The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the FOMC Meeting, Inflation, Fed Econ Projections, Earnings and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Portfolio Trades – 1 Sale for 3 Accounts

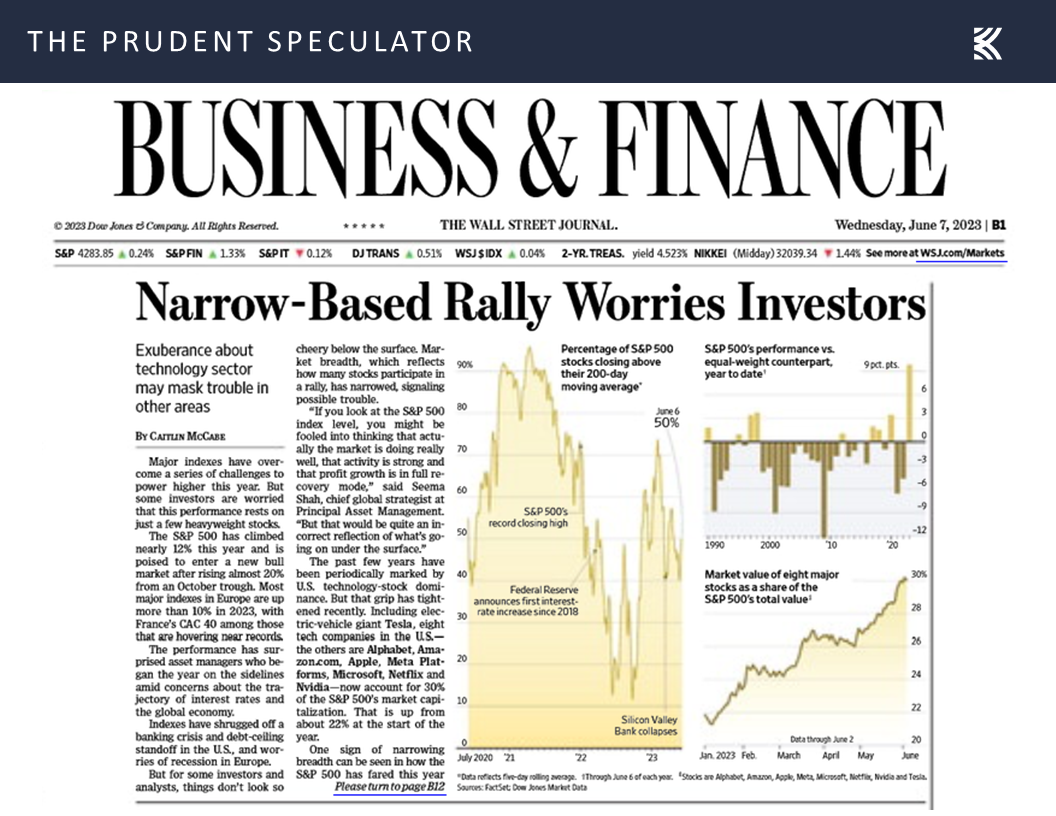

Market Breadth – Soldiers Still Beating the Generals in June

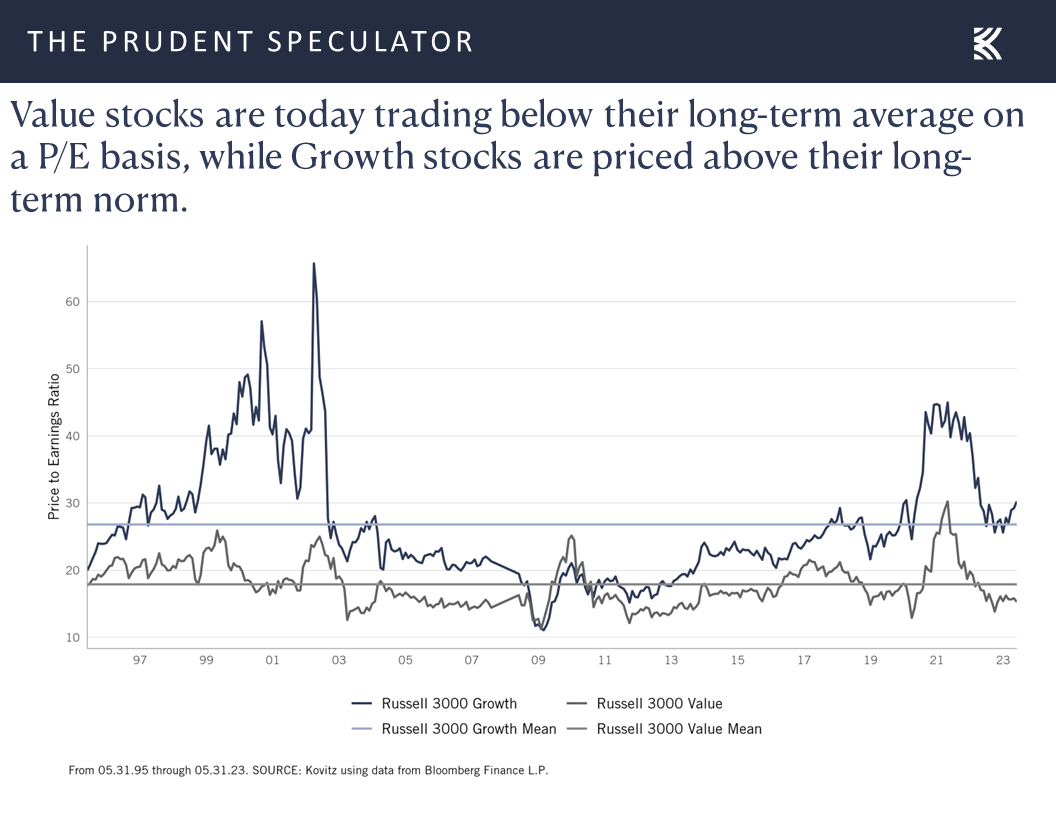

Valuations – Value Stocks Inexpensive by Historical Standards

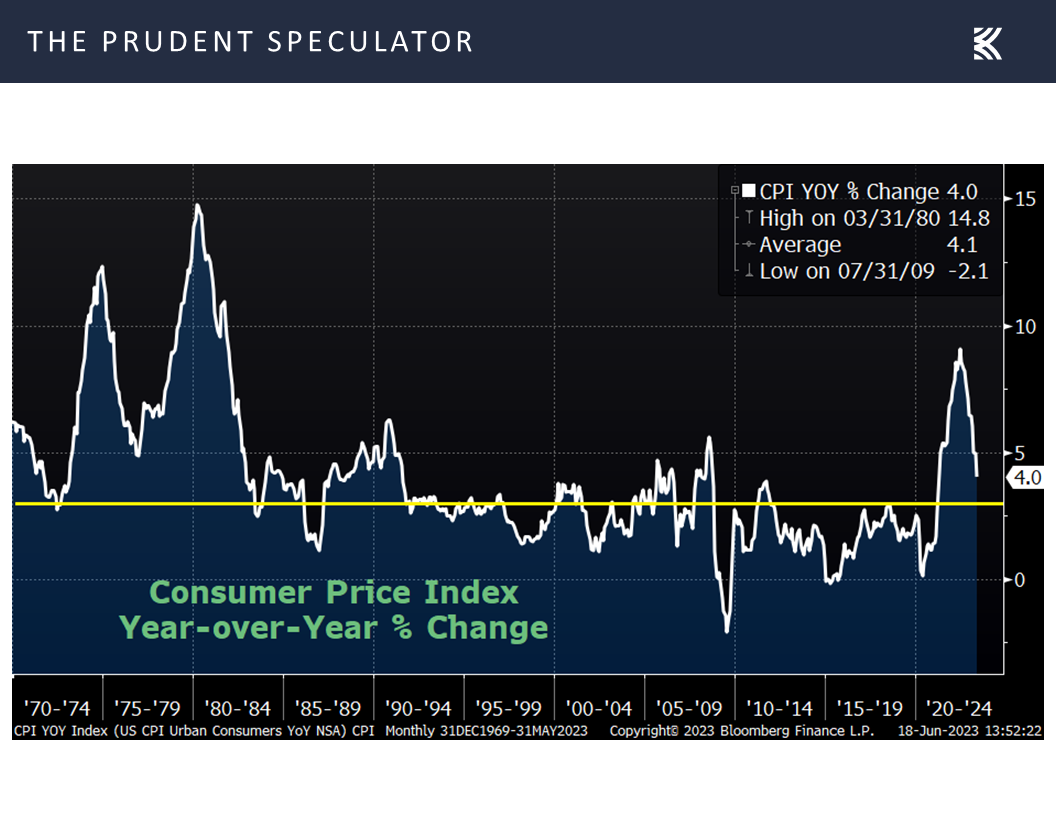

Inflation – CPI & PPI Lower Than Expected

FOMC Meeting – Fed Pauses Rate Hikes But Expects Two More 25 Basis Point Increases This Year

Fed Econ Projections – 2023 Outlook Upgraded

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

Sentiment – AAII Remains Much More Bullish

Stock News – Updates on Seven Stocks & Seven Banks

Market Breadth – Soldiers Still Beating the Generals in June

While the week ended on a down note, it was a terrific five days, with the advance in June continuing to be of the broad variety, right on cue, perhaps, after the financial press warned of the narrowness of the rally.

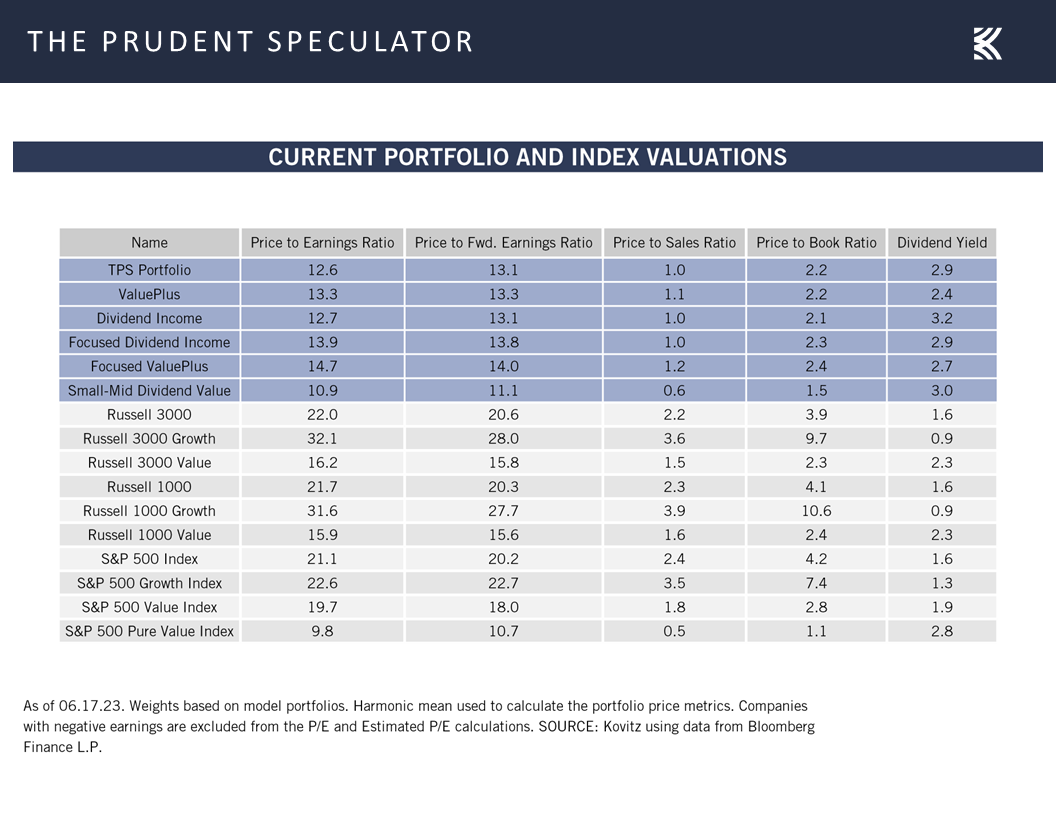

Valuations – Value Stocks Inexpensive by Historical Standards

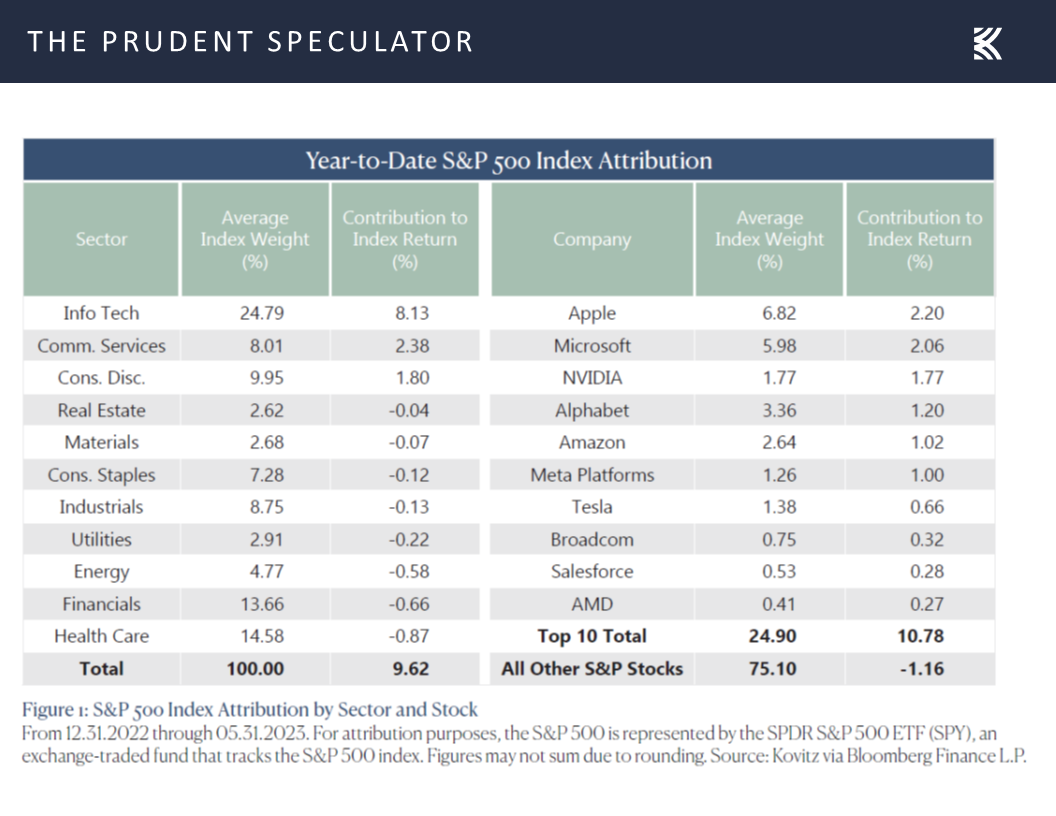

With the equal-weight S&P 500 advancing 2.5% on the week, we are now up to 38 stocks accounting for all the year’s gains in the capitalization-weighted index. Believe it or not, through the first five months of the year, the top-10 stocks in the S&P accounted for all the increase and then some, while the other 490 stocks endured a negative average contribution to the return of 1.2%.

Though it has only been half a month, we are pleased to see that the average stock in the S&P 500 has appreciated 6.7%, compared to a 5.6% gain for the index. As we said last week, we think the outperformance of the proverbial soldiers over the generals makes a lot of sense and we believe it should continue, especially as the Value stock side of the ledger is trading below the long-term average on a P/E basis, while the Growth side, is priced above its long-term norm.

Inflation – CPI & PPI Lower Than Expected

No doubt, it was a news-filled week on the economic front, starting with a better-than-expected (lower) tally on inflation at the consumer level. The CPI for May came in at 4.0%, modestly below the 4.1% projection, and down considerably from April’s reading of 4.9%. Tempering that positive somewhat was a more modest drop in the core (excludes volatile food and energy) rate of inflation to 5.3%, compared to 5.5% in April, and an estimate of 5.2%.

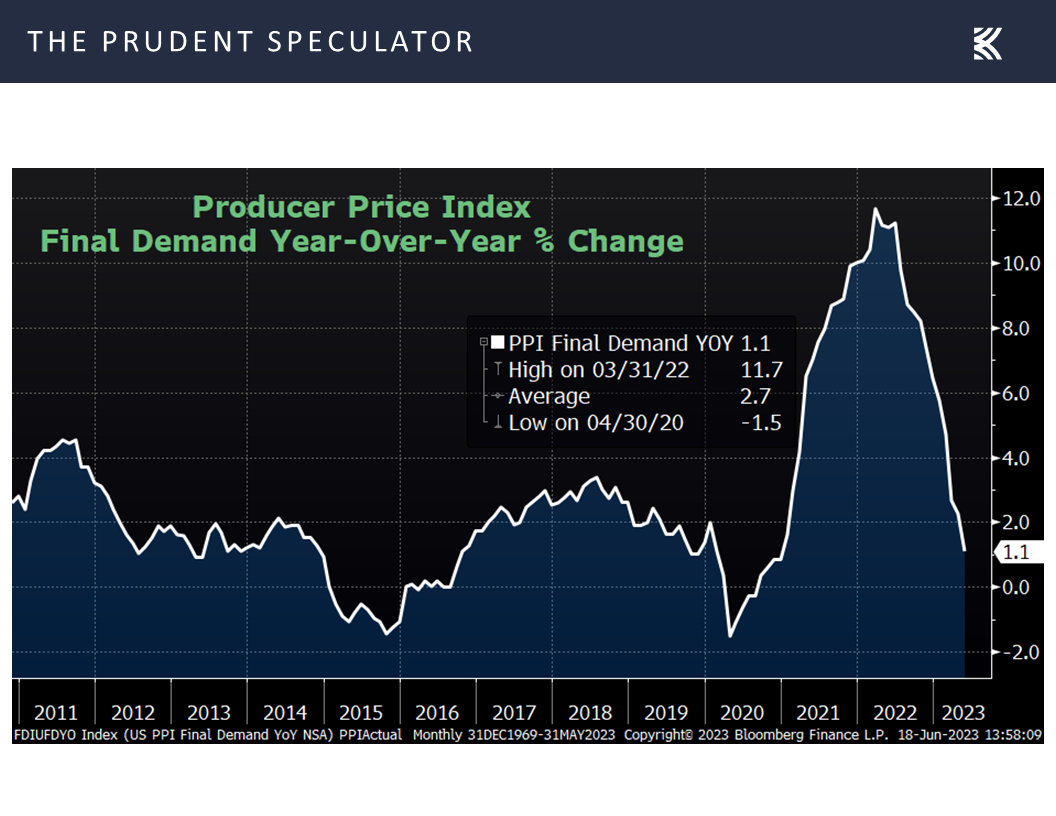

The plunge in inflation at the wholesale level was even more dramatic with the producer price index (PPI) falling last month to a 1.1% increase on a year-over-year basis, down from 2.3% in April and well below expectations of a 1.5% rise. Incredibly, given all of the worries about inflation, the PPI for May came in 1.6 percentage points below the average over the last dozen years.

FOMC Meeting – Fed Pauses Rate Hikes But Expects Two More 25 Basis Point Increases This Year

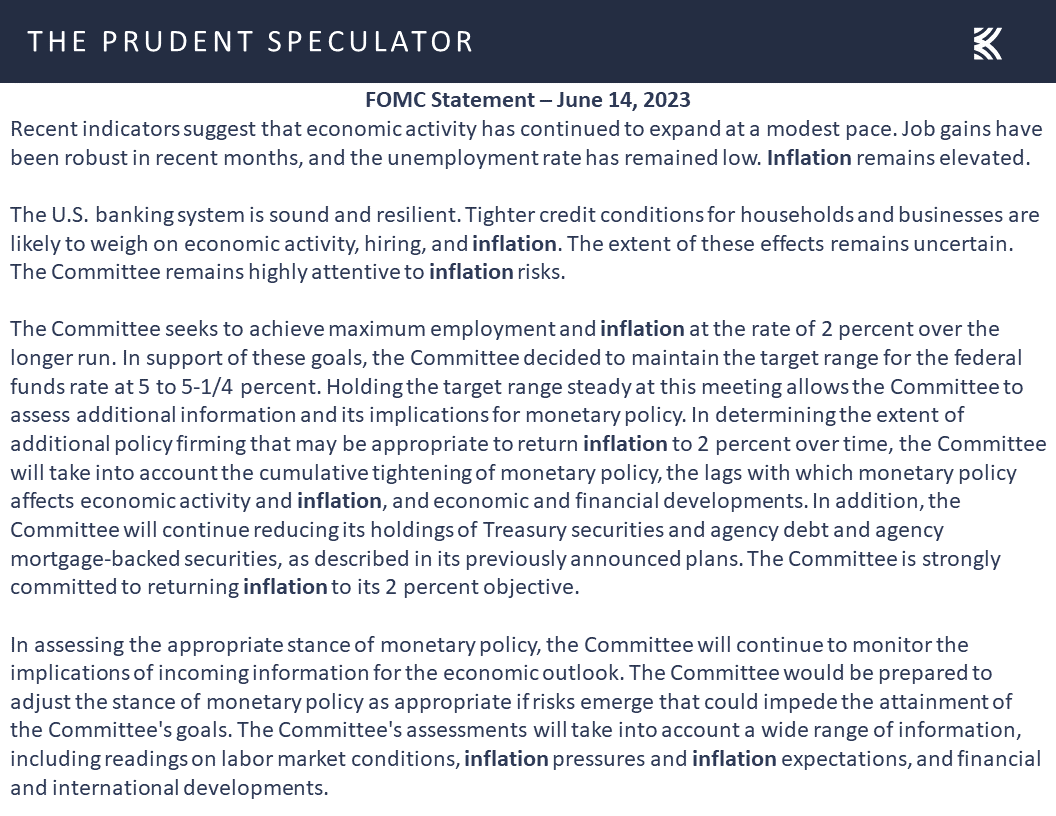

Of course, concerns about inflation remained front and center at last week’s Federal Open Market Committee meeting, with the FOMC Statement mentioning the word nine times,

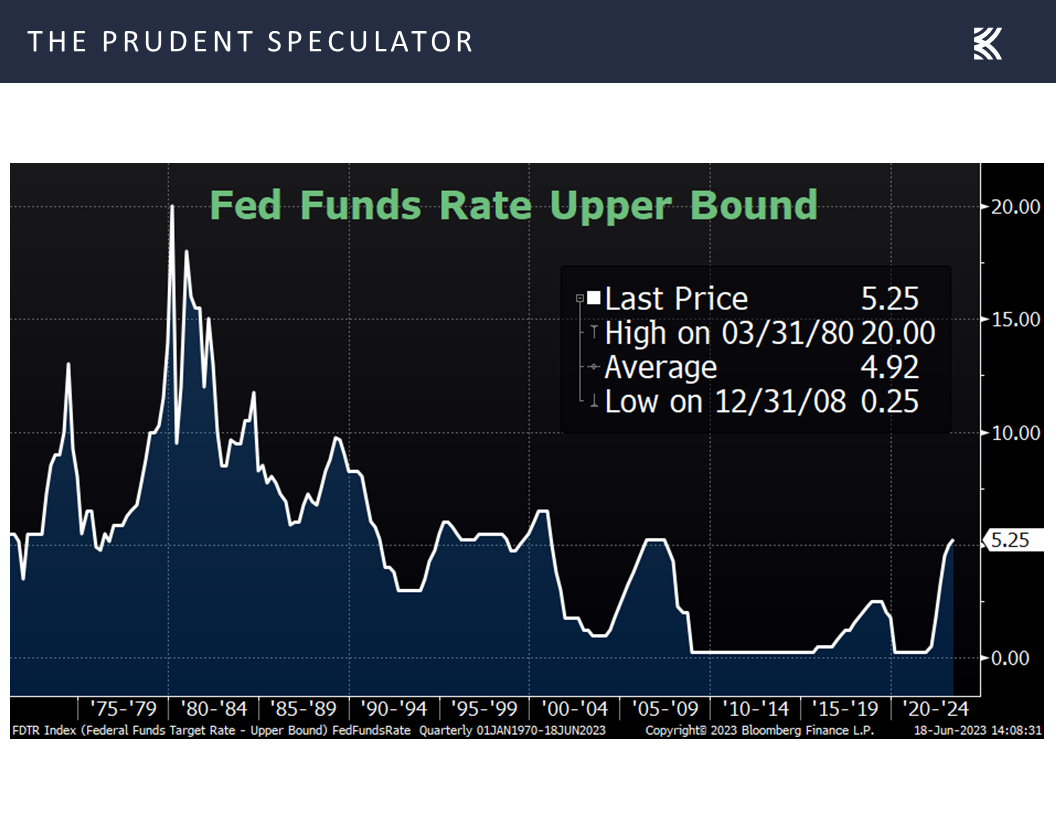

even as Jerome H. Powell & Co. chose to leave the target for the Federal Funds rate unchanged at a range of 5.0% to 5.25%.

Fed Econ Projections – 2023 Outlook Upgraded

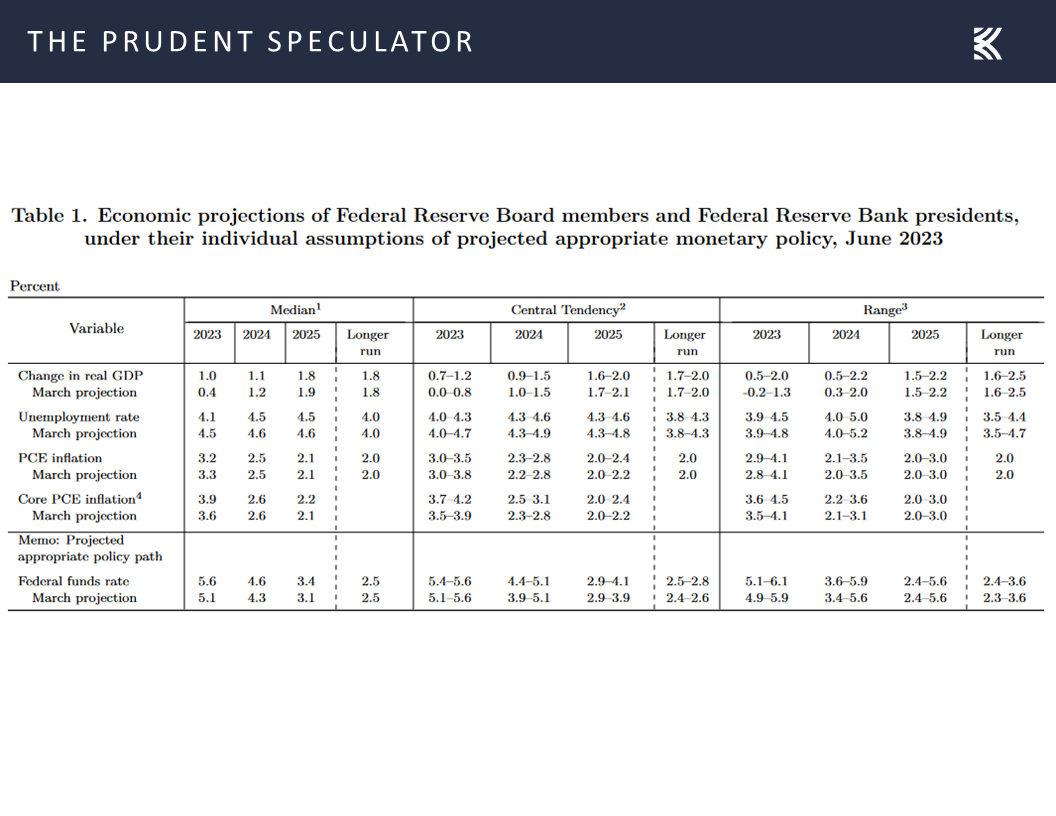

Interestingly, the updated quarterly economic projections of Federal Reserve Board members and Federal Reserve Bank presidents saw an increase in GDP growth to 1.0% this year, up from 0.4% in March, and a reduction in the unemployment rate to 4.1%, down from 4.5% three months ago. PCE inflation was also expected to dip to 3.2%, down from 3.3%, though the Core PCE rate that is most important to the Fed is forecast to rise to 3.9%, up from 3.6%.

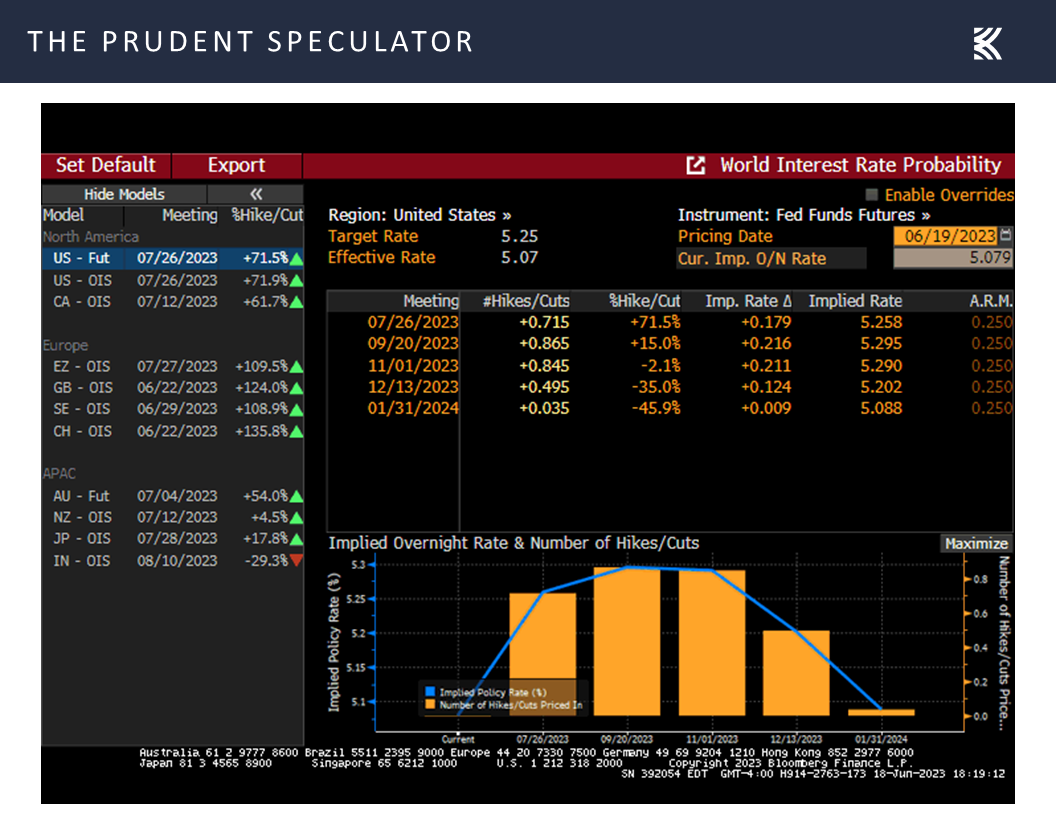

The key number in those estimates, however, was the expectation of a 5.6% year-end Fed Funds rate target, up from 5.1%. This is in sharp contrast to the current view of the Fed Funds futures market, which is suggesting a 5.20% effective rate at the end of 2023

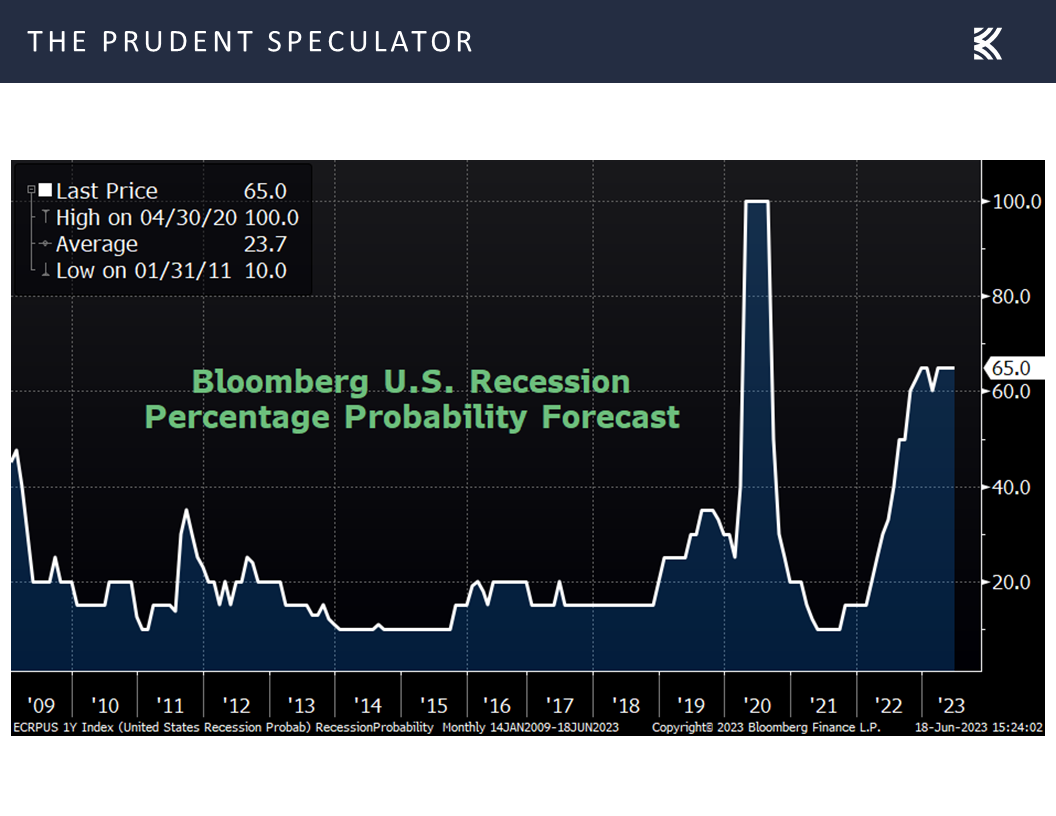

Is it any wonder that John Kenneth Galbraith said, “The only function of economic forecasting is to make astrology look respectable!” After all, Bloomberg calculations have suggested a 60% or greater chance of U.S. recession in the next 12 months since last August,

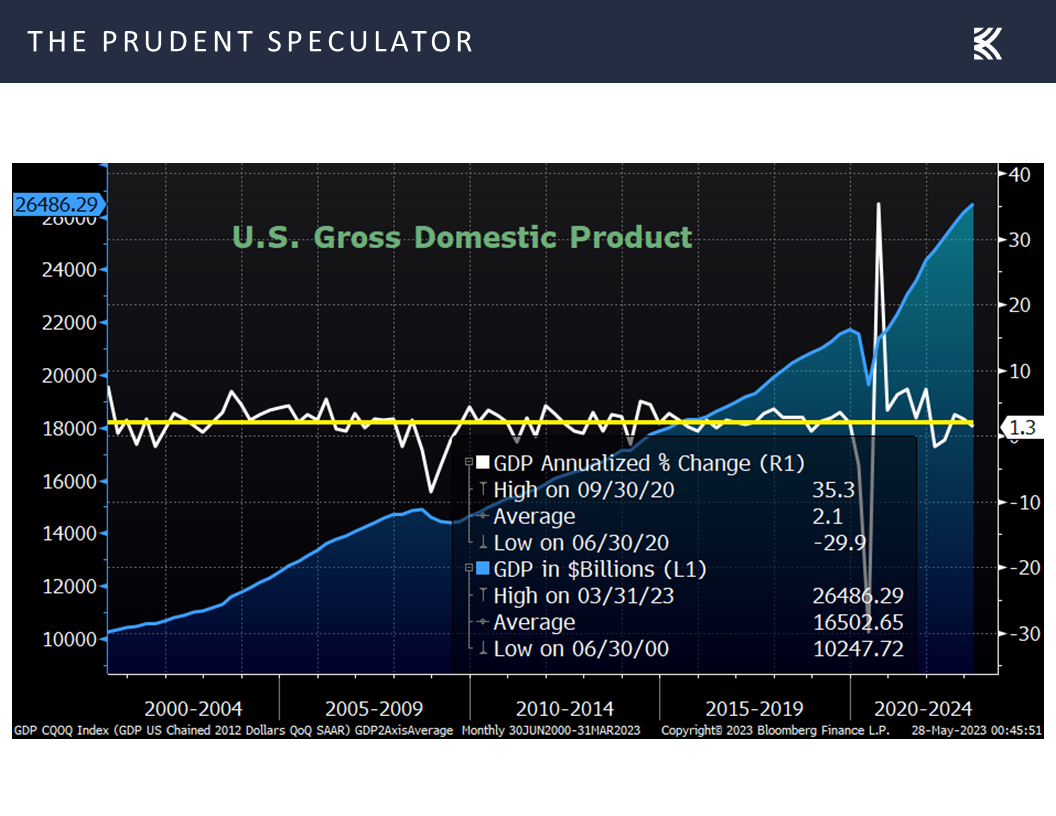

yet Q3 and Q4 2022 real (inflation-adjusted) GDP growth came in at 3.2% and 2.6%, respectively, while Q1 2023 growth was 1.3%,

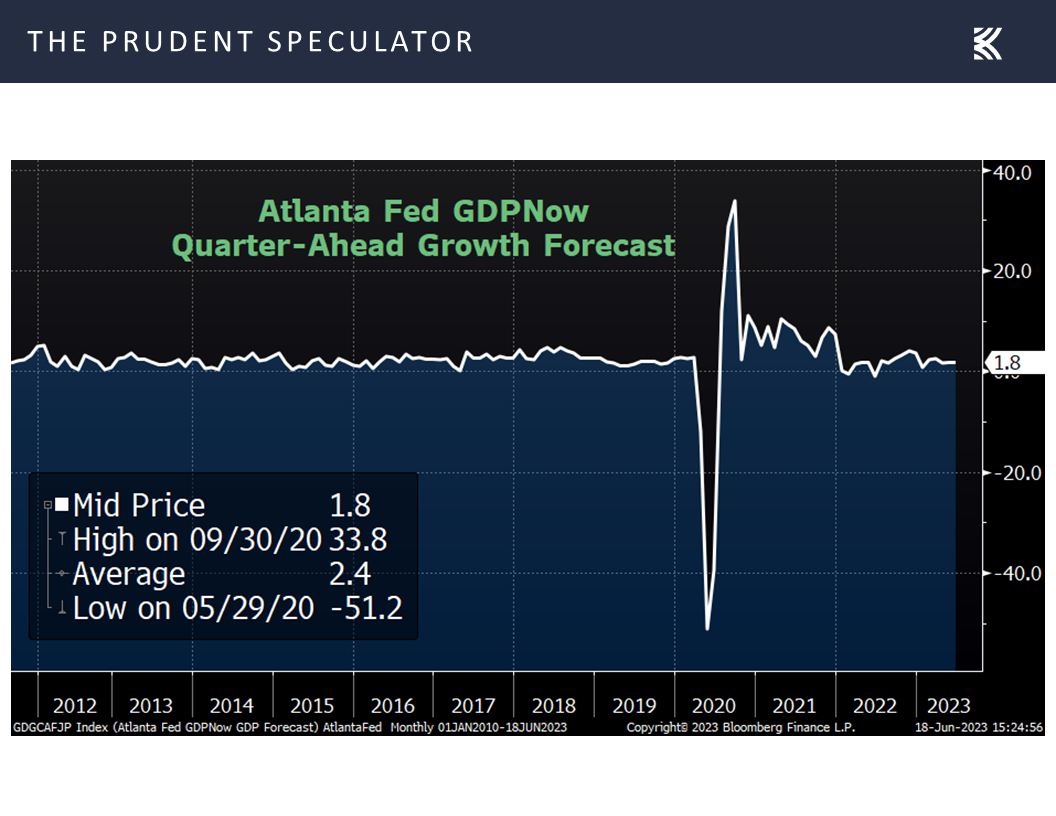

…and the current projection from the Atlanta Fed for Q2 domestic growth is 1.8%.

…and the current projection from the Atlanta Fed for Q2 domestic growth is 1.8%.

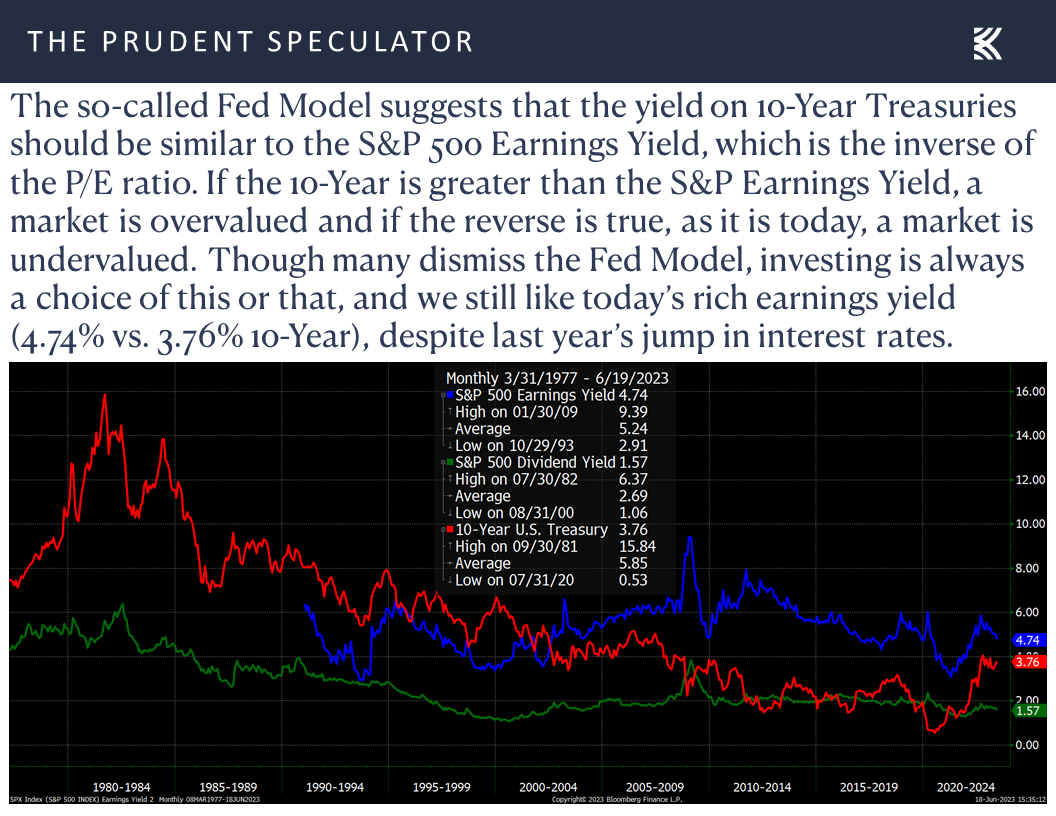

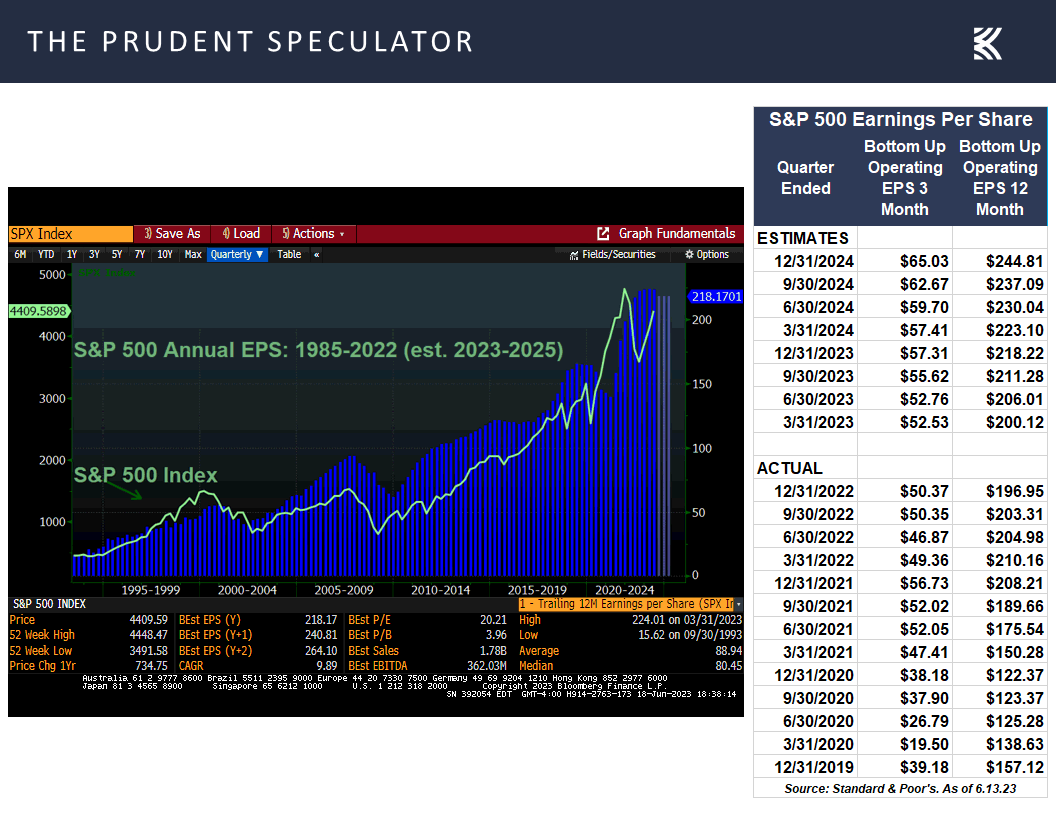

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

We’ll leave the economic prognosticating to others as we continue to believe that the stocks we own are inexpensive,

…while we think stocks in general are still reasonably priced, given that long-term interest rates are well below their norm since 1977,

…and corporate profits are likely to show solid growth this year and next, per the latest projections from Bloomberg and Standard & Poor’s.

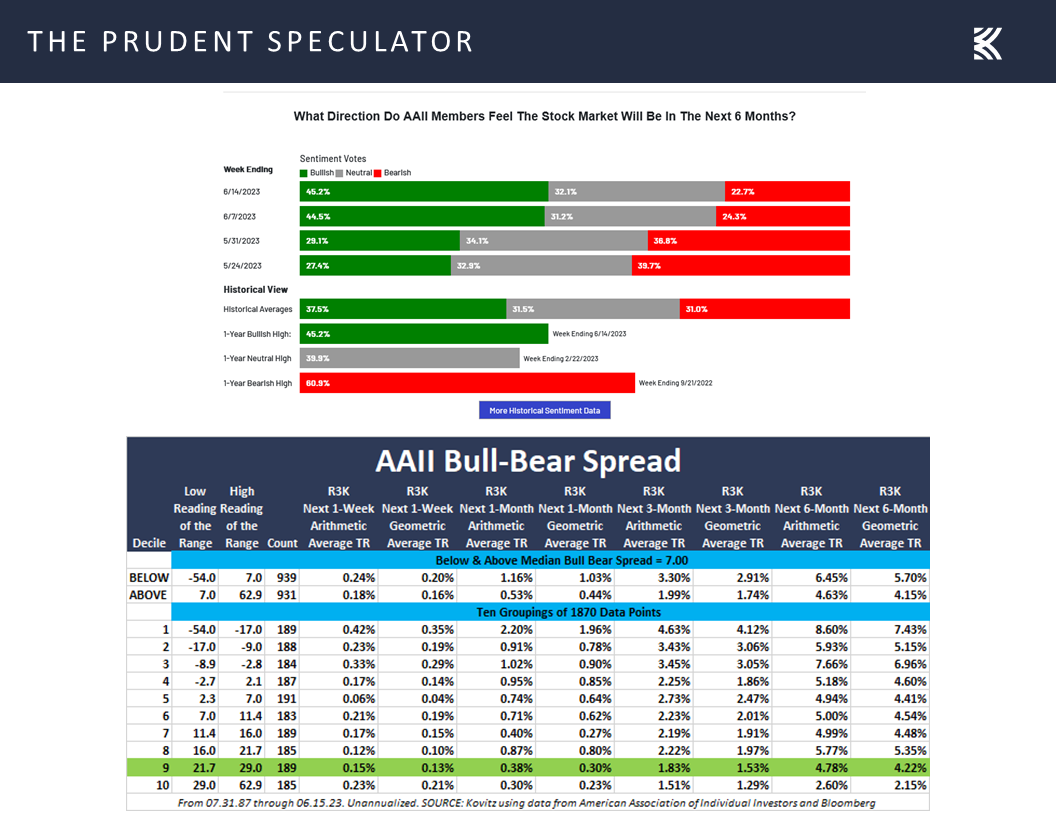

Sentiment – AAII Remains Much More Bullish

To be sure, this does not mean that the recent rally will continue, especially as investor sentiment, often a contrarian indicator, has become decidedly more bullish,

…but we see no reason why the equity markets should not remain a great place for long-term-oriented investors to compound wealth.

Stock Market News: Updates on seven stocks and seven banks

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

FOMC Meeting, Inflation, Fed Econ Projections, Earnings and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the FOMC Meeting, Inflation, Fed Econ Projections, Earnings and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Portfolio Trades – 1 Sale for 3 Accounts

Market Breadth – Soldiers Still Beating the Generals in June

Valuations – Value Stocks Inexpensive by Historical Standards

Inflation – CPI & PPI Lower Than Expected

FOMC Meeting – Fed Pauses Rate Hikes But Expects Two More 25 Basis Point Increases This Year

Fed Econ Projections – 2023 Outlook Upgraded

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

Sentiment – AAII Remains Much More Bullish

Stock News – Updates on Seven Stocks & Seven Banks

Market Breadth – Soldiers Still Beating the Generals in June

While the week ended on a down note, it was a terrific five days, with the advance in June continuing to be of the broad variety, right on cue, perhaps, after the financial press warned of the narrowness of the rally.

Valuations – Value Stocks Inexpensive by Historical Standards

With the equal-weight S&P 500 advancing 2.5% on the week, we are now up to 38 stocks accounting for all the year’s gains in the capitalization-weighted index. Believe it or not, through the first five months of the year, the top-10 stocks in the S&P accounted for all the increase and then some, while the other 490 stocks endured a negative average contribution to the return of 1.2%.

Though it has only been half a month, we are pleased to see that the average stock in the S&P 500 has appreciated 6.7%, compared to a 5.6% gain for the index. As we said last week, we think the outperformance of the proverbial soldiers over the generals makes a lot of sense and we believe it should continue, especially as the Value stock side of the ledger is trading below the long-term average on a P/E basis, while the Growth side, is priced above its long-term norm.

Inflation – CPI & PPI Lower Than Expected

No doubt, it was a news-filled week on the economic front, starting with a better-than-expected (lower) tally on inflation at the consumer level. The CPI for May came in at 4.0%, modestly below the 4.1% projection, and down considerably from April’s reading of 4.9%. Tempering that positive somewhat was a more modest drop in the core (excludes volatile food and energy) rate of inflation to 5.3%, compared to 5.5% in April, and an estimate of 5.2%.

The plunge in inflation at the wholesale level was even more dramatic with the producer price index (PPI) falling last month to a 1.1% increase on a year-over-year basis, down from 2.3% in April and well below expectations of a 1.5% rise. Incredibly, given all of the worries about inflation, the PPI for May came in 1.6 percentage points below the average over the last dozen years.

FOMC Meeting – Fed Pauses Rate Hikes But Expects Two More 25 Basis Point Increases This Year

Of course, concerns about inflation remained front and center at last week’s Federal Open Market Committee meeting, with the FOMC Statement mentioning the word nine times,

even as Jerome H. Powell & Co. chose to leave the target for the Federal Funds rate unchanged at a range of 5.0% to 5.25%.

Fed Econ Projections – 2023 Outlook Upgraded

Interestingly, the updated quarterly economic projections of Federal Reserve Board members and Federal Reserve Bank presidents saw an increase in GDP growth to 1.0% this year, up from 0.4% in March, and a reduction in the unemployment rate to 4.1%, down from 4.5% three months ago. PCE inflation was also expected to dip to 3.2%, down from 3.3%, though the Core PCE rate that is most important to the Fed is forecast to rise to 3.9%, up from 3.6%.

The key number in those estimates, however, was the expectation of a 5.6% year-end Fed Funds rate target, up from 5.1%. This is in sharp contrast to the current view of the Fed Funds futures market, which is suggesting a 5.20% effective rate at the end of 2023

Is it any wonder that John Kenneth Galbraith said, “The only function of economic forecasting is to make astrology look respectable!” After all, Bloomberg calculations have suggested a 60% or greater chance of U.S. recession in the next 12 months since last August,

yet Q3 and Q4 2022 real (inflation-adjusted) GDP growth came in at 3.2% and 2.6%, respectively, while Q1 2023 growth was 1.3%,

Earnings – Growth in Bottom-Up Operating EPS for the S&P Still Expected for ’23 and ’24

We’ll leave the economic prognosticating to others as we continue to believe that the stocks we own are inexpensive,

…while we think stocks in general are still reasonably priced, given that long-term interest rates are well below their norm since 1977,

…and corporate profits are likely to show solid growth this year and next, per the latest projections from Bloomberg and Standard & Poor’s.

Sentiment – AAII Remains Much More Bullish

To be sure, this does not mean that the recent rally will continue, especially as investor sentiment, often a contrarian indicator, has become decidedly more bullish,

…but we see no reason why the equity markets should not remain a great place for long-term-oriented investors to compound wealth.

Stock Market News: Updates on seven stocks and seven banks

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.