The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Volatility, Inflation, Valuations, Earnings and Bank Stress Tests and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

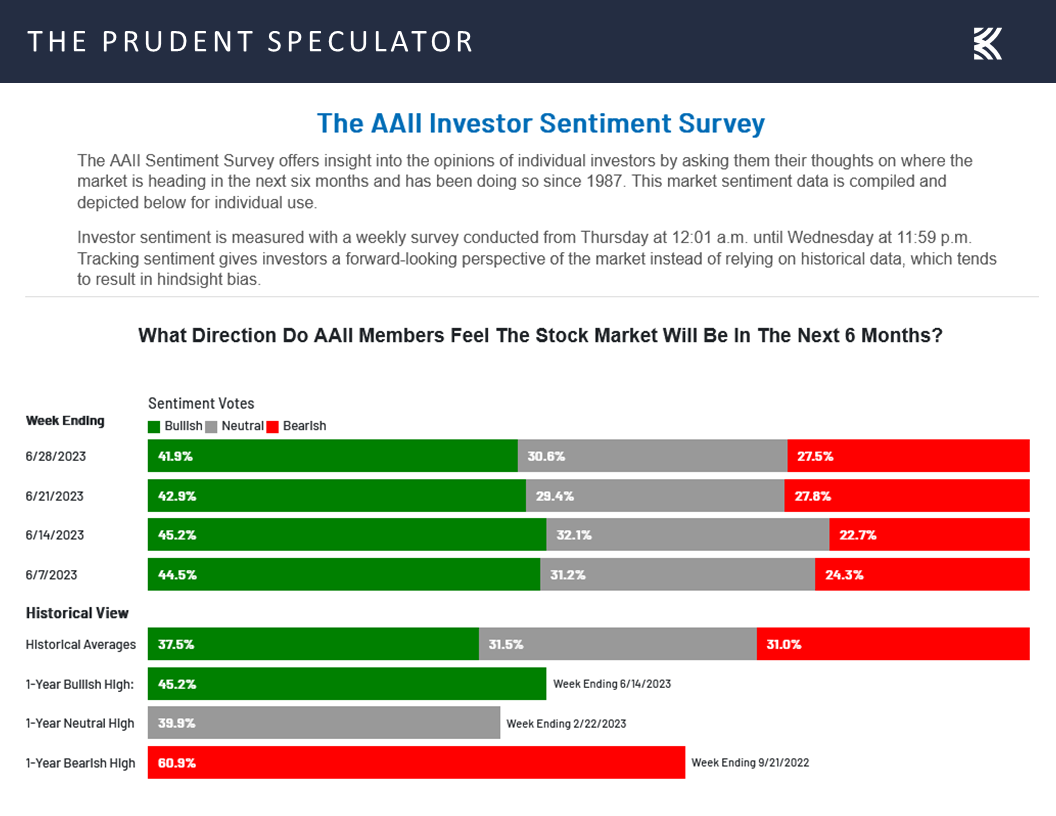

Sentiment – AAII Folks Remain Optimistic; But Stocks Rally

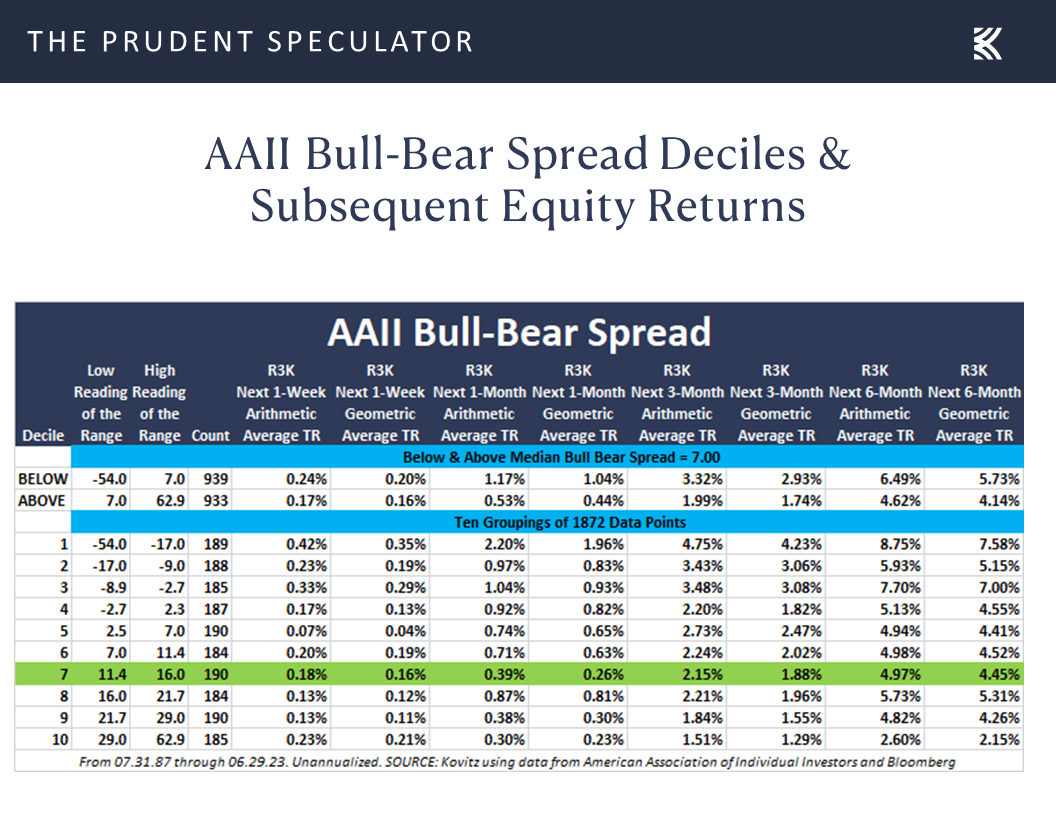

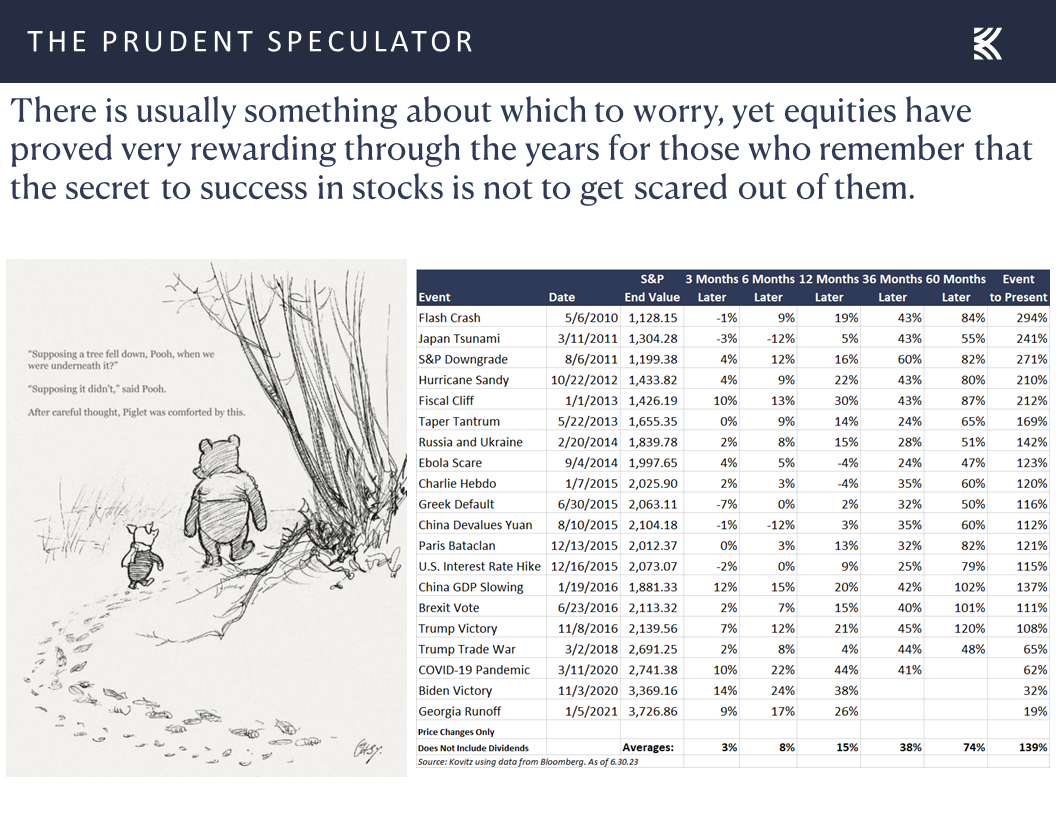

Volatility – Plenty of Disconcerting Events but Long-Term Trend in Equities is Higher

Econ Stats – Slew of Relatively Positive Numbers

Fed – Nearing the End of the Rate-Hiking Cycle

Inflation – Core PCE Better (Lower) Than Expected

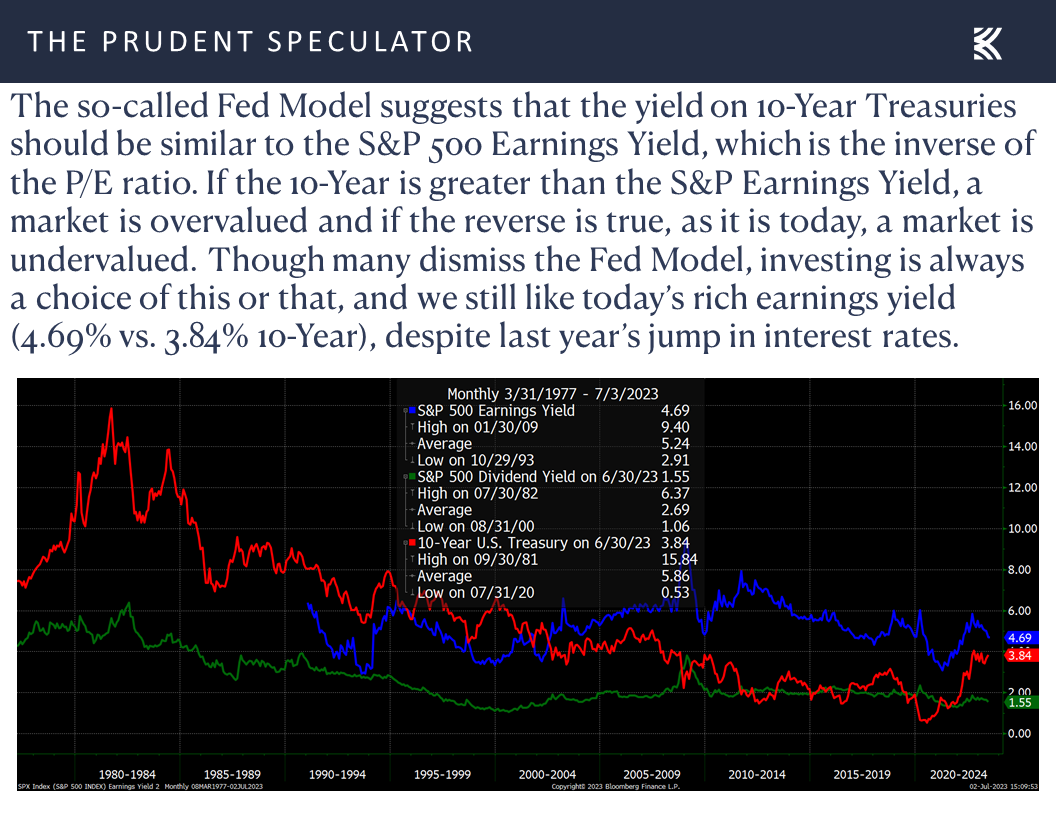

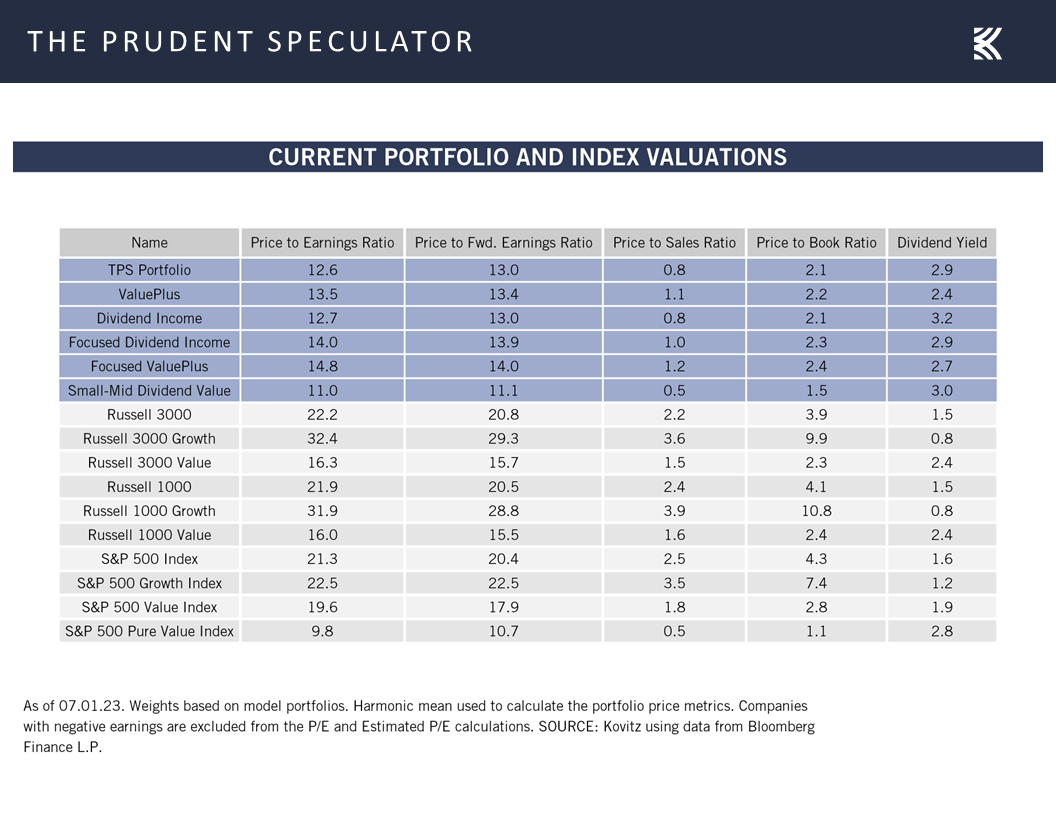

Valuations – Stocks, Especially Value, Remain Reasonably Priced

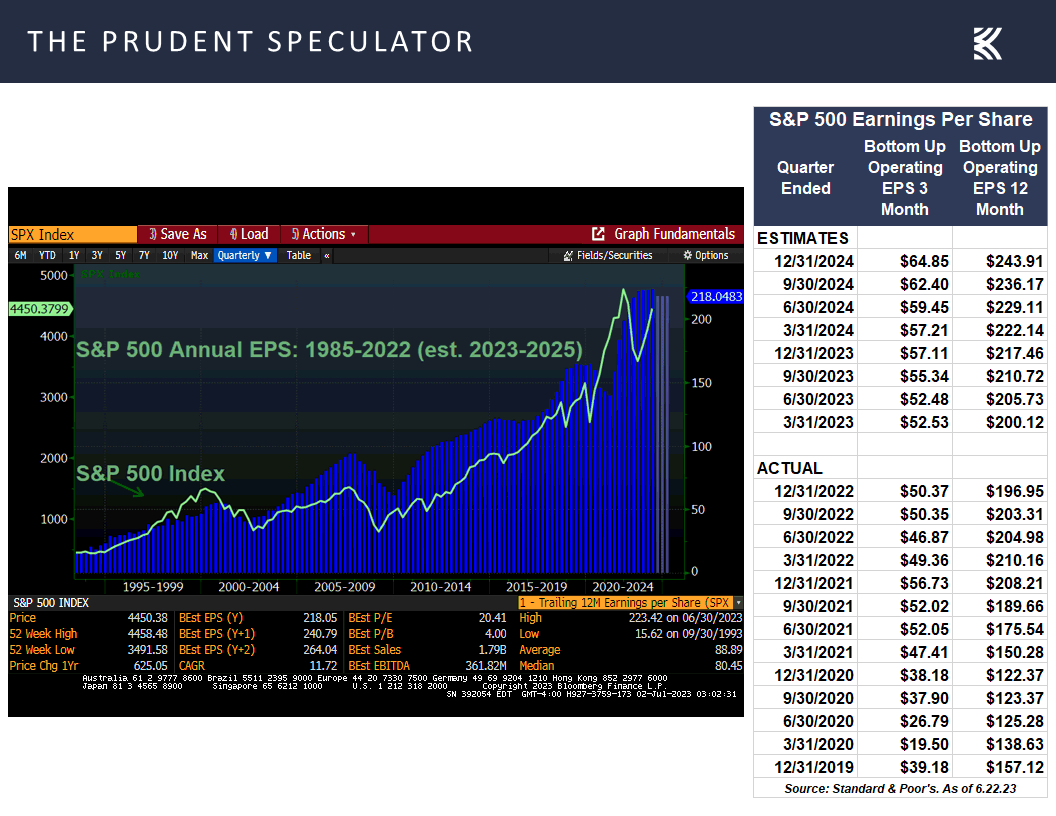

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

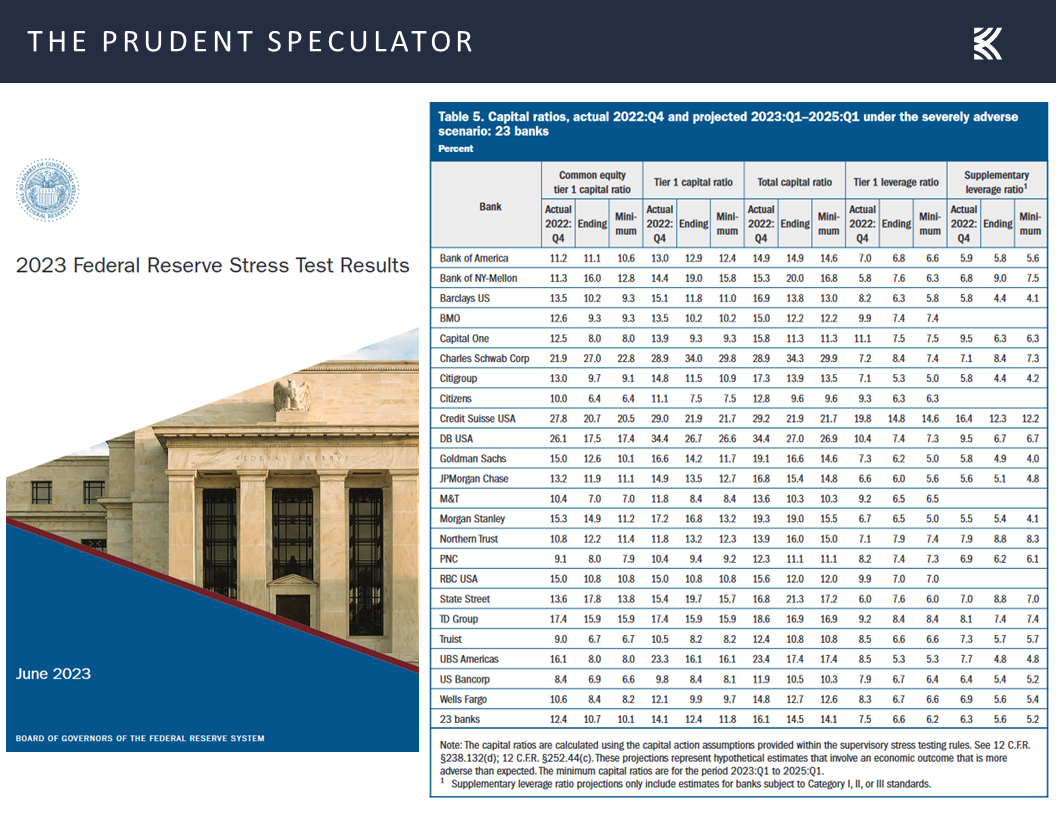

Bank Stress Tests – Passing Grades & Dividend Hikes

Stock News – Updates on three stocks across three different sectors

Sentiment – AAII Folks Remain Optimistic; But Stocks Rally

Just when it appeared an excess of bullishness might put an end to the June rally, with folks on Main Street showing quite a bit of optimism for a change, at least according to the weekly Sentiment Survey from the American Association of Individual Investors,…

the equity markets enjoyed a terrific five trading days to end the second quarter, providing more evidence that just about any way the sometimes-disconcerting data are crunched it pays to stay invested.

Volatility – Plenty of Disconcerting Events but Long-Term Trend in Equities is Higher

Certainly, there remains plenty about which to be concerned as we head into the second half of the year, but such always seems to be the case,

…yet stocks generally have provided handsome rewards, with Value leading the long-term returns race, for those who stick with them through thick and thin.

Econ Stats – Slew of Relatively Positive Numbers

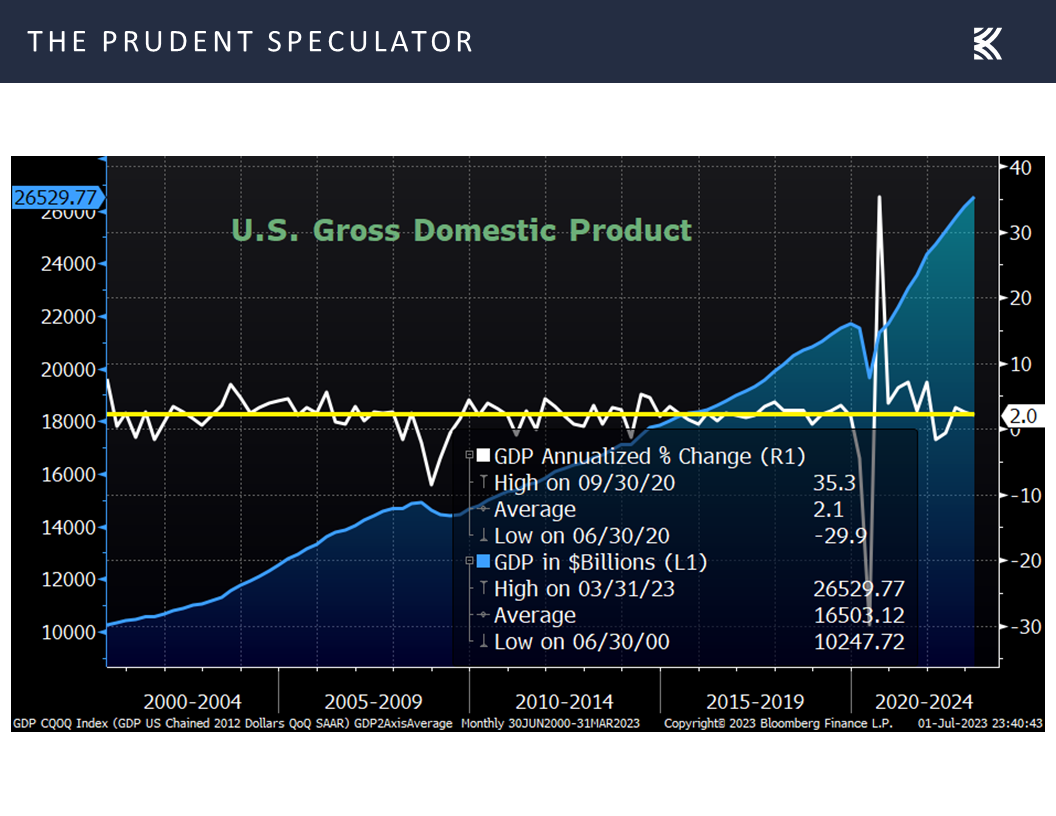

Of course, it didn’t hurt that the slew of economic data out last week generally was upbeat, with a significant upward revision to 2.0% in the real (inflation-adjusted) GDP growth calculation for the first quarter,…

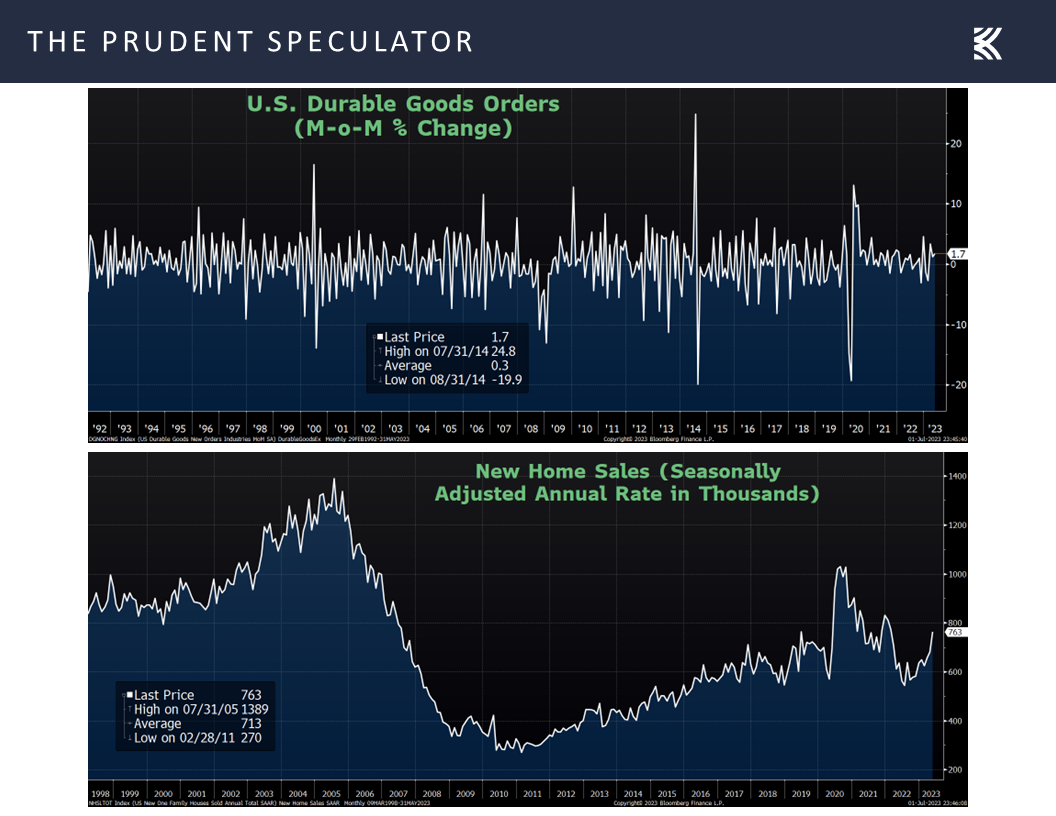

…along with significantly better-than-expected readings on durable goods orders (+1.7% vs. -0.9% forecast) and new home sales (763,000 vs. 675,000 est.) in May.

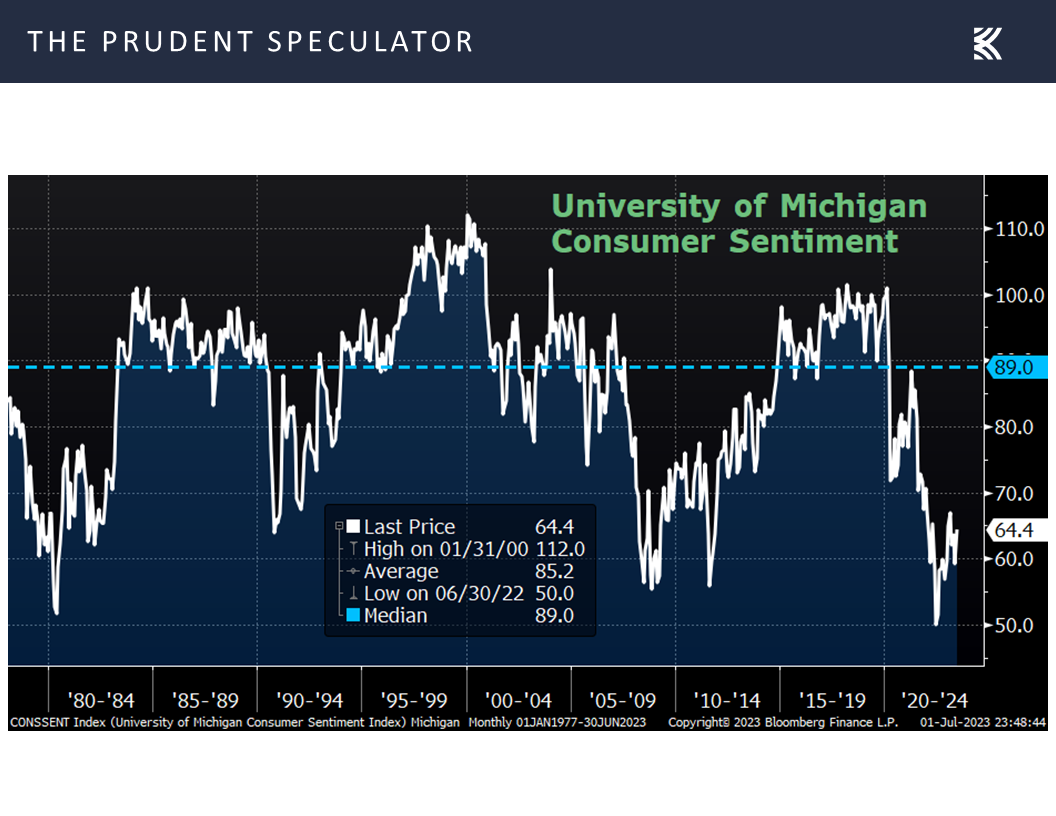

The mood of the consumer also showed improvement, with a modestly better-than-predicted increase (64.4 vs. 64.0 est. and 63.9 in May) in sentiment from the University of Michigan for June,

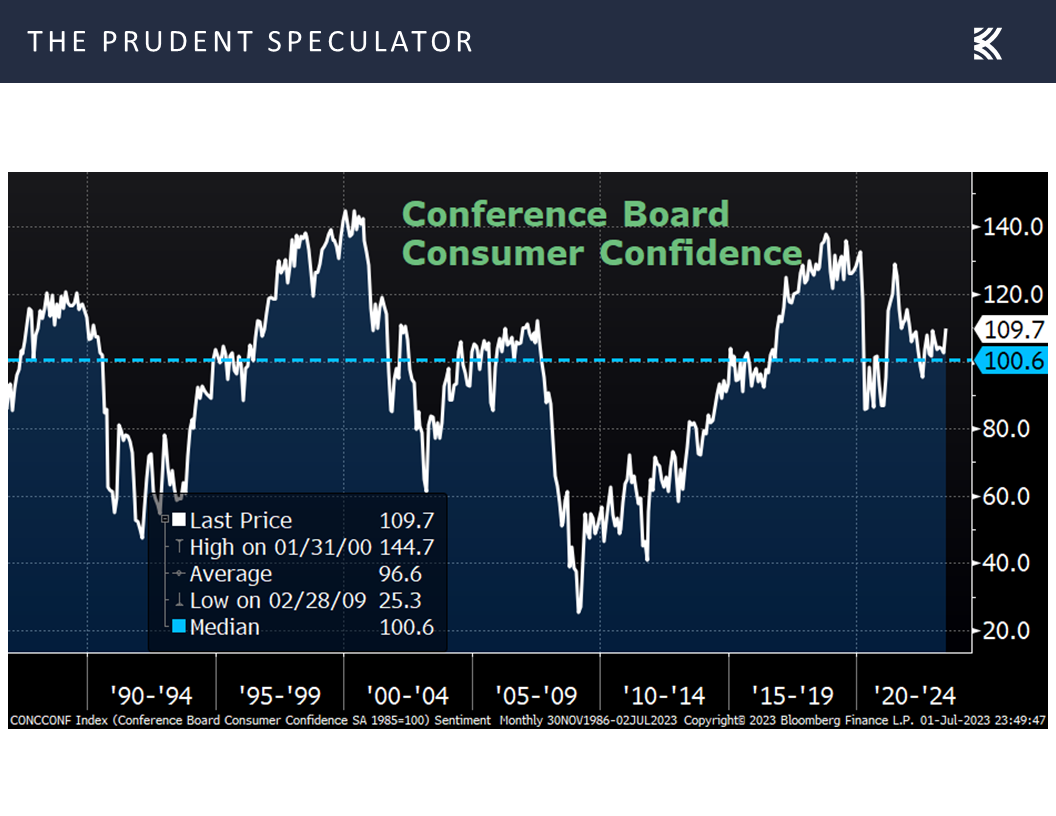

…and a big jump in confidence as tabulated by the Conference Board to 109.7, up from 102.5 in May and significantly above projections of 104.0.

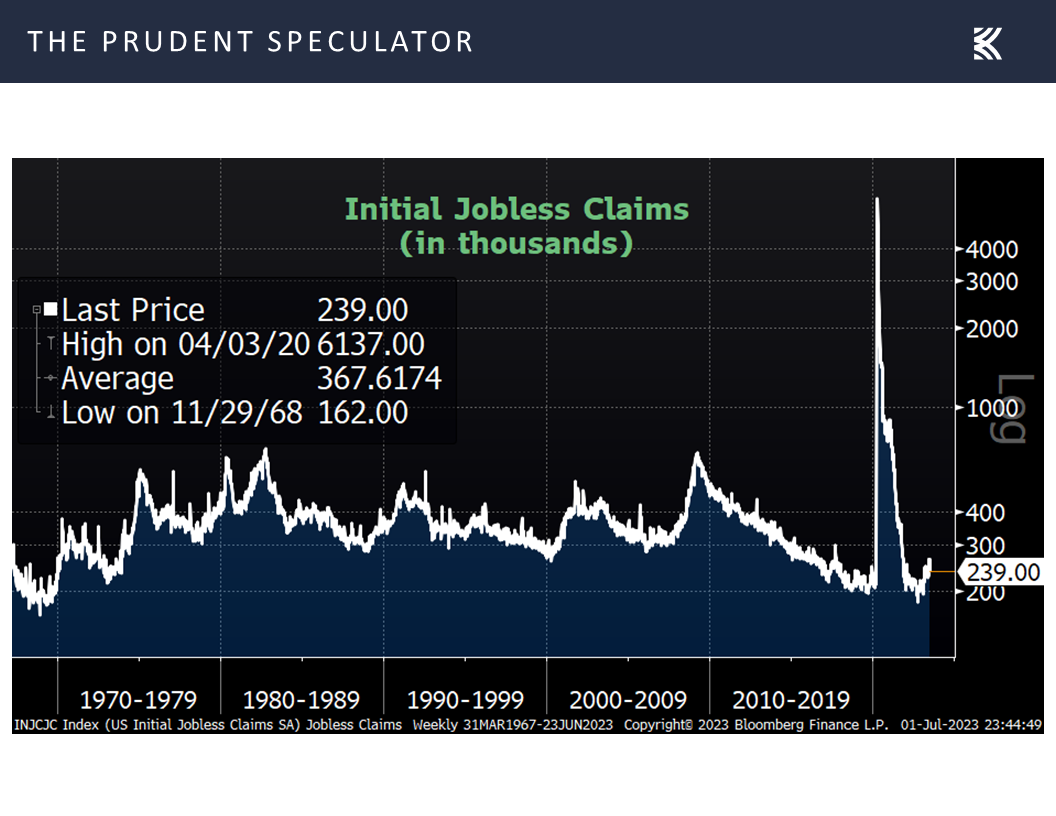

No doubt, a strong labor market is providing plenty of support, with the latest weekly tally on first-time filings for unemployment benefits dropping to 239,000, down from 265,000 the week prior,

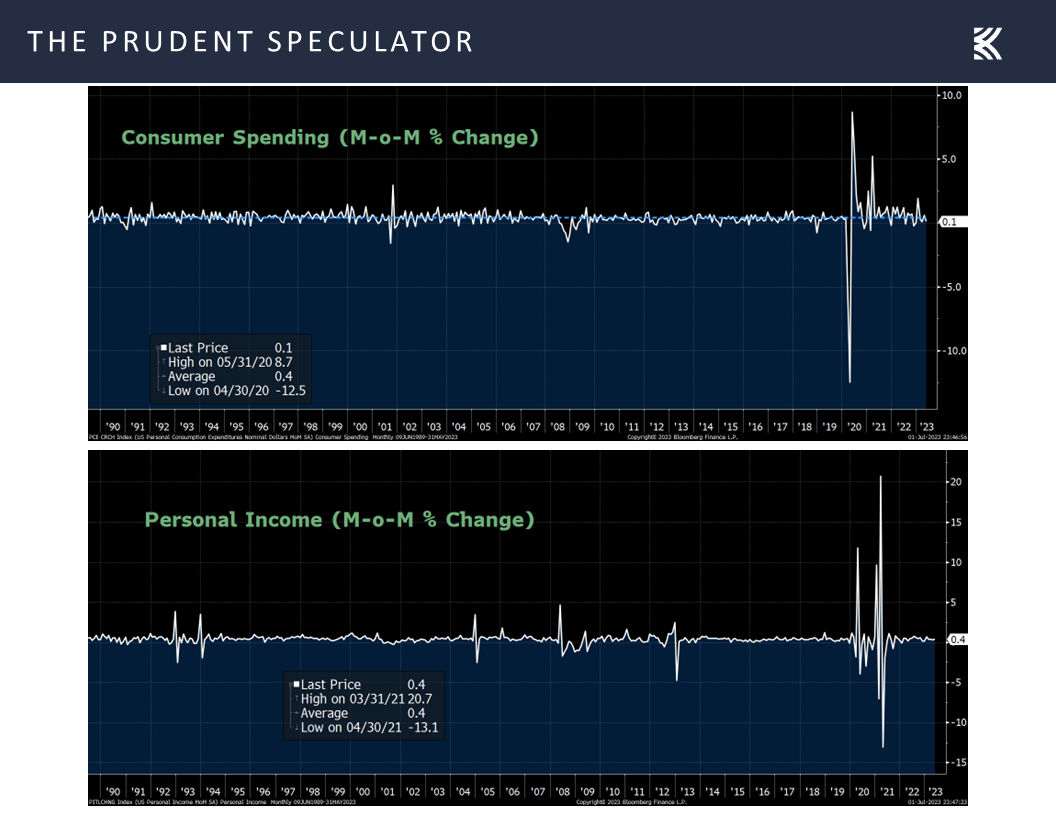

while consumer spending and personal incomes held up well in May.

Fed – Nearing the End of the Rate-Hiking Cycle

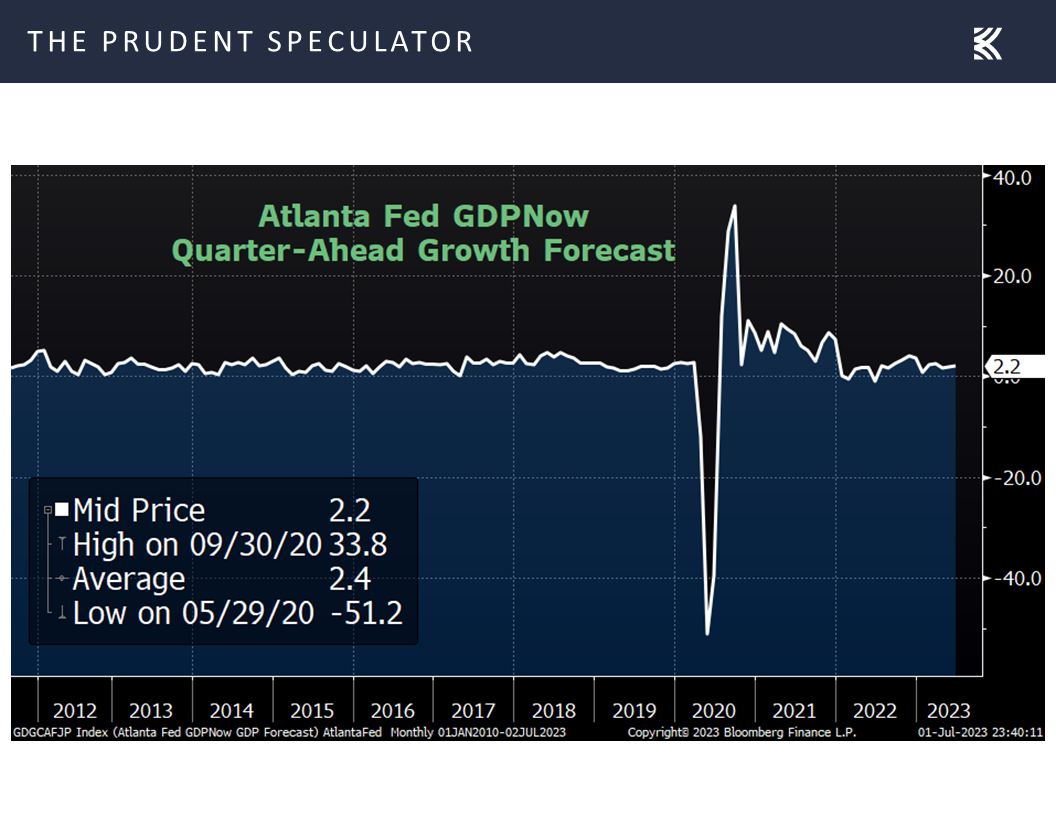

Not surprisingly, given the mostly positive economic stats, the estimate for Q2 real GDP growth from the Atlanta Fed moved up last week to 2.2%,

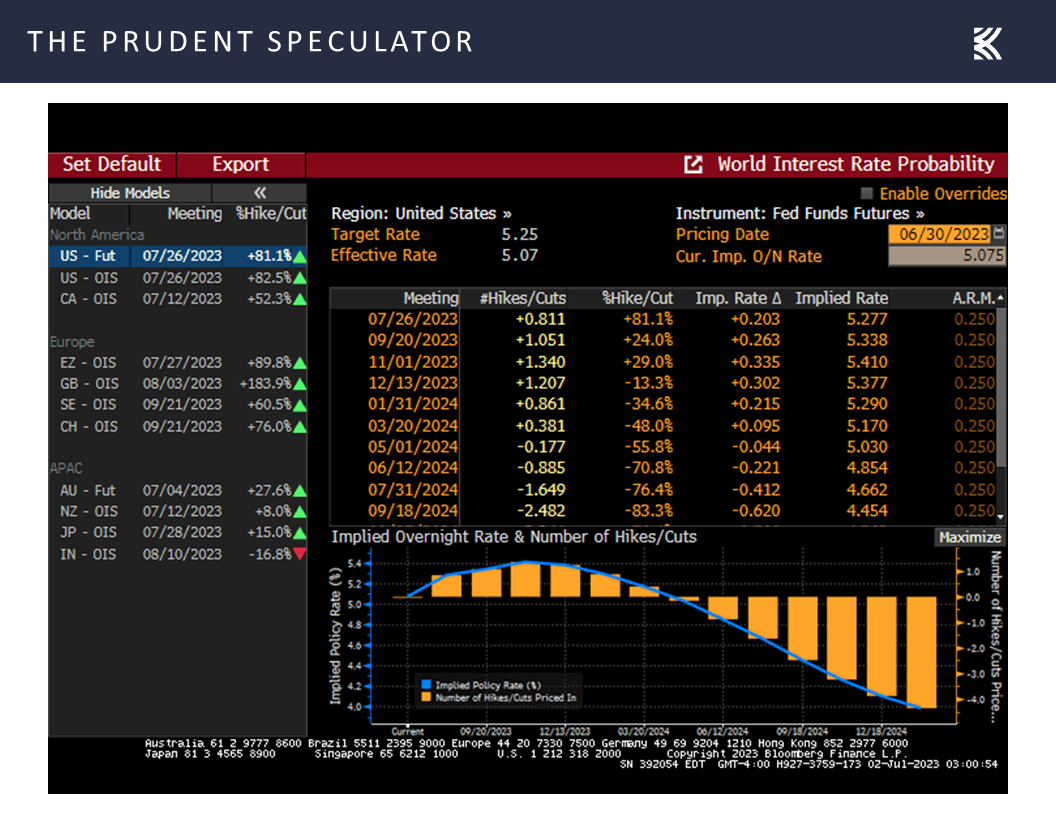

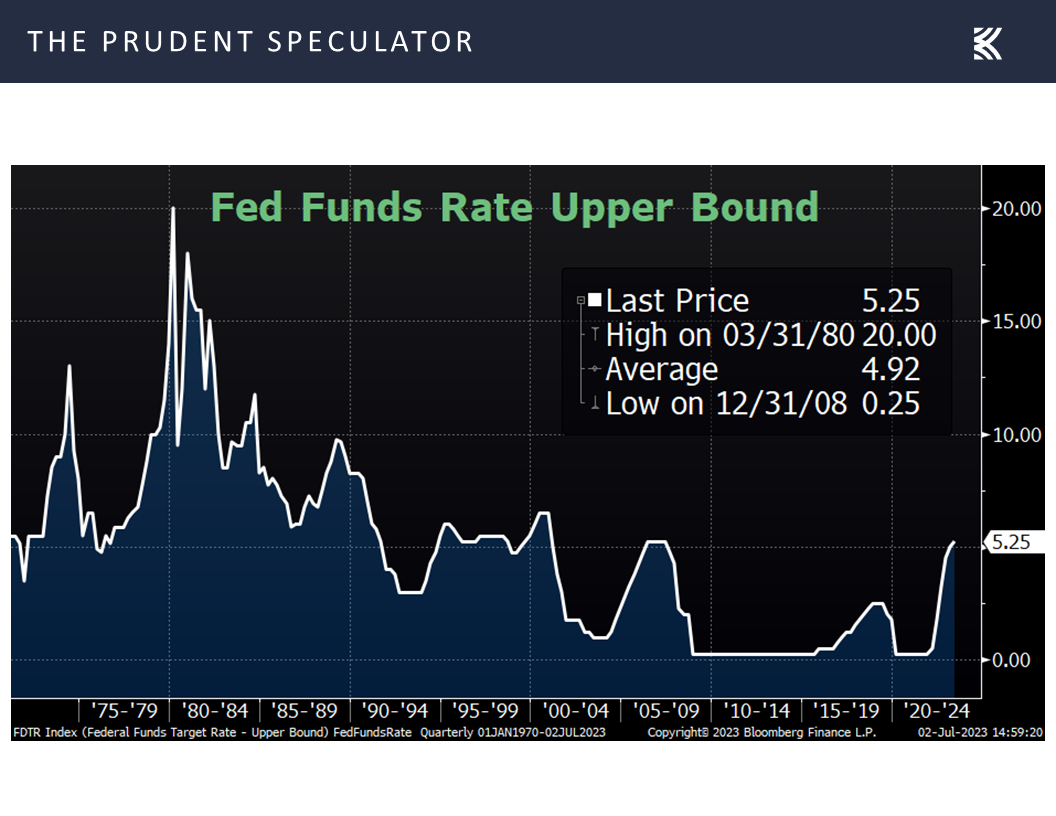

…which compelled the Fed Funds futures market to price in a higher end-of-year target of 5.38% for the benchmark interest rate, up from 5.24% at the end of the prior week.

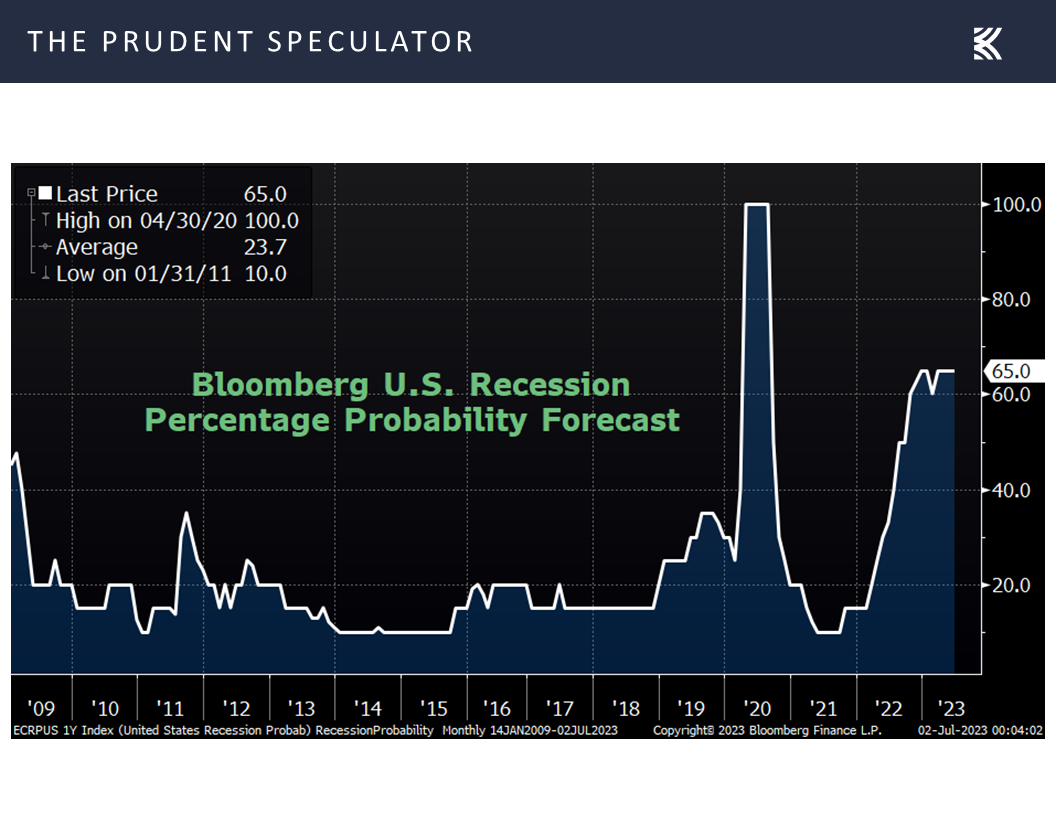

This was the case even as the probability forecast of an economic contraction in the next 12 months, as calculated by Bloomberg, continued to reside at 65%,

Inflation – Core PCE Better (Lower) Than Expected

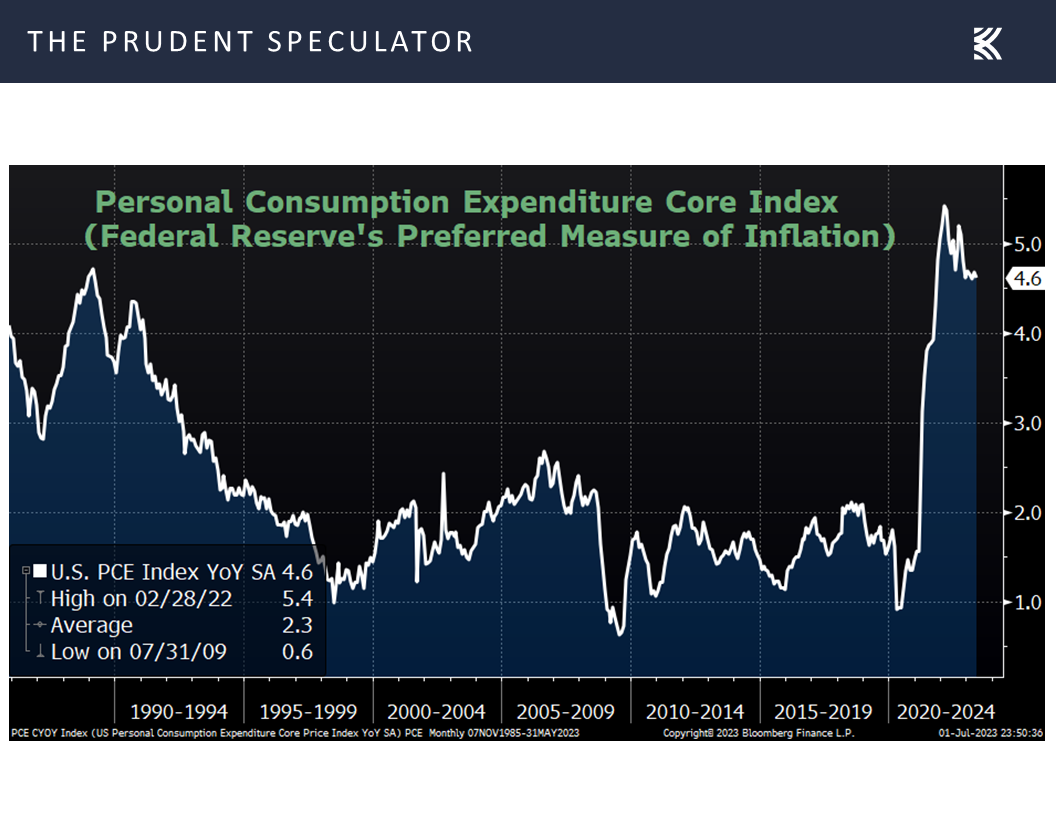

and the Federal Reserve’s preferred measure of inflation, the Personal Consumption Expenditure (PCE) Index, rose 3.8% on a year-over-year basis in May, the smallest increase since April 2021. More importantly, perhaps, the so-called Core PCE, which excludes volatile food and energy prices, rose 4.6% in May, better than estimates of a 4.7% advance and the lowest year-over-year change since October 2021.

To be sure, there is a long way to go in the fight against inflation, with Jerome H. Powell stating last week, “We’ve all seen inflation be, over and over again, more persistent and stronger than we expected.” However, the Fed Chair was quick to add, “At some point that may change, and I think we have to be ready to follow the data and be a little patient as we let this unfold.”

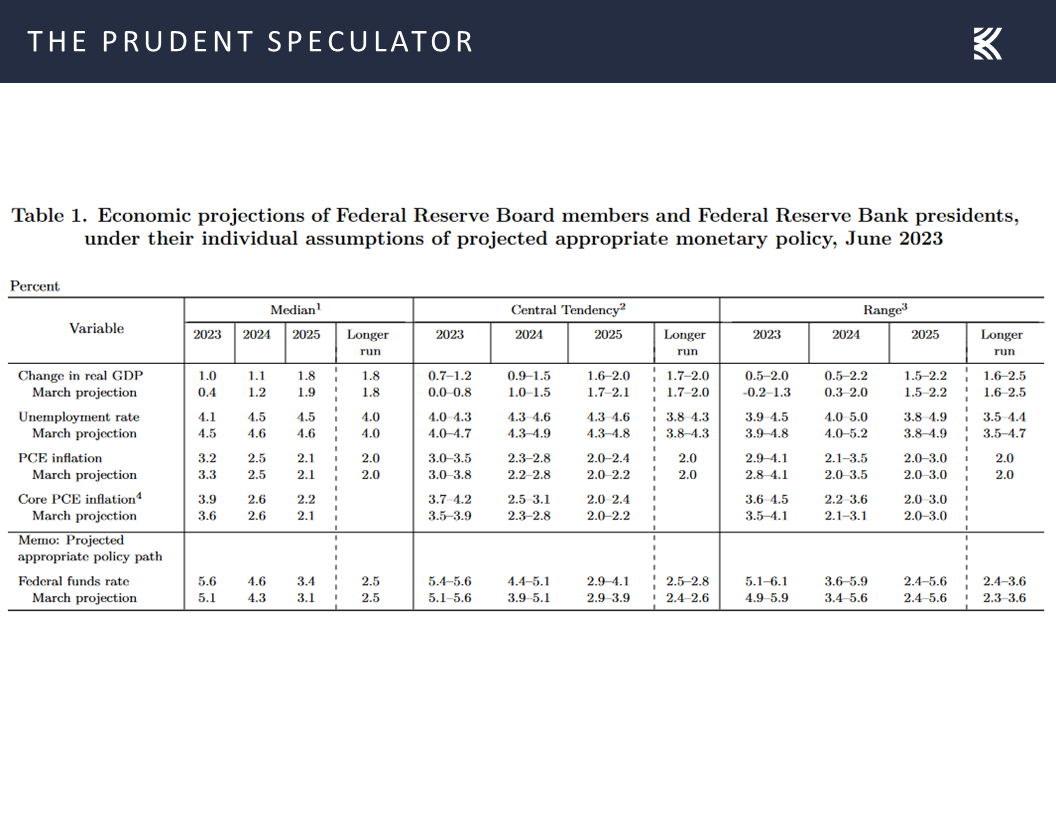

While the most recent economic projections from the Federal Reserve Board members and Federal Reserve Bank presidents argued for a 5.6% year-end Fed Funds rate,

…the Fed seemingly is near the end of its rate-hiking cycle (4.6% and 3.4% are the respective 2024 and 2025 year-end Fed Funds rate estimates), while we note that the current rate is not much higher than the average over the last 50-plus years.

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

And with longer-term inflation expectations remaining well contained, keeping a lid on long-term interest rates, we would argue that the interest rate backdrop is still supportive of equities in general,

especially as the E in the Earnings Yield is equation is expected to show solid growth this year and next,

especially as the E in the Earnings Yield is equation is expected to show solid growth this year and next,

Valuations – Stocks, Especially Value, Remain Reasonably Priced

while we continue to favor the inexpensive valuation metrics and generous dividend yields associated with our broadly diversified portfolios of what we believe to be undervalued stocks.

Bank Stress Tests – Passing Grades & Dividend Hikes

None of the above is meant to suggest that the summer rally is guaranteed to gain steam as we head into July, but we were happy to see last week the results of the Federal Reserve’s annual stress test of 23 of the nation’s largest banks. Each of the banks survived the most adverse scenario with capital levels above the regulatory minimum of 4.5%, with Fed Vice Chair Michael S. Barr stating, “Today’s results confirm that the banking system remains strong and resilient.”

A year ago, the Fed hypothetically stressed 33 banks and featured a severe global recession accompanied by a period of heightened stress in commercial real estate and corporate debt markets. But even while last year’s test incorporated counter-cyclical shocks, it failed to foresee that the plunge in bond prices due to the Fed’s rate-rising regime might contribute to the fear-driven bank runs that occurred in March.

As such, Mr. Barr was quick to add, “At the same time, this stress test is only one way to measure that strength. We should remain humble about how risks can arise and continue our work to ensure that banks are resilient to a range of economic scenarios, market shocks, and other stresses.”

This year’s stress test seemed pretty harsh as it included a severe global recession with a 40% decline in commercial real estate prices, a substantial increase in office vacancies, and a 38% decline in house prices. It also included the unemployment rate rising by 6.4 percentage points to a peak of 10% and economic output declining commensurately.

As the Fed concluded, “All 23 banks tested remained above their minimum capital requirements during the hypothetical recession, despite total projected losses of $541 billion. Under stress, the aggregate common equity risk-based capital ratio—which provides a cushion against losses—is projected to decline by 2.3 percentage points to a minimum of 10.1 percent.”

Citizens Financial (CFG – $26.08) had the lowest capital ratio under the severely adverse scenario, although regional banks posted lower capital ratios as a group than their much larger counterparts. But the biggest banks saw the largest projected net income losses, led by Citigroup’s (C – $46.04) $34.9 billion, while Goldman Sachs (GS – $322.54) posted the most theoretical losses from commercial real estate loans and credit cards.

Still, we would assert that the results of the tests were positive, while several banks announced increases to their capital return plans. These included behemoth JPMorgan Chase (JPM – $145.44), which said it will increase its dividend by 5%, after not raising the payout for two years. Goldman Sachs said it would boost its quarterly dividend by 10%, Bank NY Mellon (BK – $44.52) disclosed a 14% hike in its payout and even Citigroup gave its shareholders a $0.02 raise, even after buying back $1 billion of stock in the second quarter.

While the path forward for the economy is anyone’s guess, we take some comfort that all the banks in the test that we own made the grade. Following a tumultuous past several months for the sector, we continue to find tremendous value in shares of a variety of banks both large and small for their income generation and long-term appreciation potential.

After all, even Citizens Financial was able to proclaim, “We are pleased that the Federal Reserve’s stress test results illustrate Citizens’ strong capital position well in excess of our regulatory minimum and the resilience of our balance sheet and business model. In addition, we take further comfort in the fact that our company-run stress test results imply significantly lower capital drawdown than the Federal Reserve’s models.” The Rhode Island-based regional bank also reminded investors that the company still has $1.344 billion available under its share repurchase authorization as of the end of June.

Stock News – Updates on three stocks across three different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Bank Stress Tests, Inflation, Federal Reserve, Earnings and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Volatility, Inflation, Valuations, Earnings and Bank Stress Tests and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Sentiment – AAII Folks Remain Optimistic; But Stocks Rally

Volatility – Plenty of Disconcerting Events but Long-Term Trend in Equities is Higher

Econ Stats – Slew of Relatively Positive Numbers

Fed – Nearing the End of the Rate-Hiking Cycle

Inflation – Core PCE Better (Lower) Than Expected

Valuations – Stocks, Especially Value, Remain Reasonably Priced

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

Bank Stress Tests – Passing Grades & Dividend Hikes

Stock News – Updates on three stocks across three different sectors

Sentiment – AAII Folks Remain Optimistic; But Stocks Rally

Just when it appeared an excess of bullishness might put an end to the June rally, with folks on Main Street showing quite a bit of optimism for a change, at least according to the weekly Sentiment Survey from the American Association of Individual Investors,…

the equity markets enjoyed a terrific five trading days to end the second quarter, providing more evidence that just about any way the sometimes-disconcerting data are crunched it pays to stay invested.

Volatility – Plenty of Disconcerting Events but Long-Term Trend in Equities is Higher

Certainly, there remains plenty about which to be concerned as we head into the second half of the year, but such always seems to be the case,

…yet stocks generally have provided handsome rewards, with Value leading the long-term returns race, for those who stick with them through thick and thin.

Econ Stats – Slew of Relatively Positive Numbers

Of course, it didn’t hurt that the slew of economic data out last week generally was upbeat, with a significant upward revision to 2.0% in the real (inflation-adjusted) GDP growth calculation for the first quarter,…

…along with significantly better-than-expected readings on durable goods orders (+1.7% vs. -0.9% forecast) and new home sales (763,000 vs. 675,000 est.) in May.

The mood of the consumer also showed improvement, with a modestly better-than-predicted increase (64.4 vs. 64.0 est. and 63.9 in May) in sentiment from the University of Michigan for June,

…and a big jump in confidence as tabulated by the Conference Board to 109.7, up from 102.5 in May and significantly above projections of 104.0.

No doubt, a strong labor market is providing plenty of support, with the latest weekly tally on first-time filings for unemployment benefits dropping to 239,000, down from 265,000 the week prior,

while consumer spending and personal incomes held up well in May.

Fed – Nearing the End of the Rate-Hiking Cycle

Not surprisingly, given the mostly positive economic stats, the estimate for Q2 real GDP growth from the Atlanta Fed moved up last week to 2.2%,

…which compelled the Fed Funds futures market to price in a higher end-of-year target of 5.38% for the benchmark interest rate, up from 5.24% at the end of the prior week.

This was the case even as the probability forecast of an economic contraction in the next 12 months, as calculated by Bloomberg, continued to reside at 65%,

Inflation – Core PCE Better (Lower) Than Expected

and the Federal Reserve’s preferred measure of inflation, the Personal Consumption Expenditure (PCE) Index, rose 3.8% on a year-over-year basis in May, the smallest increase since April 2021. More importantly, perhaps, the so-called Core PCE, which excludes volatile food and energy prices, rose 4.6% in May, better than estimates of a 4.7% advance and the lowest year-over-year change since October 2021.

To be sure, there is a long way to go in the fight against inflation, with Jerome H. Powell stating last week, “We’ve all seen inflation be, over and over again, more persistent and stronger than we expected.” However, the Fed Chair was quick to add, “At some point that may change, and I think we have to be ready to follow the data and be a little patient as we let this unfold.”

While the most recent economic projections from the Federal Reserve Board members and Federal Reserve Bank presidents argued for a 5.6% year-end Fed Funds rate,

…the Fed seemingly is near the end of its rate-hiking cycle (4.6% and 3.4% are the respective 2024 and 2025 year-end Fed Funds rate estimates), while we note that the current rate is not much higher than the average over the last 50-plus years.

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

And with longer-term inflation expectations remaining well contained, keeping a lid on long-term interest rates, we would argue that the interest rate backdrop is still supportive of equities in general,

Valuations – Stocks, Especially Value, Remain Reasonably Priced

while we continue to favor the inexpensive valuation metrics and generous dividend yields associated with our broadly diversified portfolios of what we believe to be undervalued stocks.

Bank Stress Tests – Passing Grades & Dividend Hikes

None of the above is meant to suggest that the summer rally is guaranteed to gain steam as we head into July, but we were happy to see last week the results of the Federal Reserve’s annual stress test of 23 of the nation’s largest banks. Each of the banks survived the most adverse scenario with capital levels above the regulatory minimum of 4.5%, with Fed Vice Chair Michael S. Barr stating, “Today’s results confirm that the banking system remains strong and resilient.”

A year ago, the Fed hypothetically stressed 33 banks and featured a severe global recession accompanied by a period of heightened stress in commercial real estate and corporate debt markets. But even while last year’s test incorporated counter-cyclical shocks, it failed to foresee that the plunge in bond prices due to the Fed’s rate-rising regime might contribute to the fear-driven bank runs that occurred in March.

As such, Mr. Barr was quick to add, “At the same time, this stress test is only one way to measure that strength. We should remain humble about how risks can arise and continue our work to ensure that banks are resilient to a range of economic scenarios, market shocks, and other stresses.”

This year’s stress test seemed pretty harsh as it included a severe global recession with a 40% decline in commercial real estate prices, a substantial increase in office vacancies, and a 38% decline in house prices. It also included the unemployment rate rising by 6.4 percentage points to a peak of 10% and economic output declining commensurately.

As the Fed concluded, “All 23 banks tested remained above their minimum capital requirements during the hypothetical recession, despite total projected losses of $541 billion. Under stress, the aggregate common equity risk-based capital ratio—which provides a cushion against losses—is projected to decline by 2.3 percentage points to a minimum of 10.1 percent.”

Citizens Financial (CFG – $26.08) had the lowest capital ratio under the severely adverse scenario, although regional banks posted lower capital ratios as a group than their much larger counterparts. But the biggest banks saw the largest projected net income losses, led by Citigroup’s (C – $46.04) $34.9 billion, while Goldman Sachs (GS – $322.54) posted the most theoretical losses from commercial real estate loans and credit cards.

Still, we would assert that the results of the tests were positive, while several banks announced increases to their capital return plans. These included behemoth JPMorgan Chase (JPM – $145.44), which said it will increase its dividend by 5%, after not raising the payout for two years. Goldman Sachs said it would boost its quarterly dividend by 10%, Bank NY Mellon (BK – $44.52) disclosed a 14% hike in its payout and even Citigroup gave its shareholders a $0.02 raise, even after buying back $1 billion of stock in the second quarter.

While the path forward for the economy is anyone’s guess, we take some comfort that all the banks in the test that we own made the grade. Following a tumultuous past several months for the sector, we continue to find tremendous value in shares of a variety of banks both large and small for their income generation and long-term appreciation potential.

After all, even Citizens Financial was able to proclaim, “We are pleased that the Federal Reserve’s stress test results illustrate Citizens’ strong capital position well in excess of our regulatory minimum and the resilience of our balance sheet and business model. In addition, we take further comfort in the fact that our company-run stress test results imply significantly lower capital drawdown than the Federal Reserve’s models.” The Rhode Island-based regional bank also reminded investors that the company still has $1.344 billion available under its share repurchase authorization as of the end of June.

Stock News – Updates on three stocks across three different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.