The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Earnings, AAII Sentiment, Valuations and more Economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week in Review – Lousy Last Two, but Nice Five Days

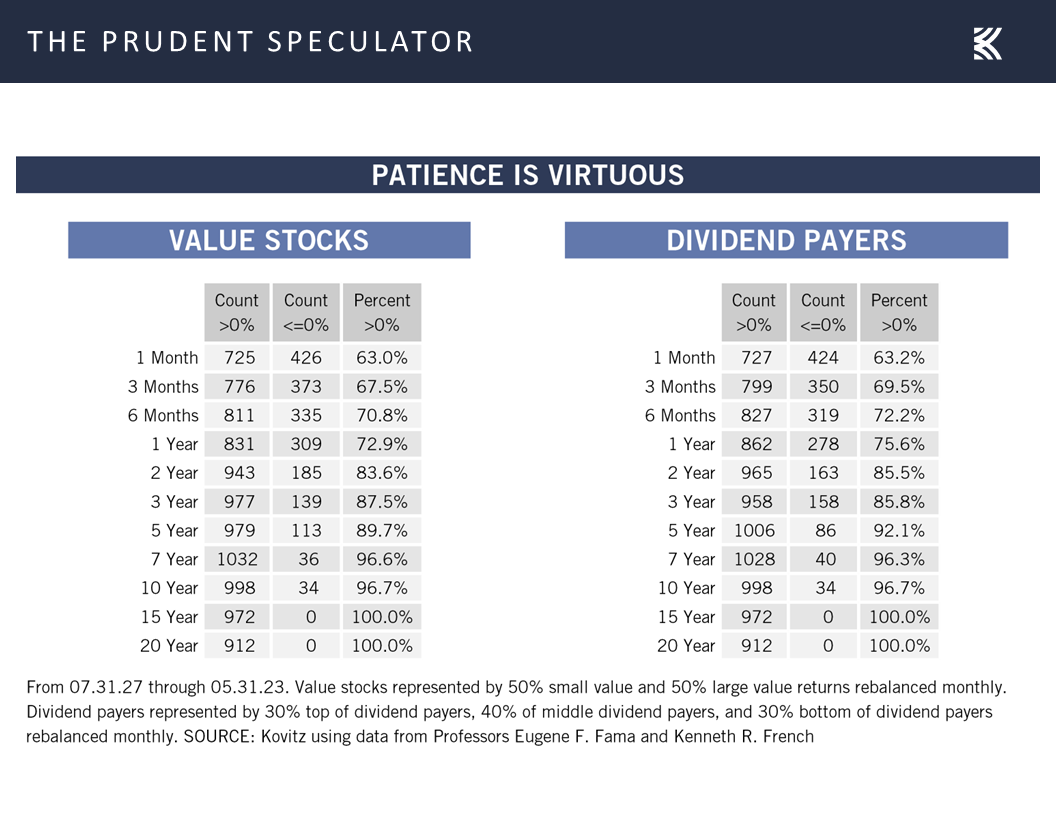

Patience – The Longer the Hold, The Lower the Chance of Loss

Time in the Market – Best to Ignore Those Who Think Market Timing Works

Prediction is Difficult – Economists Lower Recession Forecasts

Econ News – Mixed Numbers

Earnings – Strong Q2 Results; Growth Still the Forecast This Year and in 2024

Sentiment – AAII Bullishness is Very Elevated

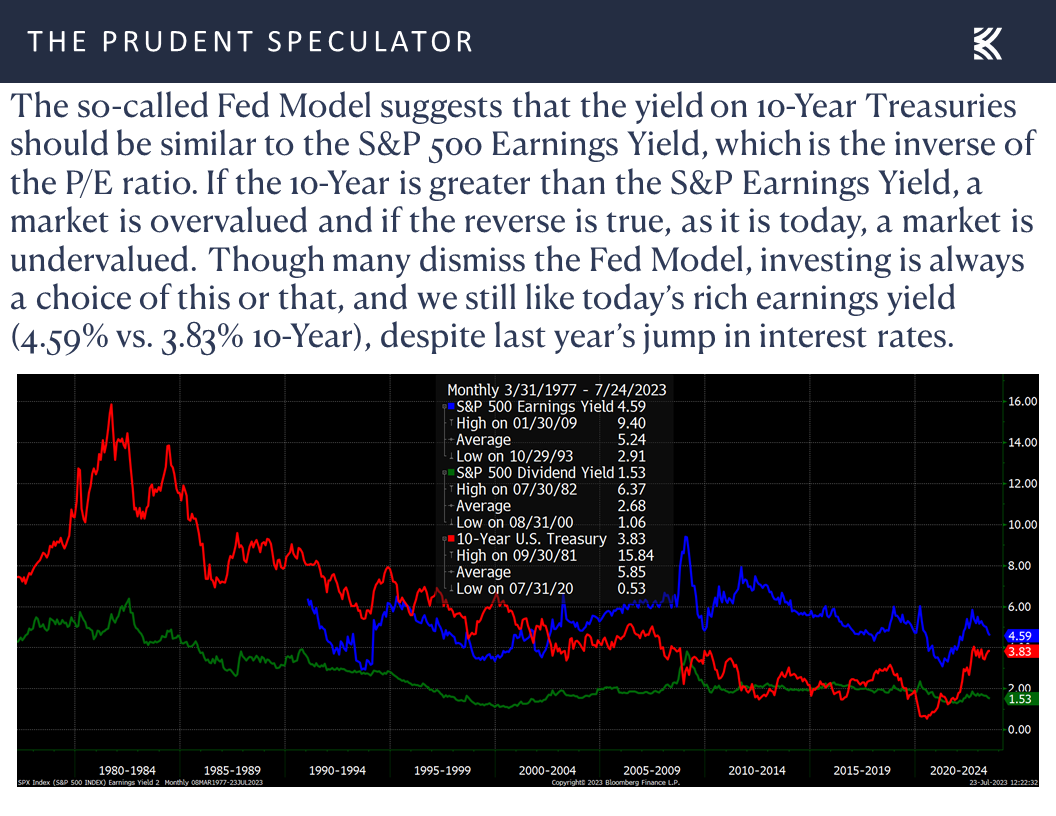

Valuations – Inexpensive Multiples for our Stocks

Cues from Value, Not From Price – Interesting Moves for VZ & PNC

Stock News – Updates on eighteen stocks across ten different sectors

Week in Review – Lousy Last Two, but Nice Five Days

Although the Dow Jones Industrial Average gained ground every day, pushing the daily winning streak for the price-weighted index to 10, the trading week again ended on a sour note, given that the average stock in the broad-based Russell 3000 index declined 1.0% over the Thursday-Friday period.

Happily, as was the case last week, performance looked a whole lot different with a bit longer measuring stick as the average stock, led by those of the Value persuasion, advanced more than 1% for the full five days. Indeed, lengthening the holding period can do wonders as history shows that the longer stocks are held, the greater the chance that they will appreciate in value.

Patience – The Longer the Hold, The Lower the Chance of Loss

As the table below illustrates, if one held Value Stocks for one month, the chance of a positive total return was 63.0%. Hold for 6 months and the odds improved to 70.8% but go out three years and the green ink percentage rose to 87.5%. Even better for those of us with a true long-term time horizon, the change of losing money in Value has been just 3.3% for all 10-year holding periods and 0% for all 15-year periods!

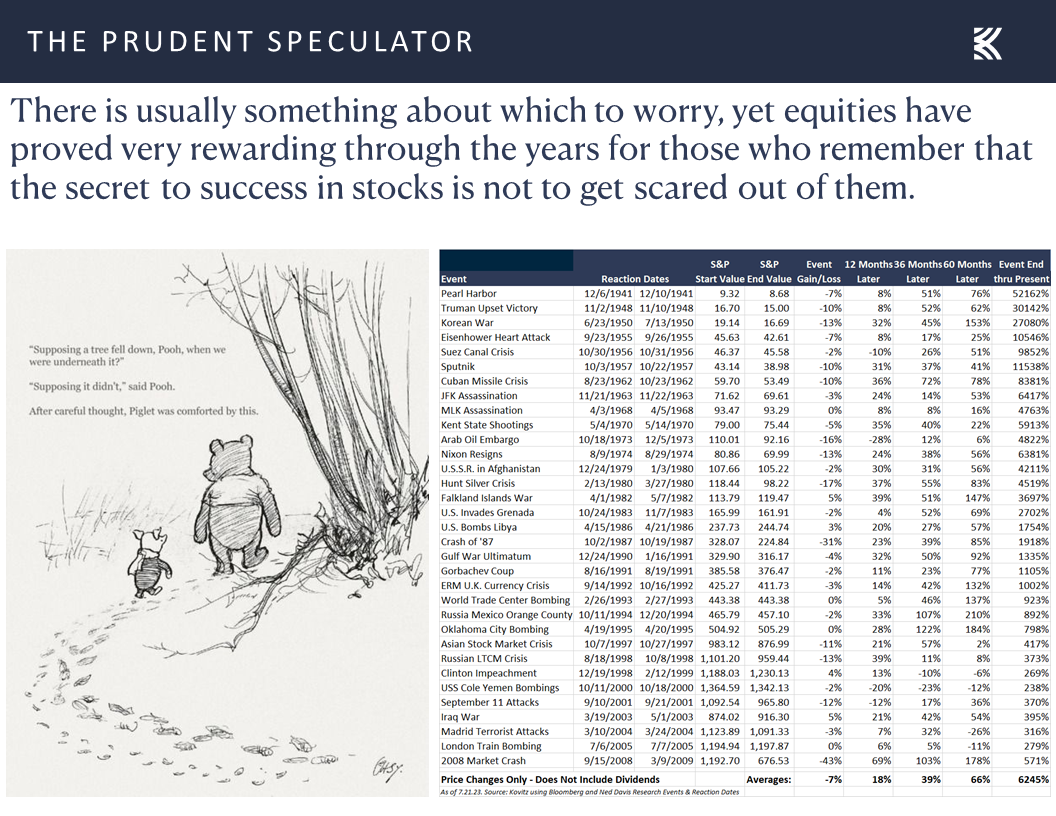

Time in the Market – Best to Ignore Those Who Think Market Timing Works

Of course, we realize that it is not always easy to keep the faith, so we constantly publish empirical evidence to illustrate that the secret to success in stocks is not to get scared out of them,

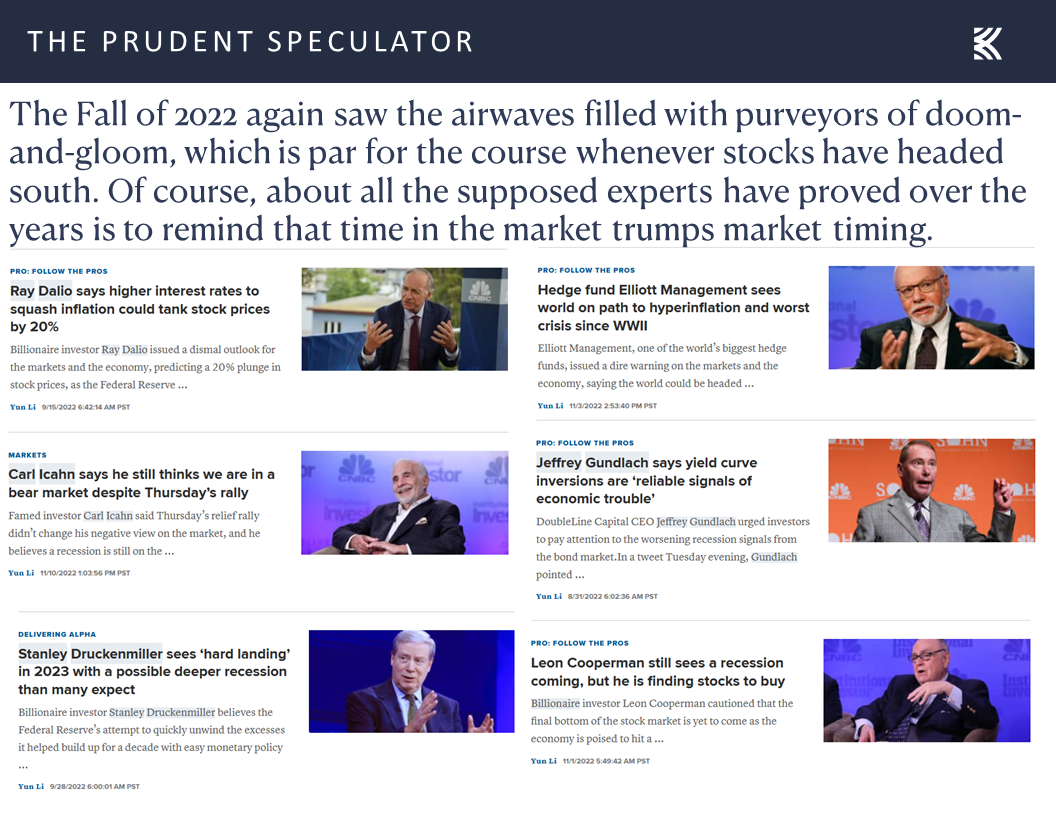

while we do our best to remind investors that just because a prominent investment professional is provided plenty of airtime in the financial press does not mean that his or her prognostications will come true, as we saw last fall,

and seemingly again a couple of months ago.

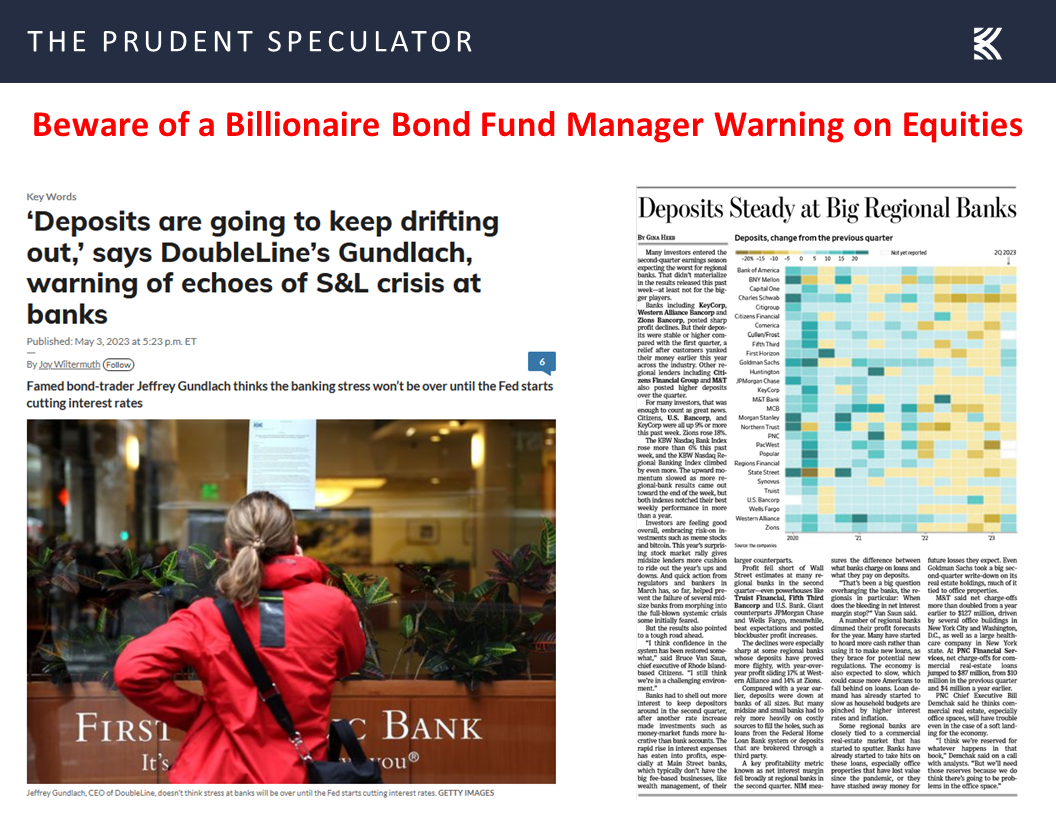

We might be accused of cherry-picking, but the doom-and-gloom chorus often sings loudest and garners the most attention from the media at precisely the wrong time. Obviously, there is plenty of ball to be played in this year’s banking drama, but as yet there has been no systemic flight of deposits, despite arguments from the fellow above (who might have a bias or two against stocks) to the contrary.

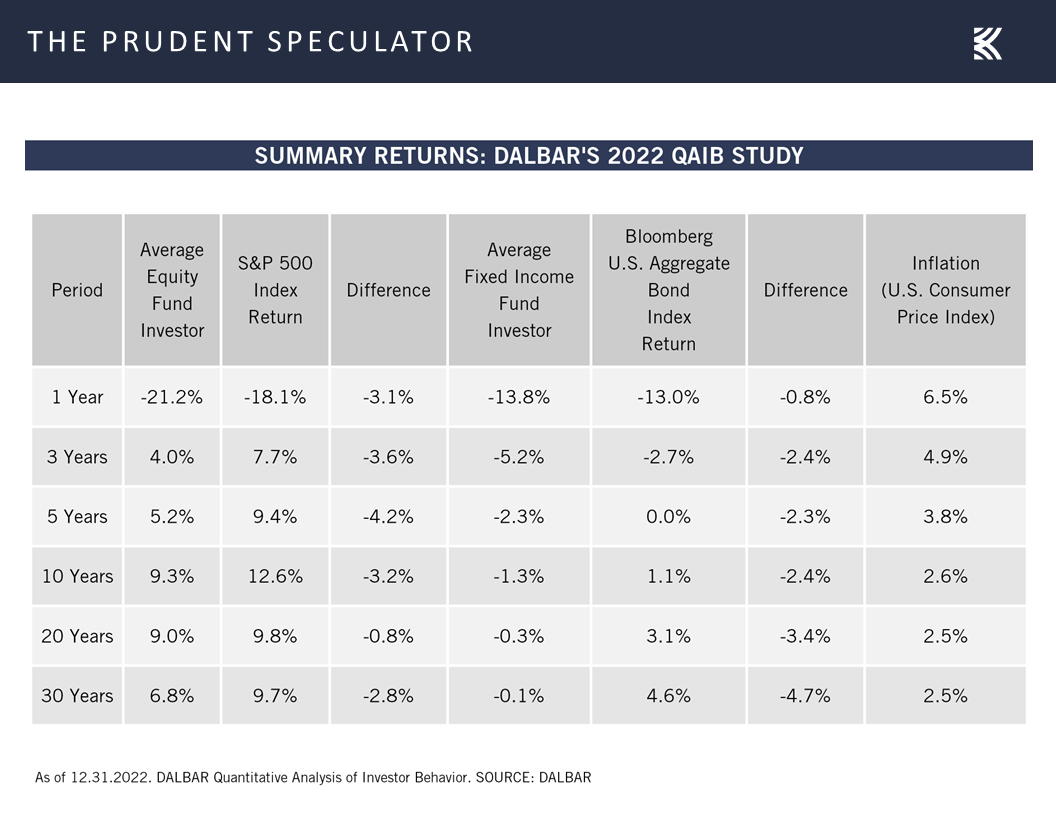

Unfortunately, many succumb to the siren song of market timing, even as plenty of data supports the argument that the only problem with market timing is getting the timing right. Interestingly, fixed income traders have worse luck than those who try to time their moves into and out of stocks, at least according to analytics compiled by DALBAR Inc. on mutual fund flows over the last three decades.

Prediction is Difficult – Economists Lower Recession Forecasts

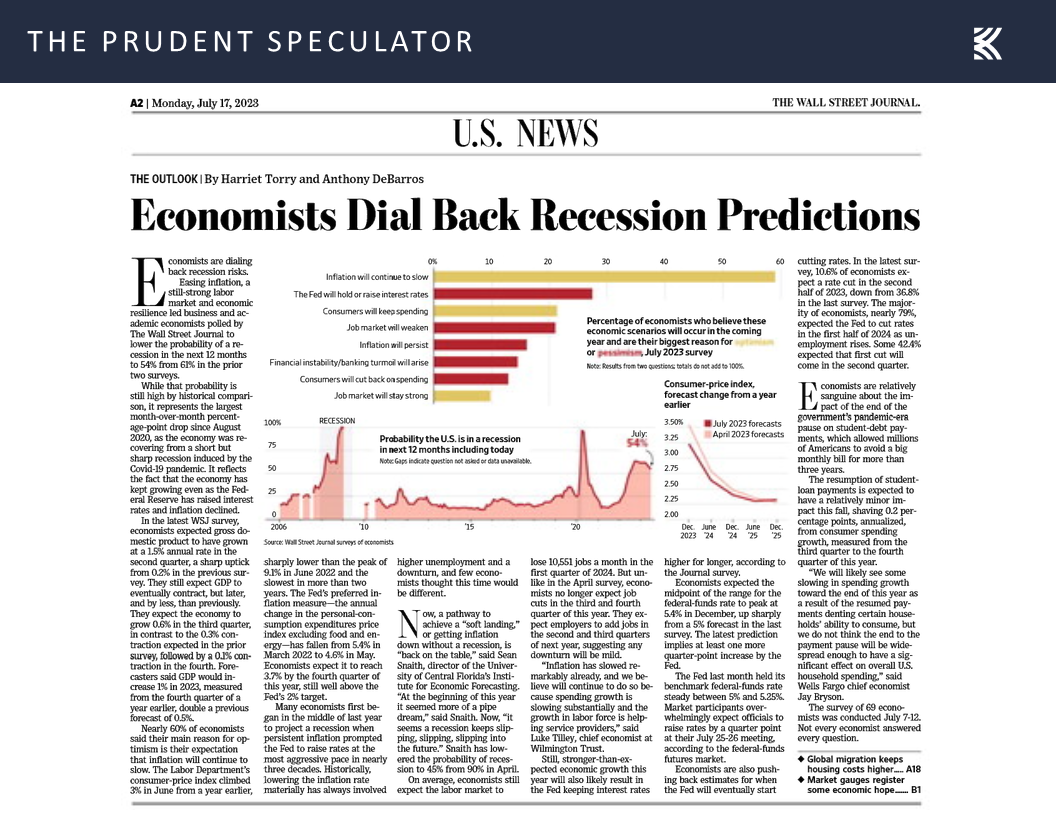

While the noted economist Paul Samuelson said, “The stock market has predicted nine of the last five recessions,” it would seem that economists themselves also aren’t very good at forecasting!

Econ News – Mixed Numbers

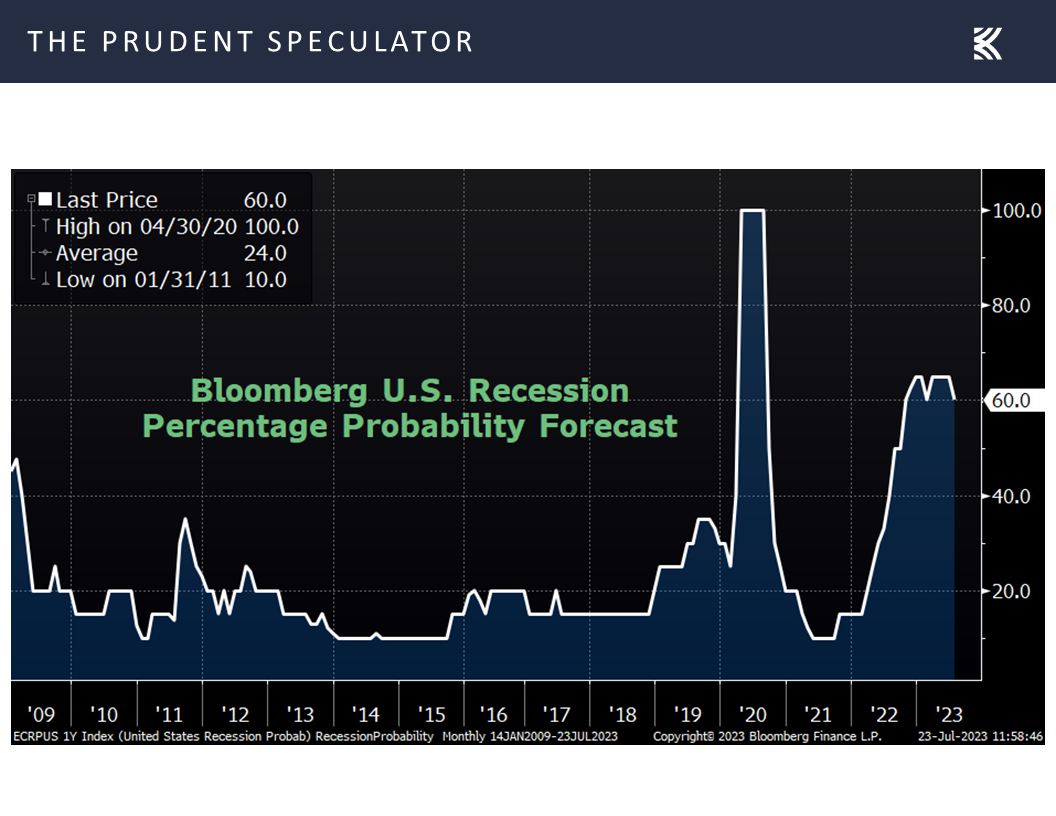

After all, the supposed experts have been calling for a U.S. recession for nearly a year now, but last week they hedged their bets a bit, with Bloomberg calculations today suggesting “only” a 60% chance of an economic contraction, down from 65% for much of 2023.

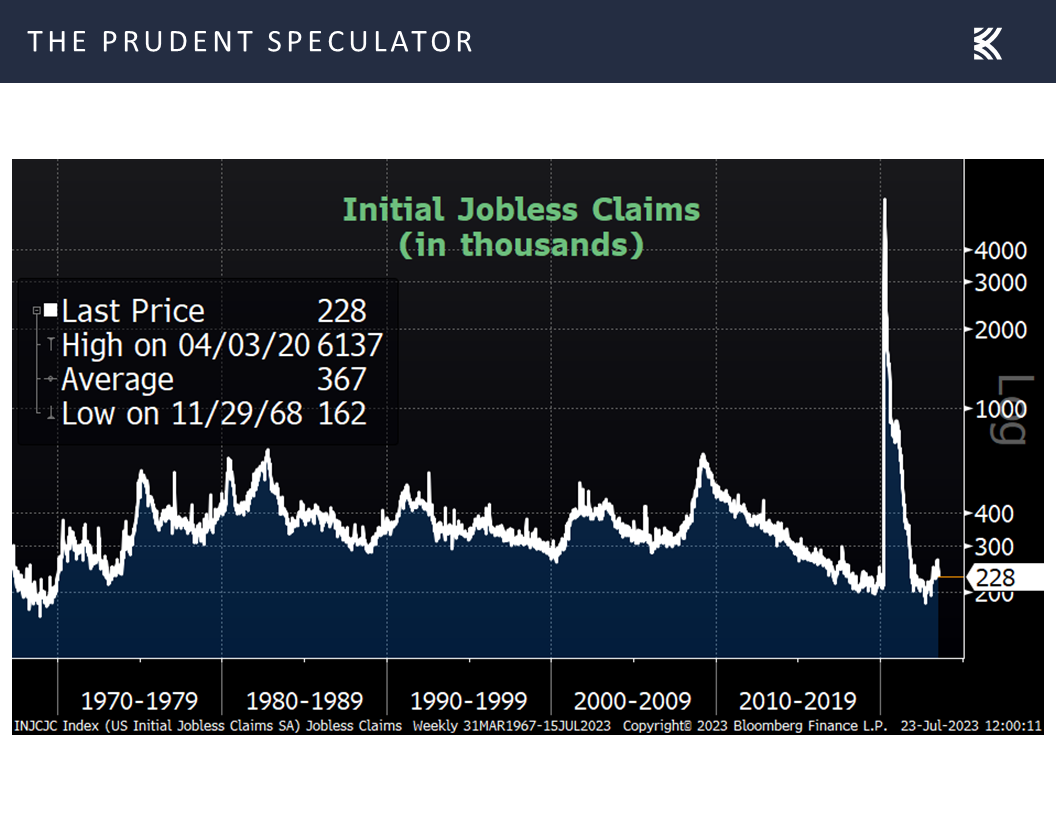

That lower probability is in keeping with comments from Bank of America (BAC – $31.98) CEO Brian Moynihan who said last week, “We continue to see a healthy U.S. economy that is growing at a slower pace, with a resilient job market.” Illustrating the labor point, first-time filings for unemployment benefits in the latest week fell to a historically very low 228,000, fewer than expected and down from 237,000 in the week prior.

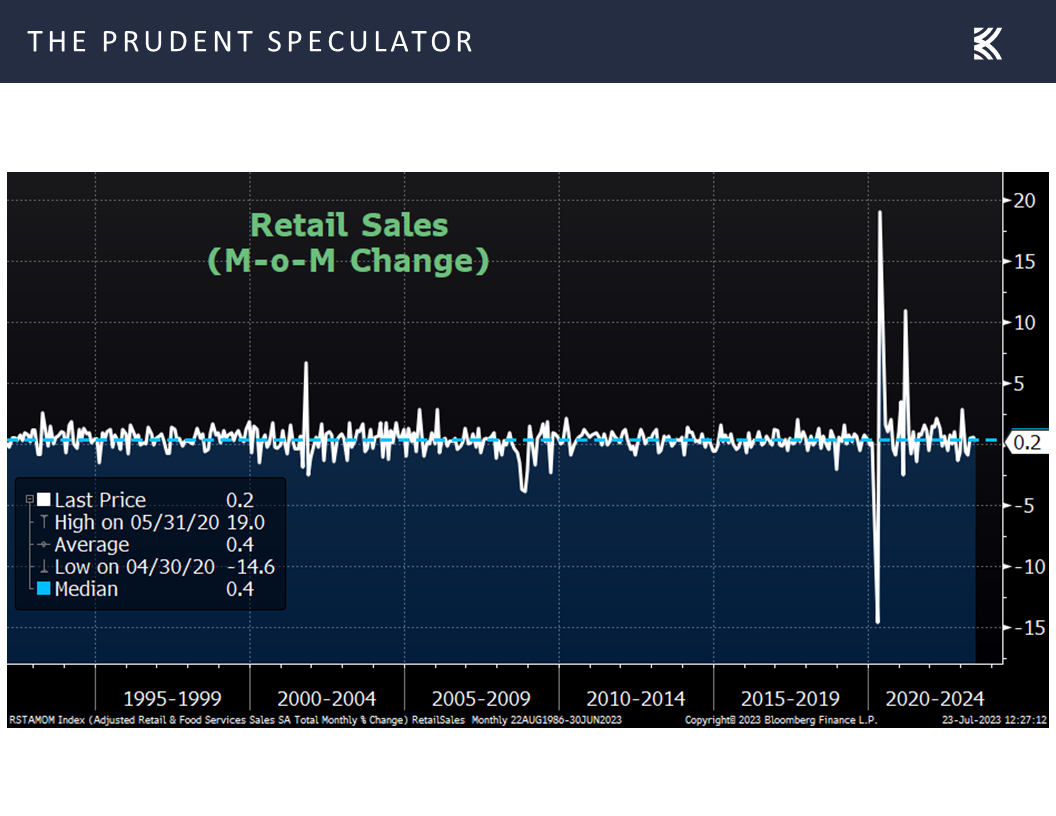

Bank of America CFO Alastair Borthwick added, “The overall health of the U.S. consumer remained strong,” which was supported by the report last week of a solid 0.2% increase in overall retail sales in June.

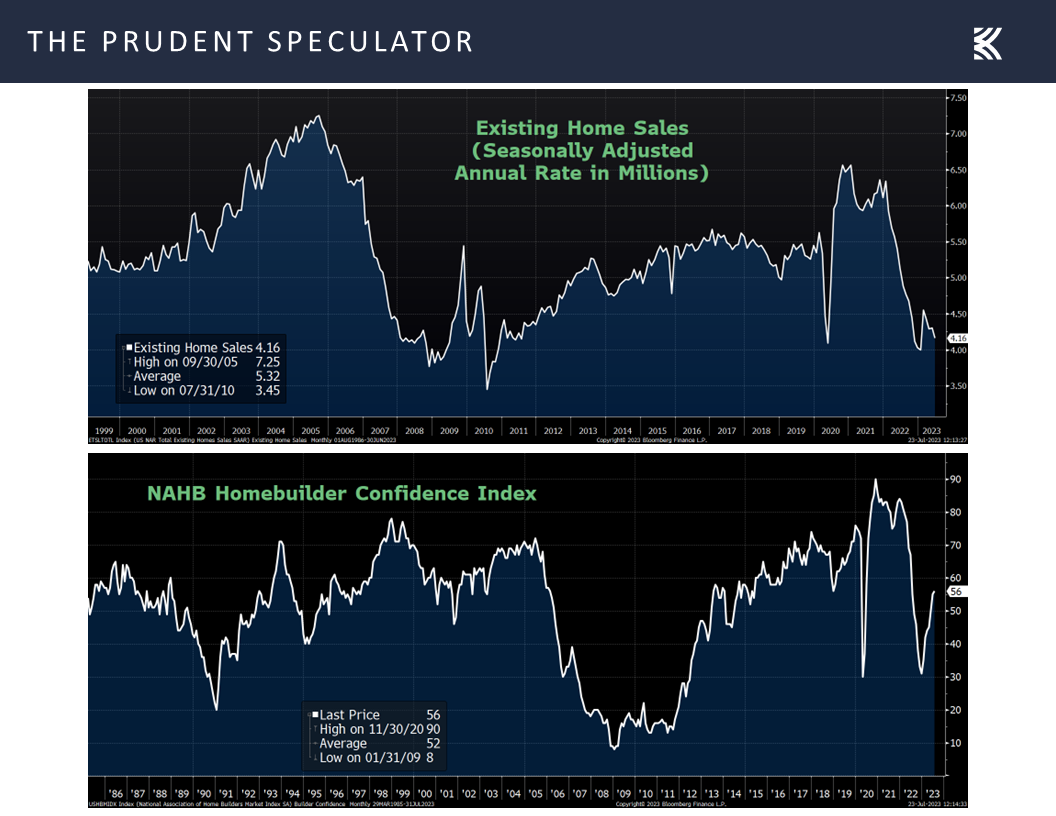

To be sure, the latest data from June on roofs over heads, ranging from existing home sales to homebuilder confidence,

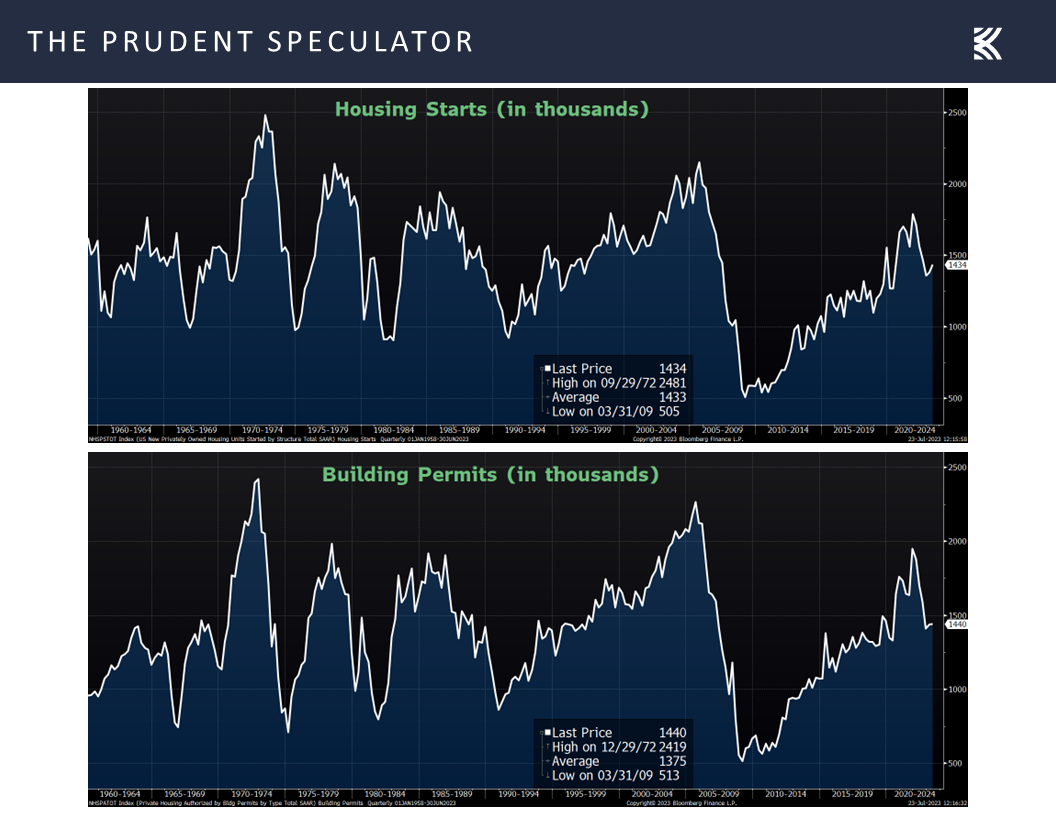

to housing starts and building permits,

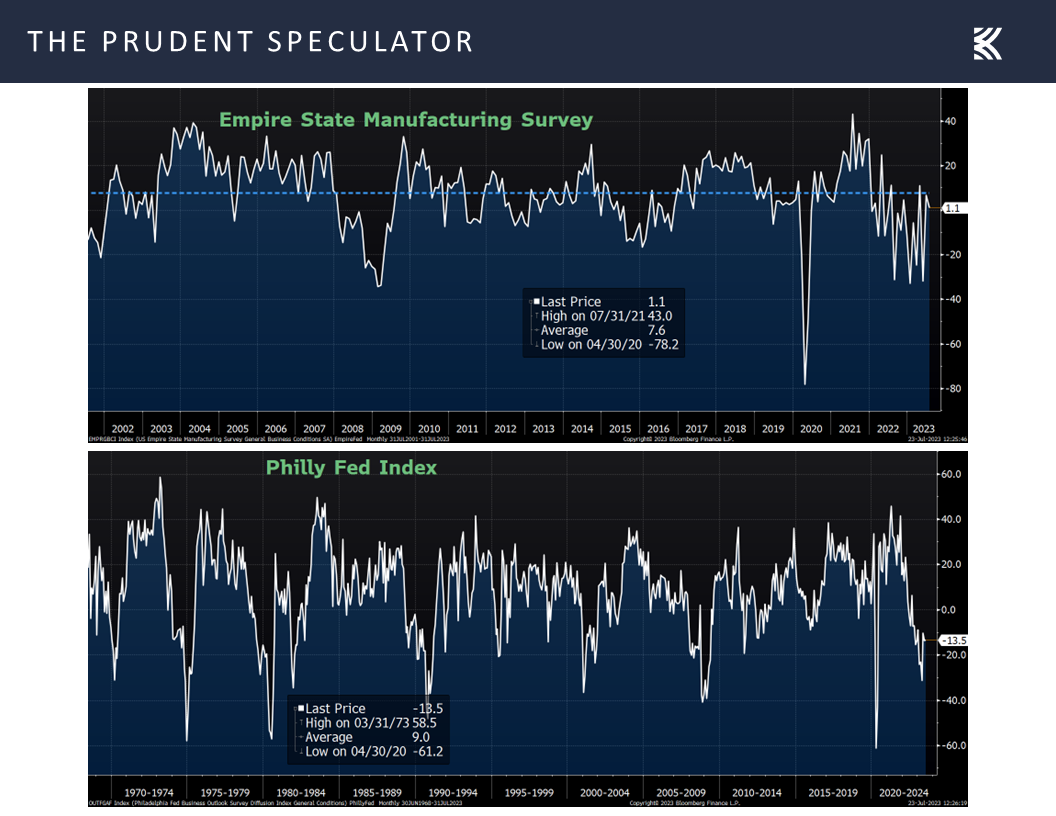

came in below expectations, while the outlook for factory activity on the East Coast was uninspiring, with both the Empire and Philadelphia Fed Manufacturing Survey’s continuing to reside well below their long-term averages.

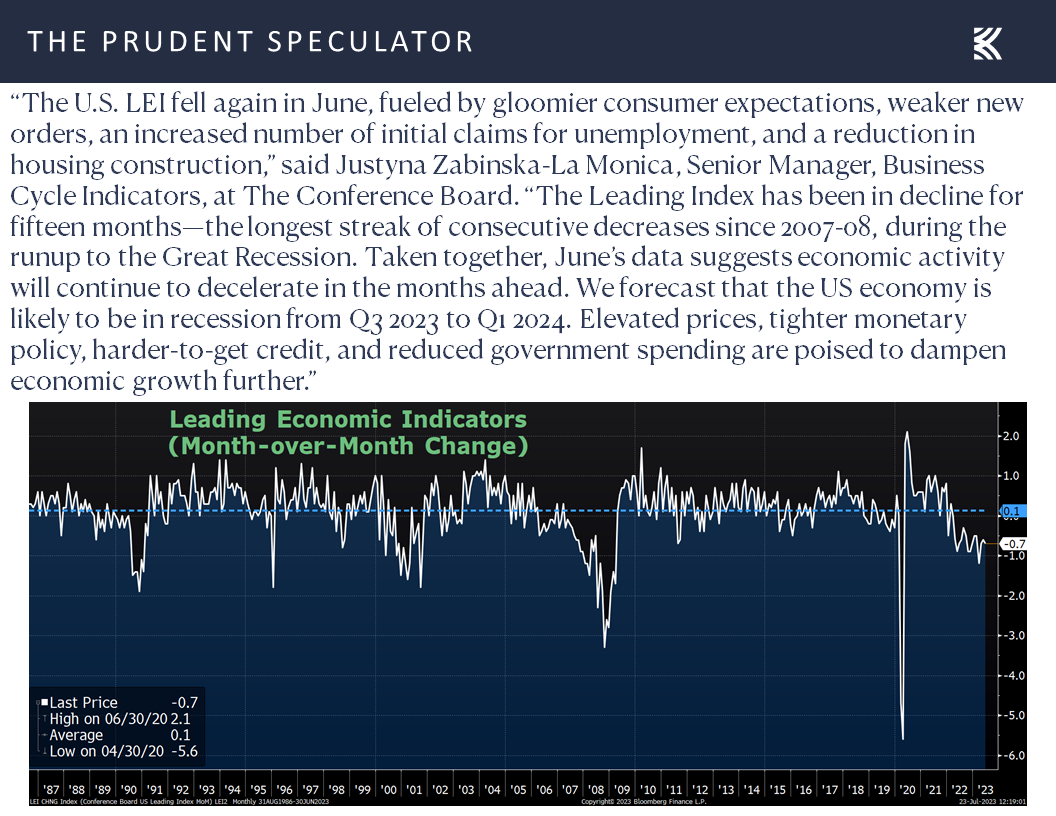

More importantly, perhaps, the widely anticipated monthly Leading Economic Index from the Conference Board remained very weak in July at a minus 0.7% reading, coming in below forecasts of minus 0.6% and arguing that a recession remains on the horizon.

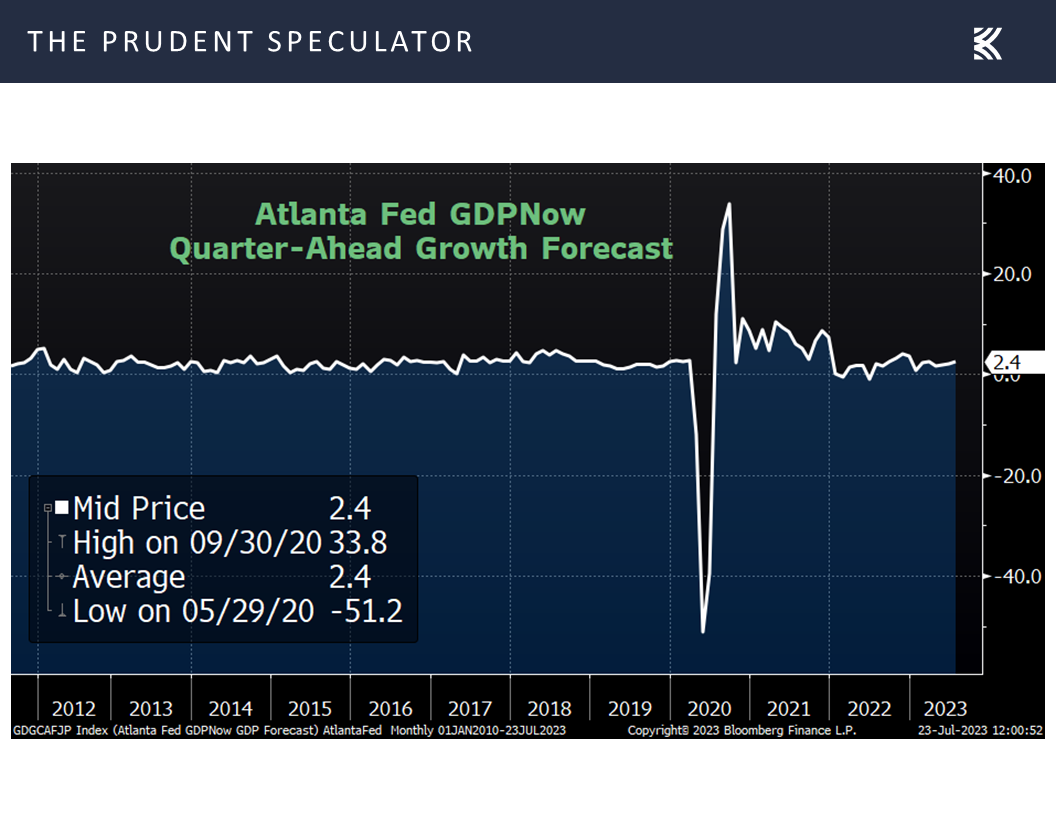

Needless to say, we do not know if two quarters of negative real GDP growth (asserted to be the definition of a recession) will occur, but we note that the current economic prediction from the Atlanta Fed for Q2 growth is 2.4%,

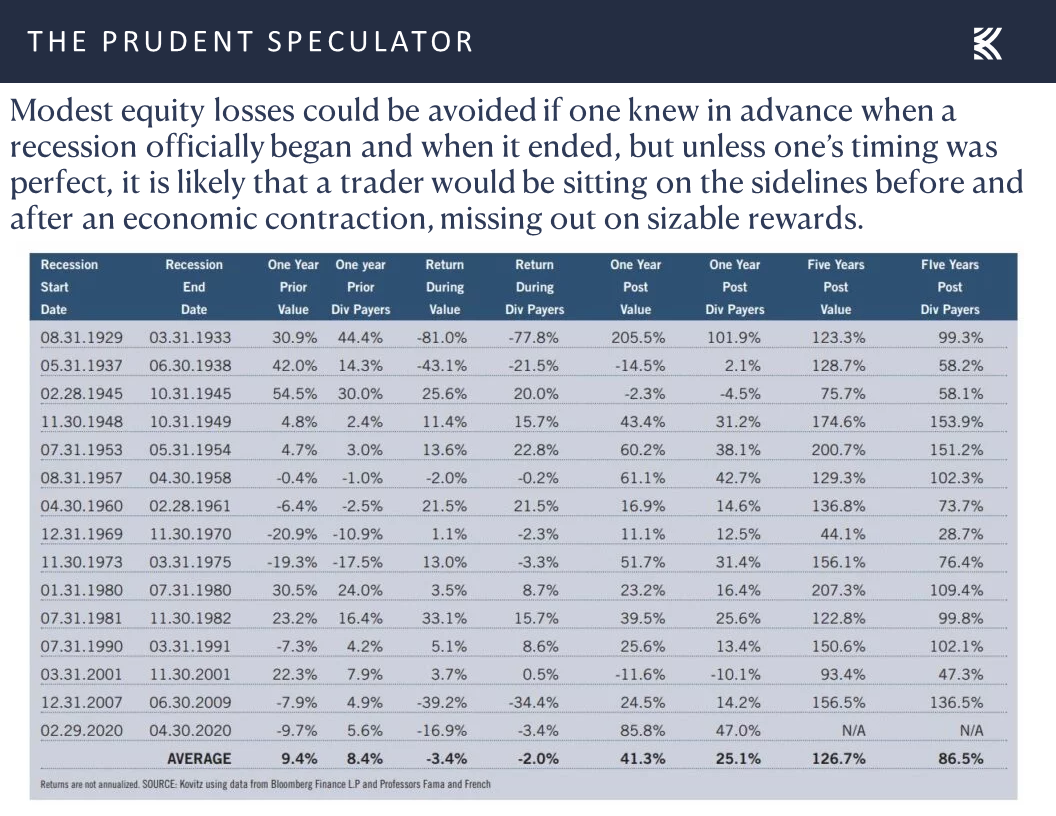

and we continue to assert that there is no historical evidence to suggest that a recession would be reason for those with a multi-year investment time horizon to sell their stocks.

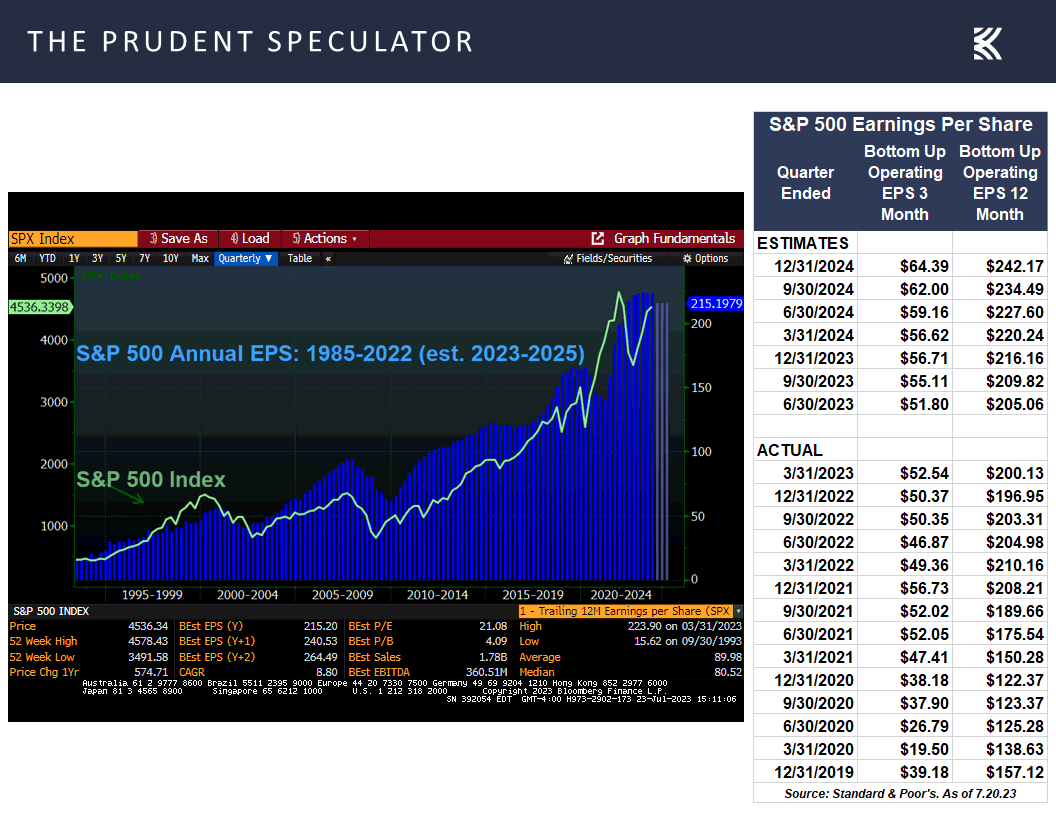

Earnings – Strong Q2 Results; Growth Still the Forecast This Year and in 2024

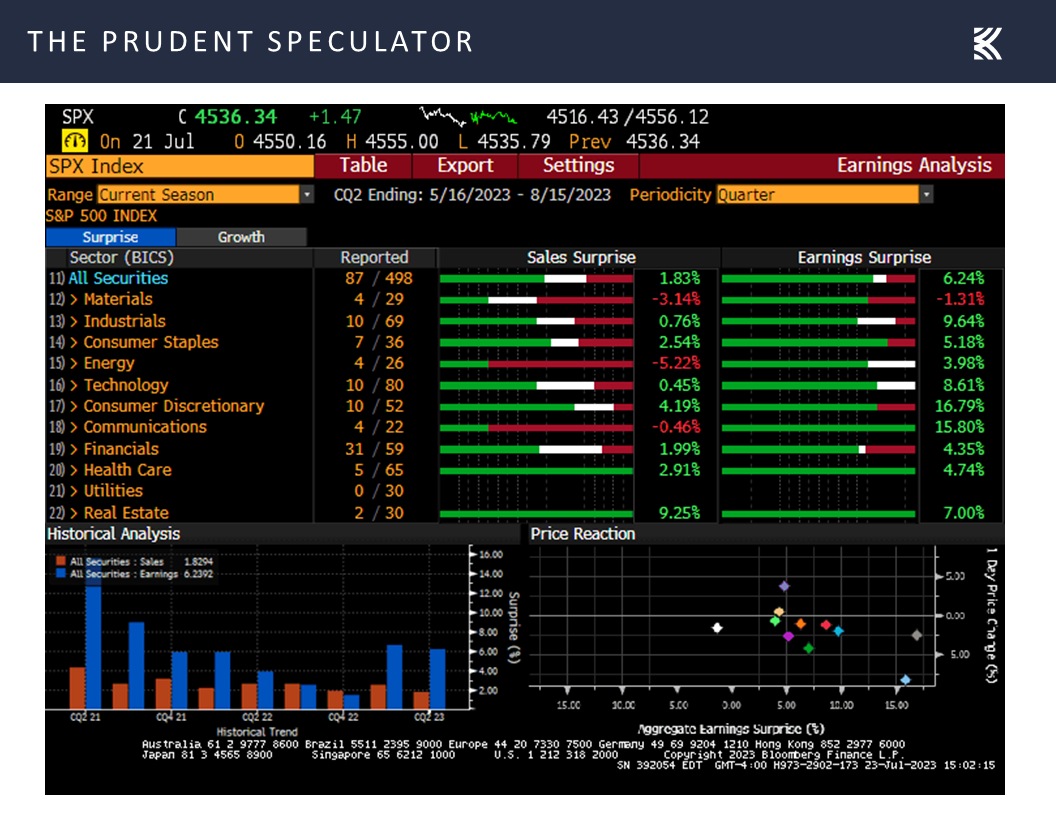

This is especially true as, despite all the economic uncertainty, second quarter corporate profit reports have thus far been very good with 78.2% of the S&P 500 beating bottom-line estimates and 54.0% topping revenue projections.

Further, the outlook for handsome earnings growth this year and in 2024 from both Bloomberg and Standard & Poor’s remains intact, even as we understand that analysts are often rosy in their outlooks.

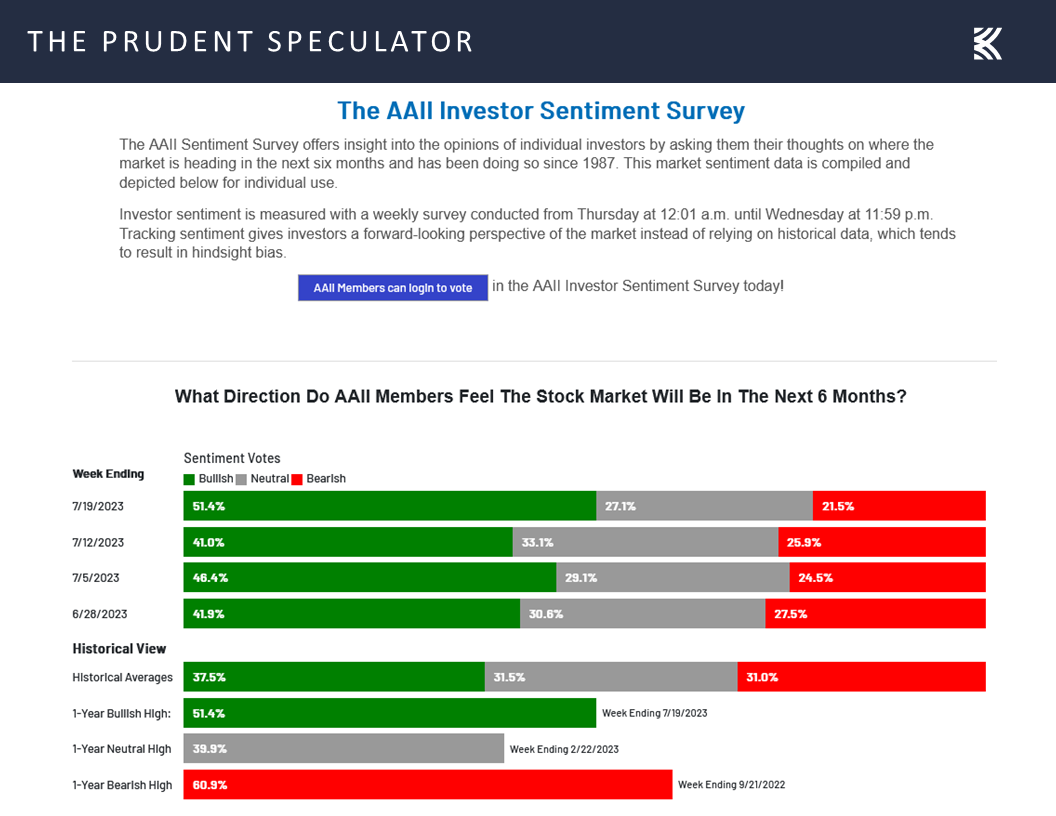

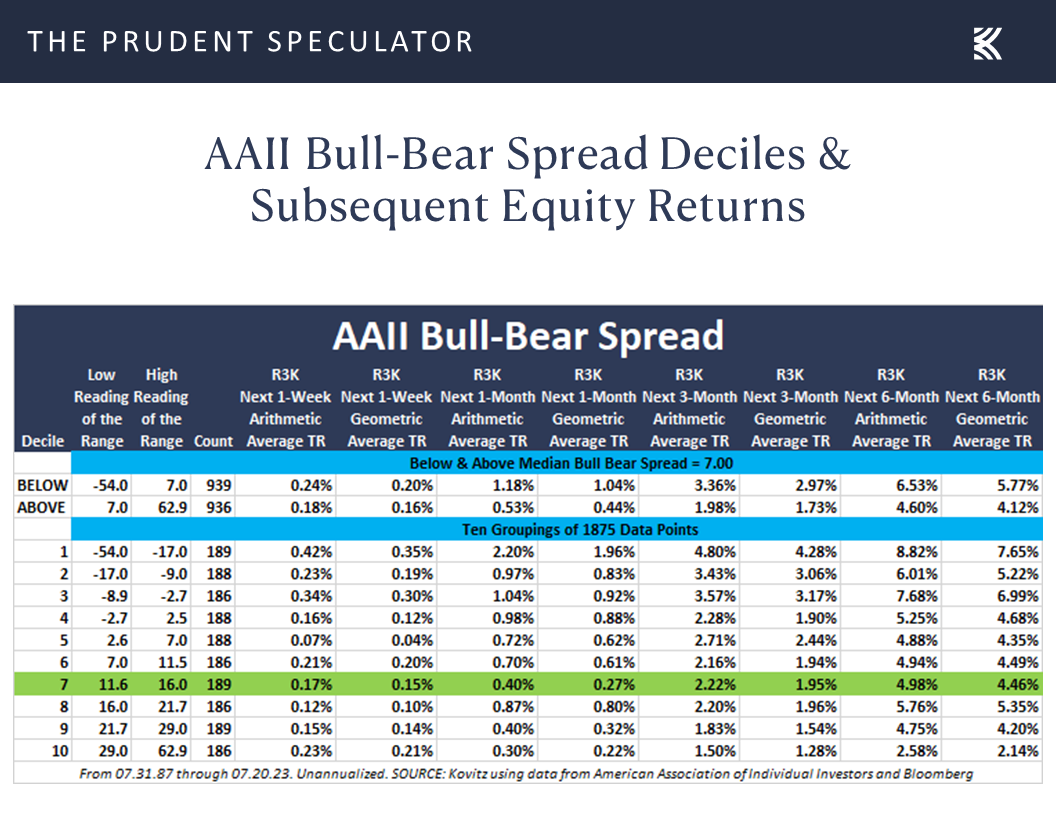

Sentiment – AAII Bullishness is Very Elevated

While we concede that enthusiasm for stocks on Main Street is running hot, with the latest Sentiment Survey from the American Association of Individual Investors (AAII) showing a 29.9-percentage-point gap in favor of the Bulls,

but the contrarian nature of this indicator merely suggests that equity market gains (yes, gains) going forward might be lower on average than usual.

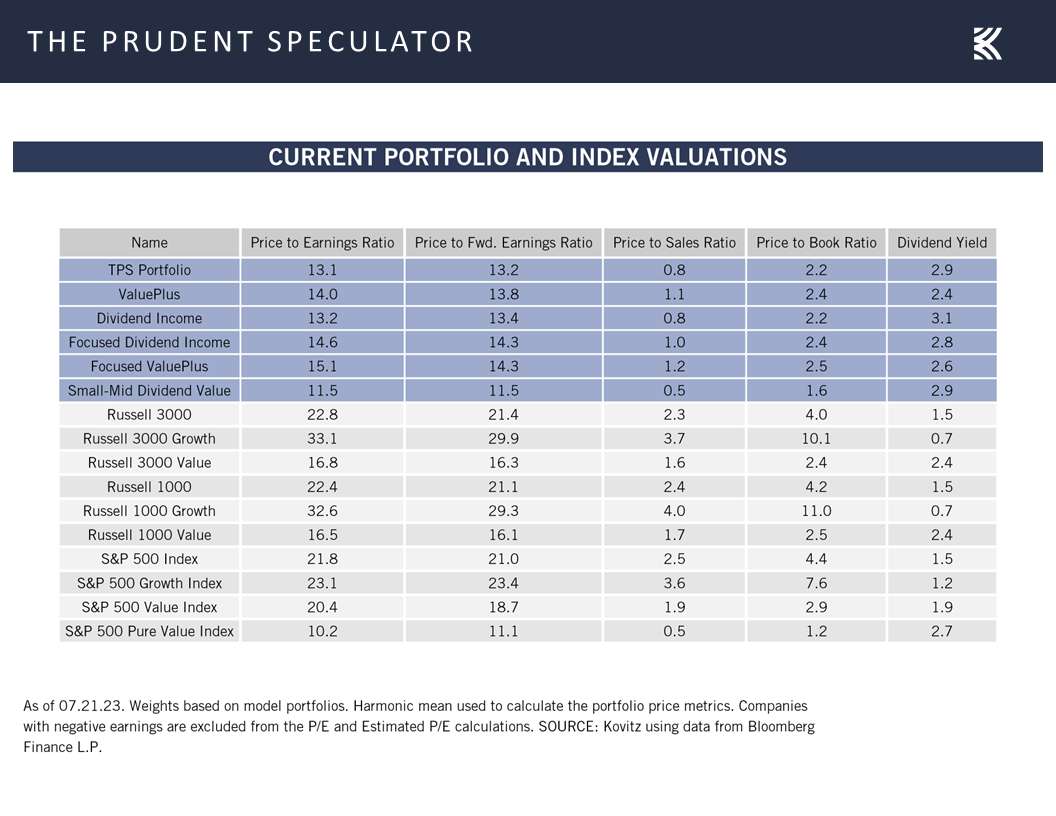

Valuations – Inexpensive Multiples for our Stocks

Indeed, we see no reason to alter our long-term enthusiasm for our broadly diversified portfolios of what we believe to be undervalued stocks,

especially as the equity market overall is still not richly valued, despite the jump in interest rates since the end of 2021,

while the Federal Reserve is arguably nearing the end of its rate-hiking cycle.

Cues from Value, Not From Price – Interesting Moves for VZ & PNC

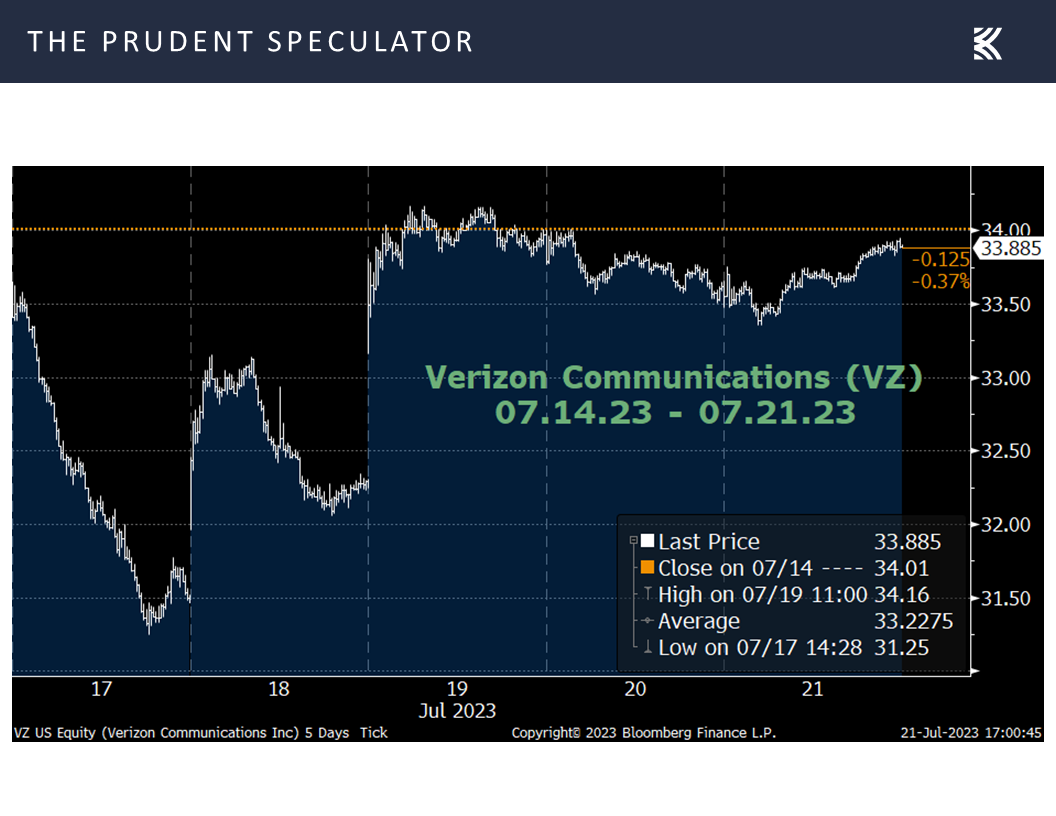

Warren Buffett states, “For some reason people take their cues from price action rather than from values. Price is what you pay. Value is what you get.” Looking at trading last week in telecommunications giant Verizon Communications (VZ – $33.88), we again see that Wall Street analysts often care little about Value and mostly about Price in their upgrade and downgrade decisions.

Even after damage had been inflicted the week prior on already battered shares of VZ and fellow telecom titan AT&T after an extensive investigative report (https://www.wsj.com/articles/lead-cables-telecoms-att-toxic-5b34408b) was published in The Wall Street Journal on July 9, the analyst community waited until Monday, July 17, to decide that the stocks were no longer worthy of their love. The downgrades of ratings and target prices in response to the then-8-day-old lead-sheathing revelation sent the price of Verizon down another 7.5% to lows not seen in nearly 13 years, with one Bloomberg News story warning the following:

Analysts at Oppenheimer estimate that the fallout for the telecommunications sector stemming from the WSJ’s investigation into toxic lead cables won’t be less than $5B and not more than $50B. The analysts say they have a 90% confidence level about that range, adding that it will likely take the form of a class-action settlement. “Much of this is likely already reflected in the stocks, but we think the stocks will continue to suffer in an information vacuum,” they say. They add that the process of litigation and appeals will likely be a decade-plus process.

No doubt, the concerns raised in the Journal piece are not something easily dismissed as no level of lead exposure deemed safe was identified, while the investigation reportedly found elevated levels of lead at “roughly 80% of sediment samples taken next to underwater cables.”

However, none of this had been cause for much alarm prior to the report, with Verizon’s 2022 10-K filing offering no mention in its five pages of Risk Factors. And neither Verizon nor AT&T was compelled to address the report in the days that followed its release. Further, multiple major environmental groups have been aware of these cables for decades with no major wholesale remediation plan enforced or recommended. Moreover, there appears to be no evidence that suggests the telecommunications providers have failed to follow proper procedures in leaving the cables in place.

Of course, given the accelerated plunge in the stock prices, the companies became vocal later Monday and on Tuesday. A Verizon spokesperson said the company’s copper network is composed of less than 540,000 miles of cable and that lead-sheathed cable makes up a “small percentage” of that, while AT&T in an impromptu investor call said less than 10% of its nationwide copper-wire telecom network has lead-clad cables. AT&T laid outs ifs “Framework” for how it is evaluating its lead-sheathing risk and the company released a spirited rebuttal to the Journal story:

https://about.att.com/ecms/dam/pages/legacy-cable/2023-07-18_Calif_Sportfishing_v_Pac_Bell-Defendants_Supplemental_Status_Report.pdf.

The info from AT&T evidently caused a major rethink as stocks of both companies rebounded strongly over the balance of the week, with one Wall Street shop stating, “The [AT&T] framework suggests minimal health risk, minimal cable exposure, minimal financial risk (we estimate $246 million/year), and remedied over many years, if any risk at all.”

Obviously, “minimal” risk is a far cry from the $5 billion to $50 billion Oppenheimer estimate mentioned. While there are differing opinions about the consequences of disturbing equipment (that is no longer in use) versus leaving it in place, we understand that the matter will not be resolved any time soon. Still, we think the punishment meted out to VZ shares of late has been excessive, especially as we do not see any danger at this stage to the robust dividend payout, where the yield now stands at 7.7%.

Certainly, analysts and traders who chose to shoot first and ask questions later in their decision to bail on Verizon will argue that, despite the bounce back, the stock is still off 14% on the year and down significantly from its late-2019 high above $60. Further, the balance sheet has substantial debt, while earnings this year and next are likely to be stagnant.

However, we think substantial value exists, as a forward P/E ratio of 7.3 keeps us very enthused about the long-term total return potential for the stock. This is especially true, given that the S&P 500 Utilities Index, arguably a competing area of investment for income-focused folks, trades for roughly 18 times forward earnings and yields a bit more than 3%. Our Target Price for VZ is now $56, so we will continue to take our cues from the value and not from the price.

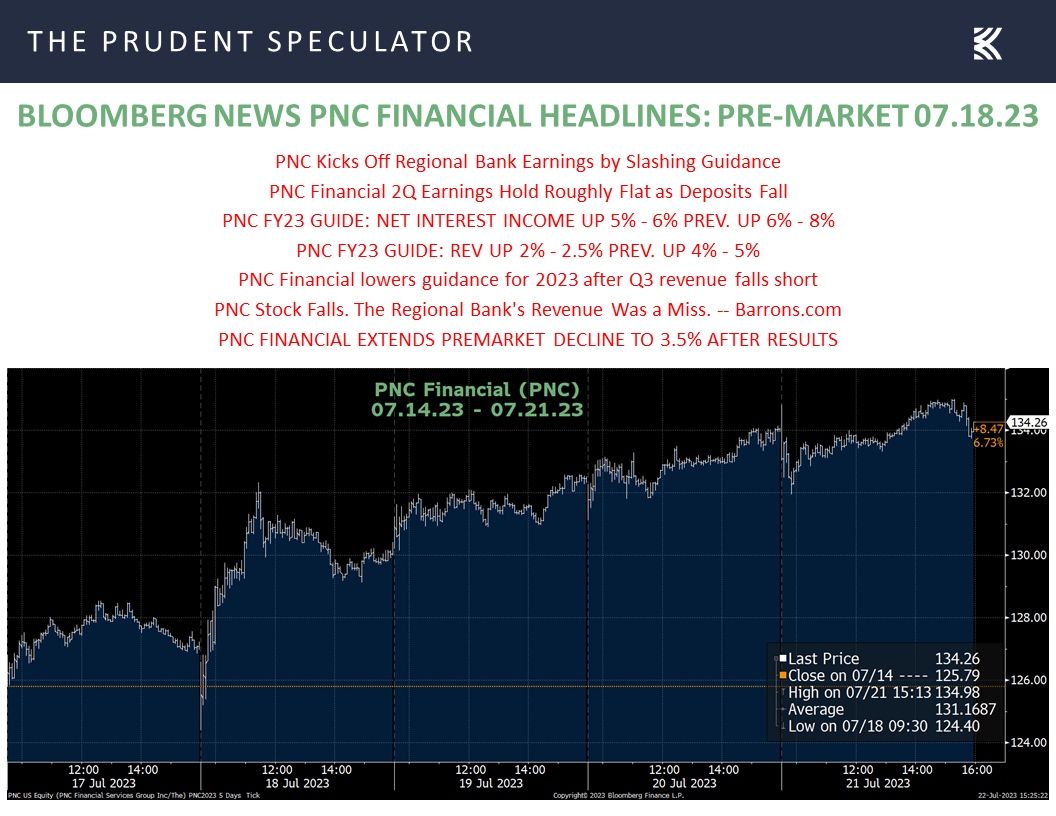

After all, short-term price movements often tell us little about where a stock is headed in the long-term…and we sometimes see how wrong they might be even about the short-term. Case in point, despite the best efforts of the financial news headline writers,

shares of PNC Financial (PNC – $134.26) rose nearly 7% last week after the super-regional bank reported Q2 financial results that were generally in line with expectations and lacked negative surprises that investors arguably hadn’t already discounted in their punishment of the entire regional banking sector this year.

For Q2, PNC said its adjusted EPS came in at $3.36, versus the consensus analyst estimate of $3.27. The quarter benefited from lower credit costs and expenses. Despite fears over banking credit quality, PNC is executing with strength and both delinquencies and nonperforming loans actually are improving. Net interest income fell 2% quarter over quarter, given rising funding costs and modest loan contraction. The bank’s net interest margin endured slight contraction and came in at 2.79%. Despite unavoidable rising funding costs, PNC is still projecting net interest income growth of 5% to 6% for the year.

CEO Bill Demchak said, “For the second quarter, PNC delivered solid financial results and maintained strong credit quality metrics, reflecting the power of our national franchise and the competitive positioning of our balance sheet in the current environment. The Federal Reserve’s annual stress test recently demonstrated PNC’s through-the cycle financial strength and stability, and starting in the fourth quarter, our stress capital buffer requirement will improve to the regulatory minimum of 2.5%. In consideration of our strong capital levels and the board’s confidence in our strategy and outlook, in July the board approved a 5-cent increase to our quarterly stock dividend.”

Looking forward, we expect PNC to benefit from its leading technology, its robust deposit franchise, healthy capital levels and prudent expense management. We also remain constructive on its acquisition of BBVA’s U.S. retail operation in 2021. Yes, we understand that financial results this year may not live up to some optimistic forecasts, but a 15% drop in the share price year-to-date, not to mention last week’s trading action, argues to us that plenty of bad news is “in” the stock price. Those willing to take their cues from Value will like that PNC trades for 11.4 times the current potentially trough NTM EPS estimate and that the yield is a very generous 4.6%. Our Target Price for high-quality PNC is now $191.

Stock News – Updates on eighteen stocks across ten different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Earnings, AAII Sentiment, Valuations and more Economic News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Earnings, AAII Sentiment, Valuations and more Economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week in Review – Lousy Last Two, but Nice Five Days

Patience – The Longer the Hold, The Lower the Chance of Loss

Time in the Market – Best to Ignore Those Who Think Market Timing Works

Prediction is Difficult – Economists Lower Recession Forecasts

Econ News – Mixed Numbers

Earnings – Strong Q2 Results; Growth Still the Forecast This Year and in 2024

Sentiment – AAII Bullishness is Very Elevated

Valuations – Inexpensive Multiples for our Stocks

Cues from Value, Not From Price – Interesting Moves for VZ & PNC

Stock News – Updates on eighteen stocks across ten different sectors

Week in Review – Lousy Last Two, but Nice Five Days

Although the Dow Jones Industrial Average gained ground every day, pushing the daily winning streak for the price-weighted index to 10, the trading week again ended on a sour note, given that the average stock in the broad-based Russell 3000 index declined 1.0% over the Thursday-Friday period.

Happily, as was the case last week, performance looked a whole lot different with a bit longer measuring stick as the average stock, led by those of the Value persuasion, advanced more than 1% for the full five days. Indeed, lengthening the holding period can do wonders as history shows that the longer stocks are held, the greater the chance that they will appreciate in value.

Patience – The Longer the Hold, The Lower the Chance of Loss

As the table below illustrates, if one held Value Stocks for one month, the chance of a positive total return was 63.0%. Hold for 6 months and the odds improved to 70.8% but go out three years and the green ink percentage rose to 87.5%. Even better for those of us with a true long-term time horizon, the change of losing money in Value has been just 3.3% for all 10-year holding periods and 0% for all 15-year periods!

Time in the Market – Best to Ignore Those Who Think Market Timing Works

Of course, we realize that it is not always easy to keep the faith, so we constantly publish empirical evidence to illustrate that the secret to success in stocks is not to get scared out of them,

while we do our best to remind investors that just because a prominent investment professional is provided plenty of airtime in the financial press does not mean that his or her prognostications will come true, as we saw last fall,

and seemingly again a couple of months ago.

We might be accused of cherry-picking, but the doom-and-gloom chorus often sings loudest and garners the most attention from the media at precisely the wrong time. Obviously, there is plenty of ball to be played in this year’s banking drama, but as yet there has been no systemic flight of deposits, despite arguments from the fellow above (who might have a bias or two against stocks) to the contrary.

Unfortunately, many succumb to the siren song of market timing, even as plenty of data supports the argument that the only problem with market timing is getting the timing right. Interestingly, fixed income traders have worse luck than those who try to time their moves into and out of stocks, at least according to analytics compiled by DALBAR Inc. on mutual fund flows over the last three decades.

Prediction is Difficult – Economists Lower Recession Forecasts

While the noted economist Paul Samuelson said, “The stock market has predicted nine of the last five recessions,” it would seem that economists themselves also aren’t very good at forecasting!

Econ News – Mixed Numbers

After all, the supposed experts have been calling for a U.S. recession for nearly a year now, but last week they hedged their bets a bit, with Bloomberg calculations today suggesting “only” a 60% chance of an economic contraction, down from 65% for much of 2023.

That lower probability is in keeping with comments from Bank of America (BAC – $31.98) CEO Brian Moynihan who said last week, “We continue to see a healthy U.S. economy that is growing at a slower pace, with a resilient job market.” Illustrating the labor point, first-time filings for unemployment benefits in the latest week fell to a historically very low 228,000, fewer than expected and down from 237,000 in the week prior.

Bank of America CFO Alastair Borthwick added, “The overall health of the U.S. consumer remained strong,” which was supported by the report last week of a solid 0.2% increase in overall retail sales in June.

To be sure, the latest data from June on roofs over heads, ranging from existing home sales to homebuilder confidence,

to housing starts and building permits,

came in below expectations, while the outlook for factory activity on the East Coast was uninspiring, with both the Empire and Philadelphia Fed Manufacturing Survey’s continuing to reside well below their long-term averages.

More importantly, perhaps, the widely anticipated monthly Leading Economic Index from the Conference Board remained very weak in July at a minus 0.7% reading, coming in below forecasts of minus 0.6% and arguing that a recession remains on the horizon.

Needless to say, we do not know if two quarters of negative real GDP growth (asserted to be the definition of a recession) will occur, but we note that the current economic prediction from the Atlanta Fed for Q2 growth is 2.4%,

and we continue to assert that there is no historical evidence to suggest that a recession would be reason for those with a multi-year investment time horizon to sell their stocks.

Earnings – Strong Q2 Results; Growth Still the Forecast This Year and in 2024

This is especially true as, despite all the economic uncertainty, second quarter corporate profit reports have thus far been very good with 78.2% of the S&P 500 beating bottom-line estimates and 54.0% topping revenue projections.

Further, the outlook for handsome earnings growth this year and in 2024 from both Bloomberg and Standard & Poor’s remains intact, even as we understand that analysts are often rosy in their outlooks.

Sentiment – AAII Bullishness is Very Elevated

While we concede that enthusiasm for stocks on Main Street is running hot, with the latest Sentiment Survey from the American Association of Individual Investors (AAII) showing a 29.9-percentage-point gap in favor of the Bulls,

but the contrarian nature of this indicator merely suggests that equity market gains (yes, gains) going forward might be lower on average than usual.

Valuations – Inexpensive Multiples for our Stocks

Indeed, we see no reason to alter our long-term enthusiasm for our broadly diversified portfolios of what we believe to be undervalued stocks,

especially as the equity market overall is still not richly valued, despite the jump in interest rates since the end of 2021,

while the Federal Reserve is arguably nearing the end of its rate-hiking cycle.

Cues from Value, Not From Price – Interesting Moves for VZ & PNC

Warren Buffett states, “For some reason people take their cues from price action rather than from values. Price is what you pay. Value is what you get.” Looking at trading last week in telecommunications giant Verizon Communications (VZ – $33.88), we again see that Wall Street analysts often care little about Value and mostly about Price in their upgrade and downgrade decisions.

Even after damage had been inflicted the week prior on already battered shares of VZ and fellow telecom titan AT&T after an extensive investigative report (https://www.wsj.com/articles/lead-cables-telecoms-att-toxic-5b34408b) was published in The Wall Street Journal on July 9, the analyst community waited until Monday, July 17, to decide that the stocks were no longer worthy of their love. The downgrades of ratings and target prices in response to the then-8-day-old lead-sheathing revelation sent the price of Verizon down another 7.5% to lows not seen in nearly 13 years, with one Bloomberg News story warning the following:

Analysts at Oppenheimer estimate that the fallout for the telecommunications sector stemming from the WSJ’s investigation into toxic lead cables won’t be less than $5B and not more than $50B. The analysts say they have a 90% confidence level about that range, adding that it will likely take the form of a class-action settlement. “Much of this is likely already reflected in the stocks, but we think the stocks will continue to suffer in an information vacuum,” they say. They add that the process of litigation and appeals will likely be a decade-plus process.

No doubt, the concerns raised in the Journal piece are not something easily dismissed as no level of lead exposure deemed safe was identified, while the investigation reportedly found elevated levels of lead at “roughly 80% of sediment samples taken next to underwater cables.”

However, none of this had been cause for much alarm prior to the report, with Verizon’s 2022 10-K filing offering no mention in its five pages of Risk Factors. And neither Verizon nor AT&T was compelled to address the report in the days that followed its release. Further, multiple major environmental groups have been aware of these cables for decades with no major wholesale remediation plan enforced or recommended. Moreover, there appears to be no evidence that suggests the telecommunications providers have failed to follow proper procedures in leaving the cables in place.

Of course, given the accelerated plunge in the stock prices, the companies became vocal later Monday and on Tuesday. A Verizon spokesperson said the company’s copper network is composed of less than 540,000 miles of cable and that lead-sheathed cable makes up a “small percentage” of that, while AT&T in an impromptu investor call said less than 10% of its nationwide copper-wire telecom network has lead-clad cables. AT&T laid outs ifs “Framework” for how it is evaluating its lead-sheathing risk and the company released a spirited rebuttal to the Journal story:

https://about.att.com/ecms/dam/pages/legacy-cable/2023-07-18_Calif_Sportfishing_v_Pac_Bell-Defendants_Supplemental_Status_Report.pdf.

The info from AT&T evidently caused a major rethink as stocks of both companies rebounded strongly over the balance of the week, with one Wall Street shop stating, “The [AT&T] framework suggests minimal health risk, minimal cable exposure, minimal financial risk (we estimate $246 million/year), and remedied over many years, if any risk at all.”

Obviously, “minimal” risk is a far cry from the $5 billion to $50 billion Oppenheimer estimate mentioned. While there are differing opinions about the consequences of disturbing equipment (that is no longer in use) versus leaving it in place, we understand that the matter will not be resolved any time soon. Still, we think the punishment meted out to VZ shares of late has been excessive, especially as we do not see any danger at this stage to the robust dividend payout, where the yield now stands at 7.7%.

Certainly, analysts and traders who chose to shoot first and ask questions later in their decision to bail on Verizon will argue that, despite the bounce back, the stock is still off 14% on the year and down significantly from its late-2019 high above $60. Further, the balance sheet has substantial debt, while earnings this year and next are likely to be stagnant.

However, we think substantial value exists, as a forward P/E ratio of 7.3 keeps us very enthused about the long-term total return potential for the stock. This is especially true, given that the S&P 500 Utilities Index, arguably a competing area of investment for income-focused folks, trades for roughly 18 times forward earnings and yields a bit more than 3%. Our Target Price for VZ is now $56, so we will continue to take our cues from the value and not from the price.

After all, short-term price movements often tell us little about where a stock is headed in the long-term…and we sometimes see how wrong they might be even about the short-term. Case in point, despite the best efforts of the financial news headline writers,

shares of PNC Financial (PNC – $134.26) rose nearly 7% last week after the super-regional bank reported Q2 financial results that were generally in line with expectations and lacked negative surprises that investors arguably hadn’t already discounted in their punishment of the entire regional banking sector this year.

For Q2, PNC said its adjusted EPS came in at $3.36, versus the consensus analyst estimate of $3.27. The quarter benefited from lower credit costs and expenses. Despite fears over banking credit quality, PNC is executing with strength and both delinquencies and nonperforming loans actually are improving. Net interest income fell 2% quarter over quarter, given rising funding costs and modest loan contraction. The bank’s net interest margin endured slight contraction and came in at 2.79%. Despite unavoidable rising funding costs, PNC is still projecting net interest income growth of 5% to 6% for the year.

CEO Bill Demchak said, “For the second quarter, PNC delivered solid financial results and maintained strong credit quality metrics, reflecting the power of our national franchise and the competitive positioning of our balance sheet in the current environment. The Federal Reserve’s annual stress test recently demonstrated PNC’s through-the cycle financial strength and stability, and starting in the fourth quarter, our stress capital buffer requirement will improve to the regulatory minimum of 2.5%. In consideration of our strong capital levels and the board’s confidence in our strategy and outlook, in July the board approved a 5-cent increase to our quarterly stock dividend.”

Looking forward, we expect PNC to benefit from its leading technology, its robust deposit franchise, healthy capital levels and prudent expense management. We also remain constructive on its acquisition of BBVA’s U.S. retail operation in 2021. Yes, we understand that financial results this year may not live up to some optimistic forecasts, but a 15% drop in the share price year-to-date, not to mention last week’s trading action, argues to us that plenty of bad news is “in” the stock price. Those willing to take their cues from Value will like that PNC trades for 11.4 times the current potentially trough NTM EPS estimate and that the yield is a very generous 4.6%. Our Target Price for high-quality PNC is now $191.

Stock News – Updates on eighteen stocks across ten different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.