The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Middle East, Inflation, Economic News, and Corporate Profits. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Week in Review – Stocks Retreat Again

Volatility – Normal Part of the Equity Process

Middle East – Perspective on Geopolitical Events

Inflation – CPI Higher and PPI Lower than Expected

Interest Rates – 10-Year Yield Jumps

History Lessons – Stocks Haven’t Minded Rising Inflation or Rising Rates, on Average

Econ News – Labor Market Strong; GDP Solid; Sentiment Weakens

Corporate Profits – Healthy EPS Growth Projected for ’24 and ’25

Valuations – Value Stocks Still Attractively Priced

Stock News – Updates on three stocks in the financial sector

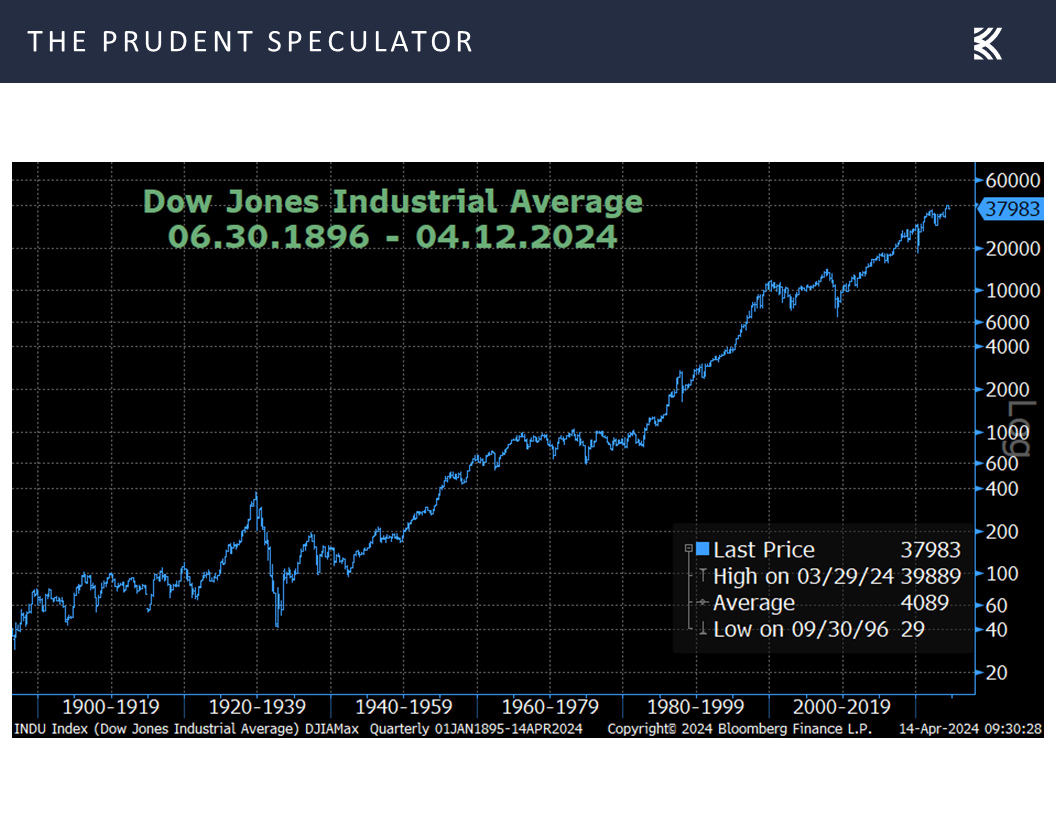

Week in Review – Stocks Retreat Again

With the Dow Jones Industrial Average enduring two days last week of losses of more than 400 points and the popular index ending the five days with a more-than-900-point skid, the equity markets offered yet another reminder that short-term setbacks are always part of the equation. Of course, a simple price chart (ignores dividends and the impact of their reinvestment) shows that the long-term trend in the Dow has been markedly higher.

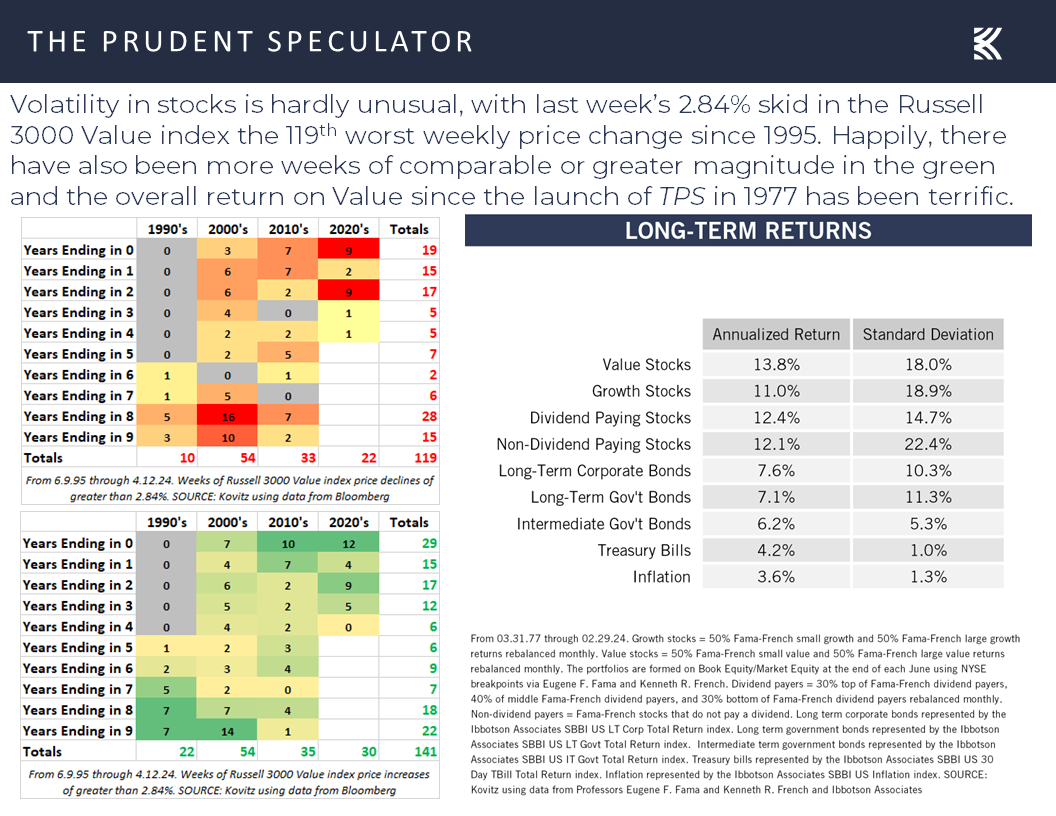

Volatility – Normal Part of the Equity Process

Alas, the Russell 3000 Value index suffered an even steeper percentage decline than the Dow last week with a loss of 2.84%. Believe it or not, this marked the 119th worst week since the formation of that benchmark in 1995, so 118 weeks were worse over the past 29 years. Happily, there have been 141 weeks where the gains have been 2.84% or greater during the same nearly three-decade period, and the overall return for Value stocks since the launch of The Prudent Speculator more than 47 years ago has been an excellent 13.8% per annum.

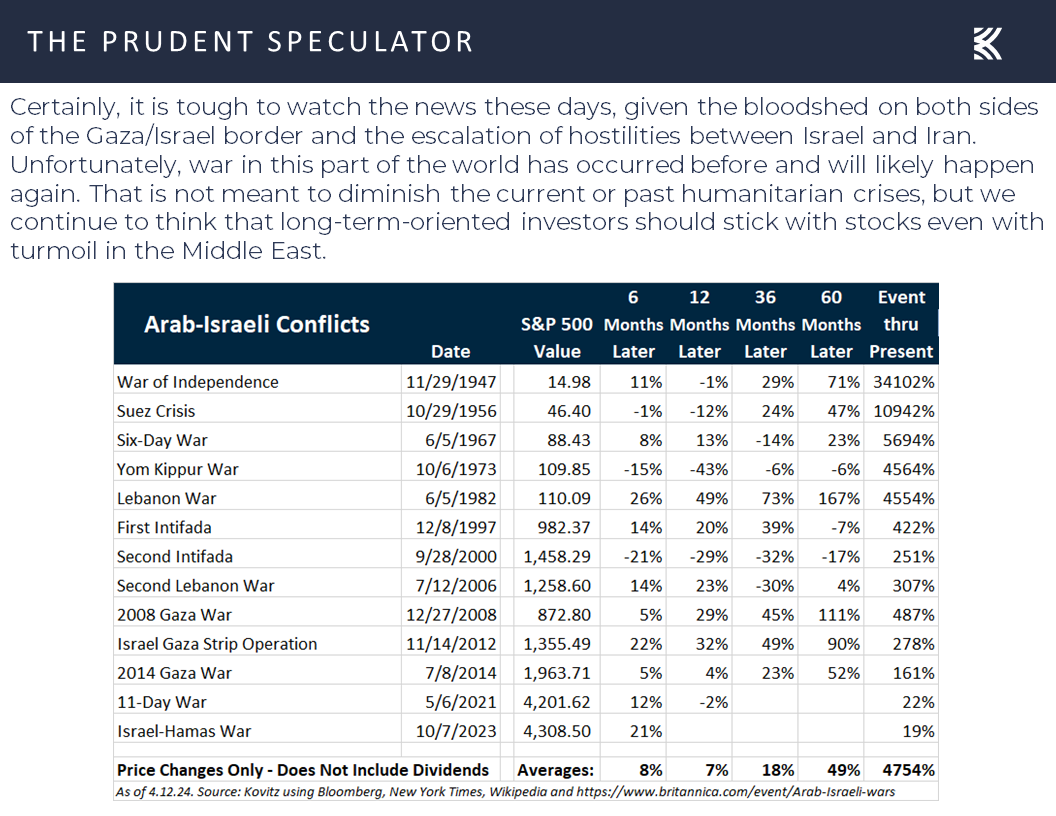

Middle East – Perspective on Geopolitical Events

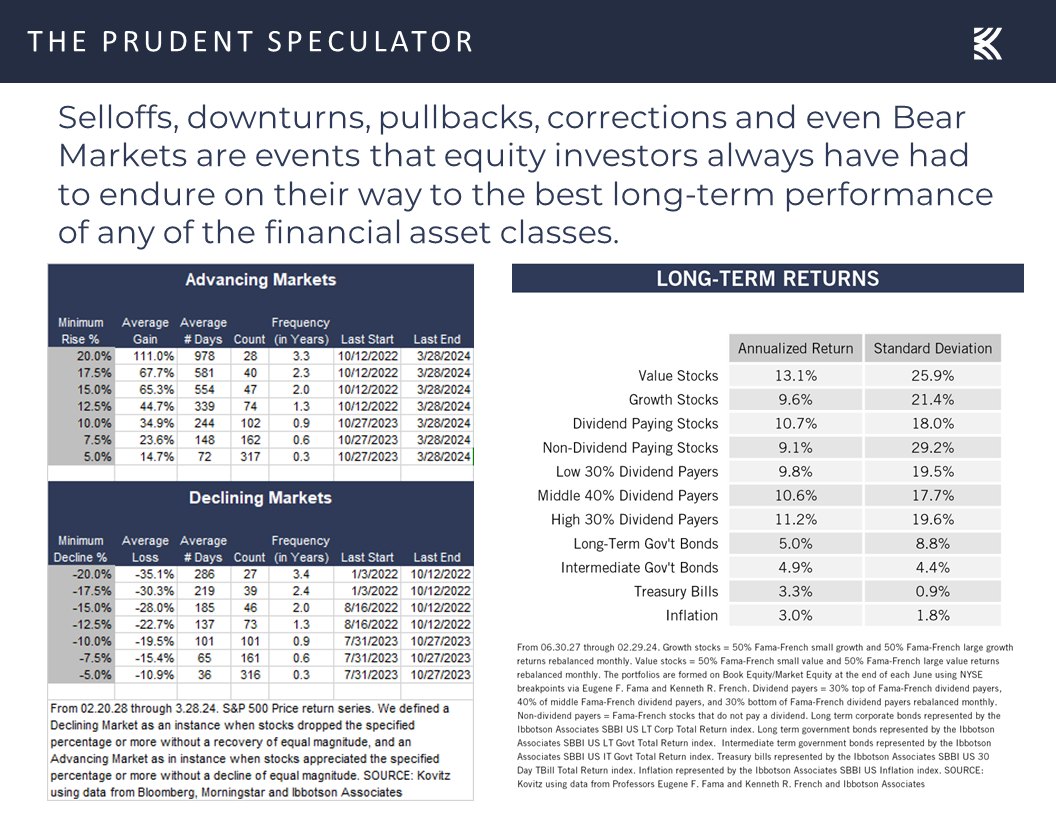

Volatility is very much par for the course as looking at the S&P 500 going all the way back to 1928, there have been 5% or greater drops without a gain of equal magnitude three times a year on average, while corrections of 10% have happened every 11 months on average and 20% Bear Markets have occurred every 3.4 years on average. And, despite those trips south, the overall return on Value stocks has been 13.1% per annum going back more than nine decades.

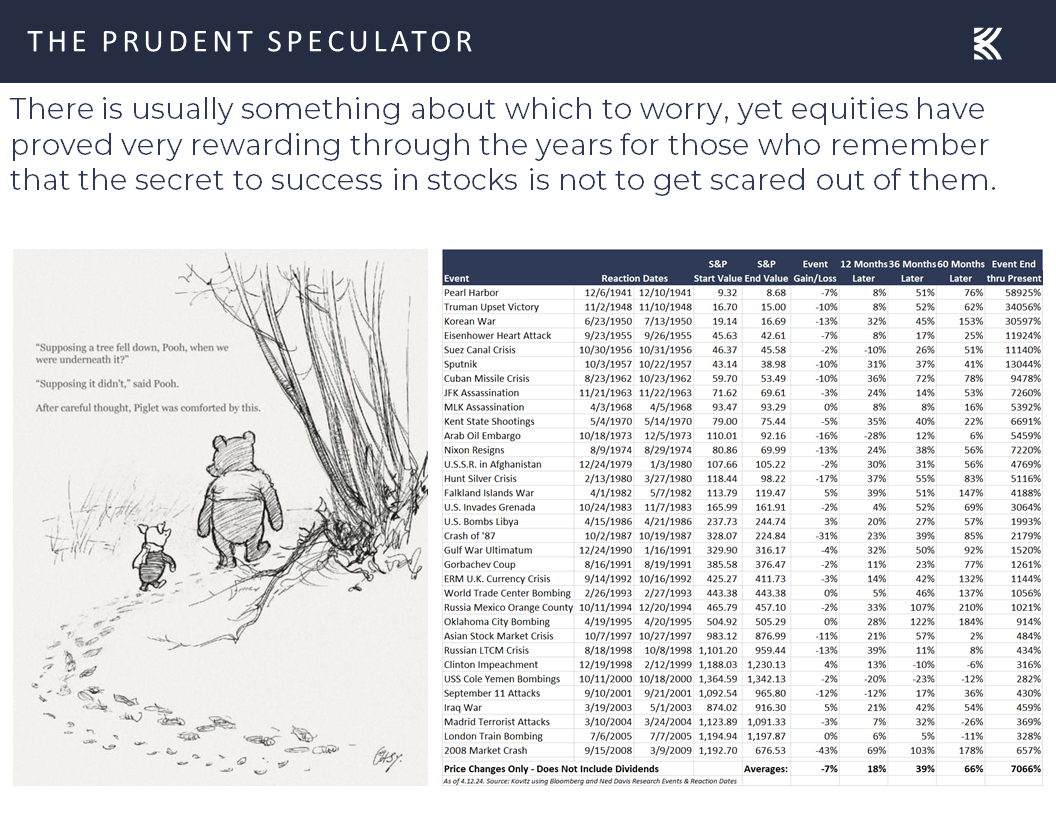

No doubt, there have been plenty of disconcerting events on the geopolitical stage along the way with which long-term-oriented investors have had to contend, including more than a few Arab-Israeli conflicts and Saturday’s launch of a drone and missile attack on Israel by Iran adds to the risk of a dangerous escalation cycle in the Middle East.

While the method of the so-called retaliatory attack (from Iranian soil) was a surprise, the plunge in stock prices on Friday had a lot to do with news that an Iranian strike on Israel was imminent, so the U.S. equity market futures on Sunday evening were suggesting that some traders sold the rumor last week and may now be buying the news as the new week begins.

Time will tell if cooler heads prevail as the Iranian attack thus far was more bark than bite and the Israeli missile defense systems with help, evidently, from the U.S., U.K. and France, managed to shoot down or neutralize some 300 projectiles. It is hard to believe that Israel will not respond in some fashion, but history shows that every near-term stock market setback has been overcome in the fullness of time, including conflagrations that have directly involved the United States. So, while we must be braced for additional downside volatility, as Israel’s War Cabinet Minister Benny Gantz said his country would “exact a price from Iran in a way and time that suits us,” we are planning no changes to our portfolios due to this past weekend’s developments.

Inflation – CPI Higher and PPI Lower than Expected

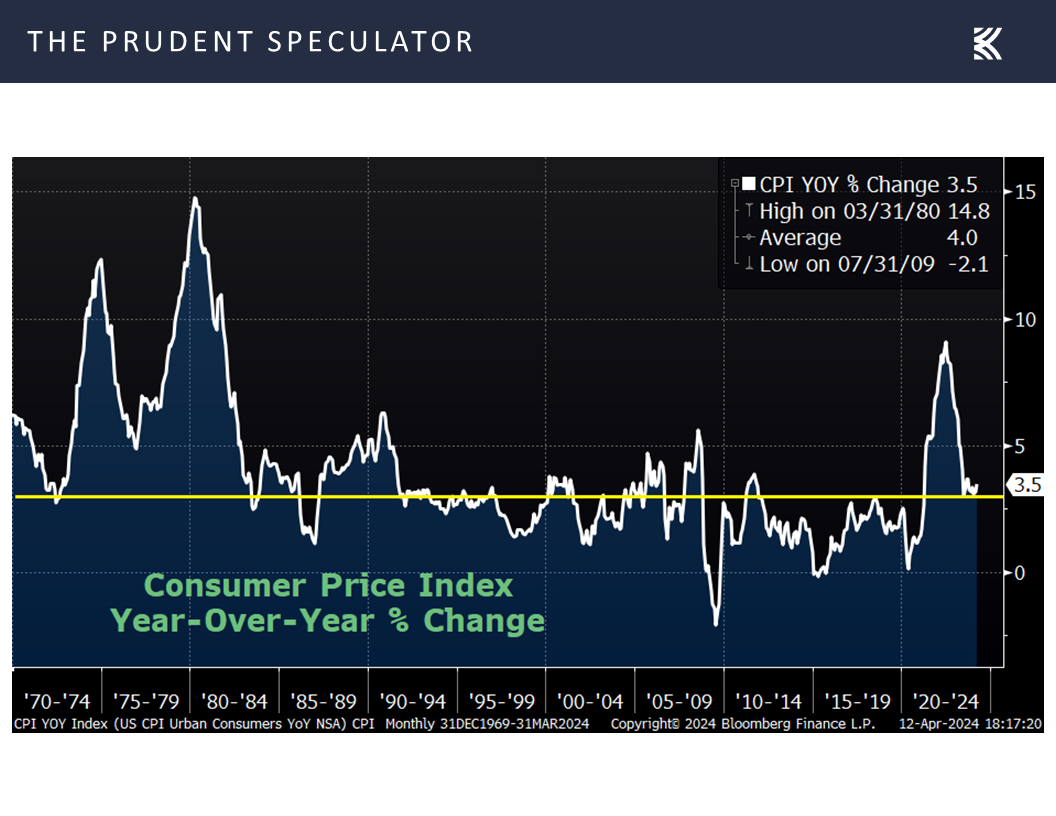

To be sure, unrest in the Middle East was not the only issue troubling traders last week as inflation at the consumer level for March came in higher than expected with the full Consumer Price Index (CPI) rising 3.5% (est. 3.4%) on a year-over-year basis,

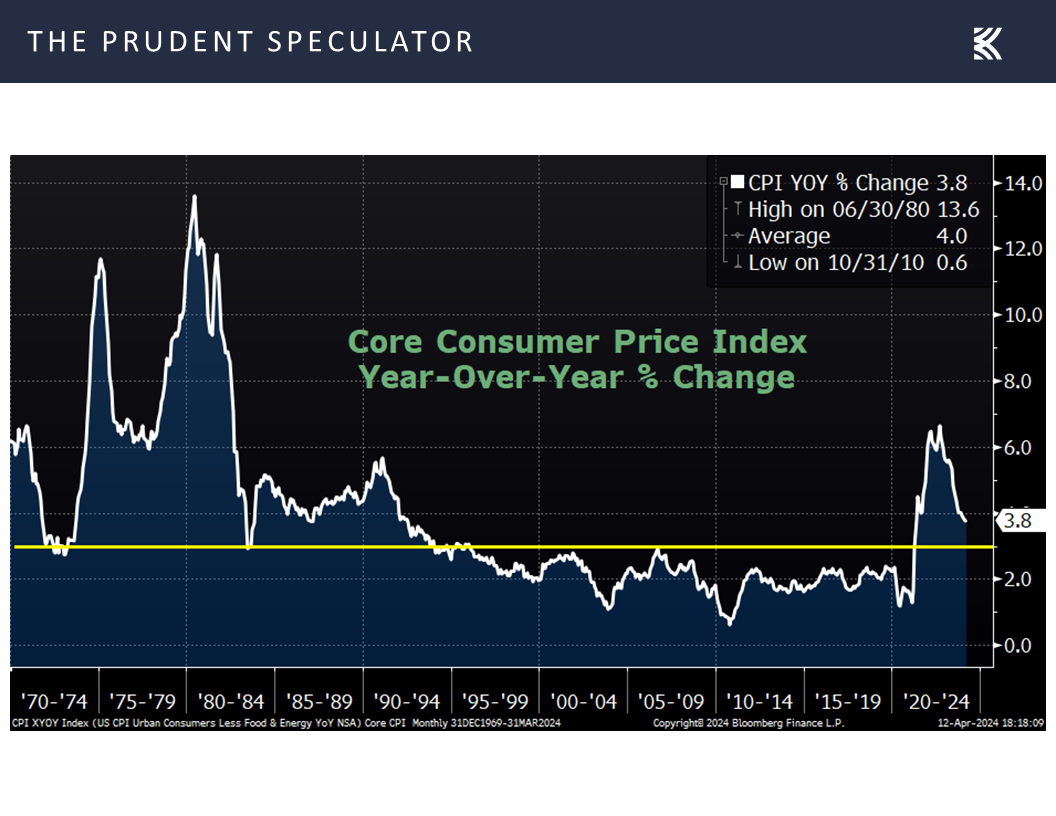

and the core CPI (excludes volatile food and energy prices) climbing 3.8% (est. 3.7%).

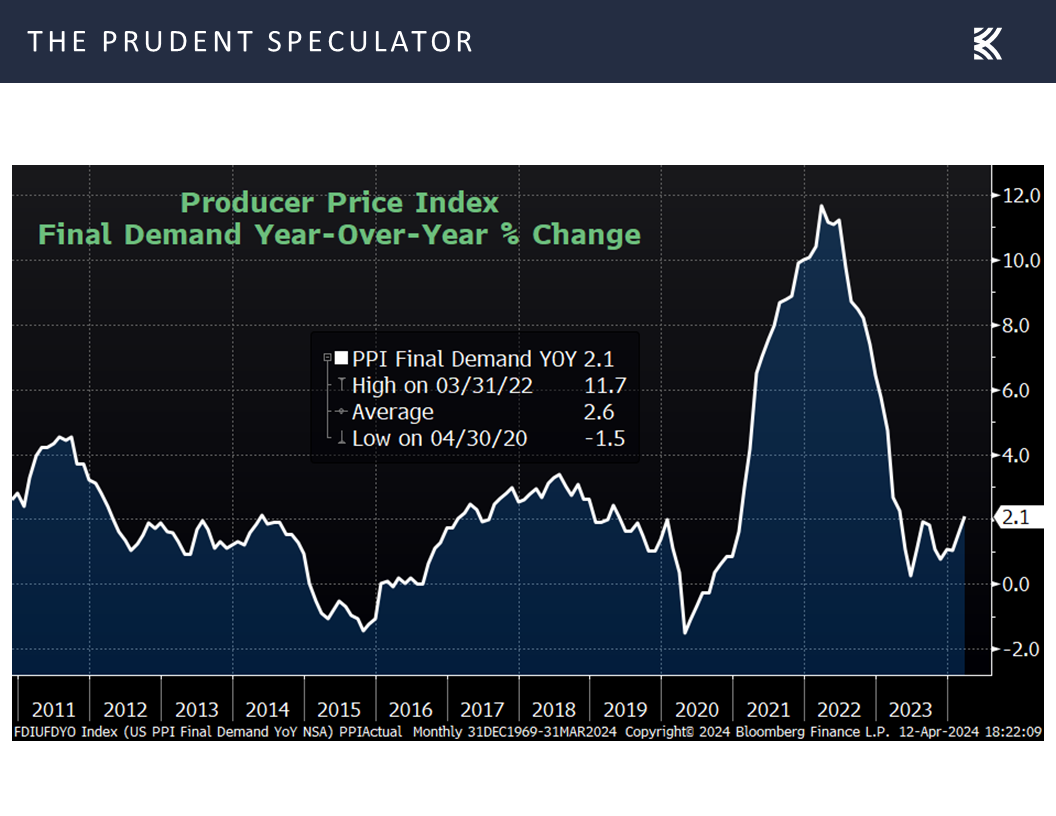

Countering those inflation worries somewhat, the rise in prices at the wholesale level in March came in lower than expected with the Producer Price Index advancing 2.1% (est. 2.2%), though the increase was up from 1.6% in February,

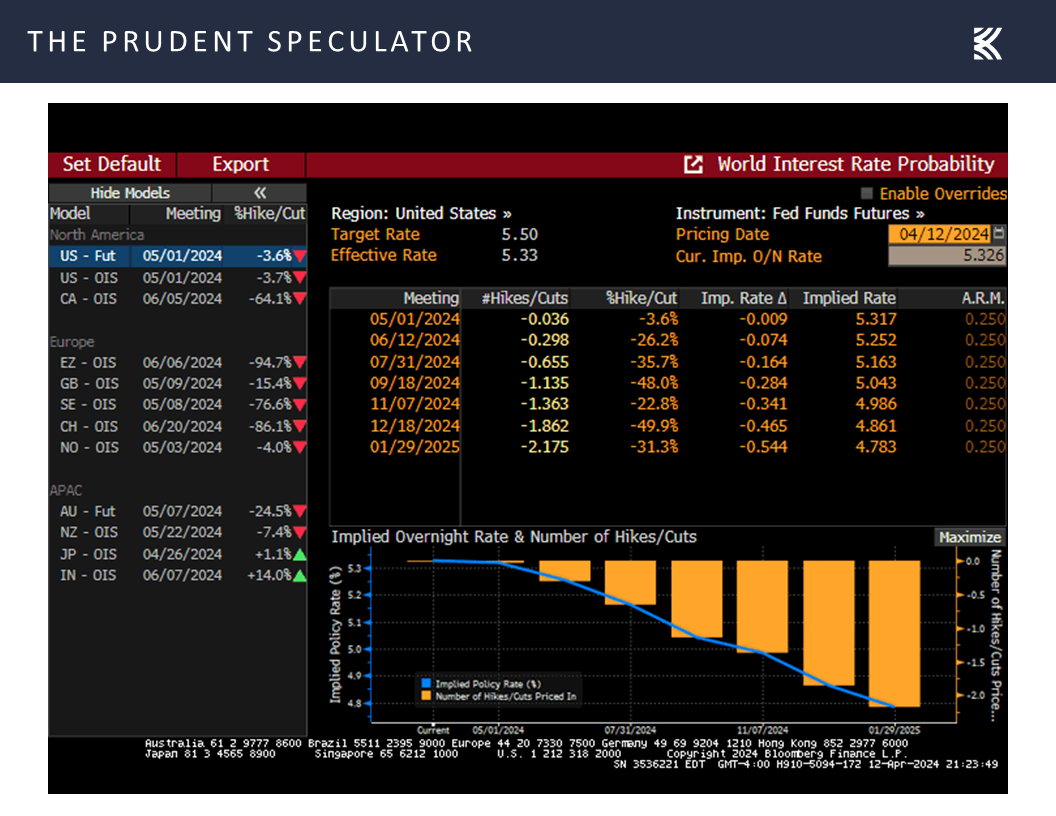

and the betting odds in the futures market saw a big jump in the projected year-end 2024 Fed Funds rate to 4.86%, up from 4.68% at the end of the preceding week.

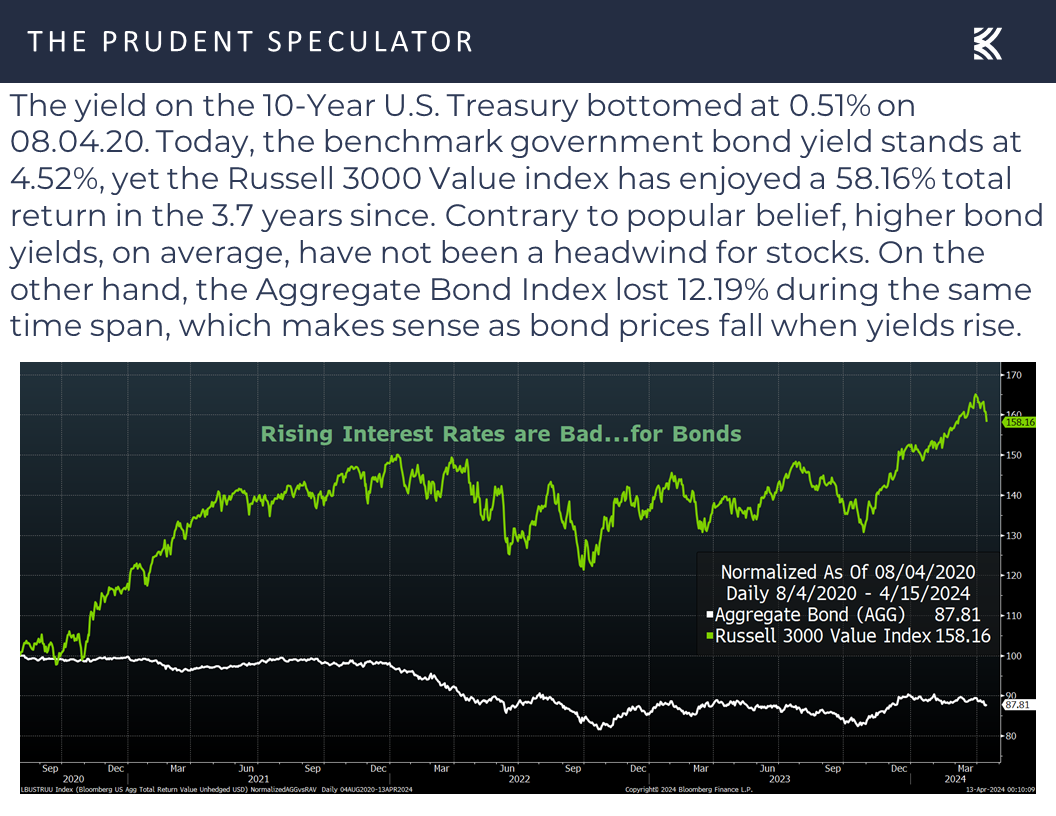

Interest Rates – 10-Year Yield Jumps

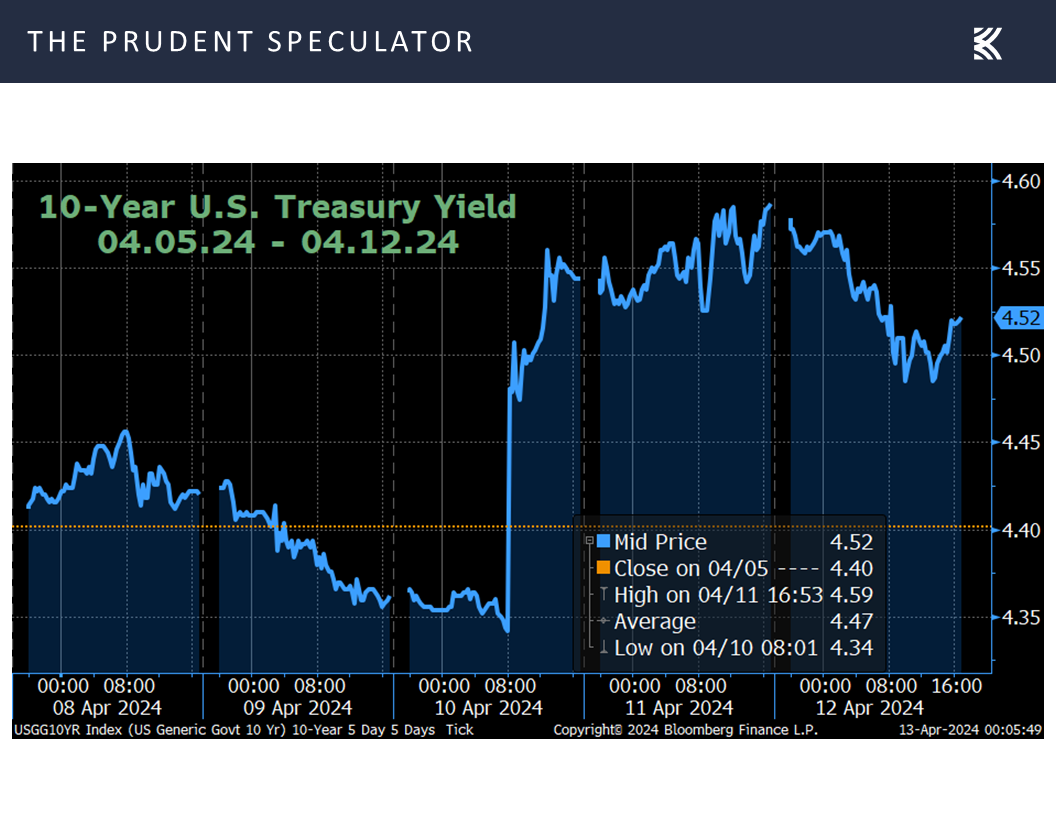

while the yield on the benchmark U.S. 10-Year Treasury bond jumped to 4.52%, up from 4.40% the week prior.

History Lessons – Stocks Haven’t Minded Rising Inflation or Rising Rates, on Average

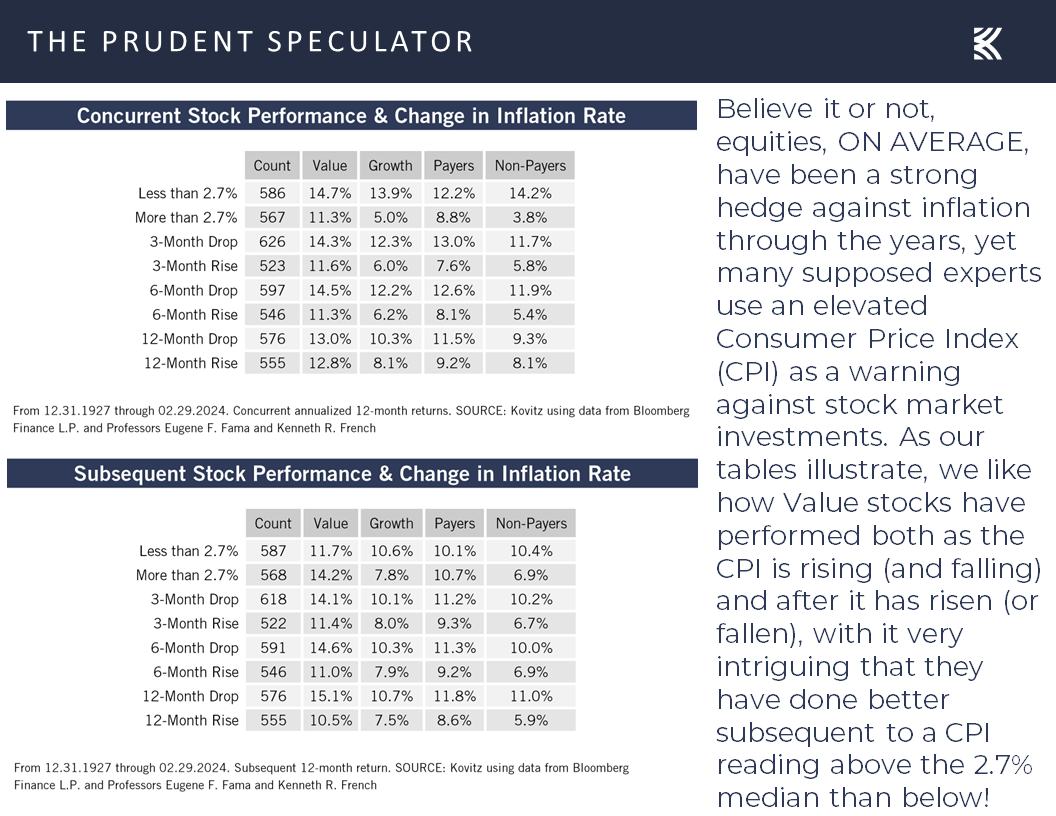

Obviously, many traders have been betting on Fed rate cuts and lower bond yields, so the knee-jerk reaction was to sell stocks last week, even as history shows that equities have proved rewarding, on average, whether inflation is rising or falling or whether it is high or low,

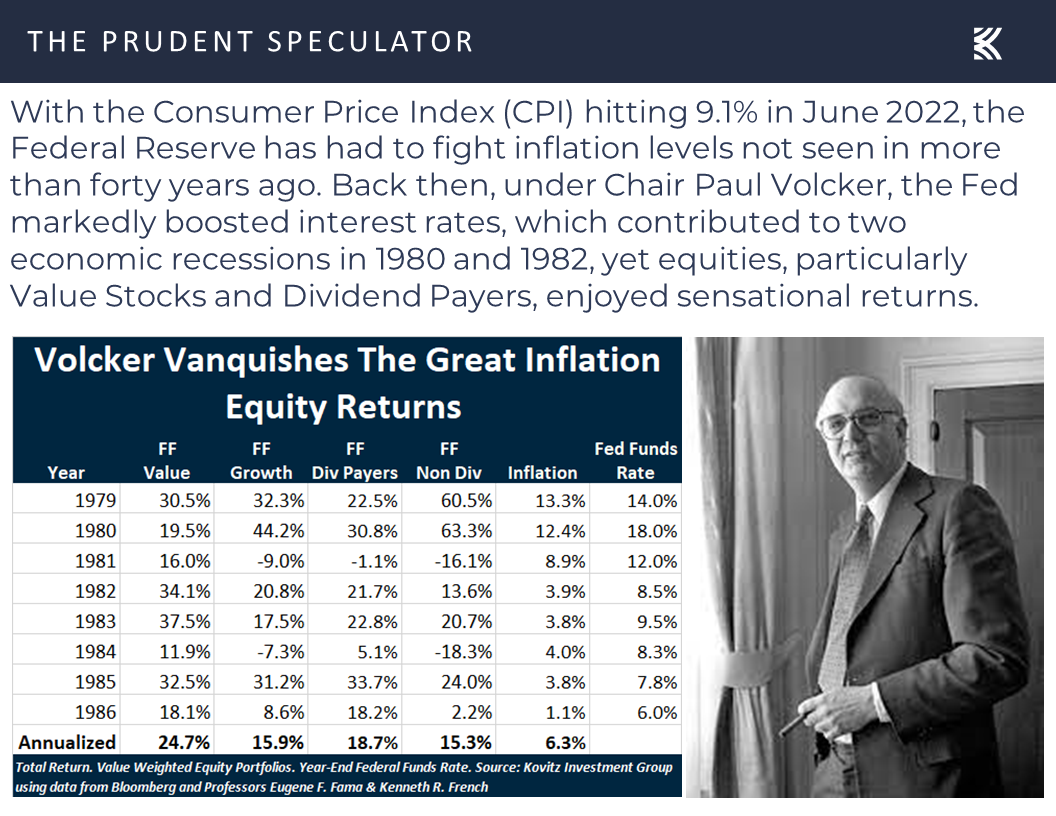

while the last major Fed battle to contain prices resulted in extraordinary stock-price gains (24.7% per annum for Value from 1978 to 1986), even with two recessions also in the mix!

Further, we note that rising Treasury yields in the fullness of time historically have proved only to be bad…for bonds!

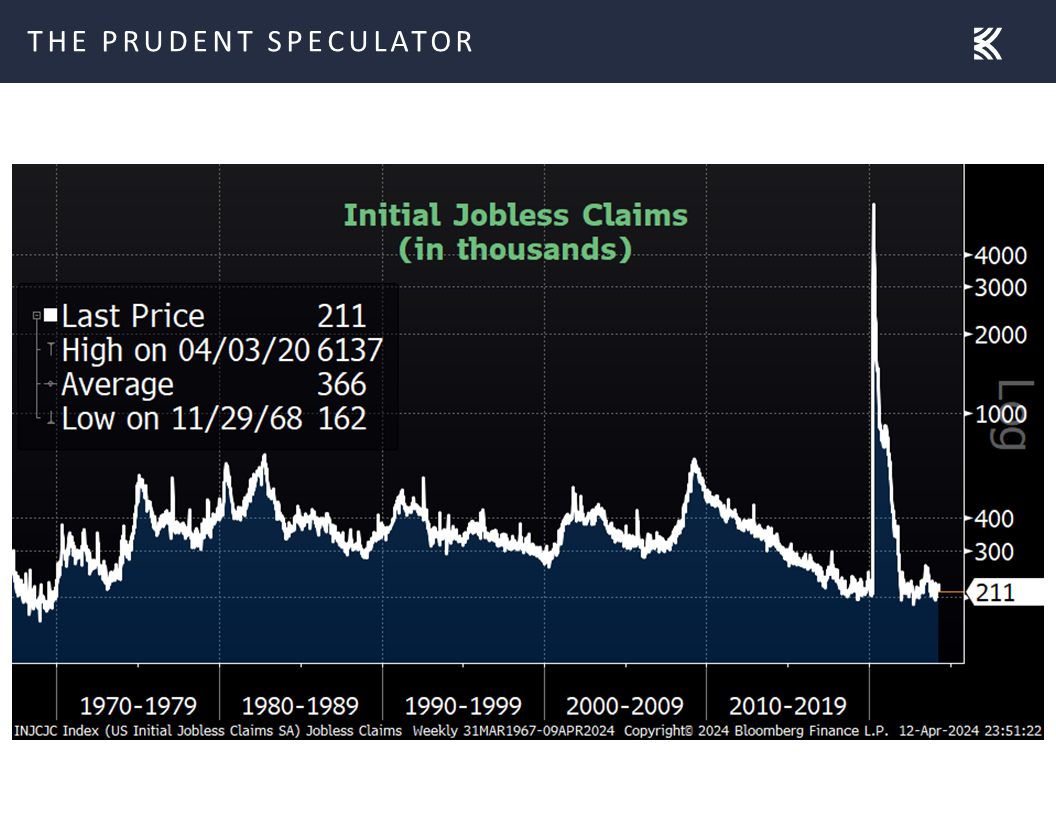

Econ News – Labor Market Strong; GDP Solid; Sentiment Weakens

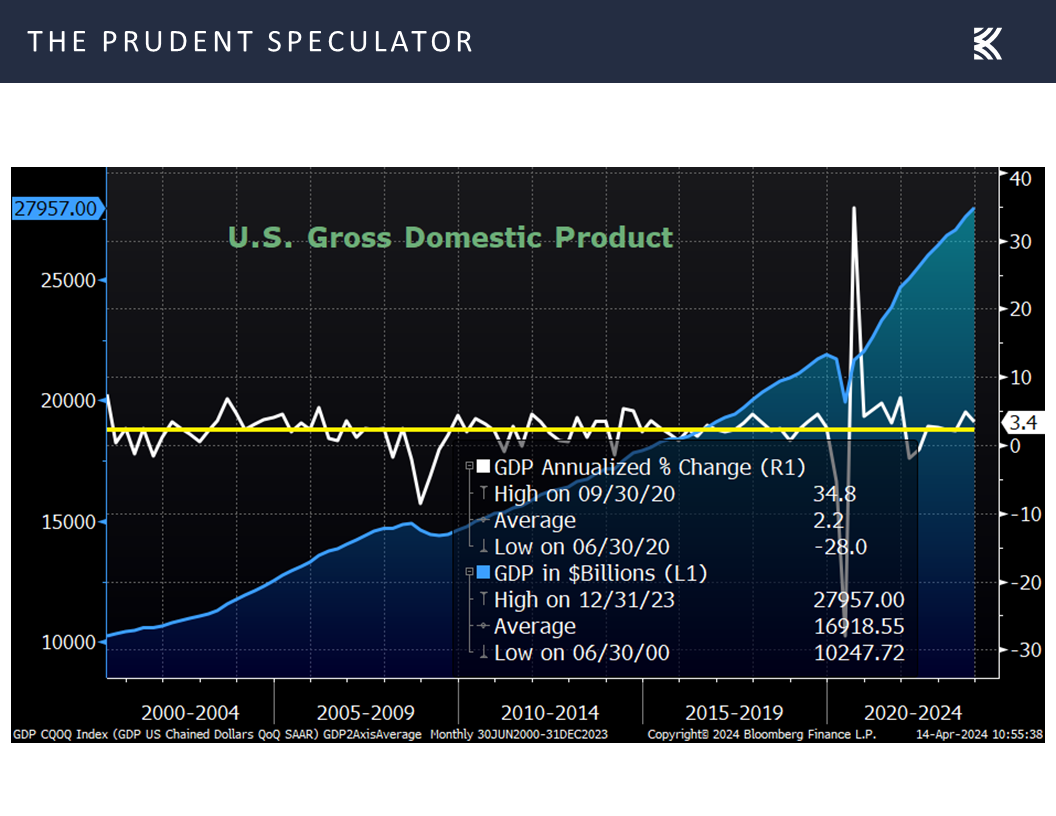

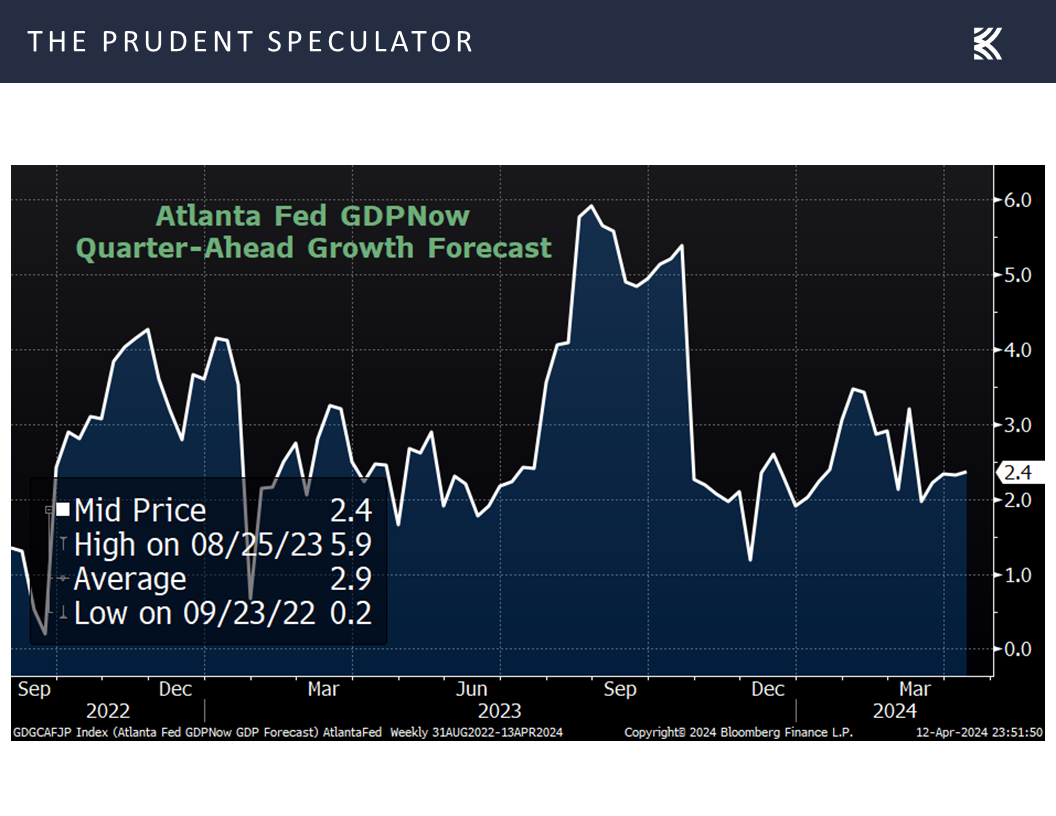

Certainly, we realize that the major U.S. equity market indexes across the board have rallied significantly off the October lows, so there is some good news baked into prices. The economy has proved more resilient than most had projected, with the labor market remaining very robust,

GDP growth last year exceeding expectations, with a 3.4% real (inflation-adjusted) rate of growth in Q4 2023

and a 2.4% rate of growth currently predicted for Q1 2024,

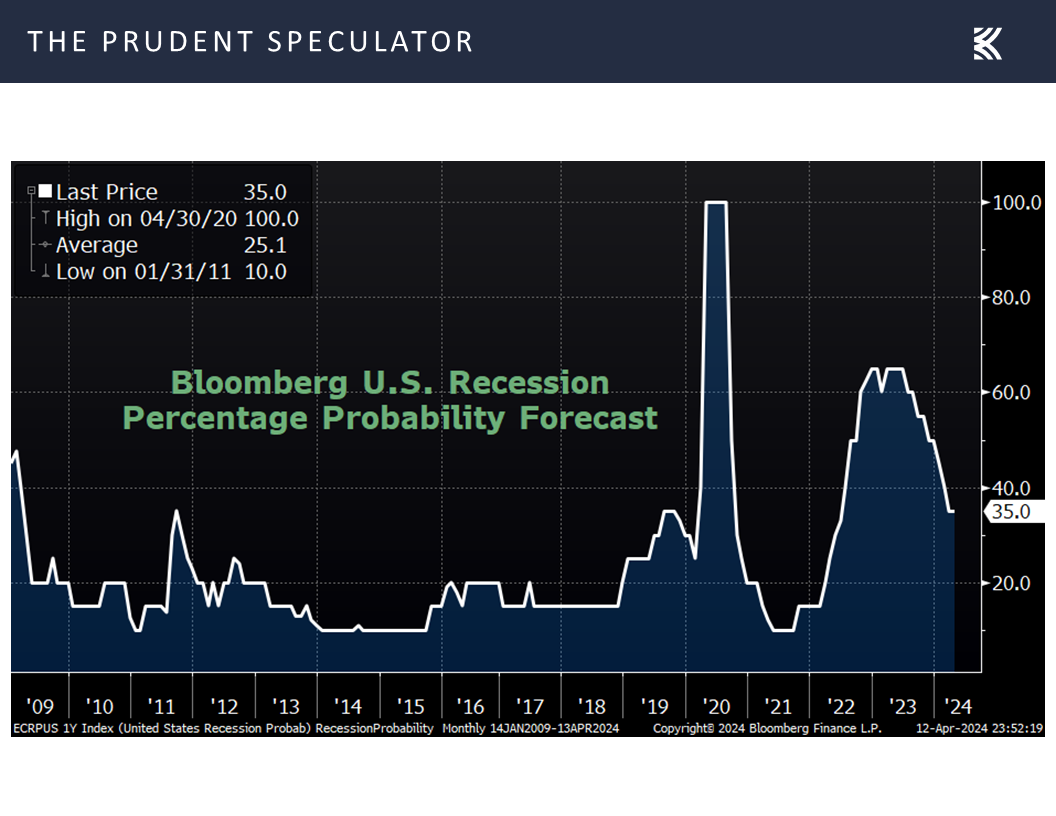

while the chance of recession in the next 12 months, per calculations from data provider Bloomberg, now stand at 35%, down from 55% just six months ago,

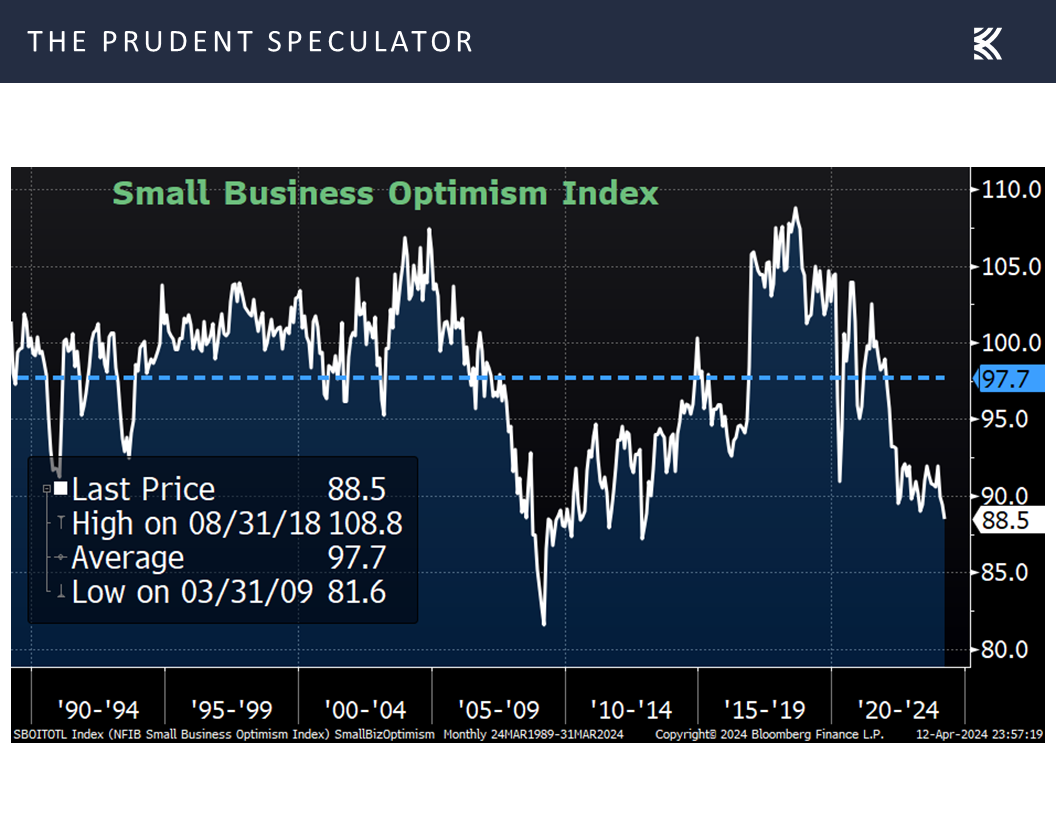

There can be no assurance that the economy will continue to hold up, and we note that reports last week on Small Business Optimism for March,

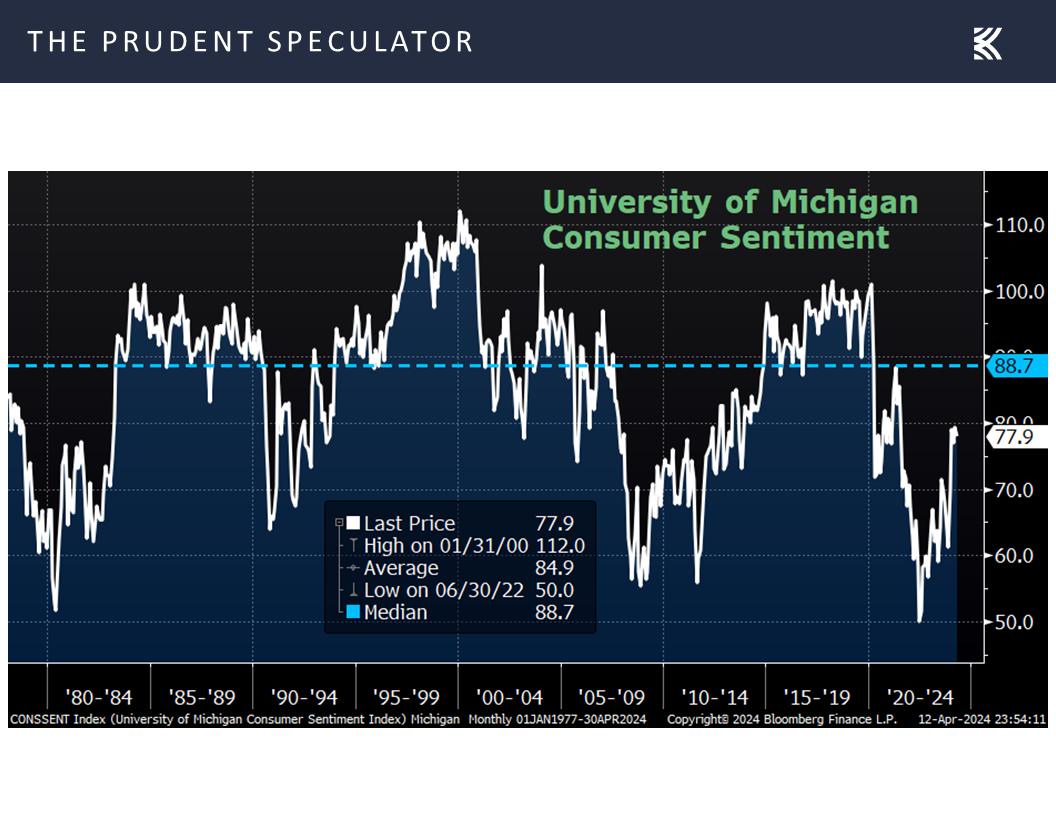

and confidence on Main Street for April both were weaker-than-expected,

Corporate Profits – Healthy EPS Growth Projected for ’24 and ’25

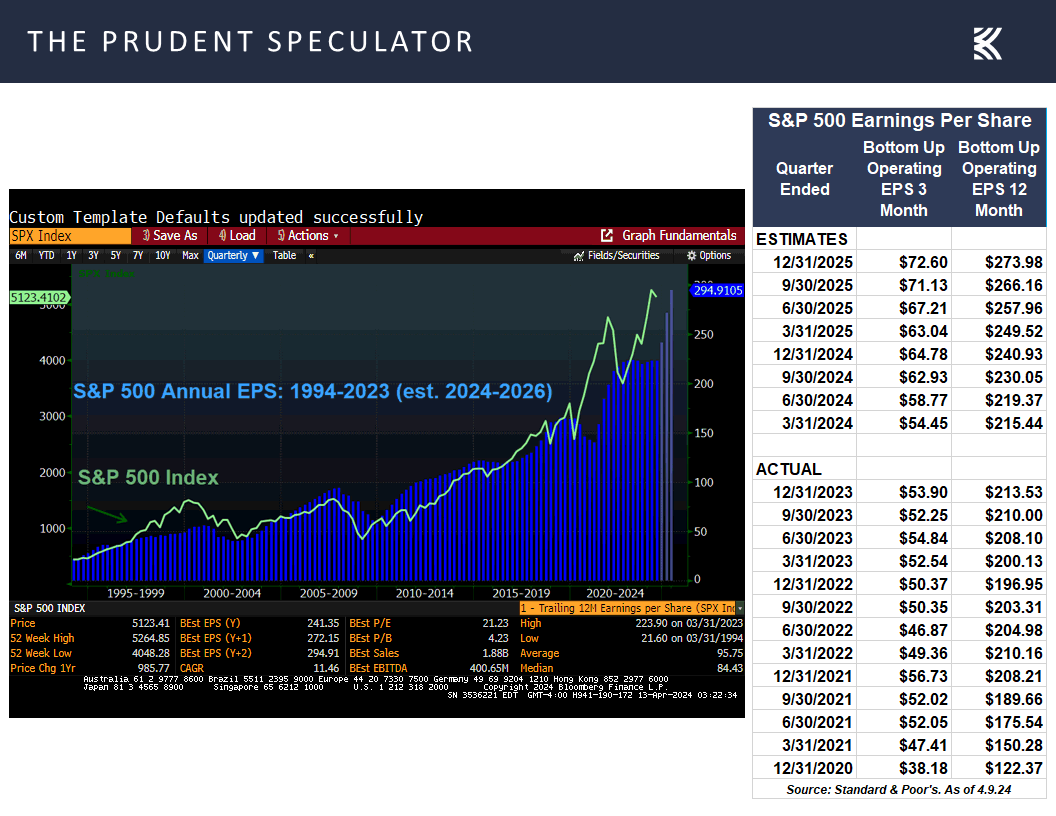

but the outlook for corporate profit growth this year and next remains very favorable,

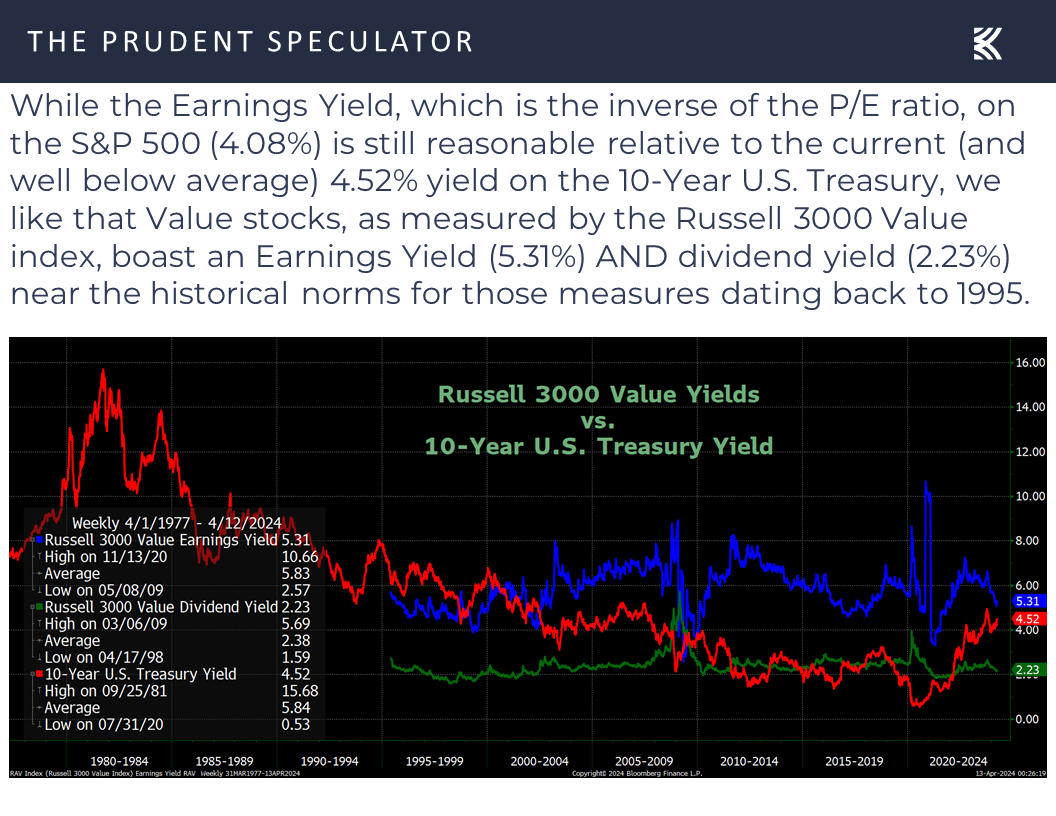

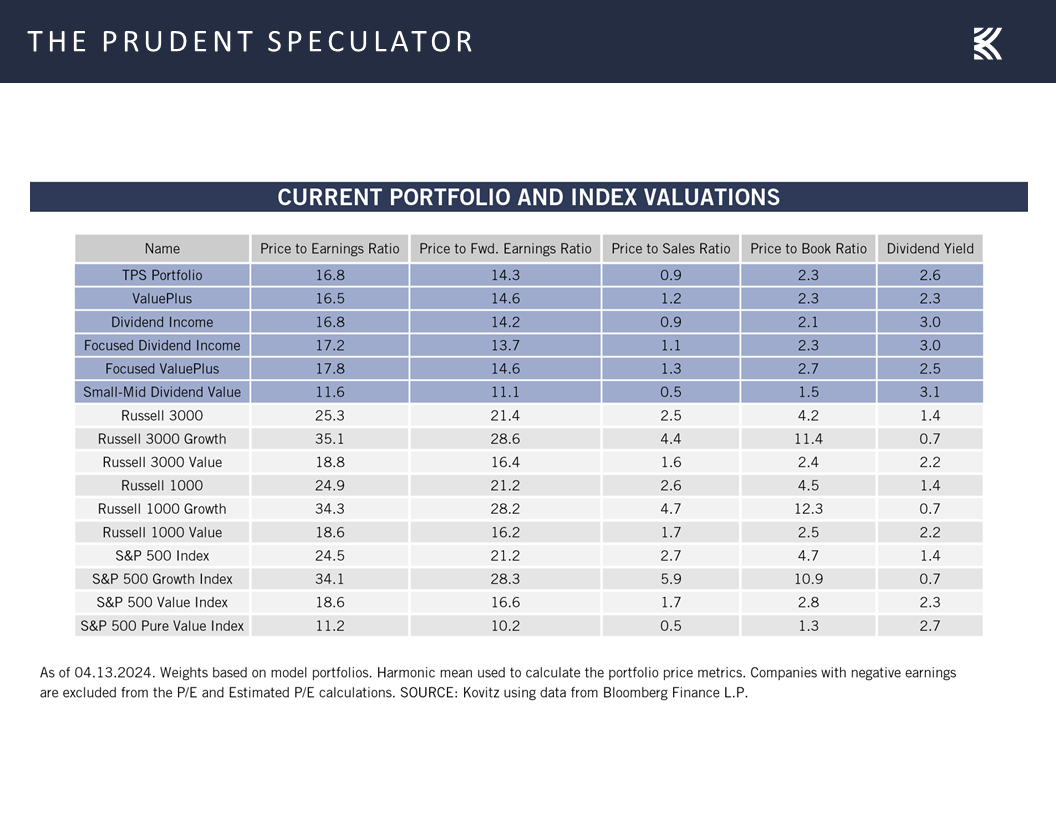

and valuations for Value stocks in general,

Valuations – Value Stocks Still Attractively Priced

and our broadly diversified portfolios of what we believe are undervalued stocks in particular continue to be attractive.

Stock News – Updates on three stocks in the financial sector

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Middle East, Inflation, Economic News and Corporate Profits

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Middle East, Inflation, Economic News, and Corporate Profits. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Week in Review – Stocks Retreat Again

Volatility – Normal Part of the Equity Process

Middle East – Perspective on Geopolitical Events

Inflation – CPI Higher and PPI Lower than Expected

Interest Rates – 10-Year Yield Jumps

History Lessons – Stocks Haven’t Minded Rising Inflation or Rising Rates, on Average

Econ News – Labor Market Strong; GDP Solid; Sentiment Weakens

Corporate Profits – Healthy EPS Growth Projected for ’24 and ’25

Valuations – Value Stocks Still Attractively Priced

Stock News – Updates on three stocks in the financial sector

Week in Review – Stocks Retreat Again

With the Dow Jones Industrial Average enduring two days last week of losses of more than 400 points and the popular index ending the five days with a more-than-900-point skid, the equity markets offered yet another reminder that short-term setbacks are always part of the equation. Of course, a simple price chart (ignores dividends and the impact of their reinvestment) shows that the long-term trend in the Dow has been markedly higher.

Volatility – Normal Part of the Equity Process

Alas, the Russell 3000 Value index suffered an even steeper percentage decline than the Dow last week with a loss of 2.84%. Believe it or not, this marked the 119th worst week since the formation of that benchmark in 1995, so 118 weeks were worse over the past 29 years. Happily, there have been 141 weeks where the gains have been 2.84% or greater during the same nearly three-decade period, and the overall return for Value stocks since the launch of The Prudent Speculator more than 47 years ago has been an excellent 13.8% per annum.

Middle East – Perspective on Geopolitical Events

Volatility is very much par for the course as looking at the S&P 500 going all the way back to 1928, there have been 5% or greater drops without a gain of equal magnitude three times a year on average, while corrections of 10% have happened every 11 months on average and 20% Bear Markets have occurred every 3.4 years on average. And, despite those trips south, the overall return on Value stocks has been 13.1% per annum going back more than nine decades.

No doubt, there have been plenty of disconcerting events on the geopolitical stage along the way with which long-term-oriented investors have had to contend, including more than a few Arab-Israeli conflicts and Saturday’s launch of a drone and missile attack on Israel by Iran adds to the risk of a dangerous escalation cycle in the Middle East.

While the method of the so-called retaliatory attack (from Iranian soil) was a surprise, the plunge in stock prices on Friday had a lot to do with news that an Iranian strike on Israel was imminent, so the U.S. equity market futures on Sunday evening were suggesting that some traders sold the rumor last week and may now be buying the news as the new week begins.

Time will tell if cooler heads prevail as the Iranian attack thus far was more bark than bite and the Israeli missile defense systems with help, evidently, from the U.S., U.K. and France, managed to shoot down or neutralize some 300 projectiles. It is hard to believe that Israel will not respond in some fashion, but history shows that every near-term stock market setback has been overcome in the fullness of time, including conflagrations that have directly involved the United States. So, while we must be braced for additional downside volatility, as Israel’s War Cabinet Minister Benny Gantz said his country would “exact a price from Iran in a way and time that suits us,” we are planning no changes to our portfolios due to this past weekend’s developments.

Inflation – CPI Higher and PPI Lower than Expected

To be sure, unrest in the Middle East was not the only issue troubling traders last week as inflation at the consumer level for March came in higher than expected with the full Consumer Price Index (CPI) rising 3.5% (est. 3.4%) on a year-over-year basis,

and the core CPI (excludes volatile food and energy prices) climbing 3.8% (est. 3.7%).

Countering those inflation worries somewhat, the rise in prices at the wholesale level in March came in lower than expected with the Producer Price Index advancing 2.1% (est. 2.2%), though the increase was up from 1.6% in February,

and the betting odds in the futures market saw a big jump in the projected year-end 2024 Fed Funds rate to 4.86%, up from 4.68% at the end of the preceding week.

Interest Rates – 10-Year Yield Jumps

while the yield on the benchmark U.S. 10-Year Treasury bond jumped to 4.52%, up from 4.40% the week prior.

History Lessons – Stocks Haven’t Minded Rising Inflation or Rising Rates, on Average

Obviously, many traders have been betting on Fed rate cuts and lower bond yields, so the knee-jerk reaction was to sell stocks last week, even as history shows that equities have proved rewarding, on average, whether inflation is rising or falling or whether it is high or low,

while the last major Fed battle to contain prices resulted in extraordinary stock-price gains (24.7% per annum for Value from 1978 to 1986), even with two recessions also in the mix!

Further, we note that rising Treasury yields in the fullness of time historically have proved only to be bad…for bonds!

Econ News – Labor Market Strong; GDP Solid; Sentiment Weakens

Certainly, we realize that the major U.S. equity market indexes across the board have rallied significantly off the October lows, so there is some good news baked into prices. The economy has proved more resilient than most had projected, with the labor market remaining very robust,

GDP growth last year exceeding expectations, with a 3.4% real (inflation-adjusted) rate of growth in Q4 2023

and a 2.4% rate of growth currently predicted for Q1 2024,

while the chance of recession in the next 12 months, per calculations from data provider Bloomberg, now stand at 35%, down from 55% just six months ago,

There can be no assurance that the economy will continue to hold up, and we note that reports last week on Small Business Optimism for March,

and confidence on Main Street for April both were weaker-than-expected,

Corporate Profits – Healthy EPS Growth Projected for ’24 and ’25

but the outlook for corporate profit growth this year and next remains very favorable,

and valuations for Value stocks in general,

Valuations – Value Stocks Still Attractively Priced

and our broadly diversified portfolios of what we believe are undervalued stocks in particular continue to be attractive.

Stock News – Updates on three stocks in the financial sector

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.