The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss economic updates, valuations, volatility and sentiment. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 10 Buys for 4 Portfolios

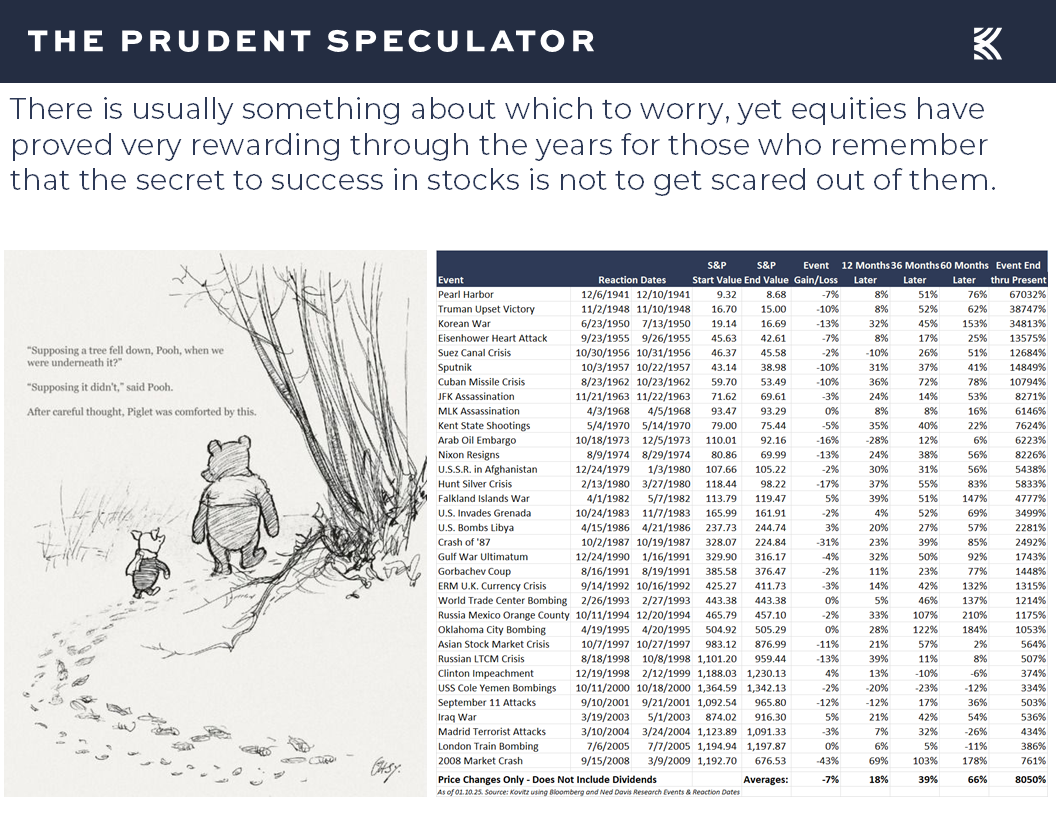

Headlines – 2025 Off to a Miserable Start but Stocks Always Have Overcome Disconcerting Events in the Fullness of Time

Calendar – First 5 Days, Seasonality, Years Ending in 5 Historical Numbers

Econ Update – Better-than-Expected Numbers, Solid Growth Outlook Intact

Corporate Profits – Healthy EPS Growth Still the Forecast

Interest Rates – Stocks Have Performed Fine, on Average, No Matter the Direction of Rates

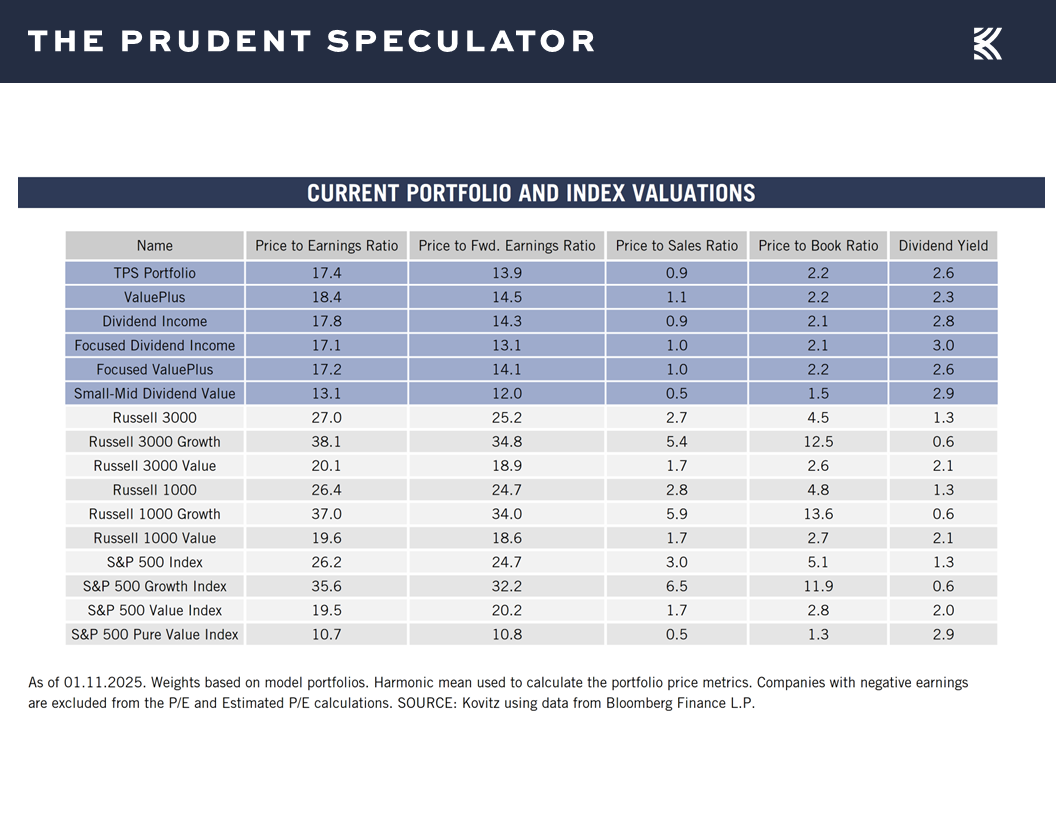

Valuations – Value Stocks Remain Reasonably Priced

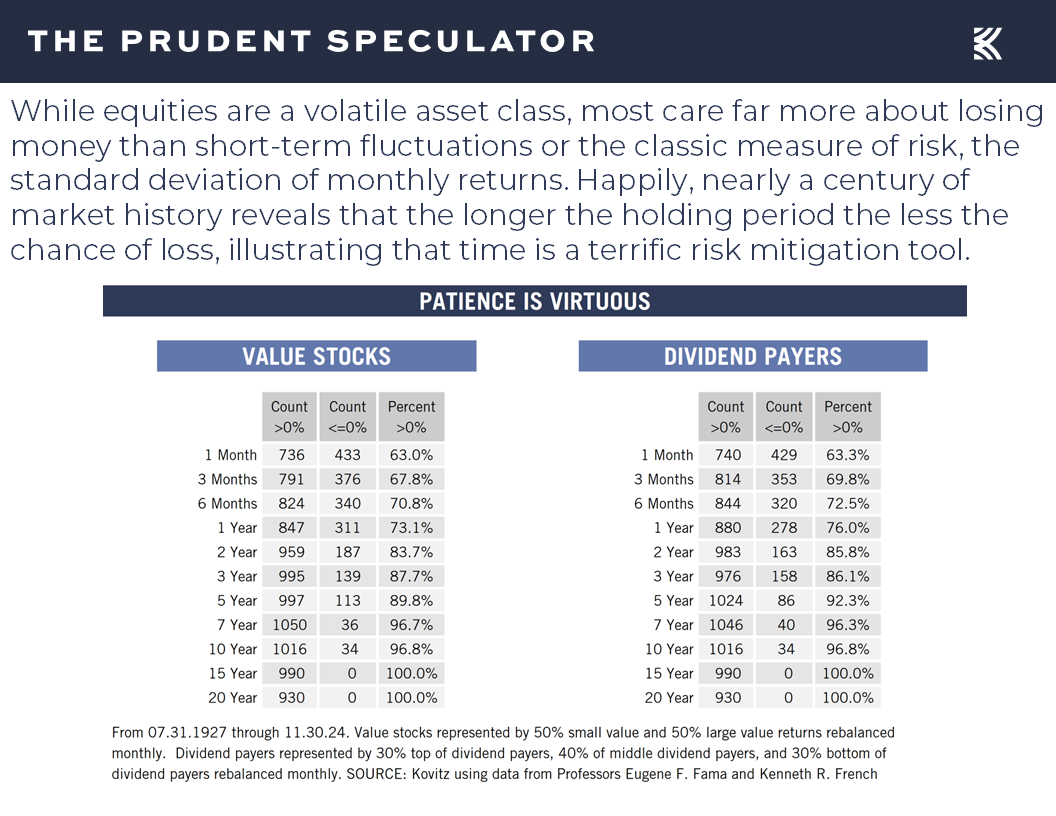

Volatility – The Longer the Measuring Stick the Lower the Chance of Loss

Sentiment – AAII Bullishness Retreats

Stock News – Updates on ALL, GBX, XOM & JNJ

Headlines – 2025 Off to a Miserable Start but Stocks Always Have Overcome Disconcerting Events in the Fullness of Time

We want to thank the folks who have reached out to check on us. The Los Angeles wildfires are some 60 miles to the north of our offices, so we are a fair distance from the cataclysmic scenes. Still, the air quality isn’t great and those who have been followers of the newsletter for several decades likely will remember that we had three different Al Frank offices in Santa Monica, with our founder owning a home on Montana Avenue, with all those locations just south of Pacific Palisades.

Obviously, equity market gyrations are insignificant relative to the tragedy still unfolding to the north of us, and 2025 isn’t exactly off to a good start on the humanity front,

but we always endeavor to keep emotions out of the investment equation as we live by the Vannevar Bush admonition, “Fear can not be banished, but it can be calm and without panic; it can be mitigated by reason and evaluation.” After all, we know that stocks throughout history have always overcome every disconcerting event in the fullness of time,

with the inevitable trips to the downside followed by even greater moves to the upside, so much so that long-term performance since the launch of The Prudent Speculator in March 1977 have been terrific, including returns on Value stocks of some 14% per annum through the end of November 2024.

Calendar – First 5 Days, Seasonality, Years Ending in 5 Historical Numbers

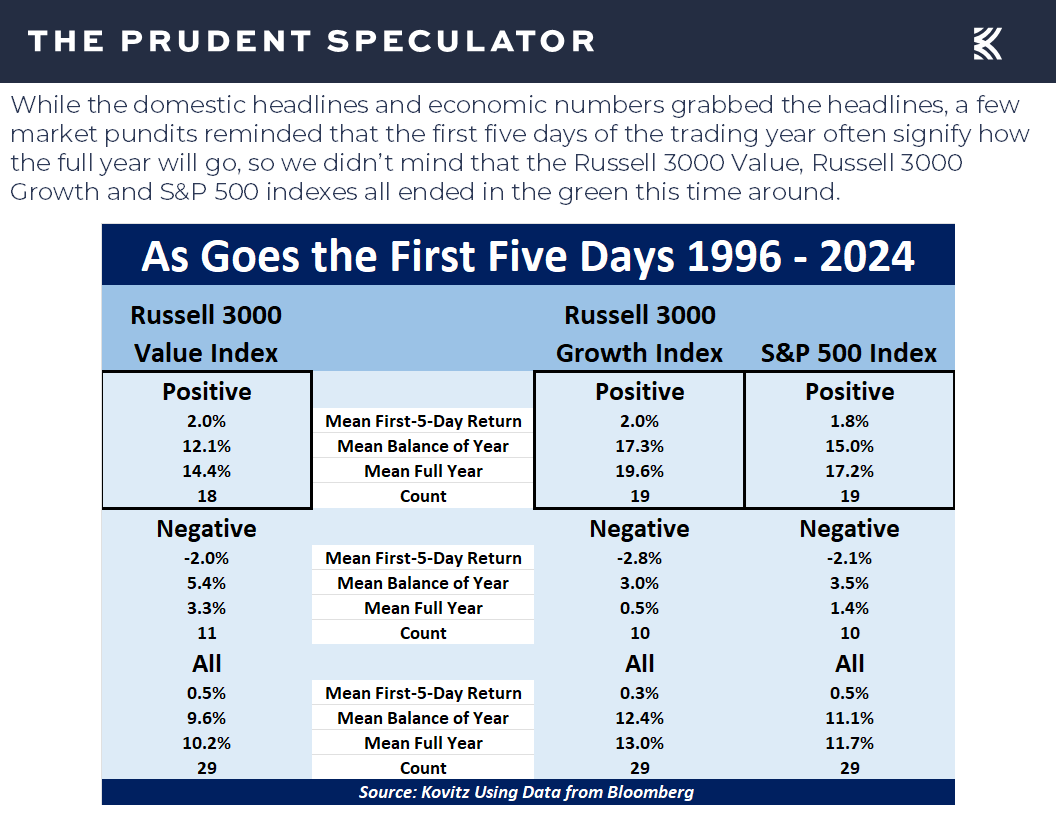

Of course, until Friday, equities generally had shaken off the awful 2025 headlines, with the first five days of trading in the new year showing gains on the major market averages, an indicator that some argue bodes well for returns this year,

while we continue to reside in the seasonally more favorable six months of the year,

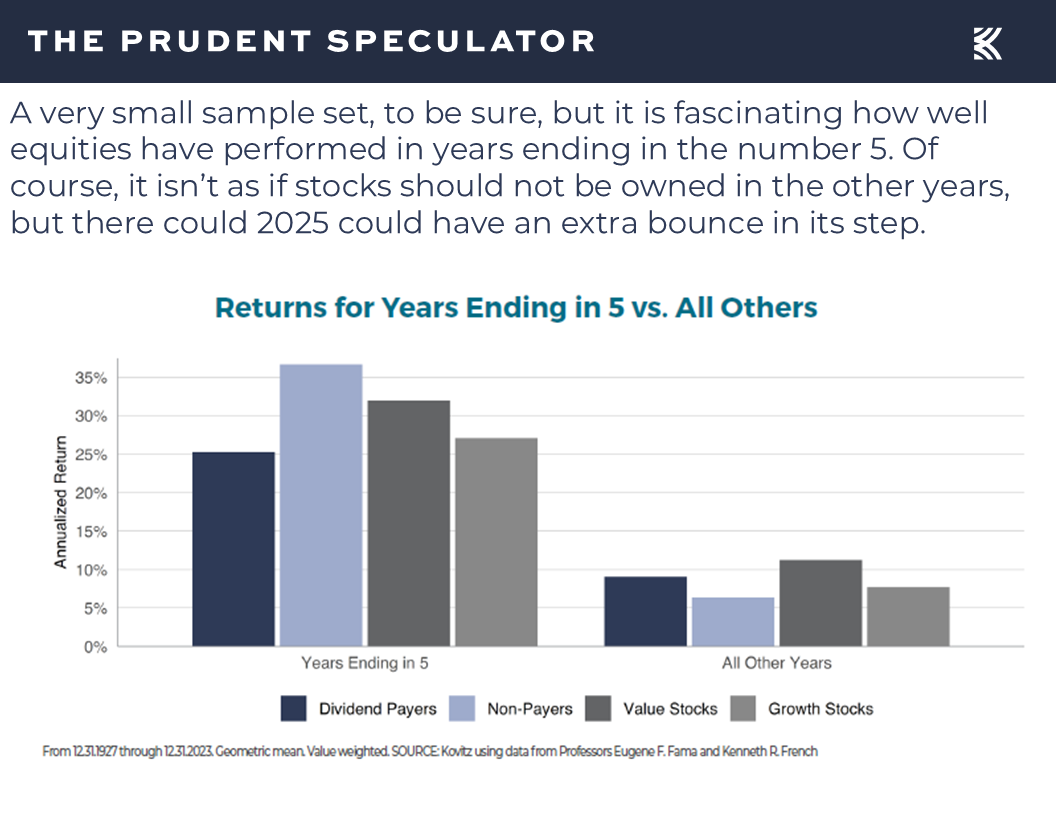

and years ending in 5 historically have been very good, on average.

Econ Update – Better-than-Expected Numbers, Solid Growth Outlook Intact

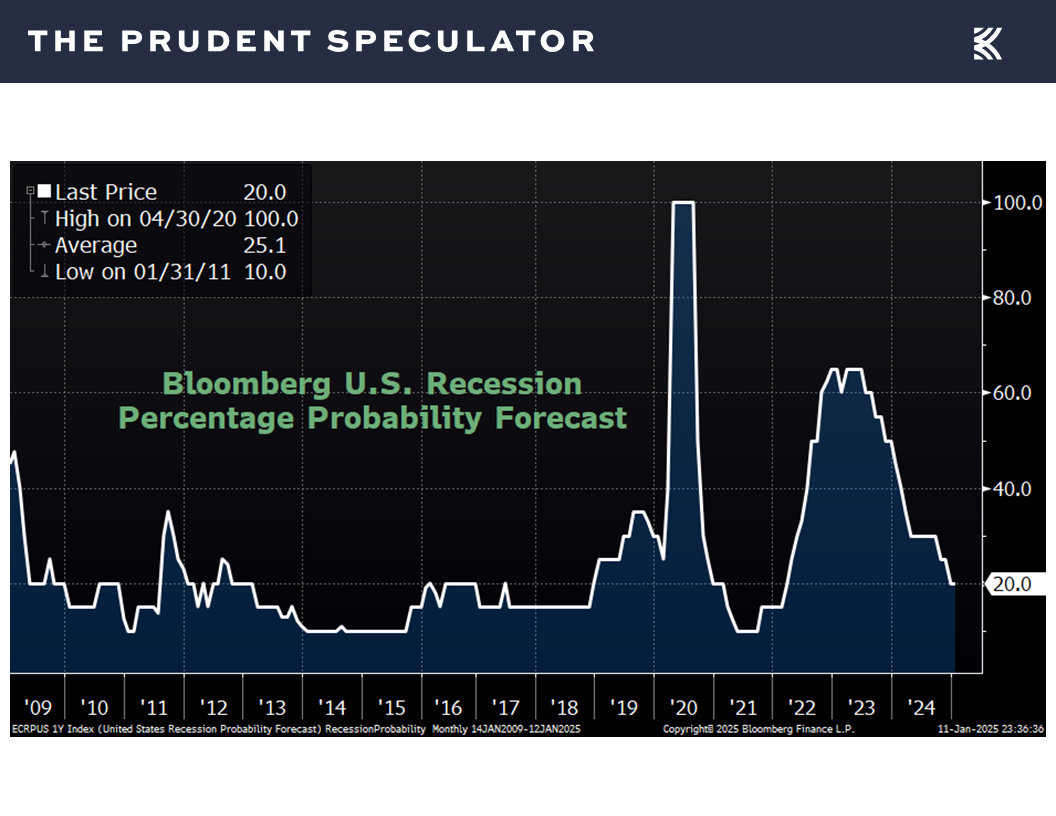

More importantly, the U.S. economy remains in solid shape, with Bloomberg’s current tabulation of recession probability residing at a very low 20%,

and the latest estimate from the Atlanta Fed for Q4 real (inflation-adjusted) GDP growth moving up last week to 2.7%.

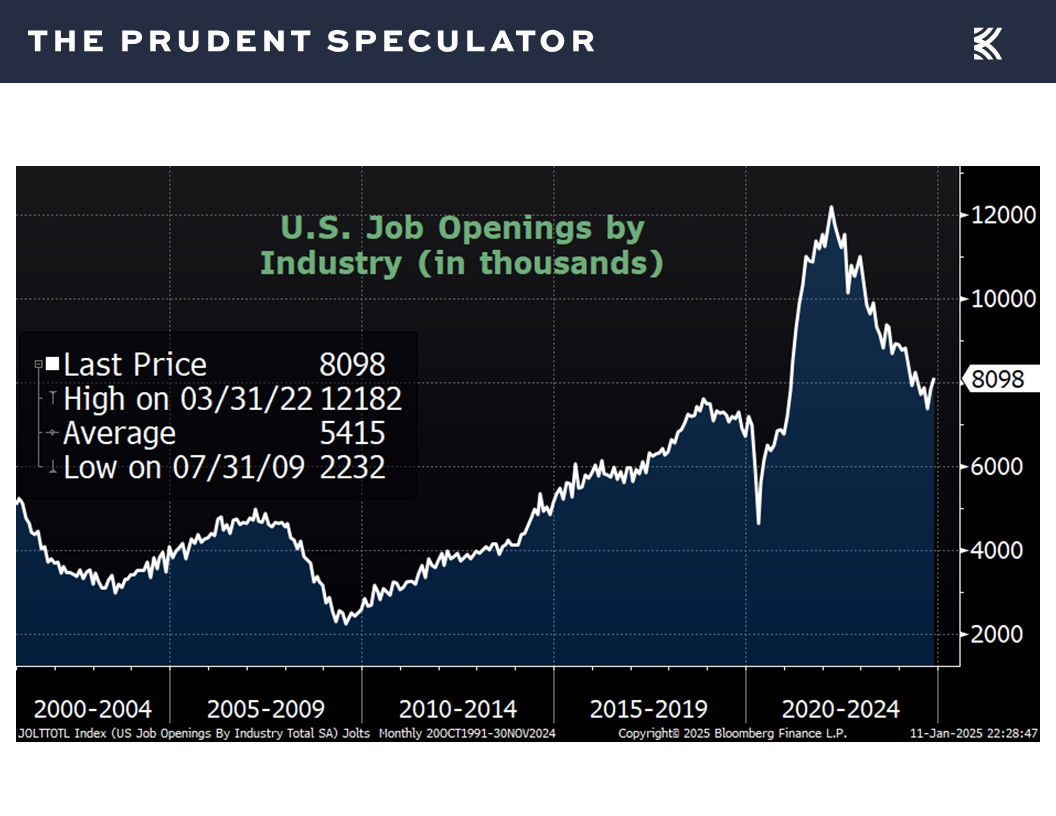

That GDP projection included a greater-than expected 8.1 million job openings in November,

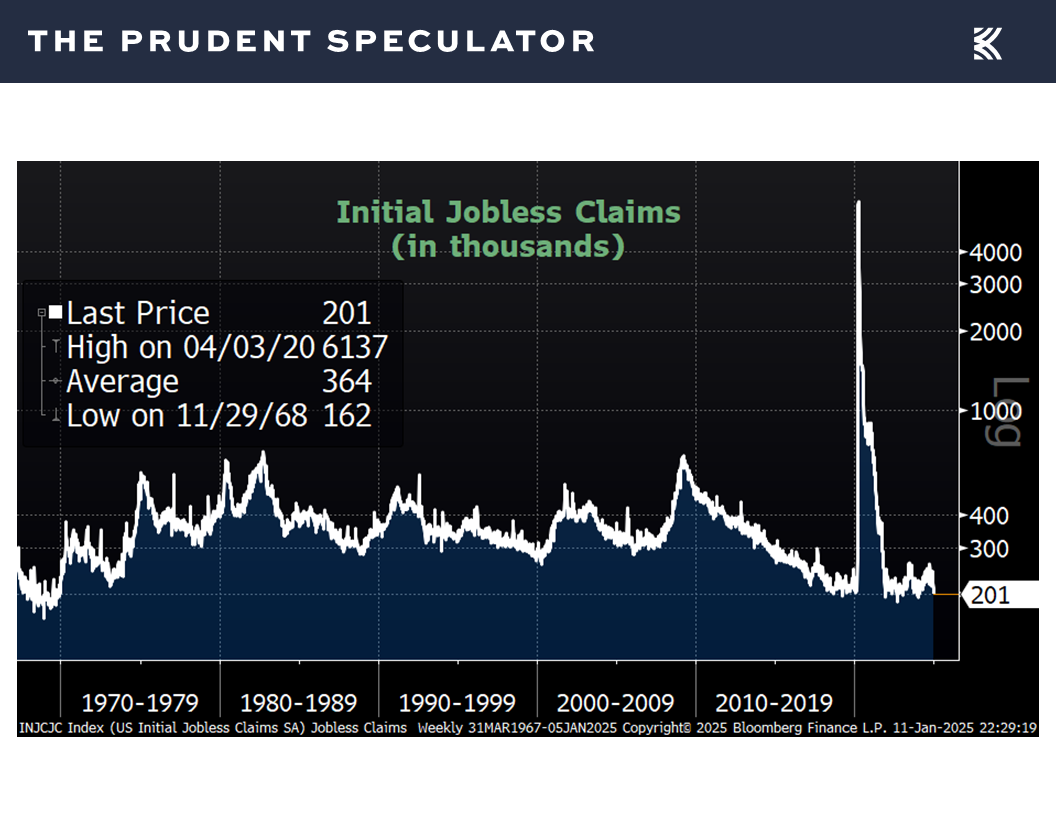

another drop in weekly first-time filings for jobless benefits,

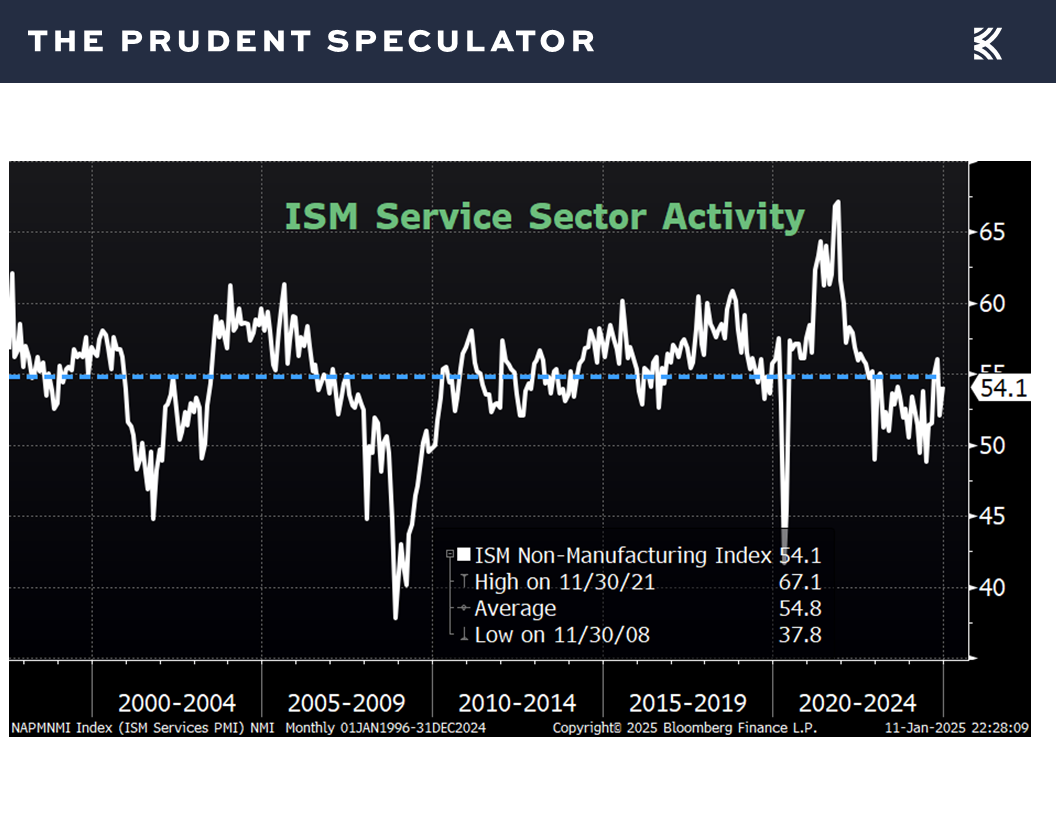

and a better-than-forecast increase in the ISM Non-Manufacturing Index for December to a reading of 54.1, up from 52.1 in November.

However, the Atlanta Fed projection did not include Friday’s significantly higher-than-forecast rise of 256,000 in nonfarm payrolls for December, well above estimates of a 165,000 increase and the revised tally for November of 212,000,

which led to a lower-than-estimated jobless rate of 4.1%.

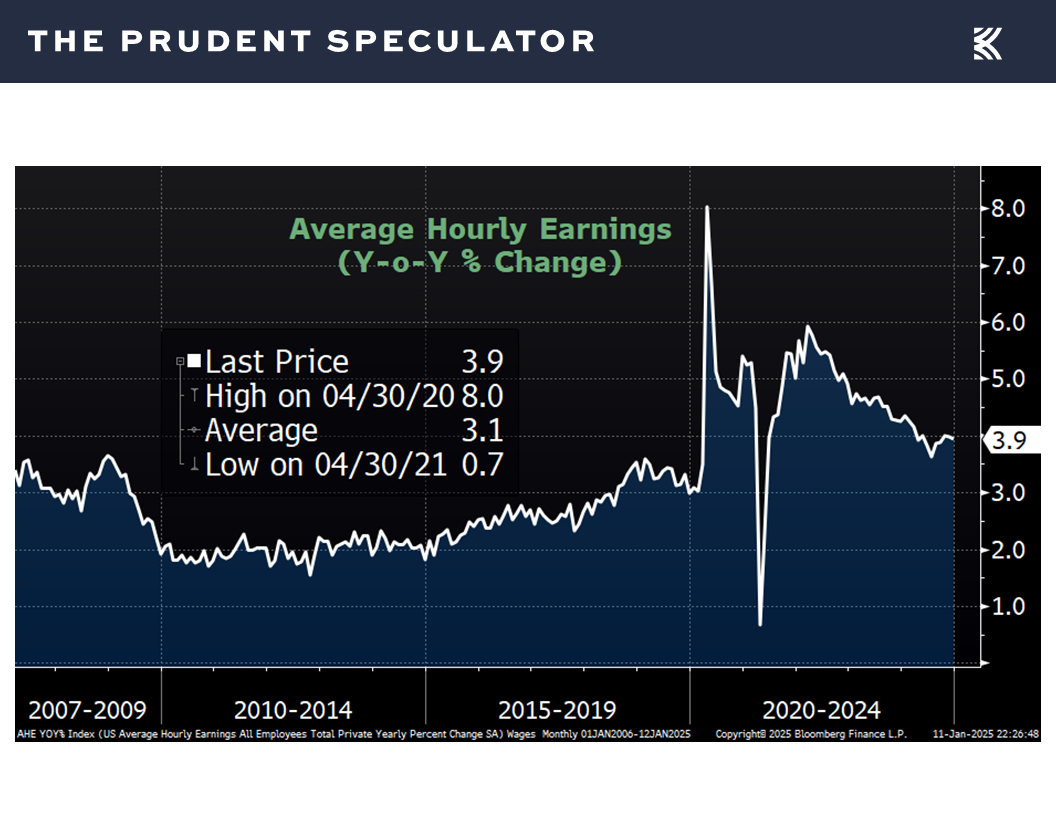

It also did not include a slightly weaker-than-expected increase of 3.9% in year-over-year wage growth,

or a modest pullback to 73.2 in the University of Michigan’s initial reading of consumer sentiment for January versus 74.0 for December.

Still, we think, as evidently do investors in the Fed Fund futures market, which saw a reduction in the outlook for further interest rates cuts from the Federal Reserve,

Corporate Profits – Healthy EPS Growth Still the Forecast

that the sum of the numbers last week supports continued strength in the economy, which should bode well for corporate profit growth, the long-time driver of stock prices.

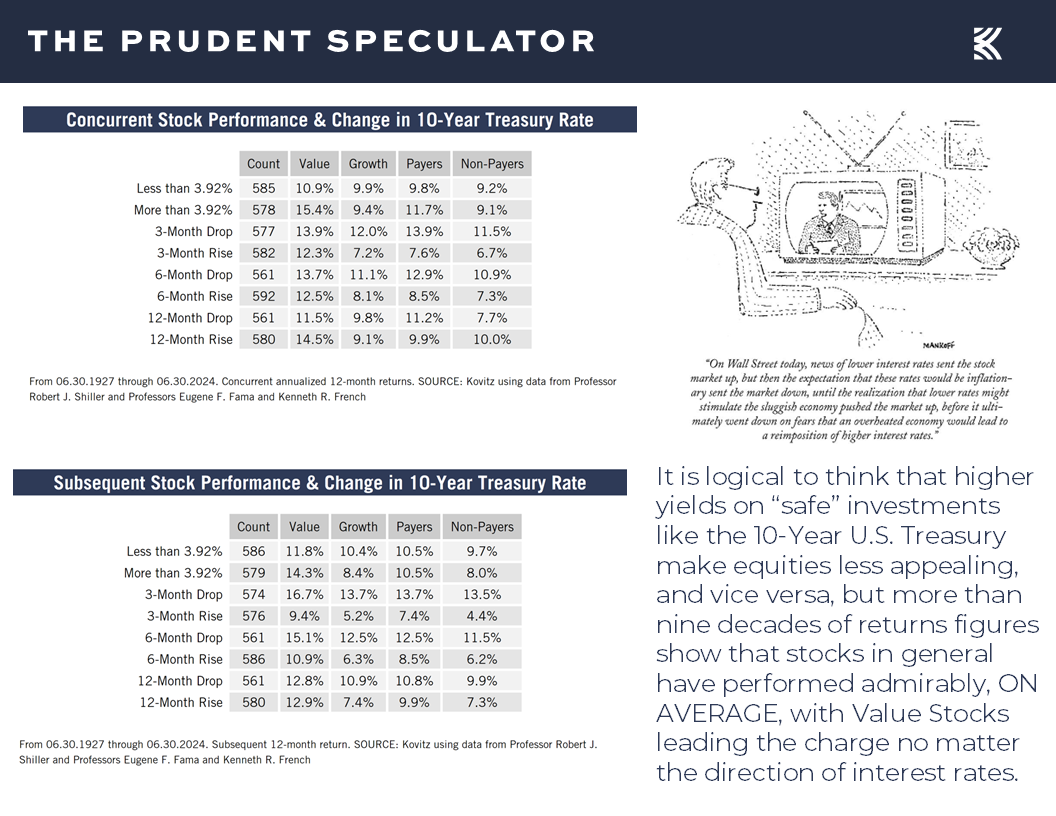

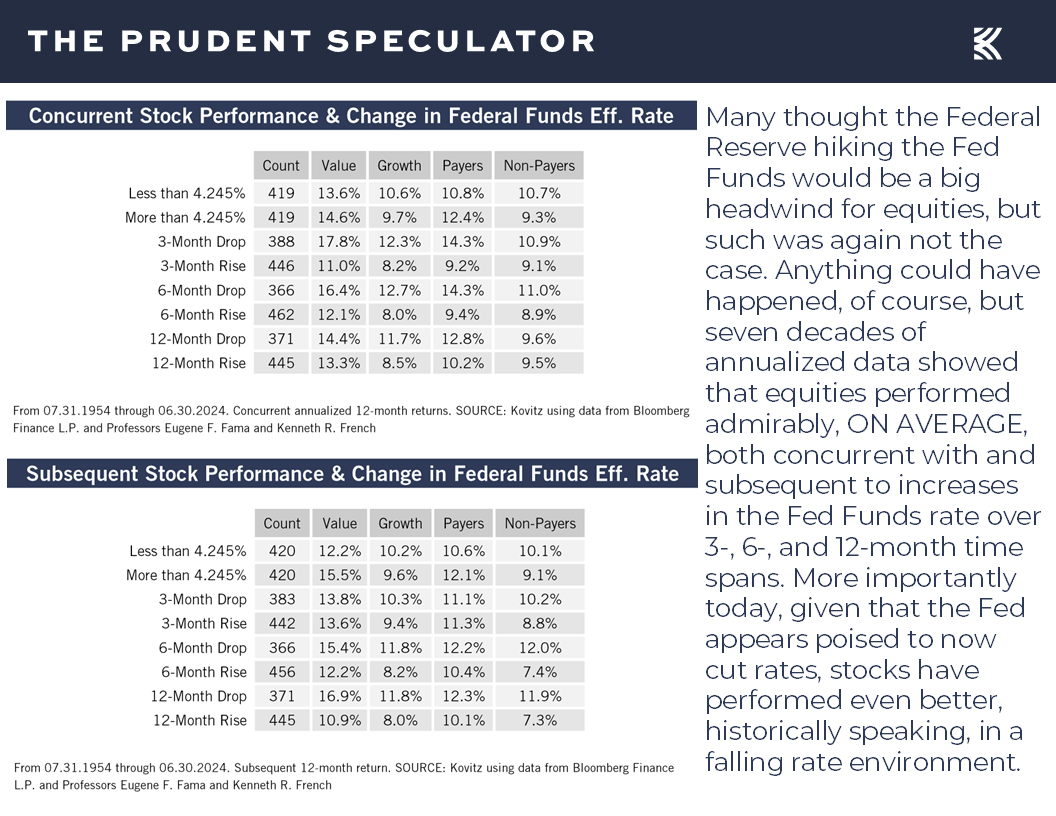

Interest Rates – Stocks Have Performed Fine, on Average, No Matter the Direction of Rates

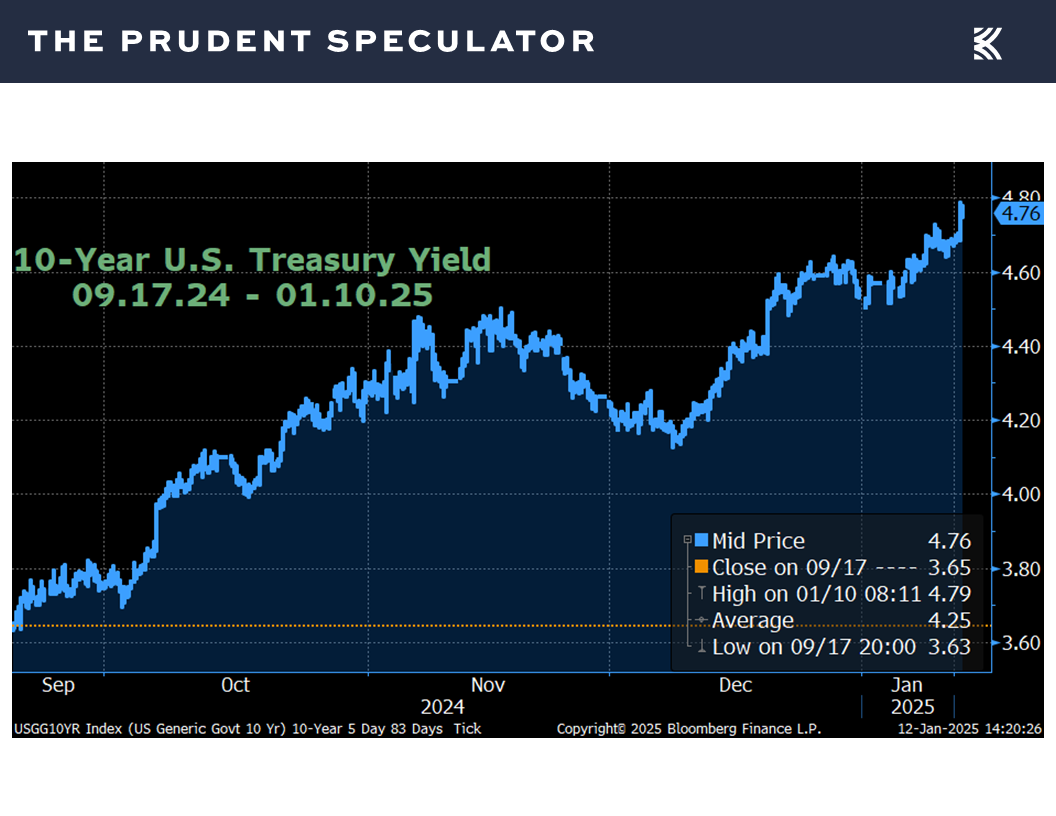

To be sure, there has been plenty of chatter that rising interest rates are becoming a headwind for stocks,

but nearly a century of market history illustrates that equities have performed fine whether government bond yields are climbing or falling,

which has also been the case since 1954 whether the Fed is tightening or easing monetary policy.

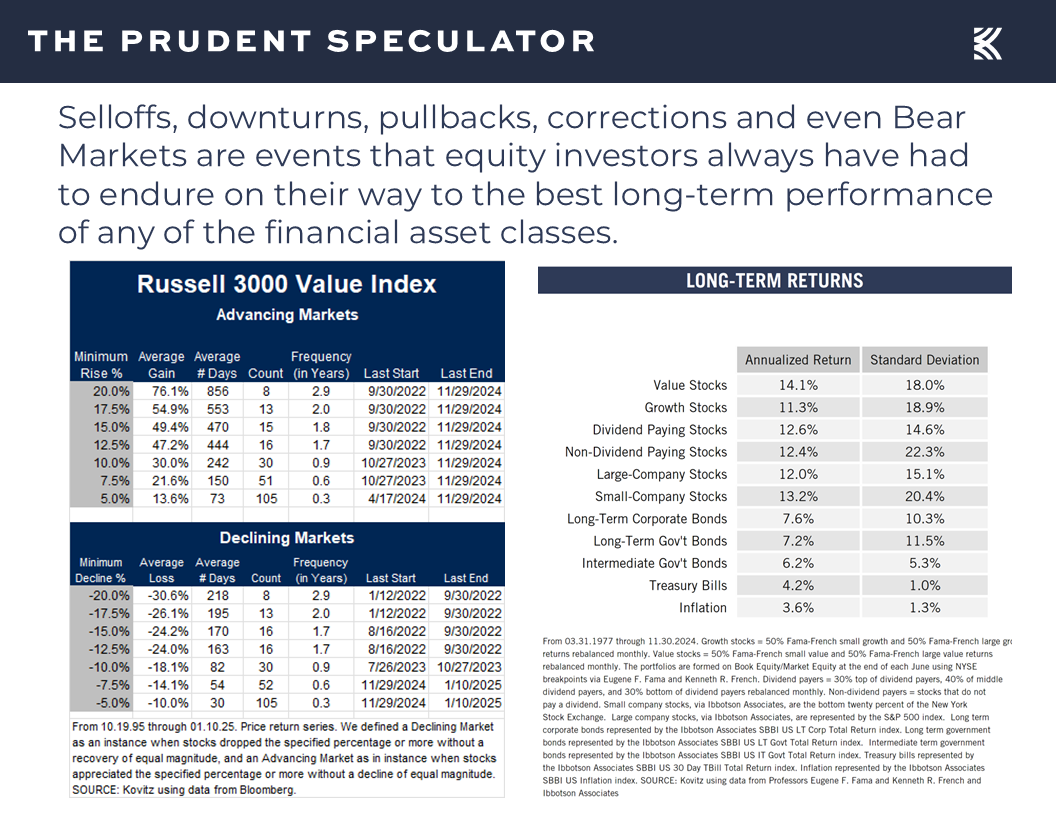

Valuations – Value Stocks Remain Reasonably Priced

Yes, a higher so-called risk-free rate should make equities less attractive, but we are not at such a level today for Value stocks,

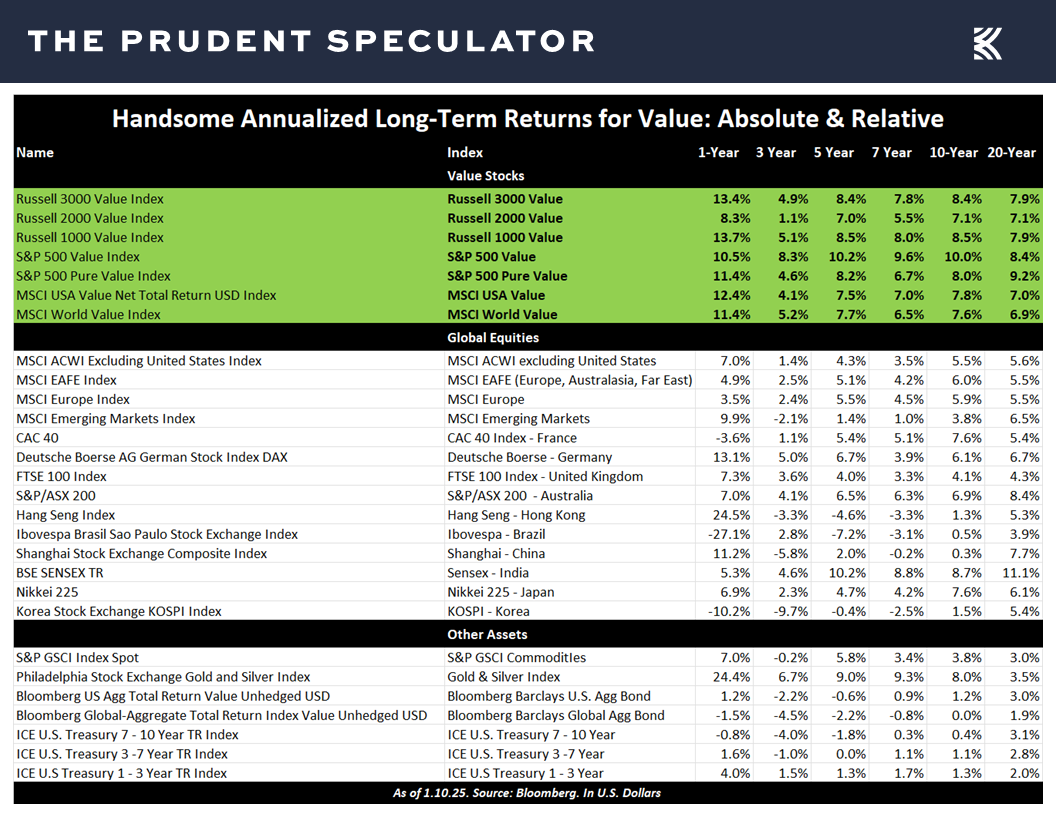

while the only thing that can be said with certainty is that rising bond yields are bad…for bond prices. Indeed, take a look at the miserable near- and long-term annualized returns for the Bloomberg Barclays U.S. Aggregate and Global Aggregate Bond indexes in the table below, which also shows the performance of the various Value stock indexes.

Volatility – The Longer the Measuring Stick the Lower the Chance of Loss

Yes, stock prices are much more volatile than bonds, but those with a long-term time horizon certainly have the odds in their favor should they invest in equities,

and we continue to sleep well at night given the inexpensive valuation metrics on our broadly diversified portfolios of what we believe are undervalued stocks.

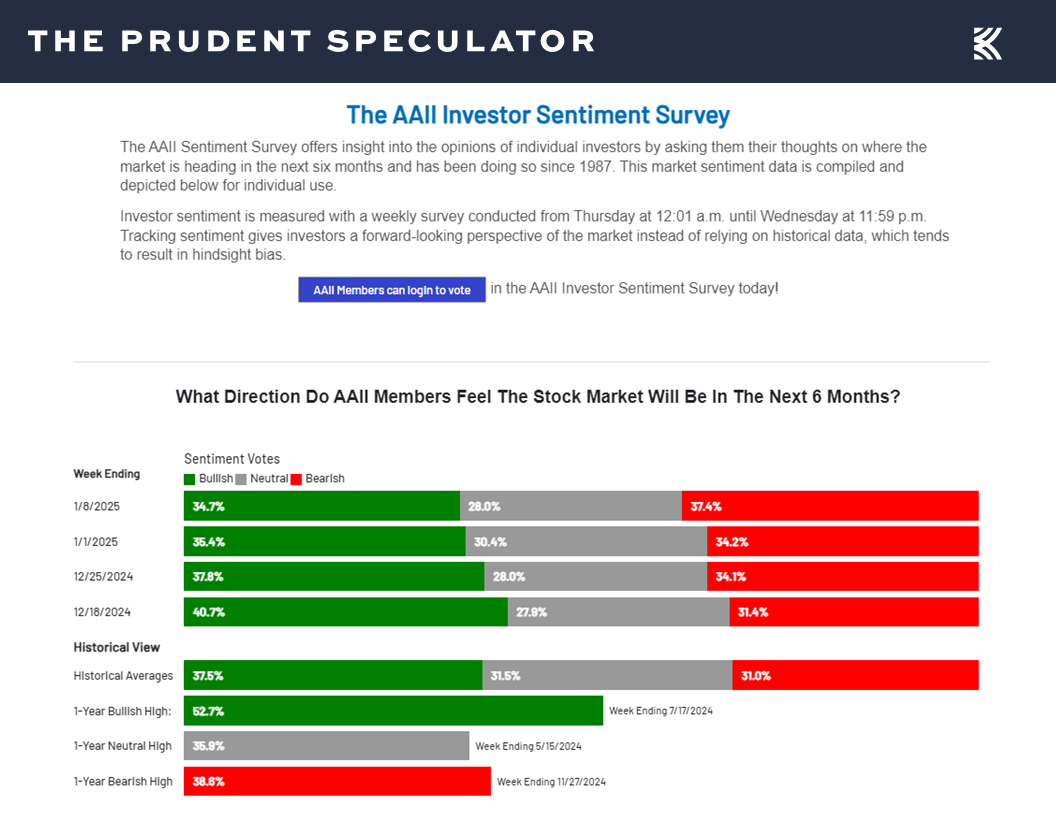

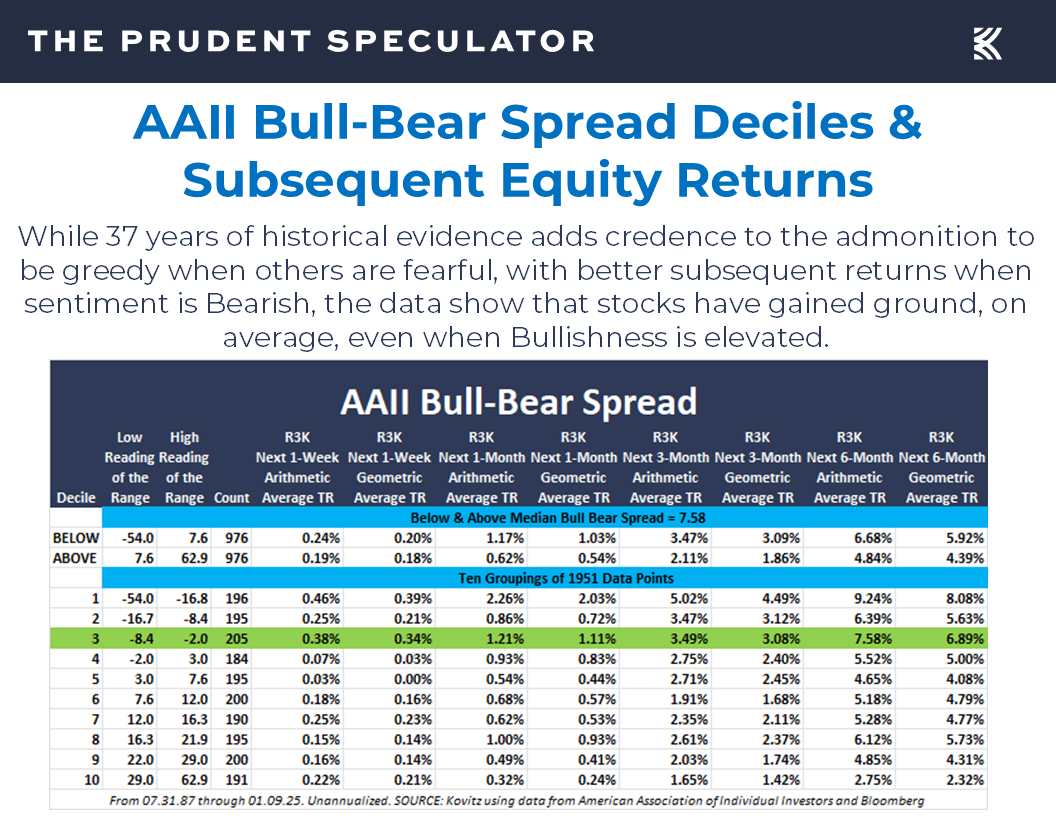

Sentiment – AAII Bullishness Retreats

That does not mean that Friday’s big swoon won’t give way to additional downside, but we see no reason to alter our long-term enthusiasm for equites, especially as short-term worries about too much investor optimism have continued to be mitigated.

Happily, the latest sentiment survey from the American Association of Individual Investors (AAII) now shows more Bears than Bulls, which historically has led to better-than-average near-term equity returns.

Stock News – Updates on five stocks across four different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Economic Update, Valuations, Volatility and Sentiment

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss economic updates, valuations, volatility and sentiment. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 10 Buys for 4 Portfolios

Headlines – 2025 Off to a Miserable Start but Stocks Always Have Overcome Disconcerting Events in the Fullness of Time

Calendar – First 5 Days, Seasonality, Years Ending in 5 Historical Numbers

Econ Update – Better-than-Expected Numbers, Solid Growth Outlook Intact

Corporate Profits – Healthy EPS Growth Still the Forecast

Interest Rates – Stocks Have Performed Fine, on Average, No Matter the Direction of Rates

Valuations – Value Stocks Remain Reasonably Priced

Volatility – The Longer the Measuring Stick the Lower the Chance of Loss

Sentiment – AAII Bullishness Retreats

Stock News – Updates on ALL, GBX, XOM & JNJ

Headlines – 2025 Off to a Miserable Start but Stocks Always Have Overcome Disconcerting Events in the Fullness of Time

We want to thank the folks who have reached out to check on us. The Los Angeles wildfires are some 60 miles to the north of our offices, so we are a fair distance from the cataclysmic scenes. Still, the air quality isn’t great and those who have been followers of the newsletter for several decades likely will remember that we had three different Al Frank offices in Santa Monica, with our founder owning a home on Montana Avenue, with all those locations just south of Pacific Palisades.

Obviously, equity market gyrations are insignificant relative to the tragedy still unfolding to the north of us, and 2025 isn’t exactly off to a good start on the humanity front,

but we always endeavor to keep emotions out of the investment equation as we live by the Vannevar Bush admonition, “Fear can not be banished, but it can be calm and without panic; it can be mitigated by reason and evaluation.” After all, we know that stocks throughout history have always overcome every disconcerting event in the fullness of time,

with the inevitable trips to the downside followed by even greater moves to the upside, so much so that long-term performance since the launch of The Prudent Speculator in March 1977 have been terrific, including returns on Value stocks of some 14% per annum through the end of November 2024.

Calendar – First 5 Days, Seasonality, Years Ending in 5 Historical Numbers

Of course, until Friday, equities generally had shaken off the awful 2025 headlines, with the first five days of trading in the new year showing gains on the major market averages, an indicator that some argue bodes well for returns this year,

while we continue to reside in the seasonally more favorable six months of the year,

and years ending in 5 historically have been very good, on average.

Econ Update – Better-than-Expected Numbers, Solid Growth Outlook Intact

More importantly, the U.S. economy remains in solid shape, with Bloomberg’s current tabulation of recession probability residing at a very low 20%,

and the latest estimate from the Atlanta Fed for Q4 real (inflation-adjusted) GDP growth moving up last week to 2.7%.

That GDP projection included a greater-than expected 8.1 million job openings in November,

another drop in weekly first-time filings for jobless benefits,

and a better-than-forecast increase in the ISM Non-Manufacturing Index for December to a reading of 54.1, up from 52.1 in November.

However, the Atlanta Fed projection did not include Friday’s significantly higher-than-forecast rise of 256,000 in nonfarm payrolls for December, well above estimates of a 165,000 increase and the revised tally for November of 212,000,

which led to a lower-than-estimated jobless rate of 4.1%.

It also did not include a slightly weaker-than-expected increase of 3.9% in year-over-year wage growth,

or a modest pullback to 73.2 in the University of Michigan’s initial reading of consumer sentiment for January versus 74.0 for December.

Still, we think, as evidently do investors in the Fed Fund futures market, which saw a reduction in the outlook for further interest rates cuts from the Federal Reserve,

Corporate Profits – Healthy EPS Growth Still the Forecast

that the sum of the numbers last week supports continued strength in the economy, which should bode well for corporate profit growth, the long-time driver of stock prices.

Interest Rates – Stocks Have Performed Fine, on Average, No Matter the Direction of Rates

To be sure, there has been plenty of chatter that rising interest rates are becoming a headwind for stocks,

but nearly a century of market history illustrates that equities have performed fine whether government bond yields are climbing or falling,

which has also been the case since 1954 whether the Fed is tightening or easing monetary policy.

Valuations – Value Stocks Remain Reasonably Priced

Yes, a higher so-called risk-free rate should make equities less attractive, but we are not at such a level today for Value stocks,

while the only thing that can be said with certainty is that rising bond yields are bad…for bond prices. Indeed, take a look at the miserable near- and long-term annualized returns for the Bloomberg Barclays U.S. Aggregate and Global Aggregate Bond indexes in the table below, which also shows the performance of the various Value stock indexes.

Volatility – The Longer the Measuring Stick the Lower the Chance of Loss

Yes, stock prices are much more volatile than bonds, but those with a long-term time horizon certainly have the odds in their favor should they invest in equities,

and we continue to sleep well at night given the inexpensive valuation metrics on our broadly diversified portfolios of what we believe are undervalued stocks.

Sentiment – AAII Bullishness Retreats

That does not mean that Friday’s big swoon won’t give way to additional downside, but we see no reason to alter our long-term enthusiasm for equites, especially as short-term worries about too much investor optimism have continued to be mitigated.

Happily, the latest sentiment survey from the American Association of Individual Investors (AAII) now shows more Bears than Bulls, which historically has led to better-than-average near-term equity returns.

Stock News – Updates on five stocks across four different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.