The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Federal Reserve Meeting, Inflation, Valuations and Historical Evidence. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Week in Review – Big Headlines Make for Volatile 5 Trading Days

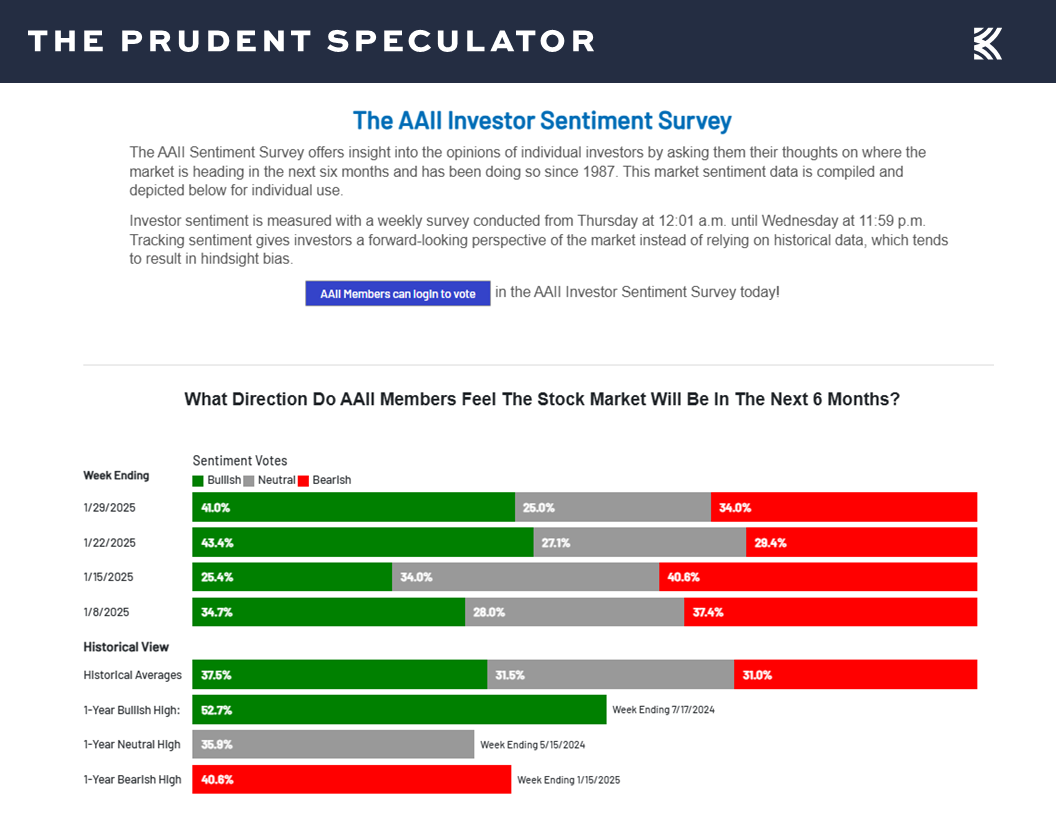

Sentiment – Traders Often Zig When They Should Have Zagged

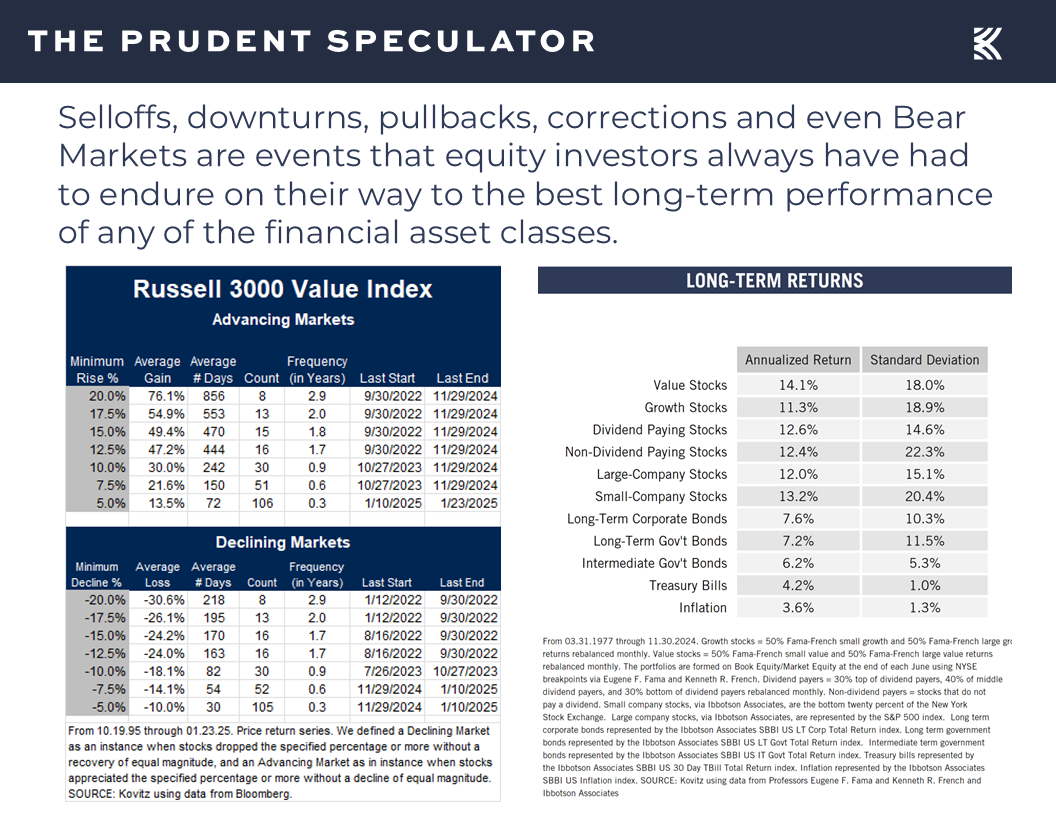

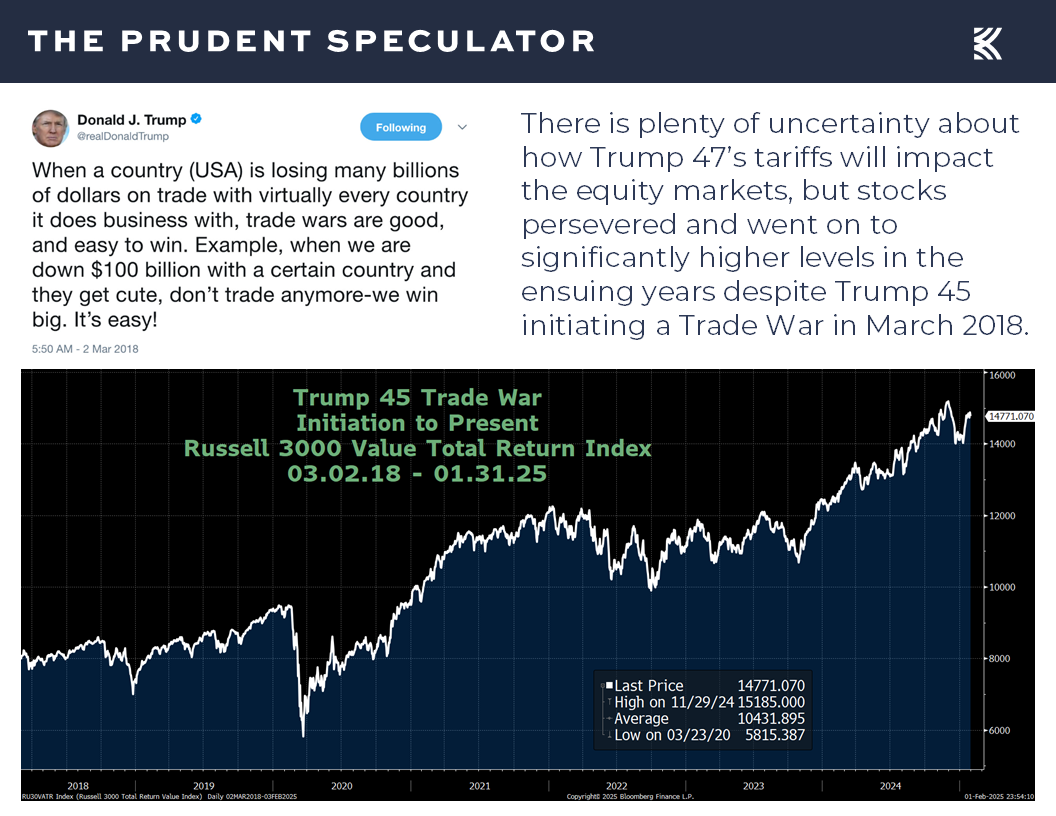

Historical Evidence – Markets Overcame Trump 45 Tariffs…and Everything Else in the Fullness of Time

Valuations – Value Stocks Remain Reasonably Priced

Econ Outlook – Solid Real U.S. GDP Growth Projected for 2025

Fed Meeting – Fed Funds Rate Holds Steady; Powell & Co. Still Data-Dependent

Inflation – PCE Numbers as Expected

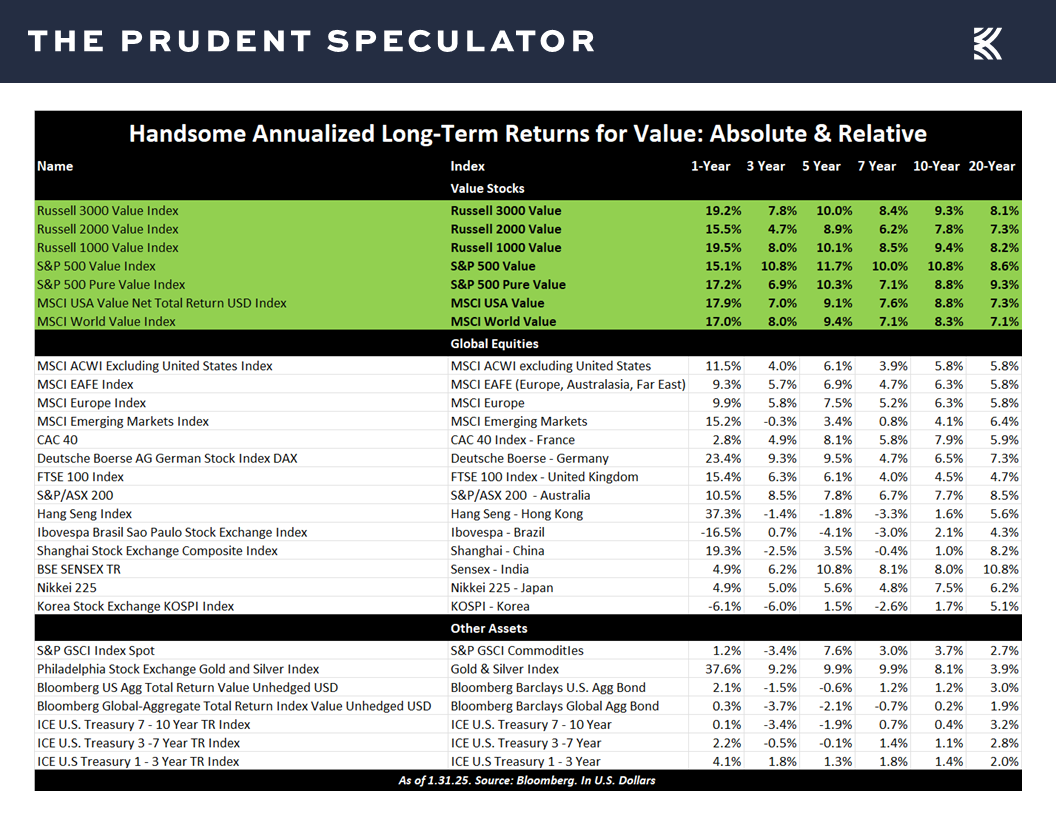

Staying the Course – Value has Produced Handsome Returns Over the Past Two Decades

Stock News – Updates on fourteen stocks across eight different sectors

Week in Review – Big Headlines Make for Volatile 5 Trading Days

From DeepSeek to the Fed to a Deadly Air Collision to Tariffs, it was an extraordinary week of news that made for a more-wild-than-usual equity market roller-coaster ride,

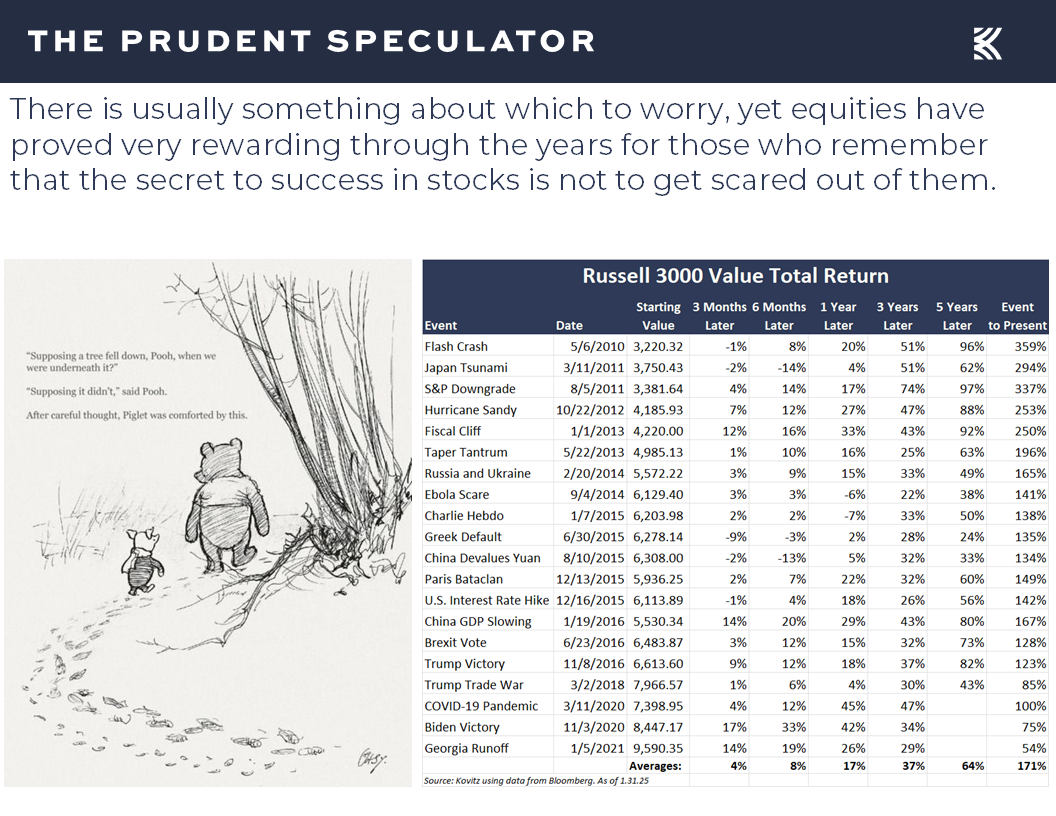

with the major market averages giving back a portion of the gains posted over the preceding two weeks, though they still turned in a terrific month of January and reminded again that while downside volatility is always part of the investment equation, handsome rewards have accrued to those who remember that the secret to success in stocks is not to get scared out of them.

Sentiment – Traders Often Zig When They Should Have Zagged

Keeping on an even keel is easier said than done as folks were pessimistic heading into the middle-of-January’s big advance and optimistic prior to last week’s downturn,

Historical Evidence – Markets Overcame Trump 45 Tariffs…and Everything Else in the Fullness of Time

illustrating why we say the only problem with market timing is getting the timing right.

We will have more to say on DeepSeek in the February edition of The Prudent Speculator, but it does not alter our favorable long-term view of our A.I.-exposed companies, such as data center plays Digital Realty (DLR – $163.86) and Eaton Corp (ETN – $326.44), service and solutions providers Hewlett Packard Enterprise (HPE – $21.19) and Oracle (ORCL – $170.06) and chipmakers Broadcom (AVGO – $221.27) and Micron Tech (MU – $91.24), all of which were hit hard last week.

Still, we understand that there is plenty of near-term uncertainty in Tech Land, especially with China also being slapped with tariffs. Of course, we have been down the Trump tariff road before, and the right course of action then was to stick with our broadly diversified portfolios of what we believe to be undervalued stocks,

as has been the case for every disconcerting event over the last 15 years, with near-term weakness always overcome in the fullness of time,

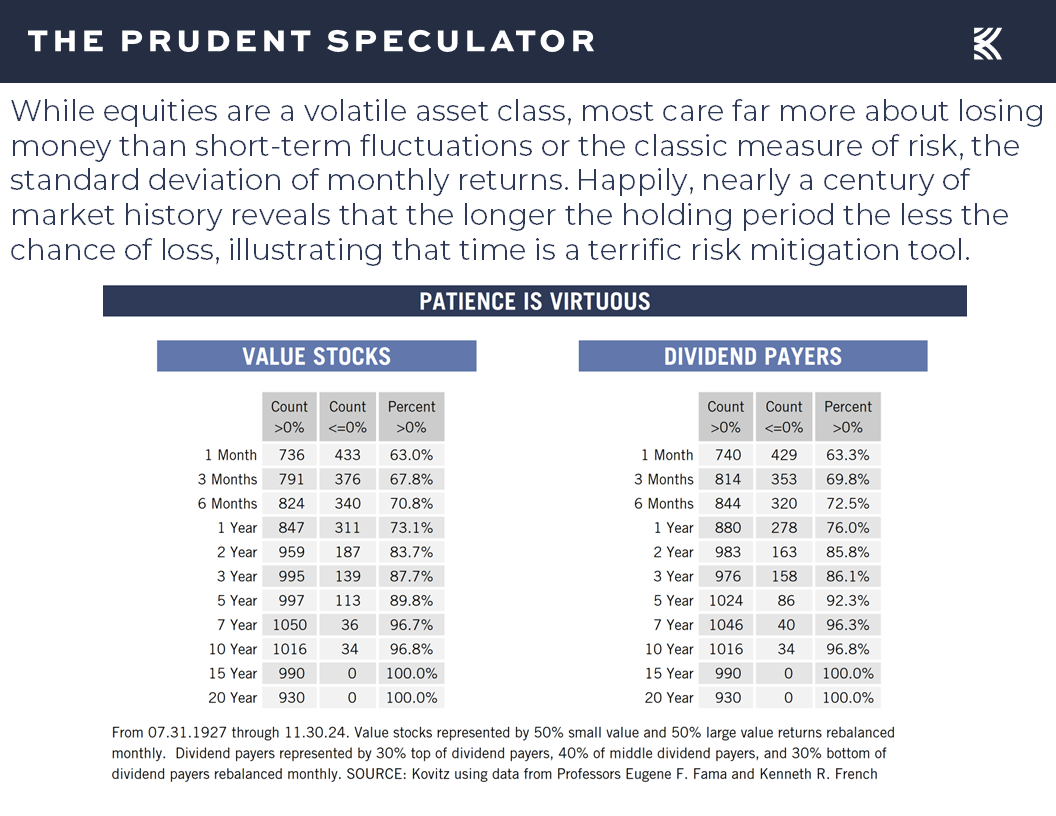

validating the historical evidence that shows the longer stocks are held, the less the chance of losing money.

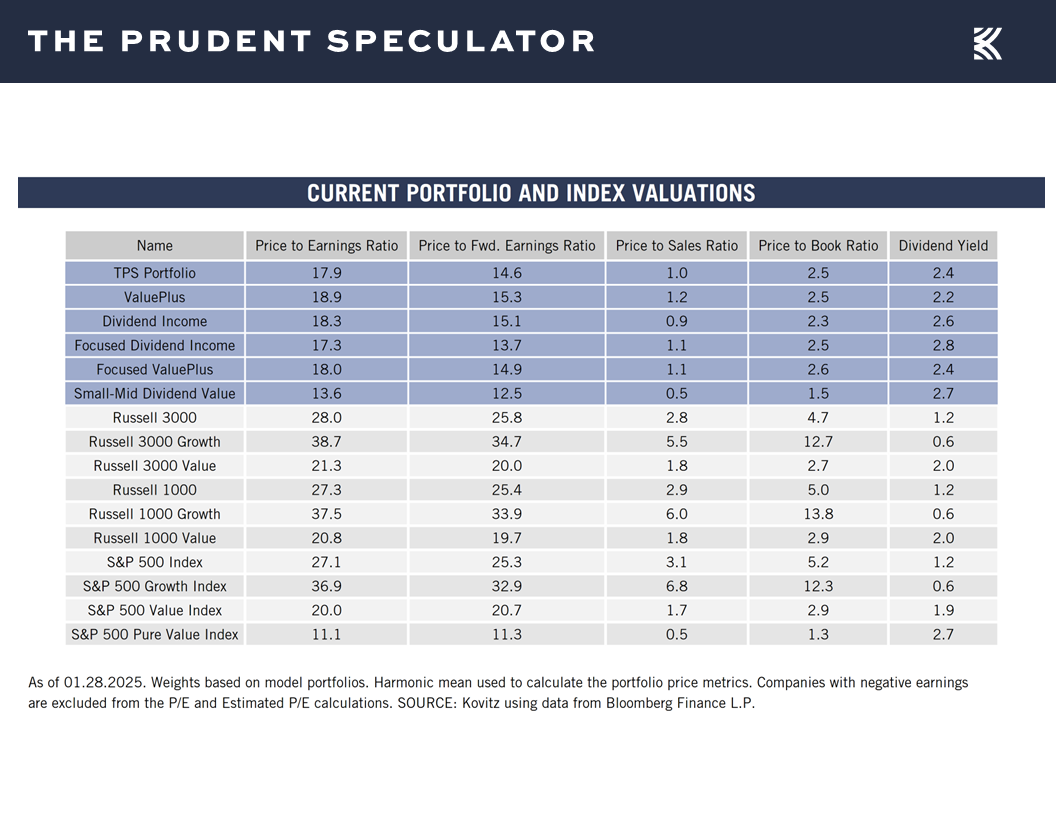

Valuations – Value Stocks Remain Reasonably Priced

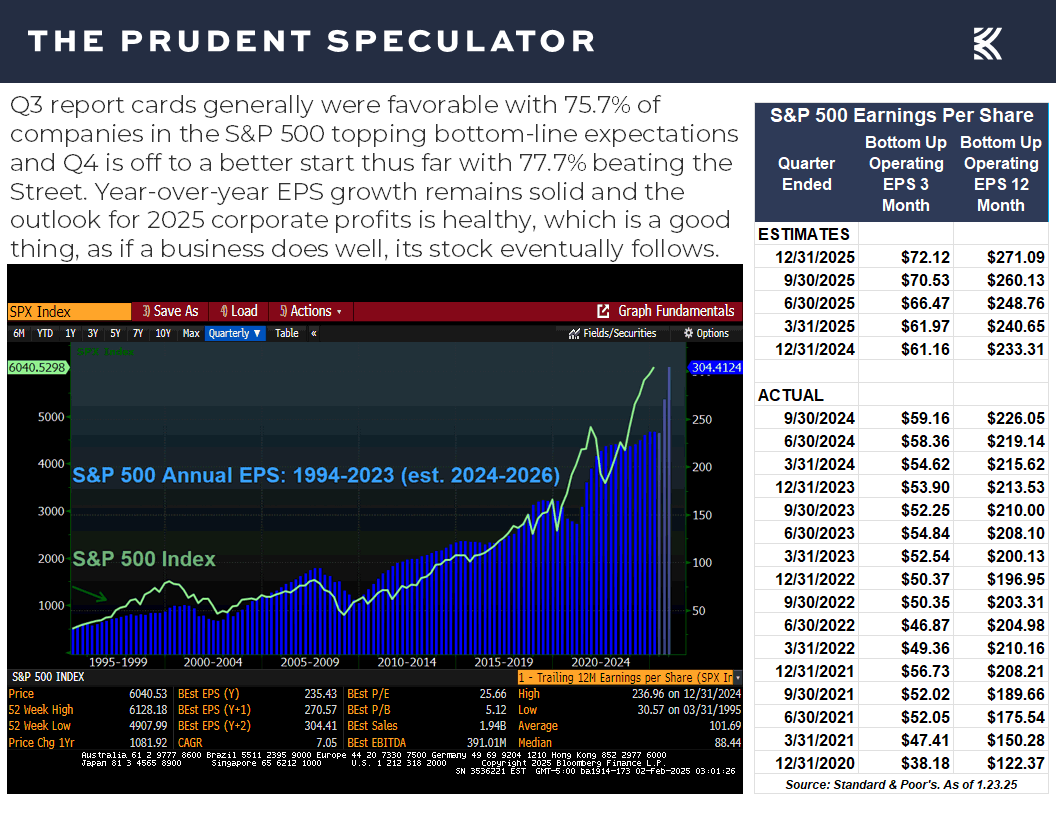

Certainly, we have to be braced for a continuation of the selling in the near term, as currently robust estimates for corporate profit growth are likely to come down on tariff worries,

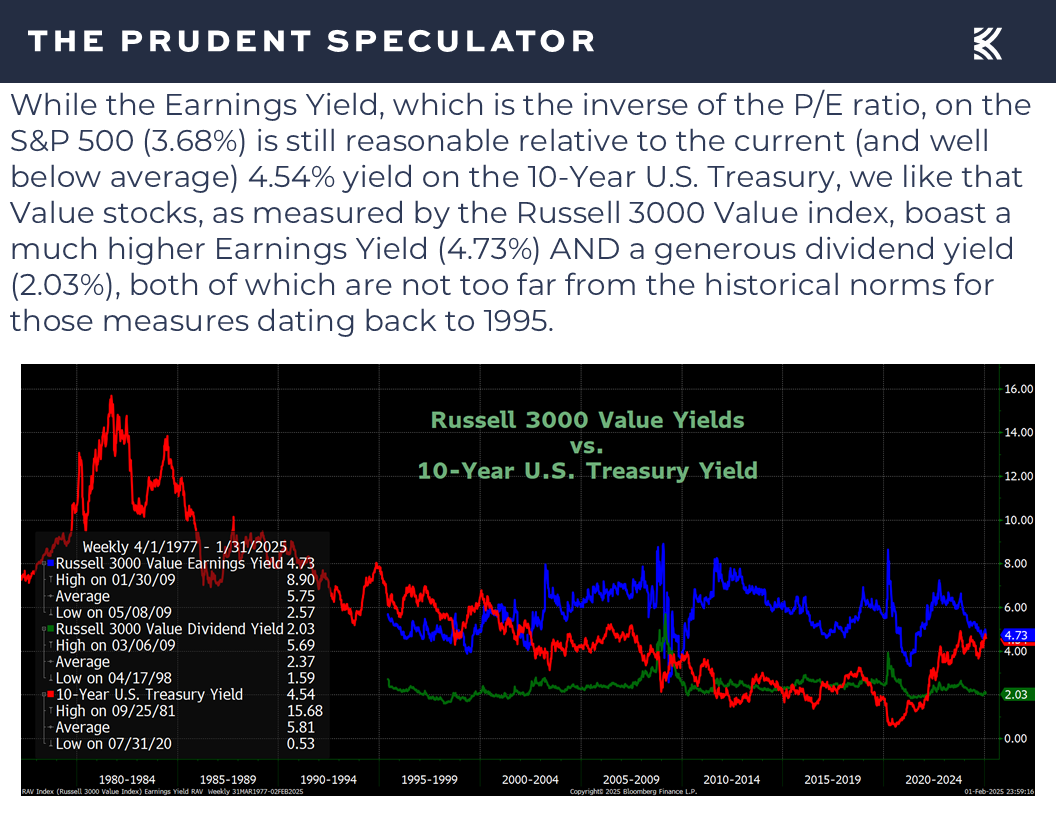

but we remain very comfortable with the reasonable valuations for Value stocks in general,

and the even-more inexpensive price metrics and higher dividend yields for our portfolios.

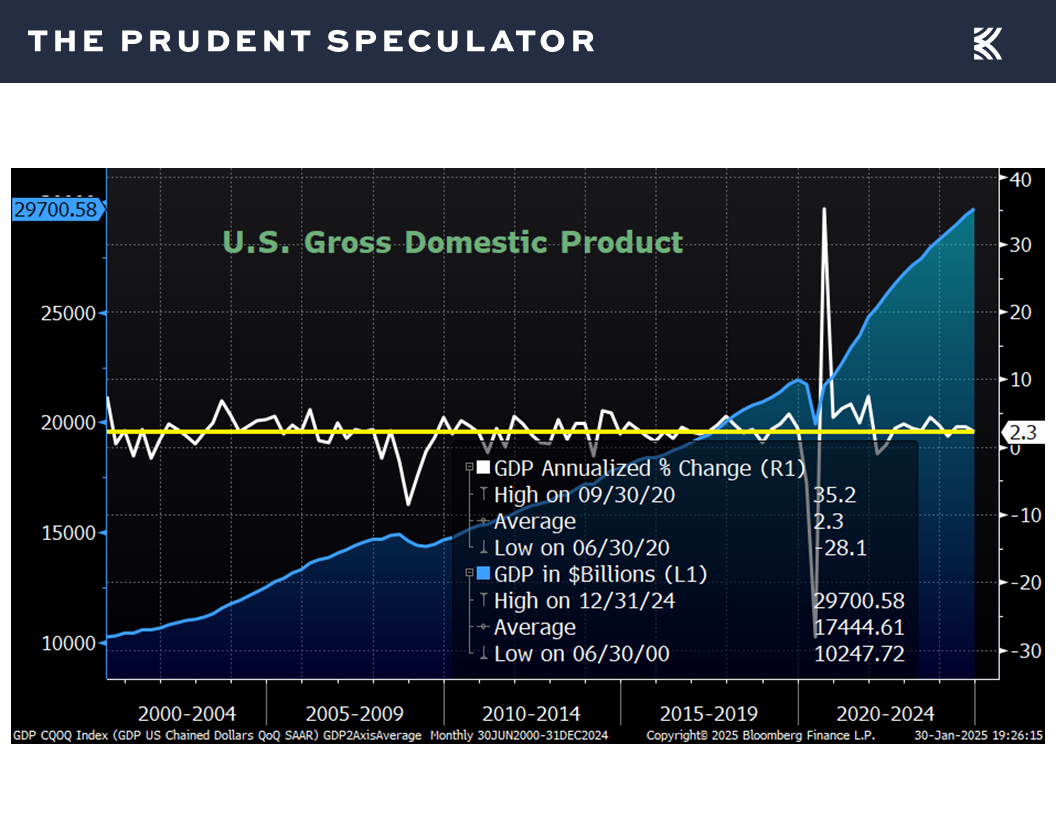

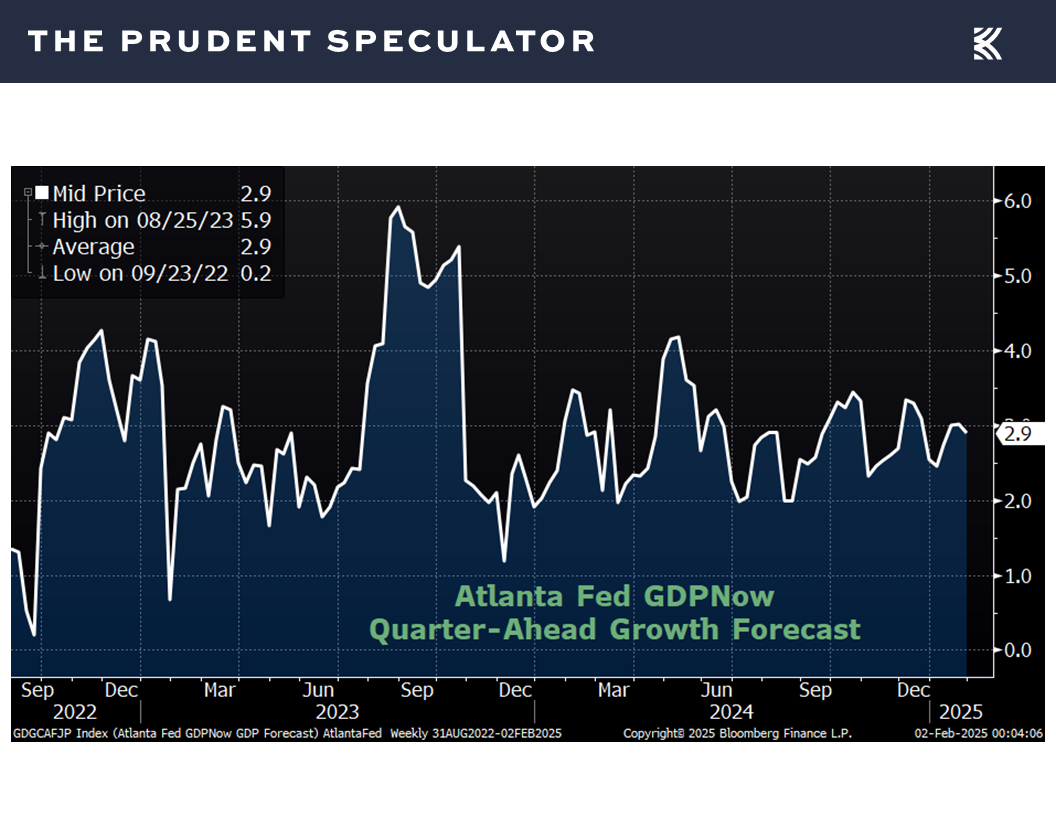

Econ Outlook – Solid Real U.S. GDP Growth Projected for 2025

We also note that the U.S. economy is on solid footing today, with the first estimate last week for Q4 2024 real (inflation-adjusted) GDP growth coming in at 2.3%,

the latest projection for Q1 2025 real GDP growth from the Atlanta Fed standing at 2.9%,

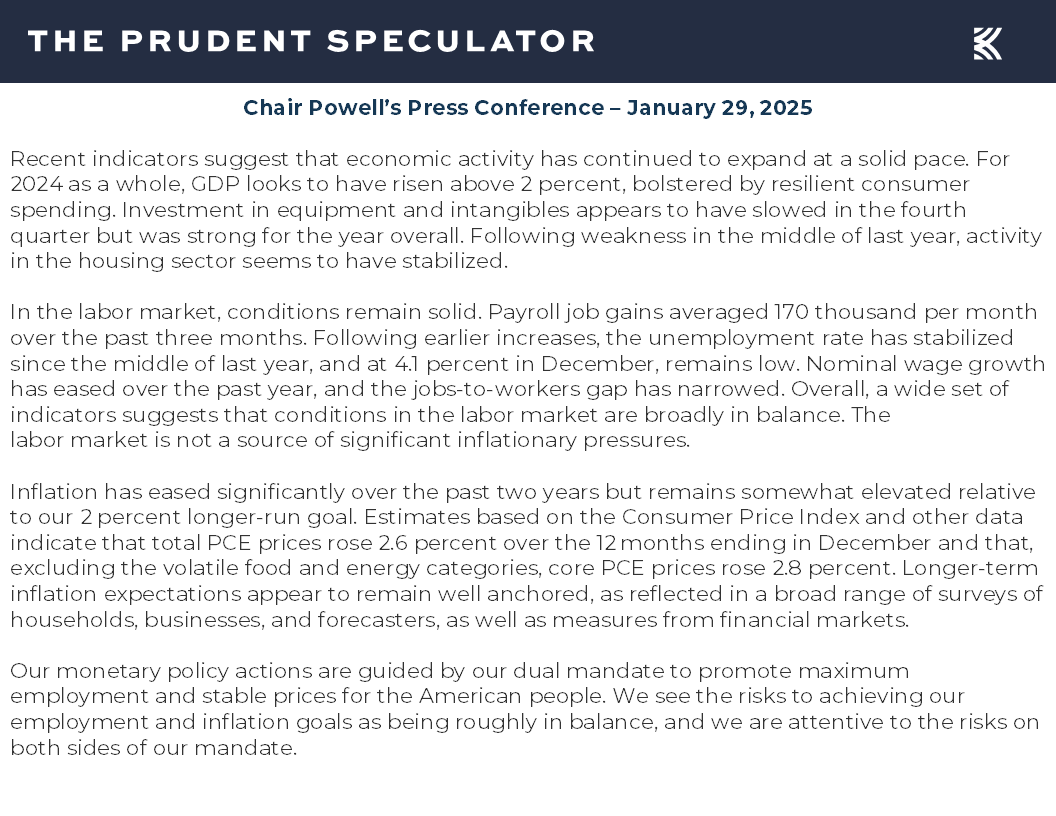

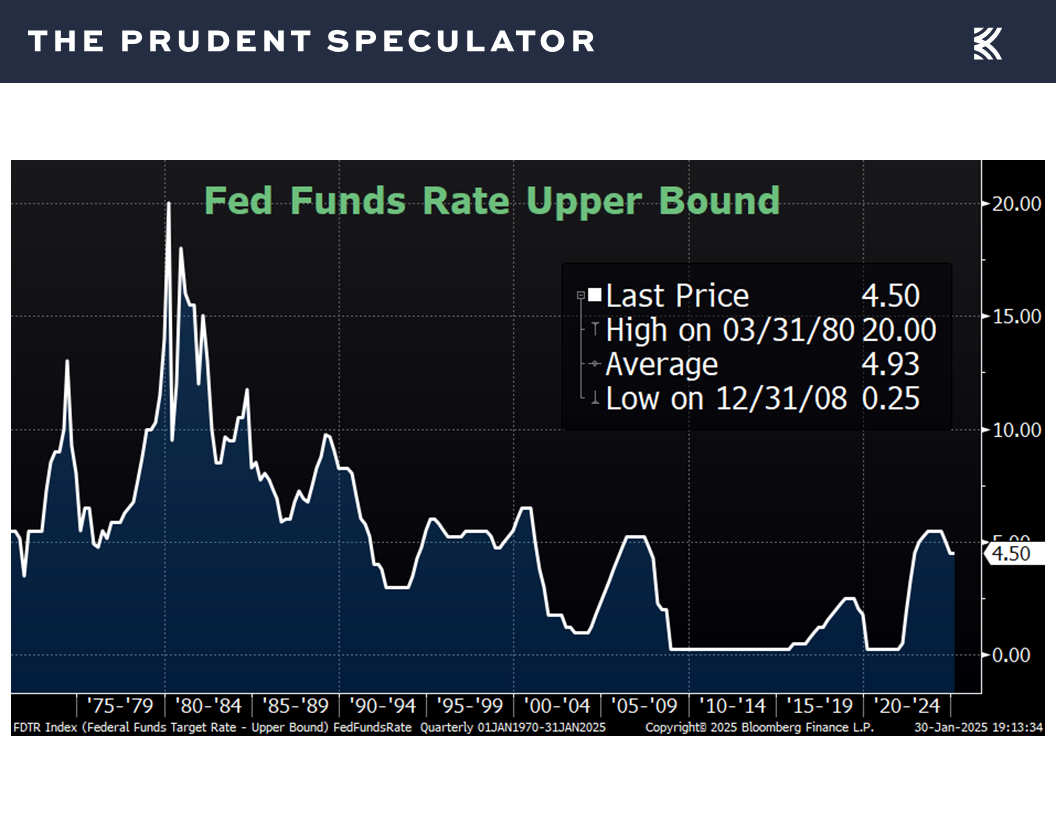

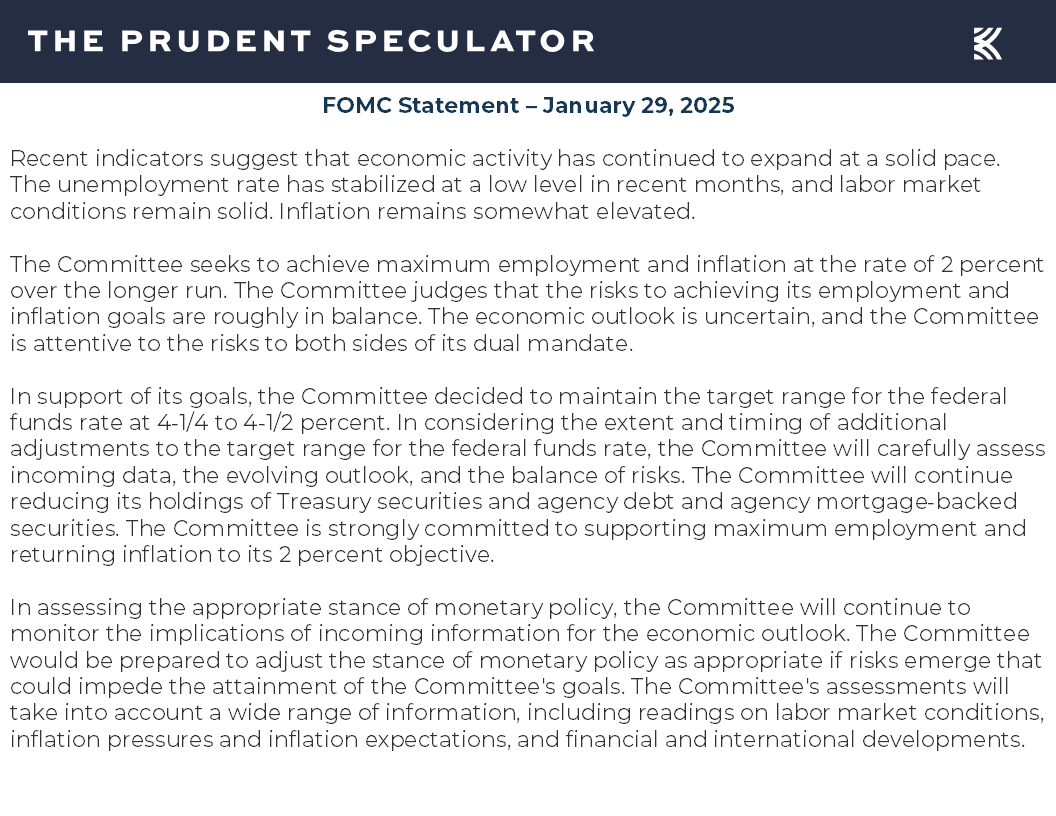

Fed Meeting – Fed Funds Rate Holds Steady; Powell & Co. Still Data-Dependent

and Jerome H. Powell sounding relatively upbeat in his economic assessment this past Wednesday.

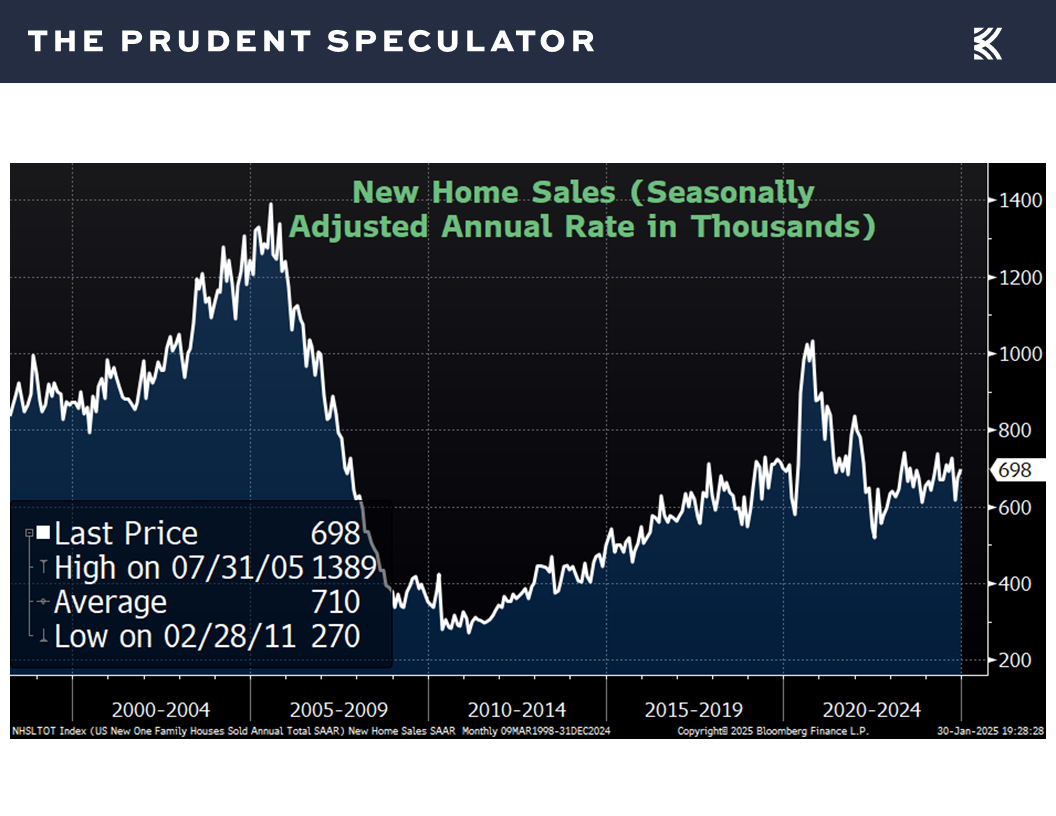

The Federal Reserve Chair’s comments about stability in the housing market were seemingly supported by a better-than-expected read in December on new home sales,

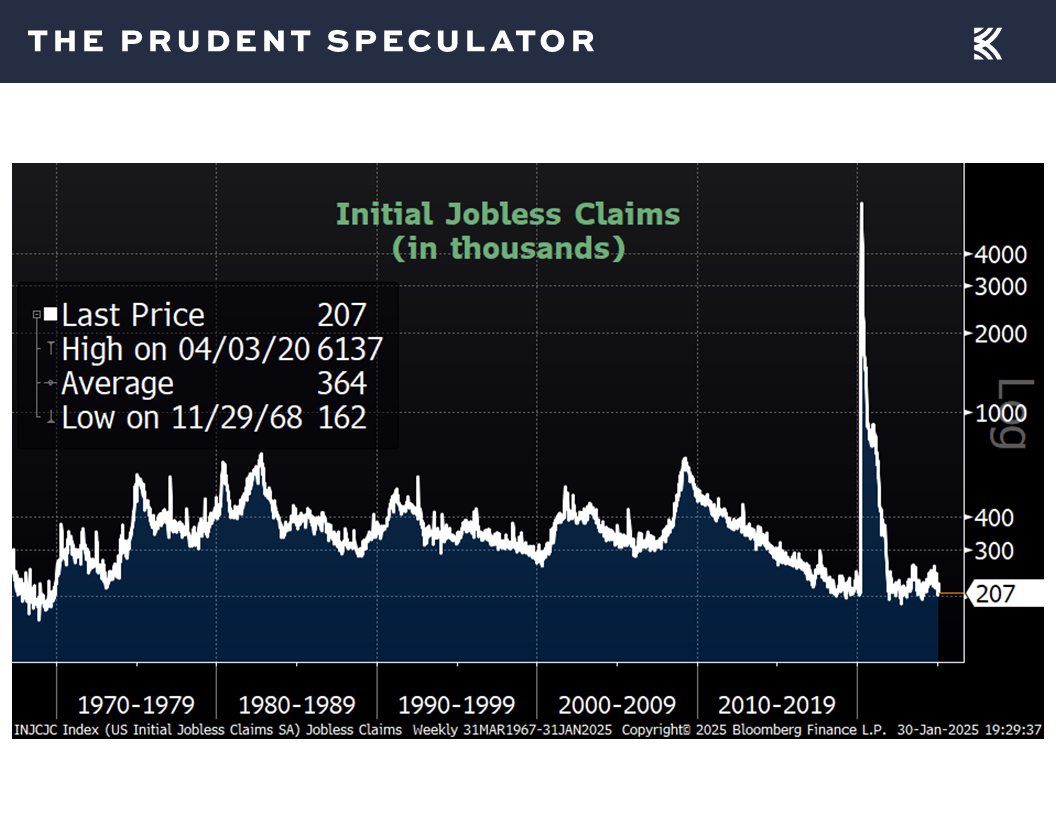

and his positivity on the labor situation was bolstered by a drop in weekly first-time filings for unemployment benefits to a very low 207,000.

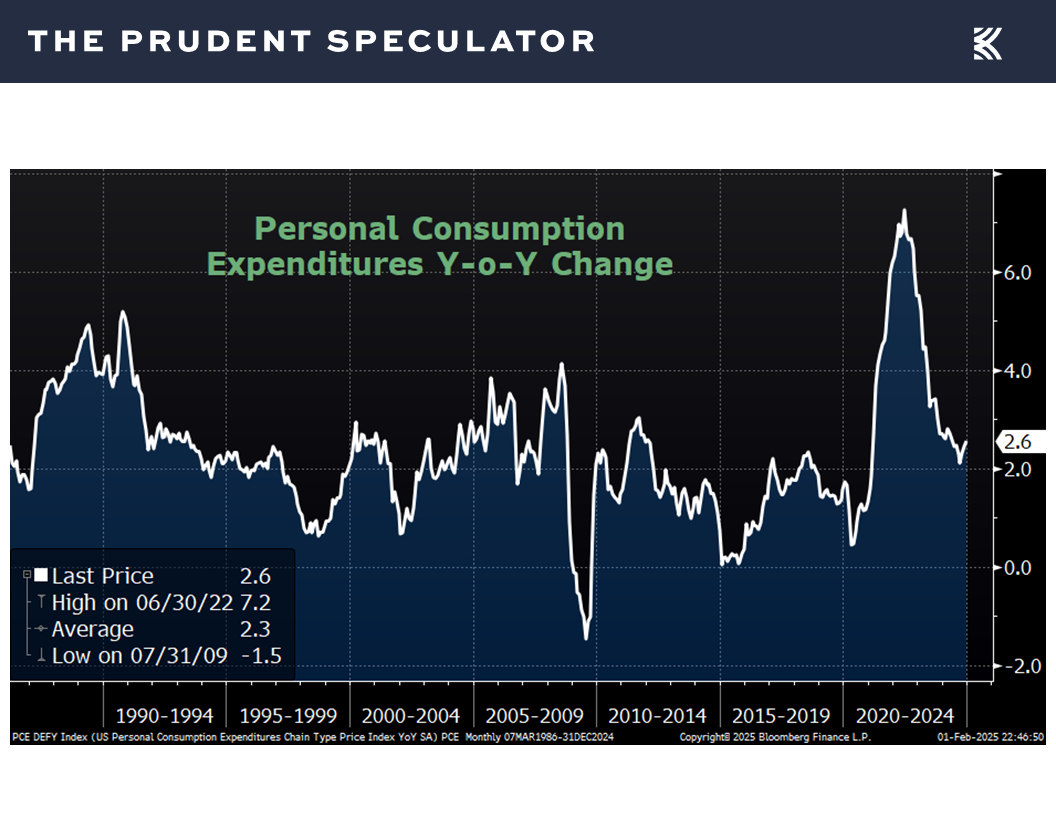

To be sure, the Fed is equally focused on the inflation equation, and numbers out late last week matched expectations, with the personal consumption expenditure index (PCE) rising 2.6% on a year-over-year basis in December,

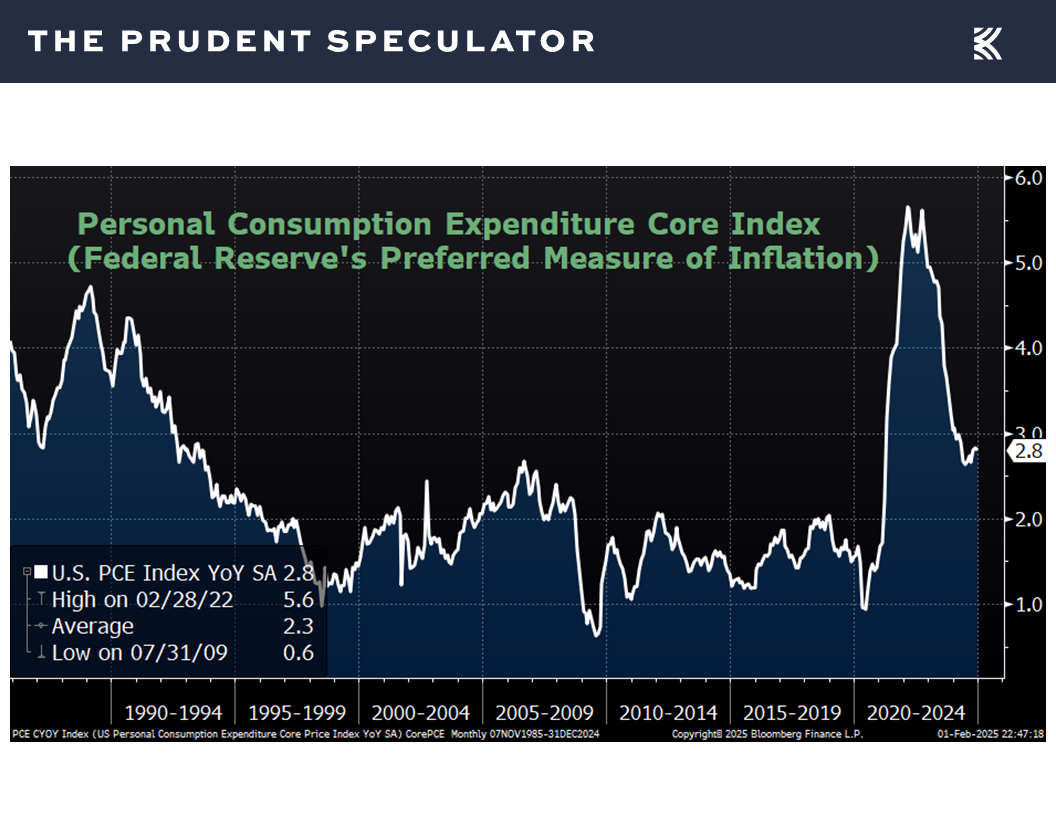

and the Fed’s preferred measure, the Core PCE, which includes volatile food and energy prices, climbing 2.8%, also on a year-over-year basis.

The Fed has a dual mandate of maximizing employment while maintaining price stability, so we shall see how tariffs might impact both sides, but Powell & Co. chose to leave the target for the Fed Funds rate unchanged at a range of 4.25% to 4.5% last week,

while suggesting that risks to its employment and inflation goals are “roughly in balance,”

Inflation – PCE Numbers as Expected

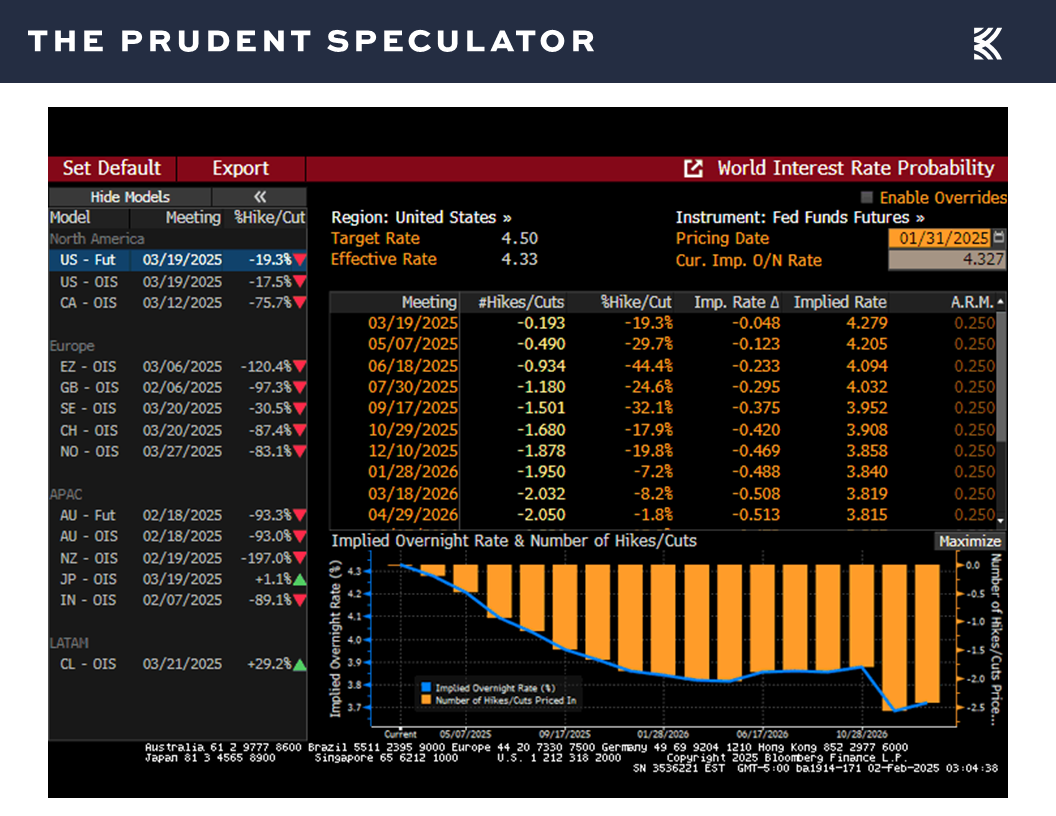

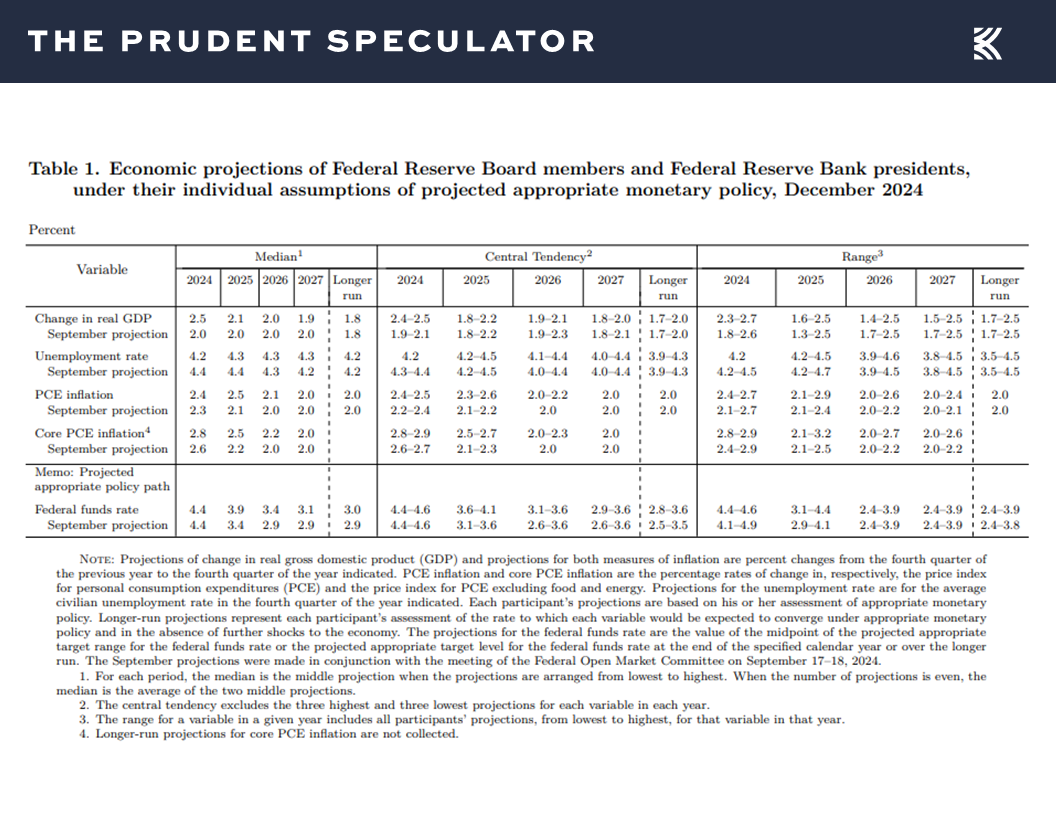

with market expectations for the year-end-2025 Fed Funds rate of 3.86%,

still in line with the projections offered in December by Federal Reserve members and Federal Reserve Bank presidents.

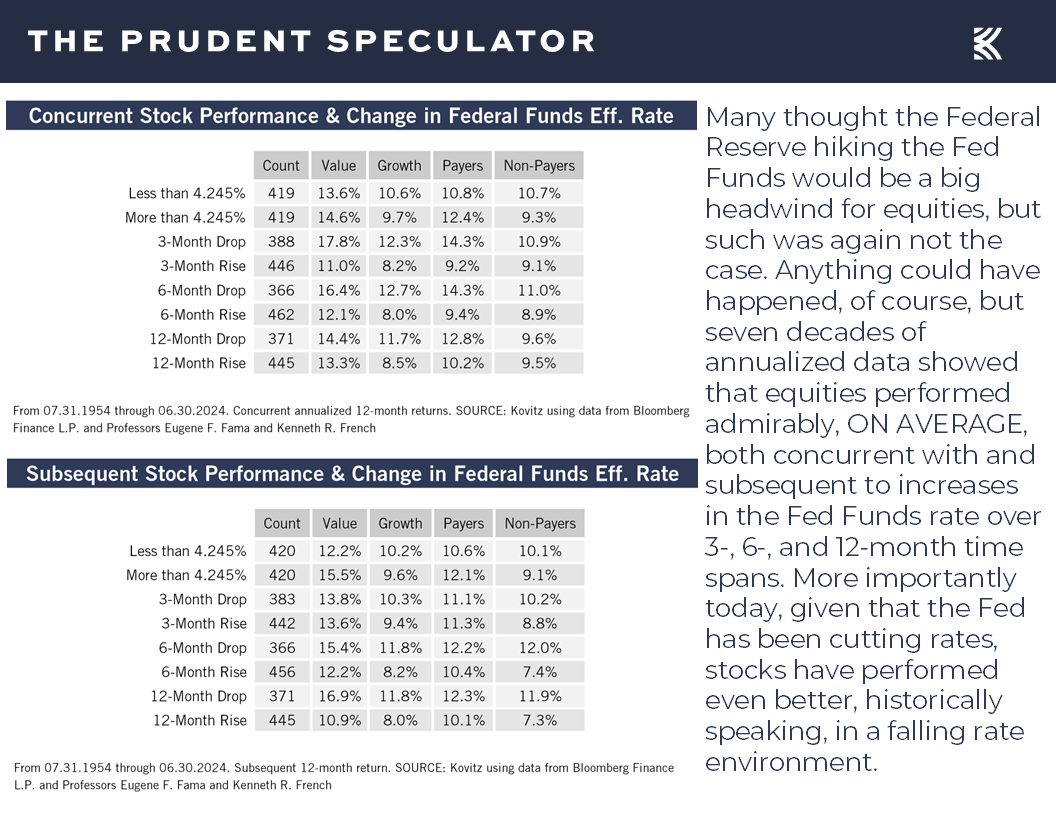

True, lower interest rates, all things equal, should make stocks even more attractive, but equities have performed fine, on average, over the last seven decades whether the Fed Funds rate has been falling or rising.

Staying the Course – Value has Produced Handsome Returns Over the Past Two Decades

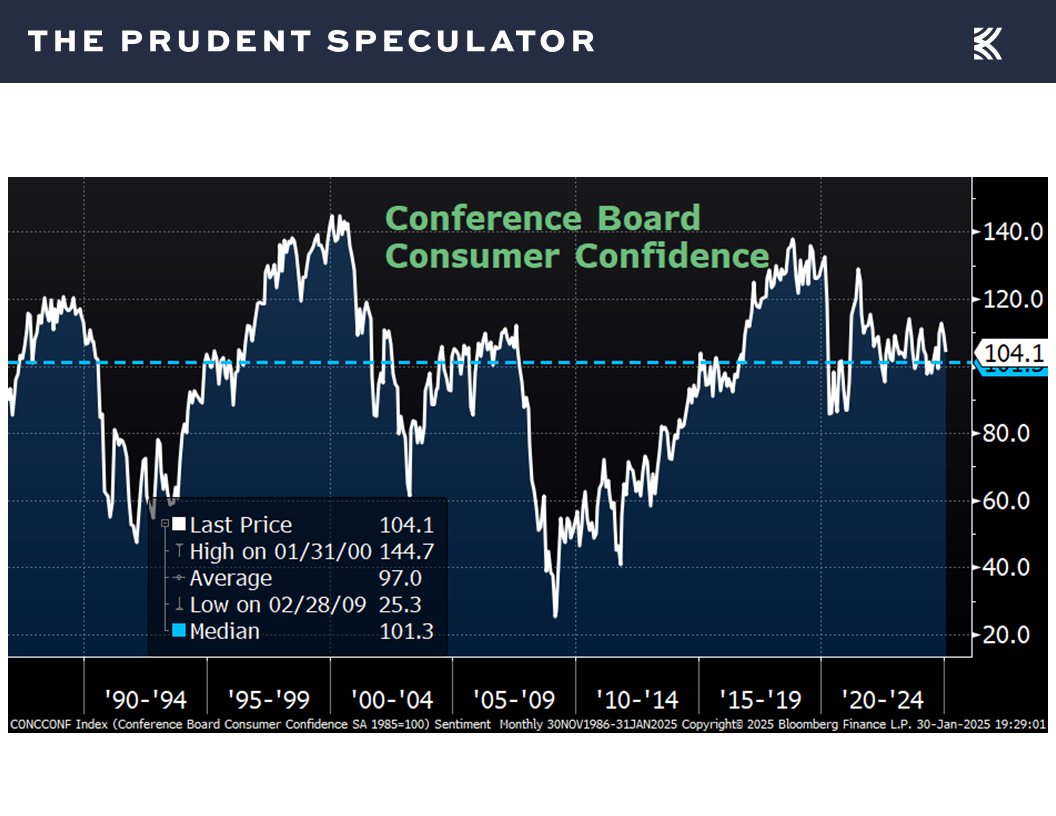

So, while we realize that consumer confidence retreated in January to a weaker-than-expected level of 104.1,

and the equity futures are suggesting equities are in for rough sledding when trading resumes today, we continue to believe that inexpensively priced stocks will provide solid returns as has been the case across the last two decades.

Stock News – Updates on fourteen stocks across eight different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Federal Reserve Meeting, Inflation, Valuations and Historical Evidence

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Federal Reserve Meeting, Inflation, Valuations and Historical Evidence. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Week in Review – Big Headlines Make for Volatile 5 Trading Days

Sentiment – Traders Often Zig When They Should Have Zagged

Historical Evidence – Markets Overcame Trump 45 Tariffs…and Everything Else in the Fullness of Time

Valuations – Value Stocks Remain Reasonably Priced

Econ Outlook – Solid Real U.S. GDP Growth Projected for 2025

Fed Meeting – Fed Funds Rate Holds Steady; Powell & Co. Still Data-Dependent

Inflation – PCE Numbers as Expected

Staying the Course – Value has Produced Handsome Returns Over the Past Two Decades

Stock News – Updates on fourteen stocks across eight different sectors

Week in Review – Big Headlines Make for Volatile 5 Trading Days

From DeepSeek to the Fed to a Deadly Air Collision to Tariffs, it was an extraordinary week of news that made for a more-wild-than-usual equity market roller-coaster ride,

with the major market averages giving back a portion of the gains posted over the preceding two weeks, though they still turned in a terrific month of January and reminded again that while downside volatility is always part of the investment equation, handsome rewards have accrued to those who remember that the secret to success in stocks is not to get scared out of them.

Sentiment – Traders Often Zig When They Should Have Zagged

Keeping on an even keel is easier said than done as folks were pessimistic heading into the middle-of-January’s big advance and optimistic prior to last week’s downturn,

Historical Evidence – Markets Overcame Trump 45 Tariffs…and Everything Else in the Fullness of Time

illustrating why we say the only problem with market timing is getting the timing right.

We will have more to say on DeepSeek in the February edition of The Prudent Speculator, but it does not alter our favorable long-term view of our A.I.-exposed companies, such as data center plays Digital Realty (DLR – $163.86) and Eaton Corp (ETN – $326.44), service and solutions providers Hewlett Packard Enterprise (HPE – $21.19) and Oracle (ORCL – $170.06) and chipmakers Broadcom (AVGO – $221.27) and Micron Tech (MU – $91.24), all of which were hit hard last week.

Still, we understand that there is plenty of near-term uncertainty in Tech Land, especially with China also being slapped with tariffs. Of course, we have been down the Trump tariff road before, and the right course of action then was to stick with our broadly diversified portfolios of what we believe to be undervalued stocks,

as has been the case for every disconcerting event over the last 15 years, with near-term weakness always overcome in the fullness of time,

validating the historical evidence that shows the longer stocks are held, the less the chance of losing money.

Valuations – Value Stocks Remain Reasonably Priced

Certainly, we have to be braced for a continuation of the selling in the near term, as currently robust estimates for corporate profit growth are likely to come down on tariff worries,

but we remain very comfortable with the reasonable valuations for Value stocks in general,

and the even-more inexpensive price metrics and higher dividend yields for our portfolios.

Econ Outlook – Solid Real U.S. GDP Growth Projected for 2025

We also note that the U.S. economy is on solid footing today, with the first estimate last week for Q4 2024 real (inflation-adjusted) GDP growth coming in at 2.3%,

the latest projection for Q1 2025 real GDP growth from the Atlanta Fed standing at 2.9%,

Fed Meeting – Fed Funds Rate Holds Steady; Powell & Co. Still Data-Dependent

and Jerome H. Powell sounding relatively upbeat in his economic assessment this past Wednesday.

The Federal Reserve Chair’s comments about stability in the housing market were seemingly supported by a better-than-expected read in December on new home sales,

and his positivity on the labor situation was bolstered by a drop in weekly first-time filings for unemployment benefits to a very low 207,000.

To be sure, the Fed is equally focused on the inflation equation, and numbers out late last week matched expectations, with the personal consumption expenditure index (PCE) rising 2.6% on a year-over-year basis in December,

and the Fed’s preferred measure, the Core PCE, which includes volatile food and energy prices, climbing 2.8%, also on a year-over-year basis.

The Fed has a dual mandate of maximizing employment while maintaining price stability, so we shall see how tariffs might impact both sides, but Powell & Co. chose to leave the target for the Fed Funds rate unchanged at a range of 4.25% to 4.5% last week,

while suggesting that risks to its employment and inflation goals are “roughly in balance,”

Inflation – PCE Numbers as Expected

with market expectations for the year-end-2025 Fed Funds rate of 3.86%,

still in line with the projections offered in December by Federal Reserve members and Federal Reserve Bank presidents.

True, lower interest rates, all things equal, should make stocks even more attractive, but equities have performed fine, on average, over the last seven decades whether the Fed Funds rate has been falling or rising.

Staying the Course – Value has Produced Handsome Returns Over the Past Two Decades

So, while we realize that consumer confidence retreated in January to a weaker-than-expected level of 104.1,

and the equity futures are suggesting equities are in for rough sledding when trading resumes today, we continue to believe that inexpensively priced stocks will provide solid returns as has been the case across the last two decades.

Stock News – Updates on fourteen stocks across eight different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.