The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss AAII Sentiment, Economic News, Recessions and Stagflation. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – Three Sales Across 4 Portfolios

Buckingham AAII Appearance – San Diego, April 12, 2025

Week – Friday Plunge Sends the 5 Days into the Red

Corrections – 10% Declines Happen with Surprising Frequency

Sentiment – Major AAII Contrarian Buy Signal

Econ News – “Hard” Numbers Solid but “Soft” Figures Weaken; GDP Growth Still the Forecast

Recessions – Risk Isn’t High Today, But History Shows Staying the Course the Right Move Even if a Contraction Eventually Was to Occur

Inflation – Long-Term Expectations and PCE Rise; Stocks a Great Hedge Historically

Stagflation – Historical Equity Returns from 1973-1982

Patience – The Longer the Hold the Better the Chance of Success

Valuations – Liking the Metrics on our Portfolios

Stock News – Updates on 3 auto-makers and a paper manufacturer

Buckingham AAII Appearance – San Diego, April 12, 2025

Your Editor will be speaking in San Diego on Saturday, April 12, 2025, at 9:00 AM. Registration info for that presentation is available here:

Upcoming Chapter Events – AAII San Diego

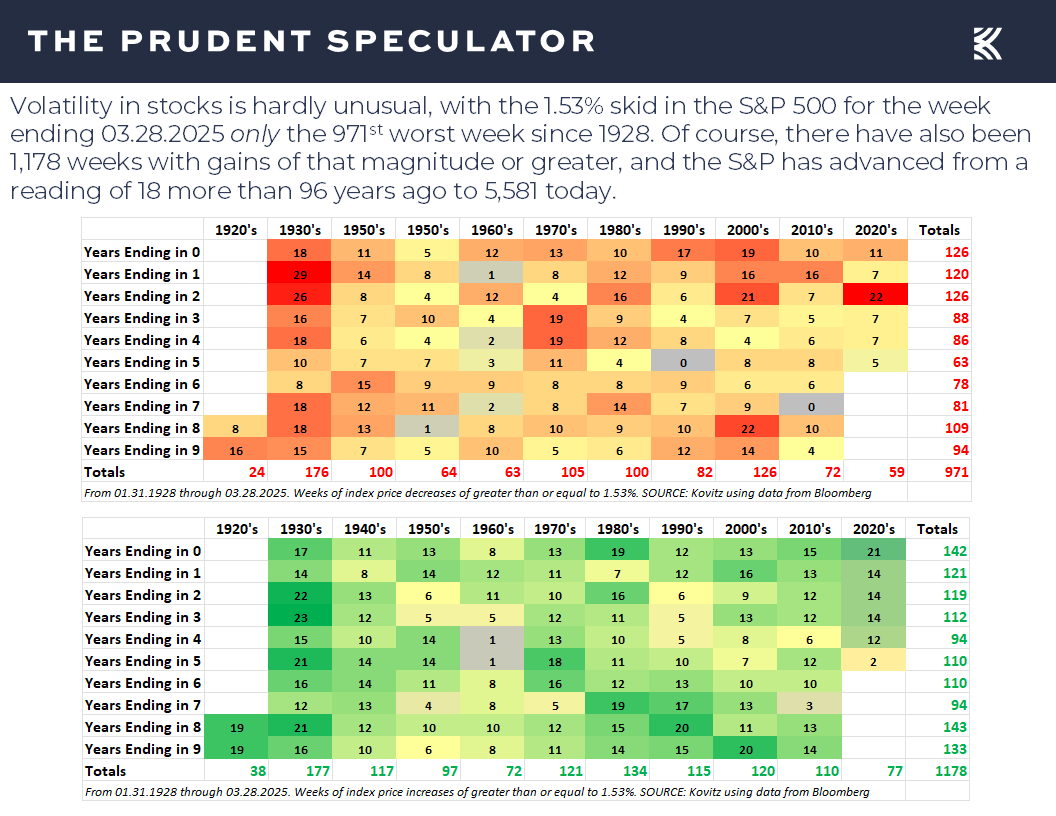

Week – Friday Plunge Sends the 5 Days into the Red

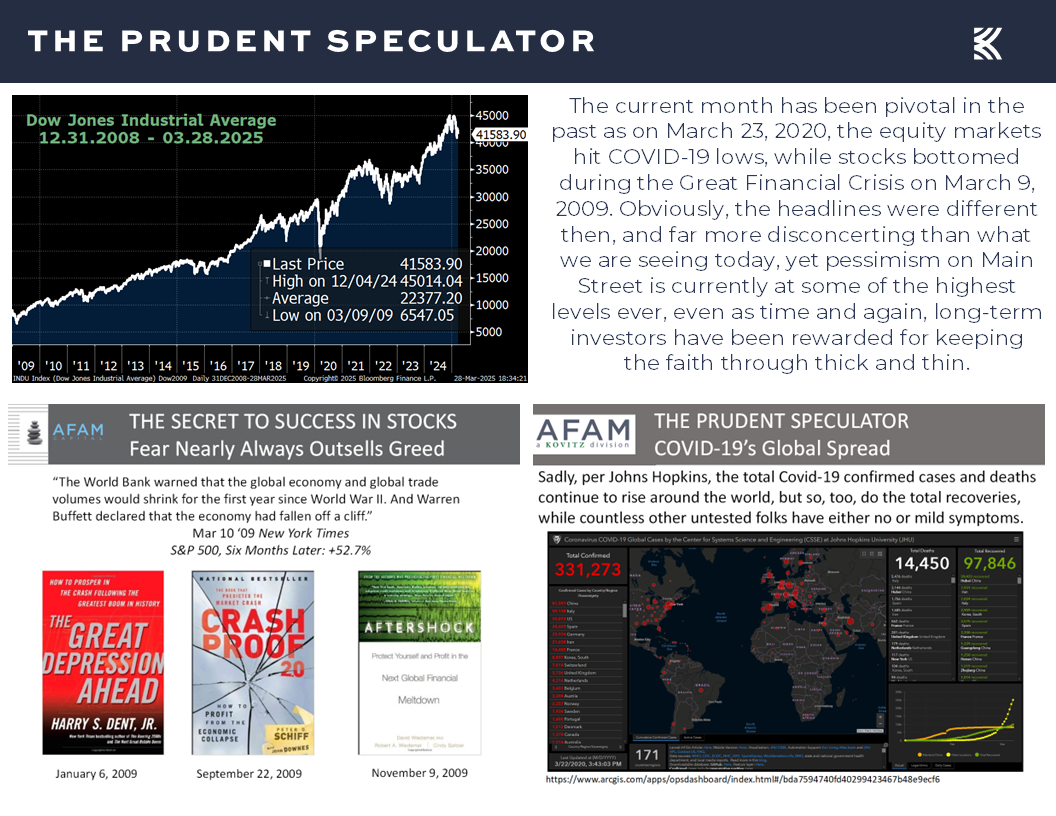

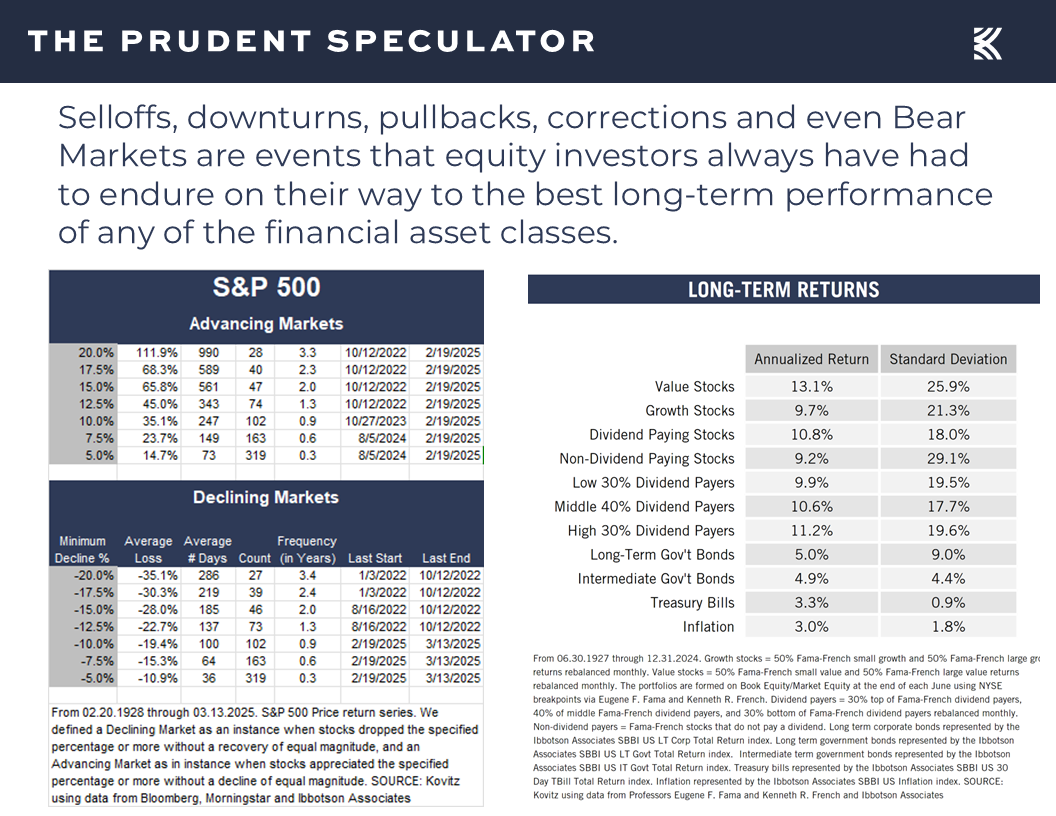

With all the decline and then some coming on Friday, stocks endured another tough week of trading as the S&P 500 retreated 1.53% on a price basis over the latest five-day period. Believe it or not, there have been 970 weeks over the last 97 years with a drop of equal or greater magnitude, or 10 weekly occurrences per annum on average, so volatility is par for the equity market course.

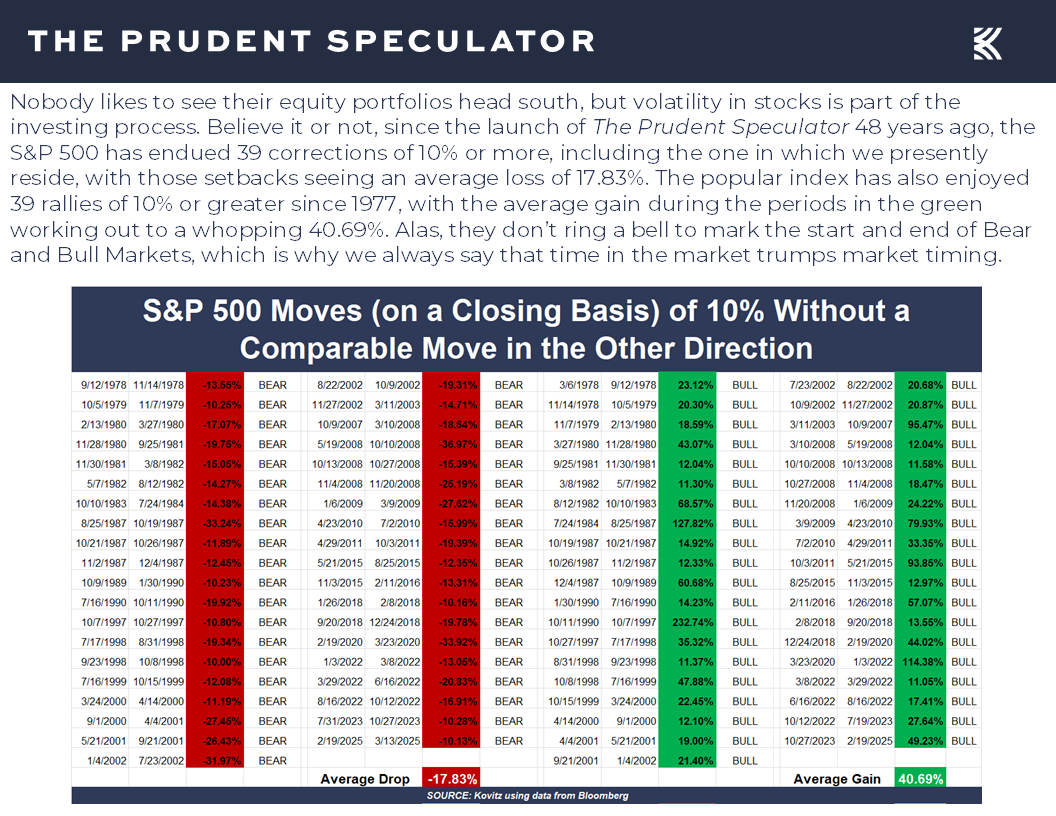

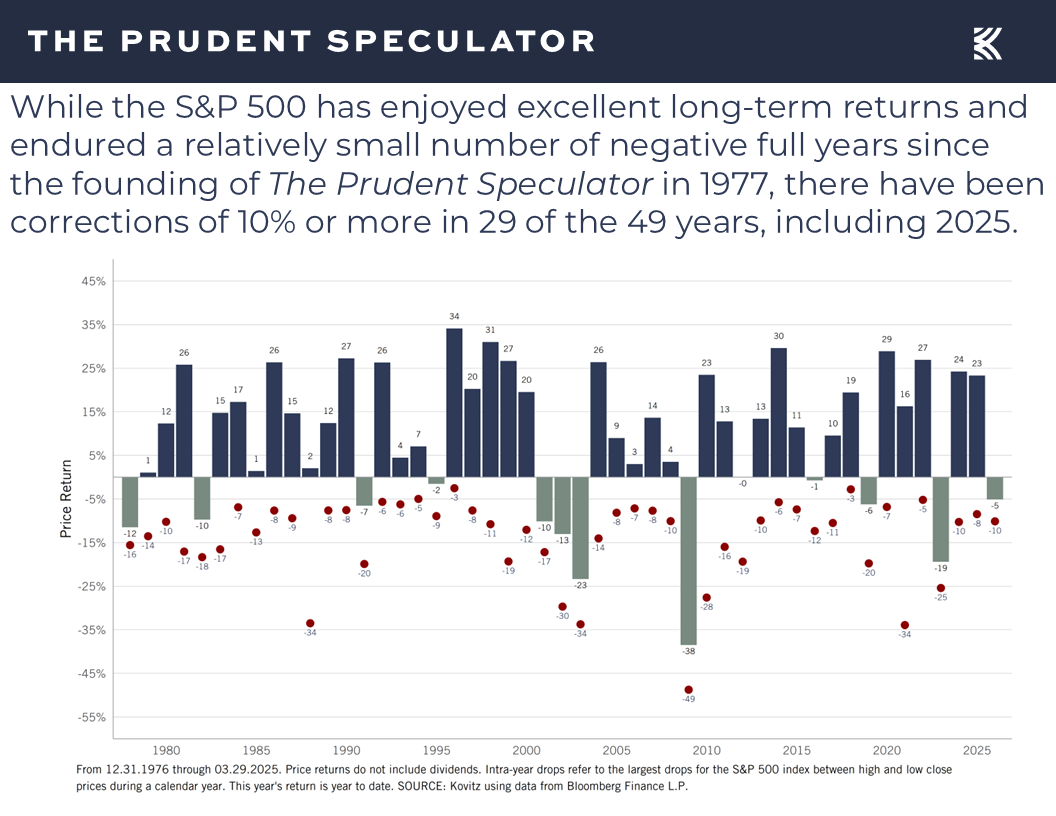

Corrections – 10% Declines Happen with Surprising Frequency

While the S&P thus far has held above its low of March 13, 2025, in which it entered the 39th correction of 10% since the launch of The Prudent Speculator 48 years ago,

sizable pullbacks happen every year, with the current skid thus far modest by historical standards.

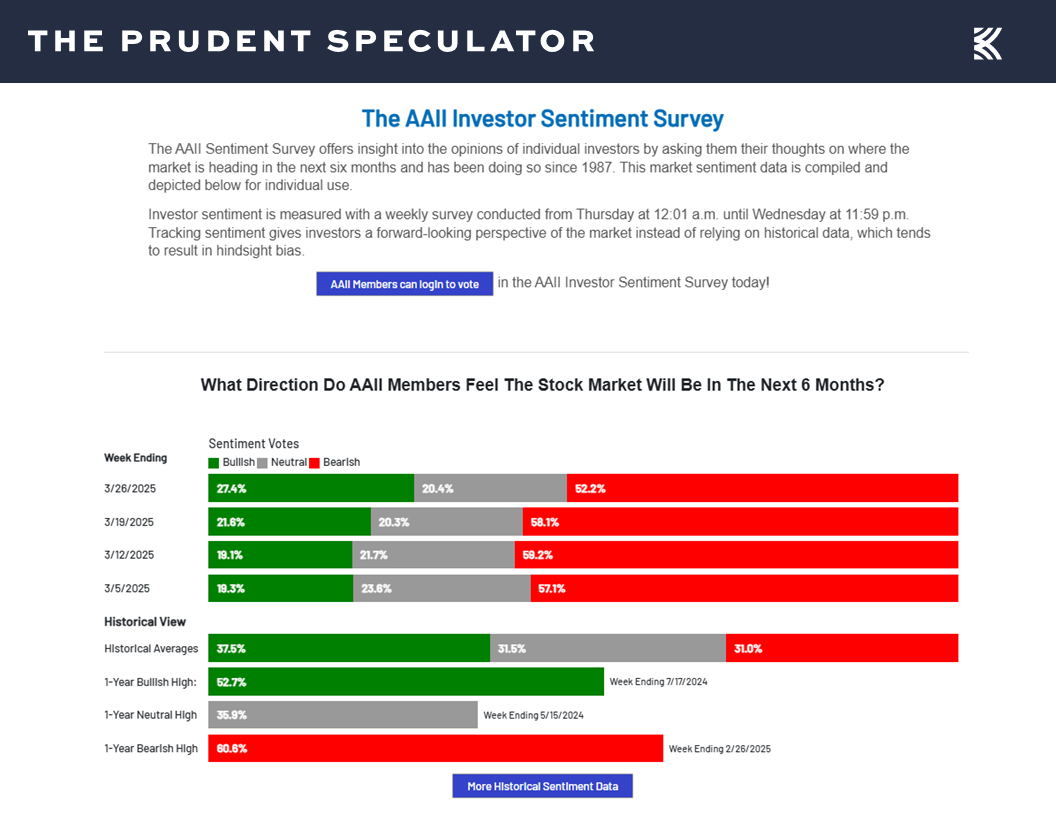

Sentiment – Major AAII Contrarian Buy Signal

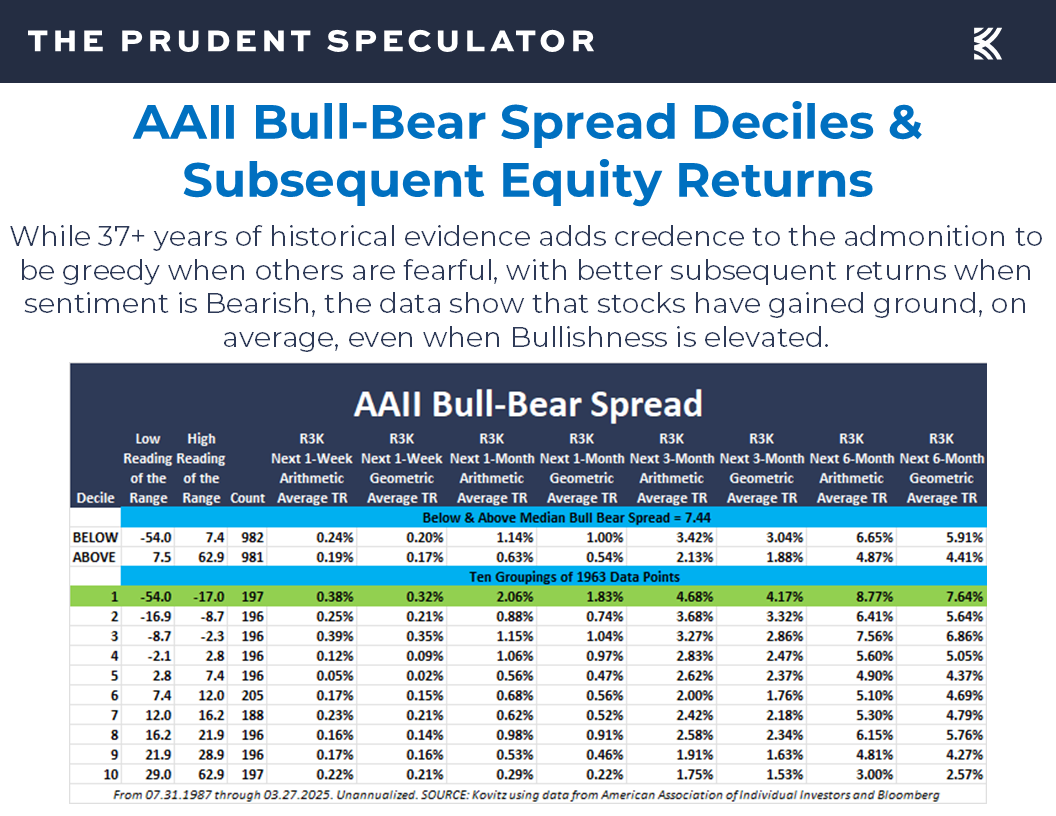

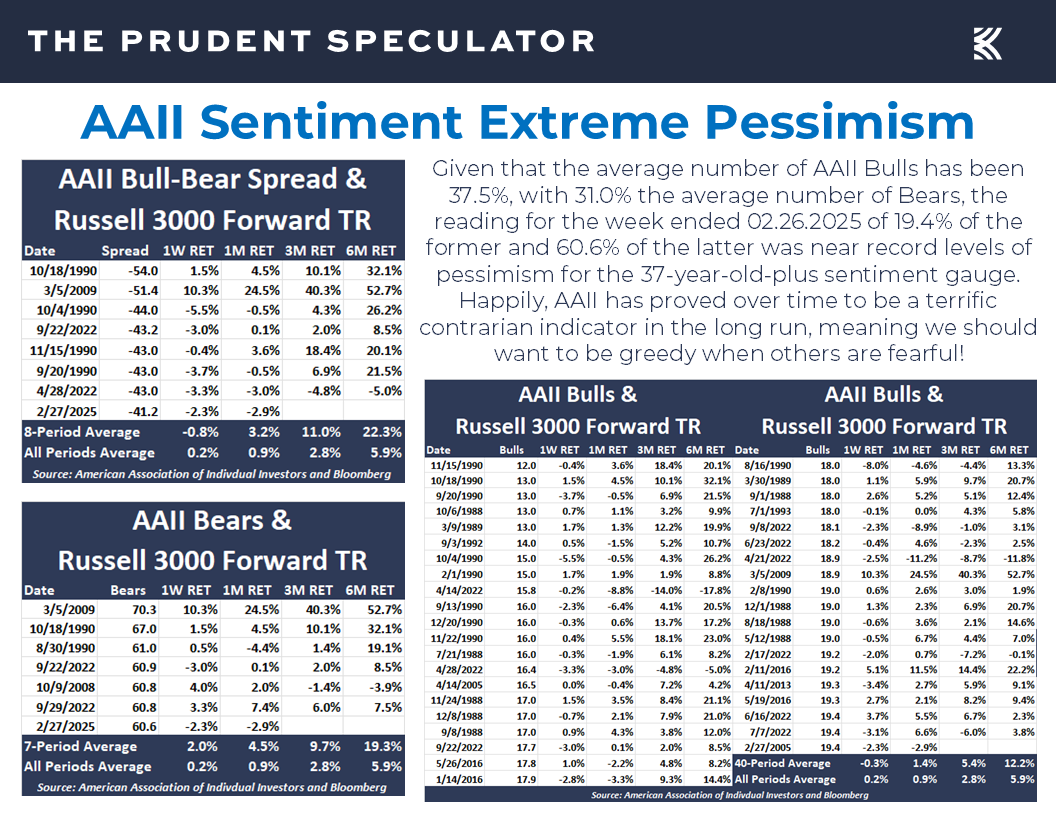

Of course, though the size of the setback is relatively tame, it is fascinating to see the level of consternation gripping folks on Main Street, with the latest Sentiment Survey from the American Association of Individual Investors (AAII) continuing to show a preponderance of pessimism,

as the overall Bearishness is on par or worse than it was at the equity market bottoms during the Great Financial Crisis and the COVID-19 Pandemic.

Past performance is never a guarantee of future performance, but nearly 38 years of AAII market history shows that it generally has paid off handsomely to be greedy when others are fearful,

and very greedy when others are very fearful,

while over the long-term, equities have enjoyed far more time in the green than they have in the red, so much so that returns for Value Stocks and Dividend Payers have averaged double-digit annual percentages going all the way back to the 1920s.

Econ News – “Hard” Numbers Solid but “Soft” Figures Weaken; GDP Growth Still the Forecast

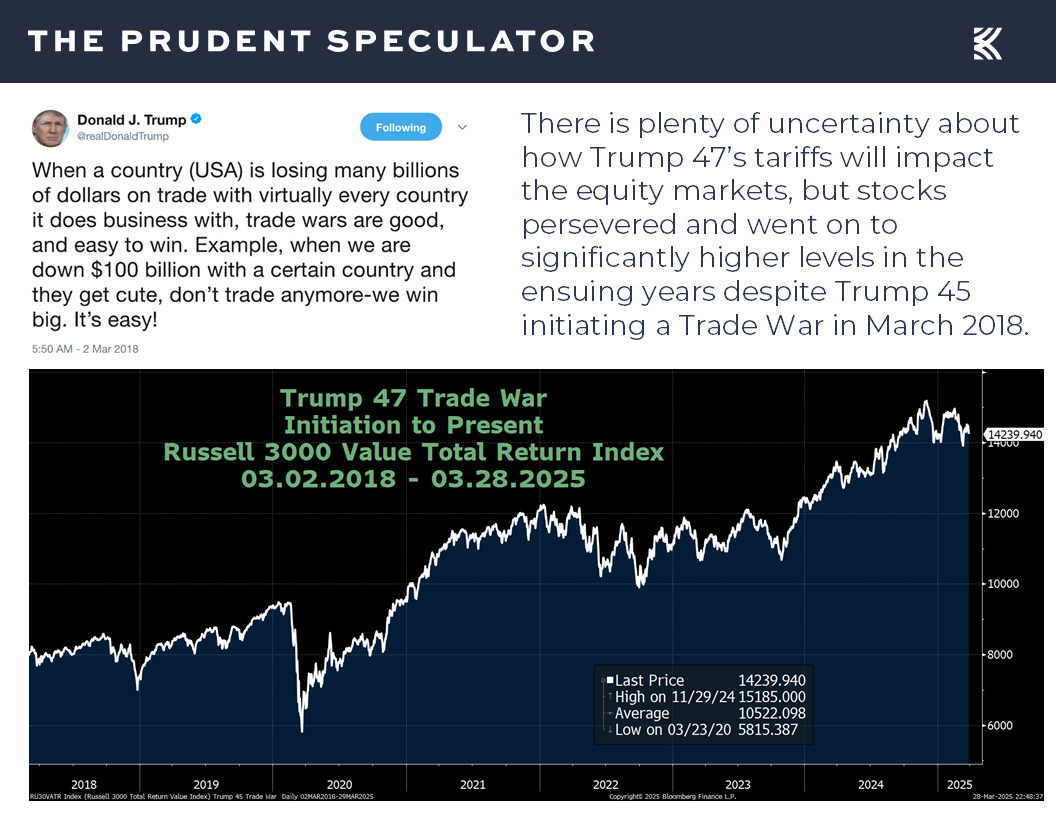

Of course, though we have long believed that uncertainty is the friend to the buyer of long-term value, we realize that tariffs, real and threatened, are not helping investors remain on an even emotional keel, especially with so-called “Liberation Day” happening on April 2. Obviously, this time is different, as is every time, but we have been down the tariff road previously,

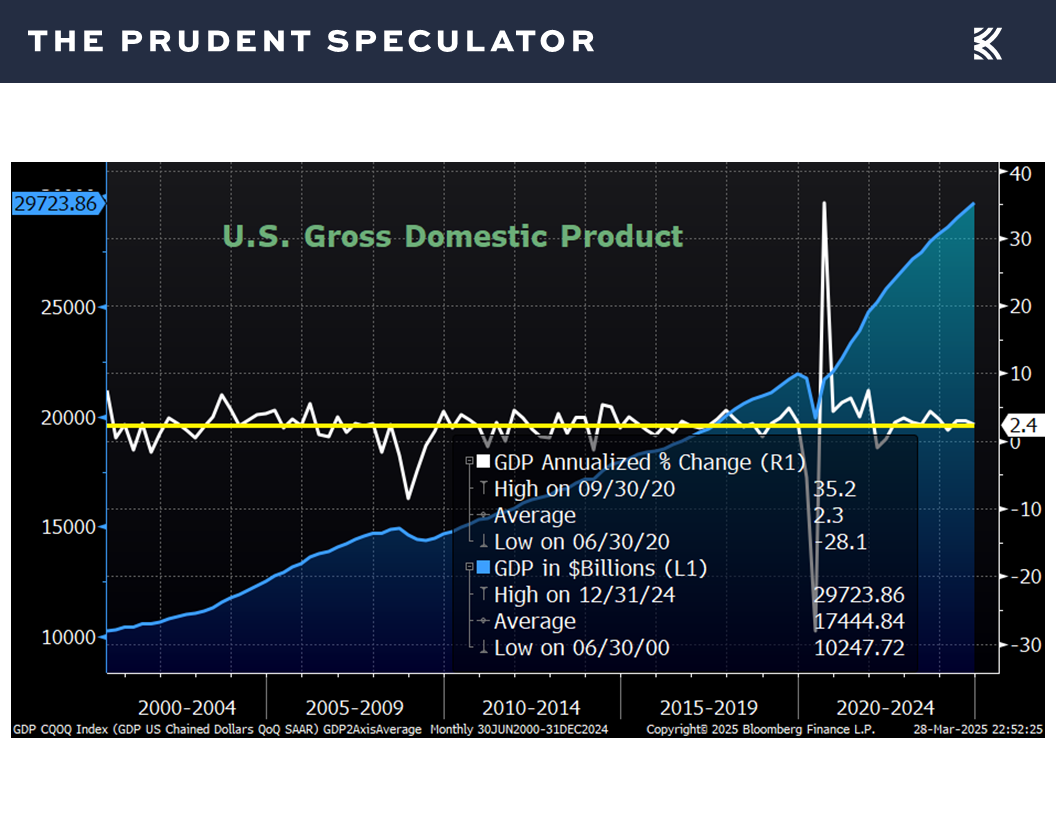

while the U.S. economy entered 2025 in good shape, relatively speaking, with Q4 2024 real (inflation-adjusted) GDP growth having been revised up last week to 2.4%,

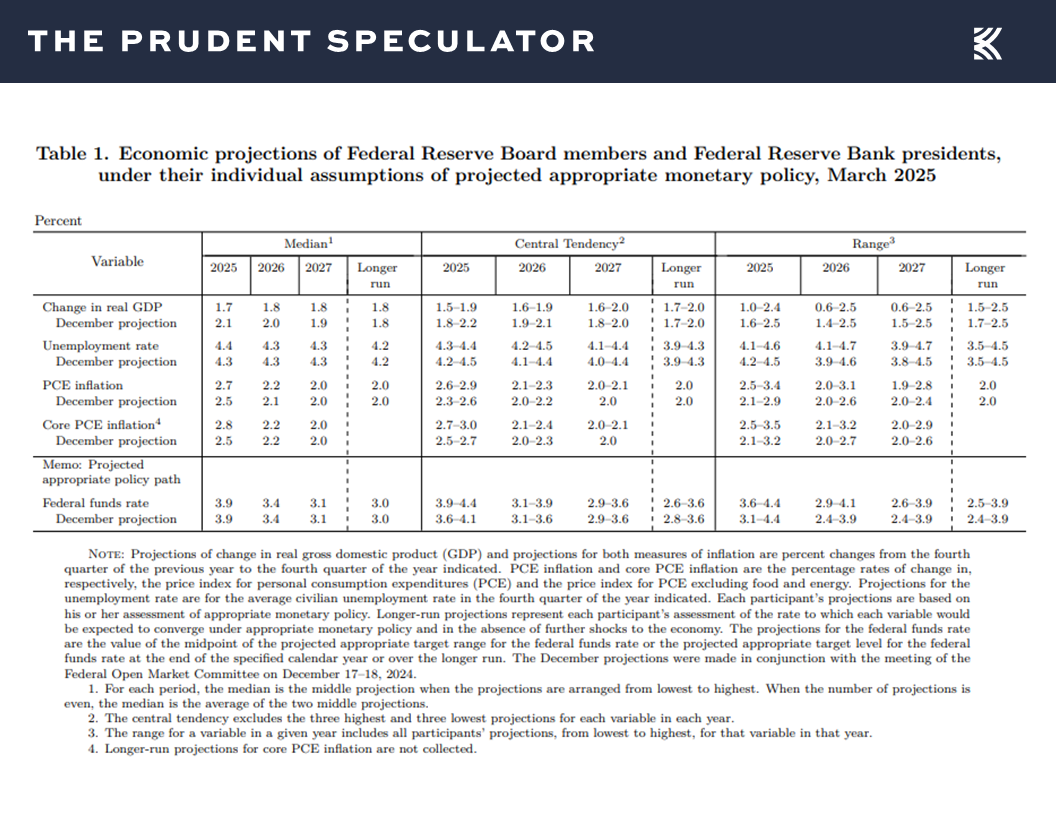

and the Federal Reserve recently projecting 1.7% real GDP growth for this year,

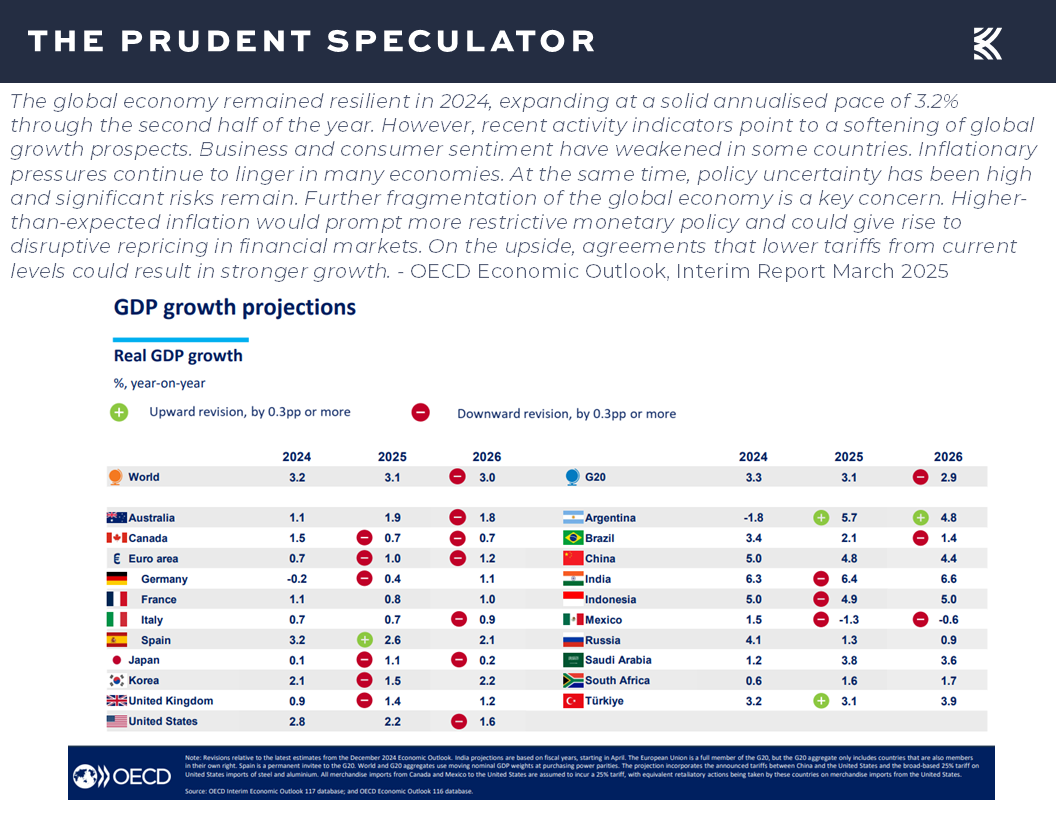

and the OECD offering 2.2% U.S. GDP growth as its latest estimate.

To be sure, those forecasts are now nearly two weeks old, and the latest estimate from the Atlanta Fed is calling for an economic contraction for Q1 2025,

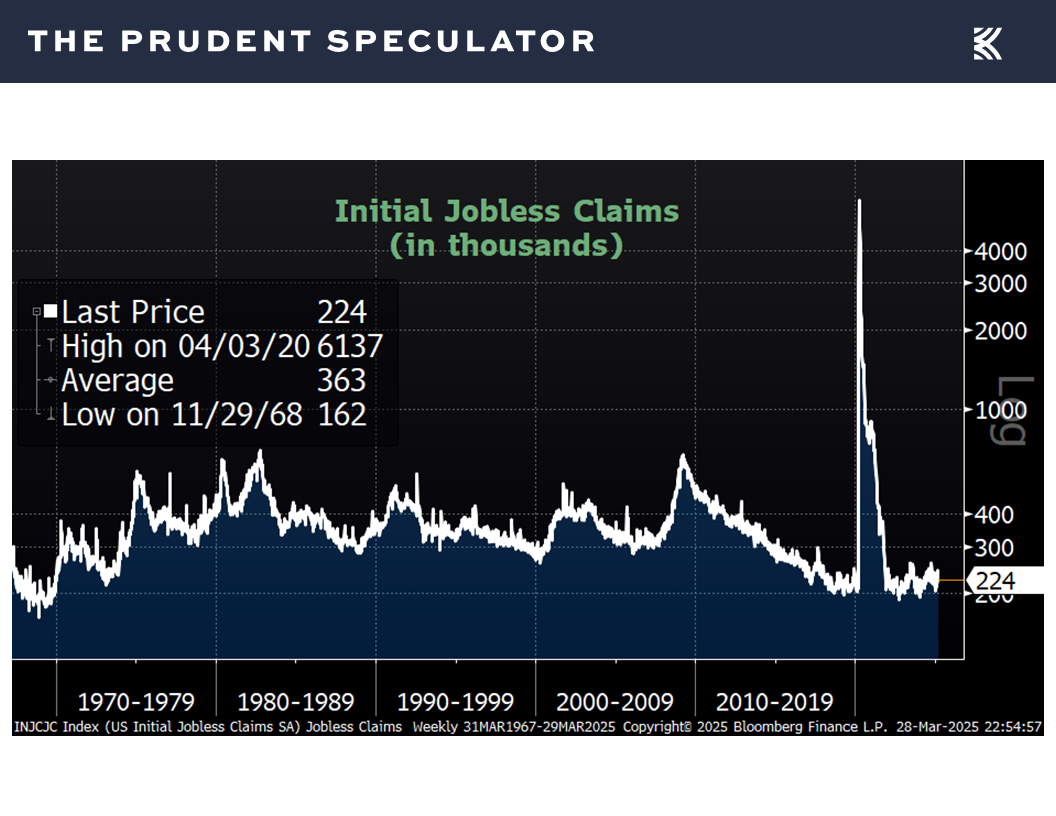

but the “hard” statistics out last week showed the economy to be holding up well. First-time filings for unemployment benefits of 224,000 in the latest week was slightly better than expected and continued to reside near multi-generational lows,

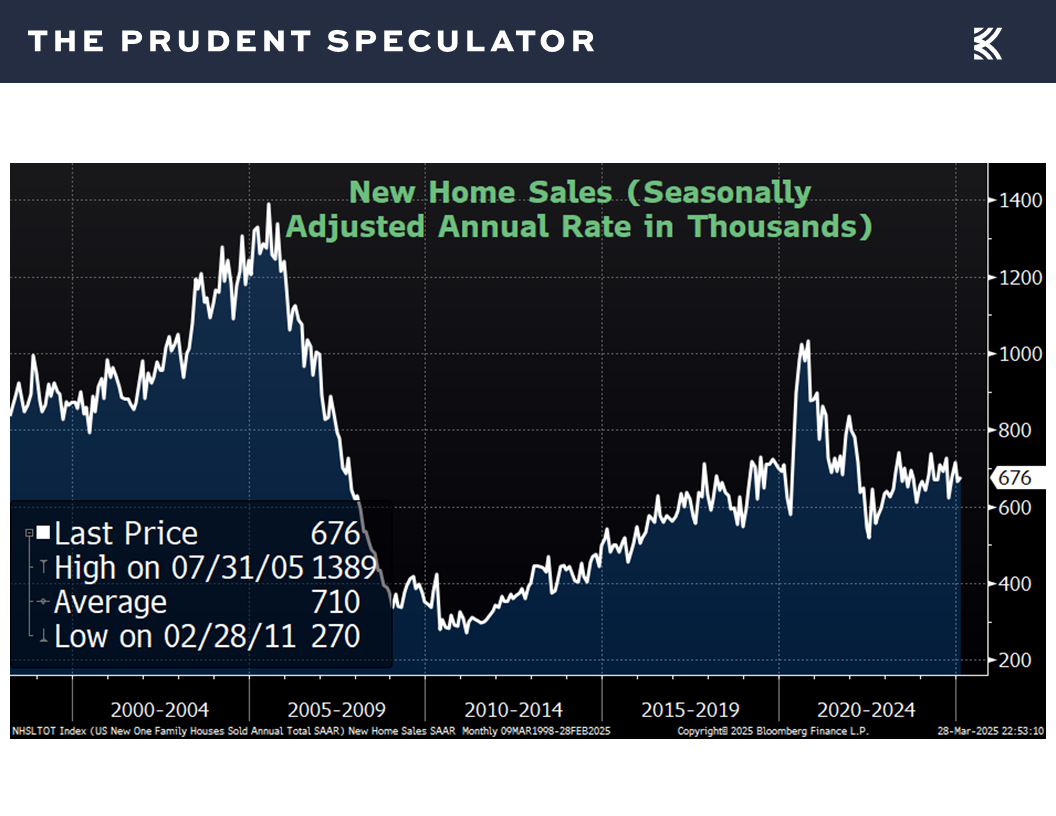

new home sales increased in February to a seasonally adjusted annual rate of 676,000, up from a revised 664,000 in January,

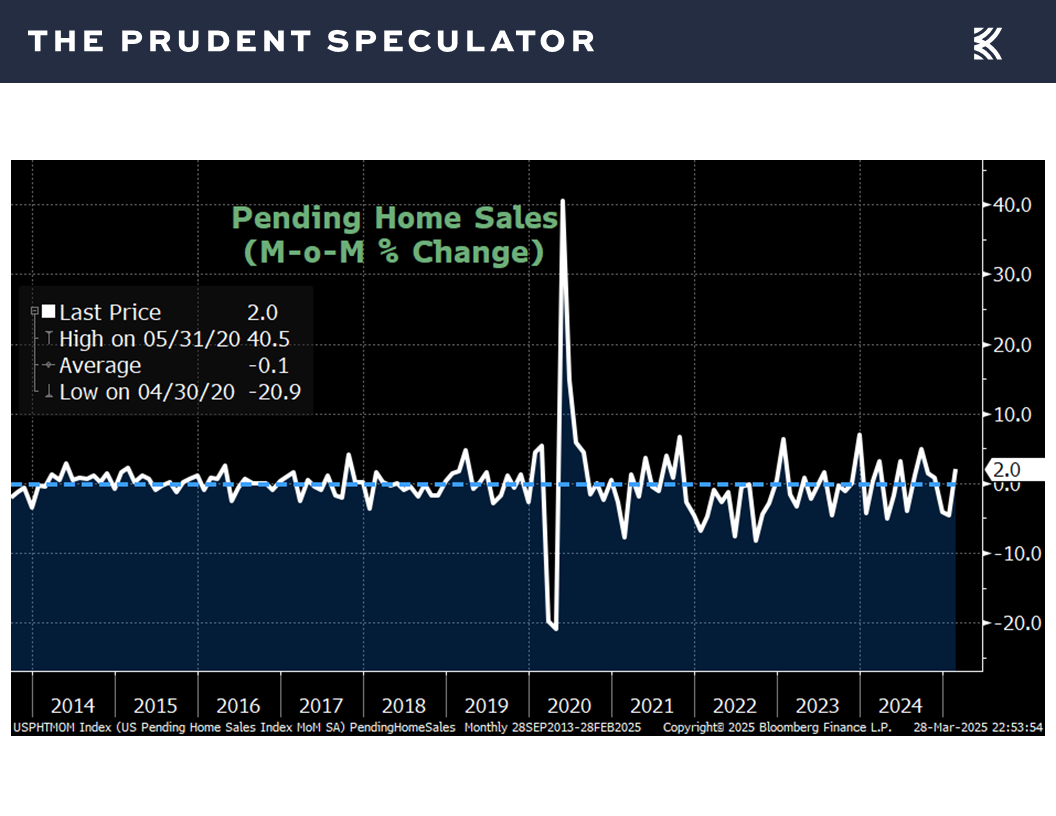

pending home sales last month rose 2.0% as compared to January, better than the 1.0% projected increase,

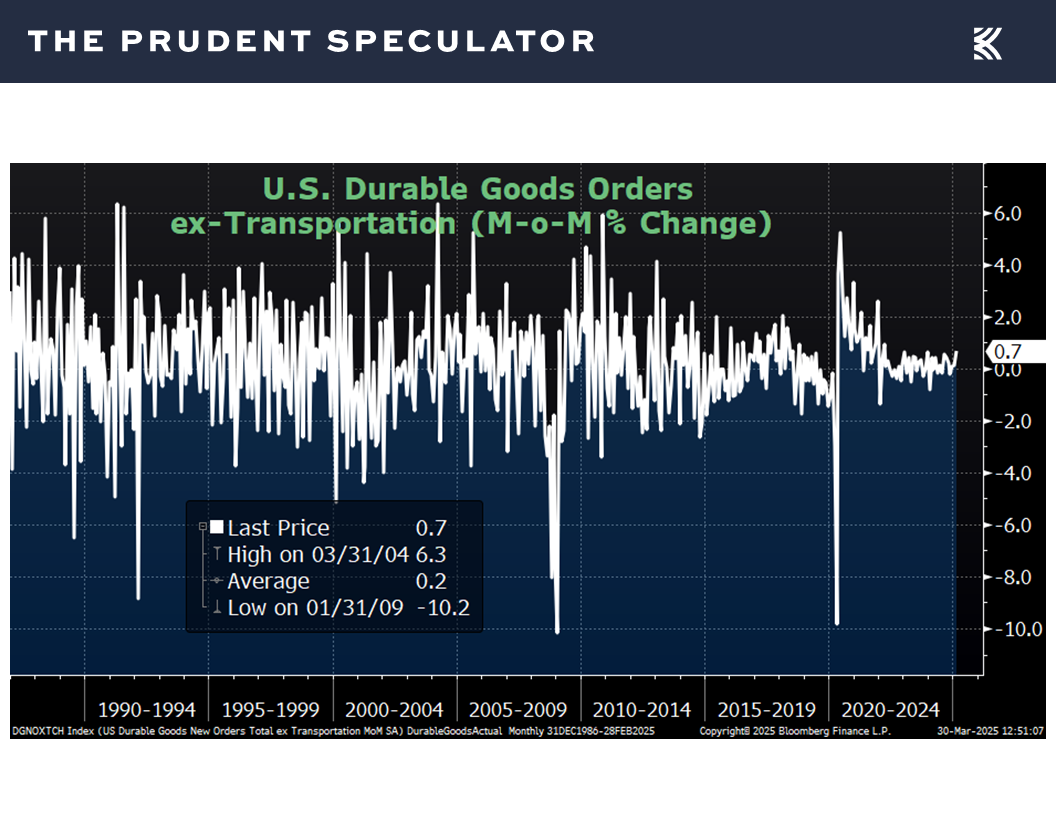

and durable goods orders excluding the volatile transportation sector climbed a better-than-forecast 0.7% in February.

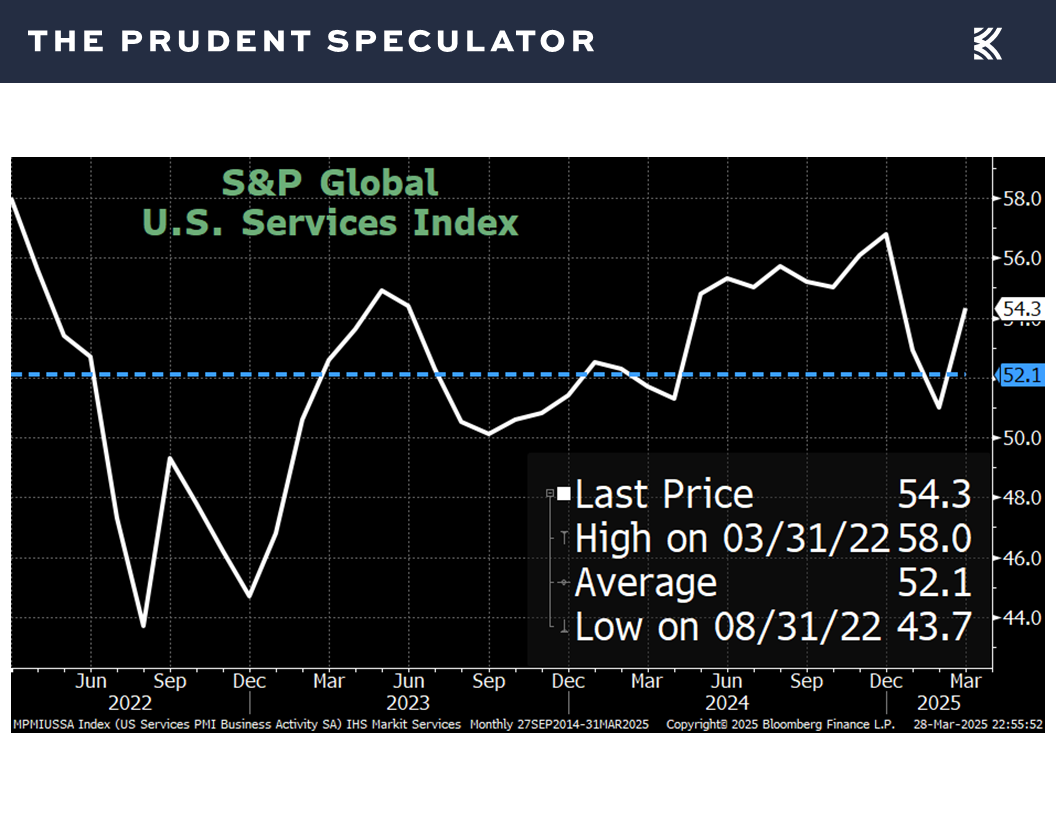

To be sure, those “hard” figures on what has been happening in the economy are a rear-view-mirror view, and so-called “soft” numbers of how folks are feeling about the economy going forward are not painting a rosy picture. Indeed, although S&P Global’s U.S. Services Purchasing Manager Index (PMI) rose to 54.3 in March, nicely above expectation and the 51.0 reading for February,

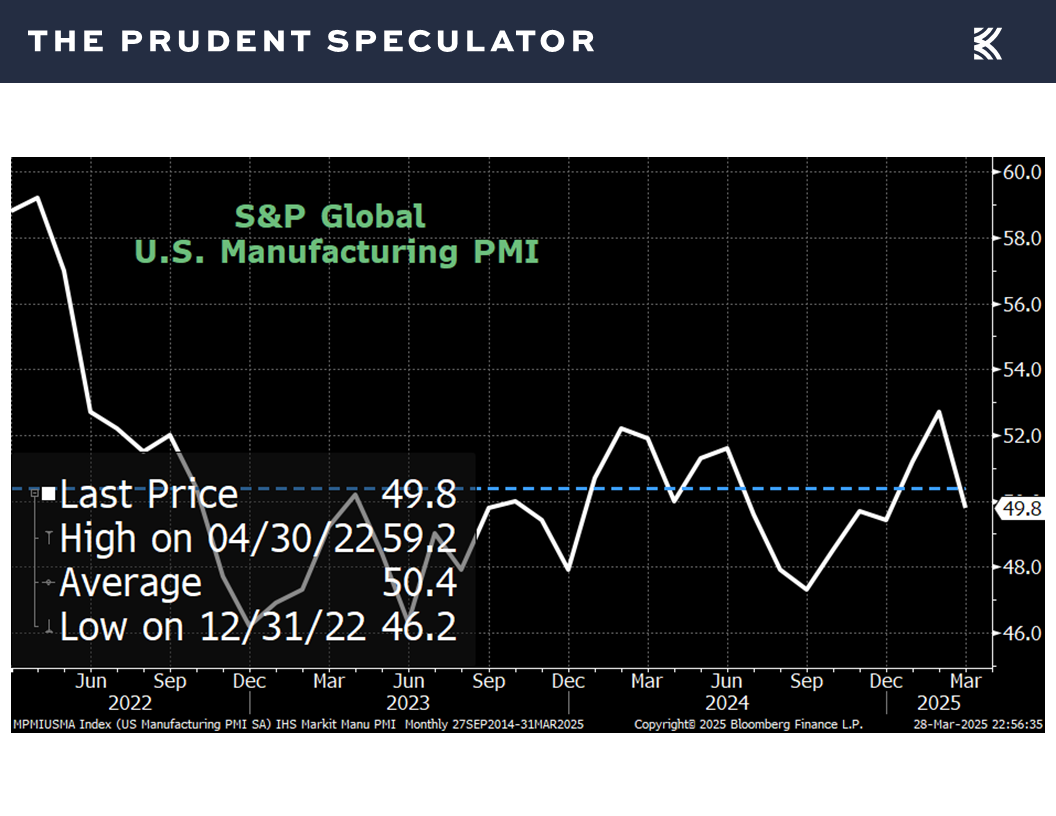

S&P Global’s U.S. Manufacturing PMI fell to 49.8 this month from 52.7 the month prior, and well below the 51.7 forecast.

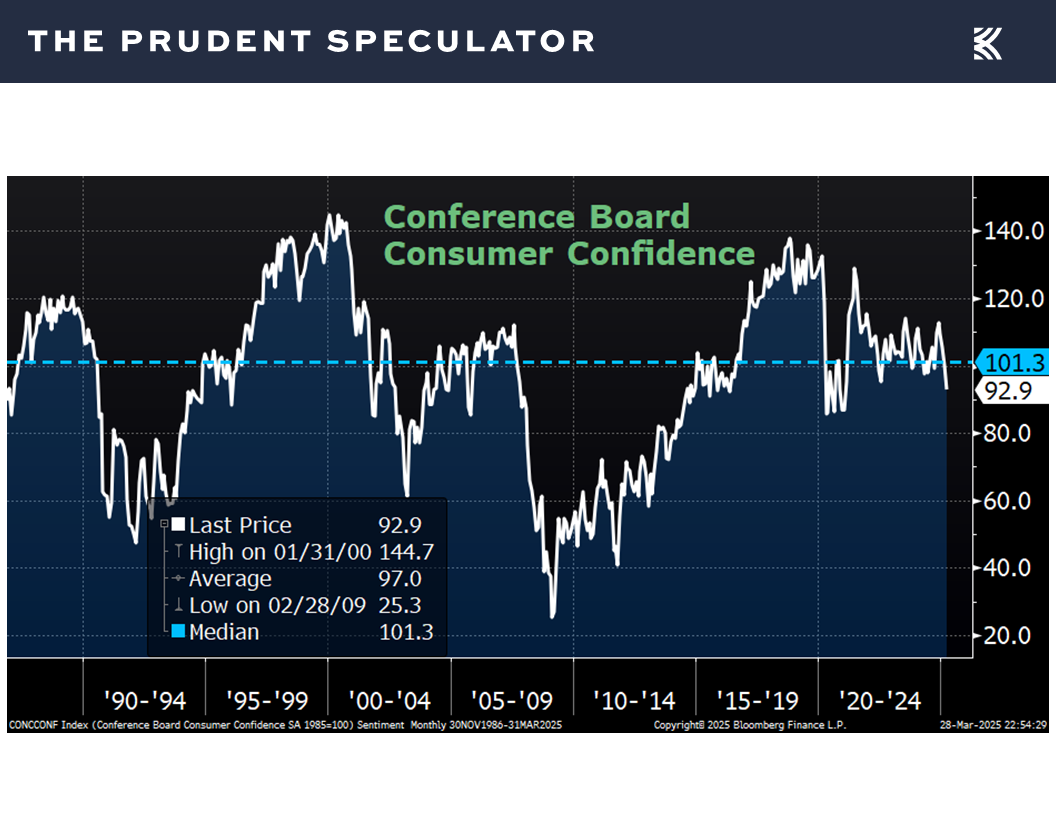

Meanwhile, two gauges on the health of the consumer came in very weak, with the Conference Board’s Consumer Confidence tally for March falling to 92.9, below estimates of 94.0 and down from a revised 100.1 in February,

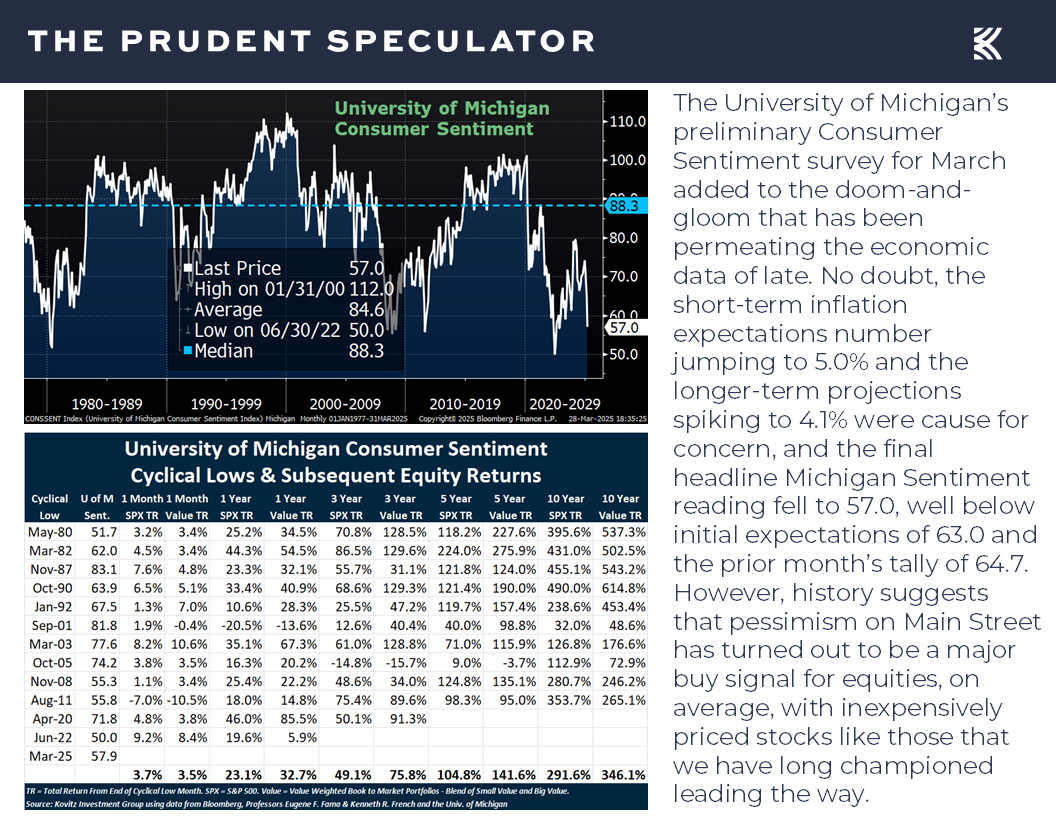

and the Univ. of Michigan’s final Consumer Sentiment reading edging down to 57.0 from a preliminary figure of 57.9, though history suggests equity investors might not be unhappy that folks are not enthusiastic about their near-term prospects.

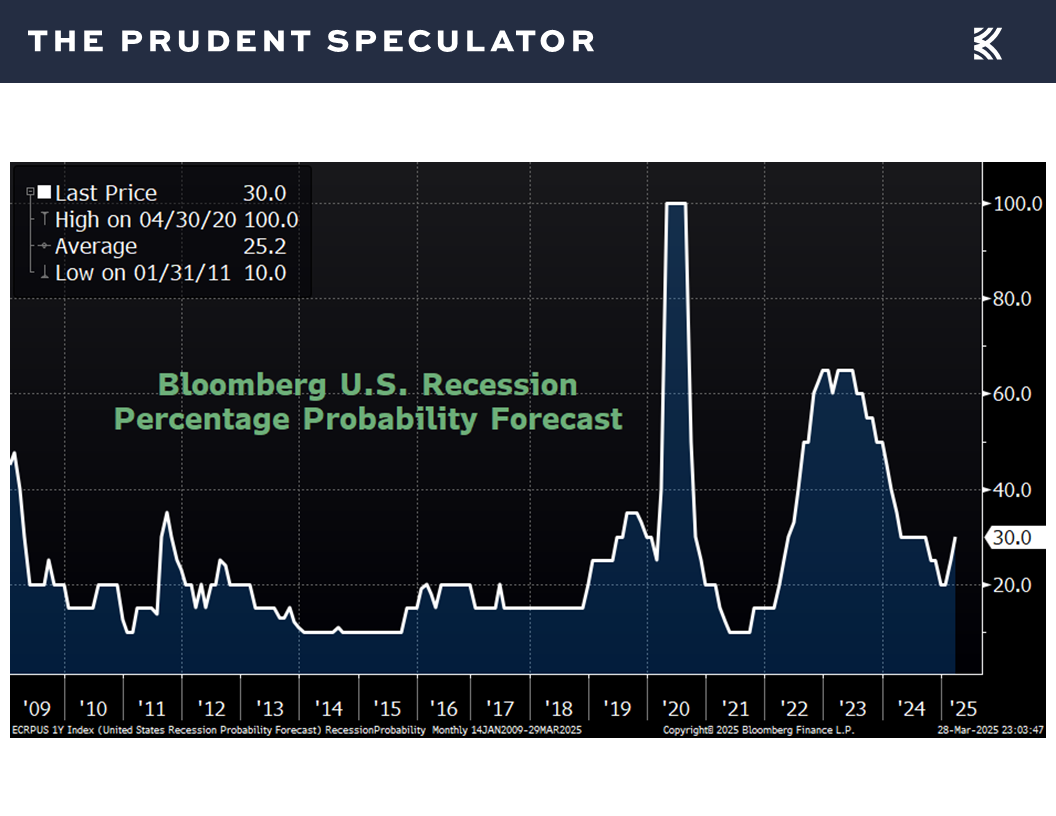

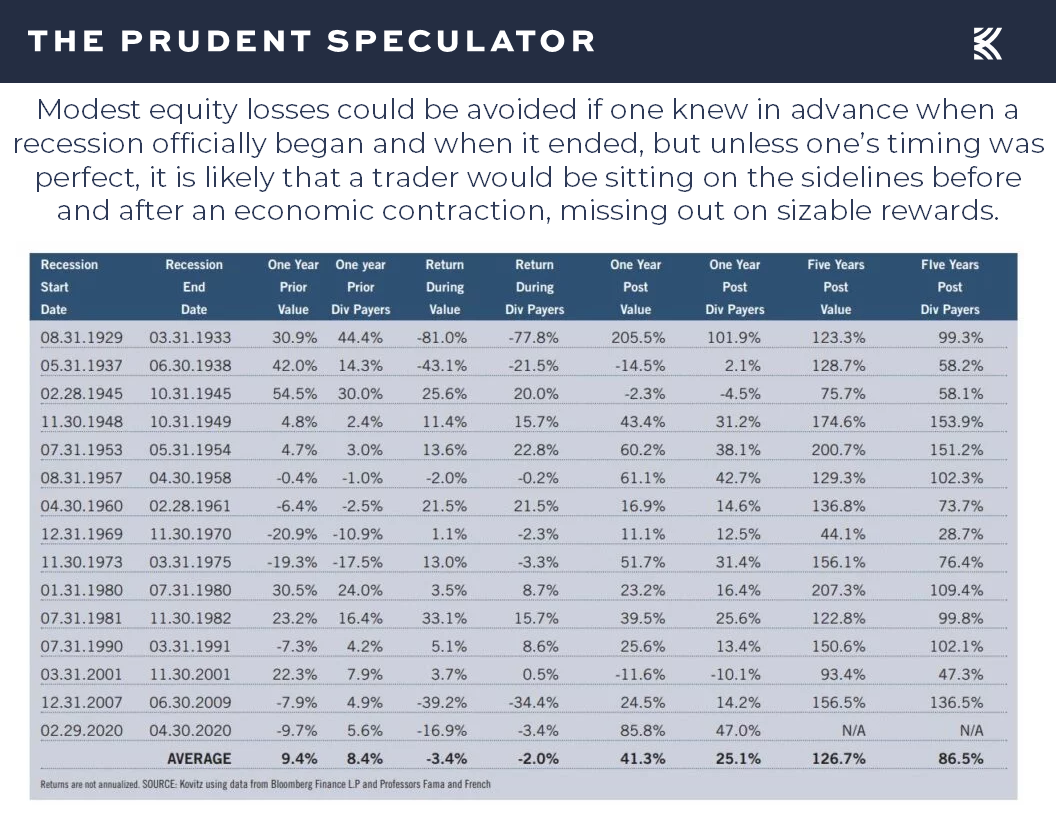

Recessions – Risk Isn’t High Today, But History Shows Staying the Course the Right Move Even if a Contraction Eventually Was to Occur

While Federal Reserve Chair Jerome H. Powell had the following to say at his Press Conference on March 19, 2025,

So, let’s start with the hard data. You know, we do see pretty solid hard data still. So, growth looks like it’s maybe moderating a bit, consumer spending moderating a bit, but still at a solid pace. Unemployment’s 4.1 percent, job creation most recently has been at a healthy level. Inflation has started to move up now, we think partly in response to tariffs and there may be a delay in further progress over the course of this year. So, that’s the hard data. Overall, it’s a solid picture. The survey data, of both household and businesses, show significant rise in uncertainty and significant concerns about downside risks. So how do we think about that? And that’s the, that is the question, as I mentioned the other day, as you pointed out, the relationship between survey data and actual economic activity hasn’t been very tight, there have been plenty of times where people are saying very downbeat things about the economy and then going out and buying a new car. But we don’t know that that will be the case here. We will be watching very carefully for signs of weakness in the real data. Of course we will. But I, you know, given where we are, we think our policy is in a good place to react to what comes, and we think that the right thing to do is to wait here for, you know, for greater clarity about what the economy is doing.

…we respect that recession worries have been ratcheting higher,

but we offer the friendly reminder that even those paid to determine the start and end dates of economic contractions have a very difficult time, while equity market gains prior to recessions have been solid, on average, and the post-recession performance for Value Stocks and Dividend Payers has been sensational, again on average.

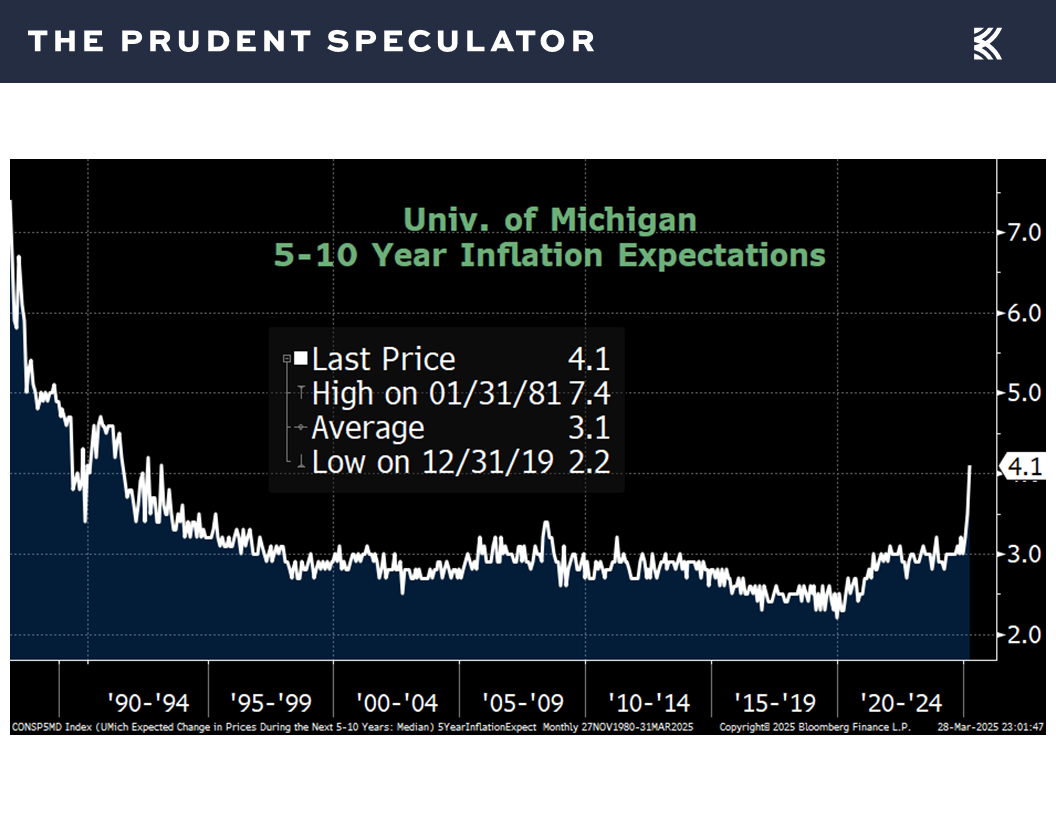

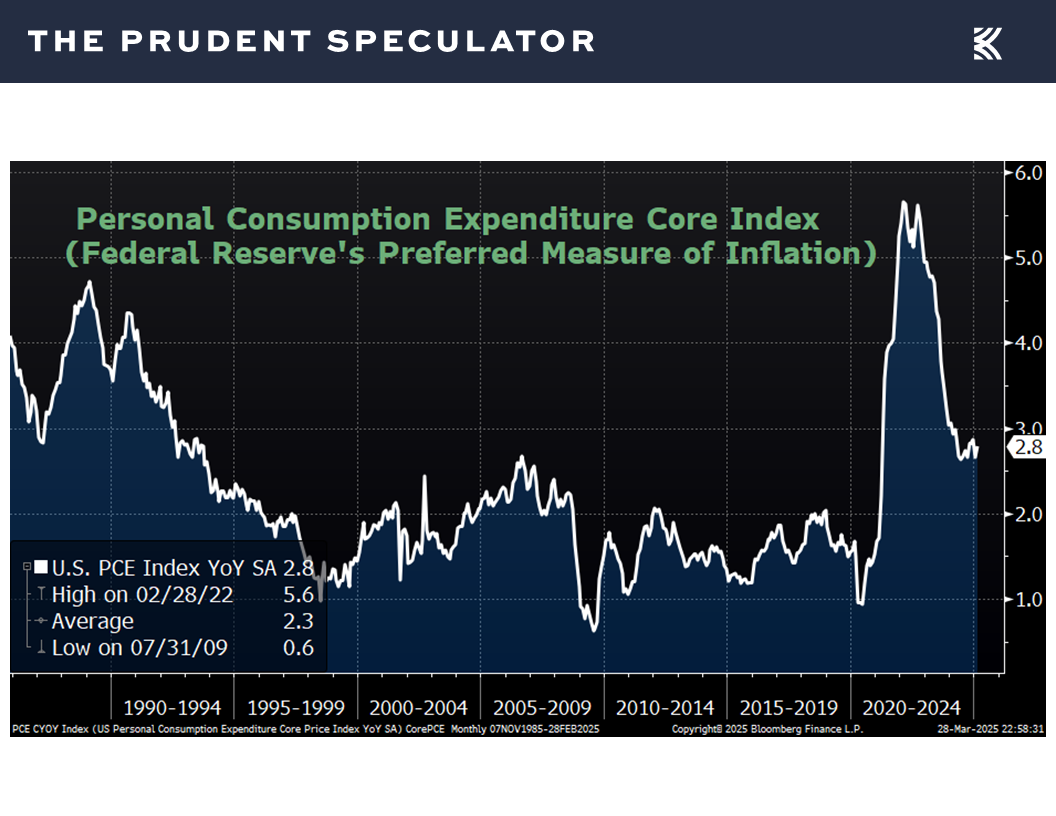

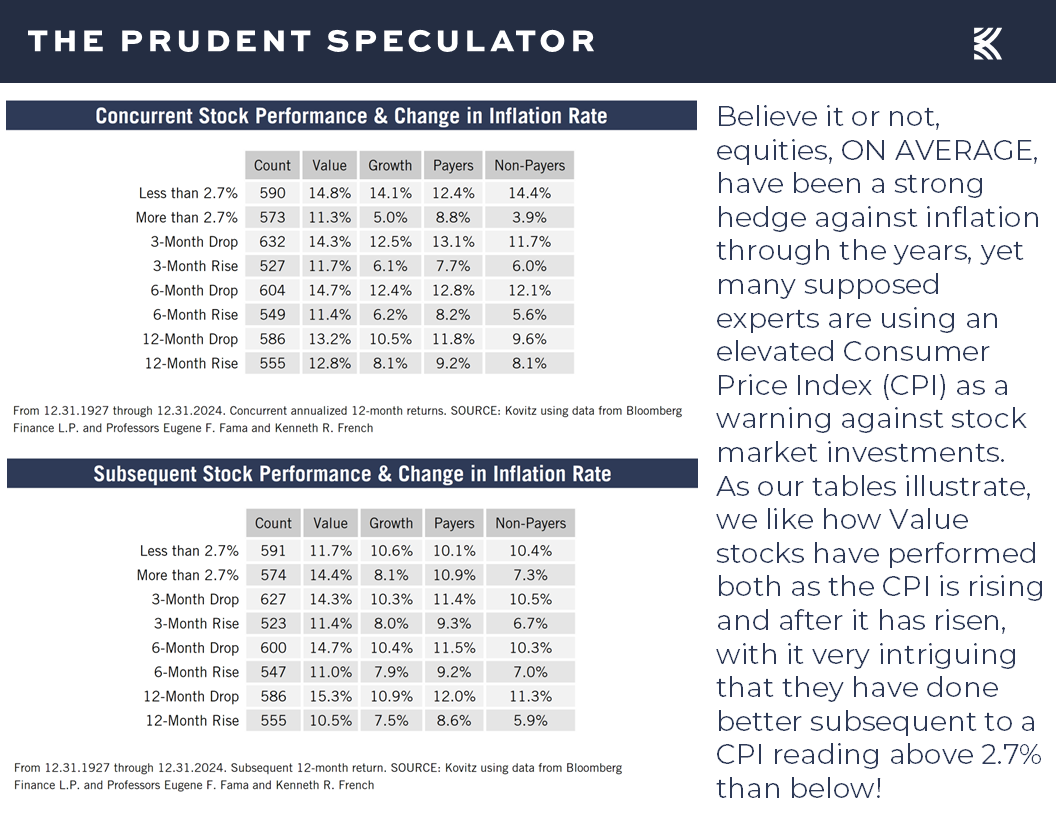

Inflation – Long-Term Expectations and PCE Rise; Stocks a Great Hedge Historically

No doubt, many are also concerned about inflation, given that the Univ. of Michigan’s long-term inflation expectations number rose last week to 4.1%, a multi-decade high,

while the Federal Reserve’s preferred measure of pricing pressures, the Core (excluded food and energy) Personal Consumption Expenditures (PCE) for February edged higher to a 2.8% increase, above the 2.7% estimate and up from a revised 2.7% in January.

Clearly, elevated inflation is not something to be dismissed, but history shows that equities, especially Value Stocks and Dividend Payers, have performed fine, on average, whether consumer prices are rising or falling, both concurrent with and subsequent to moves in the underlying index.

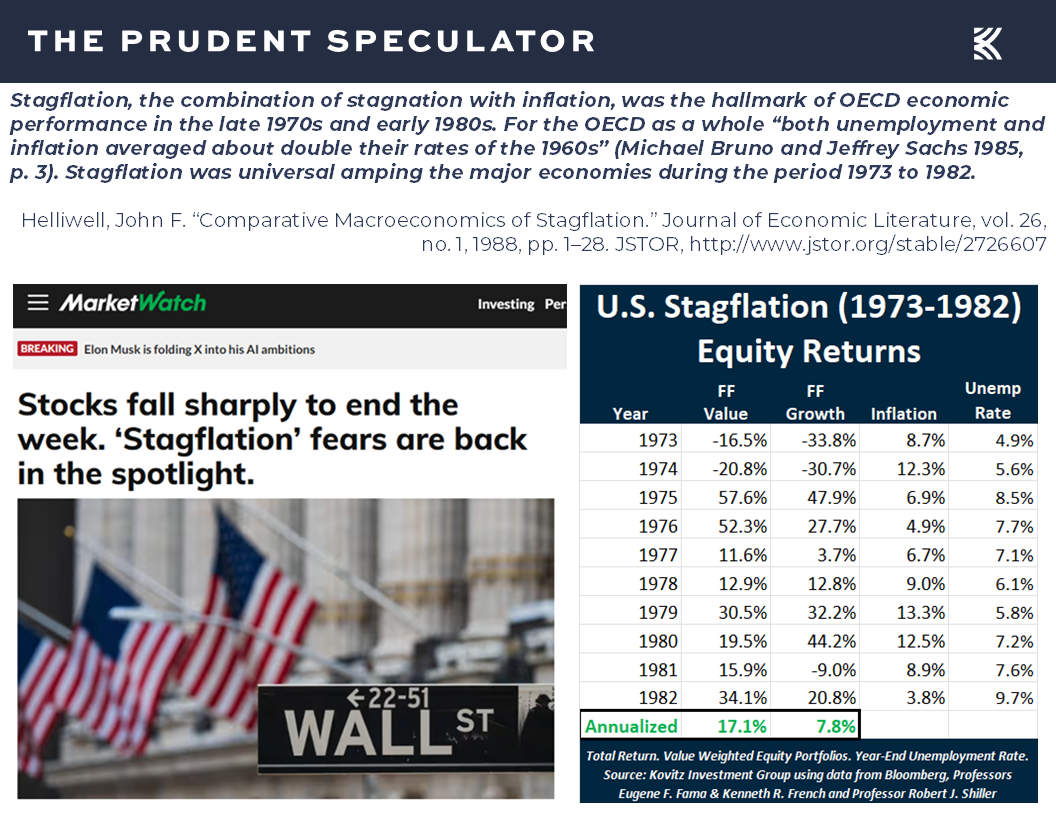

Stagflation – Historical Equity Returns from 1973-1982

Yes, we have started to hear talk of the dreaded stagflation (economic stagnation with inflation), as happened in the U.S. from 1973 to 1982, but we are a long way away from that environment. That does not mean that it couldn’t materialize, so we thought it valuable to look at what happened with stocks over that prior 10-year period. Happily, though it was an awful first two years, the performance for Value Stocks for the full 10-years was 17.1% per annum, well above the long-term average!

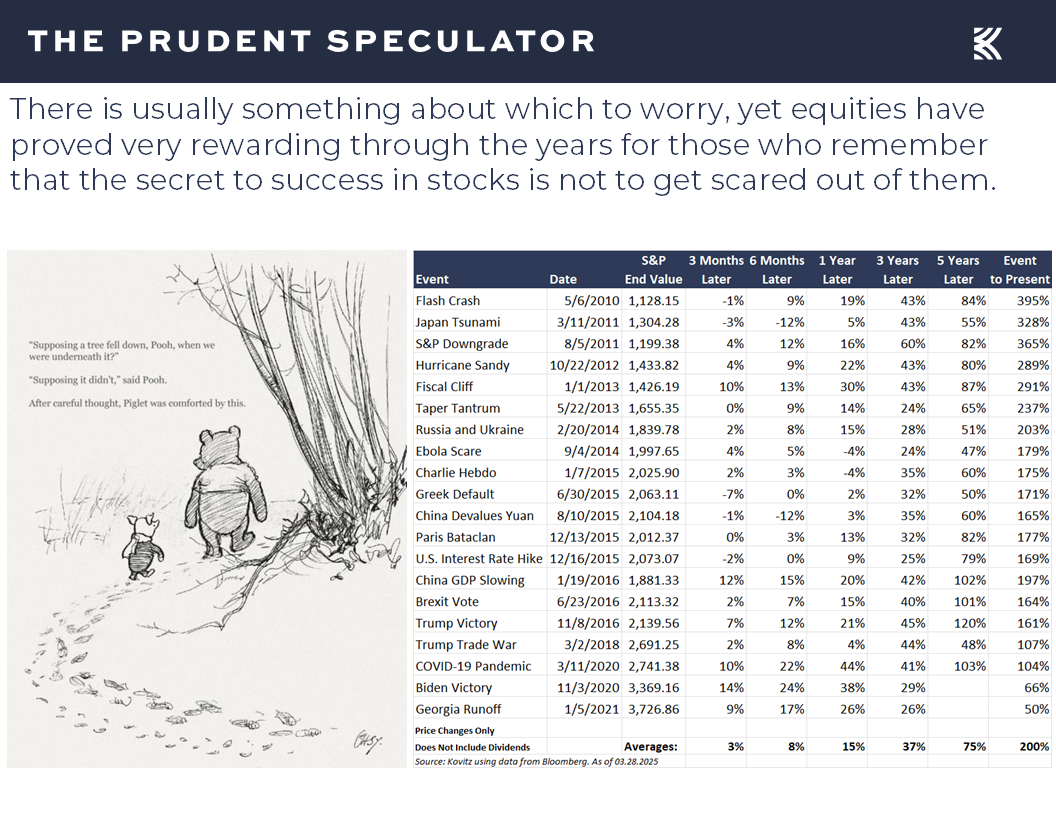

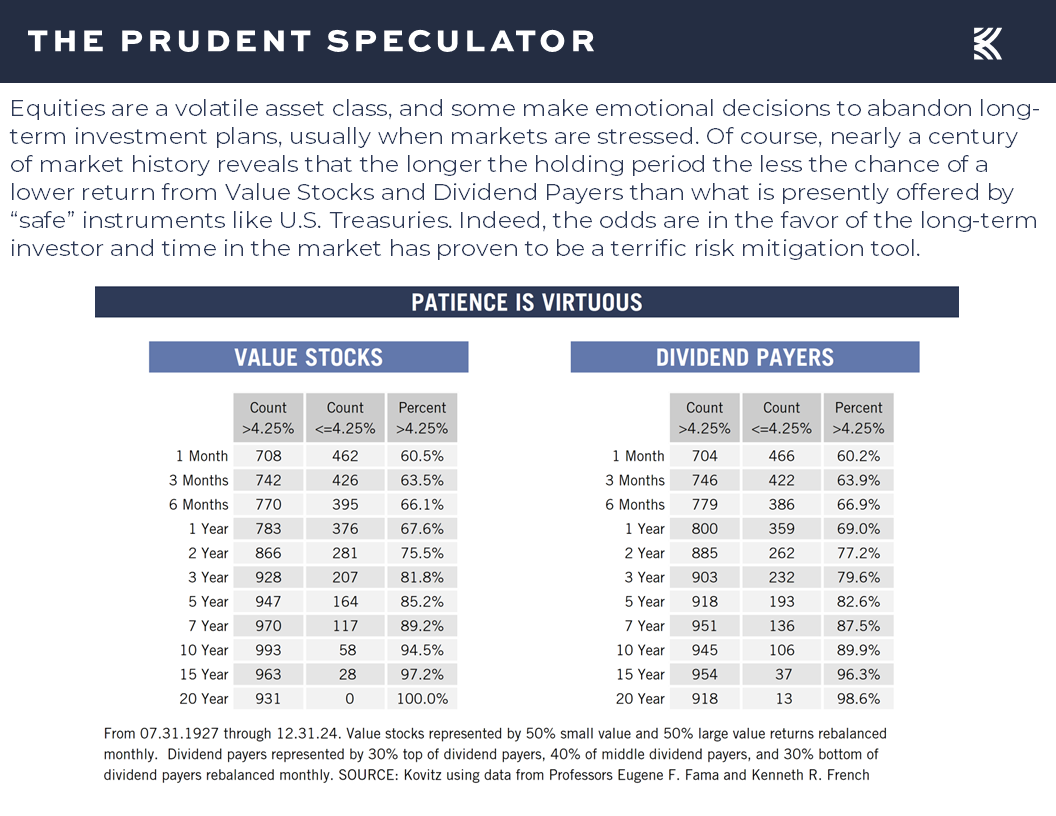

Patience – The Longer the Hold the Better the Chance of Success

Anything can happen in the weeks and months ahead, and the equity futures are suggesting that the new trading week is likely to begin on a sour note, so we continue to be braced for additional downside volatility, but we know that market history shows that all disconcerting events have been overcome and then some in the fullness of time,

while a patient long-term-oriented approach is a major risk mitigation tool.

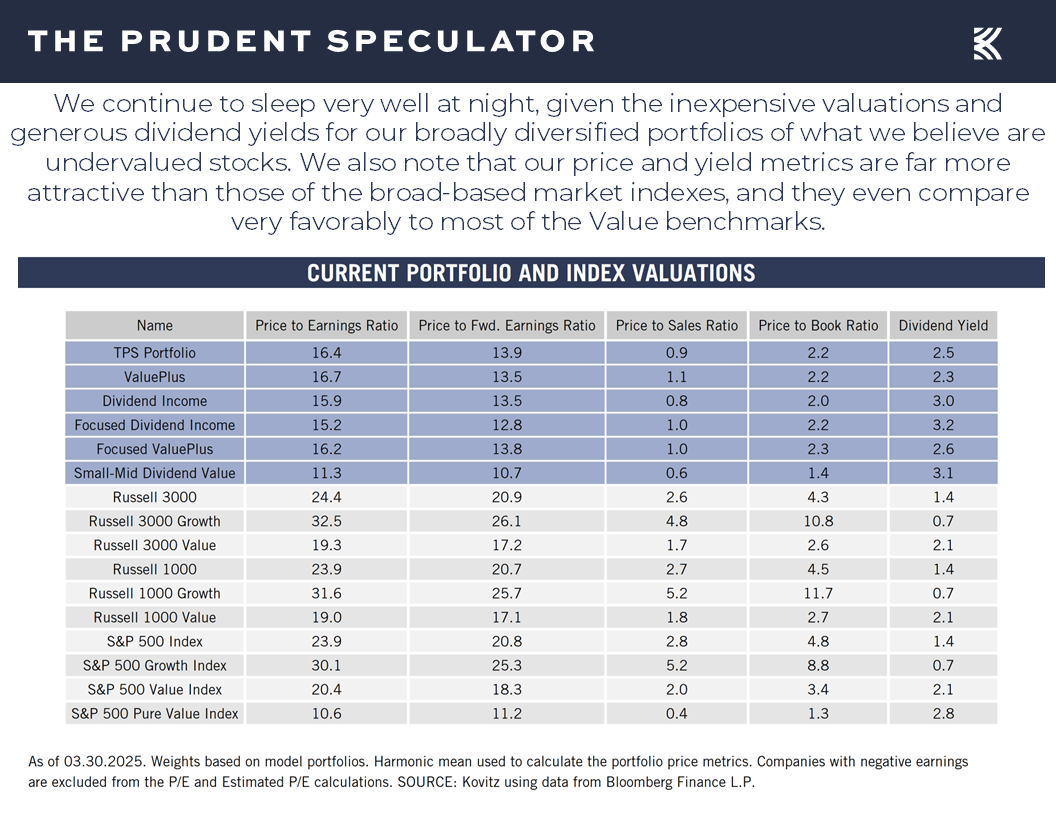

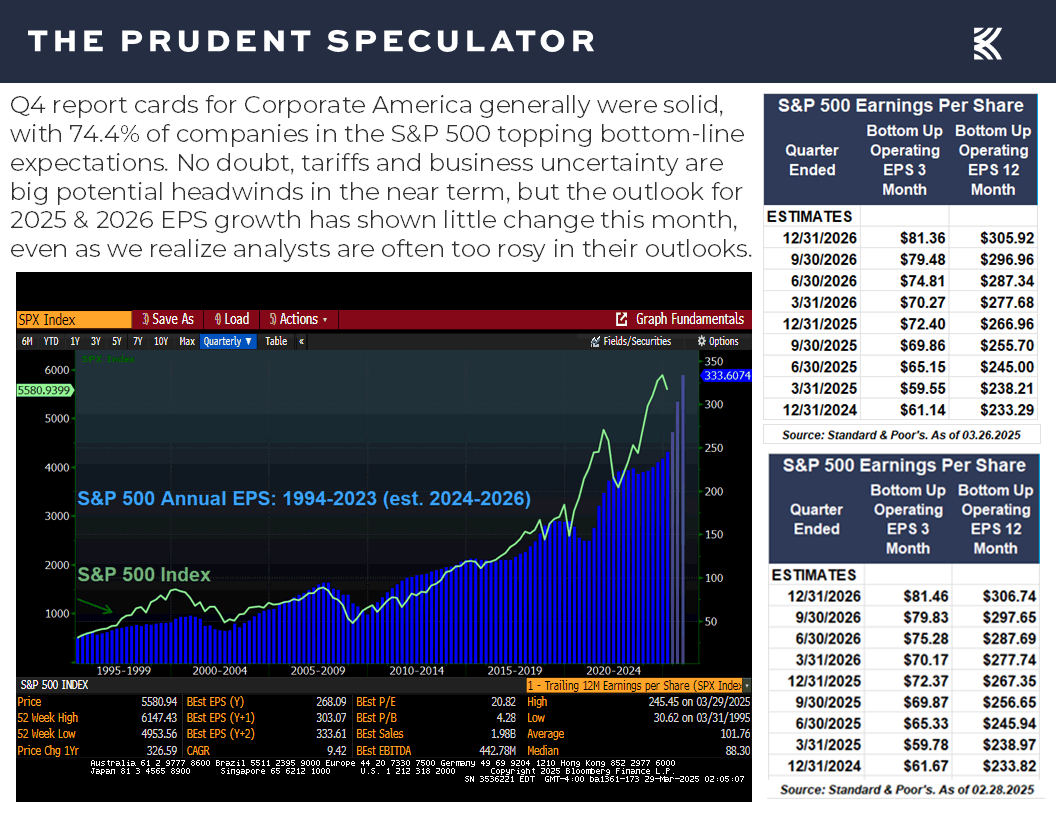

Valuations – Liking the Metrics on our Portfolios

Even more important, we remain very comfortable with the reasonable valuation metrics and generous dividend yields on our broadly diversified portfolios of what we believe are undervalued stocks,

especially as the outlook for corporate profit growth this year and next remains solid…at least as of this moment.

Stock News – Updates on 3 auto-makers and a paper manufacturer

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

AAII Sentiment, Economic News, Recessions and Stagflation

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss AAII Sentiment, Economic News, Recessions and Stagflation. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – Three Sales Across 4 Portfolios

Buckingham AAII Appearance – San Diego, April 12, 2025

Week – Friday Plunge Sends the 5 Days into the Red

Corrections – 10% Declines Happen with Surprising Frequency

Sentiment – Major AAII Contrarian Buy Signal

Econ News – “Hard” Numbers Solid but “Soft” Figures Weaken; GDP Growth Still the Forecast

Recessions – Risk Isn’t High Today, But History Shows Staying the Course the Right Move Even if a Contraction Eventually Was to Occur

Inflation – Long-Term Expectations and PCE Rise; Stocks a Great Hedge Historically

Stagflation – Historical Equity Returns from 1973-1982

Patience – The Longer the Hold the Better the Chance of Success

Valuations – Liking the Metrics on our Portfolios

Stock News – Updates on 3 auto-makers and a paper manufacturer

Buckingham AAII Appearance – San Diego, April 12, 2025

Your Editor will be speaking in San Diego on Saturday, April 12, 2025, at 9:00 AM. Registration info for that presentation is available here:

Upcoming Chapter Events – AAII San Diego

Week – Friday Plunge Sends the 5 Days into the Red

With all the decline and then some coming on Friday, stocks endured another tough week of trading as the S&P 500 retreated 1.53% on a price basis over the latest five-day period. Believe it or not, there have been 970 weeks over the last 97 years with a drop of equal or greater magnitude, or 10 weekly occurrences per annum on average, so volatility is par for the equity market course.

Corrections – 10% Declines Happen with Surprising Frequency

While the S&P thus far has held above its low of March 13, 2025, in which it entered the 39th correction of 10% since the launch of The Prudent Speculator 48 years ago,

sizable pullbacks happen every year, with the current skid thus far modest by historical standards.

Sentiment – Major AAII Contrarian Buy Signal

Of course, though the size of the setback is relatively tame, it is fascinating to see the level of consternation gripping folks on Main Street, with the latest Sentiment Survey from the American Association of Individual Investors (AAII) continuing to show a preponderance of pessimism,

as the overall Bearishness is on par or worse than it was at the equity market bottoms during the Great Financial Crisis and the COVID-19 Pandemic.

Past performance is never a guarantee of future performance, but nearly 38 years of AAII market history shows that it generally has paid off handsomely to be greedy when others are fearful,

and very greedy when others are very fearful,

while over the long-term, equities have enjoyed far more time in the green than they have in the red, so much so that returns for Value Stocks and Dividend Payers have averaged double-digit annual percentages going all the way back to the 1920s.

Econ News – “Hard” Numbers Solid but “Soft” Figures Weaken; GDP Growth Still the Forecast

Of course, though we have long believed that uncertainty is the friend to the buyer of long-term value, we realize that tariffs, real and threatened, are not helping investors remain on an even emotional keel, especially with so-called “Liberation Day” happening on April 2. Obviously, this time is different, as is every time, but we have been down the tariff road previously,

while the U.S. economy entered 2025 in good shape, relatively speaking, with Q4 2024 real (inflation-adjusted) GDP growth having been revised up last week to 2.4%,

and the Federal Reserve recently projecting 1.7% real GDP growth for this year,

and the OECD offering 2.2% U.S. GDP growth as its latest estimate.

To be sure, those forecasts are now nearly two weeks old, and the latest estimate from the Atlanta Fed is calling for an economic contraction for Q1 2025,

but the “hard” statistics out last week showed the economy to be holding up well. First-time filings for unemployment benefits of 224,000 in the latest week was slightly better than expected and continued to reside near multi-generational lows,

new home sales increased in February to a seasonally adjusted annual rate of 676,000, up from a revised 664,000 in January,

pending home sales last month rose 2.0% as compared to January, better than the 1.0% projected increase,

and durable goods orders excluding the volatile transportation sector climbed a better-than-forecast 0.7% in February.

To be sure, those “hard” figures on what has been happening in the economy are a rear-view-mirror view, and so-called “soft” numbers of how folks are feeling about the economy going forward are not painting a rosy picture. Indeed, although S&P Global’s U.S. Services Purchasing Manager Index (PMI) rose to 54.3 in March, nicely above expectation and the 51.0 reading for February,

S&P Global’s U.S. Manufacturing PMI fell to 49.8 this month from 52.7 the month prior, and well below the 51.7 forecast.

Meanwhile, two gauges on the health of the consumer came in very weak, with the Conference Board’s Consumer Confidence tally for March falling to 92.9, below estimates of 94.0 and down from a revised 100.1 in February,

and the Univ. of Michigan’s final Consumer Sentiment reading edging down to 57.0 from a preliminary figure of 57.9, though history suggests equity investors might not be unhappy that folks are not enthusiastic about their near-term prospects.

Recessions – Risk Isn’t High Today, But History Shows Staying the Course the Right Move Even if a Contraction Eventually Was to Occur

While Federal Reserve Chair Jerome H. Powell had the following to say at his Press Conference on March 19, 2025,

So, let’s start with the hard data. You know, we do see pretty solid hard data still. So, growth looks like it’s maybe moderating a bit, consumer spending moderating a bit, but still at a solid pace. Unemployment’s 4.1 percent, job creation most recently has been at a healthy level. Inflation has started to move up now, we think partly in response to tariffs and there may be a delay in further progress over the course of this year. So, that’s the hard data. Overall, it’s a solid picture. The survey data, of both household and businesses, show significant rise in uncertainty and significant concerns about downside risks. So how do we think about that? And that’s the, that is the question, as I mentioned the other day, as you pointed out, the relationship between survey data and actual economic activity hasn’t been very tight, there have been plenty of times where people are saying very downbeat things about the economy and then going out and buying a new car. But we don’t know that that will be the case here. We will be watching very carefully for signs of weakness in the real data. Of course we will. But I, you know, given where we are, we think our policy is in a good place to react to what comes, and we think that the right thing to do is to wait here for, you know, for greater clarity about what the economy is doing.

…we respect that recession worries have been ratcheting higher,

but we offer the friendly reminder that even those paid to determine the start and end dates of economic contractions have a very difficult time, while equity market gains prior to recessions have been solid, on average, and the post-recession performance for Value Stocks and Dividend Payers has been sensational, again on average.

Inflation – Long-Term Expectations and PCE Rise; Stocks a Great Hedge Historically

No doubt, many are also concerned about inflation, given that the Univ. of Michigan’s long-term inflation expectations number rose last week to 4.1%, a multi-decade high,

while the Federal Reserve’s preferred measure of pricing pressures, the Core (excluded food and energy) Personal Consumption Expenditures (PCE) for February edged higher to a 2.8% increase, above the 2.7% estimate and up from a revised 2.7% in January.

Clearly, elevated inflation is not something to be dismissed, but history shows that equities, especially Value Stocks and Dividend Payers, have performed fine, on average, whether consumer prices are rising or falling, both concurrent with and subsequent to moves in the underlying index.

Stagflation – Historical Equity Returns from 1973-1982

Yes, we have started to hear talk of the dreaded stagflation (economic stagnation with inflation), as happened in the U.S. from 1973 to 1982, but we are a long way away from that environment. That does not mean that it couldn’t materialize, so we thought it valuable to look at what happened with stocks over that prior 10-year period. Happily, though it was an awful first two years, the performance for Value Stocks for the full 10-years was 17.1% per annum, well above the long-term average!

Patience – The Longer the Hold the Better the Chance of Success

Anything can happen in the weeks and months ahead, and the equity futures are suggesting that the new trading week is likely to begin on a sour note, so we continue to be braced for additional downside volatility, but we know that market history shows that all disconcerting events have been overcome and then some in the fullness of time,

while a patient long-term-oriented approach is a major risk mitigation tool.

Valuations – Liking the Metrics on our Portfolios

Even more important, we remain very comfortable with the reasonable valuation metrics and generous dividend yields on our broadly diversified portfolios of what we believe are undervalued stocks,

especially as the outlook for corporate profit growth this year and next remains solid…at least as of this moment.

Stock News – Updates on 3 auto-makers and a paper manufacturer

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.