The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. This week, we cover the Banking Crisis, Interest Rates, Inflation, the Fed, Portfolio Valuations, Undervalued Stocks that were hit the hardest and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Fear & Greed: Sentiment Heads South

Banking Crisis: Central Bankers Fighting Fear

Interest Rates: Bond Rally Helps Alleviate Bank Balance Sheet Stress

Econ News: Q1 GDP Forecast Improves; Jobs Numbers Remain Strong, But Other Numbers Not So Grand

Inflation: Longer-Term Expectations Recede; PPI Pulls Back

Fed: Market Predicting Jerome H. Powell & Co. to be Much-Less Hawkish

Headwinds: Equities Have Overcome Plenty of Adversity Through the Years

Valuations: Still Liking the Metrics for our Portfolios

Shopping List: Hardest Hit Undervalued Stocks

Stock News: Updates on three stocks across three different stocks

Occasional outbreaks of those two super-contagious diseases, fear and greed, will forever occur in the investment community. The timing of these epidemics will be unpredictable. And the market aberrations produced by them will be equally unpredictable, both as to duration and degree. Therefore, we never try to anticipate the arrival or departure of either disease. Our goal is more modest: We simply attempt to be fearful when others are greedy, and to be greedy only when others are fearful.

Warren Buffett offered up that advice in 1986 when the Dow Jones Industrial Average was south of 2000 and one year before your Editor joined Al Frank at The Prudent Speculator. Obviously, with the Dow above 31000 today, the long-term trend for equities has been significantly higher, especially if dividends and their reinvestment are included, though there have been plenty of scary selloffs along the way.

Fear & Greed: Sentiment Heads South

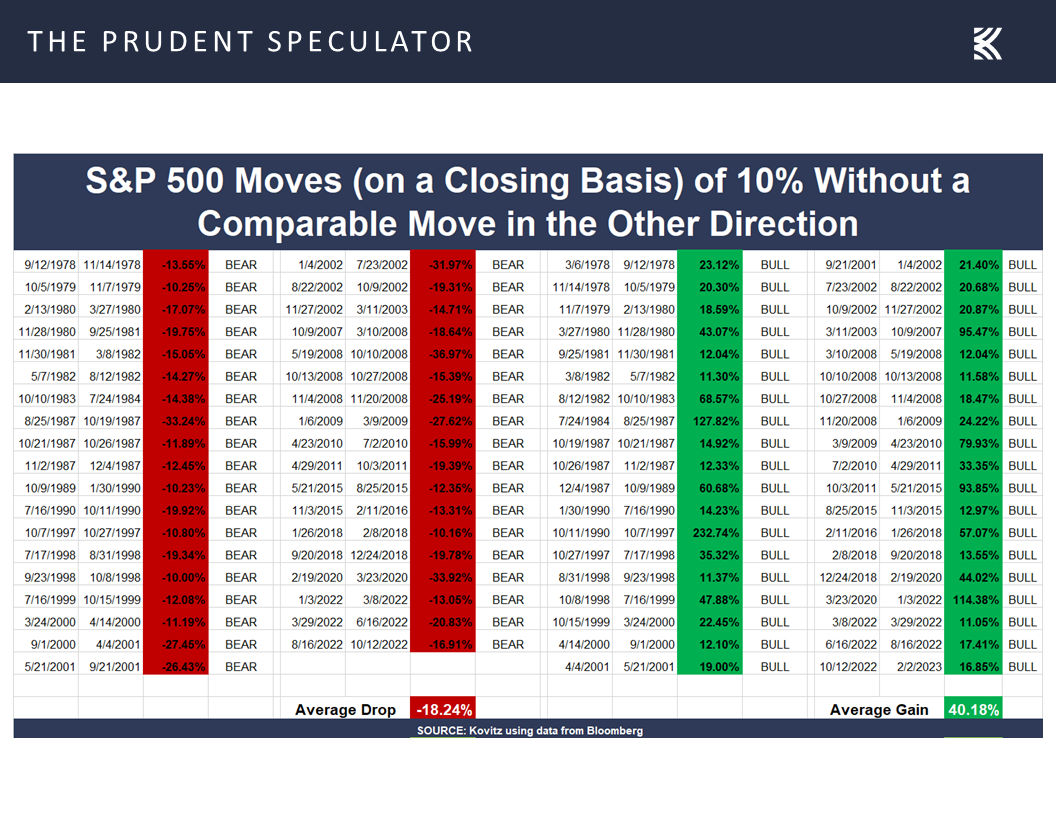

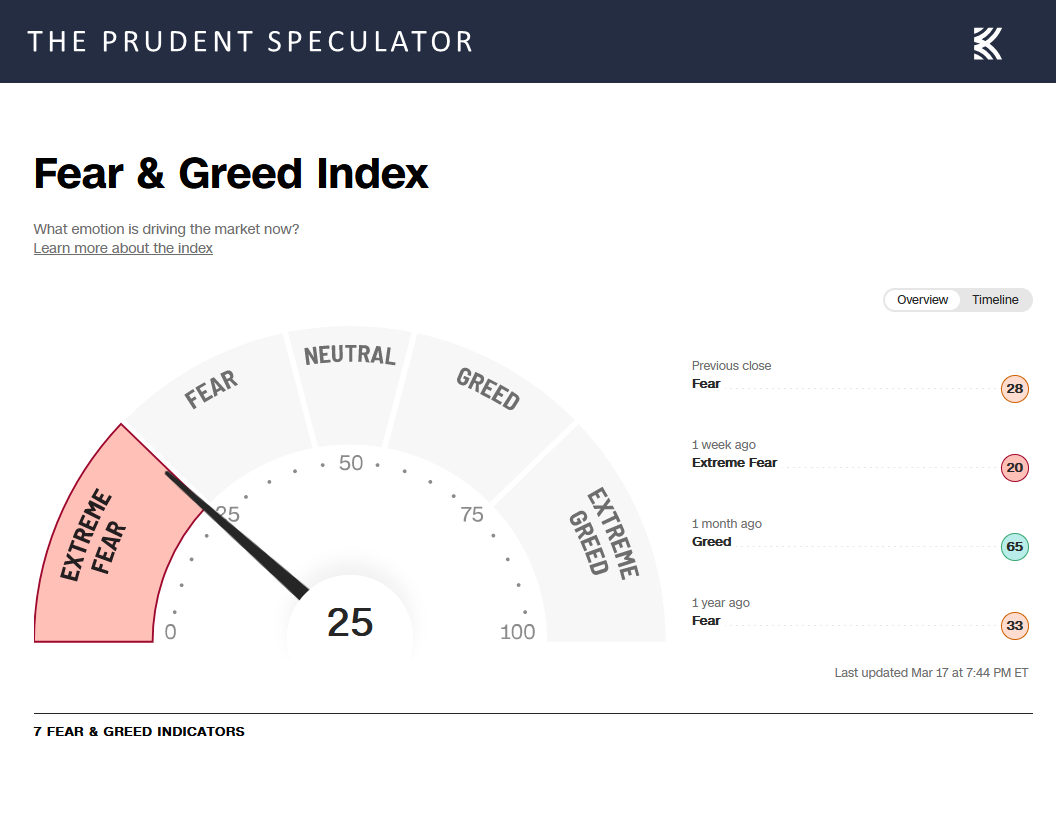

While the average gains during the times in the green in the chart above dwarf the average losses during the periods in the red, we are now in an environment where fear levels are running high, with the CNN/Money Fear & Greed Index of 7 indicators moving into Extreme Fear Territory, led in that direction by gauges on Stock Price Breadth, Market Volatility, Safe Haven Demand and Junk Bond Demand.

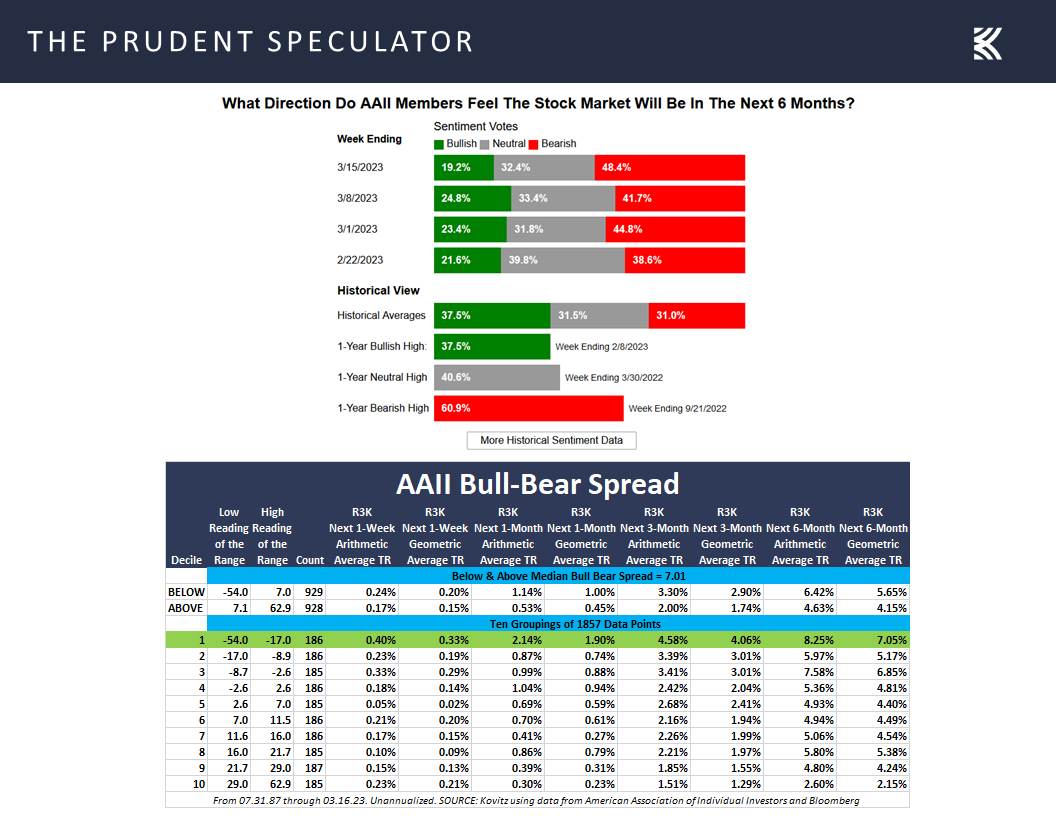

It is an even more pessimistic story for the 36-year-old Sentiment Survey from the American Association of Individual Investors (AAII). The good folks at AAII said last week…

Bullish sentiment, expectations that stock prices will rise over the next six months, fell 5.6 percentage points to 19.2%. Optimism was last lower on September 22, 2022 (17.7%). Bullish sentiment is at an unusually low level for the fourth consecutive week and the 44th time out of the past 63 weeks. Bullish sentiment is also below its historical average of 37.5% for the 67th time out of the past 69 weeks.

Bearish sentiment, expectations that stock prices will fall over the next six months, rose 6.7 percentage points to 48.4%. Pessimism was last higher on December 22, 2022 (52.3%). This is the third consecutive week and the 42nd time out of the past 63 weeks that bearish sentiment is at an unusually high level. Bearish sentiment is also above its historical average of 31.0% for the 64th time out of the past 69 weeks.

The bull-bear spread (bullish minus bearish sentiment) decreased by 12.3 percentage points to –29.2% and remains unusually low for the fourth consecutive week. The bull-bear spread is at an unusually low level for the 46th time out of the past 63 weeks.

This week’s bullish sentiment reading is the 34th lowest recorded since the Sentiment Survey started in July 1987. The survey period included the failure of Silicon Valley Bank and Signature Bank, as well as the recent headlines surrounding Credit Suisse.

Historically, the S&P 500 index has gone on to realize above-average and above-median returns during the six- and 12-month periods following unusually low readings for bullish sentiment and the bull-bear spread. Similarly, the market benchmark has gone on to realize above-average and above-median returns during the six- and 12-month periods following unusually high readings for bearish sentiment.

Banking Crisis: Central Bankers Fighting Fear

Of course, as AAII stated, the survey period included the failures of Silicon Valley Bank and Signature Bank, as well as some, but not all the drama around Credit Suisse.

On Thursday the embattled European banking giant said it would borrow up to 50 billion Swiss francs ($54 billion) from the Swiss Central bank in an effort to shore up its liquidity. Then, on Sunday a hastily arranged shotgun marriage was orchestrated in which rival UBS agreed to buy Credit Suisse for $3.25 billion in stock, with the Swiss National Bank providing 100 billion Swiss francs in liquidity assistance.

The demise of Credit Suisse was extraordinary, with Swiss President Alain Berset saying it was impossible to restore confidence in the company and Swiss Finance Minister Karin Keller-Sutter stating, “The takeover plan will offer greater stability both in Switzerland and internationally.” Swiss National Bank President Thomas Jordan, further asserted, “It was indispensable that we acted quickly and find a solution as quickly as possible, given that Credit Suisse is a systemically important bank.”

While many will argue that Credit Suisse was mismanaged, it really was a crisis of confidence that triggered the collapse as accelerating deposit outflows were cited as the core reason, just as was the case with Silicon Valley Bancorp and Signature Bank. Speaking of that duo, Janet Yellen explained last week, “No matter how strong capital and liquidity supervision are, if a bank has an overwhelming run that’s spurred by social media so that it’s seeing deposits flee at that pace, a bank can be put in danger of failing.”

That in mind, the Treasury Secretary on Thursday helped orchestrate a deposit infusion into West Coast regional bank First Republic (FRC), whose concentration of high-net-worth customers had contributed to an uninsured deposits balance of $119.5 billion (over two-thirds of total deposits) as of December 31, 2022, a significant amount of which were demand deposits.

With worries about a run on First Republic growing, a consortium of the nation’s biggest banks and some of the largest regional banks cooperated in a remarkable show of unity to try to stem depositor panic by infusing $30 billion of deposits into FRC from their own balance sheets.

Bank of America, Citigroup, JPMorgan Chase and Wells Fargo announced today they are each making a $5 billion uninsured deposit into First Republic Bank. Goldman Sachs and Morgan Stanley are each making an uninsured deposit of $2.5 billion, and BNY-Mellon, PNC Bank, State Street, Truist and U.S. Bank are each making an uninsured deposit of $1 billion, for a total deposit from the eleven banks of $30 billion. This action by America’s largest banks reflects their confidence in First Republic and in banks of all sizes, and it demonstrates their overall commitment to helping banks serve their customers and communities. Regional, midsize and small banks are critical to the health and functioning of our financial system.

Following the receiverships of Silicon Valley Bank and Signature Bank, there were outflows of uninsured deposits at a small number of banks. America’s financial system is among the best in the world, and America’s banks – large, midsize and community banks – do an extraordinary job serving the banking needs of their unique customers and communities. The banking system has strong credit, plenty of liquidity, strong capital and strong profitability. Recent events did nothing to change this.

The actions of America’s largest banks reflect their confidence in the country’s banking system. Together, we are deploying our financial strength and liquidity into the larger system, where it is needed the most. Smaller- and medium-sized banks support their local customers and businesses, create millions of jobs and help uplift communities. America’s larger banks stand united with all banks to support our economy and all of those around us.

While the numbers on deposit flows are not known, it is presumed that most of the banks involved have been beneficiaries of the banking crisis, at least in terms of new business heading their way. Given that we own 8 of the consortium’s 11 banks, we see the ability to step up to the table as a positive sign of their own financial strength.

Interest Rates: Bond Rally Helps Alleviate Bank Balance Sheet Stress

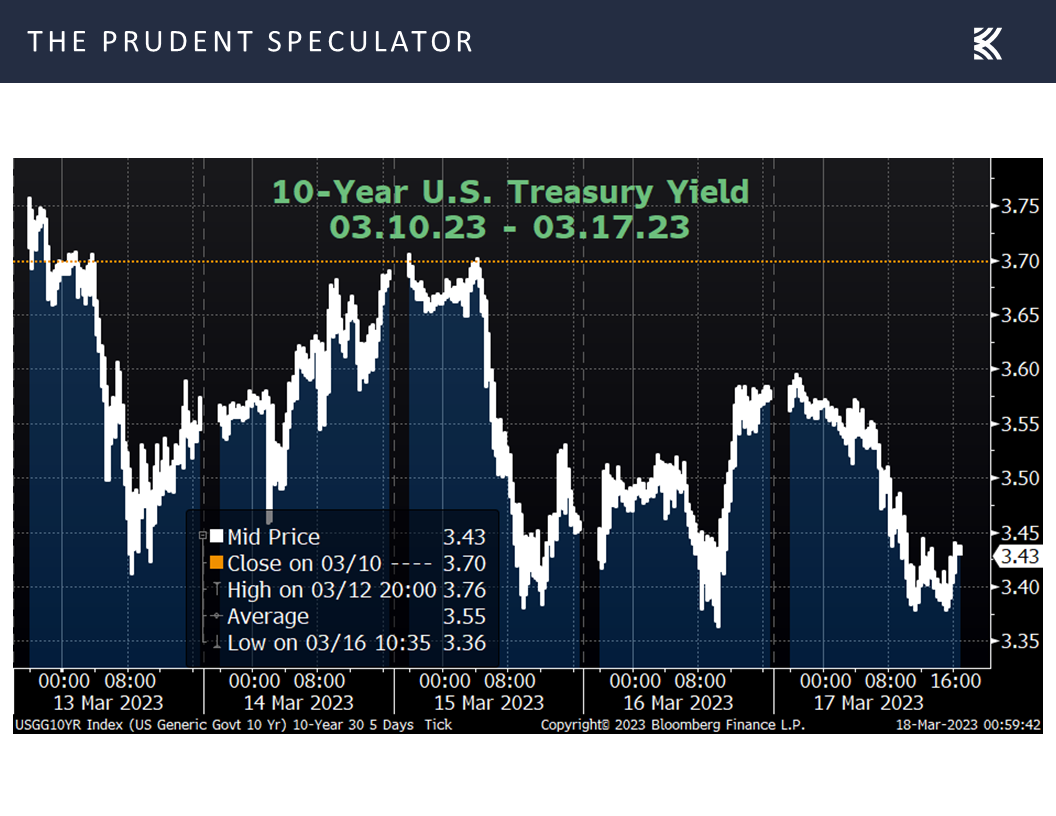

We might also add that the plunge in interest rates during the recent flight to safety, with the yield on the benchmark 10-year Treasury at 3.43%, down from 3.87% at the start of the year and over 4.02% on March 2,

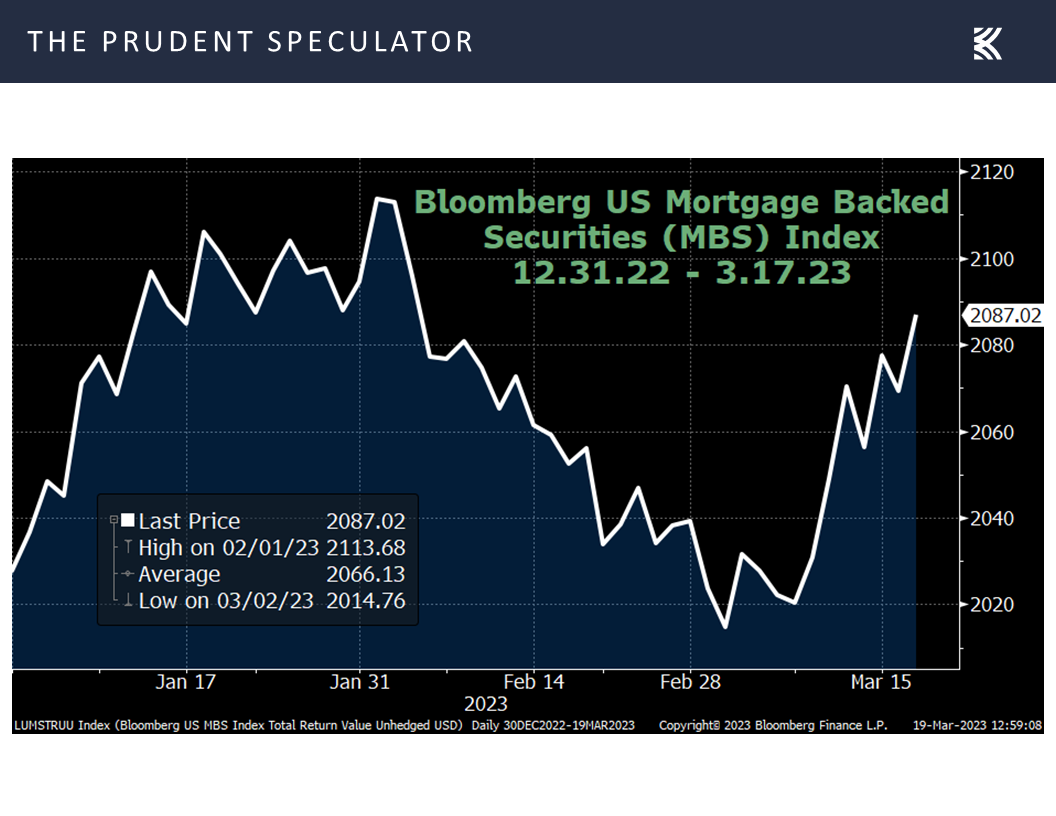

as well as a sizable rally in mortgage backed securities, an index of which has gained more than 2% since the end of February and is now up on the year,

is helping to alleviate some of the unrealized losses on debt instruments on bank balance sheets.

is helping to alleviate some of the unrealized losses on debt instruments on bank balance sheets.

We are not suggesting that banks are in better shape today than they were at the start of the year, and our pruning of Target Prices illustrates the point as greater regulation and stronger capital requirements, along with potentially reduced loan demand, constrained loan supply and greater non-performing assets are likely byproducts of the bank mess. However, we agree with Ms. Yellen and Federal Reserve Chair Jerome H. Powell who said on Sunday, “The capital and liquidity positions of the U.S. banking system are strong, and the U.S. financial system is resilient.”

Econ News: Q1 GDP Forecast Improves; Jobs Numbers Remain Strong, But Other Numbers Not So Grand

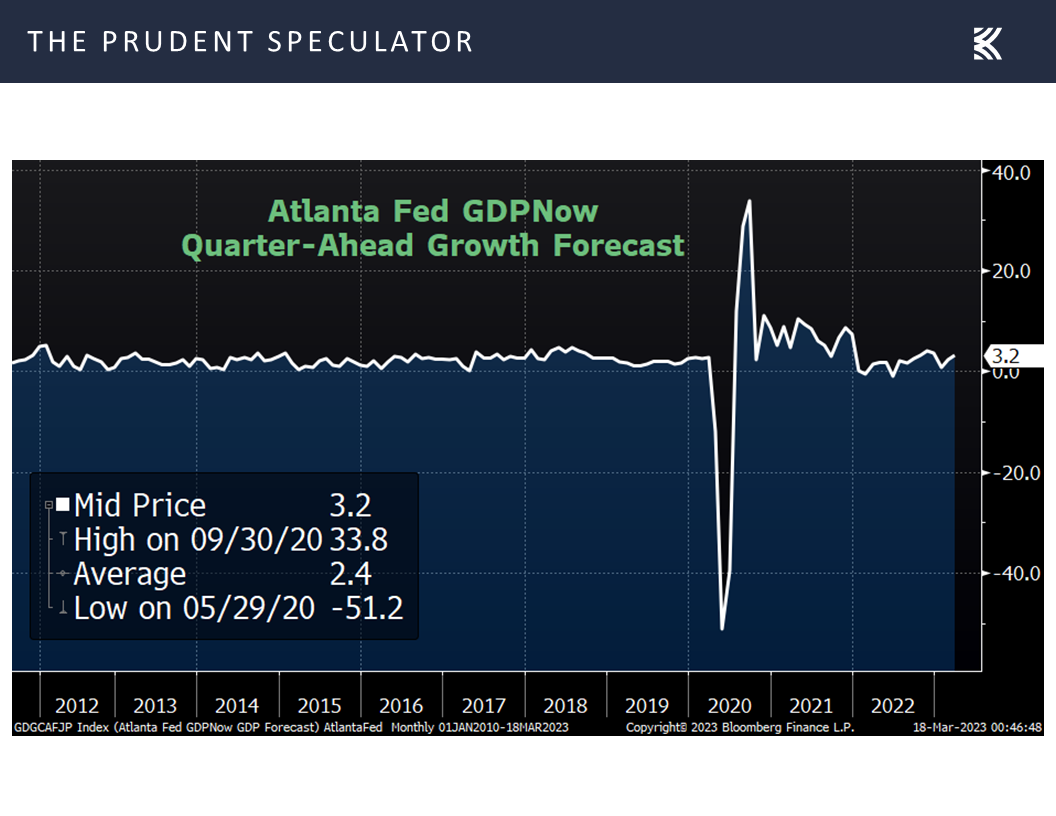

We might add that the U.S. economy has proven to be quite resilient in its own right, with the Atlanta Fed’s forecast for Q1 inflation-adjusted GDP growth climbing to 3.2% last week,

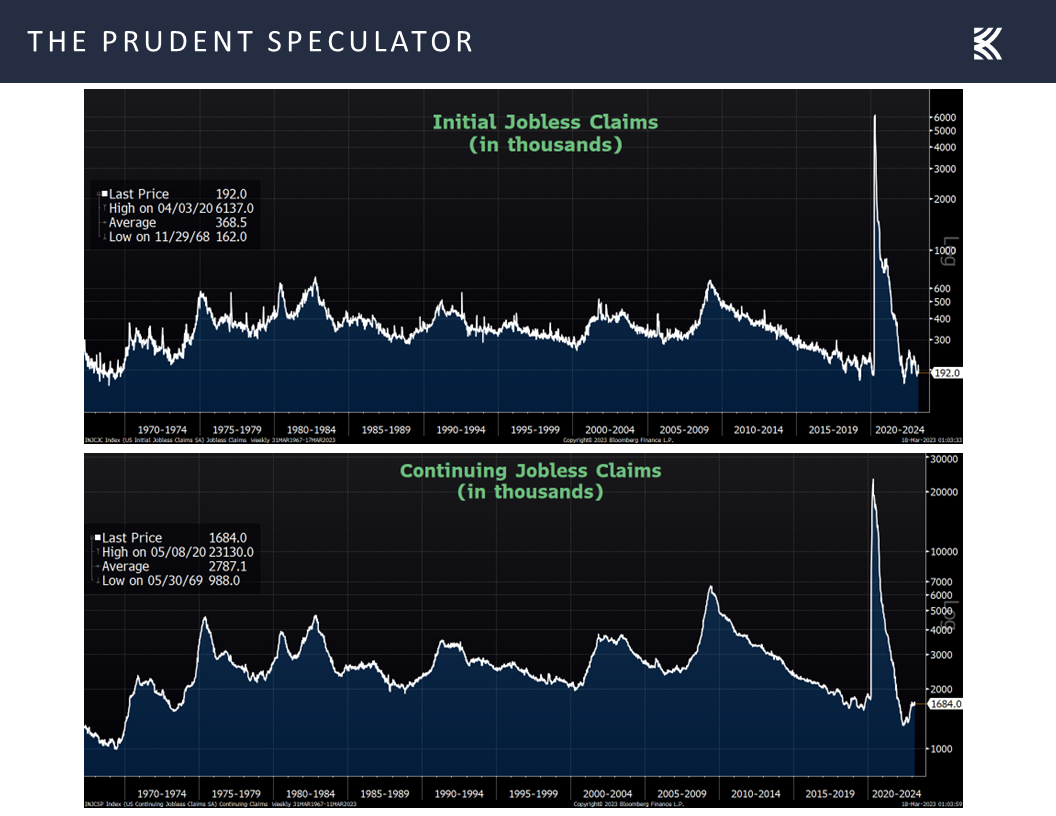

as the jobs market remains remarkably robust, with first-time filings for unemployment benefits pulling back below 200,000 in the latest week, near lows not seen since the 1960s when the labor force was far smaller.

as the jobs market remains remarkably robust, with first-time filings for unemployment benefits pulling back below 200,000 in the latest week, near lows not seen since the 1960s when the labor force was far smaller.

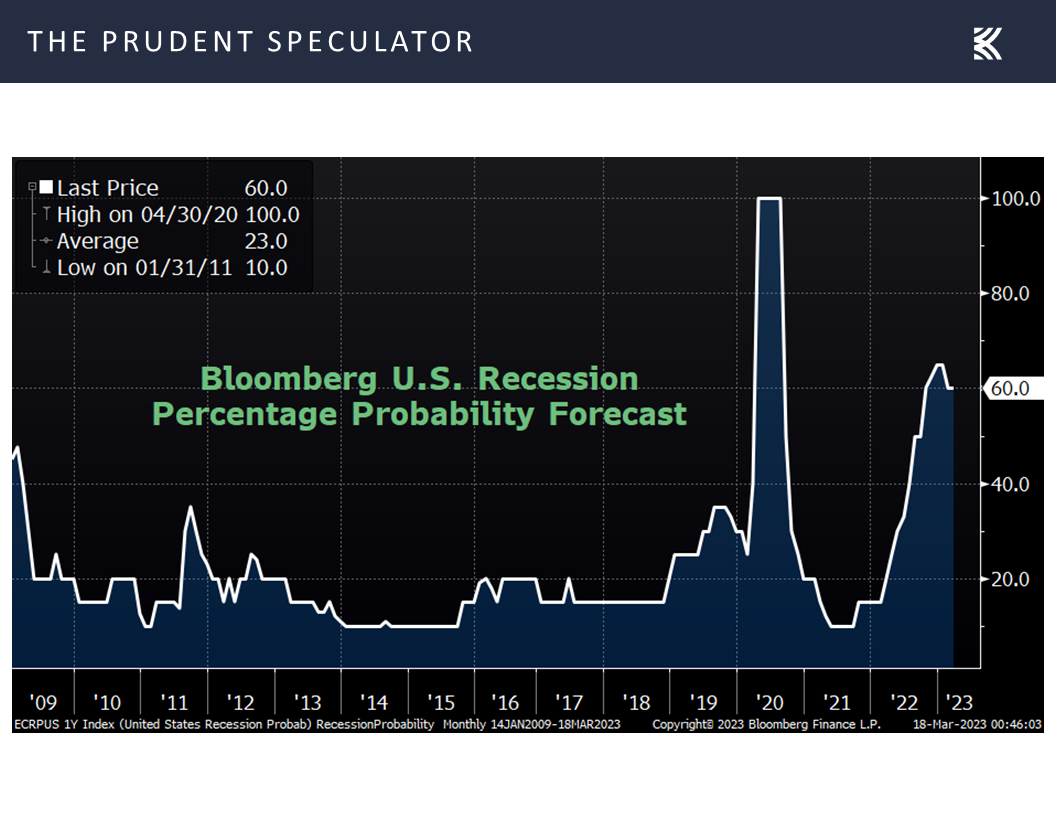

True, the odds of recession in the next 12 months, per calculations from Bloomberg, continue to be high,

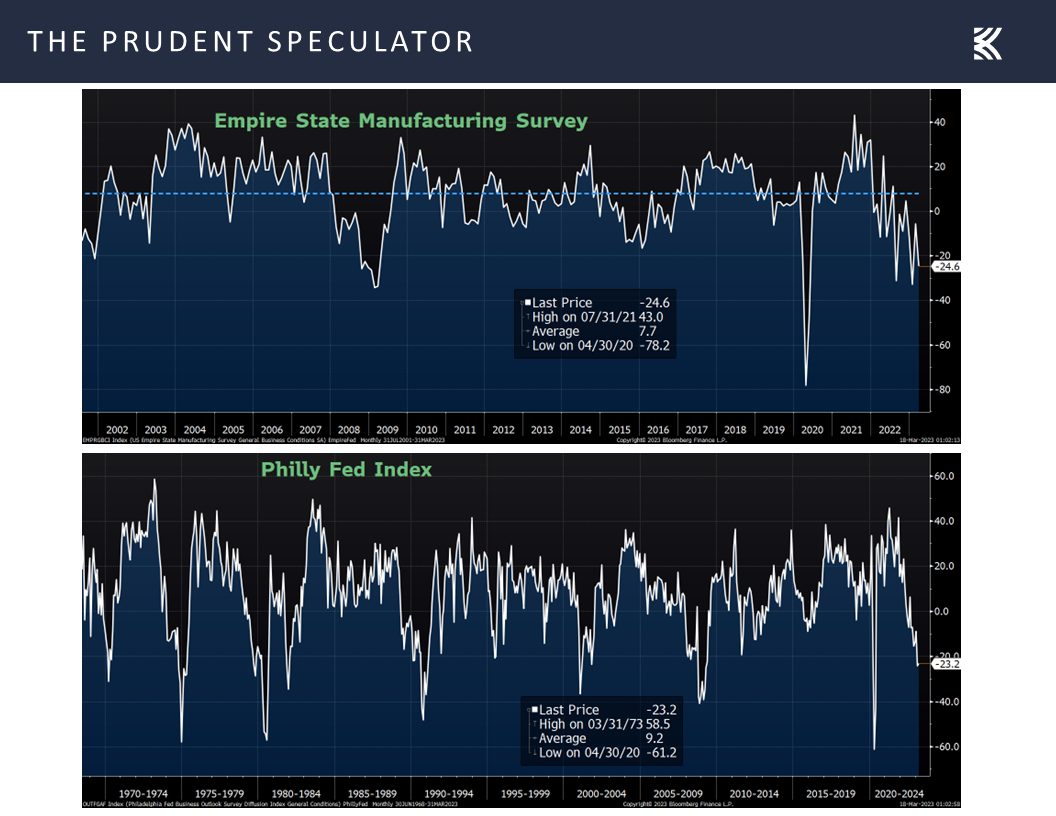

and the outlook for East Coast factory activity deteriorated last week, with both the Empire and Philadelphia Fed’s Manufacturing indexes for March coming in well below expectations.

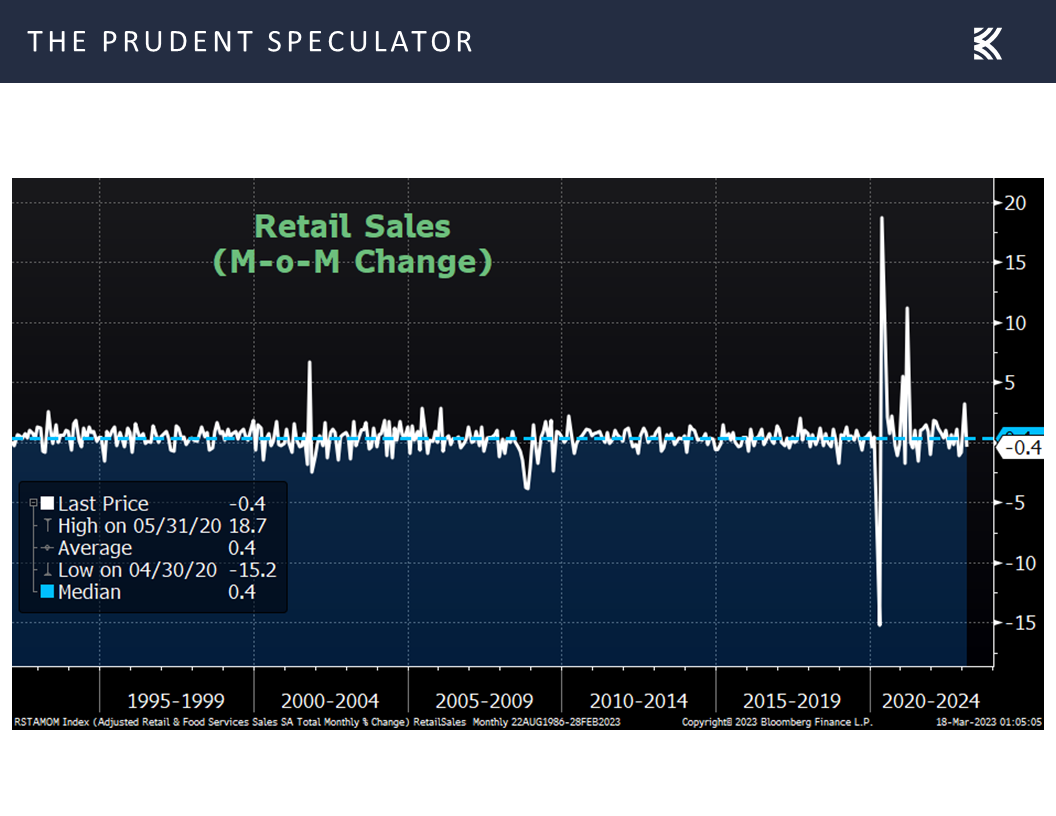

On the other hand, the latest read on retail sales was in line with forecasts of a 0.4% pullback from January’s robust tally,

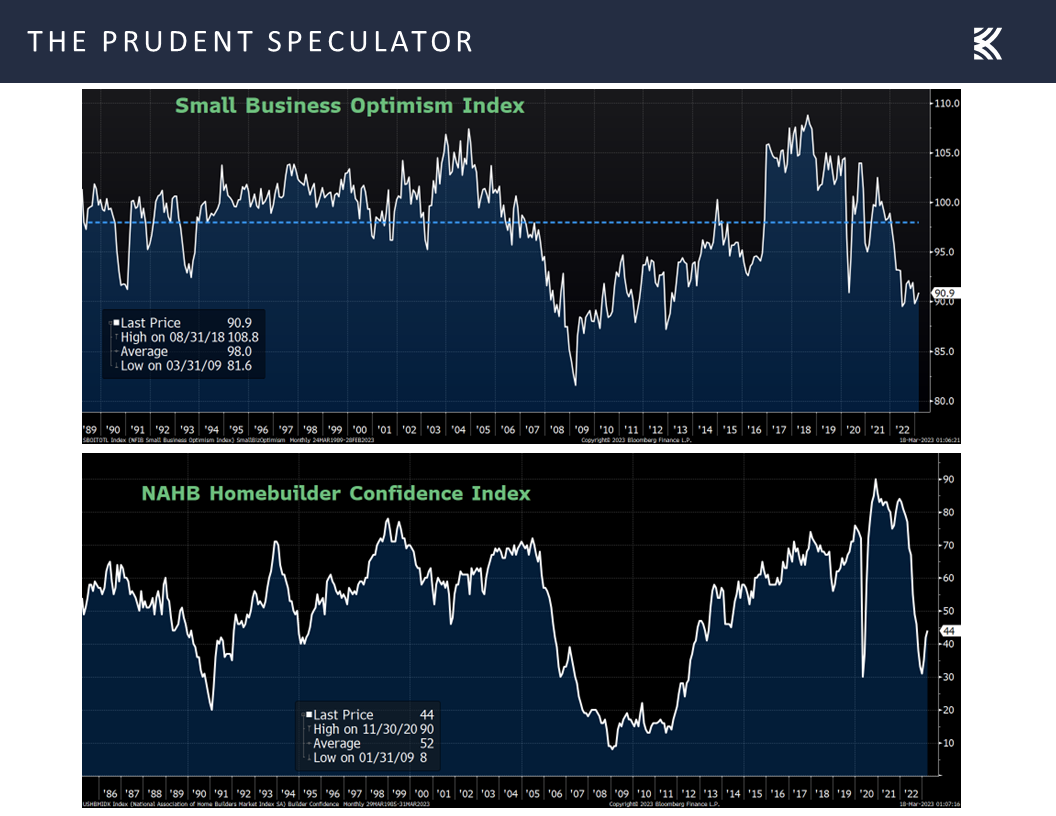

and the Small Business Optimism and Homebuilder Confidence gauges topped projections.

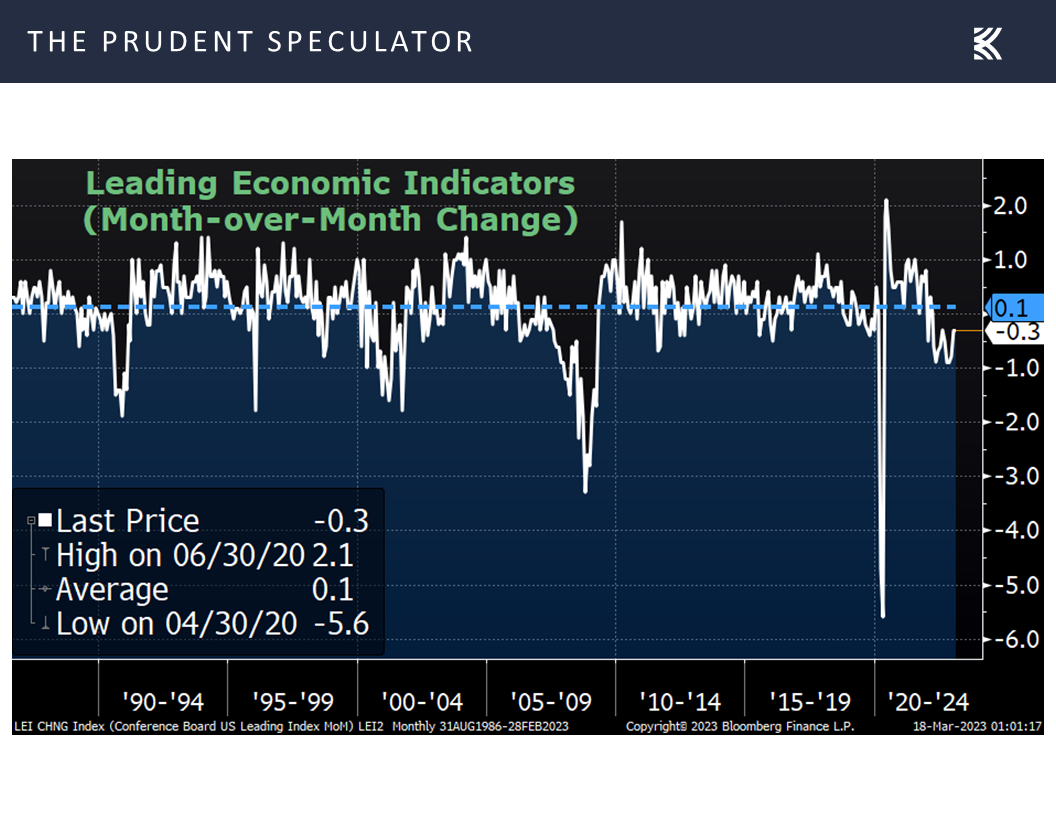

To be sure, the economic outlook is cloudy to say the least, and we respect commentary released on Friday with the Leading Economic Index (LEI) by the Conference Board, even as the February gauge was in line with or a little better than expectations.

The LEI for the U.S. fell again in February, marking its eleventh consecutive monthly decline. Negative or flat contributions from eight of the index’s ten components more than offset improving stock prices and a better-than-expected reading for residential building permits. While the rate of month-over-month declines in the LEI have moderated in recent months, the leading economic index still points to risk of recession in the U.S. economy. The most recent financial turmoil in the US banking sector is not reflected in the LEI data but could have a negative impact on the outlook if it persists. Overall, The Conference Board forecasts rising interest rates paired with declining consumer spending will most likely push the U.S. economy into recession in the near term.

Inflation: Longer-Term Expectations Recede; PPI Pulls Back

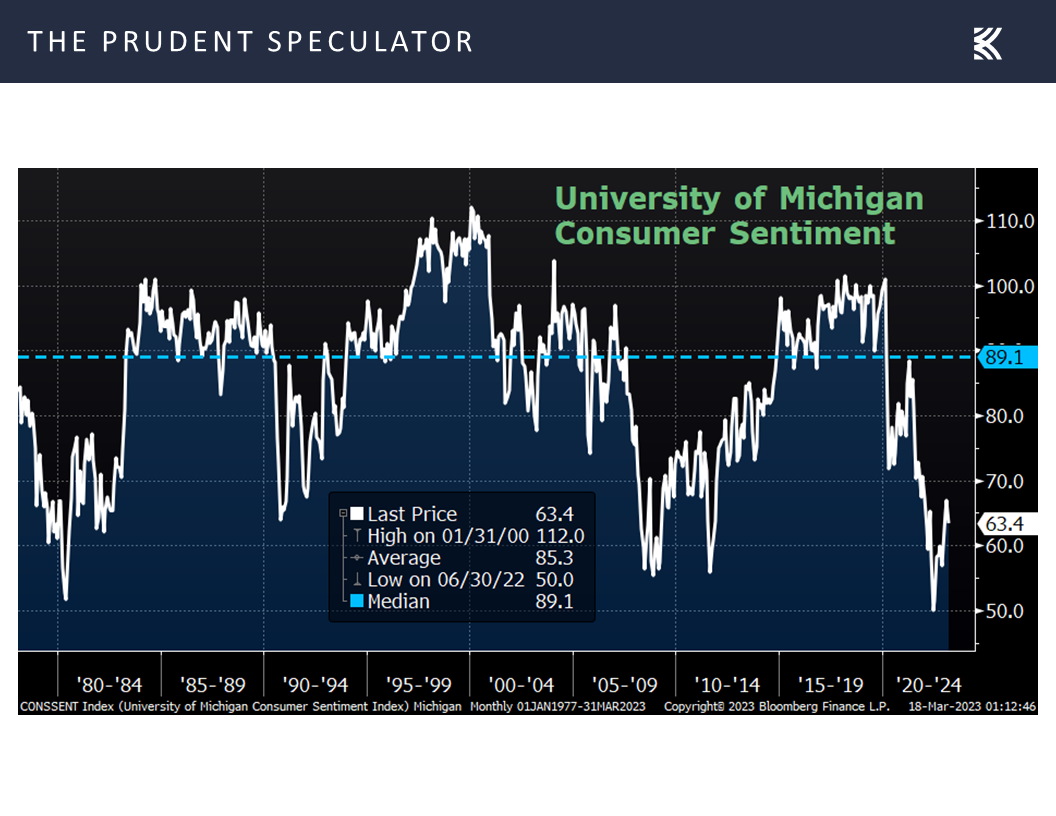

We also realize that the latest measure of consumer sentiment from the University of Michigan retreated to a worse-than-expected 63.4, down from 67.0 the month prior,

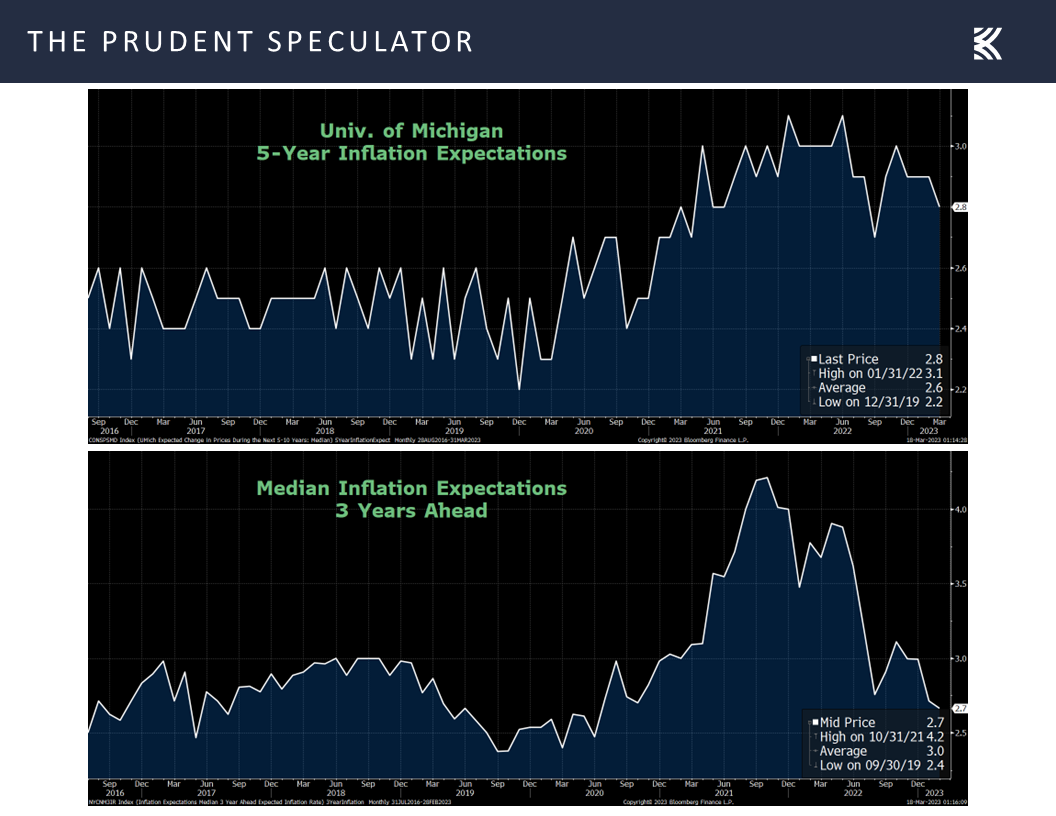

though there was some modestly good news in that consumers expect prices to increase 3.8% in the next year, down from 4.1% in the prior month. Longer-term 5-year inflation expectations also pulled back to 2.8% from the month prior, while the New York Fed’s latest Survey of Consumer Expectations saw the three-year projection hold steady at 2.7%, indicating that progress is being made via the Federal Reserve rate hikes.

though there was some modestly good news in that consumers expect prices to increase 3.8% in the next year, down from 4.1% in the prior month. Longer-term 5-year inflation expectations also pulled back to 2.8% from the month prior, while the New York Fed’s latest Survey of Consumer Expectations saw the three-year projection hold steady at 2.7%, indicating that progress is being made via the Federal Reserve rate hikes.

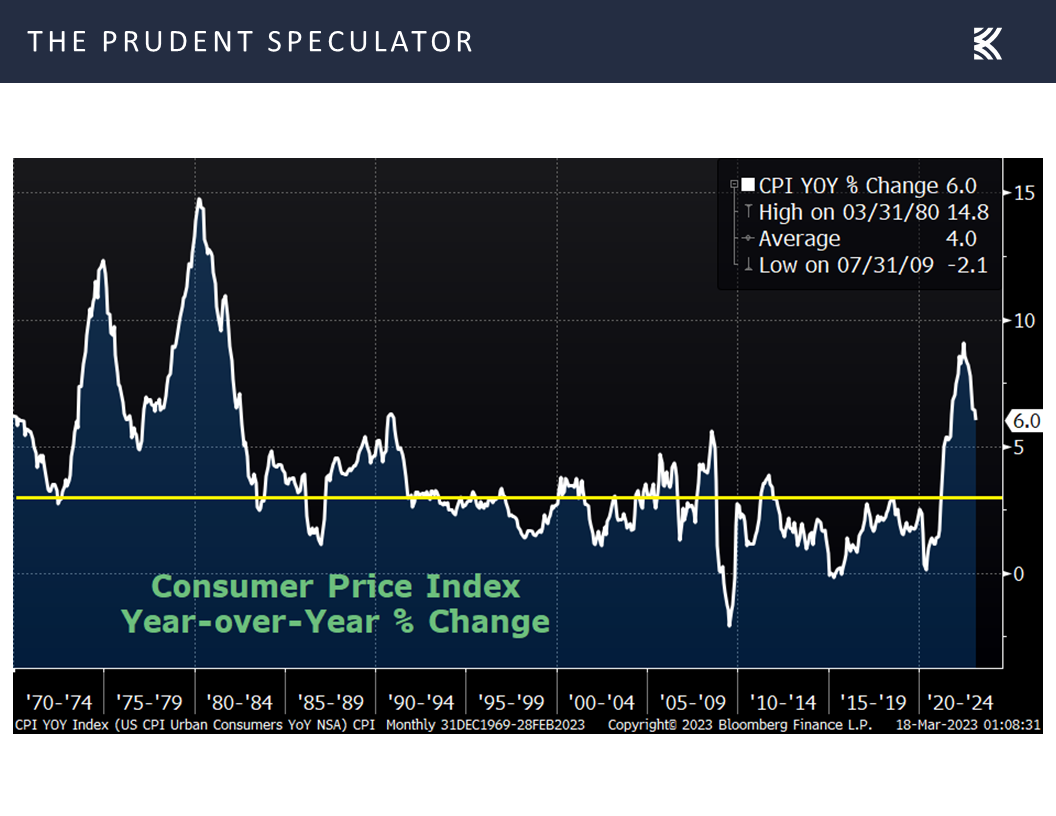

Interestingly, if not for the bank turmoil, the broad market might have rallied last week as the Consumer Price Index year-over-year change of 6.0% in February was as expected,

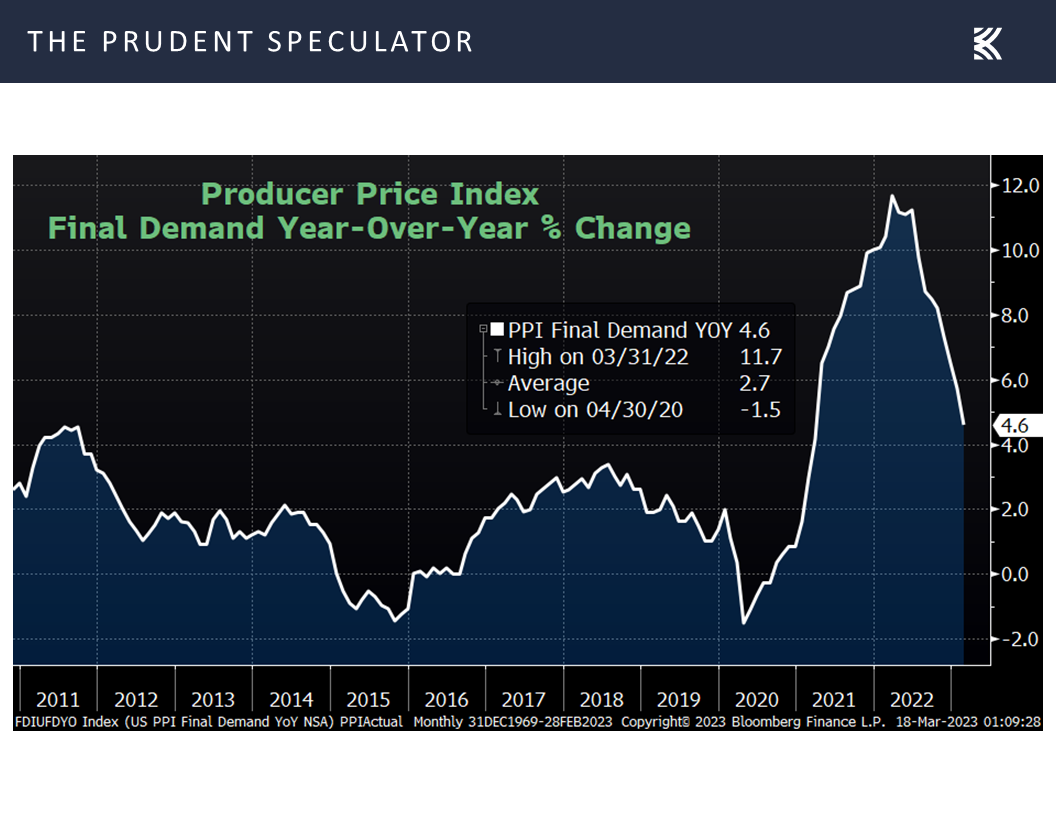

but the Producer Price Index saw a significant drop to 4.6% in its year-over-year change last month versus 5.7% in January.

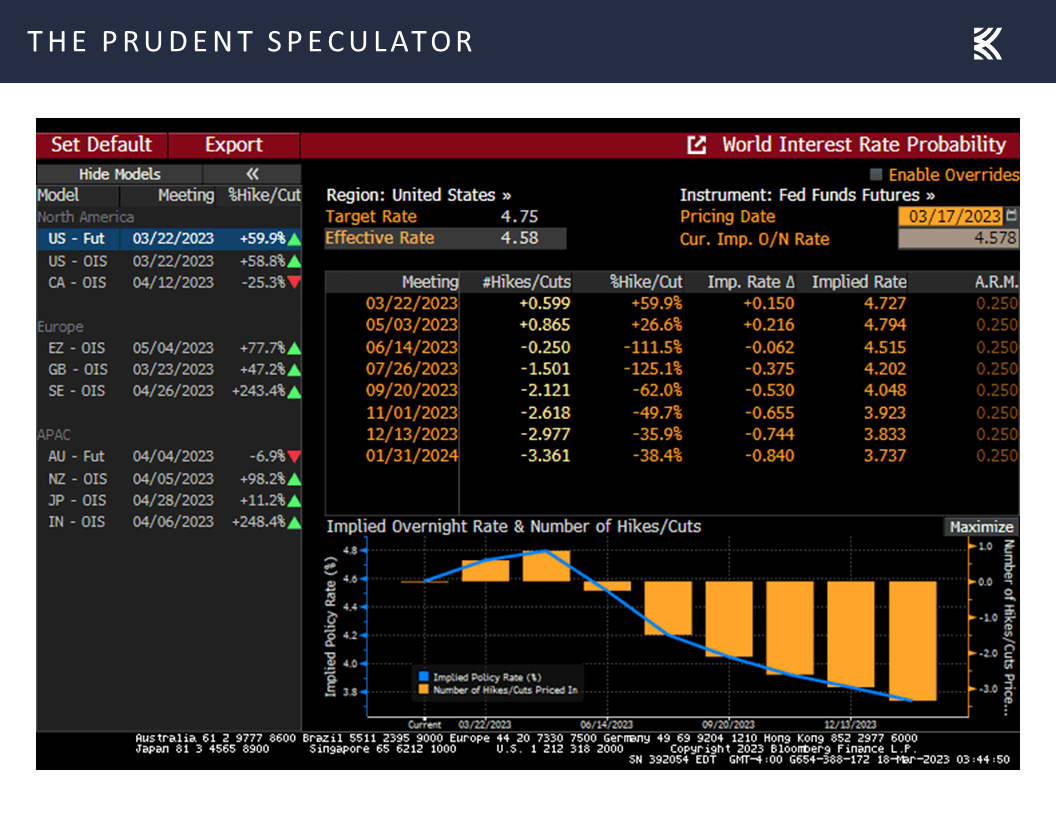

Fed: Market Predicting Jerome H. Powell & Co. to be Much-Less Hawkish

The turmoil in the banking sector must be considered when the Federal Open Market Committee meets this week, and the likelihood of another 25-basis-point bump in the Fed Funds rate is now a coin flip, per the futures market bets. However, the peak Fed Funds rate target has dropped to 4.79% as of Friday compared to 5.29% a week ago, while the year-end 2023 prediction stands at 3.83% versus 4.89%.

Headwinds: Equities Have Overcome Plenty of Adversity Through the Years

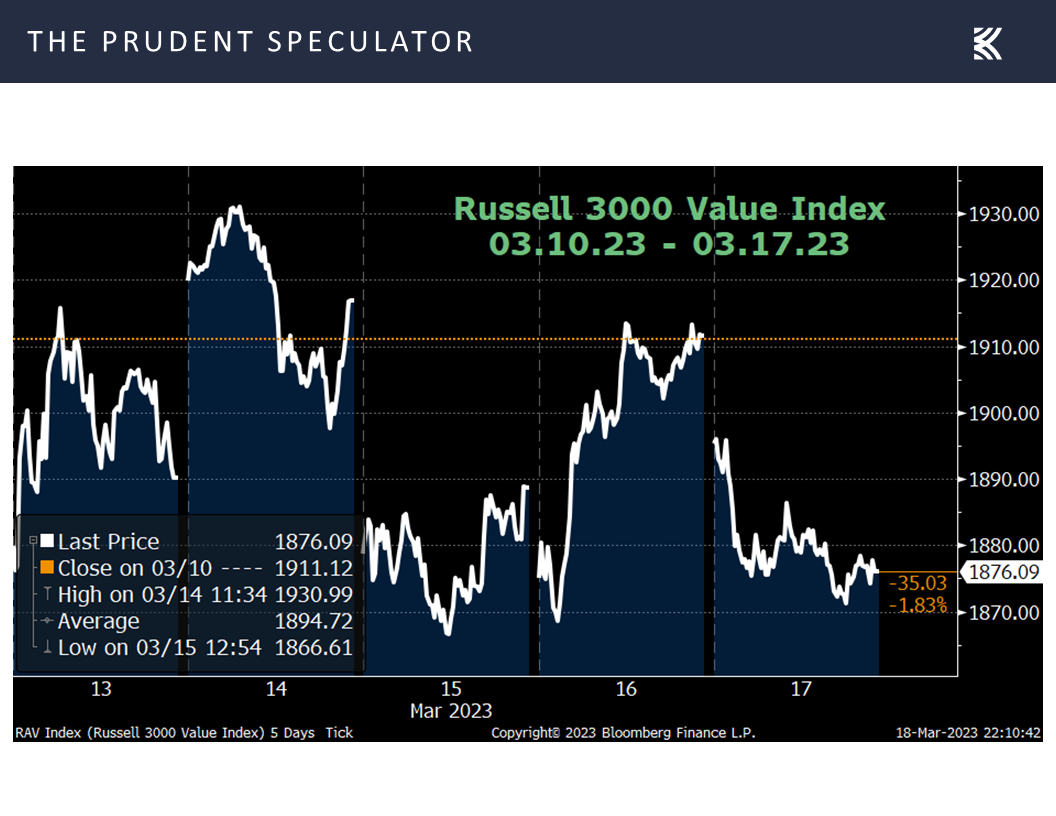

It has been a roller-coaster ride of late, with financial stocks especially hard-hit last week and the Value indexes taking it on the chin, while the average stock in the broad-based Russell 3000 index has now suffered a negative total return of 12.4% in the six-plus weeks since the end of January.

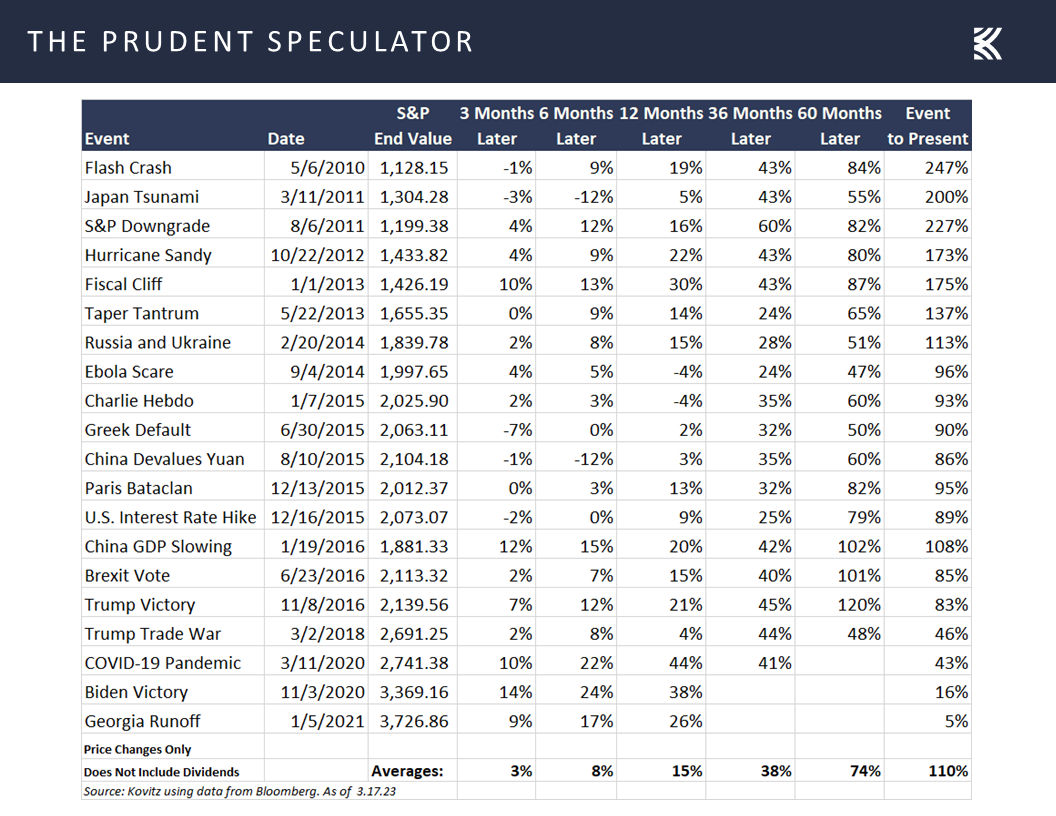

Certainly, we understand that many will see the proverbial glass as half empty in the attempt to rescue First Republic and the Credit Suisse fire-sale, and we won’t be surprised to see bank stocks come in for another round of selling when trading resumes this week, with the overall market likely dragged down in the process. Of course, we have navigated plenty of scary headlines before, with each frightening event overcome in the fullness of time,

so much so that long-term returns on equities have been terrific, despite numerous downturns, selloffs, corrections and even Bear Markets along the way.

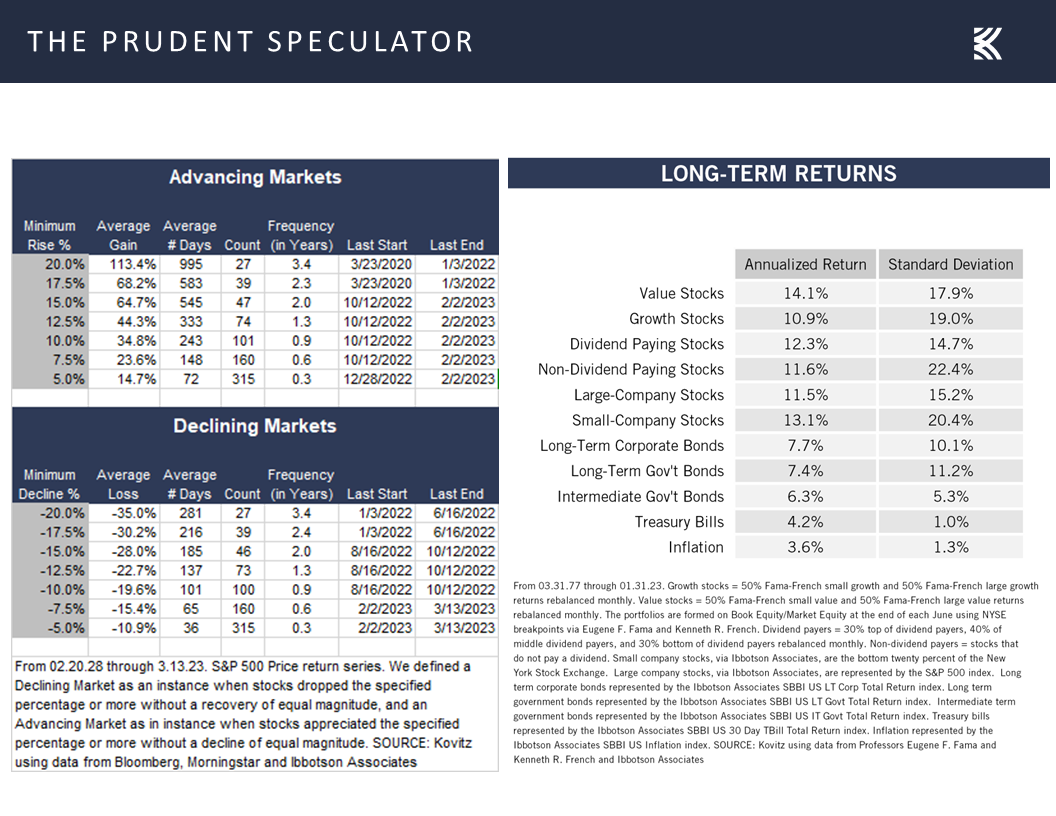

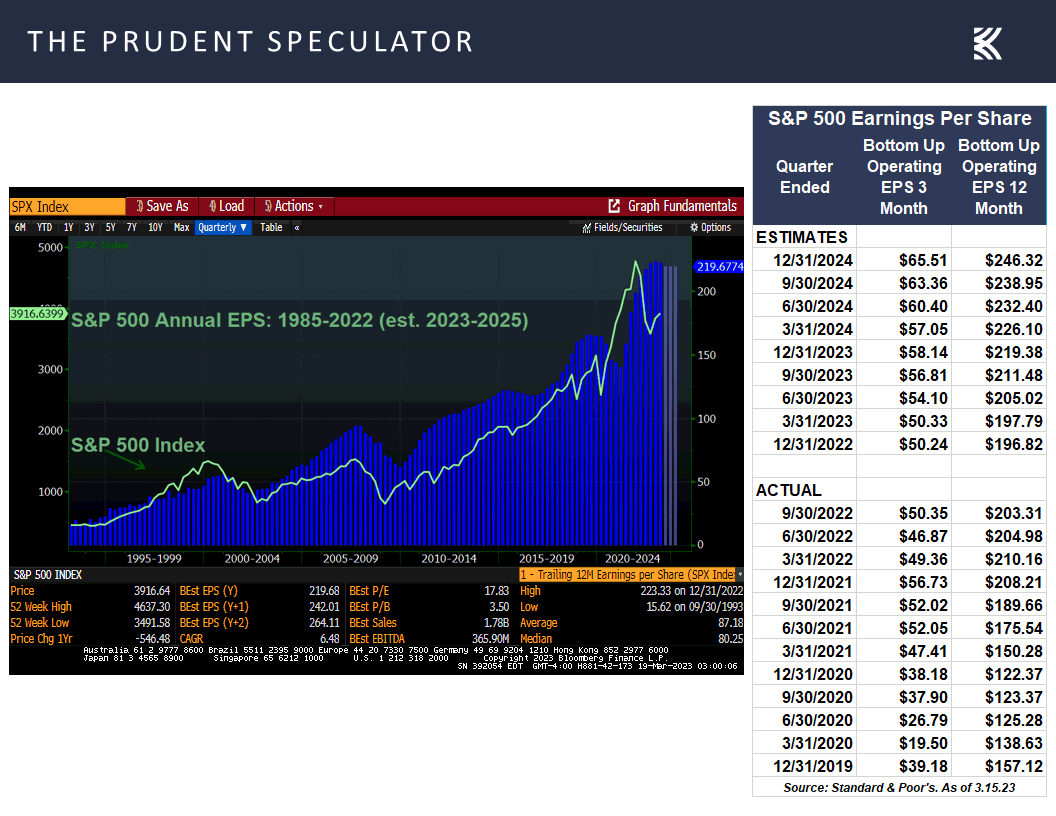

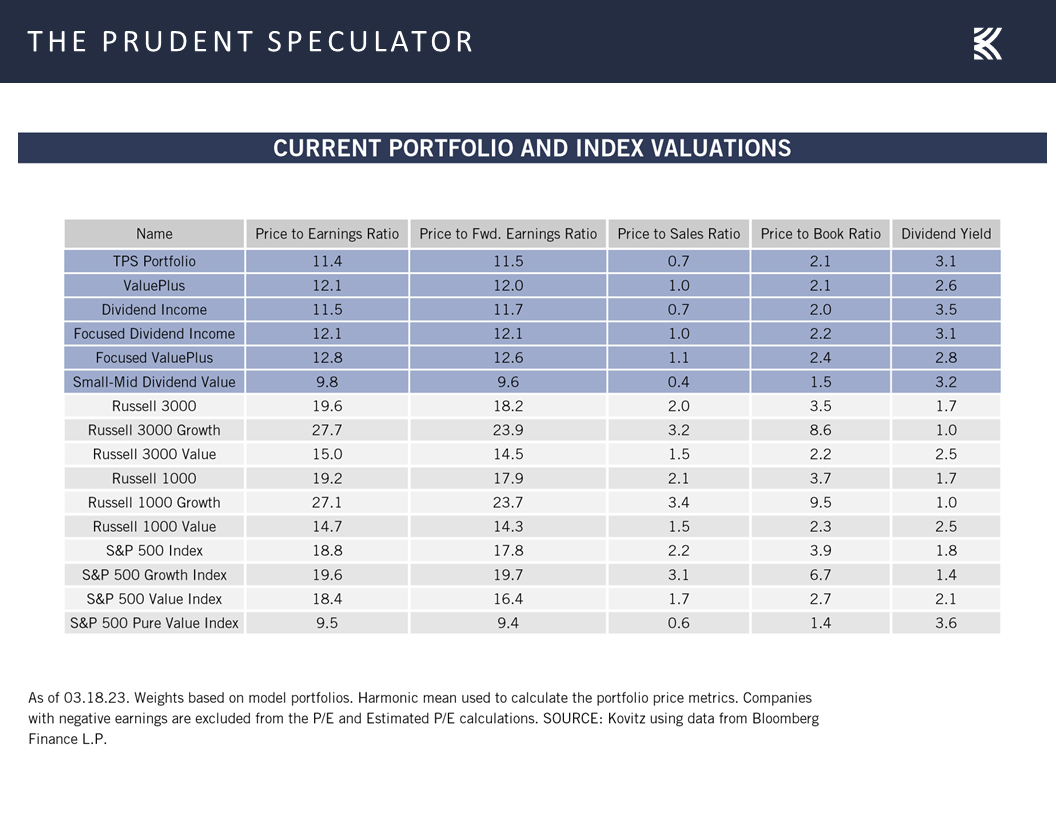

Valuations: Still Liking the Metrics for our Portfolios

We suspect that earnings estimates, which still call for healthy EPS growth for the S&P 500 this year and next, will be coming down,

but we continue to like the inexpensive valuations and generous yields on our broadly diversified portfolios of what we believe to be undervalued stocks.

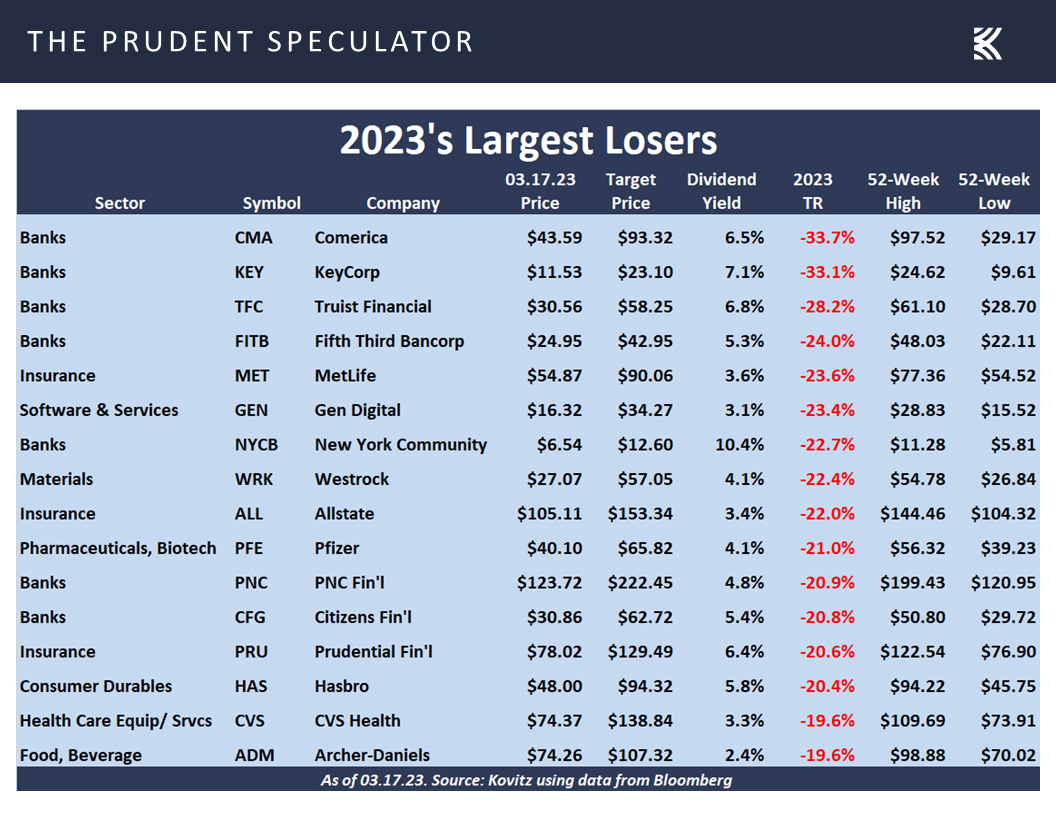

Shopping List: Hardest Hit Undervalued Stocks

With so much bad news arguably priced into many of our holdings, we think that there are plenty of opportunities these days for those with a strong stomach and a long-term time horizon. Of course, as always, we advocate broad industry and sector diversification, even as it is tempting to follow many of the corporate insiders who have been buying shares of their own banks.

Stock News & Earnings – Updates on three stocks across three different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Banking Crisis: Central Bankers Fighting Fear, Interest Rates and Market Predicting Jerome H. Powell

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. This week, we cover the Banking Crisis, Interest Rates, Inflation, the Fed, Portfolio Valuations, Undervalued Stocks that were hit the hardest and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Fear & Greed: Sentiment Heads South

Banking Crisis: Central Bankers Fighting Fear

Interest Rates: Bond Rally Helps Alleviate Bank Balance Sheet Stress

Econ News: Q1 GDP Forecast Improves; Jobs Numbers Remain Strong, But Other Numbers Not So Grand

Inflation: Longer-Term Expectations Recede; PPI Pulls Back

Fed: Market Predicting Jerome H. Powell & Co. to be Much-Less Hawkish

Headwinds: Equities Have Overcome Plenty of Adversity Through the Years

Valuations: Still Liking the Metrics for our Portfolios

Shopping List: Hardest Hit Undervalued Stocks

Stock News: Updates on three stocks across three different stocks

Week In Review:

Warren Buffett offered up that advice in 1986 when the Dow Jones Industrial Average was south of 2000 and one year before your Editor joined Al Frank at The Prudent Speculator. Obviously, with the Dow above 31000 today, the long-term trend for equities has been significantly higher, especially if dividends and their reinvestment are included, though there have been plenty of scary selloffs along the way.

Fear & Greed: Sentiment Heads South

While the average gains during the times in the green in the chart above dwarf the average losses during the periods in the red, we are now in an environment where fear levels are running high, with the CNN/Money Fear & Greed Index of 7 indicators moving into Extreme Fear Territory, led in that direction by gauges on Stock Price Breadth, Market Volatility, Safe Haven Demand and Junk Bond Demand.

It is an even more pessimistic story for the 36-year-old Sentiment Survey from the American Association of Individual Investors (AAII). The good folks at AAII said last week…

Bullish sentiment, expectations that stock prices will rise over the next six months, fell 5.6 percentage points to 19.2%. Optimism was last lower on September 22, 2022 (17.7%). Bullish sentiment is at an unusually low level for the fourth consecutive week and the 44th time out of the past 63 weeks. Bullish sentiment is also below its historical average of 37.5% for the 67th time out of the past 69 weeks.

Bearish sentiment, expectations that stock prices will fall over the next six months, rose 6.7 percentage points to 48.4%. Pessimism was last higher on December 22, 2022 (52.3%). This is the third consecutive week and the 42nd time out of the past 63 weeks that bearish sentiment is at an unusually high level. Bearish sentiment is also above its historical average of 31.0% for the 64th time out of the past 69 weeks.

The bull-bear spread (bullish minus bearish sentiment) decreased by 12.3 percentage points to –29.2% and remains unusually low for the fourth consecutive week. The bull-bear spread is at an unusually low level for the 46th time out of the past 63 weeks.

This week’s bullish sentiment reading is the 34th lowest recorded since the Sentiment Survey started in July 1987. The survey period included the failure of Silicon Valley Bank and Signature Bank, as well as the recent headlines surrounding Credit Suisse.

Historically, the S&P 500 index has gone on to realize above-average and above-median returns during the six- and 12-month periods following unusually low readings for bullish sentiment and the bull-bear spread. Similarly, the market benchmark has gone on to realize above-average and above-median returns during the six- and 12-month periods following unusually high readings for bearish sentiment.

Banking Crisis: Central Bankers Fighting Fear

Of course, as AAII stated, the survey period included the failures of Silicon Valley Bank and Signature Bank, as well as some, but not all the drama around Credit Suisse.

On Thursday the embattled European banking giant said it would borrow up to 50 billion Swiss francs ($54 billion) from the Swiss Central bank in an effort to shore up its liquidity. Then, on Sunday a hastily arranged shotgun marriage was orchestrated in which rival UBS agreed to buy Credit Suisse for $3.25 billion in stock, with the Swiss National Bank providing 100 billion Swiss francs in liquidity assistance.

The demise of Credit Suisse was extraordinary, with Swiss President Alain Berset saying it was impossible to restore confidence in the company and Swiss Finance Minister Karin Keller-Sutter stating, “The takeover plan will offer greater stability both in Switzerland and internationally.” Swiss National Bank President Thomas Jordan, further asserted, “It was indispensable that we acted quickly and find a solution as quickly as possible, given that Credit Suisse is a systemically important bank.”

While many will argue that Credit Suisse was mismanaged, it really was a crisis of confidence that triggered the collapse as accelerating deposit outflows were cited as the core reason, just as was the case with Silicon Valley Bancorp and Signature Bank. Speaking of that duo, Janet Yellen explained last week, “No matter how strong capital and liquidity supervision are, if a bank has an overwhelming run that’s spurred by social media so that it’s seeing deposits flee at that pace, a bank can be put in danger of failing.”

That in mind, the Treasury Secretary on Thursday helped orchestrate a deposit infusion into West Coast regional bank First Republic (FRC), whose concentration of high-net-worth customers had contributed to an uninsured deposits balance of $119.5 billion (over two-thirds of total deposits) as of December 31, 2022, a significant amount of which were demand deposits.

With worries about a run on First Republic growing, a consortium of the nation’s biggest banks and some of the largest regional banks cooperated in a remarkable show of unity to try to stem depositor panic by infusing $30 billion of deposits into FRC from their own balance sheets.

Bank of America, Citigroup, JPMorgan Chase and Wells Fargo announced today they are each making a $5 billion uninsured deposit into First Republic Bank. Goldman Sachs and Morgan Stanley are each making an uninsured deposit of $2.5 billion, and BNY-Mellon, PNC Bank, State Street, Truist and U.S. Bank are each making an uninsured deposit of $1 billion, for a total deposit from the eleven banks of $30 billion. This action by America’s largest banks reflects their confidence in First Republic and in banks of all sizes, and it demonstrates their overall commitment to helping banks serve their customers and communities. Regional, midsize and small banks are critical to the health and functioning of our financial system.

Following the receiverships of Silicon Valley Bank and Signature Bank, there were outflows of uninsured deposits at a small number of banks. America’s financial system is among the best in the world, and America’s banks – large, midsize and community banks – do an extraordinary job serving the banking needs of their unique customers and communities. The banking system has strong credit, plenty of liquidity, strong capital and strong profitability. Recent events did nothing to change this.

The actions of America’s largest banks reflect their confidence in the country’s banking system. Together, we are deploying our financial strength and liquidity into the larger system, where it is needed the most. Smaller- and medium-sized banks support their local customers and businesses, create millions of jobs and help uplift communities. America’s larger banks stand united with all banks to support our economy and all of those around us.

While the numbers on deposit flows are not known, it is presumed that most of the banks involved have been beneficiaries of the banking crisis, at least in terms of new business heading their way. Given that we own 8 of the consortium’s 11 banks, we see the ability to step up to the table as a positive sign of their own financial strength.

Interest Rates: Bond Rally Helps Alleviate Bank Balance Sheet Stress

We might also add that the plunge in interest rates during the recent flight to safety, with the yield on the benchmark 10-year Treasury at 3.43%, down from 3.87% at the start of the year and over 4.02% on March 2,

as well as a sizable rally in mortgage backed securities, an index of which has gained more than 2% since the end of February and is now up on the year,

We are not suggesting that banks are in better shape today than they were at the start of the year, and our pruning of Target Prices illustrates the point as greater regulation and stronger capital requirements, along with potentially reduced loan demand, constrained loan supply and greater non-performing assets are likely byproducts of the bank mess. However, we agree with Ms. Yellen and Federal Reserve Chair Jerome H. Powell who said on Sunday, “The capital and liquidity positions of the U.S. banking system are strong, and the U.S. financial system is resilient.”

Econ News: Q1 GDP Forecast Improves; Jobs Numbers Remain Strong, But Other Numbers Not So Grand

We might add that the U.S. economy has proven to be quite resilient in its own right, with the Atlanta Fed’s forecast for Q1 inflation-adjusted GDP growth climbing to 3.2% last week,

True, the odds of recession in the next 12 months, per calculations from Bloomberg, continue to be high,

and the outlook for East Coast factory activity deteriorated last week, with both the Empire and Philadelphia Fed’s Manufacturing indexes for March coming in well below expectations.

On the other hand, the latest read on retail sales was in line with forecasts of a 0.4% pullback from January’s robust tally,

and the Small Business Optimism and Homebuilder Confidence gauges topped projections.

To be sure, the economic outlook is cloudy to say the least, and we respect commentary released on Friday with the Leading Economic Index (LEI) by the Conference Board, even as the February gauge was in line with or a little better than expectations.

The LEI for the U.S. fell again in February, marking its eleventh consecutive monthly decline. Negative or flat contributions from eight of the index’s ten components more than offset improving stock prices and a better-than-expected reading for residential building permits. While the rate of month-over-month declines in the LEI have moderated in recent months, the leading economic index still points to risk of recession in the U.S. economy. The most recent financial turmoil in the US banking sector is not reflected in the LEI data but could have a negative impact on the outlook if it persists. Overall, The Conference Board forecasts rising interest rates paired with declining consumer spending will most likely push the U.S. economy into recession in the near term.

Inflation: Longer-Term Expectations Recede; PPI Pulls Back

We also realize that the latest measure of consumer sentiment from the University of Michigan retreated to a worse-than-expected 63.4, down from 67.0 the month prior,

Interestingly, if not for the bank turmoil, the broad market might have rallied last week as the Consumer Price Index year-over-year change of 6.0% in February was as expected,

but the Producer Price Index saw a significant drop to 4.6% in its year-over-year change last month versus 5.7% in January.

Fed: Market Predicting Jerome H. Powell & Co. to be Much-Less Hawkish

The turmoil in the banking sector must be considered when the Federal Open Market Committee meets this week, and the likelihood of another 25-basis-point bump in the Fed Funds rate is now a coin flip, per the futures market bets. However, the peak Fed Funds rate target has dropped to 4.79% as of Friday compared to 5.29% a week ago, while the year-end 2023 prediction stands at 3.83% versus 4.89%.

Headwinds: Equities Have Overcome Plenty of Adversity Through the Years

It has been a roller-coaster ride of late, with financial stocks especially hard-hit last week and the Value indexes taking it on the chin, while the average stock in the broad-based Russell 3000 index has now suffered a negative total return of 12.4% in the six-plus weeks since the end of January.

Certainly, we understand that many will see the proverbial glass as half empty in the attempt to rescue First Republic and the Credit Suisse fire-sale, and we won’t be surprised to see bank stocks come in for another round of selling when trading resumes this week, with the overall market likely dragged down in the process. Of course, we have navigated plenty of scary headlines before, with each frightening event overcome in the fullness of time,

so much so that long-term returns on equities have been terrific, despite numerous downturns, selloffs, corrections and even Bear Markets along the way.

Valuations: Still Liking the Metrics for our Portfolios

We suspect that earnings estimates, which still call for healthy EPS growth for the S&P 500 this year and next, will be coming down,

but we continue to like the inexpensive valuations and generous yields on our broadly diversified portfolios of what we believe to be undervalued stocks.

Shopping List: Hardest Hit Undervalued Stocks

With so much bad news arguably priced into many of our holdings, we think that there are plenty of opportunities these days for those with a strong stomach and a long-term time horizon. Of course, as always, we advocate broad industry and sector diversification, even as it is tempting to follow many of the corporate insiders who have been buying shares of their own banks.

Stock News & Earnings – Updates on three stocks across three different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.