The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the The Case for Value, EPS Outlook, Interest Rates and More. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Buckingham European Train Journey – Value Crushed Growth Last Week

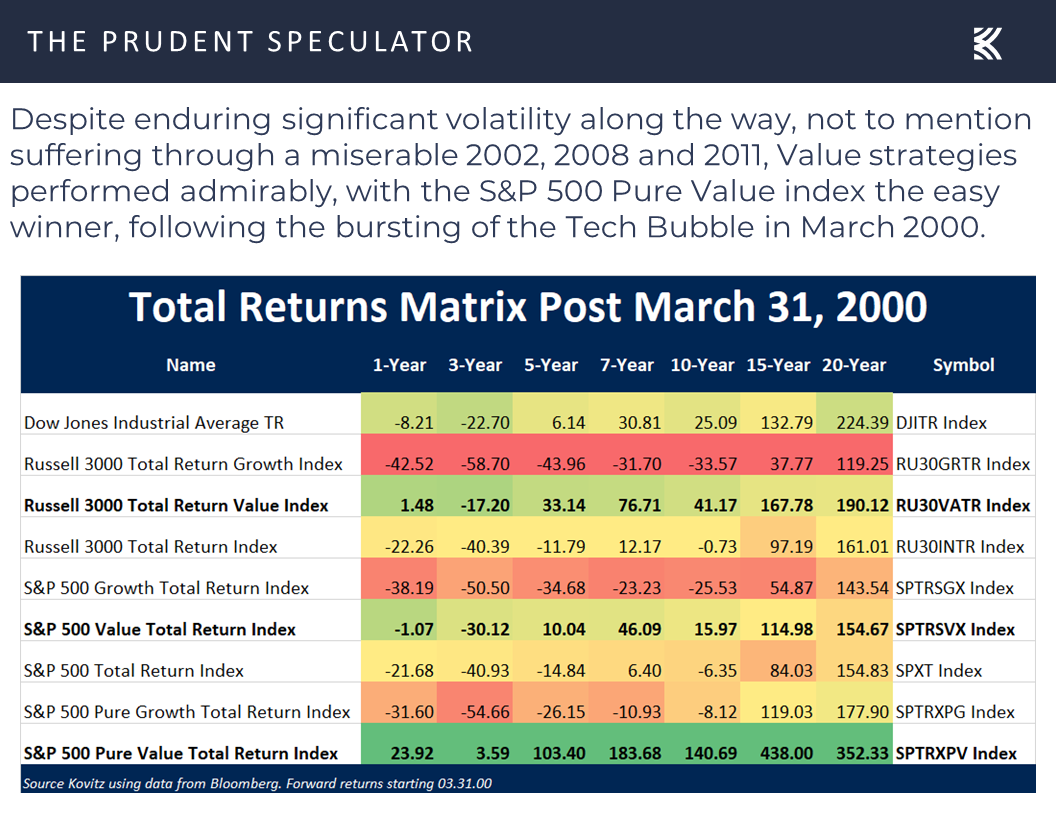

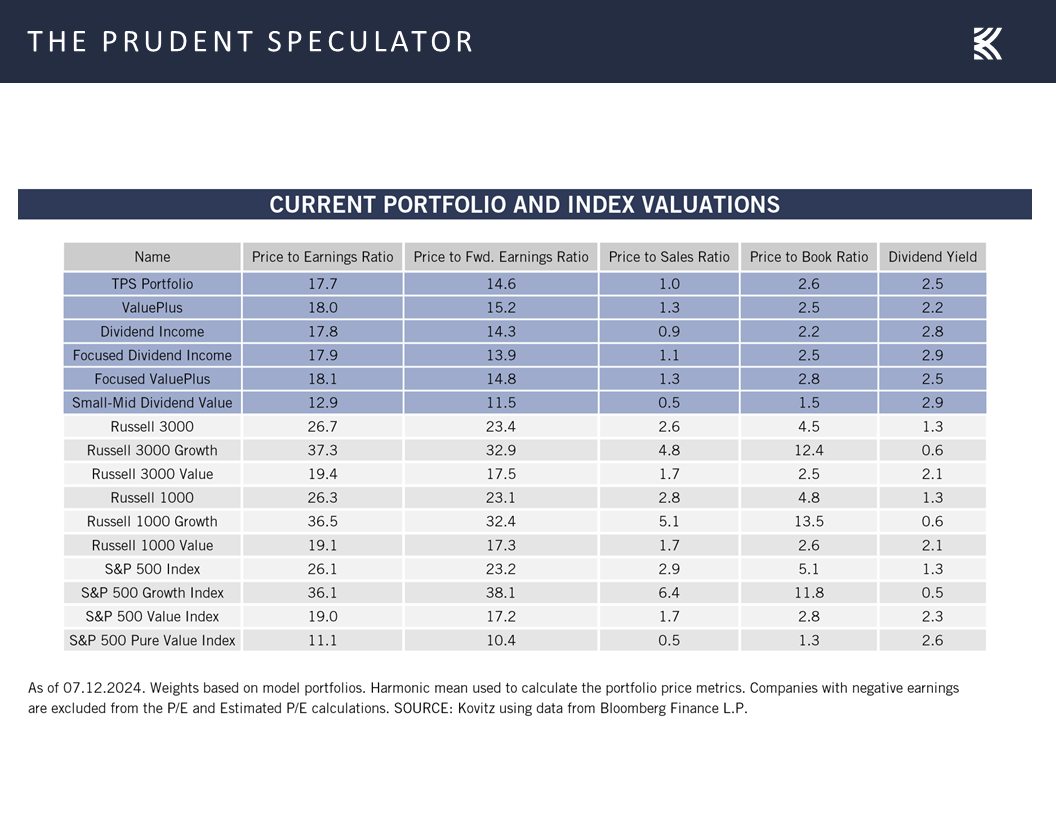

The Case for Value – Reasonable Valuations, Return Gap vs. Growth & Historical Propensity for Outperformance

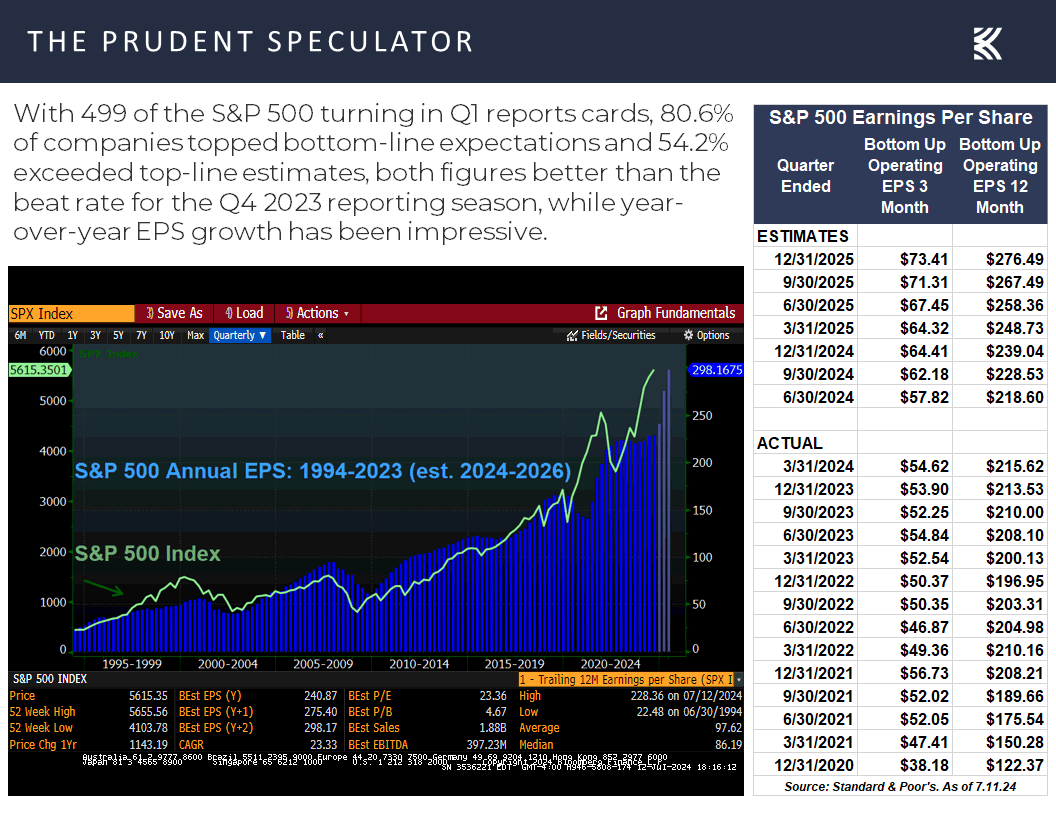

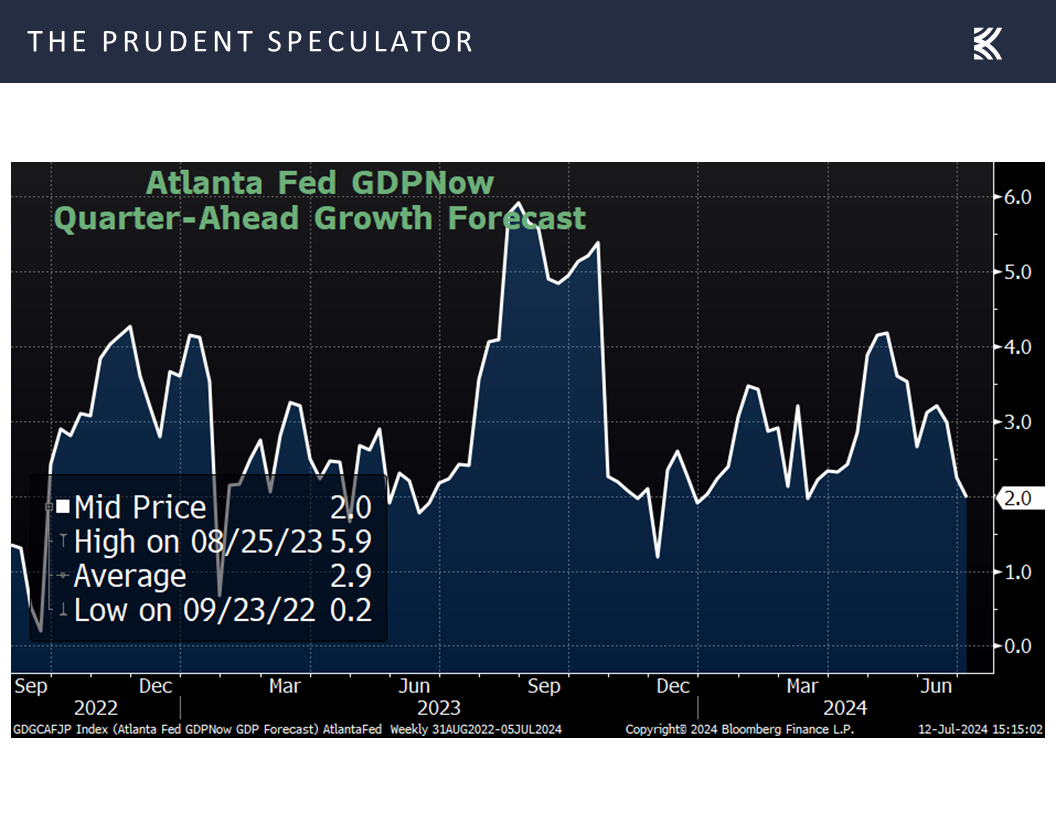

EPS Outlook – Solid GDP Supports Corporate Profit Growth

Fed – Powell Dovish on Capitol Hill

Inflation – Lower-than-Expected CPI Numbers

Interest Rates – Fed Rate Cuts More Likely; 10-Year Yield Drops

Volatility – Scary Headlines & Plenty of Gyrations Along the Way but Long-Term Trend is Up

Stock News – Updates on AAPL, GLW, GBX, C, BK & JPM

Buckingham European Train Journey – Value Crushed Growth Last Week

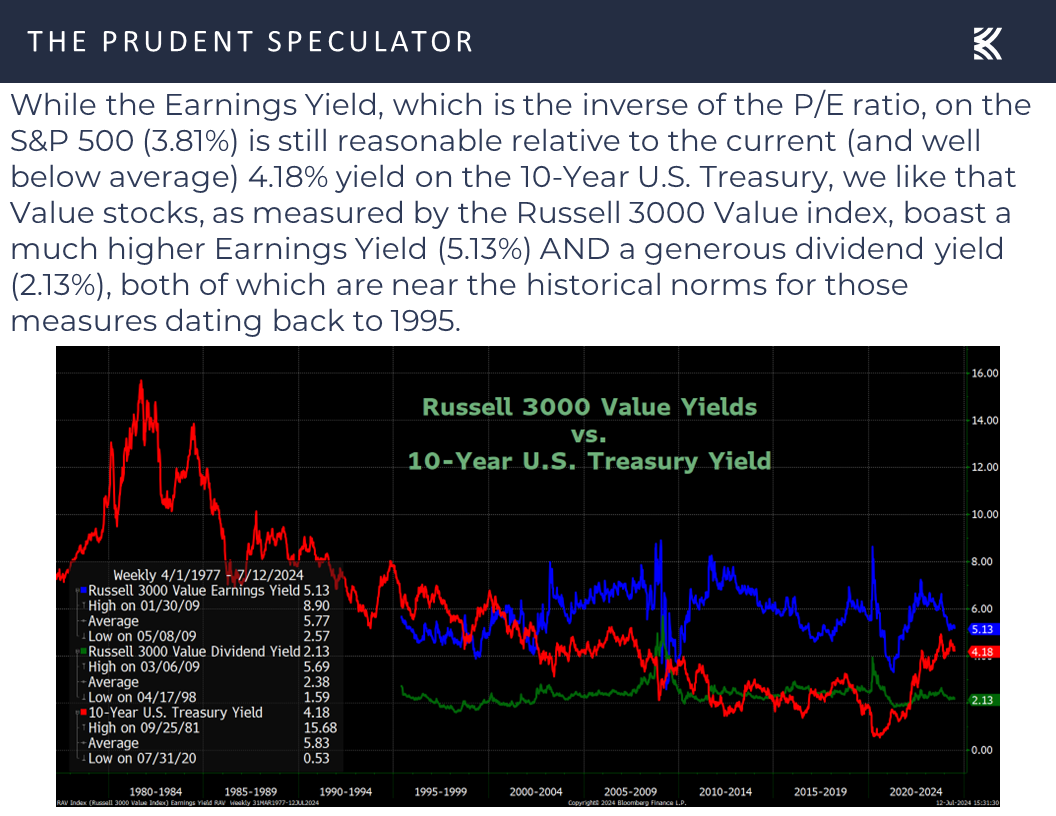

Indeed, while we have been asserting that Value stocks like those that we have long favored are very much reasonably priced relative to interest rates,

The Case for Value – Reasonable Valuations, Return Gap vs. Growth & Historical Propensity for Outperformance

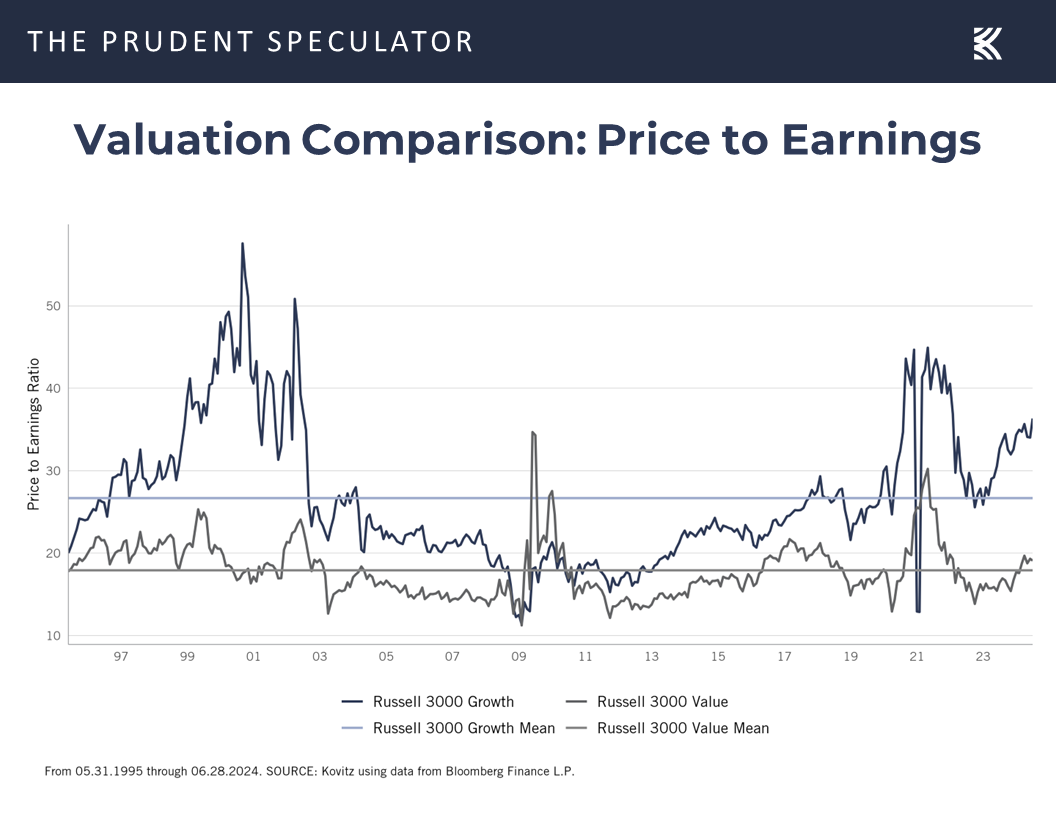

and certainly relative to their Growth counterparts on historical earnings multiples,

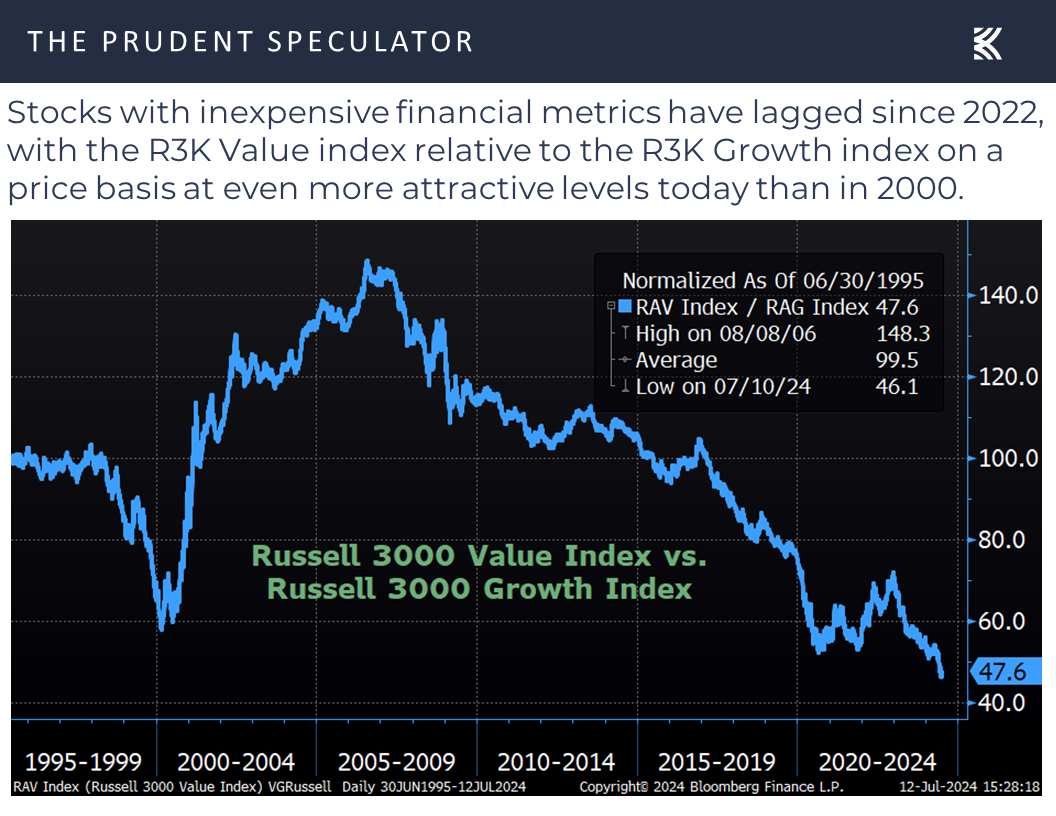

it was very nice to see the Russell 3000 Value index outperform the Russell 3000 Growth index by some 300 basis points last week, especially as there is plenty of room for the trend to continue just to get back to equilibrium,

much less see Value reassert its long-term propensity for superior returns.

No doubt, a Value renaissance has occurred before, though unlike the often-profitless Dot.com companies that fueled the Tech Bubble, the current A.I.-infused euphoria has been led by mega-cap tech stocks that seem to be minting money.

Time will tell whether Growth stocks will live up to the expectations built into their lofty valuations, but we sleep very well at night with the attractive price tags and income generation potential of the baskets of stocks we own in our broadly diversified portfolios,

Time will tell whether Growth stocks will live up to the expectations built into their lofty valuations, but we sleep very well at night with the attractive price tags and income generation potential of the baskets of stocks we own in our broadly diversified portfolios,

EPS Outlook – Solid GDP Supports Corporate Profit Growth

especially given that corporate profits are likely to remain healthy,

with decent GDP growth,

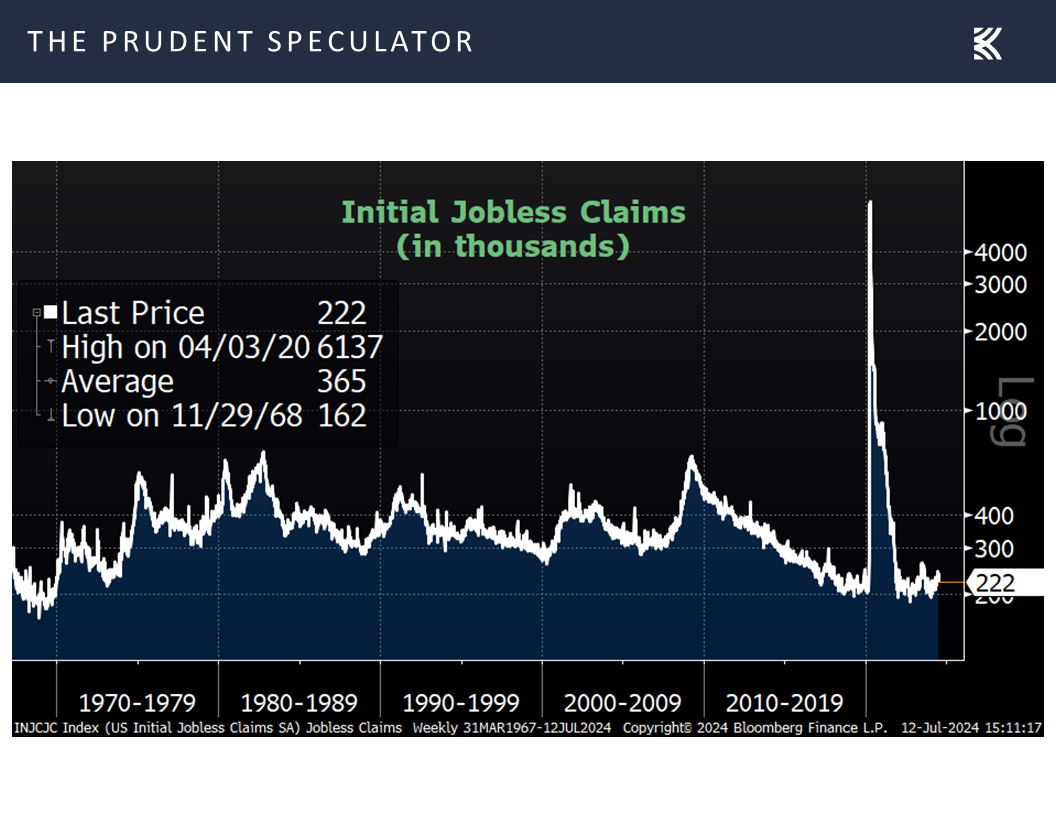

and a solid labor market, with near-multi-generational lows in first-time filings for unemployment benefits.

Fed – Powell Dovish on Capitol Hill

Of course, it also didn’t hurt last week that Jerome H. Powell said on Capitol Hill, “In light of the progress made both in lowering inflation and in cooling the labor market over the past two years, elevated inflation is not the only risk we face. Reducing policy restraint too late or too little could unduly weaken economic activity and employment.”

He added “The U.S. economy continues to expand at a solid pace,” despite a deceleration in GDP growth. “Private domestic demand remains robust, however, with slower but still-solid increases in consumer spending.”

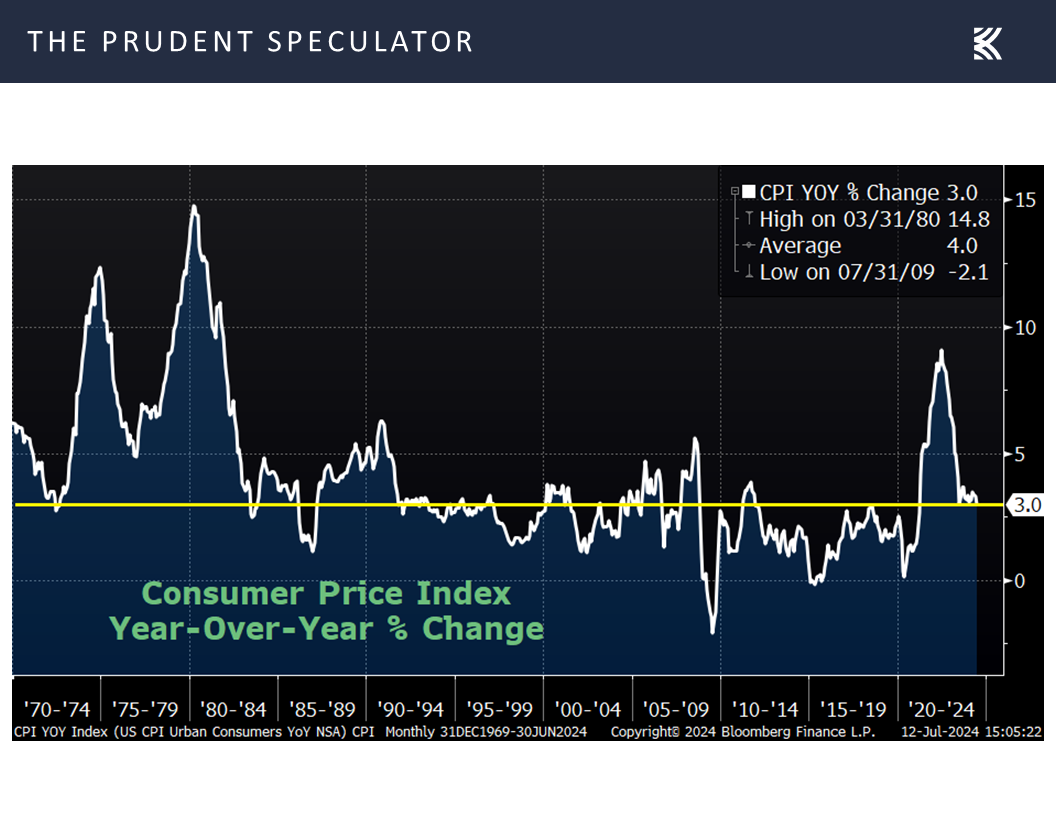

Those comments from the Federal Reserve Chair preceded positive news on inflation when the consumer price index (CPI) for June unexpectedly dipped to a 3.0% annualized rate of growth, down from 3.3% in May and below forecasts for a 3.1% advance,

Inflation – Lower-than-Expected CPI Numbers

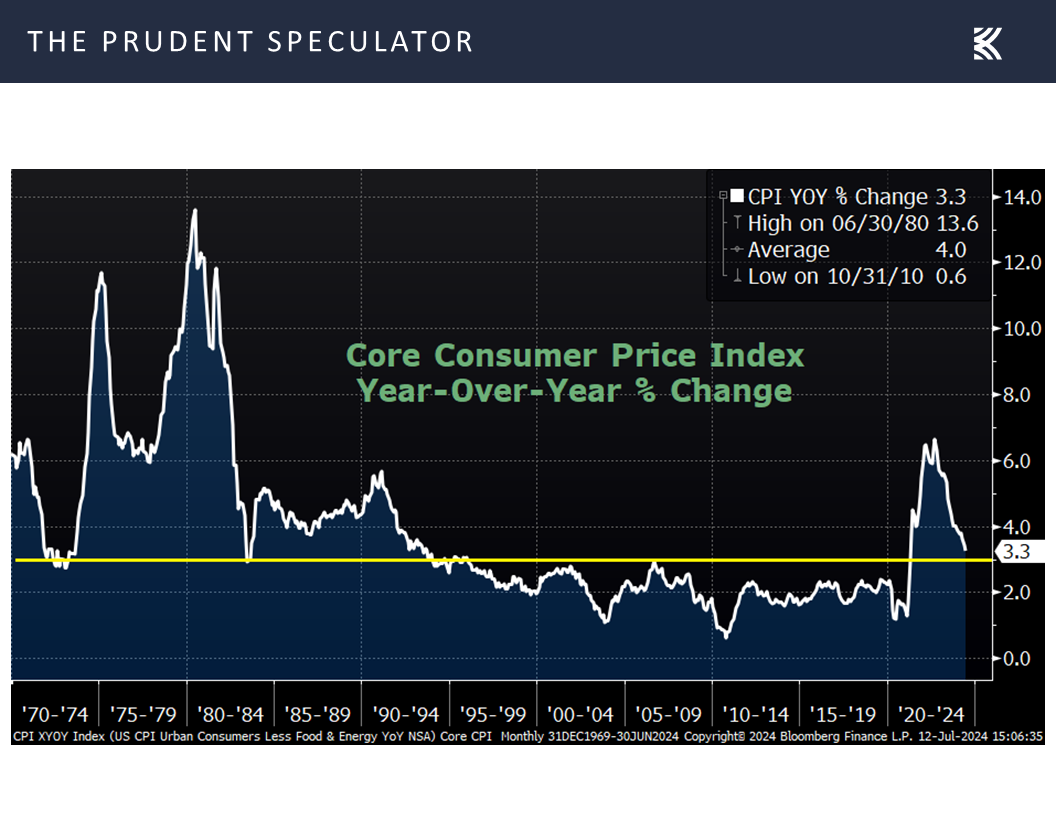

while the core CPI (excludes volatile food and energy prices) came in at a 3.3% increase, compared to estimates of 3.4% and May’s reading of 3.4%.

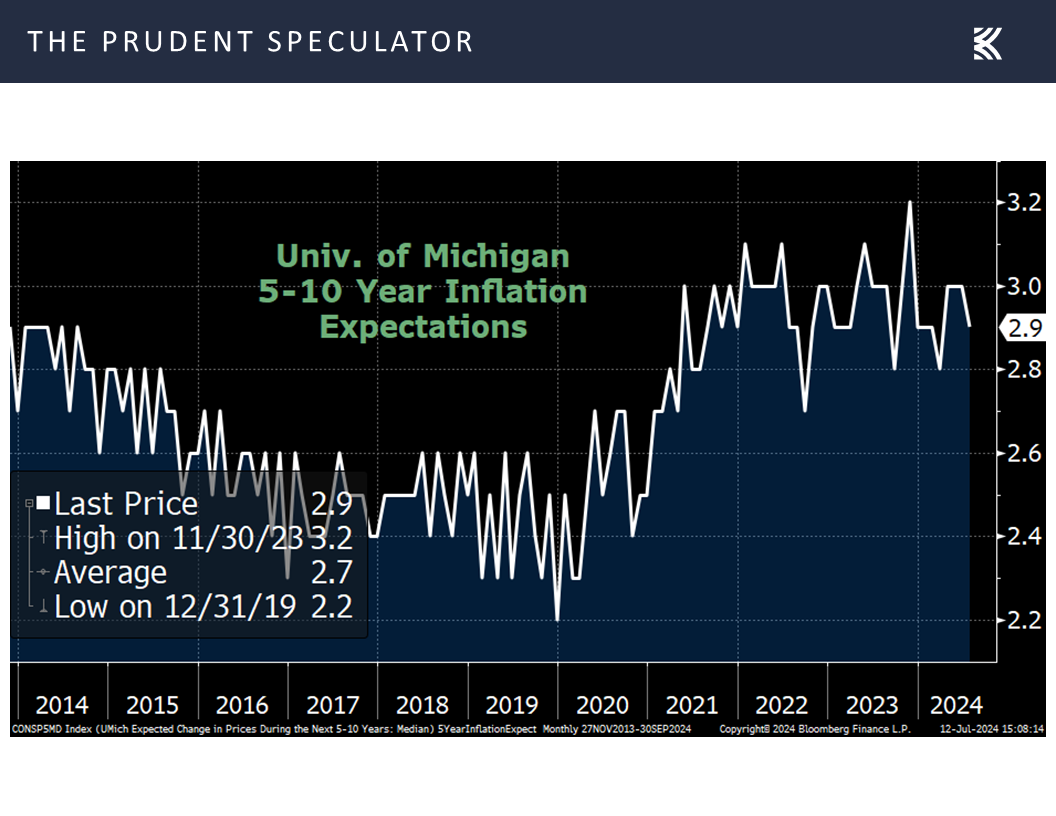

Mr. Powell’s optimism on the progress that has been made on inflation was echoed by longer-term inflation expectations dropping to 2.9% in the latest University of Michigan survey,

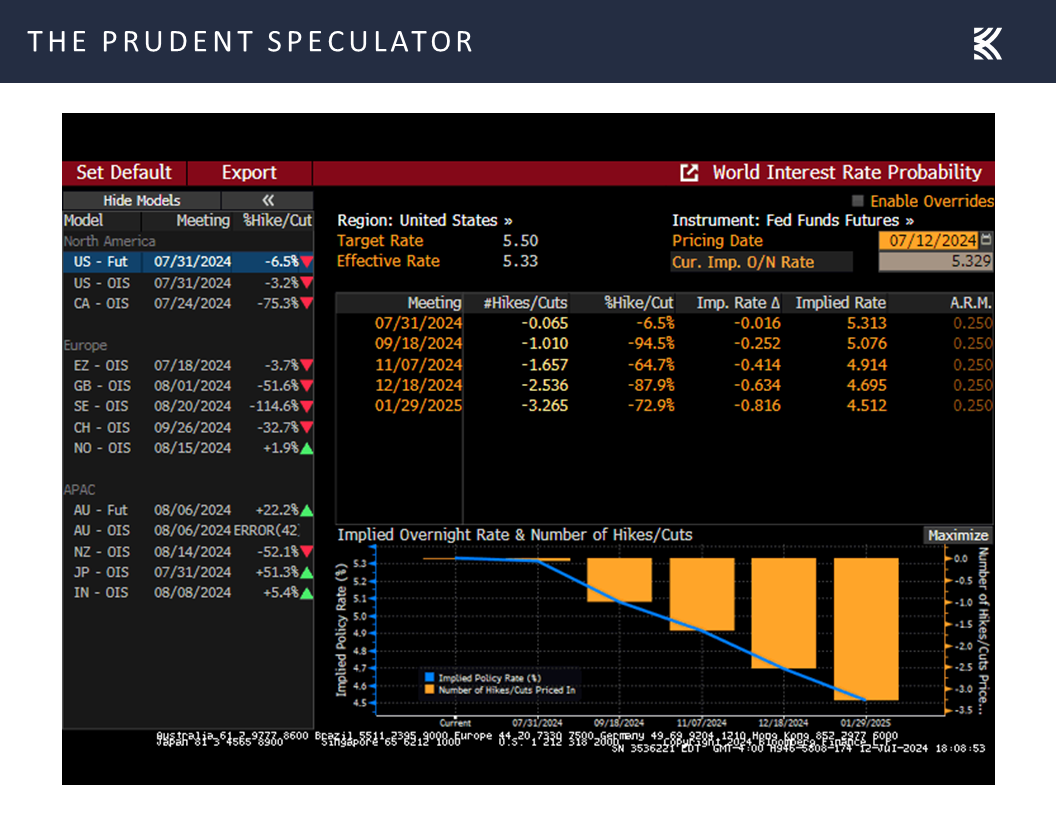

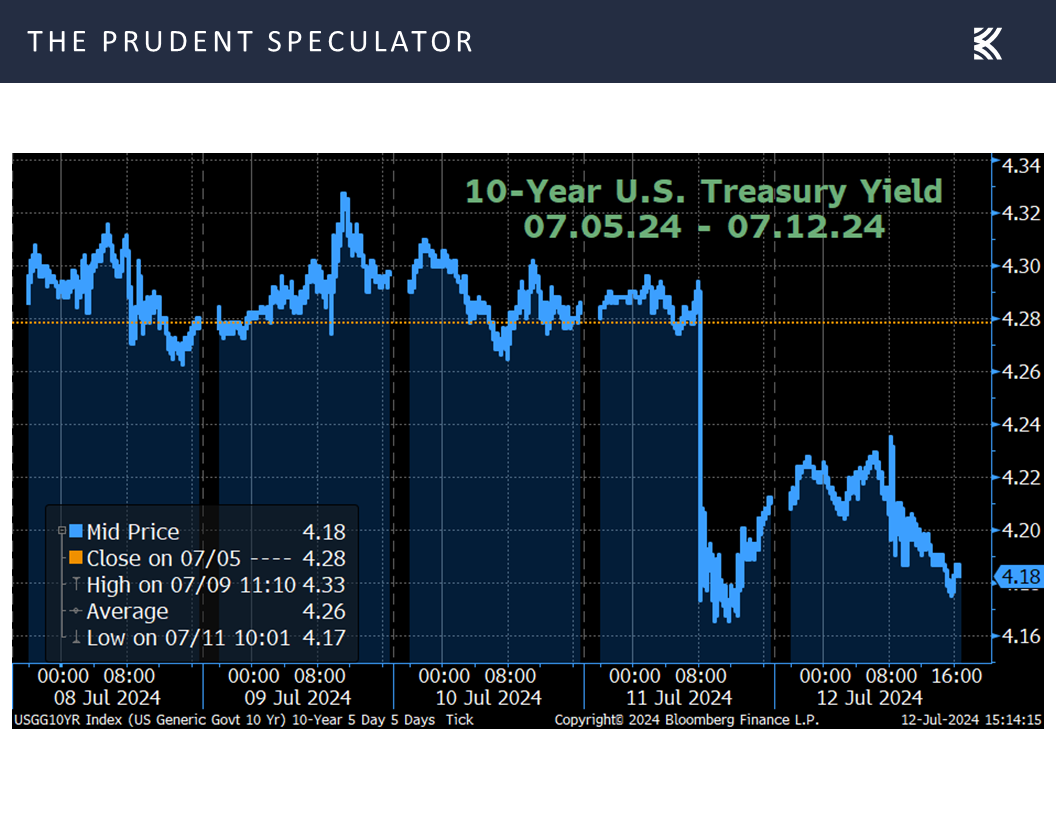

Interest Rates – Fed Rate Cuts More Likely; 10-Year Yield Drops

which improved the odds of Fed rate cuts, as measured by the futures market betting that the year-end Fed Funds rate will decline to 4.70%, down from 4.82% the week prior,

and helped send the yield on the benchmark 10-year U.S. Treasury down to 4.18% from 4.28% last week.

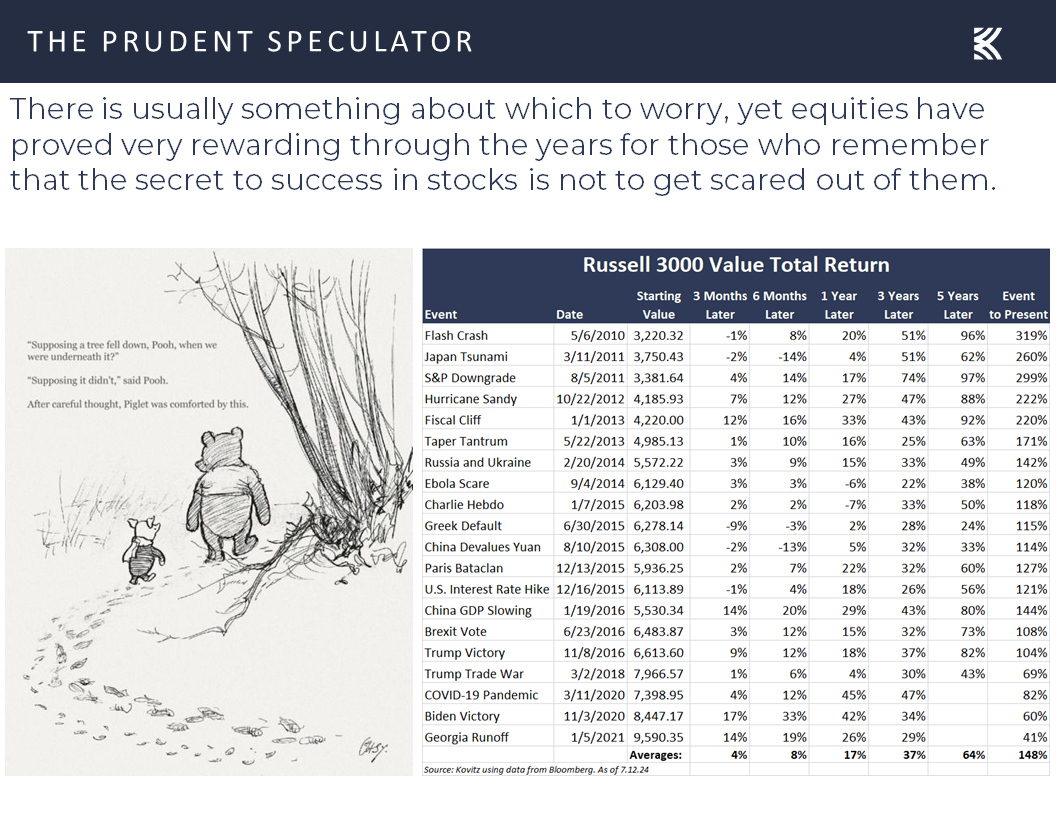

Volatility – Scary Headlines & Plenty of Gyrations Along the Way but Long-Term Trend is Up

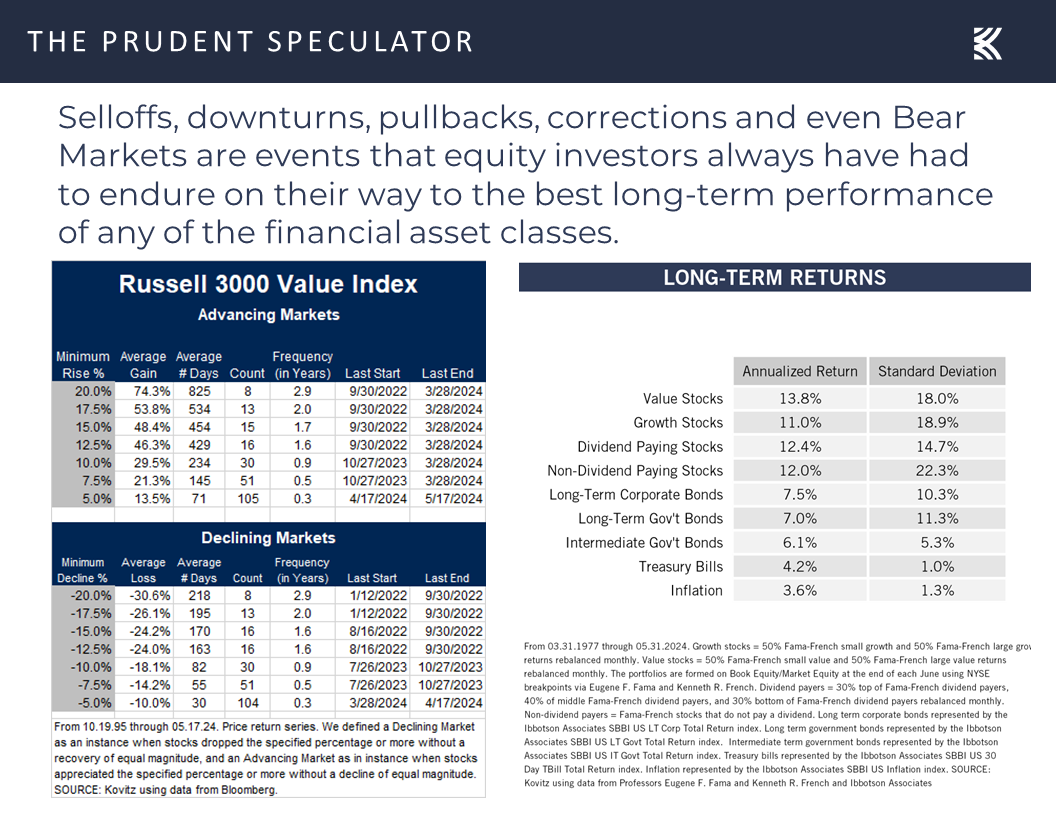

Certainly, we realize that one week does not a trend make, and we understand that there are plenty of possible headlines that could send stocks lower in the short run, while downside volatility is always part of the investment equation, but we continue to be enthusiastic about the prospects for Value in the long run.

Stock News – Updates on six stocks across four different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

The Case for Value, EPS Outlook, Interest Rates and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the The Case for Value, EPS Outlook, Interest Rates and More. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Buckingham European Train Journey – Value Crushed Growth Last Week

The Case for Value – Reasonable Valuations, Return Gap vs. Growth & Historical Propensity for Outperformance

EPS Outlook – Solid GDP Supports Corporate Profit Growth

Fed – Powell Dovish on Capitol Hill

Inflation – Lower-than-Expected CPI Numbers

Interest Rates – Fed Rate Cuts More Likely; 10-Year Yield Drops

Volatility – Scary Headlines & Plenty of Gyrations Along the Way but Long-Term Trend is Up

Stock News – Updates on AAPL, GLW, GBX, C, BK & JPM

Buckingham European Train Journey – Value Crushed Growth Last Week

Indeed, while we have been asserting that Value stocks like those that we have long favored are very much reasonably priced relative to interest rates,

The Case for Value – Reasonable Valuations, Return Gap vs. Growth & Historical Propensity for Outperformance

and certainly relative to their Growth counterparts on historical earnings multiples,

it was very nice to see the Russell 3000 Value index outperform the Russell 3000 Growth index by some 300 basis points last week, especially as there is plenty of room for the trend to continue just to get back to equilibrium,

much less see Value reassert its long-term propensity for superior returns.

No doubt, a Value renaissance has occurred before, though unlike the often-profitless Dot.com companies that fueled the Tech Bubble, the current A.I.-infused euphoria has been led by mega-cap tech stocks that seem to be minting money.

EPS Outlook – Solid GDP Supports Corporate Profit Growth

especially given that corporate profits are likely to remain healthy,

with decent GDP growth,

and a solid labor market, with near-multi-generational lows in first-time filings for unemployment benefits.

Fed – Powell Dovish on Capitol Hill

Of course, it also didn’t hurt last week that Jerome H. Powell said on Capitol Hill, “In light of the progress made both in lowering inflation and in cooling the labor market over the past two years, elevated inflation is not the only risk we face. Reducing policy restraint too late or too little could unduly weaken economic activity and employment.”

He added “The U.S. economy continues to expand at a solid pace,” despite a deceleration in GDP growth. “Private domestic demand remains robust, however, with slower but still-solid increases in consumer spending.”

Those comments from the Federal Reserve Chair preceded positive news on inflation when the consumer price index (CPI) for June unexpectedly dipped to a 3.0% annualized rate of growth, down from 3.3% in May and below forecasts for a 3.1% advance,

Inflation – Lower-than-Expected CPI Numbers

while the core CPI (excludes volatile food and energy prices) came in at a 3.3% increase, compared to estimates of 3.4% and May’s reading of 3.4%.

Mr. Powell’s optimism on the progress that has been made on inflation was echoed by longer-term inflation expectations dropping to 2.9% in the latest University of Michigan survey,

Interest Rates – Fed Rate Cuts More Likely; 10-Year Yield Drops

which improved the odds of Fed rate cuts, as measured by the futures market betting that the year-end Fed Funds rate will decline to 4.70%, down from 4.82% the week prior,

and helped send the yield on the benchmark 10-year U.S. Treasury down to 4.18% from 4.28% last week.

Volatility – Scary Headlines & Plenty of Gyrations Along the Way but Long-Term Trend is Up

Certainly, we realize that one week does not a trend make, and we understand that there are plenty of possible headlines that could send stocks lower in the short run, while downside volatility is always part of the investment equation, but we continue to be enthusiastic about the prospects for Value in the long run.

Stock News – Updates on six stocks across four different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.