The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Economic Outlook, AAII Sentiment, Interest Rates and Corporate Profits. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Newsletter Portfolio Trades – Sold AYI

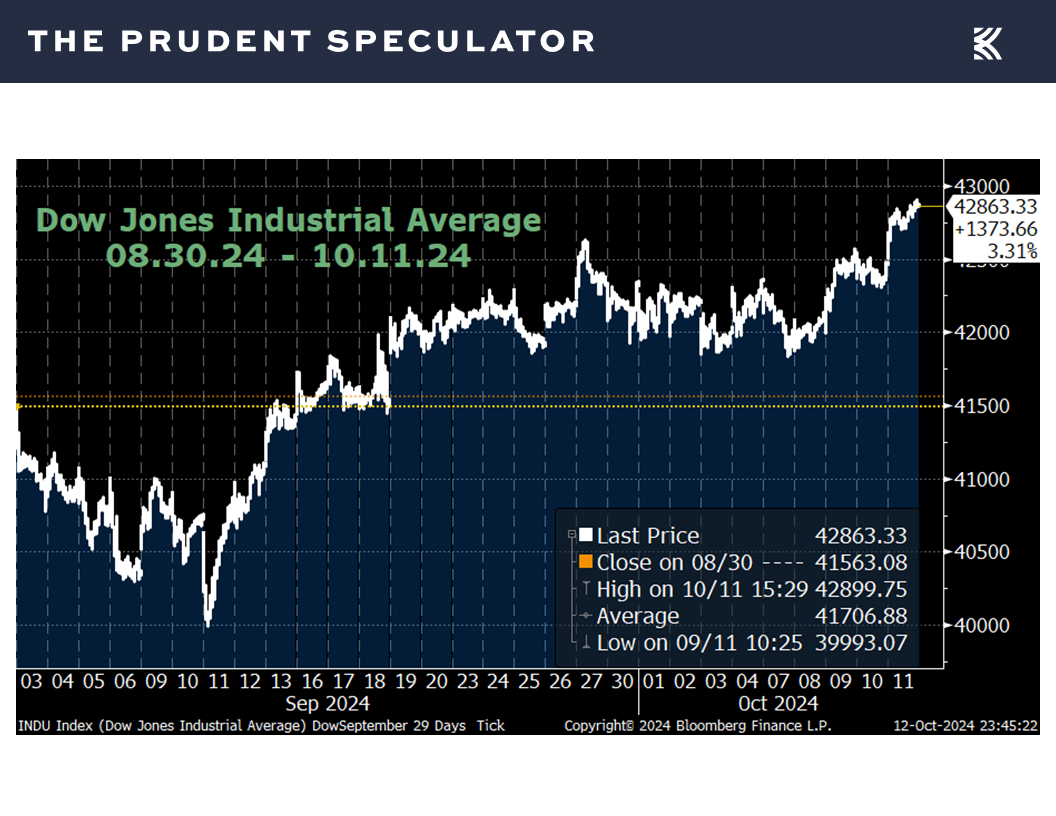

Trading Week – Scary Season Rally Continues

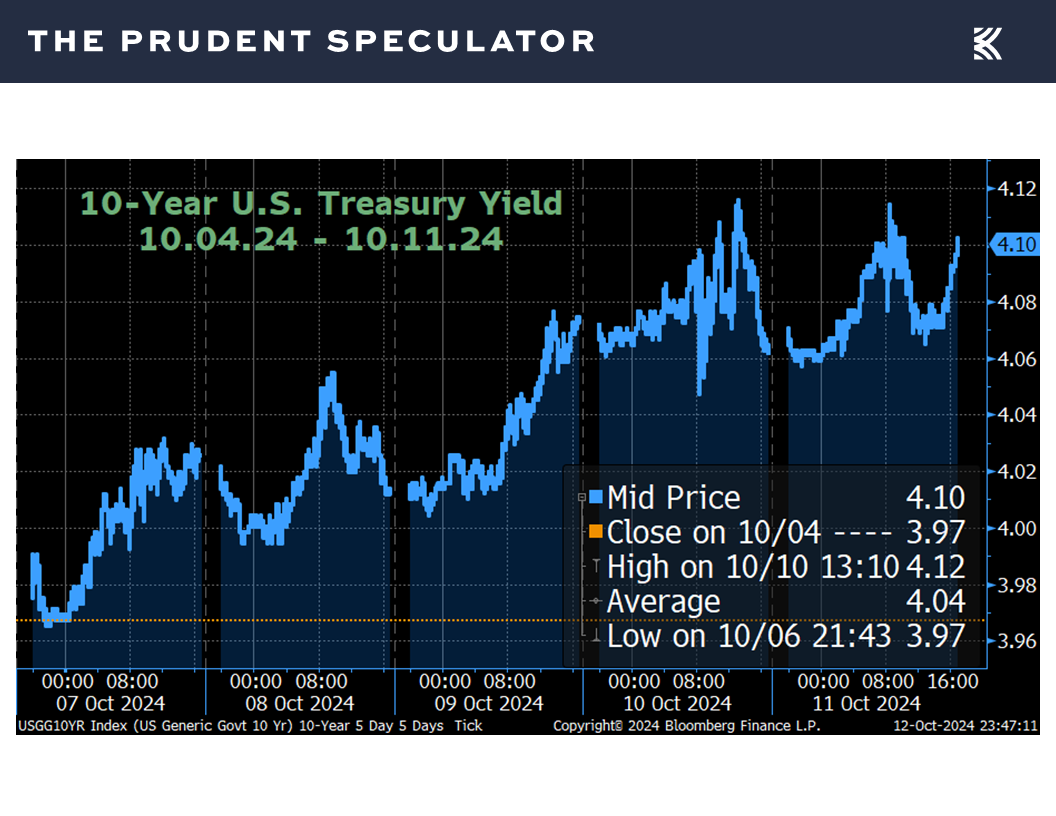

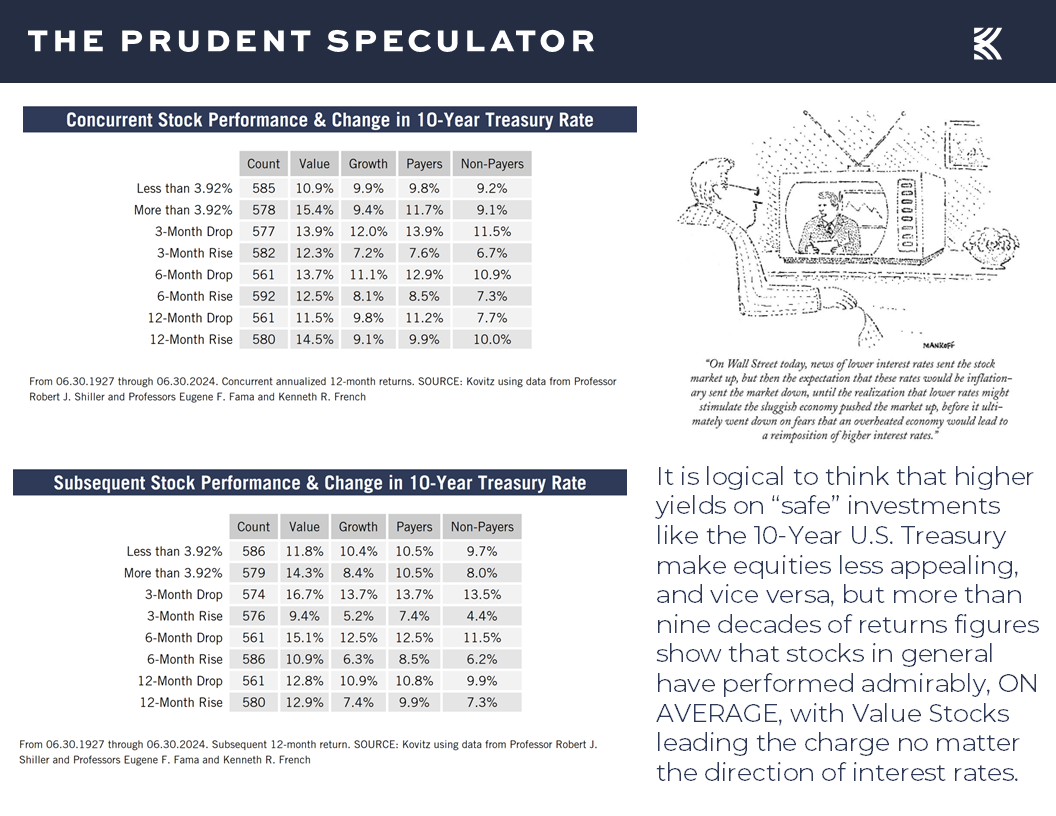

Interest Rates – Yields Jump; Stocks Haven’t Minded Historically, on Average

Headwinds – Ups and Downs but Long-Term Trend in Stocks Has Been Higher

Profits – Favorable EPS Outlook

Econ Outlook – Weaker-than-Expected Stats and Higher Inflation, but Numbers In Line with Fed Projections

Sentiment – AAII Bullishness Spikes

Media – Pessimism Still Sells More Newspapers

Market of Stocks – Tech Bubble Bursting in 2000 Didn’t Sink All Boats

Valuations – Liking our Metrics

Stock News – Updates on BLK, BK, JPM, GOOG, APD & PFE

Trading Week – Scary Season Rally Continues

There is still half a month to go, but the historically seasonally weaker two-month September-October time span continued to provide support for our long-held assertion that time in the market trumps market timing as equities managed to again gain ground last week.

The move higher extended the bounce from the September 11 break below 40000 on the popular Dow Jones Industrial Average to more than 2800 points and pushed the advance since the start of the supposedly scary period to more than 1300 points, or 3.31%, not counting dividends.

Interest Rates – Yields Jump; Stocks Haven’t Minded Historically, on Average

Interestingly, the 1%+ rally over the last five trading sessions came despite another big jump in interest rates, with the yield on the benchmark 10-Year U.S. Treasury climbing from 3.97% to 4.10%.

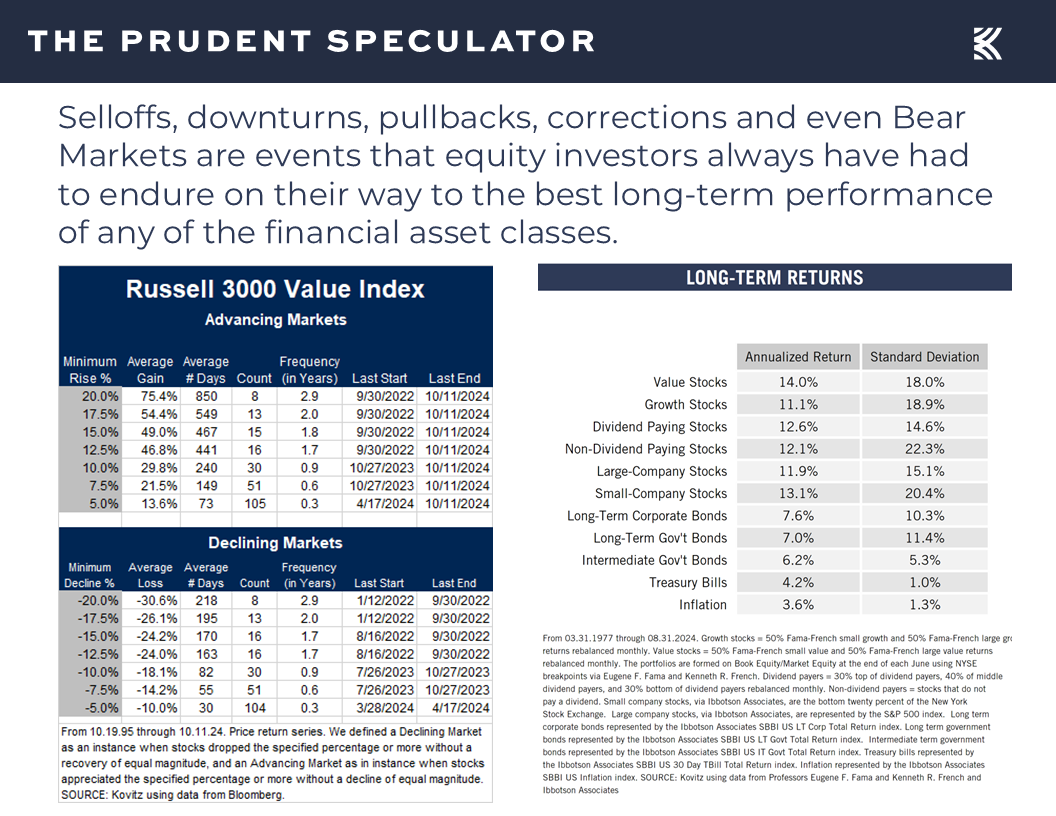

Headwinds – Ups and Downs but Long-Term Trend in Stocks Has Been Higher

Of course, students of market history know very well that stocks have performed fine, on average, whether interest rates are rising or falling,

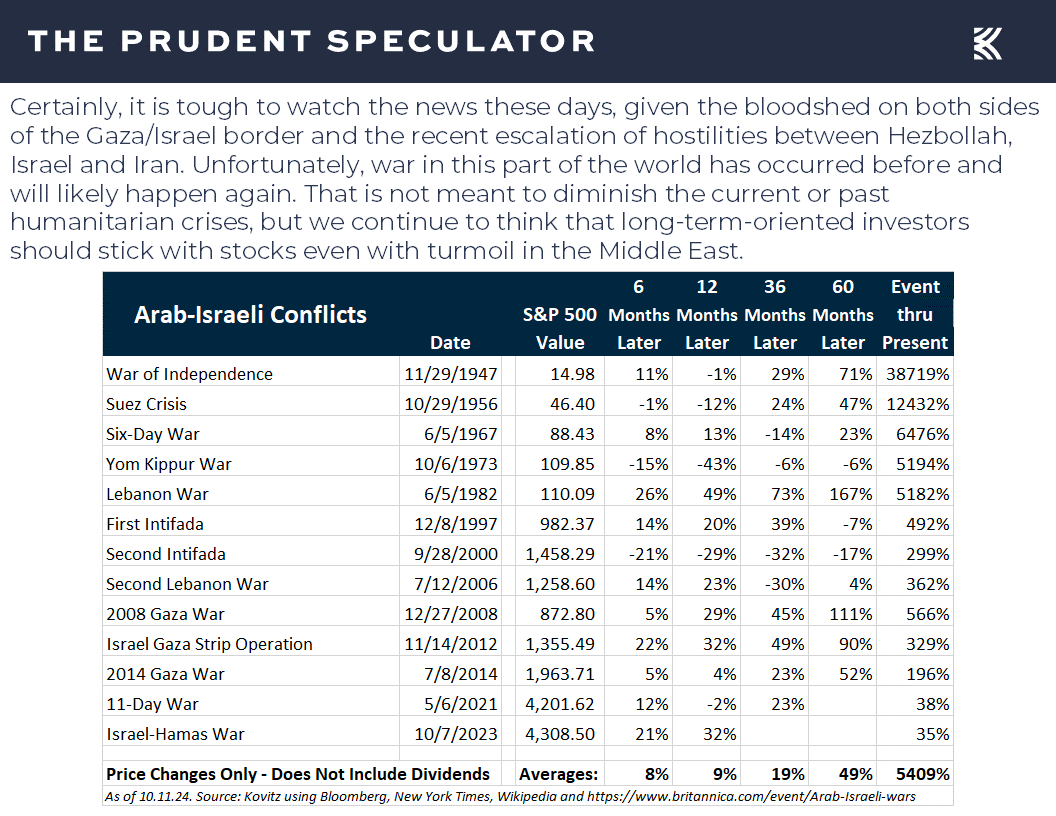

just as they understand that disconcerting events on the global stage, such as Arab-Israeli conflicts, also are not reason to alter a long-term commitment to equities.

No doubt, it is easier with the major market averages at all-time highs to buy the argument that sticking with stocks through thick and thin is the way to go, but we never forget that downside volatility is always part of the investment process. Indeed, even as Value Stocks, like those we have long championed, have enjoyed an average annualized rate of return of 14.0% since the launch of The Prudent Speculator in March 1977, there have been numerous downturns along the way, with 5% setbacks taking place three times per year on average and 10% corrections happening every 11 months or so.

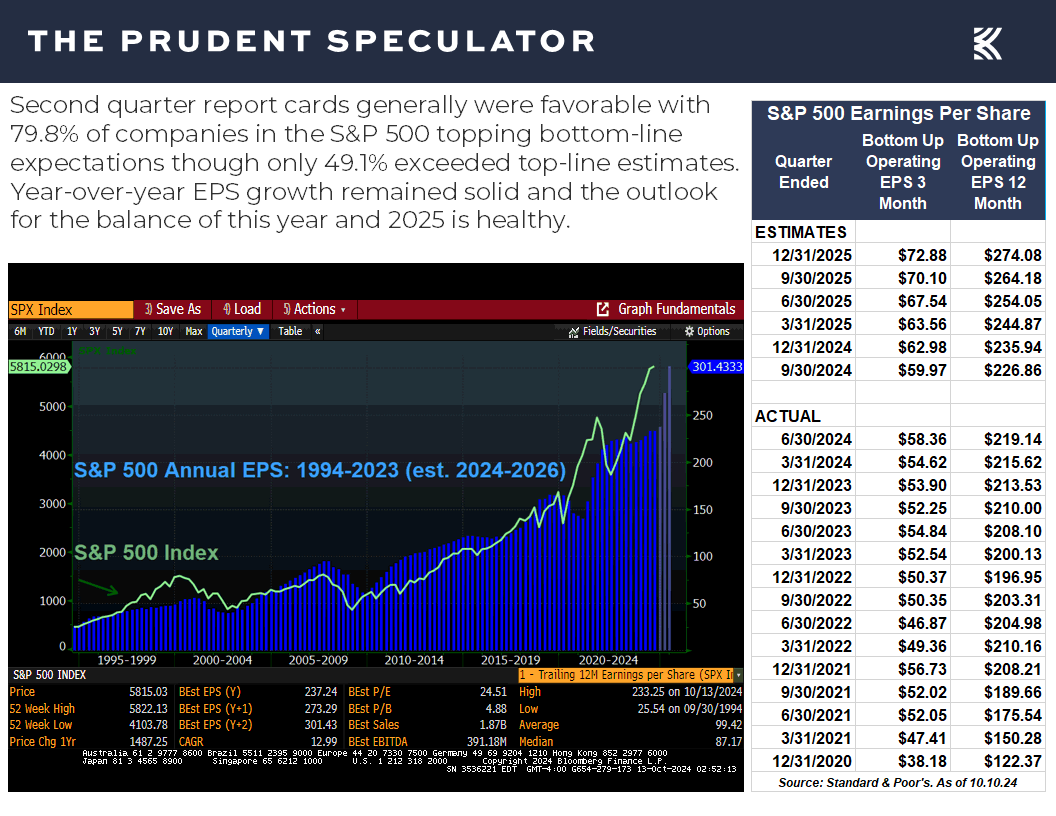

Profits – Favorable EPS Outlook

To be sure, the long-term trend has been up, as companies become more valuable over time as corporate profits have marched steadily higher, aside from a few interruptions generally associated with recessions.

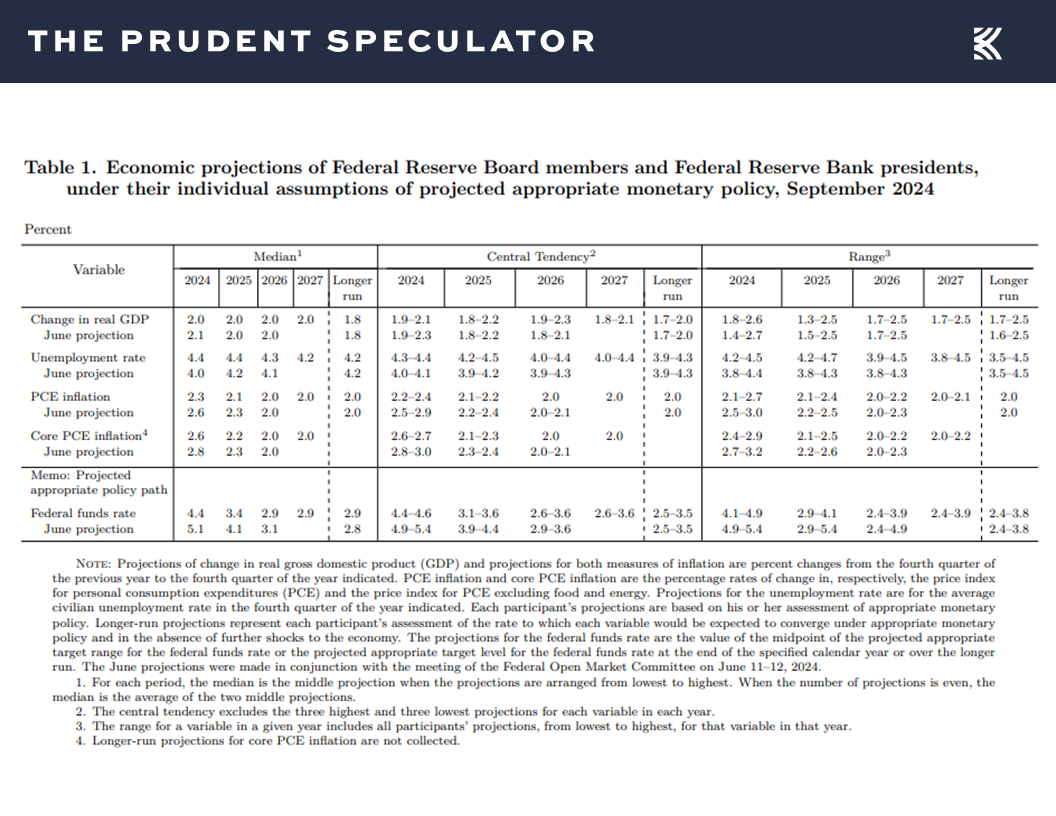

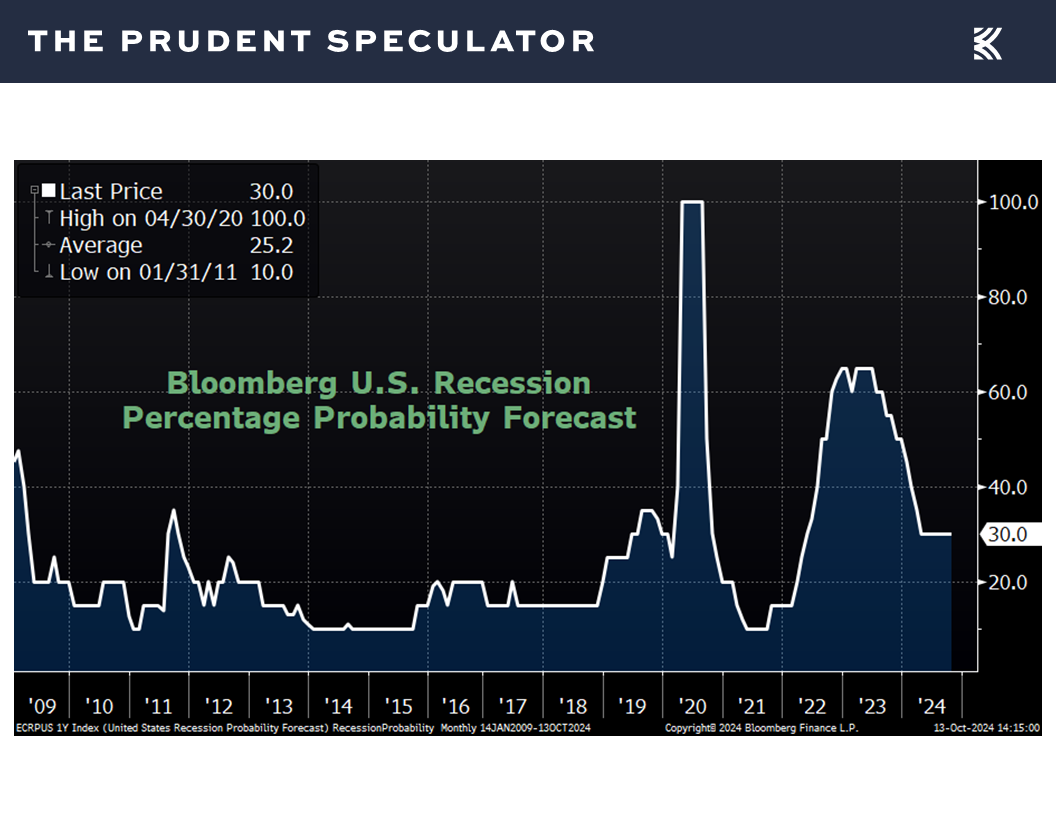

Econ Outlook – Weaker-than-Expected Stats and Higher Inflation, but Numbers In Line with Fed Projections

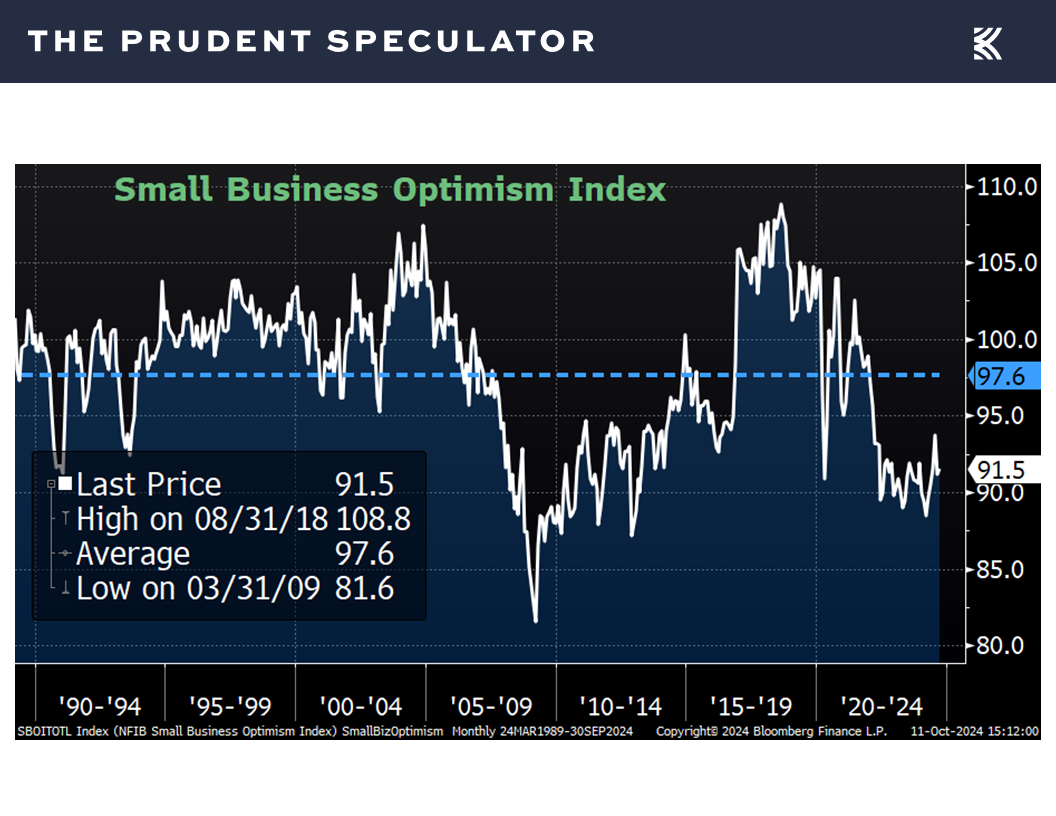

The health of the economy is thus super important for the prospects for stocks, so some might have been surprised that the markets continued to move north last week, given that the NFIB Small Business Optimism index for September came in at a weaker-than-expected 91.5,

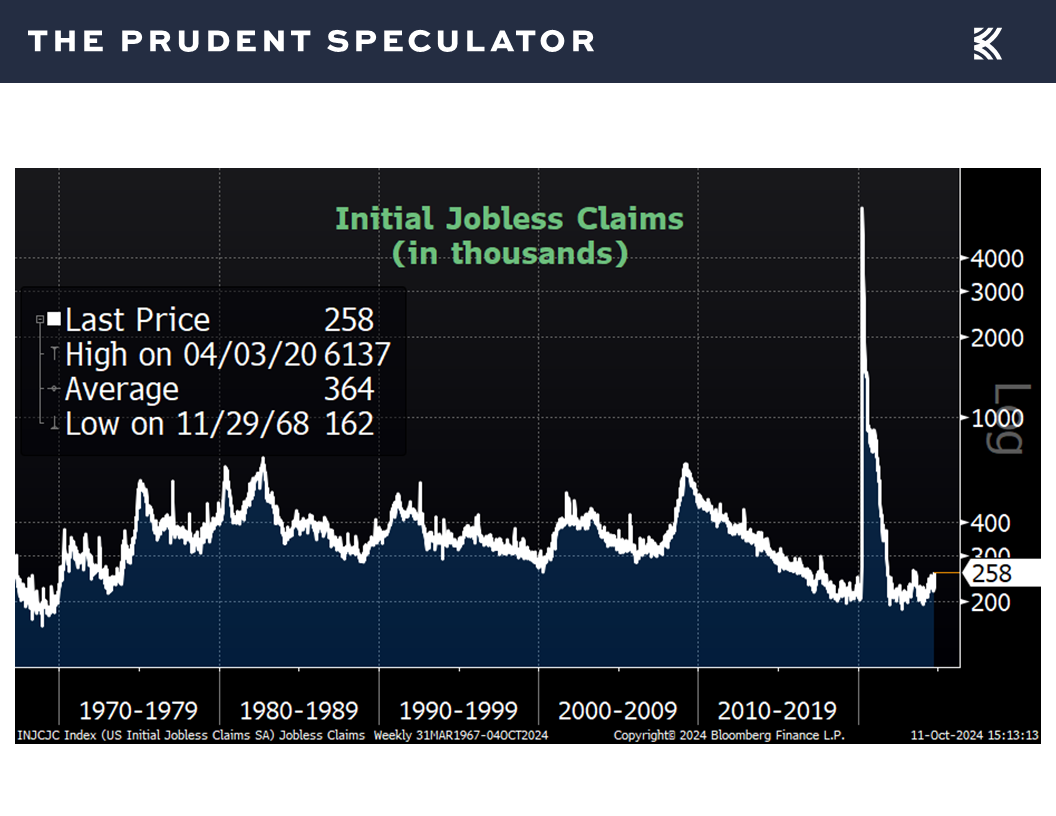

first-time filings for unemployment benefits in the latest week jumped to a much-high-than-forecast tally of 258,000,

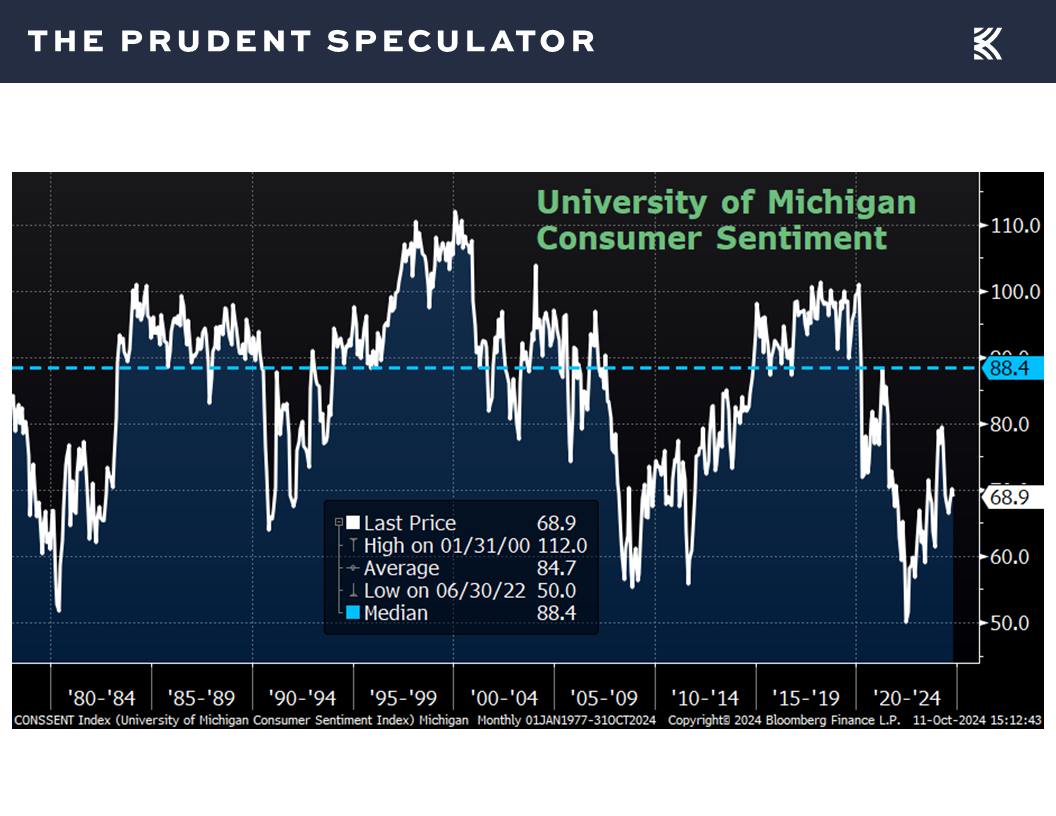

and the University of Michigan’s preliminary Consumer Sentiment reading for October fell to 68.9, below estimates of 71.0 and down from the final September figure of 70.1.

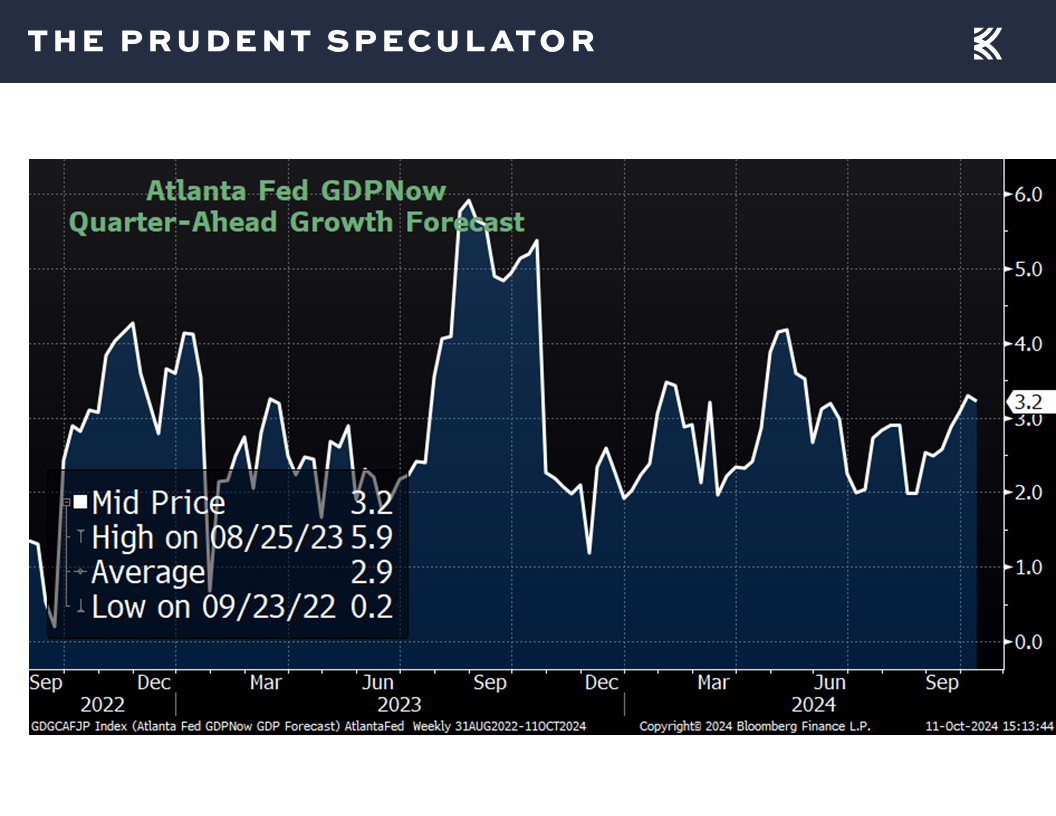

Of course, the latest forecast for real (inflation-adjusted) U.S. GDP growth for Q3 from the Atlanta Fed was a healthy 3.2%,

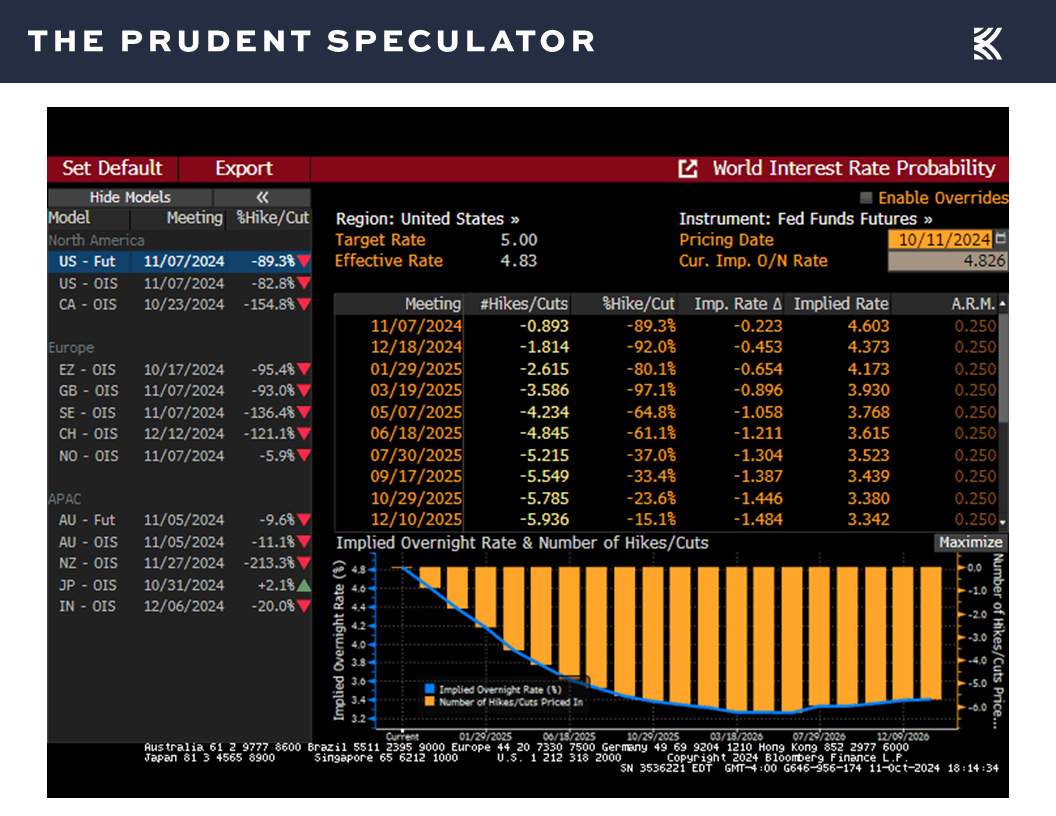

while the Fed Funds futures market saw wagers that the Fed will be less aggressive, not more aggressive, in cutting interest rate to support the economy, with the year-end ’24 and year-end ’25 betting now standing at a yield of 4.37% and 3.34%, respectively, up from 4.28% and 3.29% a week ago.

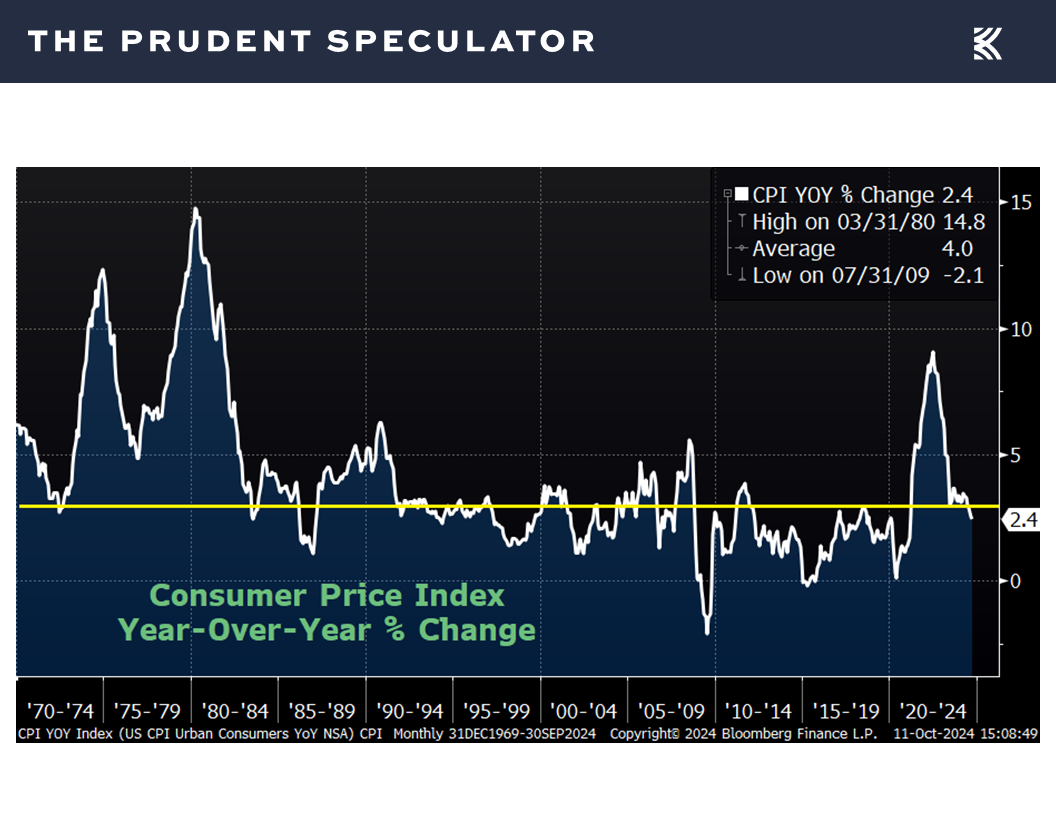

True, the odds of Jerome H. Powell & Co. being more patient in further reducing rates were also influenced by a slightly higher-than-expected print (2.4% vs. 2.3% est.) for September on inflation at the consumer level (CPI),

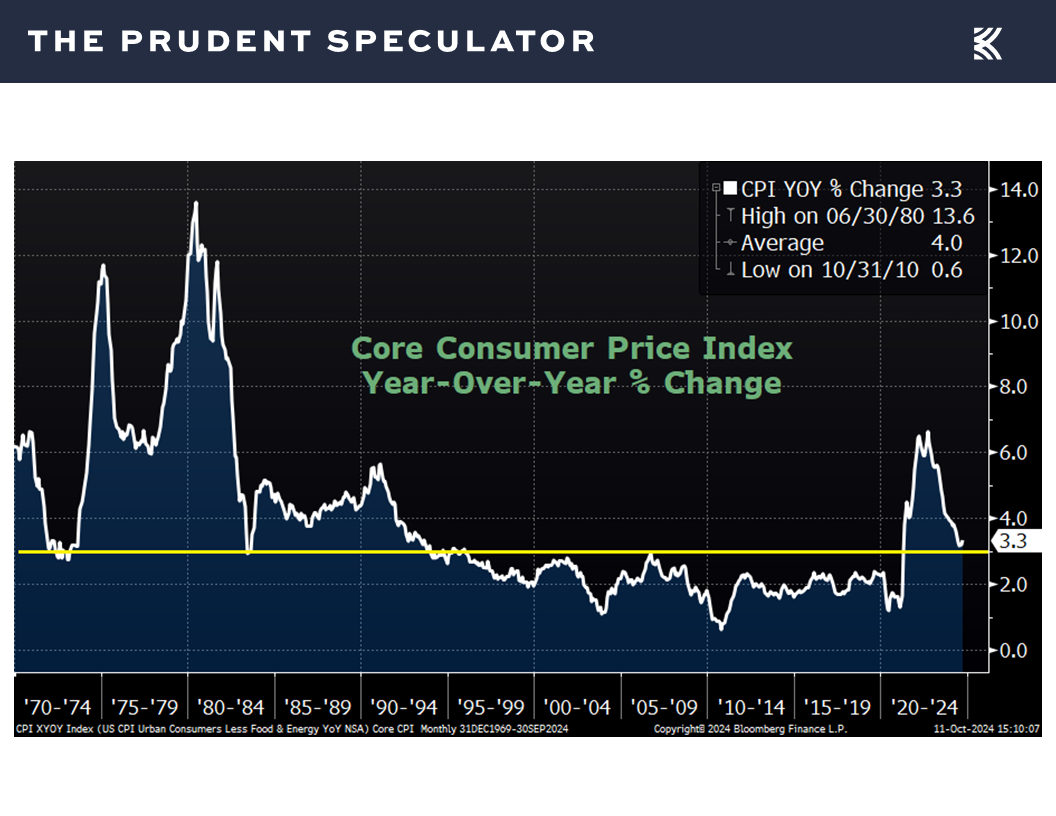

as well as the Core CPI (excludes volatile food and energy prices) rate (3.3% vs. 3.2% est.) last month,

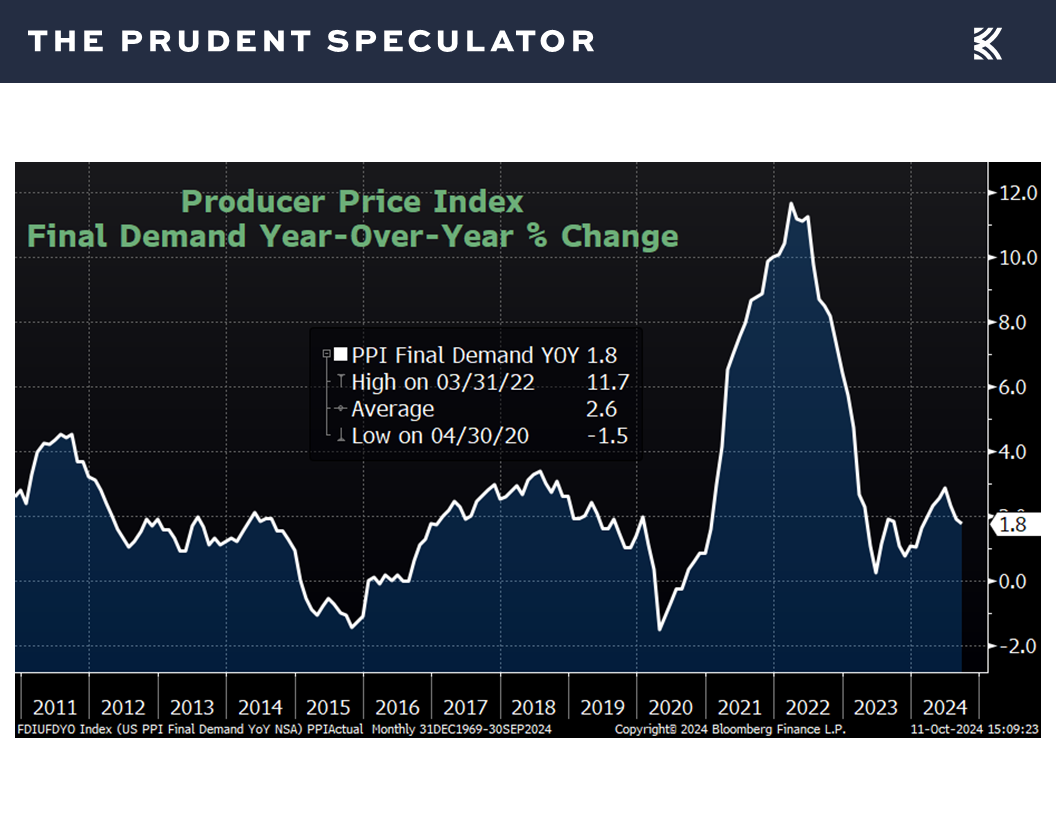

even as inflation at the wholesale level (the Producer Price Index) came in at a relatively low 1.8%.

Still, we don’t think anything we saw last week on the economic front was too much of a surprise and the Fed Funds futures arguably are now more in tune with the most recent projections out last month from the Federal Reserve Board members and Federal Reserve Bank presidents.

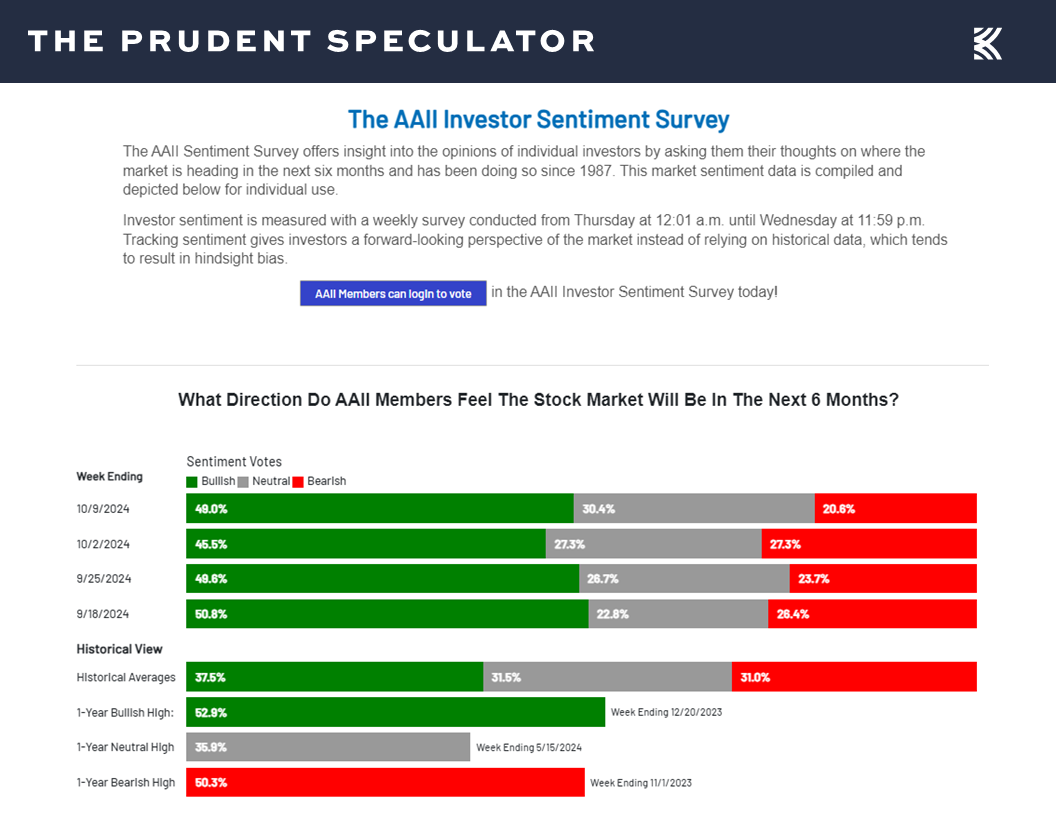

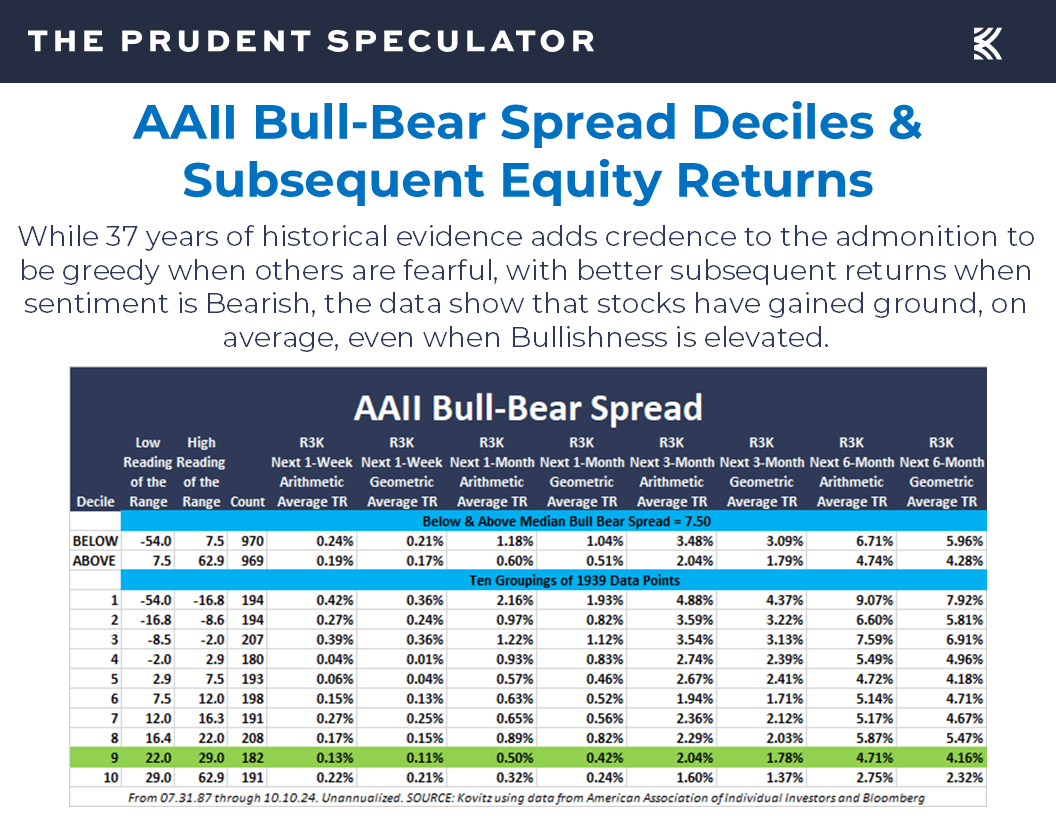

Sentiment – AAII Bullishness Spikes

Certainly, anything can happen as we move forward, and we respect that Bullishness moved markedly higher and Bearishness fell sharply on Main Street last week, which might raise some contrarian eyebrows,

though 37 years of market history for the American Association of Individual Investors sentiment gauge show that being greedy when others are fearful is supported by subsequent return data, while the opposite is not really the case.

Media – Pessimism Still Sells More Newspapers

Still, we were glad to see that the pessimistic song remains the same for the New York Times business columnist that we referenced in this month’s Editor’s Note in The Prudent Speculator. He was at is again this Sunday, this time warning readers that stocks can’t keep rising at this pace for long.

Obviously, stocks will have another trip south at some point, but the challenge is in knowing when that might occur. After all, the supposed experts were suggesting that the odds of recession were 60%+ at the beginning of 2023, and those who went to the sidelines in anticipation of such an event have thus far suffered a massive setback in reaching their long-term investment objectives, given the big equity rally last year and this year.

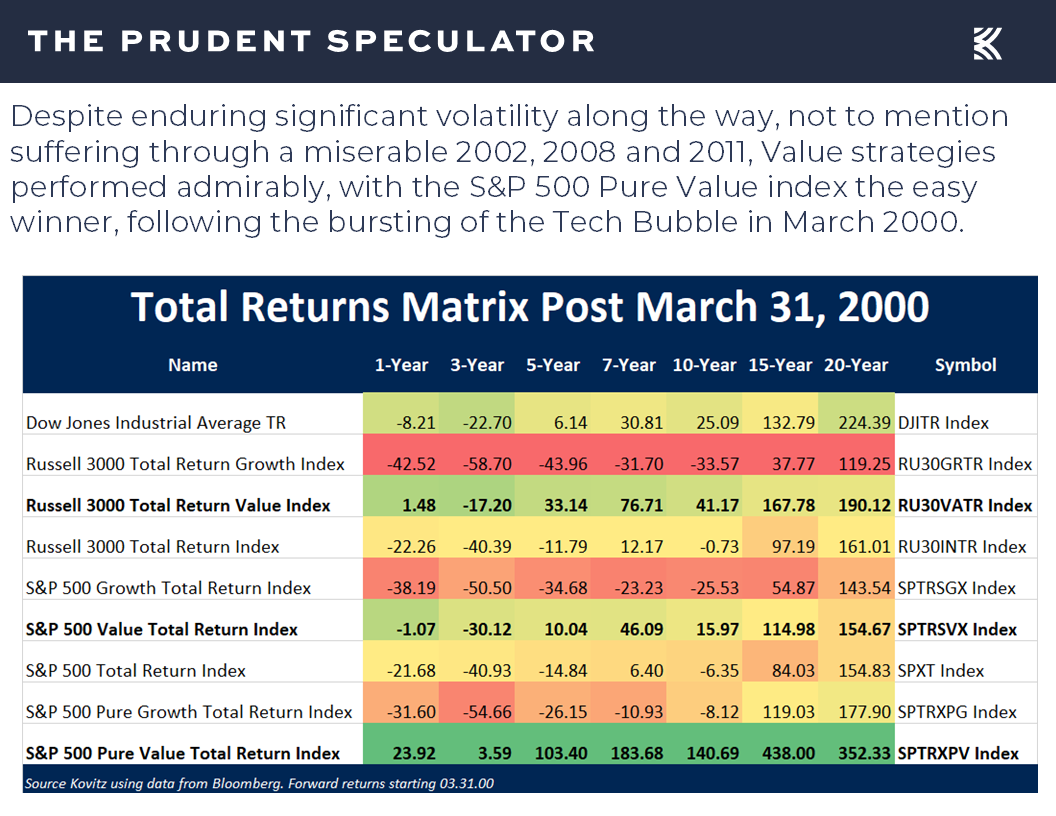

Market of Stocks – Tech Bubble Bursting in 2000 Didn’t Sink All Boats

That does not mean that we expect the recent upside run to continue unabated, especially as we think there are richly valued areas of the market. We also confess that we are running a bit higher cash balance these days at the strategy level for our managed account clients, but our long-term optimism remains intact. This is especially true as it is a market of stocks and not simply a stock market, as was seen when the Tech Bubble referenced in the Times article burst back in 2000.

The author offered a cautionary tale: “The question is whether exuberance is quickly turning from the rational variety to the 1990s irrational version,” Yardeni Research said. Irrational exuberance about the prospects for technology stocks in the late 1990s created a disastrous bubble, which burst in March 2000, and it took years to recover. The S&P 500 had negative returns for the next decade.” Of course, as the table below illustrates, Value performed admirably in the 10 years following the Tech Bubble, even though that decade included 9/11 and the Great Financial Crisis!

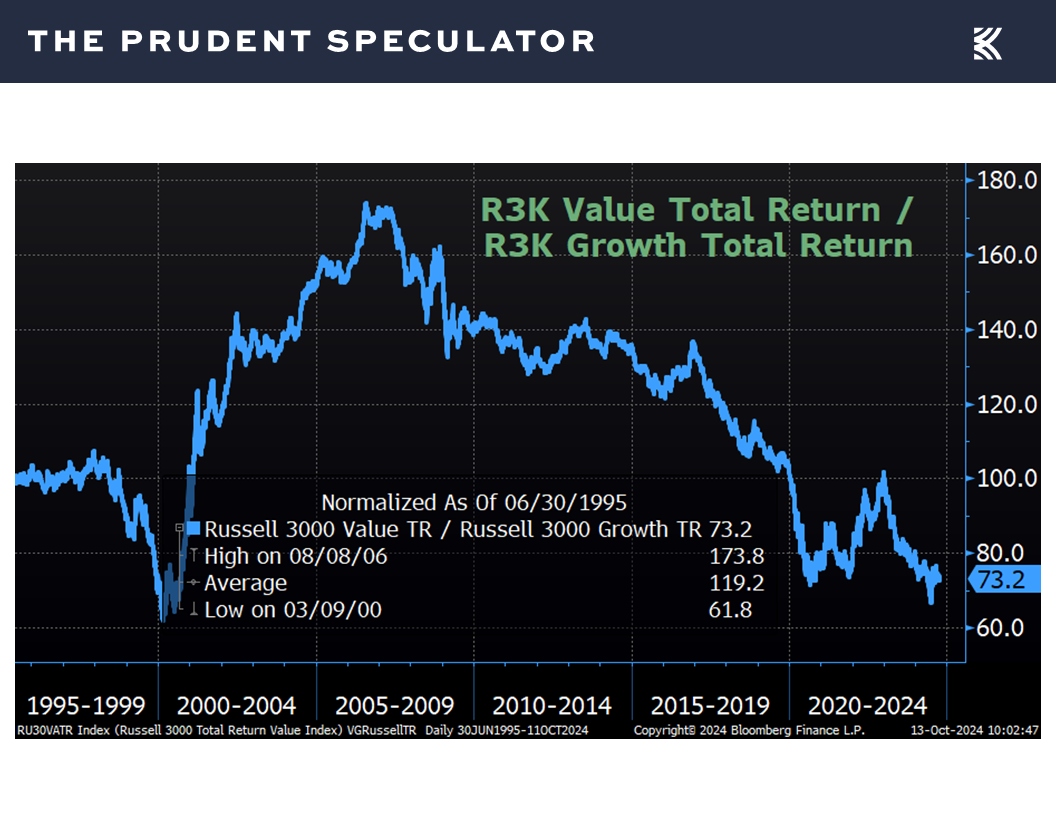

While we concede that we still have a handful of big positions what we believe are more reasonably priced stocks that have graduated into the Growth bucket (Apple, Microsoft, Alphabet, etc.), we think Value in general remains at a very attractive level relative to Growth,

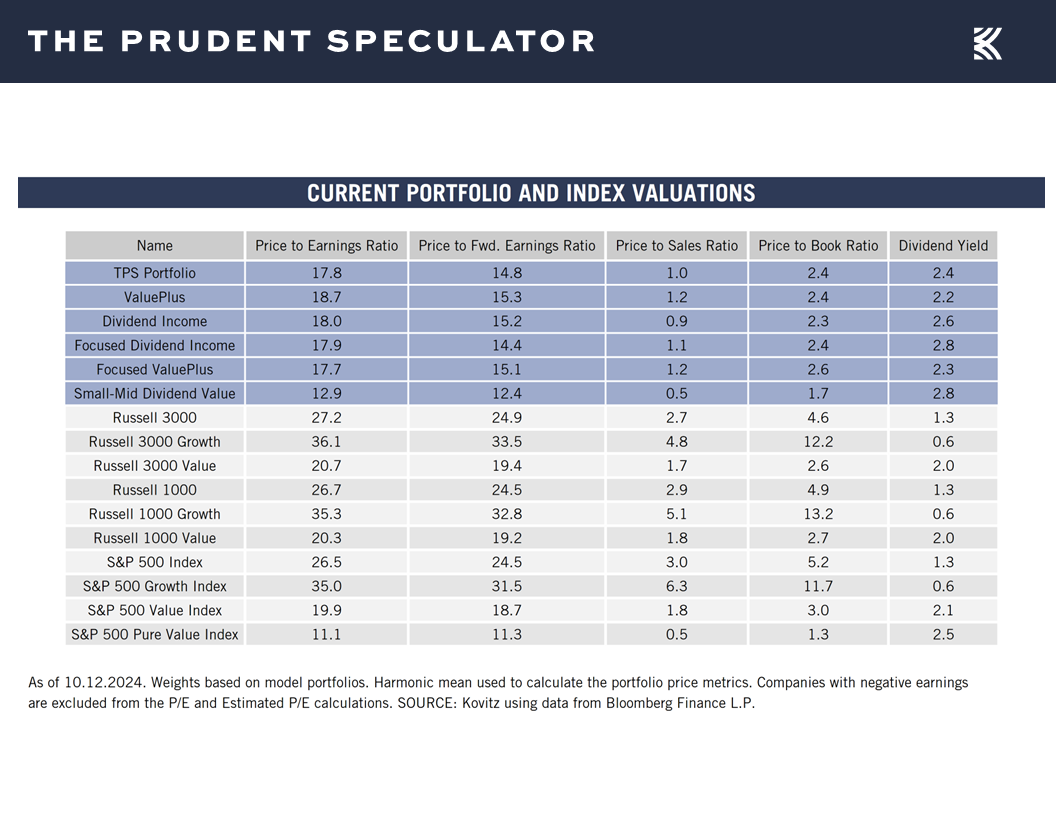

Valuations – Liking our Metrics

and we very much like the overall metrics on our broadly diversified portfolios.

Stock News – Updates on six stocks across four different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Economic Outlook, AAII Sentiment, Interest Rates and Corporate Profits

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Economic Outlook, AAII Sentiment, Interest Rates and Corporate Profits. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Newsletter Portfolio Trades – Sold AYI

Trading Week – Scary Season Rally Continues

Interest Rates – Yields Jump; Stocks Haven’t Minded Historically, on Average

Headwinds – Ups and Downs but Long-Term Trend in Stocks Has Been Higher

Profits – Favorable EPS Outlook

Econ Outlook – Weaker-than-Expected Stats and Higher Inflation, but Numbers In Line with Fed Projections

Sentiment – AAII Bullishness Spikes

Media – Pessimism Still Sells More Newspapers

Market of Stocks – Tech Bubble Bursting in 2000 Didn’t Sink All Boats

Valuations – Liking our Metrics

Stock News – Updates on BLK, BK, JPM, GOOG, APD & PFE

Trading Week – Scary Season Rally Continues

There is still half a month to go, but the historically seasonally weaker two-month September-October time span continued to provide support for our long-held assertion that time in the market trumps market timing as equities managed to again gain ground last week.

The move higher extended the bounce from the September 11 break below 40000 on the popular Dow Jones Industrial Average to more than 2800 points and pushed the advance since the start of the supposedly scary period to more than 1300 points, or 3.31%, not counting dividends.

Interest Rates – Yields Jump; Stocks Haven’t Minded Historically, on Average

Interestingly, the 1%+ rally over the last five trading sessions came despite another big jump in interest rates, with the yield on the benchmark 10-Year U.S. Treasury climbing from 3.97% to 4.10%.

Headwinds – Ups and Downs but Long-Term Trend in Stocks Has Been Higher

Of course, students of market history know very well that stocks have performed fine, on average, whether interest rates are rising or falling,

just as they understand that disconcerting events on the global stage, such as Arab-Israeli conflicts, also are not reason to alter a long-term commitment to equities.

No doubt, it is easier with the major market averages at all-time highs to buy the argument that sticking with stocks through thick and thin is the way to go, but we never forget that downside volatility is always part of the investment process. Indeed, even as Value Stocks, like those we have long championed, have enjoyed an average annualized rate of return of 14.0% since the launch of The Prudent Speculator in March 1977, there have been numerous downturns along the way, with 5% setbacks taking place three times per year on average and 10% corrections happening every 11 months or so.

Profits – Favorable EPS Outlook

To be sure, the long-term trend has been up, as companies become more valuable over time as corporate profits have marched steadily higher, aside from a few interruptions generally associated with recessions.

Econ Outlook – Weaker-than-Expected Stats and Higher Inflation, but Numbers In Line with Fed Projections

The health of the economy is thus super important for the prospects for stocks, so some might have been surprised that the markets continued to move north last week, given that the NFIB Small Business Optimism index for September came in at a weaker-than-expected 91.5,

first-time filings for unemployment benefits in the latest week jumped to a much-high-than-forecast tally of 258,000,

and the University of Michigan’s preliminary Consumer Sentiment reading for October fell to 68.9, below estimates of 71.0 and down from the final September figure of 70.1.

Of course, the latest forecast for real (inflation-adjusted) U.S. GDP growth for Q3 from the Atlanta Fed was a healthy 3.2%,

while the Fed Funds futures market saw wagers that the Fed will be less aggressive, not more aggressive, in cutting interest rate to support the economy, with the year-end ’24 and year-end ’25 betting now standing at a yield of 4.37% and 3.34%, respectively, up from 4.28% and 3.29% a week ago.

True, the odds of Jerome H. Powell & Co. being more patient in further reducing rates were also influenced by a slightly higher-than-expected print (2.4% vs. 2.3% est.) for September on inflation at the consumer level (CPI),

as well as the Core CPI (excludes volatile food and energy prices) rate (3.3% vs. 3.2% est.) last month,

even as inflation at the wholesale level (the Producer Price Index) came in at a relatively low 1.8%.

Still, we don’t think anything we saw last week on the economic front was too much of a surprise and the Fed Funds futures arguably are now more in tune with the most recent projections out last month from the Federal Reserve Board members and Federal Reserve Bank presidents.

Sentiment – AAII Bullishness Spikes

Certainly, anything can happen as we move forward, and we respect that Bullishness moved markedly higher and Bearishness fell sharply on Main Street last week, which might raise some contrarian eyebrows,

though 37 years of market history for the American Association of Individual Investors sentiment gauge show that being greedy when others are fearful is supported by subsequent return data, while the opposite is not really the case.

Media – Pessimism Still Sells More Newspapers

Still, we were glad to see that the pessimistic song remains the same for the New York Times business columnist that we referenced in this month’s Editor’s Note in The Prudent Speculator. He was at is again this Sunday, this time warning readers that stocks can’t keep rising at this pace for long.

Obviously, stocks will have another trip south at some point, but the challenge is in knowing when that might occur. After all, the supposed experts were suggesting that the odds of recession were 60%+ at the beginning of 2023, and those who went to the sidelines in anticipation of such an event have thus far suffered a massive setback in reaching their long-term investment objectives, given the big equity rally last year and this year.

Market of Stocks – Tech Bubble Bursting in 2000 Didn’t Sink All Boats

That does not mean that we expect the recent upside run to continue unabated, especially as we think there are richly valued areas of the market. We also confess that we are running a bit higher cash balance these days at the strategy level for our managed account clients, but our long-term optimism remains intact. This is especially true as it is a market of stocks and not simply a stock market, as was seen when the Tech Bubble referenced in the Times article burst back in 2000.

The author offered a cautionary tale: “The question is whether exuberance is quickly turning from the rational variety to the 1990s irrational version,” Yardeni Research said. Irrational exuberance about the prospects for technology stocks in the late 1990s created a disastrous bubble, which burst in March 2000, and it took years to recover. The S&P 500 had negative returns for the next decade.” Of course, as the table below illustrates, Value performed admirably in the 10 years following the Tech Bubble, even though that decade included 9/11 and the Great Financial Crisis!

While we concede that we still have a handful of big positions what we believe are more reasonably priced stocks that have graduated into the Growth bucket (Apple, Microsoft, Alphabet, etc.), we think Value in general remains at a very attractive level relative to Growth,

Valuations – Liking our Metrics

and we very much like the overall metrics on our broadly diversified portfolios.

Stock News – Updates on six stocks across four different sectors

About the Author

Phil Edwards

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.