The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Economic News, Earnings, Volatility and more Stock News. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Contrarian Sentiment – More AAII Bears than Bulls

Week in Review – Stocks Rebound a Bit

Historical Evidence – Rising Interest Rates, Higher Fed Funds Rate & Elevated Inflation Not Negatives for Stocks, On Average

Economic News – Q1 GDP Below Expectations; Q2 Outlook Robust

Earnings – Solid Growth Estimated in ’24 & ’25

Volatility – Ups and Downs But Long-Term Trend is Up

Valuations – Inexpensive Metrics for TPS Portfolio

Stock News – Updates on CAH, VZ, TFC, ARE, GM, SYF, HAS, NSC, LRCX, WHR, META, IBM, WM, NEM, MSFT & GOOG

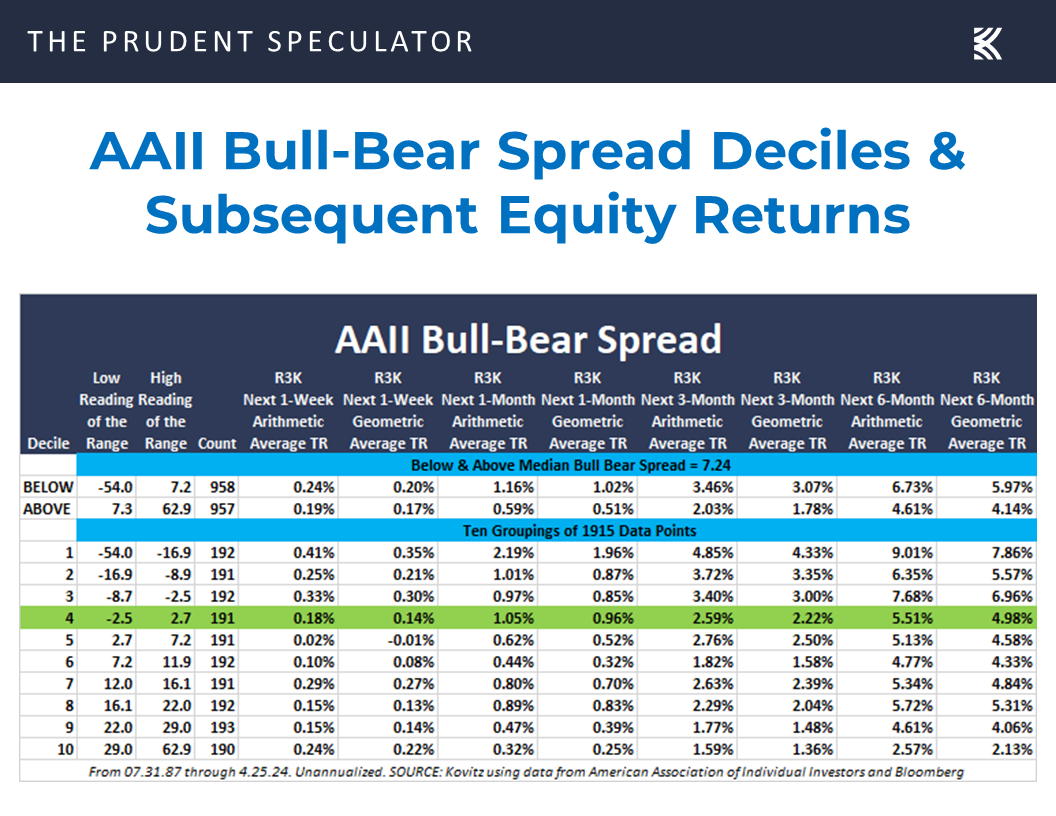

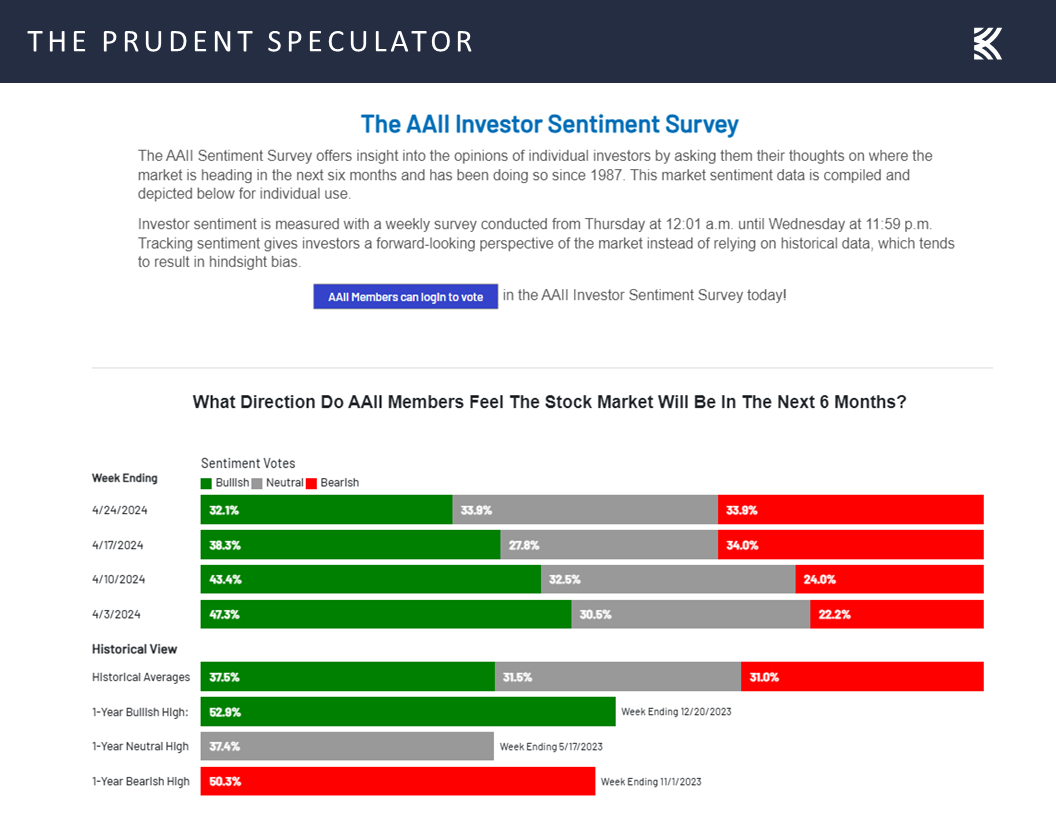

Contrarian Sentiment – More AAII Bears than Bulls

Although 37 years of evaluating forward returns based on the American Association of Individual Investor (AAII) Bull-Bear Spread shows that investors should stick with stocks no matter the reading on the weekly measure,

we can’t help but think that last week’s bounce in equities had something to do with those folks on Main Street becoming more pessimistic than optimistic about the prospects for the Dow Jones Industrial Average over the next six months for the first time since late-October – early November 2023!

Week in Review – Stocks Rebound a Bit

Illustrating why investor sentiment is often viewed as a contrarian indicator, the Dow Jones Industrial Average has returned 14.16% since November 2, the last time there were more AAII Bears than Bulls, and the average stock in the Russell 3000 index has performed a couple of percentage points better, though all the latter’s gains came in 2023, as it has been tough sledding for the proverbial soldiers this year, even as the generals are nicely higher, on average.

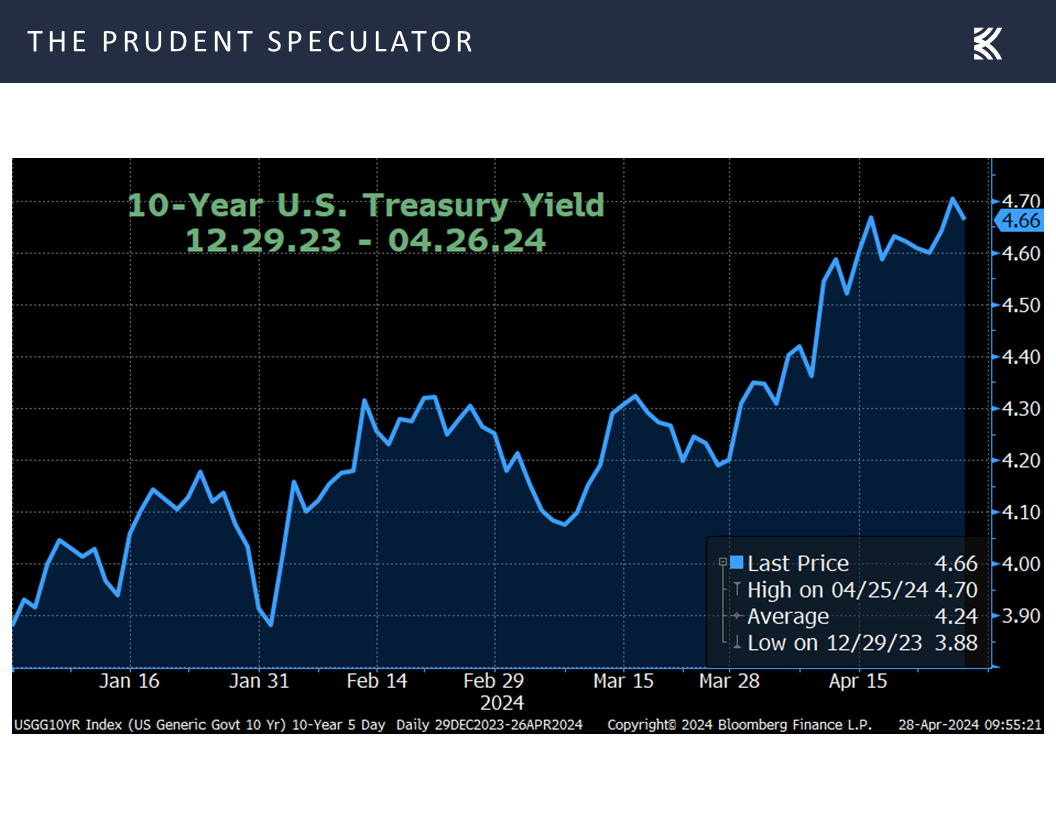

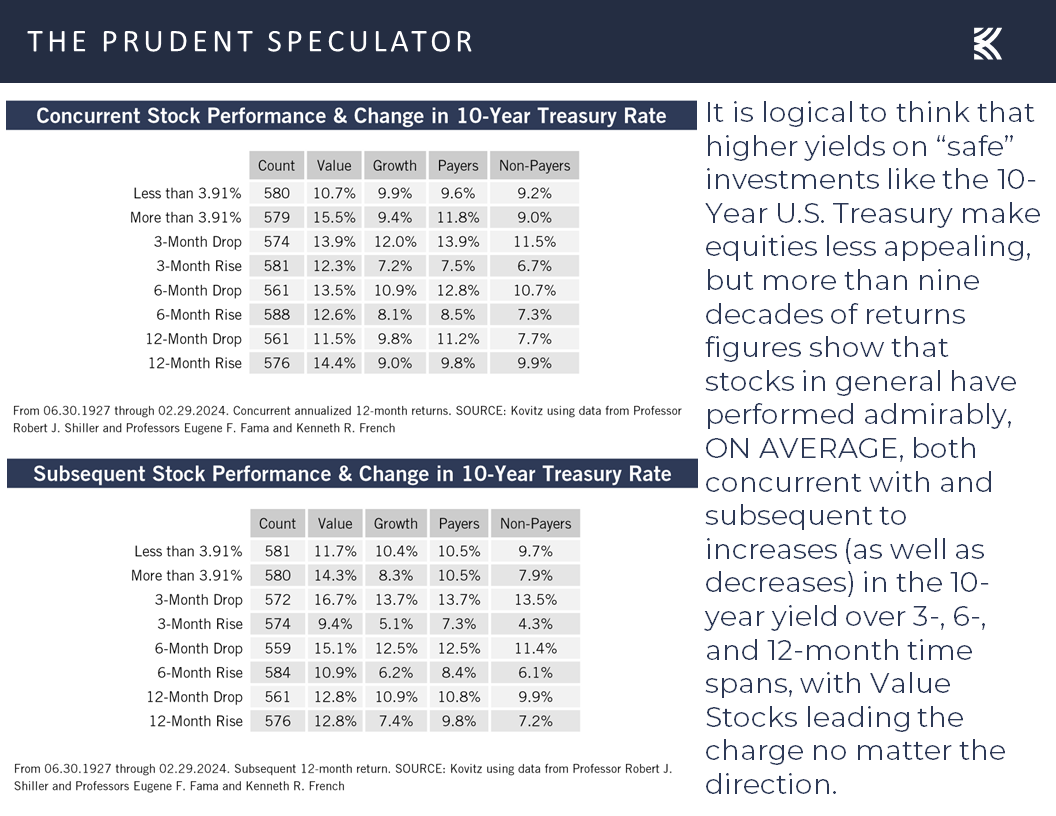

Historical Evidence – Rising Interest Rates, Higher Fed Funds Rate & Elevated Inflation Not Negatives for Stocks, On Average

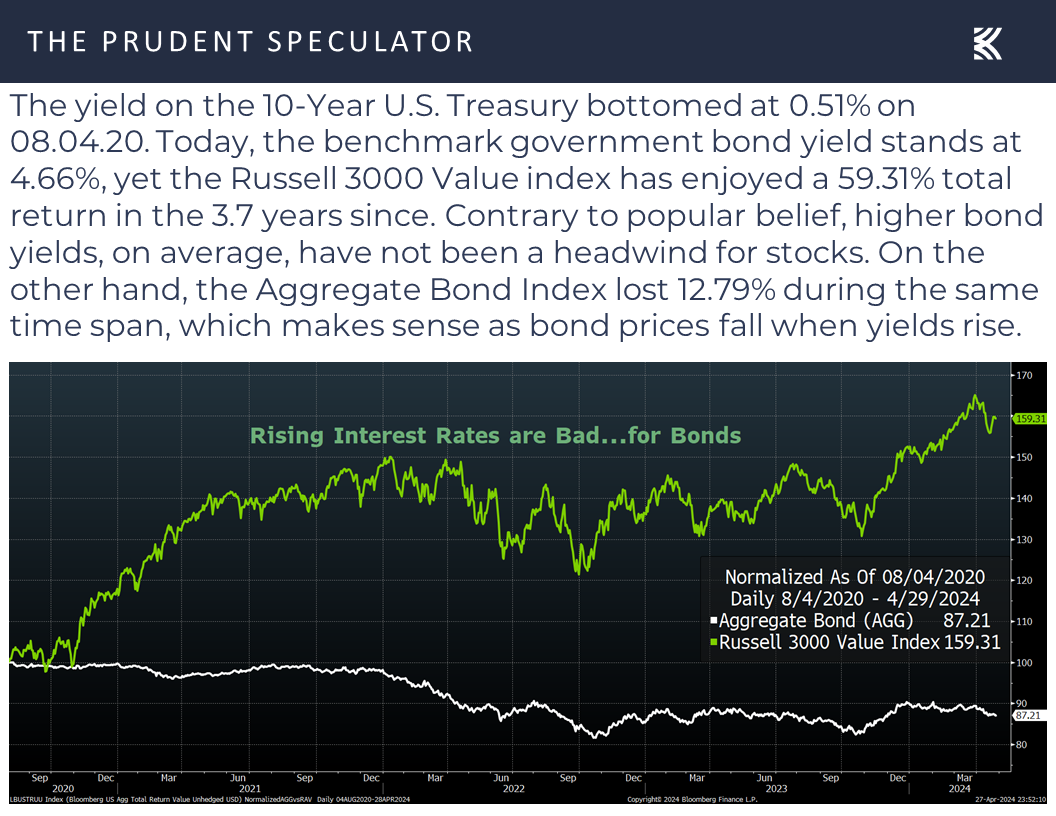

After all, the supposed experts tell us that stocks do not like higher interest rates, and the yield on the 10-Year U.S. Treasury has soared this year from 3.88% to 4.66%,

but history suggests otherwise for rising government bond yields,

and the only thing that can be said with certainty is that increasing interest rates are bad for bonds.

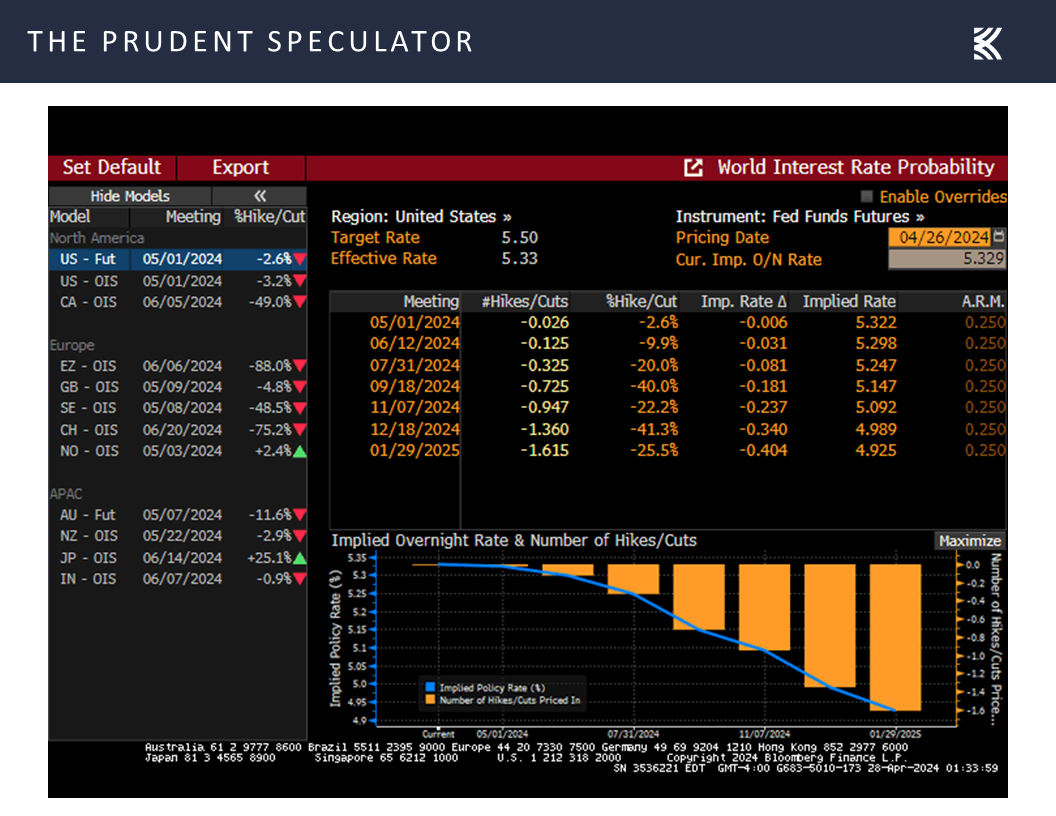

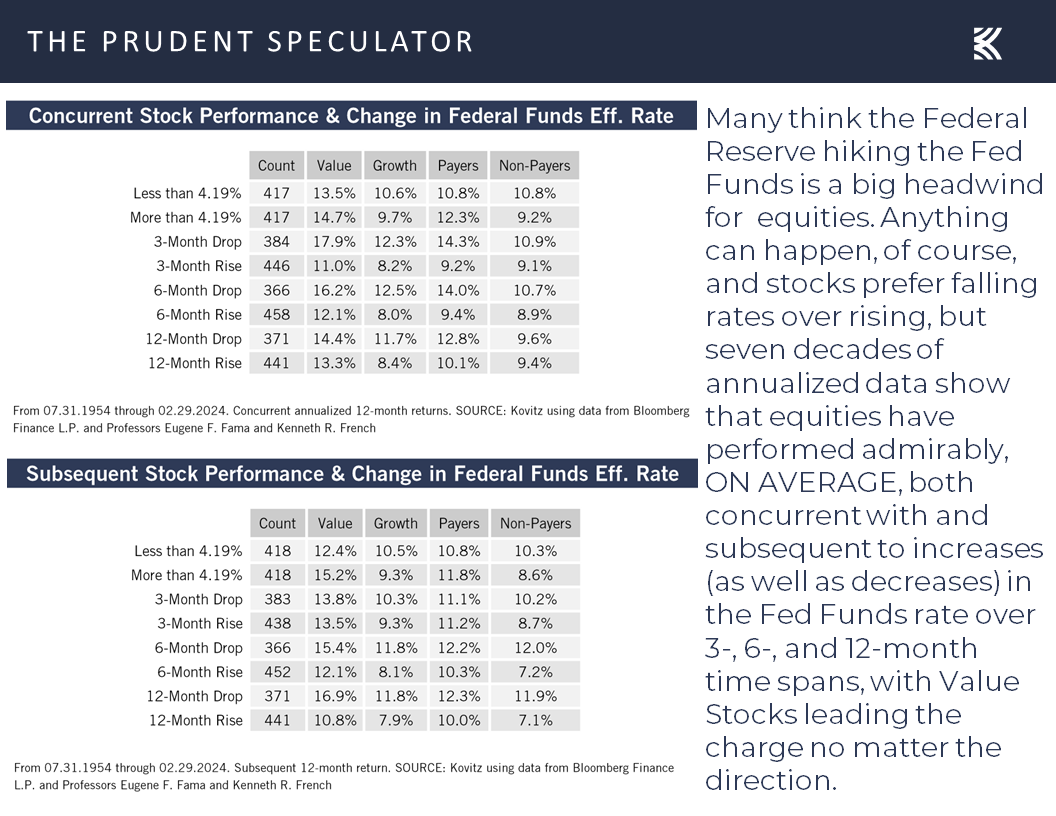

We know that many also are worried that the current betting in the futures market is suggesting that the Federal Reserve is not enthused about cutting its target for the Fed Funds rate any time soon,

but history shows that Value stocks, on average, have performed better both concurrent with and subsequent to a higher-than-normal Fed Funds rate versus a lower one.

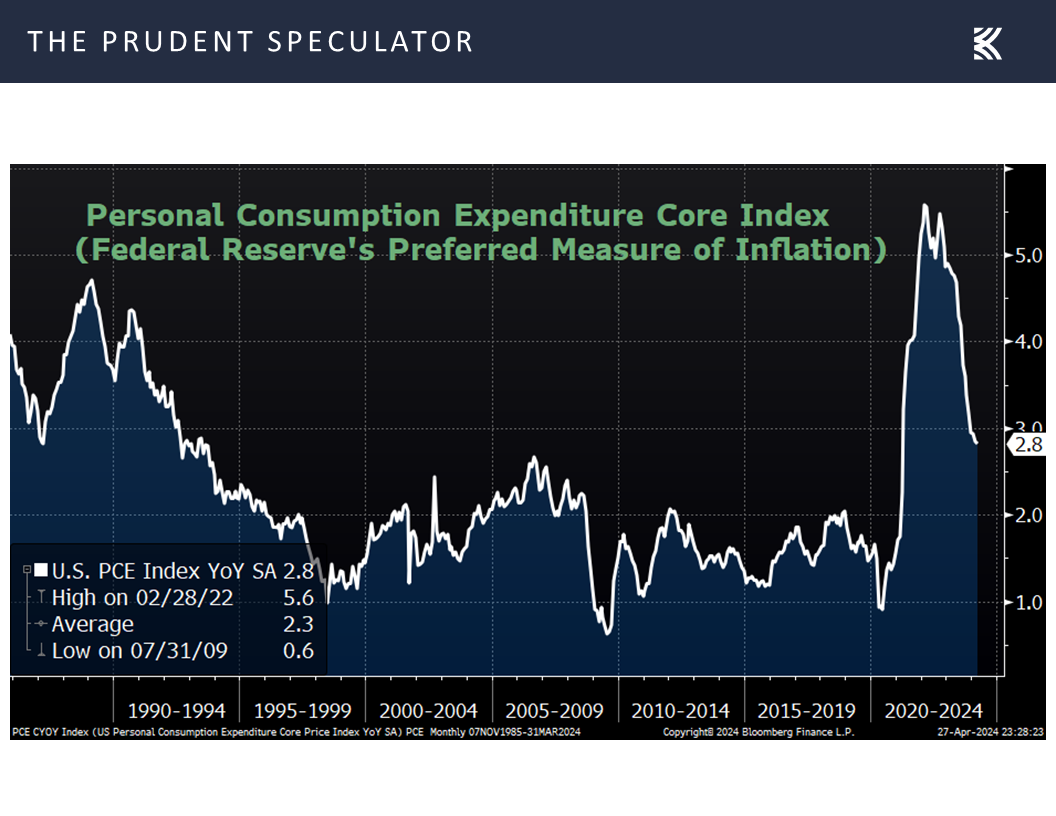

No doubt, the latest inflation figures, with the Fed’s preferred measure, the Personal Consumption Expenditure Core (PCE) index, holding steady at 2.8%, versus expectations for a decline to 2.7%,

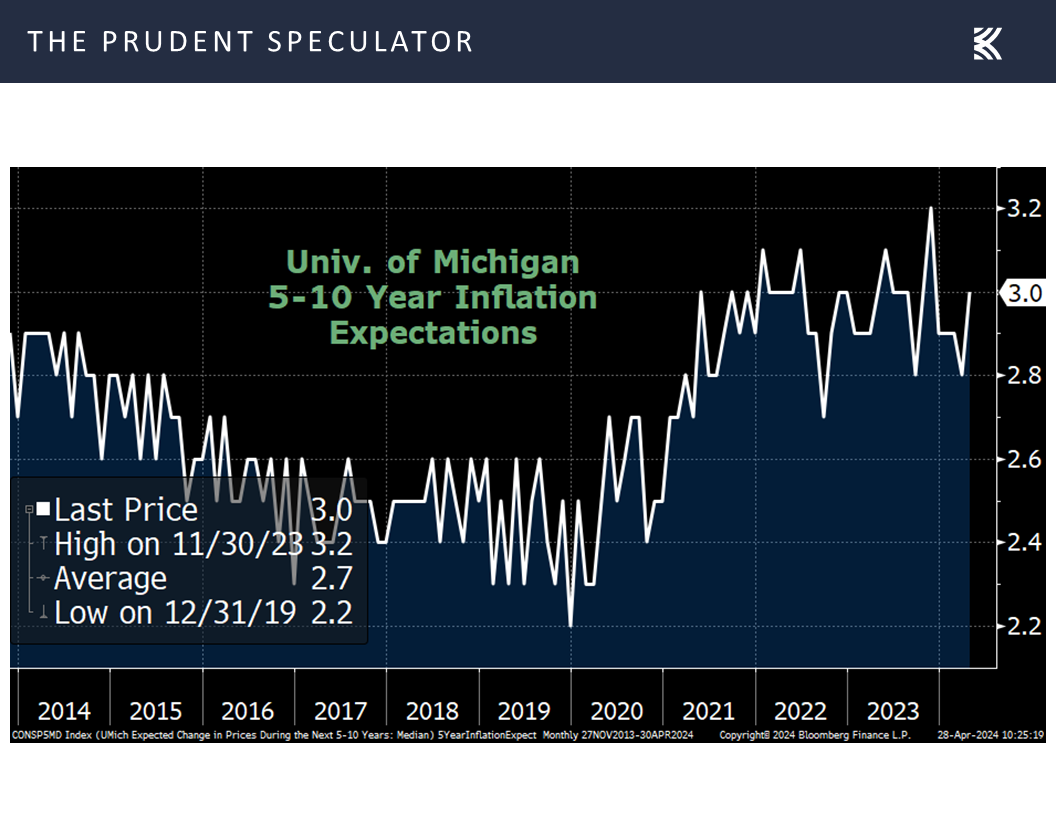

and the University of Michigan’s short-term inflation expectations rising to 3.2% this month from 2.9% in March, with longer-term expectations ticking up to 3.0%, didn’t help those hoping for Fed rate cuts.

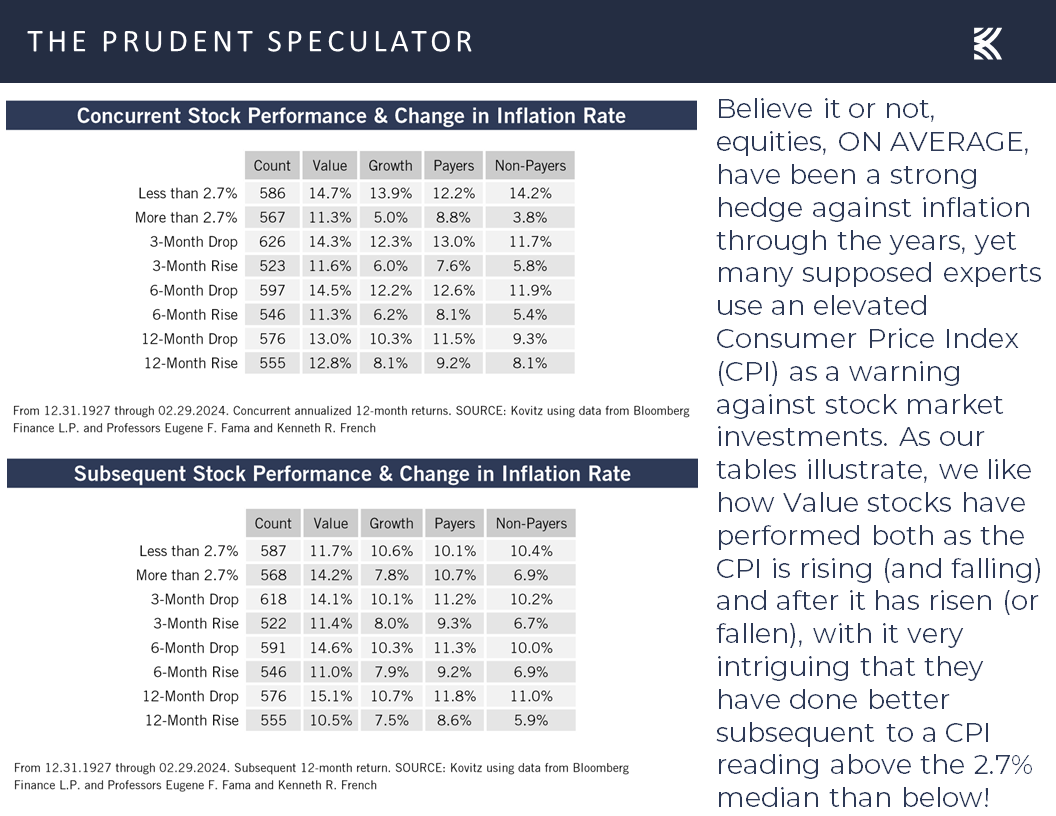

However, history shows that Value stocks have performed well, on average, whether inflation is rising or falling, or whether it is high or low,

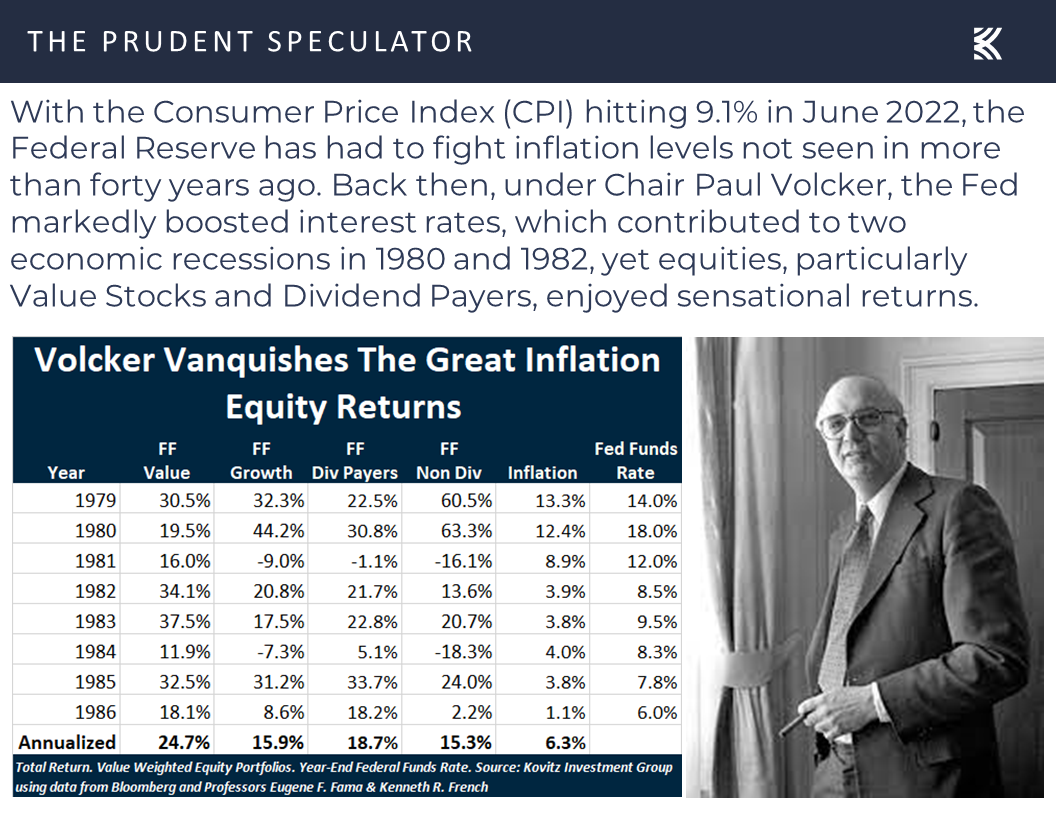

and the last time central bankers in the U.S. had a major battle with elevated consumer prices ended spectacularly well for equities in general and Value stocks in particular.

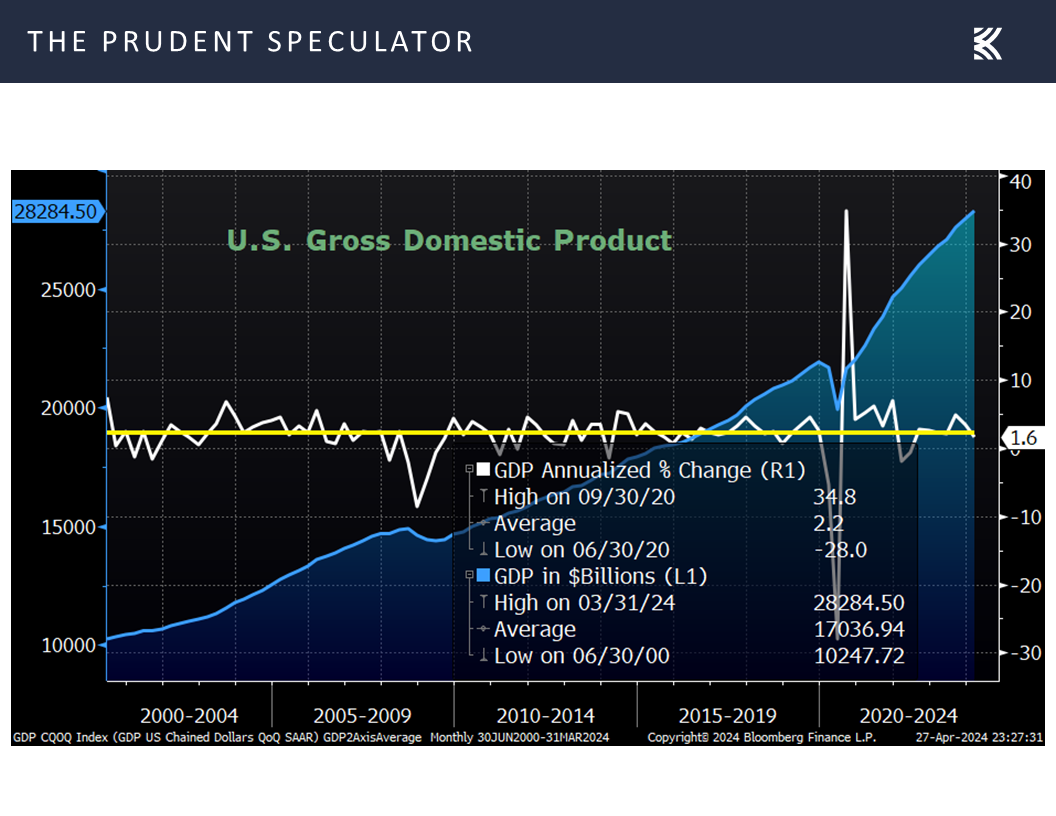

Econ News – Q1 GDP Below Expectations; Q2 Outlook Robust

To be sure, interest rates and the Fed are not the only thing troubling investors these days, as we learned last week that the first estimate of real (inflation-adjusted) U.S. GDP growth for Q1 rose a much-worse-than-expected 1.6%, though The New York Times asserted, “Economists were largely unconcerned by the slowdown, which stemmed mostly from big shifts in business inventories and international trade, components that often swing wildly from one quarter to the next. Measures of underlying demand were significantly stronger, offering no hint of the recession that forecasters spent much of last year warning was on the way.”

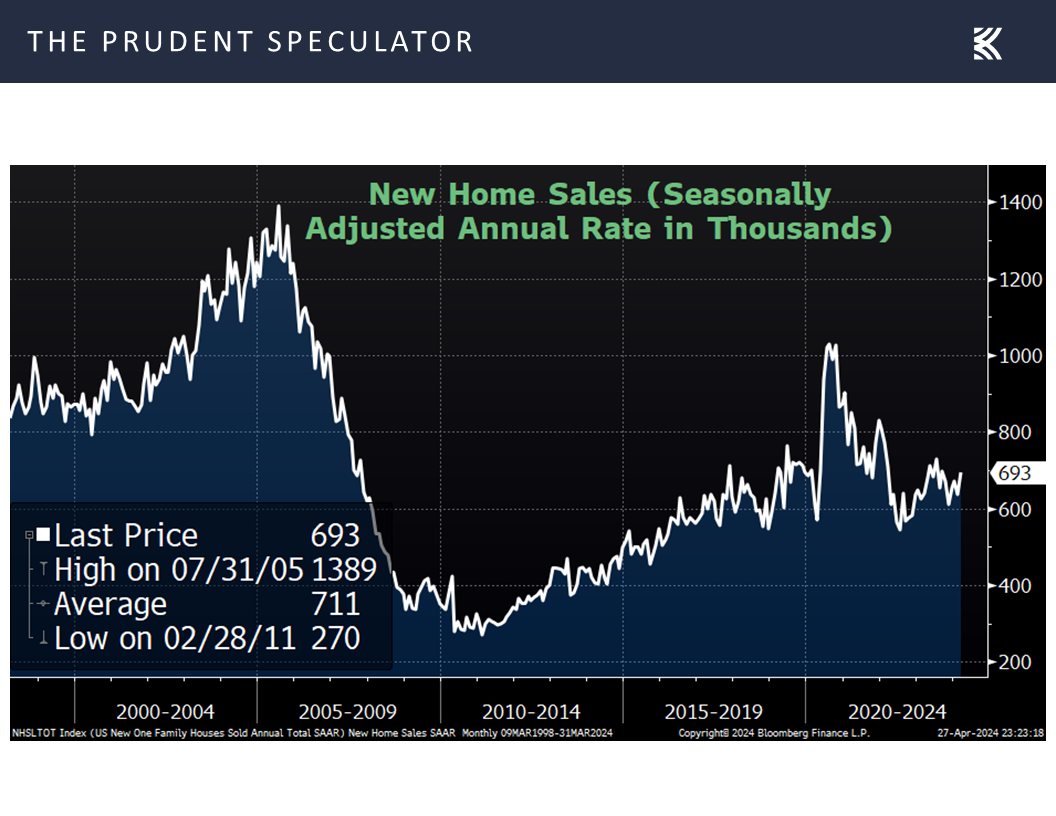

Further, the latest readings on new home sales for March at 693,000 came in better than the 668,000 consensus forecast,

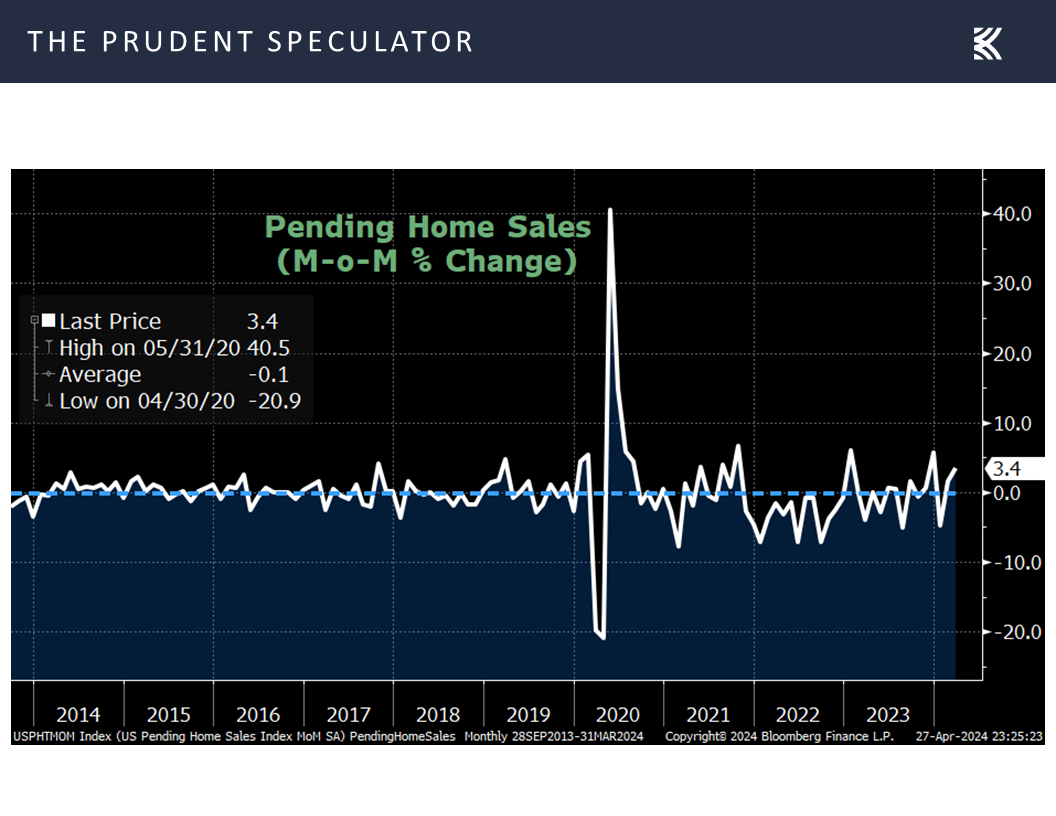

pending home sales for March increased a much-better-than-expected 3.4% over February,

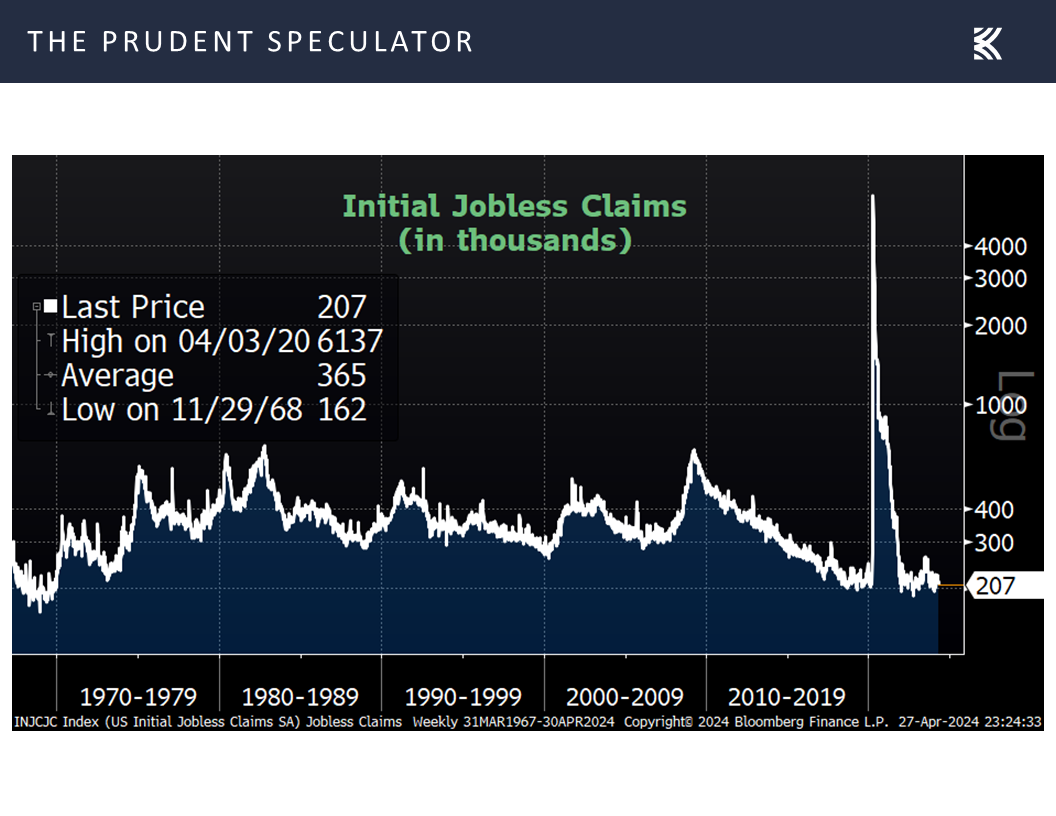

and first-time filings for unemployment benefits in the latest week fell to 207,000, lower than projections and a sign of continued strength in the labor market.

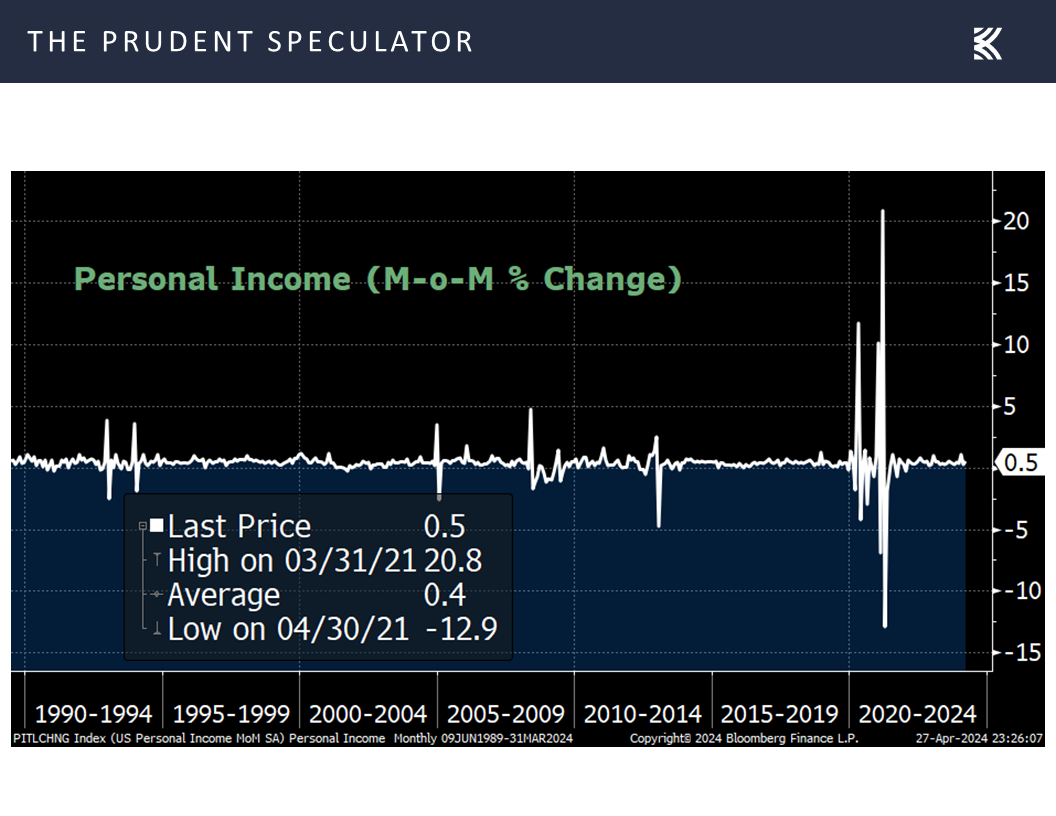

Personal income also rose 0.5% in March, in line with estimates,

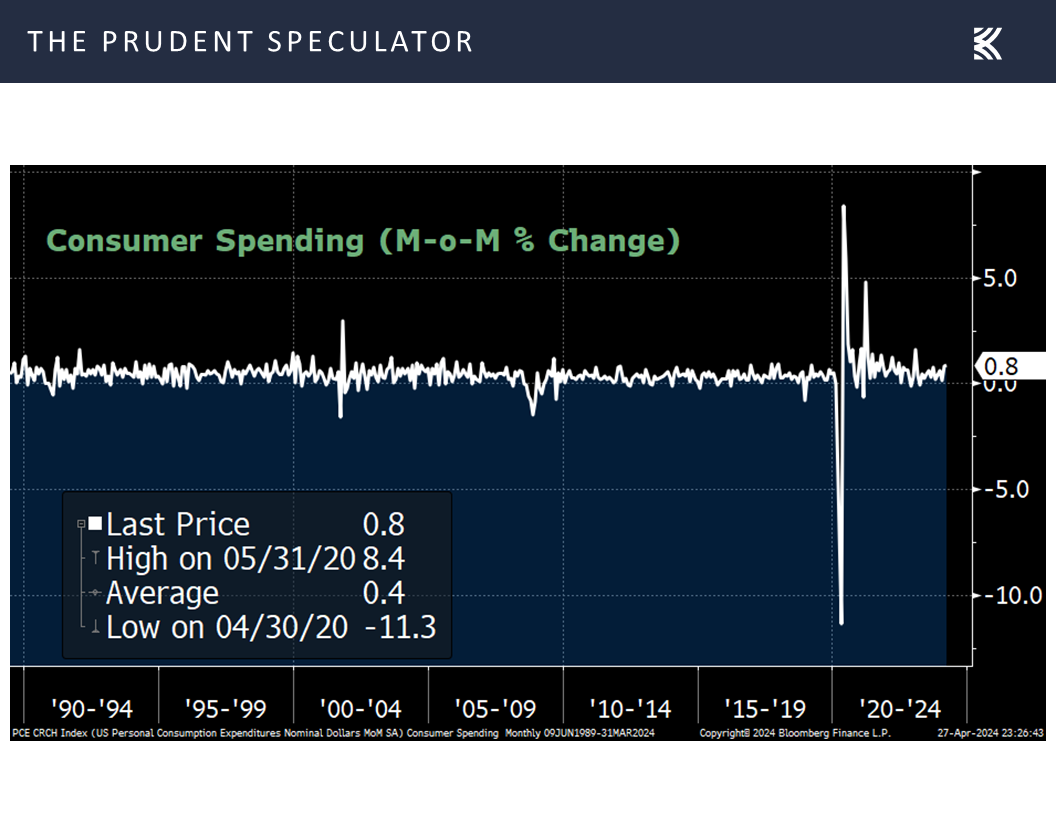

while consumer spending climbed 0.8%, higher than the 0.6% projection,

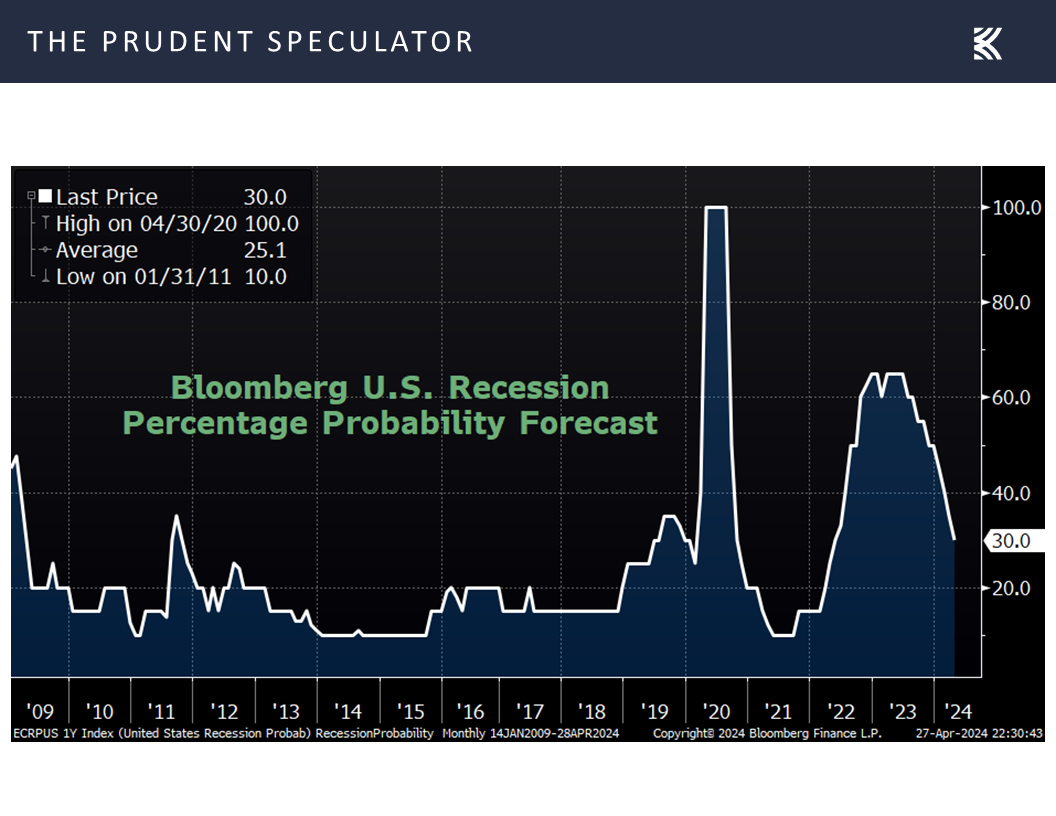

adding support for the recent decline to 30% in the odds of recession over the next 12 months as tabulated by Bloomberg.

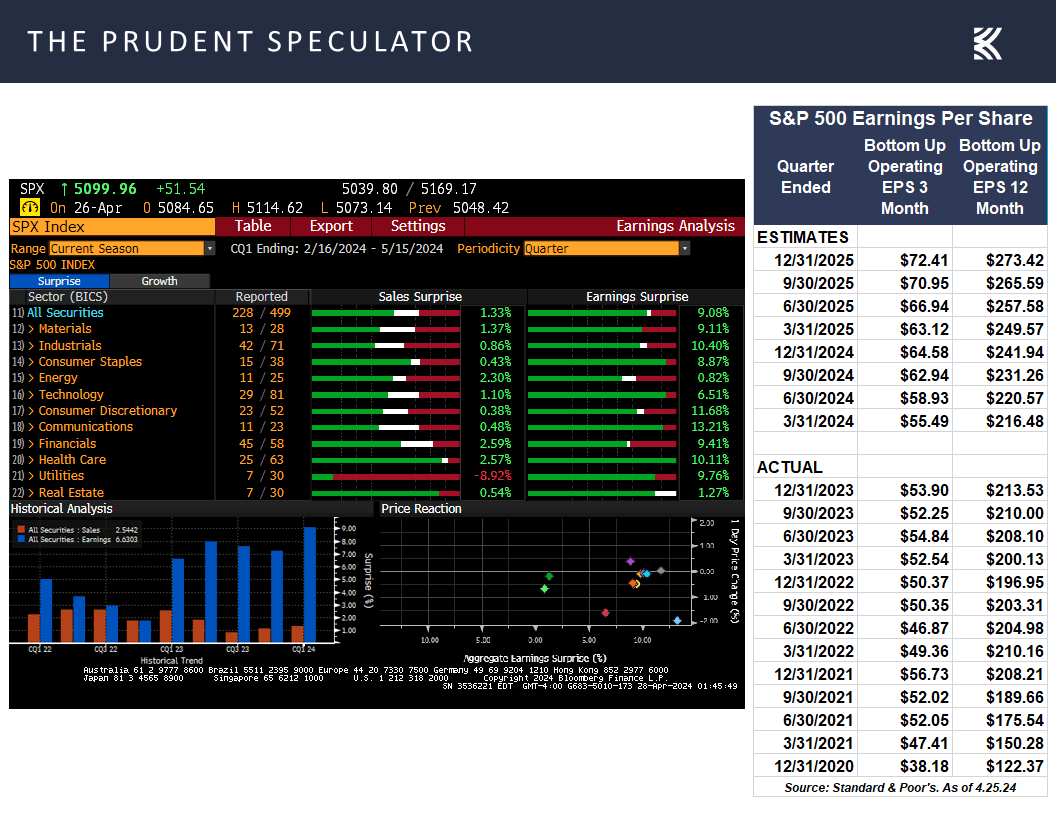

Earnings – Solid Growth Estimated in ’24 & ’25

More importantly, given that equity prices historically have appreciated over time as corporate profits have grown,

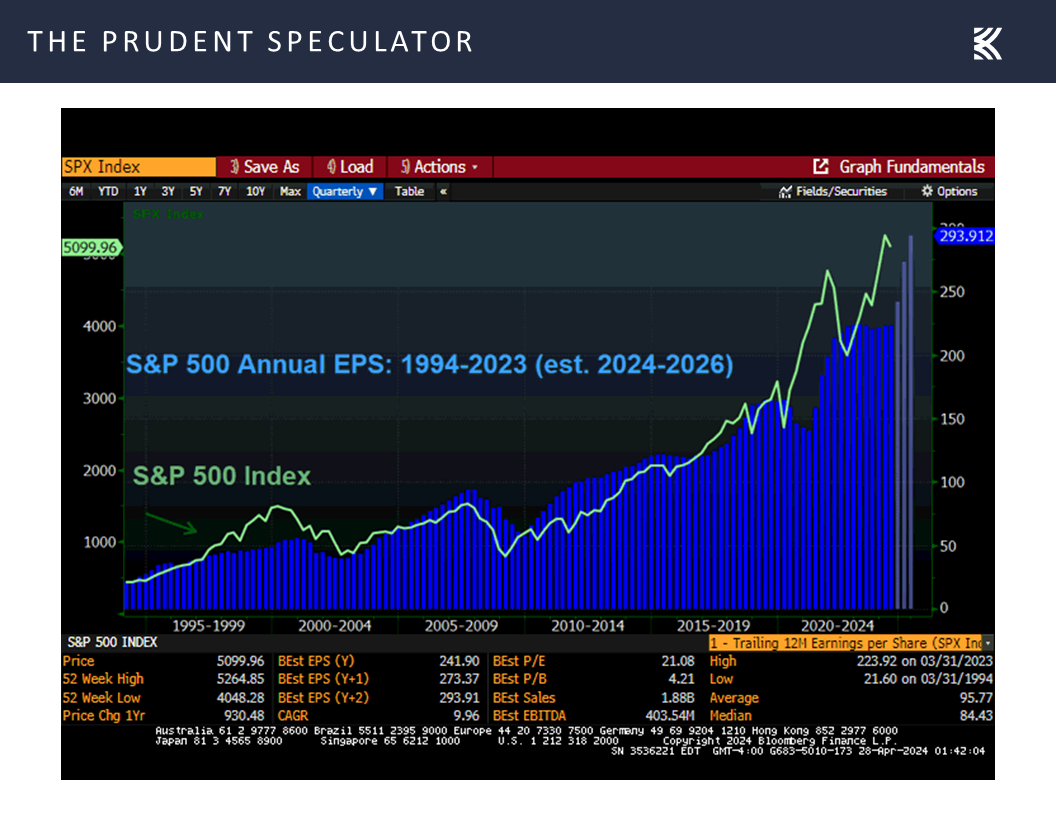

last week’s hefty batch of report cards turned in by Corporate America continued to show that Q1 results were terrific, with a greater-than-usual 80.6% of S&P 500 constituents topping bottom-line estimates so far this season.

True, forward guidance left a lot to be desired at some companies, but the outlook for growth in EPS this year and next remains solid, which would improve the E part of the Earnings to Price (Earnings Yield) equation and increase the likelihood of an increase in the D part of the Dividends to Price (Dividend Yield) calculation,

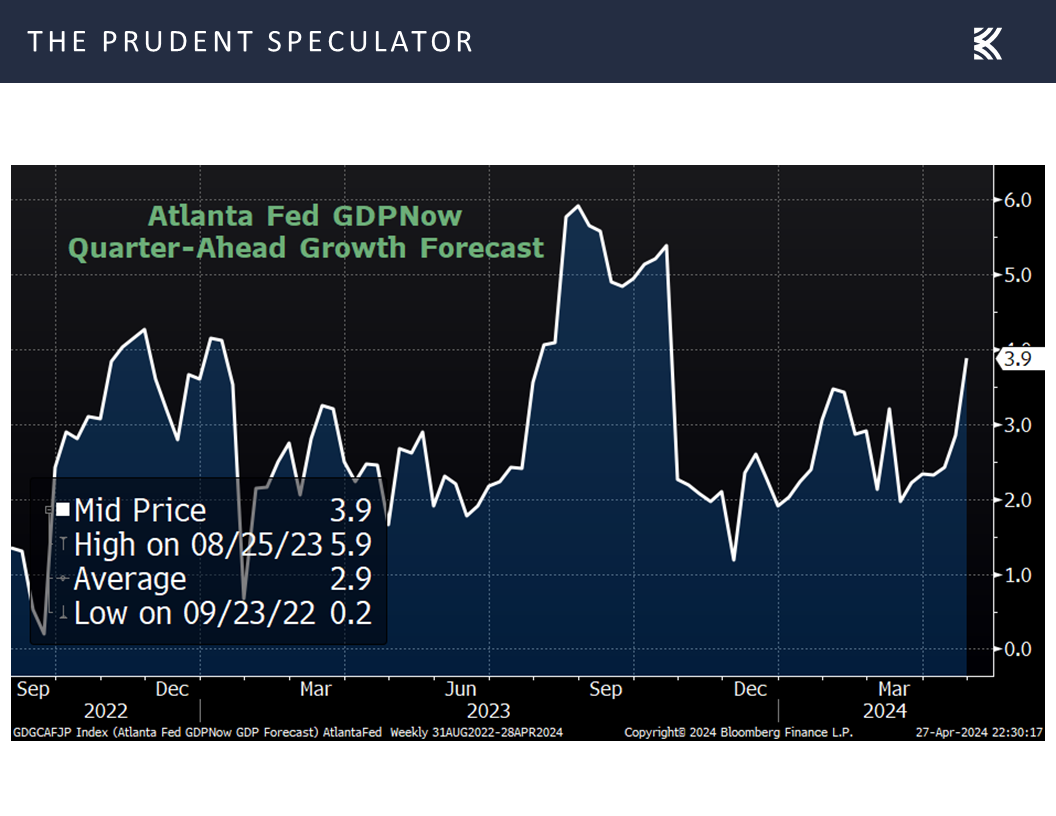

especially given that the first estimate for Q2 real GDP growth from the Atlanta Fed came in at a very robust 3.9%.

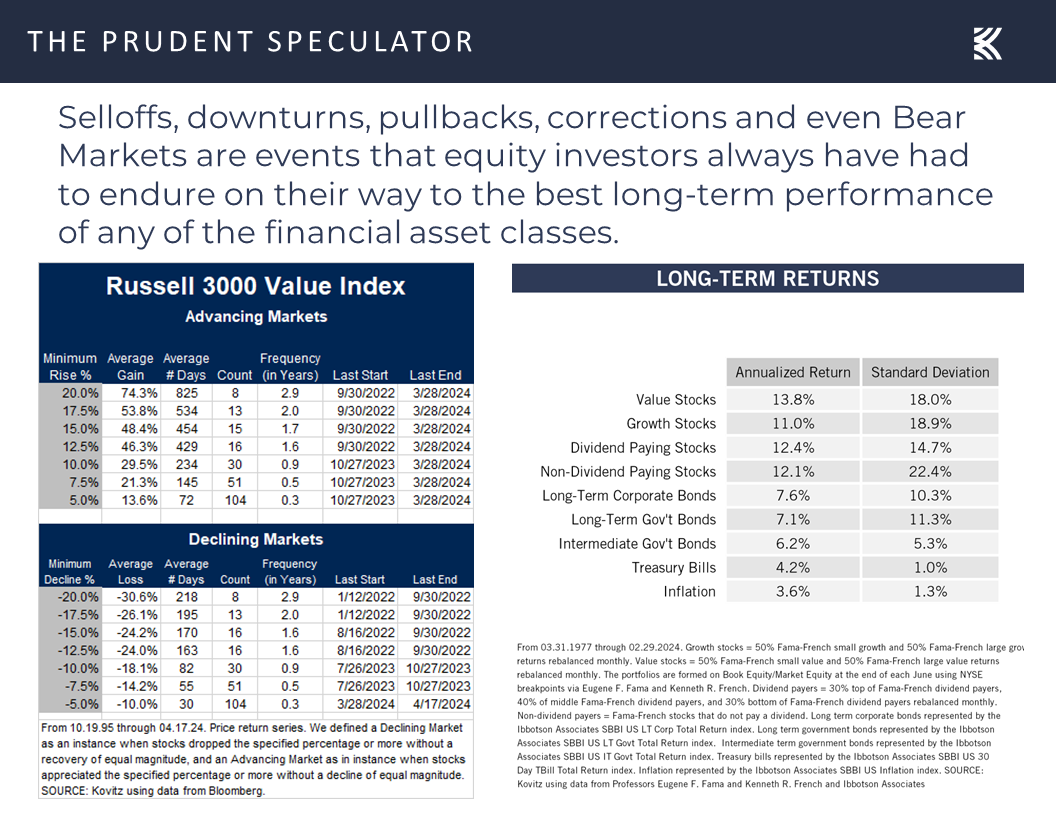

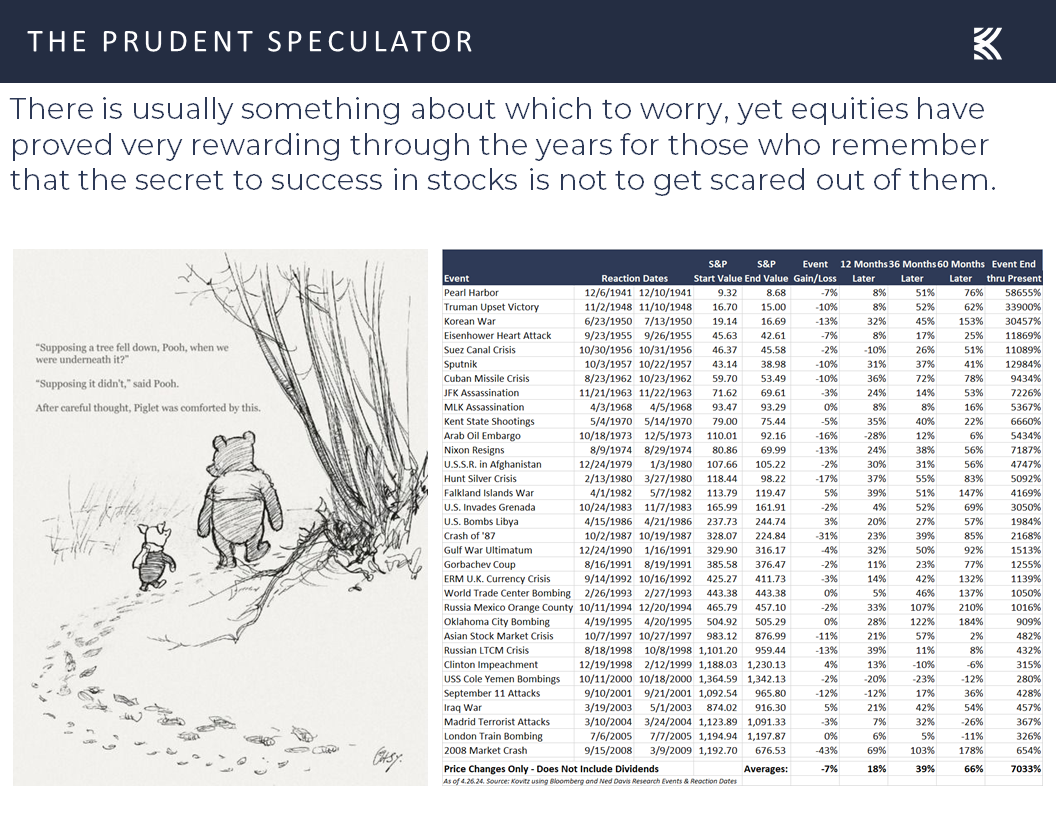

Volatility – Ups and Downs But Long-Term Trend is Up

Certainly, we have to be braced for equity market volatility, which is always part of the investment process,

and events on the geopolitical stage will always be a major wildcard, but stocks have also proved rewarding in the fullness of time,

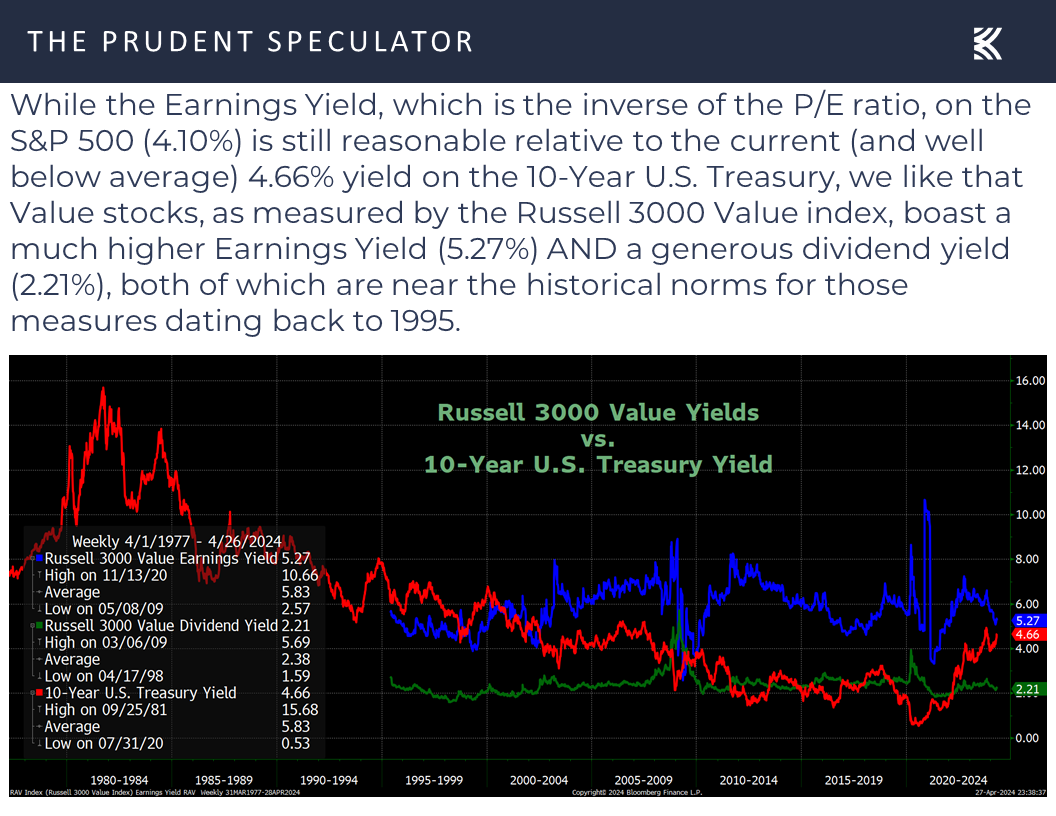

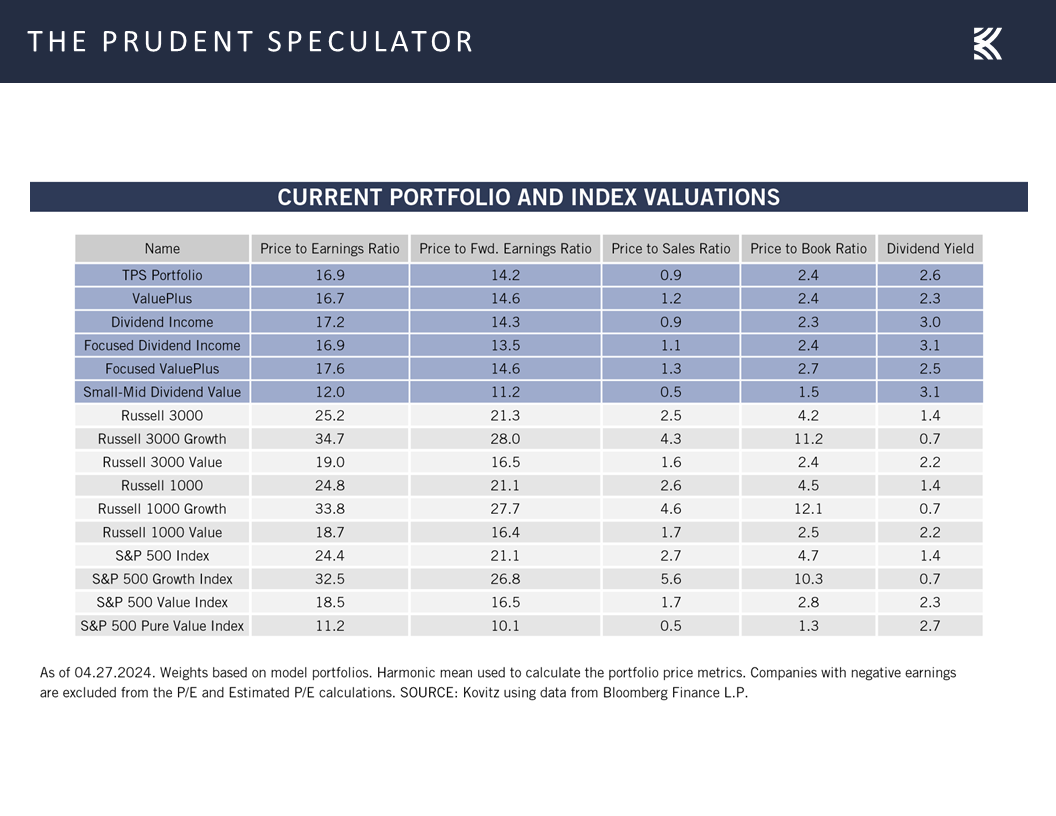

Valuations – Inexpensive Metrics for TPS Portfolio

and we continue to sleep very well at night with the reasonable valuation metrics for our broadly diversified portfolios.

Stock News – Updates on sixteen stocks across ten different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Economic News, Earnings, Volatility and more Stock News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Economic News, Earnings, Volatility and more Stock News. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Contrarian Sentiment – More AAII Bears than Bulls

Week in Review – Stocks Rebound a Bit

Historical Evidence – Rising Interest Rates, Higher Fed Funds Rate & Elevated Inflation Not Negatives for Stocks, On Average

Economic News – Q1 GDP Below Expectations; Q2 Outlook Robust

Earnings – Solid Growth Estimated in ’24 & ’25

Volatility – Ups and Downs But Long-Term Trend is Up

Valuations – Inexpensive Metrics for TPS Portfolio

Stock News – Updates on CAH, VZ, TFC, ARE, GM, SYF, HAS, NSC, LRCX, WHR, META, IBM, WM, NEM, MSFT & GOOG

Contrarian Sentiment – More AAII Bears than Bulls

Although 37 years of evaluating forward returns based on the American Association of Individual Investor (AAII) Bull-Bear Spread shows that investors should stick with stocks no matter the reading on the weekly measure,

we can’t help but think that last week’s bounce in equities had something to do with those folks on Main Street becoming more pessimistic than optimistic about the prospects for the Dow Jones Industrial Average over the next six months for the first time since late-October – early November 2023!

Week in Review – Stocks Rebound a Bit

Illustrating why investor sentiment is often viewed as a contrarian indicator, the Dow Jones Industrial Average has returned 14.16% since November 2, the last time there were more AAII Bears than Bulls, and the average stock in the Russell 3000 index has performed a couple of percentage points better, though all the latter’s gains came in 2023, as it has been tough sledding for the proverbial soldiers this year, even as the generals are nicely higher, on average.

Historical Evidence – Rising Interest Rates, Higher Fed Funds Rate & Elevated Inflation Not Negatives for Stocks, On Average

After all, the supposed experts tell us that stocks do not like higher interest rates, and the yield on the 10-Year U.S. Treasury has soared this year from 3.88% to 4.66%,

but history suggests otherwise for rising government bond yields,

and the only thing that can be said with certainty is that increasing interest rates are bad for bonds.

We know that many also are worried that the current betting in the futures market is suggesting that the Federal Reserve is not enthused about cutting its target for the Fed Funds rate any time soon,

but history shows that Value stocks, on average, have performed better both concurrent with and subsequent to a higher-than-normal Fed Funds rate versus a lower one.

No doubt, the latest inflation figures, with the Fed’s preferred measure, the Personal Consumption Expenditure Core (PCE) index, holding steady at 2.8%, versus expectations for a decline to 2.7%,

and the University of Michigan’s short-term inflation expectations rising to 3.2% this month from 2.9% in March, with longer-term expectations ticking up to 3.0%, didn’t help those hoping for Fed rate cuts.

However, history shows that Value stocks have performed well, on average, whether inflation is rising or falling, or whether it is high or low,

and the last time central bankers in the U.S. had a major battle with elevated consumer prices ended spectacularly well for equities in general and Value stocks in particular.

Econ News – Q1 GDP Below Expectations; Q2 Outlook Robust

To be sure, interest rates and the Fed are not the only thing troubling investors these days, as we learned last week that the first estimate of real (inflation-adjusted) U.S. GDP growth for Q1 rose a much-worse-than-expected 1.6%, though The New York Times asserted, “Economists were largely unconcerned by the slowdown, which stemmed mostly from big shifts in business inventories and international trade, components that often swing wildly from one quarter to the next. Measures of underlying demand were significantly stronger, offering no hint of the recession that forecasters spent much of last year warning was on the way.”

Further, the latest readings on new home sales for March at 693,000 came in better than the 668,000 consensus forecast,

pending home sales for March increased a much-better-than-expected 3.4% over February,

and first-time filings for unemployment benefits in the latest week fell to 207,000, lower than projections and a sign of continued strength in the labor market.

Personal income also rose 0.5% in March, in line with estimates,

while consumer spending climbed 0.8%, higher than the 0.6% projection,

adding support for the recent decline to 30% in the odds of recession over the next 12 months as tabulated by Bloomberg.

Earnings – Solid Growth Estimated in ’24 & ’25

More importantly, given that equity prices historically have appreciated over time as corporate profits have grown,

last week’s hefty batch of report cards turned in by Corporate America continued to show that Q1 results were terrific, with a greater-than-usual 80.6% of S&P 500 constituents topping bottom-line estimates so far this season.

True, forward guidance left a lot to be desired at some companies, but the outlook for growth in EPS this year and next remains solid, which would improve the E part of the Earnings to Price (Earnings Yield) equation and increase the likelihood of an increase in the D part of the Dividends to Price (Dividend Yield) calculation,

especially given that the first estimate for Q2 real GDP growth from the Atlanta Fed came in at a very robust 3.9%.

Volatility – Ups and Downs But Long-Term Trend is Up

Certainly, we have to be braced for equity market volatility, which is always part of the investment process,

and events on the geopolitical stage will always be a major wildcard, but stocks have also proved rewarding in the fullness of time,

Valuations – Inexpensive Metrics for TPS Portfolio

and we continue to sleep very well at night with the reasonable valuation metrics for our broadly diversified portfolios.

Stock News – Updates on sixteen stocks across ten different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.