The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. This week, we discuss the Federal Reserve Projections, Earnings, Inflation, Recession, AAII Stock Market Sentiment and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Contra-Indicator – AAII Bulls Skid

Wall of Worry – Stock Have Overcome Plenty of Disconcerting News in the Fullness of Time

Federal Reserve News – Disconnect Between Minutes and Press Conference / GDP Projections

Weaker-than-Expected Econ Stats – Retail Sales & Jobless Claims

Better-than-Forecast Econ Numbers – Sentiment & Industrial Production

Earnings – Healthy Corporate Profits in ’23 and ’24 Still the Projection

Inflation – Sharply Lower CPI & PPI

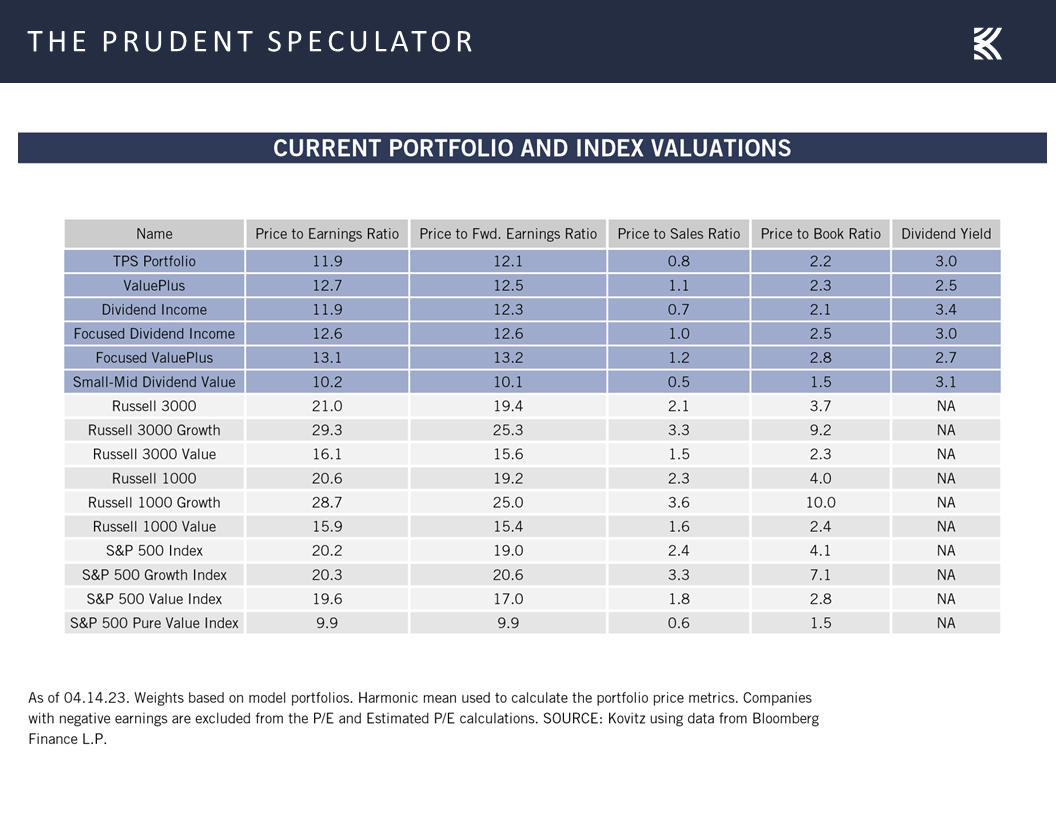

Valuations – Still Liking the Metrics for our Portfolios

Recessions – History Shows No Reason, On Average, for Long-Term-Oriented Investors to Sell Stocks

Stock News – Update on six stocks across six different sectors

Contra-Indicator – AAII Bulls Skid

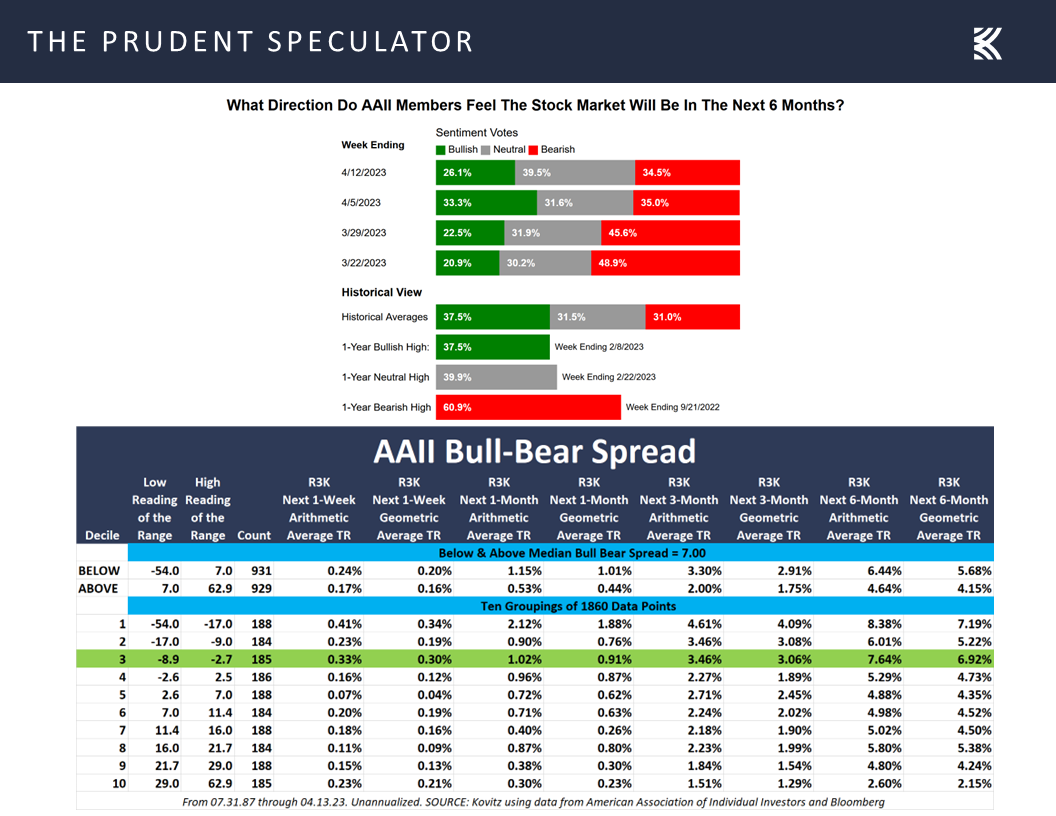

If we were going to blame the pullback during the first week of April on the good folks at the American Association of Individual Investors (AAII) becoming much more optimistic about the prospects for stocks over the ensuing six months, we suppose we should credit last week’s rebound to a renewed sense of pessimism on the contrarian AAII Sentiment gauge. Interestingly, while the AAII tally of Bears edged down 0.5 percentage points to 34.5%, the count of Bulls fell by 7.2 percentage points to 26.1%, with the Bull-Bear spread sinking to -8.4% from -1.7% the week prior.

The number of Bulls is now well below the 37.5% average and the Bears are above the 31.0% average, with forward returns historically better when the AAII Bull-Bear Spread is tilted heavily toward negativity. Certainly, no metric is infallible, but it is fascinating to see 36 years of historical evidence in the chart above confirming that, on average, it often pays to be greedy when others are fearful.

Wall of Worry – Stock Have Overcome Plenty of Disconcerting News in the Fullness of Time

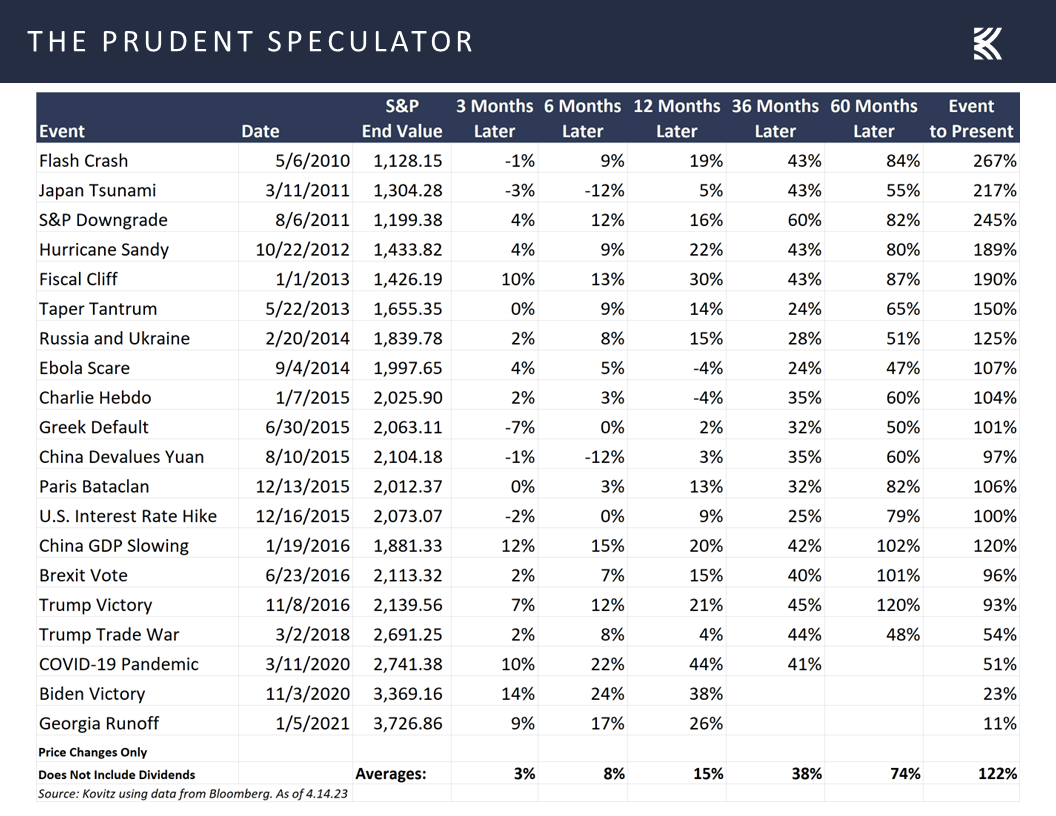

Of course, there usually is something for investors to be concerned about, as evidenced by all the disconcerting events that have occurred just since the end of the Great Financial Crisis in March 2009, yet stocks, in the fullness of time, always seem to manage to climb a wall of worry.

Federal Reserve News – Disconnect Between Minutes and Press Conference / GDP Projections

Speaking of worry, last week’s rebound was interrupted on Wednesday when the Minutes of the FOMC’s March meeting were released. The trouble seemed to be that the Fed staff forecast presented at the meeting anticipated a recession would start later this year due to banking-sector turmoil. However, Jerome H. Powell in his post-meeting Press Conference last month did not state that an economic contraction was his projection.

To be fair, he didn’t say that a recession would not occur, but when asked, “Do you still see a possibility of a soft landing for the U.S. economy,” the Fed Chair responded:

You know it’s, it’s too early to say, really, whether these events have had much of an effect. It’s hard for me to see how they would have helped the possibility—but I guess I would just say, it’s too early to say whether there really have been changes in that. You know, the question will be how long this period is sustained. The longer it’s sustained, then the greater will be the likely declines in—or tightening in credit standards, credit availability, so we’ll just have to see. I do still think, though, that there’s a—there’s a pathway to that. I think that pathway still exists and, you know, we’re certainly trying to find it.

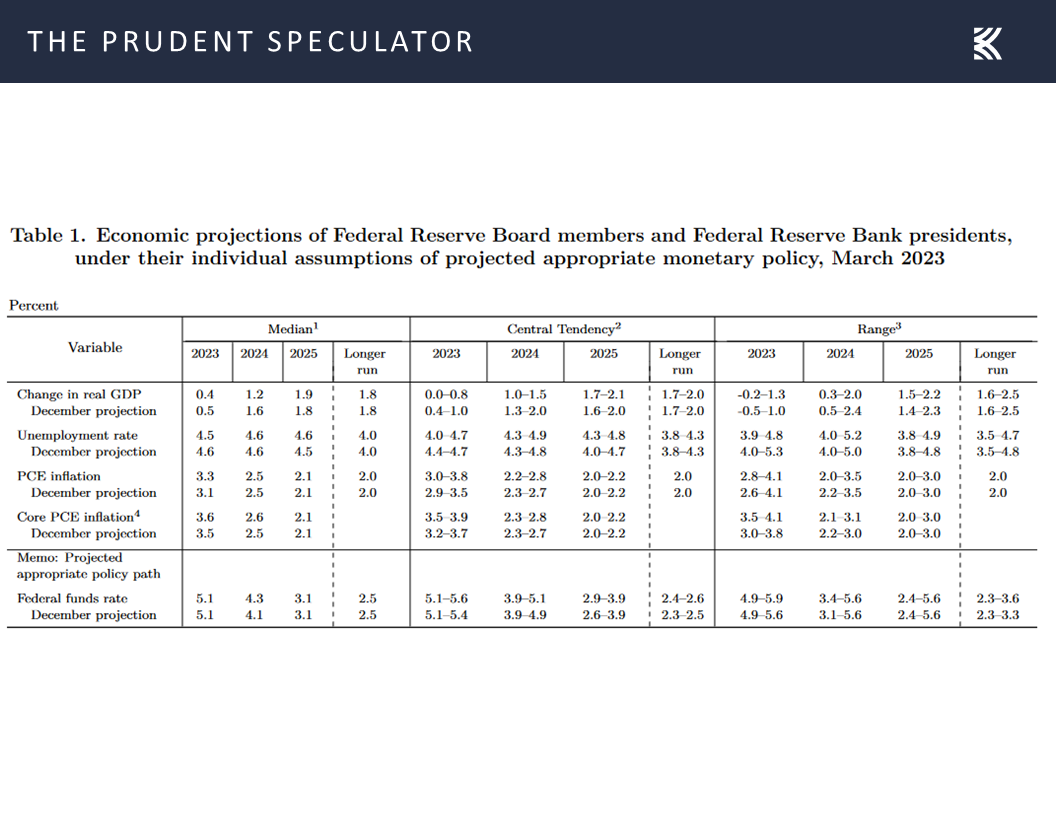

In addition, the economic projections from Federal Reserve Board Members and Federal Reserve Bank Presidents prepared for that Fed Meeting still called for modest real (inflation-adjusted) GDP growth of 0.4% this year and 1.2% in 2024. Yes, those were downgrades to the outlook, but they did not predict a contraction on a year-over-year basis.

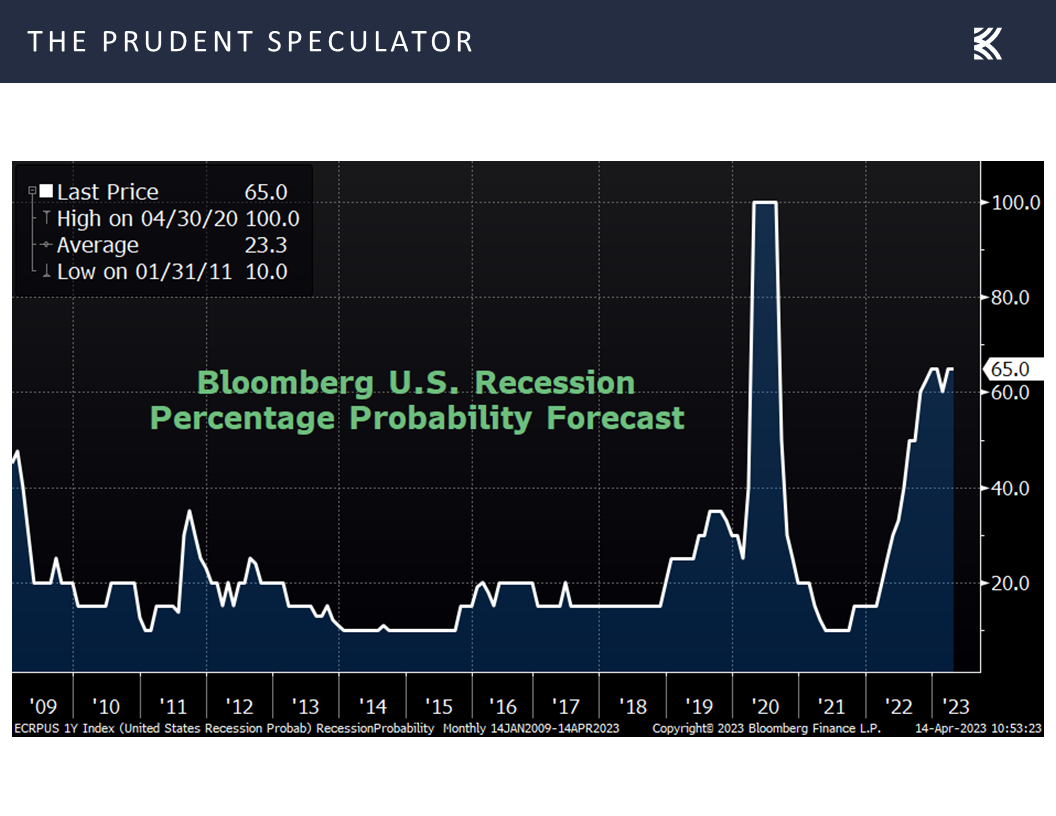

True, Bloomberg calculates that the chance of recession in the next 12 months stands at 65% today,

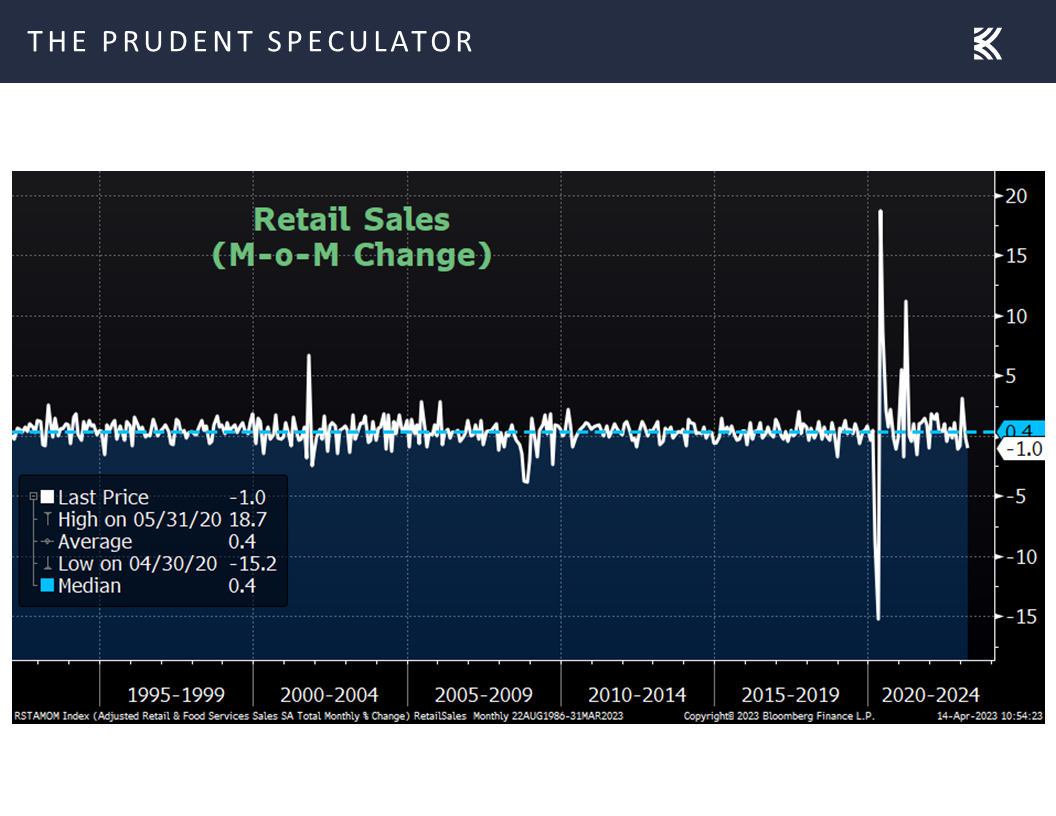

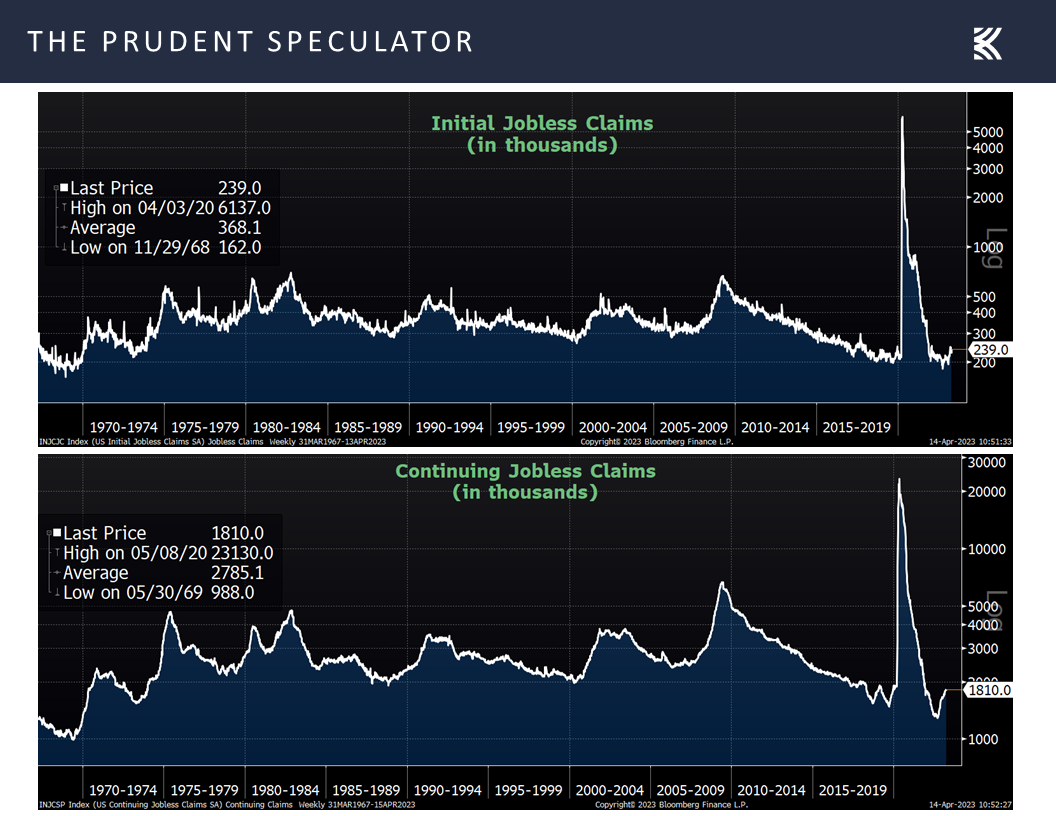

Weaker-than-Expected Econ Stats – Retail Sales & Jobless Claims

with the latest read on retail sales for March coming in below expectations with a 1.0% decline,

and the number of first-time filings for jobless benefits and continuing jobless claims now residing at higher levels than seen in recent months.

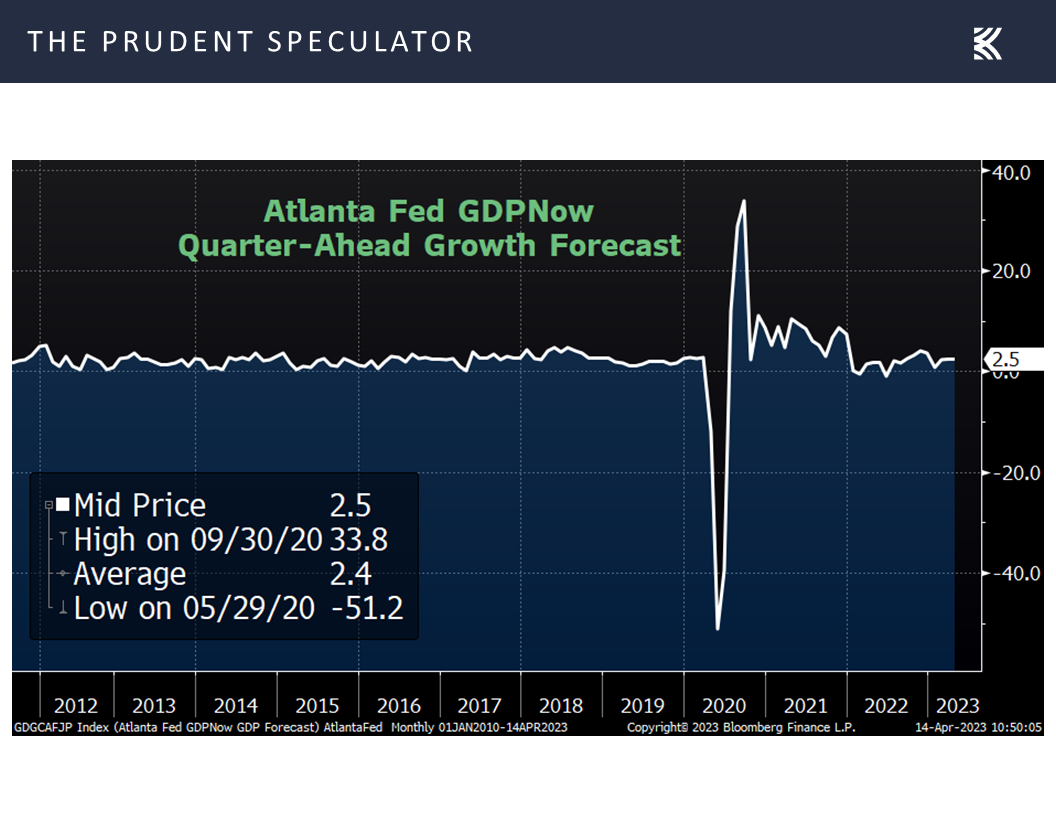

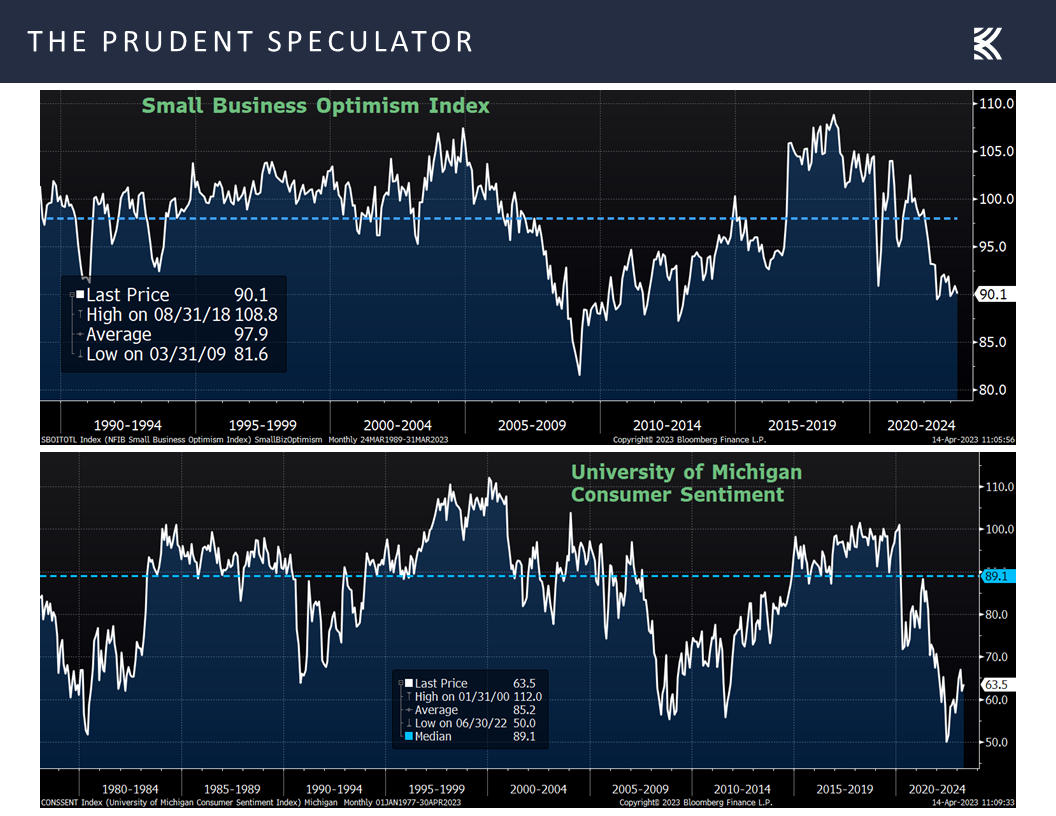

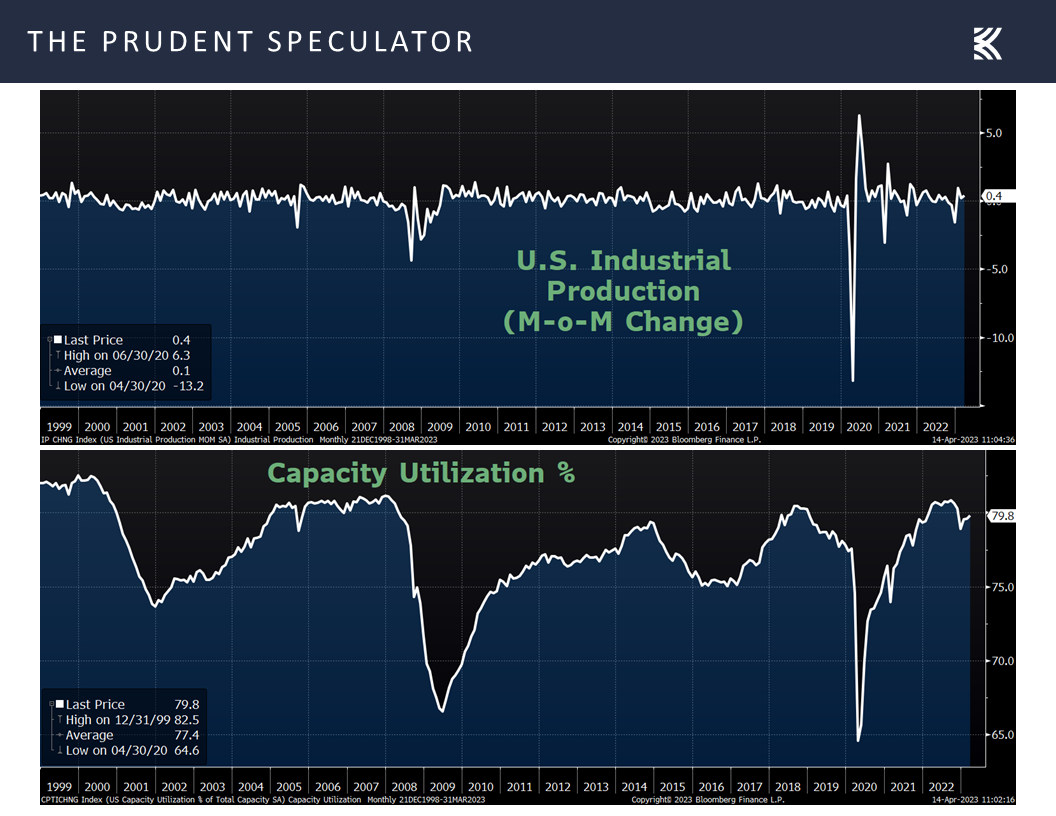

Better-than-Forecast Econ Numbers – Sentiment & Industrial Production

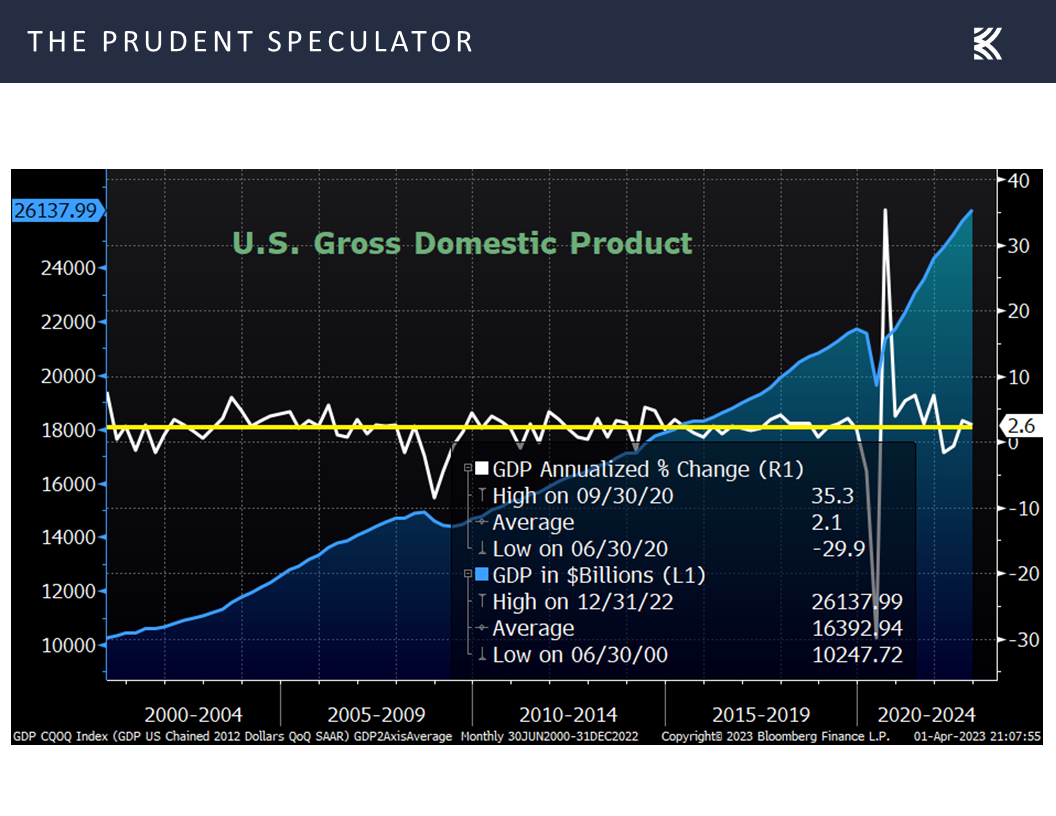

On the other hand, the latest projection from the Atlanta Fed for Q1 U.S. GDP growth rose to 2.5% last week, up from 1.5% a week ago

as the mood of small business owners and folks on Main Street both came in better than expected, even as the respective figures were hardly anything to write home about

and tallies for industrial production and capacity utilization topped estimates,

suggesting to us that the economy is likely to hold up reasonably well, especially on a nominal basis

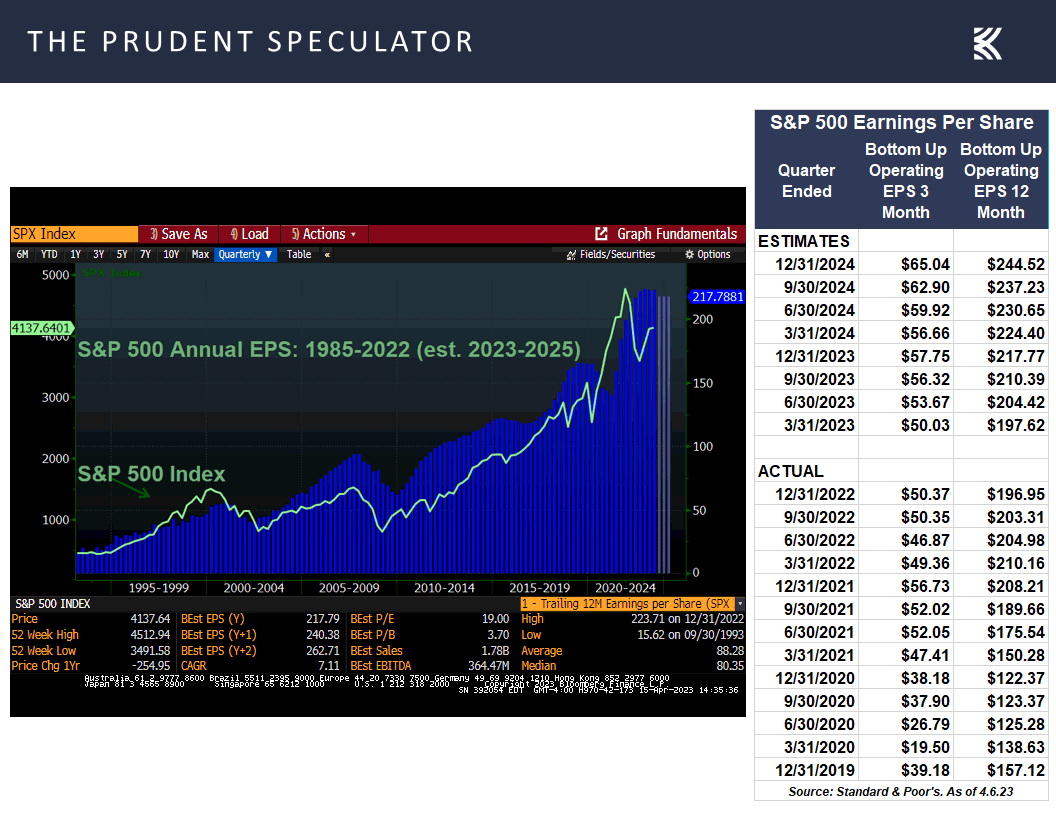

Earnings – Healthy Corporate Profits in ’23 and ’24 Still the Projection

which should provide support for corporate profits, even if current analyst estimates likely are a bit too rosy.

Inflation – Sharply Lower CPI & PPI

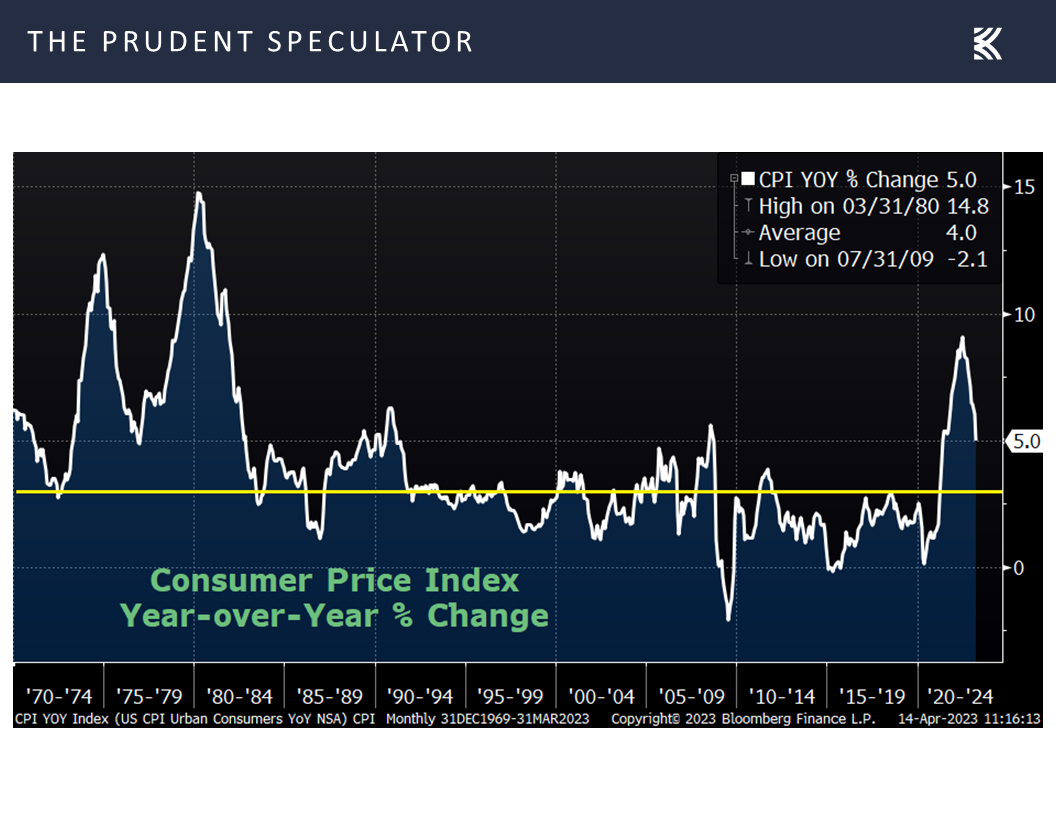

The most important of the economic numbers out last week were those related to inflation. Happily, both the consumer price index, which rose “only” 5.0% on a year-over-year basis in March, down from a 6.0% jump the month prior

and the producer price index, which increased 2.7% in March, versus a 4.9% rise in February,

and the producer price index, which increased 2.7% in March, versus a 4.9% rise in February,

suggest that the Fed is making some progress on the inflation front, even as San Francisco Fed President Mary Daly said on Wednesday, “While the full impact of this policy tightening is still making its way through the system, the strength of the economy and the elevated readings on inflation suggest that there is more work to do.”

suggest that the Fed is making some progress on the inflation front, even as San Francisco Fed President Mary Daly said on Wednesday, “While the full impact of this policy tightening is still making its way through the system, the strength of the economy and the elevated readings on inflation suggest that there is more work to do.”

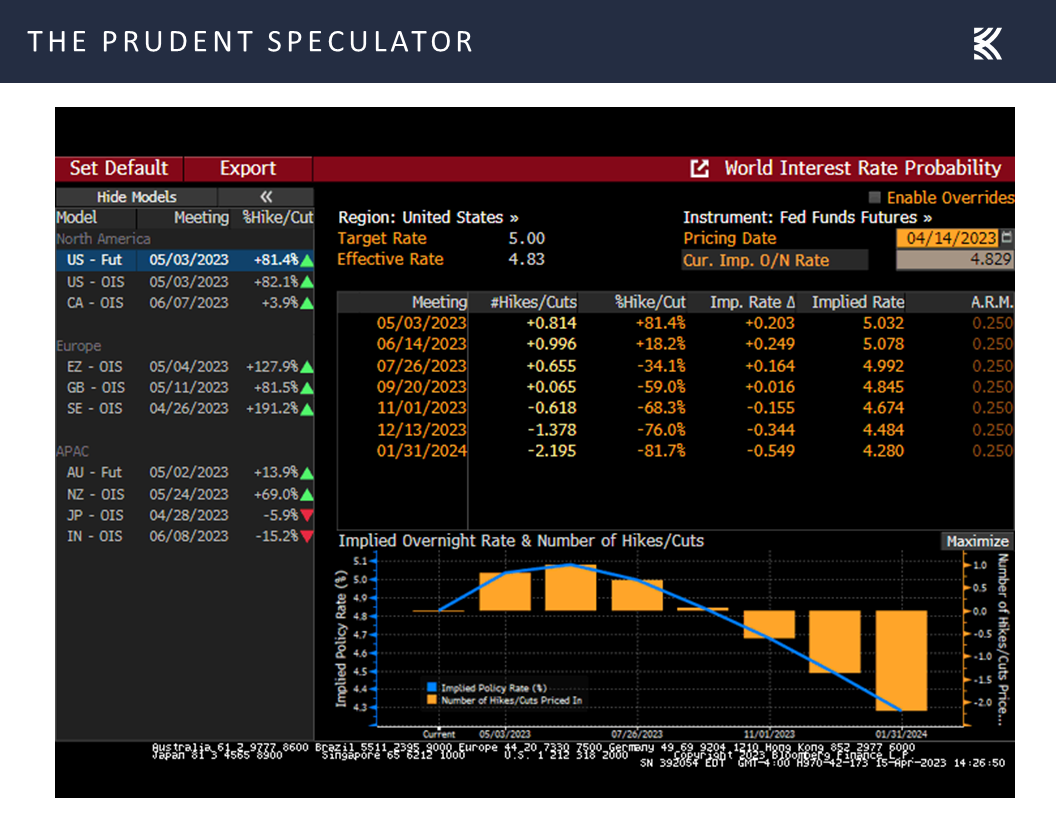

Market expectations for additional Federal Reserve rate hikes ticked higher last week, with the futures now pricing in a 5.08% peak in the Fed Funds rate this year and a year-end level of 4.48%. Those numbers compare to a 5.00% high and a 4.26% end-of-year figure indicated by the futures the week prior

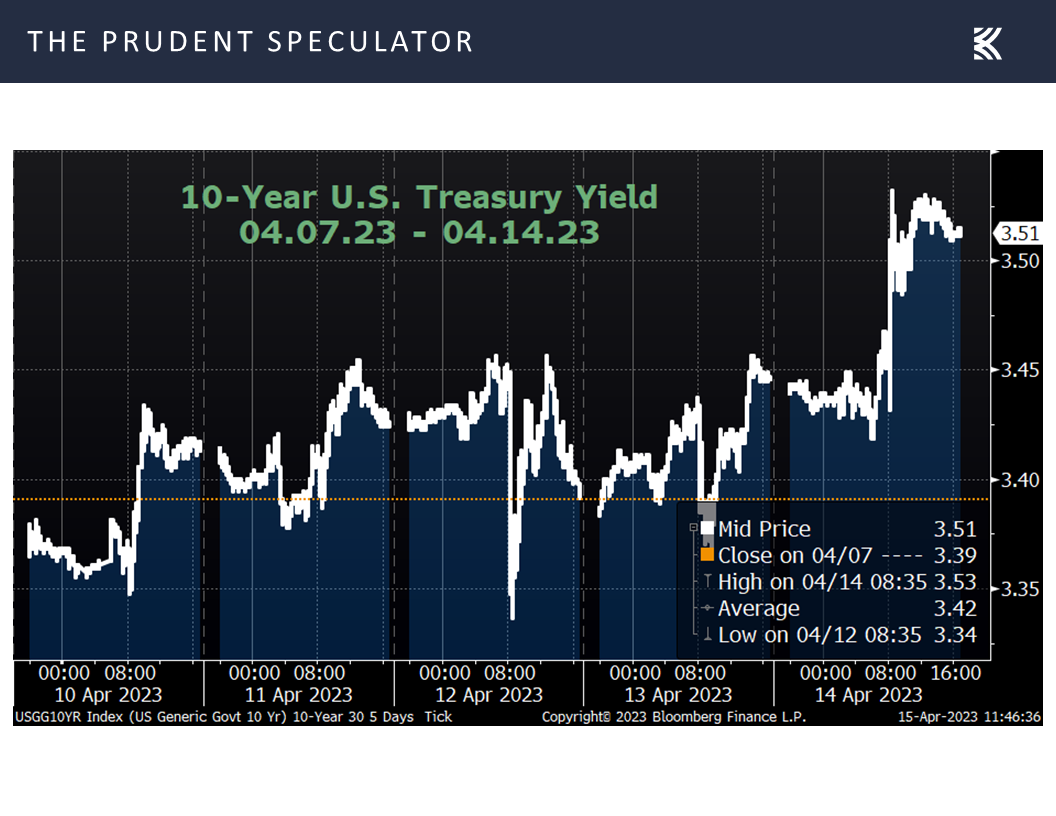

with the higher-for-longer shift in interest-rate sentiment contributing to a bump up in the yield last week on the benchmark 10-Year U.S. Treasury

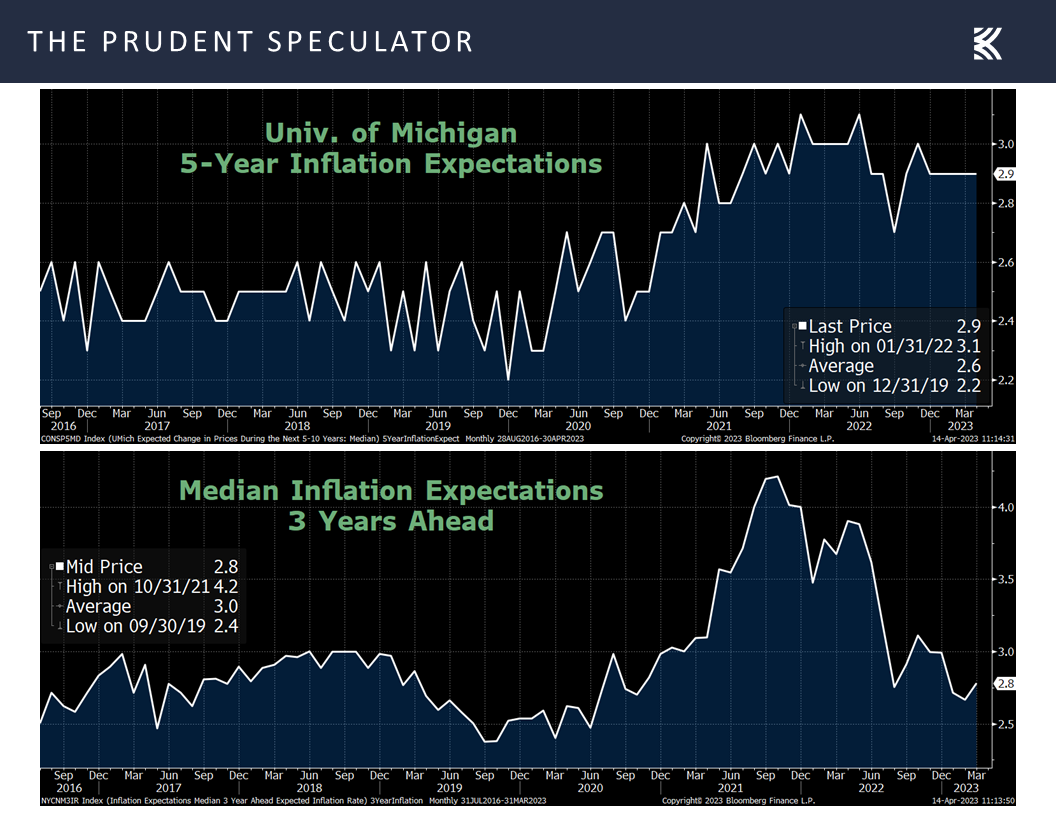

even as longer-term inflation expectations remain fairly contained.

even as longer-term inflation expectations remain fairly contained.

Valuations – Still Liking the Metrics for our Portfolios

Obviously, the health of the economy remains a big question mark, but we continue to like the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks

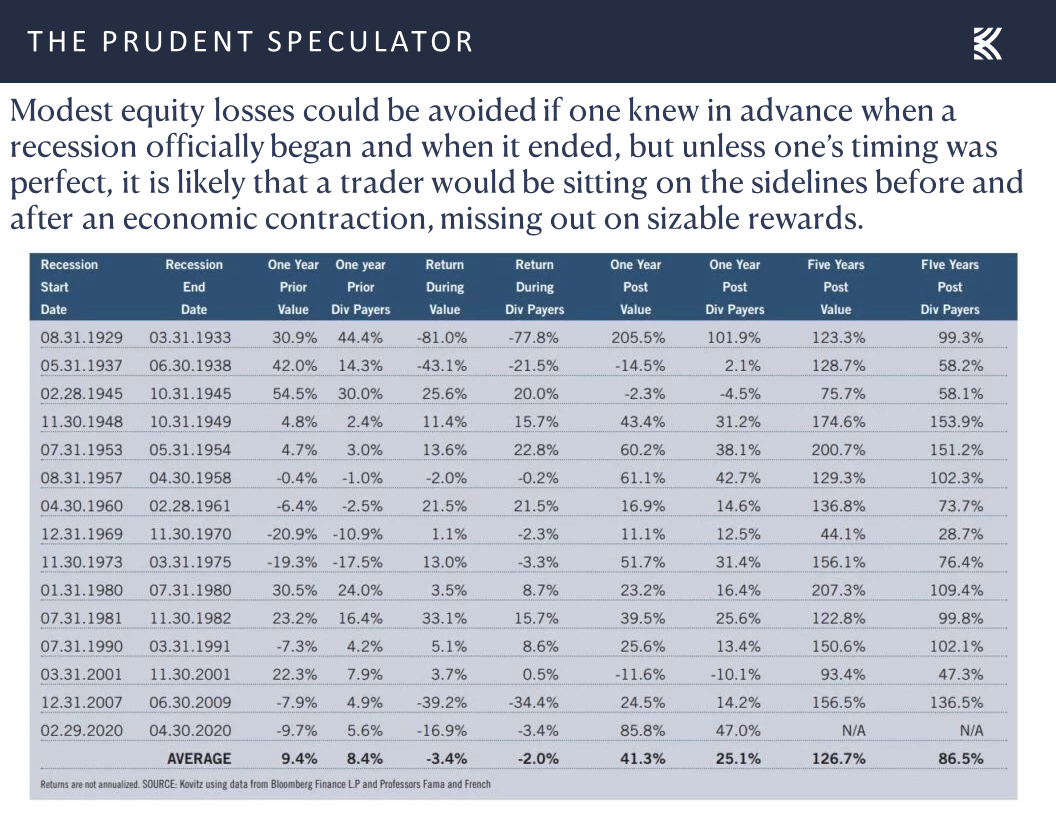

Recessions – History Shows No Reason, On Average, for Long-Term-Oriented Investors to Sell Stocks

and we take comfort in what market history has to say about recessions and the performance of Value Stocks and Dividend Payers, like those that we have long championed.

Stock Market News: Updates on six stocks across six different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Federal Reserve Projections, AAII Stock Market Sentiment, Inflation, Recessions and more Economic News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. This week, we discuss the Federal Reserve Projections, Earnings, Inflation, Recession, AAII Stock Market Sentiment and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Contra-Indicator – AAII Bulls Skid

Wall of Worry – Stock Have Overcome Plenty of Disconcerting News in the Fullness of Time

Federal Reserve News – Disconnect Between Minutes and Press Conference / GDP Projections

Weaker-than-Expected Econ Stats – Retail Sales & Jobless Claims

Better-than-Forecast Econ Numbers – Sentiment & Industrial Production

Earnings – Healthy Corporate Profits in ’23 and ’24 Still the Projection

Inflation – Sharply Lower CPI & PPI

Valuations – Still Liking the Metrics for our Portfolios

Recessions – History Shows No Reason, On Average, for Long-Term-Oriented Investors to Sell Stocks

Stock News – Update on six stocks across six different sectors

Contra-Indicator – AAII Bulls Skid

If we were going to blame the pullback during the first week of April on the good folks at the American Association of Individual Investors (AAII) becoming much more optimistic about the prospects for stocks over the ensuing six months, we suppose we should credit last week’s rebound to a renewed sense of pessimism on the contrarian AAII Sentiment gauge. Interestingly, while the AAII tally of Bears edged down 0.5 percentage points to 34.5%, the count of Bulls fell by 7.2 percentage points to 26.1%, with the Bull-Bear spread sinking to -8.4% from -1.7% the week prior.

The number of Bulls is now well below the 37.5% average and the Bears are above the 31.0% average, with forward returns historically better when the AAII Bull-Bear Spread is tilted heavily toward negativity. Certainly, no metric is infallible, but it is fascinating to see 36 years of historical evidence in the chart above confirming that, on average, it often pays to be greedy when others are fearful.

Wall of Worry – Stock Have Overcome Plenty of Disconcerting News in the Fullness of Time

Of course, there usually is something for investors to be concerned about, as evidenced by all the disconcerting events that have occurred just since the end of the Great Financial Crisis in March 2009, yet stocks, in the fullness of time, always seem to manage to climb a wall of worry.

Federal Reserve News – Disconnect Between Minutes and Press Conference / GDP Projections

Speaking of worry, last week’s rebound was interrupted on Wednesday when the Minutes of the FOMC’s March meeting were released. The trouble seemed to be that the Fed staff forecast presented at the meeting anticipated a recession would start later this year due to banking-sector turmoil. However, Jerome H. Powell in his post-meeting Press Conference last month did not state that an economic contraction was his projection.

To be fair, he didn’t say that a recession would not occur, but when asked, “Do you still see a possibility of a soft landing for the U.S. economy,” the Fed Chair responded:

You know it’s, it’s too early to say, really, whether these events have had much of an effect. It’s hard for me to see how they would have helped the possibility—but I guess I would just say, it’s too early to say whether there really have been changes in that. You know, the question will be how long this period is sustained. The longer it’s sustained, then the greater will be the likely declines in—or tightening in credit standards, credit availability, so we’ll just have to see. I do still think, though, that there’s a—there’s a pathway to that. I think that pathway still exists and, you know, we’re certainly trying to find it.

In addition, the economic projections from Federal Reserve Board Members and Federal Reserve Bank Presidents prepared for that Fed Meeting still called for modest real (inflation-adjusted) GDP growth of 0.4% this year and 1.2% in 2024. Yes, those were downgrades to the outlook, but they did not predict a contraction on a year-over-year basis.

True, Bloomberg calculates that the chance of recession in the next 12 months stands at 65% today,

Weaker-than-Expected Econ Stats – Retail Sales & Jobless Claims

with the latest read on retail sales for March coming in below expectations with a 1.0% decline,

and the number of first-time filings for jobless benefits and continuing jobless claims now residing at higher levels than seen in recent months.

Better-than-Forecast Econ Numbers – Sentiment & Industrial Production

On the other hand, the latest projection from the Atlanta Fed for Q1 U.S. GDP growth rose to 2.5% last week, up from 1.5% a week ago

as the mood of small business owners and folks on Main Street both came in better than expected, even as the respective figures were hardly anything to write home about

and tallies for industrial production and capacity utilization topped estimates,

suggesting to us that the economy is likely to hold up reasonably well, especially on a nominal basis

Earnings – Healthy Corporate Profits in ’23 and ’24 Still the Projection

which should provide support for corporate profits, even if current analyst estimates likely are a bit too rosy.

Inflation – Sharply Lower CPI & PPI

The most important of the economic numbers out last week were those related to inflation. Happily, both the consumer price index, which rose “only” 5.0% on a year-over-year basis in March, down from a 6.0% jump the month prior

Market expectations for additional Federal Reserve rate hikes ticked higher last week, with the futures now pricing in a 5.08% peak in the Fed Funds rate this year and a year-end level of 4.48%. Those numbers compare to a 5.00% high and a 4.26% end-of-year figure indicated by the futures the week prior

with the higher-for-longer shift in interest-rate sentiment contributing to a bump up in the yield last week on the benchmark 10-Year U.S. Treasury

Valuations – Still Liking the Metrics for our Portfolios

Obviously, the health of the economy remains a big question mark, but we continue to like the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks

Recessions – History Shows No Reason, On Average, for Long-Term-Oriented Investors to Sell Stocks

and we take comfort in what market history has to say about recessions and the performance of Value Stocks and Dividend Payers, like those that we have long championed.

Stock Market News: Updates on six stocks across six different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.