The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Case for Value, the Economy, Interest Rates, the Sentiment and more news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – A Sell and Seven Buys

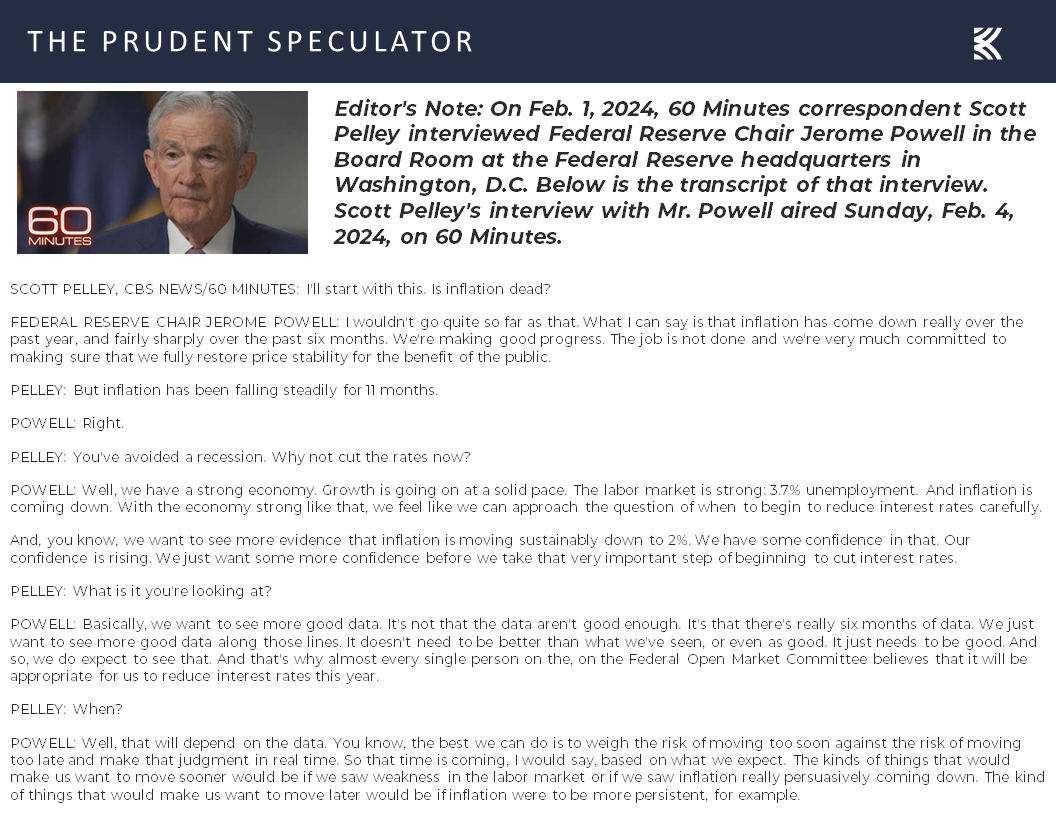

Jerome H. Powell – Fed Chair Echoes Press Conference Remarks on 60 Minutes

Economy – Inflation Coming Down, Strong Labor Market, GDP Solid

Interest Rates – Target Rate for Fed Funds & 10-Year Treasury Yield Rise; Stocks Don’t Mind

Case for Value – Inexpensive Valuations, Historical Returns, Record Returns Gap vs. Growth

Total Return – Dividends Matter; IBM a Good Performer the Last 18 Years

Sentiment – AAII Optimistic

Stock News – Updates on seventeen stocks across ten different sectors

Jerome H. Powell – Fed Chair Echoes Press Conference Remarks on 60 Minutes

It is often puzzling the events that account for short-term movements in the equity markets. For example, last week began with a sizable selloff in stocks seemingly in reaction to Jerome H. Powell’s turn on 60 Minutes the night before. The interview aired on Feb. 4, but it was taped Feb. 1, just one day after the Federal Reserve Chair’s Press Conference following the FOMC’s decision to leave the Fed Funds rate unchanged at a range of 5.25% to 5.5% and Mr. Powell’s comments that an interest rate cut was not likely at the next Fed get together in March.

Economy – Inflation Coming Down, Strong Labor Market, GDP Solid

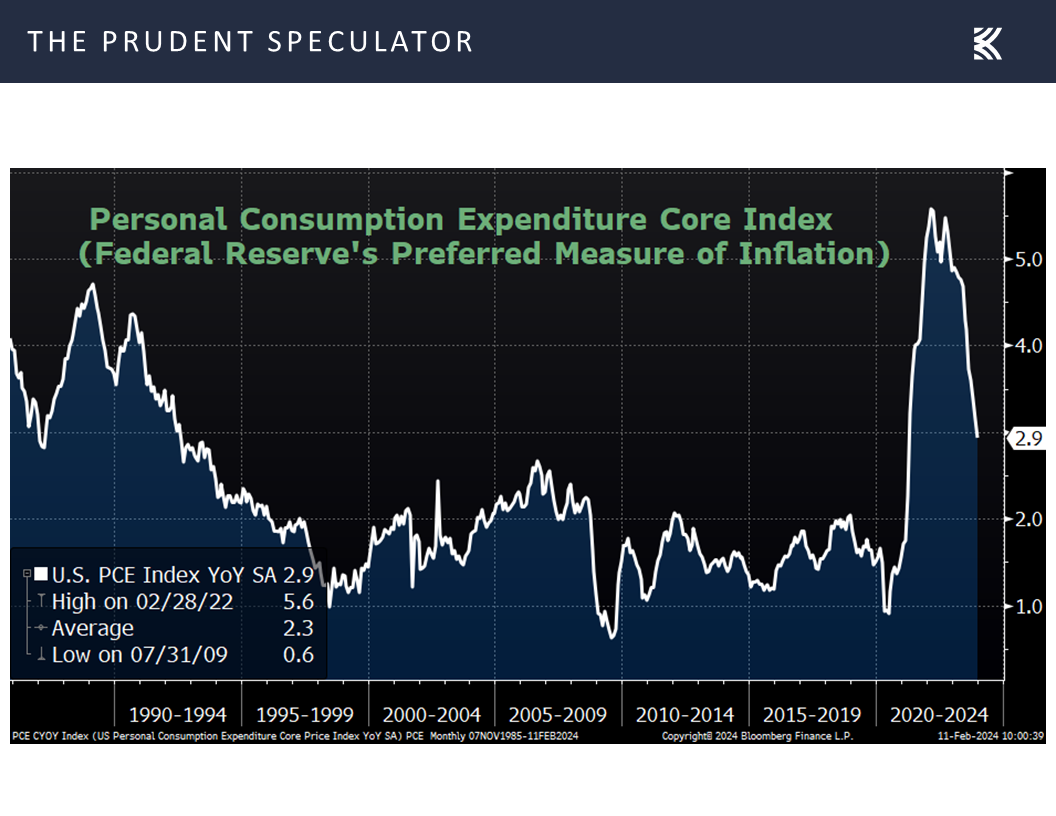

There really wasn’t anything new in the 60 Minutes interview as Chair Powell basically said the exact same thing as he said the day before at the Press Conference: Inflation has come down, but the job is not done,

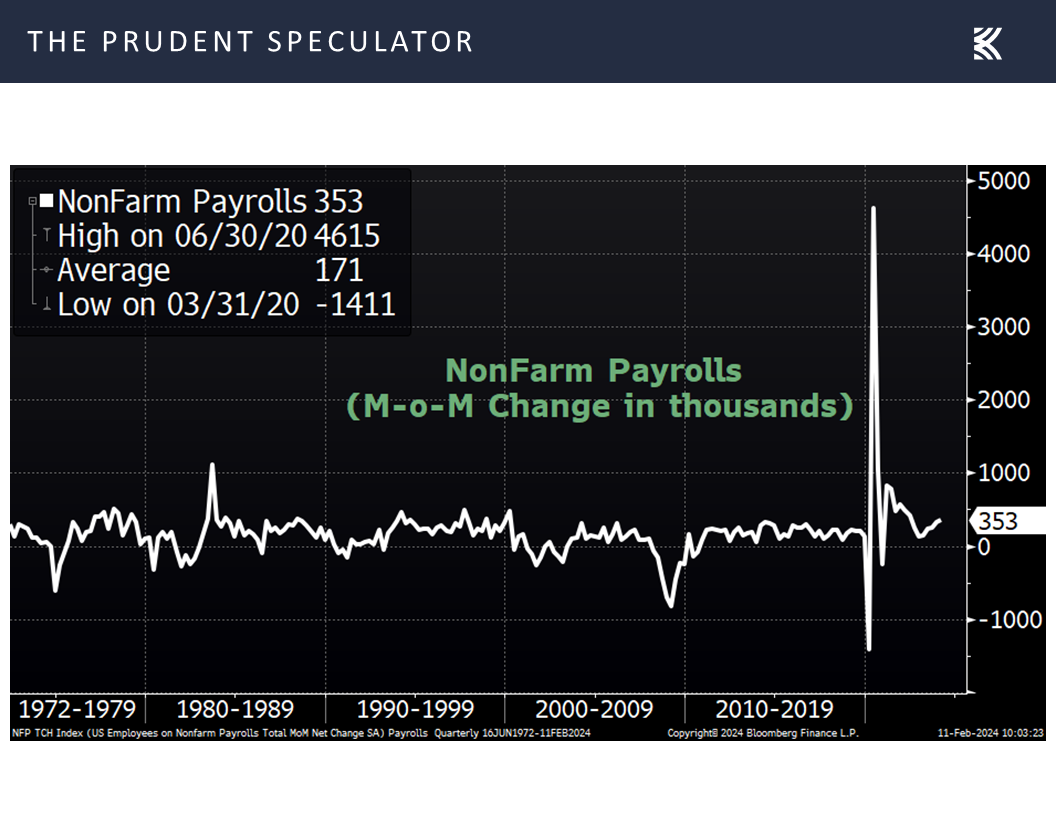

while the labor market is strong,

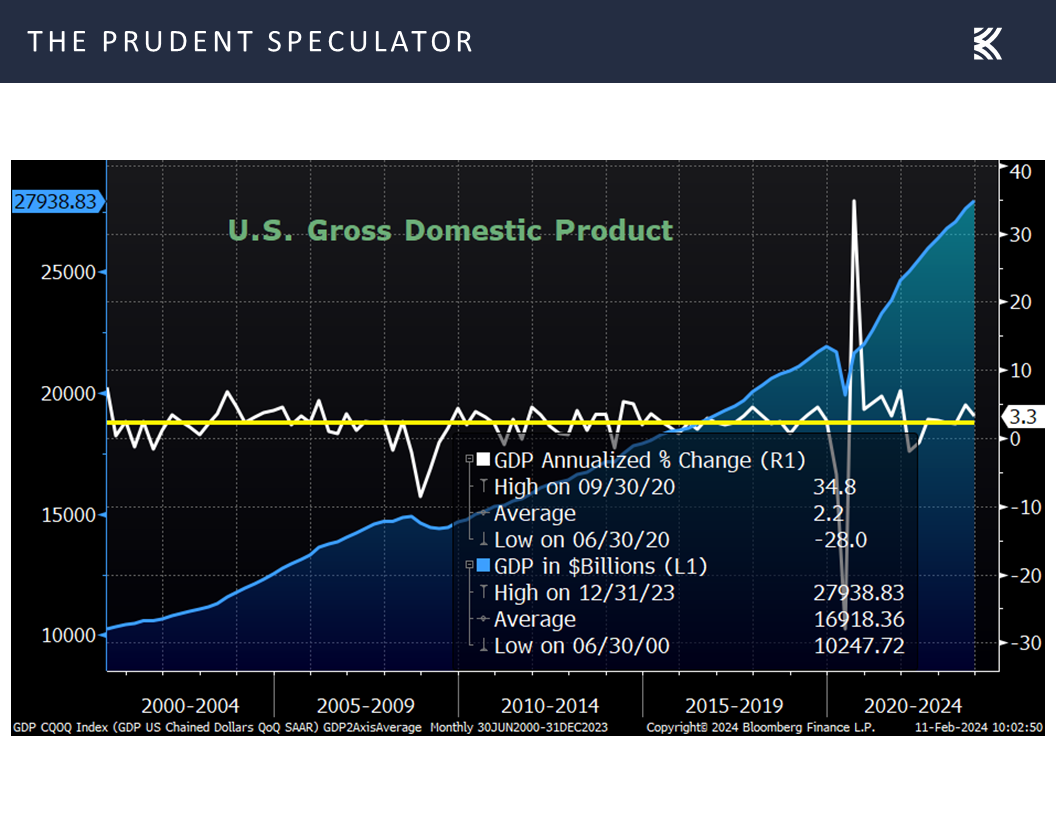

and real GDP is solid,

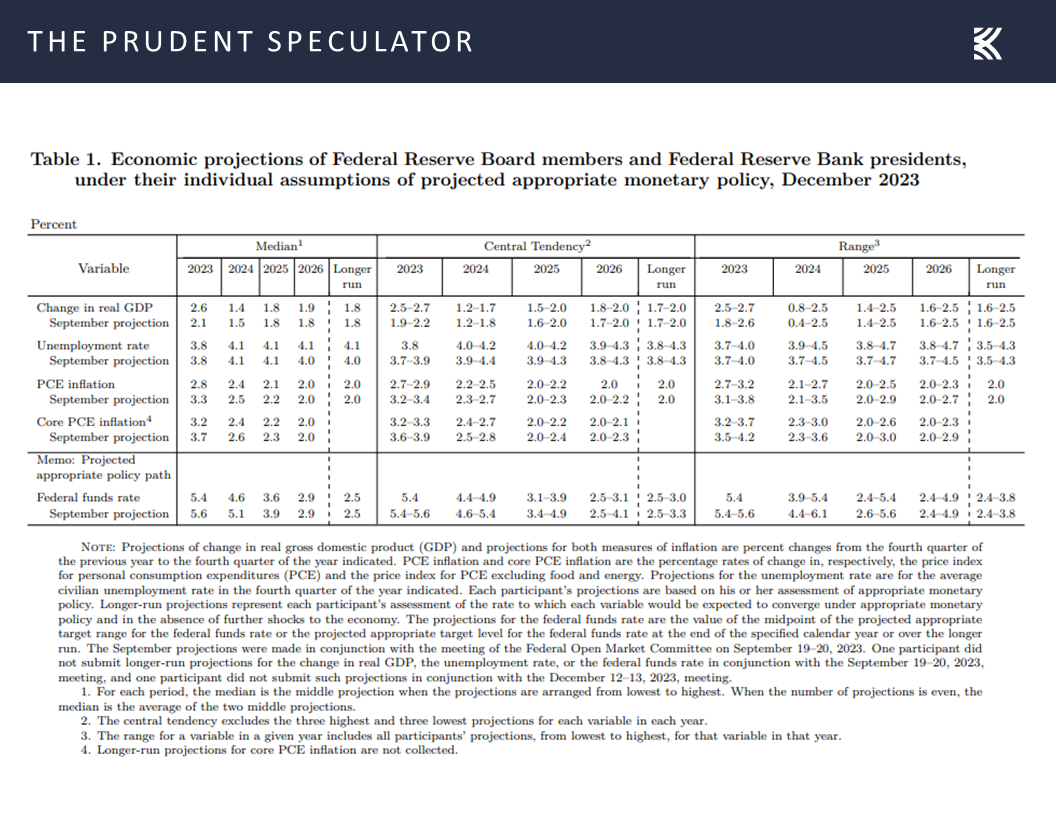

suggesting that the numbers are trending in line with the Fed’s most recently published economic projections.

Interest Rates – Target Rate for Fed Funds & 10-Year Treasury Yield Rise; Stocks Don’t Mind

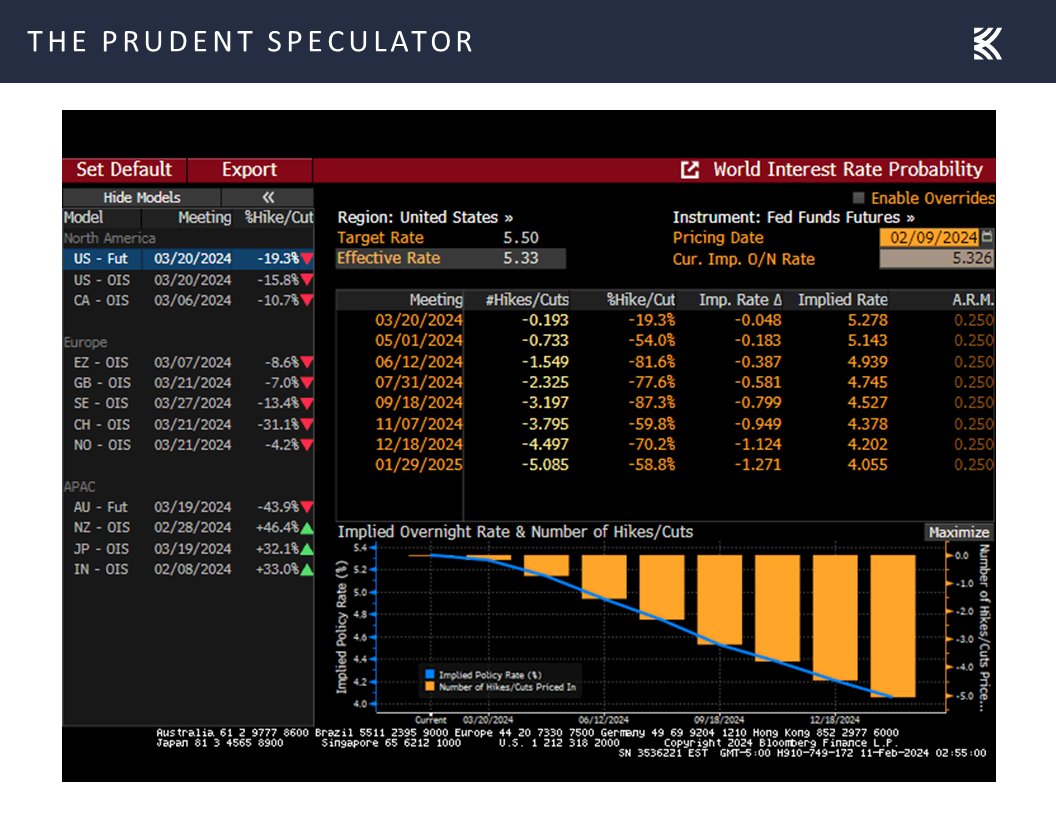

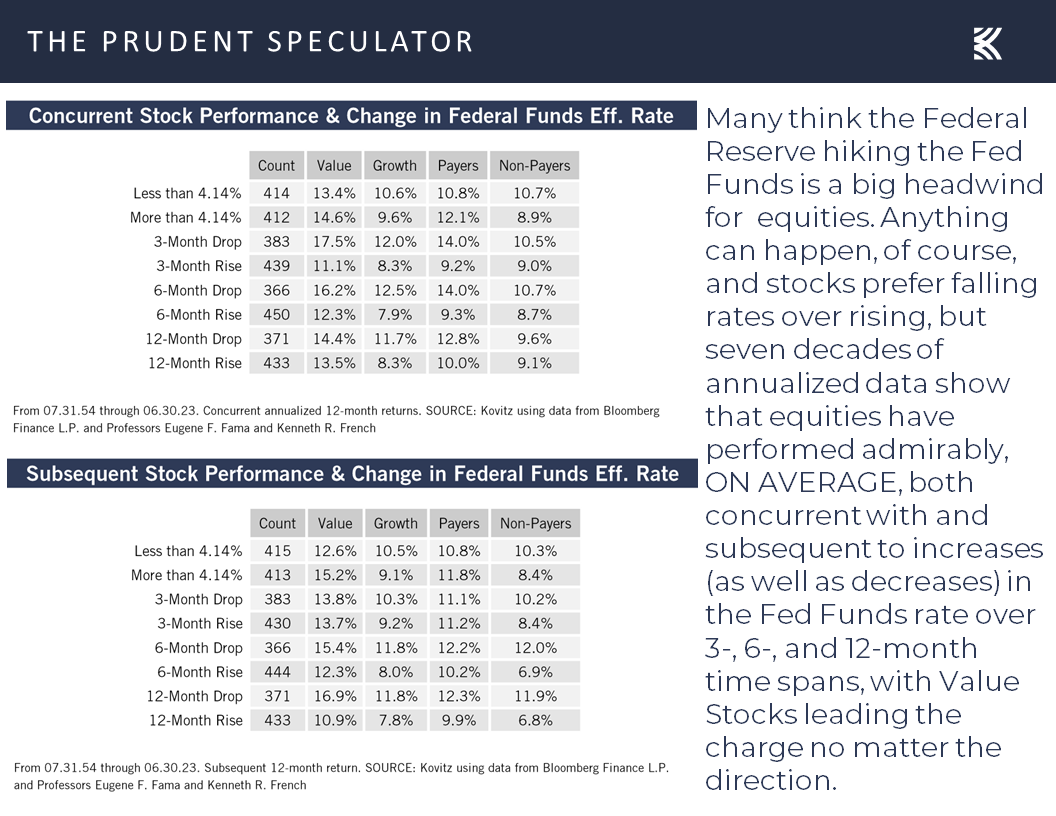

Interestingly, even as the Fed Funds futures betting odds by the end of the week had seen a boost in the year-end target rate to 4.20%, up from 4.07% at the end of the prior week,

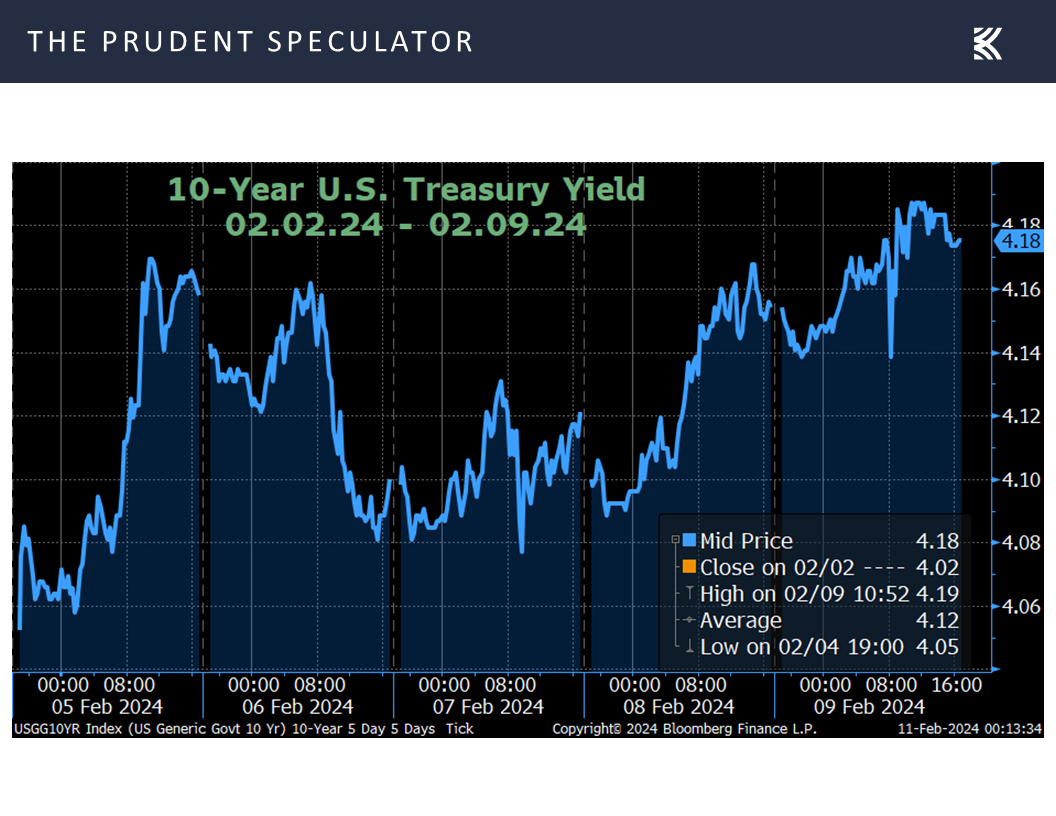

while the yield on the benchmark 10-Year U.S. Treasury jumped to 4.18% from 4.02% the Friday before,

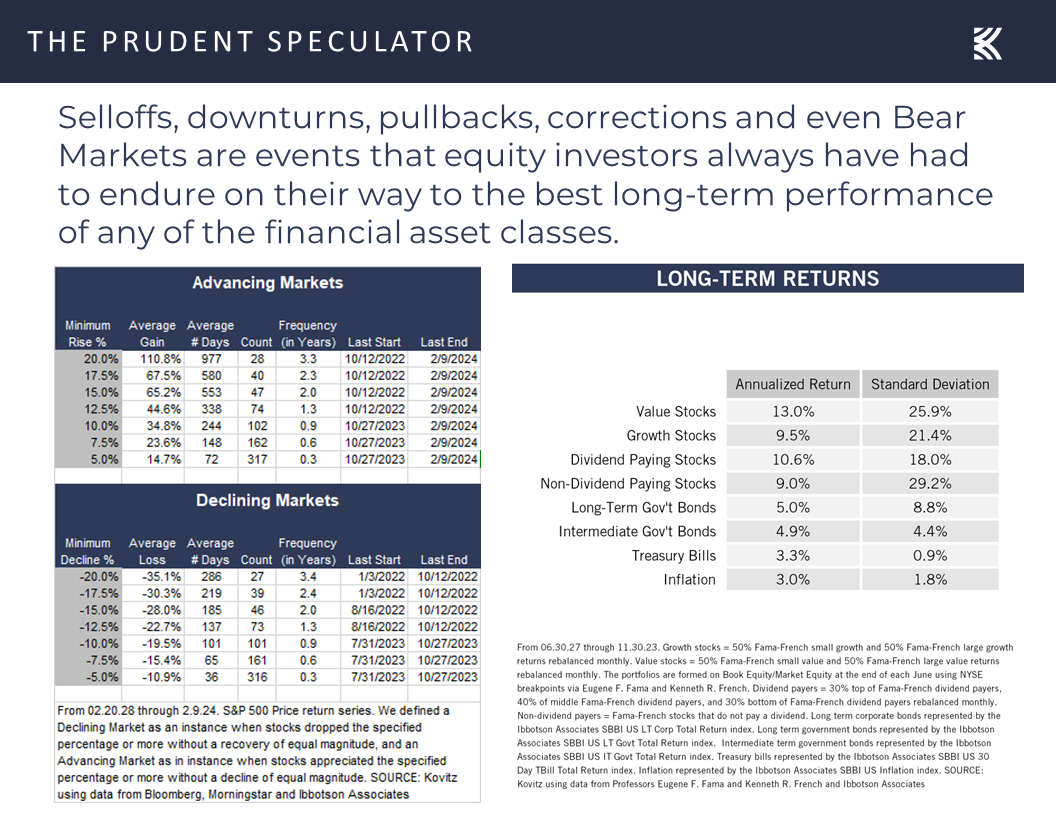

traders became more enthused about equities and bid stocks up over the balance of the week, so much so that the major market averages closed out the five days with decent gains that propelled the mega-cap dominated S&P 500 to a record high above 5000. Of course, the long-term trend in stock prices is up, despite bouts of volatility along the way,

with equities moving higher, on average, no matter the near-term direction of the Fed Funds rate,

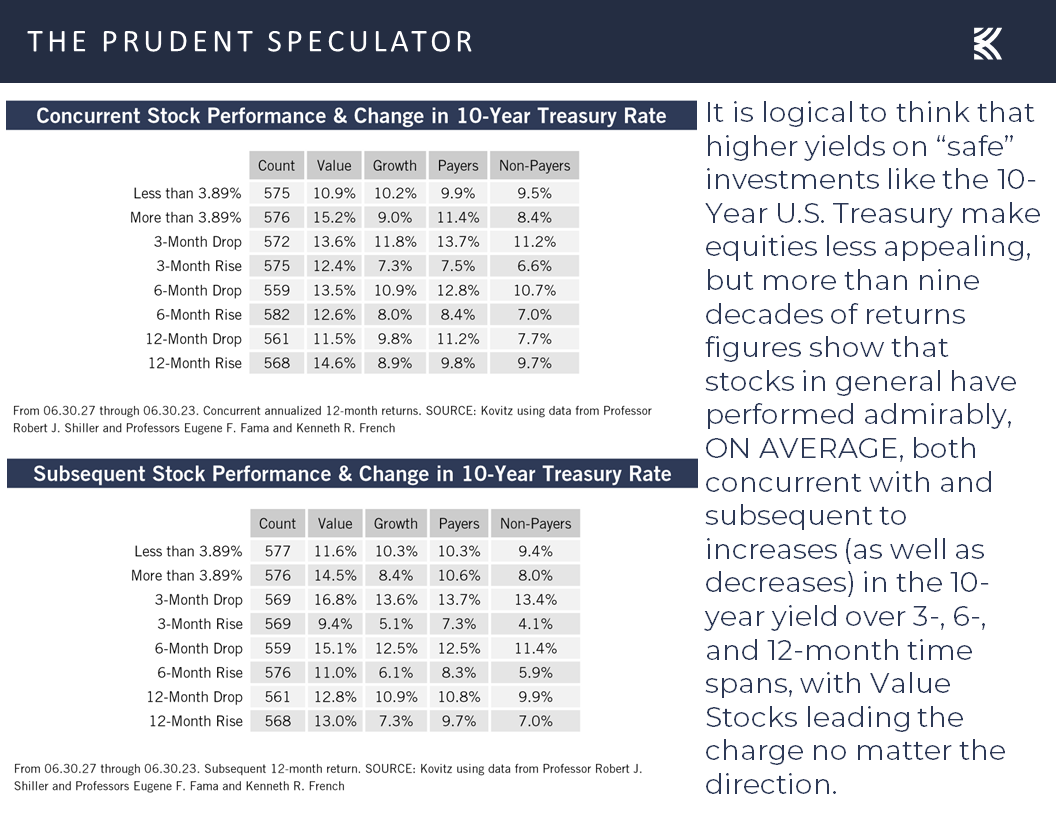

or the yield on the 10-Year U.S. Treasury.

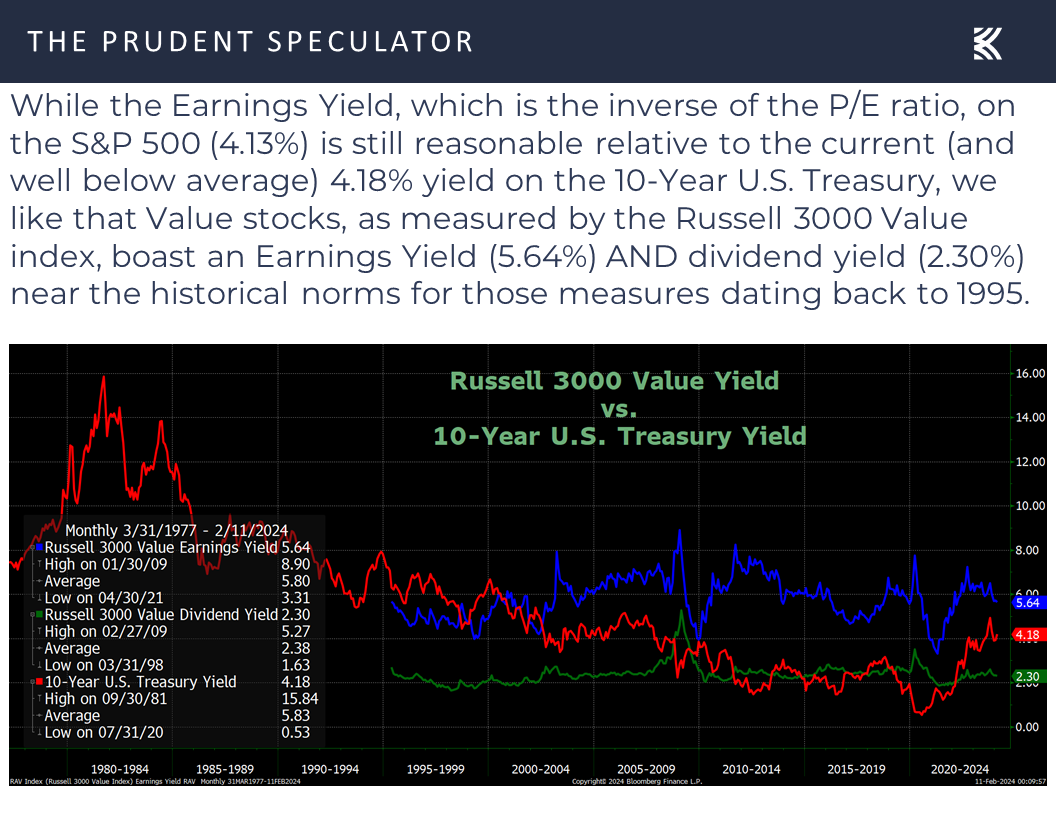

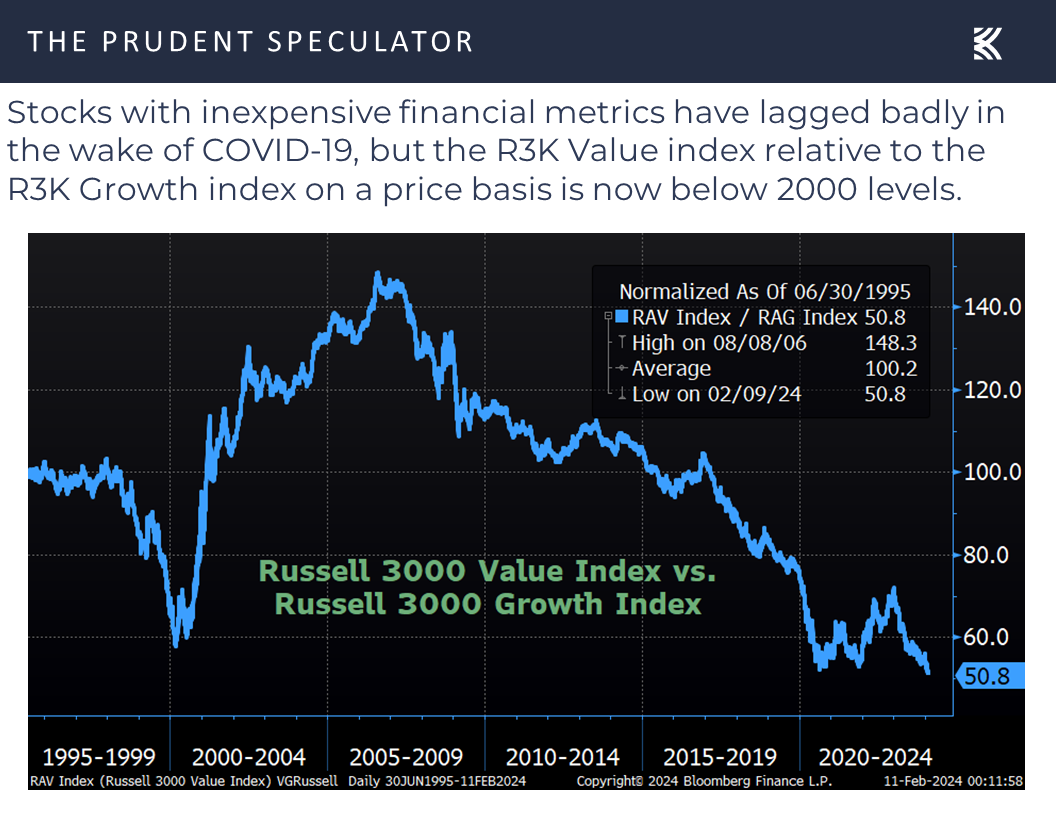

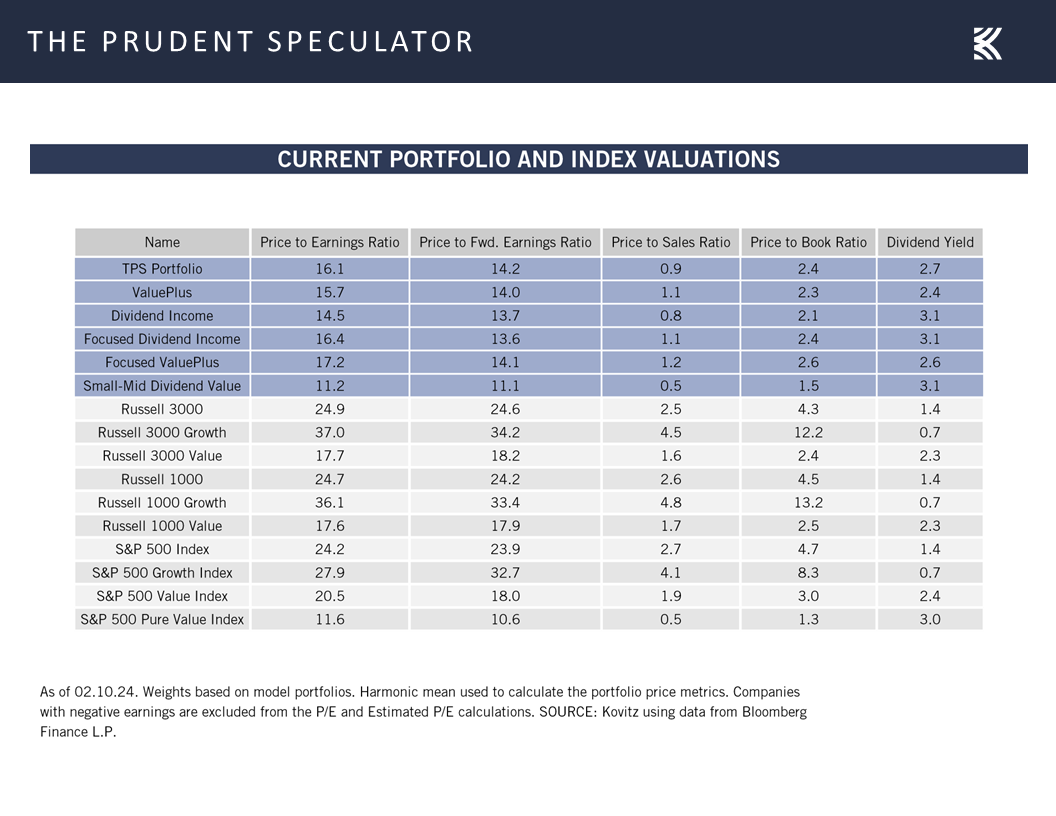

Case for Value – Inexpensive Valuations, Historical Returns, Record Returns Gap vs. Growth

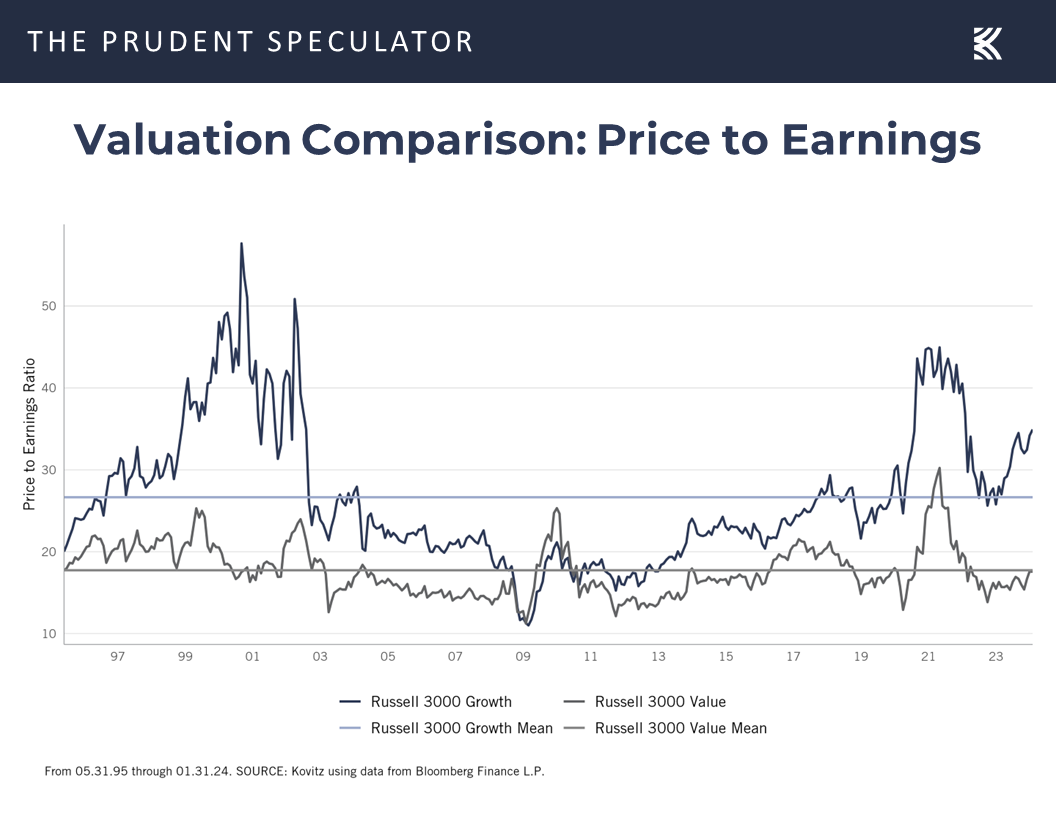

To be sure, the rising tide has not lifted all boats this year, given that the average stock in the Russell 3000 index is down 1.6%, while the Russell 2000 SmallCap index is off 0.8%. Some argue that this dispersion of returns is not a great sign for the go-forward, but we think many of the stocks that have thus far been left behind are poised to catch up, especially as we note that Value Stocks like those we have long championed are much more attractively priced relatively to Growth, on an earnings basis,

and they are not expensive on an earnings yield (the inverse of the P/E ratio) basis relative to interest rates,

with the E part of the P/E and E/P ratios likely to show handsome growth this year.

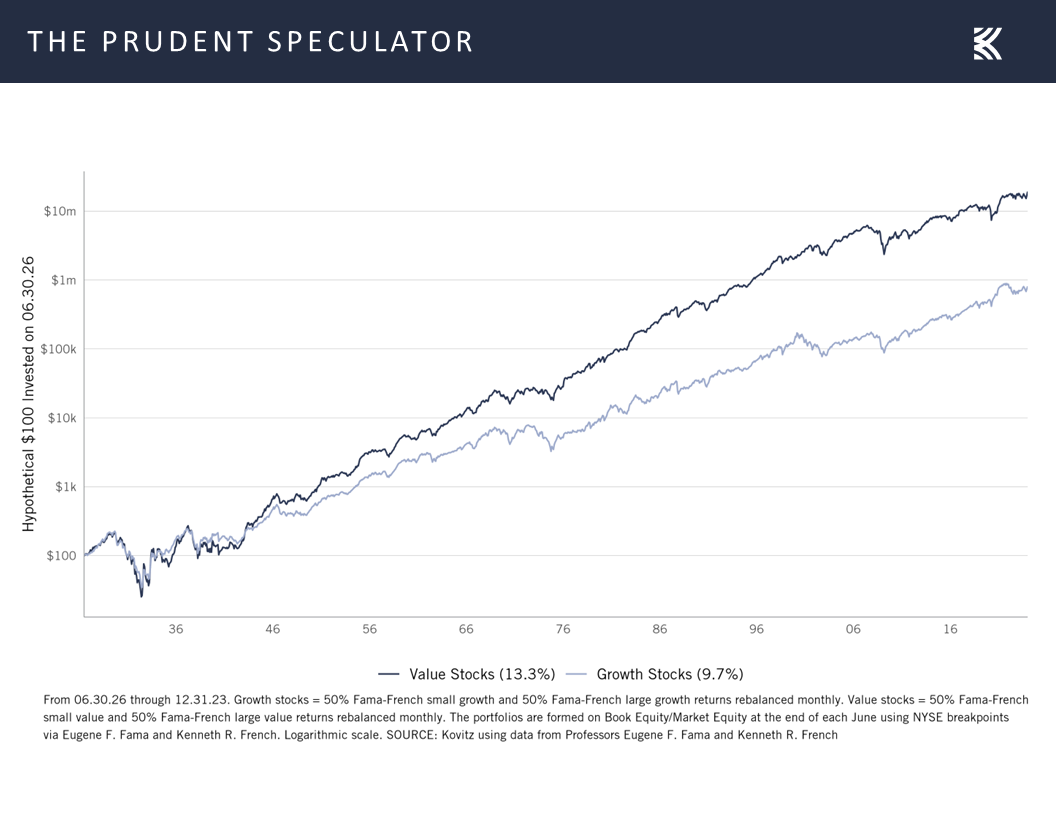

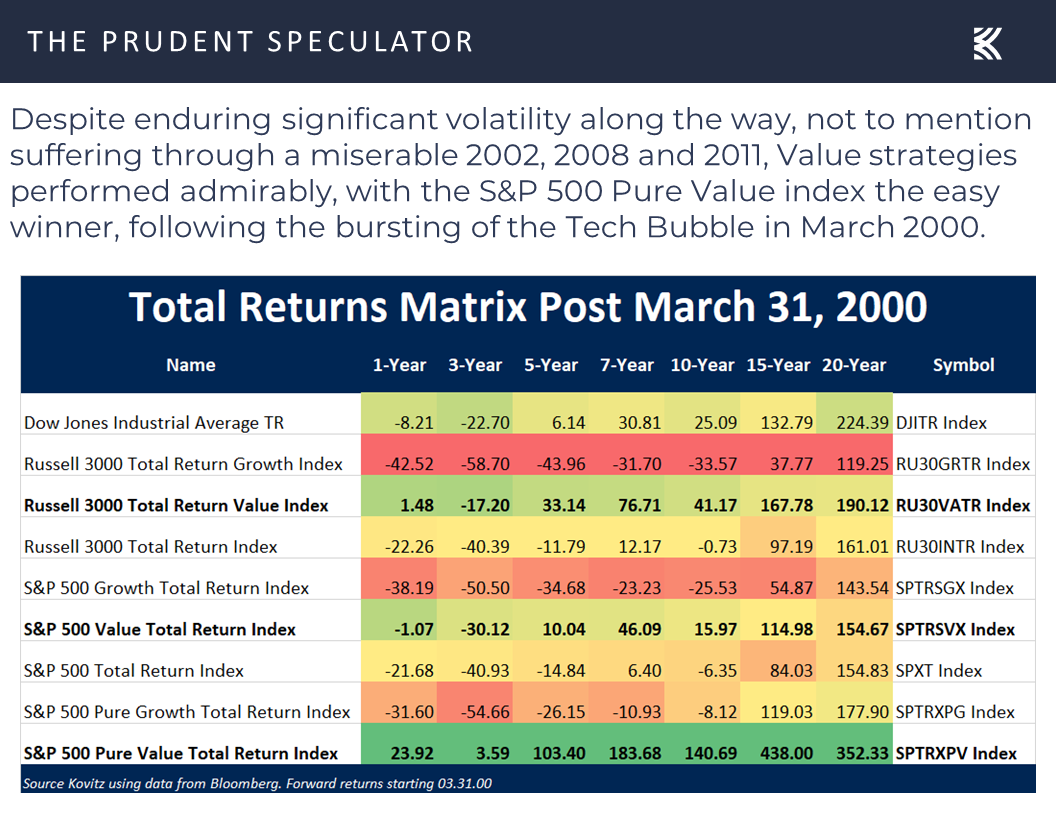

And, as students of market history are well aware, Value has delivered the best long-term returns dating back nearly 100 years,

with comparable long-term returns since the launch of The Prudent Speculator in 1977.

We also note that Value is as attractive relative to Growth as at any time in the near-30-year history of the Russell 3000 Value and Growth indexes. Incredibly, the gap in performance between the two is today wider than at the peak of the Tech Bubble,

while we can’t forget that the years that followed the turn of the Millennium were very kind to the Value indexes, especially relative to Growth and the broad-based market averages.

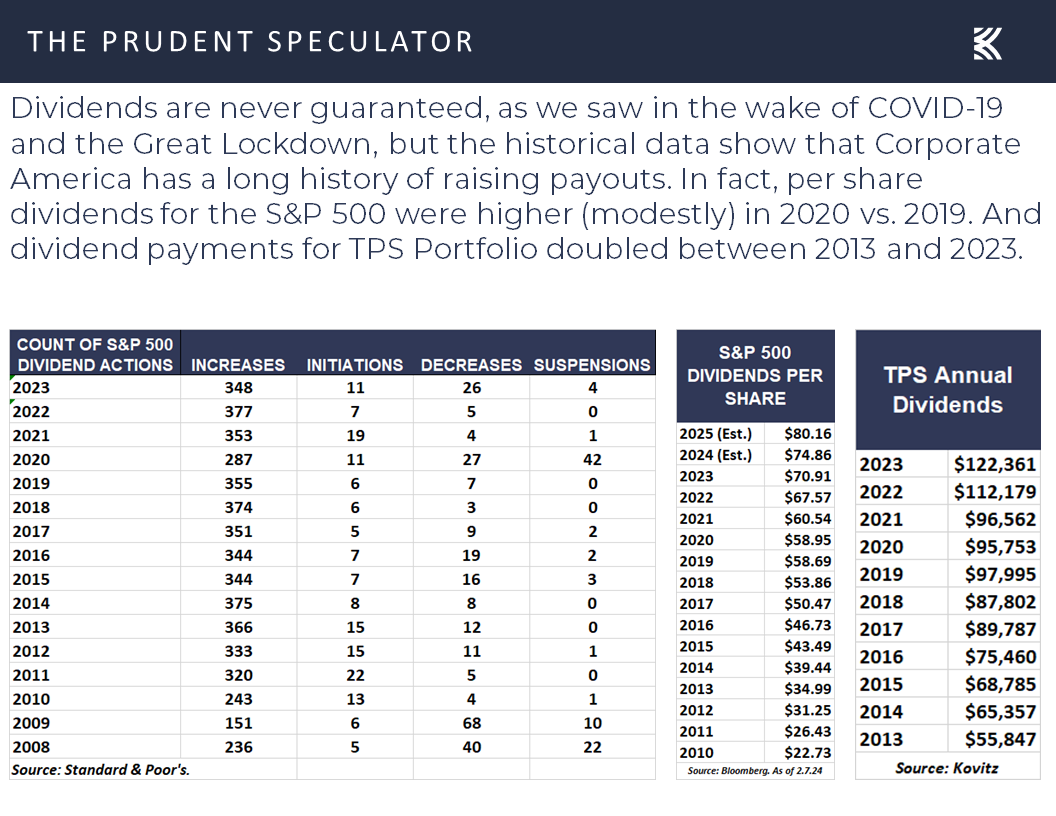

Total Return – Dividends Matter; IBM a Good Performer the Last 18 Years

We think it important to understand that the figures in the table above are total return, while the preceding Russell chart is simply price performance. No doubt, dividends and the impact of their reinvestment are critical to determining how well a long-term-oriented investor might have done.

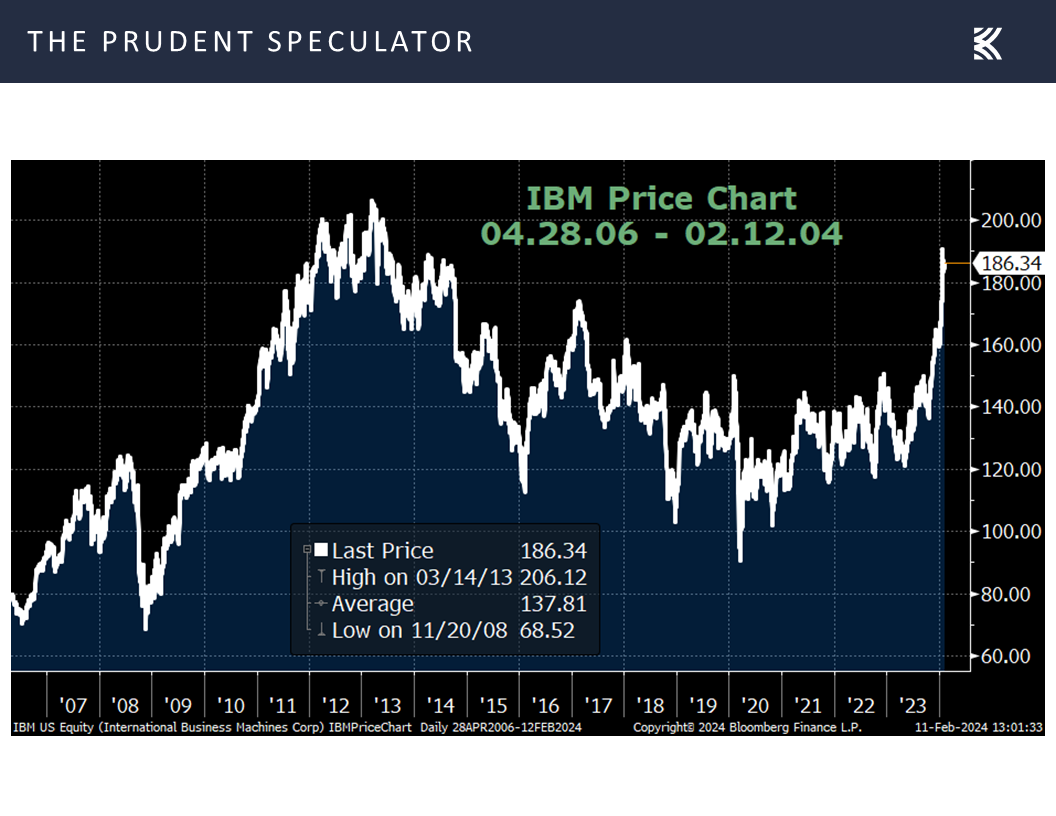

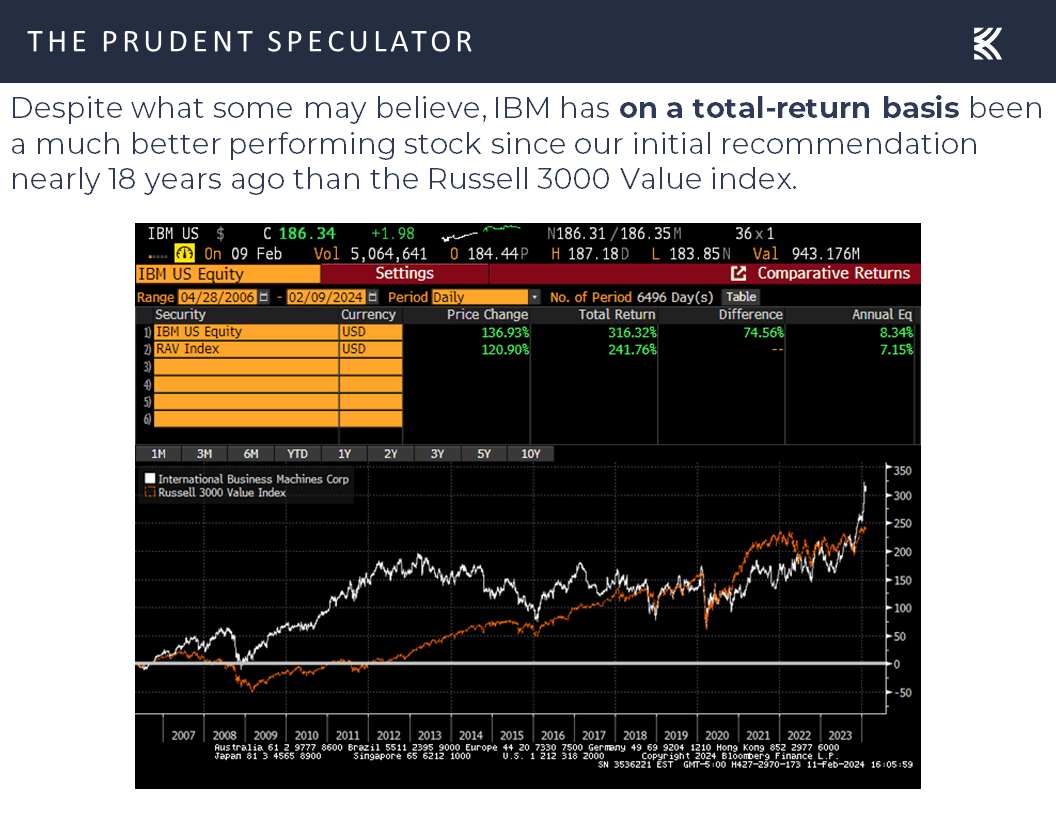

For example, we know that some readers have a dislike for our long-time holding in International Business Machines (IBM – $186.34). Our original recommendation of IBM came back in 2006 and a look at a price chart doesn’t show a ton of appreciation over the years,

but IBM has paid out substantial dividends along the way and we think it eye-opening to consider the impressive total-return comparison relative to the Russell 3000 Value index over the same time span.

Needless to say, many market watchers ignore or dismiss dividends, yet they are very much tangible and they often increase over time.

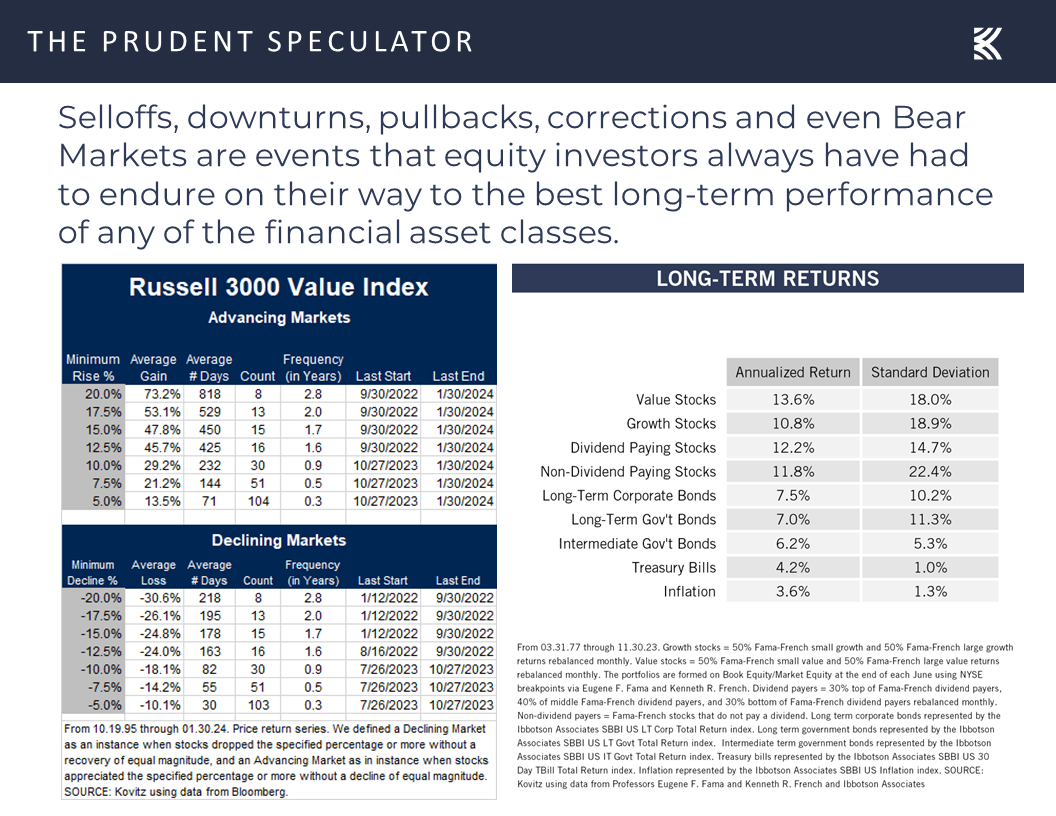

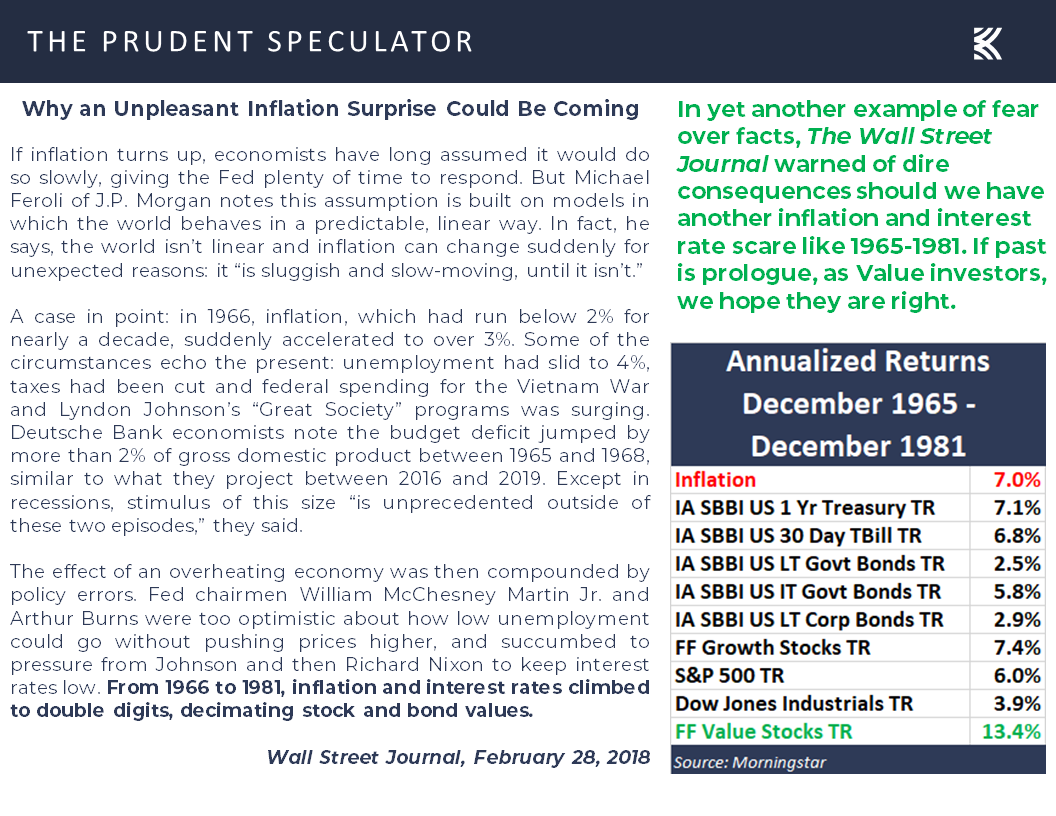

with even The Wall Street Journal guilty of faulty journalism back in 2018 in relation to a suggestion that inflation decimated stock values from 1966-1981 as the Dow went from 964 to 875 15 years later. True, inflation averaged a very high 7.0% during the span, but Value Stocks gained 13.4% PER ANNUM on a total return basis.

The Dow is a price index and not a total-return index, so if one uses it (and the S&P 500) to measure performance, it is the equivalent of ignoring the income investor receive from bonds. Imagine using a hypothetical Long-Term Government Bond Price index to measure the merits of investing in fixed income. Such an index would start at 100 in 1925 and be at 161 in 2021 based on the capital appreciation series in the 2022 Stocks, Bond, Bills and Inflation Yearbook, for an annualized price return of around 0.5% over more than nine decades! Obviously, bonds have done far better than that on a total return basis.

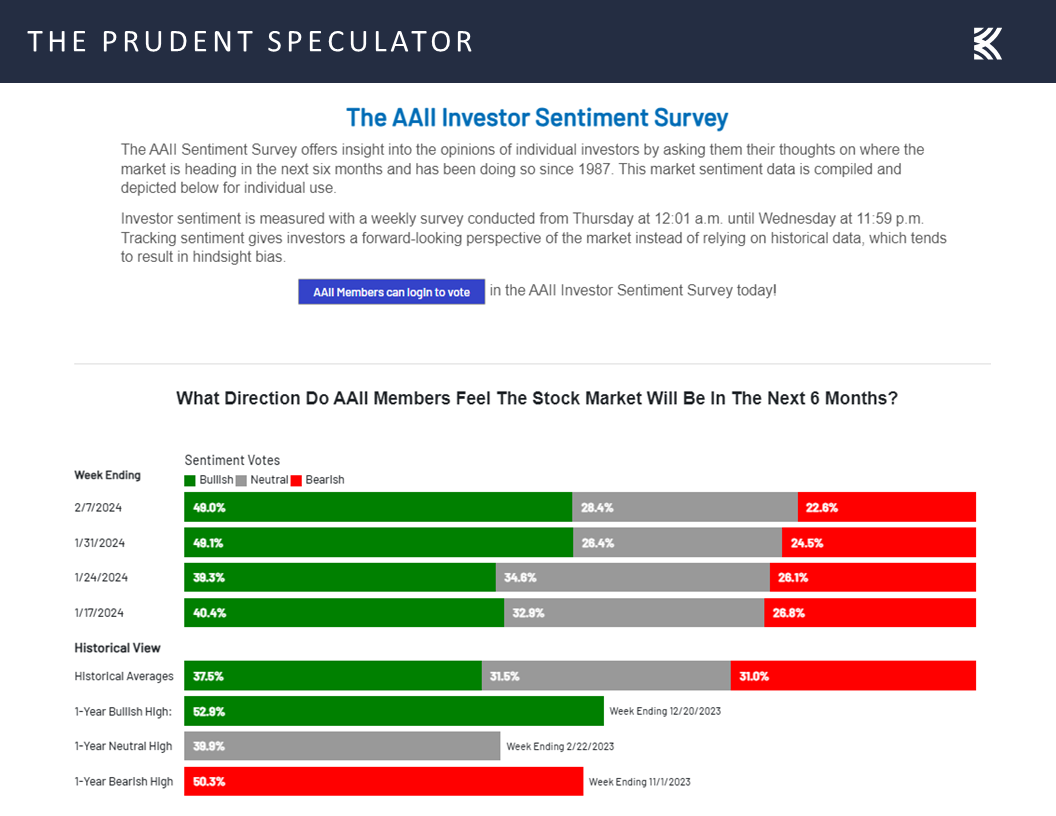

Sentiment – AAII Optimistic

While we wouldn’t be surprised to see a little pullback after the record highs on the major market averages, especially as optimism on Main Street is running high,

we remain enthused about the favorable long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks.

Stock News – Updates on seventeen stocks across ten different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Case for Value, Interest Rates, the Economy, AAII Sentiment and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Case for Value, the Economy, Interest Rates, the Sentiment and more news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – A Sell and Seven Buys

Jerome H. Powell – Fed Chair Echoes Press Conference Remarks on 60 Minutes

Economy – Inflation Coming Down, Strong Labor Market, GDP Solid

Interest Rates – Target Rate for Fed Funds & 10-Year Treasury Yield Rise; Stocks Don’t Mind

Case for Value – Inexpensive Valuations, Historical Returns, Record Returns Gap vs. Growth

Total Return – Dividends Matter; IBM a Good Performer the Last 18 Years

Sentiment – AAII Optimistic

Stock News – Updates on seventeen stocks across ten different sectors

Jerome H. Powell – Fed Chair Echoes Press Conference Remarks on 60 Minutes

It is often puzzling the events that account for short-term movements in the equity markets. For example, last week began with a sizable selloff in stocks seemingly in reaction to Jerome H. Powell’s turn on 60 Minutes the night before. The interview aired on Feb. 4, but it was taped Feb. 1, just one day after the Federal Reserve Chair’s Press Conference following the FOMC’s decision to leave the Fed Funds rate unchanged at a range of 5.25% to 5.5% and Mr. Powell’s comments that an interest rate cut was not likely at the next Fed get together in March.

Economy – Inflation Coming Down, Strong Labor Market, GDP Solid

There really wasn’t anything new in the 60 Minutes interview as Chair Powell basically said the exact same thing as he said the day before at the Press Conference: Inflation has come down, but the job is not done,

while the labor market is strong,

and real GDP is solid,

suggesting that the numbers are trending in line with the Fed’s most recently published economic projections.

Interest Rates – Target Rate for Fed Funds & 10-Year Treasury Yield Rise; Stocks Don’t Mind

Interestingly, even as the Fed Funds futures betting odds by the end of the week had seen a boost in the year-end target rate to 4.20%, up from 4.07% at the end of the prior week,

while the yield on the benchmark 10-Year U.S. Treasury jumped to 4.18% from 4.02% the Friday before,

traders became more enthused about equities and bid stocks up over the balance of the week, so much so that the major market averages closed out the five days with decent gains that propelled the mega-cap dominated S&P 500 to a record high above 5000. Of course, the long-term trend in stock prices is up, despite bouts of volatility along the way,

with equities moving higher, on average, no matter the near-term direction of the Fed Funds rate,

or the yield on the 10-Year U.S. Treasury.

Case for Value – Inexpensive Valuations, Historical Returns, Record Returns Gap vs. Growth

To be sure, the rising tide has not lifted all boats this year, given that the average stock in the Russell 3000 index is down 1.6%, while the Russell 2000 SmallCap index is off 0.8%. Some argue that this dispersion of returns is not a great sign for the go-forward, but we think many of the stocks that have thus far been left behind are poised to catch up, especially as we note that Value Stocks like those we have long championed are much more attractively priced relatively to Growth, on an earnings basis,

and they are not expensive on an earnings yield (the inverse of the P/E ratio) basis relative to interest rates,

with the E part of the P/E and E/P ratios likely to show handsome growth this year.

And, as students of market history are well aware, Value has delivered the best long-term returns dating back nearly 100 years,

with comparable long-term returns since the launch of The Prudent Speculator in 1977.

We also note that Value is as attractive relative to Growth as at any time in the near-30-year history of the Russell 3000 Value and Growth indexes. Incredibly, the gap in performance between the two is today wider than at the peak of the Tech Bubble,

while we can’t forget that the years that followed the turn of the Millennium were very kind to the Value indexes, especially relative to Growth and the broad-based market averages.

Total Return – Dividends Matter; IBM a Good Performer the Last 18 Years

We think it important to understand that the figures in the table above are total return, while the preceding Russell chart is simply price performance. No doubt, dividends and the impact of their reinvestment are critical to determining how well a long-term-oriented investor might have done.

For example, we know that some readers have a dislike for our long-time holding in International Business Machines (IBM – $186.34). Our original recommendation of IBM came back in 2006 and a look at a price chart doesn’t show a ton of appreciation over the years,

but IBM has paid out substantial dividends along the way and we think it eye-opening to consider the impressive total-return comparison relative to the Russell 3000 Value index over the same time span.

Needless to say, many market watchers ignore or dismiss dividends, yet they are very much tangible and they often increase over time.

with even The Wall Street Journal guilty of faulty journalism back in 2018 in relation to a suggestion that inflation decimated stock values from 1966-1981 as the Dow went from 964 to 875 15 years later. True, inflation averaged a very high 7.0% during the span, but Value Stocks gained 13.4% PER ANNUM on a total return basis.

The Dow is a price index and not a total-return index, so if one uses it (and the S&P 500) to measure performance, it is the equivalent of ignoring the income investor receive from bonds. Imagine using a hypothetical Long-Term Government Bond Price index to measure the merits of investing in fixed income. Such an index would start at 100 in 1925 and be at 161 in 2021 based on the capital appreciation series in the 2022 Stocks, Bond, Bills and Inflation Yearbook, for an annualized price return of around 0.5% over more than nine decades! Obviously, bonds have done far better than that on a total return basis.

Sentiment – AAII Optimistic

While we wouldn’t be surprised to see a little pullback after the record highs on the major market averages, especially as optimism on Main Street is running high,

we remain enthused about the favorable long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks.

Stock News – Updates on seventeen stocks across ten different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.