The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Debt Ceiling, Credit Rating, AI-Exposed Stocks, Corporate Profits and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

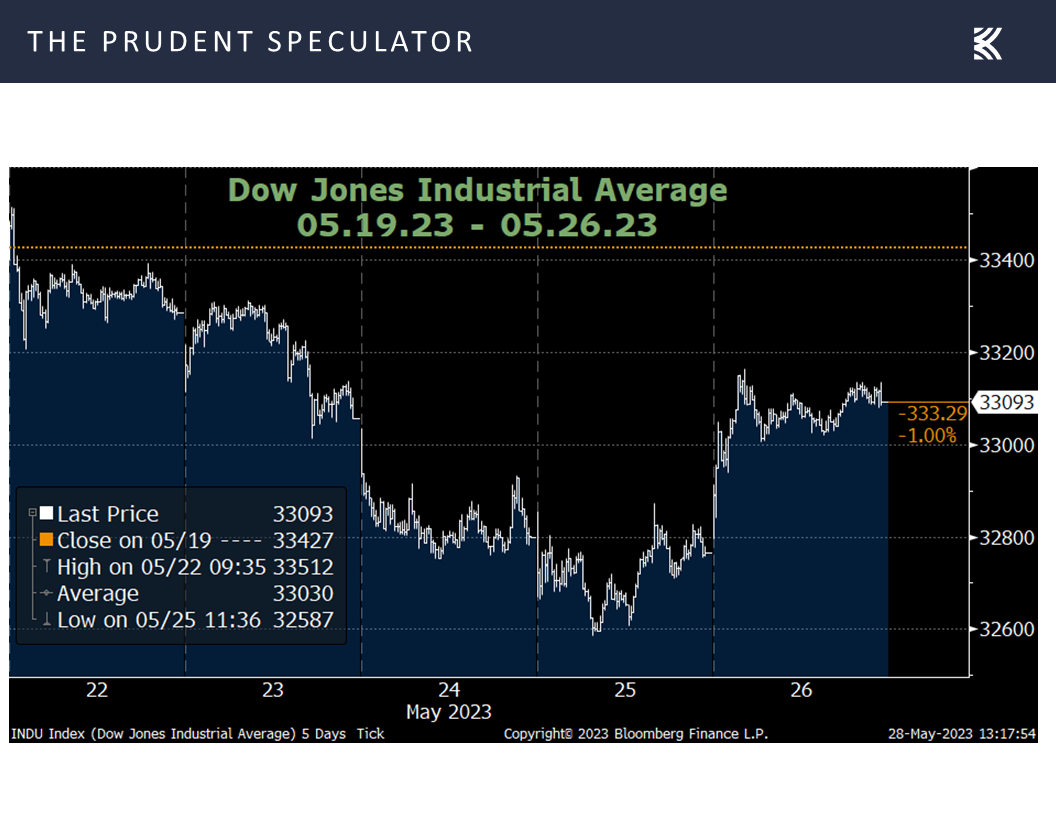

Week in Review – Volatile Five Days; Most Indexes End Lower

Debt Ceiling – Deal Talks Ebb and Flow

Credit Rating Downgrade Perspective – Fitch Brings Back Memories of August 2011…Which Two-Months Later Saw a Significant Market Bottom

Historical Perspective – Plenty of Scary Events, but the Long-Term Trend is Up

Corporate Profits – EPS Growth Still the Forecast

Econ News – More Positive Stats than Negative; Odds of Fed Rate Cuts Diminish

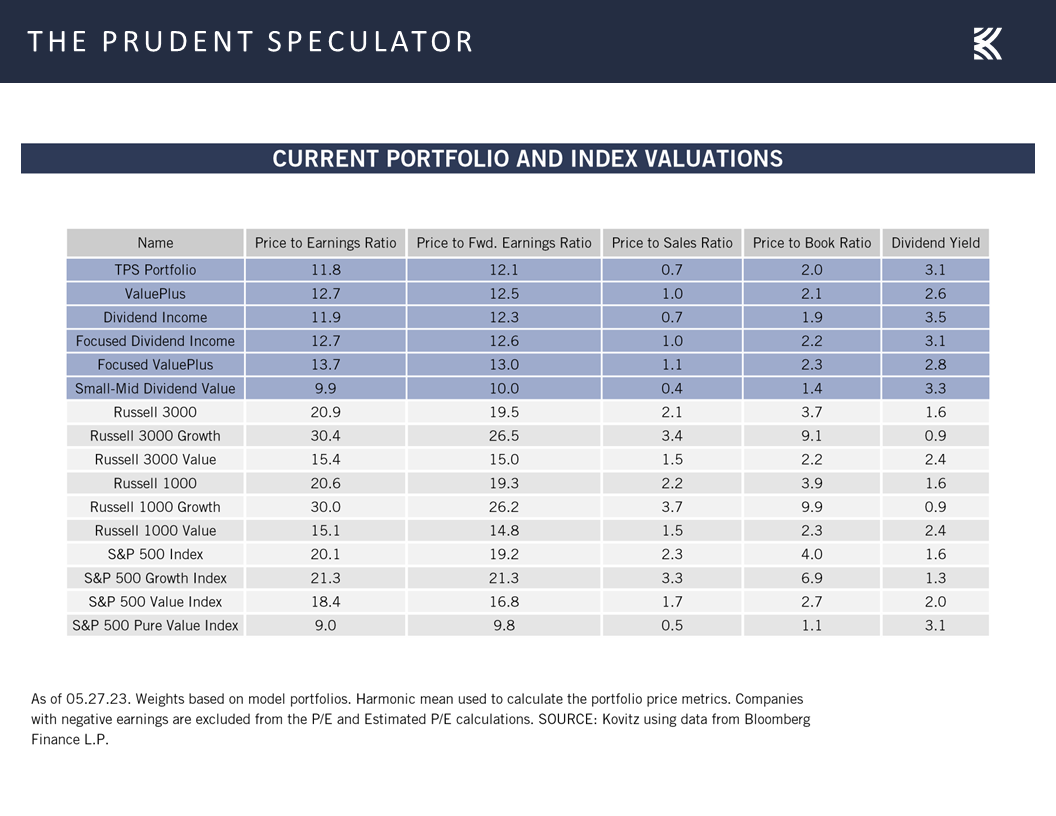

Valuations – Long-Term Interest Rates Still Historically Low; Stocks Reasonably Priced

TPS AI-Exposed Stocks – Eleven stocks

Earnings News – Updates on five stocks across three different sectors

Week in Review – Volatile Five Days; Most Indexes End Lower

All eyes were on Washington last week with debt-ceiling negotiations continuing as the so-called X-date for Uncle Sam defaulting on its obligations moved ever closer. Not surprisingly, equity prices were again volatile, rising on Friday when it appeared Speaker of the House Kevin McCarthy and President Biden were closer to a compromise and Treasury Secretary Janet Yellen pushed back the X-date to June 5 from June 1, and falling precipitously in the middle of the week when a deal looked less likely and ratings agency Fitch placed the United States’ ‘AAA’ Long-Term Foreign-Currency Issuer Default Rating on Rating Watch Negative.

Debt Ceiling – Deal Talks Ebb and Flow

Fitch warned, “The Rating Watch Negative reflects increased political partisanship that is hindering reaching a resolution to raise or suspend the debt limit despite the fast-approaching X-date (when the U.S. Treasury exhausts its cash position and capacity for extraordinary measures without incurring new debt). Fitch still expects a resolution to the debt limit before the X-date. However, we believe risks have risen that the debt limit will not be raised or suspended before the x-date and consequently that the government could begin to miss payments on some of its obligations. The brinkmanship over the debt ceiling, failure of the U.S. authorities to meaningfully tackle medium-term fiscal challenges that will lead to rising budget deficits and a growing debt burden signal downside risks to U.S. creditworthiness.”

No doubt, the Fitch move brought back memories of Standard & Poor’s actually moving forward with a downgrade of the credit rating of the United State on August 5, 2011. S&P then proclaimed, “The downgrade reflects our opinion that the plan that Congress and the Administration recently agreed to falls short of what, in our view, would be necessary to stabilize the government’s medium-term debt dynamics.”

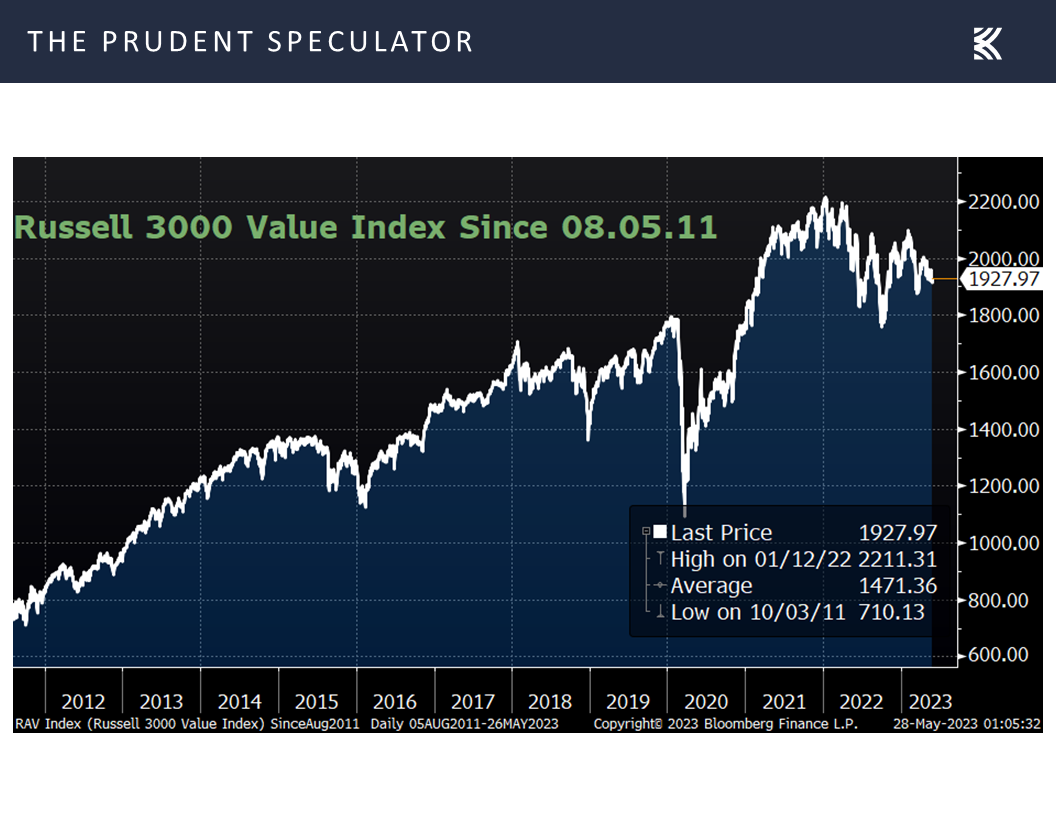

That’s right, even though the debt ceiling was raised five days earlier, S&P chose to lower its rating, which caused plenty of short-term consternation for the equity markets, with Value stocks not bottoming out until two months later. Of course, that trip south is barely noticeable when looking at a price chart of the Russell 3000 Value index over the past dozen years.

Credit Rating Downgrade Perspective – Fitch Brings Back Memories of August 2011…Which Two-Months Later Saw a Significant Market Bottom

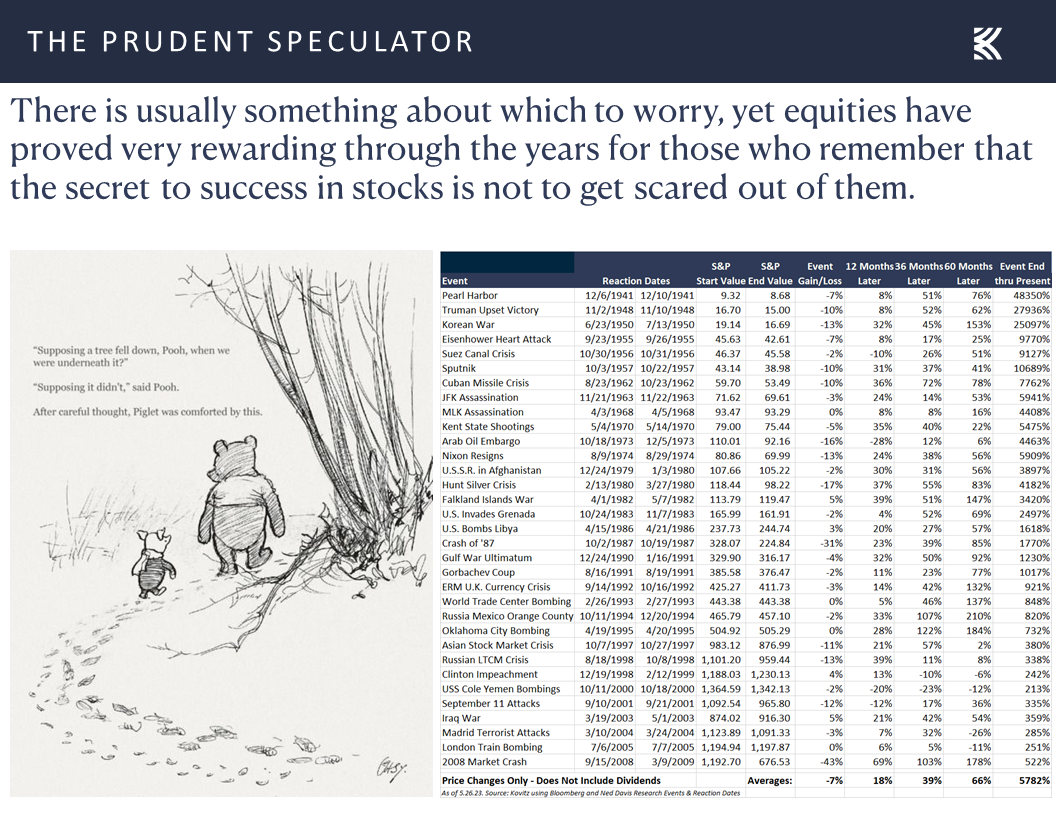

That does not mean that we should not be concerned about neat-term developments in DC, even as reports came out over the Memorial Day weekend that a tentative agreement between the White House and Republicans to avoid a U.S. default had been reached. Of course, history shows that far more money has been lost in the equity markets preparing for disconcerting events than has been lost in the events themselves and their aftermath.

Historical Perspective – Plenty of Scary Events, but the Long-Term Trend is Up

Indeed, given that the long-term trend in stock prices is higher, with substantial wealth likely to be compounded for those who remember that time in the market trumps market timing,

we continue to keep our attention focused on the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks.

Corporate Profits – EPS Growth Still the Forecast

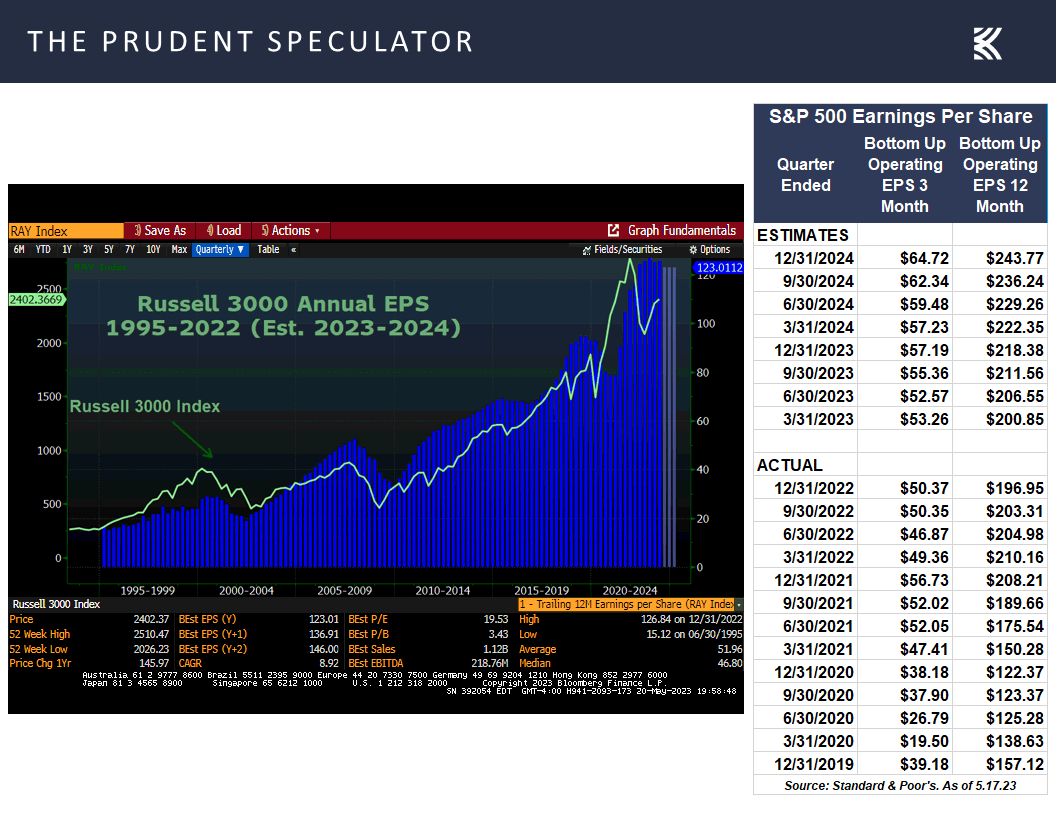

After all, corporations generally become more valuable over time as corporate profits expand,

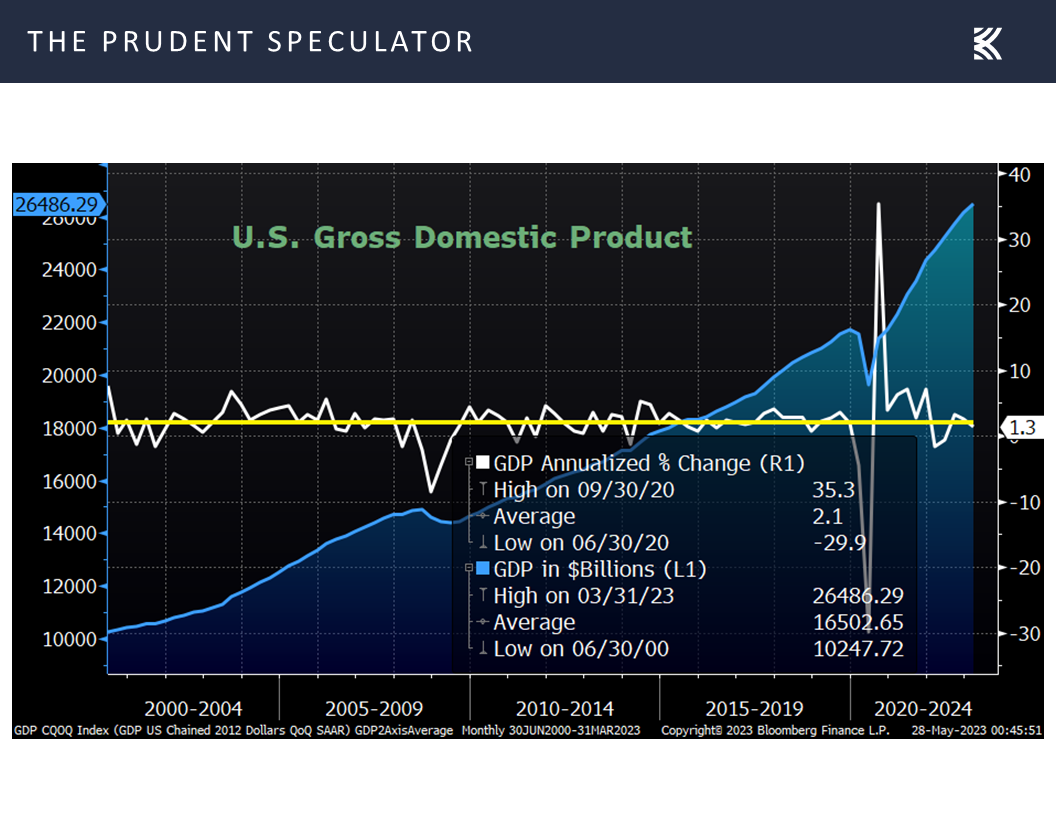

given that the multi-year trend in GDP growth is higher. After all, despite all the current consternation about the state of the economy, real (inflation-adjusted) Q1 growth was revised up last week to 1.3%, while nominal GDP hit an all-time high of $26.5 trillion, up 7.1% on a year-over-year basis in actual dollars.

Econ News – More Positive Stats than Negative; Odds of Fed Rate Cuts Diminish

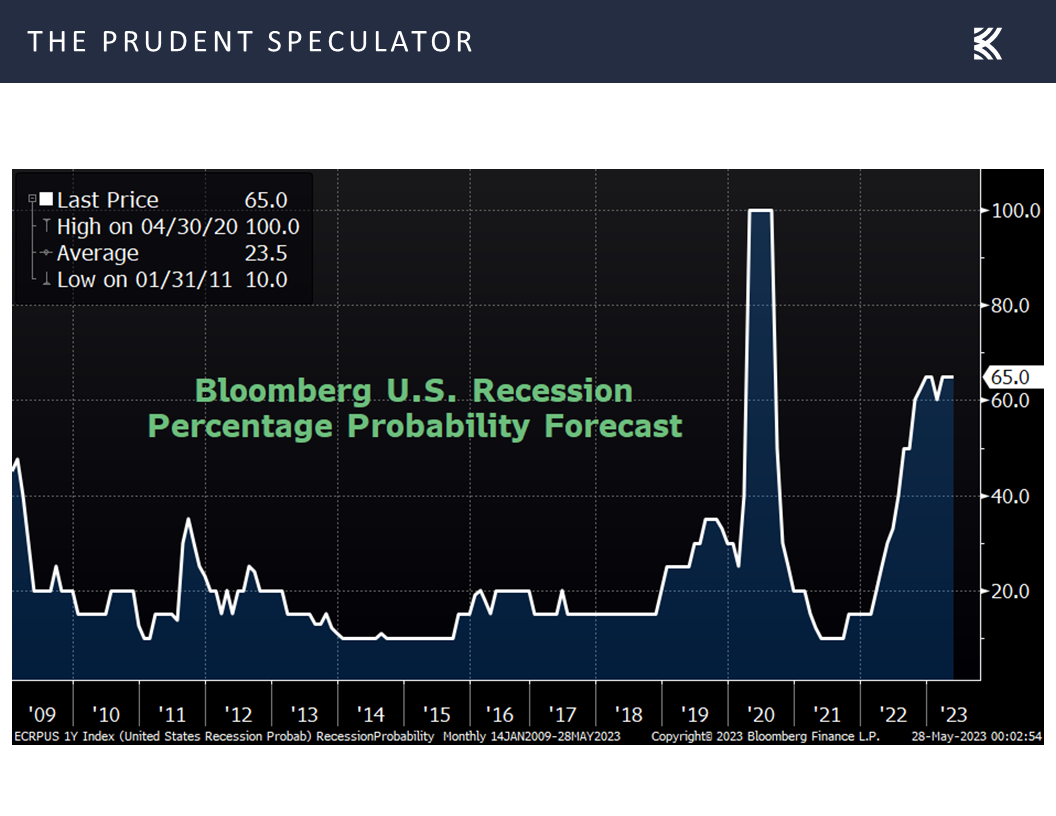

Interestingly, given that Bloomberg continues to calculate the odds of recession in the next 12 months at 65%,

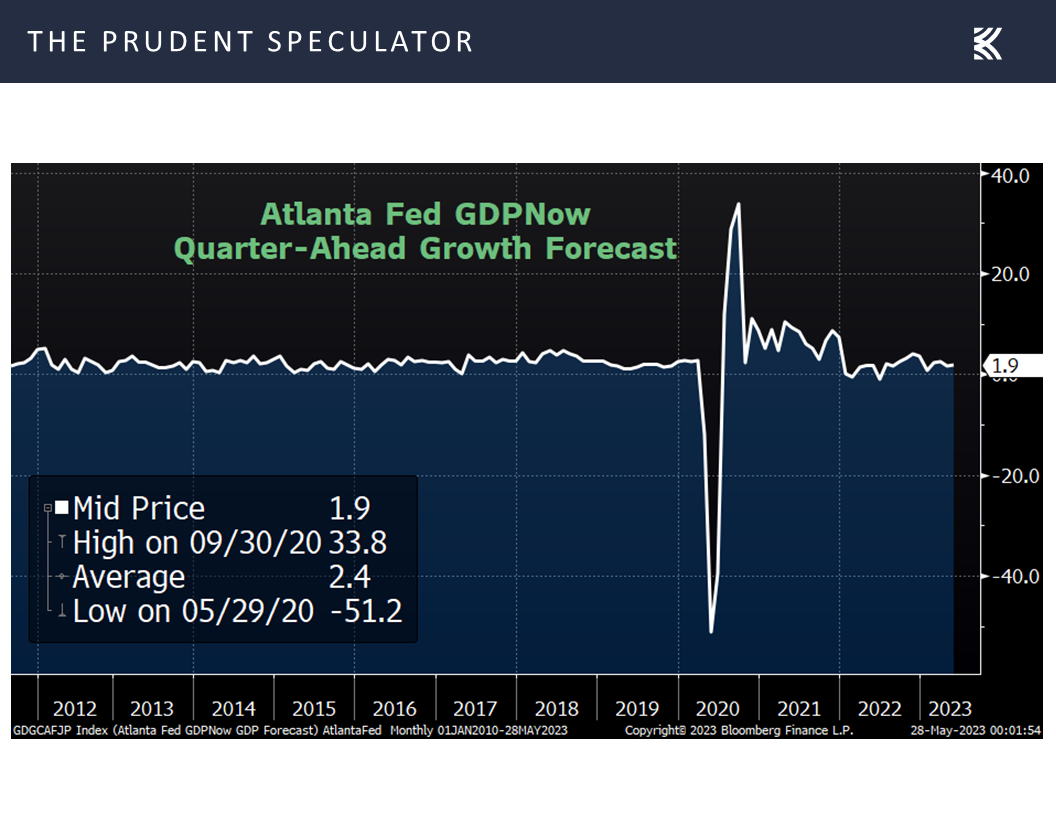

and the Atlanta Fed lowered its outlook for Q2 real GDP growth (yes, growth!) to 1.9% on Friday, down from its prior estimate of 2.9% on May 17,

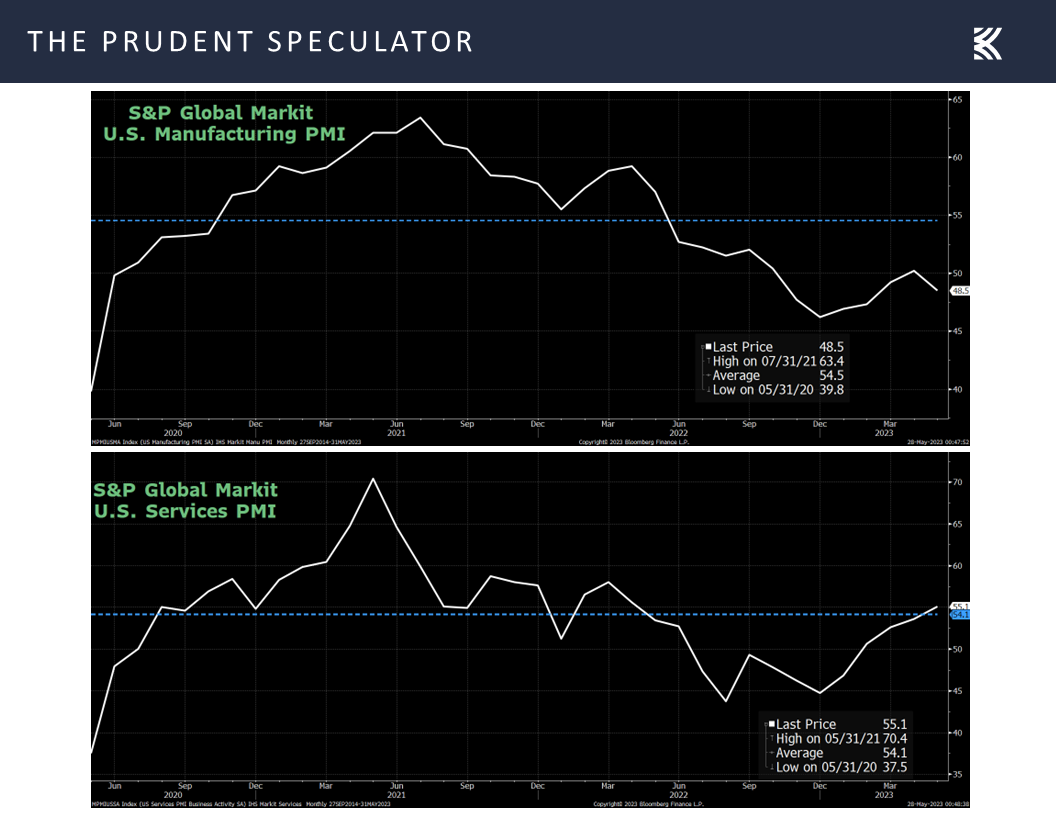

the economic numbers out last week were pretty good, relatively speaking. While the S&P Global U.S. Manufacturing gauge for May came in below expectations at 48.5, signifying contraction in the factory sector, the S&P Global U.S. Services PMI topped estimates, rising to 55.1 in May, suggesting solid growth ahead for the much-larger service economy.

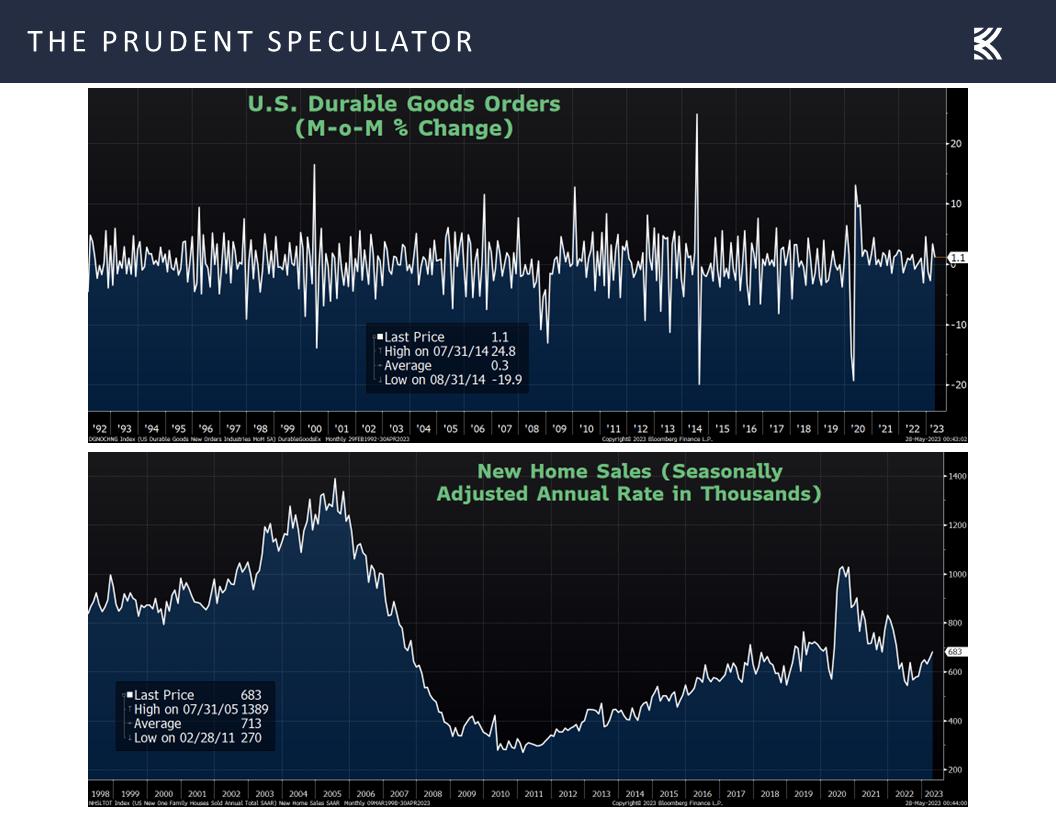

We also learned that orders for U.S. manufactured goods rose by a better-than-expected 1.1% in April and sales of new homes trumped forecasts, coming in at 683,000.

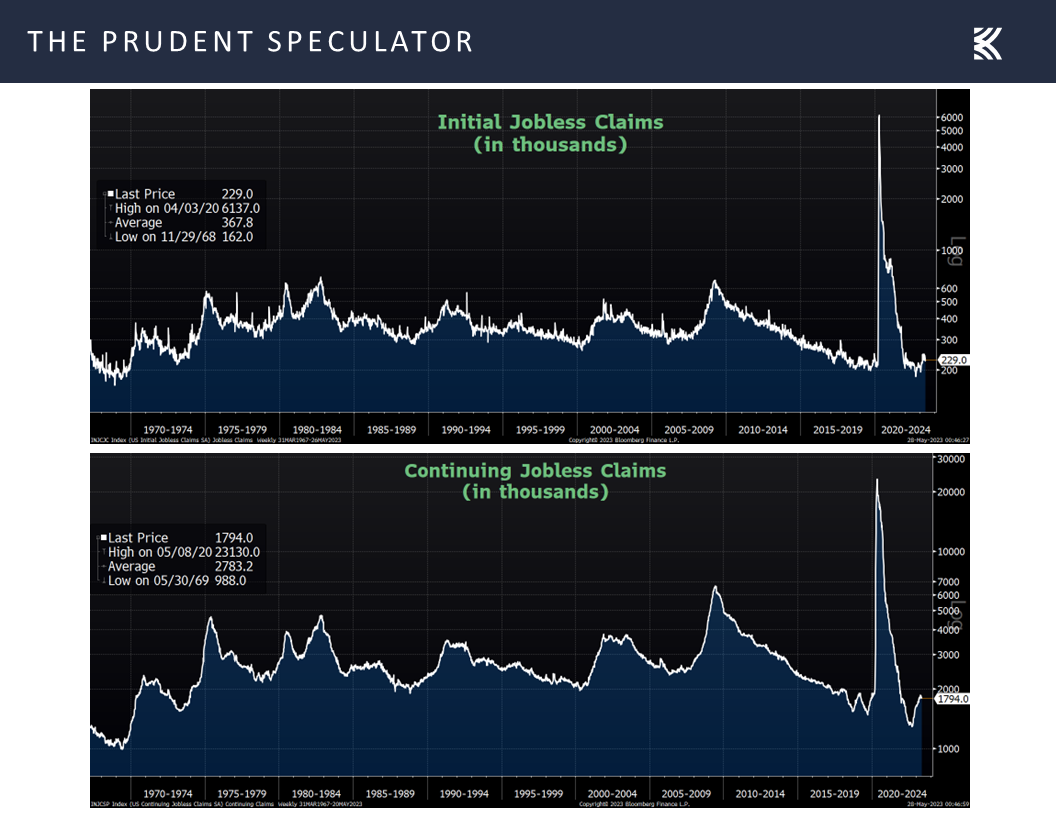

In addition, the labor market remained remarkably resilient with 229,000 first-time filings for jobless benefits in the latest week, below projections of 245,000,

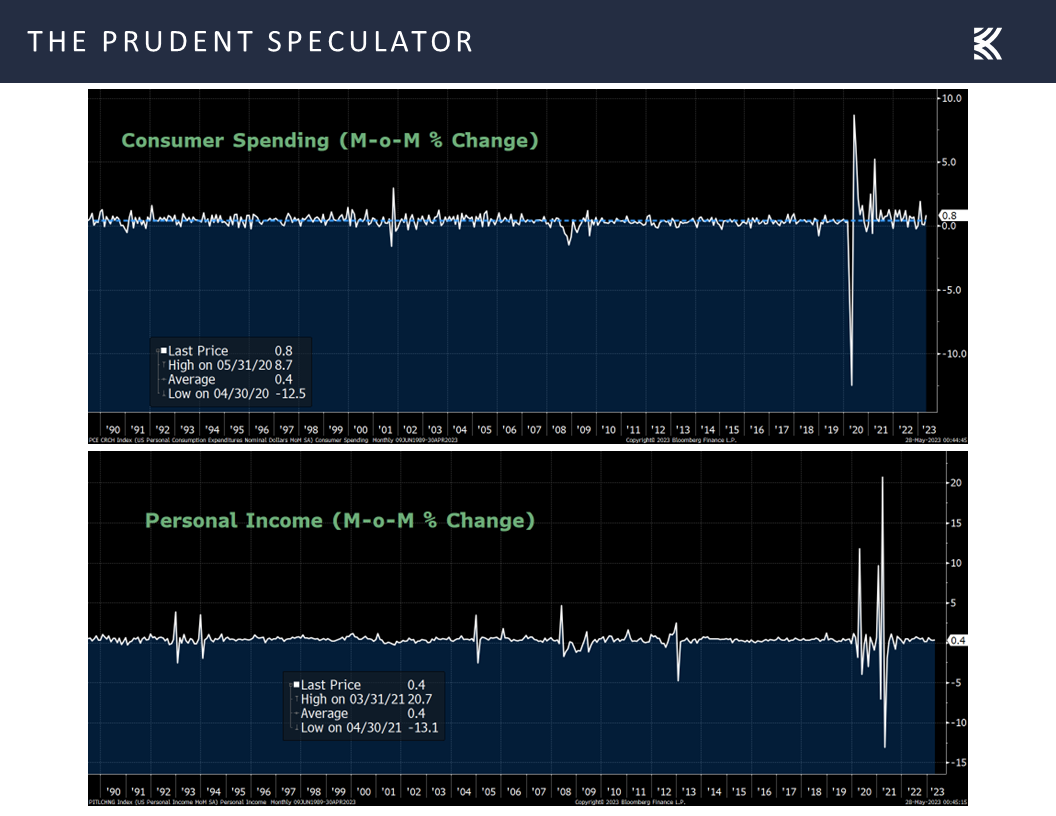

the solid employment picture supporting personal incomes and consumer spending, both of which moved higher in April,

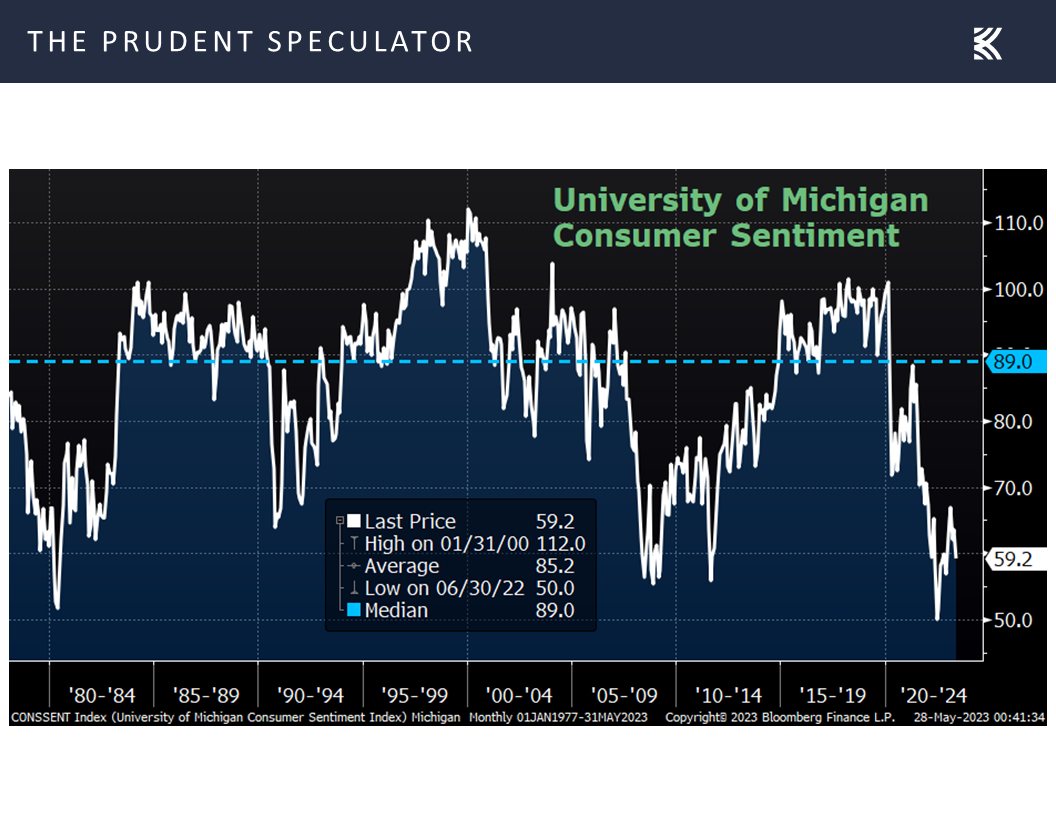

and contributing to a better-than-predicted read on consumer sentiment from the University of Michigan.

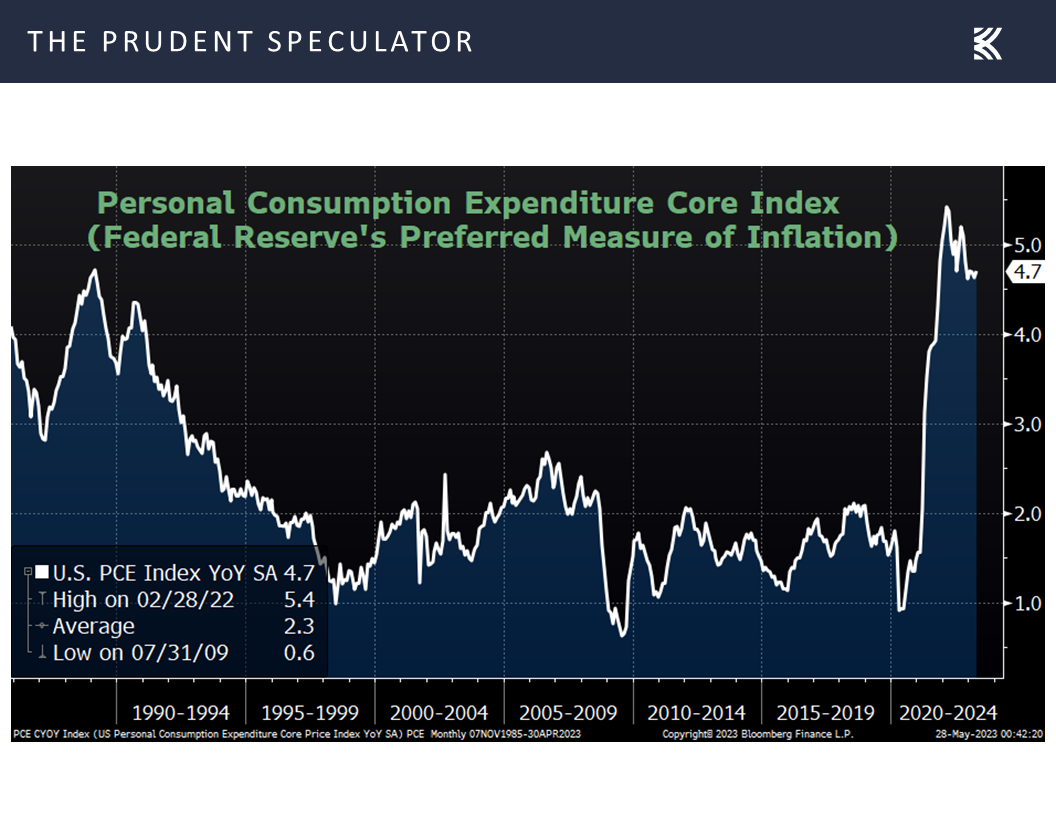

To be sure, given that that Michigan Sentiment figure is well below the historical average, happy days are not exactly here again, especially as the Federal Reserve’s favorite measure of inflation, the Personal Consumption Expenditure Core Index, ticked up to 4.7% in April,

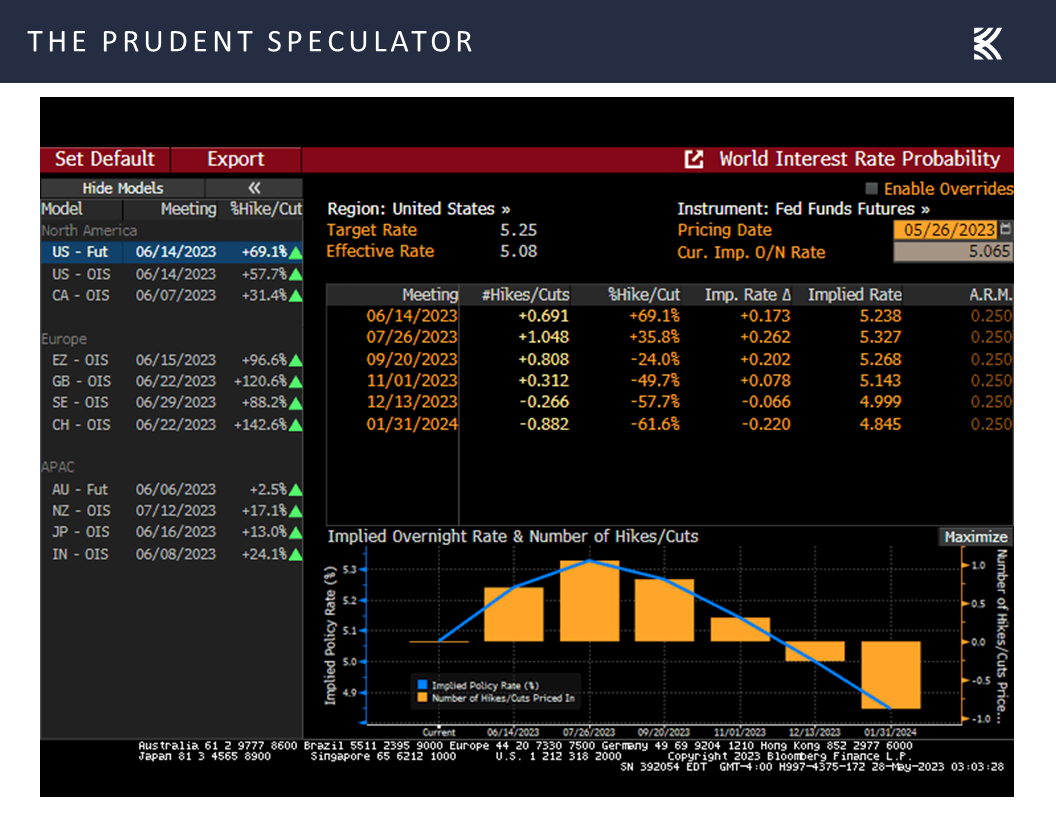

reducing the likelihood of interest rate cuts from the Federal Reserve than the odds suggested a week ago, if the highly volatile Fed Funds futures are to be believed.

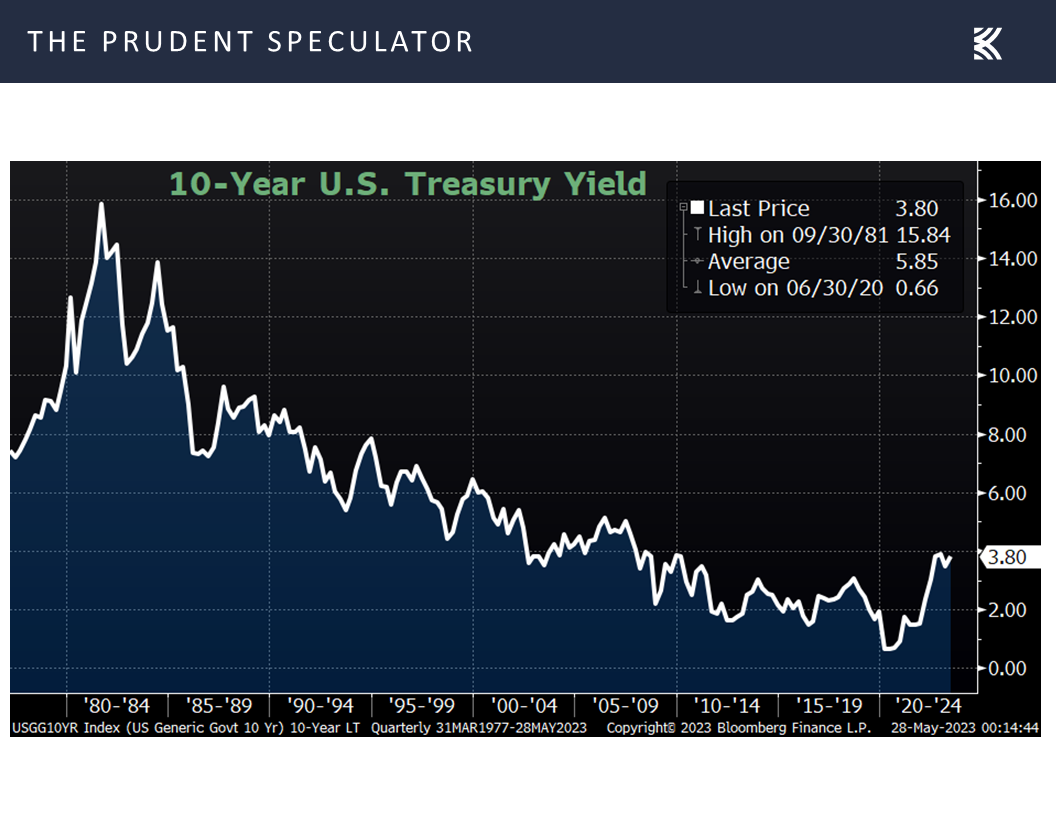

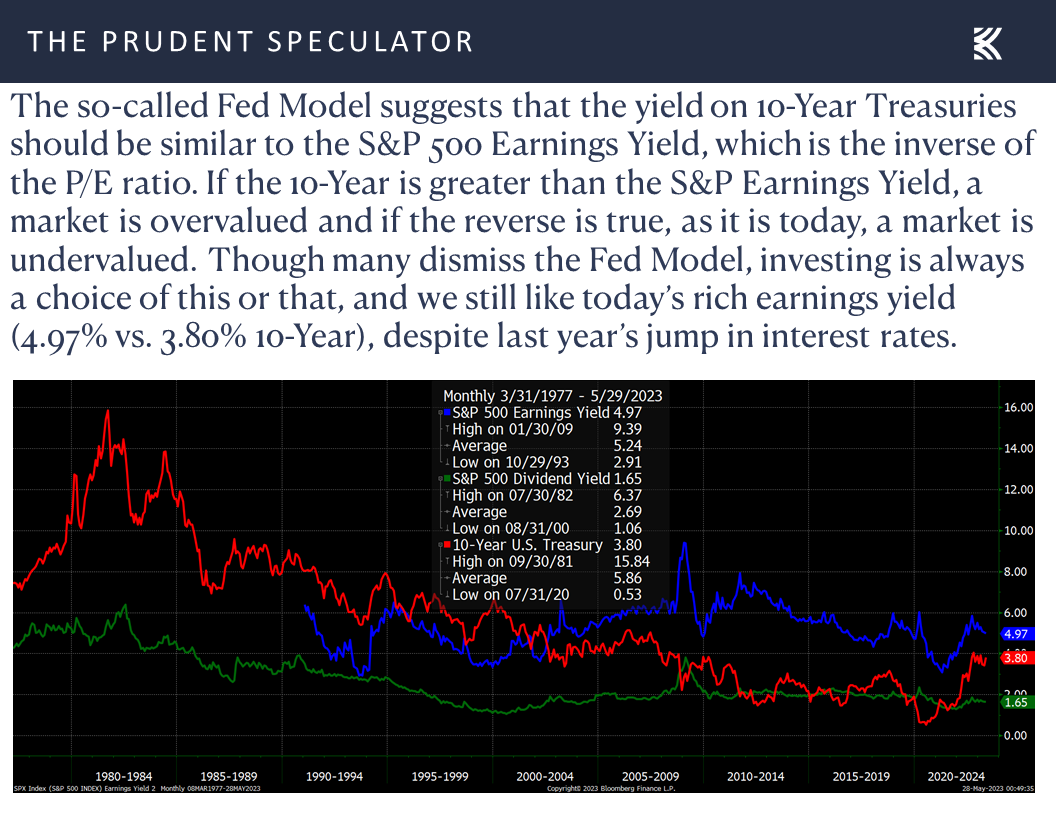

Valuations – Long-Term Interest Rates Still Historically Low; Stocks Reasonably Priced

We expect the near term to be volatile, especially as Congress still has to pass what the leaders have negotiated on the debt ceiling, but we continue to see no reason to alter our long-term enthusiasm for equities.

After all, long-term interest rates are still well below the historical average since the launch of The Prudent Speculator in 1977,

and stocks still compare favorably to government bonds on an earnings-yield basis,

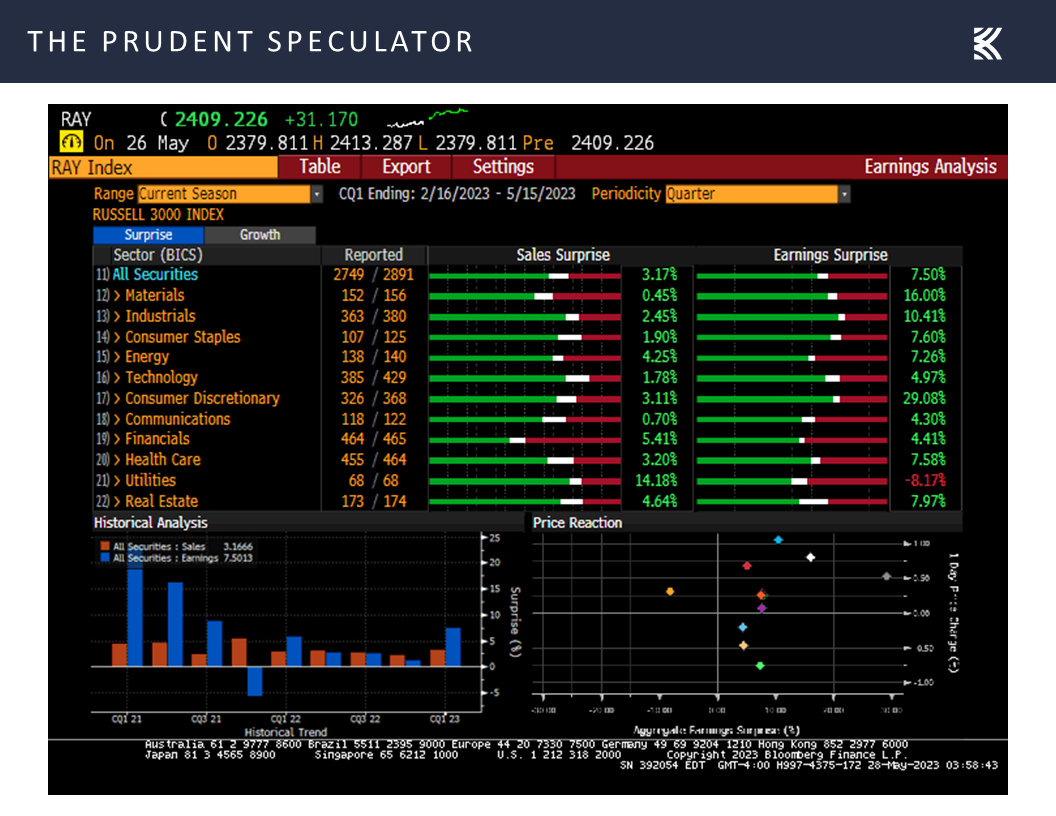

while Q1 earnings reports surprised to the upside with 63.3% of the constituents of the Russell 3000 index beating the Street.

Happily, Corporate America shares our optimism as research firm Birinyi Associates reported last week that companies in the Russell 3000 have announced plans thus far in 2023 to buy back more than $600 billion in shares this year, in line with last year’s record pace. Birinyi added that in 2022, companies announced $1.27 trillion of share repurchases and completed $1.05 trillion in buybacks, both all-time highs.

Stock Market News: Updates on five stocks across three different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Debt Ceiling, Credit Rating, AI-Exposed Stocks, Corporate Profits and more Economic News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Debt Ceiling, Credit Rating, AI-Exposed Stocks, Corporate Profits and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week in Review – Volatile Five Days; Most Indexes End Lower

Debt Ceiling – Deal Talks Ebb and Flow

Credit Rating Downgrade Perspective – Fitch Brings Back Memories of August 2011…Which Two-Months Later Saw a Significant Market Bottom

Historical Perspective – Plenty of Scary Events, but the Long-Term Trend is Up

Corporate Profits – EPS Growth Still the Forecast

Econ News – More Positive Stats than Negative; Odds of Fed Rate Cuts Diminish

Valuations – Long-Term Interest Rates Still Historically Low; Stocks Reasonably Priced

TPS AI-Exposed Stocks – Eleven stocks

Earnings News – Updates on five stocks across three different sectors

Week in Review – Volatile Five Days; Most Indexes End Lower

All eyes were on Washington last week with debt-ceiling negotiations continuing as the so-called X-date for Uncle Sam defaulting on its obligations moved ever closer. Not surprisingly, equity prices were again volatile, rising on Friday when it appeared Speaker of the House Kevin McCarthy and President Biden were closer to a compromise and Treasury Secretary Janet Yellen pushed back the X-date to June 5 from June 1, and falling precipitously in the middle of the week when a deal looked less likely and ratings agency Fitch placed the United States’ ‘AAA’ Long-Term Foreign-Currency Issuer Default Rating on Rating Watch Negative.

Debt Ceiling – Deal Talks Ebb and Flow

Fitch warned, “The Rating Watch Negative reflects increased political partisanship that is hindering reaching a resolution to raise or suspend the debt limit despite the fast-approaching X-date (when the U.S. Treasury exhausts its cash position and capacity for extraordinary measures without incurring new debt). Fitch still expects a resolution to the debt limit before the X-date. However, we believe risks have risen that the debt limit will not be raised or suspended before the x-date and consequently that the government could begin to miss payments on some of its obligations. The brinkmanship over the debt ceiling, failure of the U.S. authorities to meaningfully tackle medium-term fiscal challenges that will lead to rising budget deficits and a growing debt burden signal downside risks to U.S. creditworthiness.”

No doubt, the Fitch move brought back memories of Standard & Poor’s actually moving forward with a downgrade of the credit rating of the United State on August 5, 2011. S&P then proclaimed, “The downgrade reflects our opinion that the plan that Congress and the Administration recently agreed to falls short of what, in our view, would be necessary to stabilize the government’s medium-term debt dynamics.”

That’s right, even though the debt ceiling was raised five days earlier, S&P chose to lower its rating, which caused plenty of short-term consternation for the equity markets, with Value stocks not bottoming out until two months later. Of course, that trip south is barely noticeable when looking at a price chart of the Russell 3000 Value index over the past dozen years.

Credit Rating Downgrade Perspective – Fitch Brings Back Memories of August 2011…Which Two-Months Later Saw a Significant Market Bottom

That does not mean that we should not be concerned about neat-term developments in DC, even as reports came out over the Memorial Day weekend that a tentative agreement between the White House and Republicans to avoid a U.S. default had been reached. Of course, history shows that far more money has been lost in the equity markets preparing for disconcerting events than has been lost in the events themselves and their aftermath.

Historical Perspective – Plenty of Scary Events, but the Long-Term Trend is Up

Indeed, given that the long-term trend in stock prices is higher, with substantial wealth likely to be compounded for those who remember that time in the market trumps market timing,

we continue to keep our attention focused on the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks.

Corporate Profits – EPS Growth Still the Forecast

After all, corporations generally become more valuable over time as corporate profits expand,

given that the multi-year trend in GDP growth is higher. After all, despite all the current consternation about the state of the economy, real (inflation-adjusted) Q1 growth was revised up last week to 1.3%, while nominal GDP hit an all-time high of $26.5 trillion, up 7.1% on a year-over-year basis in actual dollars.

Econ News – More Positive Stats than Negative; Odds of Fed Rate Cuts Diminish

Interestingly, given that Bloomberg continues to calculate the odds of recession in the next 12 months at 65%,

and the Atlanta Fed lowered its outlook for Q2 real GDP growth (yes, growth!) to 1.9% on Friday, down from its prior estimate of 2.9% on May 17,

the economic numbers out last week were pretty good, relatively speaking. While the S&P Global U.S. Manufacturing gauge for May came in below expectations at 48.5, signifying contraction in the factory sector, the S&P Global U.S. Services PMI topped estimates, rising to 55.1 in May, suggesting solid growth ahead for the much-larger service economy.

We also learned that orders for U.S. manufactured goods rose by a better-than-expected 1.1% in April and sales of new homes trumped forecasts, coming in at 683,000.

In addition, the labor market remained remarkably resilient with 229,000 first-time filings for jobless benefits in the latest week, below projections of 245,000,

the solid employment picture supporting personal incomes and consumer spending, both of which moved higher in April,

and contributing to a better-than-predicted read on consumer sentiment from the University of Michigan.

To be sure, given that that Michigan Sentiment figure is well below the historical average, happy days are not exactly here again, especially as the Federal Reserve’s favorite measure of inflation, the Personal Consumption Expenditure Core Index, ticked up to 4.7% in April,

reducing the likelihood of interest rate cuts from the Federal Reserve than the odds suggested a week ago, if the highly volatile Fed Funds futures are to be believed.

Valuations – Long-Term Interest Rates Still Historically Low; Stocks Reasonably Priced

We expect the near term to be volatile, especially as Congress still has to pass what the leaders have negotiated on the debt ceiling, but we continue to see no reason to alter our long-term enthusiasm for equities.

After all, long-term interest rates are still well below the historical average since the launch of The Prudent Speculator in 1977,

and stocks still compare favorably to government bonds on an earnings-yield basis,

while Q1 earnings reports surprised to the upside with 63.3% of the constituents of the Russell 3000 index beating the Street.

Happily, Corporate America shares our optimism as research firm Birinyi Associates reported last week that companies in the Russell 3000 have announced plans thus far in 2023 to buy back more than $600 billion in shares this year, in line with last year’s record pace. Birinyi added that in 2022, companies announced $1.27 trillion of share repurchases and completed $1.05 trillion in buybacks, both all-time highs.

Stock Market News: Updates on five stocks across three different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.