The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the GDP Growth, Inflation, Valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

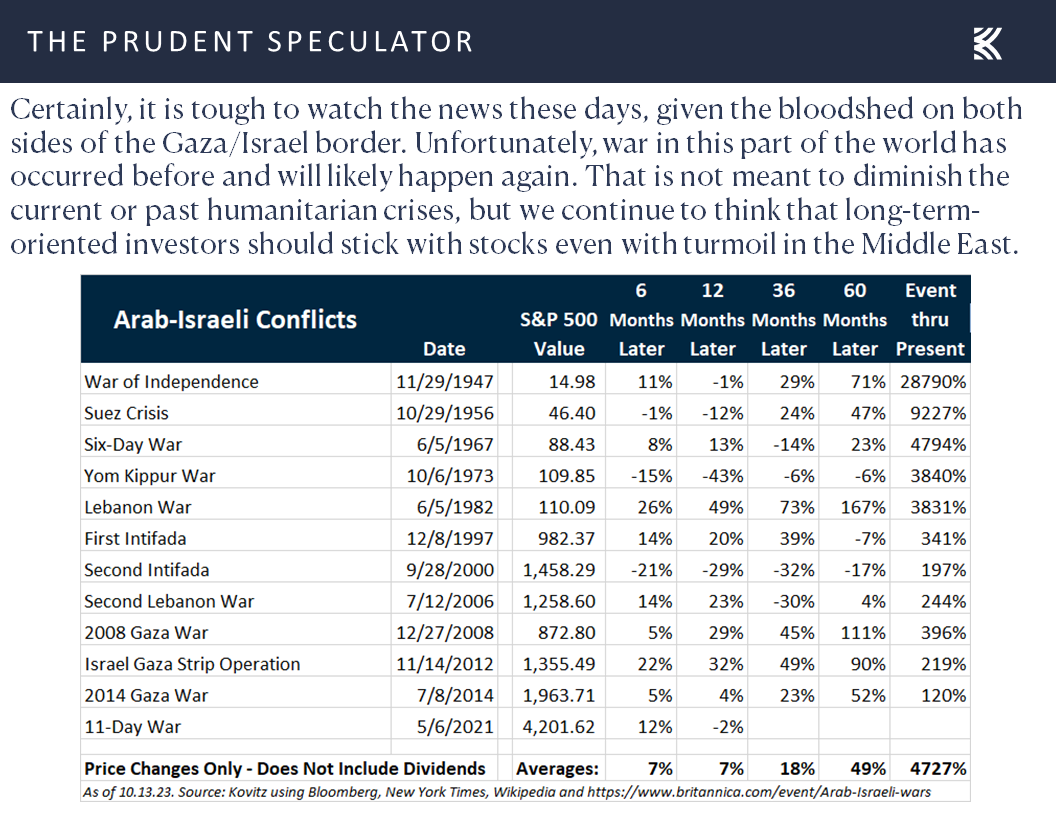

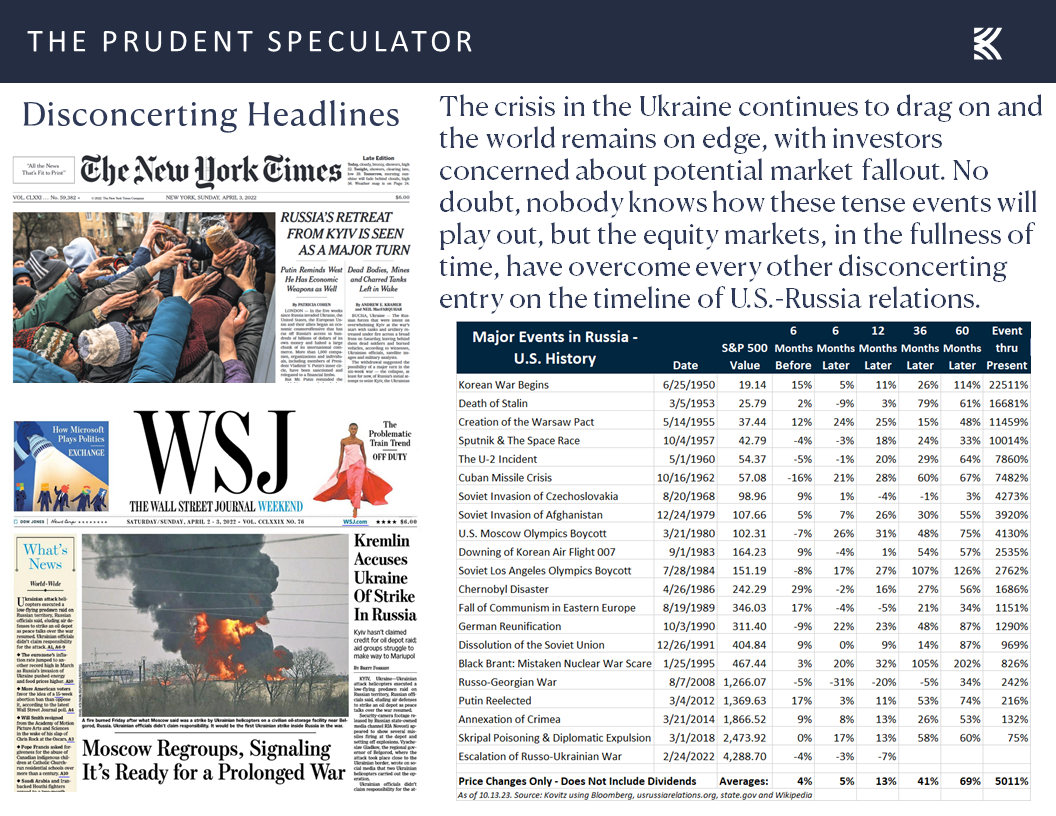

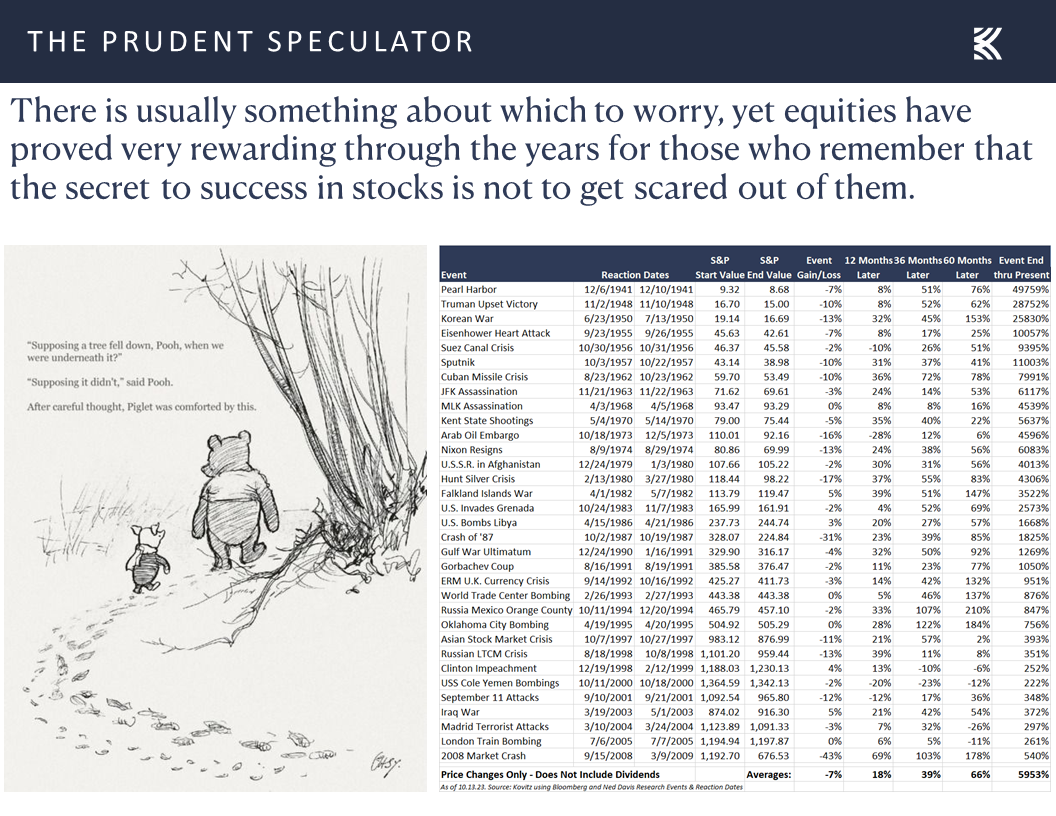

Historical Perspective – Stocks Have Persevered Through Plenty of Disconcerting Events

Growth – GDP, Corporate Profits and Stock Prices Have Marched Higher Over Time

Econ Update – Sentiment Falls; GDP Growth Projections Remain Strong

Inflation – Mixed Numbers; Stocks a Good Hedge Against Higher CPI

Valuations – Value Stocks Still Inexpensively Priced

Stock News – Updates on JPM, C, BLK, PNC, MDT, ABT, ZBH & XOM

Historical Perspective – Stocks Have Persevered Through Plenty of Disconcerting Events

not to mention the ongoing war in Ukraine,

but our job is to unemotionally navigate the equity markets through thick and thin. Helping us stay on an even keel is advice from Vannevar Bush. The American engineer and inventor said, “Fear cannot be banished, but it can be calm and without panic; it can be mitigated by reason and evaluation,” with the performance of stocks during and following prior turbulent periods providing valuable perspective.

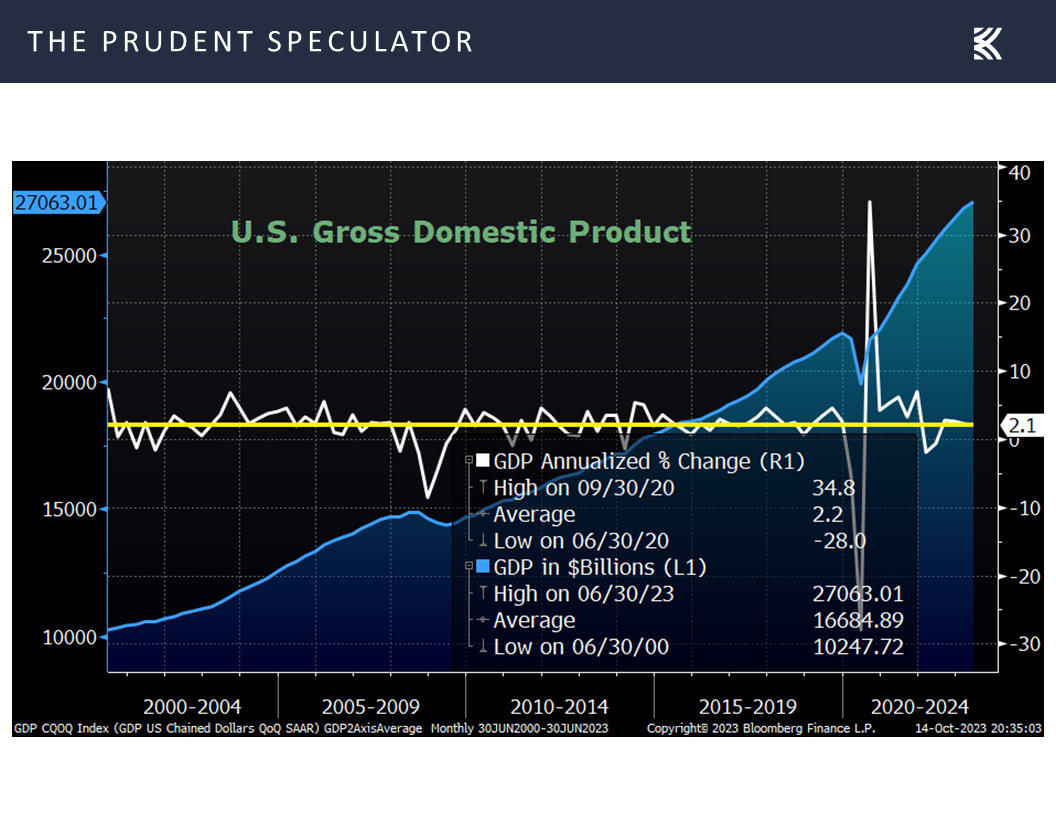

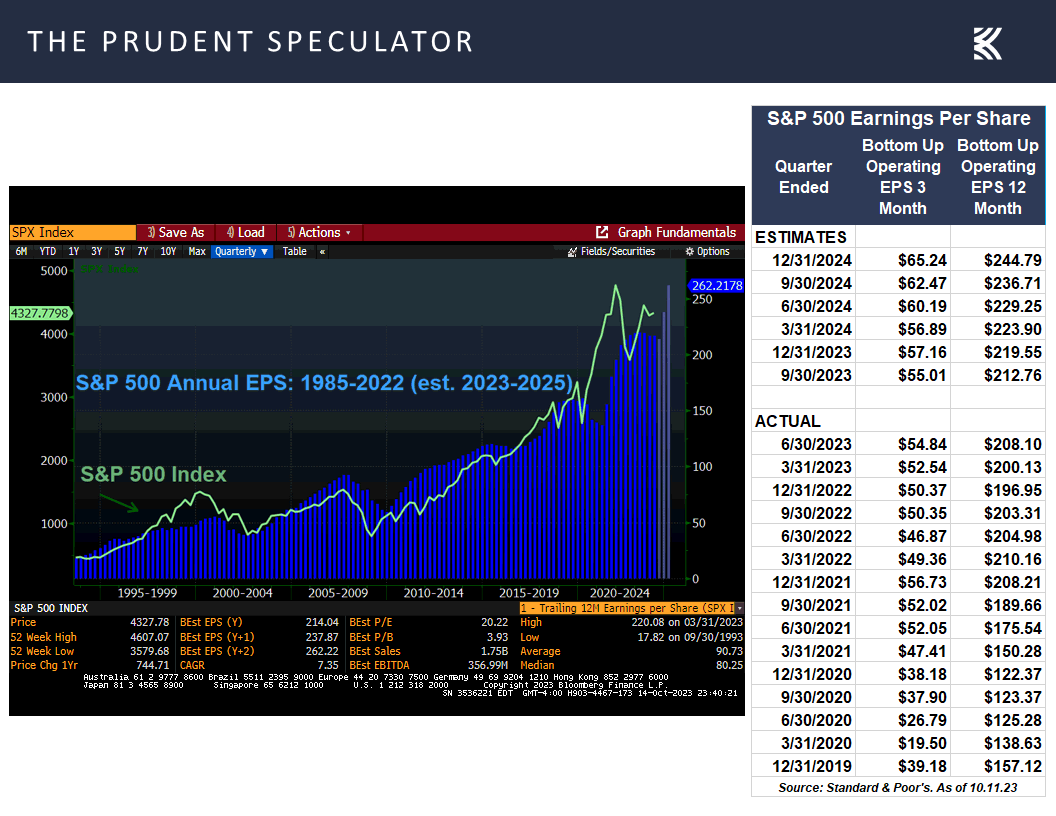

Growth – GDP, Corporate Profits and Stock Prices Have Marched Higher Over Time

To be sure, past performance is no guarantee of future returns, but the historical probabilities that those who invest in Value Stocks and Dividend Payers will enjoy very favorable returns over the long term (and even over the short and intermediate terms) are impressive,

as the U.S. economy, despite a few downticks along the way, has grown over time,

propelling corporate profits and equity prices steadily (and not so steadily) higher.

Econ Update – Sentiment Falls; GDP Growth Projections Remain Strong

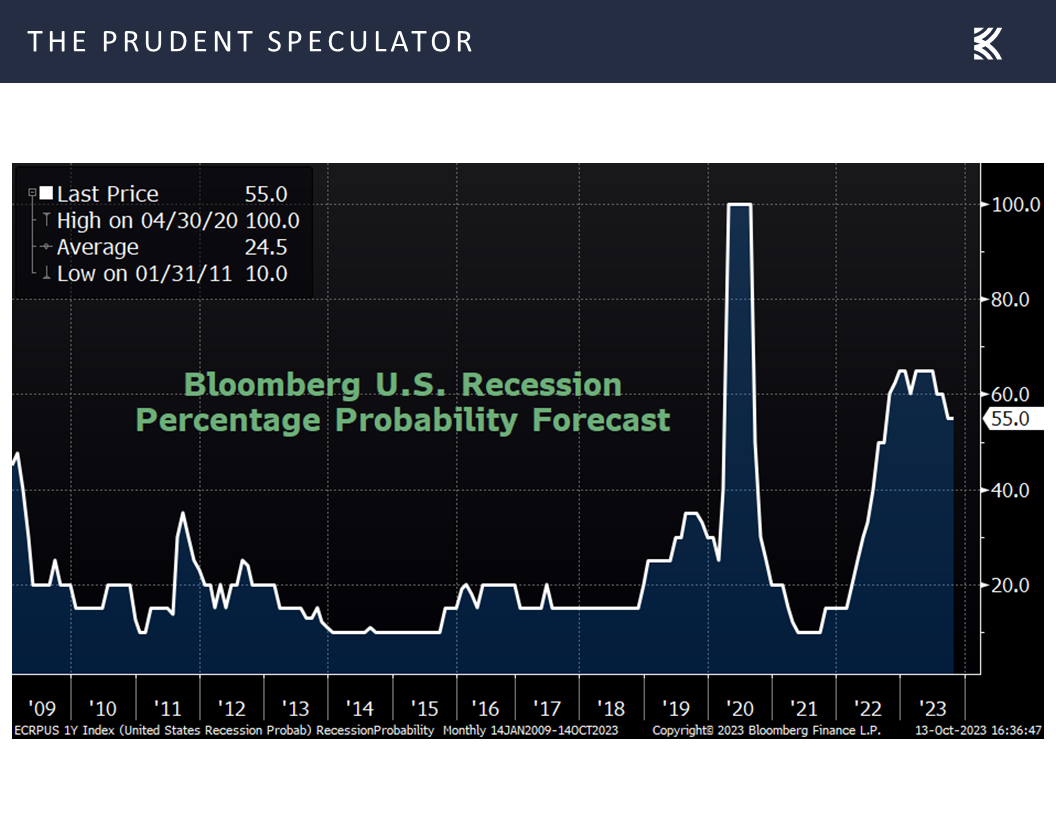

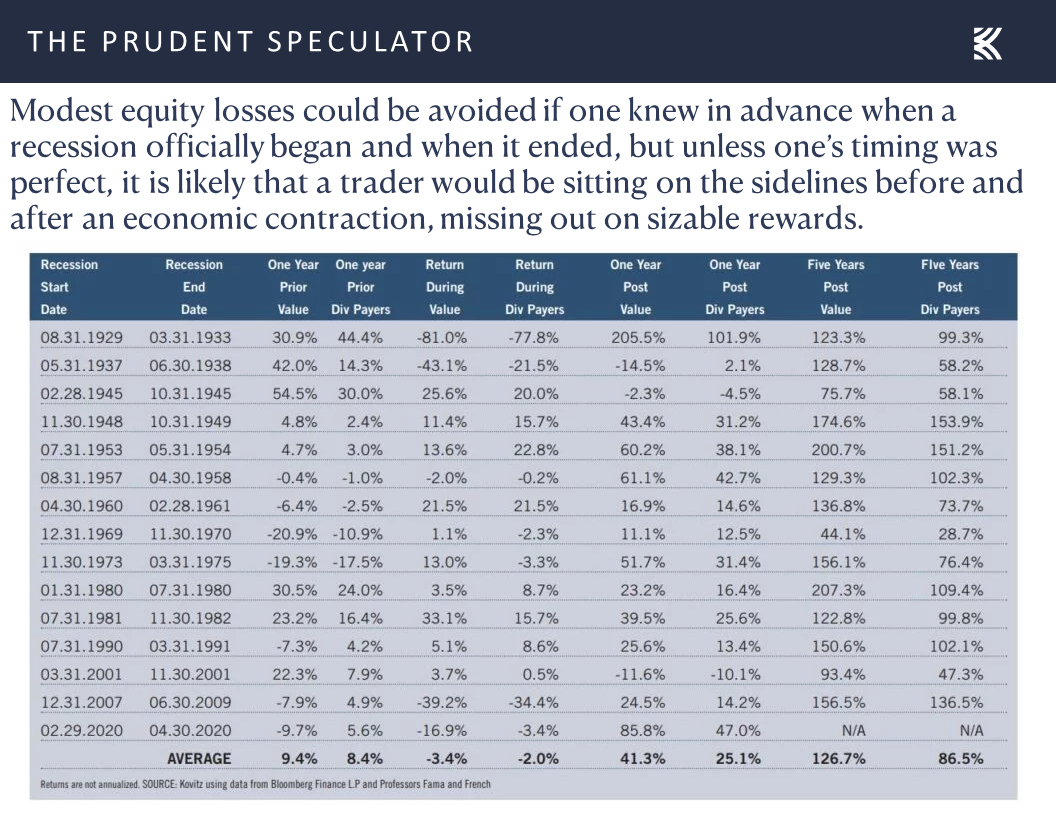

Of course, there will always be concern that an interruption in economic growth is around the corner, with the current odds of recession over the next 12 months as tabulated by Bloomberg continuing to reside at a very elevated 55%,

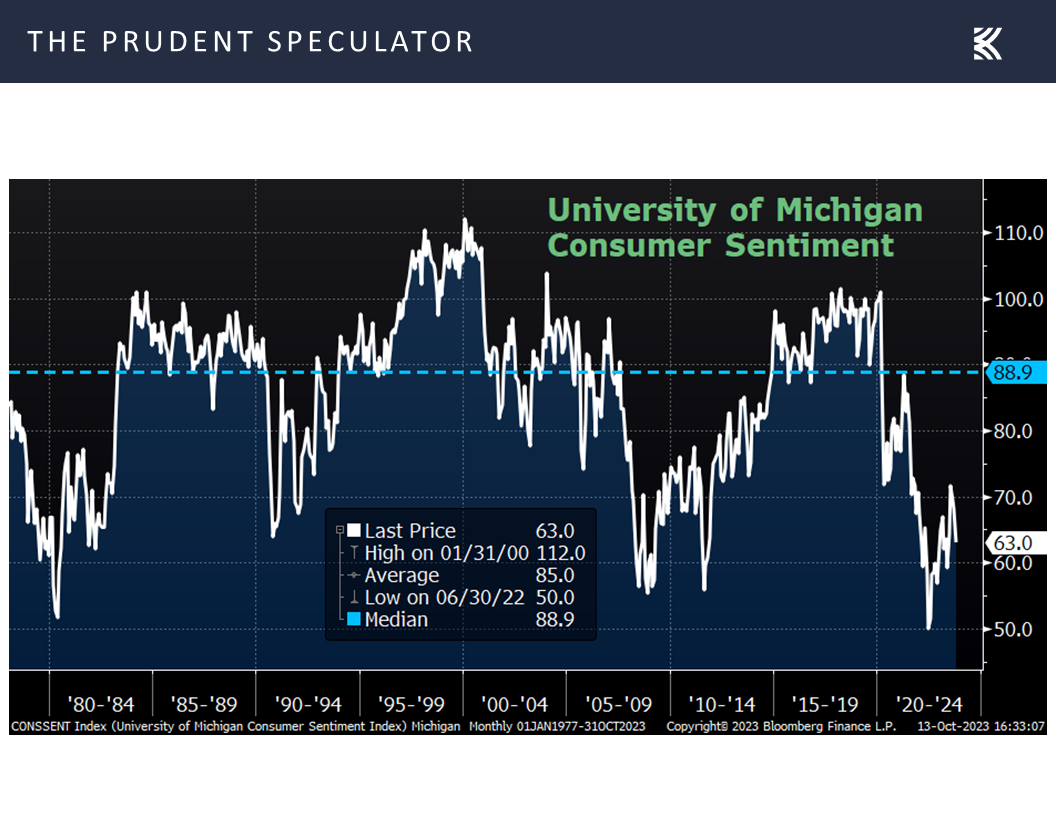

as the latest read on Main Street sentiment from the University of Michigan came in below expectations and well below average,

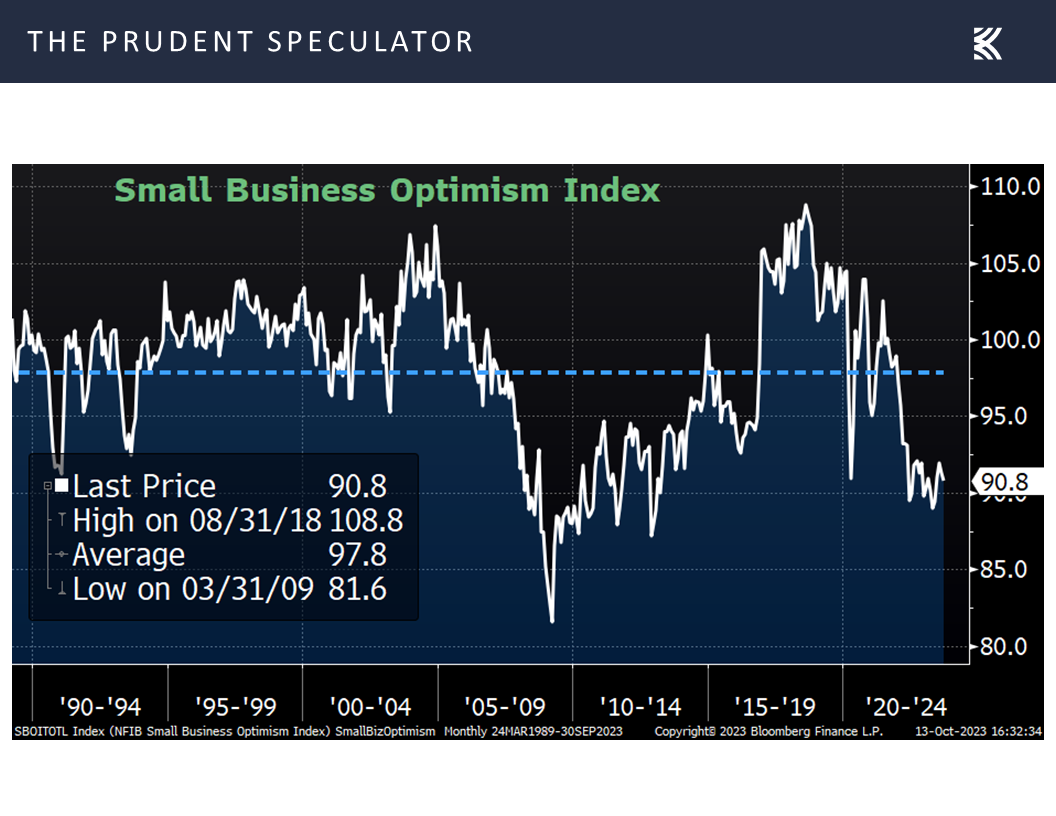

with it a similar story for optimism from small businesses.

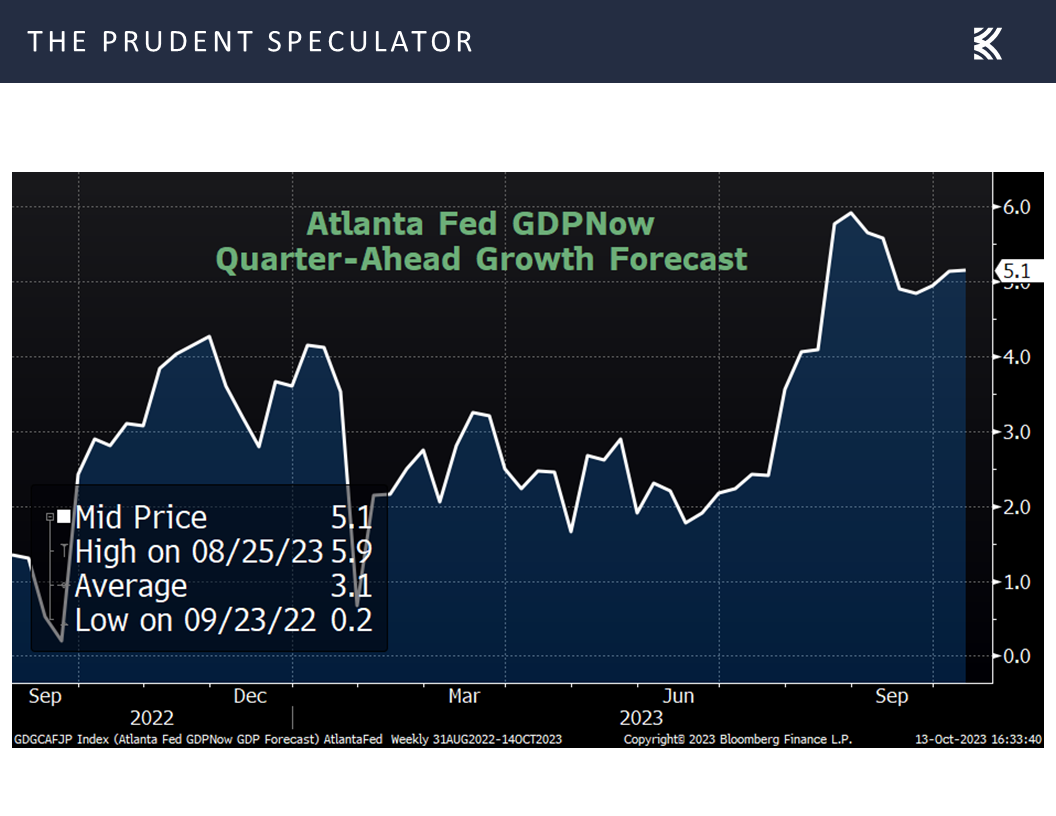

On the other hand, the latest estimate for Q3 real (inflation-adjusted) GDP growth from the Atlanta Fed was a whopping 5.1%,

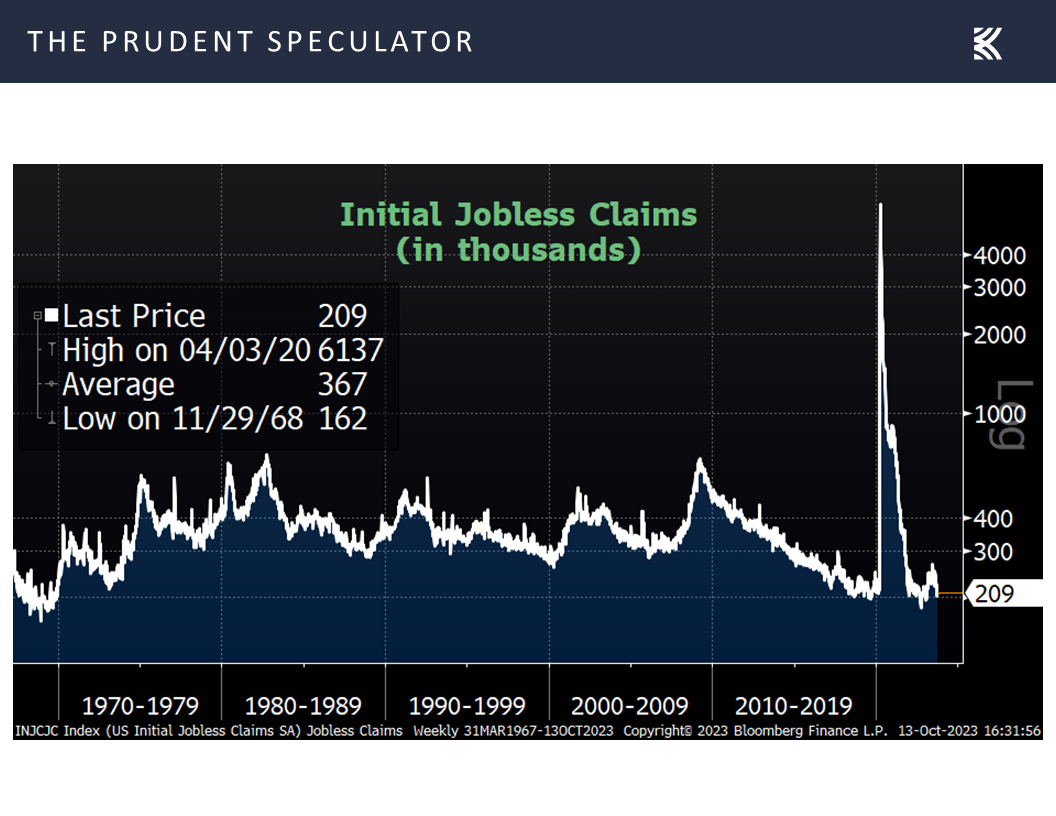

as the labor situation remains very robust with first-time filings for unemployment benefits continuing to bounce around near multi-generational lows.

Needless to say, the economic outlook is uncertain, but we continue to take comfort in the historical evidence on equity returns and recessions. Indeed, unless one could somehow exit stocks at the start of a contraction and get back in at the precise end, there is a very strong likelihood that attempting to market time would prove hazardous to one’s wealth, especially given the stellar gains, on average, in the 12 months following the end of a recession!

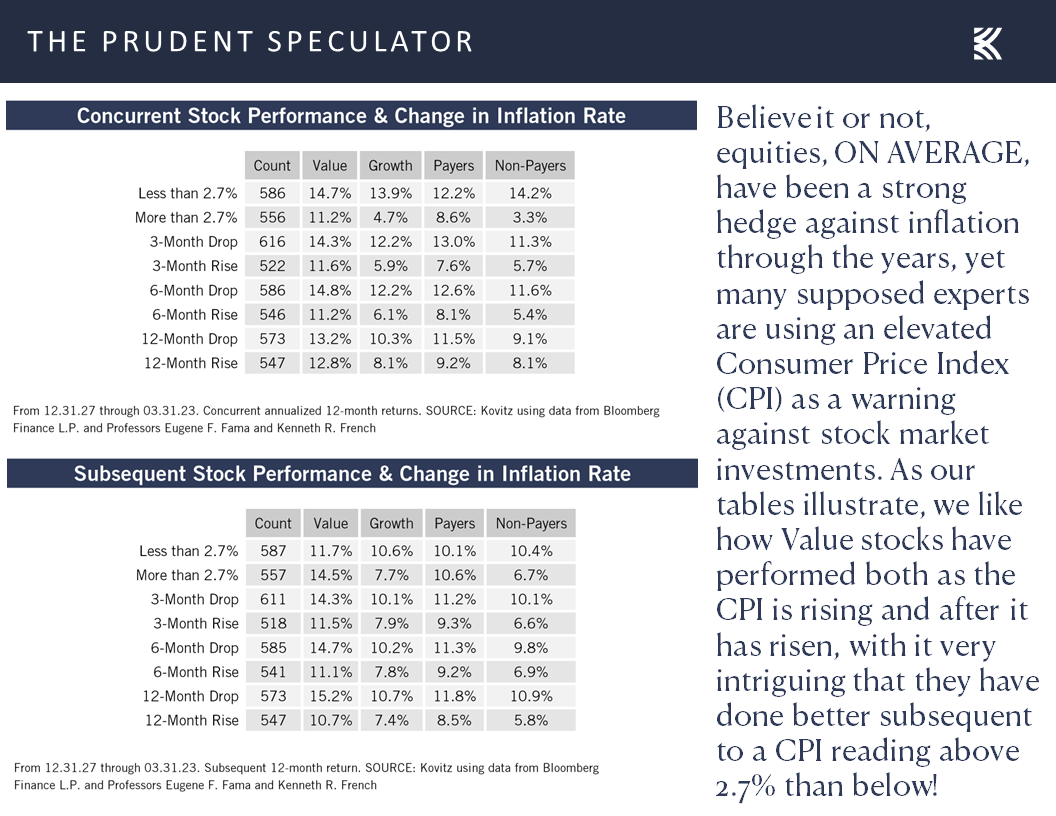

Inflation – Mixed Numbers; Stocks a Good Hedge Against Higher CPI

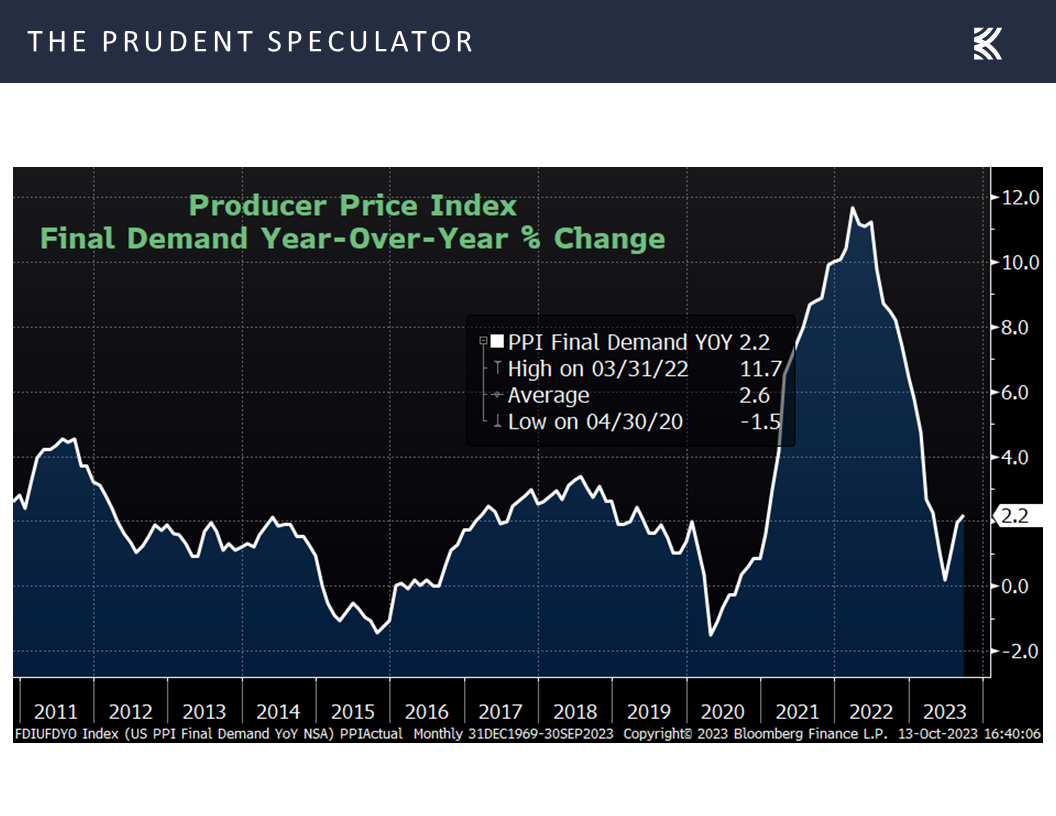

Economic growth is just one of the many worries (there are always concerns) with which investors must contend these days. Another is inflation, with the Producer Price Index (PPI) for September rising to 2.2% on a year-over-year basis, above projections of a 1.6% advance,

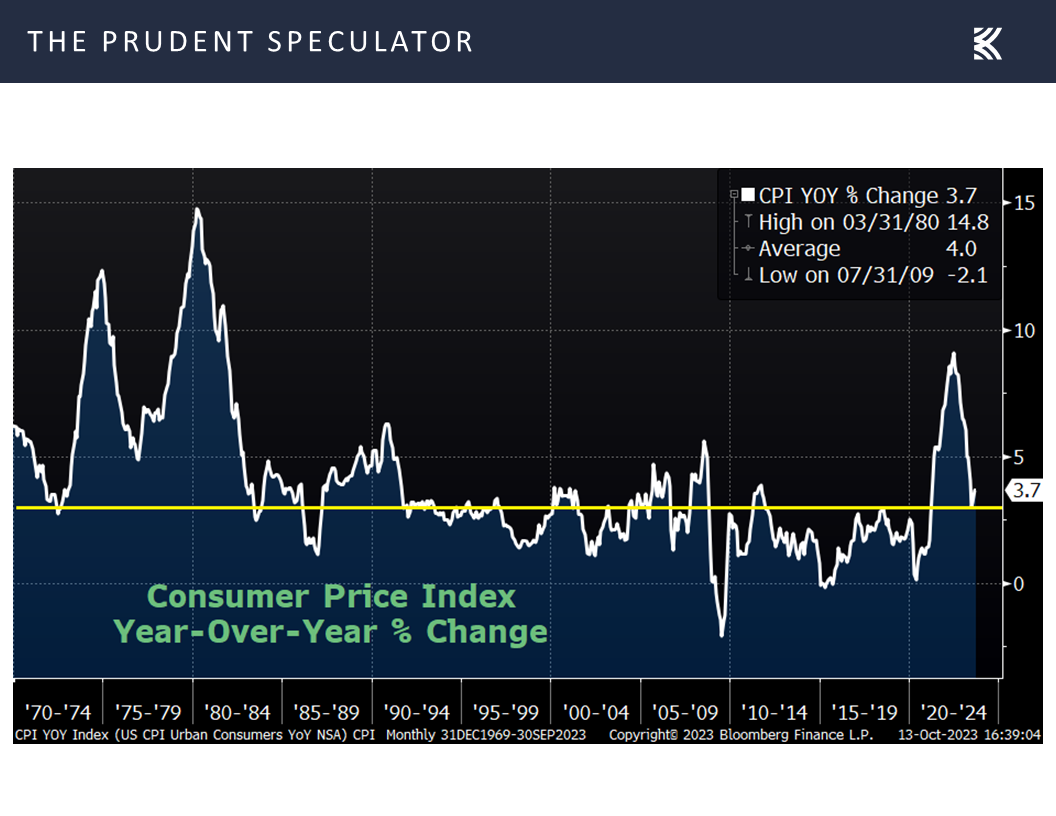

and the Consumer Price Index (CPI) climbing 3.7% year-over-year, also slightly above expectations,

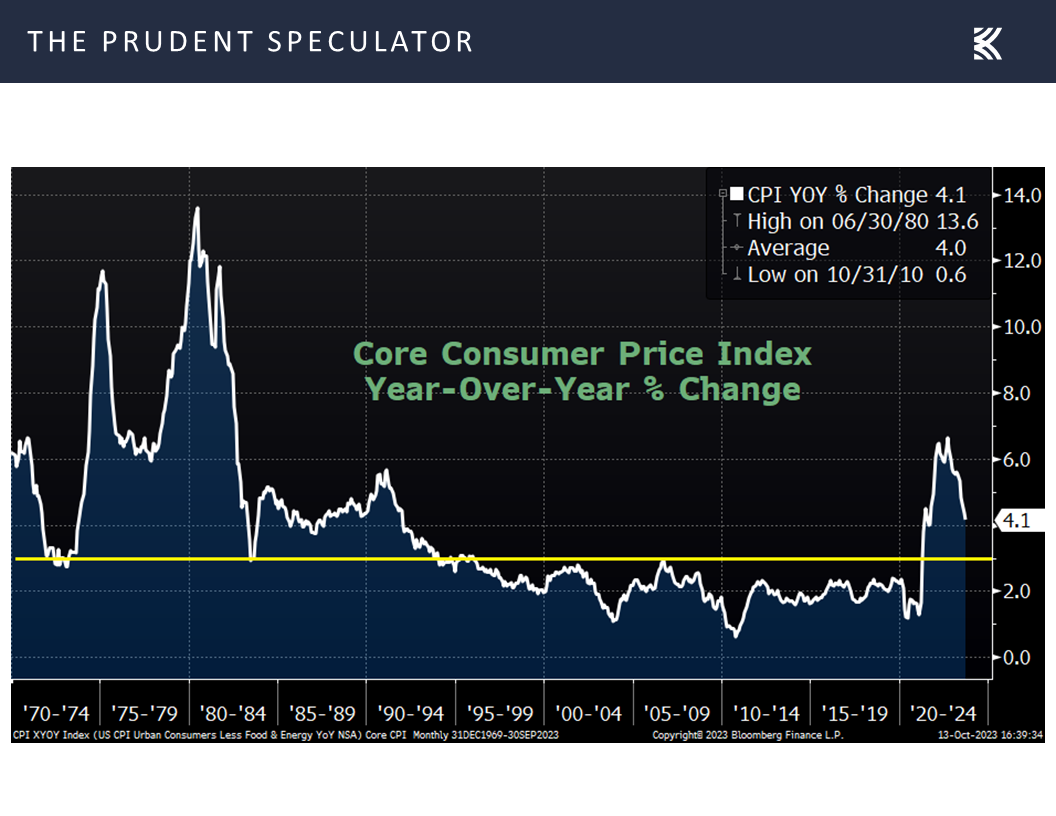

though the increase in the core CPI (excludes volatile food and energy prices) edged down to 4.1% last month from 4.3% in August.

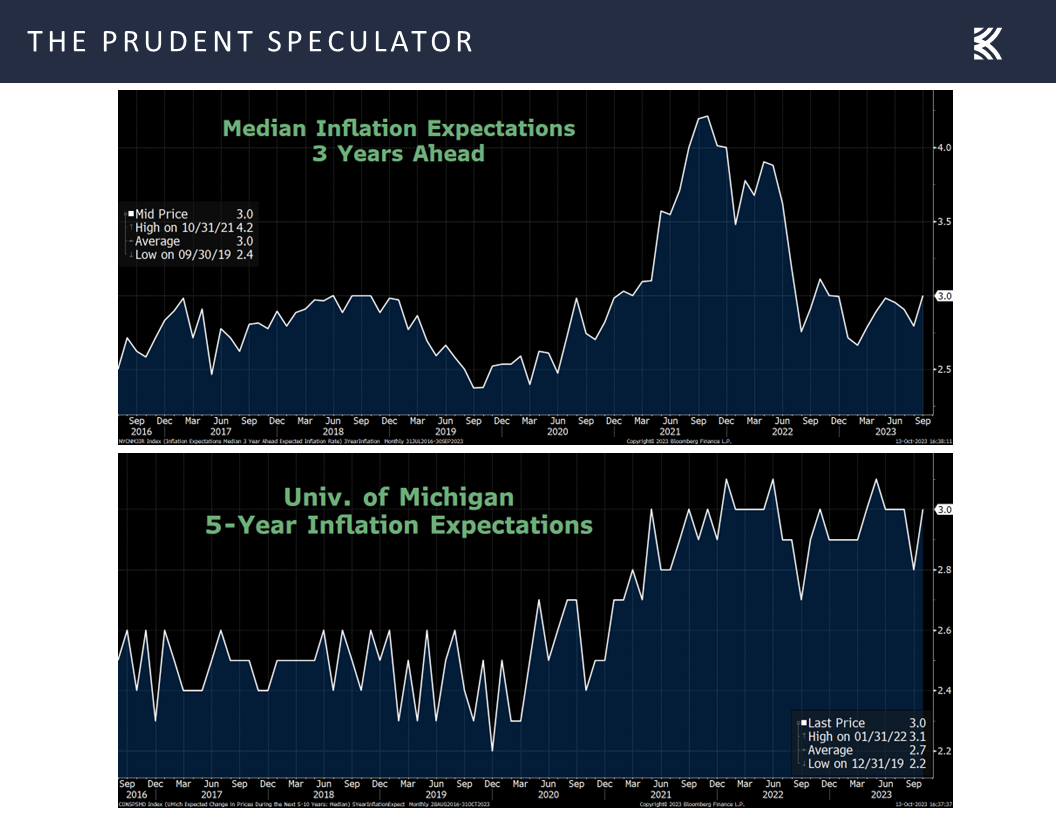

Still, there was some consternation that 3- and 5-year CPI expectations ticked up,

even as stocks historically have proved to be a very good hedge against inflation,

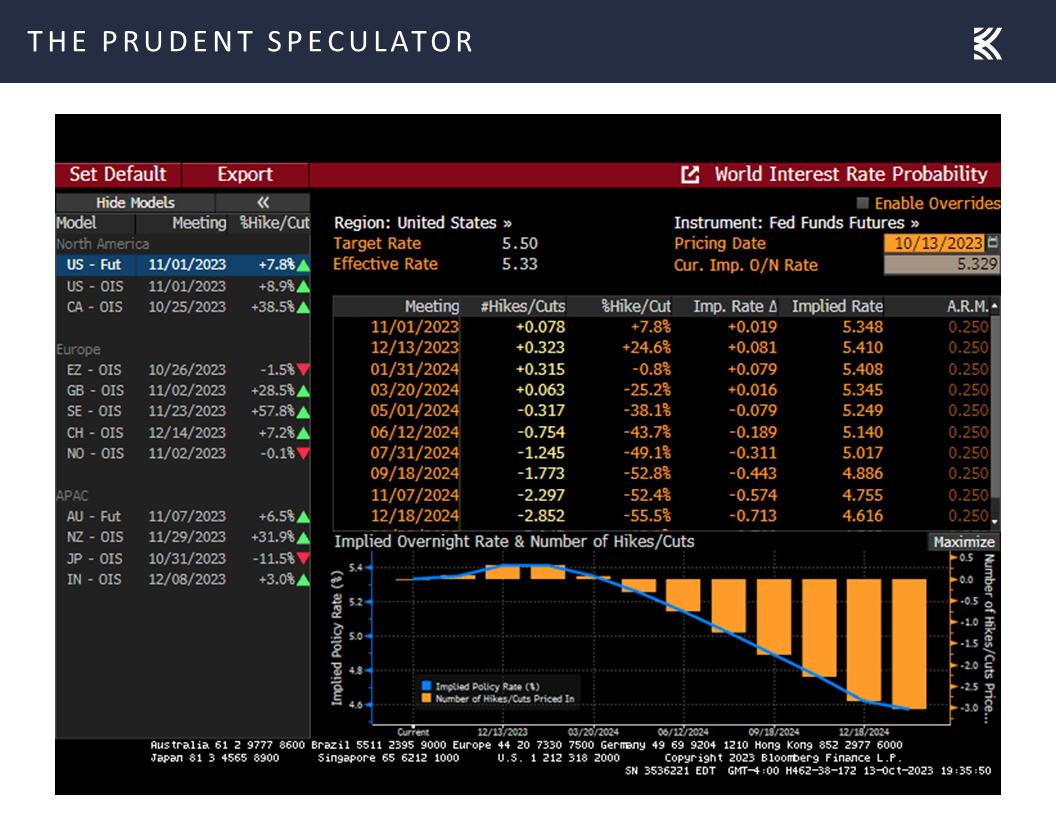

and Treasury yields actually fell last week,

as did expectations for additional hikes in the Fed Funds rate.

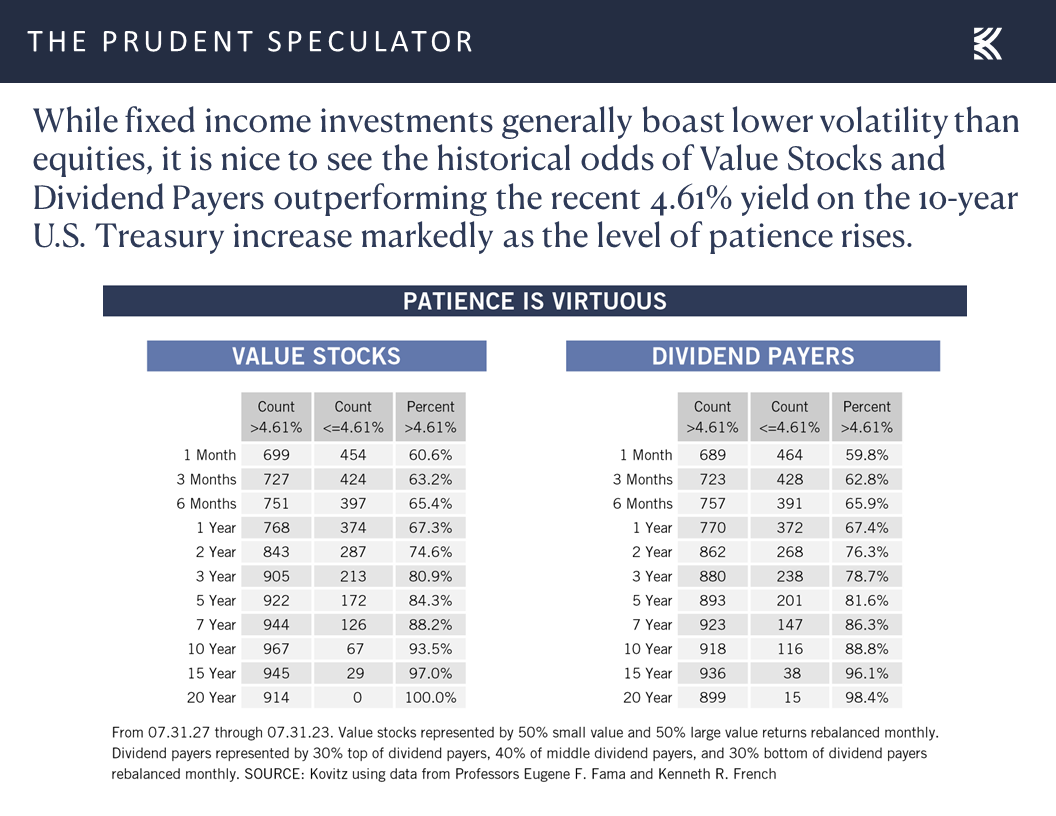

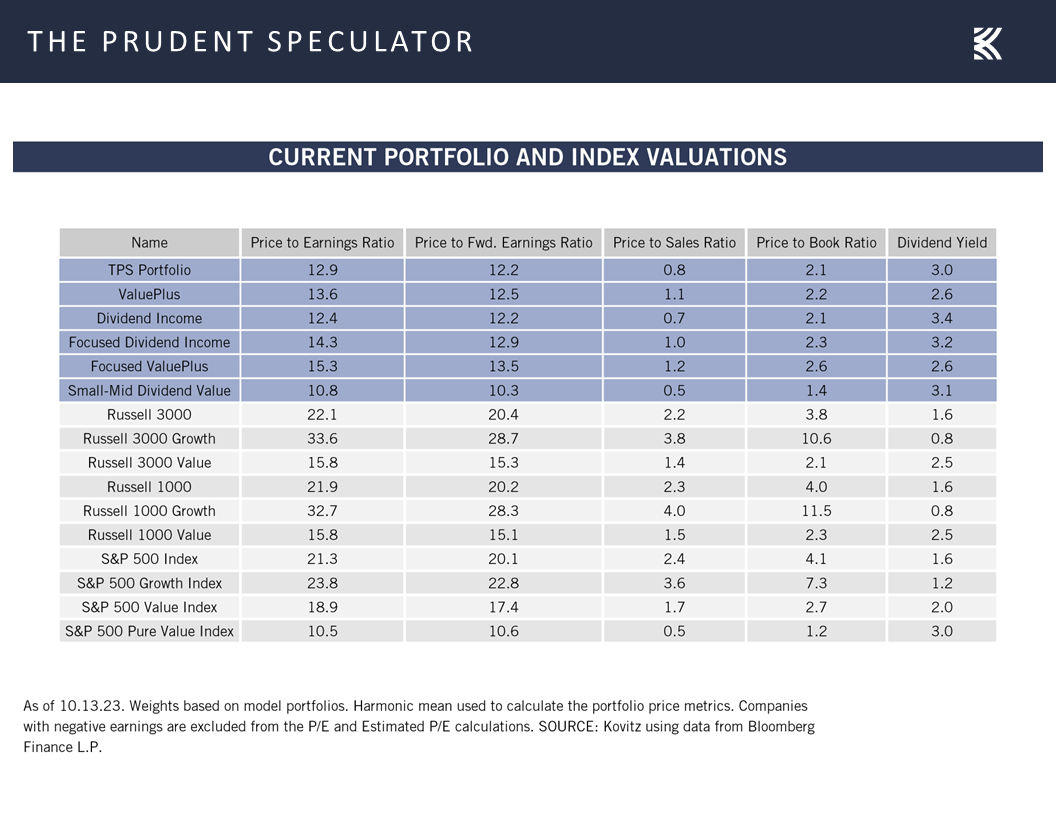

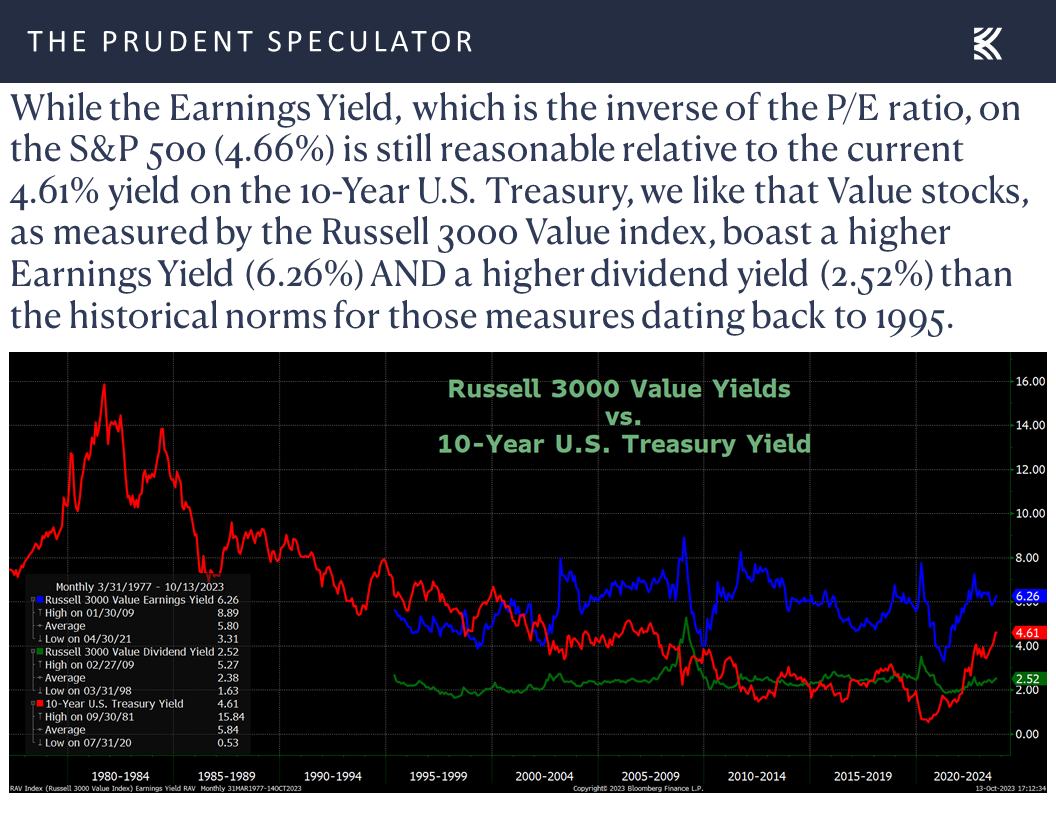

Valuations – Value Stocks Still Inexpensively Priced

As we constantly state, we are braced for additional equity market downside volatility (believe it or not, the large-cap market averages rose last week, despite the Middle East headlines), but we retain our optimism for the long-term prospects of our broadly diversified portfolio of what we believe to be undervalued stocks.

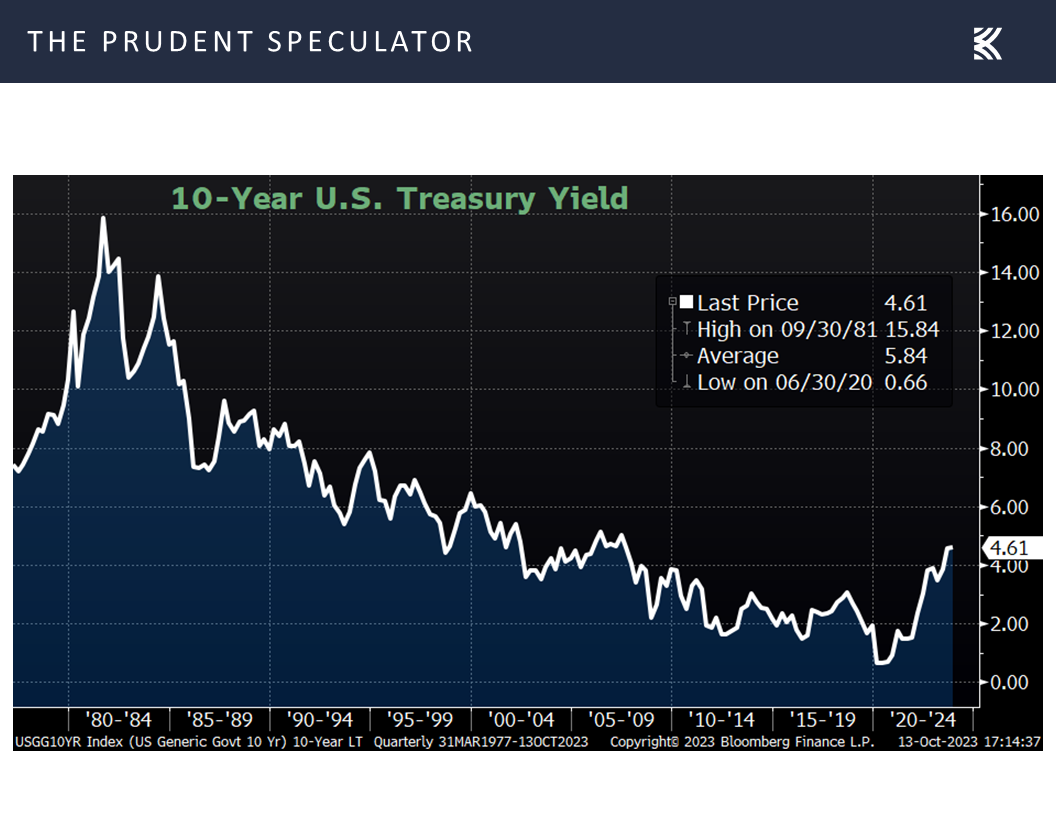

Yes, the jump in interest rates of late adds competition to stocks for those seeking income, but the 10-year Treasury yield today is still well below the average since the launch of The Prudent Speculator in 1977,

while the Value segment of the market remains inexpensively priced relative to the “risk-free” rate on an earnings yield basis.

Stock News – Updates on eight stocks across four different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

GDP Growth, Inflation, Valuations and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the GDP Growth, Inflation, Valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Historical Perspective – Stocks Have Persevered Through Plenty of Disconcerting Events

Growth – GDP, Corporate Profits and Stock Prices Have Marched Higher Over Time

Econ Update – Sentiment Falls; GDP Growth Projections Remain Strong

Inflation – Mixed Numbers; Stocks a Good Hedge Against Higher CPI

Valuations – Value Stocks Still Inexpensively Priced

Stock News – Updates on JPM, C, BLK, PNC, MDT, ABT, ZBH & XOM

Historical Perspective – Stocks Have Persevered Through Plenty of Disconcerting Events

not to mention the ongoing war in Ukraine,

but our job is to unemotionally navigate the equity markets through thick and thin. Helping us stay on an even keel is advice from Vannevar Bush. The American engineer and inventor said, “Fear cannot be banished, but it can be calm and without panic; it can be mitigated by reason and evaluation,” with the performance of stocks during and following prior turbulent periods providing valuable perspective.

Growth – GDP, Corporate Profits and Stock Prices Have Marched Higher Over Time

To be sure, past performance is no guarantee of future returns, but the historical probabilities that those who invest in Value Stocks and Dividend Payers will enjoy very favorable returns over the long term (and even over the short and intermediate terms) are impressive,

as the U.S. economy, despite a few downticks along the way, has grown over time,

propelling corporate profits and equity prices steadily (and not so steadily) higher.

Econ Update – Sentiment Falls; GDP Growth Projections Remain Strong

Of course, there will always be concern that an interruption in economic growth is around the corner, with the current odds of recession over the next 12 months as tabulated by Bloomberg continuing to reside at a very elevated 55%,

as the latest read on Main Street sentiment from the University of Michigan came in below expectations and well below average,

with it a similar story for optimism from small businesses.

On the other hand, the latest estimate for Q3 real (inflation-adjusted) GDP growth from the Atlanta Fed was a whopping 5.1%,

as the labor situation remains very robust with first-time filings for unemployment benefits continuing to bounce around near multi-generational lows.

Needless to say, the economic outlook is uncertain, but we continue to take comfort in the historical evidence on equity returns and recessions. Indeed, unless one could somehow exit stocks at the start of a contraction and get back in at the precise end, there is a very strong likelihood that attempting to market time would prove hazardous to one’s wealth, especially given the stellar gains, on average, in the 12 months following the end of a recession!

Inflation – Mixed Numbers; Stocks a Good Hedge Against Higher CPI

Economic growth is just one of the many worries (there are always concerns) with which investors must contend these days. Another is inflation, with the Producer Price Index (PPI) for September rising to 2.2% on a year-over-year basis, above projections of a 1.6% advance,

and the Consumer Price Index (CPI) climbing 3.7% year-over-year, also slightly above expectations,

though the increase in the core CPI (excludes volatile food and energy prices) edged down to 4.1% last month from 4.3% in August.

Still, there was some consternation that 3- and 5-year CPI expectations ticked up,

even as stocks historically have proved to be a very good hedge against inflation,

and Treasury yields actually fell last week,

as did expectations for additional hikes in the Fed Funds rate.

Valuations – Value Stocks Still Inexpensively Priced

As we constantly state, we are braced for additional equity market downside volatility (believe it or not, the large-cap market averages rose last week, despite the Middle East headlines), but we retain our optimism for the long-term prospects of our broadly diversified portfolio of what we believe to be undervalued stocks.

Yes, the jump in interest rates of late adds competition to stocks for those seeking income, but the 10-year Treasury yield today is still well below the average since the launch of The Prudent Speculator in 1977,

while the Value segment of the market remains inexpensively priced relative to the “risk-free” rate on an earnings yield basis.

Stock News – Updates on eight stocks across four different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.