The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Federal Reserve, Economy, Earnings, Valuations and more news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – A Buy and Two Sells

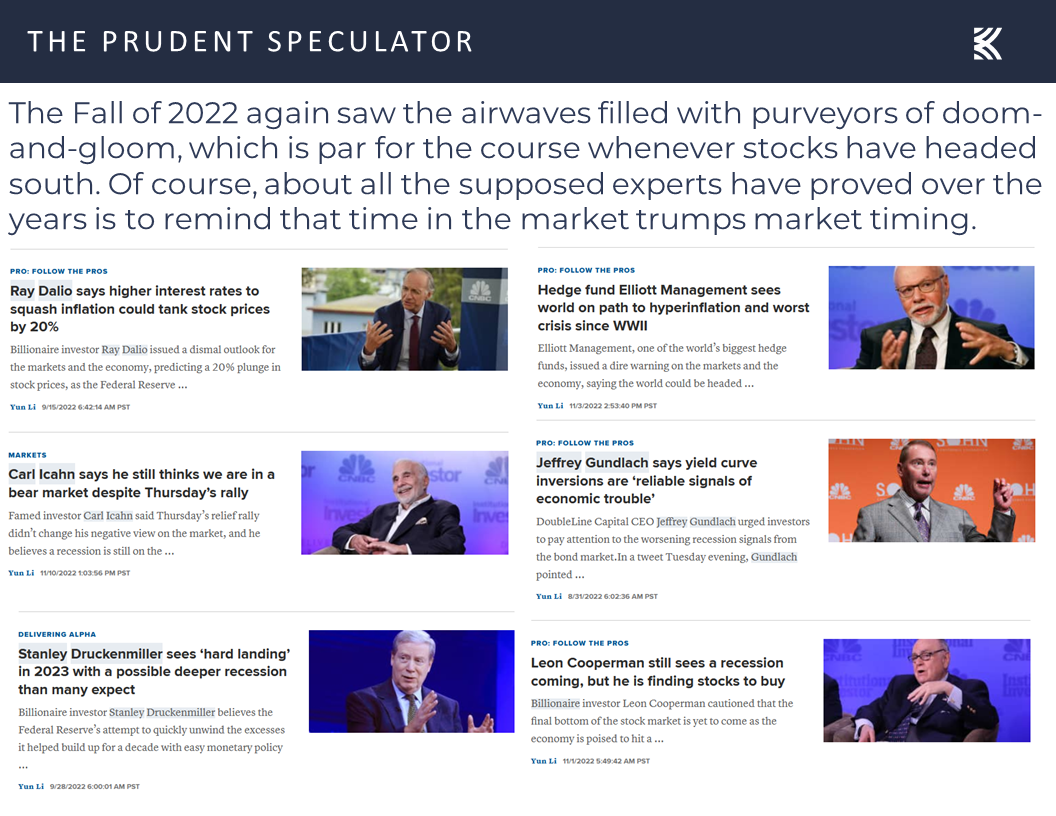

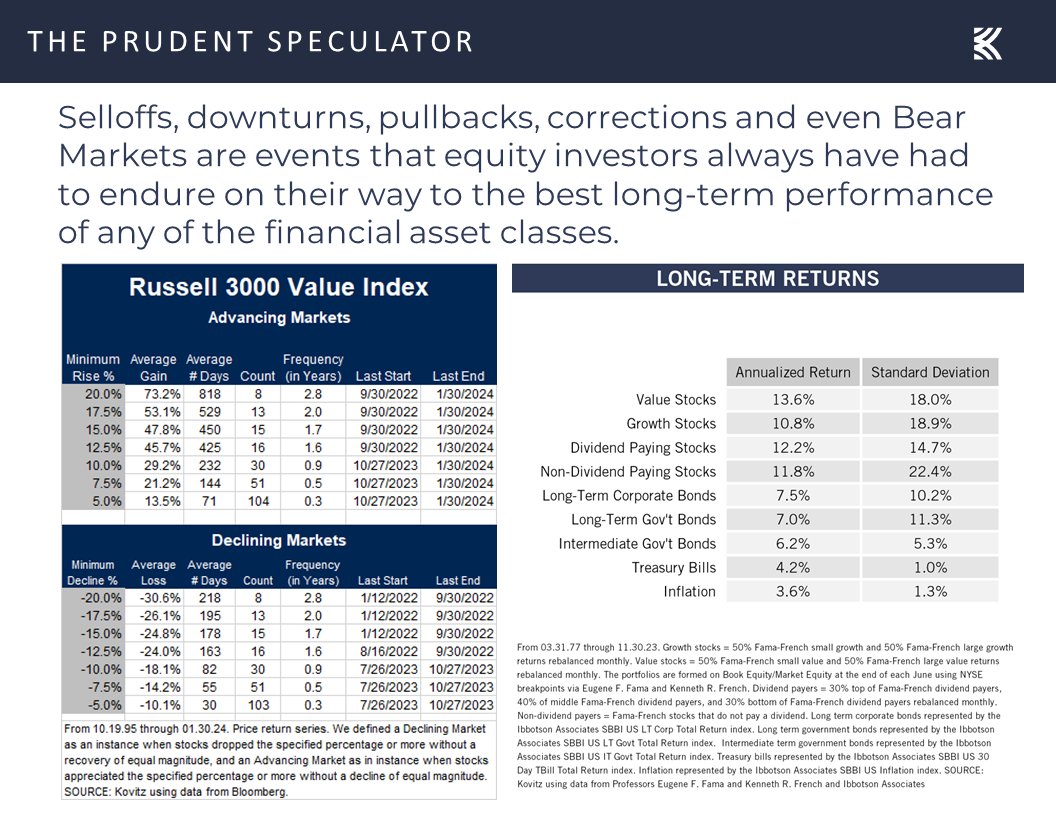

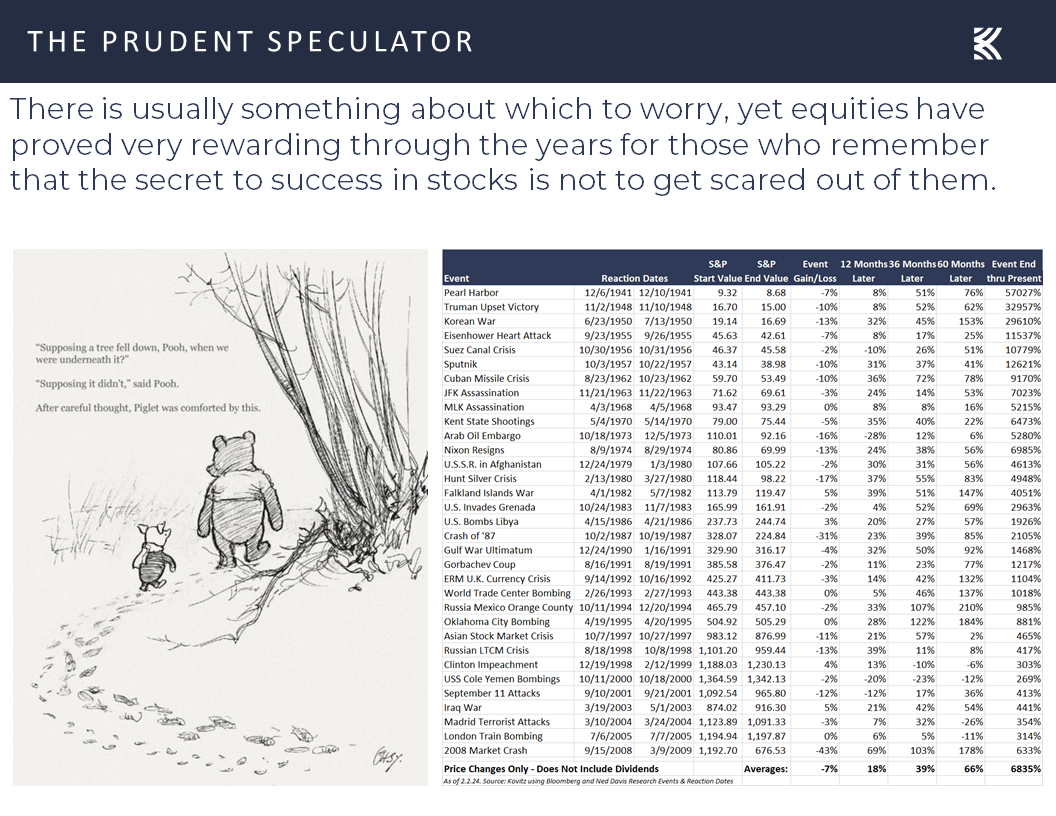

All-Time Highs – Despite Ups and Downs, Stocks Have Proved Rewarding Over the Long Term

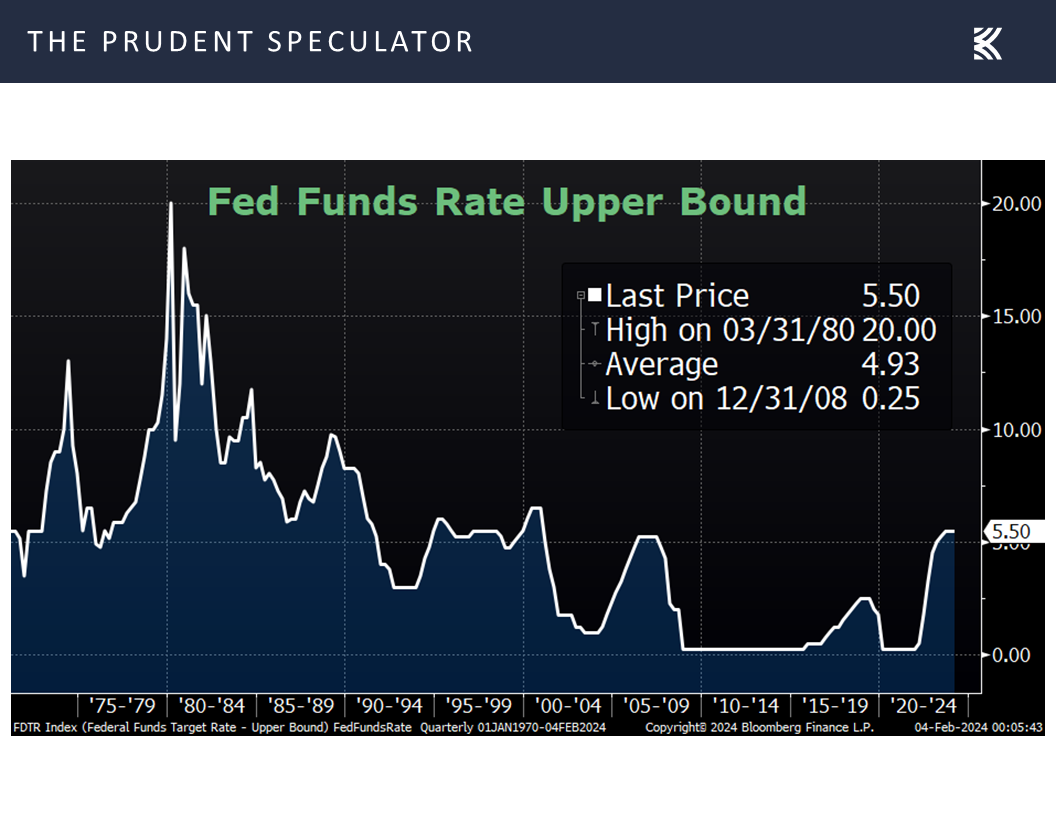

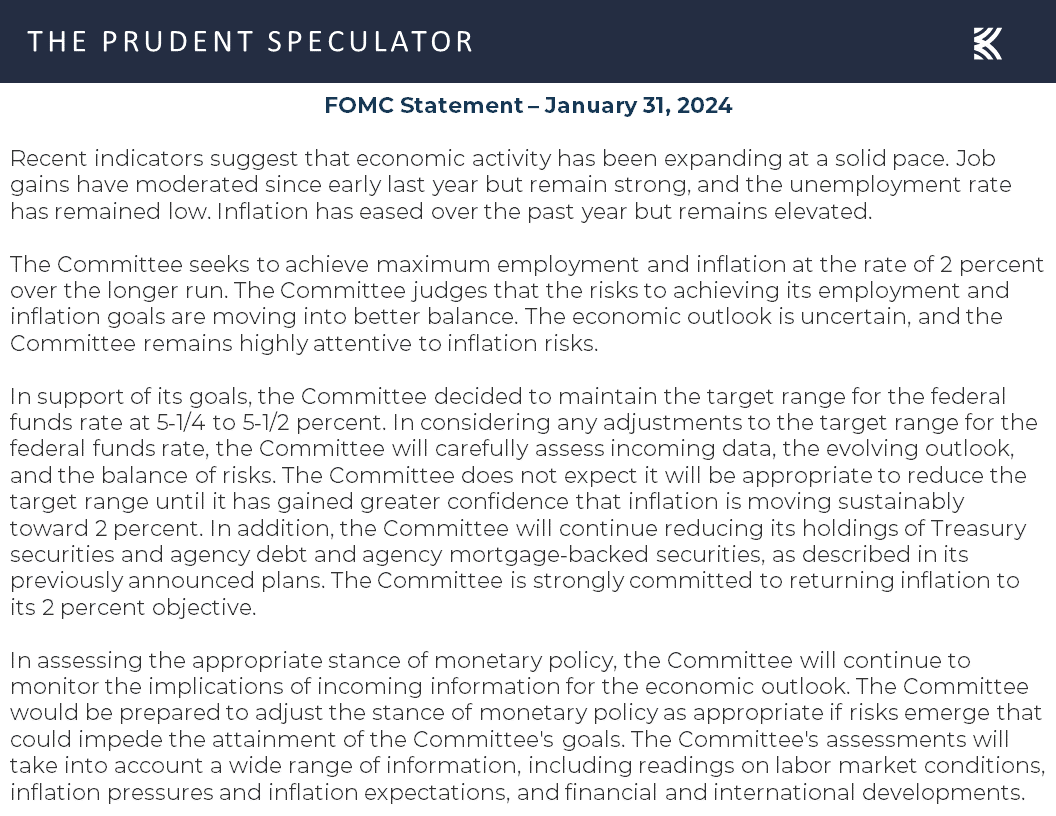

Fed – First Interest Rate Cut Not Likely to Happen in March

Economy – Strong Jobs Numbers

Earnings – Solid Q4 Numbers

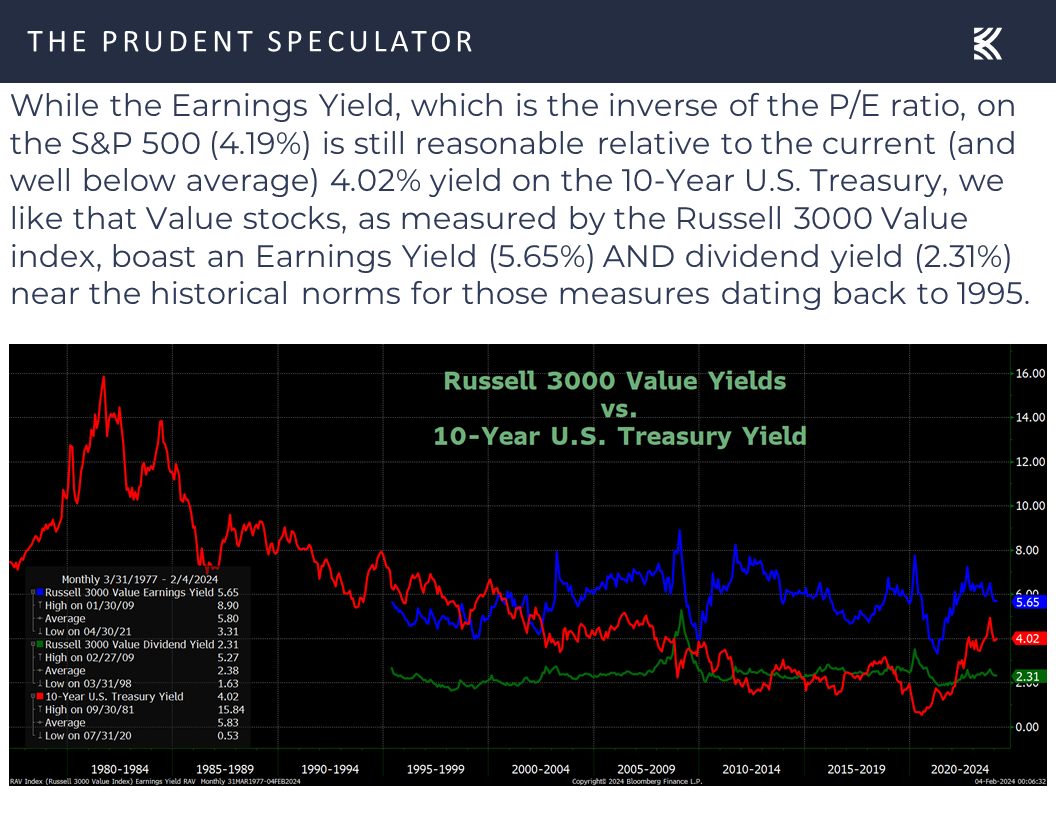

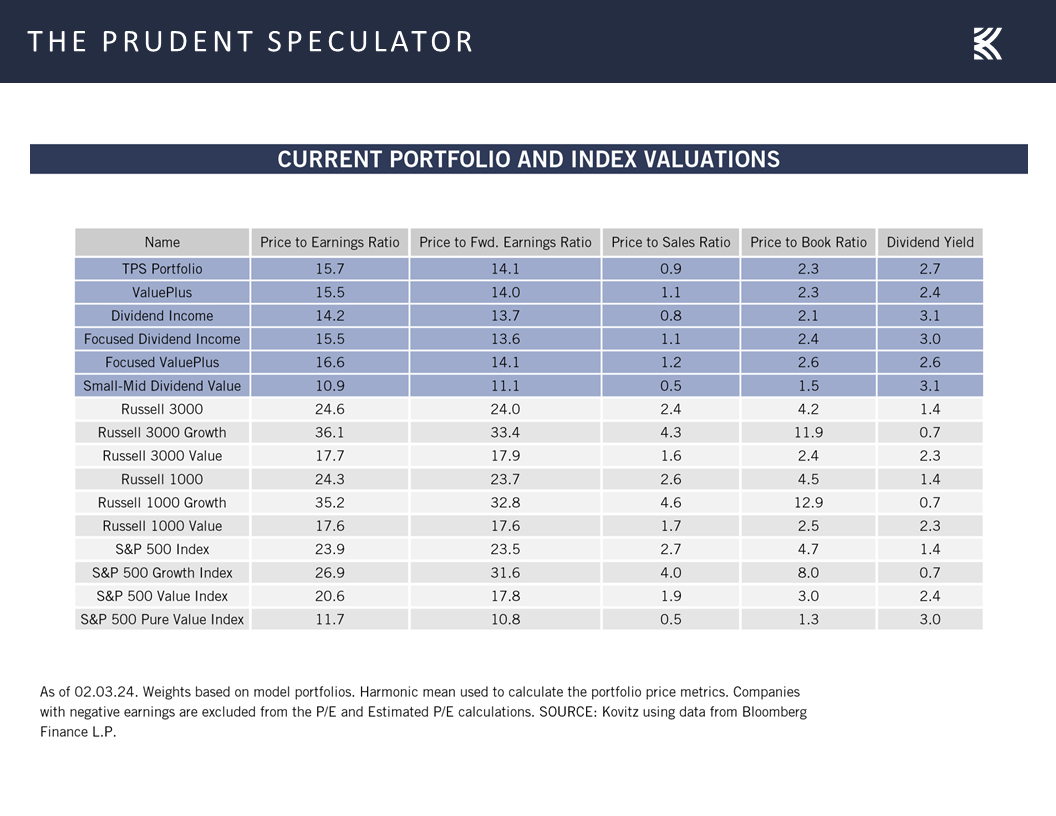

Valuations – Value Stocks Attractively Priced

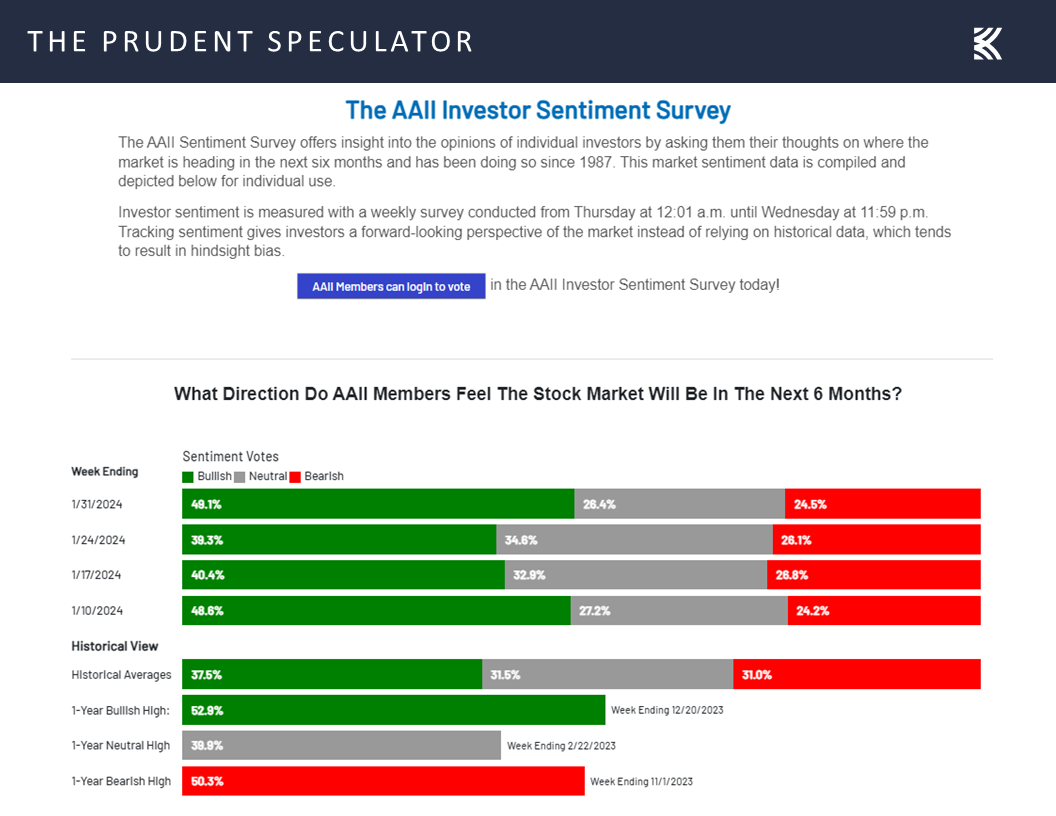

Sentiment – AAII More Optimistic

Stock News – Updates on PHG, GLW, GOOG, BHE, ETN, MRK, CAH, GEN, META, AAPL & CVX

All-Time Highs – Despite Ups and Downs, Stocks Have Proved Rewarding Over the Long Term

Certainly, prices could have moved lower still back then as corrections and Bear Markets are a normal part of the investment process, but as has occurred following every other setback, rallies and Bull Markets have taken place. Gains from those advances have dwarfed the declines, so much so that long-term returns on Value Stocks have exceeded 13% per annum since the launch of The Prudent Speculator nearly 47 years ago.

Fed – First Interest Rate Cut Not Likely to Happen in March

Of course, there have been plenty of scary selloffs along the way, with one of those downturns (1.6% tumble on the S&P 500) taking place this past Wednesday, following the Federal Reserve’s latest decision on interest rates. As expected, Jerome H. Powell & Co. left the target for the Fed Funds rate unchanged at a range of 5.25% to 5.50%,

and offered a relatively upbeat economic outlook in the accompanying FOMC statement,

but Chair Powell said at the Press Conference following the decision on rates, “I don’t think it’s likely the committee will reach a level of confidence by the time of the March meeting, but that’s to be seen,” as he dampened expectations of a Fed Funds rate cut at the next FOMC get-together. The first cut, per the Fed Funds futures market, is now expected at the May meeting, while the year-end rate moved up to 4.07% from 3.99% the week prior.

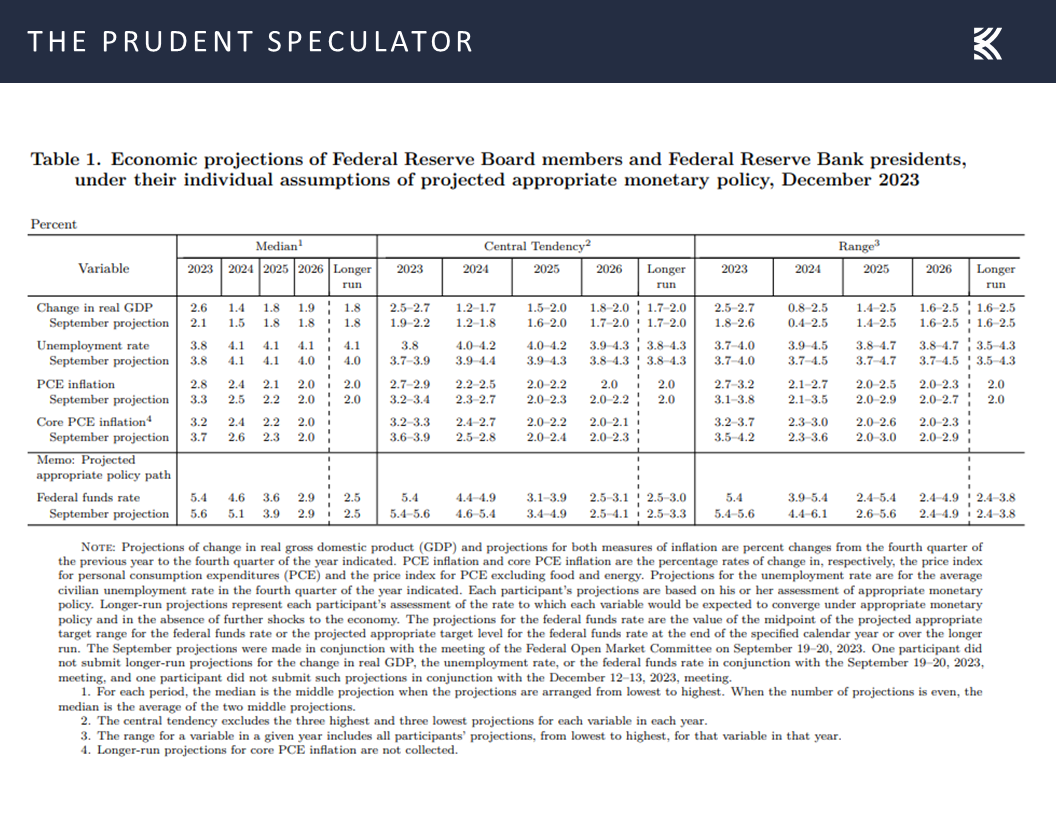

We do not think delaying the start of the easing cycle is unreasonable, given that the Fed in December forecast a year-end 2024 Fed Funds rate of 4.6%,

Economy – Strong Jobs Numbers

while Mr. Powell at his post-Fed-decision press conference stated: “Recent indicators suggest that economic activity has been expanding at a solid pace. GDP growth in the fourth quarter of last year came in at 3.3 percent. For 2023 as a whole, GDP expanded at 3.1 percent, bolstered by strong consumer demand as well as improving supply conditions. Activity in the housing sector was subdued over the past year, largely reflecting high mortgage rates. High interest rates also appear to have been weighing on business fixed investment.”

He also offered an assessment of the employment situation: “The labor market remains tight, but supply and demand conditions continue to come into better balance. Over the past three months, payroll job gains averaged 165 thousand jobs per month, a pace that is well below that seen a year ago but still strong. The unemployment rate remains low, at 3.7 percent. Strong job creation has been accompanied by an increase in the supply of workers: The labor force participation rate has moved up on balance over the past year, particularly for individuals aged 25 to 54 years, and immigration has returned to pre-pandemic levels. Nominal wage growth has been easing, and job vacancies have declined. Although the jobs-to-workers gap has narrowed, labor demand still exceeds the supply of available workers.”

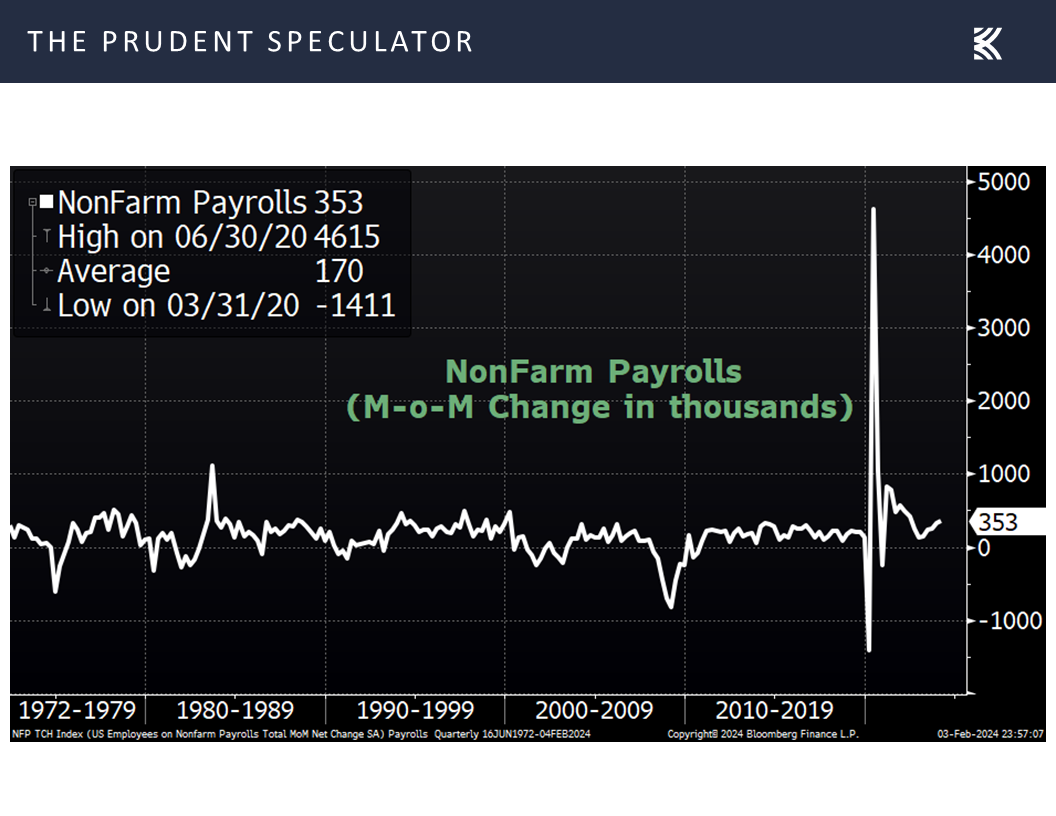

And those comments came prior to the monthly jobs report out on Friday in which there were far more new payrolls (353,000) created than expected,

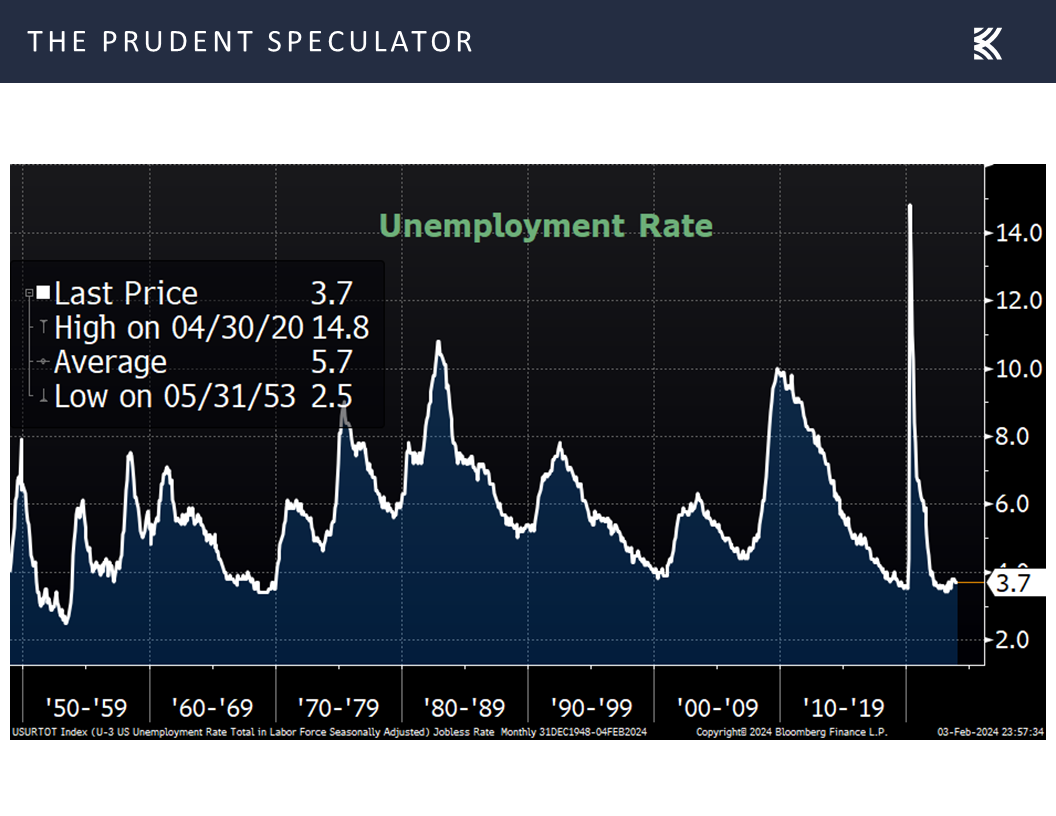

with the unemployment rate holding steady at 3.7%, also better than the 3.8% projection.

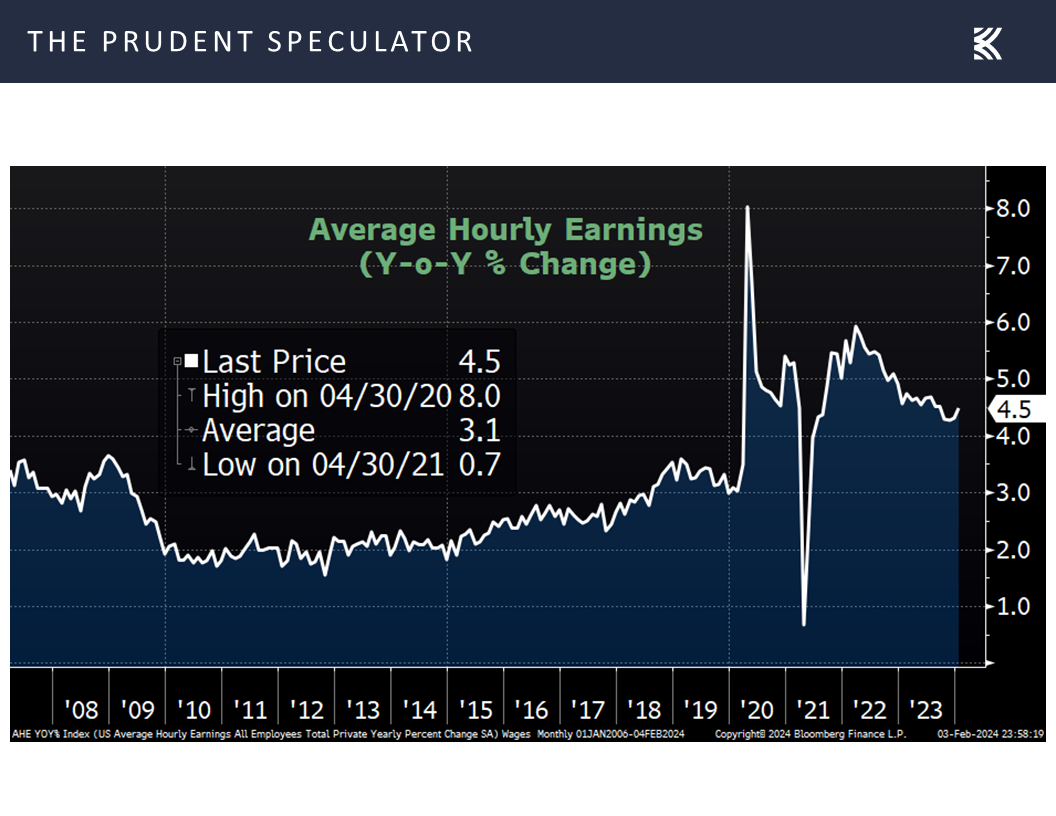

We learned, too, that average hourly earnings ticked up 4.5% in December, higher than estimated,

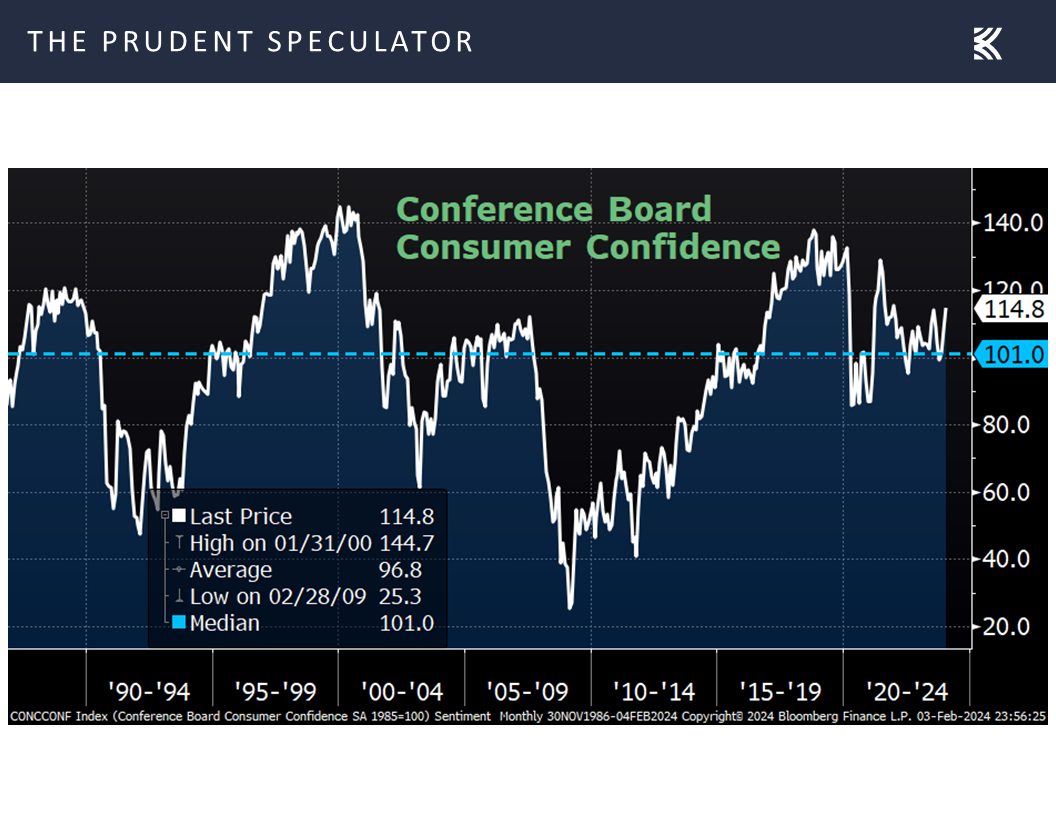

while consumer confidence, per the Conference Board,

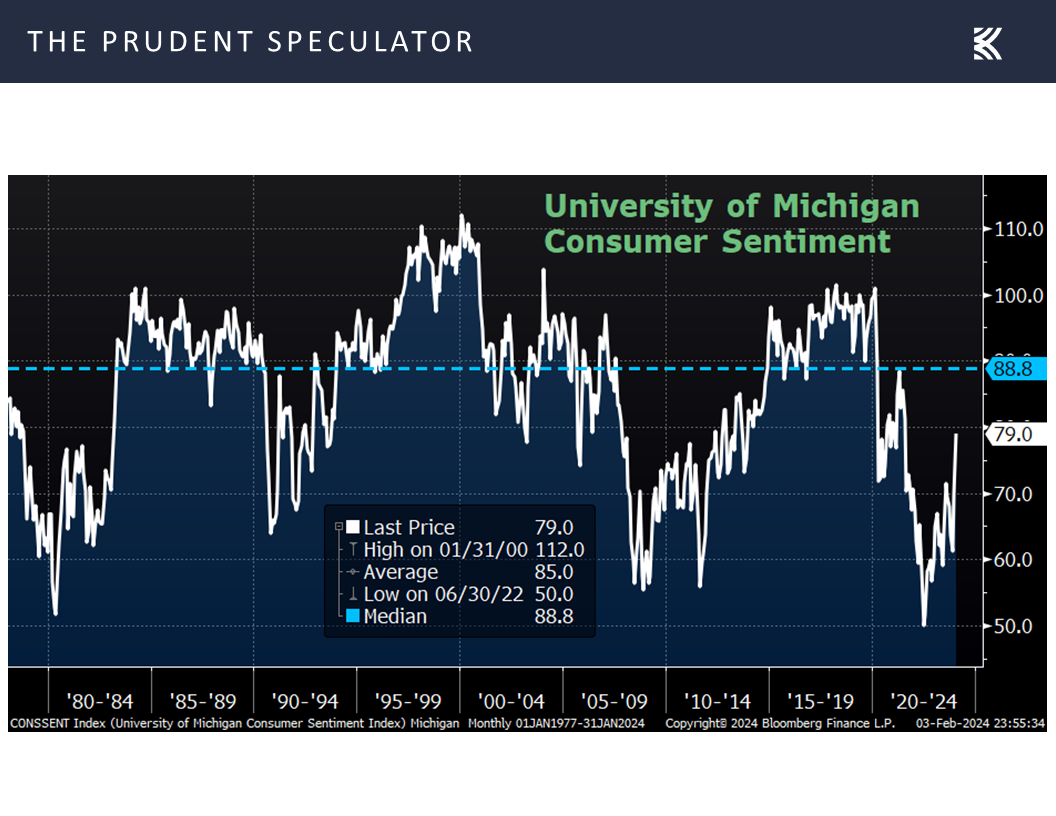

and consumer sentiment, per the Univ. of Michigan, maintained an upward trajectory.

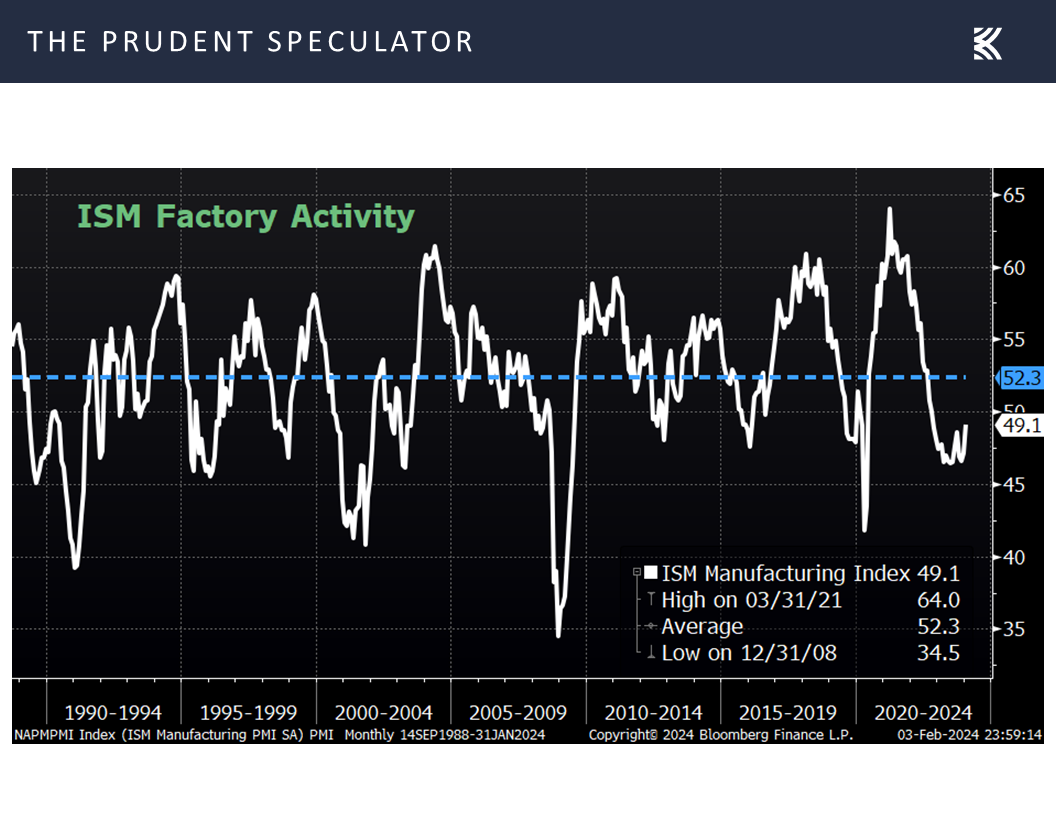

Finally, the important ISM Manufacturing Index (PMI) eclipsed projections with a rise to 49.1 in January, up from 47.1 in December, with the keeper of the index stating, “A Manufacturing PMI® above 42.5 percent, over a period of time, generally indicates an expansion of the overall economy. Therefore, the January Manufacturing PMI® indicates the overall economy grew for the 45th straight month after one month of contraction (April 2020). The past relationship between the Manufacturing PMI® and the overall economy indicates that the January reading (49.1 percent) corresponds to a change of plus-1.9 percent in real gross domestic product (GDP) on an annualized basis.”

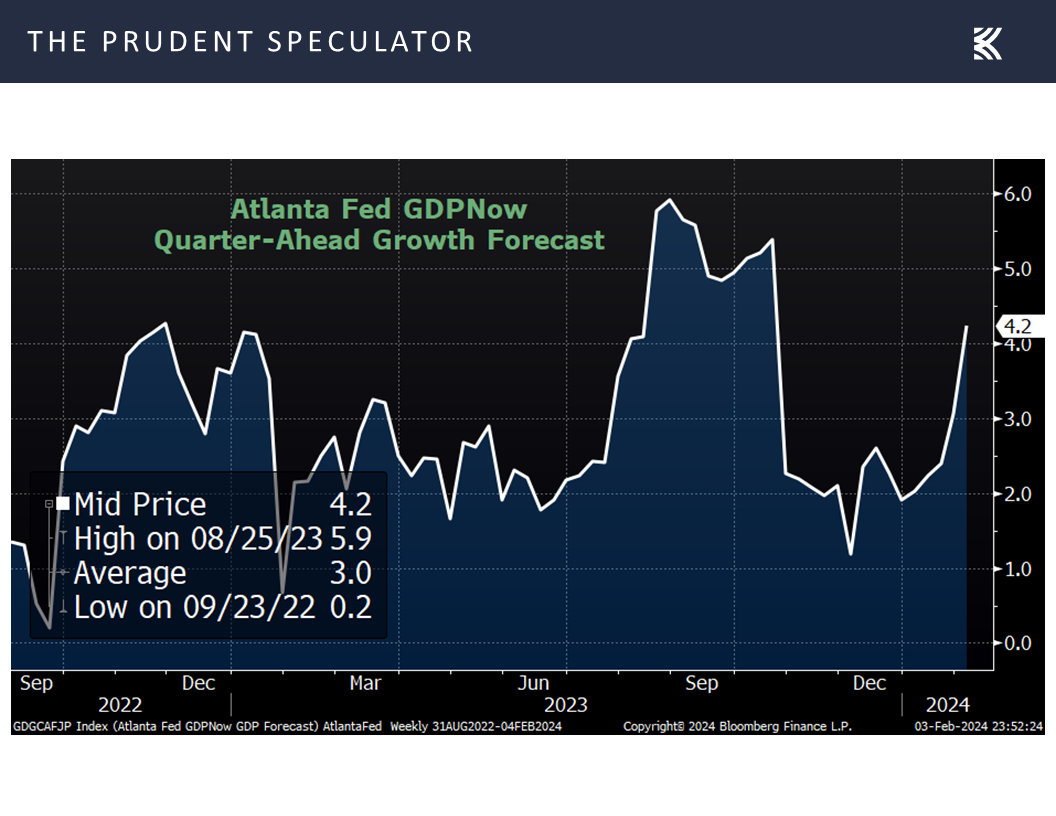

Not surprisingly, the continued stream of stronger economic figures saw the latest estimate from the Atlanta Fed for Q1 real (inflation-adjusted) GDP growth rise to a stellar 4.2% last week,

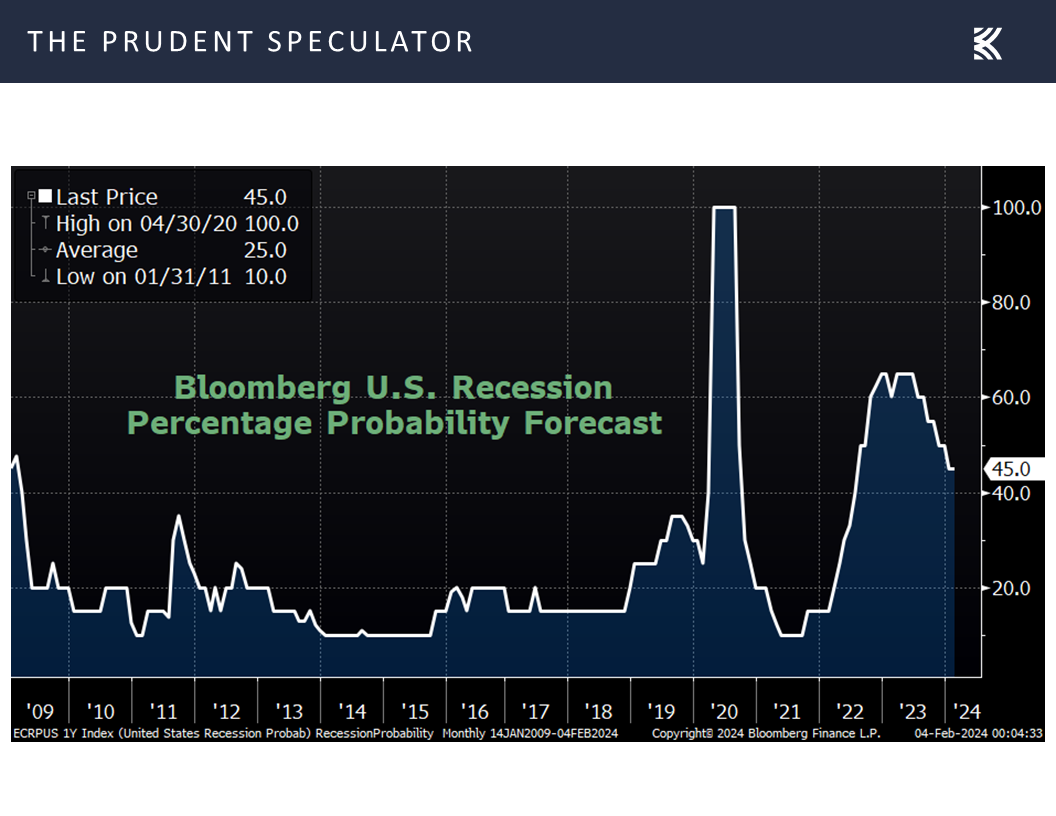

even as the odds of recession in the next 12 months, per tabulations from Bloomberg, remained at an elevated 45%.

Earnings – Solid Q4 Numbers

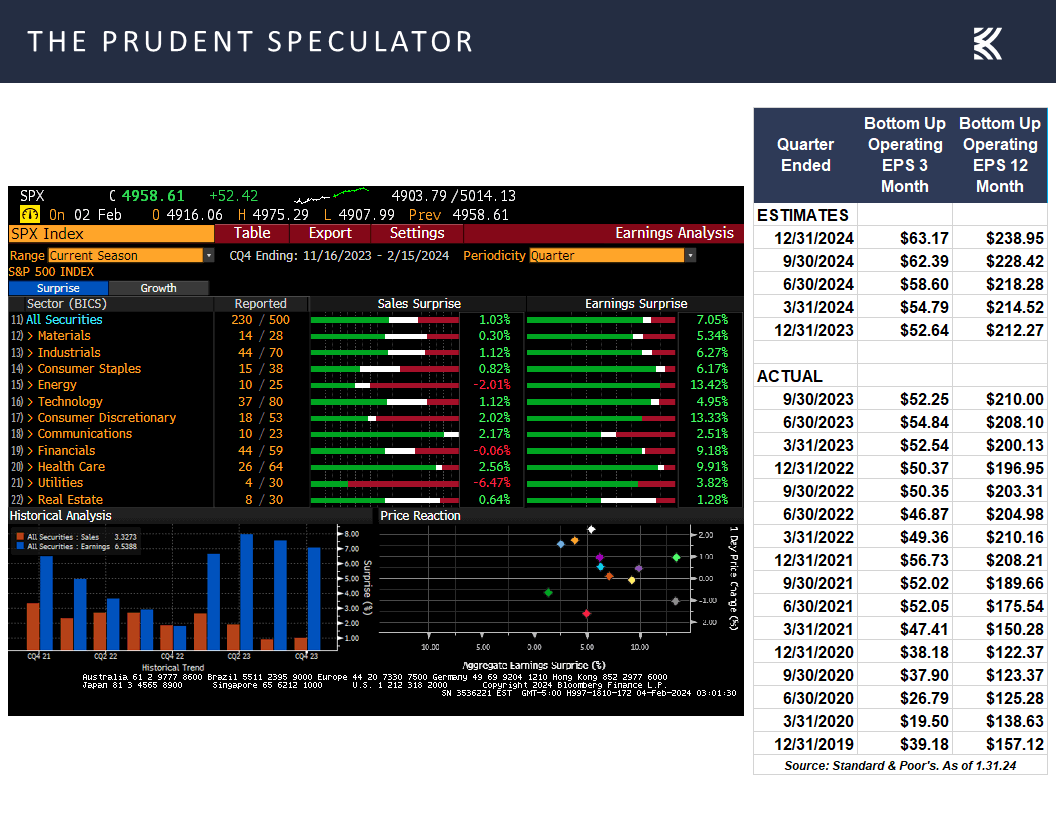

It is hard to complain about a healthier economy, given that Q4 corporate profit reports, on average, have been good (true, some of the stock price reactions to the numbers have not been great) and the outlook for the balance of 2024 is for solid bottom-line growth,

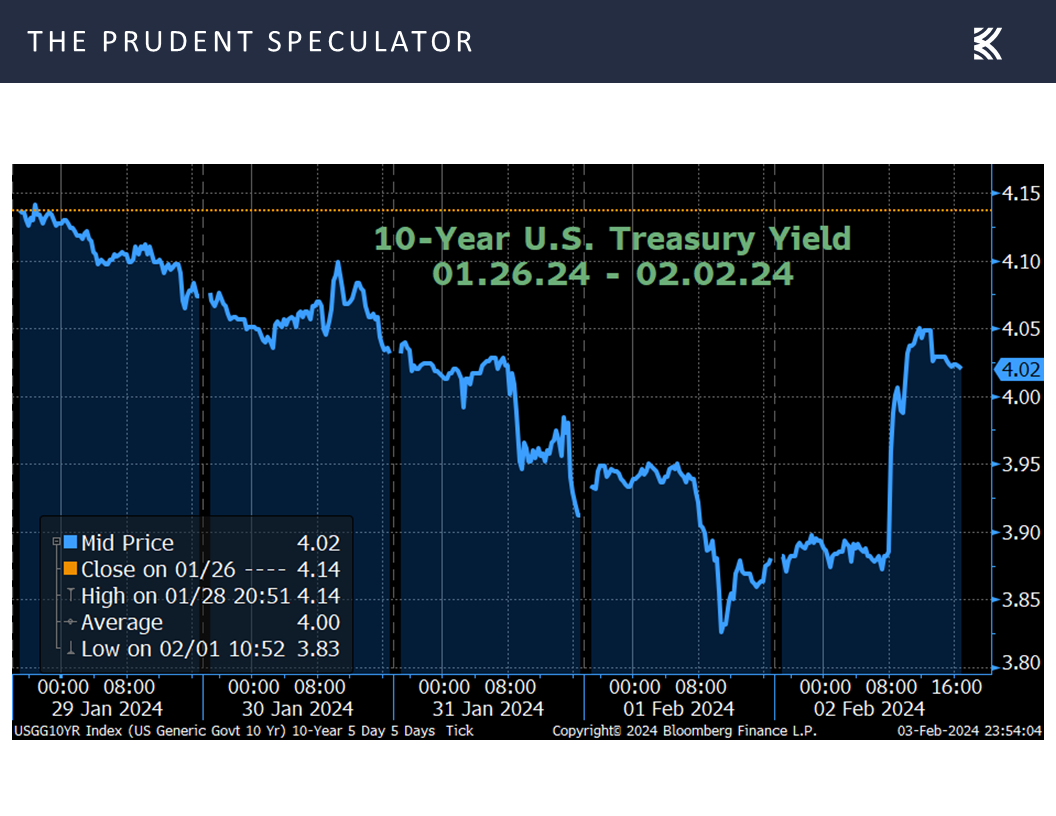

especially as the yield on the benchmark U.S. long-term government bond declined last week,

adding to the valuation argument for Value stocks in general,

Valuations – Value Stocks Attractively Priced

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular.

So, while we wouldn’t be surprised to see a little pullback after the big gains the last two days in the major market average and the sizable advance since October 27 in the average stock, and we know that there are still plenty of disconcerting geopolitical headlines, we see no reason to deviate from our long-held focus on the generous long-term rewards offered by equities.

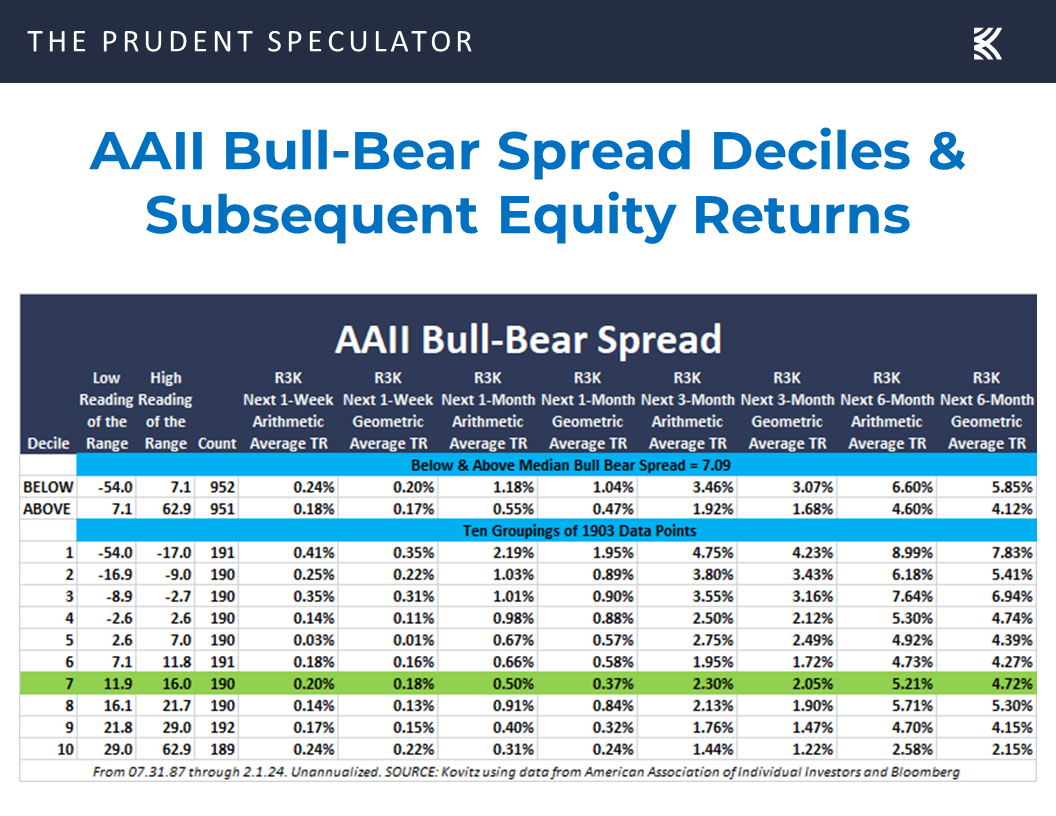

Sentiment – AAII More Optimistic

True, those with a contrarian bent may have some newfound concerns, given the jump in optimism in the latest AAII Bull-Bear Sentiment Survey,

but history shows positive short-term equity returns, on average, no matter the Bull-Bear Spread decile.

Stock News – Updates on twelve stocks across eight different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Federal Reserve, Economy, Earnings, Valuations and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Federal Reserve, Economy, Earnings, Valuations and more news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – A Buy and Two Sells

All-Time Highs – Despite Ups and Downs, Stocks Have Proved Rewarding Over the Long Term

Fed – First Interest Rate Cut Not Likely to Happen in March

Economy – Strong Jobs Numbers

Earnings – Solid Q4 Numbers

Valuations – Value Stocks Attractively Priced

Sentiment – AAII More Optimistic

Stock News – Updates on PHG, GLW, GOOG, BHE, ETN, MRK, CAH, GEN, META, AAPL & CVX

All-Time Highs – Despite Ups and Downs, Stocks Have Proved Rewarding Over the Long Term

Certainly, prices could have moved lower still back then as corrections and Bear Markets are a normal part of the investment process, but as has occurred following every other setback, rallies and Bull Markets have taken place. Gains from those advances have dwarfed the declines, so much so that long-term returns on Value Stocks have exceeded 13% per annum since the launch of The Prudent Speculator nearly 47 years ago.

Fed – First Interest Rate Cut Not Likely to Happen in March

Of course, there have been plenty of scary selloffs along the way, with one of those downturns (1.6% tumble on the S&P 500) taking place this past Wednesday, following the Federal Reserve’s latest decision on interest rates. As expected, Jerome H. Powell & Co. left the target for the Fed Funds rate unchanged at a range of 5.25% to 5.50%,

and offered a relatively upbeat economic outlook in the accompanying FOMC statement,

but Chair Powell said at the Press Conference following the decision on rates, “I don’t think it’s likely the committee will reach a level of confidence by the time of the March meeting, but that’s to be seen,” as he dampened expectations of a Fed Funds rate cut at the next FOMC get-together. The first cut, per the Fed Funds futures market, is now expected at the May meeting, while the year-end rate moved up to 4.07% from 3.99% the week prior.

We do not think delaying the start of the easing cycle is unreasonable, given that the Fed in December forecast a year-end 2024 Fed Funds rate of 4.6%,

Economy – Strong Jobs Numbers

while Mr. Powell at his post-Fed-decision press conference stated: “Recent indicators suggest that economic activity has been expanding at a solid pace. GDP growth in the fourth quarter of last year came in at 3.3 percent. For 2023 as a whole, GDP expanded at 3.1 percent, bolstered by strong consumer demand as well as improving supply conditions. Activity in the housing sector was subdued over the past year, largely reflecting high mortgage rates. High interest rates also appear to have been weighing on business fixed investment.”

He also offered an assessment of the employment situation: “The labor market remains tight, but supply and demand conditions continue to come into better balance. Over the past three months, payroll job gains averaged 165 thousand jobs per month, a pace that is well below that seen a year ago but still strong. The unemployment rate remains low, at 3.7 percent. Strong job creation has been accompanied by an increase in the supply of workers: The labor force participation rate has moved up on balance over the past year, particularly for individuals aged 25 to 54 years, and immigration has returned to pre-pandemic levels. Nominal wage growth has been easing, and job vacancies have declined. Although the jobs-to-workers gap has narrowed, labor demand still exceeds the supply of available workers.”

And those comments came prior to the monthly jobs report out on Friday in which there were far more new payrolls (353,000) created than expected,

with the unemployment rate holding steady at 3.7%, also better than the 3.8% projection.

We learned, too, that average hourly earnings ticked up 4.5% in December, higher than estimated,

while consumer confidence, per the Conference Board,

and consumer sentiment, per the Univ. of Michigan, maintained an upward trajectory.

Finally, the important ISM Manufacturing Index (PMI) eclipsed projections with a rise to 49.1 in January, up from 47.1 in December, with the keeper of the index stating, “A Manufacturing PMI® above 42.5 percent, over a period of time, generally indicates an expansion of the overall economy. Therefore, the January Manufacturing PMI® indicates the overall economy grew for the 45th straight month after one month of contraction (April 2020). The past relationship between the Manufacturing PMI® and the overall economy indicates that the January reading (49.1 percent) corresponds to a change of plus-1.9 percent in real gross domestic product (GDP) on an annualized basis.”

Not surprisingly, the continued stream of stronger economic figures saw the latest estimate from the Atlanta Fed for Q1 real (inflation-adjusted) GDP growth rise to a stellar 4.2% last week,

even as the odds of recession in the next 12 months, per tabulations from Bloomberg, remained at an elevated 45%.

Earnings – Solid Q4 Numbers

It is hard to complain about a healthier economy, given that Q4 corporate profit reports, on average, have been good (true, some of the stock price reactions to the numbers have not been great) and the outlook for the balance of 2024 is for solid bottom-line growth,

especially as the yield on the benchmark U.S. long-term government bond declined last week,

adding to the valuation argument for Value stocks in general,

Valuations – Value Stocks Attractively Priced

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular.

So, while we wouldn’t be surprised to see a little pullback after the big gains the last two days in the major market average and the sizable advance since October 27 in the average stock, and we know that there are still plenty of disconcerting geopolitical headlines, we see no reason to deviate from our long-held focus on the generous long-term rewards offered by equities.

Sentiment – AAII More Optimistic

True, those with a contrarian bent may have some newfound concerns, given the jump in optimism in the latest AAII Bull-Bear Sentiment Survey,

but history shows positive short-term equity returns, on average, no matter the Bull-Bear Spread decile.

Stock News – Updates on twelve stocks across eight different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.