The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Economic Outlook, Statistics, Interest Rates, Valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Portfolio Trades – 8 Transactions for 4 Accounts

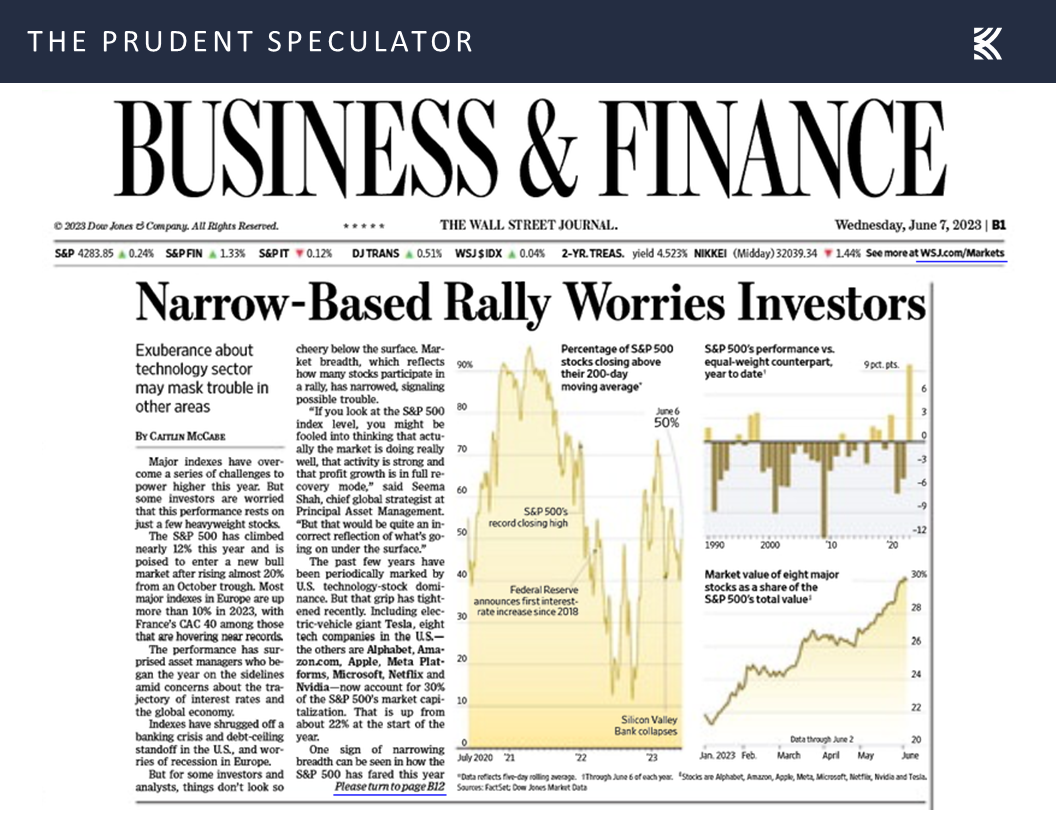

Market Breadth – Soldiers Beating the General in June

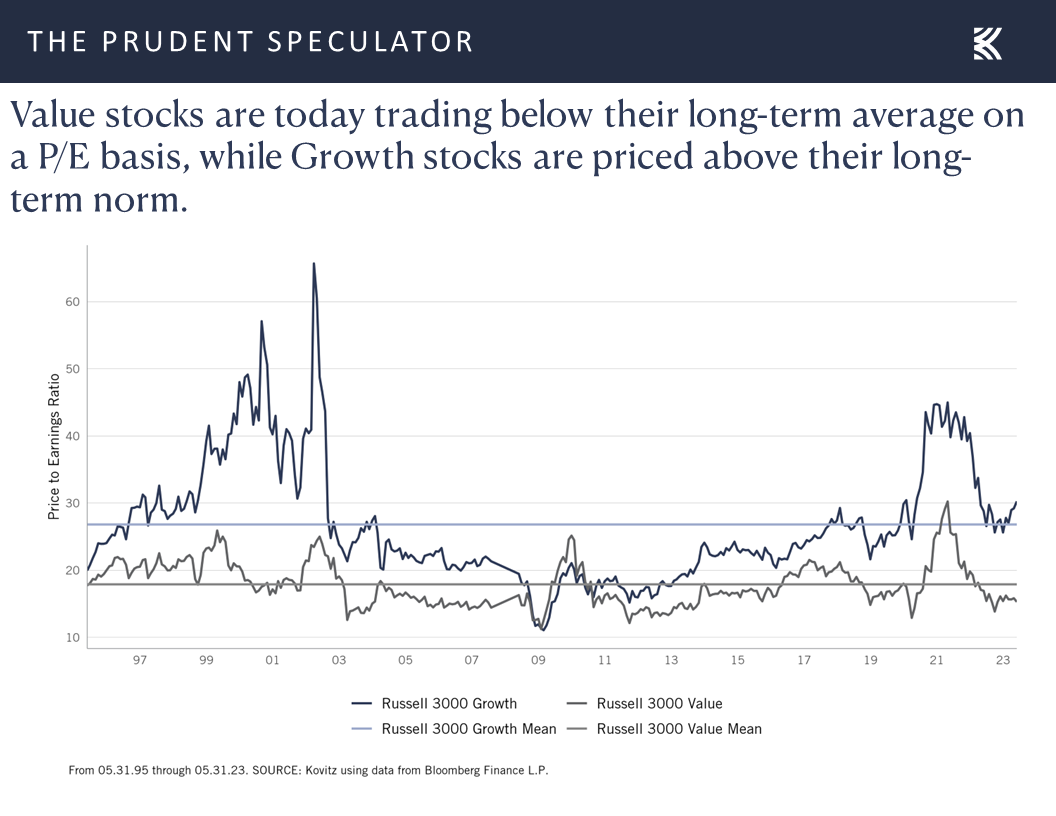

Valuations – Value Stocks Inexpensive by Historical Standards

Econ Outlook – World Bank Raises ’23 Outlook and Lowers ’24 Forecast

Econ Stats – Weaker-than-Expected Numbers but Growth Still the Q2 Projection

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

Sentiment – AAII Becomes Markedly More Bullish

Interest Rates – Fed Nearing the End of the Tightening Cycle; Long-Term Government Bond Yields Still Supportive of Equities

Stock News – Updates on Two-Dozen June Rebounders, including two additional stocks

Market Breadth – Soldiers Beating the General in June

While it has only been a handful of days, it is certainly nice to see the advance in equities broaden out in June, just as the financial press saw fit to highlight concerns about the narrow nature of the increase in the capitalization-weighted indexes this year.

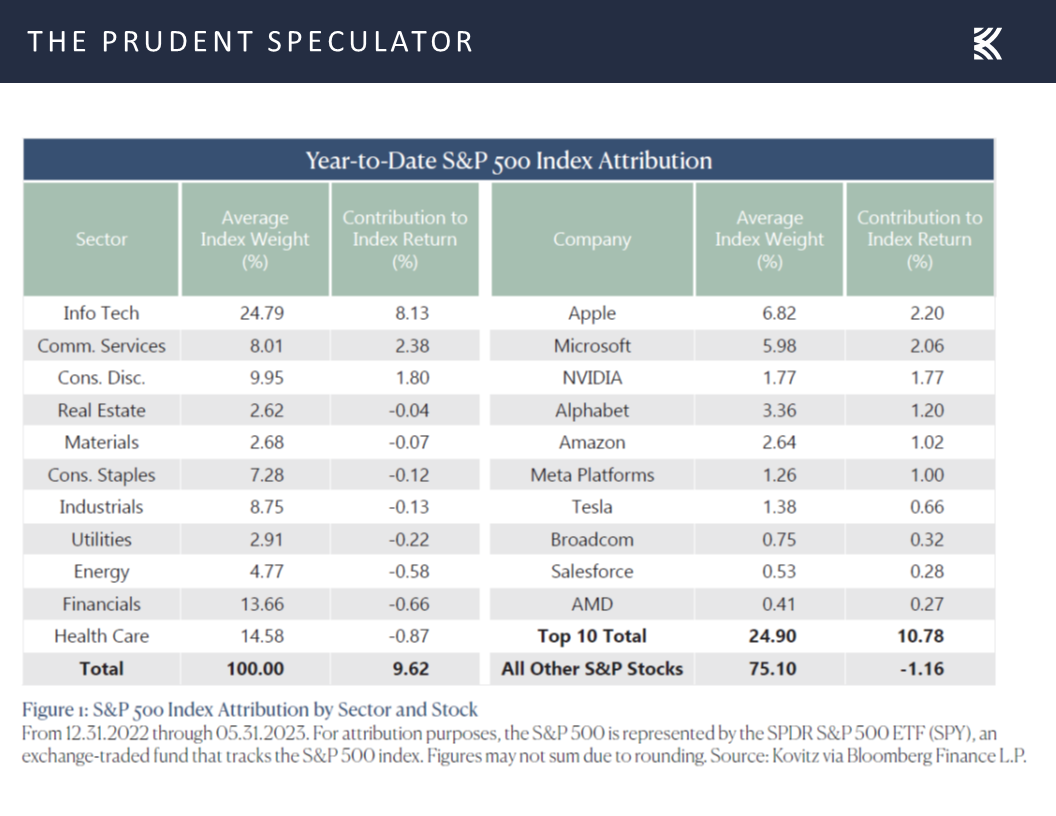

Believe it or not, through the first five months of the year, the top-10 stocks in the S&P 500 accounted for all the gains and then some, while the other 490 stocks suffered a negative average total return of 1.2%.

Happily, through the first nine day of June, the average stock in the S&P 500 has appreciated by 4.1%, compared to a 2.9% gain for the index. We think the outperformance of the proverbial soldiers over the generals makes a lot of sense and we believe it should continue, especially as the Value stock side of the ledger is trading below the long-term average on a P/E basis, while the Growth side, is priced above its long-term norm.

Valuations – Value Stocks Inexpensive by Historical Standards

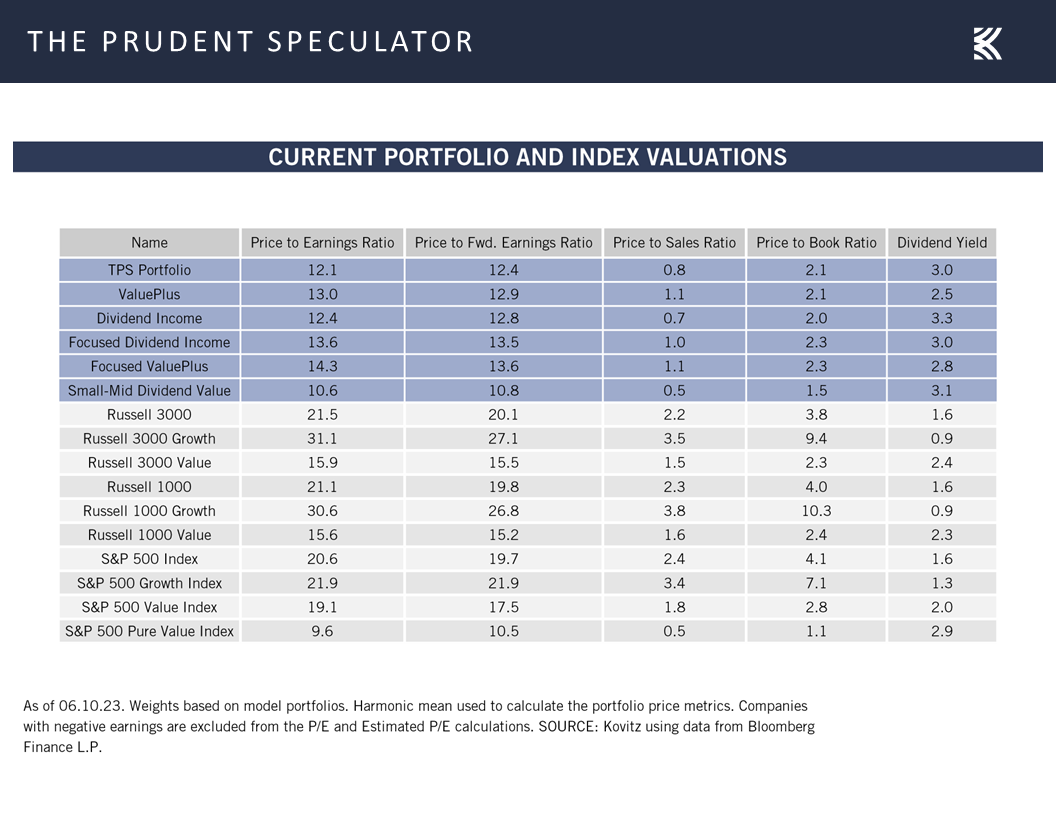

More importantly, we like that our broadly diversified portfolios of what we believe to be undervalued stocks are trading for very attractive valuation metrics and generous dividend yields,

while we continue to believe in the importance of not interrupting the miracle of compounding as the average annualized returns on equities over the years chain together to create massive capital appreciation over time.

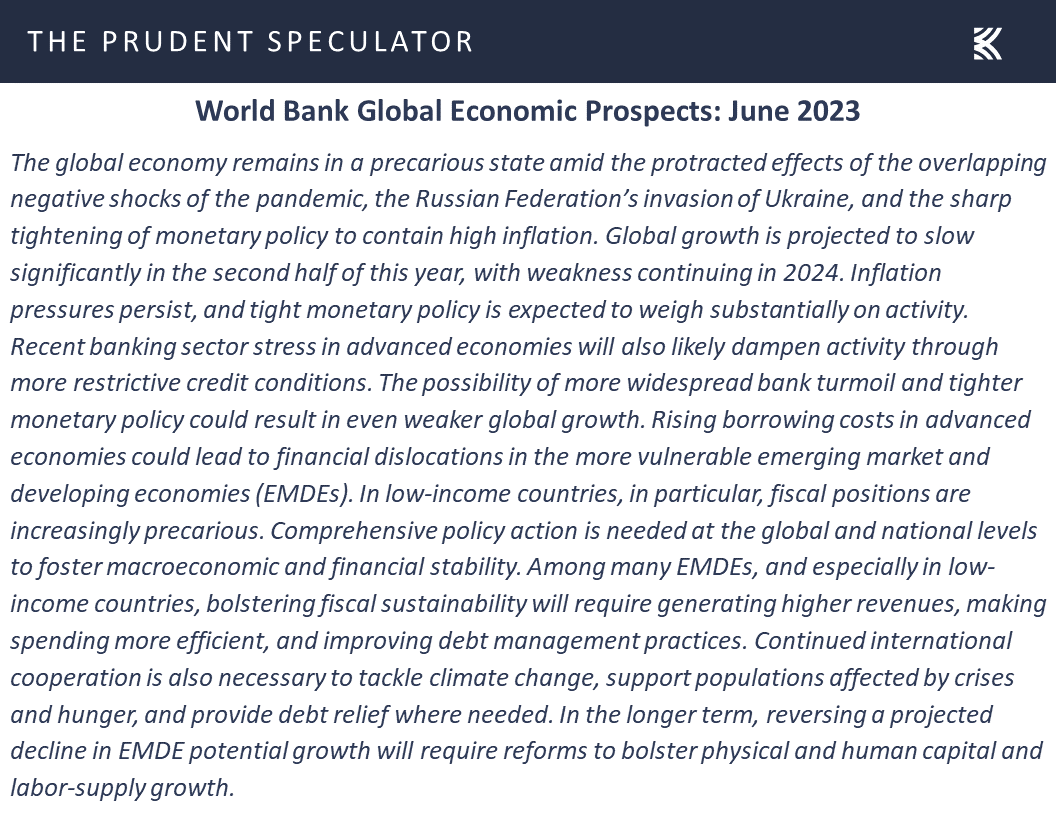

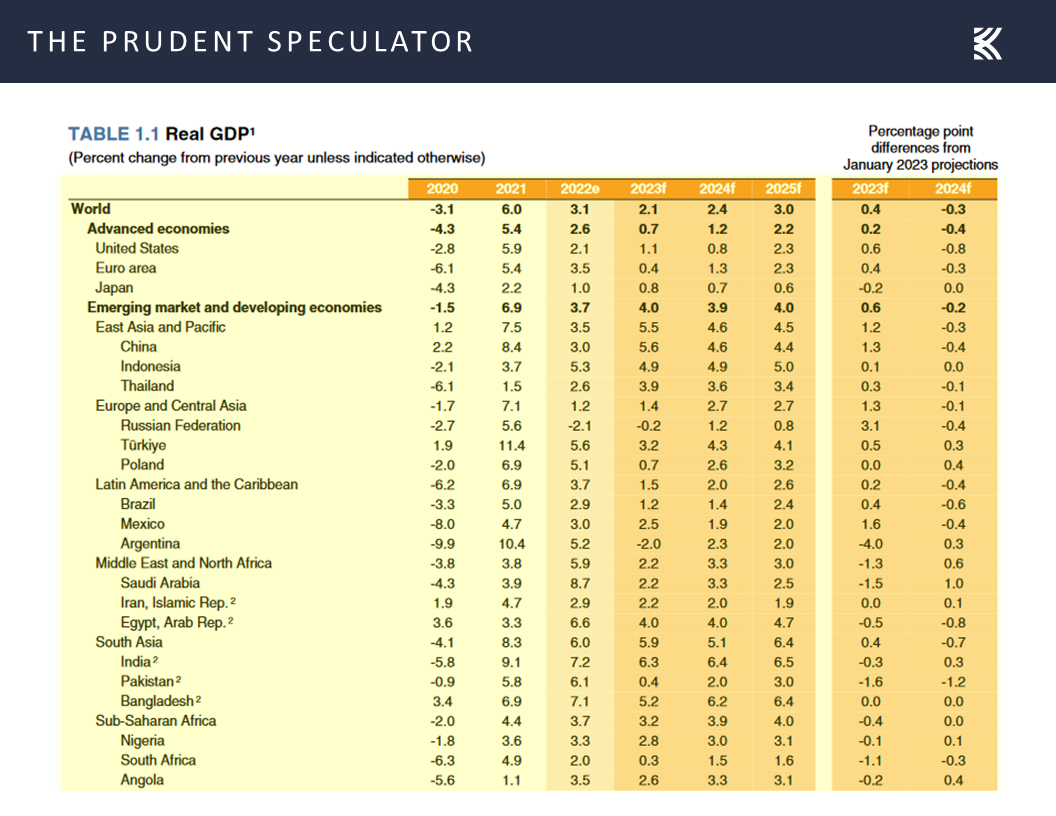

Econ Outlook – World Bank Raises ’23 Outlook and Lowers ’24 Forecast

We understand that it isn’t easy to constantly keep the faith, especially as question marks dominate the conversation on the health of the global economy. The World Bank last week updated its Global Economic Prospects report, offering the following Executive Summary,

and reducing the outlook for respective real (inflation-adjusted) World and U.S. GDP growth in 2024 to 2.4% and 0.8%.

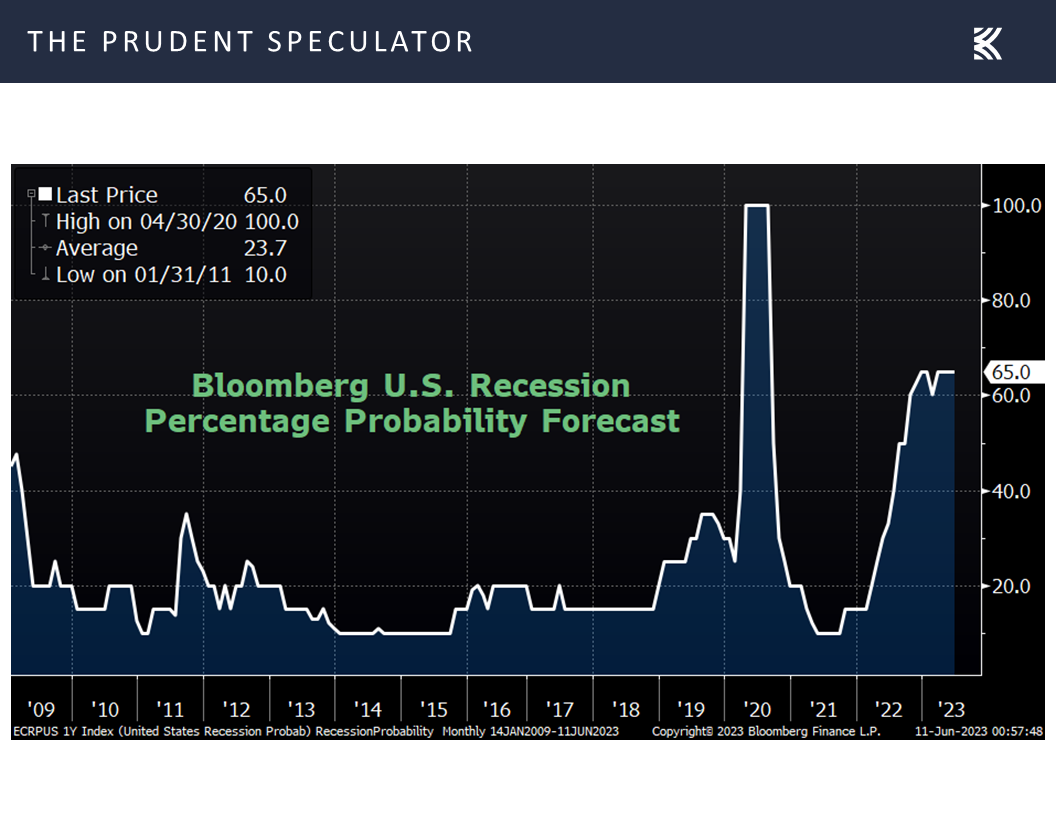

No doubt, those projections are unexciting, but the World Bank raised its 2023 estimates for real growth to 2.1% for the World and 1.1% for the U.S., up from the prior respective guesses of 1.7% and 0.5%. Of course, those figures do NOT represent a contraction of real GDP growth, which seemingly is in contradiction to the consensus view as data tabulated by Bloomberg continues to suggest a 65% probability of a recession in the U.S. over the next 12 months.

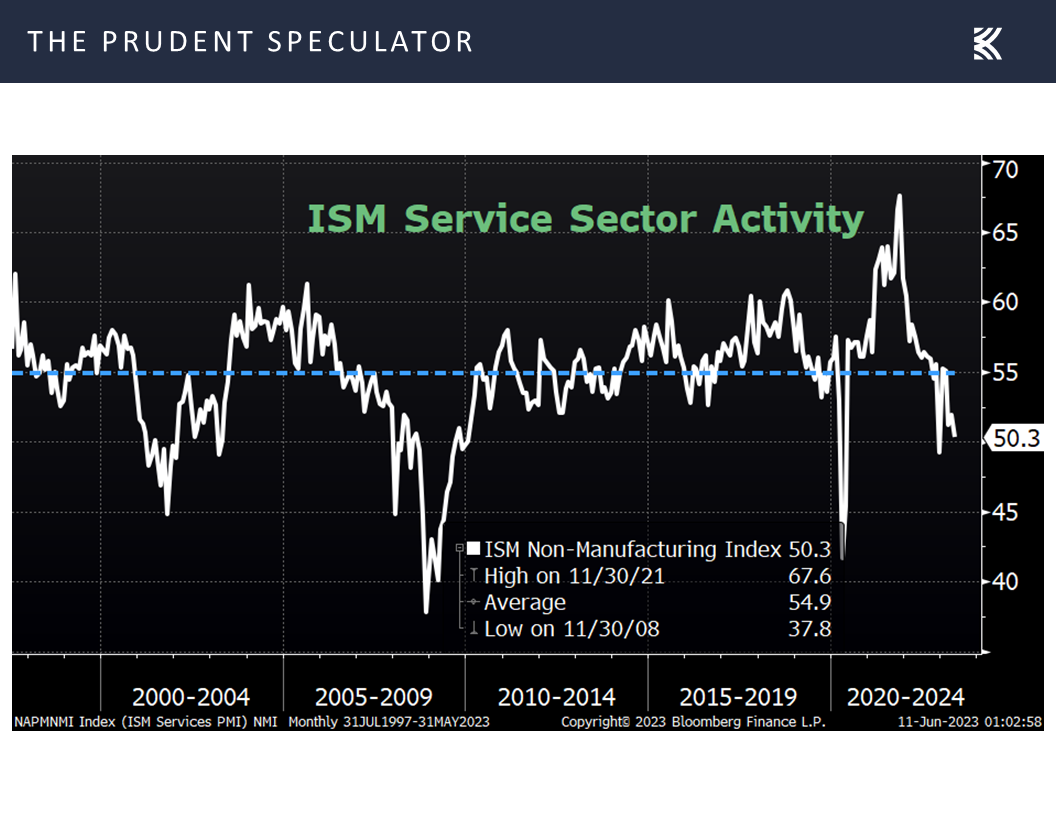

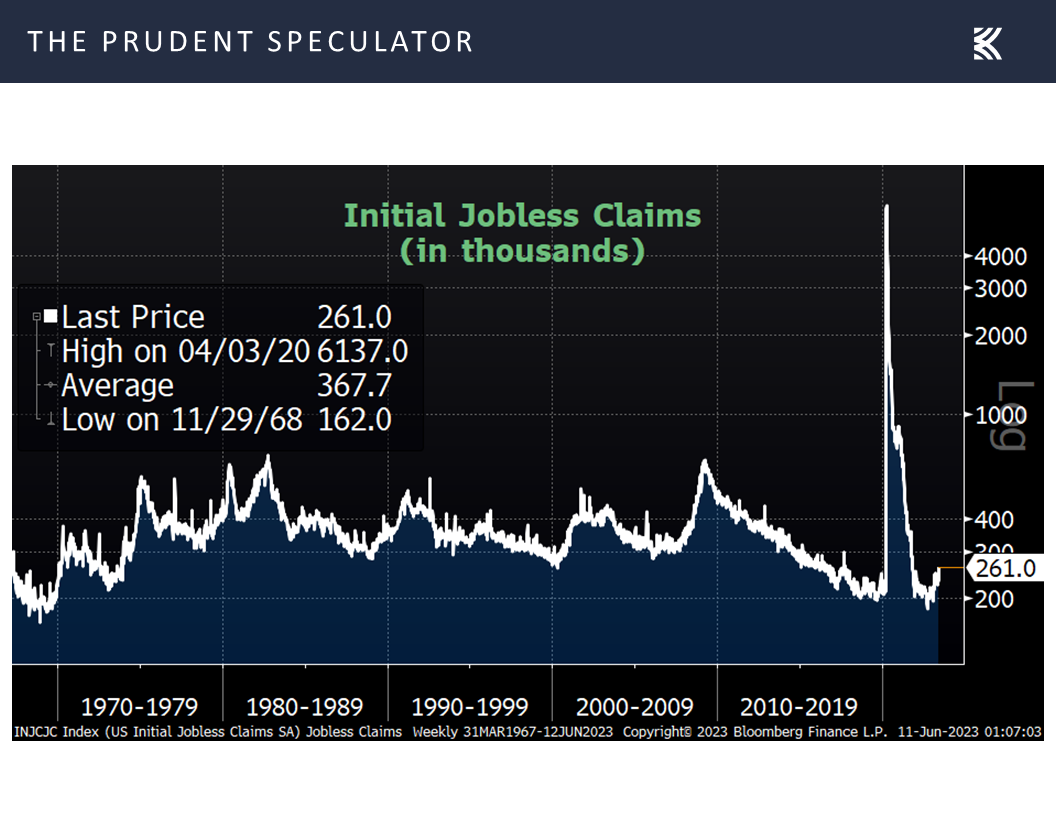

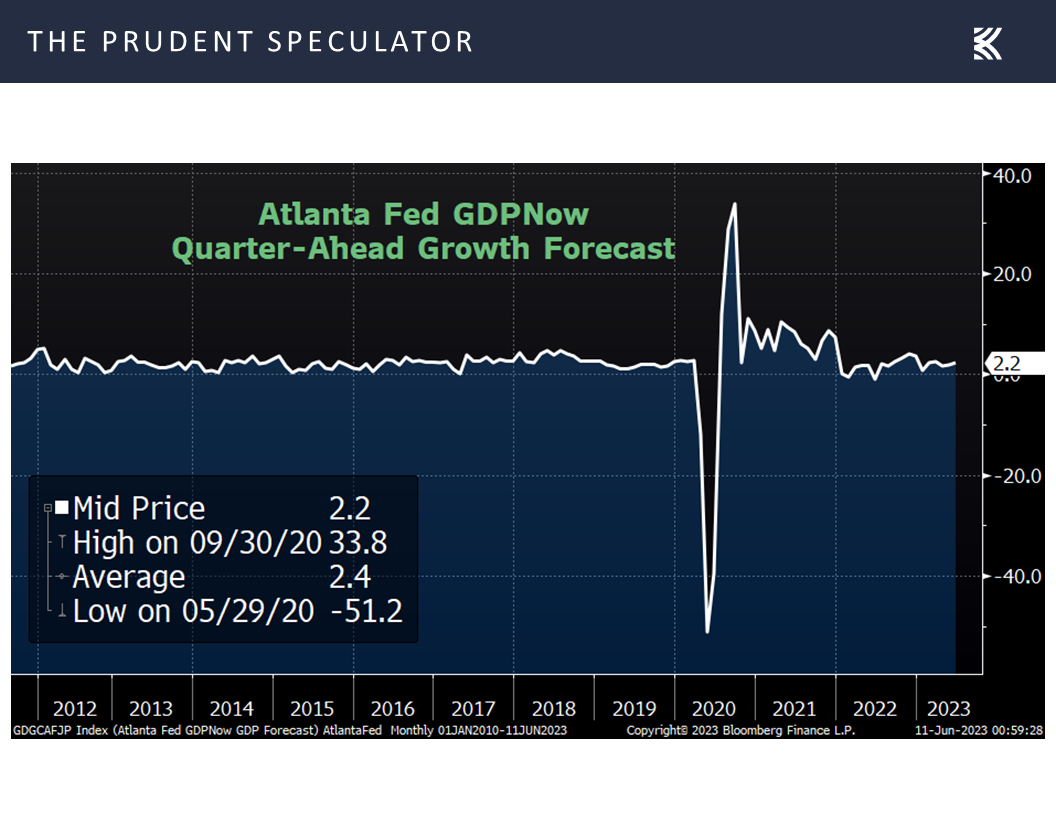

Econ Stats – Weaker-than-Expected Numbers but Growth Still the Q2 Projection

Anything can happen as we go forward and last week’s economic numbers saw a weaker-than-expected read on the health of the important services sector for May, with the Non-Manufacturing Index (NMI) coming in at 50.3, below forecasts of 52.3

and first-time filings for unemployment benefits in the latest week jump to a higher-than-projected 261,000.

However, the most recent estimate for Q2 real U.S. GDP growth (yes, growth!) from the Atlanta Fed stands at 2.2%,

while the economy has expanded on an inflation-adjusted basis for each of the last three quarters, despite a cacophony of voices arguing that a recession was around the corner.

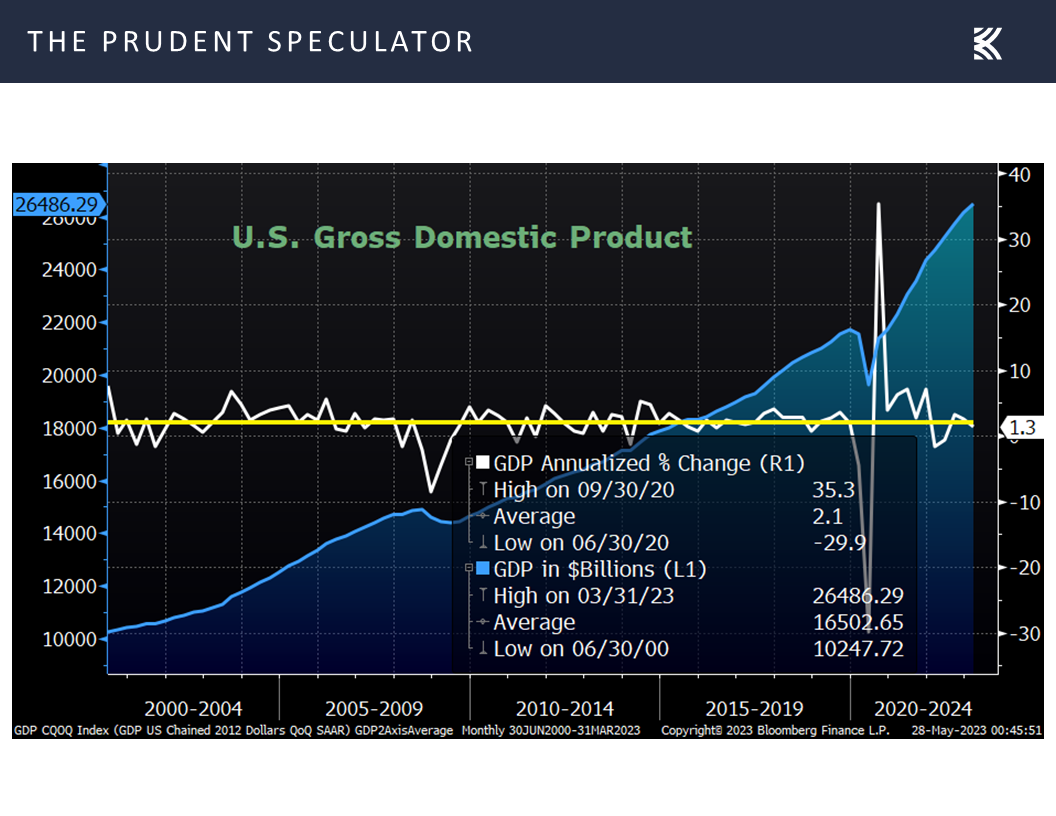

We also can’t overlook the fact that nominal GDP is likely to continue to rise significantly even if real GDP endures a modest contraction, which is why corporate profits (which are valued in nominal dollars) still are expected to show solid growth this year and next, based on projections from both Bloomberg and Standard & Poor’s.

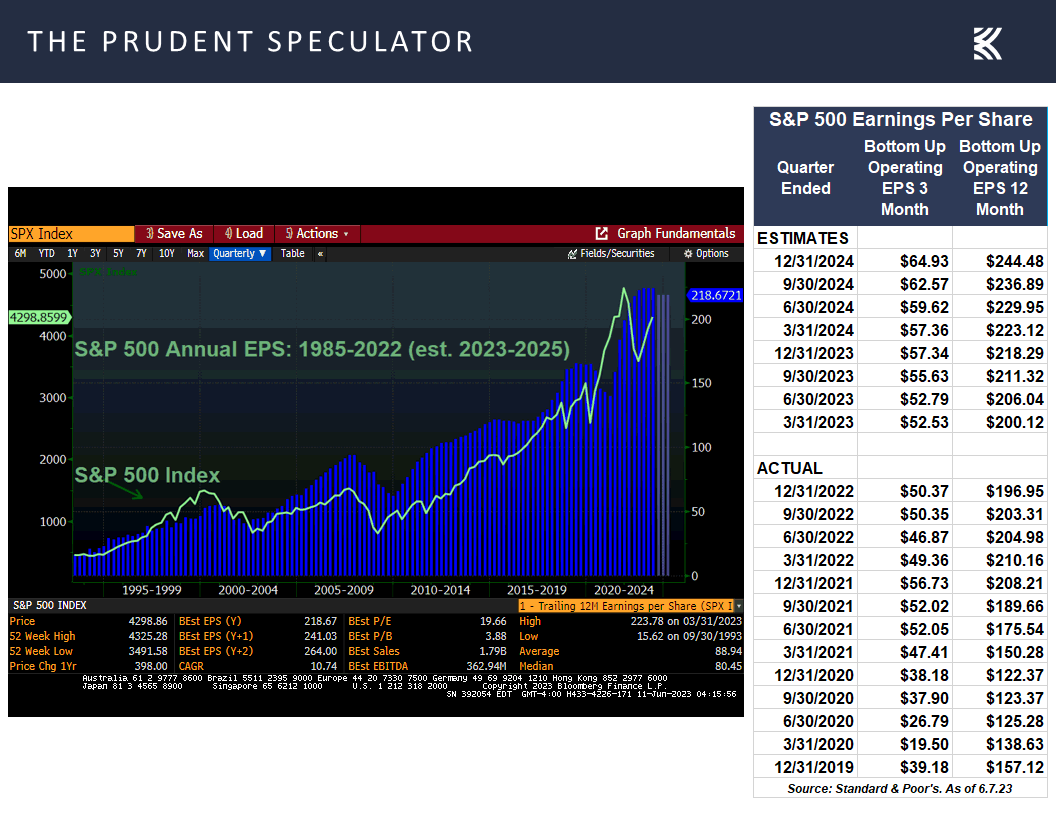

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

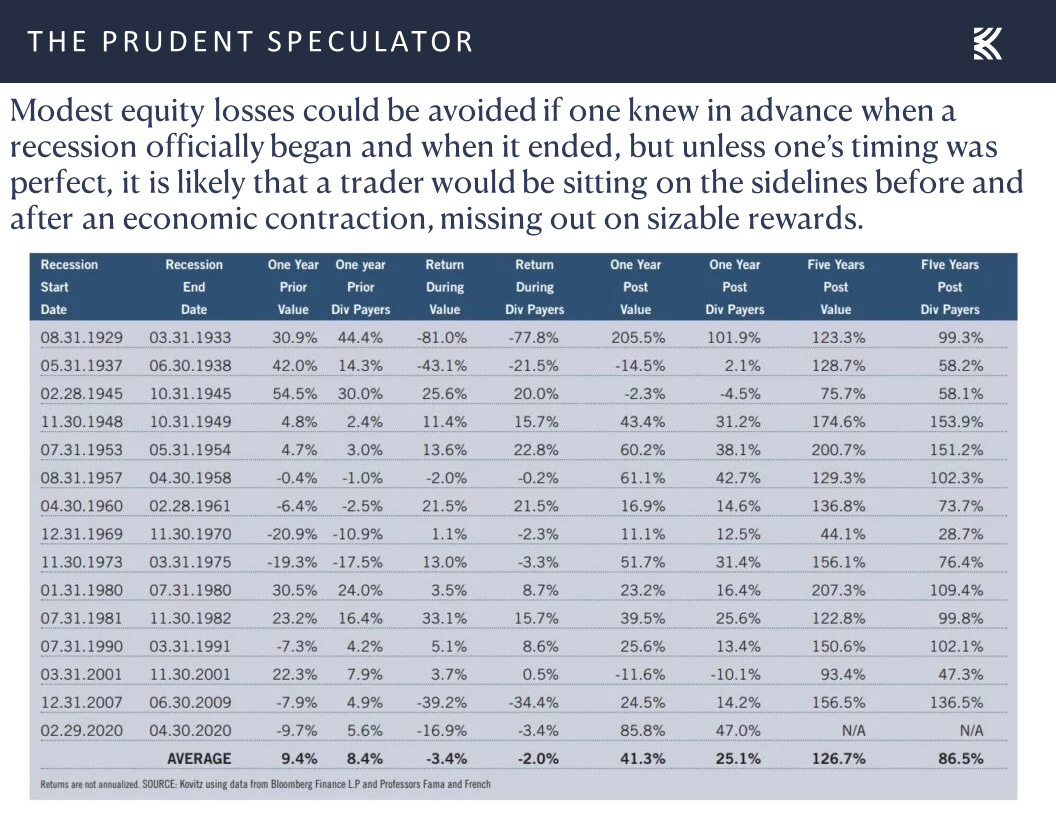

To be sure, those who are pessimistic on the economy could turn out to be correct and a recession may happen, but such an event, even if its start and end date could be known in advance, would not be reason for long-term-oriented investors to bail out of stocks. Yes, as the chart below shows, the prior 15 recessions have led to modest average losses for the kind of stocks we have long championed (Value and Dividend Payers) during the contractions, but the periods leading up to the economic downturns have been good on average, with 9.4% and 8.4% respective gains. And, most importantly, the year following a recession has been sensational, with an average 12-month advance for Value of 41.3%.

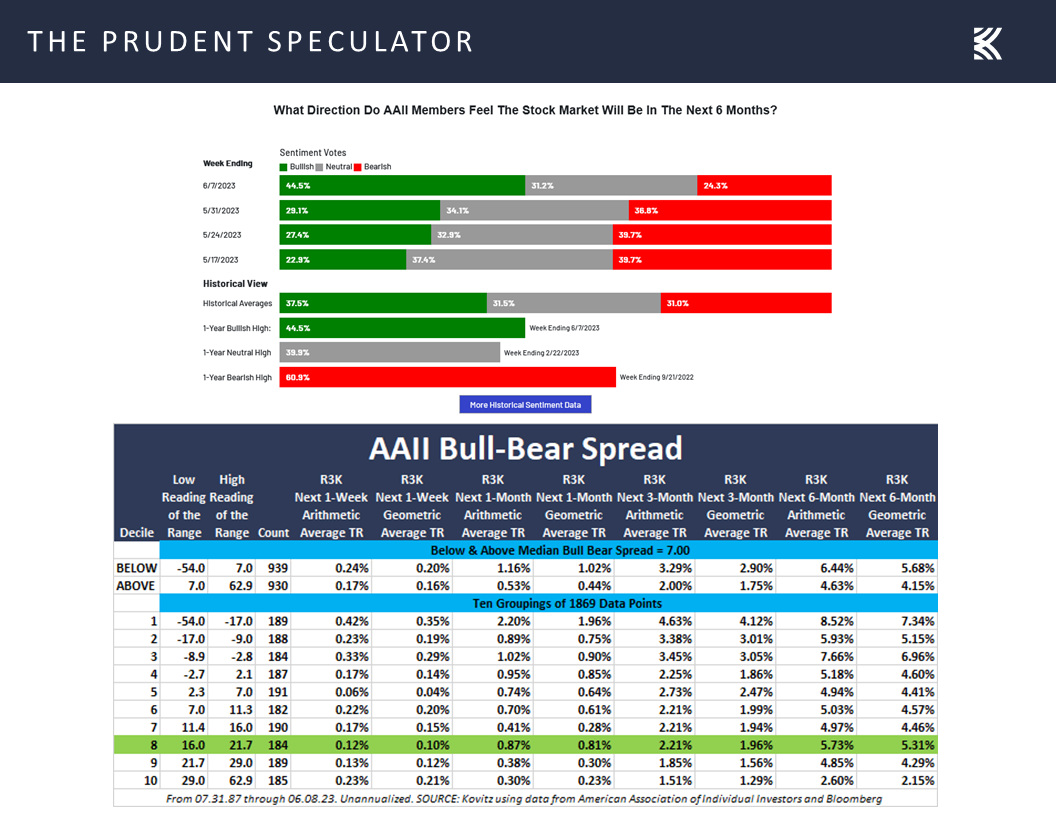

Sentiment – AAII Becomes Markedly More Bullish

We remain braced for volatility, especially as folks on Main Street became significantly more optimistic on the prospects for stocks over the next six months, with the contrarian AAII Sentiment index showing a 15.4-point jump in the number of Bulls and a 12.5-point drop in the tally of Bears last week.

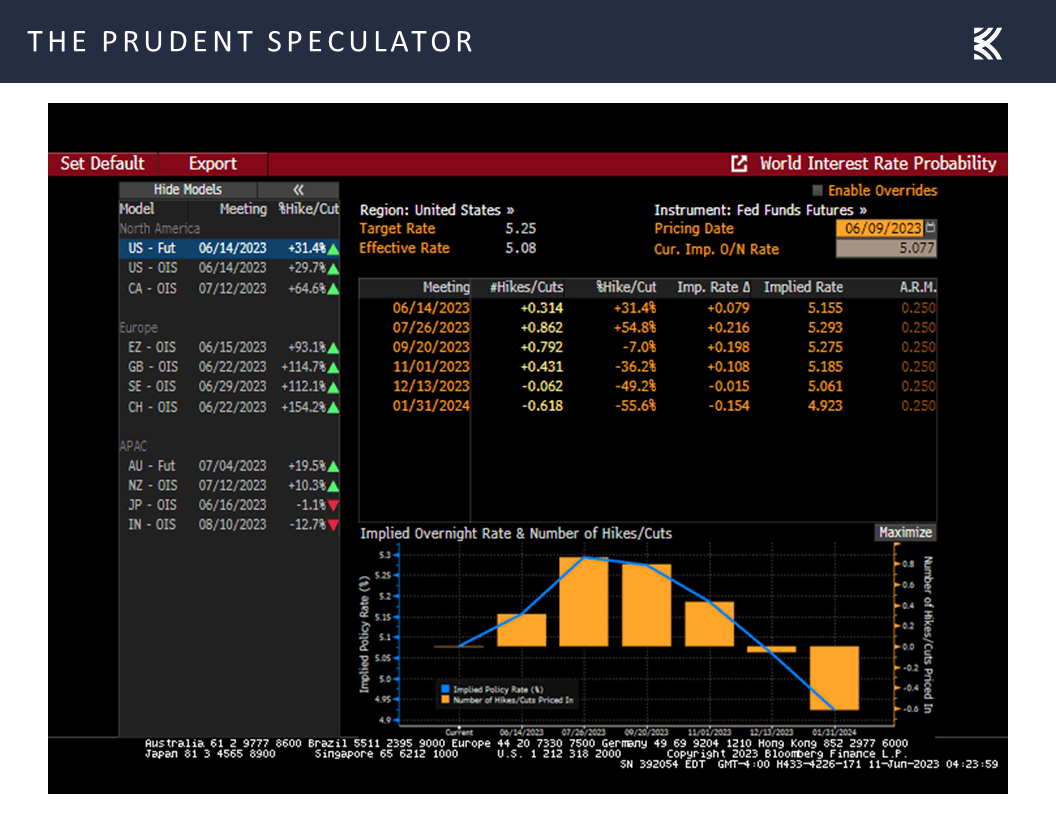

Interest Rates – Fed Nearing the End of the Tightening Cycle; Long-Term Government Bond Yields Still Supportive of Equities

True, the end of the debt-ceiling drama (at least until 2025) put a bounce in a few steps, but there is a big Fed meeting and announcement on interest rates this week. On that score, there is plenty for investors to worry about, even as we think Jerome H. Powell & Co. are nearing the end of the rate-hiking cycle,

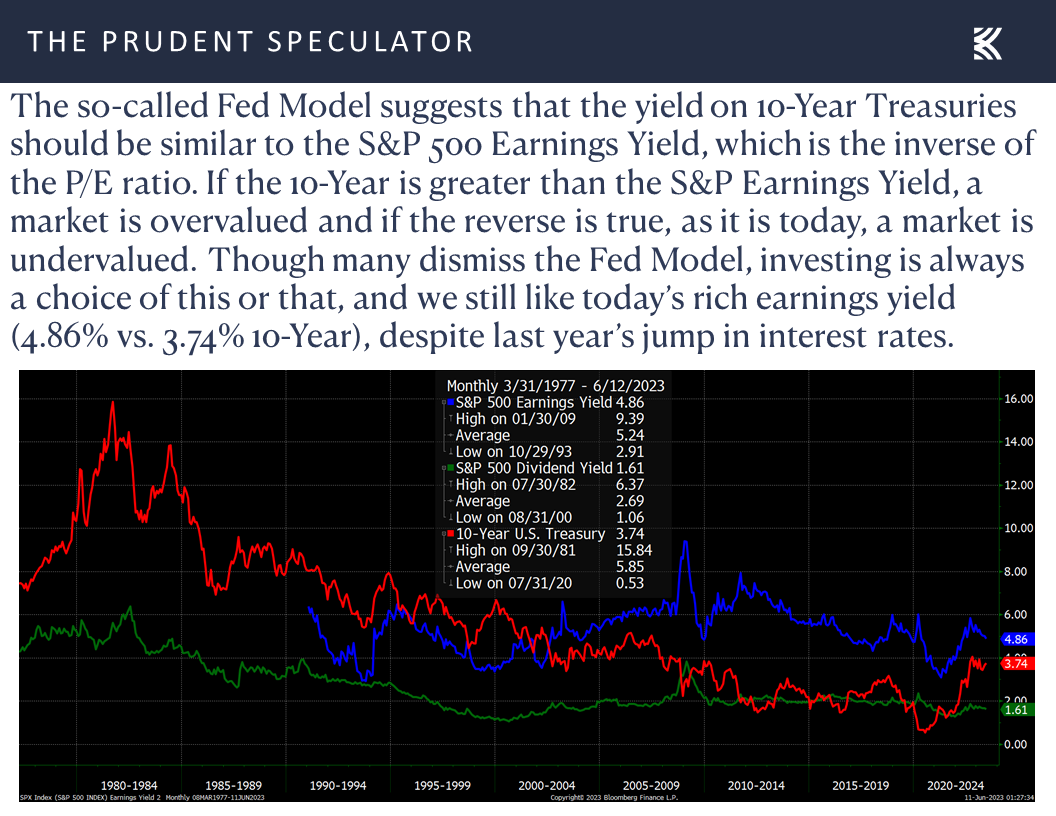

while we continue to argue that long-term government bond yields are low by historical standards, providing valuation support for stocks.

Stock News – Updates on Two-Dozen June Rebounders, including two additional stocks

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Economic Outlook, Statistics, Interest Rates, Valuations and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Economic Outlook, Statistics, Interest Rates, Valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Portfolio Trades – 8 Transactions for 4 Accounts

Market Breadth – Soldiers Beating the General in June

Valuations – Value Stocks Inexpensive by Historical Standards

Econ Outlook – World Bank Raises ’23 Outlook and Lowers ’24 Forecast

Econ Stats – Weaker-than-Expected Numbers but Growth Still the Q2 Projection

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

Sentiment – AAII Becomes Markedly More Bullish

Interest Rates – Fed Nearing the End of the Tightening Cycle; Long-Term Government Bond Yields Still Supportive of Equities

Stock News – Updates on Two-Dozen June Rebounders, including two additional stocks

Market Breadth – Soldiers Beating the General in June

While it has only been a handful of days, it is certainly nice to see the advance in equities broaden out in June, just as the financial press saw fit to highlight concerns about the narrow nature of the increase in the capitalization-weighted indexes this year.

Believe it or not, through the first five months of the year, the top-10 stocks in the S&P 500 accounted for all the gains and then some, while the other 490 stocks suffered a negative average total return of 1.2%.

Happily, through the first nine day of June, the average stock in the S&P 500 has appreciated by 4.1%, compared to a 2.9% gain for the index. We think the outperformance of the proverbial soldiers over the generals makes a lot of sense and we believe it should continue, especially as the Value stock side of the ledger is trading below the long-term average on a P/E basis, while the Growth side, is priced above its long-term norm.

Valuations – Value Stocks Inexpensive by Historical Standards

More importantly, we like that our broadly diversified portfolios of what we believe to be undervalued stocks are trading for very attractive valuation metrics and generous dividend yields,

while we continue to believe in the importance of not interrupting the miracle of compounding as the average annualized returns on equities over the years chain together to create massive capital appreciation over time.

Econ Outlook – World Bank Raises ’23 Outlook and Lowers ’24 Forecast

We understand that it isn’t easy to constantly keep the faith, especially as question marks dominate the conversation on the health of the global economy. The World Bank last week updated its Global Economic Prospects report, offering the following Executive Summary,

and reducing the outlook for respective real (inflation-adjusted) World and U.S. GDP growth in 2024 to 2.4% and 0.8%.

No doubt, those projections are unexciting, but the World Bank raised its 2023 estimates for real growth to 2.1% for the World and 1.1% for the U.S., up from the prior respective guesses of 1.7% and 0.5%. Of course, those figures do NOT represent a contraction of real GDP growth, which seemingly is in contradiction to the consensus view as data tabulated by Bloomberg continues to suggest a 65% probability of a recession in the U.S. over the next 12 months.

Econ Stats – Weaker-than-Expected Numbers but Growth Still the Q2 Projection

Anything can happen as we go forward and last week’s economic numbers saw a weaker-than-expected read on the health of the important services sector for May, with the Non-Manufacturing Index (NMI) coming in at 50.3, below forecasts of 52.3

and first-time filings for unemployment benefits in the latest week jump to a higher-than-projected 261,000.

However, the most recent estimate for Q2 real U.S. GDP growth (yes, growth!) from the Atlanta Fed stands at 2.2%,

while the economy has expanded on an inflation-adjusted basis for each of the last three quarters, despite a cacophony of voices arguing that a recession was around the corner.

We also can’t overlook the fact that nominal GDP is likely to continue to rise significantly even if real GDP endures a modest contraction, which is why corporate profits (which are valued in nominal dollars) still are expected to show solid growth this year and next, based on projections from both Bloomberg and Standard & Poor’s.

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

To be sure, those who are pessimistic on the economy could turn out to be correct and a recession may happen, but such an event, even if its start and end date could be known in advance, would not be reason for long-term-oriented investors to bail out of stocks. Yes, as the chart below shows, the prior 15 recessions have led to modest average losses for the kind of stocks we have long championed (Value and Dividend Payers) during the contractions, but the periods leading up to the economic downturns have been good on average, with 9.4% and 8.4% respective gains. And, most importantly, the year following a recession has been sensational, with an average 12-month advance for Value of 41.3%.

Sentiment – AAII Becomes Markedly More Bullish

We remain braced for volatility, especially as folks on Main Street became significantly more optimistic on the prospects for stocks over the next six months, with the contrarian AAII Sentiment index showing a 15.4-point jump in the number of Bulls and a 12.5-point drop in the tally of Bears last week.

Interest Rates – Fed Nearing the End of the Tightening Cycle; Long-Term Government Bond Yields Still Supportive of Equities

True, the end of the debt-ceiling drama (at least until 2025) put a bounce in a few steps, but there is a big Fed meeting and announcement on interest rates this week. On that score, there is plenty for investors to worry about, even as we think Jerome H. Powell & Co. are nearing the end of the rate-hiking cycle,

while we continue to argue that long-term government bond yields are low by historical standards, providing valuation support for stocks.

Stock News – Updates on Two-Dozen June Rebounders, including two additional stocks

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.