The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Federal Reserve, Economic Statistics, Interest Rates and Stocks. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Fed Meeting – 50-Basis-Point Rate Cut

Econ Stats – Mostly Better-than-Expected Numbers

GDP Outlook – Decent Growth the Prognosis, Supporting Solid EPS Growth

Rates & Stocks – Equities Have Performed Well, on Average, Whether Fed Funds or 10-Year Yield is Rising/Falling

Emotional Roller Coaster – Media Still Not Exactly Helpful

Historical Evidence – Stocks Have Overcome All Sorts of Headwinds

Sentiment – AAII Bullishness Jumps

Valuations – Liking our Metrics

Stock News – Updates on six stocks across four different sectors

Fed Meeting – 50-Basis-Point Rate Cut

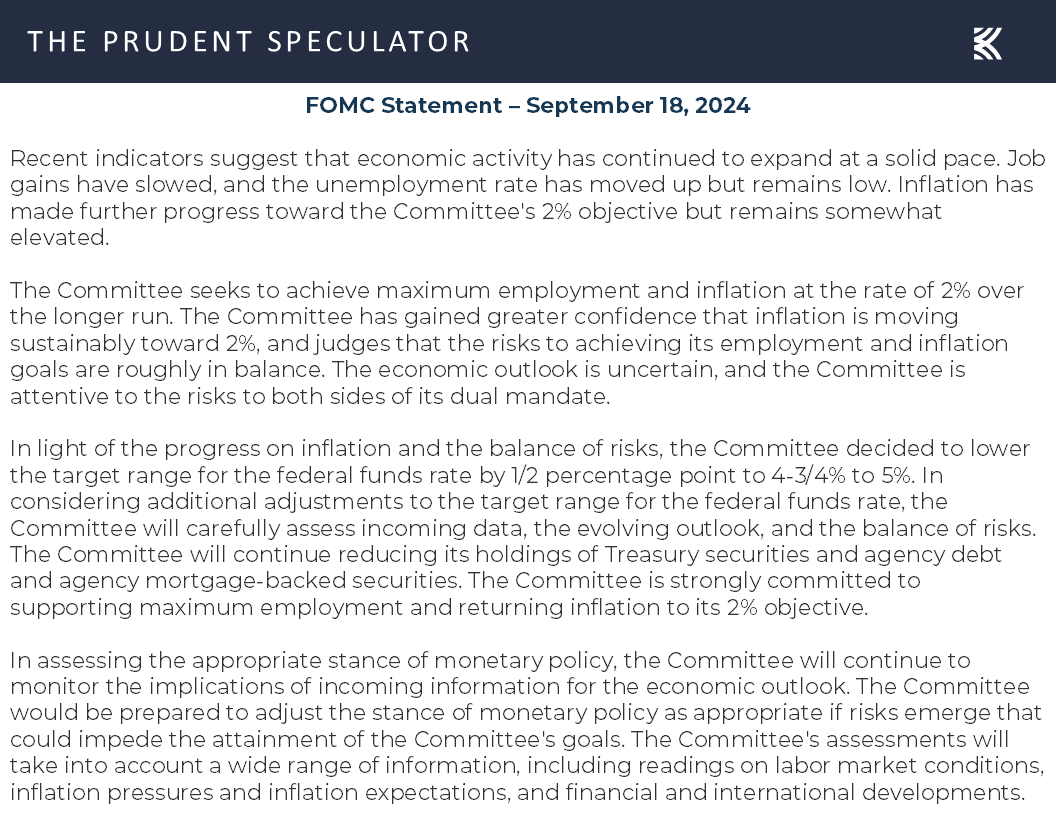

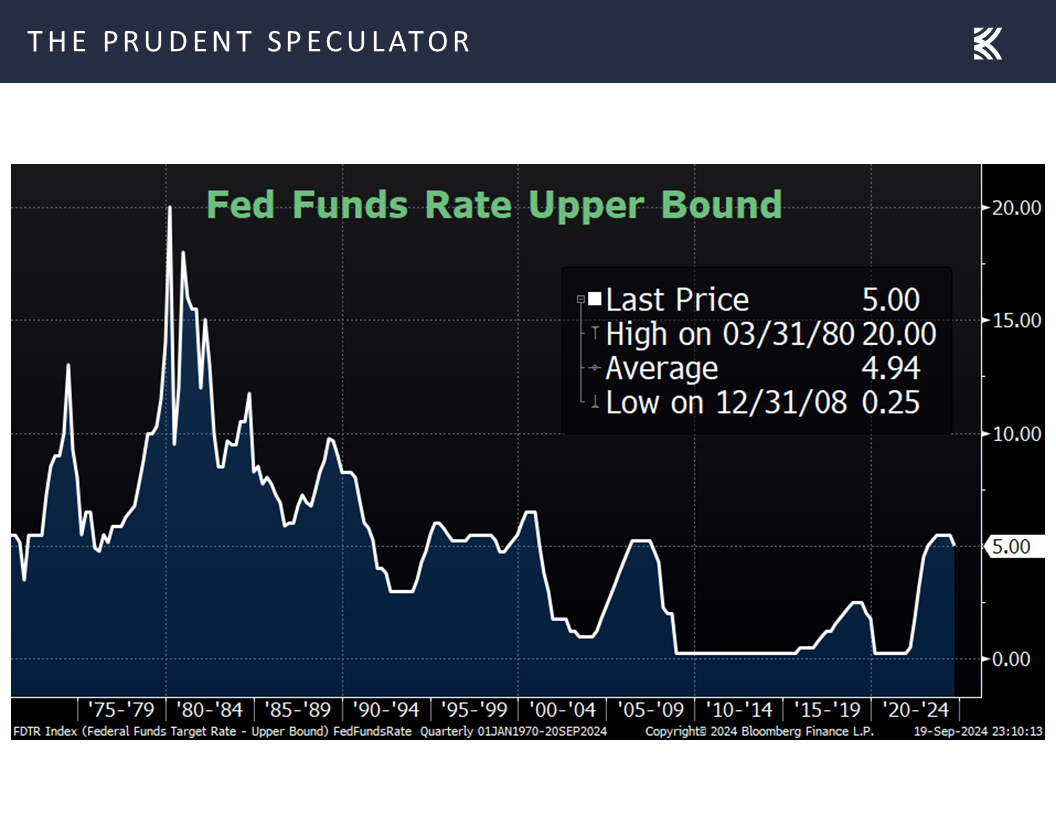

With the FOMC Statement declaring, “In light of the progress on inflation and the balance of risks, the Committee decided to lower the target range for the federal funds rate by ½ percentage point to 4-3/4% to 5%,”

Econ Stats – Mostly Better-than-Expected Numbers

the Federal Reserve last week initiated the first cut in interest rates by the U.S. central bank since the Pandemic.

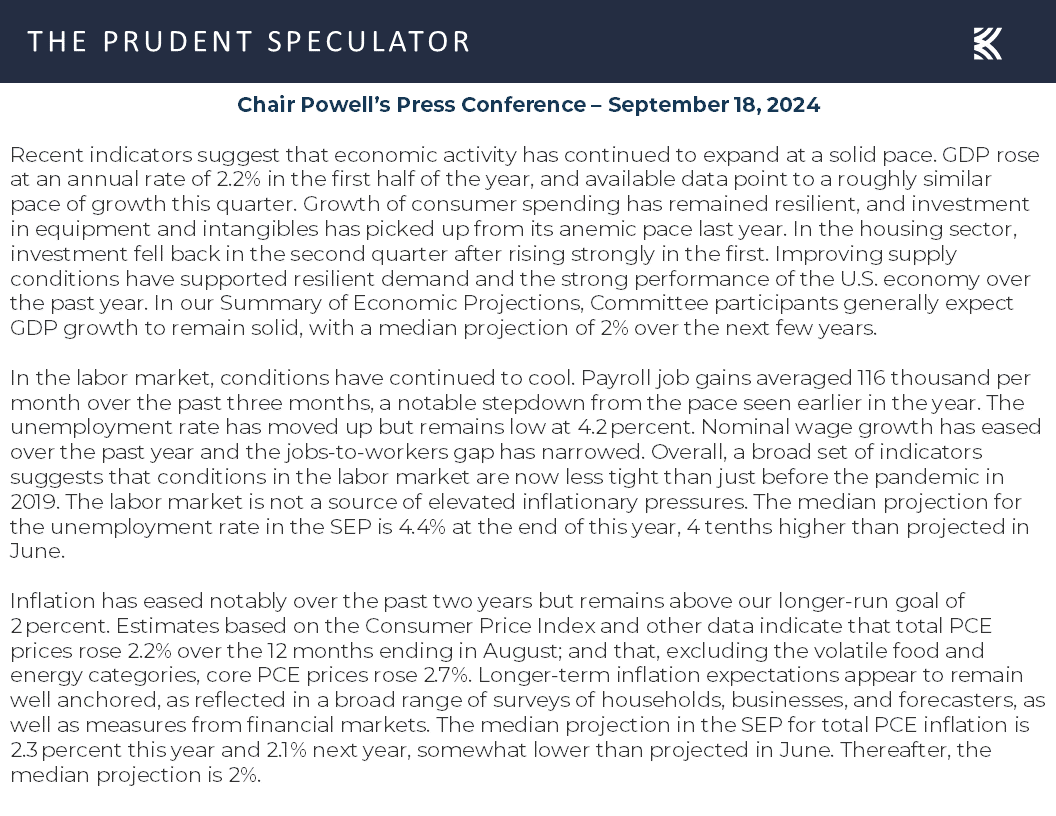

The equity markets cheered the news with the major stock market averages hitting all-time highs as Fed Chair Jerome H. Powell sounded upbeat in his prepared remarks at the Press Conference that followed the decision on rates,

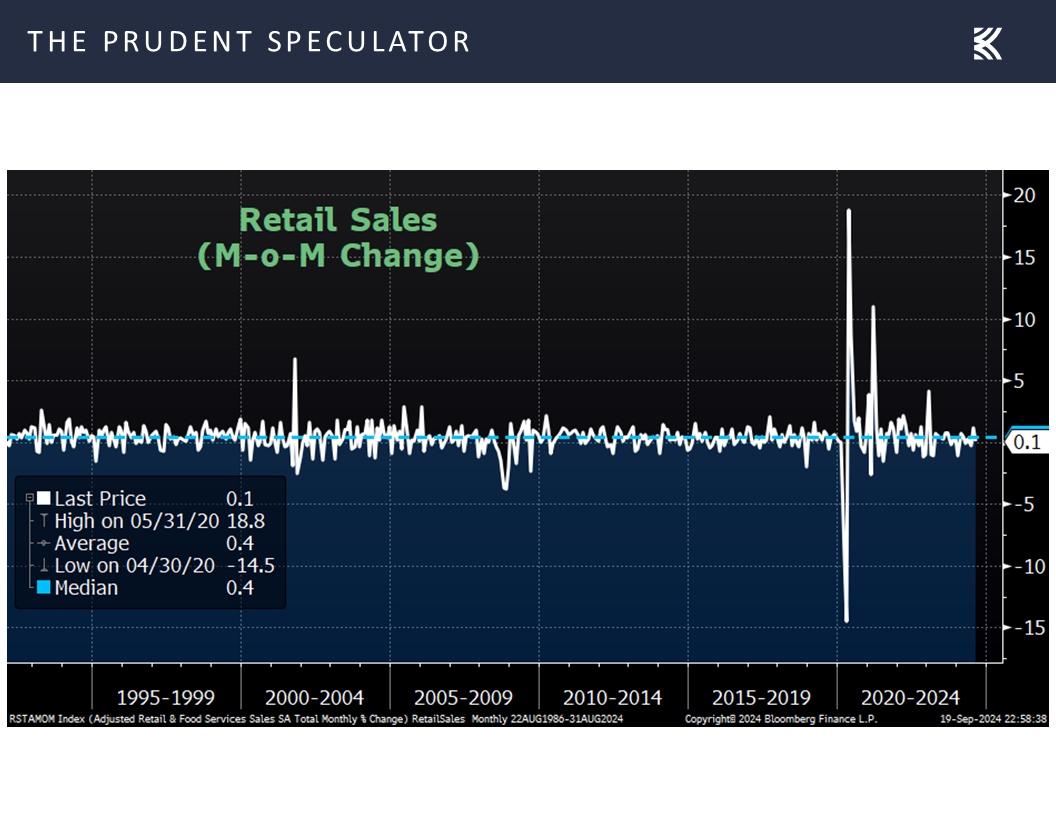

and economic data out last week generally came in better than expected, starting with the report of retail sales rising in August by 0.1%, versus the 0.2% decline that was projected,

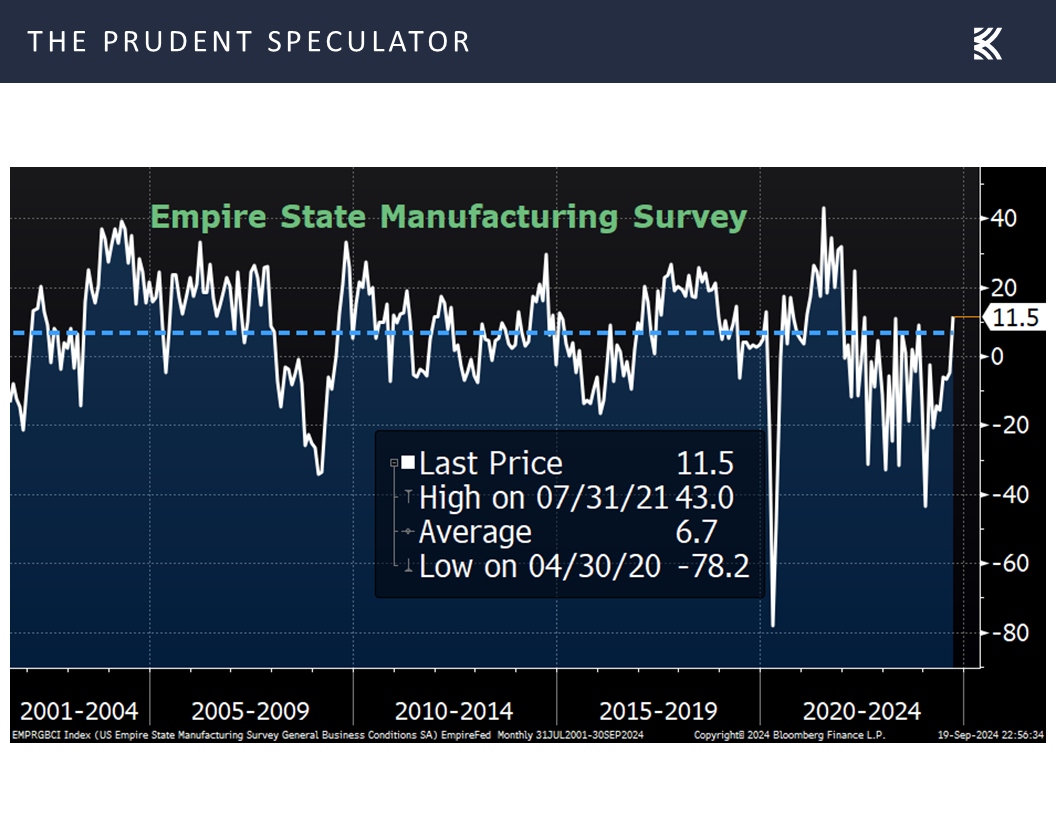

and the Empire State Manufacturing gauge of factory activity in the New York area jumping to a reading of 11.5 this month, well above estimates of -4.0 and the August figure of -4.7.

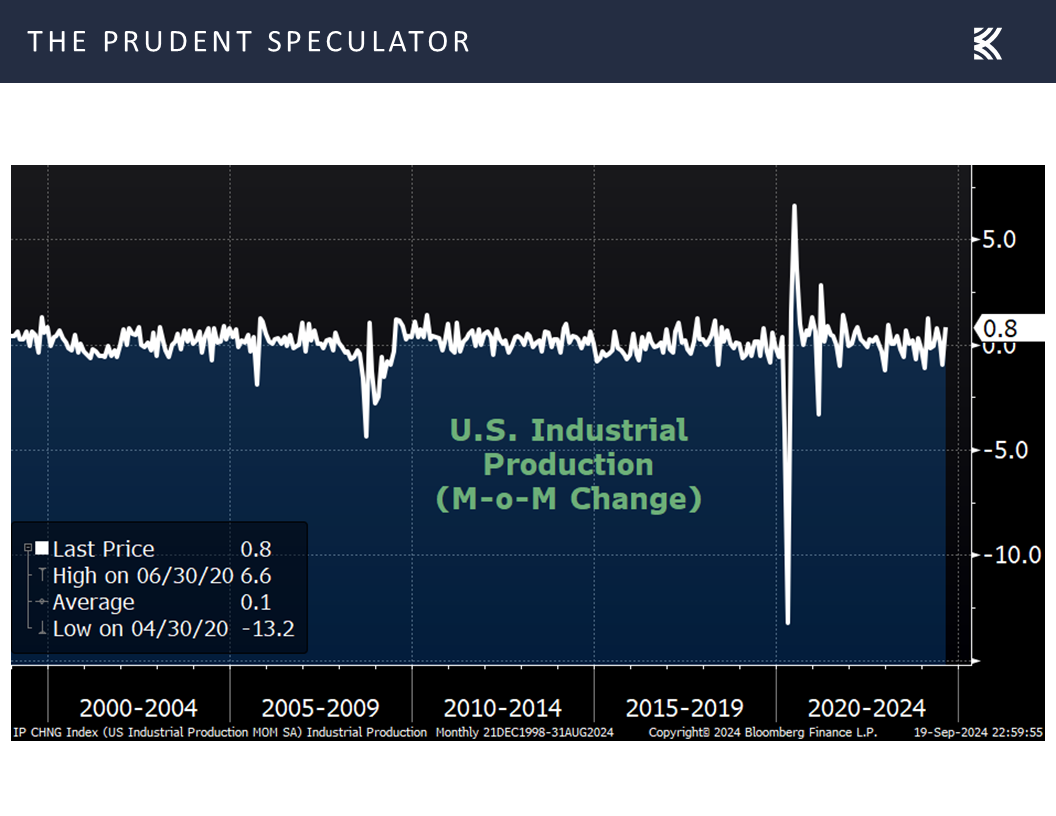

We also learned that industrial production climbed to a month-over-month improvement of 0.8% in August, compared to the estimate of a 0.2% increase and July’s revised decline of 0.9%,

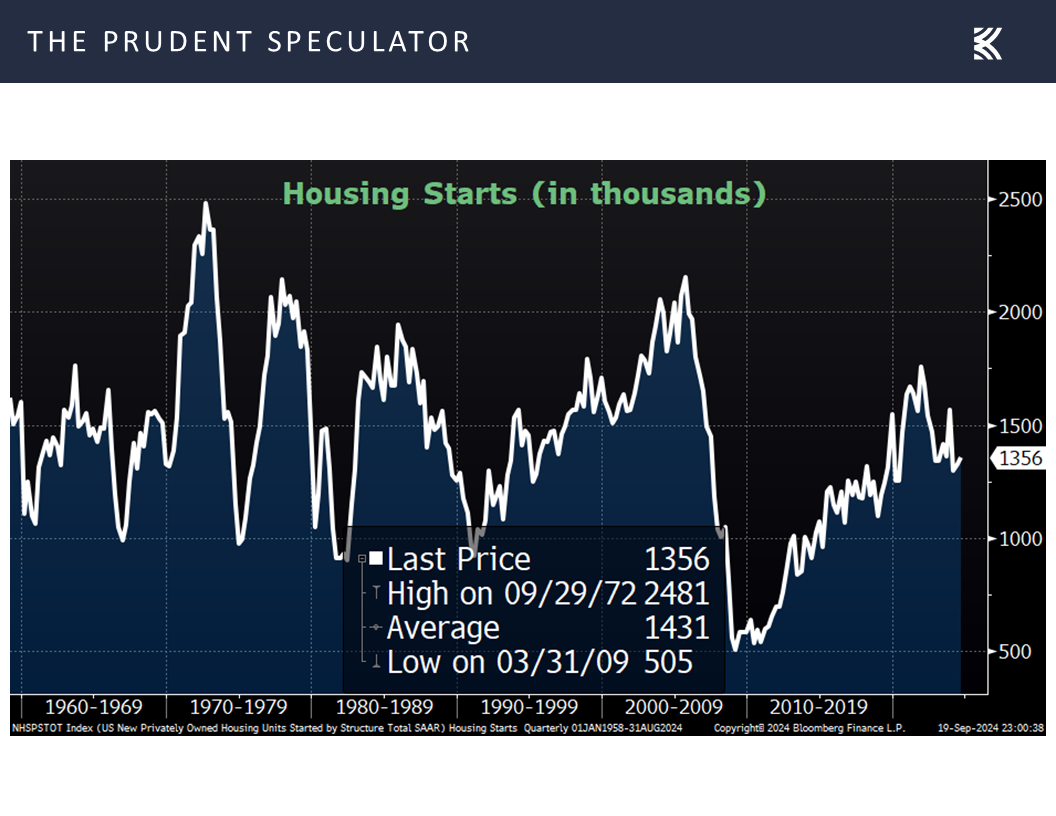

housing starts topped forecasts, coming in at 1.356 million last month, versus projections of 1.318 million and the revised tally the month prior of 1.237 million,

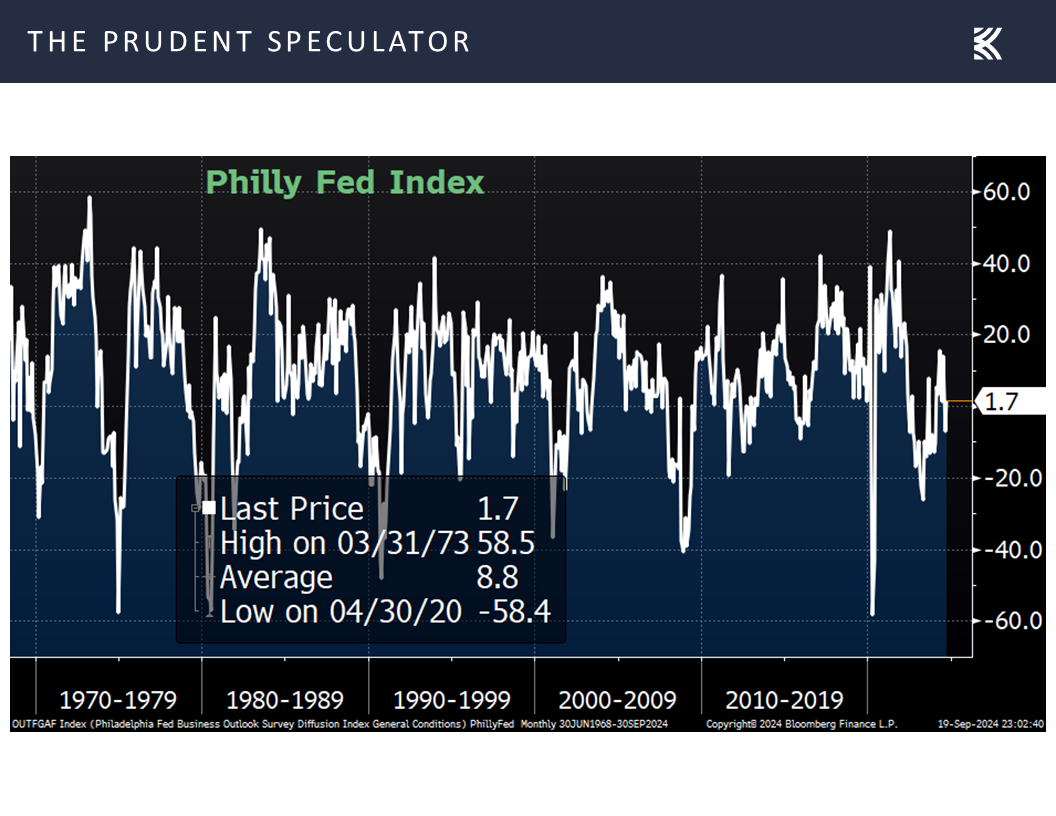

and the Philadelphia Fed Manufacturing index rebounded to 1.7 in September from -7.0 in August.

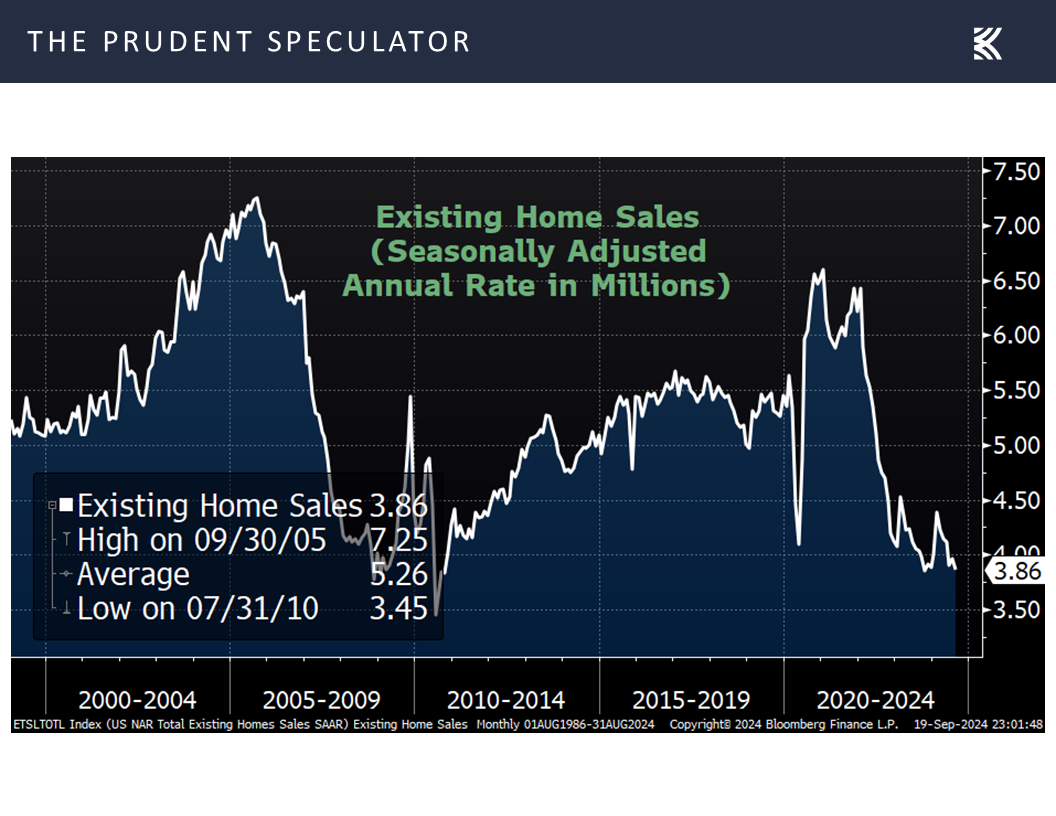

True, existing home sales for August of 3.86 million trailed expectations of 3.90 million,

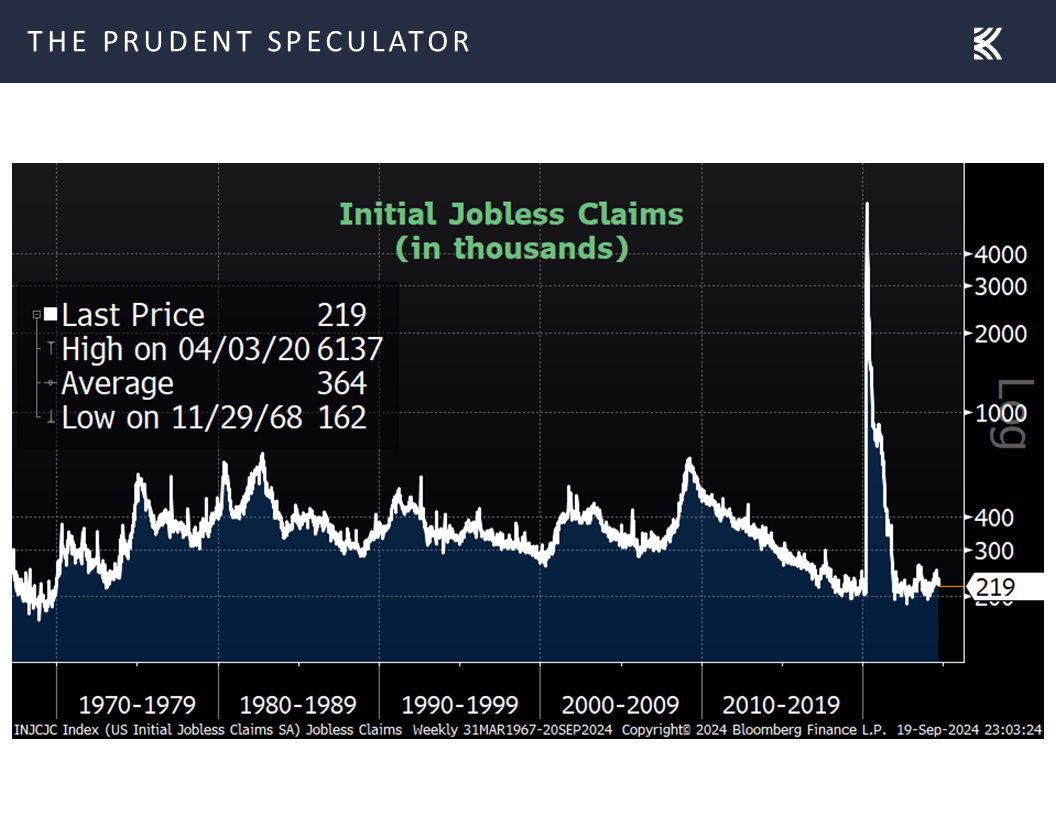

but first-time filings for jobless benefits of 219,000 in the most recent week were down from a revised 231,000 the week prior and projections of 230,000,

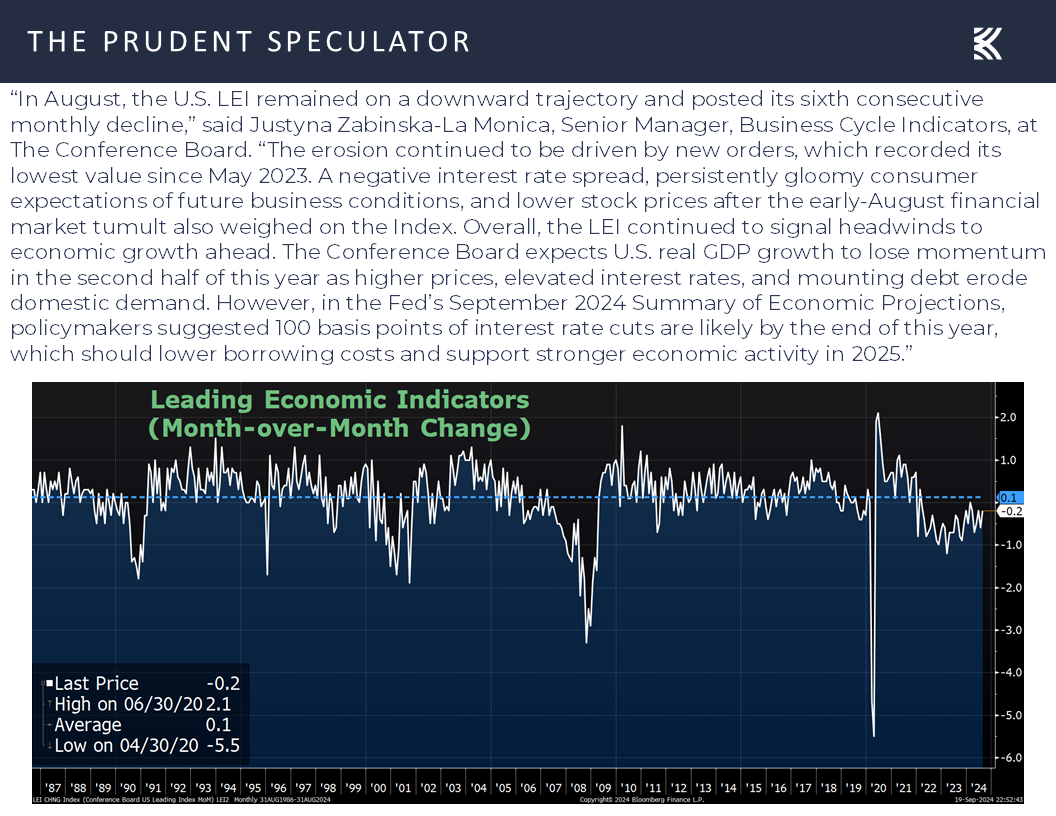

while the -0.2 reading for the Leading Economic Indicators (LEI) for August was better than the -0.3 consensus estimate,

while the -0.2 reading for the Leading Economic Indicators (LEI) for August was better than the -0.3 consensus estimate,

GDP Outlook – Decent Growth the Prognosis, Supporting Solid EPS Growth

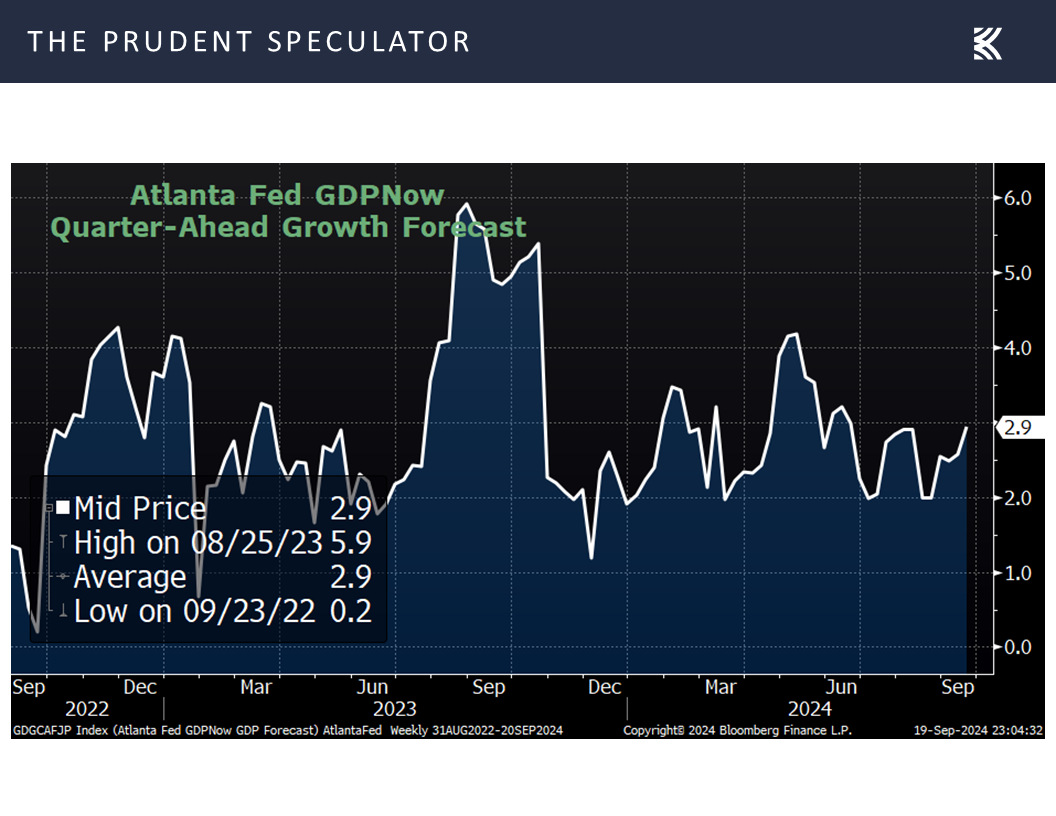

and the latest forecast for real (inflation-adjusted) U.S. GDP growth for Q3 from the Atlanta Fed stood at a solid 2.9%.

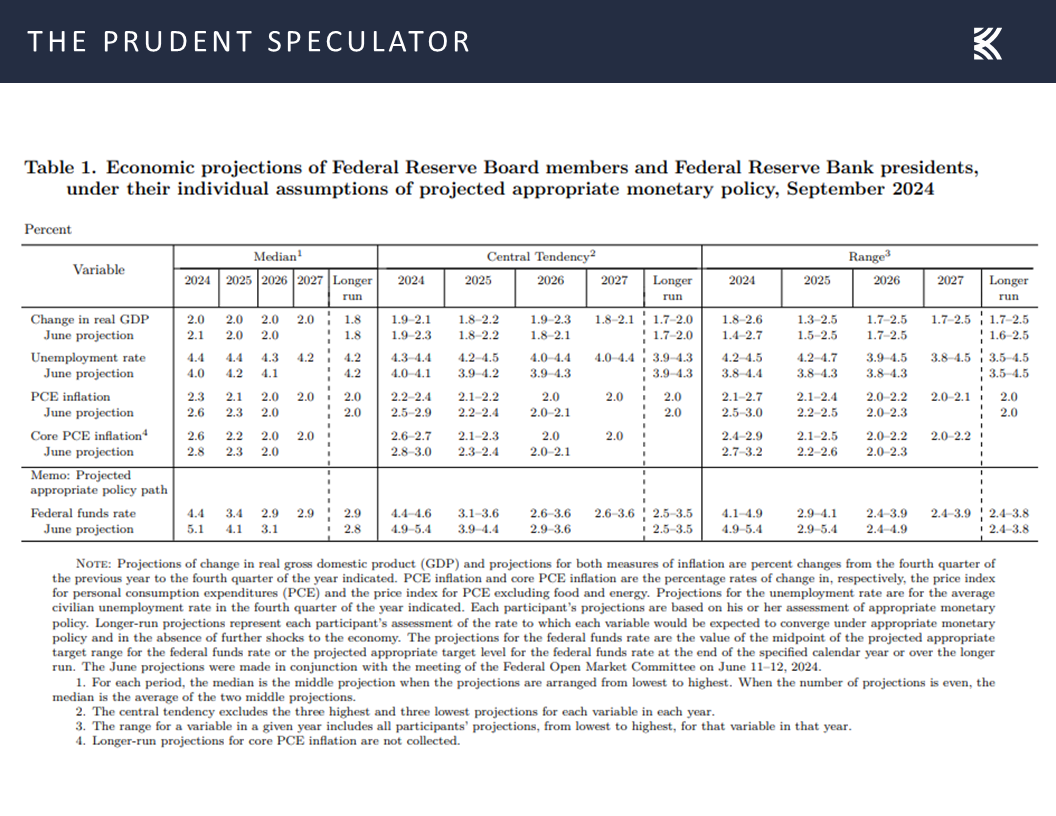

The keeper of the LEI, the Conference Board, suggested that while the economy will face headwinds over the balance of 2024, stronger economic activity is likely next year thanks to last week’s cut in the Fed Funds rate AND the expectation for additional reductions shown in the economic projections released by Federal Reserve Board members and Federal Reserve Bank presidents last week.

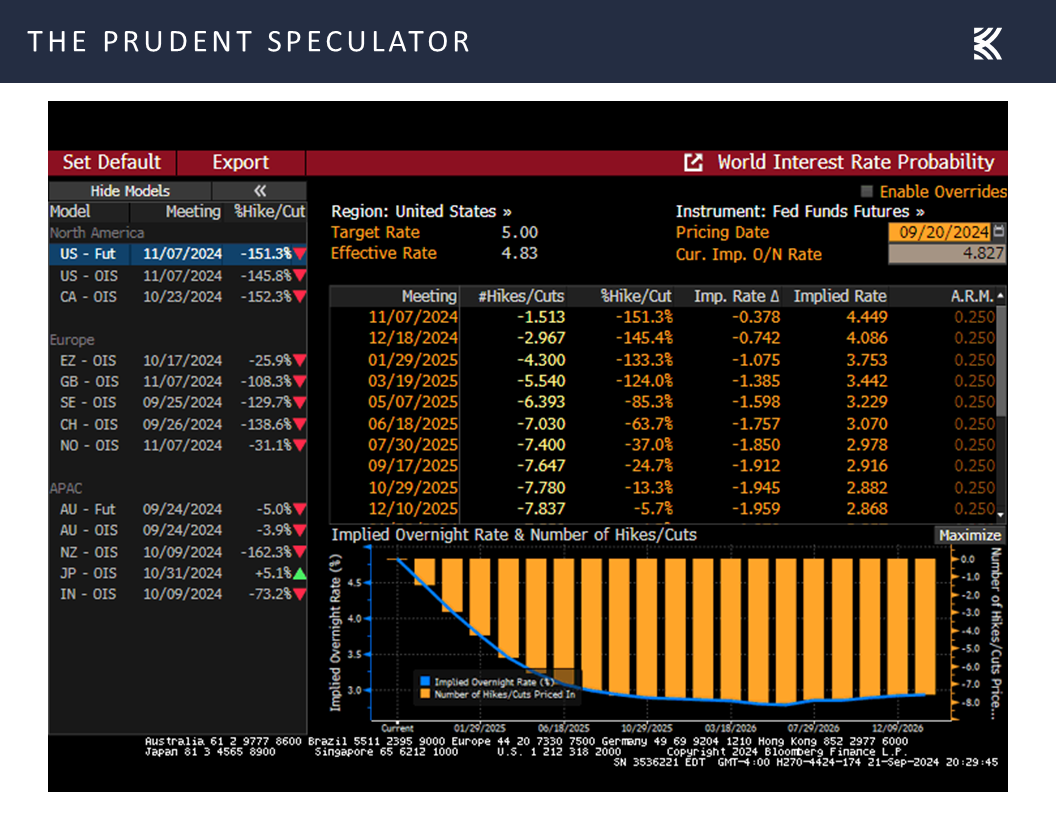

Those projections of a year-end 2024 Fed Funds rate of 4.4% and a year-end 2025 rate of 3.4% are less aggressive than what the betting in the Fed Funds futures market presently shows (4.09% this year and 2.87% next year)

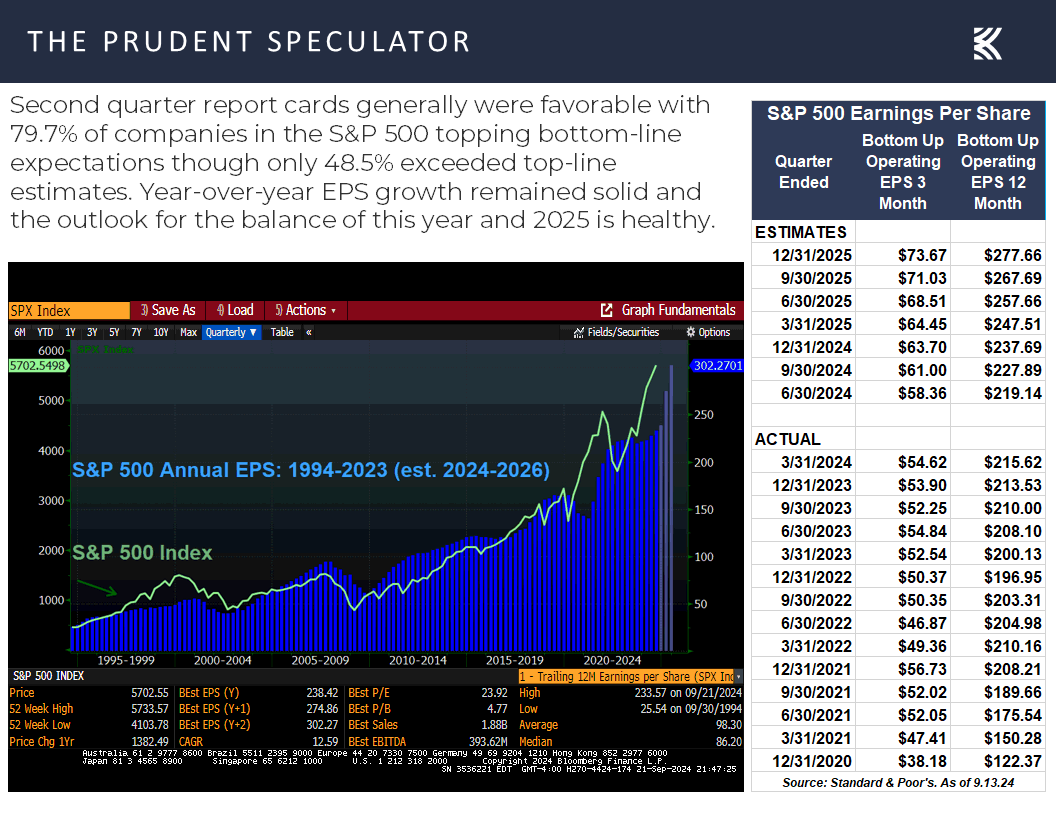

but Jerome H. Powell & Co. are estimating that real U.S. GDP growth will be 2.0% this year, next year and into 2026, which should be sufficient economic strength to support continued growth in corporate profits, which ultimately are the driver of stock prices.

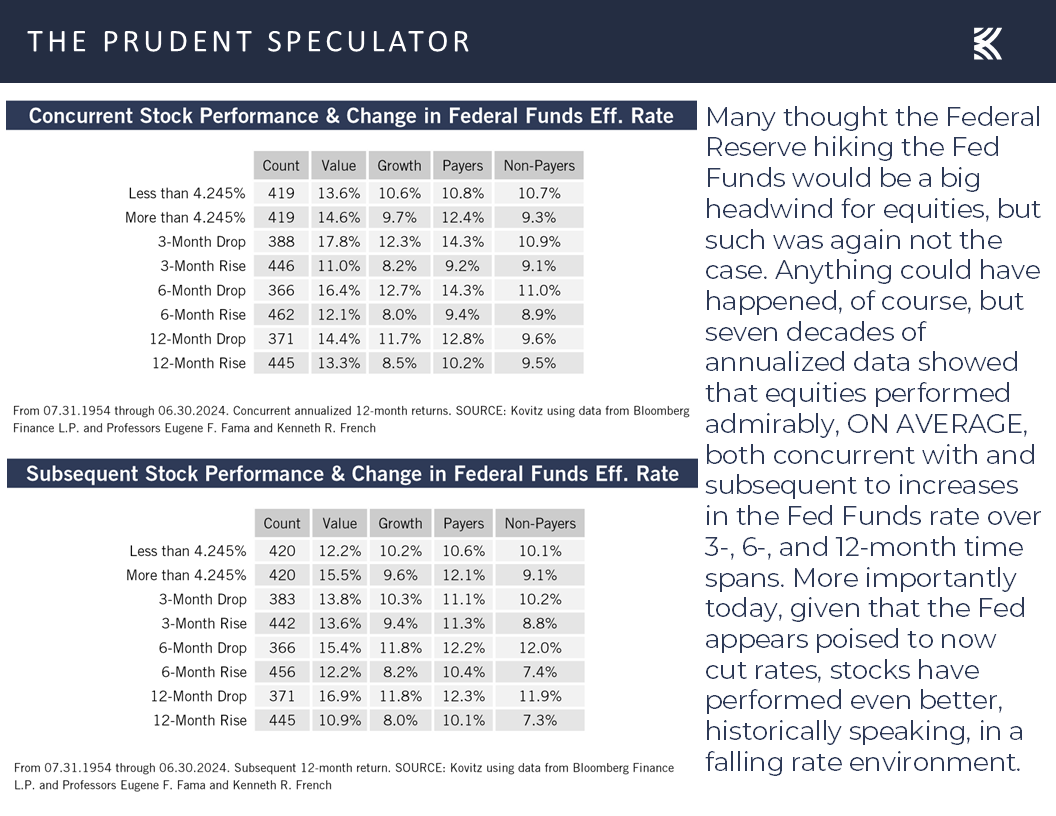

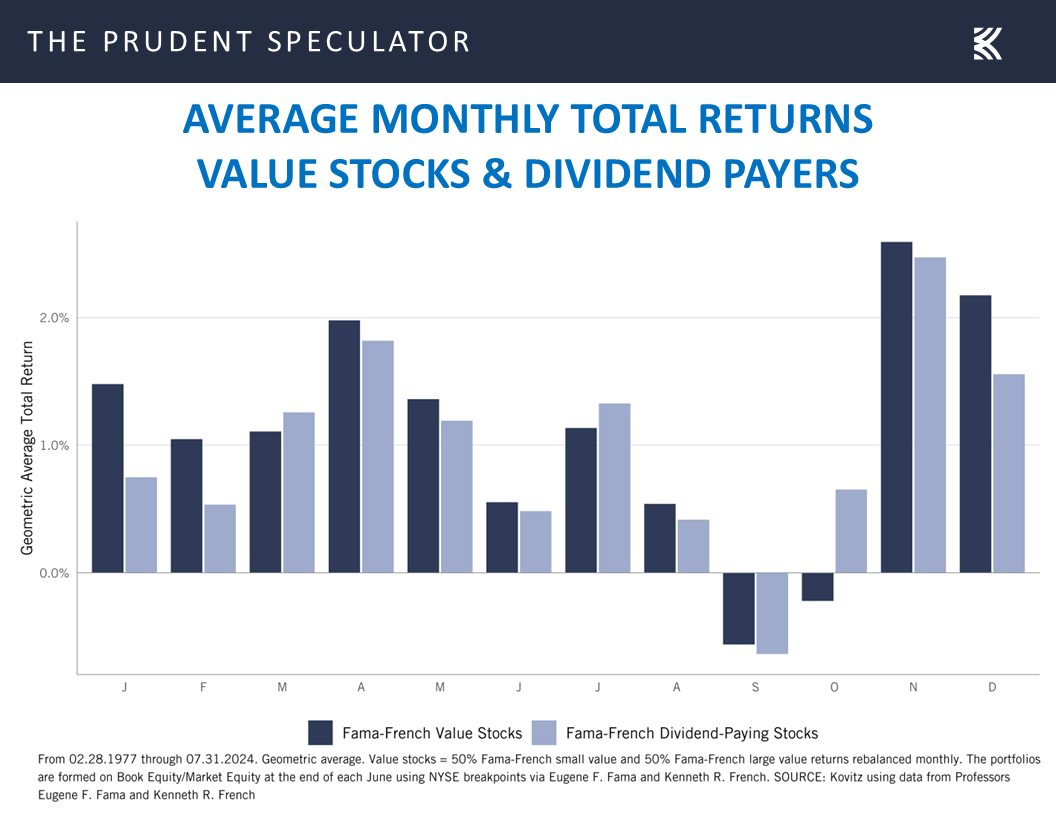

Rates & Stocks – Equities Have Performed Well, on Average, Whether Fed Funds or 10-Year Yield is Rising/Falling

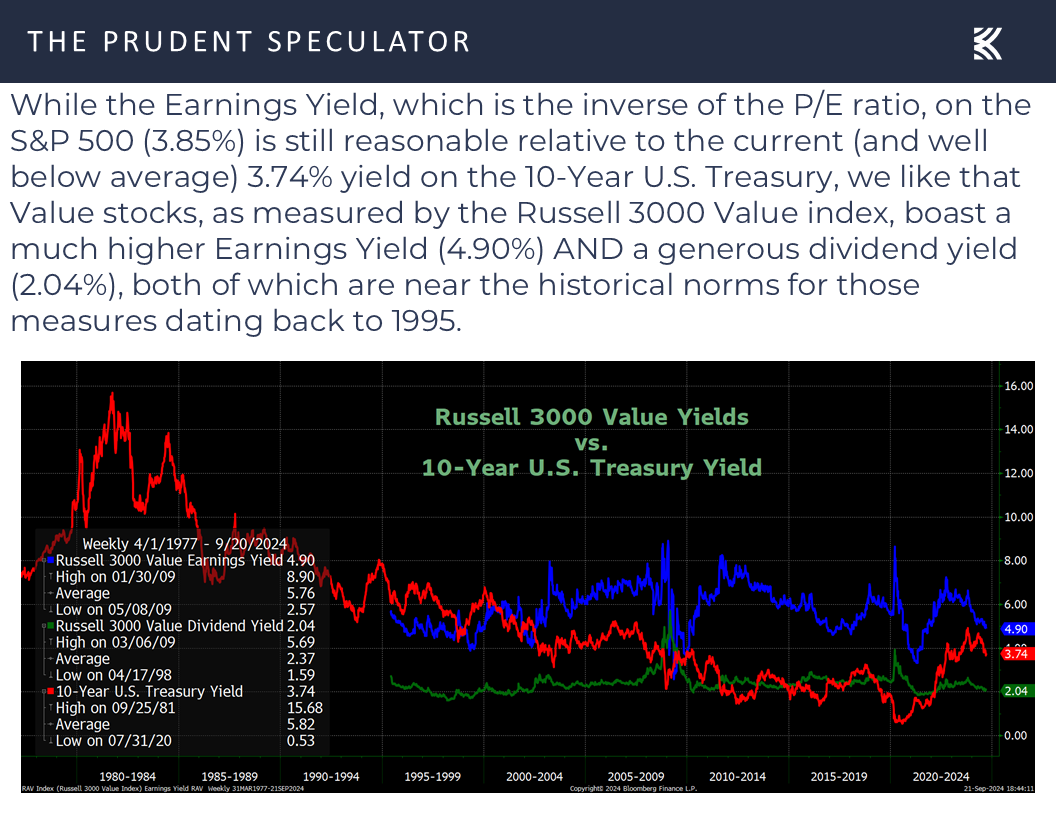

Lower interest rates, all else equal, add to the appeal of stocks from a dividend yield and earnings yield standpoint,

but history shows that equities, especially those of the Value variety, have performed well both concurrent with and subsequent to reductions AND increases in the Fed Funds rate.

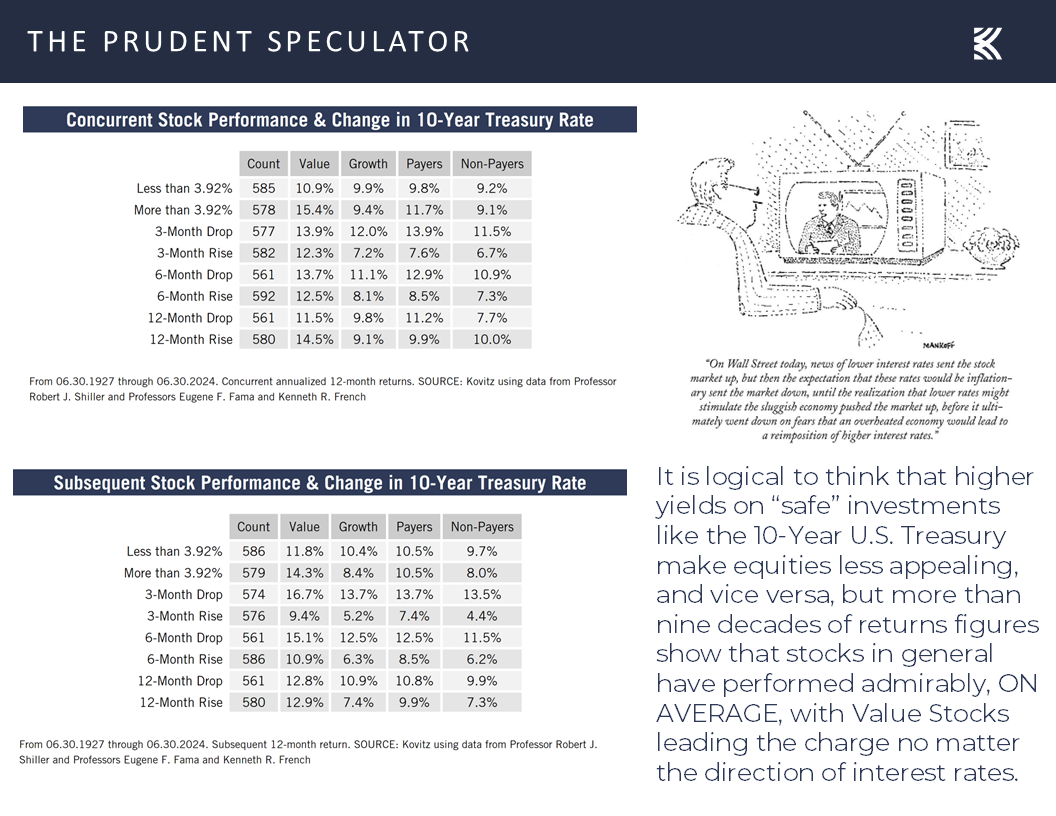

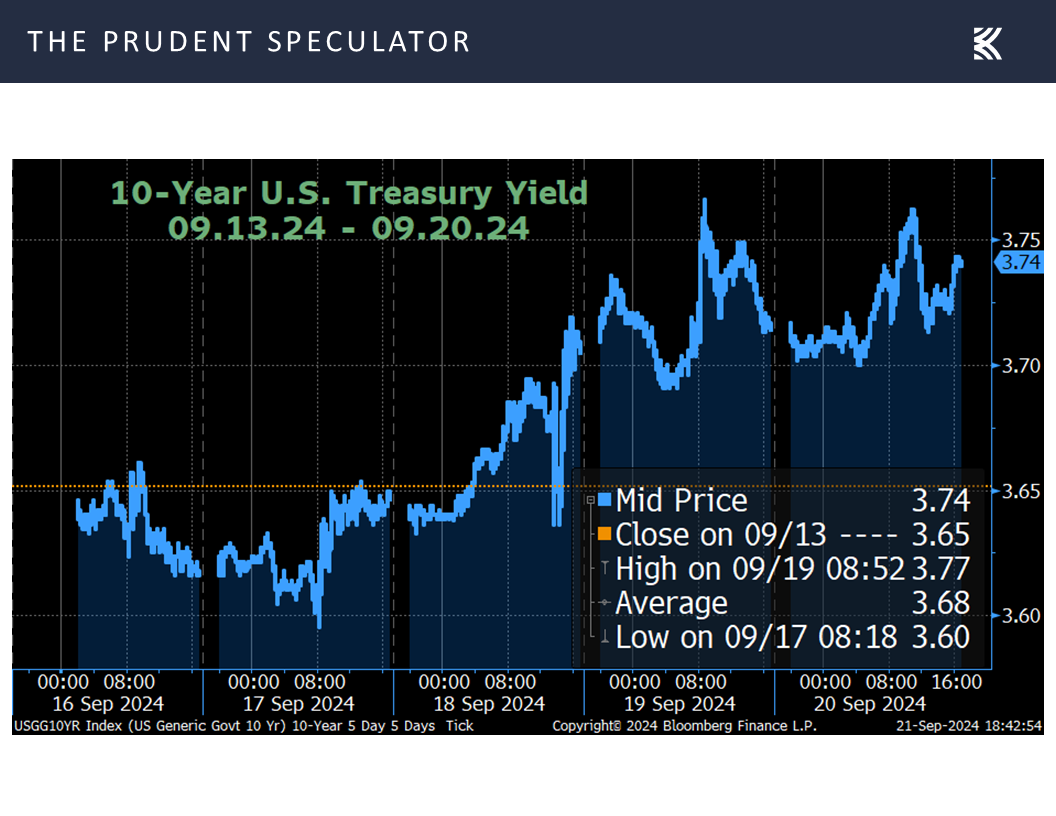

The same can be said for stocks in conjunction with upward and downward movements in the 10-Year U.S. Treasury yield,

with last week’s nice increase in equity prices, despite the benchmark government bond yield rising from 3.65% to 3.74%, illustrating the point.

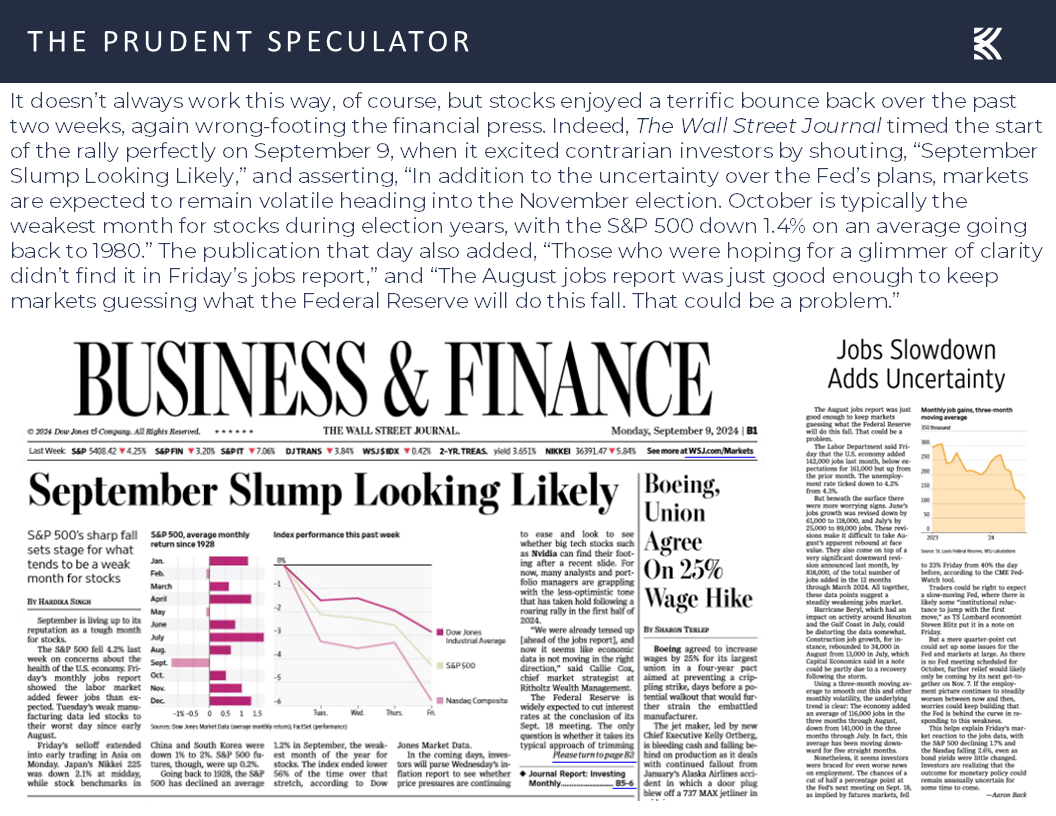

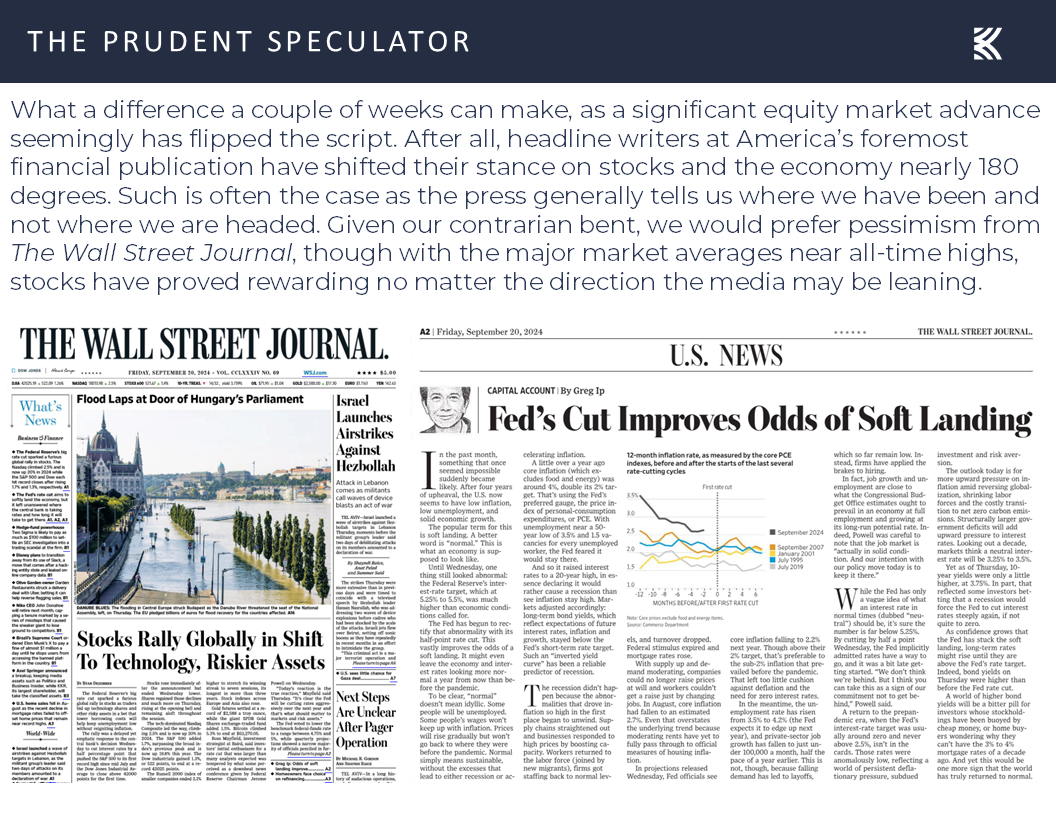

Emotional Roller Coaster – Media Still Not Exactly Helpful

Interestingly, it was just two weeks ago that fear was evident for market participants, at least judging by what the newspapers were saying,

in worrying about what the Fed would do and highlighting that we now reside in the seasonal week September-October period,

so it is fascinating to see the shift in tone in the financial press, even as not a whole lot changed on the economic and corporate profit front over the last two weeks.

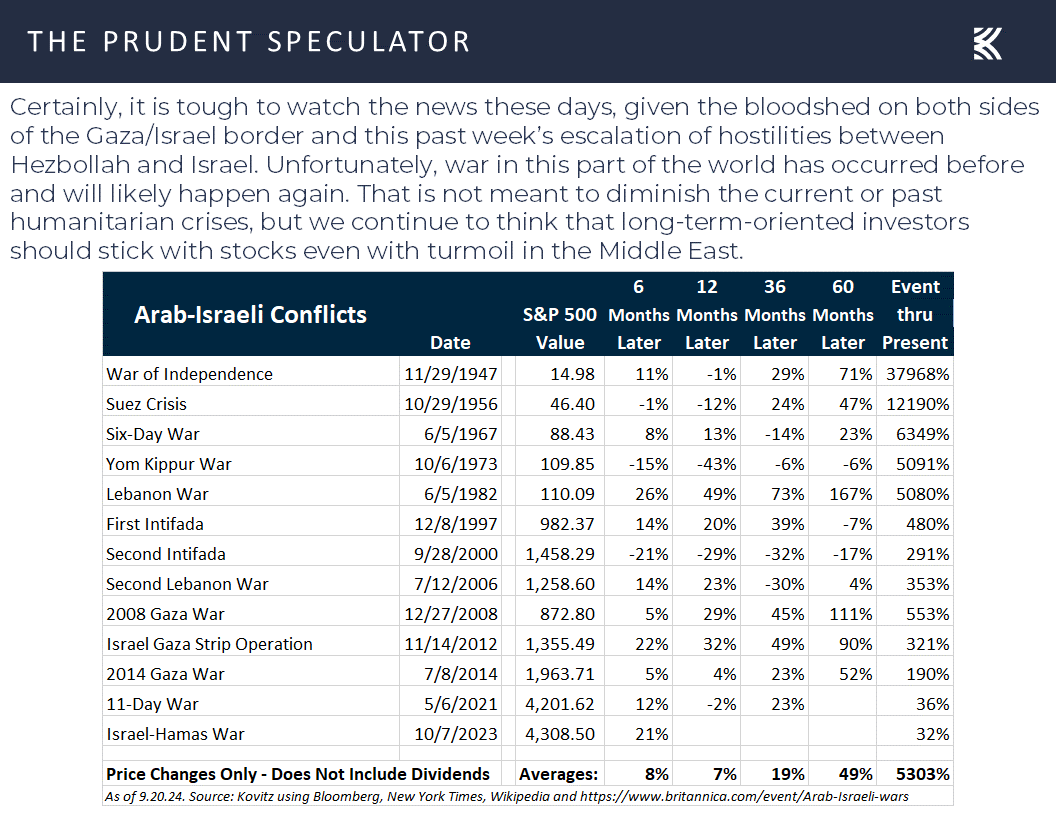

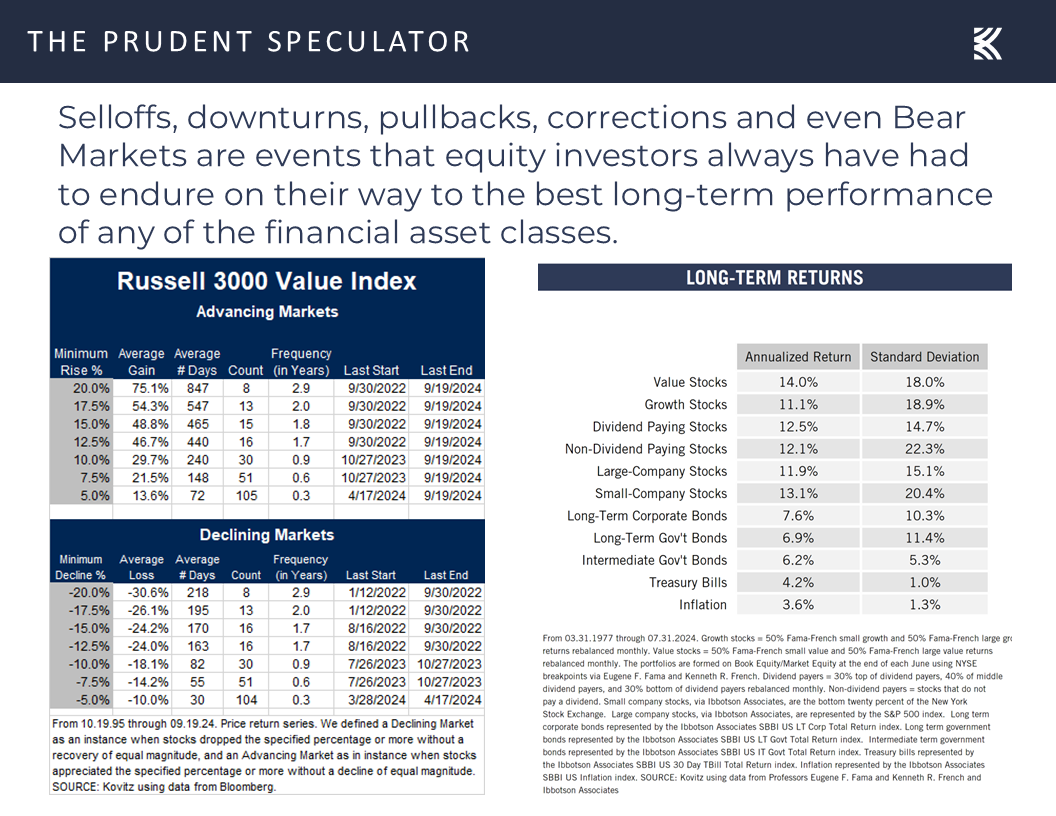

Historical Evidence – Stocks Have Overcome All Sorts of Headwinds

In actuality, we could argue that news on the global stage worsened with the escalation of hostilities between Israel and Hezbollah, though there has long been conflict in the Middle East through which stock prices have persevered.

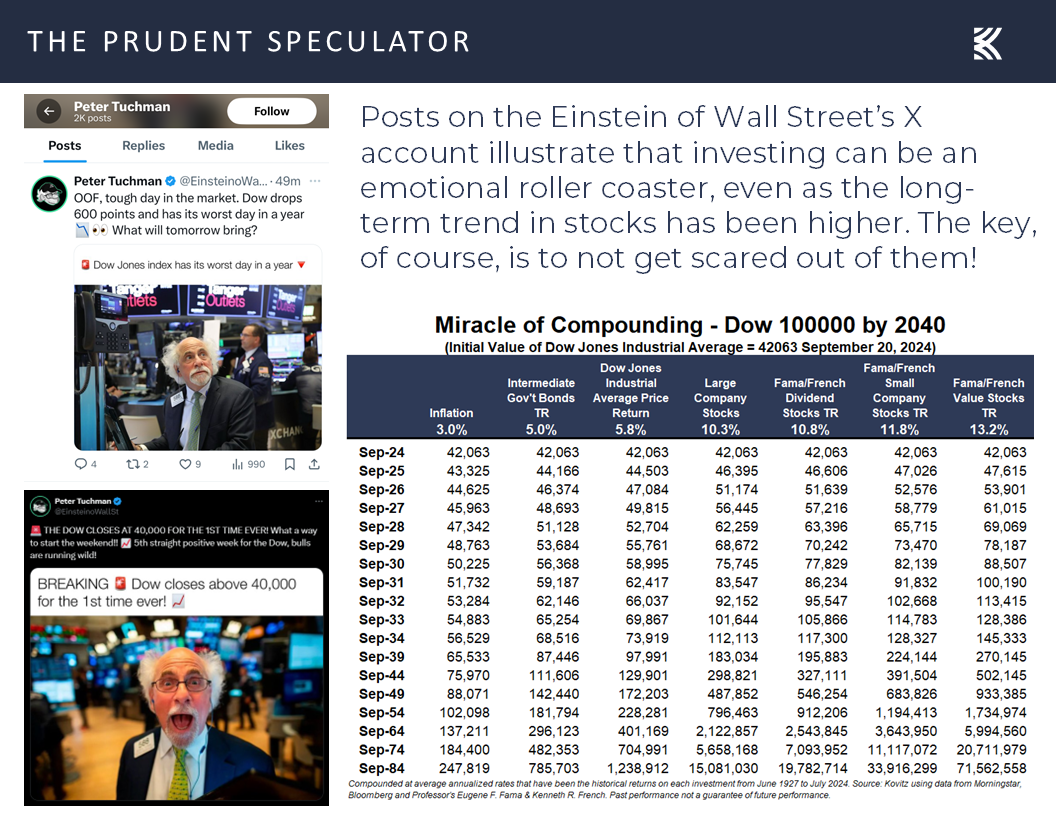

As we constantly state, we endeavor to stay on an even keel, keeping our emotions in check as equities have always proved rewarding in the fullness of time for those who remember that the secret to success in stocks is to not get scared out of them. Indeed, through the Miracle of Compounding, great fortunes can accrue even with relatively modest returns. For example, the Dow Jones Industrial Average would eclipse 100,000 in less than 16 years simply by showing 5.8% per annum price appreciation, which has been the historical rate of return for the popular benchmark. As the table below shows, the Dow would make it to six figures in just eight years if it was a total return and not a price index, and if it enjoyed the 13.2% total return that has been the average for Value stocks since 1927.

To be sure, there always will be plenty of scary volatility along the way,

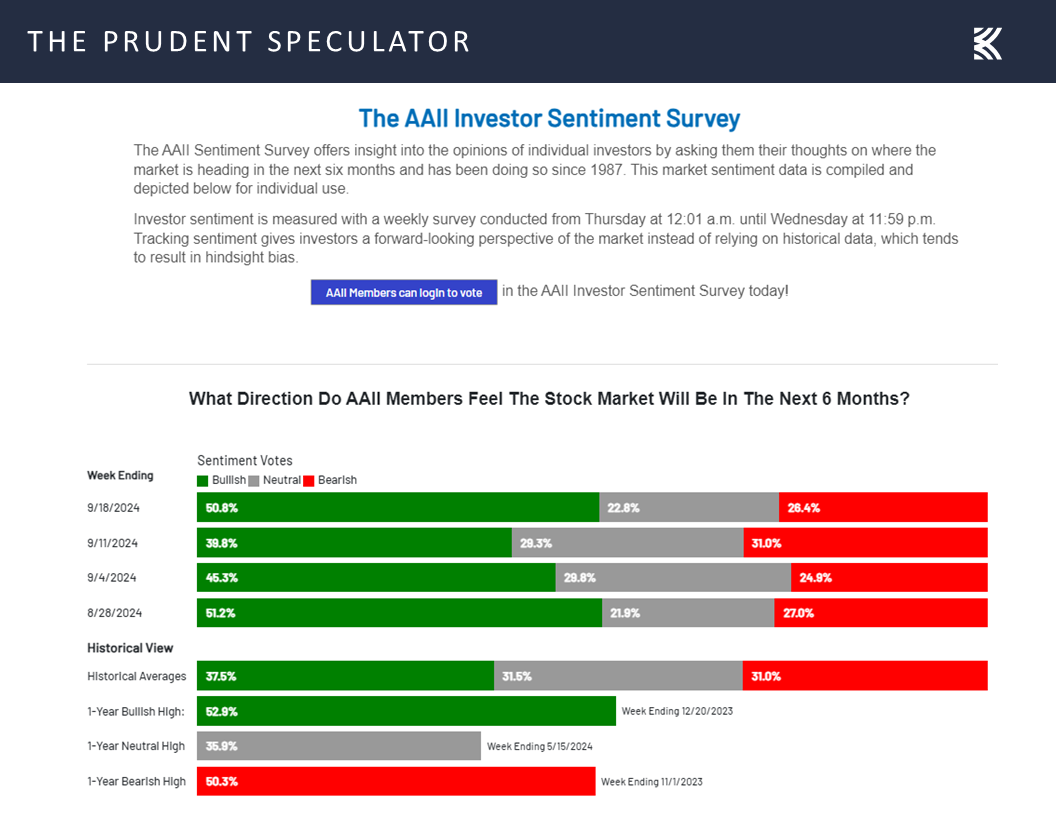

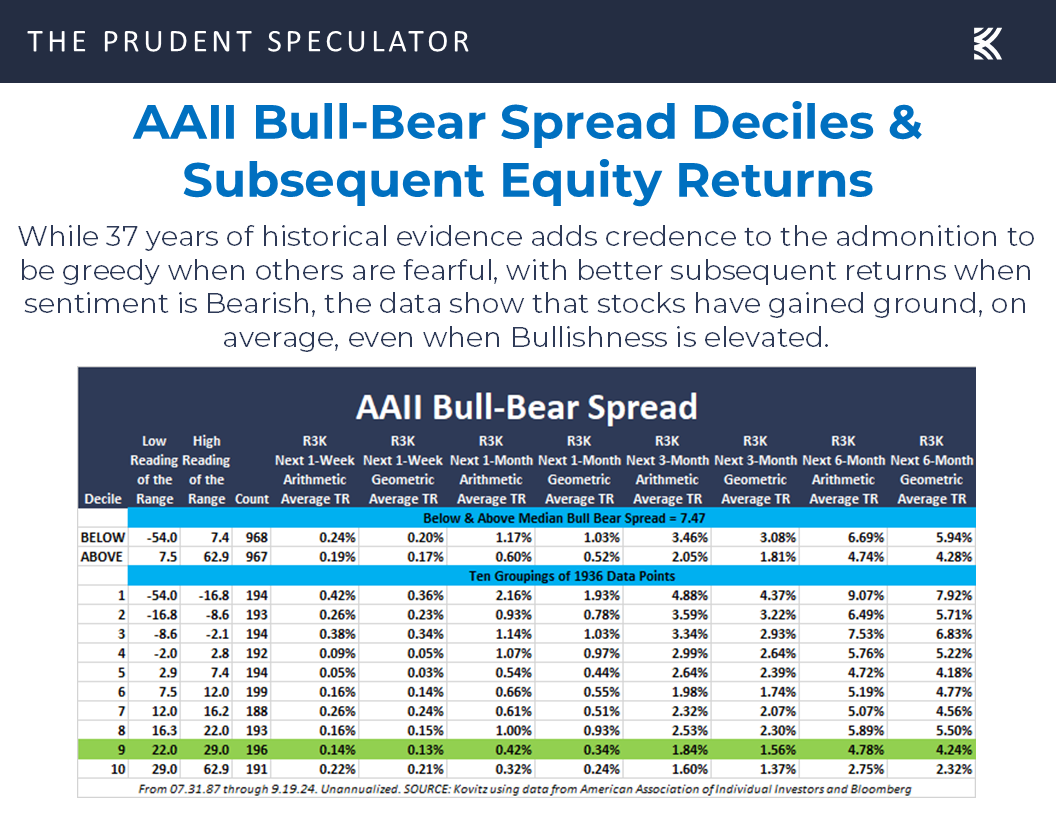

Sentiment – AAII Bullishness Jumps

so we must always be braced for downside movements, while we note that optimism on Main Street (a contra-indicator) spiked last week,

though the AAII Investor Sentiment survey, on average since 1987, has told us to expect positive, albeit lower, equity market total returns when folks are less fearful,

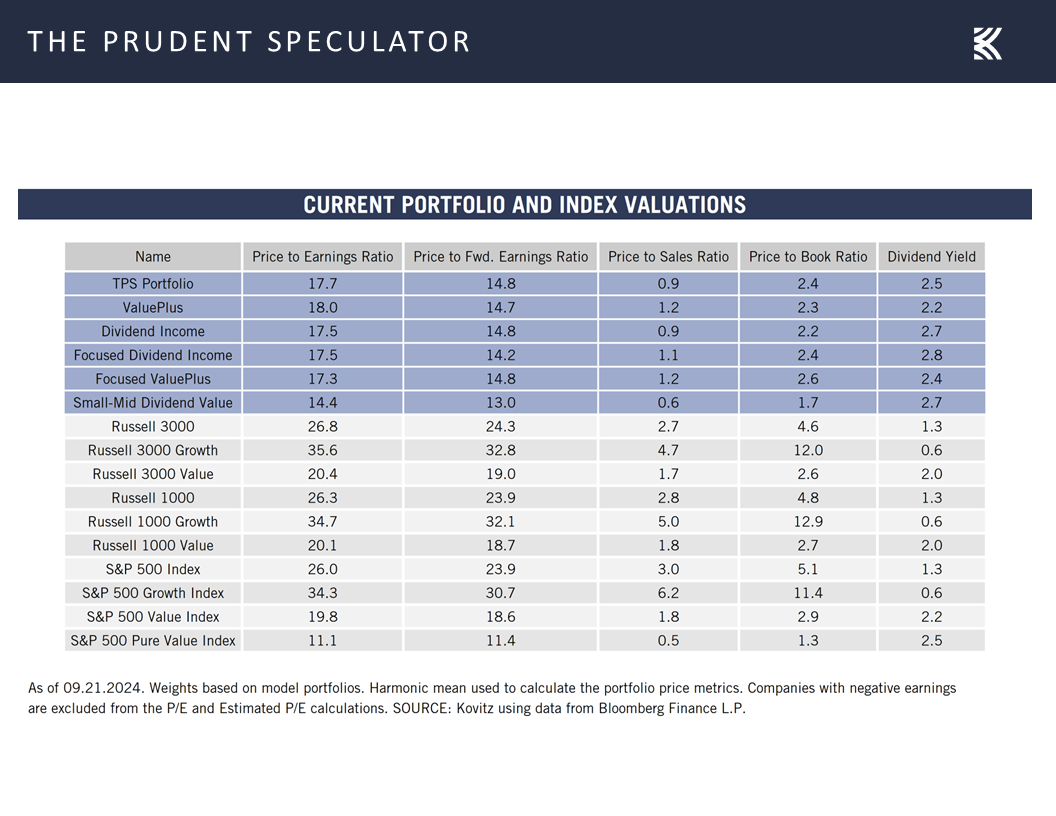

Valuations – Liking our Metrics

while we continue to sleep very well at night with the inexpensive financial valuation metrics and generous dividend yields for our broadly diversified portfolios of what we believe to be undervalued stocks.

Stock News – Updates on six stocks across four different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Federal Reserve, Economic Statistics, Interest Rates and Stocks

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Federal Reserve, Economic Statistics, Interest Rates and Stocks. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Fed Meeting – 50-Basis-Point Rate Cut

Econ Stats – Mostly Better-than-Expected Numbers

GDP Outlook – Decent Growth the Prognosis, Supporting Solid EPS Growth

Rates & Stocks – Equities Have Performed Well, on Average, Whether Fed Funds or 10-Year Yield is Rising/Falling

Emotional Roller Coaster – Media Still Not Exactly Helpful

Historical Evidence – Stocks Have Overcome All Sorts of Headwinds

Sentiment – AAII Bullishness Jumps

Valuations – Liking our Metrics

Stock News – Updates on six stocks across four different sectors

Fed Meeting – 50-Basis-Point Rate Cut

With the FOMC Statement declaring, “In light of the progress on inflation and the balance of risks, the Committee decided to lower the target range for the federal funds rate by ½ percentage point to 4-3/4% to 5%,”

Econ Stats – Mostly Better-than-Expected Numbers

the Federal Reserve last week initiated the first cut in interest rates by the U.S. central bank since the Pandemic.

The equity markets cheered the news with the major stock market averages hitting all-time highs as Fed Chair Jerome H. Powell sounded upbeat in his prepared remarks at the Press Conference that followed the decision on rates,

and economic data out last week generally came in better than expected, starting with the report of retail sales rising in August by 0.1%, versus the 0.2% decline that was projected,

and the Empire State Manufacturing gauge of factory activity in the New York area jumping to a reading of 11.5 this month, well above estimates of -4.0 and the August figure of -4.7.

We also learned that industrial production climbed to a month-over-month improvement of 0.8% in August, compared to the estimate of a 0.2% increase and July’s revised decline of 0.9%,

housing starts topped forecasts, coming in at 1.356 million last month, versus projections of 1.318 million and the revised tally the month prior of 1.237 million,

and the Philadelphia Fed Manufacturing index rebounded to 1.7 in September from -7.0 in August.

True, existing home sales for August of 3.86 million trailed expectations of 3.90 million,

but first-time filings for jobless benefits of 219,000 in the most recent week were down from a revised 231,000 the week prior and projections of 230,000,

GDP Outlook – Decent Growth the Prognosis, Supporting Solid EPS Growth

and the latest forecast for real (inflation-adjusted) U.S. GDP growth for Q3 from the Atlanta Fed stood at a solid 2.9%.

The keeper of the LEI, the Conference Board, suggested that while the economy will face headwinds over the balance of 2024, stronger economic activity is likely next year thanks to last week’s cut in the Fed Funds rate AND the expectation for additional reductions shown in the economic projections released by Federal Reserve Board members and Federal Reserve Bank presidents last week.

Those projections of a year-end 2024 Fed Funds rate of 4.4% and a year-end 2025 rate of 3.4% are less aggressive than what the betting in the Fed Funds futures market presently shows (4.09% this year and 2.87% next year)

but Jerome H. Powell & Co. are estimating that real U.S. GDP growth will be 2.0% this year, next year and into 2026, which should be sufficient economic strength to support continued growth in corporate profits, which ultimately are the driver of stock prices.

Rates & Stocks – Equities Have Performed Well, on Average, Whether Fed Funds or 10-Year Yield is Rising/Falling

Lower interest rates, all else equal, add to the appeal of stocks from a dividend yield and earnings yield standpoint,

but history shows that equities, especially those of the Value variety, have performed well both concurrent with and subsequent to reductions AND increases in the Fed Funds rate.

The same can be said for stocks in conjunction with upward and downward movements in the 10-Year U.S. Treasury yield,

with last week’s nice increase in equity prices, despite the benchmark government bond yield rising from 3.65% to 3.74%, illustrating the point.

Emotional Roller Coaster – Media Still Not Exactly Helpful

Interestingly, it was just two weeks ago that fear was evident for market participants, at least judging by what the newspapers were saying,

in worrying about what the Fed would do and highlighting that we now reside in the seasonal week September-October period,

so it is fascinating to see the shift in tone in the financial press, even as not a whole lot changed on the economic and corporate profit front over the last two weeks.

Historical Evidence – Stocks Have Overcome All Sorts of Headwinds

In actuality, we could argue that news on the global stage worsened with the escalation of hostilities between Israel and Hezbollah, though there has long been conflict in the Middle East through which stock prices have persevered.

As we constantly state, we endeavor to stay on an even keel, keeping our emotions in check as equities have always proved rewarding in the fullness of time for those who remember that the secret to success in stocks is to not get scared out of them. Indeed, through the Miracle of Compounding, great fortunes can accrue even with relatively modest returns. For example, the Dow Jones Industrial Average would eclipse 100,000 in less than 16 years simply by showing 5.8% per annum price appreciation, which has been the historical rate of return for the popular benchmark. As the table below shows, the Dow would make it to six figures in just eight years if it was a total return and not a price index, and if it enjoyed the 13.2% total return that has been the average for Value stocks since 1927.

To be sure, there always will be plenty of scary volatility along the way,

Sentiment – AAII Bullishness Jumps

so we must always be braced for downside movements, while we note that optimism on Main Street (a contra-indicator) spiked last week,

though the AAII Investor Sentiment survey, on average since 1987, has told us to expect positive, albeit lower, equity market total returns when folks are less fearful,

Valuations – Liking our Metrics

while we continue to sleep very well at night with the inexpensive financial valuation metrics and generous dividend yields for our broadly diversified portfolios of what we believe to be undervalued stocks.

Stock News – Updates on six stocks across four different sectors

About the Author

Phil Edwards

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.