The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Fed Funds, Interest Rates, an Economic outlook and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week In Review – Some Stability, But Average Stock Still Struggling in August

Patience – Lots to Worry About Along the Way, But Over Time Equities Have Proved Rewarding

Interest Rates – Mortgage & Treasury Yields Elevated, But Below the Historical Average

Jackson Hole – Fed Chair Says Fed Will Tread Carefully, But Prepared to Raise Rates Further

Fed Funds – History Lesson on Rising Rates and Equity Returns

Econ Outlook – Data are Mixed; Healthy Corporate Profits Still the Expectation

Contrarian Sentiment – More Bears than AAII Bulls

Stock News – Updates on eight stocks across four different sectors

Week In Review – Some Stability, But Average Stock Still Struggling in August

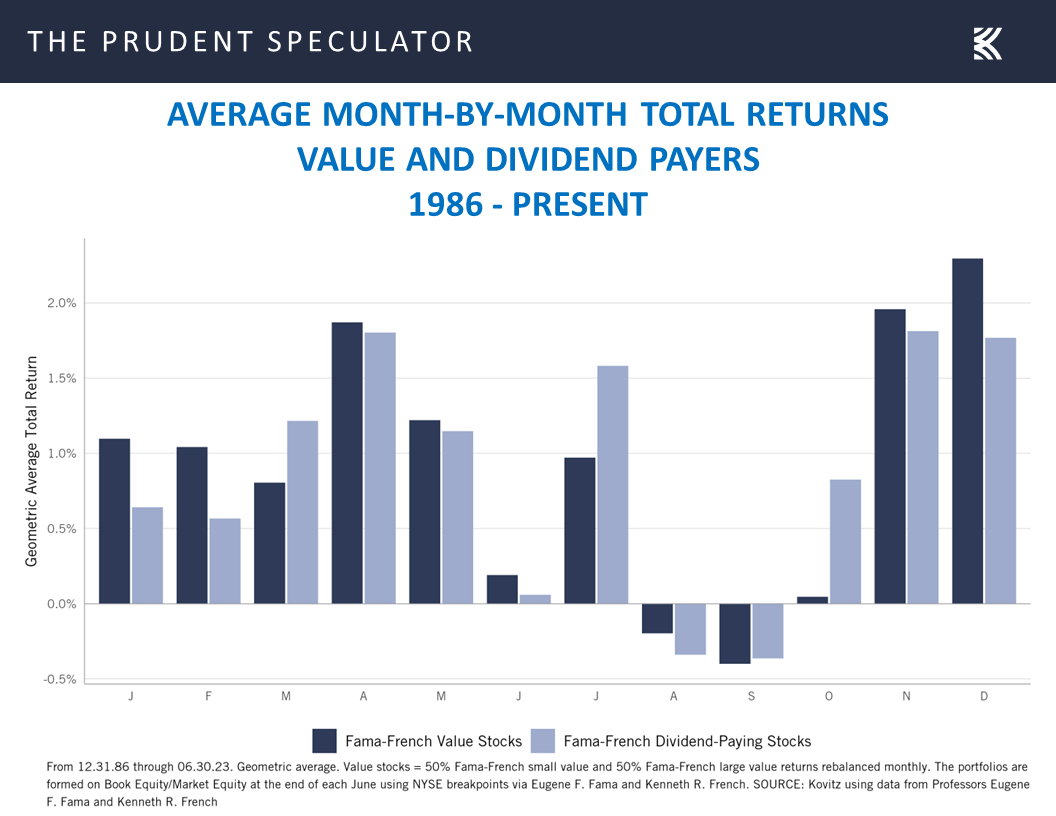

The average stock in the Russell 3000 index ended the latest trading week down 0.60%, but the equity markets staunched some of the August bleeding. Of course, some might argue that the wounds suffered this month are par for the course, given that August and September are the only two months of the year, on average, where Value Stocks and Dividend Payers have been in the red since your Editor arrived at The Prudent Speculator more than 36 years ago.

Patience – Lots to Worry About Along the Way, But Over Time Equities Have Proved Rewarding

Happily, the other 10 months have seen gains on average, so much so that the kind of stocks that we have long favored have enjoyed the best returns since the launch of our publication back in March 1977, with those who have stuck with equities through thick and thin enjoying the miracle of compounding.

Obviously, it isn’t always easy to keep the faith, especially given that the constant gyrations in stock prices are often exacerbated by disconcerting major news events, but time and again stocks have overcome near-term difficulties to go on to post terrific long-term gains.

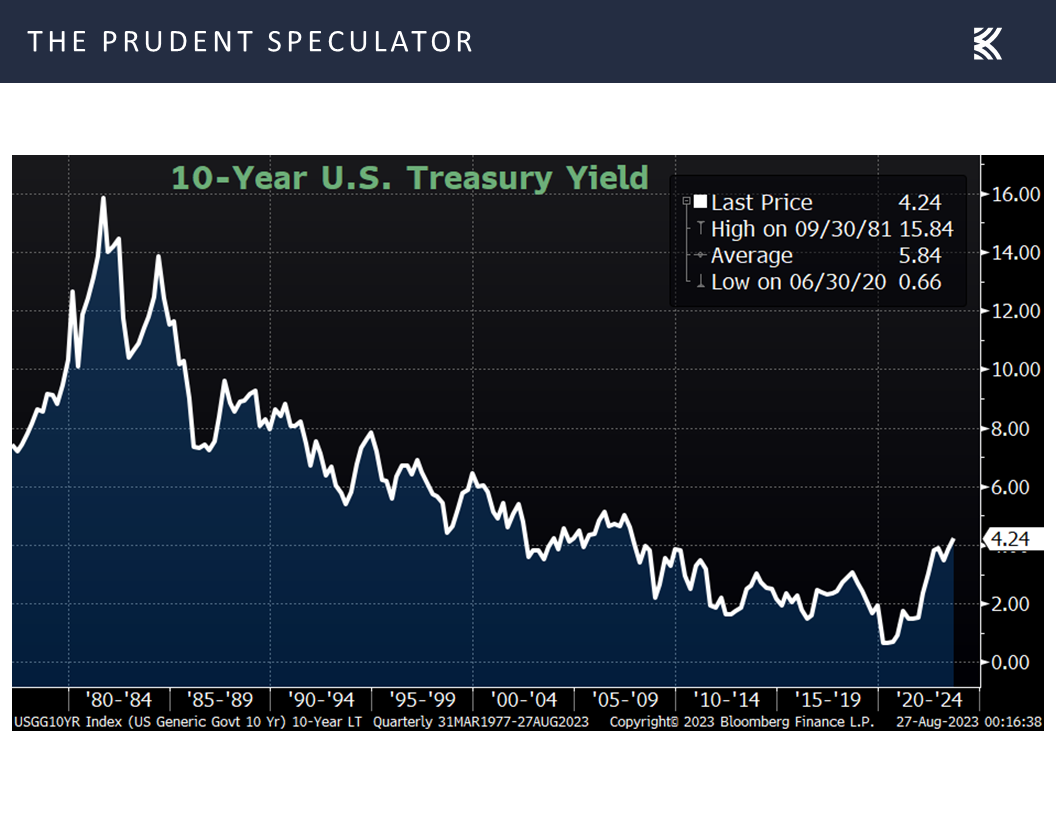

Interest Rates – Mortgage & Treasury Yields Elevated, But Below the Historical Average

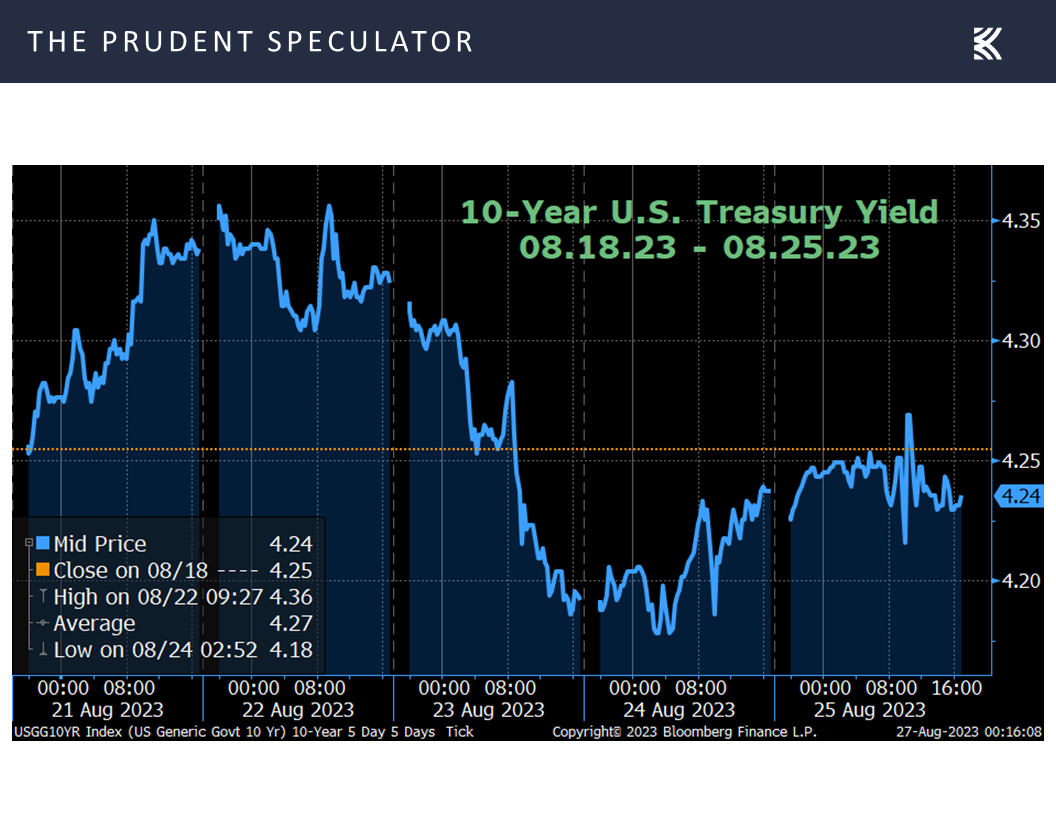

At the top of the worry list for investors these days is the jump in interest rates though the yield on the benchmark 10-year U.S. Treasury held steady last week,

with the 4.24% rate at a 16-year high, but still at a level that is well below the average since the launch of The Prudent Speculator.

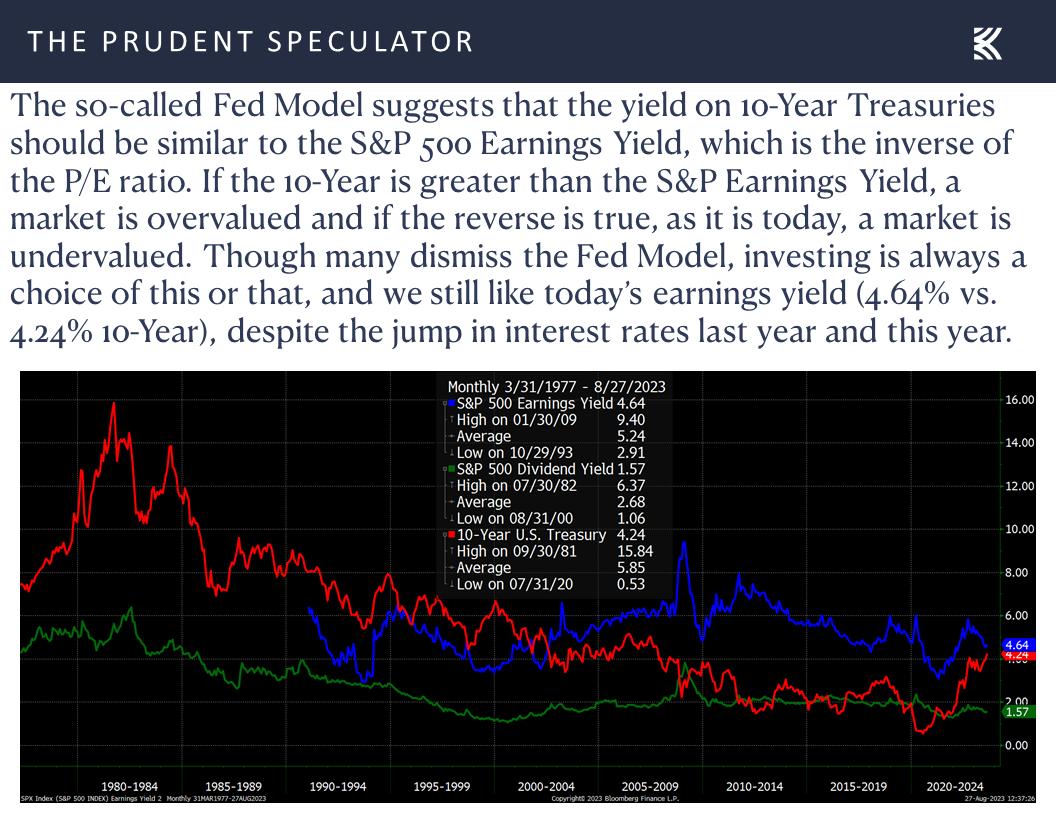

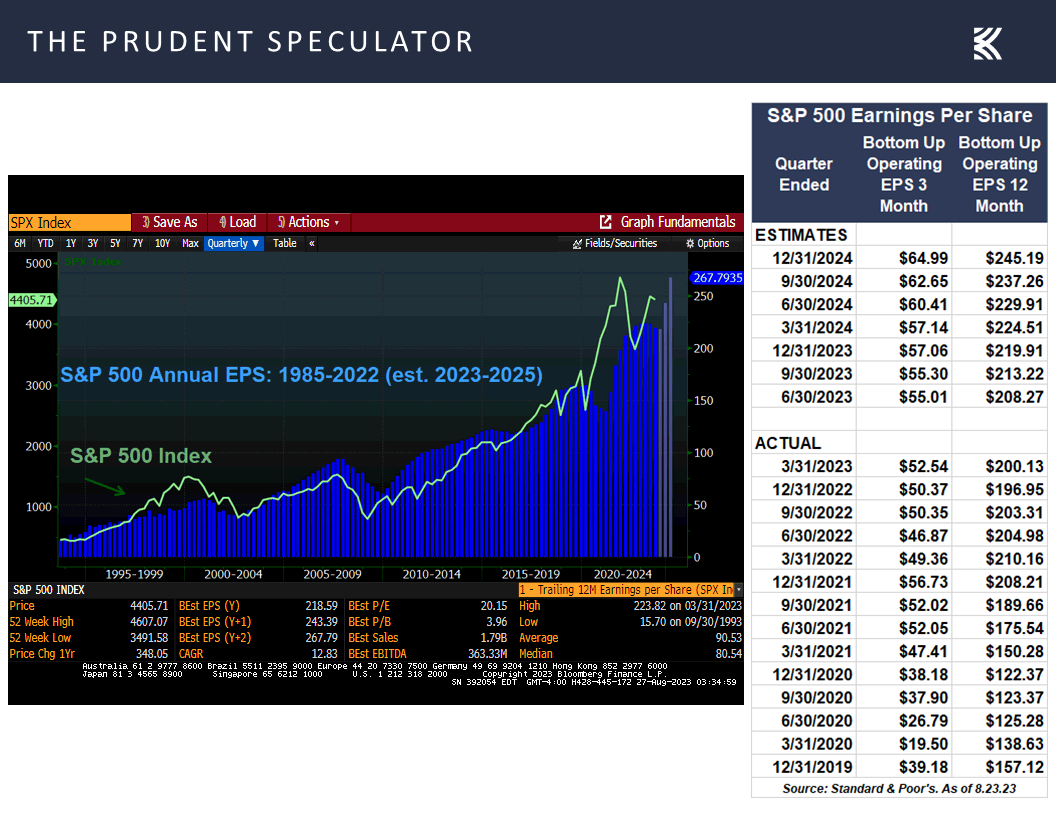

Believe it or not, a case can be made that even the S&P 500 is still reasonably valued in the current interest rate environment,

while we continue to assert that our broadly diversified portfolios of what we believe to be undervalued stocks are inexpensively priced.

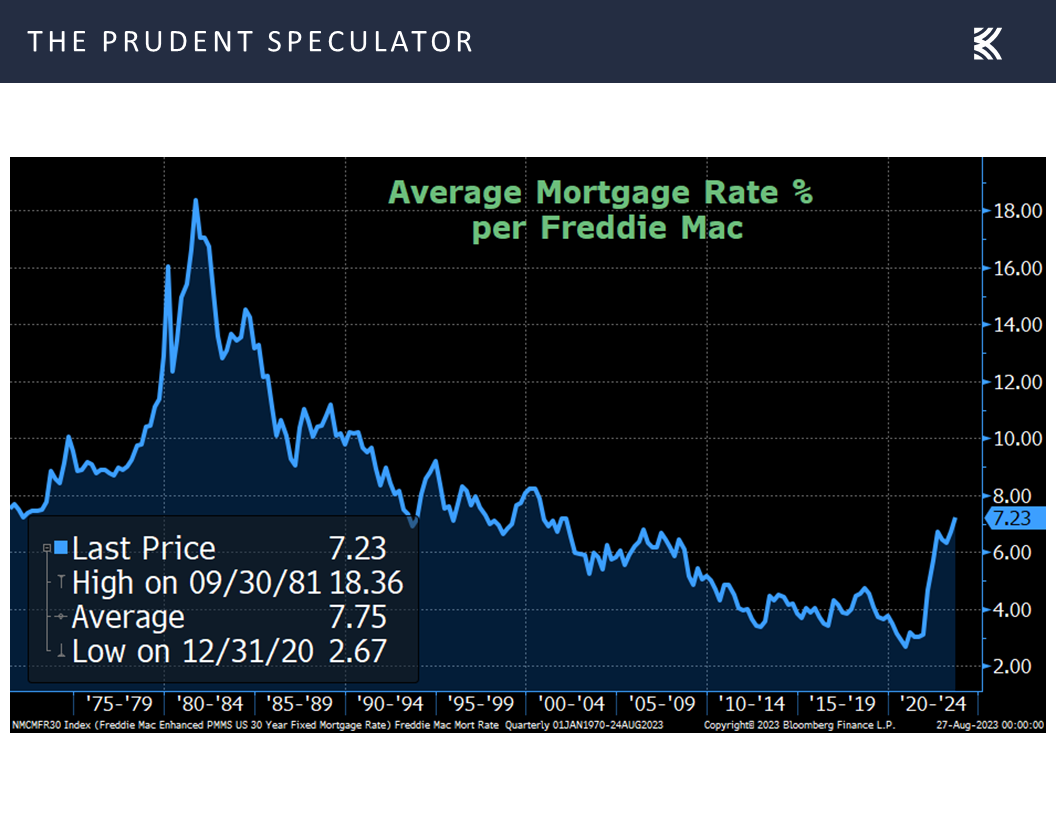

To be sure, rising interest rates are taking a toll on the housing sector with the spike in borrowing costs (they are still below the long-term average),

keeping many folks in their houses and their locked-in-very-low low mortgage rates, which is putting a lid on the supply of existing homes, and, interestingly, boosting demand for new homes.

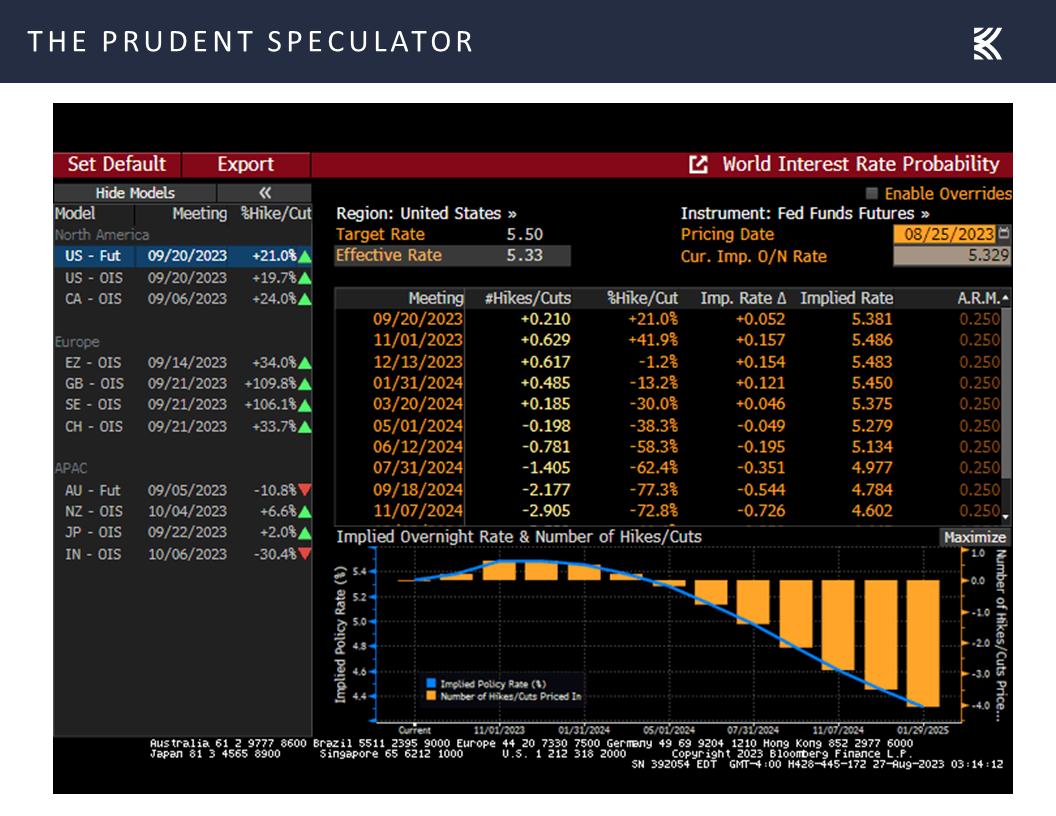

Not surprisingly, given that current expectations per the futures market are that the Federal Reserve is near the end of its rate-hiking cycle, with one more 25-basis-point increase possible this year before several cuts take place in 2024,

Jackson Hole – Fed Chair Says Fed Will Tread Carefully, But Prepared to Raise Rates Further

investors were hanging on every word of Jerome H. Powell’s speech this past Friday morning at the Jackson Hole economic confab. The introduction of Inflation: Progress and the Path Ahead, read:

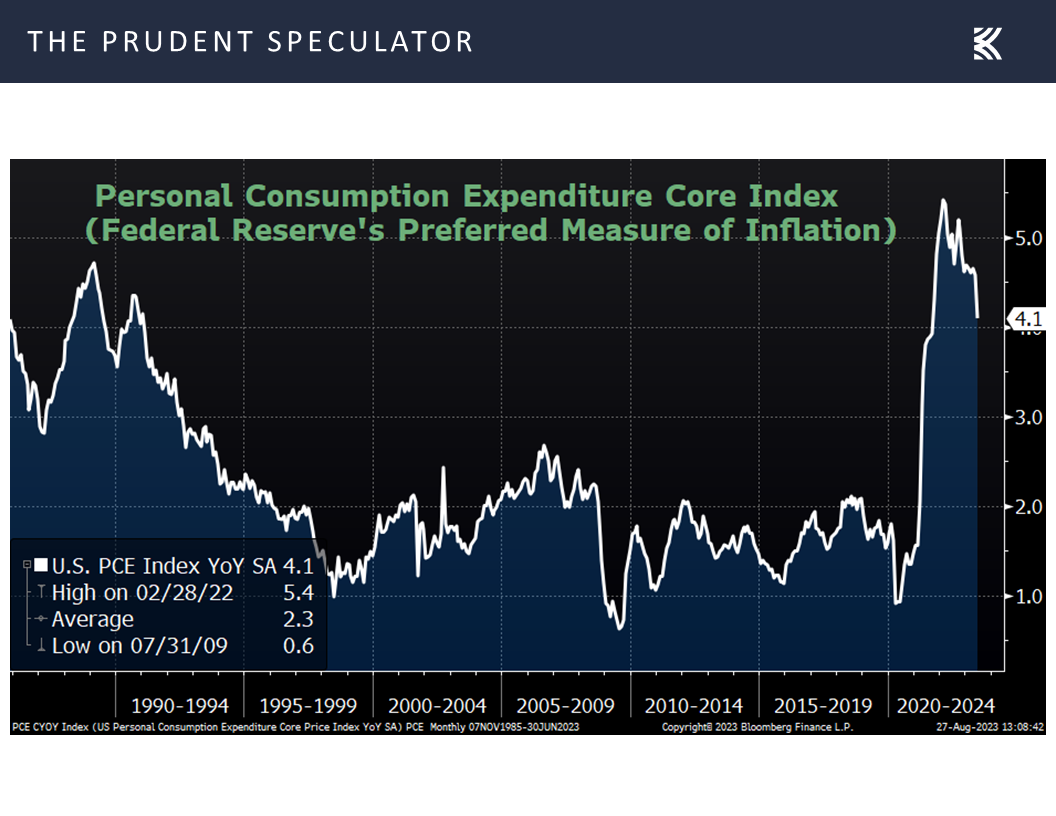

Good morning. At last year’s Jackson Hole symposium, I delivered a brief, direct message. My remarks this year will be a bit longer, but the message is the same: It is the Fed’s job to bring inflation down to our 2 percent goal, and we will do so. We have tightened policy significantly over the past year. Although inflation has moved down from its peak—a welcome development—it remains too high. We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.

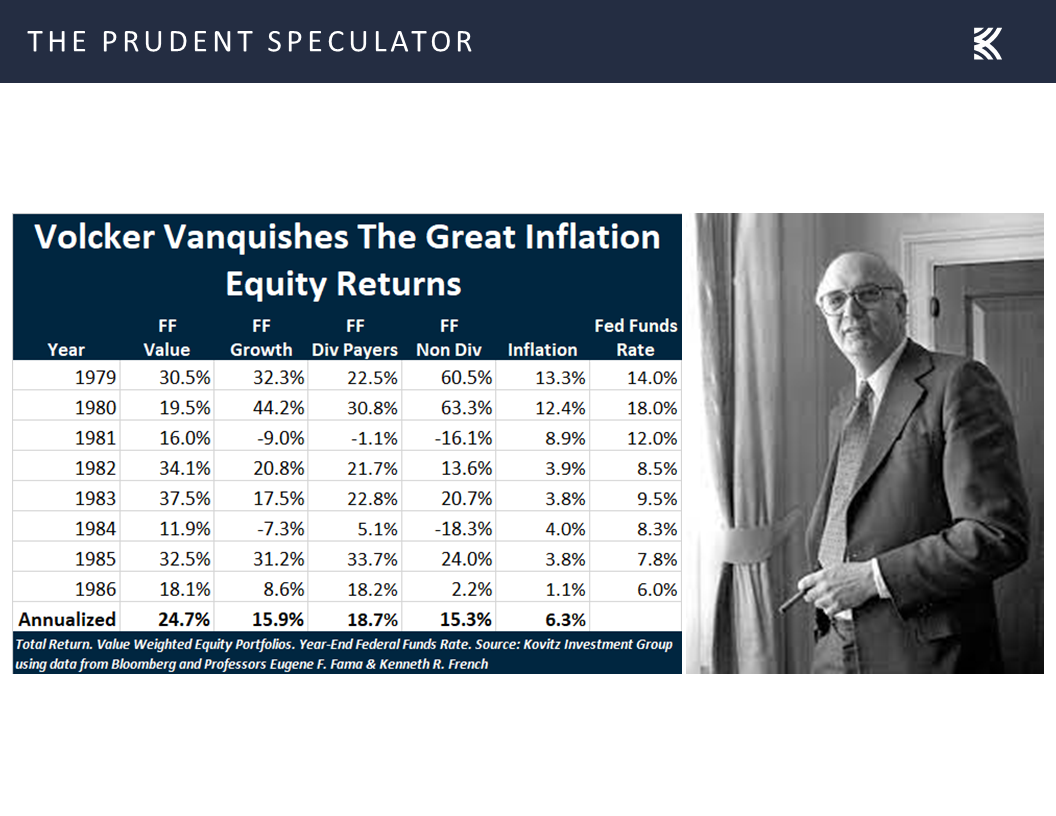

Certainly, Chair Powell’s tough “we will do so” talk on inflation might suggest that the tighter stance toward monetary policy will continue, but we definitely will not mind if the current battle has the same result for equities as the last time the Fed had to aggressively fight inflation. Incredibly, despite the economy enduring two recessions in the process, the Volcker Fed years (1979 yo 1986) resulted in sensational returns for Value Stocks and Dividend Payers.

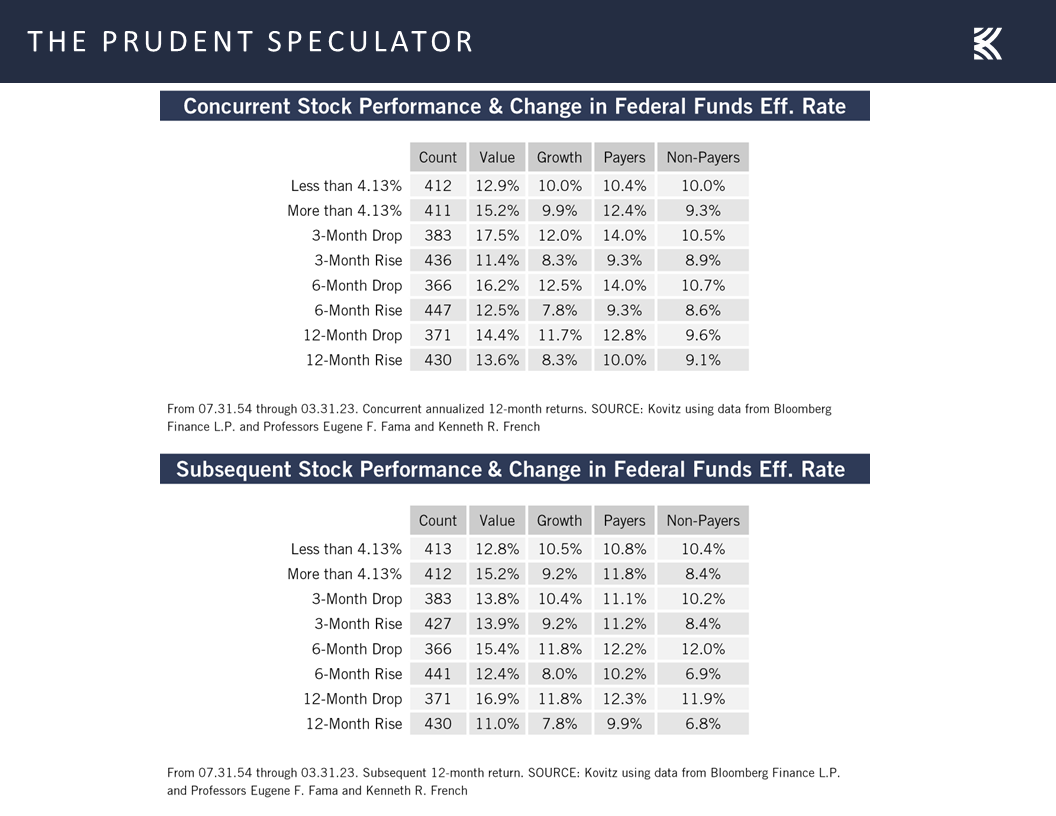

Fed Funds – History Lesson on Rising Rates and Equity Returns

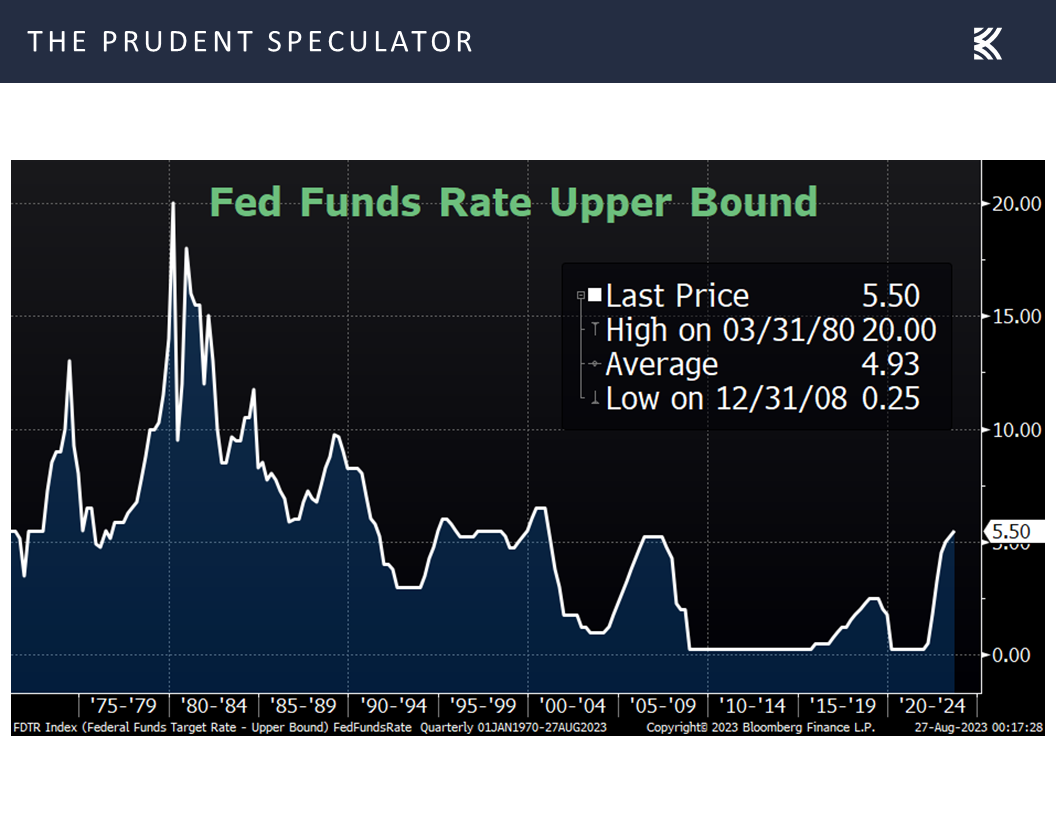

Yes, the Fed Funds rate was significantly higher back then than it is today

but stocks historically have performed well, on average, whether the Fed Funds rate is rising or falling. And, Value Stocks and Dividend Payers have done better, on average, when the Fed Funds rate is above the 4.13% median!

Econ Outlook – Data are Mixed; Healthy Corporate Profits Still the Expectation

Turning toward the health of the economy, Chair Powell offered comments below,

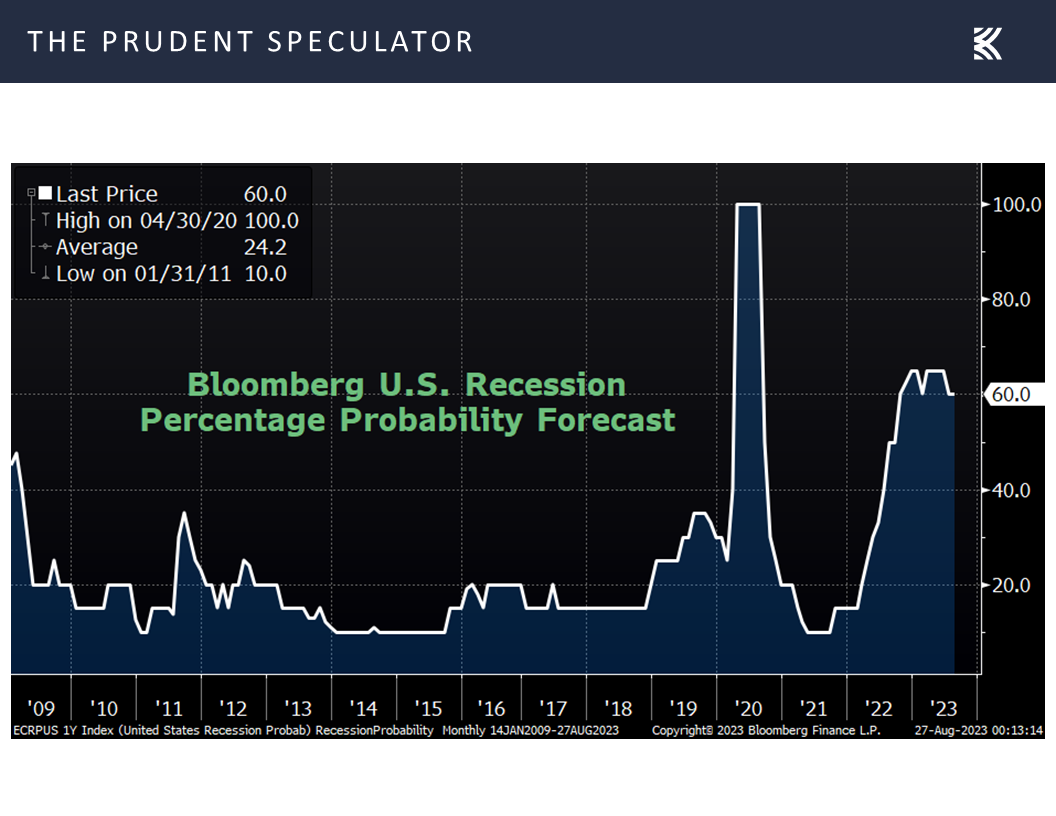

which seemed to suggest that the current odds of recession at 60% as tabulated by Bloomberg might be too high,

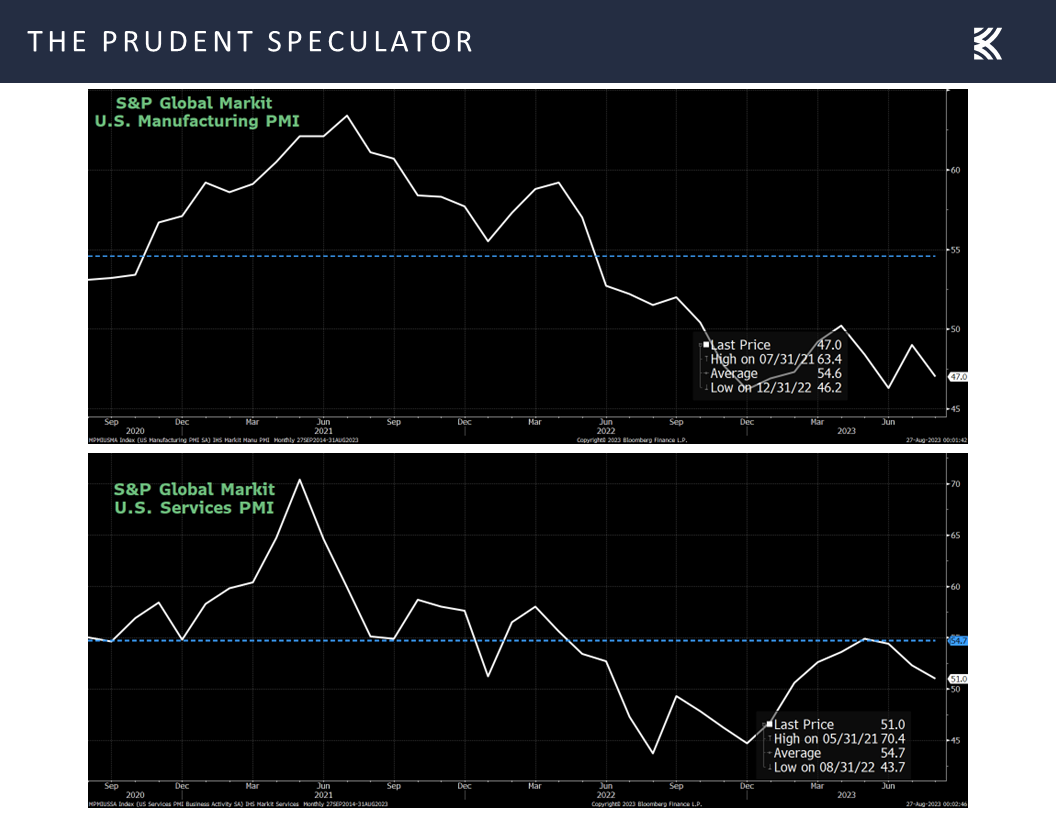

even as the latest read on the state of the factory and service sectors for August from S&P Global Markit came in below expectations and down from July’s tallies,

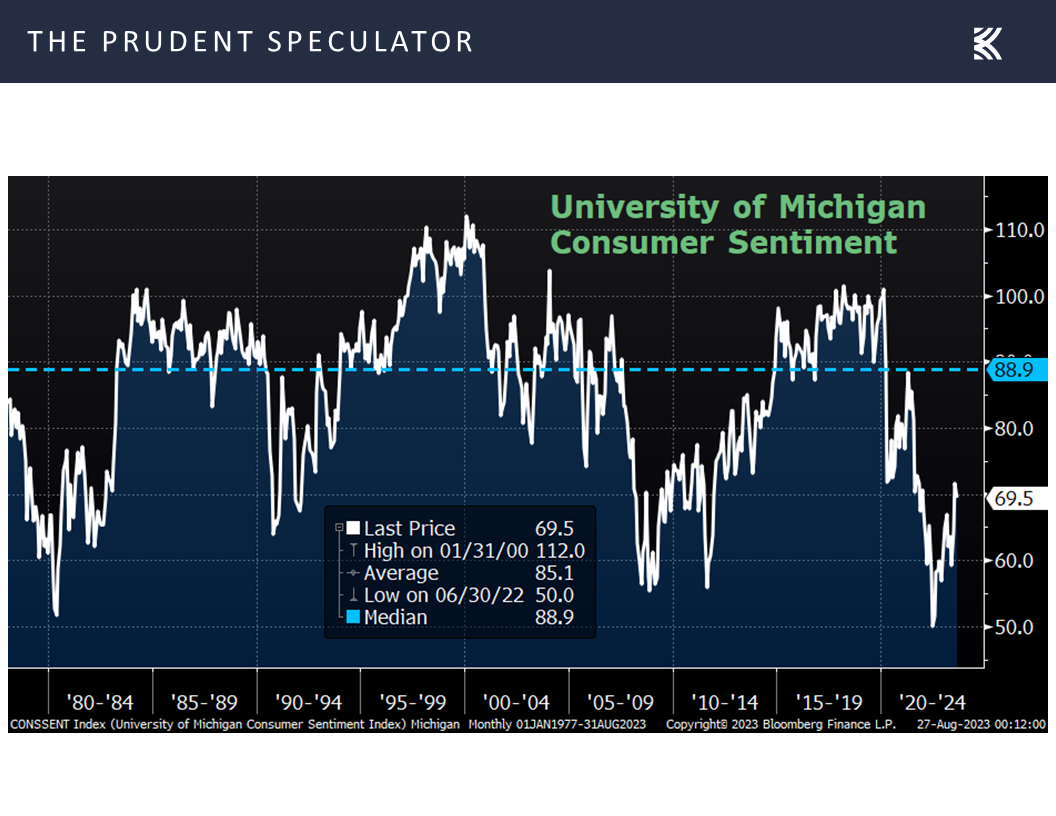

consumer sentiment for August, per the Univ. of Michigan, dropped to 69.5, below July’s number and the estimate, both of which were 71.2,

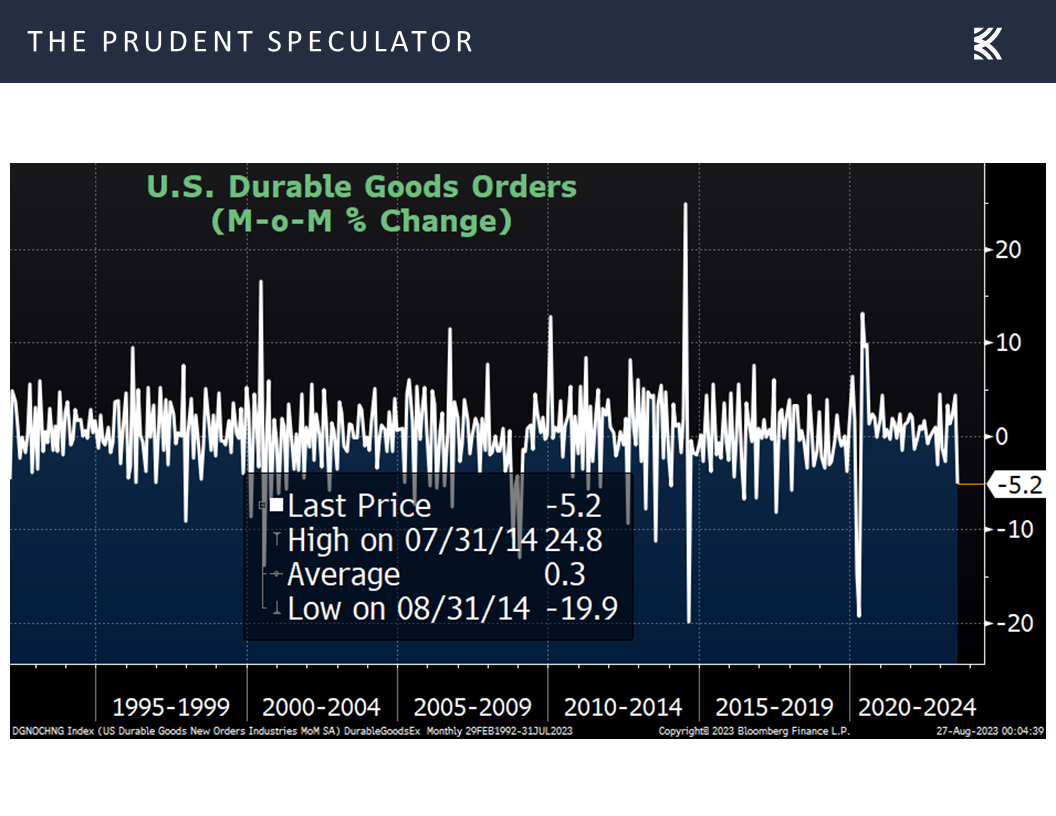

and orders for big-ticket items dipped 5.2% in July.

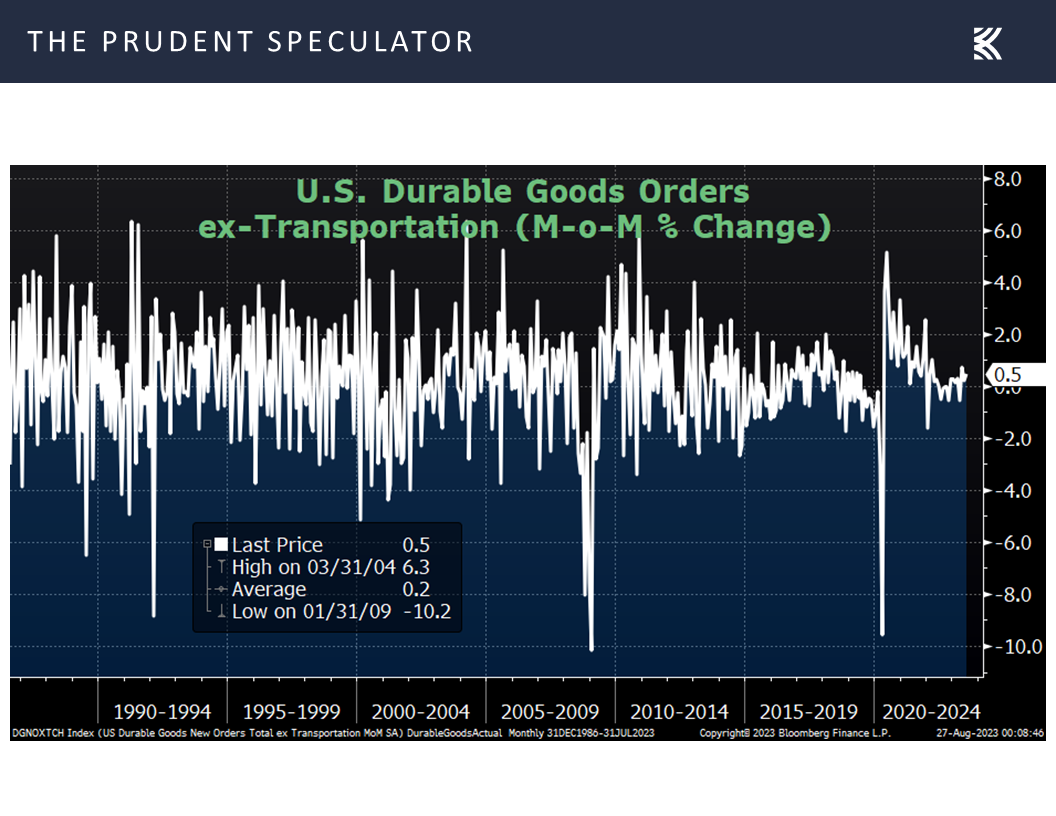

Of course, the durable goods figure rose a better-than-forecast 0.5% if the volatile transportation sector was excluded,

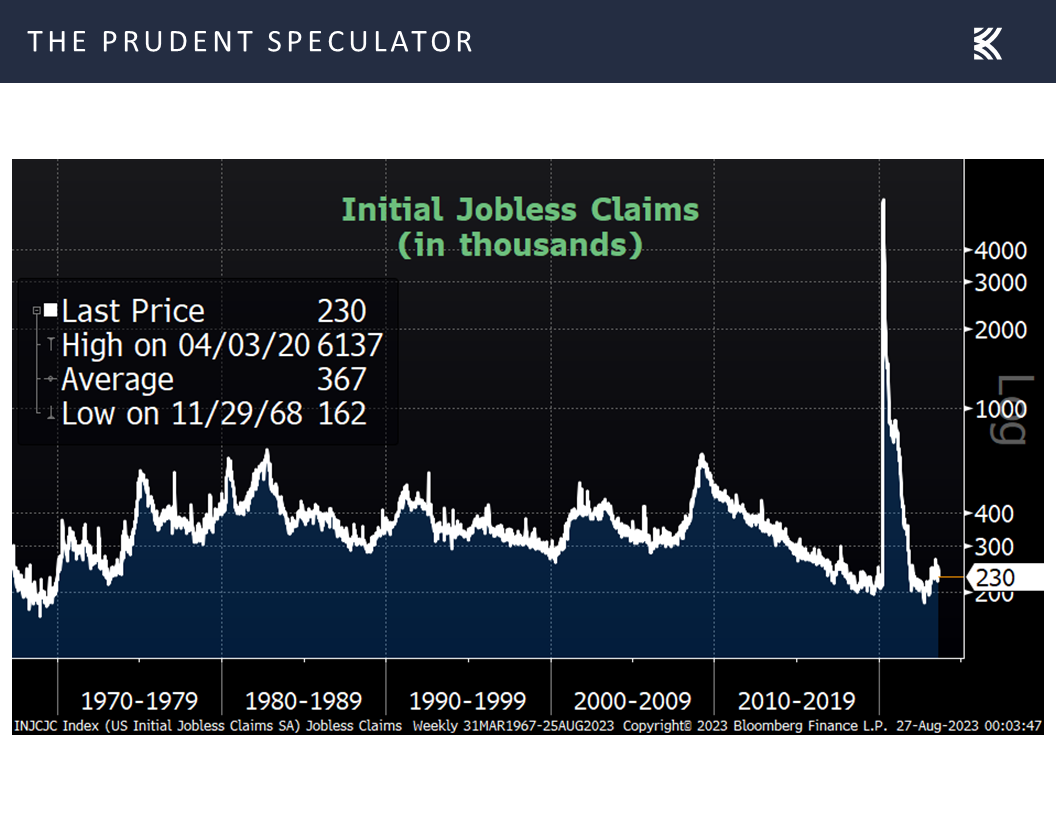

while first-time filings for unemployment benefits in the latest week fell to a better-than-expected 230,000,

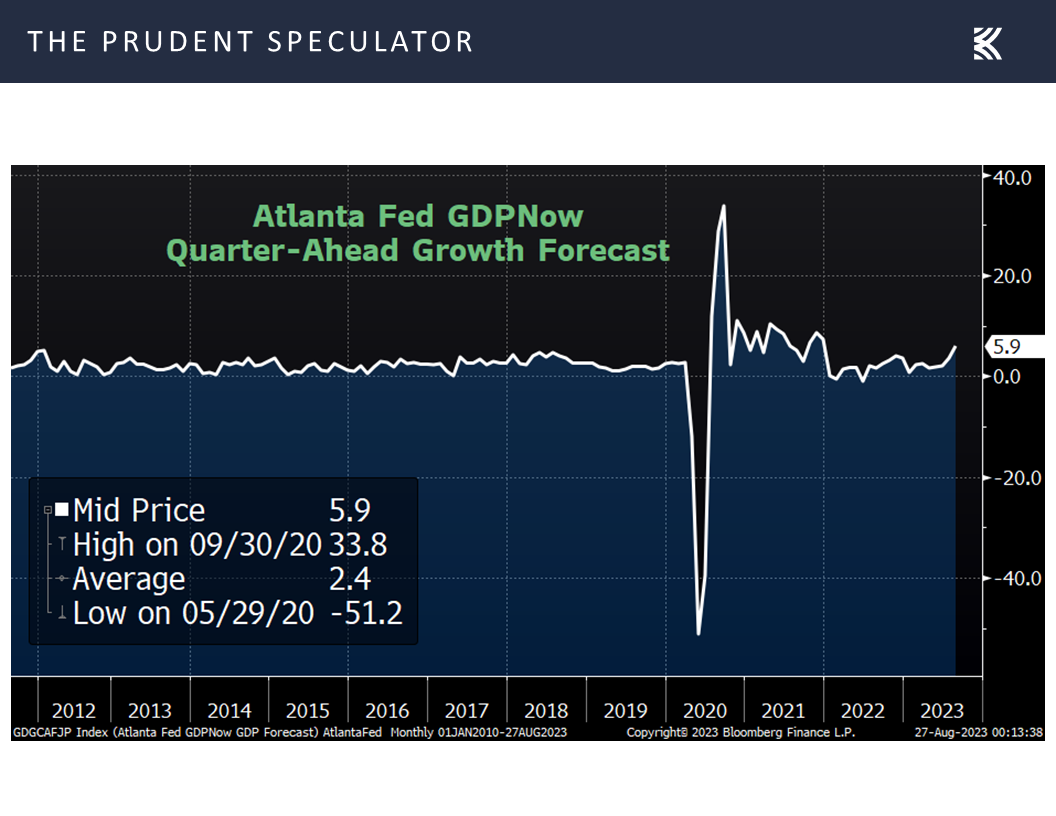

and the most recent estimate for real (inflation-adjusted) U.S. GDP growth for Q3 from the Atlanta Fed climbed to a very robust 5.9%.

There are plenty of cross currents, so it is probably no surprise that Chair Powell offered a relatively balanced conclusion to his important Jackson Hole speech:

As is often the case, we are navigating by the stars under cloudy skies. In such circumstances, risk-management considerations are critical. At upcoming meetings, we will assess our progress based on the totality of the data and the evolving outlook and risks. Based on this assessment, we will proceed carefully as we decide whether to tighten further or, instead, to hold the policy rate constant and await further data. Restoring price stability is essential to achieving both sides of our dual mandate. We will need price stability to achieve a sustained period of strong labor market conditions that benefit all.

We will keep at it until the job is done.

*****

From our perspective, nothing we heard in the Powell speech (the Fed will continue to be data dependent) changes our view on the favorable long-term prospects for equities. We believe that the economy will remain healthy enough to support growth in corporate profits, which has been the long-term driver of the upward trend in stock prices.

Contrarian Sentiment – More Bears than AAII Bulls

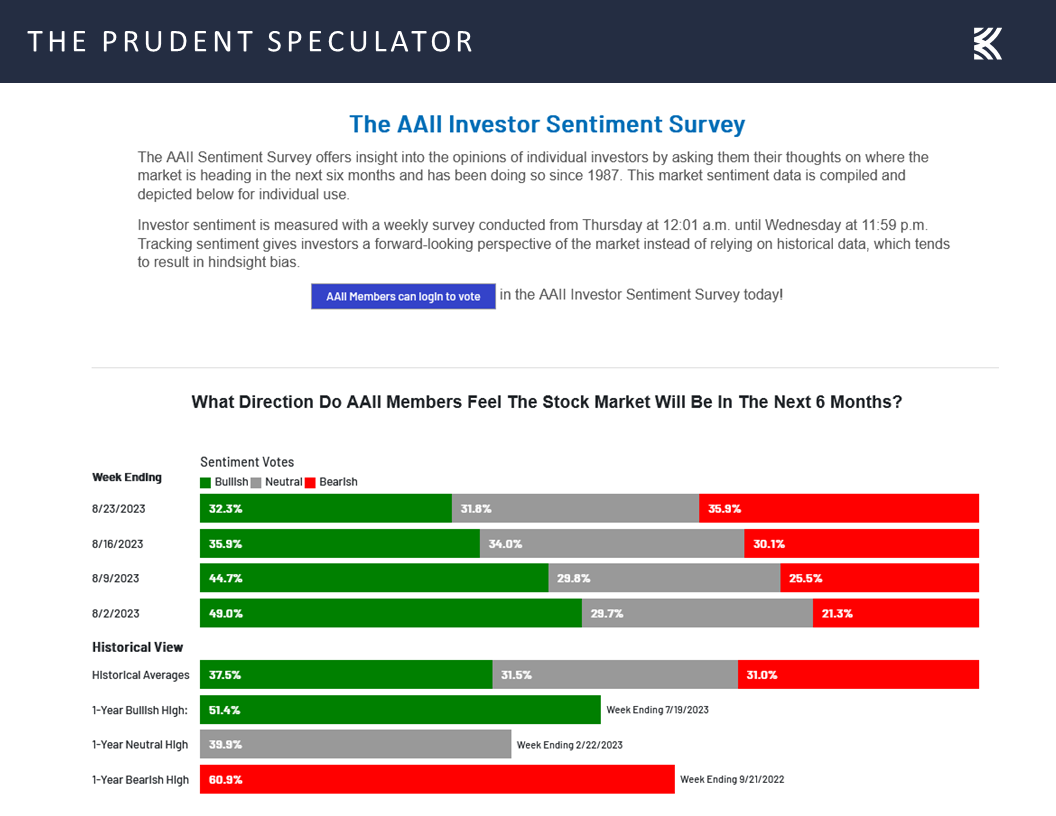

And, given our contrarian bias, we like that the mood on Main Street has darkened in recent weeks, with this past Thursday’s release of the latest Sentiment Survey from the American Association of Individual Investors (AAII) showing more Bears than Bulls. Incredibly, it was just three weeks ago that the Bulls trounced the Bears, with sharply lower prices in the interim somehow causing folks to like stocks less.

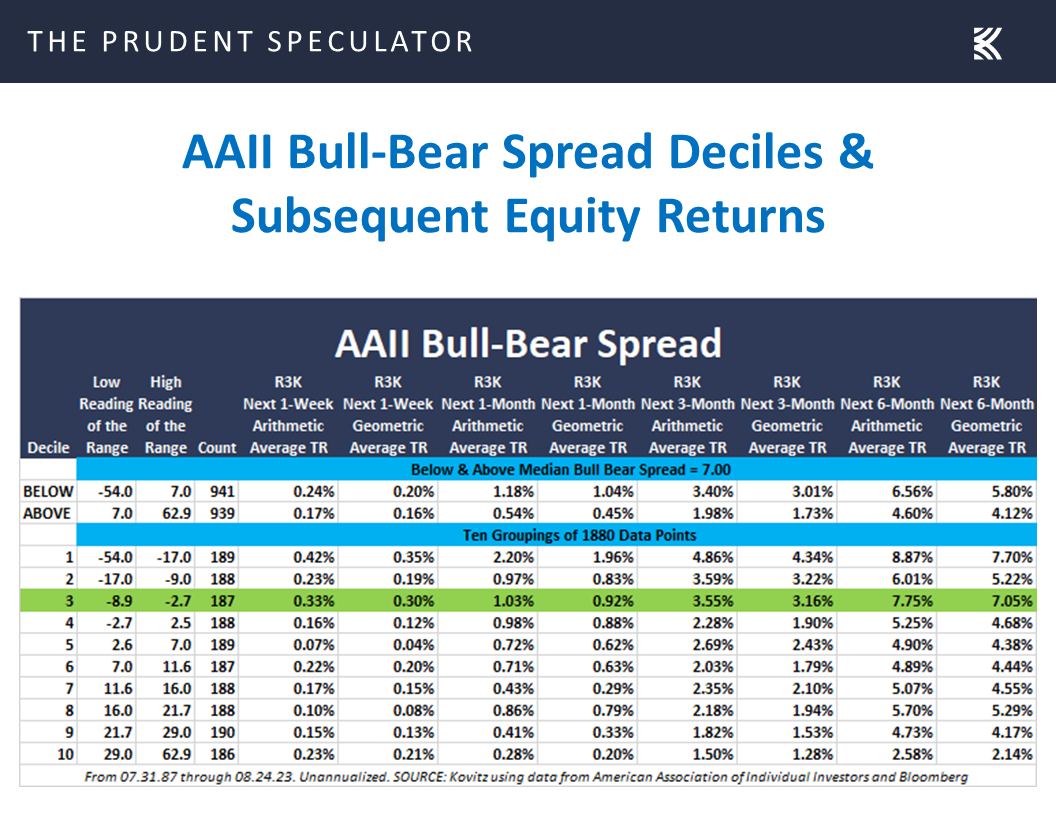

With the historical evidence showing that the first part of Warren Buffett’s admonition, “Be greedy when others are fearful and fearful when others are greedy,” is far more accurate than the last part, we don’t mind that the AAII Bull-Bear spread is now in the third lowest decile. After all, subsequent returns have been better when Main Street is pessimistic than when it is optimistic,

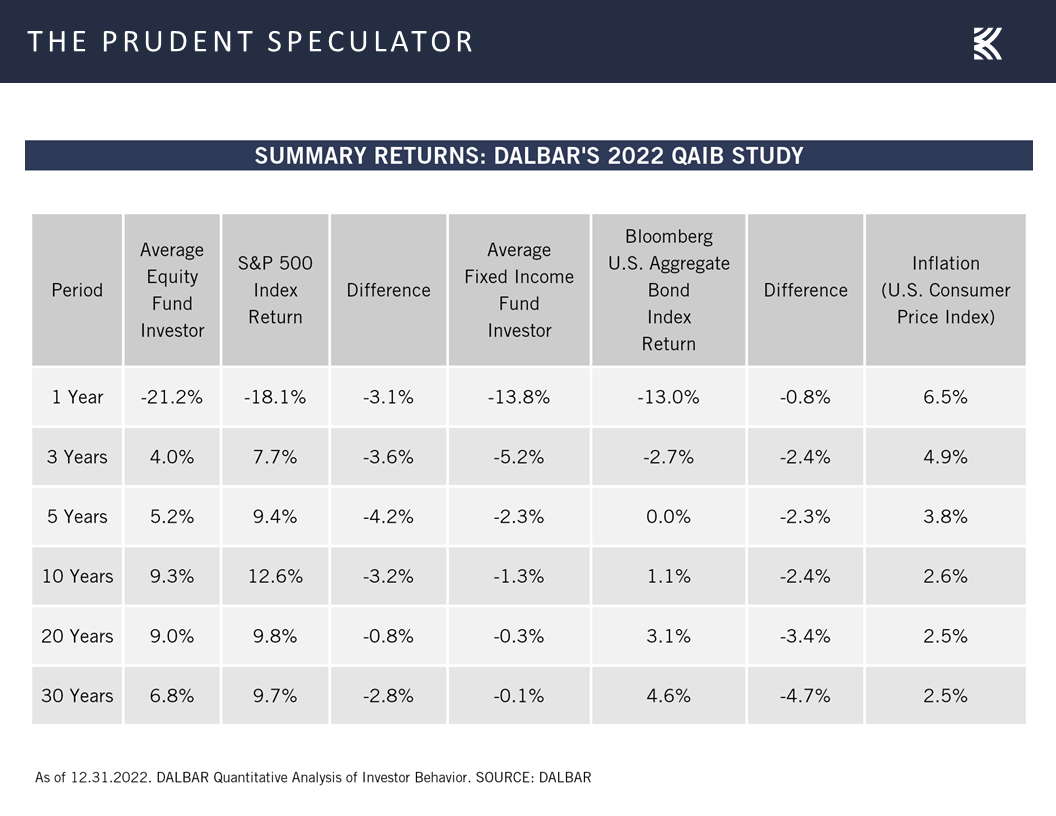

illustrating why we always say that the only problem with market timing is getting the timing right…whether, as data from DALBAR shows, one is an equity or fixed income investor.

Stock News – Updates on eight stocks across four different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Fed Funds, Interest Rates and an Economic Outlook

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Fed Funds, Interest Rates, an Economic outlook and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week In Review – Some Stability, But Average Stock Still Struggling in August

Patience – Lots to Worry About Along the Way, But Over Time Equities Have Proved Rewarding

Interest Rates – Mortgage & Treasury Yields Elevated, But Below the Historical Average

Jackson Hole – Fed Chair Says Fed Will Tread Carefully, But Prepared to Raise Rates Further

Fed Funds – History Lesson on Rising Rates and Equity Returns

Econ Outlook – Data are Mixed; Healthy Corporate Profits Still the Expectation

Contrarian Sentiment – More Bears than AAII Bulls

Stock News – Updates on eight stocks across four different sectors

Week In Review – Some Stability, But Average Stock Still Struggling in August

The average stock in the Russell 3000 index ended the latest trading week down 0.60%, but the equity markets staunched some of the August bleeding. Of course, some might argue that the wounds suffered this month are par for the course, given that August and September are the only two months of the year, on average, where Value Stocks and Dividend Payers have been in the red since your Editor arrived at The Prudent Speculator more than 36 years ago.

Patience – Lots to Worry About Along the Way, But Over Time Equities Have Proved Rewarding

Happily, the other 10 months have seen gains on average, so much so that the kind of stocks that we have long favored have enjoyed the best returns since the launch of our publication back in March 1977, with those who have stuck with equities through thick and thin enjoying the miracle of compounding.

Obviously, it isn’t always easy to keep the faith, especially given that the constant gyrations in stock prices are often exacerbated by disconcerting major news events, but time and again stocks have overcome near-term difficulties to go on to post terrific long-term gains.

Interest Rates – Mortgage & Treasury Yields Elevated, But Below the Historical Average

At the top of the worry list for investors these days is the jump in interest rates though the yield on the benchmark 10-year U.S. Treasury held steady last week,

with the 4.24% rate at a 16-year high, but still at a level that is well below the average since the launch of The Prudent Speculator.

Believe it or not, a case can be made that even the S&P 500 is still reasonably valued in the current interest rate environment,

while we continue to assert that our broadly diversified portfolios of what we believe to be undervalued stocks are inexpensively priced.

To be sure, rising interest rates are taking a toll on the housing sector with the spike in borrowing costs (they are still below the long-term average),

keeping many folks in their houses and their locked-in-very-low low mortgage rates, which is putting a lid on the supply of existing homes, and, interestingly, boosting demand for new homes.

Not surprisingly, given that current expectations per the futures market are that the Federal Reserve is near the end of its rate-hiking cycle, with one more 25-basis-point increase possible this year before several cuts take place in 2024,

Jackson Hole – Fed Chair Says Fed Will Tread Carefully, But Prepared to Raise Rates Further

investors were hanging on every word of Jerome H. Powell’s speech this past Friday morning at the Jackson Hole economic confab. The introduction of Inflation: Progress and the Path Ahead, read:

Good morning. At last year’s Jackson Hole symposium, I delivered a brief, direct message. My remarks this year will be a bit longer, but the message is the same: It is the Fed’s job to bring inflation down to our 2 percent goal, and we will do so. We have tightened policy significantly over the past year. Although inflation has moved down from its peak—a welcome development—it remains too high. We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.

Certainly, Chair Powell’s tough “we will do so” talk on inflation might suggest that the tighter stance toward monetary policy will continue, but we definitely will not mind if the current battle has the same result for equities as the last time the Fed had to aggressively fight inflation. Incredibly, despite the economy enduring two recessions in the process, the Volcker Fed years (1979 yo 1986) resulted in sensational returns for Value Stocks and Dividend Payers.

Fed Funds – History Lesson on Rising Rates and Equity Returns

Yes, the Fed Funds rate was significantly higher back then than it is today

but stocks historically have performed well, on average, whether the Fed Funds rate is rising or falling. And, Value Stocks and Dividend Payers have done better, on average, when the Fed Funds rate is above the 4.13% median!

Econ Outlook – Data are Mixed; Healthy Corporate Profits Still the Expectation

Turning toward the health of the economy, Chair Powell offered comments below,

which seemed to suggest that the current odds of recession at 60% as tabulated by Bloomberg might be too high,

even as the latest read on the state of the factory and service sectors for August from S&P Global Markit came in below expectations and down from July’s tallies,

consumer sentiment for August, per the Univ. of Michigan, dropped to 69.5, below July’s number and the estimate, both of which were 71.2,

and orders for big-ticket items dipped 5.2% in July.

Of course, the durable goods figure rose a better-than-forecast 0.5% if the volatile transportation sector was excluded,

while first-time filings for unemployment benefits in the latest week fell to a better-than-expected 230,000,

and the most recent estimate for real (inflation-adjusted) U.S. GDP growth for Q3 from the Atlanta Fed climbed to a very robust 5.9%.

There are plenty of cross currents, so it is probably no surprise that Chair Powell offered a relatively balanced conclusion to his important Jackson Hole speech:

As is often the case, we are navigating by the stars under cloudy skies. In such circumstances, risk-management considerations are critical. At upcoming meetings, we will assess our progress based on the totality of the data and the evolving outlook and risks. Based on this assessment, we will proceed carefully as we decide whether to tighten further or, instead, to hold the policy rate constant and await further data. Restoring price stability is essential to achieving both sides of our dual mandate. We will need price stability to achieve a sustained period of strong labor market conditions that benefit all.

We will keep at it until the job is done.

*****

From our perspective, nothing we heard in the Powell speech (the Fed will continue to be data dependent) changes our view on the favorable long-term prospects for equities. We believe that the economy will remain healthy enough to support growth in corporate profits, which has been the long-term driver of the upward trend in stock prices.

Contrarian Sentiment – More Bears than AAII Bulls

And, given our contrarian bias, we like that the mood on Main Street has darkened in recent weeks, with this past Thursday’s release of the latest Sentiment Survey from the American Association of Individual Investors (AAII) showing more Bears than Bulls. Incredibly, it was just three weeks ago that the Bulls trounced the Bears, with sharply lower prices in the interim somehow causing folks to like stocks less.

With the historical evidence showing that the first part of Warren Buffett’s admonition, “Be greedy when others are fearful and fearful when others are greedy,” is far more accurate than the last part, we don’t mind that the AAII Bull-Bear spread is now in the third lowest decile. After all, subsequent returns have been better when Main Street is pessimistic than when it is optimistic,

illustrating why we always say that the only problem with market timing is getting the timing right…whether, as data from DALBAR shows, one is an equity or fixed income investor.

Stock News – Updates on eight stocks across four different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.