exposure, be it to augment a sector with minimal ownership or to add to a particularly undervalued industry. Illustrative of this process were new recommendations in 2022 of stocks in the Health Care, Communication Services, Consumer Discretionary, Energy and Real Estate sectors. There is a great deal of art accompanying the science of portfolio construction and sector and industry group weightings are always used as a guide and not as the gospel. Over time, the gaps have narrowed, but inevitably there will be dispersion across the newsletter portfolios due to the timing of purchases and modest differences in the names held, even as the same desire for broad diversification has always been pervasive.

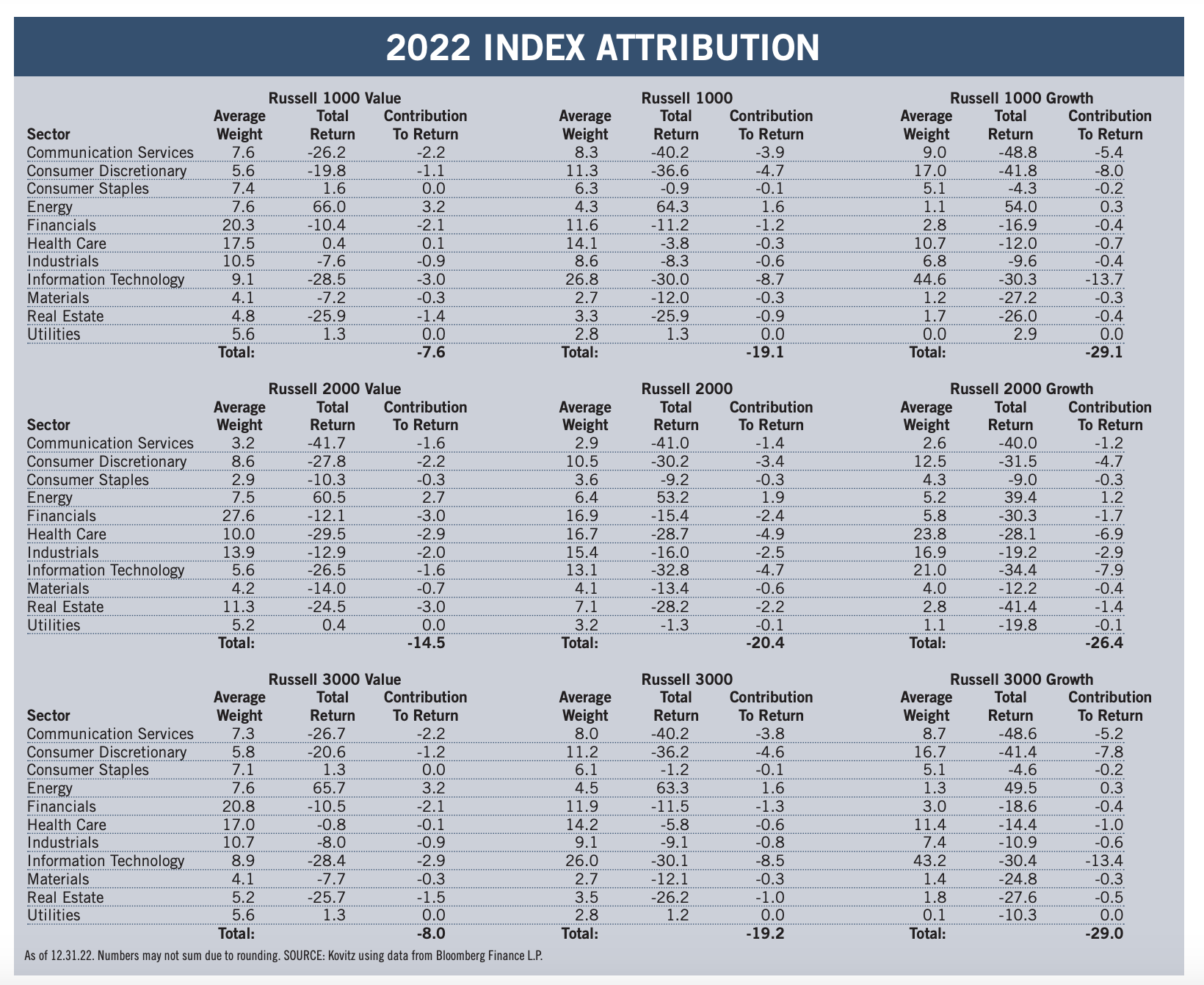

Value vs. Growth Sector Attribution

The following two paragraphs hardly do the subject justice, but the simple attribution displayed below helps to better understand which market sectors contributed the most (or least) to index returns. Given our willingness to buy stocks of any market capitalization, we look at the large-cap Russell 1000, the small-cap Russell 2000 and the all-cap Russell 3000 indexes, as well as the Value and Growth versions of each benchmark. We note that our portfolios, with what we believe to be their inexpensive valuations, have long resembled the Value indexes in terms of their financial metrics, even as our sector weightings have more often than not been lighter in Financials and heavier in Information Technology stocks.

It was one of the largest return chasms in history between Value and Growth for the Russell indexes, with the latter ending 2022 deep into a Bear Market and the former posting sizable losses as well. Returns for the Russell 2000 indexes had the smallest dispersion, even as the Value component beat the Growth, due almost entirely to smaller weightings in Health Care and Info Tech. The largercap Russell 1000 and 3000 Value benchmarks benefitted from lighter exposure to Consumer Discretionaries and Info Tech (both endured awful performance, large and small), while big gains and a greater weighting in Energy offset some of the losses, with near break-even returns in Health Care and Utilities helping the relative cause.

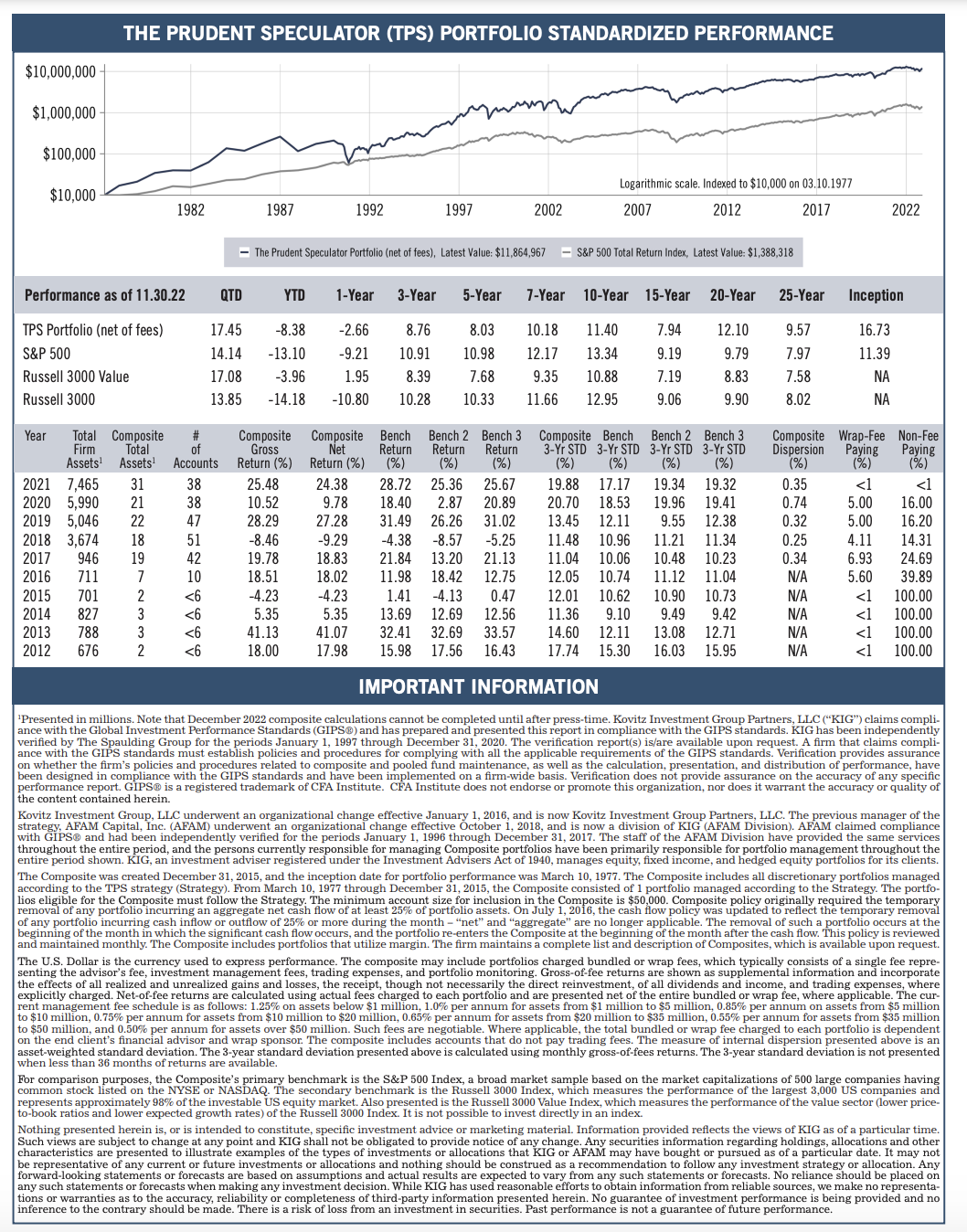

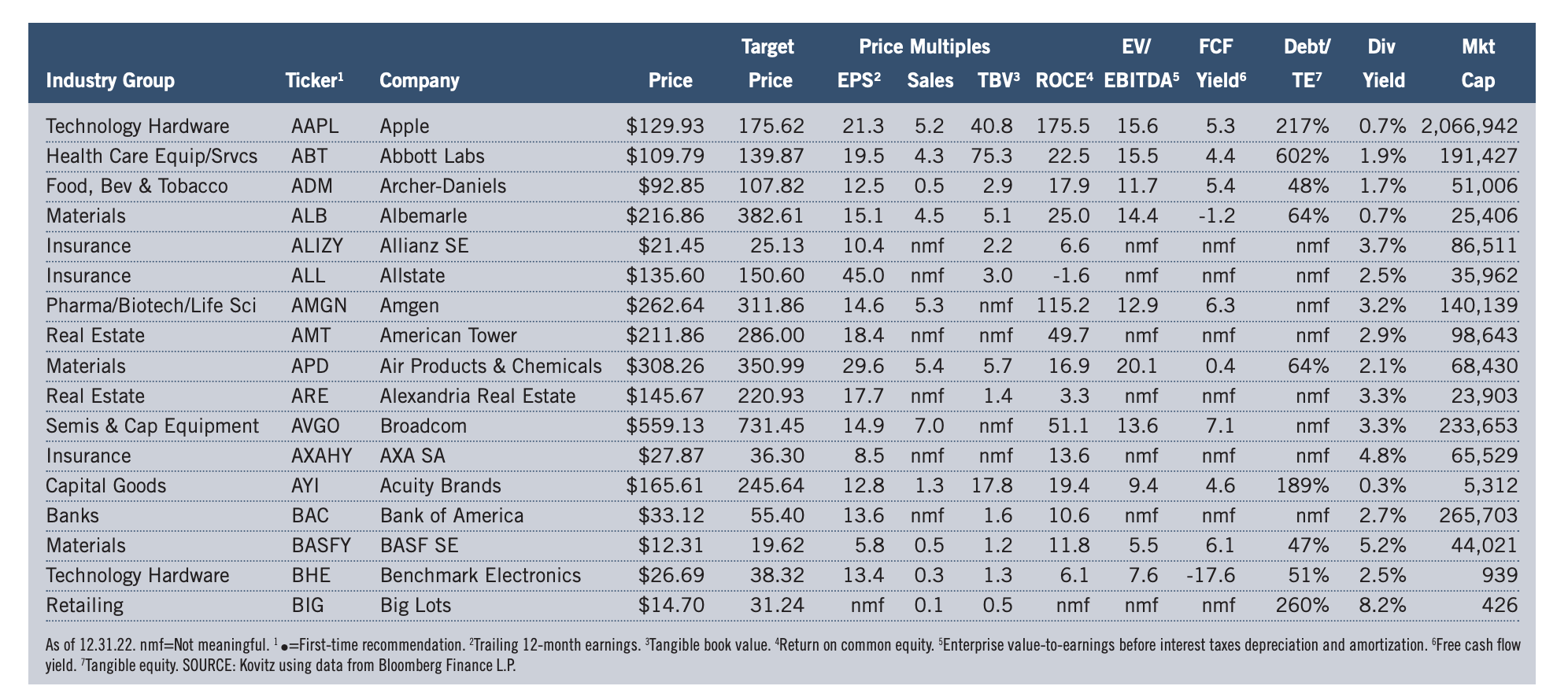

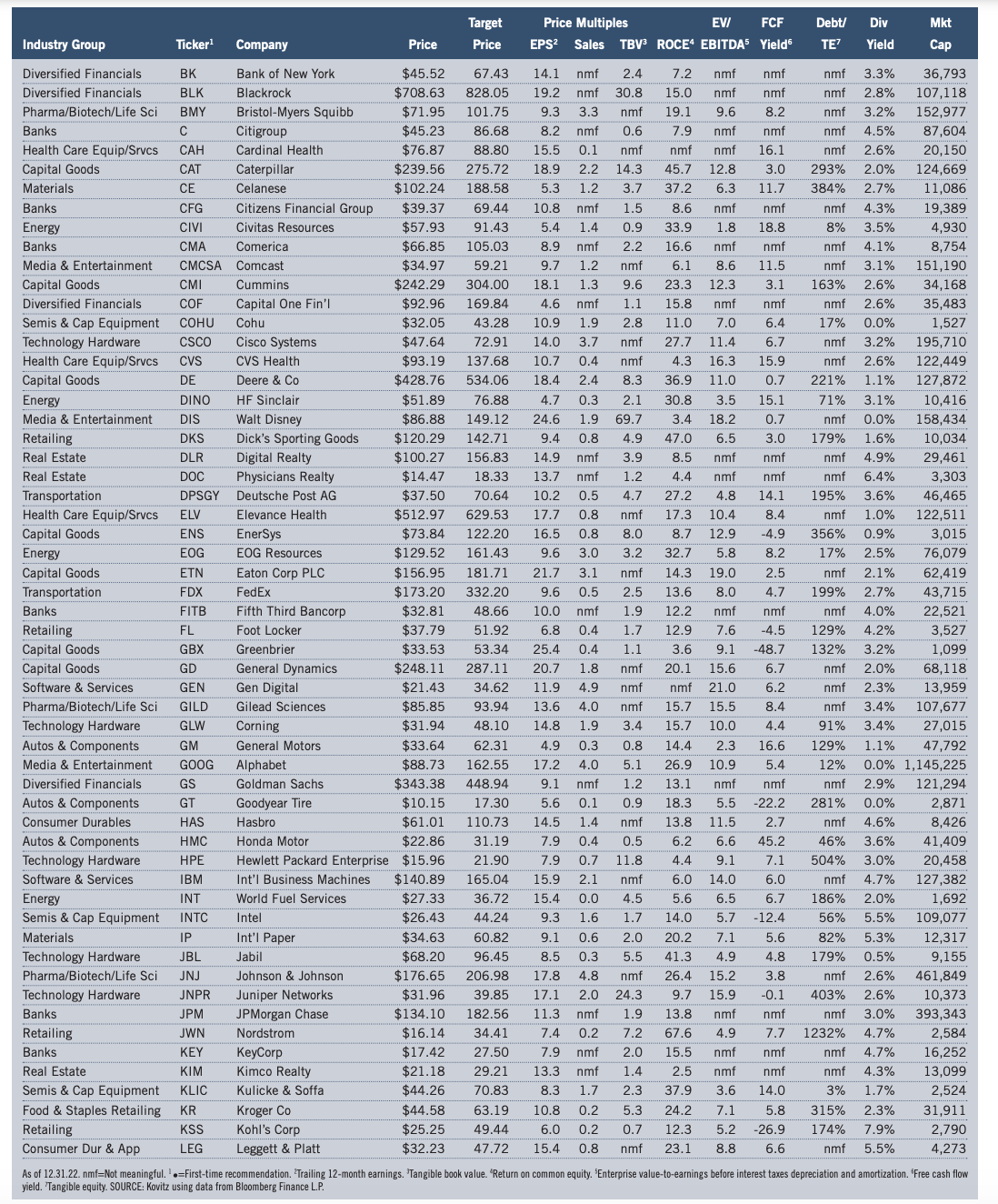

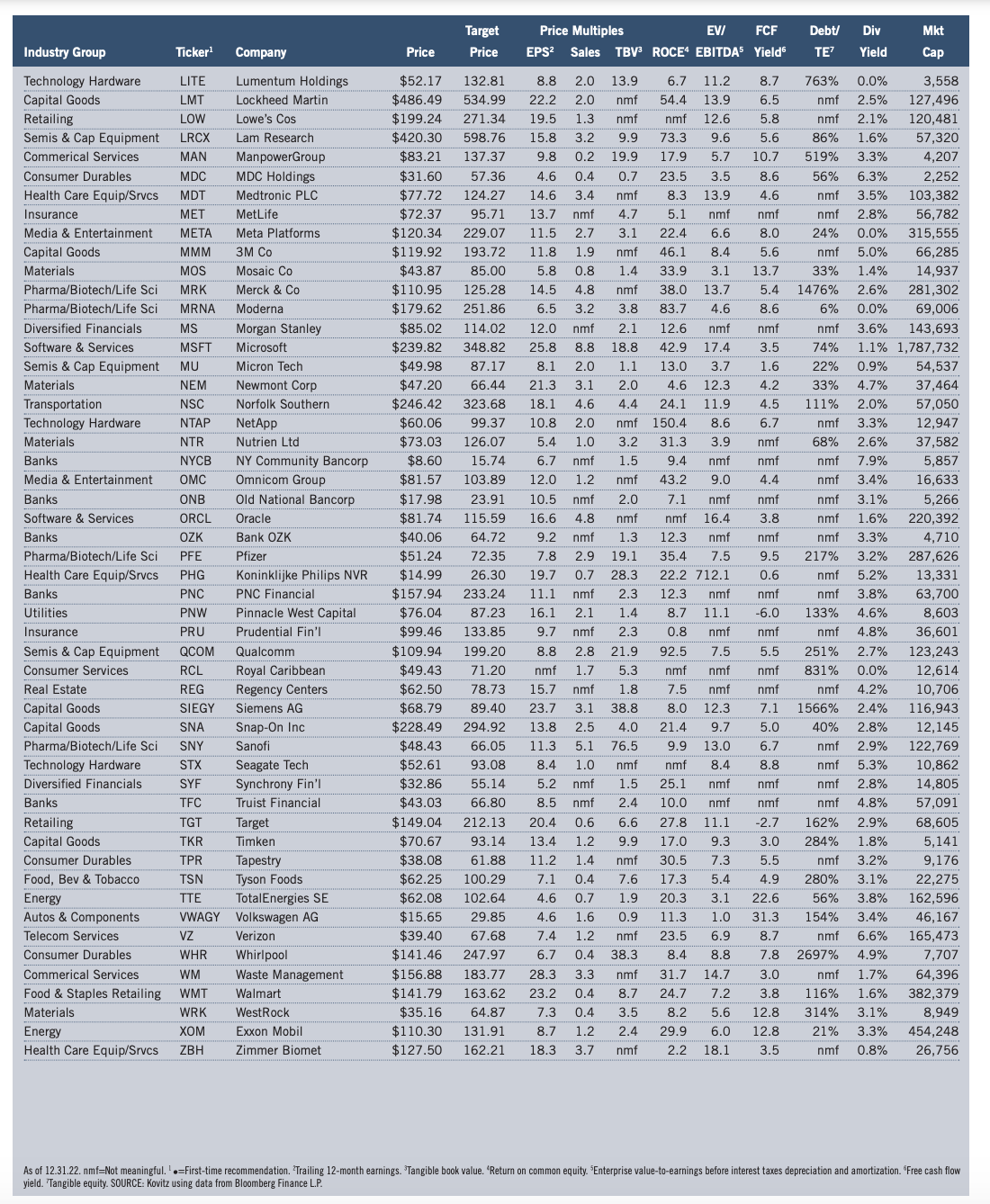

Complete Stock List

In this space, we list all of the stocks we own across our multi-cap-value managed account strategies and in our four newsletter portfolios. See the last page for pertinent information on our flagship TPS strategy, which has been in existence since the launch of The Prudent Speculator in March 1977.

Readers are likely aware that TPS has long been monitored by The Hulbert Financial Digest (“Hulbert”). As industry watchdog Mark Hulbert states, “Hulbert was founded in 1980 with the goal of tracking investment advisory newsletters. Ever since it has been the premiere source of objective and independent performance ratings for the industry.” For info on the newsletters tracked by Hulbert, visit: http://hulbertratings.com/since-inception/

Keeping in mind that all stocks are rated as “Buys” until such time as we issue an official Sales Alert, we believe that all of the companies in the tables on these pages trade for significant discounts to our determination of longterm fair value and/or offer favorable risk/reward profiles. Note that, while we always seek substantial capital gains, we require lower appreciation potential for stocks that we deem to have more stable earnings streams, more diversified businesses and stronger balance sheets. The natural corollary is that riskier companies must offer far greater upside to warrant a recommendation. Further, as total return is how performance is ultimately judged, we explicitly factor dividend payments into our analytical work.

While we always like to state that we like all of our children equally, meaning that we would be fine in purchasing any of the 100+ stocks, we remind subscribers that we very much advocate broad portfolio diversification with TPS Portfolio holding more than eighty of these companies. Of course, we respect that some folks may prefer a more concentrated portfolio, however our minimum comfort level in terms of number of overall holdings in a broadly diversified portfolio is at least thirty!

TPS rankings and performance are derived from hypothetical transactions “entered” by Hulbert based on recommendations provided within TPS, and according to Hulbert’s own procedures, irrespective of specific prices shown within TPS, where applicable. Such performance does not reflect the actual experience of any TPS subscriber. Hulbert applies a hypothetical commission to all “transactions” based on an average rate that is charged by the largest discount brokers in the U.S., and which rate is solely determined by Hulbert. Hulbert’s performance calculations do not incorporate the effects of taxes, fees, or other expenses. TPS pays an annual fee to be monitored and ranked by Hulbert. With respect to “since inception” performance, Hulbert has compared TPS to 19 other newsletters across 62 strategies (as of the date of this publication). Past performance is not an indication of future results. For additional information about Hulbert’s methodology, visit: http://hulbertratings.com/methodology/.

Portfolio Builder

Research Team Highlights

The Prudent Speculator follows an approach to investing that focuses on broadly diversified investments in undervalued stocks for their long-term appreciation potential. Does that mean we build portfolios of 20 stocks…30…? More like 50 and up. We like stocks. And we like a lot of ‘em. We don’t rely nearly as much on “how many” as we do “in which,” but we tend to invest in far more names than most. This expansive diversification, we find, potentially serves us well in two ways: we can further minimize the risk of individual stock ownership, while maximizing the likelihood of finding the truly big winners among the undervalued masses.

As for the “in which” part, readers should know we discriminate among potential investments primarily by their relative valuation metrics and our assessments of stock-specific risk. We buy only those stocks we find to be undervalued along several lines relative to their own trading history, those of their peers or that of the market in general. Our Target Prices incorporate a range of fundamental risks (e.g. credit, customer and competitive dynamic) that we believe the companies may face over our normal three-to-five-year investing time horizon.

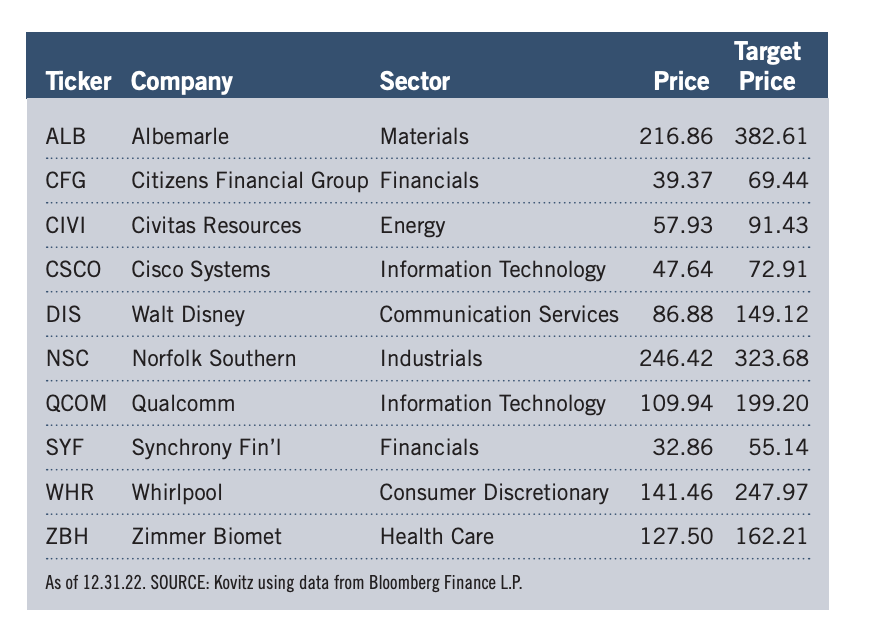

Each month in this column, we highlight 10 stocks with which readers might populate their portfolios. The list is not selected based on performance, as the following methodological hierarchy is utilized: 1) First time recommendations; 2) Stocks that are unowned or under-owned in one of our four newsletter portfolios; 3) Companies that have not been highlighted in the prior five monthly editions of The Prudent Speculator; 4) Editor’s choice. Note that we are in no way suggesting that these stocks replace those featured in prior months as we will always issue a Sales Alert should we choose to exit a position.

Portfolio Builder Notes

This month, we will raise to $11,000 the stakes in Synchrony Financial, Whirlpool and Zimmer Biomet in Buckingham Portfolio. In our hypothetical accounts, we will boost to $19,000 the stake in Walt Disney in Millennium Portfolio. We have enough stock and/or sector exposure to Albemarle, Cisco Systems, Citizens Financial, Civitas Resources, Norfolk Southern and Qualcomm in our newsletter portfolios, so no additional purchases of those six this month. As is our custom, we will wait two trading days until Friday, January 6, to transact.

New Stock Picks for the Month

About This Month’s Stock Selection

Albemarle (ALB)

Albemarle is a global specialty chemicals company with leading positions in lithium, bromine and refining catalysts. ALB has top-tier lithium assets through its brine operations in Chile and spodumene operations in Western Australia, which are among the lowest cost globally. Shares are well below their $325 peak in November, even as booming lithium demand for electric vehicles has pushed the EPS estimate to $28 for ALB this year. An economic downturn is a risk, but CFO Scott Tozier reminded, “Of the three businesses, bromine and our lithium specialties demand is likely the most leveraged to global economic trends in consumer and industrial spending, automotive and building and construction. At the same time, they benefit from having diverse end-markets, meaning they can allocate production to higher growth or higher margin end-markets as needed. Bromine and lithium specialties also tend to rebound quickly after recession. Finally, catalysts, demand is closely linked to transportation fuel demand. In a typical recession, catalysts is relatively resilient. Think about it this way, oil prices generally drop in a recession and that drives higher fuel demand, which equals higher catalysts demand for refining and typically the catalysts business would benefit from lower raw material costs.” We think ALB is a value-priced growth stock.

Citizens Financial Group (CFG)

Citizens Financial Group is a regional bank founded in 1828 that has over $200 billion of assets across 1,000 branches primarily located in New England and the MidAtlantic. Following the purchase of HSBC branches in its market and the acquisition of Investors Bancorp in 2021, Citizens has grown its deposit franchise by over 17% yearover-year. We think the moves complement and round out its existing territory, while adding JMP Group (securities) into the fold (also in 2021) brings diversification through additional fee generation. Dealmaking and capital markets activity has slowed, but higher net interest spreads and a focus on maximizing operating leverage for an expanded operation prime the bank for higher returns in the current year. Shares trade for a single-digit estimated P/E ratio and offer a 4.3% dividend yield.

Civitas Resources (CIVI)

Formerly known as Bonanza Creek, Civitas is the combination of several oil & gas concerns purchased over the past two years to create a company that bills itself as the largest pure-play oil & gas producer in Colorado. Assets are scattered throughout the Denver-Julesburg Basin of the Rocky Mountains. CIVI claims to have industry-low lease-operating and per-barrel expenses with production that consists of 40% oil and the remainder a combination of gas and natural gas liquids. Management has a propensity for deals, which it has mostly financed with equity. We think this has given prospective investors pause, even as global energy supply constraints and favorable commodity prices have enabled massive income payments ($6.29 per share) in the past year. A clean balance sheet ought to support the stock should demand fade and energy prices weaken, and we like that CIVI has committed to returning 50% of free cash flow back to shareholders (mostly in the form of special and variable dividends). Shares trade for a low-single-digit multiple of each of the consensus double-digit EPS estimates for the next two years, while the “fixed” dividend represents a 3.5% yield on its own

Cisco Systems (CSCO)

Cisco Systems is a tech powerhouse that specializes in Internet Protocol (IP)-based networking equipment for professional, telecom provider and residential use. CSCO has exceeded analyst EPS projections for ten straight quarters, and despite the commodity-like nature of its hardware offerings, analysts project EPS growth between 5% and 8% for each of the next three years. While margins contracted last quarter, the company’s order book has been growing and the digital transformation (to software and subscription hardware) has been valuable from a revenue standpoint. Revenue was up 6% in the latest quarter and we expect continued growth for the figure as we remain enthusiastic about CSCO’s competitive position in the commodity switching space. The challenges of 2022 pushed the P/E ratio below 14 and the yield above 3%.

Walt Disney (DIS)

Disney operates one of the largest diversified media companies in the U.S., is a global leader in producing branded family entertainment, and owns one of the best intellectual property portfolios in the world. Earnings in fiscal Q4 came in substantially behind analyst estimates, causing the stock to plunge and pushing DIS near the multi-year lows set early in the pandemic. In late November, Disney swapped out CEO Bob Chapek in favor of a second stint for former CEO Bob Iger. While Disney’s shareholder returns during Mr. Iger’s first term were phenomenal, we suspect investors have concerns about the internal health of Disney’s corporate offices and the ability of Mr. Iger to swiftly improve the company’s culture and financials. Disney+ is not yet profitable and sports rights remain expensive. Earnings estimates have been revised down, so the stock is not as cheap as one might expect given the 40% whack since the end of 2021, but we continue to be fans of Disney’s deep library of content, committed fan base and willingness to adapt.

Norfolk Southern (NSC)

Norfolk Southern is a leading North American transportation provider, operating 20,000 rail route miles in 22 states and the District of Columbia, serving every major container port in the Eastern U.S., and providing efficient connections to other rail carriers. Faced with labor renegotiations and service hiccups in the past year, management has tweaked its game plan for capitalizing on network efficiency toward a focus on the intermodal and truck-torail conversion. We find this to be a reasonable strategy given NSC’s robust intermodal segment and as operator of the most extensive network in the East. Norfolk will likely have to stomach higher wages as it is faced with building its workforce (even as it has recently trimmed its conductor pipeline) and a slower economy could impact volumes. Nevertheless, share price consolidation over the last couple of years makes the valuation reasonable at 18 times forward earnings estimates. We continue to appreciate the competitive benefit that rail networks are virtually impossible to replicate, along with their efficiency in transporting certain freight. The dividend yield is 2.0%.

Qualcomm (QCOM)

Qualcomm is a designer and manufacturer of wireless communications equipment. The company holds many wireless-related patents and is a key contributor to the development of CDMA, a communications technology that is heavily used around the world. The quarterly reports in the second half of fiscal 2022 were soft, resulting in the QCOM shares being cut nearly in half at the same time that analysts trimmed the consensus earnings estimate from more than $13 to nearly $10. Challenges remain on the horizon, China’s reopening pivot has been problematic and there are significant questions about near-term demand trends, all of which may cause the bumpy ride for QCOM to be extended. On the plus side, margins can improve, supply chains can stabilize and the Chinese handset market continues to mature. We can see why traders might have jitters, but long-term investors should be excited to scoop up a QCOM that is on sale. Shares trade for less than 11 times forward earnings estimates, while the dividend yield is 2.7% and the balance sheet has only a modest amount of debt and plenty of cash.

Synchrony Financial (SYF)

Synchrony is one of the largest issuers of private label credit cards in the U.S., but also offers co-branded products, installment loans and consumer financing for smalland medium-sized businesses, as well as healthcare providers. For its private-label credit business, SYF performs the underwriting for programs that enable partners to encourage repeat business and engender customer loyalty by earning promotions and rewards. Even though payment rates remain somewhat elevated, we expect credit line usage to build over time as consumer liquidity is drawn down in coming quarters, likely elevating interest income. CEO Brian Doubles recently said that current net chargeoffs of around 3% were “just a little more than half of our long-term average,” demonstrating a consumer base that remains healthy. And, SYF boasts significant equity capital (a CET1 ratio of 14.3%) and reserves for potential future loan losses (over 10% of loans) should the economy turn south. Shares skidded 27% last year, presenting a favorable entry point, as the NTM P/E is 5.4 and the dividend yield is 2.8%, while management has bought back 40% of the stock over the past 5 years.

Whirlpool (WHR)

Whirlpool is the top major appliance manufacturer in the world, with seven brands that each have more than $1billion in sales. Shares were battered in 2022 (down 37%) as home sales slowed following the Fed’s steep and aggressive rate increases. The stock now trades for a single-digit NTM P/E multiple (the current EPS estimate for 2023 is $16.58) and has a dividend yield of almost 5%. Like most businesses involved in manufacturing, Whirlpool has had to contend with supply constraints and raw material cost inflation over the past several quarters, which when coupled with higher interest rates has created some stiff near-term headwinds. However, these challenges are nothing new for Whirlpool as the company has navigated similar bumps in the road during its 111 years of operations. WHR generates solid free cash flow and we see scenarios where the company continues to benefit from renovations in North America in the near term. Longer term, we think Whirlpool will benefit from non-North American markets driving growth as the rest of the world progresses technologically and emerging markets incorporate modern conveniences into daily living.

Zimmer Biomet (ZBH)

Zimmer Biomet is a global leader in orthopedic implants (hips, knees, spine, trauma and dental) and related orthopedic surgical products. ZBH is by far the king in hip and knee implants and has operations in 25+ countries. Management recently stated that macro issues are a challenge, but the company is seeing an offset via COVID-19 recovery due to pent-up demand for elective surgeries. Despite ongoing operational headwinds, we continue to believe that over the long term favorable demographics will drive solid demand for large-joint replacement. While a strong fourth-quarter rally left ZBH mildly higher in price in 2022, the stock still sports a below-industry average forward P/E ratio of less than 19 and there are relatively easy revenue and profit comparisons as we move into 2023. Management believes innovation and more emphasis on non-elective procedures is a way to keep revenue and earnings growing. We appreciate ZBH’s efforts to rework its product lineup with cutting edge technology like its ZBEdge ecosystem, a suite of integrated digital and robotic technologies, and the momentum built for its ROSA Robotics equipment. We continue to like Zimmer’s global revenue stream and its focus on cultivating close relationships with orthopedic surgeons who most often make the brand choice for their procedures. Further, Zimmer has accumulated an impressive portfolio of patents (owning or controlling approximately 4,500 issued patents and applications around the world).

Our Value Stock Portfolio’s Historical Performance Data