The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss a case for value, inflation, earnings, econ data and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week in Review – Soldiers Outflank the Generals

Case for Value – Historical Outperformance & Reasonable Metrics

Fed Speak – Proceeding Carefully as Risks are Becoming More Balanced

Inflation – Core PCE Falls; Interest Rates Continue to Decline

Econ Data – Housing & ISM Numbers Weak; Jobs and Q3 GDP Strong

Earnings – Handsome Profit Growth Expected in ’24

Staying the Course – Inexpensive Stocks, Patience and the Calendar on our Side

Stock News – Updates on six stocks across six different sectors

Week in Review – Soldiers Outflank the Generals

It was our kind of week as the Most-Wonderful-Time-of-the-Year rally broadened out considerably over the past five trading sessions with the average stock gaining much more than most of the large-cap-dominated indexes and the Russell 3000 Value index outperforming its Growth counterpart by a wide margin.

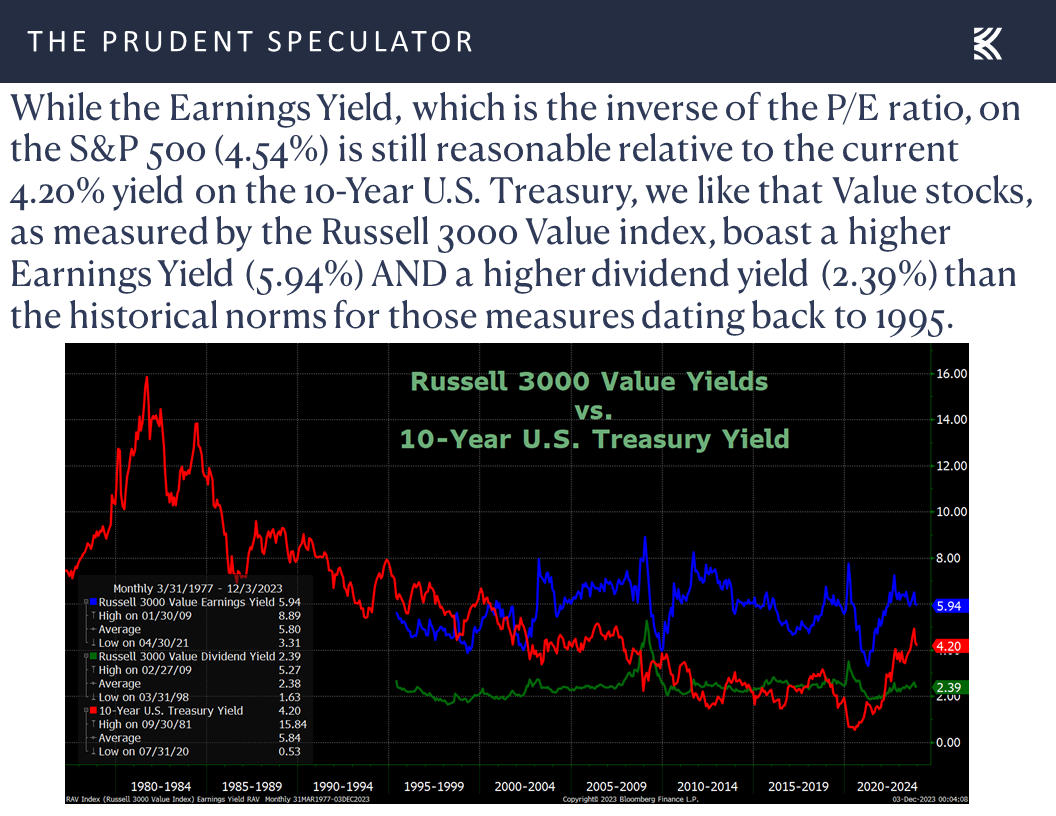

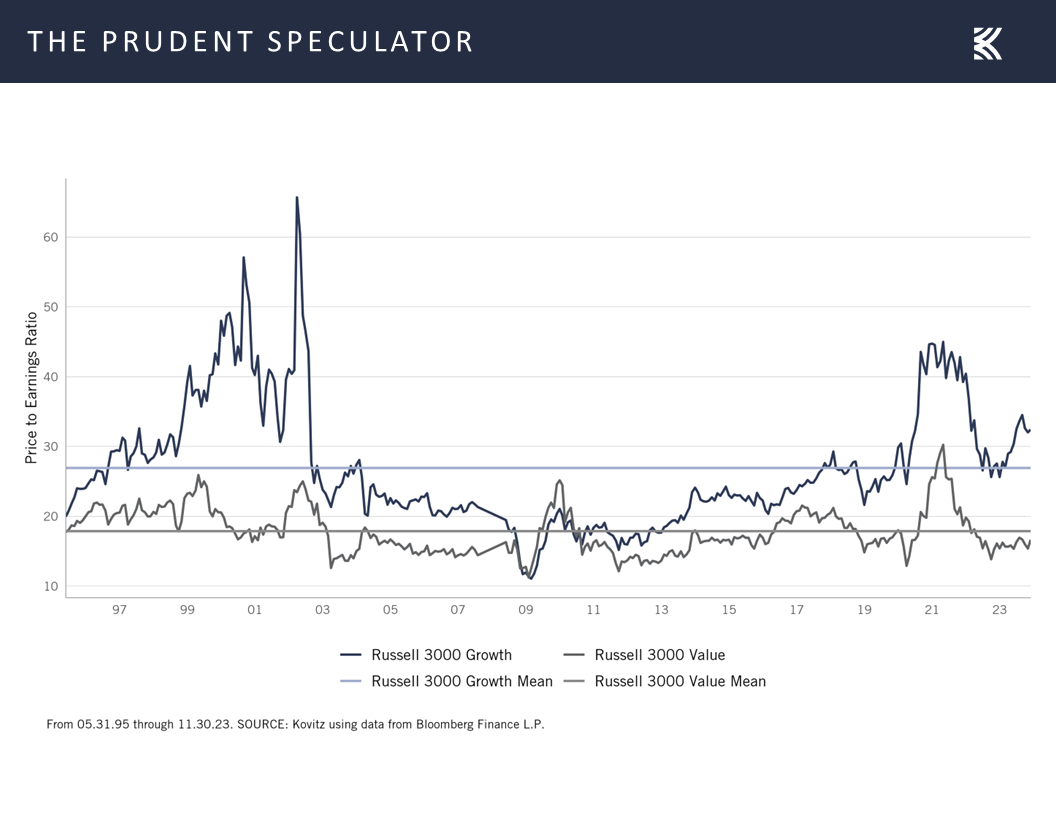

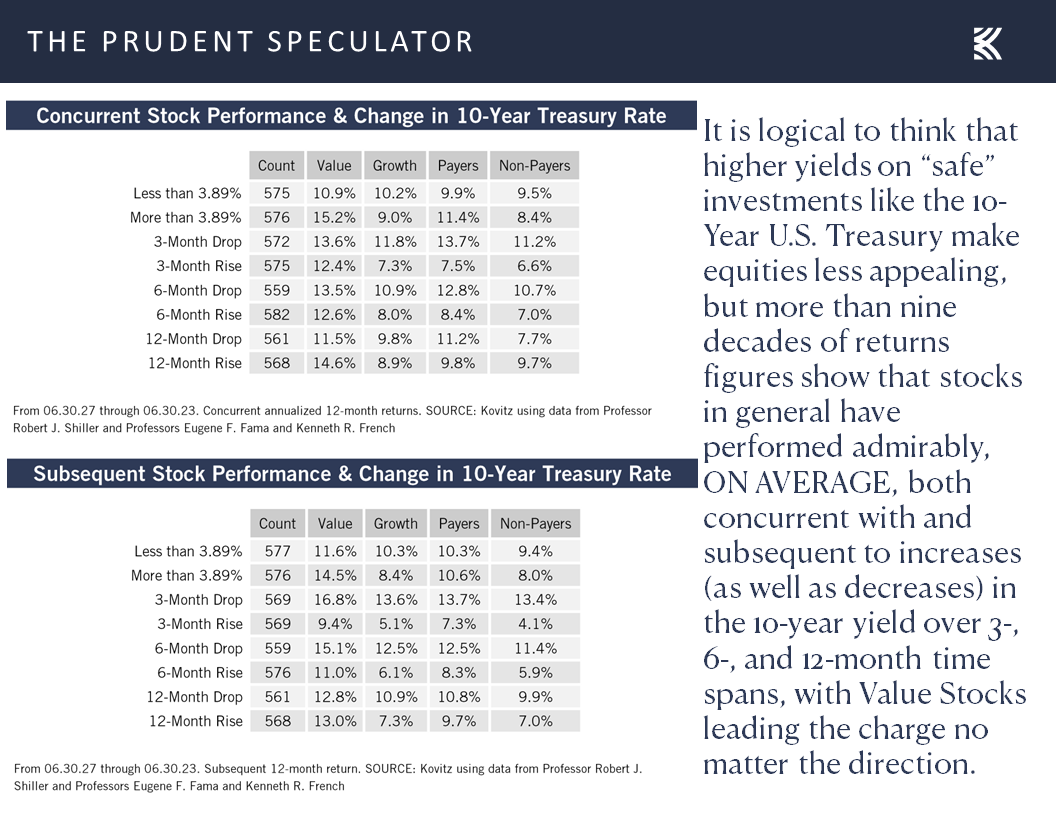

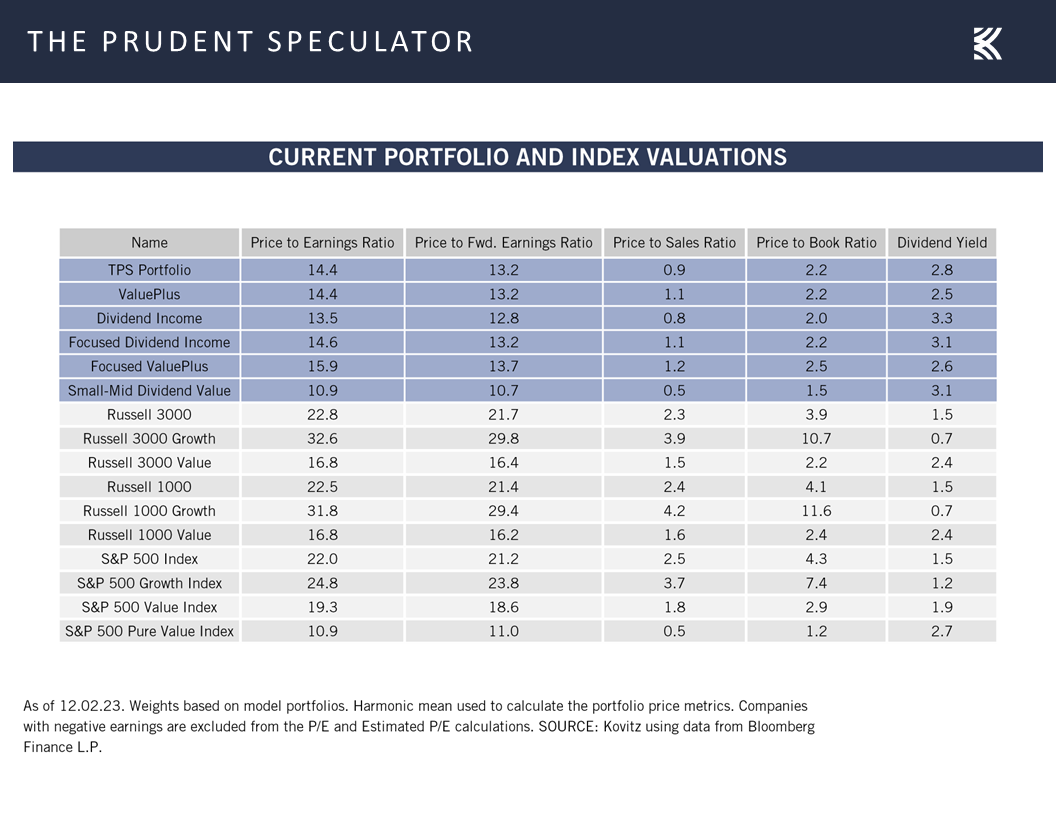

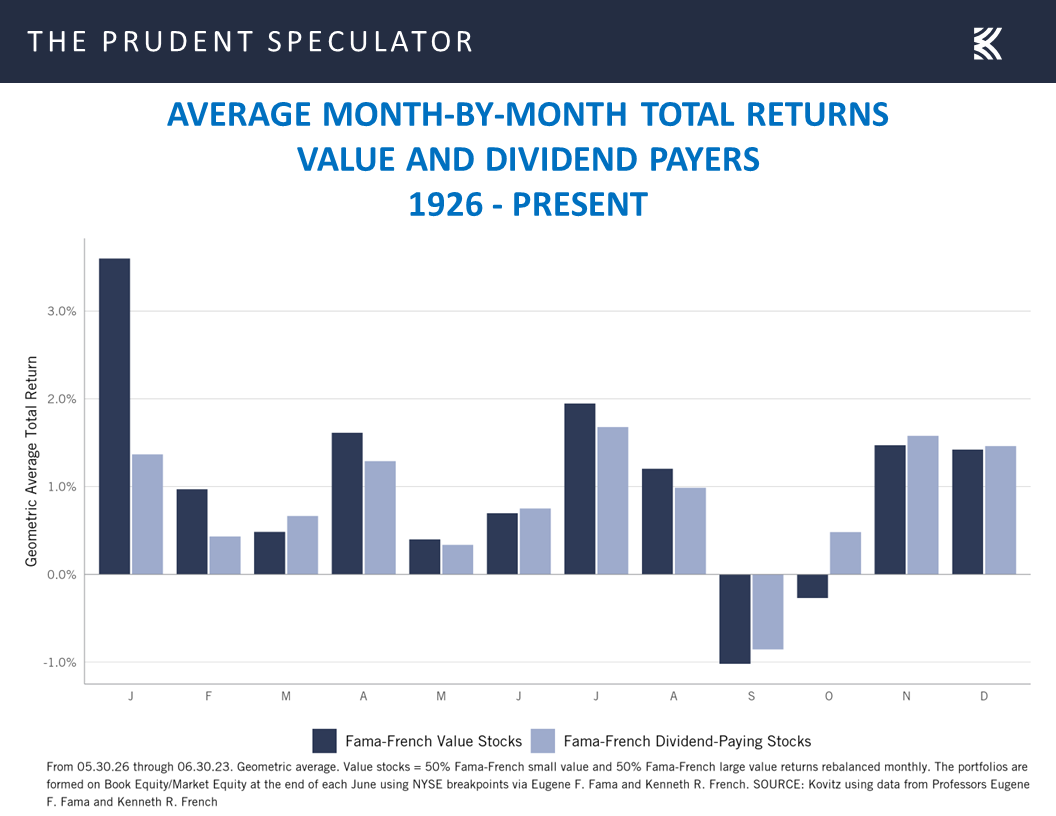

While we think Value stocks should be of great interest today, given that historically they have done the best,

and they are attractively priced on an absolute basis,

Case for Value – Historical Outperformance & Reasonable Metrics

and especially on a relative-to-Growth basis, when today’s metrics are compared to the historical norms,

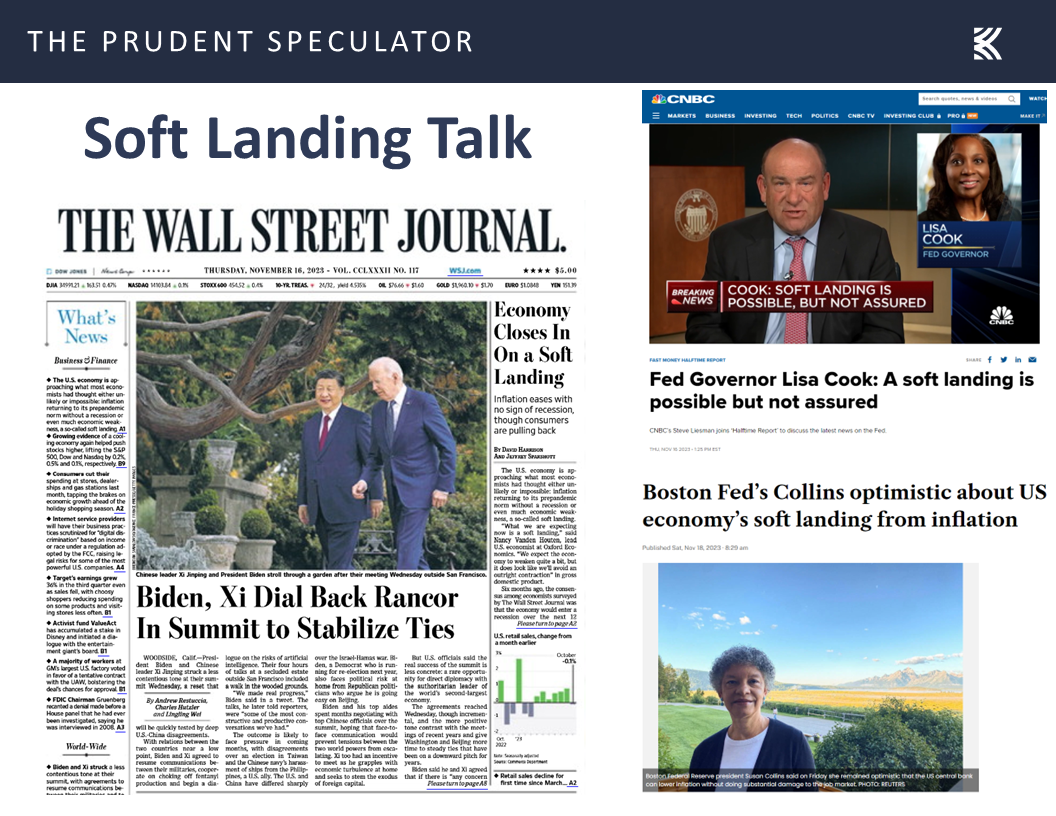

the catalyst for the renewed interest evidently was talk from Federal Reserve officials.

Fed Speak – Proceeding Carefully as Risks are Becoming More Balanced

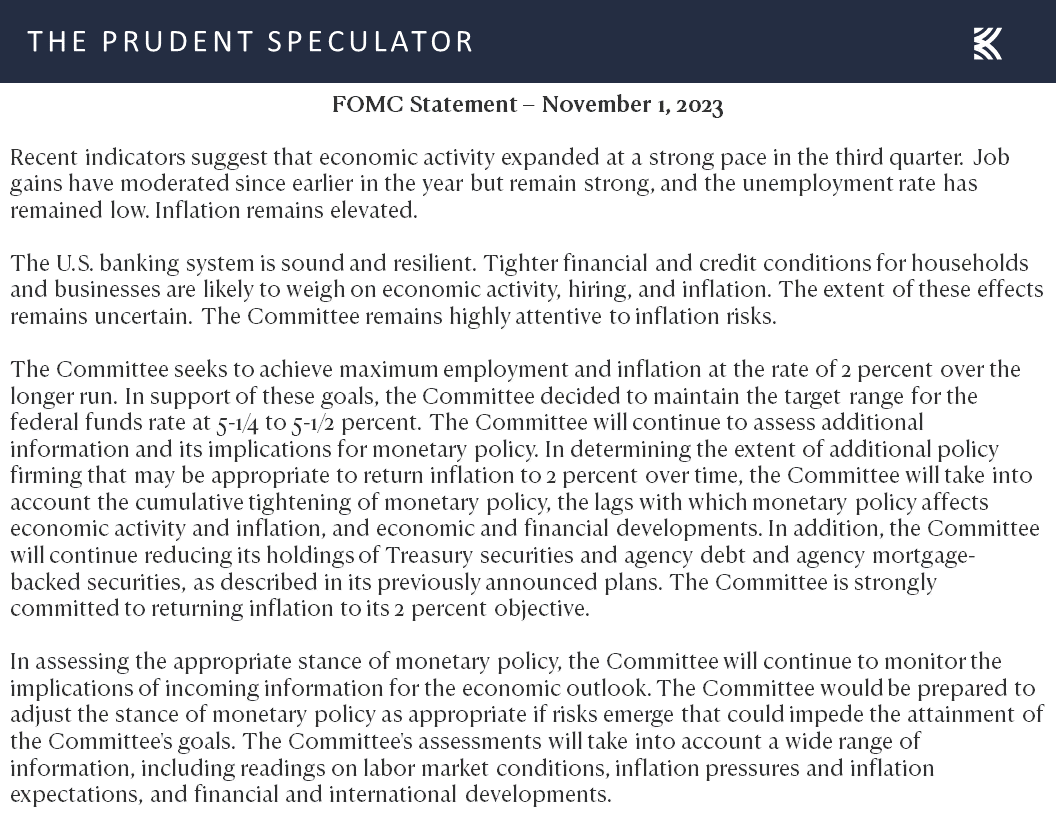

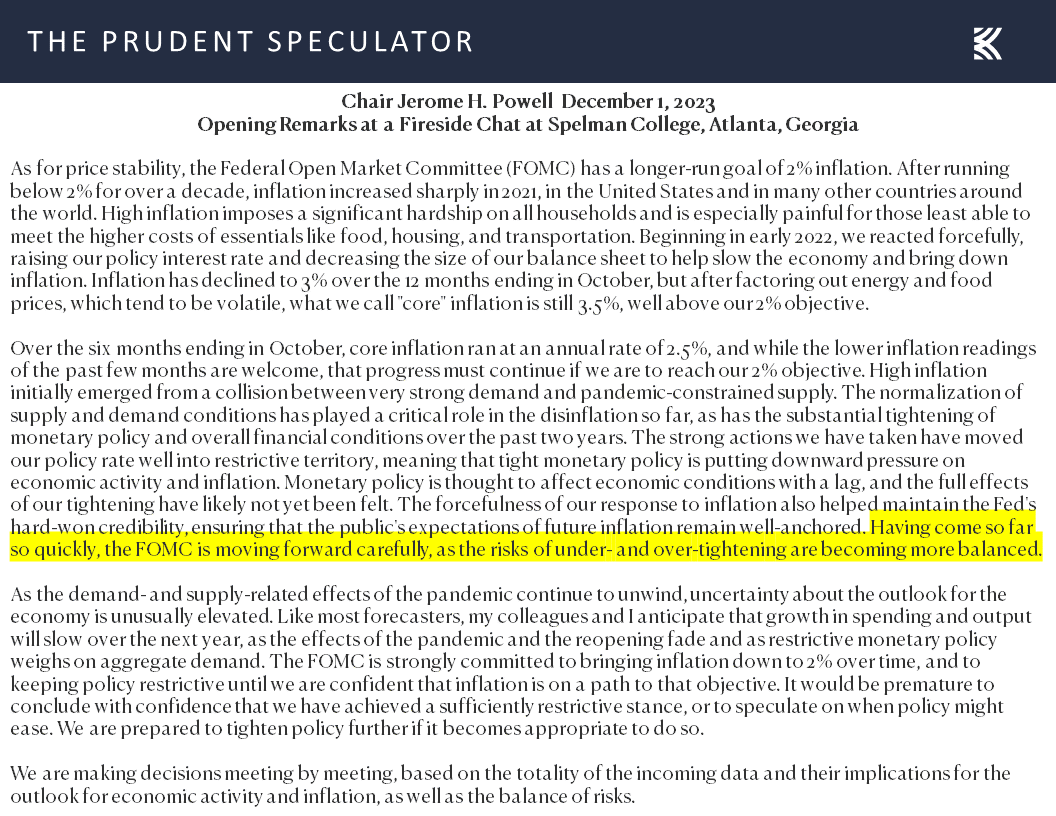

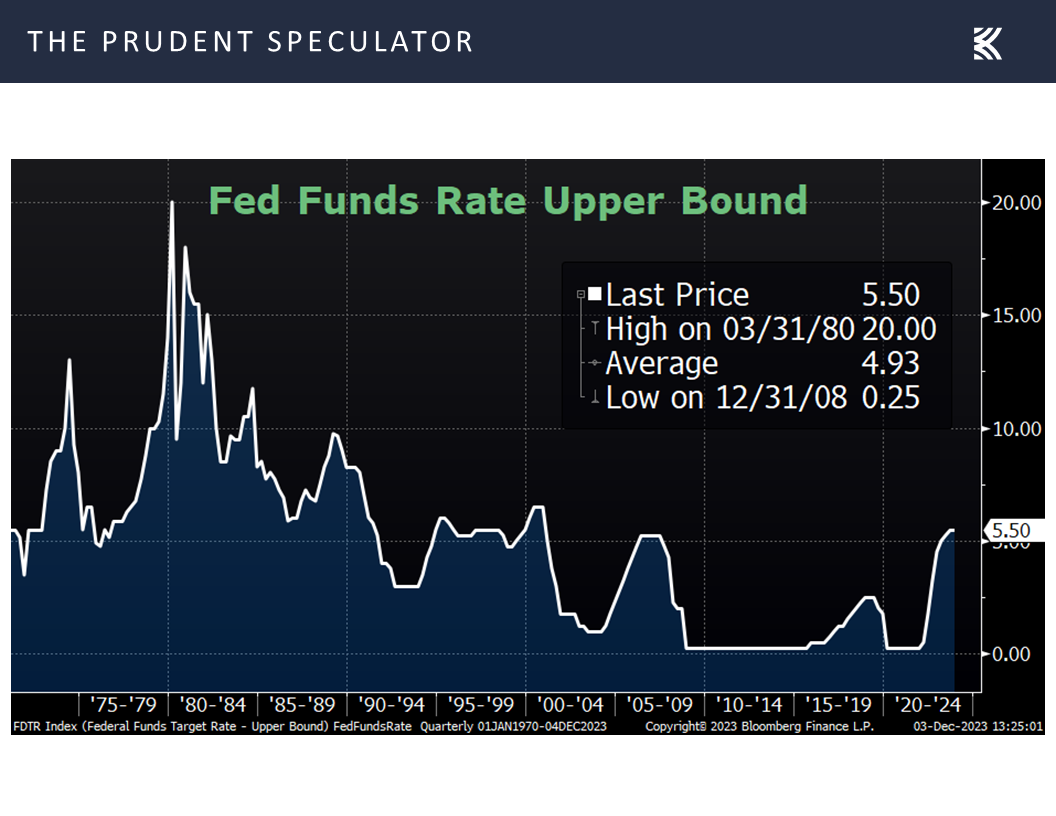

While we do not think we have heard much different in the Fed Speak from U.S. central bankers since the target for the Fed Funds rate was left unchanged at 5.25% to 5.50% and the FOMC Statement was released on November 1,

market participants have gained much greater conviction that Jerome Powell & Co. are finished with additional tightening of monetary policy this cycle as The New York Times proclaimed last week, “Fed Officials Hint That Rate Increases Are Over, and Investors Celebrate!”

We suppose we could construe the Fed Chair’s continued usage on Friday of language like, “The FOMC is moving forward carefully,” as confirmation that the Fed is done, especially as Mr. Powell added, “The risks of under- or over-tightening are becoming more balanced,”

Inflation – Core PCE Falls; Interest Rates Continue to Decline

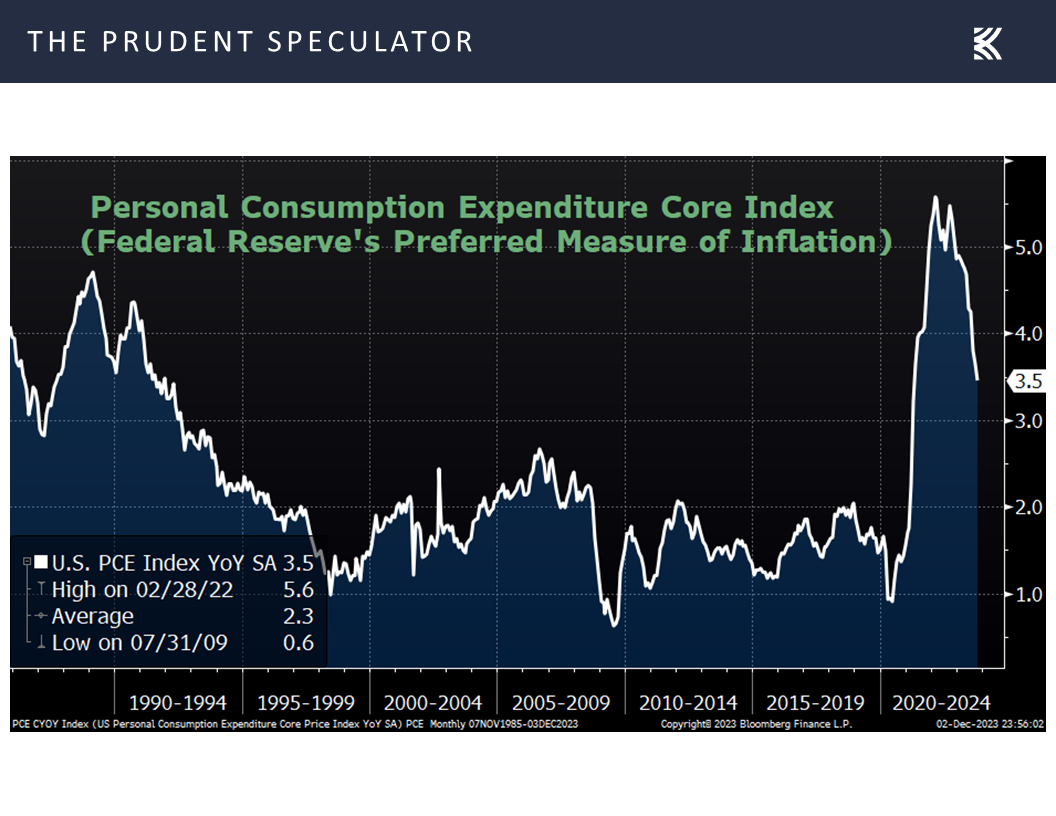

while the latest read on inflation showed a continued decline in the Fed’s preferred measure of inflation, the Personal Consumption Expenditure Core Index, to 3.5% in October, down from 3.7% the month prior.

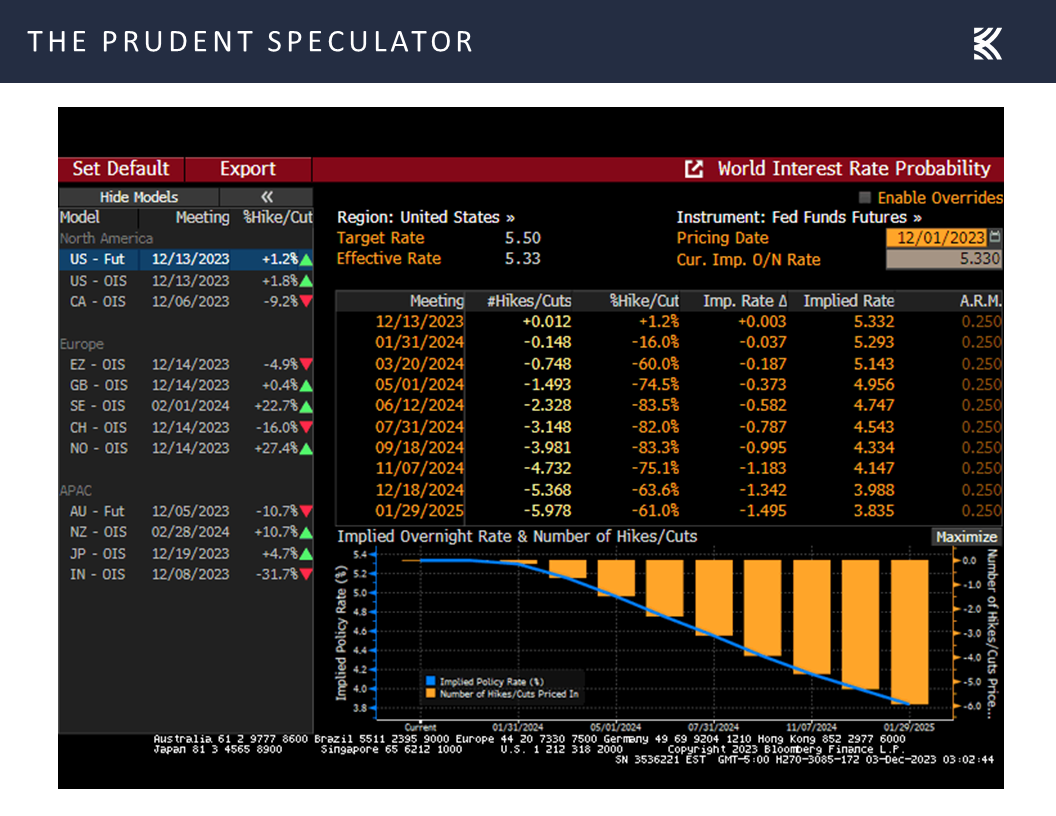

Certainly, the futures market decided a while ago that the Fed is done with rate hikes and the betting last week added two more cuts in the Fed Funds rate,

to a level below 4% by the end of next year,

and long-term interest rates continued their plunge over the last month, with the benchmark 10-Year U.S. Treasury yield dropping from 4.93% on Halloween to a current level of 4.20%.

No doubt, conventional wisdom would suggest that lower bond yields are better for equities and vice versa, but history shows that stocks perform fine whether interest rates are rising or falling, with Value preferring a yield above the long-term norm of 3.89%.

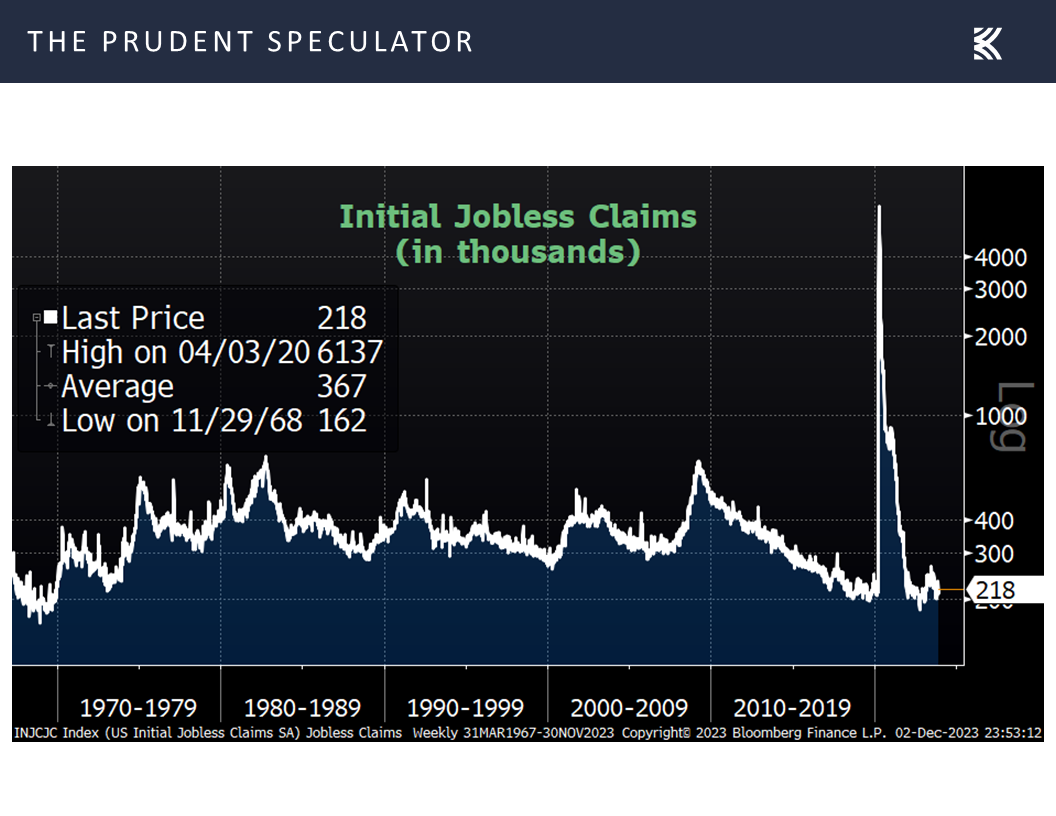

Econ Data – Housing & ISM Numbers Weak; Jobs and Q3 GDP Strong

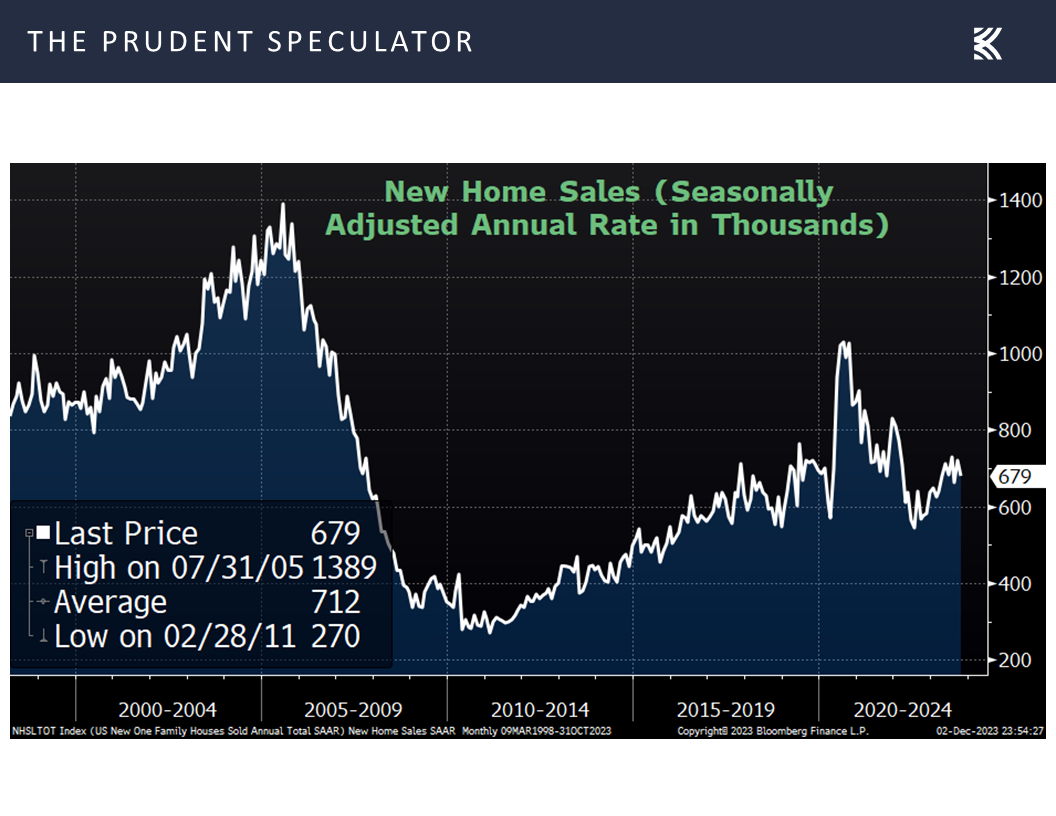

Interestingly, the rally in stocks took place even as the latest housing numbers (from October) continued to decline, be it for new home sales,

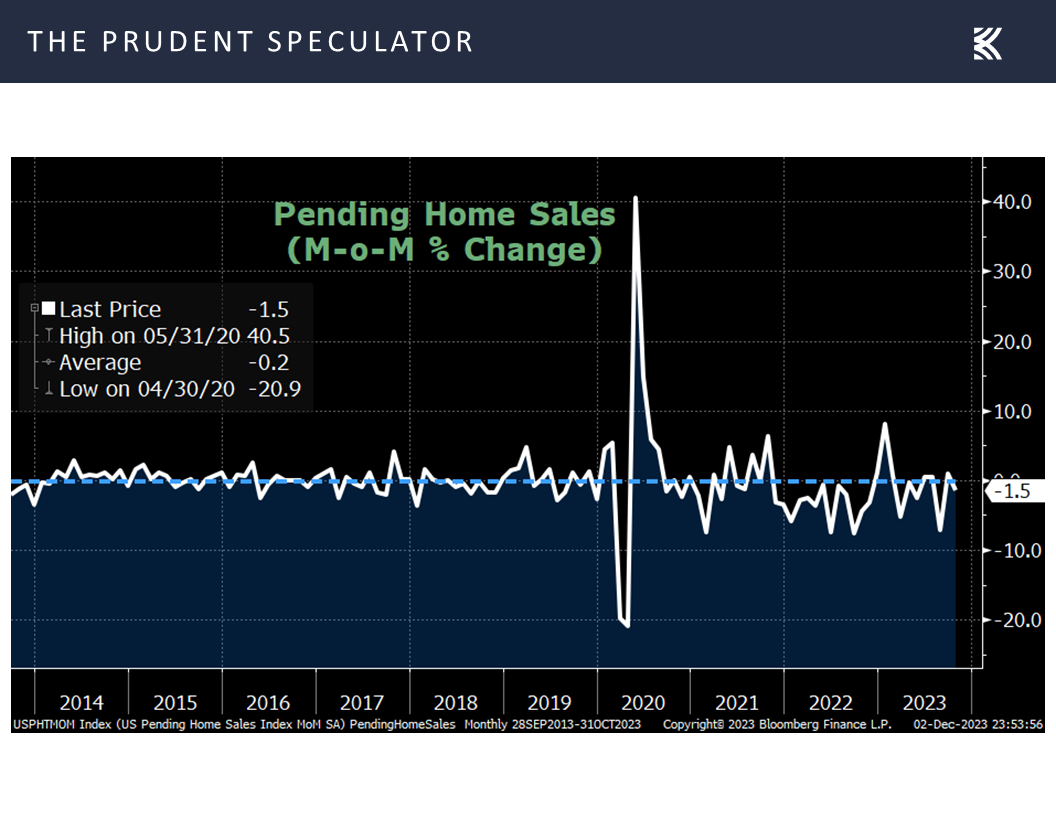

or pending sales of existing homes,

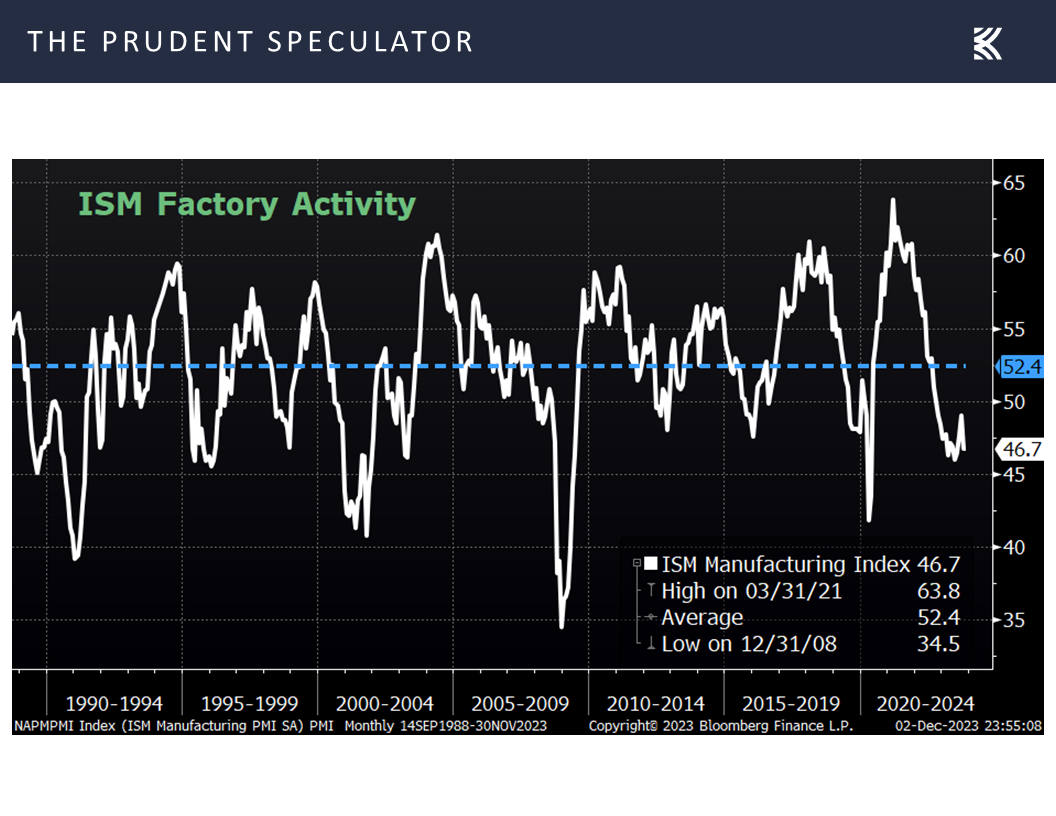

while the November ISM Manufacturing index came in below expectations at a reading of 46.7, which supposedly corresponds to a change of minus 0.7% in real (inflation-adjusted) gross domestic product (GDP) on an annualized basis.

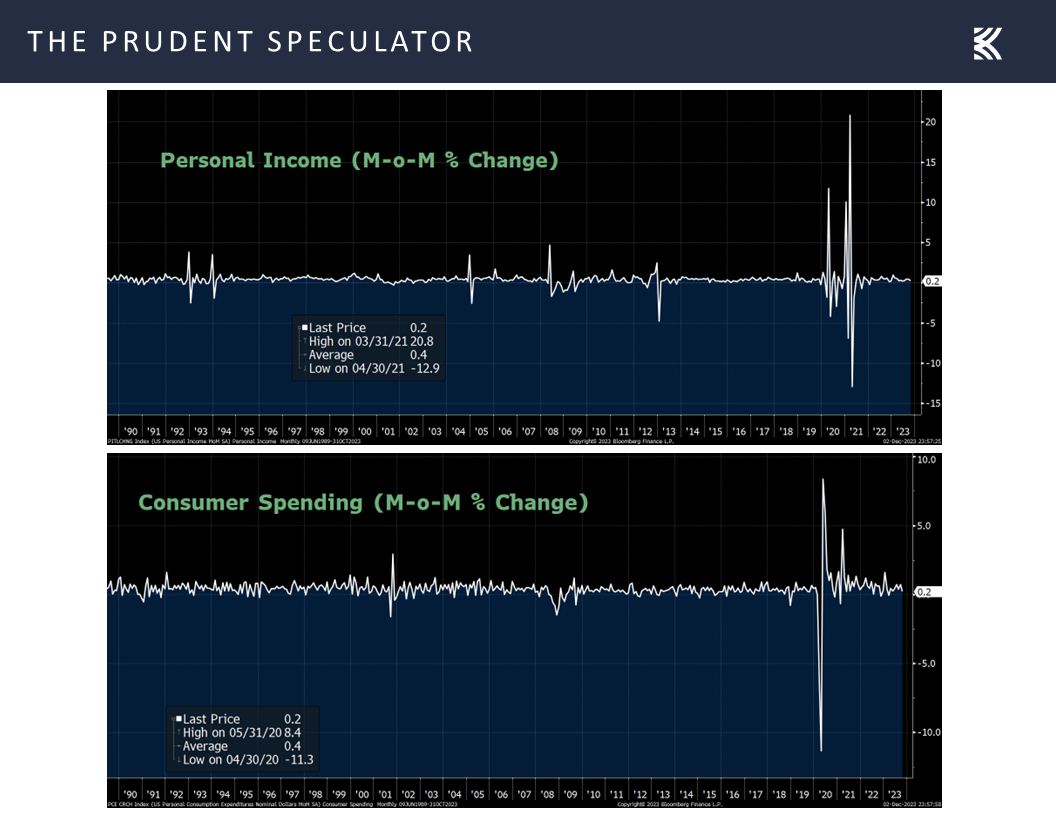

On the other hand, both personal incomes and spending held up well in October,

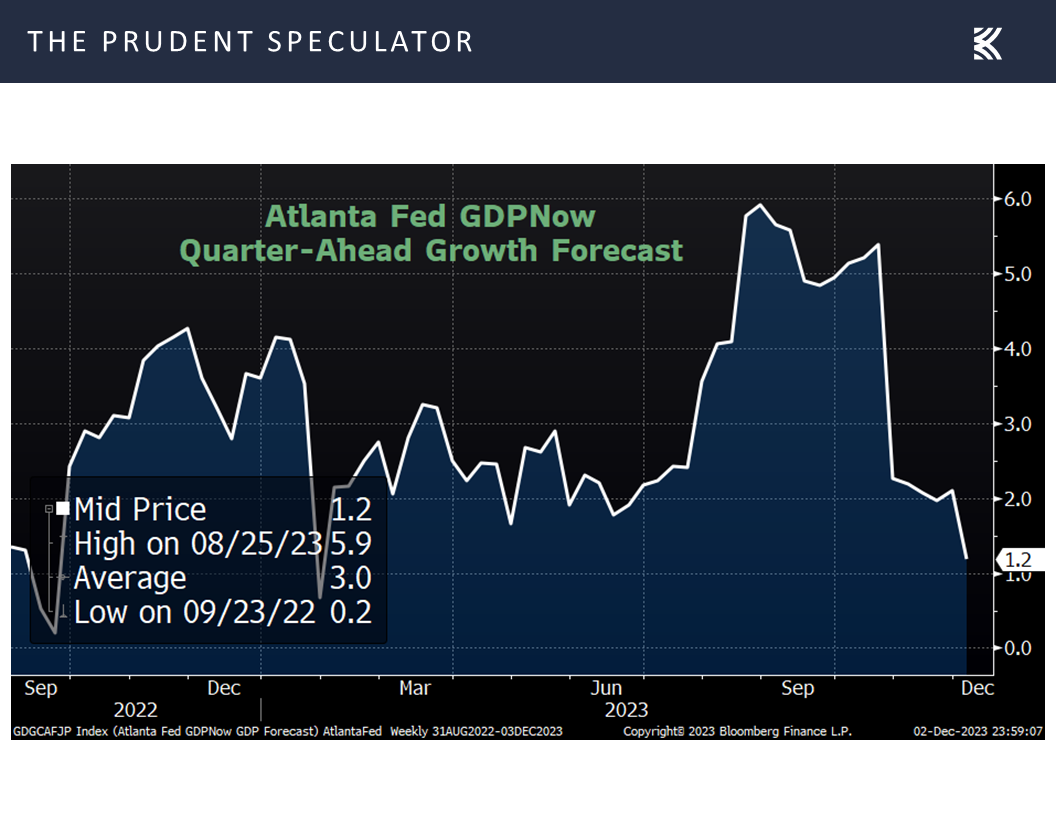

while the Atlanta Fed projects that Q4 U.S. real GDP growth will increase 1.2%,

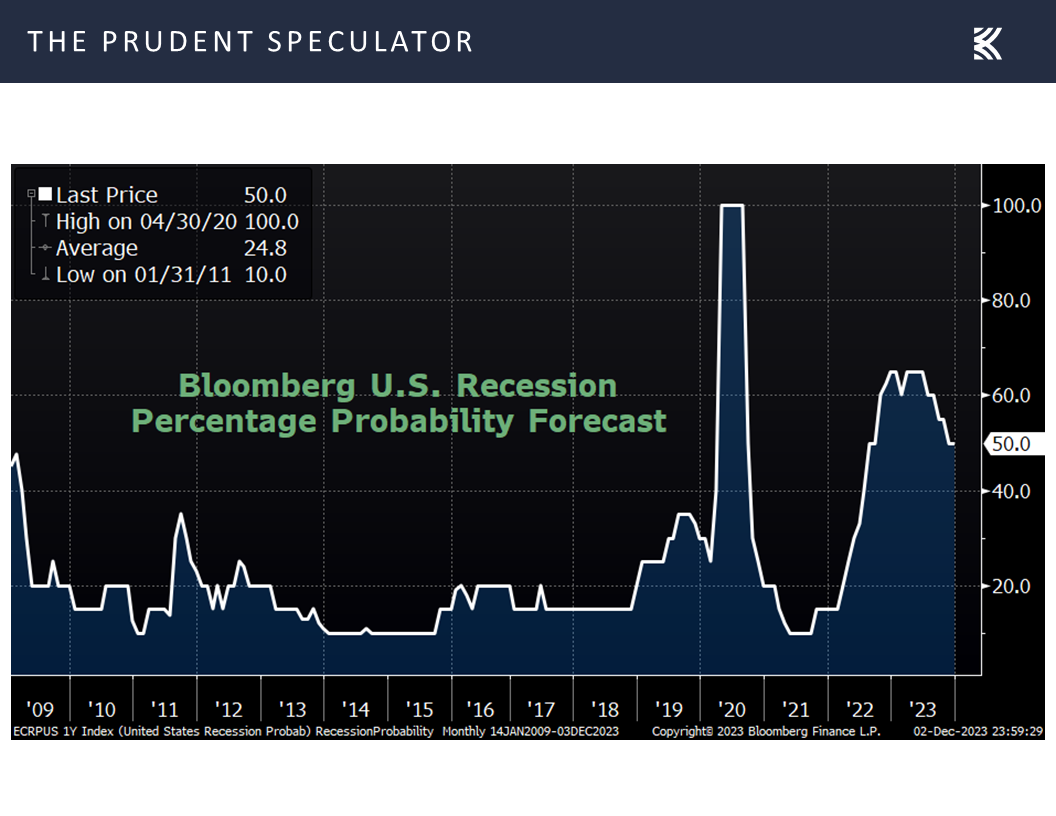

the odds of recession in the next 12 months, per tabulations from Bloomberg, edged down to 50%,

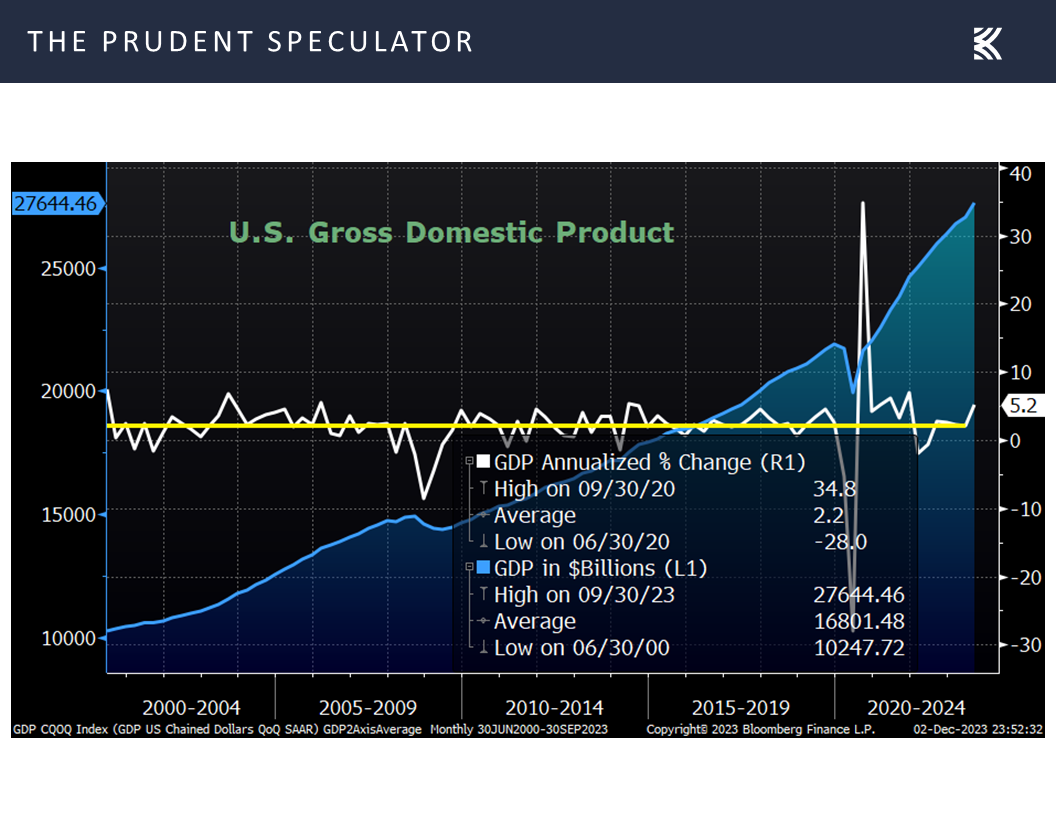

and Q3 real GDP growth was revised upward to a very impressive 5.2% from an already robust 4.9%.

Also on Friday, Chair Powell talked about the other half of the Federal Reserve’s dual mandate, namely maximizing employment:

I am glad to say that, by many measures, conditions in the labor market are very strong. A couple of years ago, as the pandemic receded and the economy reopened, the number of job openings grew to greatly exceed the supply of people available to work, leaving a widespread shortage of workers. Today, labor market conditions remain very strong, and the economy is returning to a better balance between the demand for and supply of workers.

The pace at which the economy is creating new jobs remains strong, and has been slowing toward a more sustainable level. That gradual slowing has come in part due to the efforts of the Fed to slow the growth of the economy to help reduce inflation. After declining sharply during the pandemic, the supply of workers has bounced back, as people have come back into the labor force and as immigration has returned to pre-pandemic levels. Partly because of that labor force growth, the unemployment rate has edged up over the second half of the year, though it remains historically low at 3.9%. The increase in participation has been particularly strong among women in the prime working ages of 25 to 54, which surged to an all-time high earlier this year, and which remains well above pre-pandemic levels. Wage growth remains high but has been gradually moving toward levels that would be more consistent with 2% price inflation over time, and real wages are growing again as inflation declines.

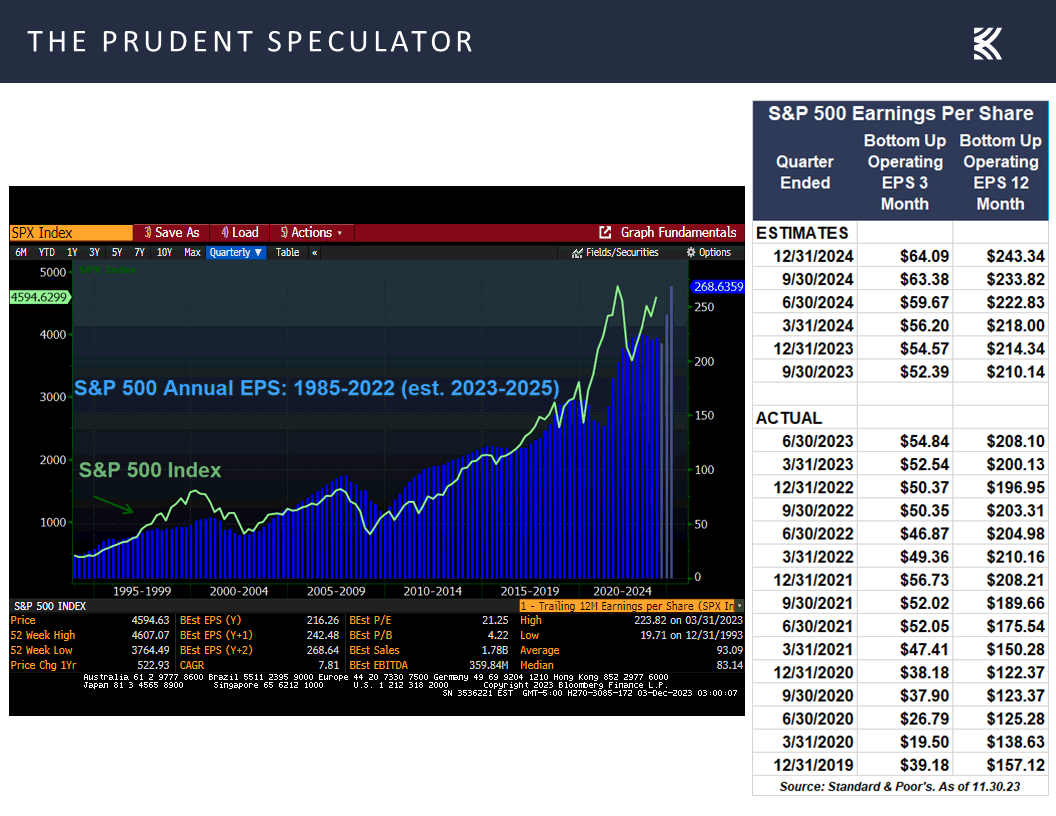

Earnings – Handsome Profit Growth Expected in ’24

Time will tell whether the Fed will be able to pull off a so-called soft landing,

but we continue to see a generally favorable economic backdrop supporting healthy and growing corporate profits,

which would only add to the appeal of the valuations for our broadly diversified portfolios of what we believe to be undervalued stocks.

Staying the Course – Inexpensive Stocks, Patience and the Calendar on our Side

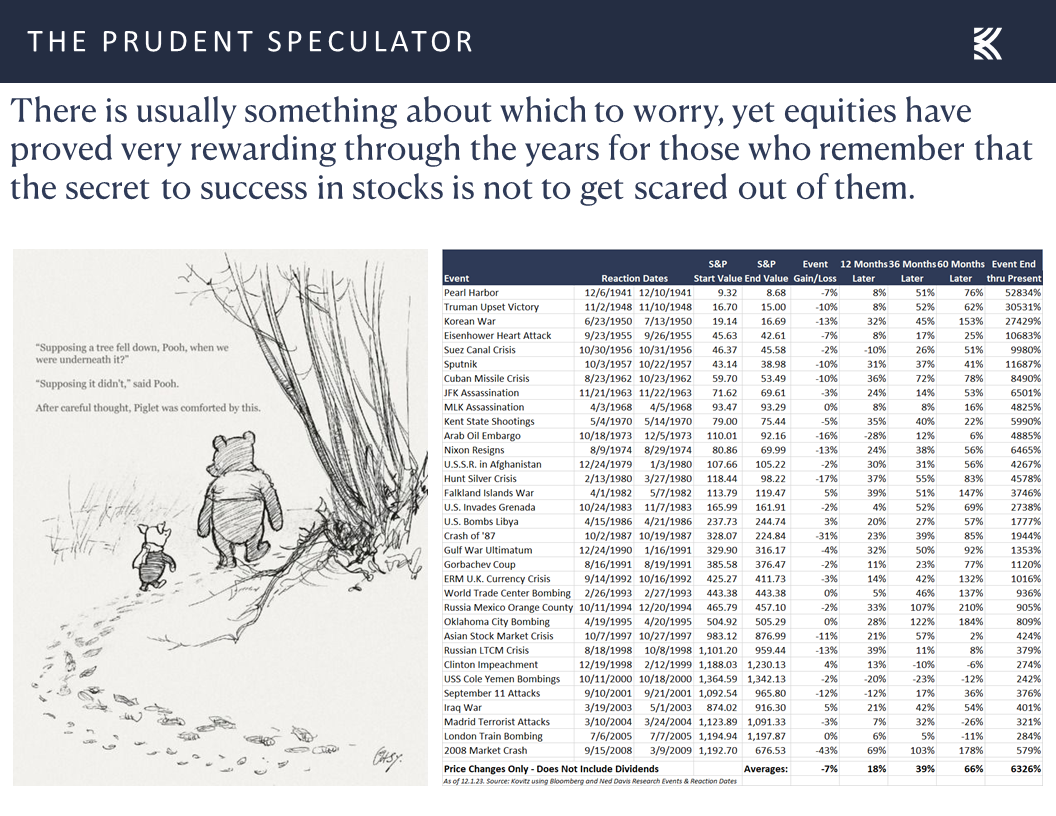

To be sure, it isn’t easy these days to read the papers or look at television and online coverage of the events in Israel/Gaza/Ukraine, so we realize that geopolitical developments are always a wildcard, but equities heretofore have always managed to overcome scary headlines to go on to post handsome gains for those who remember that the secret to success in stocks is to not get scared out of them.

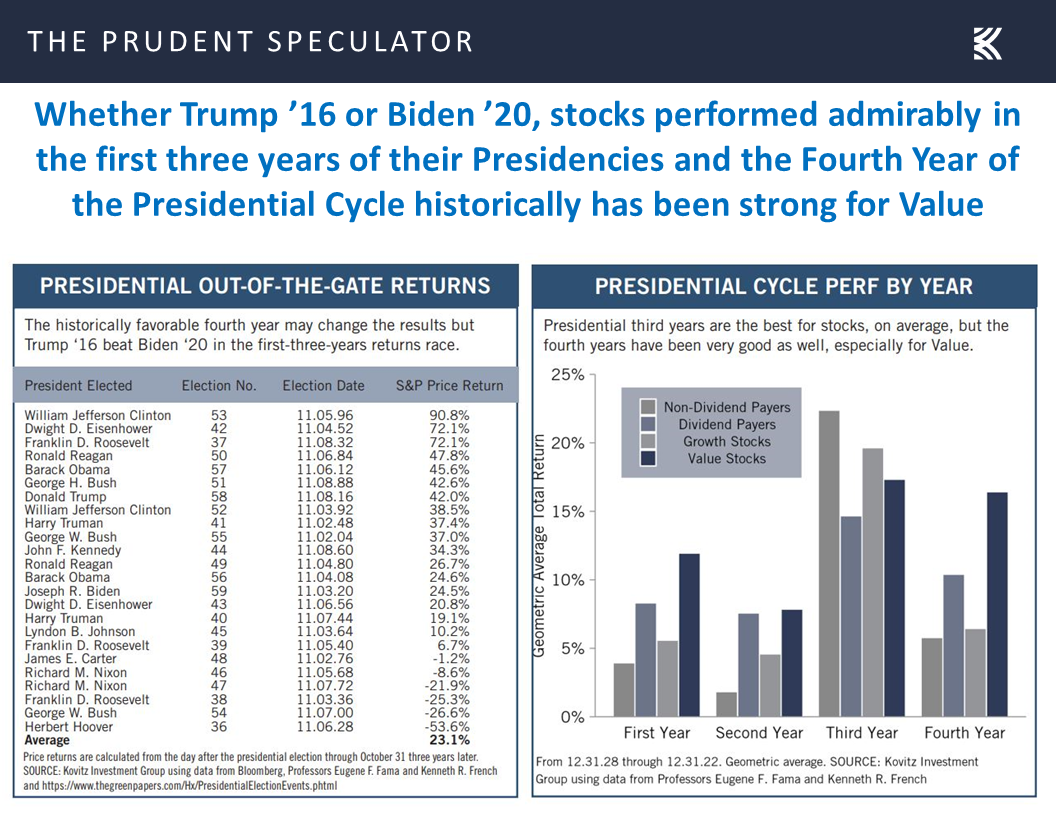

So, while we are always braced for downside volatility, we remain optimistic about the long-term prospects for equities, and we are buoyed by the calendar, not just for the seasonally favorable November to April timespan,

but also for the upcoming historically more-positive Fourth Year of the Presidential Cycle.

Stock News – Updates on six stocks across three different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Case for Value, Inflation, Earnings, Econ Data and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss a case for value, inflation, earnings, econ data and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week in Review – Soldiers Outflank the Generals

Case for Value – Historical Outperformance & Reasonable Metrics

Fed Speak – Proceeding Carefully as Risks are Becoming More Balanced

Inflation – Core PCE Falls; Interest Rates Continue to Decline

Econ Data – Housing & ISM Numbers Weak; Jobs and Q3 GDP Strong

Earnings – Handsome Profit Growth Expected in ’24

Staying the Course – Inexpensive Stocks, Patience and the Calendar on our Side

Stock News – Updates on six stocks across six different sectors

Week in Review – Soldiers Outflank the Generals

It was our kind of week as the Most-Wonderful-Time-of-the-Year rally broadened out considerably over the past five trading sessions with the average stock gaining much more than most of the large-cap-dominated indexes and the Russell 3000 Value index outperforming its Growth counterpart by a wide margin.

While we think Value stocks should be of great interest today, given that historically they have done the best,

and they are attractively priced on an absolute basis,

Case for Value – Historical Outperformance & Reasonable Metrics

and especially on a relative-to-Growth basis, when today’s metrics are compared to the historical norms,

the catalyst for the renewed interest evidently was talk from Federal Reserve officials.

Fed Speak – Proceeding Carefully as Risks are Becoming More Balanced

While we do not think we have heard much different in the Fed Speak from U.S. central bankers since the target for the Fed Funds rate was left unchanged at 5.25% to 5.50% and the FOMC Statement was released on November 1,

market participants have gained much greater conviction that Jerome Powell & Co. are finished with additional tightening of monetary policy this cycle as The New York Times proclaimed last week, “Fed Officials Hint That Rate Increases Are Over, and Investors Celebrate!”

We suppose we could construe the Fed Chair’s continued usage on Friday of language like, “The FOMC is moving forward carefully,” as confirmation that the Fed is done, especially as Mr. Powell added, “The risks of under- or over-tightening are becoming more balanced,”

Inflation – Core PCE Falls; Interest Rates Continue to Decline

while the latest read on inflation showed a continued decline in the Fed’s preferred measure of inflation, the Personal Consumption Expenditure Core Index, to 3.5% in October, down from 3.7% the month prior.

Certainly, the futures market decided a while ago that the Fed is done with rate hikes and the betting last week added two more cuts in the Fed Funds rate,

to a level below 4% by the end of next year,

and long-term interest rates continued their plunge over the last month, with the benchmark 10-Year U.S. Treasury yield dropping from 4.93% on Halloween to a current level of 4.20%.

No doubt, conventional wisdom would suggest that lower bond yields are better for equities and vice versa, but history shows that stocks perform fine whether interest rates are rising or falling, with Value preferring a yield above the long-term norm of 3.89%.

Econ Data – Housing & ISM Numbers Weak; Jobs and Q3 GDP Strong

Interestingly, the rally in stocks took place even as the latest housing numbers (from October) continued to decline, be it for new home sales,

or pending sales of existing homes,

while the November ISM Manufacturing index came in below expectations at a reading of 46.7, which supposedly corresponds to a change of minus 0.7% in real (inflation-adjusted) gross domestic product (GDP) on an annualized basis.

On the other hand, both personal incomes and spending held up well in October,

while the Atlanta Fed projects that Q4 U.S. real GDP growth will increase 1.2%,

the odds of recession in the next 12 months, per tabulations from Bloomberg, edged down to 50%,

and Q3 real GDP growth was revised upward to a very impressive 5.2% from an already robust 4.9%.

Also on Friday, Chair Powell talked about the other half of the Federal Reserve’s dual mandate, namely maximizing employment:

I am glad to say that, by many measures, conditions in the labor market are very strong. A couple of years ago, as the pandemic receded and the economy reopened, the number of job openings grew to greatly exceed the supply of people available to work, leaving a widespread shortage of workers. Today, labor market conditions remain very strong, and the economy is returning to a better balance between the demand for and supply of workers.

The pace at which the economy is creating new jobs remains strong, and has been slowing toward a more sustainable level. That gradual slowing has come in part due to the efforts of the Fed to slow the growth of the economy to help reduce inflation. After declining sharply during the pandemic, the supply of workers has bounced back, as people have come back into the labor force and as immigration has returned to pre-pandemic levels. Partly because of that labor force growth, the unemployment rate has edged up over the second half of the year, though it remains historically low at 3.9%. The increase in participation has been particularly strong among women in the prime working ages of 25 to 54, which surged to an all-time high earlier this year, and which remains well above pre-pandemic levels. Wage growth remains high but has been gradually moving toward levels that would be more consistent with 2% price inflation over time, and real wages are growing again as inflation declines.

Earnings – Handsome Profit Growth Expected in ’24

Time will tell whether the Fed will be able to pull off a so-called soft landing,

but we continue to see a generally favorable economic backdrop supporting healthy and growing corporate profits,

which would only add to the appeal of the valuations for our broadly diversified portfolios of what we believe to be undervalued stocks.

Staying the Course – Inexpensive Stocks, Patience and the Calendar on our Side

To be sure, it isn’t easy these days to read the papers or look at television and online coverage of the events in Israel/Gaza/Ukraine, so we realize that geopolitical developments are always a wildcard, but equities heretofore have always managed to overcome scary headlines to go on to post handsome gains for those who remember that the secret to success in stocks is to not get scared out of them.

So, while we are always braced for downside volatility, we remain optimistic about the long-term prospects for equities, and we are buoyed by the calendar, not just for the seasonally favorable November to April timespan,

but also for the upcoming historically more-positive Fourth Year of the Presidential Cycle.

Stock News – Updates on six stocks across three different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.