The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss RFK Appointment, Inflation, Valuations and more Stock News. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Election 2024 – Stocks Retreat

RFK Appointment – Health Care Stock Traders Shoot First and Ask Questions Later

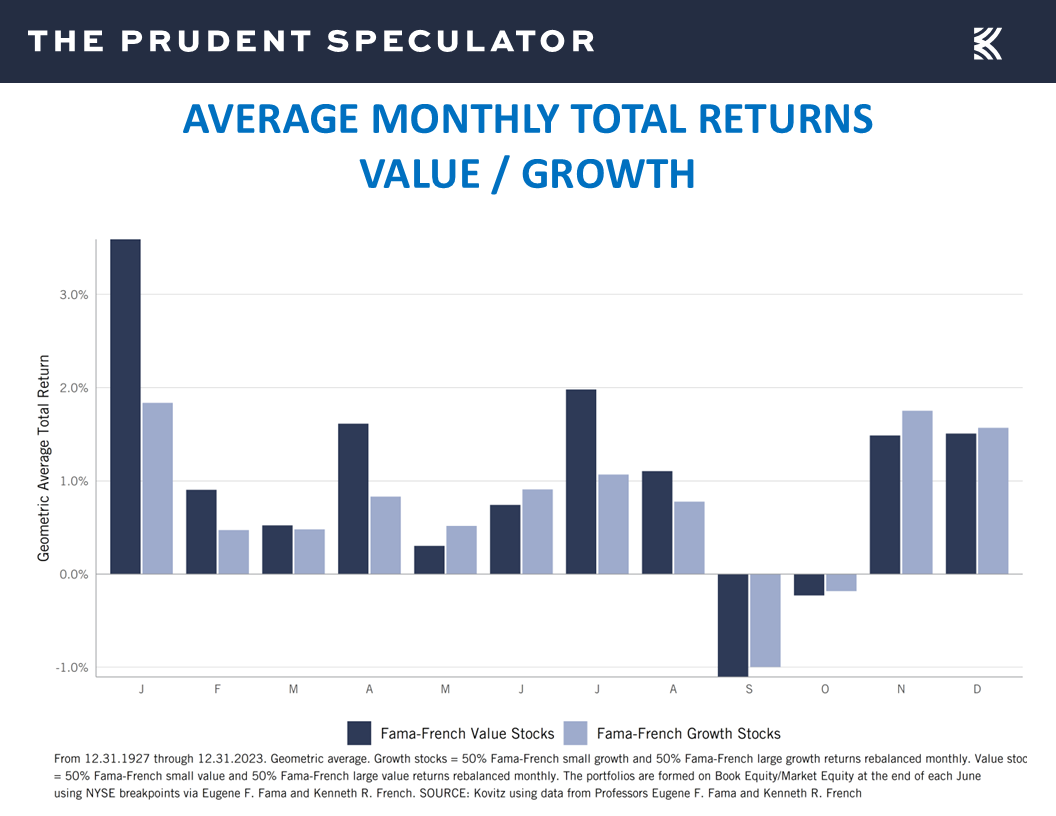

Seasonality – Most Wonderful Time of the Year

Econ Outlook – Favorable Stats; Solid GDP Growth the Forecast; Powell Upbeat

Rates – Stocks Have Performed Fine Whether Fed is Easing/Tightening or 10-Year Yield is Rising/Falling

Inflation – CPI & PPI Tick Higher

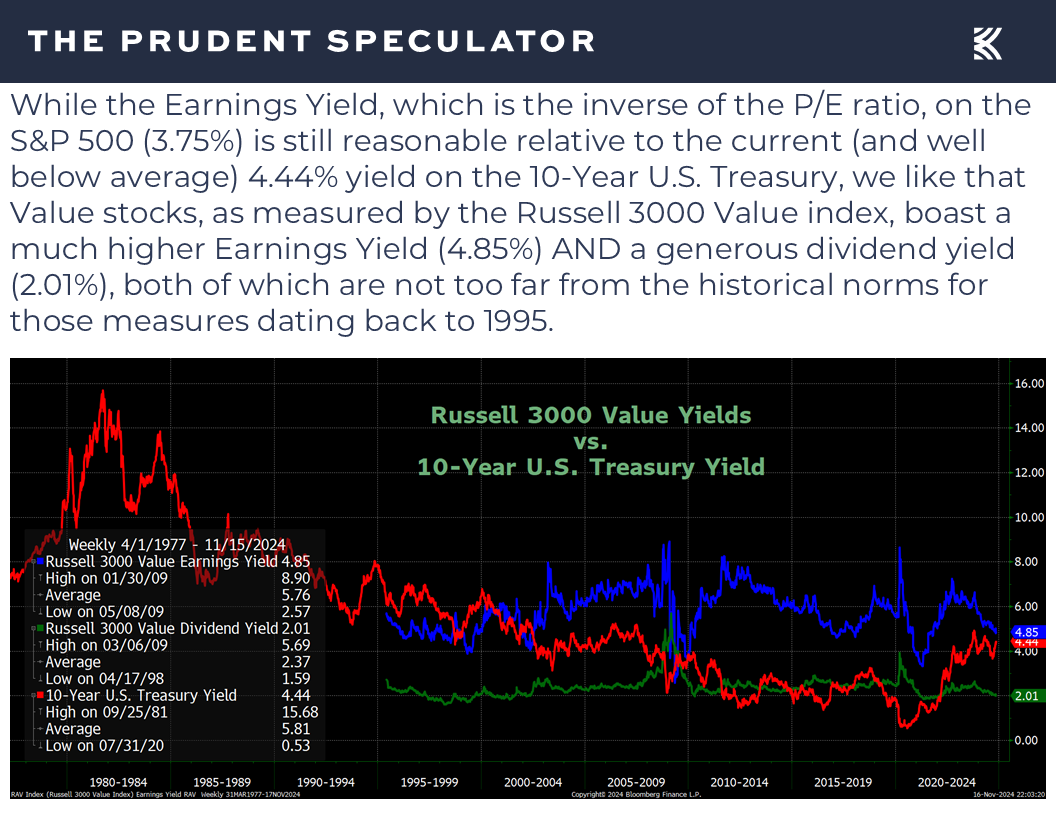

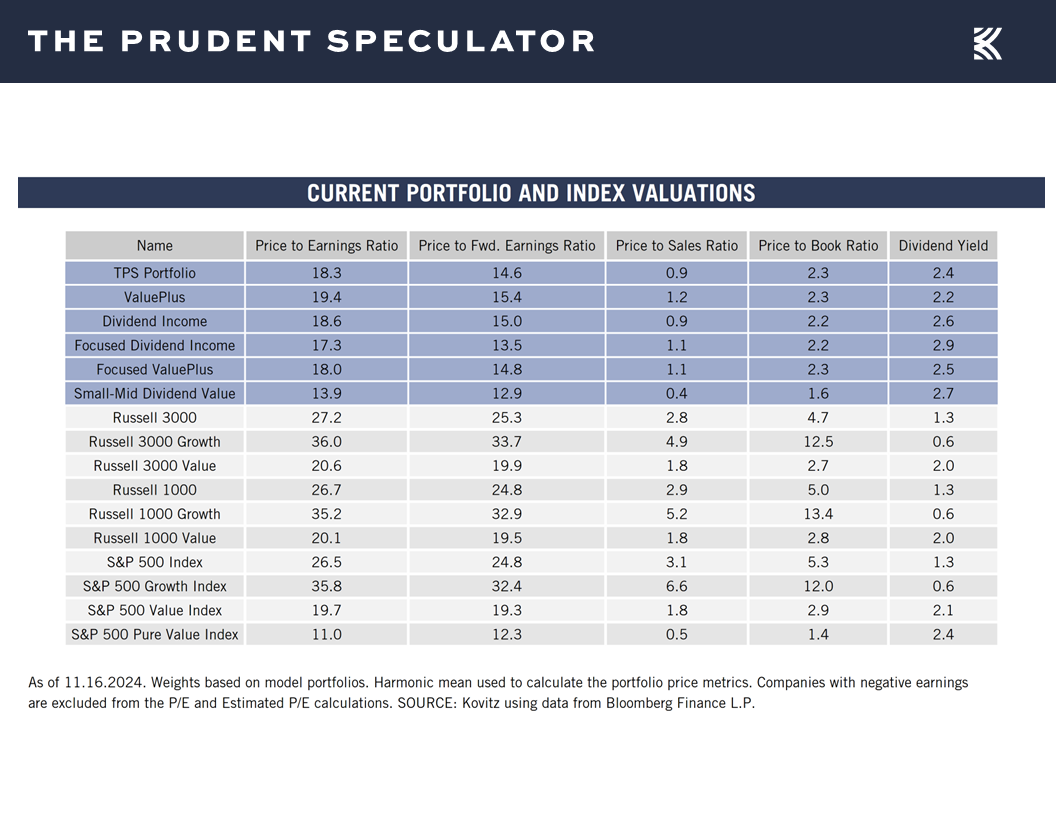

Valuations – Value Stocks Reasonably Priced

Stock News – Updates on nine stocks across six different sectors

Election 2024 – Stocks Retreat

The post-election rally hit a few potholes last week as investors were reminded that significant market volatility is always something with which we have had to contend to be able to enjoy terrific long-term returns.

RFK Appointment – Health Care Stock Traders Shoot First and Ask Questions Later

No doubt, traders were reminded that a Trump presidency (and any presidency for that matter) is not without a few curveballs, while a lack of great liquidity in individual stocks can lead to sizable price moves. Such was seen on Friday following the nomination of Robert F. Kennedy, Jr. as head of the Department of Health and Human Services, which sent Health Care stocks skidding and making the sector the worst-performing since Election Day.

Of course, there is some question about whether Mr. Kennedy will be confirmed for the job, while it is not clear exactly what policies he will attempt to or be able to implement. Certainly, we are not thinking that happy days will be here again for the pharmaceutical industry with RFK as the health czar, but the supposed vaccine skeptic told NPR earlier this month, “We’re not going to take vaccines away from anybody.” Further, we note that the drug industry has long navigated a less-than-friendly political climate.

While we have pulled back our Target Prices a smidge, we think traders are prone to shoot first and ask questions later and we have often seen that the proverbial bark is much worse than the bite when it comes to Washington. After all, there are numerous constituencies to consider, so immediate sweeping changes are tough to pull off, meaning that we are much more inclined to add to already undervalued stocks that were hit hard last week, especially if the herd stampedes toward the exits further in the days and weeks ahead.

Our shopping list would include vaccine (and many other drugs) makers Pfizer (PFE – $24.80) and Merck (MRK – $96.31), managed care provider Elevance Health (ELV – $400.69) and even advertising giant Omnicom Group (OMC – $96.86), the latter hit hard on Friday on worries about pharmaceutical marketing spend.

Seasonality – Most Wonderful Time of the Year

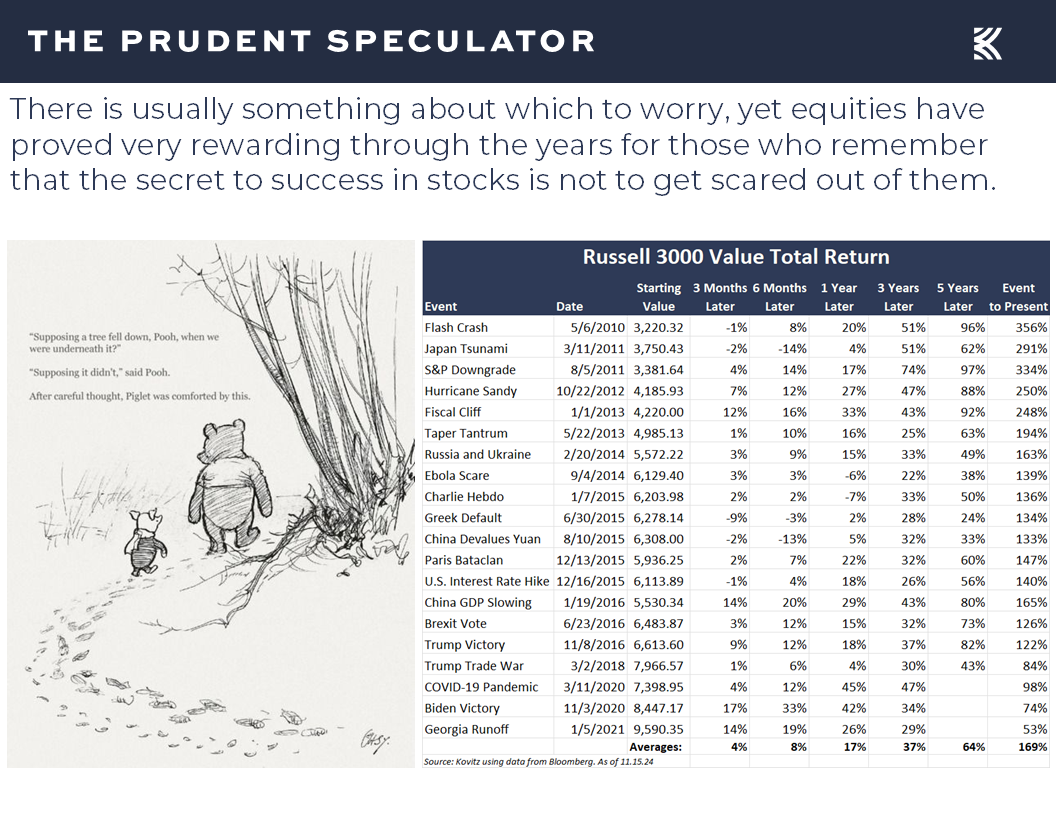

We have to expect plenty of market gyrations in the near term as traders make their bets on the winners and losers in the new administration. However, we offer the reminder that stocks have performed well, on average, no matter who is in the White House, even as the history books show that equities prefer supposedly less business-friendly Democrats in control in Washington.

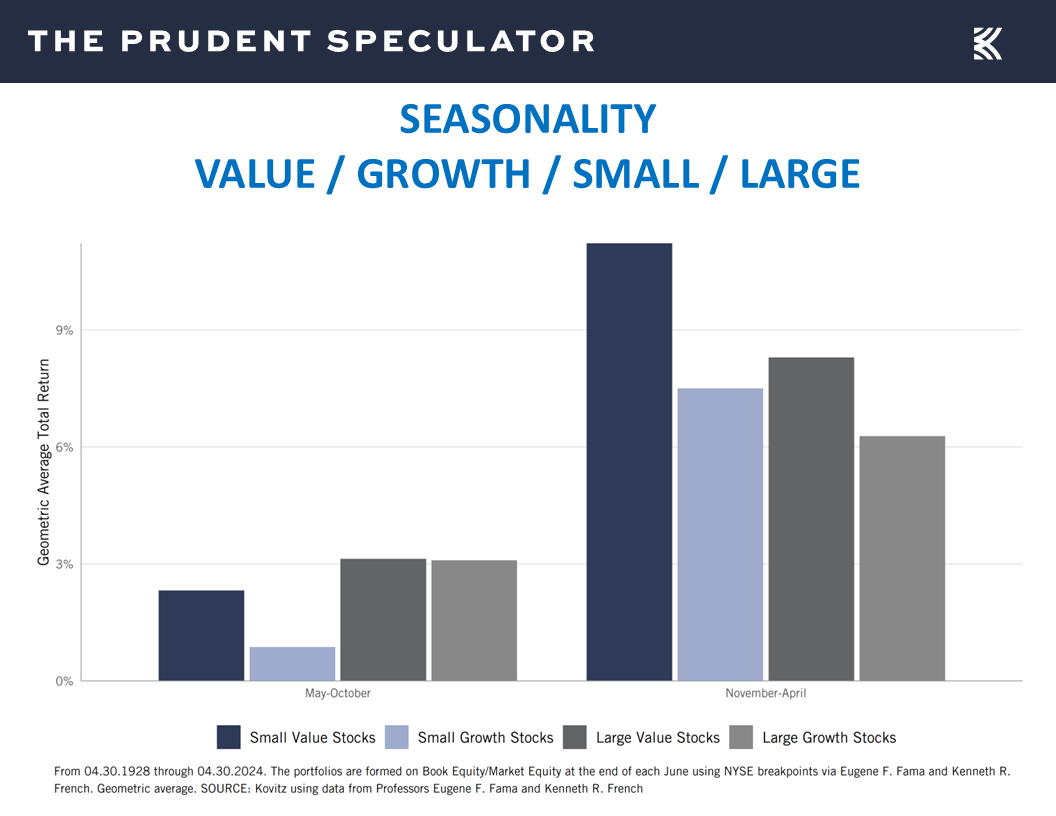

We also should not forget that we are now in the seasonally more favorable six-month time span,

with the long-term evidence showing that November, December and January have been the best three months of the year, on average.

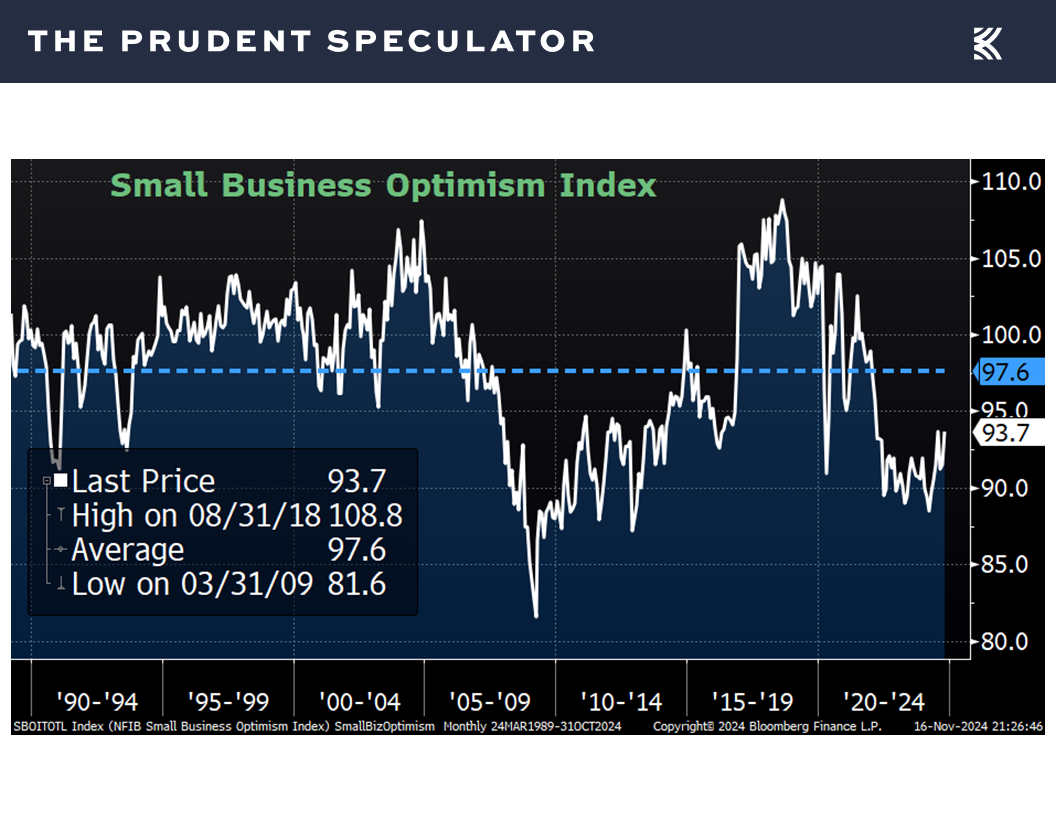

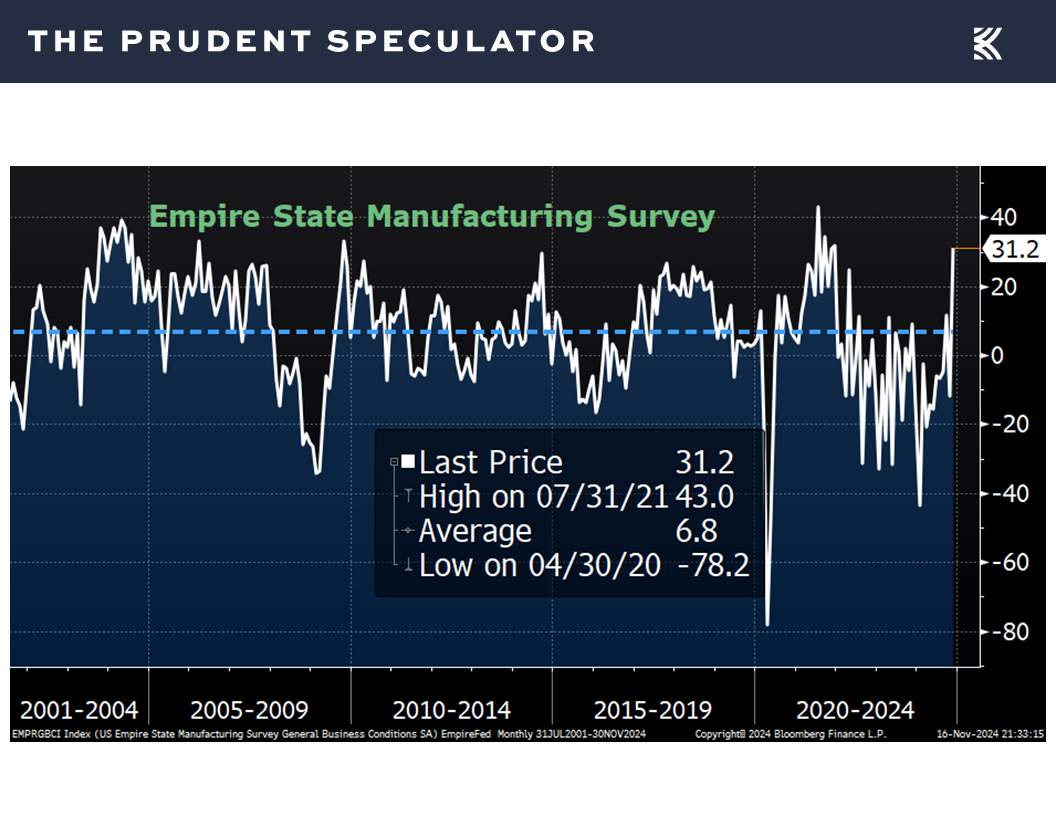

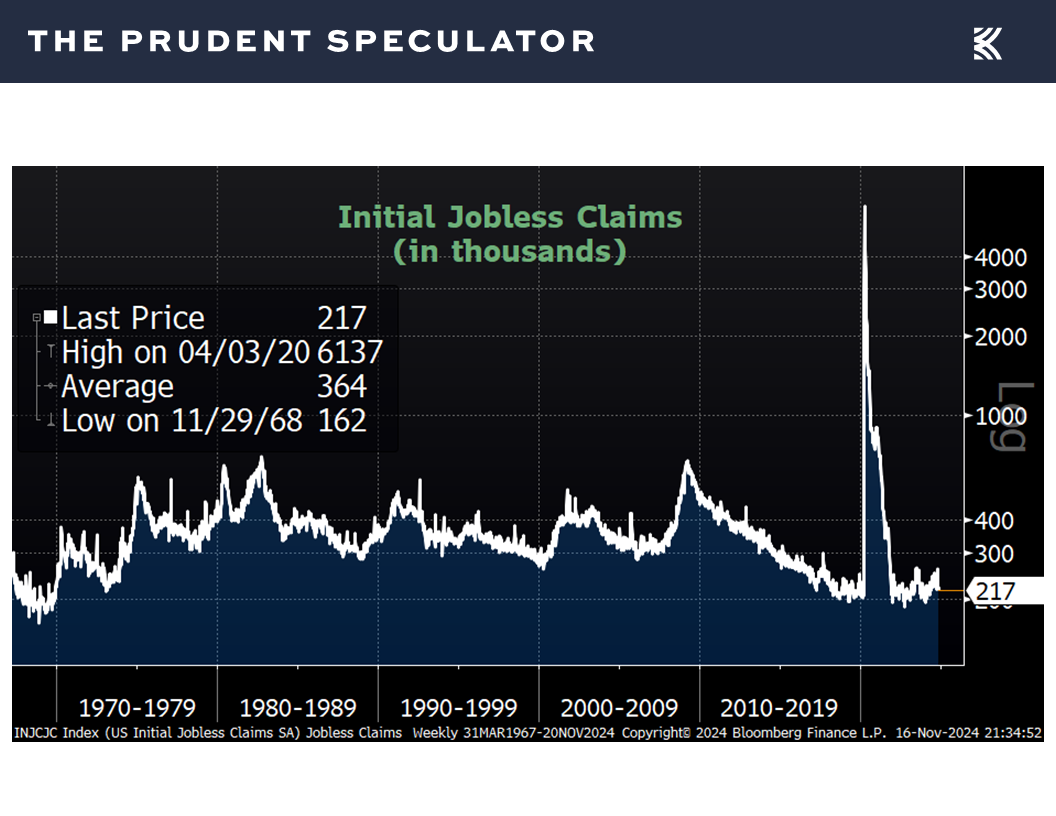

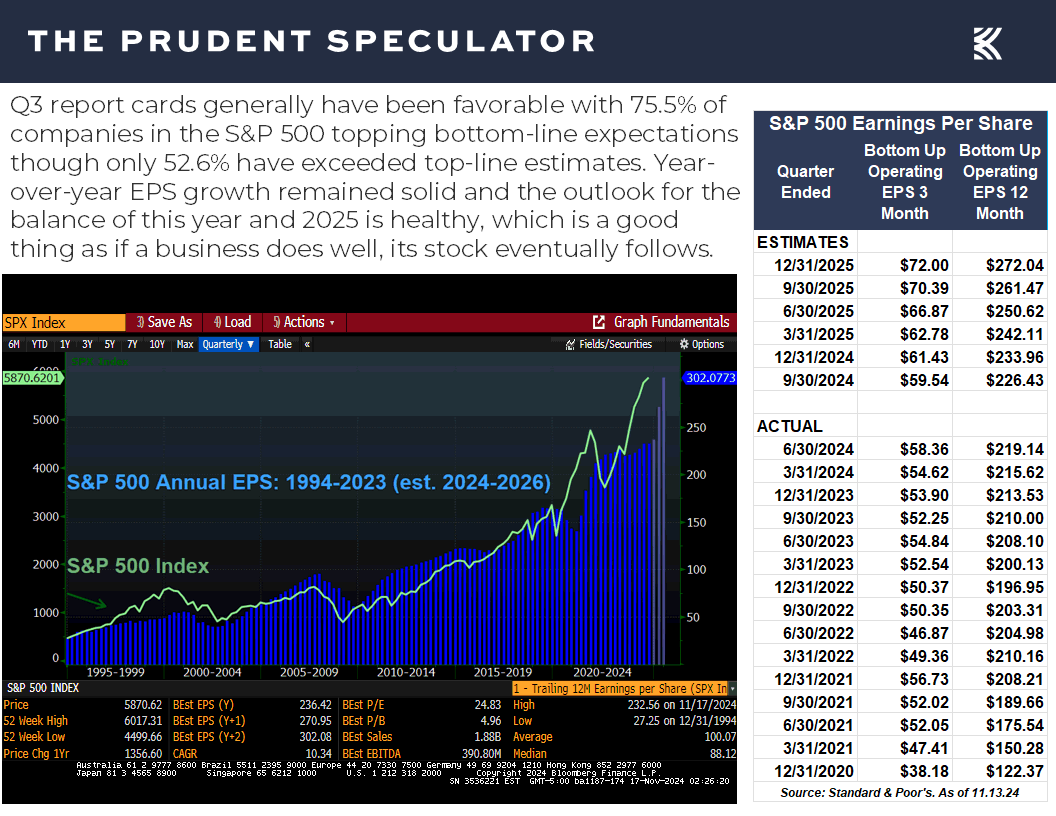

Econ Outlook – Favorable Stats; Solid GDP Growth the Forecast; Powell Upbeat

To be sure, stock prices often defy conventional wisdom in their short-term movements as the lousy market week just endured arguably was due to the release of favorable economic data! Indeed, the NFIB Small Business Optimism index for October came in at 93.7, ahead of the estimate of 92.0 and up from 91.5 in September,

the Empire State Manufacturing survey of factory activity in the New York area for November soared to a reading of 31.2, blowing away projections and reversing the -11.9 tally in October,

first-time filings for unemployment benefits in the latest week declined to 217,000 from 221,000 the week prior, continuing to reside near multi-generational lows,

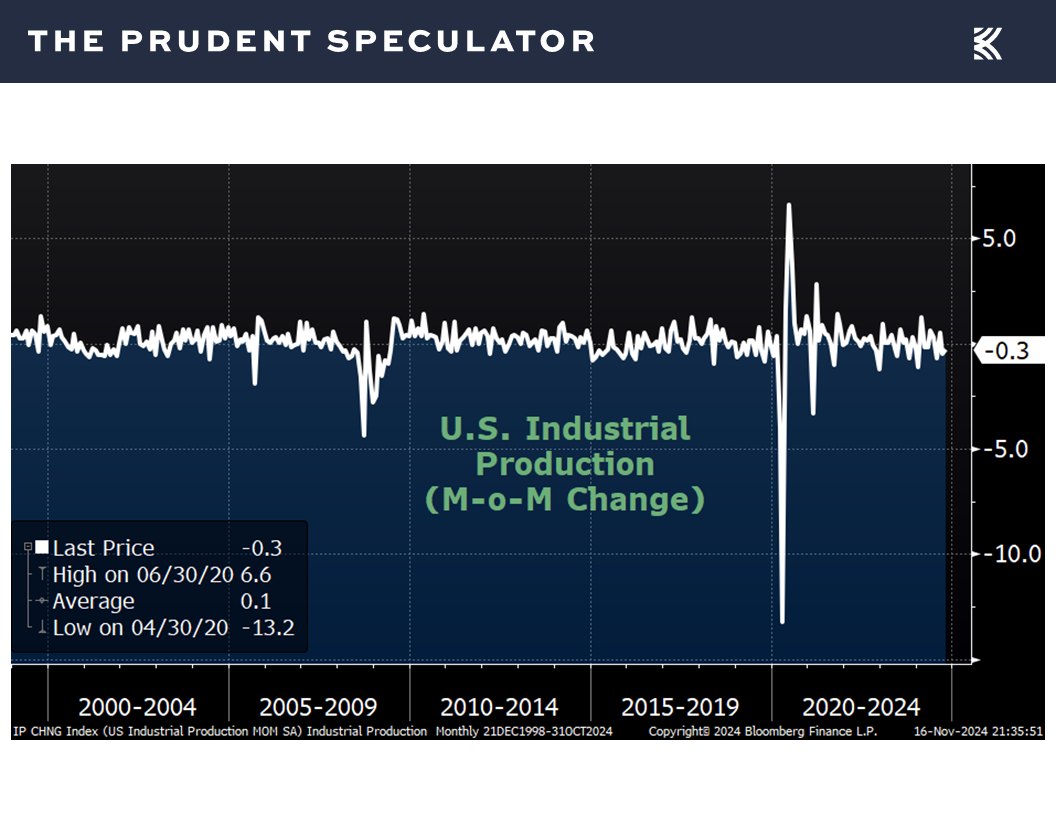

industrial production pulled back by 0.3% in October, but this was better than the 0.4% decline that was expected,

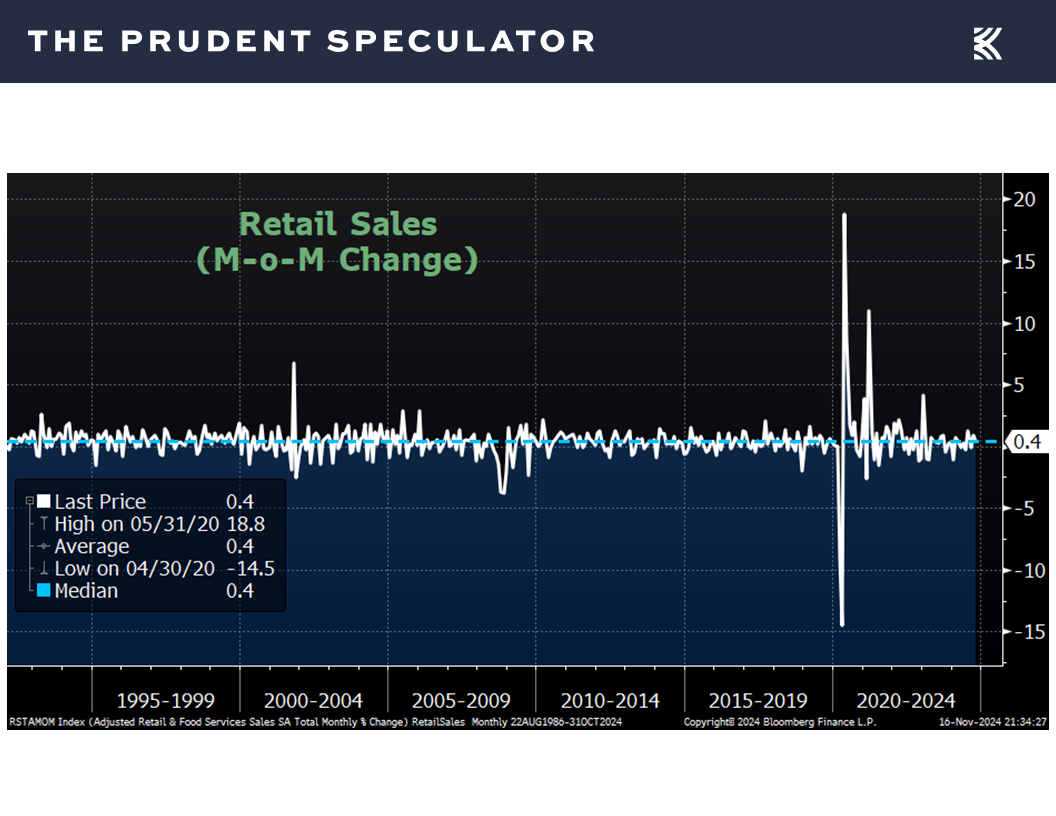

and retail sales for October rose 0.4%, ahead of the 0.3% growth forecast.

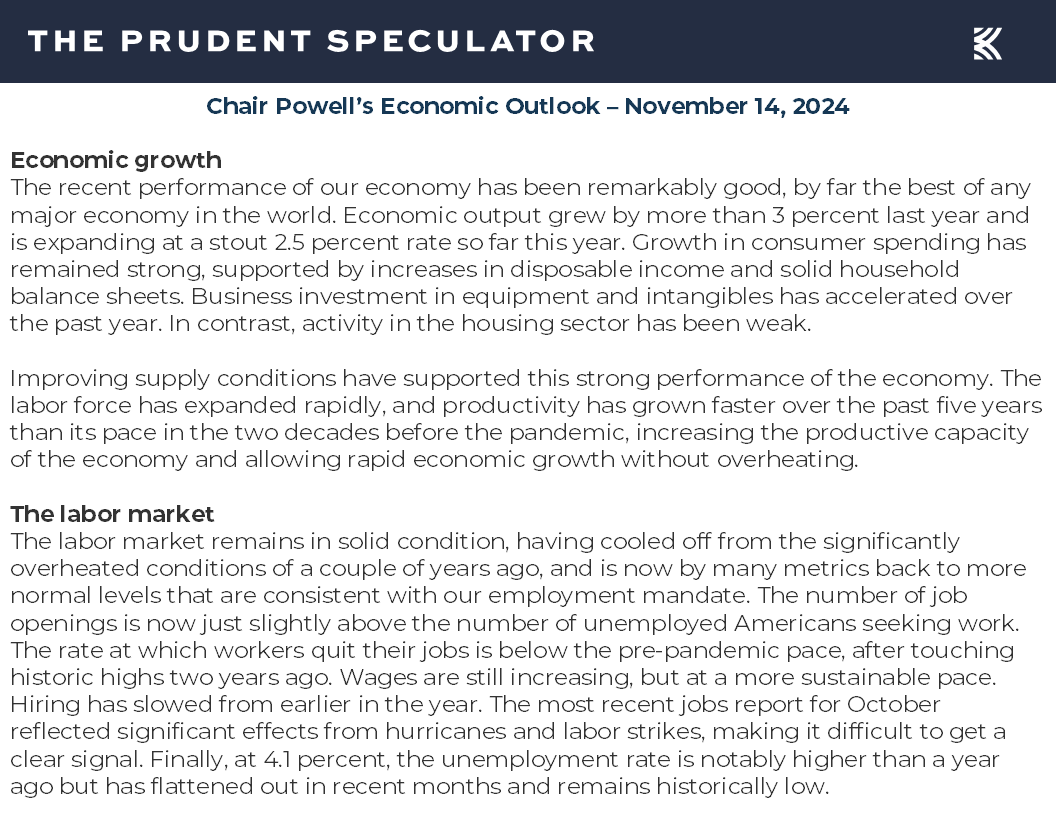

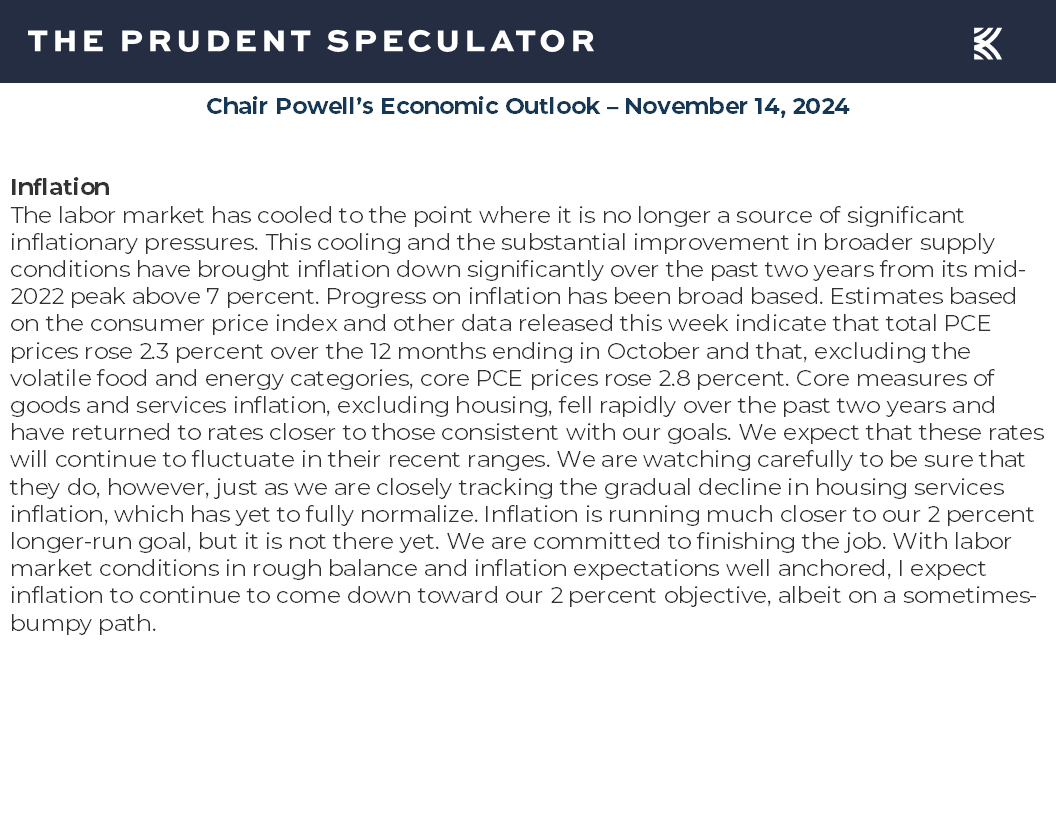

Not surprisingly, Federal Reserve Chair Jerome H. Powell sounded upbeat on the U.S. economy in comments offered in an important speech on November 14,

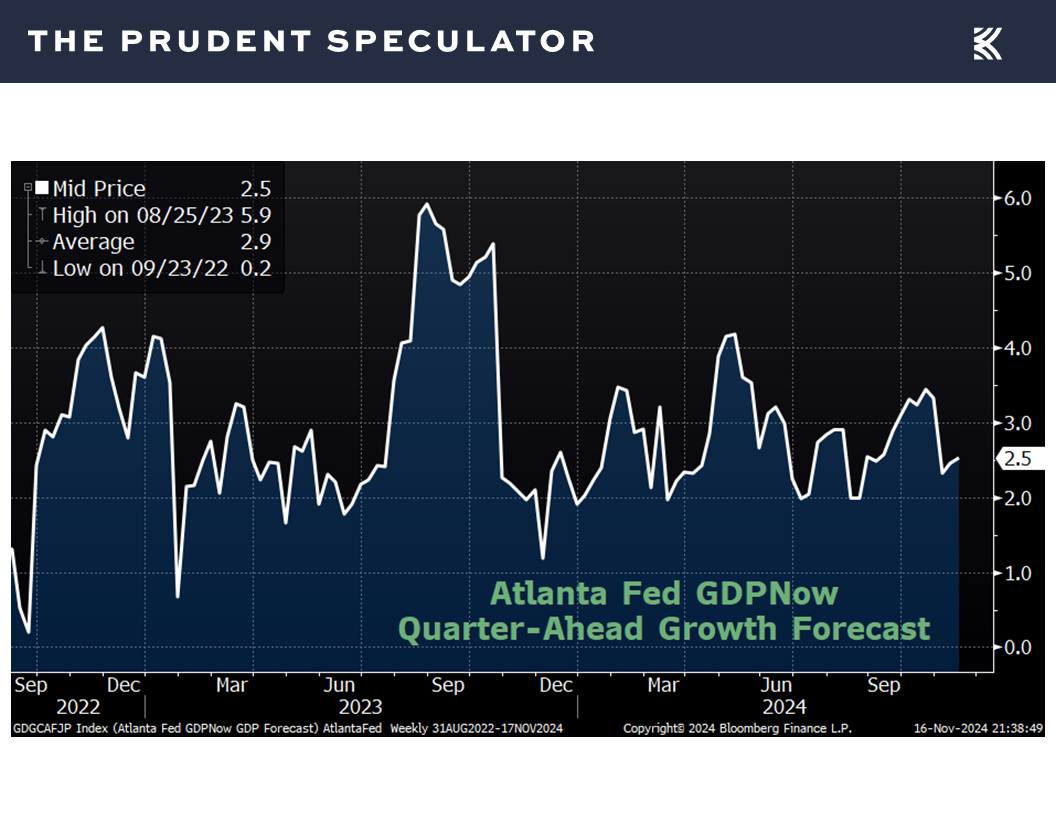

while the latest estimate for Q4 real (inflation-adjusted) GDP growth from the Atlanta Fed held steady at a solid 2.5%,

with a favorable economic backdrop a positive and not a negative by our way of thinking, given that corporate profit growth is a major reason why stock prices have risen over the long term.

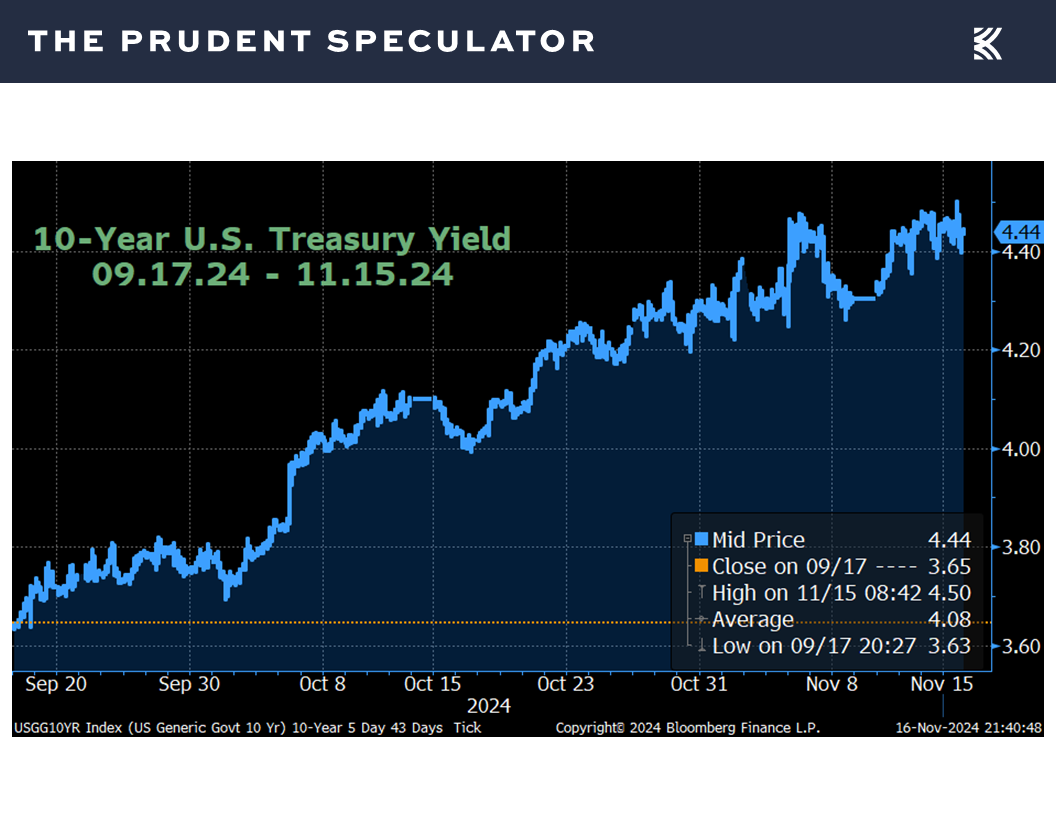

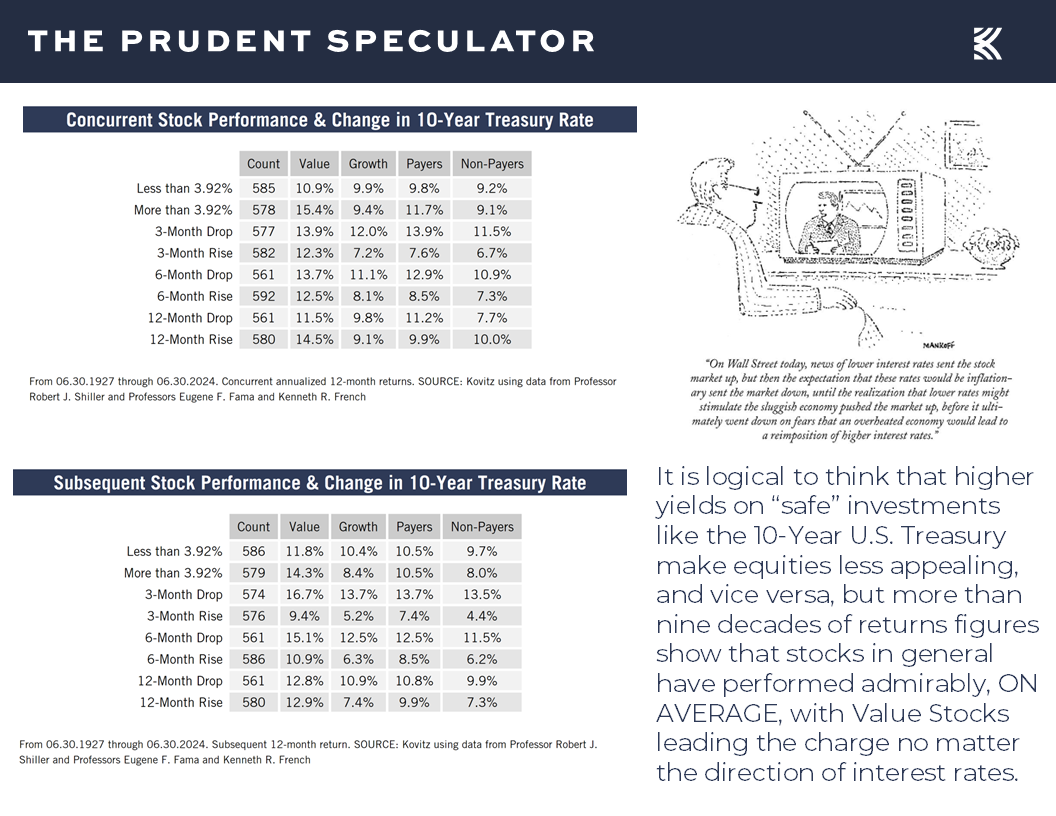

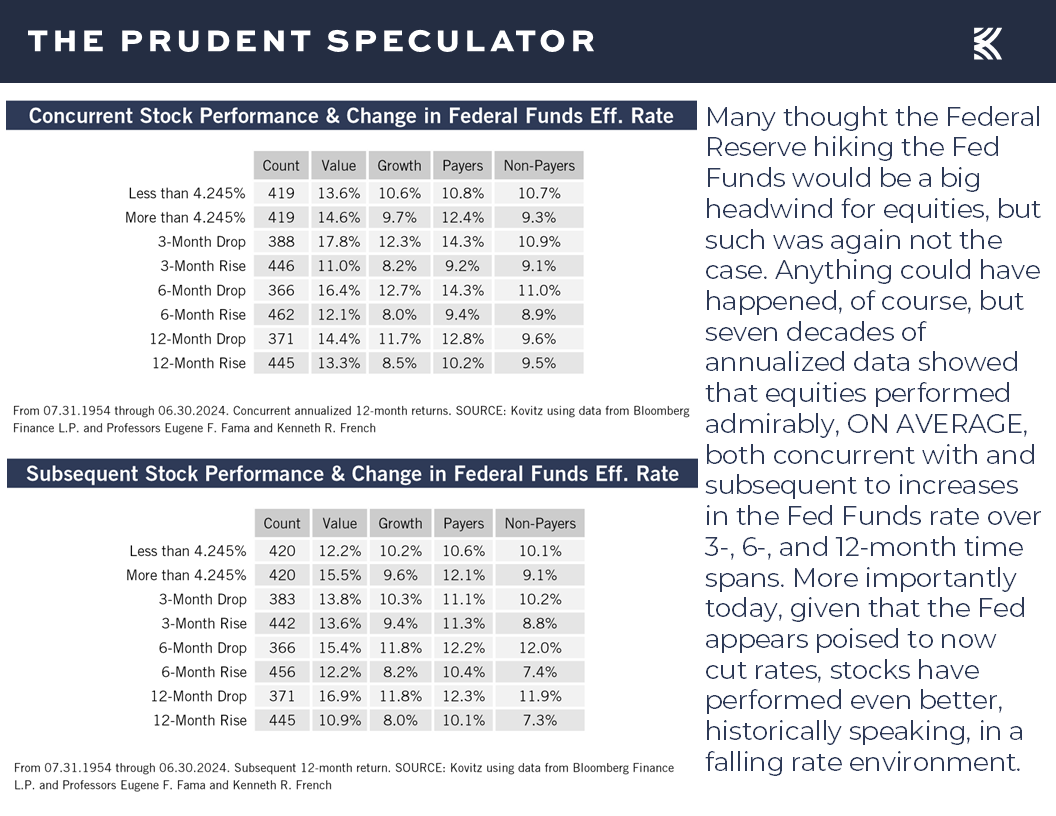

Rates – Stocks Have Performed Fine Whether Fed is Easing/Tightening or 10-Year Yield is Rising/Falling

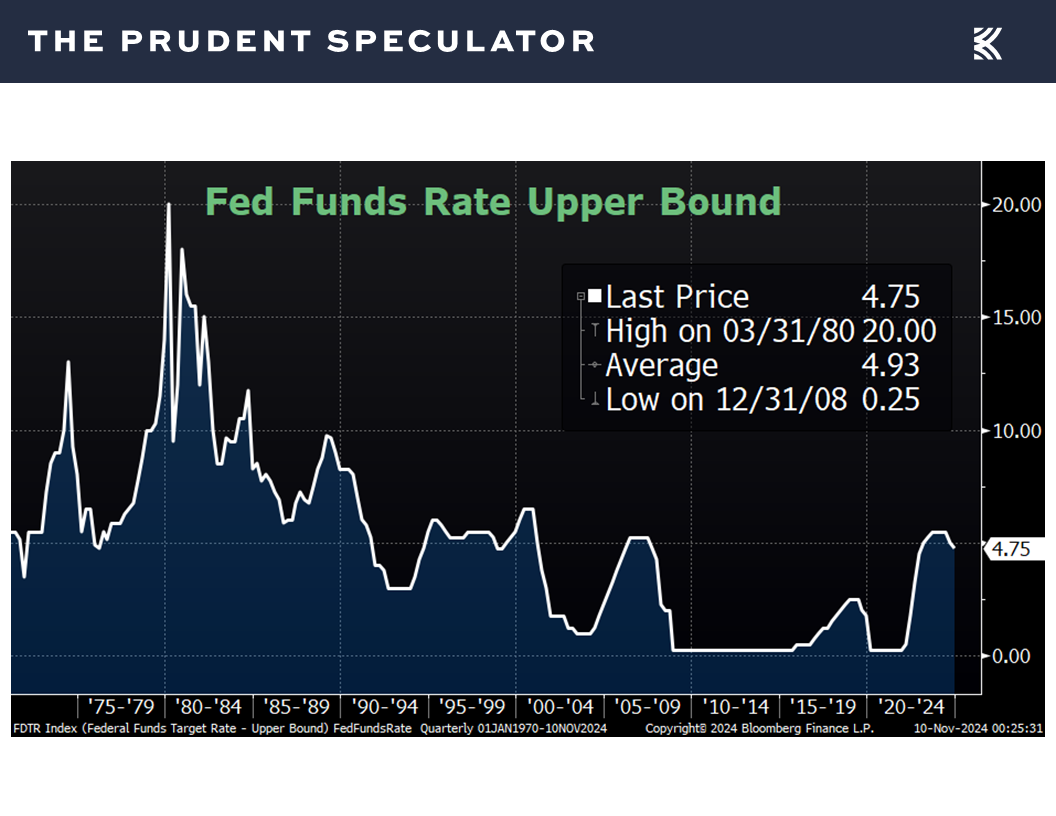

True, the positive data on economic growth sent interest rates higher, pushing the yield on the 10-Year U.S. Treasury up to 4.44%, well above the 3.65% yield the day two months ago when the Federal Reserve initiated its current easing of monetary policy,

by cutting the target for the Fed Funds rate from the then 5.5% upper bound.

History shows that much like what has transpired since September 17, equities have managed solid gains, on average, whether the benchmark government bond yield is rising or falling,

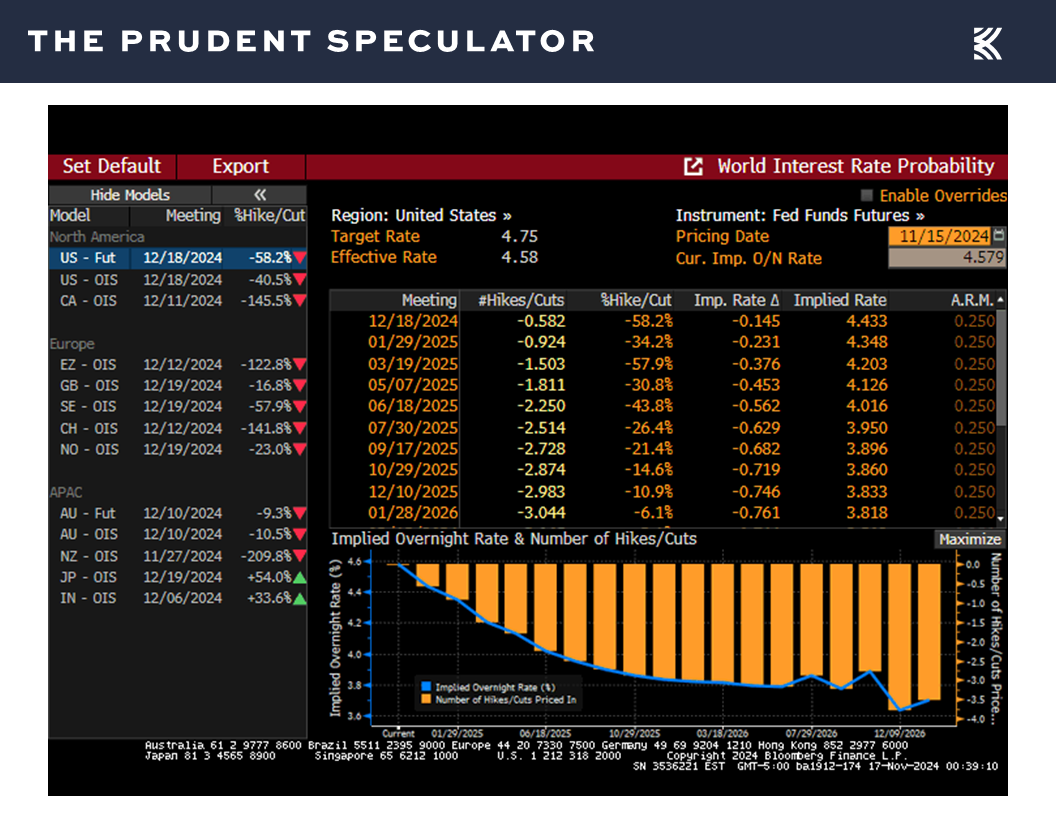

but we understand that the question on the minds of many traders today is what it the likelihood of additional rate cuts, as the betting in the Fed Funds futures market saw wagers fall on another reduction at the December FOMC Meeting and an increase in the expected year-end 2025 rate to 3.83%, up a tick from 3.82% at the end of the previous week.

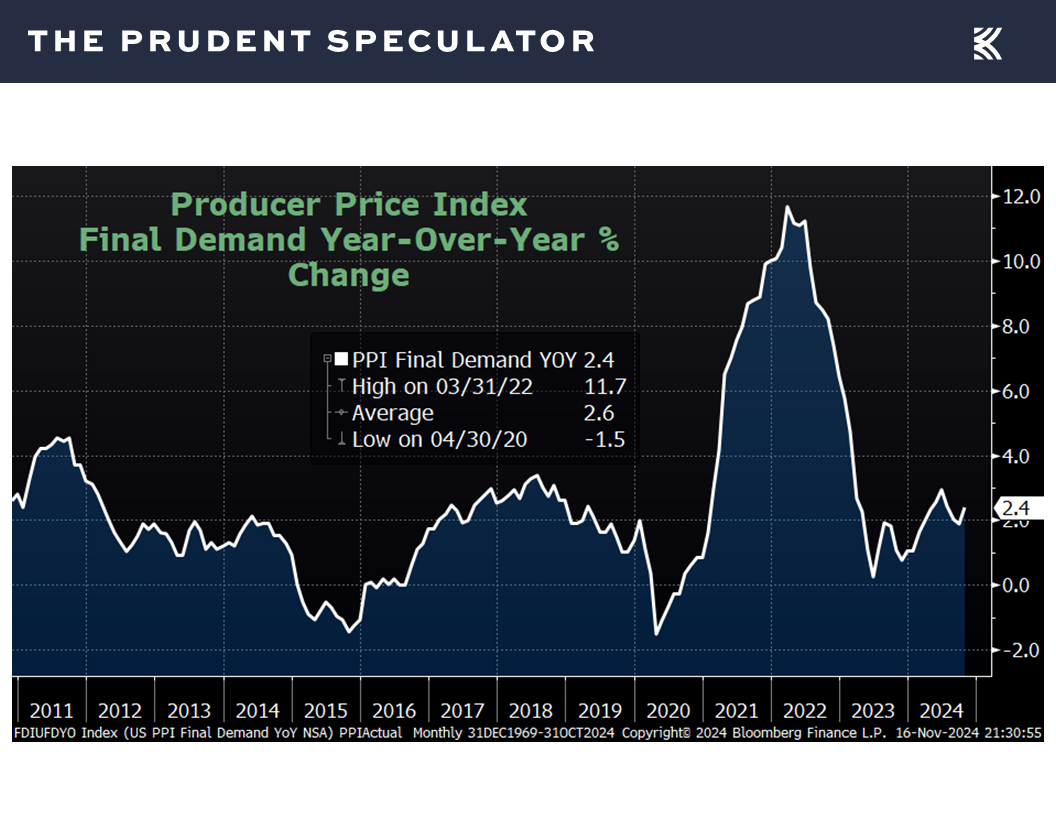

Inflation – CPI & PPI Tick Higher

The odds of a friendlier Fed were not helped when Boston Fed President Susan Collins said on Thursday, “Another rate cut in December is certainly on the table, but it’s not a done deal. There’s more data that we will see between now and December, and we’ll have to continue to weigh what makes sense.”

We also note that Chair Powell discussed inflation in his speech on Thursday, stating, “Inflation is running much closer to our 2 percent longer-run goal, but it is not there yet. We are committed to finishing the job,”

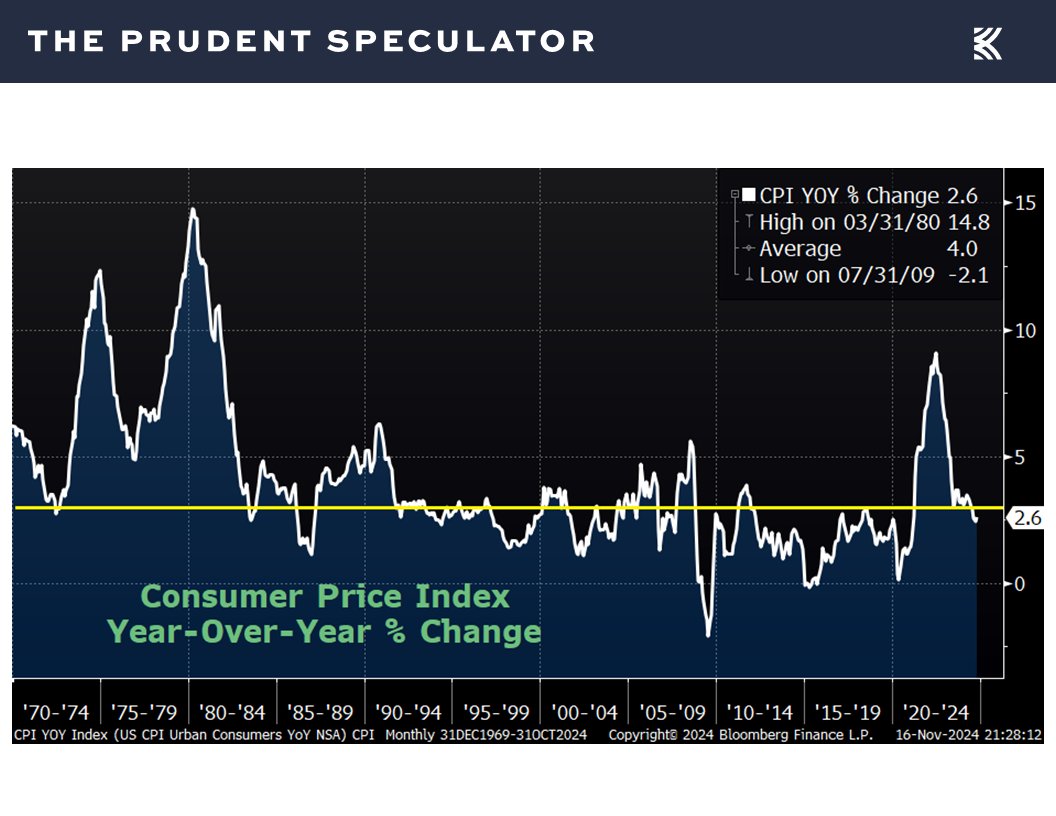

while the Consumer Price Index (CPI) ticked up in October to a 2.6% year-over-year increase, in line with expectations, but up from a 2.4% rise in September,

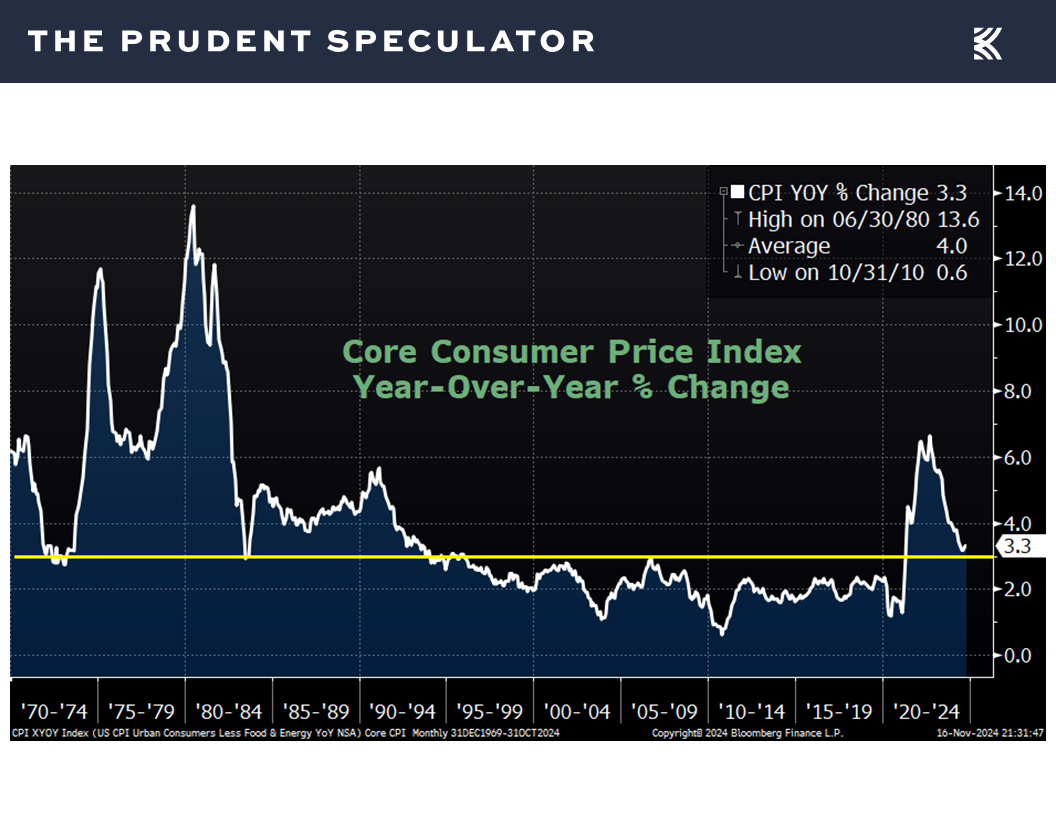

the Core CPI, which excludes volatile food and energy prices, held constant last month at a 3.3% advance

and prices at the wholesale level rose more than expected with a 2.4% increase.

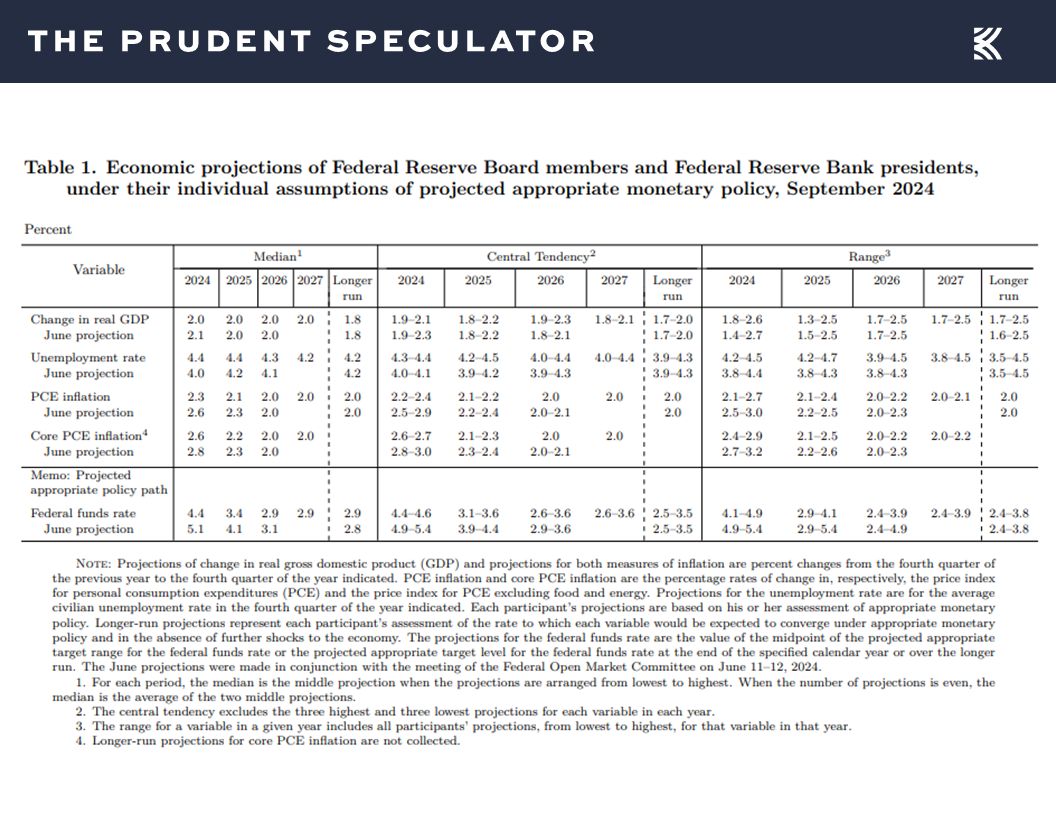

Those inflation figures were not too dissimilar from the projections offered two months ago by Federal Reserve Board members and Federal Reserve Bank presidents,

and we lose little sleep about Jerome H. Powell & Co., given what the evidence shows for stock prices (they have risen, on average) and increases or decreases in the Fed Funds rate.

So, while we are always braced for disconcerting headlines, we know that the long-term trend in equity prices is up,

Valuations – Value Stocks Reasonably Priced

and we see no reason to alter our enthusiasm for reasonably priced Value stocks in general,

and our broadly diversified portfolios of what we believe are undervalued stocks in particular.

Stock News – Updates on nine stocks across six different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

RFK Appointment, Inflation, Valuations and more Stock News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss RFK Appointment, Inflation, Valuations and more Stock News. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Election 2024 – Stocks Retreat

RFK Appointment – Health Care Stock Traders Shoot First and Ask Questions Later

Seasonality – Most Wonderful Time of the Year

Econ Outlook – Favorable Stats; Solid GDP Growth the Forecast; Powell Upbeat

Rates – Stocks Have Performed Fine Whether Fed is Easing/Tightening or 10-Year Yield is Rising/Falling

Inflation – CPI & PPI Tick Higher

Valuations – Value Stocks Reasonably Priced

Stock News – Updates on nine stocks across six different sectors

Election 2024 – Stocks Retreat

The post-election rally hit a few potholes last week as investors were reminded that significant market volatility is always something with which we have had to contend to be able to enjoy terrific long-term returns.

RFK Appointment – Health Care Stock Traders Shoot First and Ask Questions Later

No doubt, traders were reminded that a Trump presidency (and any presidency for that matter) is not without a few curveballs, while a lack of great liquidity in individual stocks can lead to sizable price moves. Such was seen on Friday following the nomination of Robert F. Kennedy, Jr. as head of the Department of Health and Human Services, which sent Health Care stocks skidding and making the sector the worst-performing since Election Day.

Of course, there is some question about whether Mr. Kennedy will be confirmed for the job, while it is not clear exactly what policies he will attempt to or be able to implement. Certainly, we are not thinking that happy days will be here again for the pharmaceutical industry with RFK as the health czar, but the supposed vaccine skeptic told NPR earlier this month, “We’re not going to take vaccines away from anybody.” Further, we note that the drug industry has long navigated a less-than-friendly political climate.

While we have pulled back our Target Prices a smidge, we think traders are prone to shoot first and ask questions later and we have often seen that the proverbial bark is much worse than the bite when it comes to Washington. After all, there are numerous constituencies to consider, so immediate sweeping changes are tough to pull off, meaning that we are much more inclined to add to already undervalued stocks that were hit hard last week, especially if the herd stampedes toward the exits further in the days and weeks ahead.

Our shopping list would include vaccine (and many other drugs) makers Pfizer (PFE – $24.80) and Merck (MRK – $96.31), managed care provider Elevance Health (ELV – $400.69) and even advertising giant Omnicom Group (OMC – $96.86), the latter hit hard on Friday on worries about pharmaceutical marketing spend.

Seasonality – Most Wonderful Time of the Year

We have to expect plenty of market gyrations in the near term as traders make their bets on the winners and losers in the new administration. However, we offer the reminder that stocks have performed well, on average, no matter who is in the White House, even as the history books show that equities prefer supposedly less business-friendly Democrats in control in Washington.

We also should not forget that we are now in the seasonally more favorable six-month time span,

with the long-term evidence showing that November, December and January have been the best three months of the year, on average.

Econ Outlook – Favorable Stats; Solid GDP Growth the Forecast; Powell Upbeat

To be sure, stock prices often defy conventional wisdom in their short-term movements as the lousy market week just endured arguably was due to the release of favorable economic data! Indeed, the NFIB Small Business Optimism index for October came in at 93.7, ahead of the estimate of 92.0 and up from 91.5 in September,

the Empire State Manufacturing survey of factory activity in the New York area for November soared to a reading of 31.2, blowing away projections and reversing the -11.9 tally in October,

first-time filings for unemployment benefits in the latest week declined to 217,000 from 221,000 the week prior, continuing to reside near multi-generational lows,

industrial production pulled back by 0.3% in October, but this was better than the 0.4% decline that was expected,

and retail sales for October rose 0.4%, ahead of the 0.3% growth forecast.

Not surprisingly, Federal Reserve Chair Jerome H. Powell sounded upbeat on the U.S. economy in comments offered in an important speech on November 14,

while the latest estimate for Q4 real (inflation-adjusted) GDP growth from the Atlanta Fed held steady at a solid 2.5%,

with a favorable economic backdrop a positive and not a negative by our way of thinking, given that corporate profit growth is a major reason why stock prices have risen over the long term.

Rates – Stocks Have Performed Fine Whether Fed is Easing/Tightening or 10-Year Yield is Rising/Falling

True, the positive data on economic growth sent interest rates higher, pushing the yield on the 10-Year U.S. Treasury up to 4.44%, well above the 3.65% yield the day two months ago when the Federal Reserve initiated its current easing of monetary policy,

by cutting the target for the Fed Funds rate from the then 5.5% upper bound.

History shows that much like what has transpired since September 17, equities have managed solid gains, on average, whether the benchmark government bond yield is rising or falling,

but we understand that the question on the minds of many traders today is what it the likelihood of additional rate cuts, as the betting in the Fed Funds futures market saw wagers fall on another reduction at the December FOMC Meeting and an increase in the expected year-end 2025 rate to 3.83%, up a tick from 3.82% at the end of the previous week.

Inflation – CPI & PPI Tick Higher

The odds of a friendlier Fed were not helped when Boston Fed President Susan Collins said on Thursday, “Another rate cut in December is certainly on the table, but it’s not a done deal. There’s more data that we will see between now and December, and we’ll have to continue to weigh what makes sense.”

We also note that Chair Powell discussed inflation in his speech on Thursday, stating, “Inflation is running much closer to our 2 percent longer-run goal, but it is not there yet. We are committed to finishing the job,”

while the Consumer Price Index (CPI) ticked up in October to a 2.6% year-over-year increase, in line with expectations, but up from a 2.4% rise in September,

the Core CPI, which excludes volatile food and energy prices, held constant last month at a 3.3% advance

and prices at the wholesale level rose more than expected with a 2.4% increase.

Those inflation figures were not too dissimilar from the projections offered two months ago by Federal Reserve Board members and Federal Reserve Bank presidents,

and we lose little sleep about Jerome H. Powell & Co., given what the evidence shows for stock prices (they have risen, on average) and increases or decreases in the Fed Funds rate.

So, while we are always braced for disconcerting headlines, we know that the long-term trend in equity prices is up,

Valuations – Value Stocks Reasonably Priced

and we see no reason to alter our enthusiasm for reasonably priced Value stocks in general,

and our broadly diversified portfolios of what we believe are undervalued stocks in particular.

Stock News – Updates on nine stocks across six different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.