The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Inflation, Interest Rates, AAII Sentiment and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Portfolio Trades – Trimmed JBL in Four Accounts

Week In Review – Sizable Rebound For Stocks

Sentiment – AAII Folks are Bearish

History – Time in the Market Trumps Market Timing

Econ Stats – Bad News is Good News

Interest Rates – Treasury Yields Pull Back; Fed Funds Outlook Moderates

Inflation – PCE Holds Steady

Growth – Long-Term Trend in GDP, Earnings and Dividends is Higher

Valuations – Value Stocks Are Attractively Priced

Stock News – Updates on four stocks across 3 different sectors

Week In Review – Sizable Rebound For Stocks

After a less-than-stellar first three weeks of August, the last four trading days of the month and the first day of September saw equities stage a handsome rebound, with excellent gains across the board and the S&P 500 advancing 2.50% on a price basis,

Sentiment – AAII Folks are Bearish

Even as folks on Main Street remained pessimistic about the prospects for stocks over the next six months. Indeed, the latest Sentiment Survey from the American Association of Individual Investors (AAII) saw the percentage who are Bearish again exceed those who are Bullish, continuing the reversal of opinion from earlier in August when far more were optimistic.

‘Twas ever thus, our founder Al Frank liked to say as investor sentiment historically has proven to be a contrarian indicator, with forward returns better when the masses are not enthused about the prospects for equities, and not as good (though still positive, on average), when they are excited about stocks.

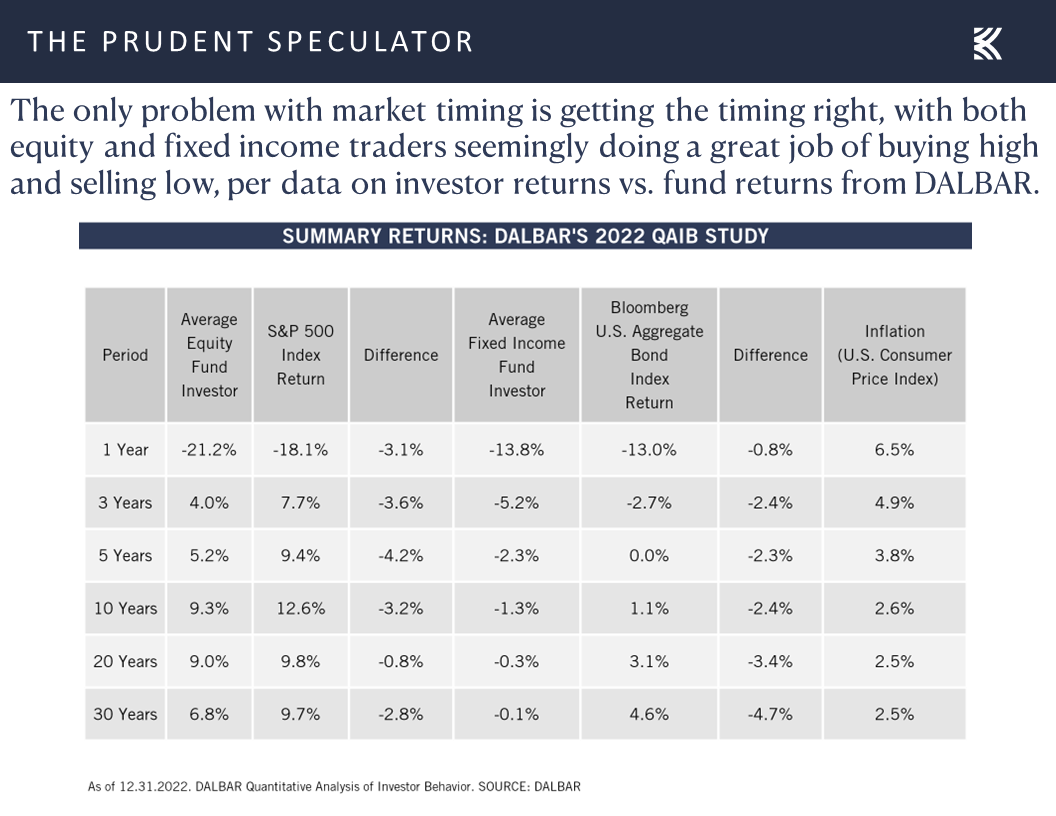

History – Time in the Market Trumps Market Timing

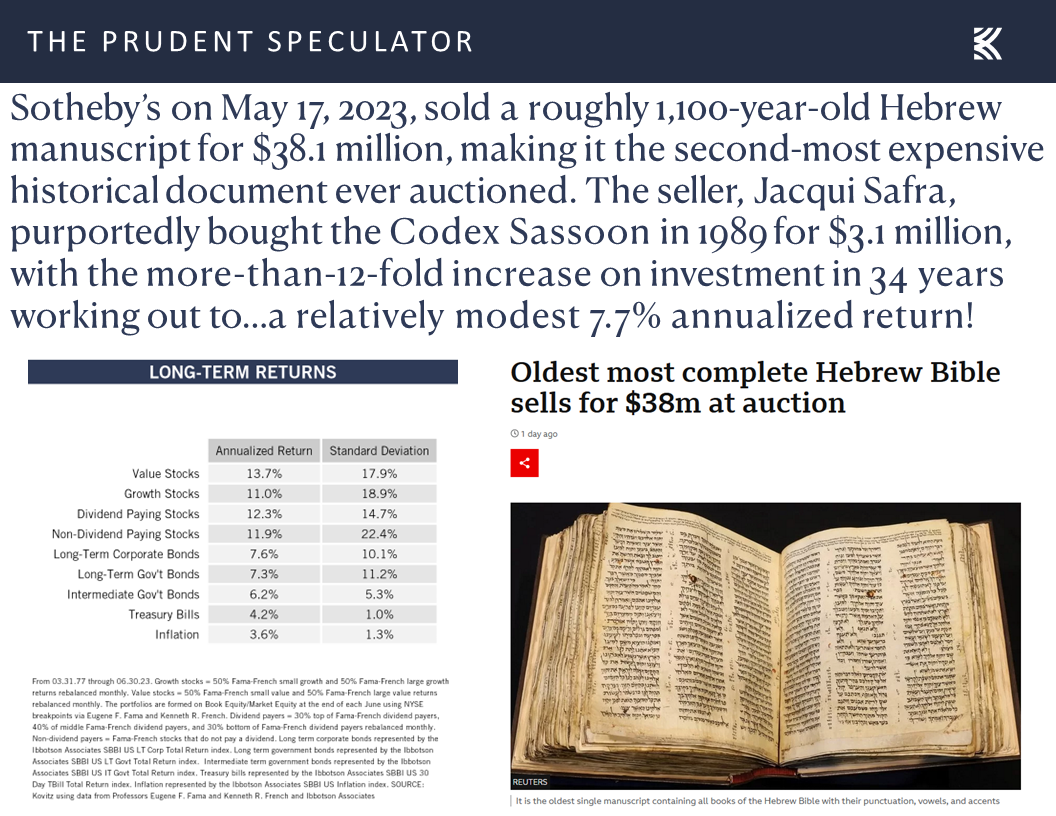

Of course, those betting against equities are bucking the historical odds that have seen Value Stocks gain 13.7% per annum and Dividend Payers climb 12.3% per year since the launch of The Prudent Speculator back in March 1977,

while the evidence is overwhelming against trying to time the movements into and out of the always fickle financial markets.

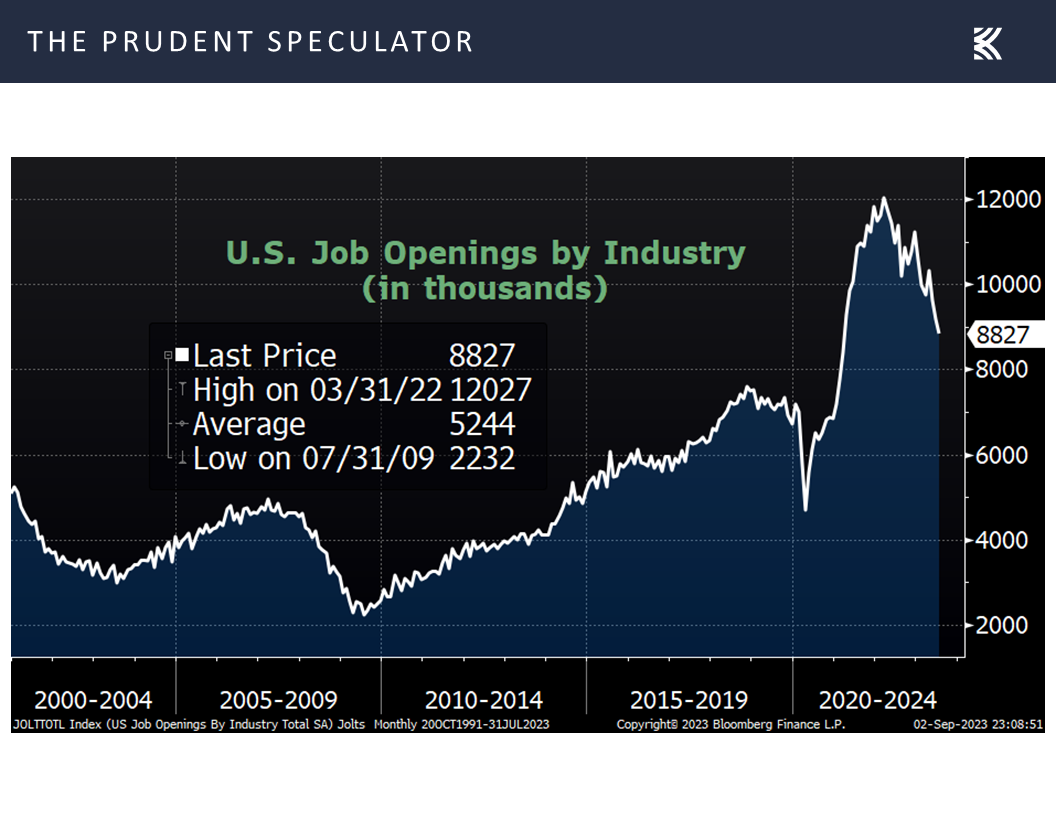

Econ Stats – Bad News is Good News

Speaking of fickle, traders of late have evidently decided that less favorable economic news is good for stocks and vice versa. Last week’s equity market advance arguably was fueled by a reduction in excess U.S. labor demand as the number of job openings (JOLTS) in July dropped to 8.83 million, down from a revised 9.16 million in June and below estimates in the 9.5 million range.

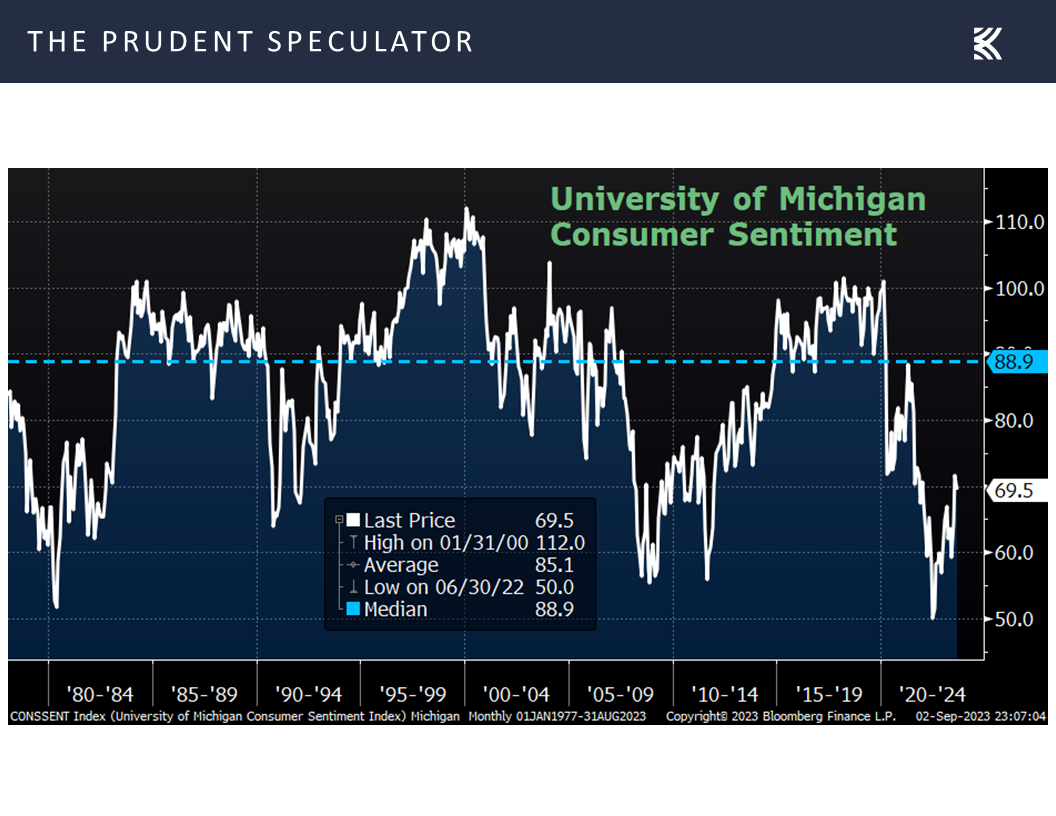

Also helping the thinking that economic growth is not too robust were weaker-than-expected readings on Consumer Sentiment (69.5 vs. 71.2 est.) from the Univ. of Michigan,

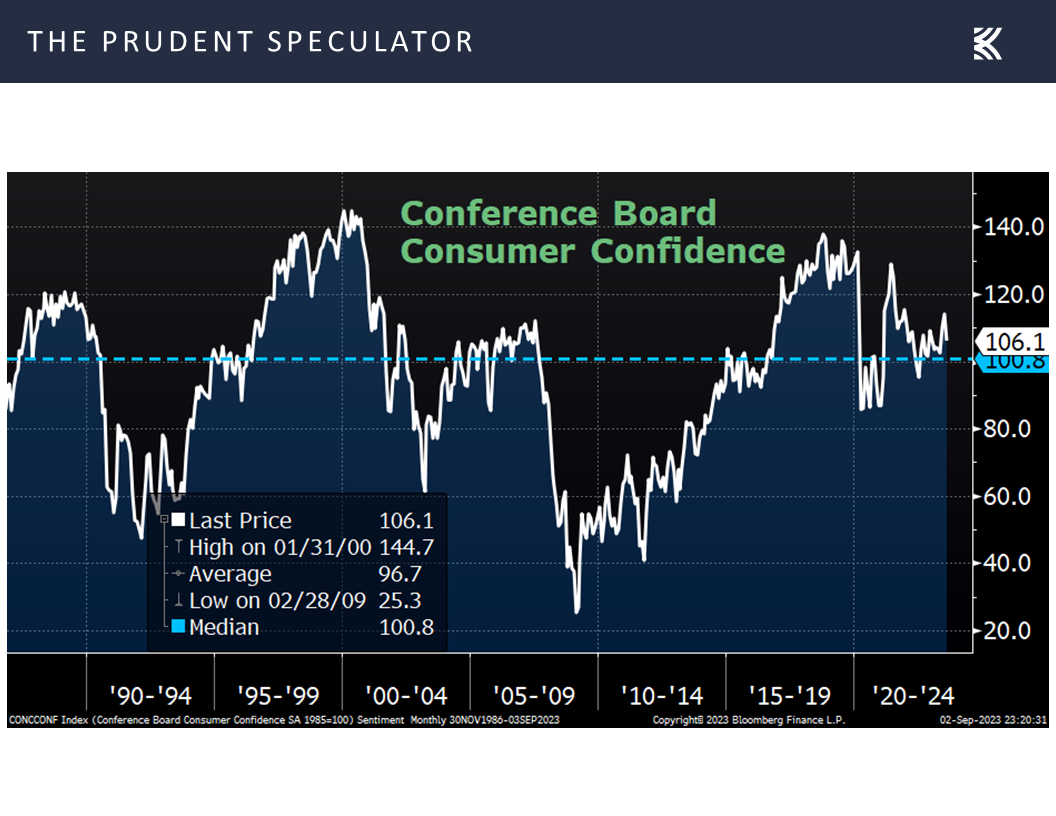

and Consumer Confidence (106.1 vs. 116.0 est.) from the Conference Board.

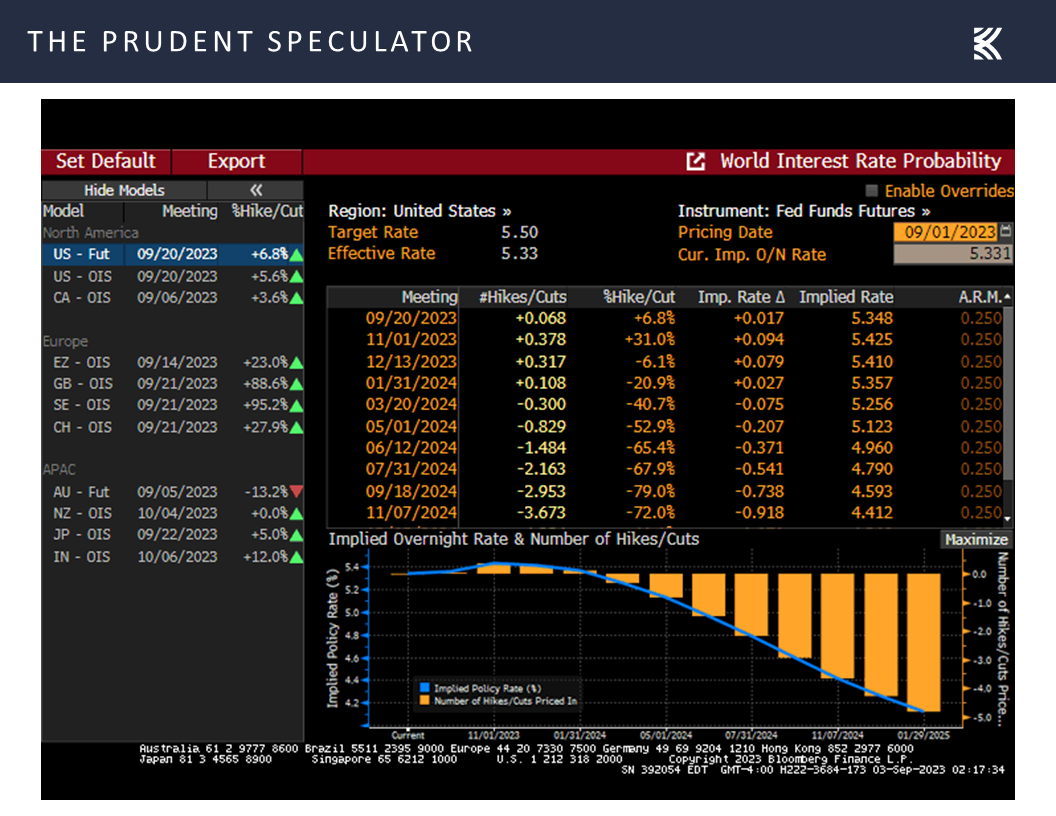

Interest Rates – Treasury Yields Pull Back; Fed Funds Outlook Moderates

The logic behind the view that slower-than-projected economic growth is a positive is that the Federal Reserve will be less inclined to hike interest rates again at the upcoming FOMC Meeting September 19-20. Indeed, though the Fed Funds futures presently are suggesting a 32% chance of a rate hike when the decision on interest rates is announced at the subsequent FOMC Meeting on November 1, the odds of an increase this month now stand at just 6.8%.

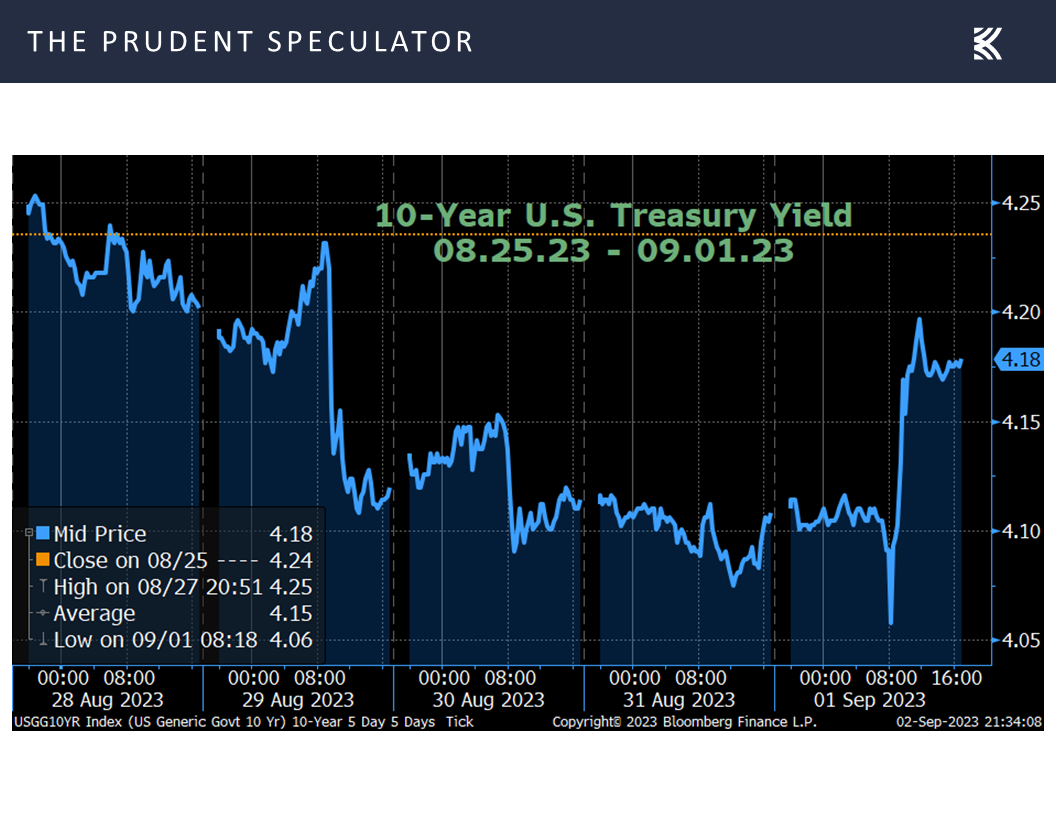

Those percentages are down from the week prior, and led to a drop in interest rates for the 10-Year U.S. Treasury last week as benchmark government bond prices rallied.

Inflation – PCE Holds Steady

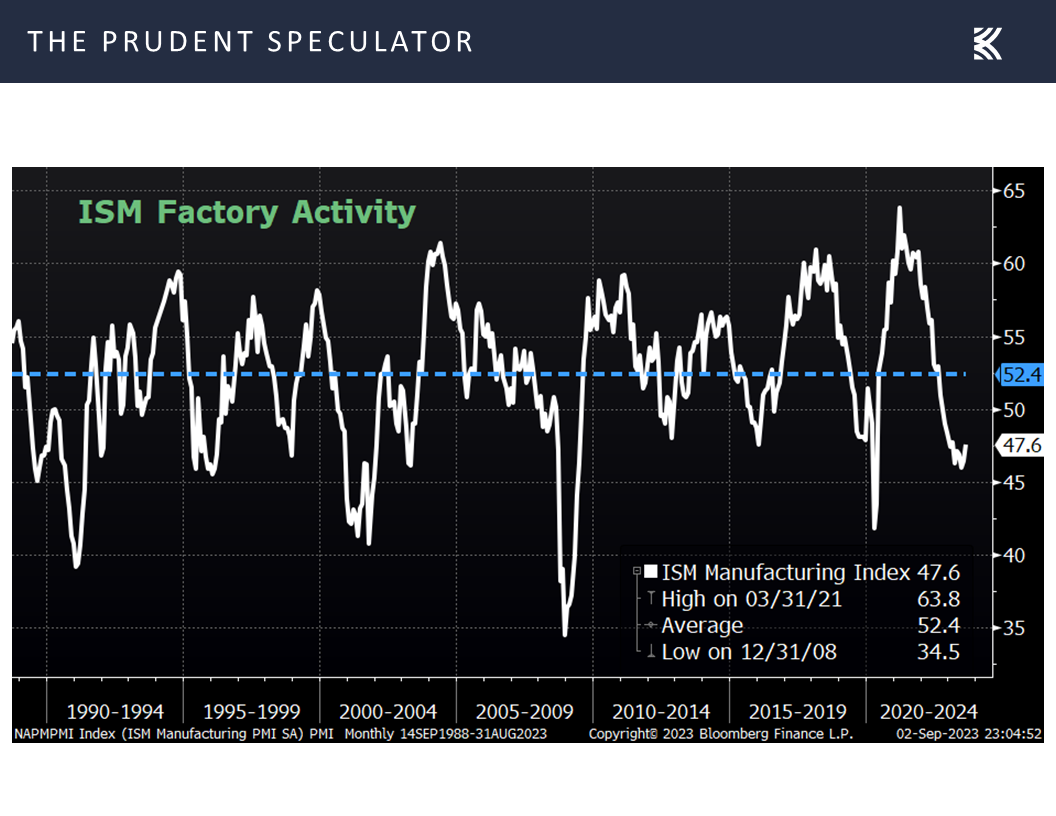

That said, as the 5-day yield chart above shows, there was plenty of uncertainty surrounding interest rates on Friday, following a stronger-than-estimated (but still way below average) reading on the health of the manufacturing sector from the Institute for Supply Management (ISM)

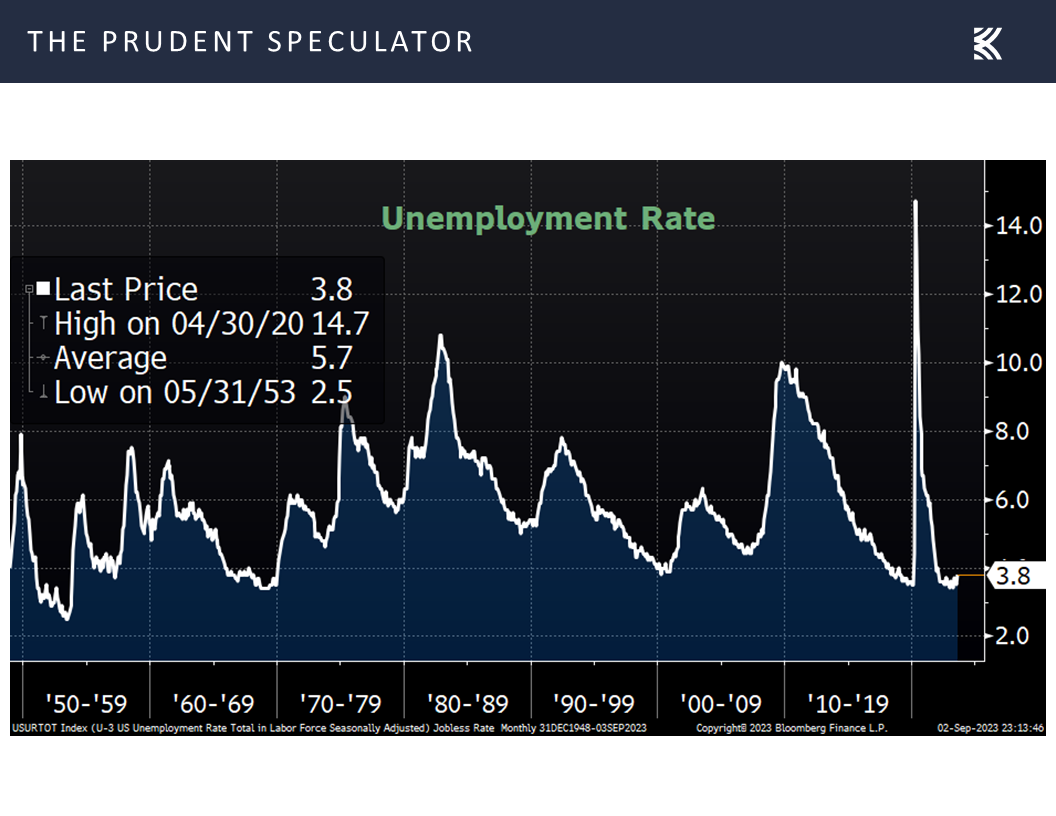

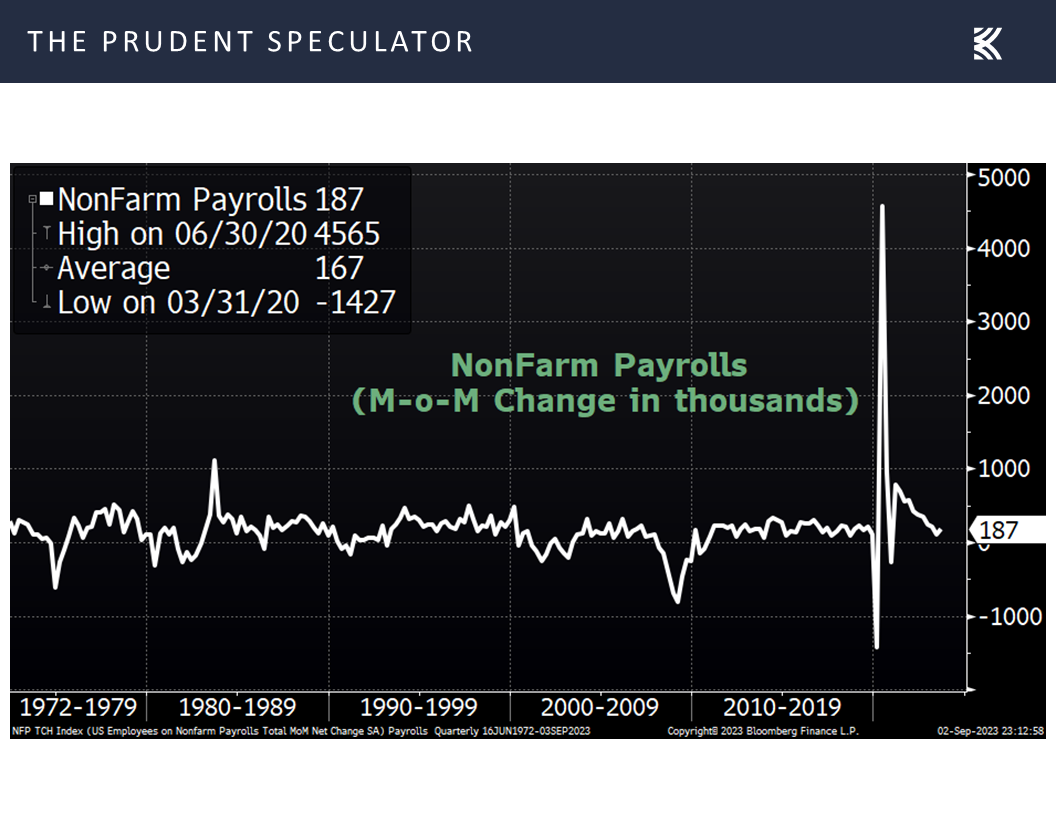

and the release of the critical Employment Situation Report from the Bureau of Labor Statistics that morning. Looking at the latter, on the one hand, the unemployment rate for August jumped to a higher-than-expected 3.8%, up from 3.5% in July,

but the increase was caused by more people entering the work force as the number of new jobs created came in at 187,000, which was above economist forecasts,

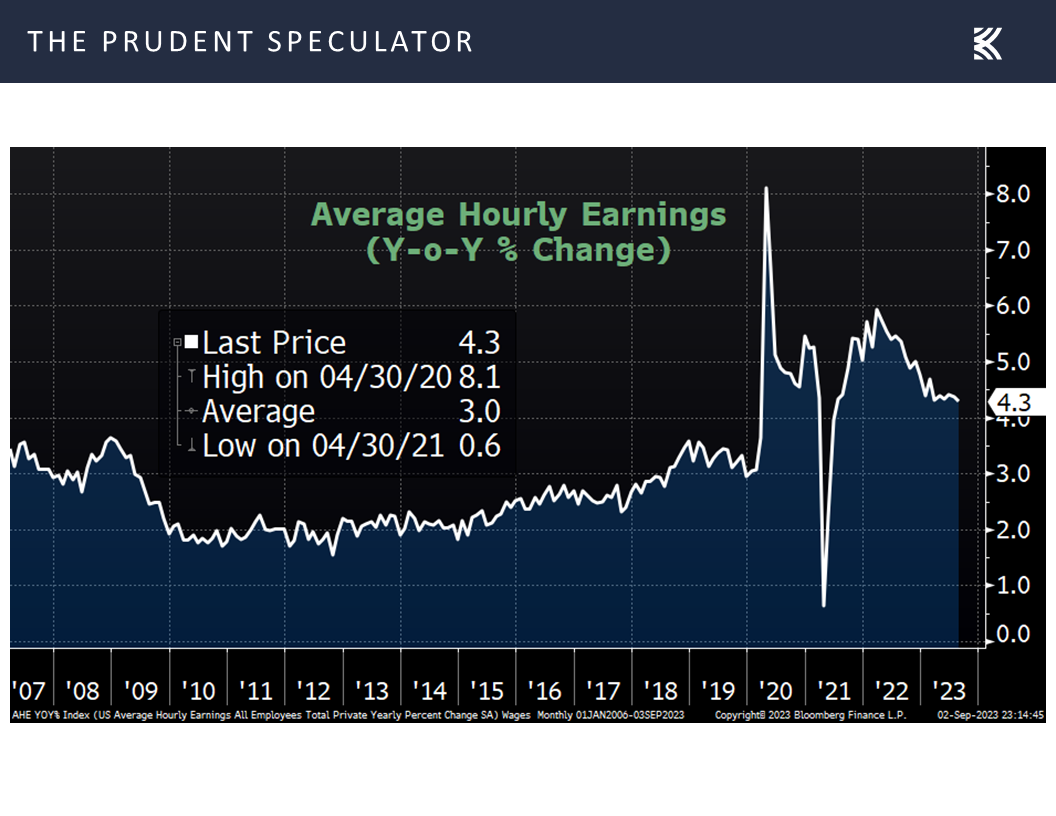

and wages rose 4.3% on a year-over-year basis, in line with projections but still well above pre-pandemic levels.

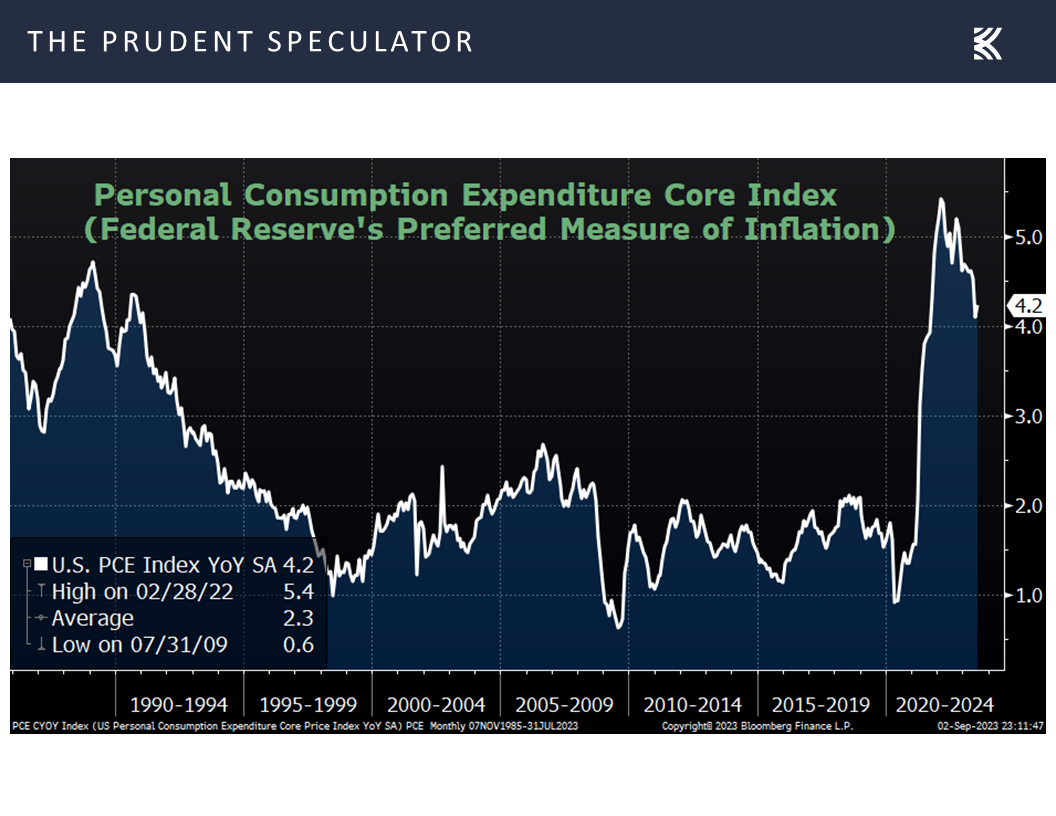

No doubt, the Federal Reserve remains concerned about inflation, so even though Jerome H. Powell & Co.’s preferred measure, the Core Personal Consumption Expenditures Index (PCE), held steady at a 4.2% increase in July,

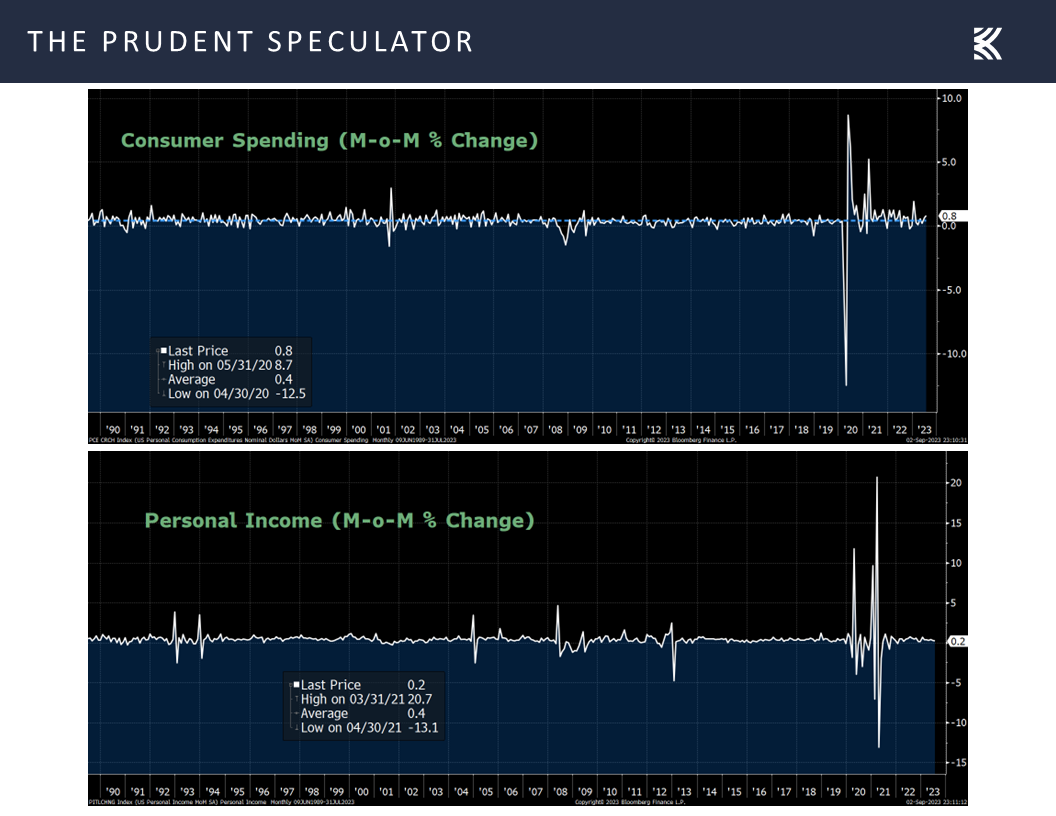

some were concerned that the 0.8% increase in personal spending exceeded expectations, while others were comforted that personal incomes rose only 0.2%, a smaller gain than estimated.

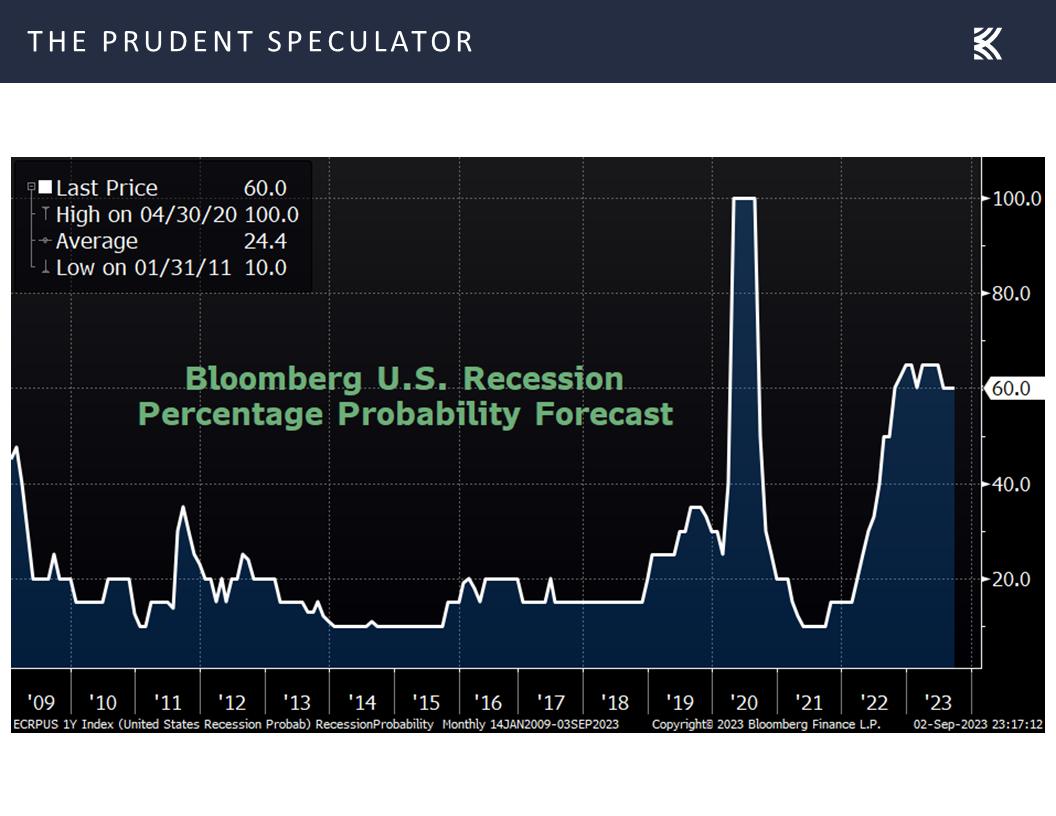

Believe it or not, when all of the economic stats were considered, there was no change in Bloomberg’s calculation of the 60% recession probability for the U.S. over the next 12 months,

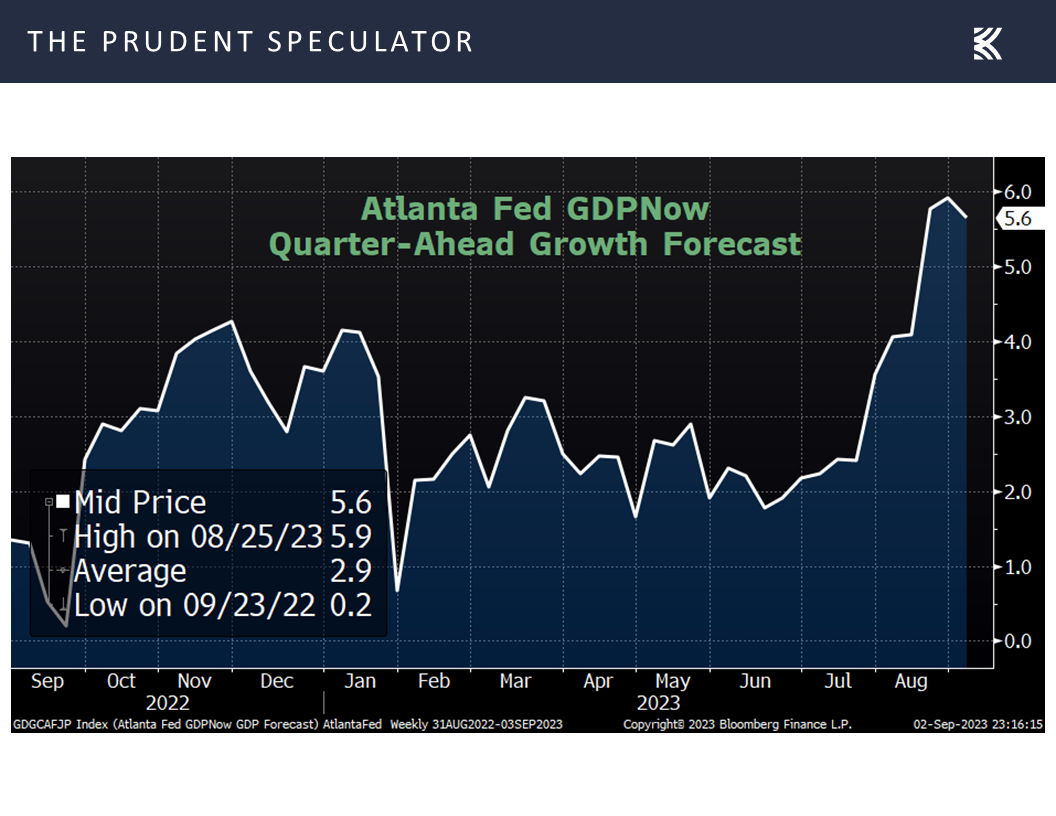

while the estimate for Q3 real (inflation-adjusted) U.S. GDP growth remained at a very strong 5.6% per the Atlanta Fed.

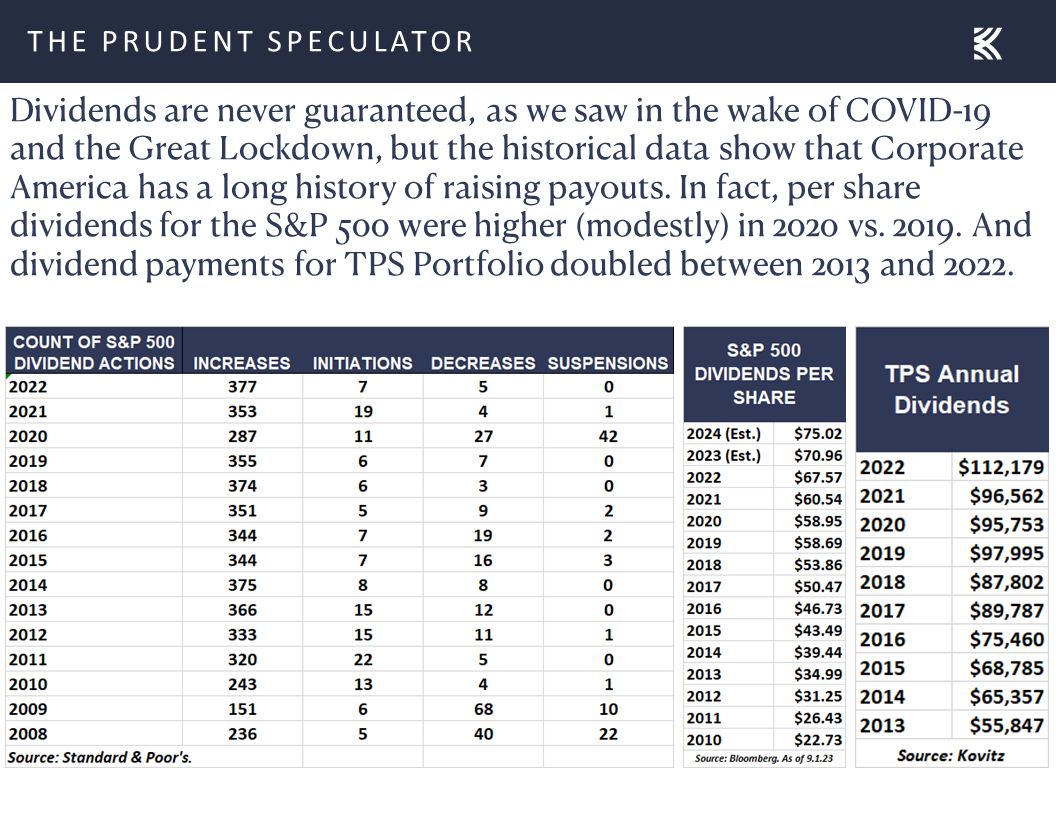

Growth – Long-Term Trend in GDP, Earnings and Dividends is Higher

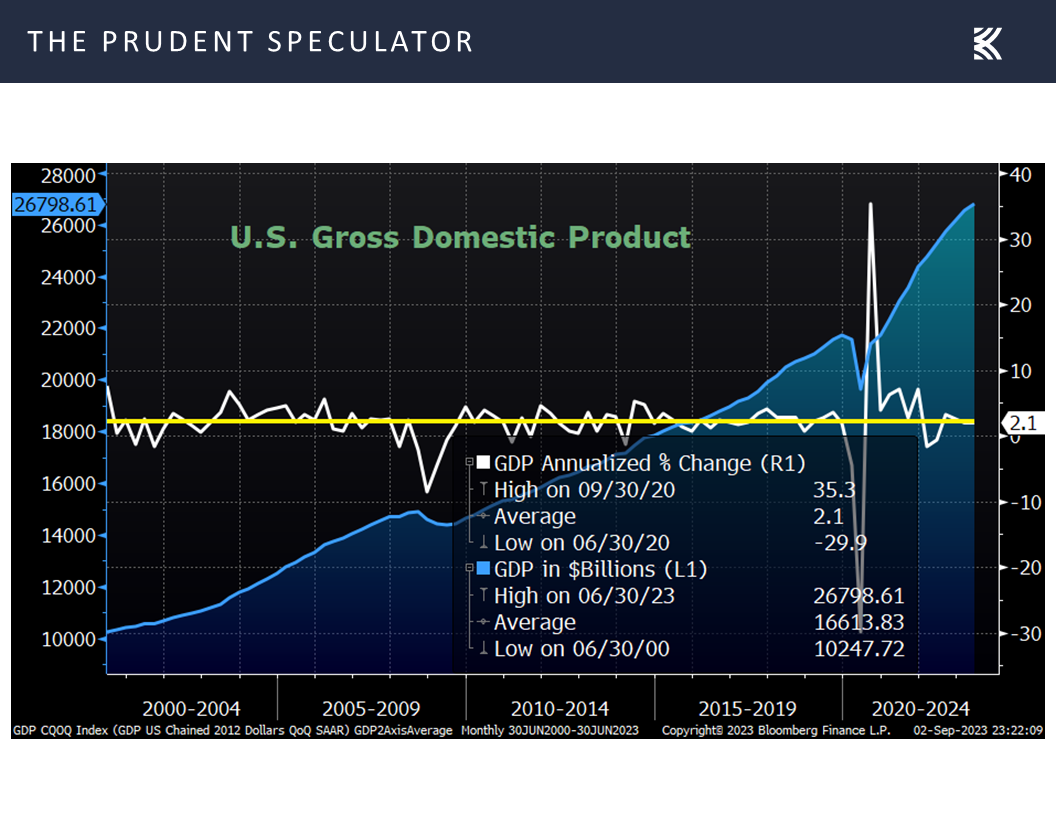

Obviously, economic prognostication is fraught with peril, so we will leave the hand wringing on the Fed, interest rates and GDP to the talking heads. Yes, all are important, but when it comes to stocks, we can’t forget that equities represent ownership in actual businesses, most of which grow in value over time, and that they are not merely pieces of paper. Over the long term, the U.S. economy has grown,

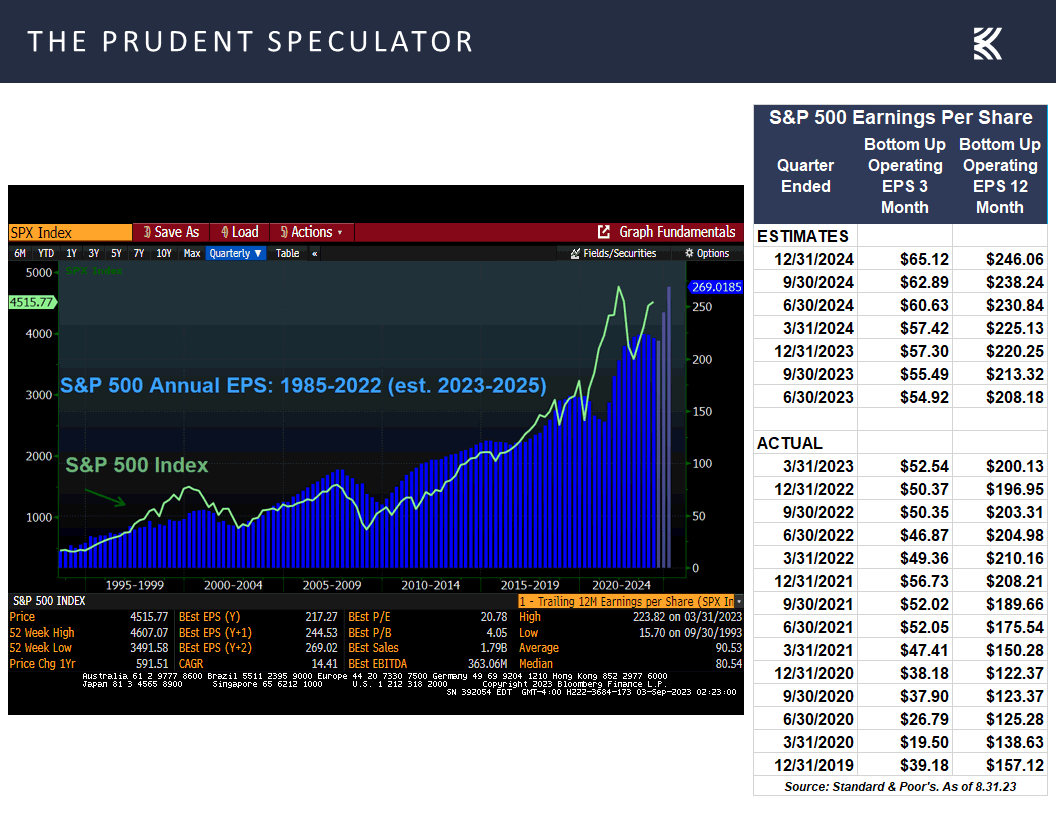

as have corporate profits,

and dividend payouts.

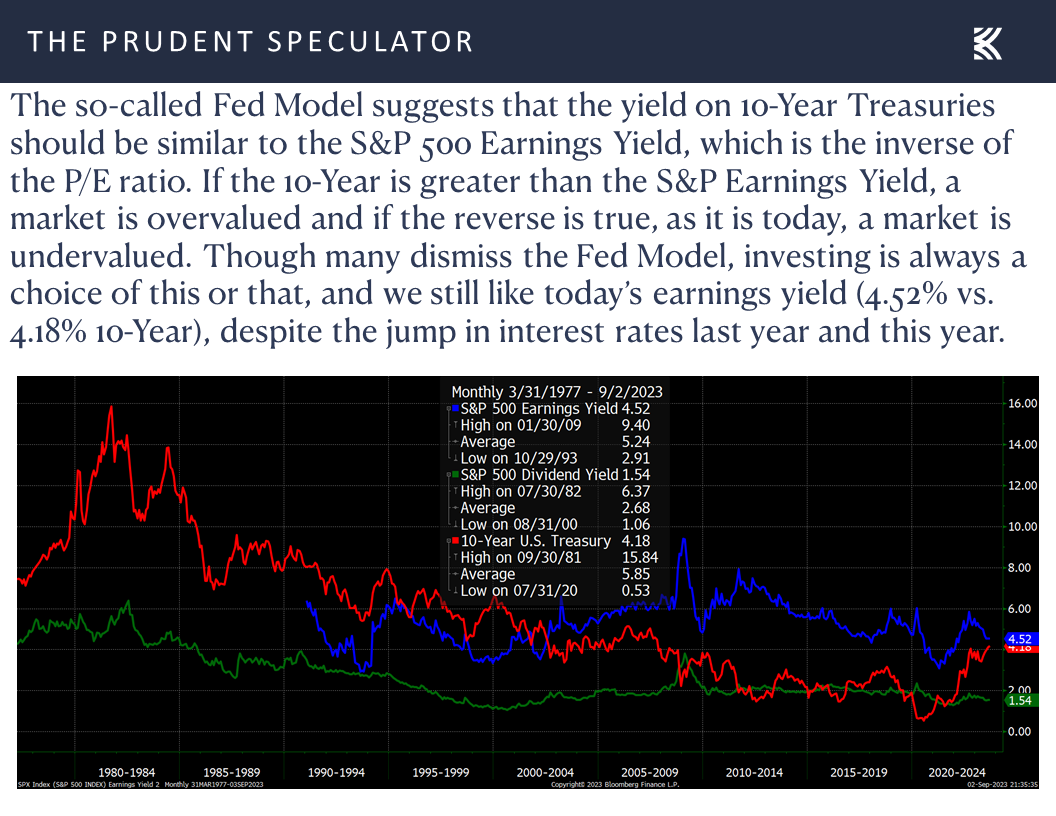

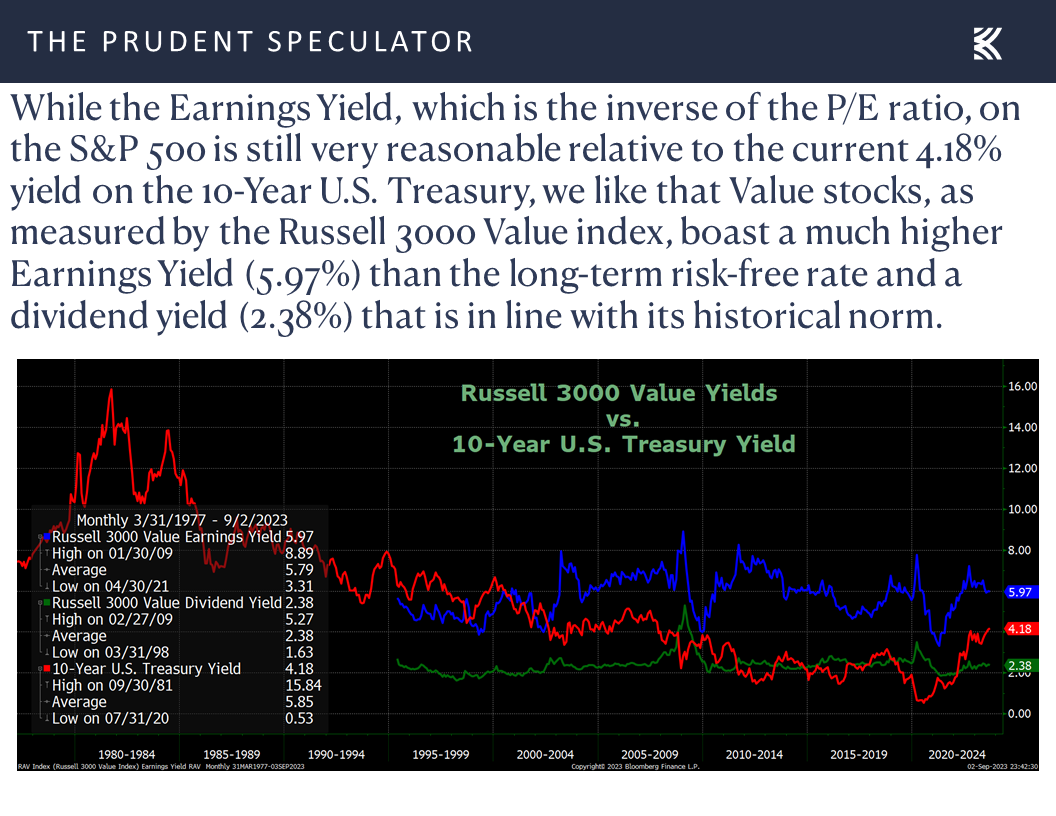

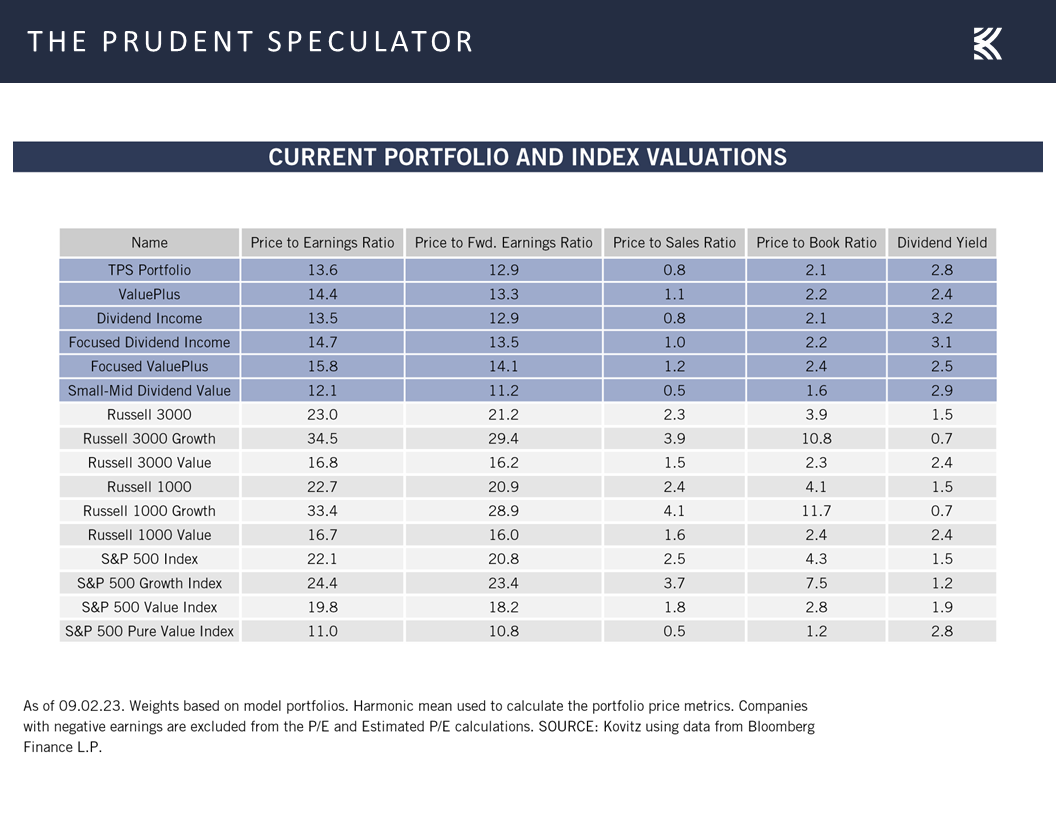

And with equities in general still not overly expensive by our way of thinking,

and Value remaining attractively priced relative to its norms,

Valuations – Value Stocks Are Attractively Priced

we can’t help but like the valuation metrics and the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks.

Stock News – Updates on four stocks across three different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Inflation, Interest Rates, AAII Sentiment and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Inflation, Interest Rates, AAII Sentiment and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Portfolio Trades – Trimmed JBL in Four Accounts

Week In Review – Sizable Rebound For Stocks

Sentiment – AAII Folks are Bearish

History – Time in the Market Trumps Market Timing

Econ Stats – Bad News is Good News

Interest Rates – Treasury Yields Pull Back; Fed Funds Outlook Moderates

Inflation – PCE Holds Steady

Growth – Long-Term Trend in GDP, Earnings and Dividends is Higher

Valuations – Value Stocks Are Attractively Priced

Stock News – Updates on four stocks across 3 different sectors

Week In Review – Sizable Rebound For Stocks

After a less-than-stellar first three weeks of August, the last four trading days of the month and the first day of September saw equities stage a handsome rebound, with excellent gains across the board and the S&P 500 advancing 2.50% on a price basis,

Sentiment – AAII Folks are Bearish

Even as folks on Main Street remained pessimistic about the prospects for stocks over the next six months. Indeed, the latest Sentiment Survey from the American Association of Individual Investors (AAII) saw the percentage who are Bearish again exceed those who are Bullish, continuing the reversal of opinion from earlier in August when far more were optimistic.

‘Twas ever thus, our founder Al Frank liked to say as investor sentiment historically has proven to be a contrarian indicator, with forward returns better when the masses are not enthused about the prospects for equities, and not as good (though still positive, on average), when they are excited about stocks.

History – Time in the Market Trumps Market Timing

Of course, those betting against equities are bucking the historical odds that have seen Value Stocks gain 13.7% per annum and Dividend Payers climb 12.3% per year since the launch of The Prudent Speculator back in March 1977,

while the evidence is overwhelming against trying to time the movements into and out of the always fickle financial markets.

Econ Stats – Bad News is Good News

Speaking of fickle, traders of late have evidently decided that less favorable economic news is good for stocks and vice versa. Last week’s equity market advance arguably was fueled by a reduction in excess U.S. labor demand as the number of job openings (JOLTS) in July dropped to 8.83 million, down from a revised 9.16 million in June and below estimates in the 9.5 million range.

Also helping the thinking that economic growth is not too robust were weaker-than-expected readings on Consumer Sentiment (69.5 vs. 71.2 est.) from the Univ. of Michigan,

and Consumer Confidence (106.1 vs. 116.0 est.) from the Conference Board.

Interest Rates – Treasury Yields Pull Back; Fed Funds Outlook Moderates

The logic behind the view that slower-than-projected economic growth is a positive is that the Federal Reserve will be less inclined to hike interest rates again at the upcoming FOMC Meeting September 19-20. Indeed, though the Fed Funds futures presently are suggesting a 32% chance of a rate hike when the decision on interest rates is announced at the subsequent FOMC Meeting on November 1, the odds of an increase this month now stand at just 6.8%.

Those percentages are down from the week prior, and led to a drop in interest rates for the 10-Year U.S. Treasury last week as benchmark government bond prices rallied.

Inflation – PCE Holds Steady

That said, as the 5-day yield chart above shows, there was plenty of uncertainty surrounding interest rates on Friday, following a stronger-than-estimated (but still way below average) reading on the health of the manufacturing sector from the Institute for Supply Management (ISM)

and the release of the critical Employment Situation Report from the Bureau of Labor Statistics that morning. Looking at the latter, on the one hand, the unemployment rate for August jumped to a higher-than-expected 3.8%, up from 3.5% in July,

but the increase was caused by more people entering the work force as the number of new jobs created came in at 187,000, which was above economist forecasts,

and wages rose 4.3% on a year-over-year basis, in line with projections but still well above pre-pandemic levels.

No doubt, the Federal Reserve remains concerned about inflation, so even though Jerome H. Powell & Co.’s preferred measure, the Core Personal Consumption Expenditures Index (PCE), held steady at a 4.2% increase in July,

some were concerned that the 0.8% increase in personal spending exceeded expectations, while others were comforted that personal incomes rose only 0.2%, a smaller gain than estimated.

Believe it or not, when all of the economic stats were considered, there was no change in Bloomberg’s calculation of the 60% recession probability for the U.S. over the next 12 months,

while the estimate for Q3 real (inflation-adjusted) U.S. GDP growth remained at a very strong 5.6% per the Atlanta Fed.

Growth – Long-Term Trend in GDP, Earnings and Dividends is Higher

Obviously, economic prognostication is fraught with peril, so we will leave the hand wringing on the Fed, interest rates and GDP to the talking heads. Yes, all are important, but when it comes to stocks, we can’t forget that equities represent ownership in actual businesses, most of which grow in value over time, and that they are not merely pieces of paper. Over the long term, the U.S. economy has grown,

as have corporate profits,

and dividend payouts.

And with equities in general still not overly expensive by our way of thinking,

and Value remaining attractively priced relative to its norms,

Valuations – Value Stocks Are Attractively Priced

we can’t help but like the valuation metrics and the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks.

Stock News – Updates on four stocks across three different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.