The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Economic Data, Federal Reserve, Interest Rates and Seasonality. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Week In Review – Stocks Rally, Despite Escalation of Ukraine/Russia Hostilities

Econ Data – Mixed Numbers; Solid GDP Growth Still the Forecast

Corporate Profits – EPS Estimates Increase Slightly

Fed Speak – Still Data Dependent; Odds of Fed Rate Cuts Dampen

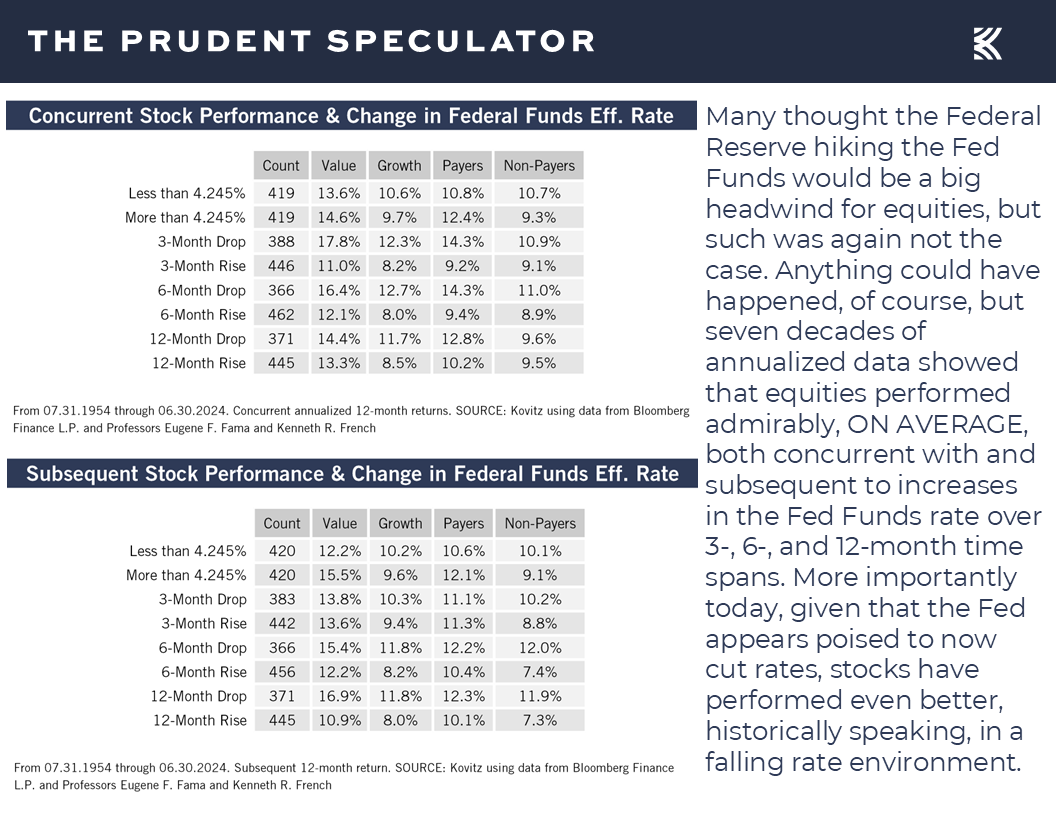

Interest Rates – Stocks Have Performed Fine Whether Fed is Easing/Tightening or 10-Year Yield is Rising/Falling

Valuations – Value Stocks Reasonably Priced

Seasonality – Most Wonderful Time of the Year

Sentiment – Bullishness Pulls Back

Stock News – Updates on GOOG, QCOM, MDT, ADM, TGT, DE, NTAP, LOW & WMT

Week In Review – Stocks Rally, Despite Escalation of Ukraine/Russia Hostilities

Providing another reminder that despite numerous bouts of downside volatility, handsome long-term rewards are available to those who stick with stocks,

the major equity market averages ended a roller-coaster of a trading week at or near all-time highs, even as the confrontation between Russia and Ukraine seemingly entered a more disconcerting phase,

Econ Data – Mixed Numbers; Solid GDP Growth Still the Forecast

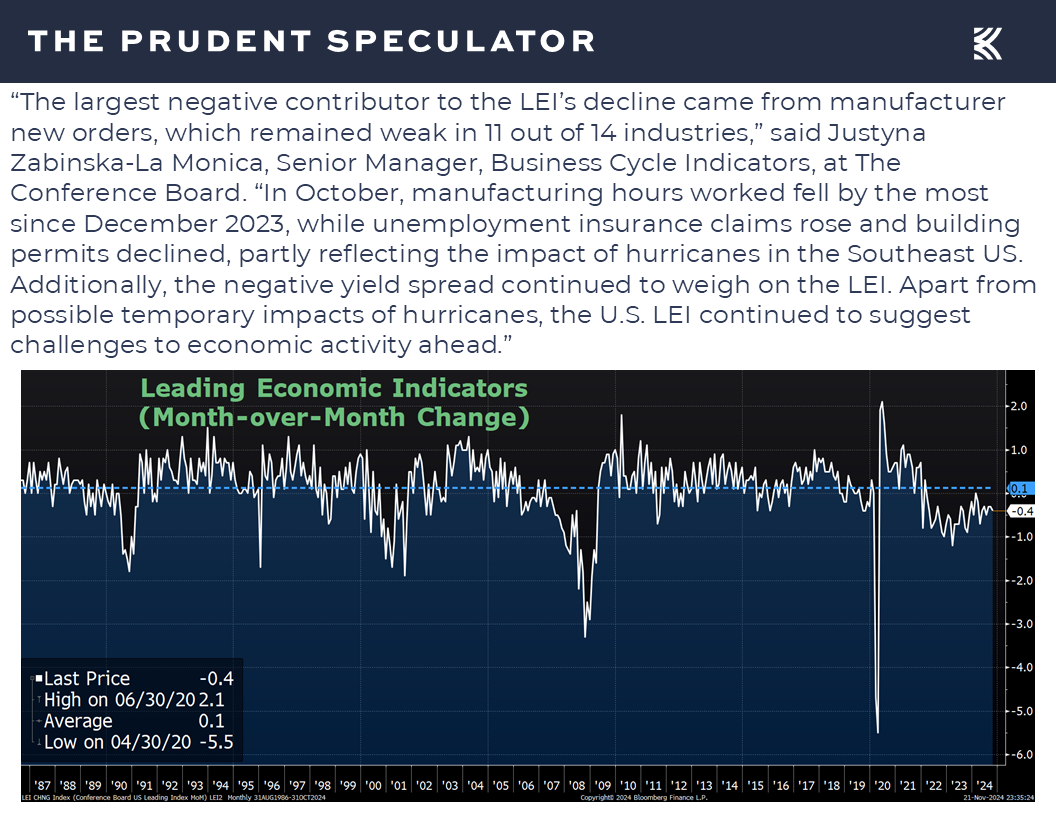

and the latest economic data was more negative than positive, with the forward-looking Leading Economic Index from the Conference Board coming in below expectations with a 0.4% decline in October.

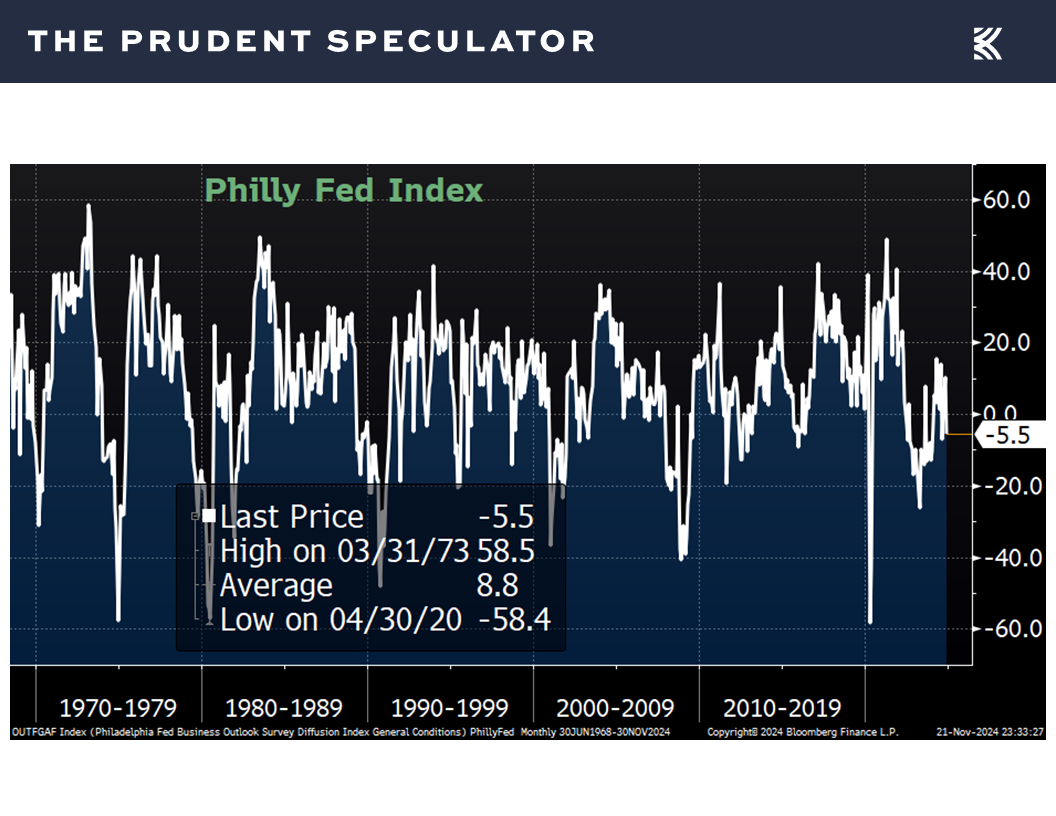

The Conference Board cited weakness in manufacturing, which was confirmed by the Philadelphia Fed’s gauge of East Coast factory activity for November dropping to a reading of -5.5, well below projections of 8.0.

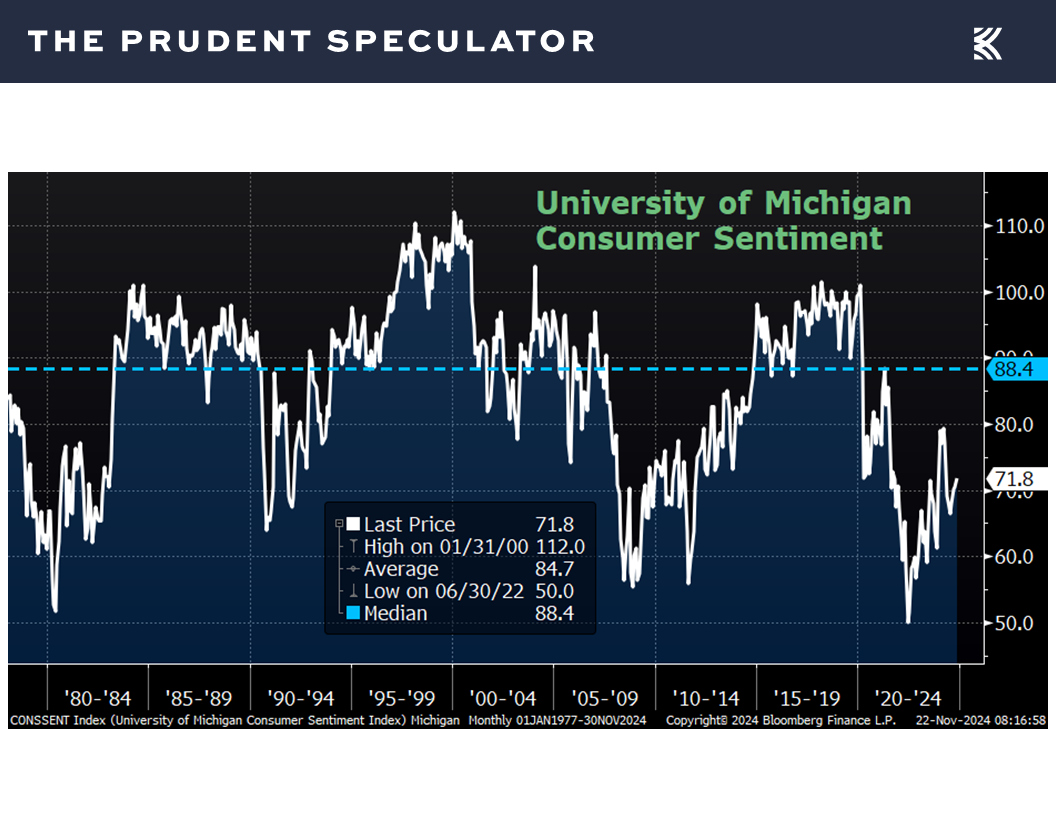

We also learned that the final tally of consumer confidence for November from the Univ. of Michigan declined to 71.8, down from 73.0 in October and below forecasts of 73.9,

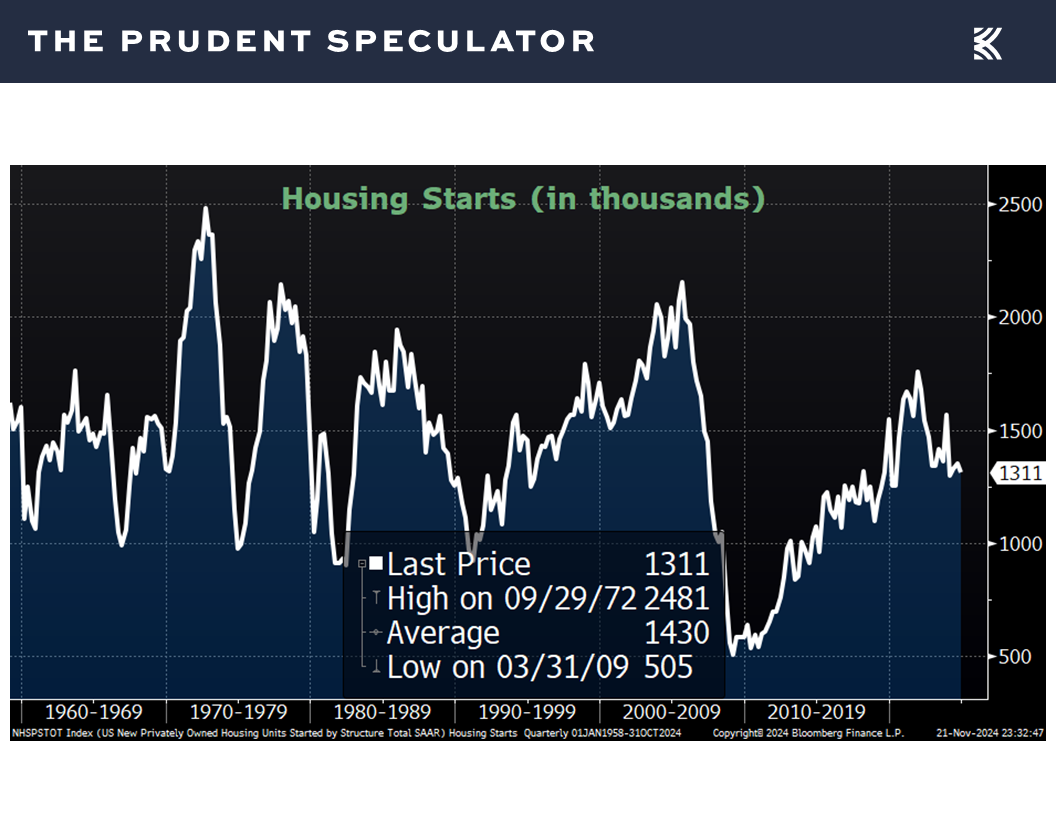

and that housing starts fell to 1.311 million in October, down from a revised 1.353 million the month prior and below the consensus estimate of 1.334 million.

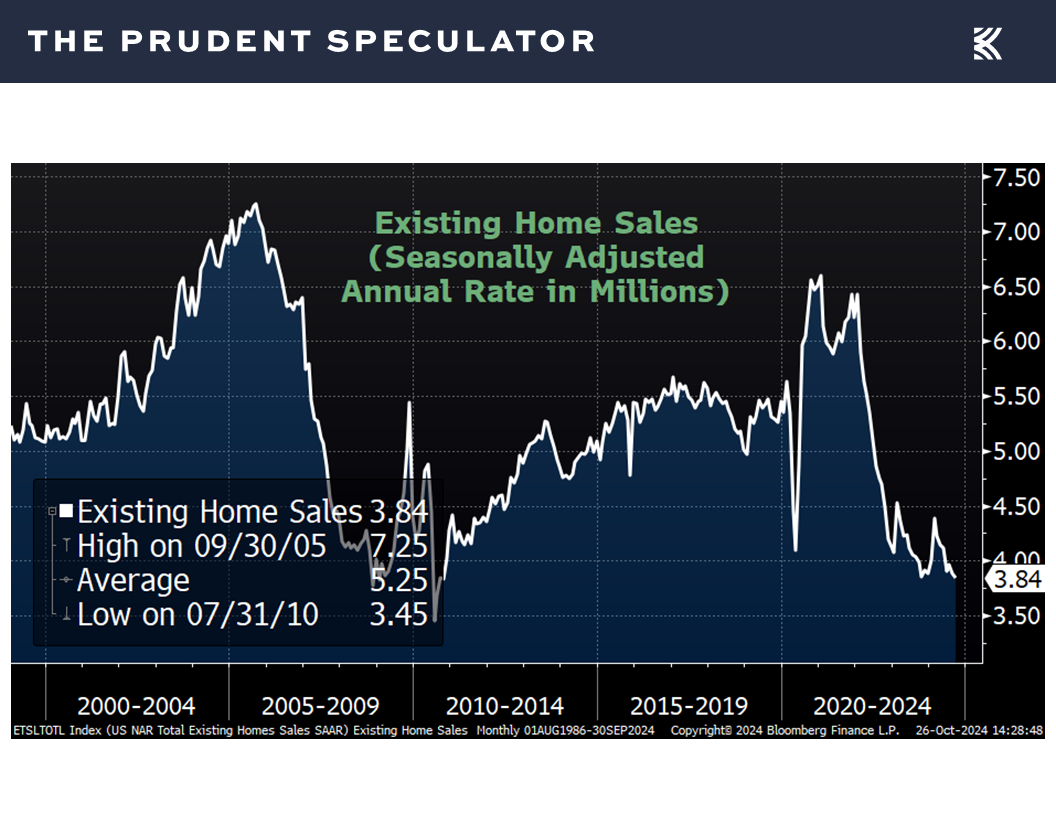

On the other hand, sales of existing homes for October climbed to a slightly better than expected 3.96 million,

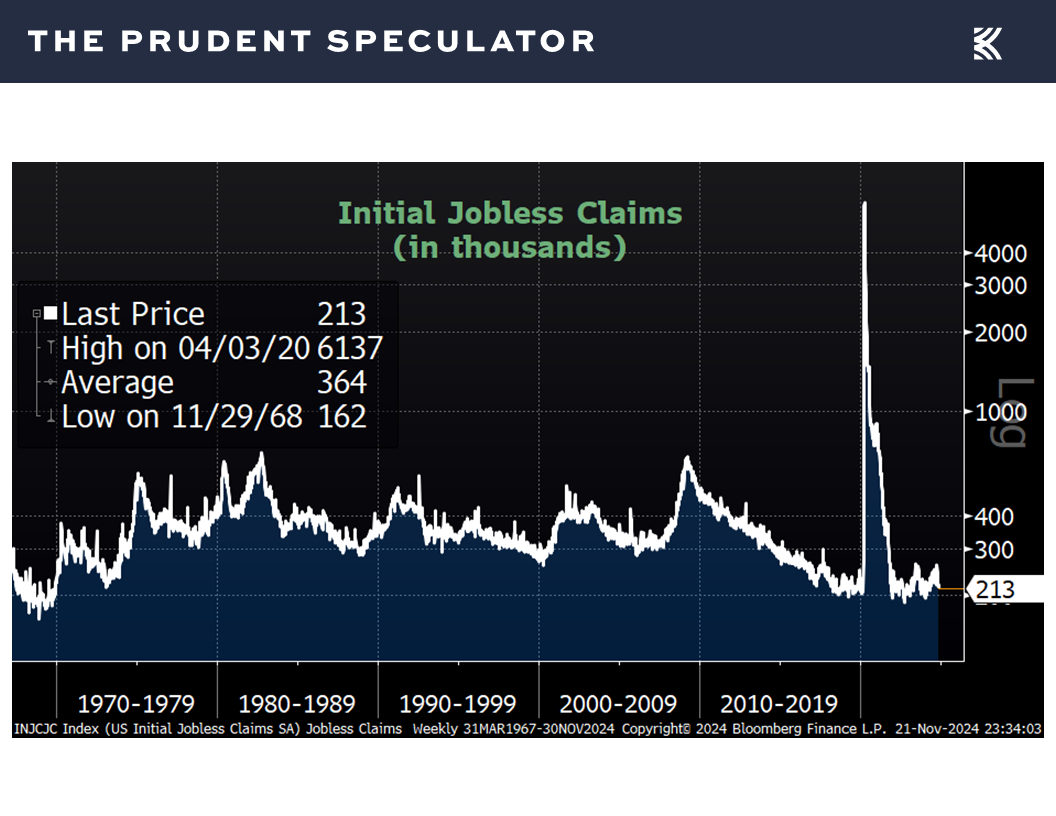

first-time filings for unemployment benefits of 213,000 in the latest week was lower than the 220,000 projection and continued to reside near multi-generational lows,

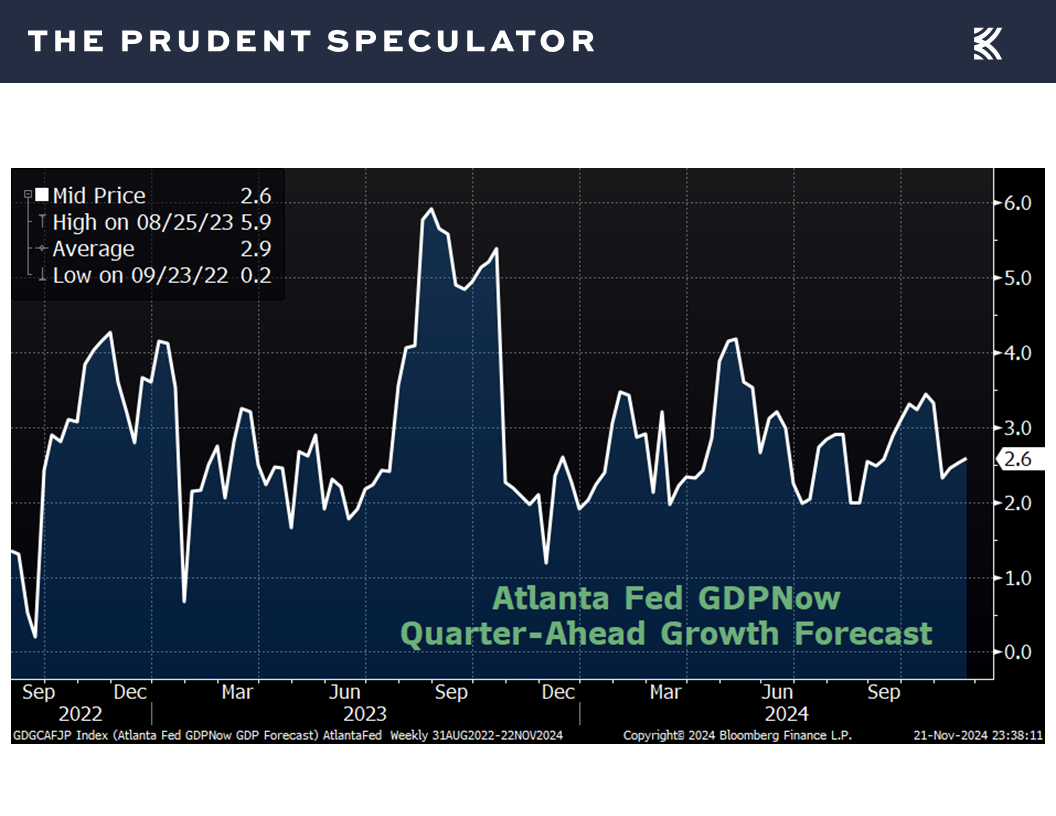

and the latest estimate for Q4 real (inflation-adjusted) U.S. GDP growth inched up to a solid 2.6%,

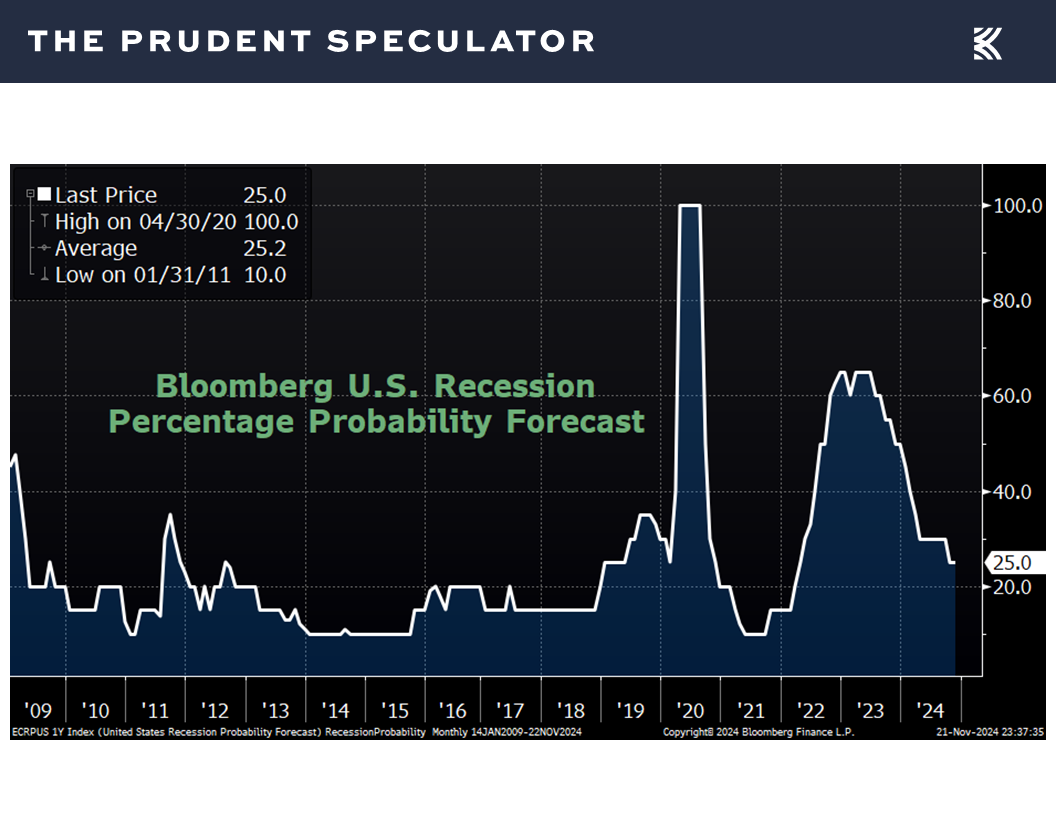

and the odds of recession in the next 12 months, as tabulated by data provider Bloomberg, held steady at a very low 25%.

Corporate Profits – EPS Estimates Increase Slightly

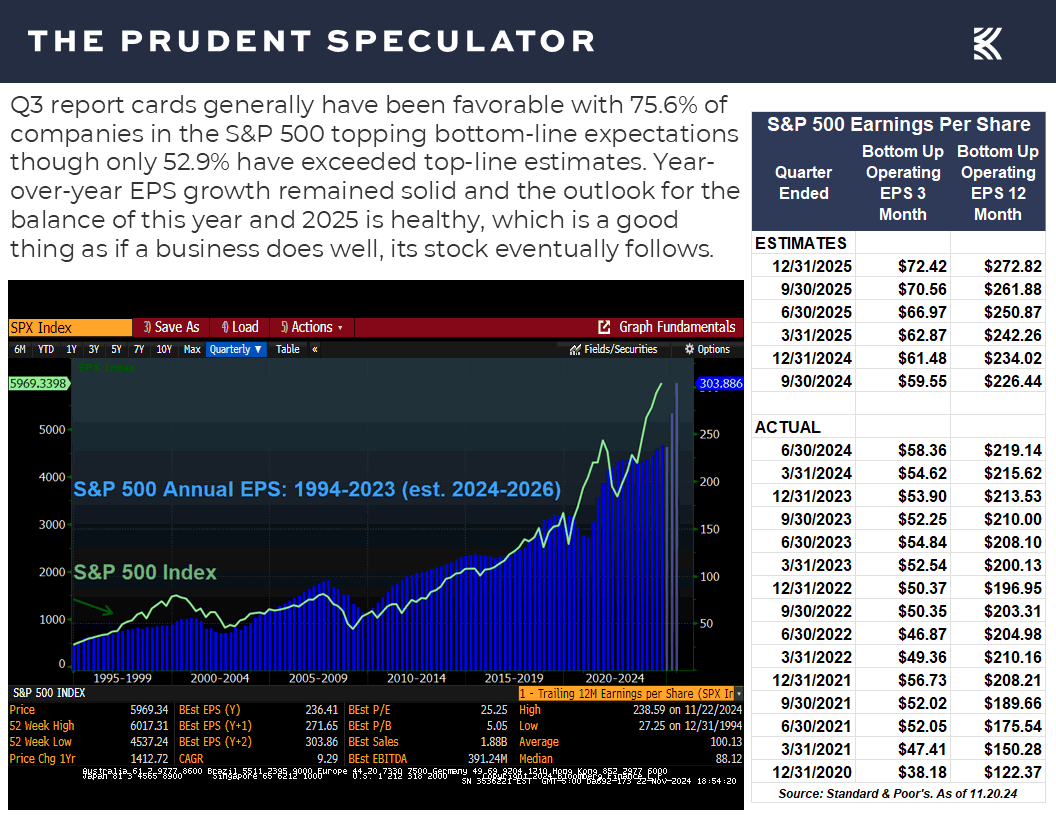

Despite the arguably mixed picture on the economic front, the outlook for corporate profit growth, which historically has been the driver of higher stock prices, improved a tad, at least according to the latest estimates for the S&P 500 offered by Standard & Poor’s,

Fed Speak – Still Data Dependent; Odds of Fed Rate Cuts Dampen

though it seemed a good deal of the financial market news last week was centered on comments from Federal Reserve officials about the prospects for additional interest rate cuts.

Boston Fed President Susan Collins said, “While the final destination is uncertain, I believe some additional policy easing is needed, as policy currently remains at least somewhat restrictive.”

However, Fed Governor Michelle Bowman stated, “I would prefer to proceed cautiously in bringing the policy rate down to better assess how far we are from the end point, while recognizing that we have not yet achieved our inflation goal and closely watching the evolution of the labor market.”

And Kansas City Fed President Jeffrey Schmid added, “While now is the time to begin dialing back the restrictiveness of monetary policy, it remains to be seen how much further interest rates will decline or where they might eventually settle.”

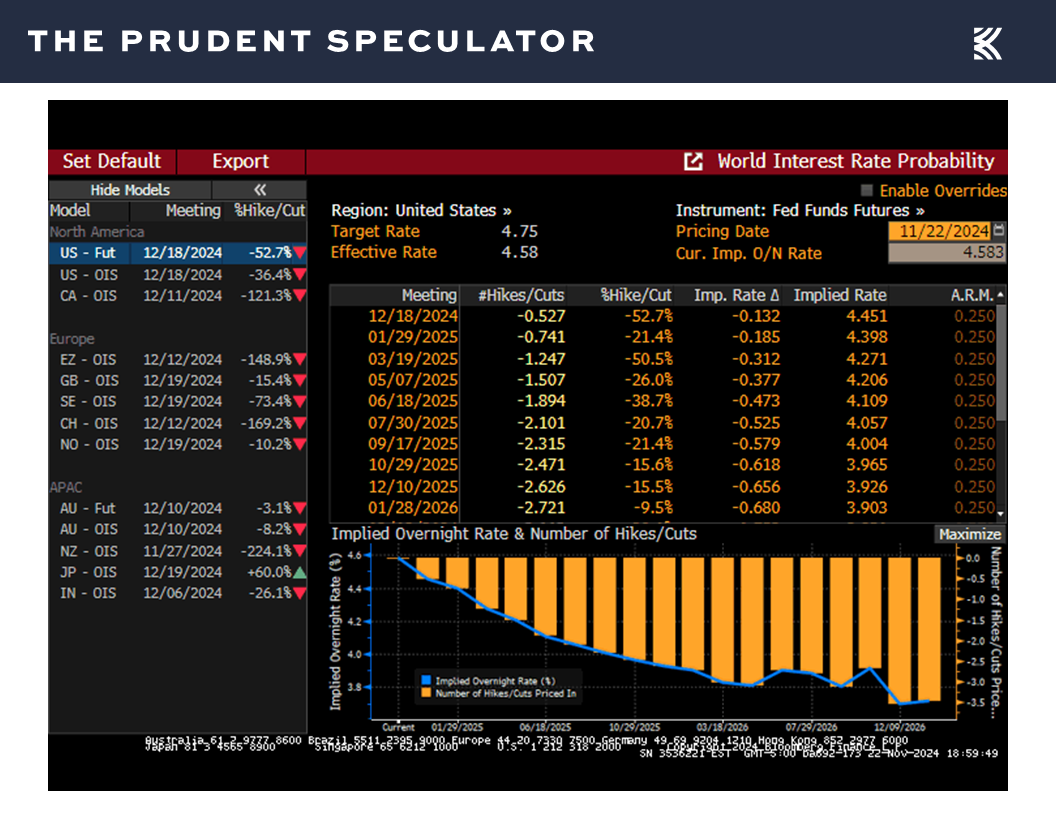

No doubt, Jerome H. Powell & Co. will remain data dependent as they consider additional cuts in the Fed Funds rate, but the players in the futures market were wagering on a bit less easing of monetary policy than at the end of the week prior, with the current betting for the respective year-end ’24 and ’25 rates ticking up to 4.45% and 3.93%,

above the projections offered by the Fed two months ago.

Of course, stocks have performed fine, on average, whether the Fed is raising or lowering interest rates,

Interest Rates – Stocks Have Performed Fine Whether Fed is Easing/Tightening or 10-Year Yield is Rising/Falling

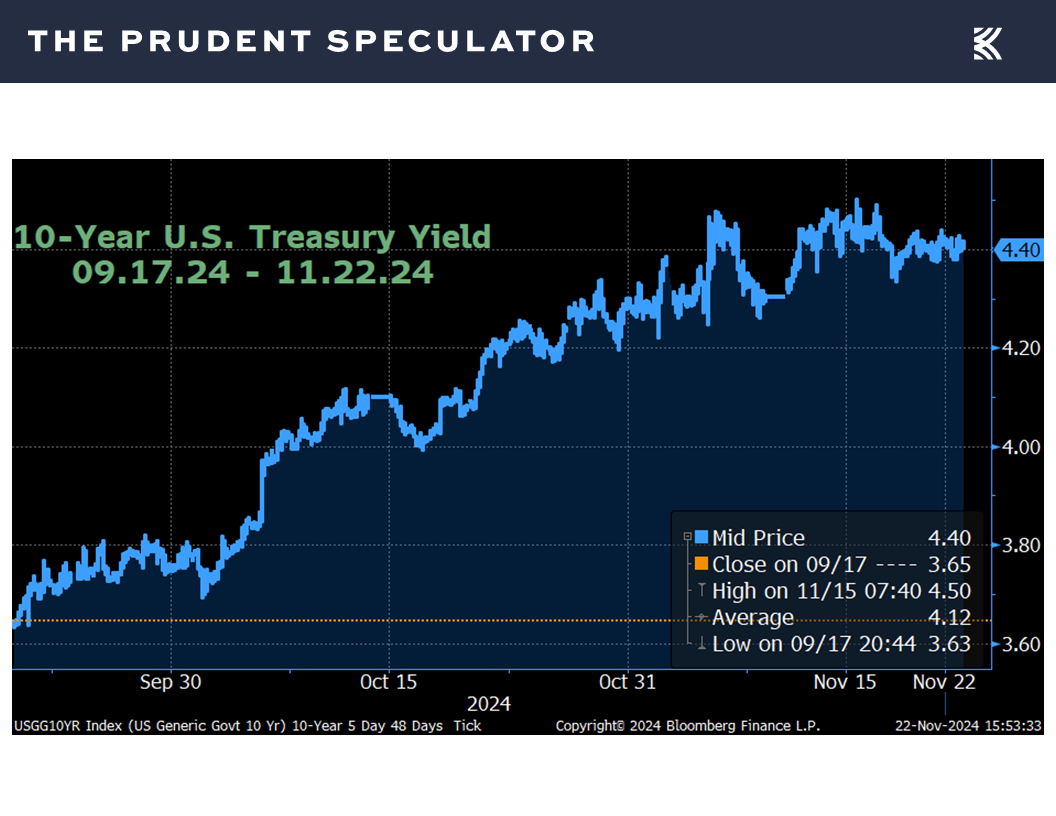

while the markets have moved nicely higher despite the yield on the benchmark 10-Year U.S. Treasury jumping from 3.65% the day before the Fed started its current rate cutting cycle to 4.40% today,

providing another reminder that higher bond yields are no reason to abandon equities.

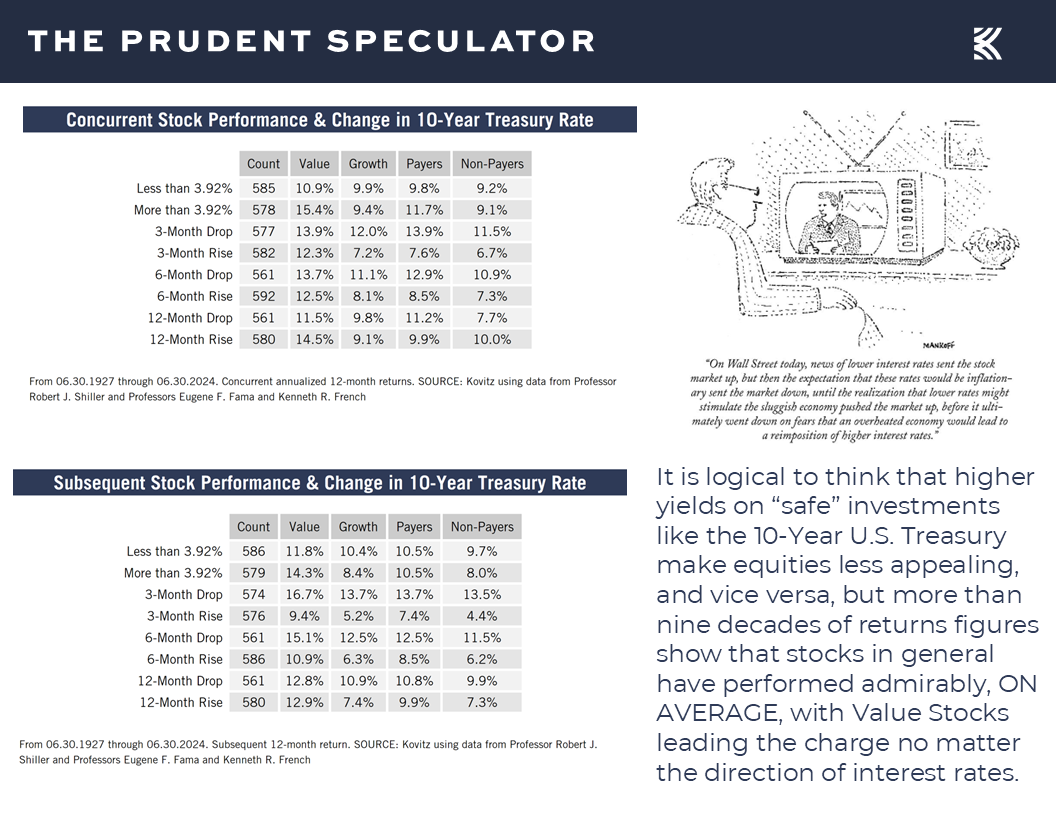

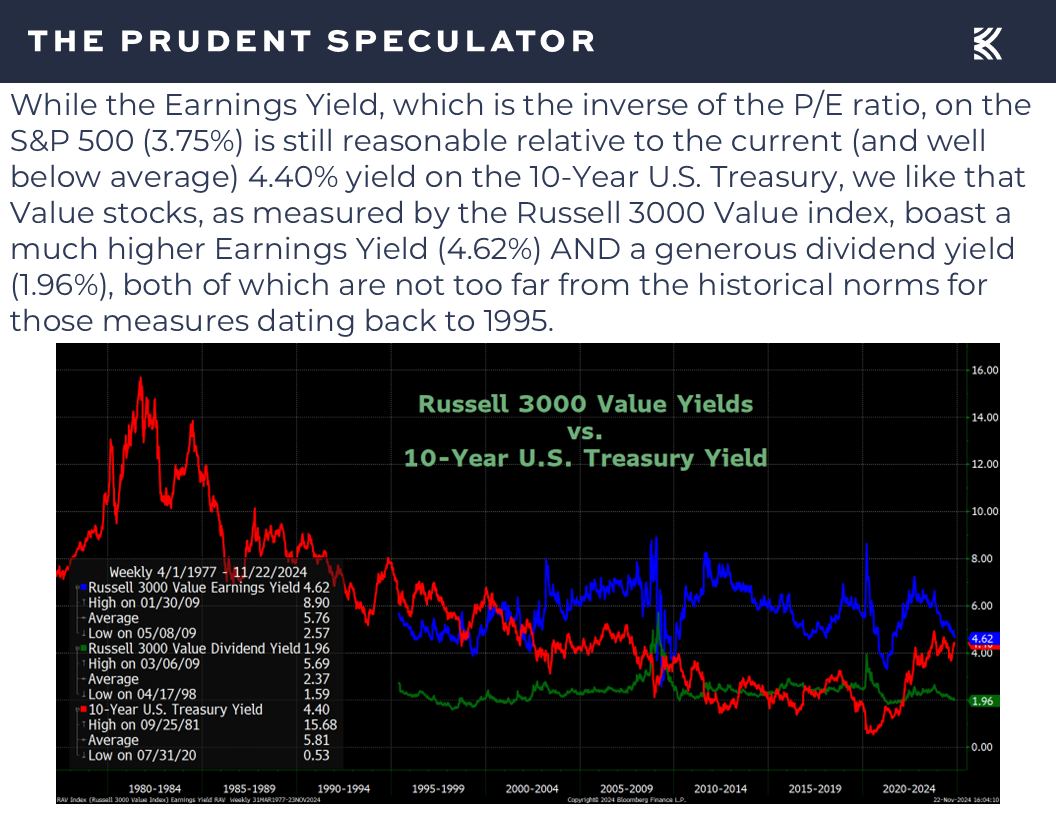

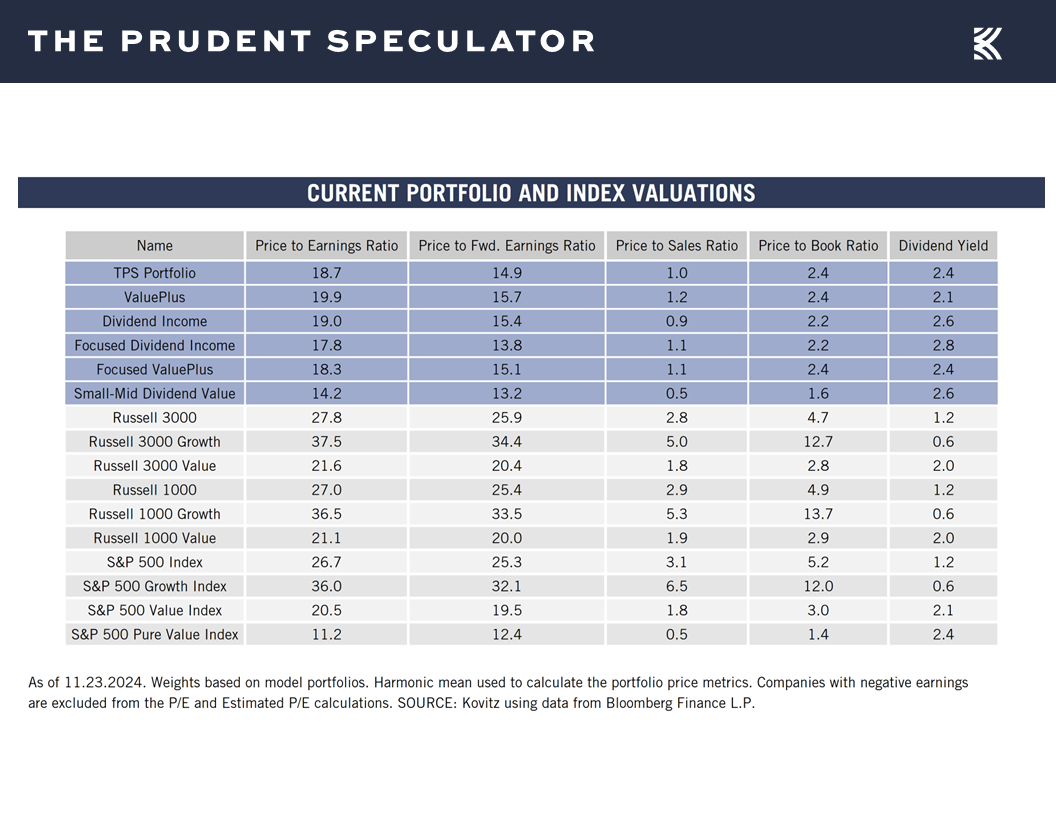

Valuations – Value Stocks Reasonably Priced

This is especially true, given that Value stocks continue to be reasonably priced relative to interest rates,

and our broadly diversified portfolios of what we believe are undervalued stocks boast even more appealing valuation metrics.

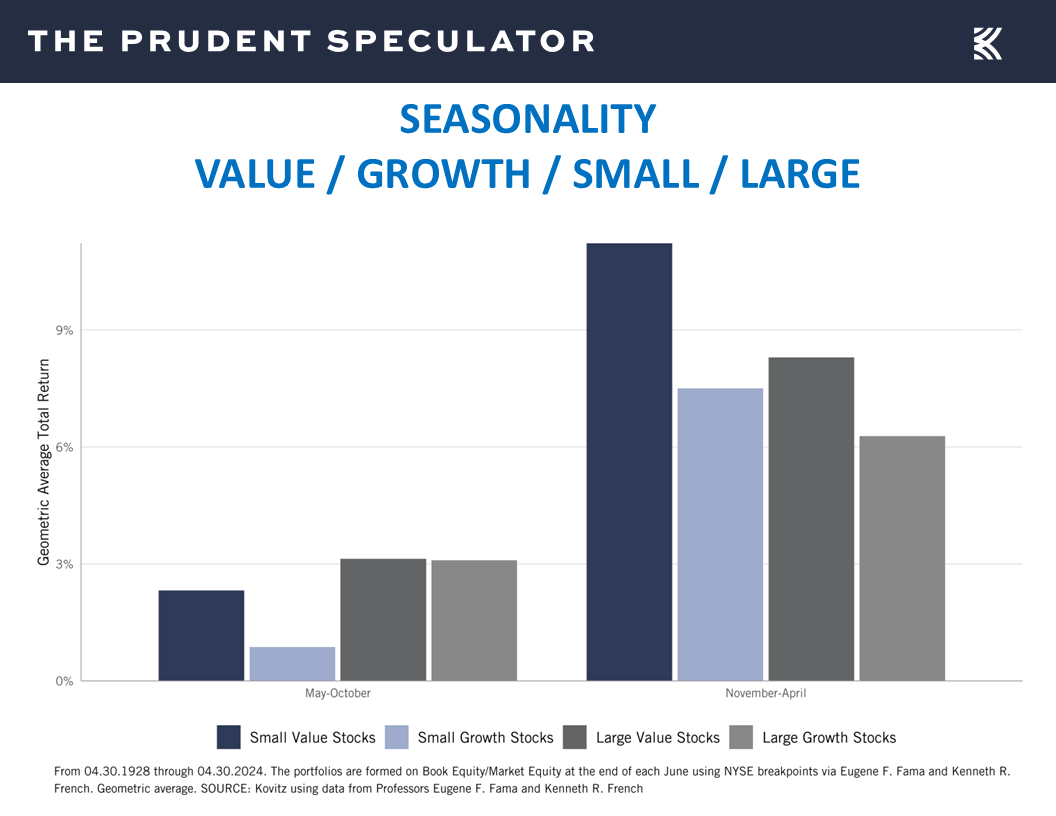

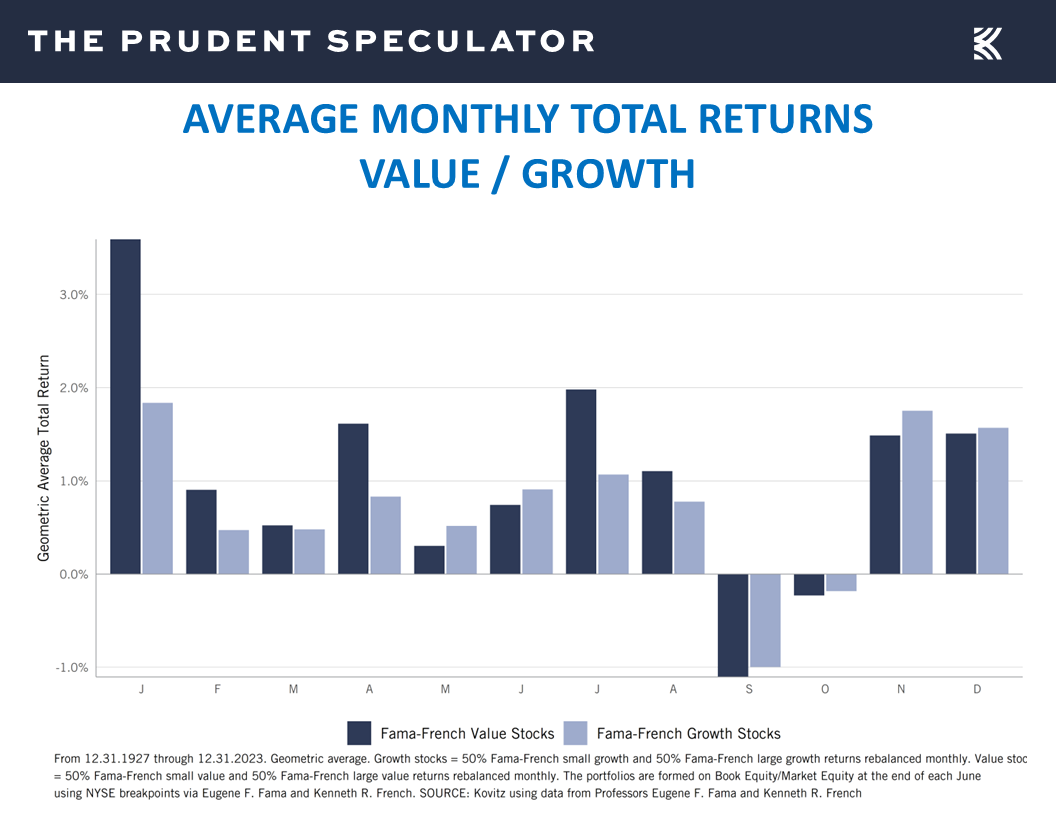

Seasonality – Most Wonderful Time of the Year

We also note that we are now in the seasonally more favorable six months of the year,

with November, December and January historically the most wonderful period,

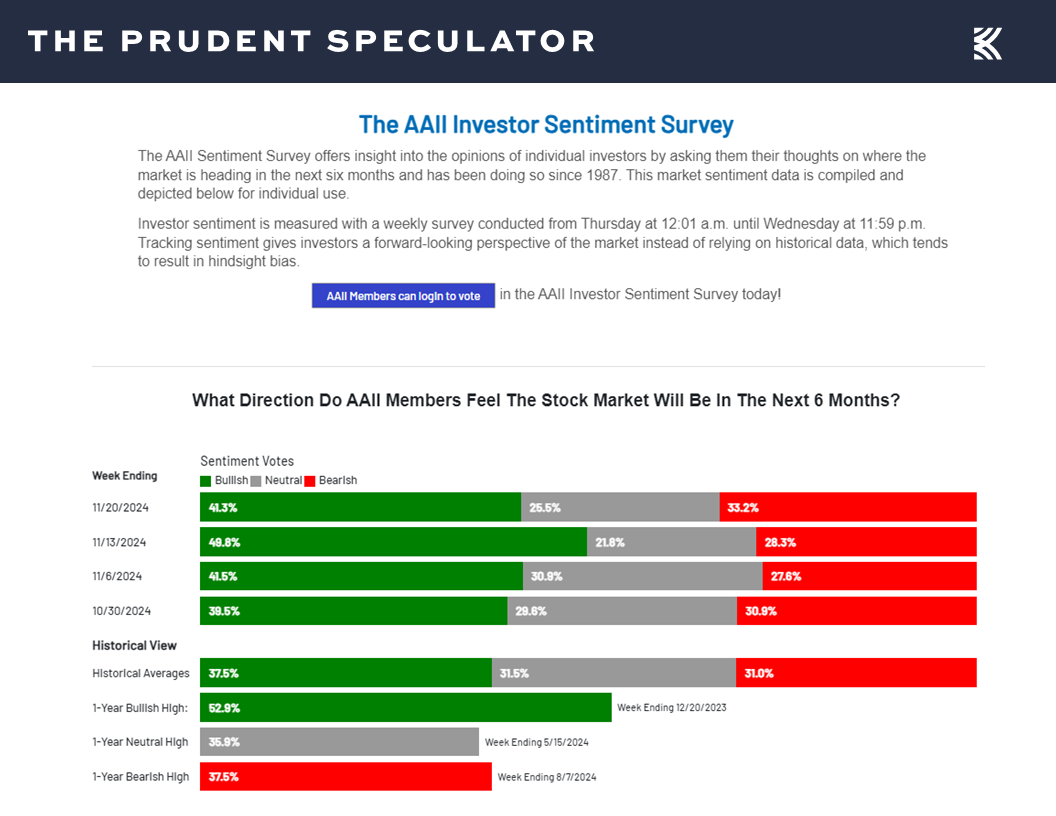

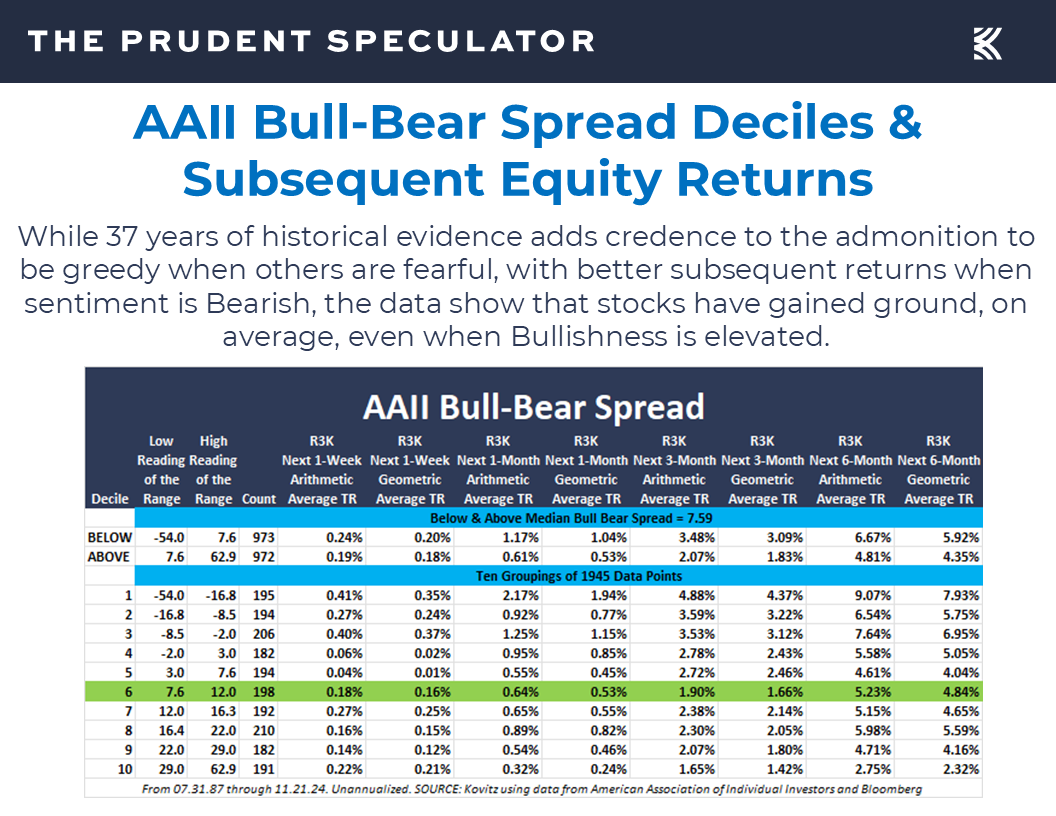

Sentiment – Bullishness Pulls Back

with it also nice to see a pullback in bullish enthusiasm on Main Street last week,

though the contrarian AAII sentiment gauge shows that while pessimism historically has been better for near-term returns, one should hold onto stocks no matter the AAII Bull-Bear reading.

We are always braced for downside volatility as there are often scary headlines, but we see no reason why stocks won’t continue to reward long-term-oriented investors.

Stock News – Updates on nine stocks across five different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Economic Data, Federal Reserve, Interest Rates and Seasonality

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Economic Data, Federal Reserve, Interest Rates and Seasonality. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Week In Review – Stocks Rally, Despite Escalation of Ukraine/Russia Hostilities

Econ Data – Mixed Numbers; Solid GDP Growth Still the Forecast

Corporate Profits – EPS Estimates Increase Slightly

Fed Speak – Still Data Dependent; Odds of Fed Rate Cuts Dampen

Interest Rates – Stocks Have Performed Fine Whether Fed is Easing/Tightening or 10-Year Yield is Rising/Falling

Valuations – Value Stocks Reasonably Priced

Seasonality – Most Wonderful Time of the Year

Sentiment – Bullishness Pulls Back

Stock News – Updates on GOOG, QCOM, MDT, ADM, TGT, DE, NTAP, LOW & WMT

Week In Review – Stocks Rally, Despite Escalation of Ukraine/Russia Hostilities

Providing another reminder that despite numerous bouts of downside volatility, handsome long-term rewards are available to those who stick with stocks,

the major equity market averages ended a roller-coaster of a trading week at or near all-time highs, even as the confrontation between Russia and Ukraine seemingly entered a more disconcerting phase,

Econ Data – Mixed Numbers; Solid GDP Growth Still the Forecast

and the latest economic data was more negative than positive, with the forward-looking Leading Economic Index from the Conference Board coming in below expectations with a 0.4% decline in October.

The Conference Board cited weakness in manufacturing, which was confirmed by the Philadelphia Fed’s gauge of East Coast factory activity for November dropping to a reading of -5.5, well below projections of 8.0.

We also learned that the final tally of consumer confidence for November from the Univ. of Michigan declined to 71.8, down from 73.0 in October and below forecasts of 73.9,

and that housing starts fell to 1.311 million in October, down from a revised 1.353 million the month prior and below the consensus estimate of 1.334 million.

On the other hand, sales of existing homes for October climbed to a slightly better than expected 3.96 million,

first-time filings for unemployment benefits of 213,000 in the latest week was lower than the 220,000 projection and continued to reside near multi-generational lows,

and the latest estimate for Q4 real (inflation-adjusted) U.S. GDP growth inched up to a solid 2.6%,

and the odds of recession in the next 12 months, as tabulated by data provider Bloomberg, held steady at a very low 25%.

Corporate Profits – EPS Estimates Increase Slightly

Despite the arguably mixed picture on the economic front, the outlook for corporate profit growth, which historically has been the driver of higher stock prices, improved a tad, at least according to the latest estimates for the S&P 500 offered by Standard & Poor’s,

Fed Speak – Still Data Dependent; Odds of Fed Rate Cuts Dampen

though it seemed a good deal of the financial market news last week was centered on comments from Federal Reserve officials about the prospects for additional interest rate cuts.

Boston Fed President Susan Collins said, “While the final destination is uncertain, I believe some additional policy easing is needed, as policy currently remains at least somewhat restrictive.”

However, Fed Governor Michelle Bowman stated, “I would prefer to proceed cautiously in bringing the policy rate down to better assess how far we are from the end point, while recognizing that we have not yet achieved our inflation goal and closely watching the evolution of the labor market.”

And Kansas City Fed President Jeffrey Schmid added, “While now is the time to begin dialing back the restrictiveness of monetary policy, it remains to be seen how much further interest rates will decline or where they might eventually settle.”

No doubt, Jerome H. Powell & Co. will remain data dependent as they consider additional cuts in the Fed Funds rate, but the players in the futures market were wagering on a bit less easing of monetary policy than at the end of the week prior, with the current betting for the respective year-end ’24 and ’25 rates ticking up to 4.45% and 3.93%,

above the projections offered by the Fed two months ago.

Of course, stocks have performed fine, on average, whether the Fed is raising or lowering interest rates,

Interest Rates – Stocks Have Performed Fine Whether Fed is Easing/Tightening or 10-Year Yield is Rising/Falling

while the markets have moved nicely higher despite the yield on the benchmark 10-Year U.S. Treasury jumping from 3.65% the day before the Fed started its current rate cutting cycle to 4.40% today,

providing another reminder that higher bond yields are no reason to abandon equities.

Valuations – Value Stocks Reasonably Priced

This is especially true, given that Value stocks continue to be reasonably priced relative to interest rates,

and our broadly diversified portfolios of what we believe are undervalued stocks boast even more appealing valuation metrics.

Seasonality – Most Wonderful Time of the Year

We also note that we are now in the seasonally more favorable six months of the year,

with November, December and January historically the most wonderful period,

Sentiment – Bullishness Pulls Back

with it also nice to see a pullback in bullish enthusiasm on Main Street last week,

though the contrarian AAII sentiment gauge shows that while pessimism historically has been better for near-term returns, one should hold onto stocks no matter the AAII Bull-Bear reading.

We are always braced for downside volatility as there are often scary headlines, but we see no reason why stocks won’t continue to reward long-term-oriented investors.

Stock News – Updates on nine stocks across five different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.