The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss GDP Growth, Dividend Stocks, Interest Rates, Valuations and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

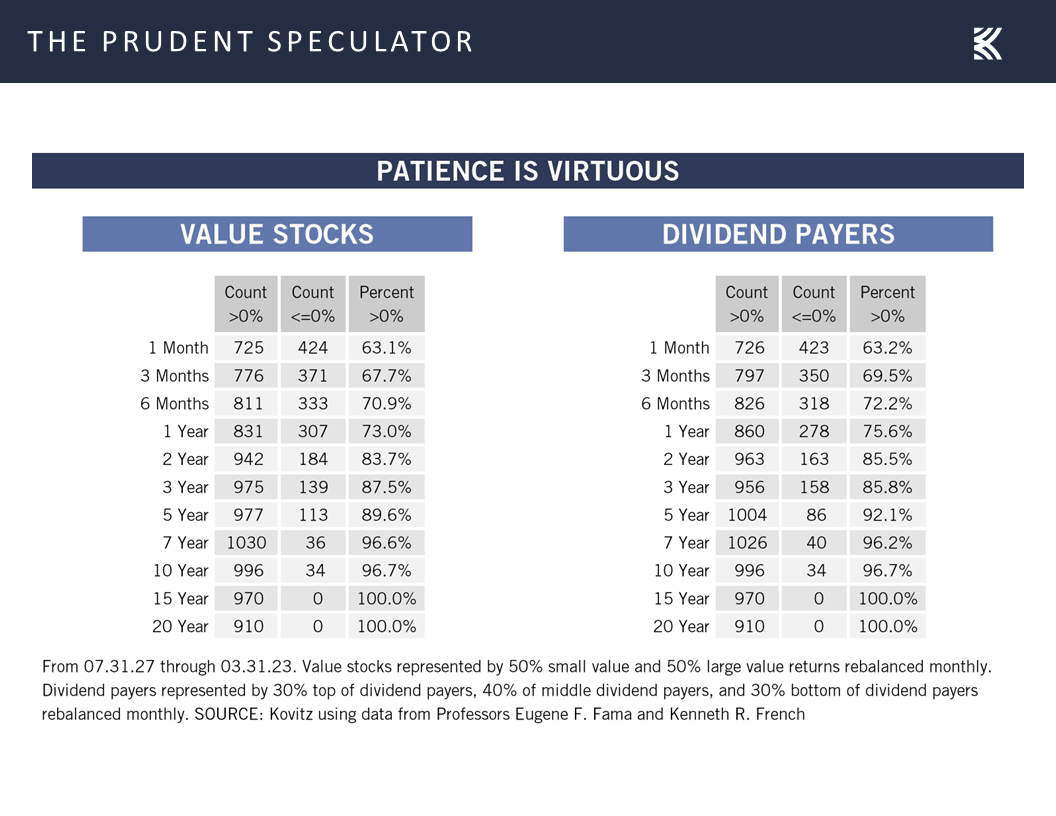

Probabilities – The Longer the Hold, the Less the Chance of Loss

Growth – GDP, Corporate Profits and Dividends Rise Over Time

Econ Data – Mixed Numbers; 1.7% Q2 GDP Growth Projected

Interest Rates – 10-Year Yield Low By Historical Standards

Valuations – Liking the Multiples on our Portfolios

Contrarian Sentiment – AAII Still Very Pessimistic

Stock News – Updates on eighteen stocks across thirteen different sectors

Probabilities – The Longer the Hold, the Less the Chance of Loss

It was another roller-coaster ride with a mid-week plunge giving way to a big month-end rally that pushed the major market averages into the green for the past five trading sessions. Certainly, it doesn’t always work out that holding for a week will quickly recoup one or two days of losses, but history does suggest that patience is a virtue when it comes to investing.

Indeed, having been in Sin City last week for the MoneyShow, there is no better place to emphasize the probabilities of winning. After all, baccarat, blackjack, craps or roulette offer the best odds and slot machines generally the worst chance of winning, but the house always has the edge. Play long enough and you will lose.

Contrast that with the equities market, where the chance of making money in Value Stocks and Dividend Payers increases the longer the hold. True, there is no assurance that the past is prologue, but looking at data since 1927 from Professors Eugene F. Fama and Kenneth R. French shows the chance of a positive return rises from an already impressive 63% for a one-month hold to 73.0% for Value and 75.6% for Dividend Payers for a one-year hold. And the chance of making money rises to more than 96% for 10-year holding periods.

Certainly, there have been plenty of ups and downs along the way, but stocks have proved very rewarding for those who remember that the secret to success is not to get scared out of them.

Growth – GDP, Corporate Profits and Dividends Rise Over Time

The reason that stocks have performed so well is that companies generally become more valuable over time, given that corporate profits have grown,

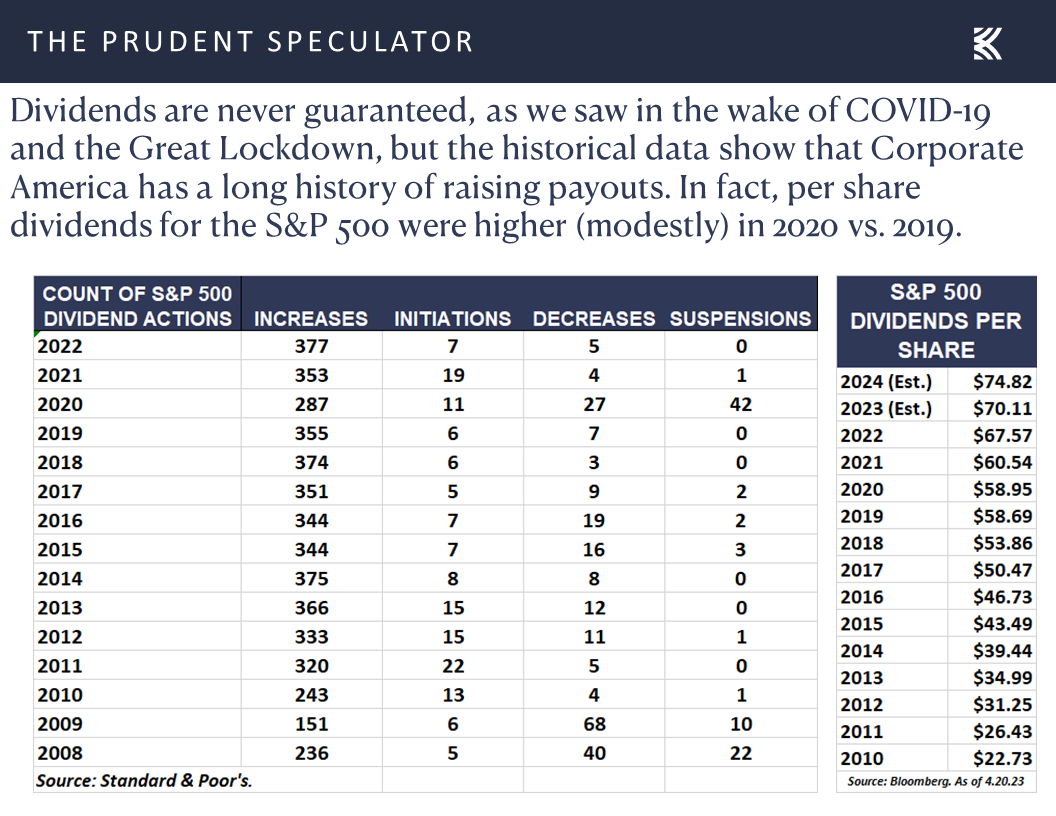

and dividend payouts have risen.

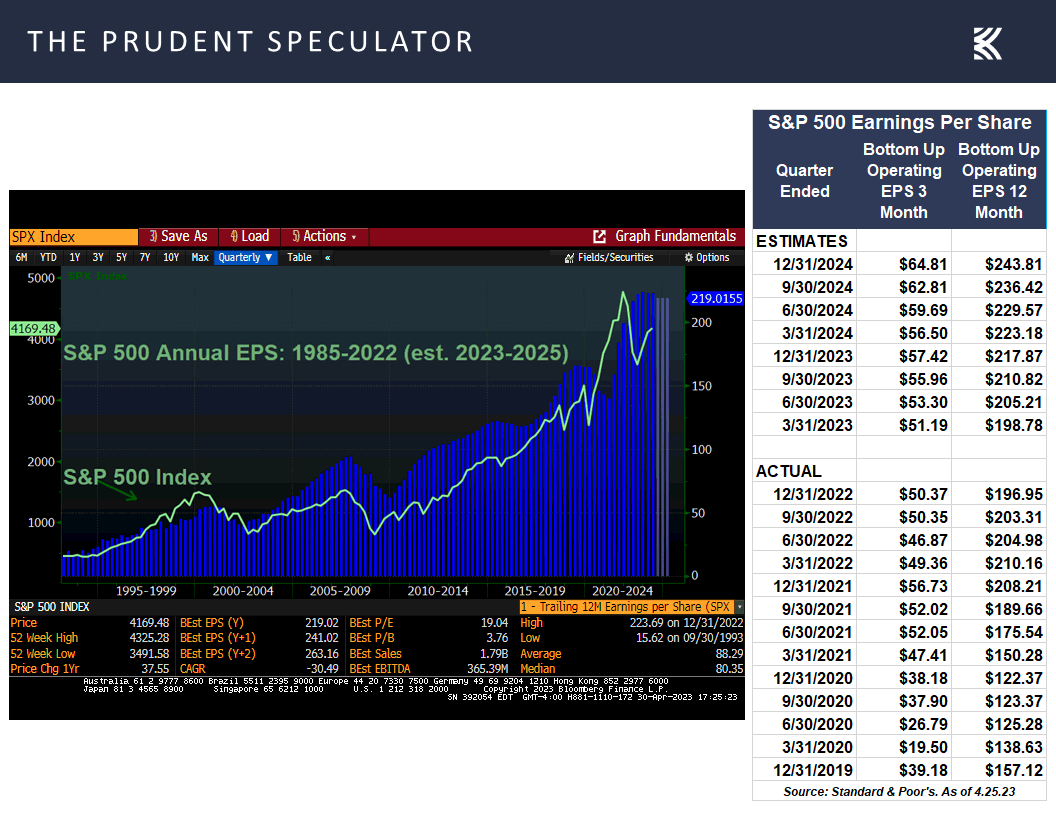

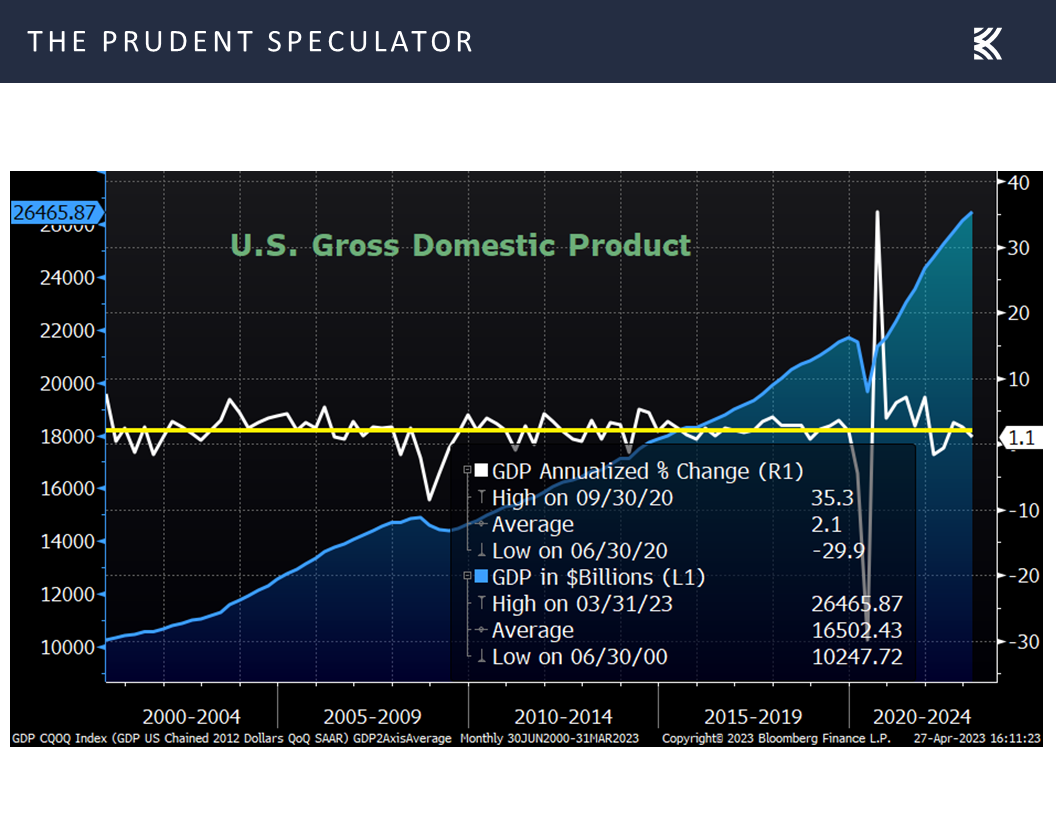

It isn’t rocket science. After all, U.S. GDP (the blue line in the chart below) on a nominal (absolute) basis grows over time, with only two dips over the past 25 years. In fact, in the first quarter of 2023, nominal GDP rose to $26.465 trillion, up an impressive 7.0% on a year-over-year basis, even as so many have been concerned about a recession.

Econ Data – Mixed Numbers; 1.7% Q2 GDP Growth Projected

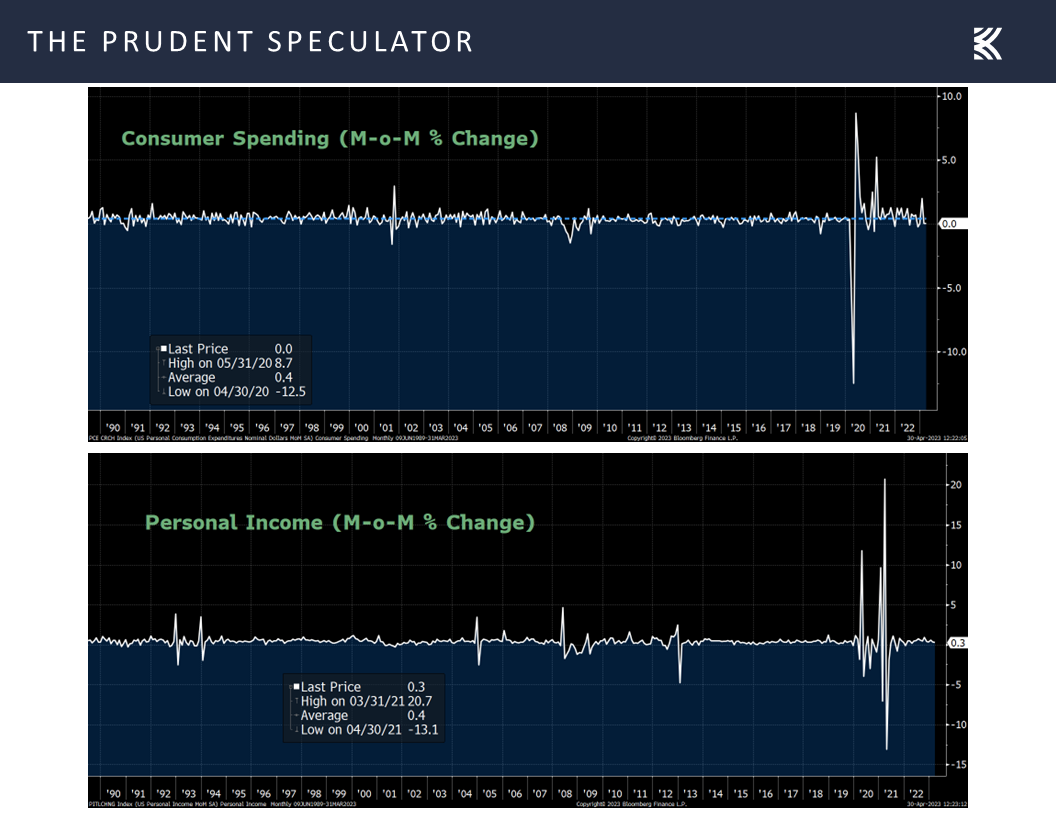

Yes, the economy grew only 1.1% in Q1 2023 on an inflation-adjusted basis, while consumer spending and personal income tallies for March were below average,

but Q1 report cards from Corporate America generally have been terrific. In fact, of the 265 members of the S&P 500 to have announced results thus far, a much-greater-than-usual 80.2% have topped bottom-line expectations, while 66.2% have beaten top-line projections.

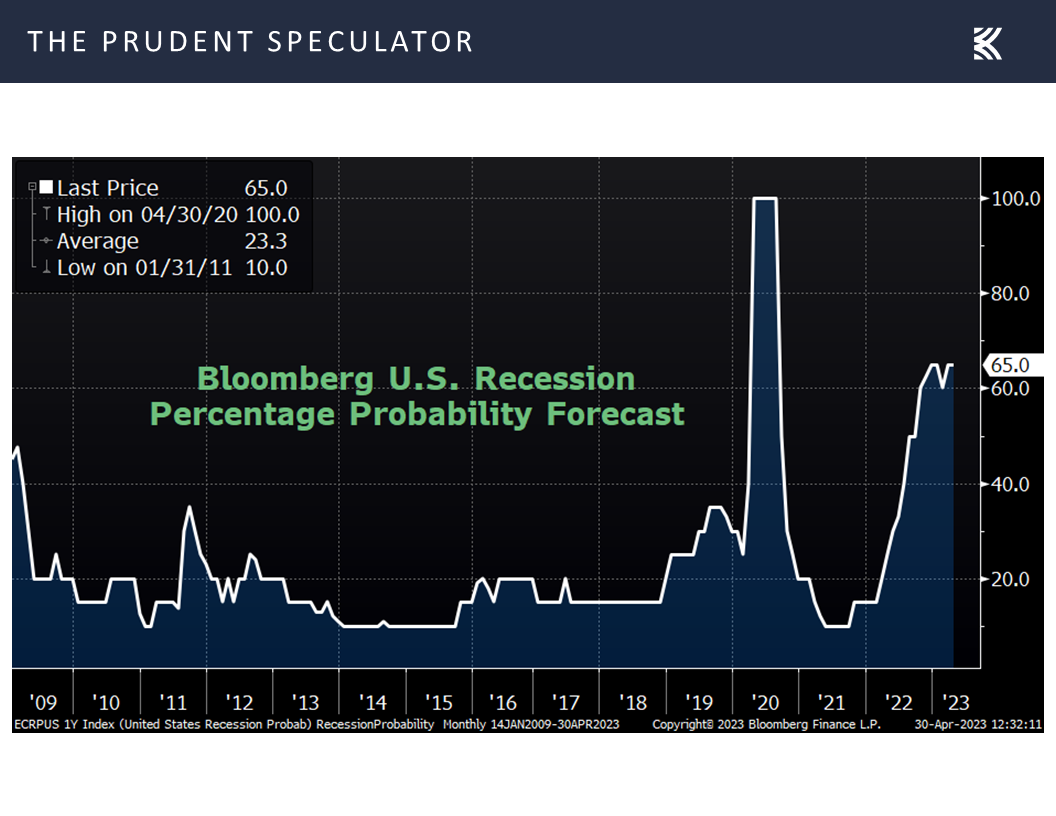

To be sure, market reactions to the Q1 results have not always been positive as management teams have been cautious in their outlooks. That is not surprising in that the odds of an economic contraction over the next 12 months, as calculated by Bloomberg, remain at 65%,

with the latest readings on the mood of the consumer coming in at levels that aren’t exactly inspiring a lot of confidence.

with the latest readings on the mood of the consumer coming in at levels that aren’t exactly inspiring a lot of confidence.

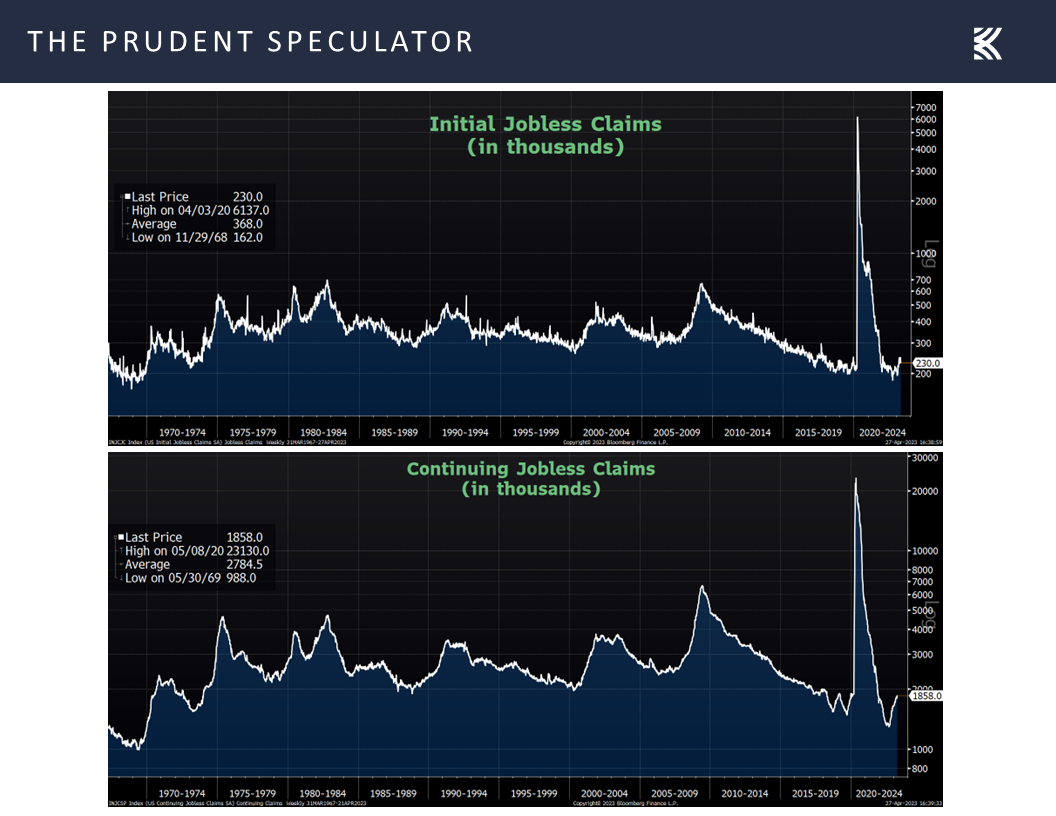

…while the labor picture remains healthy, with a dip in the number of initial jobless claims in the latest week,

and the initial estimate for Q2 inflation-adjusted GDP growth from the Atlanta Fed stood at a solid 1.7%.

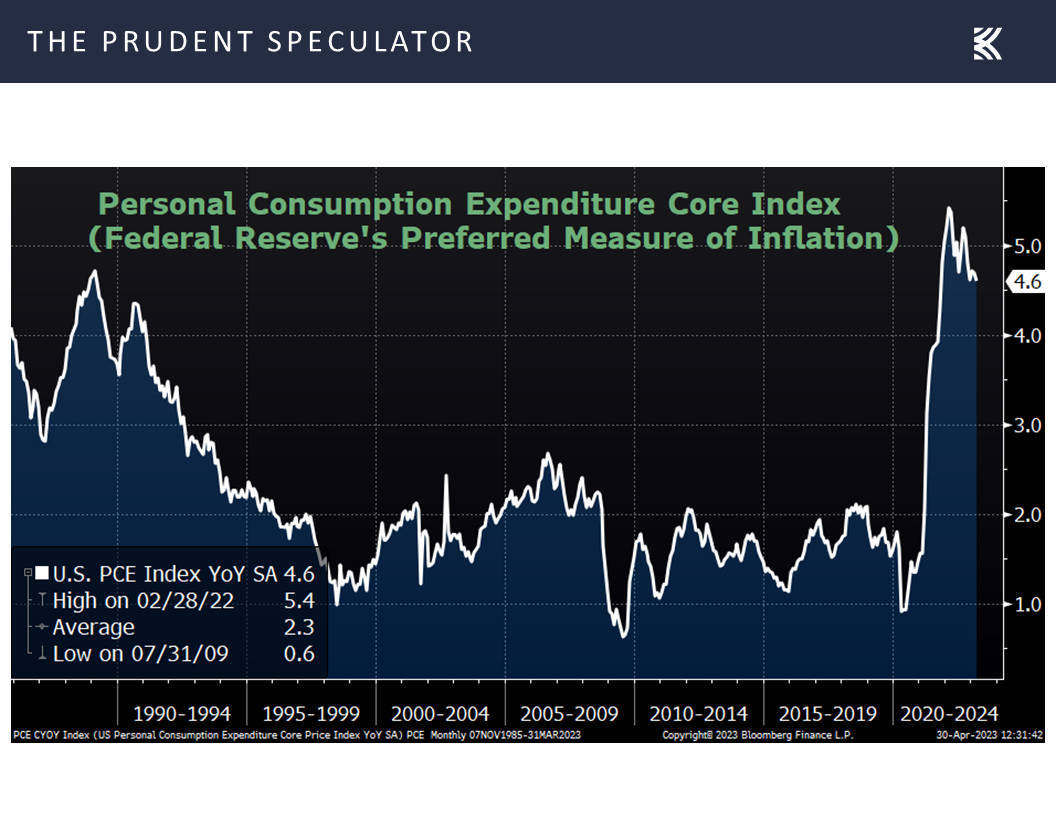

No doubt, there is plenty about which to be concerned, including the drama around the future of First Republic Bank and a Federal Open Market Committee Meeting this week. Jerome H. Powell & Co. are expected to again hike their target for the Fed Funds rate, given that inflation remains elevated, with the core personal consumption expenditures (PCE) index rising 4.6% in March.

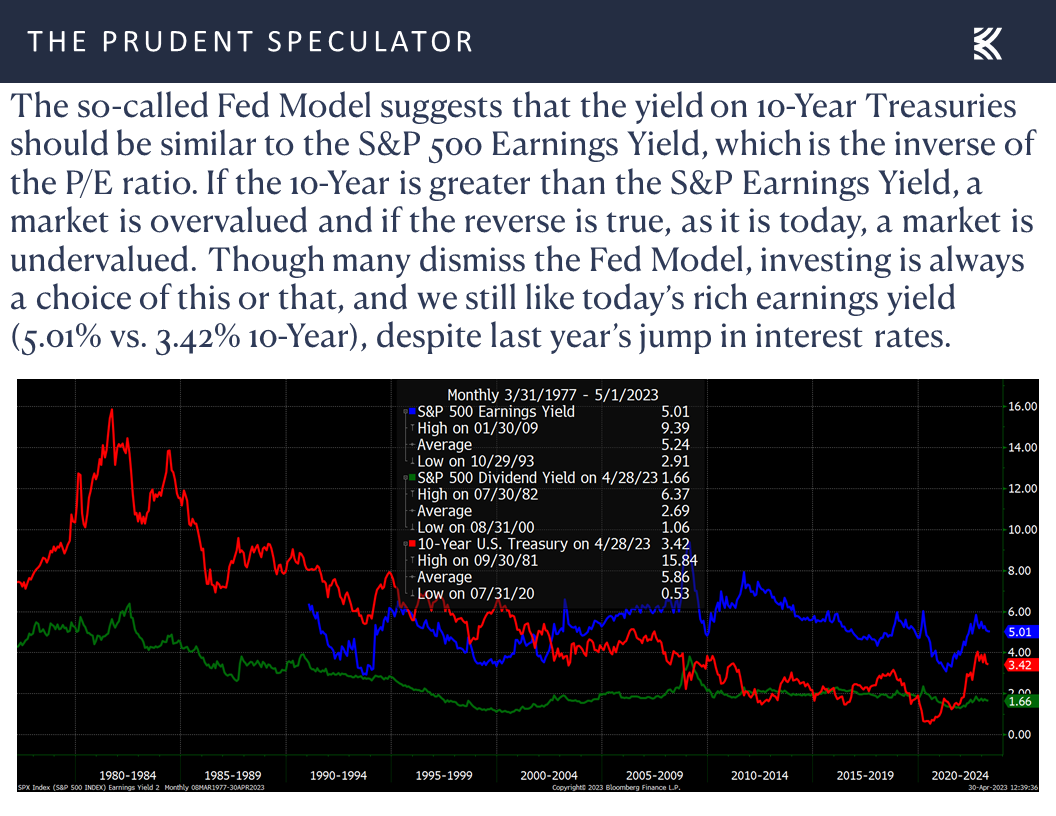

Interest Rates – 10-Year Yield Low By Historical Standards

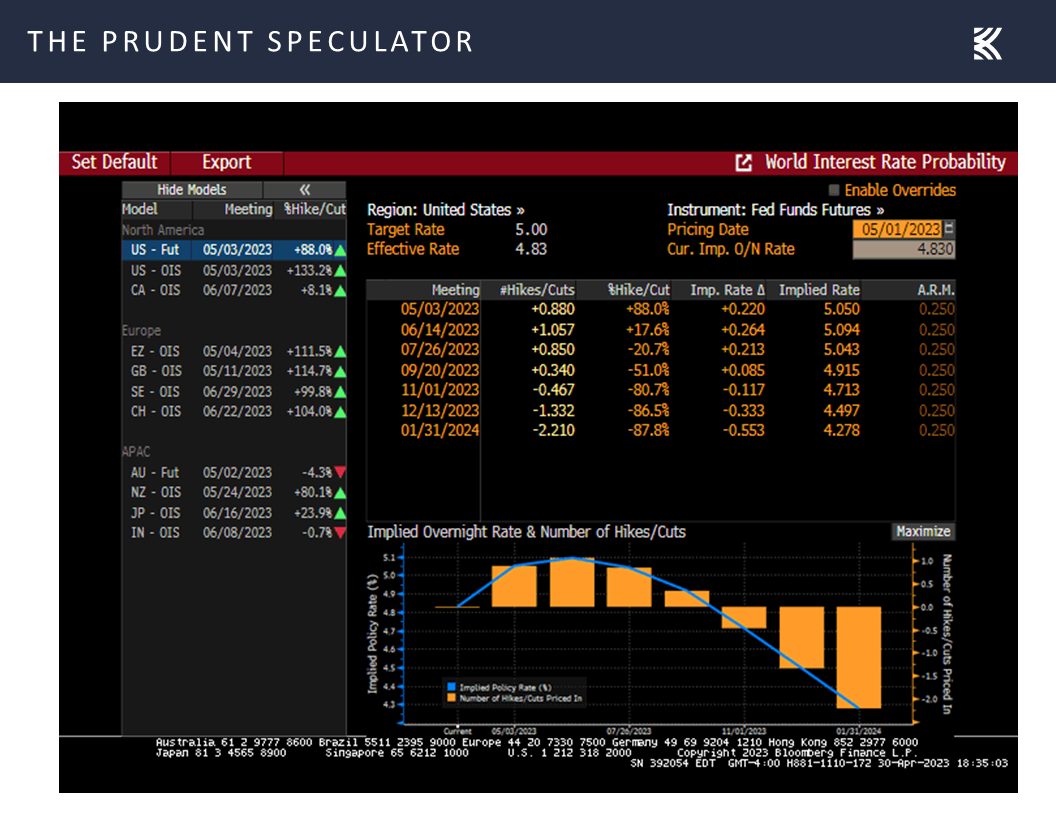

A 25-basis-point increase is generally the market view, as evidenced by the Fed Funds Futures, but that gauge is looking for a peak in the Fed Funds rate at 5.09%, with cuts beginning in the not-too-distant future that will take the important lending rate down to 4.50% by the end of 2023.

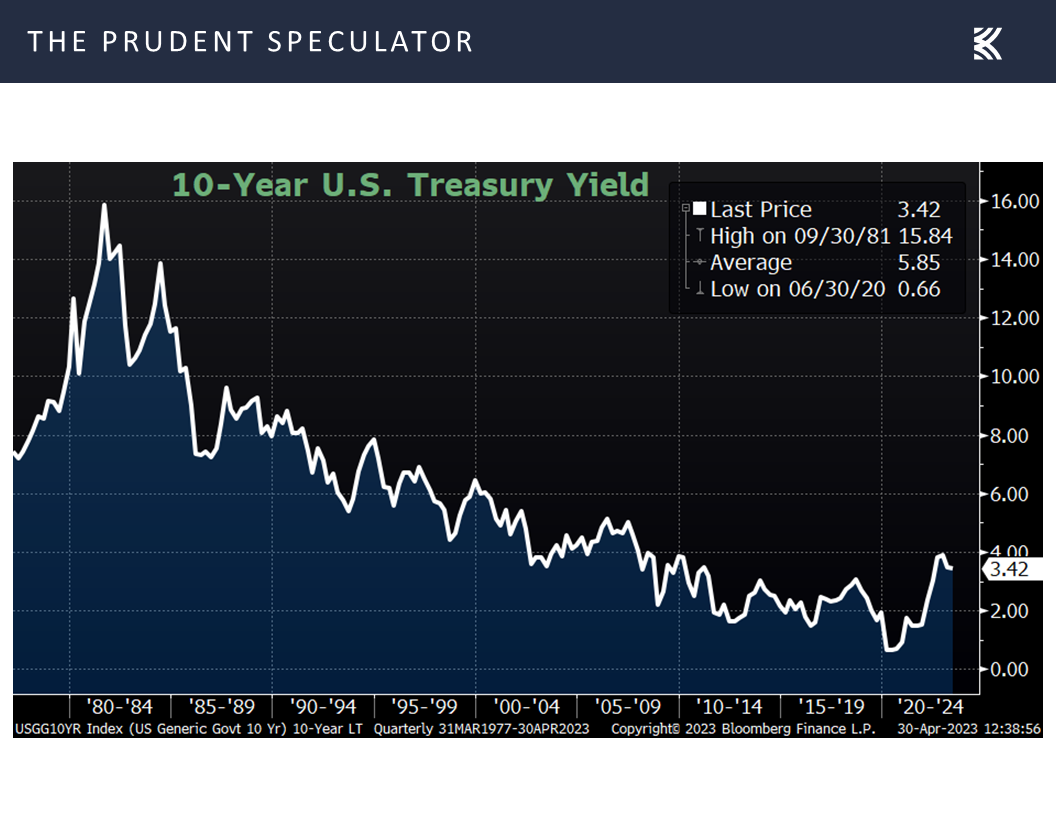

Certainly, interest rates are a critical input into the equity market equation, but the current 3.42% yield on the benchmark 10-Year U.S. Treasury remains well below the 5.85% average since The Prudent Speculator was launched in 1977,

while stocks in general continue to be attractively valued, in our view, given that the earnings yield (the inverse of the P/E ratio) on the S&P 500 still compares favorably.

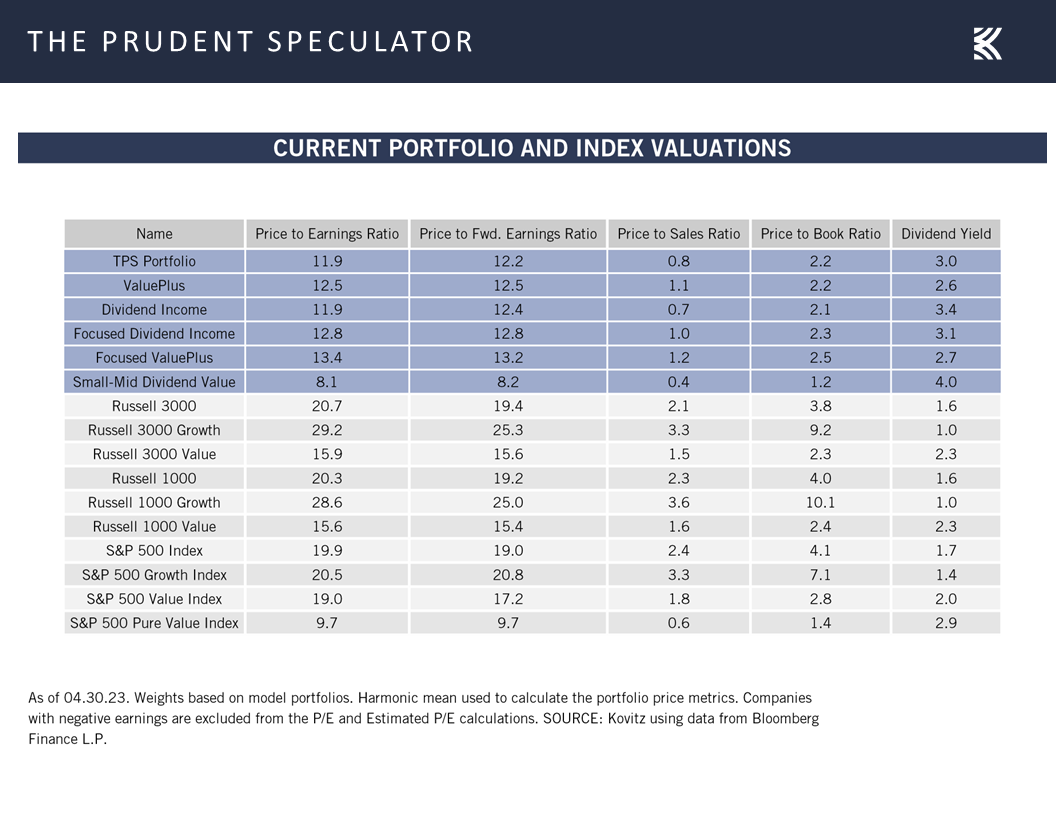

Valuations – Liking the Multiples on our Portfolios

More importantly, we like the inexpensive valuation metrics associated with our broadly diversified portfolios of what we believe to be undervalued stocks.

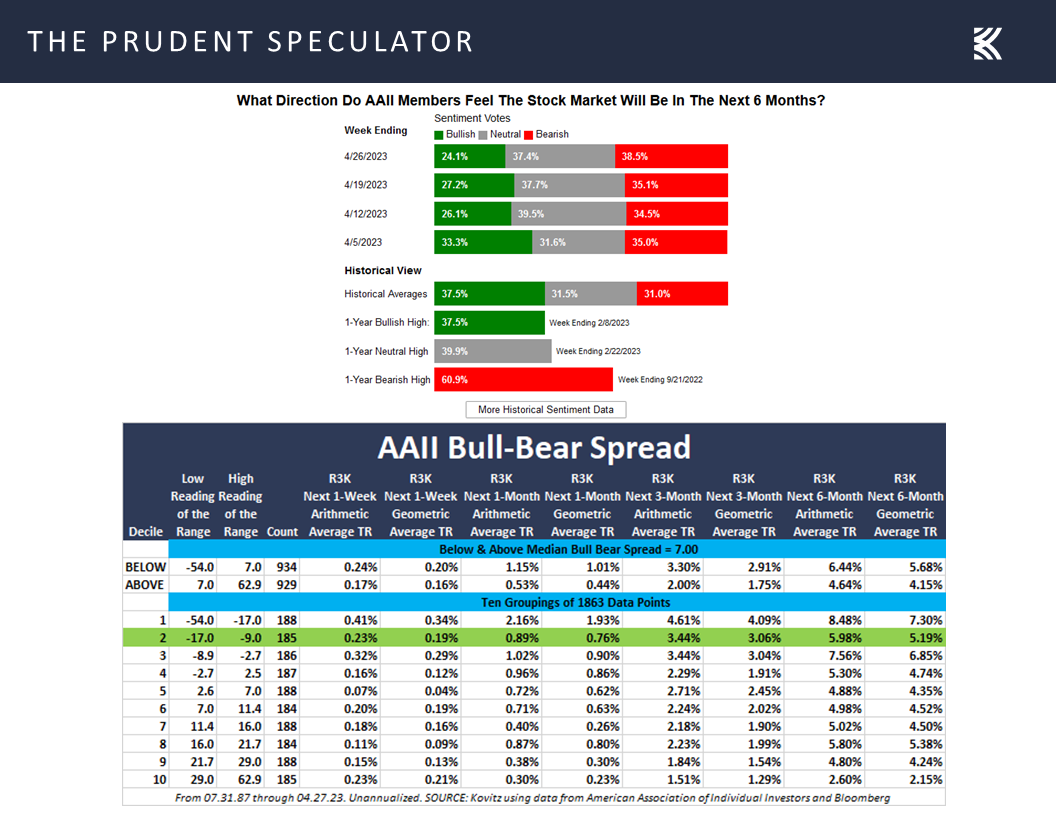

Contrarian Sentiment – AAII Still Very Pessimistic

As always. we are braced for downside volatility, but we like that folks on Main Street are unusually pessimistic today, with the latest weekly AAII Bull-Bear Sentiment gauge (a strong contrarian measure) showing 24.1% Bulls and 38.5% Bears,

Stock Market News: Updates on eighteen stocks across thirteen different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

GDP Growth, Dividend Stocks on the Rise and Interest Rates

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss GDP Growth, Dividend Stocks, Interest Rates, Valuations and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Probabilities – The Longer the Hold, the Less the Chance of Loss

Growth – GDP, Corporate Profits and Dividends Rise Over Time

Econ Data – Mixed Numbers; 1.7% Q2 GDP Growth Projected

Interest Rates – 10-Year Yield Low By Historical Standards

Valuations – Liking the Multiples on our Portfolios

Contrarian Sentiment – AAII Still Very Pessimistic

Stock News – Updates on eighteen stocks across thirteen different sectors

Probabilities – The Longer the Hold, the Less the Chance of Loss

It was another roller-coaster ride with a mid-week plunge giving way to a big month-end rally that pushed the major market averages into the green for the past five trading sessions. Certainly, it doesn’t always work out that holding for a week will quickly recoup one or two days of losses, but history does suggest that patience is a virtue when it comes to investing.

Indeed, having been in Sin City last week for the MoneyShow, there is no better place to emphasize the probabilities of winning. After all, baccarat, blackjack, craps or roulette offer the best odds and slot machines generally the worst chance of winning, but the house always has the edge. Play long enough and you will lose.

Contrast that with the equities market, where the chance of making money in Value Stocks and Dividend Payers increases the longer the hold. True, there is no assurance that the past is prologue, but looking at data since 1927 from Professors Eugene F. Fama and Kenneth R. French shows the chance of a positive return rises from an already impressive 63% for a one-month hold to 73.0% for Value and 75.6% for Dividend Payers for a one-year hold. And the chance of making money rises to more than 96% for 10-year holding periods.

Certainly, there have been plenty of ups and downs along the way, but stocks have proved very rewarding for those who remember that the secret to success is not to get scared out of them.

Growth – GDP, Corporate Profits and Dividends Rise Over Time

The reason that stocks have performed so well is that companies generally become more valuable over time, given that corporate profits have grown,

and dividend payouts have risen.

It isn’t rocket science. After all, U.S. GDP (the blue line in the chart below) on a nominal (absolute) basis grows over time, with only two dips over the past 25 years. In fact, in the first quarter of 2023, nominal GDP rose to $26.465 trillion, up an impressive 7.0% on a year-over-year basis, even as so many have been concerned about a recession.

Econ Data – Mixed Numbers; 1.7% Q2 GDP Growth Projected

Yes, the economy grew only 1.1% in Q1 2023 on an inflation-adjusted basis, while consumer spending and personal income tallies for March were below average,

but Q1 report cards from Corporate America generally have been terrific. In fact, of the 265 members of the S&P 500 to have announced results thus far, a much-greater-than-usual 80.2% have topped bottom-line expectations, while 66.2% have beaten top-line projections.

To be sure, market reactions to the Q1 results have not always been positive as management teams have been cautious in their outlooks. That is not surprising in that the odds of an economic contraction over the next 12 months, as calculated by Bloomberg, remain at 65%,

with the latest readings on the mood of the consumer coming in at levels that aren’t exactly inspiring a lot of confidence.

with the latest readings on the mood of the consumer coming in at levels that aren’t exactly inspiring a lot of confidence.

…while the labor picture remains healthy, with a dip in the number of initial jobless claims in the latest week,

and the initial estimate for Q2 inflation-adjusted GDP growth from the Atlanta Fed stood at a solid 1.7%.

No doubt, there is plenty about which to be concerned, including the drama around the future of First Republic Bank and a Federal Open Market Committee Meeting this week. Jerome H. Powell & Co. are expected to again hike their target for the Fed Funds rate, given that inflation remains elevated, with the core personal consumption expenditures (PCE) index rising 4.6% in March.

Interest Rates – 10-Year Yield Low By Historical Standards

A 25-basis-point increase is generally the market view, as evidenced by the Fed Funds Futures, but that gauge is looking for a peak in the Fed Funds rate at 5.09%, with cuts beginning in the not-too-distant future that will take the important lending rate down to 4.50% by the end of 2023.

Certainly, interest rates are a critical input into the equity market equation, but the current 3.42% yield on the benchmark 10-Year U.S. Treasury remains well below the 5.85% average since The Prudent Speculator was launched in 1977,

while stocks in general continue to be attractively valued, in our view, given that the earnings yield (the inverse of the P/E ratio) on the S&P 500 still compares favorably.

Valuations – Liking the Multiples on our Portfolios

More importantly, we like the inexpensive valuation metrics associated with our broadly diversified portfolios of what we believe to be undervalued stocks.

Contrarian Sentiment – AAII Still Very Pessimistic

As always. we are braced for downside volatility, but we like that folks on Main Street are unusually pessimistic today, with the latest weekly AAII Bull-Bear Sentiment gauge (a strong contrarian measure) showing 24.1% Bulls and 38.5% Bears,

Stock Market News: Updates on eighteen stocks across thirteen different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.