The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Federal Reserve, Debt Ceiling, Corporate Profits, Valuations and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Five Days in Review – First Up Week of May

Debt Ceiling – Historical Perspective

Contrarian Sentiment – Wall & Main Street Both Pessimistic

Econ News – Mixed Data, But Q2 GDP Outlook Improves

Fed Speak – Interest Rates May Not Need to Be Raised Much Higher

Valuations – Stocks Reasonably Priced; Liking the Metrics for our Portfolios

Corporate Profits – EPS Growth Still the Forecast

Keeping the Faith – Don’t Interrupt Compounding Unnecessarily

Stock News – Updates on nine stocks across six different sectors

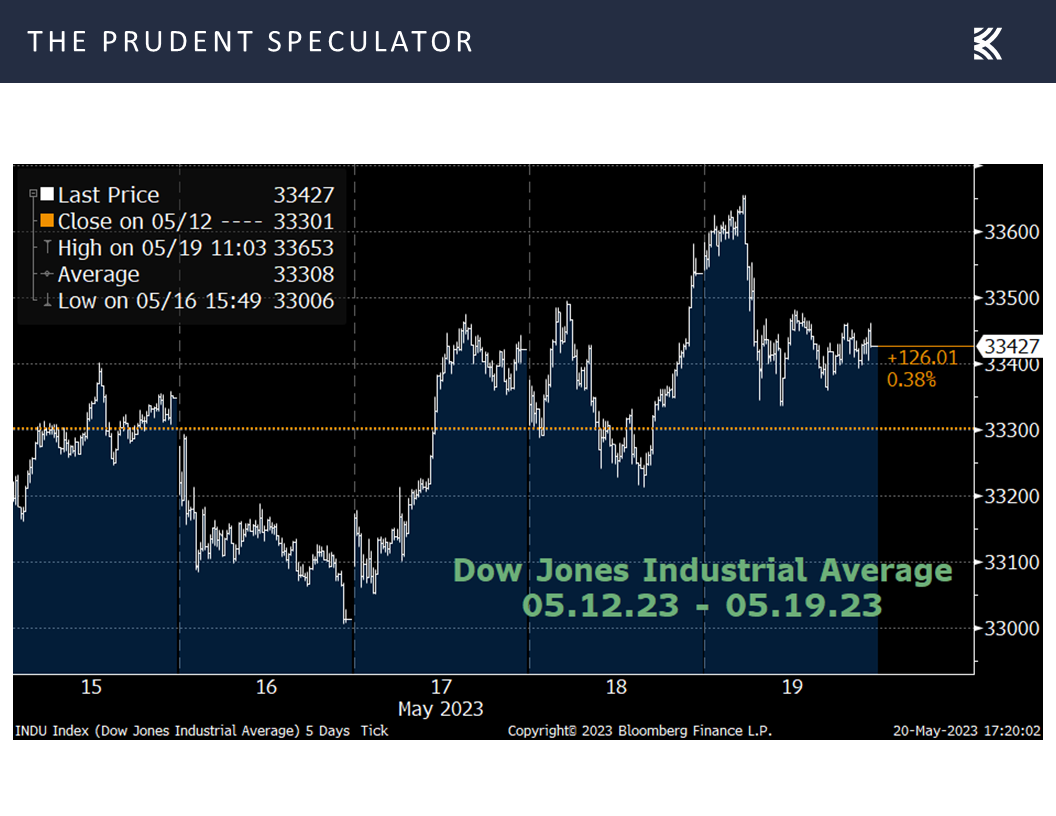

Five Days in Review – First Up Week of May

The equity market roller-coaster ride seemingly gyrated more wildly than usual over the last five days, though the Dow Jones Industrial Average ended with a modest gain for the period,

completing the first positive week in the seasonally less favorable (though still positive) time of the year.

Debt Ceiling – Historical Perspective

The primary catalyst for the move higher in the middle of the week was optimism about that the country would not default on its obligations via the raising of the debt ceiling. As the Treasury’s website states, “Since 1960, Congress has acted 78 separate times to permanently raise, temporarily extend, or revise the definition of the debt limit – 49 times under Republican presidents and 29 times under Democratic presidents. Congressional leaders in both parties have recognized that this is necessary.”

Of course, stocks proceeded to tumble on Friday when House Speaker Kevin McCarthy said it was time to “press pause” on the talks until President Biden returned from the G-7 Summit in Japan. The rhetoric over the weekend was not exactly encouraging as Mr. Biden said, “Republicans need to move from their extreme position,” while Mr. McCarthy claimed, “The White House has moved backwards.”

However, on Sunday afternoon, the duo spoke telephonically on the President’s flight back from Japan, with the House leader suggesting the phone calls were “productive” and that there would be an in-person meeting on Monday.

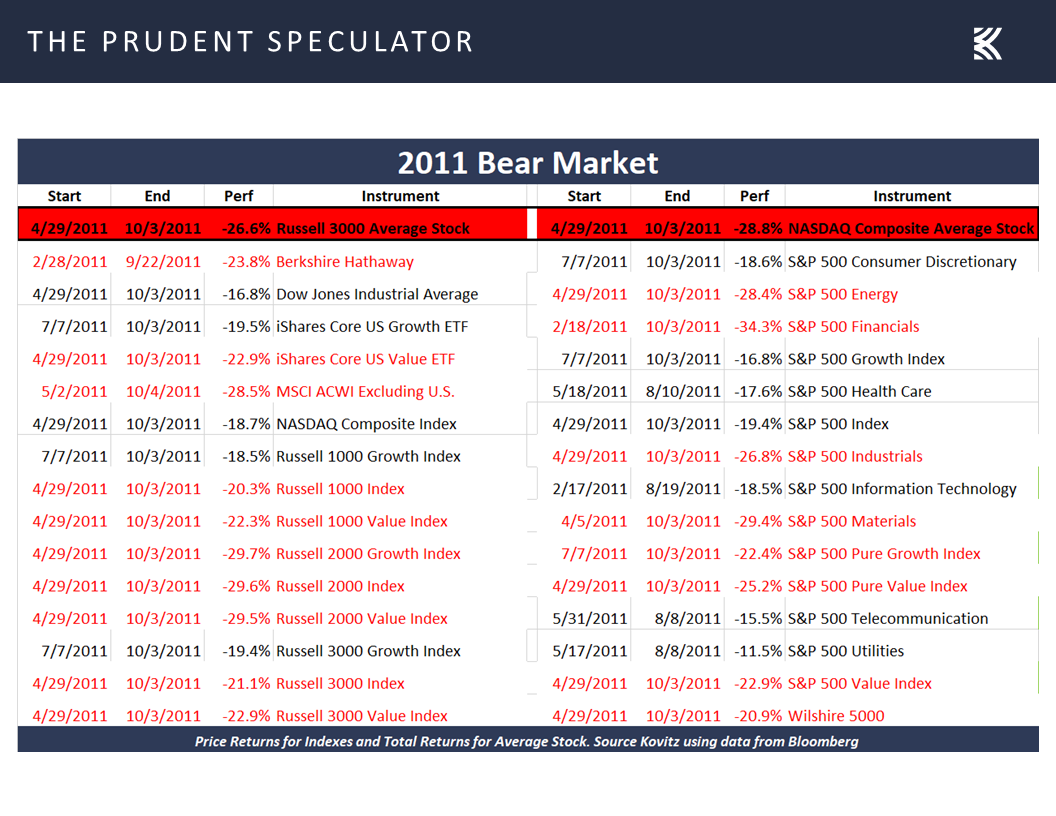

Sounds like typical posturing and we do expect some sort of compromise to be reached, especially with Treasury Secretary Janet Yellen continuing to warn of catastrophe were Uncle Sam to not make good on its obligations. Certainly, we must be braced for downside volatility and we realize that the debt ceiling crisis in 2011 led to a Bear Market for the average stock and many indexes.

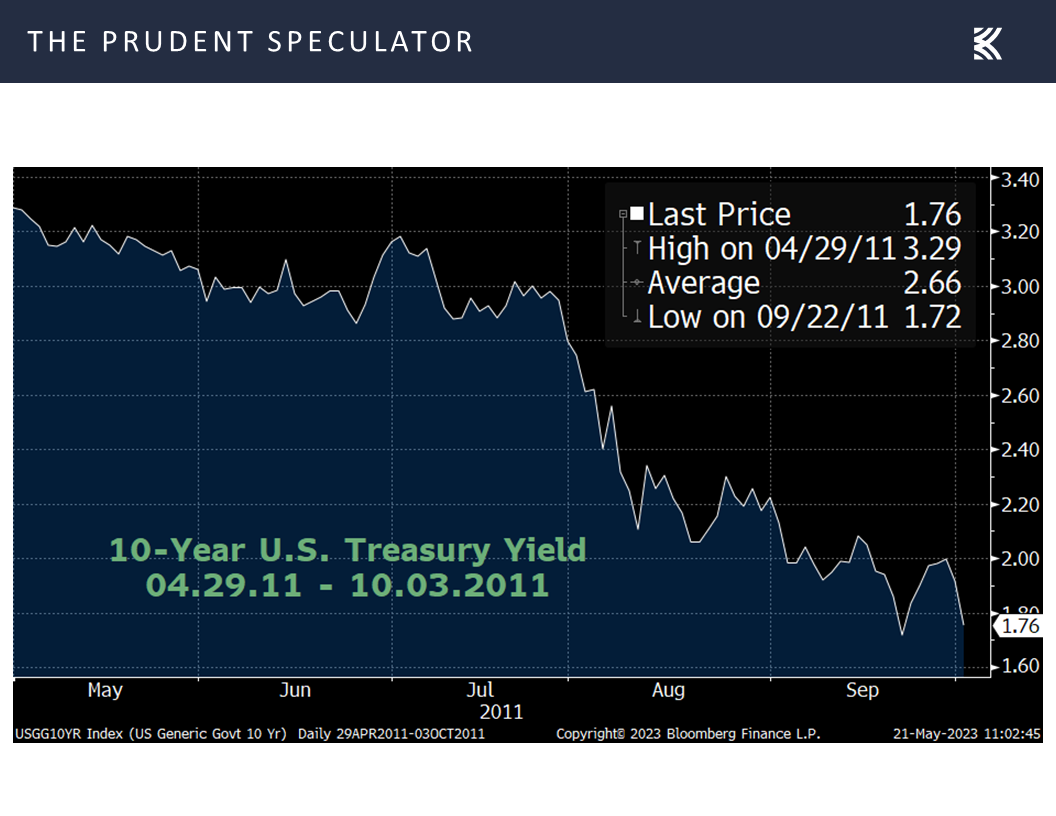

However, while we know there will be plenty of drama in the days and weeks to come, we note the Winston Churchill quip, “You can always count on the Americans to do the right thing after they have tried everything else.” We can debate what the “right thing” is regarding the country getting its financial house in order, but we find it fascinating that from April 2011 to October 2011, government bond prices soared, and yields plunged, precisely the opposite of what would happen if a corporation was facing a default on its debt.

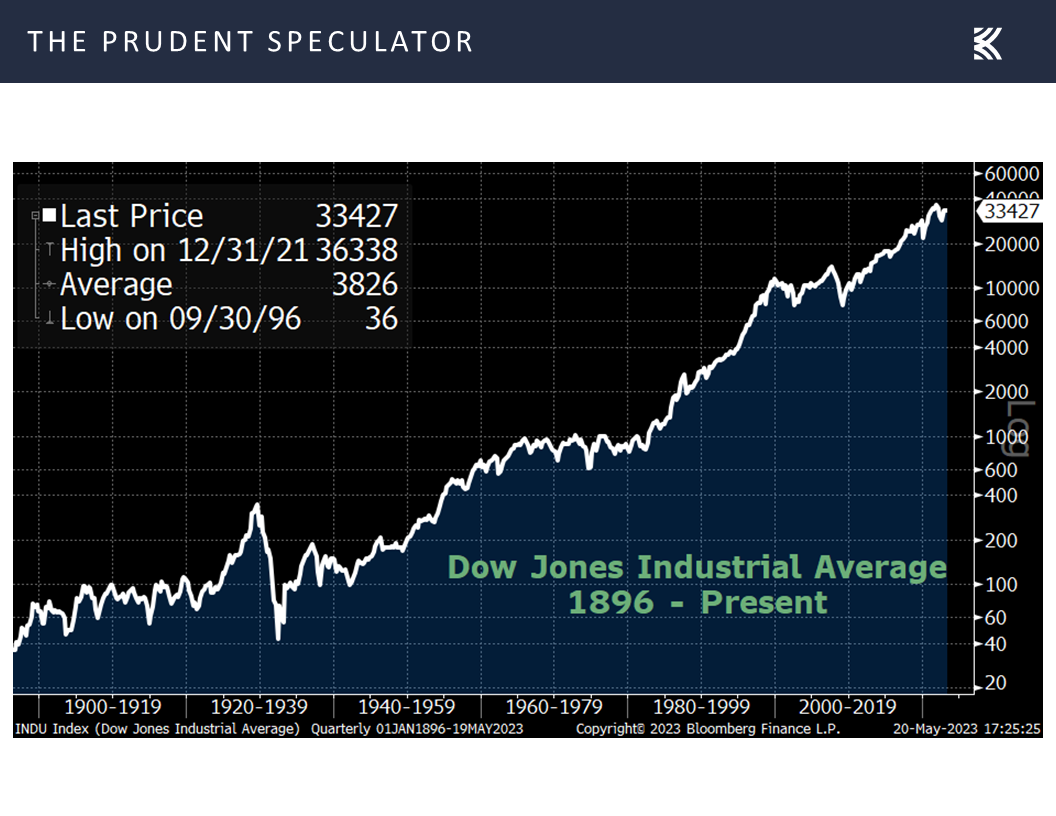

We also cannot forget that the Dow Jones Industrial Average was in the 11000 range at the height of the 2011 crisis, which shows as a minor downward blip on the logarithmic price chart of the popular benchmark dating back to its inception in 1896.

Contrarian Sentiment – Wall & Main Street Both Pessimistic

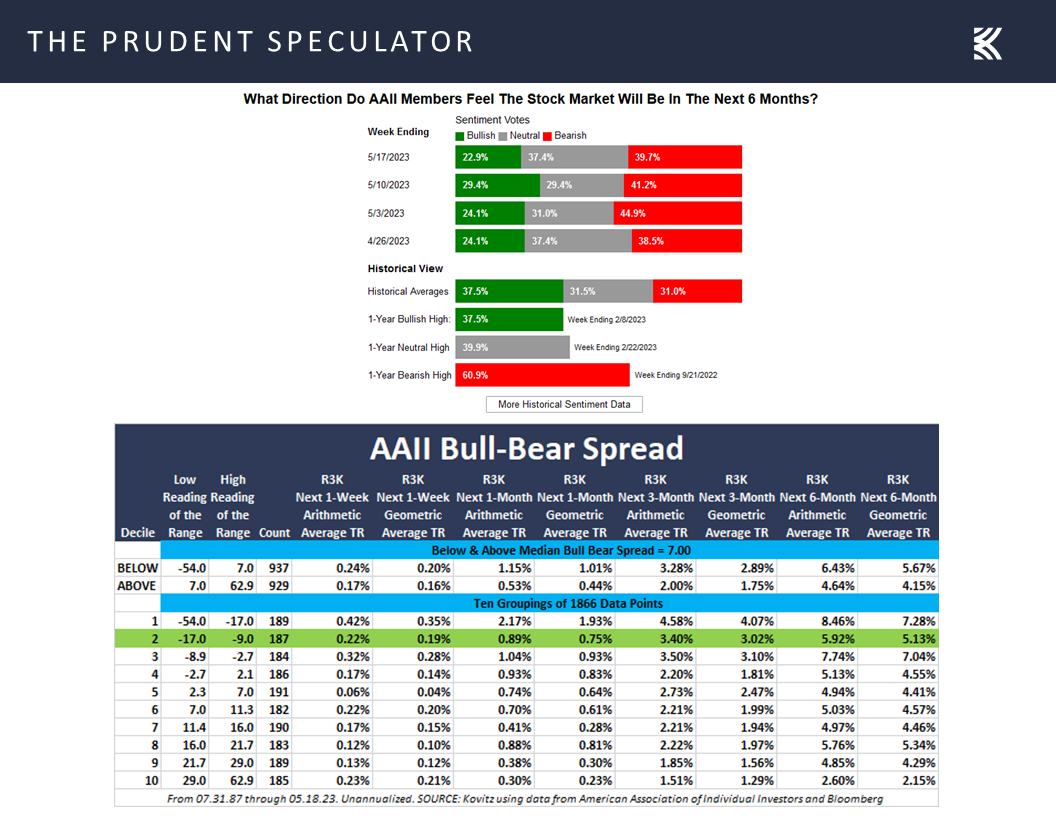

We might argue that the rebound last week was due in part to negative investor sentiment (a contrarian positive) as The Wall Street Journal wrote,…

Investors have a sour outlook on U.S. stocks. Contrarians say that is good news for the market.

Turmoil in the banking sector has dragged fund managers’ enthusiasm for stocks to a 2023 ebb, according to Bank of America’s most recent monthly survey. The stress adds to worries including lingering inflation, higher interest rates and a slowing economy that have driven them to cut their stockholdings to their lowest levels relative to bonds since 2009.

Institutions have pulled a net $333.9 billion from stocks over the past 12 months, according to S&P Global Market Intelligence data, while individual investors have yanked another $28 billion. Billions have flowed into cash equivalents, driving total assets in money markets to a record $5.3 trillion as of May 10, according to the Investment Company Institute.

To some, all that doom and gloom looks like a sign of hope. Many on Wall Street view extremes in sentiment one way or the other as the time to do the opposite. Warren Buffett famously advised investors to “be greedy when others are fearful.”

…with the pessimism on Wall Street in line with the prevailing mood of folks on Main Street…and the historical subsequent return figures for the American Association of Individual Investor’s Bull-Bear Spread gauge providing plenty of support for the Oracle of Omaha’s admonition in the previous paragraph.

Econ News – Mixed Data, But Q2 GDP Outlook Improves

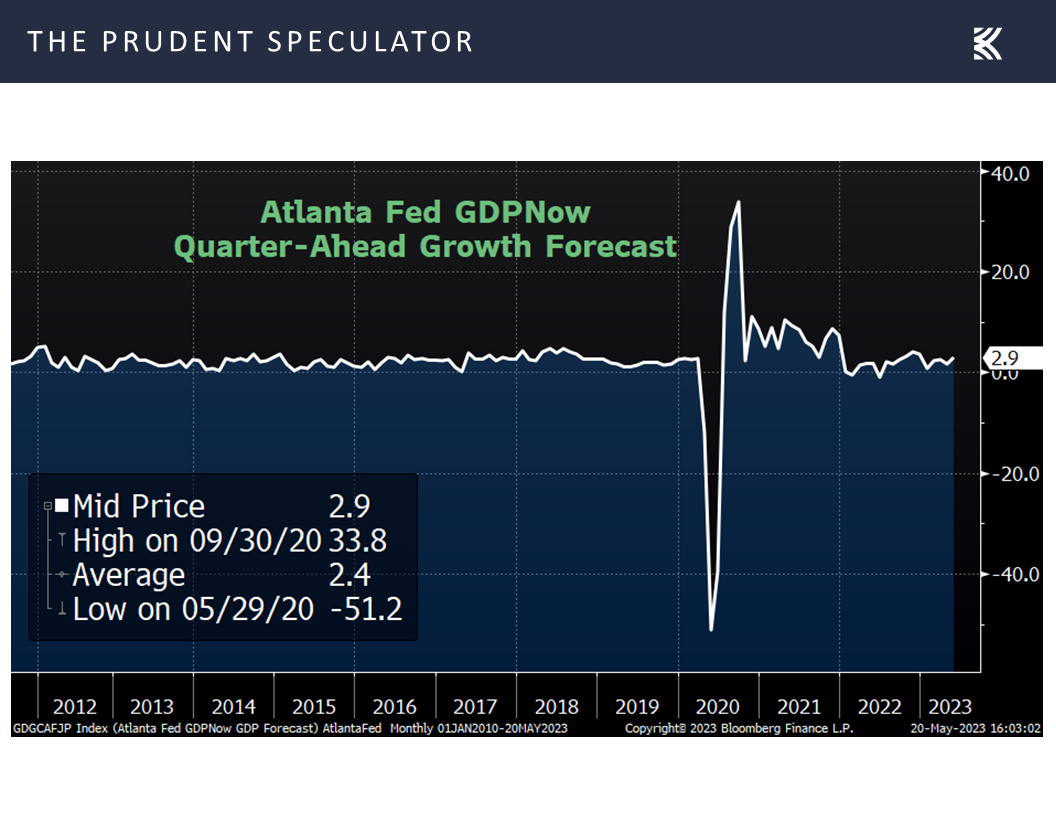

We might also attribute the bounce last week to decent news on the health of the economy, as the latest projection from the Atlanta Fed for Q2 real (inflation-adjusted) GDP growth (yes growth!) rose to 2.9%,

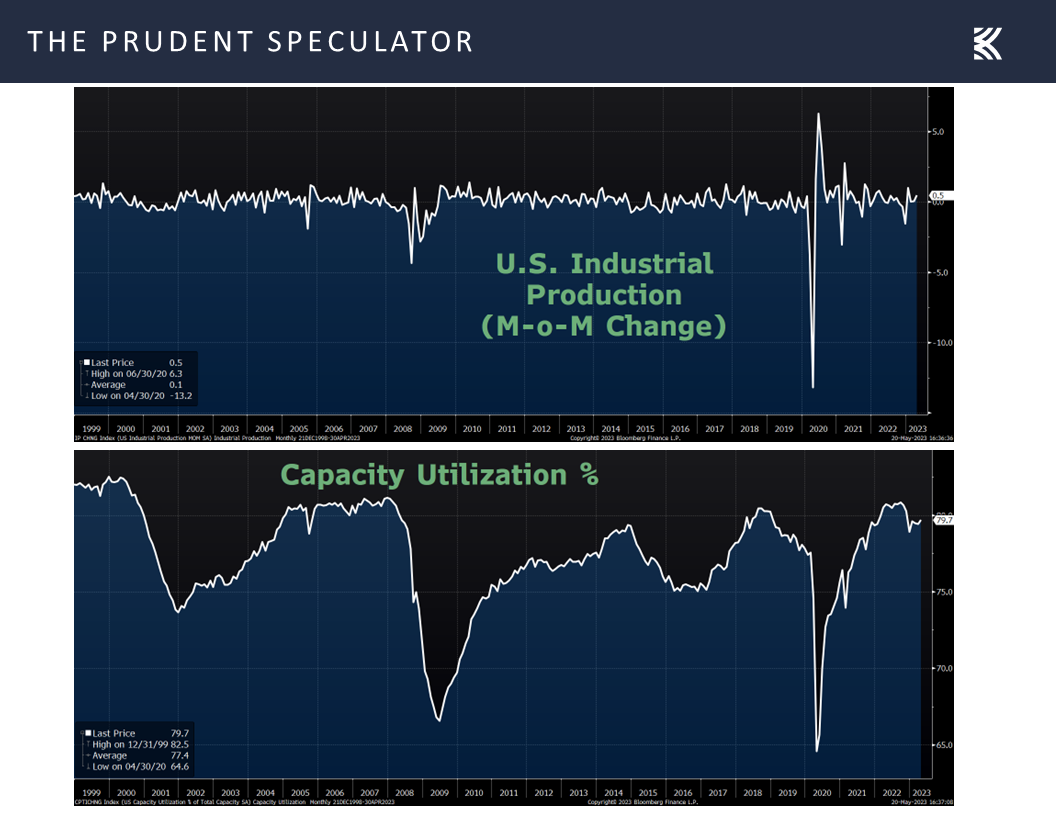

with manufacturing output rising by 0.5% in April, after two months of zero growth,

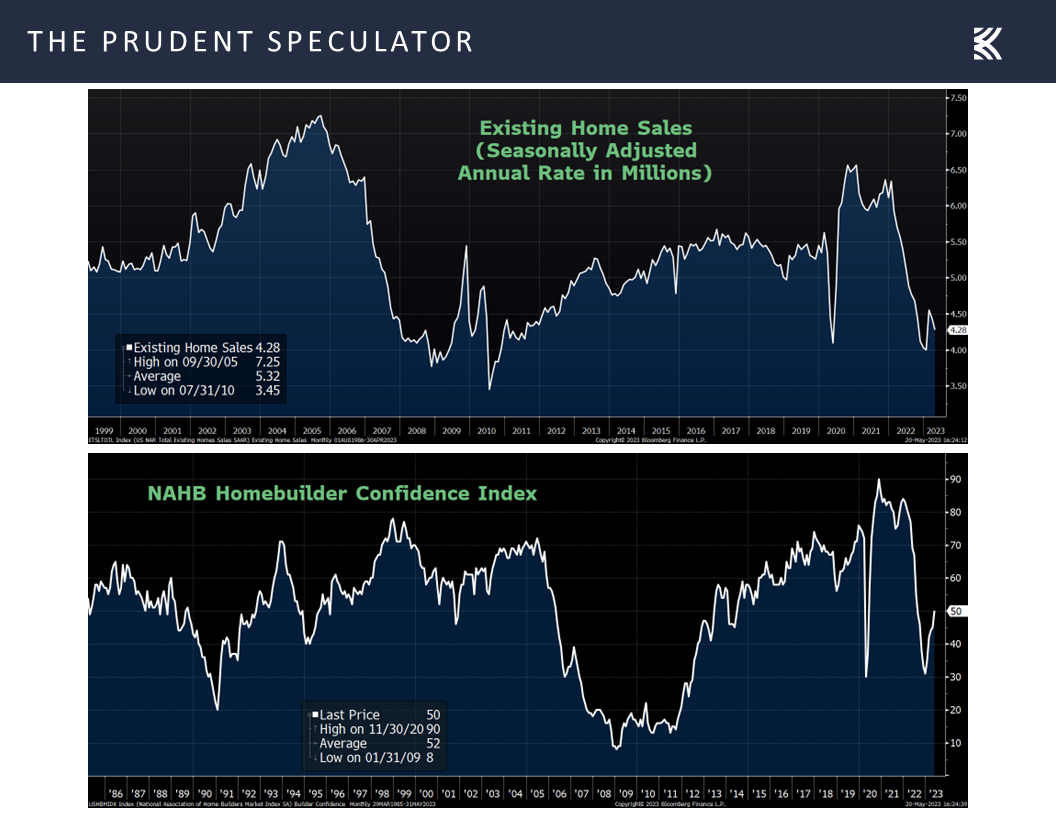

housing data (existing home sales and homebuilder confidence) coming in above pessimistic projections,

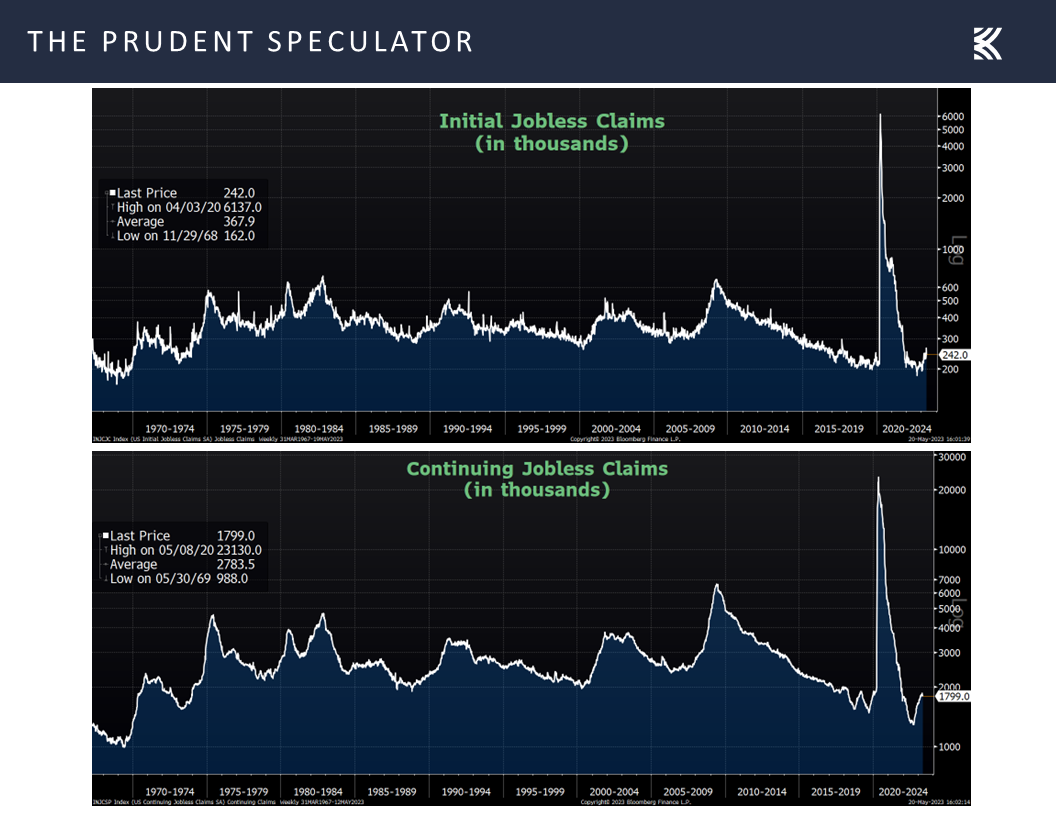

and the number of first-time filings for unemployment benefits dropping to 242,000 in the latest week, continuing to confirm the resiliency of the labor market.

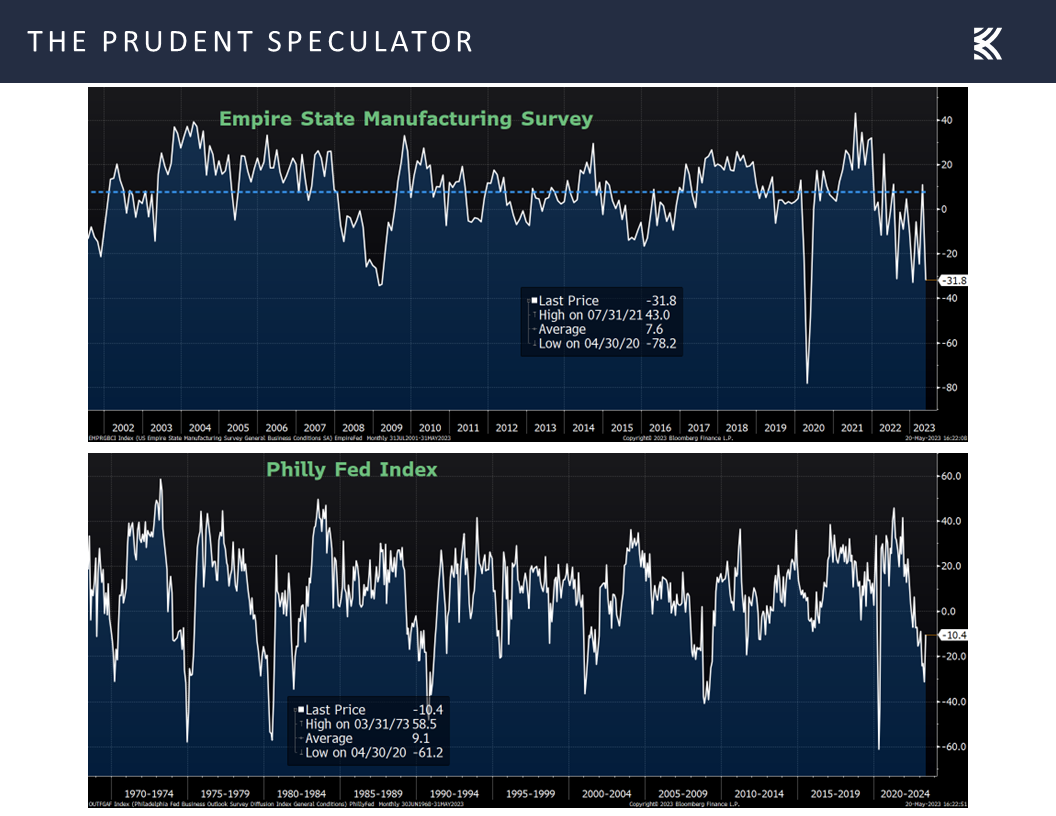

On the other hand, forward-looking figures (Empire & Philly Fed PMIs) on the state of the factory sector were still showing a likely contraction in manufacturing.

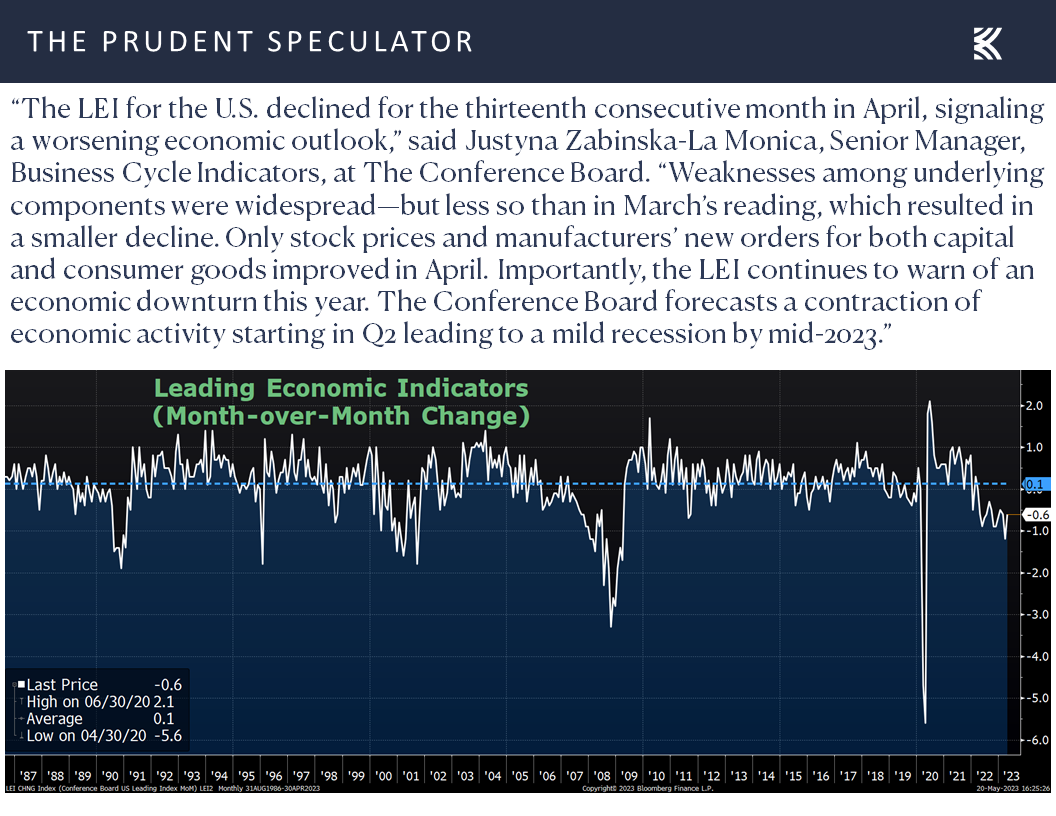

the important retail sales tally for April came in weaker than expected, though it did show an increase of 0.4%, reversing two months of declines, and the widely watched Leading Economic Index from the Conference Board for April retreated by 0.6%, which was an improvement from the 1.2% decline in March.

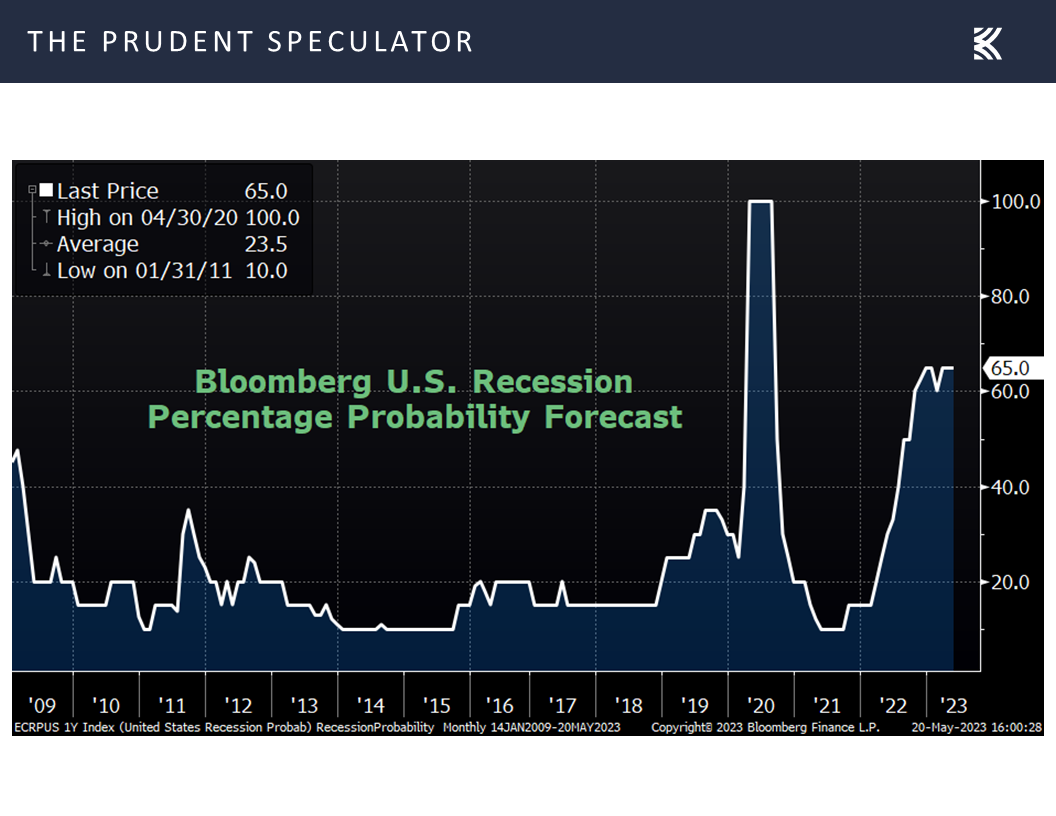

The week’s data did little to change the 65% chance of recession in the next 12 months as tabulated by Bloomberg,

Fed Speak – Interest Rates May Not Need to Be Raised Much Higher

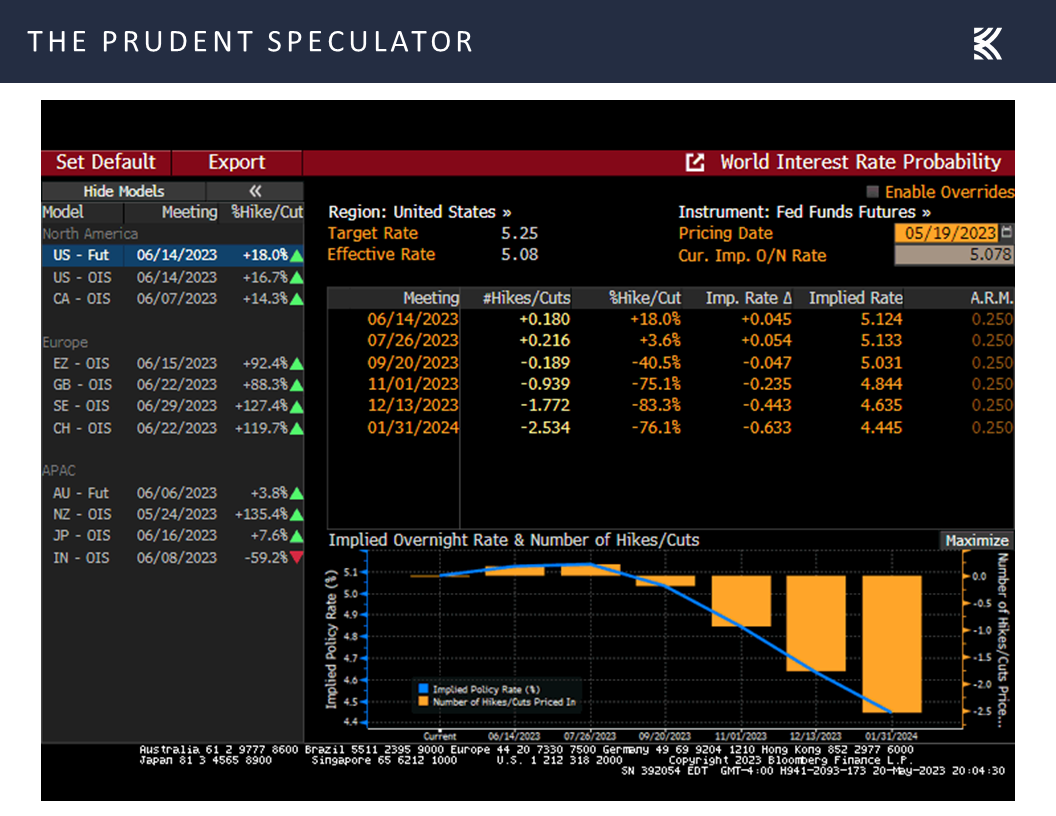

but they did reduce the likelihood that the Federal Reserve will move quickly to reduce interest rates as the Fed Funds futures are now suggesting a year-end target for that benchmark of 4.63%, up 25 basis points from the 4.38% rate projected a week ago.

On the third hand, Federal Reserve Chair Jerome H. Powell said on Friday that the level of interest rates is now high enough to be restrictive, stating, “Tighter credit conditions are likely to slow economic growth, hiring and inflation” He concluded, “So, as a result, our policy rate may not need to rise as much as it would have otherwise to achieve our goals.”

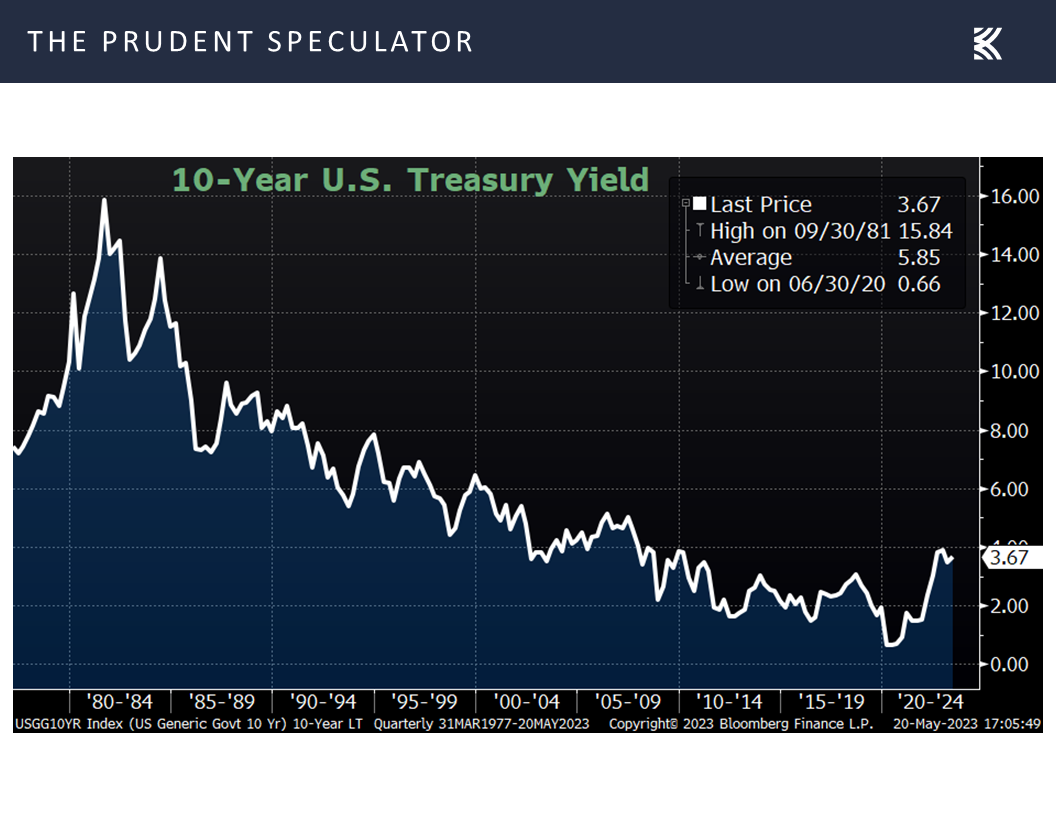

With New York Federal Reserve President John Williams also commenting on Friday, “There is no evidence that the era of very low natural rates of interest has ended,” we might conclude that interest rates are not far from their near- and intermediate-term peak levels. Of course, it should be noted that long-term Treasury yields, despite the run up the last couple of years, remain well below the historical norm,

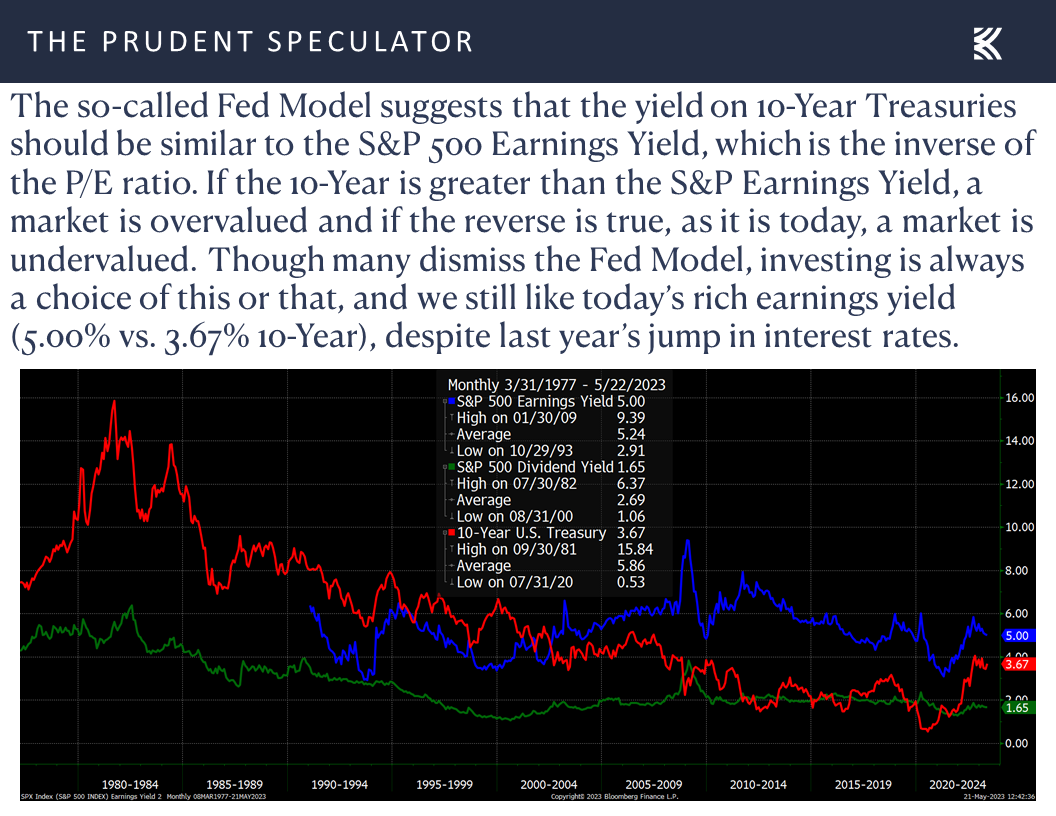

which we believe supports the case for equities on a relative-valuation earnings-yield basis,

Corporate Profits – EPS Growth Still the Forecast

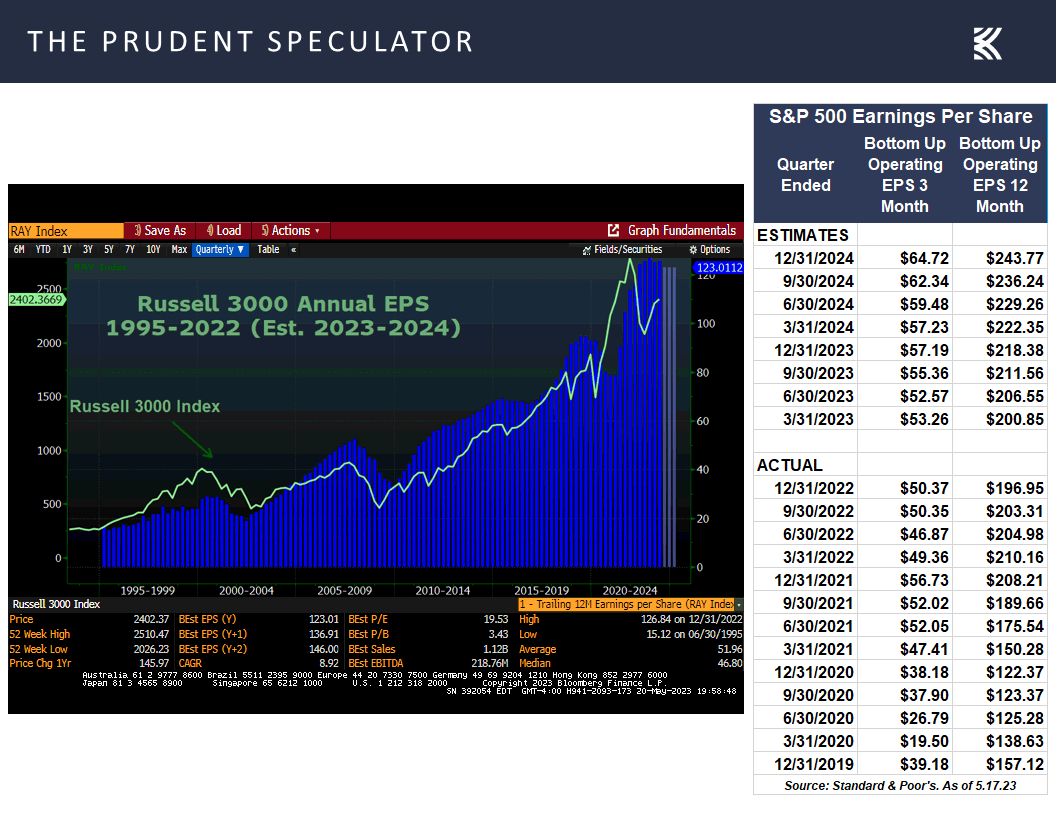

especially as corporate profits are still expected to show solid growth this year and in 2024,

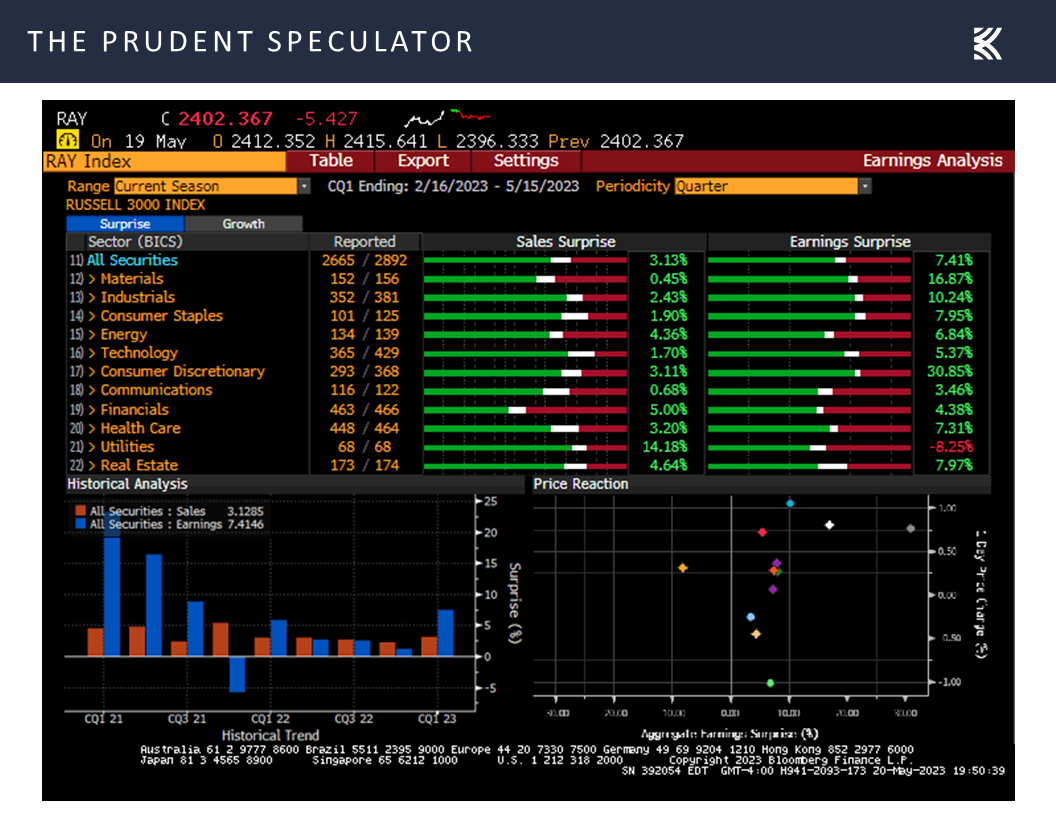

and first quarter report cards for Corporate America generally were favorable, with 63.0% of companies in the Russell 3000 index beating bottom-line expectations and 62.5% exceeding top-line forecasts, both better rates than in the quarter prior.

Valuations – Stocks Reasonably Priced; Liking the Metrics for our Portfolios

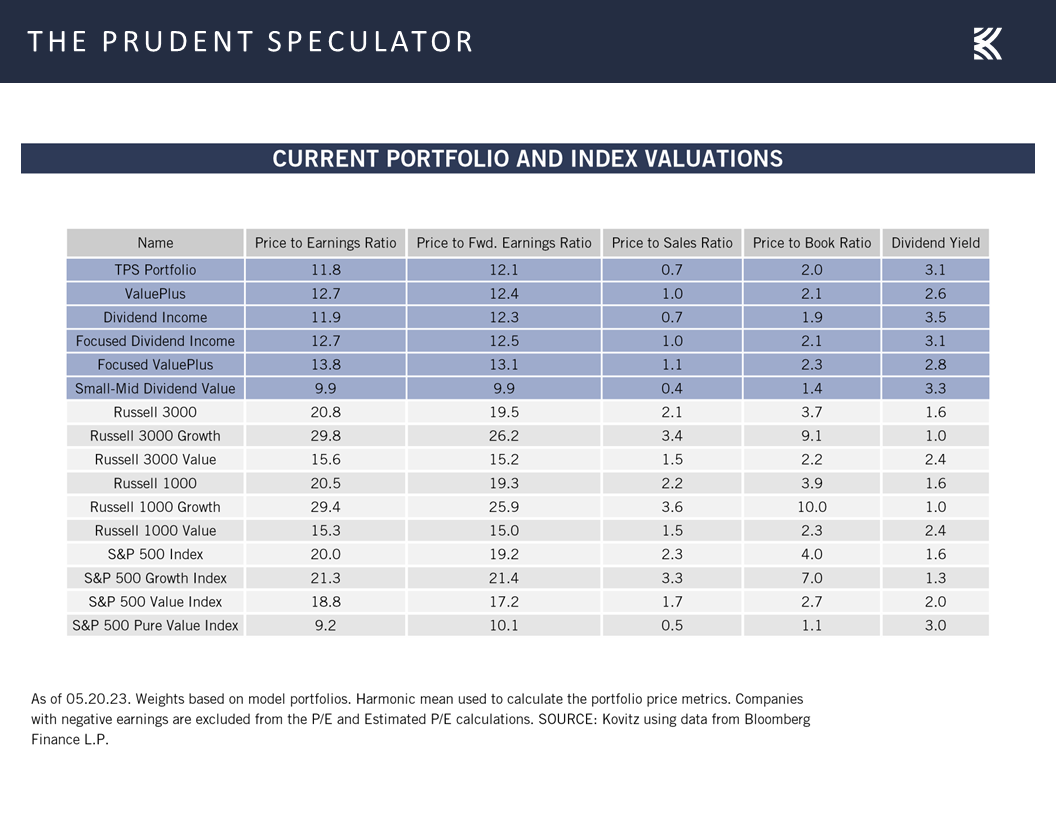

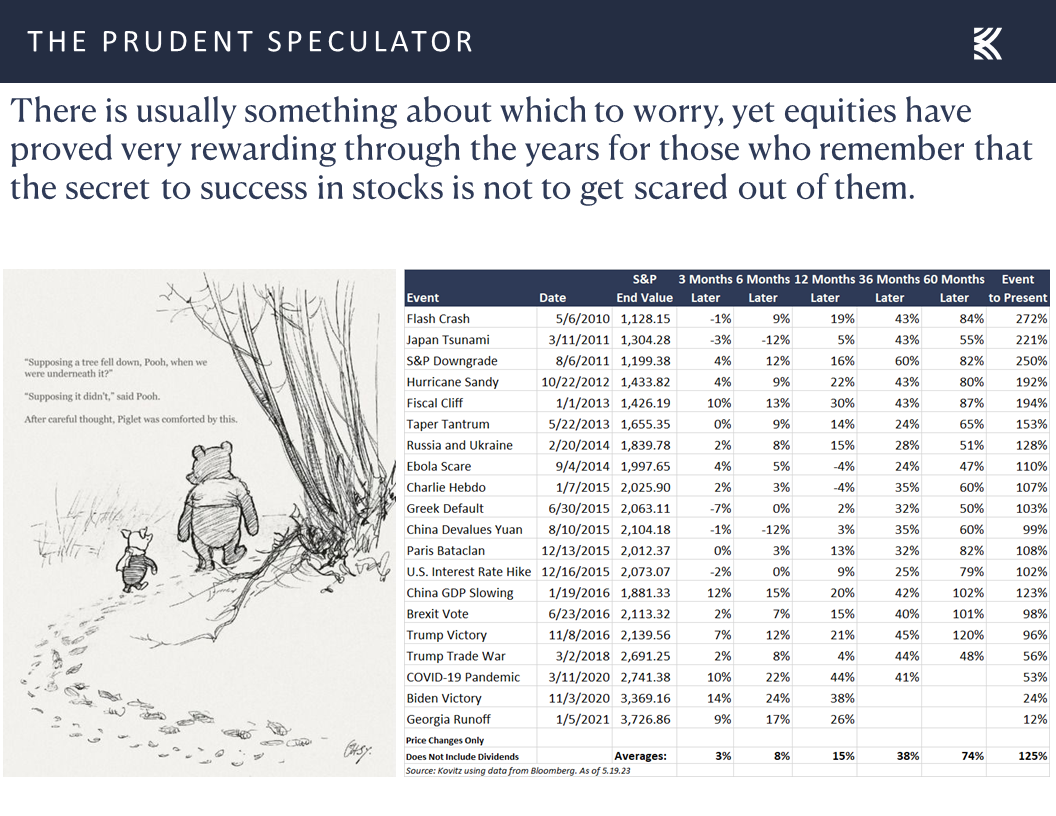

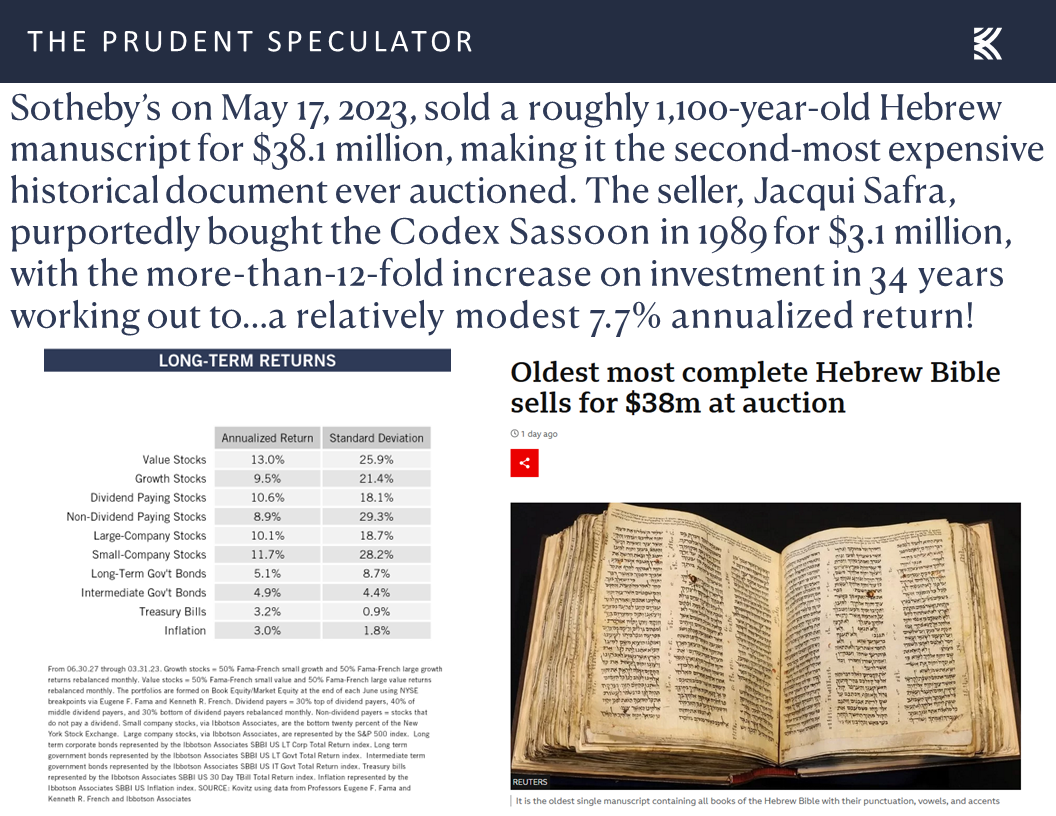

As has been the case during prior disconcerting periods (there really is always something to worry about), we simply remain focused on the inexpensive valuation metrics associated with the companies we own,

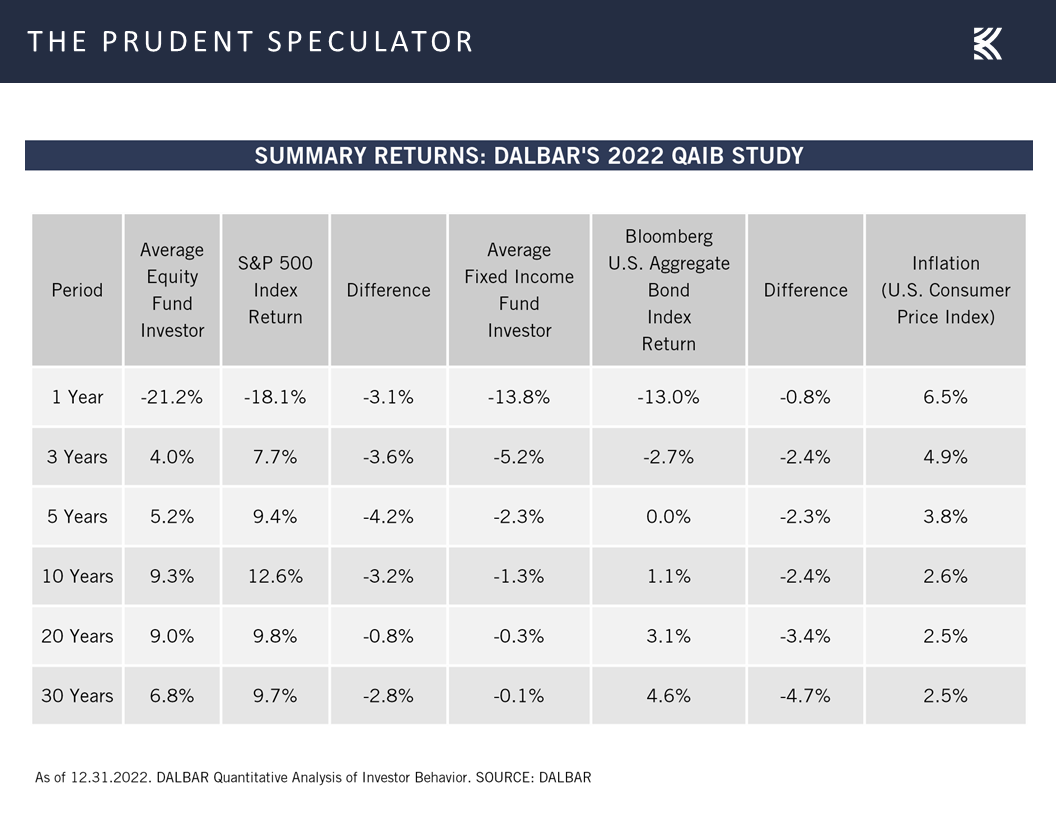

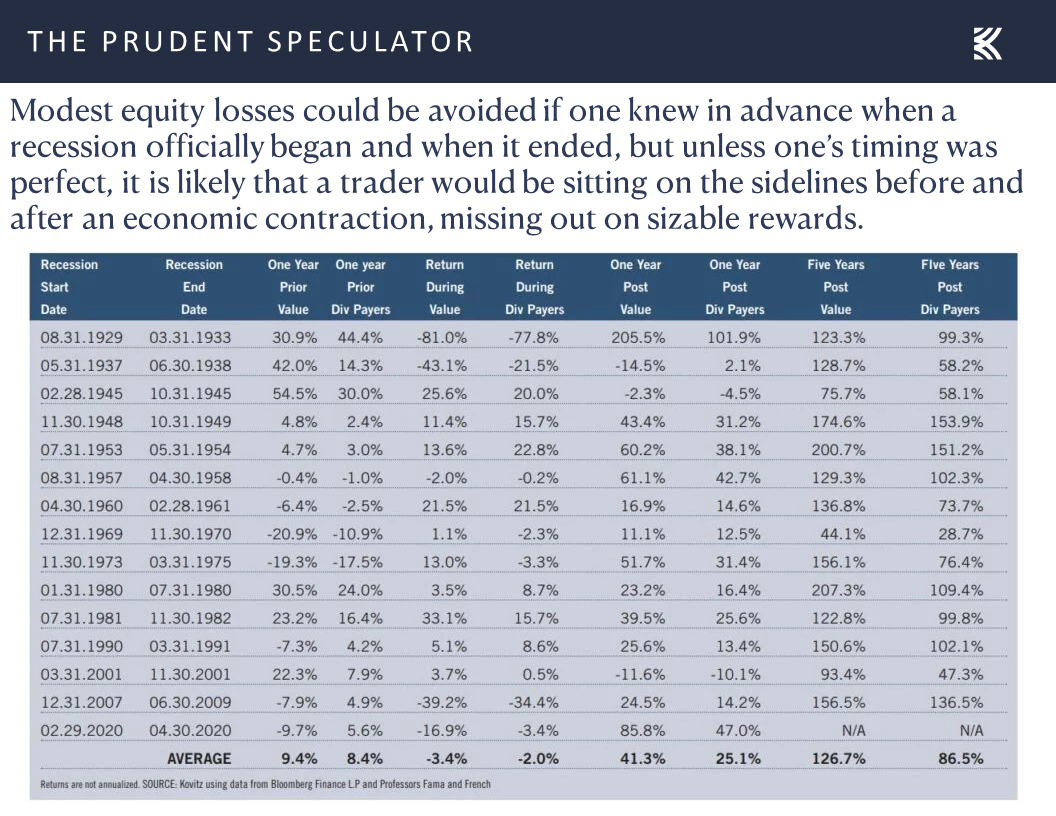

as we understand that market timing generally has proven hazardous to one’s wealth. Indeed, data over the last three decades from DALBAR show the massive returns gap between what investors in stock and bond funds have received and how the funds themselves have performed, illustrating that the only problem with market timing is getting the timing right.

Keeping the Faith – Don’t Interrupt Compounding Unnecessarily

Recent history is filled with scary events, but stocks have persevered through thick and thin,

while even recessions over the long term (if somehow their beginnings and ends were known in advance) would not be cause, on average, for investors with multi-year time horizons to abandon equities.

Obviously, anything can happen as we move forward, but as Warren Buffett’s sidekick Charlie Munger states, “The first rule of compounding: Never interrupt it unnecessarily.”

Stock Market News: Updates on nine stocks across six different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Federal Reserve, Debt Ceiling, Corporate Profits and Valuations

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Federal Reserve, Debt Ceiling, Corporate Profits, Valuations and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Five Days in Review – First Up Week of May

Debt Ceiling – Historical Perspective

Contrarian Sentiment – Wall & Main Street Both Pessimistic

Econ News – Mixed Data, But Q2 GDP Outlook Improves

Fed Speak – Interest Rates May Not Need to Be Raised Much Higher

Valuations – Stocks Reasonably Priced; Liking the Metrics for our Portfolios

Corporate Profits – EPS Growth Still the Forecast

Keeping the Faith – Don’t Interrupt Compounding Unnecessarily

Stock News – Updates on nine stocks across six different sectors

Five Days in Review – First Up Week of May

The equity market roller-coaster ride seemingly gyrated more wildly than usual over the last five days, though the Dow Jones Industrial Average ended with a modest gain for the period,

completing the first positive week in the seasonally less favorable (though still positive) time of the year.

Debt Ceiling – Historical Perspective

The primary catalyst for the move higher in the middle of the week was optimism about that the country would not default on its obligations via the raising of the debt ceiling. As the Treasury’s website states, “Since 1960, Congress has acted 78 separate times to permanently raise, temporarily extend, or revise the definition of the debt limit – 49 times under Republican presidents and 29 times under Democratic presidents. Congressional leaders in both parties have recognized that this is necessary.”

Of course, stocks proceeded to tumble on Friday when House Speaker Kevin McCarthy said it was time to “press pause” on the talks until President Biden returned from the G-7 Summit in Japan. The rhetoric over the weekend was not exactly encouraging as Mr. Biden said, “Republicans need to move from their extreme position,” while Mr. McCarthy claimed, “The White House has moved backwards.”

However, on Sunday afternoon, the duo spoke telephonically on the President’s flight back from Japan, with the House leader suggesting the phone calls were “productive” and that there would be an in-person meeting on Monday.

Sounds like typical posturing and we do expect some sort of compromise to be reached, especially with Treasury Secretary Janet Yellen continuing to warn of catastrophe were Uncle Sam to not make good on its obligations. Certainly, we must be braced for downside volatility and we realize that the debt ceiling crisis in 2011 led to a Bear Market for the average stock and many indexes.

However, while we know there will be plenty of drama in the days and weeks to come, we note the Winston Churchill quip, “You can always count on the Americans to do the right thing after they have tried everything else.” We can debate what the “right thing” is regarding the country getting its financial house in order, but we find it fascinating that from April 2011 to October 2011, government bond prices soared, and yields plunged, precisely the opposite of what would happen if a corporation was facing a default on its debt.

We also cannot forget that the Dow Jones Industrial Average was in the 11000 range at the height of the 2011 crisis, which shows as a minor downward blip on the logarithmic price chart of the popular benchmark dating back to its inception in 1896.

Contrarian Sentiment – Wall & Main Street Both Pessimistic

We might argue that the rebound last week was due in part to negative investor sentiment (a contrarian positive) as The Wall Street Journal wrote,…

Investors have a sour outlook on U.S. stocks. Contrarians say that is good news for the market.

Turmoil in the banking sector has dragged fund managers’ enthusiasm for stocks to a 2023 ebb, according to Bank of America’s most recent monthly survey. The stress adds to worries including lingering inflation, higher interest rates and a slowing economy that have driven them to cut their stockholdings to their lowest levels relative to bonds since 2009.

Institutions have pulled a net $333.9 billion from stocks over the past 12 months, according to S&P Global Market Intelligence data, while individual investors have yanked another $28 billion. Billions have flowed into cash equivalents, driving total assets in money markets to a record $5.3 trillion as of May 10, according to the Investment Company Institute.

To some, all that doom and gloom looks like a sign of hope. Many on Wall Street view extremes in sentiment one way or the other as the time to do the opposite. Warren Buffett famously advised investors to “be greedy when others are fearful.”

…with the pessimism on Wall Street in line with the prevailing mood of folks on Main Street…and the historical subsequent return figures for the American Association of Individual Investor’s Bull-Bear Spread gauge providing plenty of support for the Oracle of Omaha’s admonition in the previous paragraph.

Econ News – Mixed Data, But Q2 GDP Outlook Improves

We might also attribute the bounce last week to decent news on the health of the economy, as the latest projection from the Atlanta Fed for Q2 real (inflation-adjusted) GDP growth (yes growth!) rose to 2.9%,

with manufacturing output rising by 0.5% in April, after two months of zero growth,

housing data (existing home sales and homebuilder confidence) coming in above pessimistic projections,

and the number of first-time filings for unemployment benefits dropping to 242,000 in the latest week, continuing to confirm the resiliency of the labor market.

On the other hand, forward-looking figures (Empire & Philly Fed PMIs) on the state of the factory sector were still showing a likely contraction in manufacturing.

the important retail sales tally for April came in weaker than expected, though it did show an increase of 0.4%, reversing two months of declines, and the widely watched Leading Economic Index from the Conference Board for April retreated by 0.6%, which was an improvement from the 1.2% decline in March.

The week’s data did little to change the 65% chance of recession in the next 12 months as tabulated by Bloomberg,

Fed Speak – Interest Rates May Not Need to Be Raised Much Higher

but they did reduce the likelihood that the Federal Reserve will move quickly to reduce interest rates as the Fed Funds futures are now suggesting a year-end target for that benchmark of 4.63%, up 25 basis points from the 4.38% rate projected a week ago.

On the third hand, Federal Reserve Chair Jerome H. Powell said on Friday that the level of interest rates is now high enough to be restrictive, stating, “Tighter credit conditions are likely to slow economic growth, hiring and inflation” He concluded, “So, as a result, our policy rate may not need to rise as much as it would have otherwise to achieve our goals.”

With New York Federal Reserve President John Williams also commenting on Friday, “There is no evidence that the era of very low natural rates of interest has ended,” we might conclude that interest rates are not far from their near- and intermediate-term peak levels. Of course, it should be noted that long-term Treasury yields, despite the run up the last couple of years, remain well below the historical norm,

which we believe supports the case for equities on a relative-valuation earnings-yield basis,

Corporate Profits – EPS Growth Still the Forecast

especially as corporate profits are still expected to show solid growth this year and in 2024,

and first quarter report cards for Corporate America generally were favorable, with 63.0% of companies in the Russell 3000 index beating bottom-line expectations and 62.5% exceeding top-line forecasts, both better rates than in the quarter prior.

Valuations – Stocks Reasonably Priced; Liking the Metrics for our Portfolios

As has been the case during prior disconcerting periods (there really is always something to worry about), we simply remain focused on the inexpensive valuation metrics associated with the companies we own,

as we understand that market timing generally has proven hazardous to one’s wealth. Indeed, data over the last three decades from DALBAR show the massive returns gap between what investors in stock and bond funds have received and how the funds themselves have performed, illustrating that the only problem with market timing is getting the timing right.

Keeping the Faith – Don’t Interrupt Compounding Unnecessarily

Recent history is filled with scary events, but stocks have persevered through thick and thin,

while even recessions over the long term (if somehow their beginnings and ends were known in advance) would not be cause, on average, for investors with multi-year time horizons to abandon equities.

Obviously, anything can happen as we move forward, but as Warren Buffett’s sidekick Charlie Munger states, “The first rule of compounding: Never interrupt it unnecessarily.”

Stock Market News: Updates on nine stocks across six different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.