The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Inflation, Interest Rates, Dividends, Earnings and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Friday for the Dow – Price-Weighting Can Skew The Index

Managed Care – UnitedHealth Defies Skeptics; Still Liking ELV and CVS

Inflation – CPI & PPI Both Cooler Than Expected

Interest Rates – Big Rally Last Week in the Price of the 10-Year Treasury

Valuations – Stocks, Especially Value, Remain Reasonably Priced

Dividends – Bond Coupons Usually are Fixed but Dividends Have Risen Over Time

Jamie Dimon on the Economy – Resilient with Healthy Consumer Balance Sheets

Earnings – Profit Growth Still the Forecast This Year and in 2024

Sentiment – AAII Bullishness is Elevated

Patience – Stocks Have Proved Very Rewarding Over the Long Term

Stock News – Updates on four stocks across three different sectors

Friday for the Dow – Price-Weighting Can Skew The Index

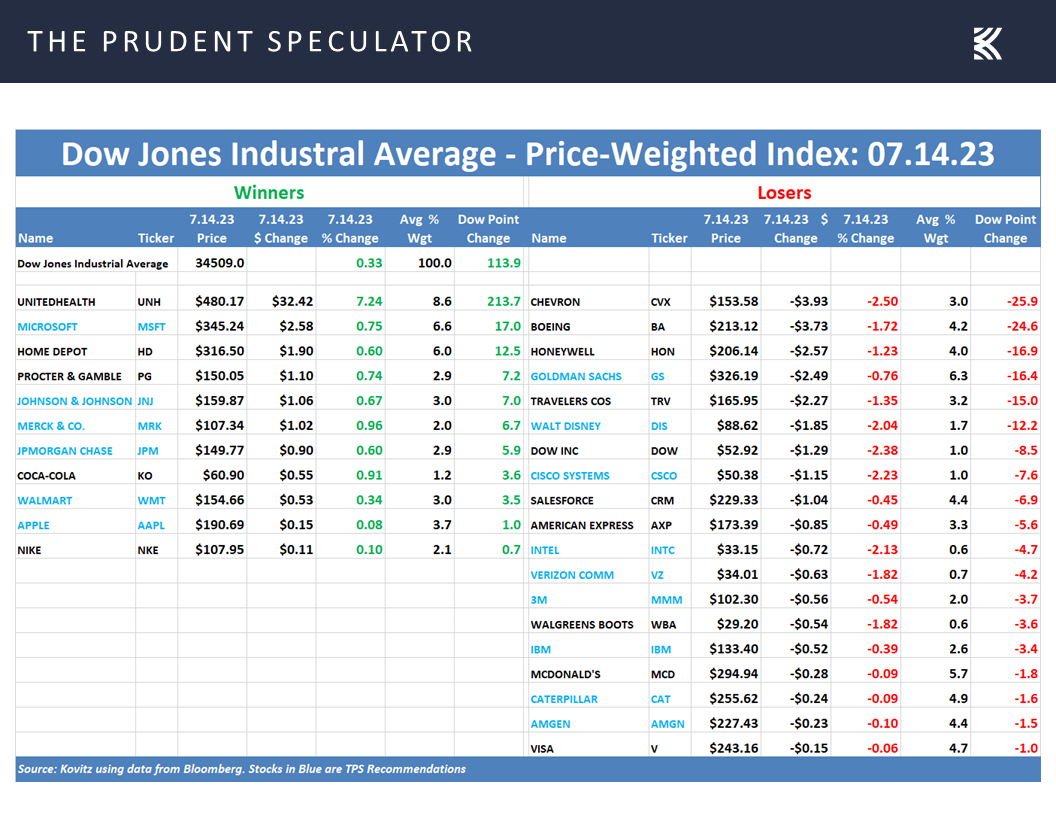

The trading week ended on a very sour note, given that the average stock in the broad-based Russell 3000 index declined 1.2% on Friday, even as the Dow Jones Industrial Average managed to close higher by 114 points, or 0.3%.

We suspect that many are aware that unlike most other market indexes, the Dow is price-weighted, meaning that the highest-priced stocks like Microsoft (MSFT – $345.24) and Home Depot have a very large impact and lower-priced stocks like Walgreens Boots, Intel (INTC – $33.15), Verizon Communications (VZ – $34.01) and Cisco Systems (CSCO – $50.38) are more or less insignificant in that they combined account for less than 3% of the 30-member benchmark.

Believe it or not, the Dow is calculated by adding up the price of all 30 components and dividing by a divisor, which today is 0.15173. This means that a $1 move up or down in the price of a Dow component translates into a 6.6 point move in the index. Obviously, a big change in a stock with a triple-digit stock price will result in a sizable advance or decline in the Dow, as was the case on Friday when managed care provider UnitedHealth (UNH), the most important Dow constituent, soared more than $32 after announcing better-than-feared Q2 financials.

Managed Care – UnitedHealth Defies Skeptics; Still Liking ELV and CVS

Incredibly, UnitedHealth’s 7.2% price increase accounted for nearly 214-points of the Dow’s 114-point advance on Friday, which means that the other 29 stocks collectively lost 100 Dow points. In fact, 19 of the 30 Dow components finished in the red on the day, providing another reminder that it is a market of stocks and not simply a stock market. We also note that we presently hold 15 Dow members (those in blue in the chart above) in our broadly diversified portfolios.

And speaking of UnitedHealth and its impact on our holdings in the managed care industry, we again witnessed another example of why we always strive to ignore short-term fluctuations in the price of the stocks that we own. A month ago, we penned an update on our managed care providers Elevance Health (ELV – $438.73) and CVS Health (CVS – $71.38) after their stocks were hit hard following a Goldman Sachs investment conference where a UnitedHealth representative highlighted his company’s increasing costs in the Medicare space.

Numerous older adults aged 65 and above covered under Medicare, who had seemingly largely stayed indoors during a long stretch of the pandemic, are getting “more comfortable accessing services for things that they might have pushed off a bit like knees and hips,” UNH management disclosed. Non-urgent surgeries and outpatient services such as heart procedures and knee and hip replacements that had been put off during and after the pandemic were picking up pace.

Short-sighted investors dumped ELV and CVS on that news, even as the former said its medical care trends and costs were in line with expectations, while folks ignored that the latter is broadly diversified across the health care spectrum. Not to everyone’s surprise, UNH reported Q2 financial results that beat both top-and bottom-line expectations, and though margins in its Medicare coverage were squeezed, multiple other parts of the firm were hitting on all cylinders.

UNH CFO John Rex also noted that elevated costs in the Medicare space would continue in Q3, but they were expected to seasonally adjust downwards in Q4. CEO Andrew Witty added during the earnings call, “If I had the choice on a slightly suppressed margin in Q2 or the very significant growth that we’ve taken in, I’ll take the growth all day long, and I’ll take that growth because it’s going to underpin years of growth going forward.” The results and earnings call seemed to ease some overdone investor concerns and sent ELV rebounding by 5.0% and allowed CVS to stay in the green on an otherwise ugly market day on Friday.

While ELV and CVS don’t report their Q2 results until early August, we think emotional reactions to bits of sensationalized news or non-full-context quotes or short-term-focused analyst upgrades and downgrades can be “unhealthy” for long-term oriented investors. We also continue to like that ELV trades at 13.1 times forward adjusted EPS estimates and CVS (which owns Aetna) at 8.3 times, versus UnitedHealth’s 18.3 times. Our Target Prices for ELV and CVS are $620 and $130, respectively.

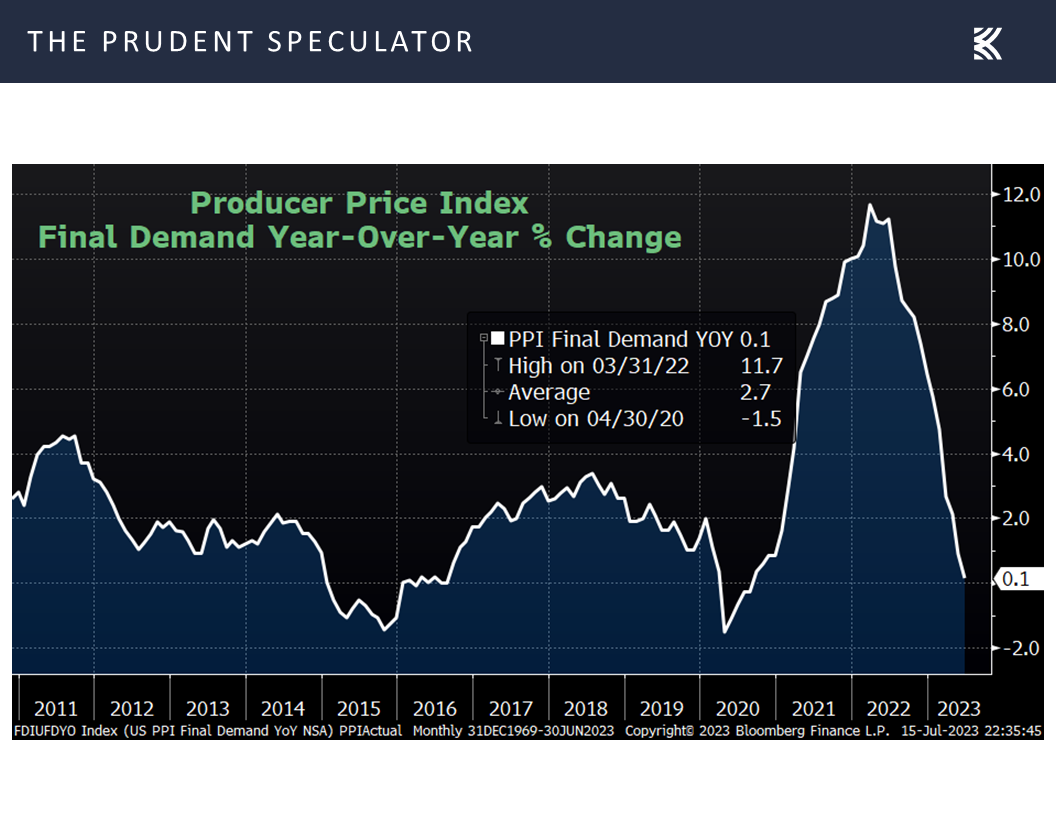

Inflation – CPI & PPI Both Cooler Than Expected

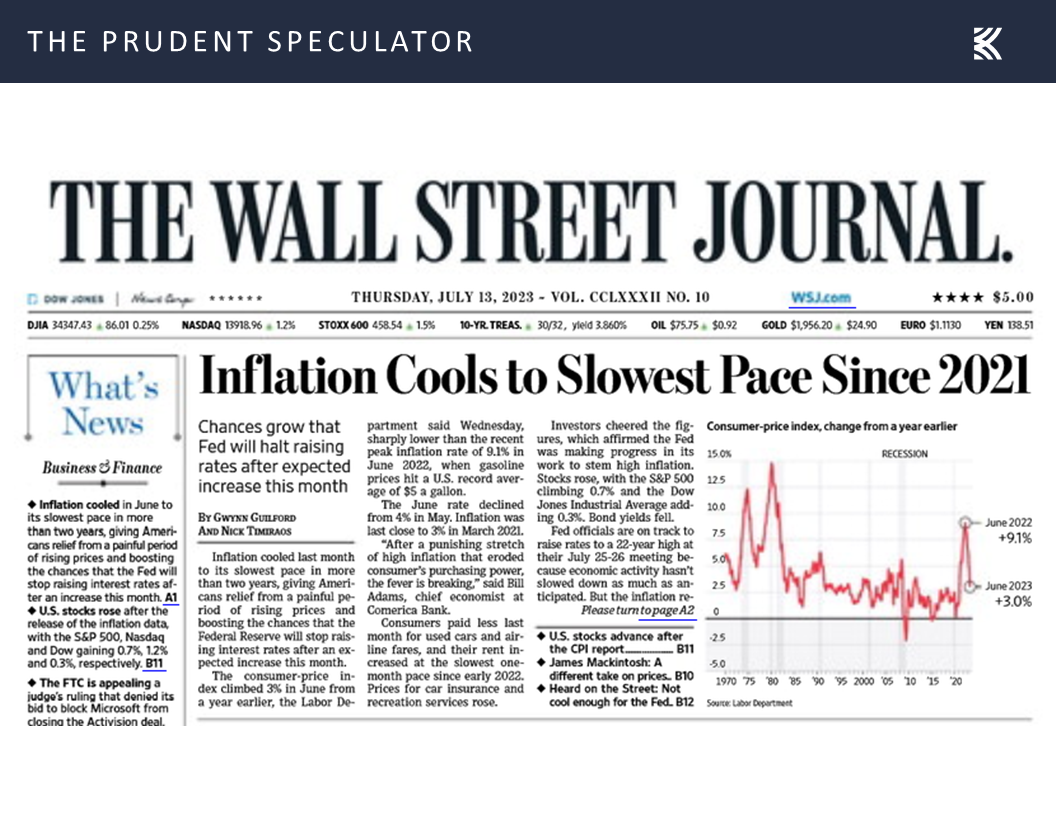

No doubt, a discussion of Friday’s miserable day of trading ignores the fact that the broad-based rally underway since the end of May resumed last week, with handsome gains across the board for equities over the full five days. The catalyst for the advance was surprisingly good news on inflation,

as the Consumer Price Index (CPI) rose only 0.2% in June, with the year-over-year increase coming in at 3.0%, which is in line with the historical norm going back to the 1920s.

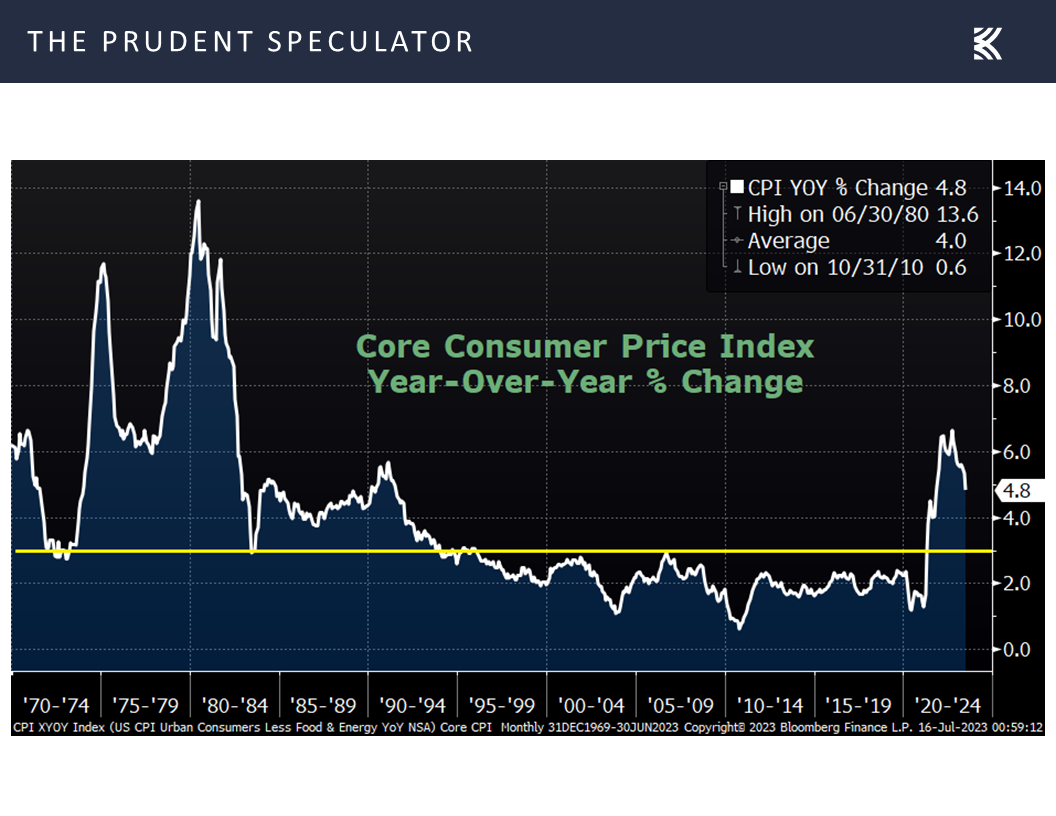

True, the so-called core CPI rate, which excludes volatile food and energy prices, climbed 4.8%, well above the Federal Reserve’s 2.0% target, but this tally slowed from a 5.3% increase in May to a nearly two-year low.

Even more impressive, perhaps, the headline figure for inflation at the wholesale level is now virtually flat, as the Producer Price Index (PPI) rose only 0.1% on a year-over-year basis. The core PPI advanced 2.6% on a year-over-year basis, but this gain was the smallest since March 2021.

To be sure, the Federal Reserve is nowhere near shouting, “Mission Accomplished,” in its fight against inflation. Fed governor Christopher Waller commented on the favorable CPI reading on Thursday, stating, “The recent report warmed my heart, but…I’ve got to make policy with my head. And I can’t do that on one data point.” And Dallas Fed President Lorie Logan, recently said, “I remain very concerned about whether inflation will return to target in a sustainable and timely way.

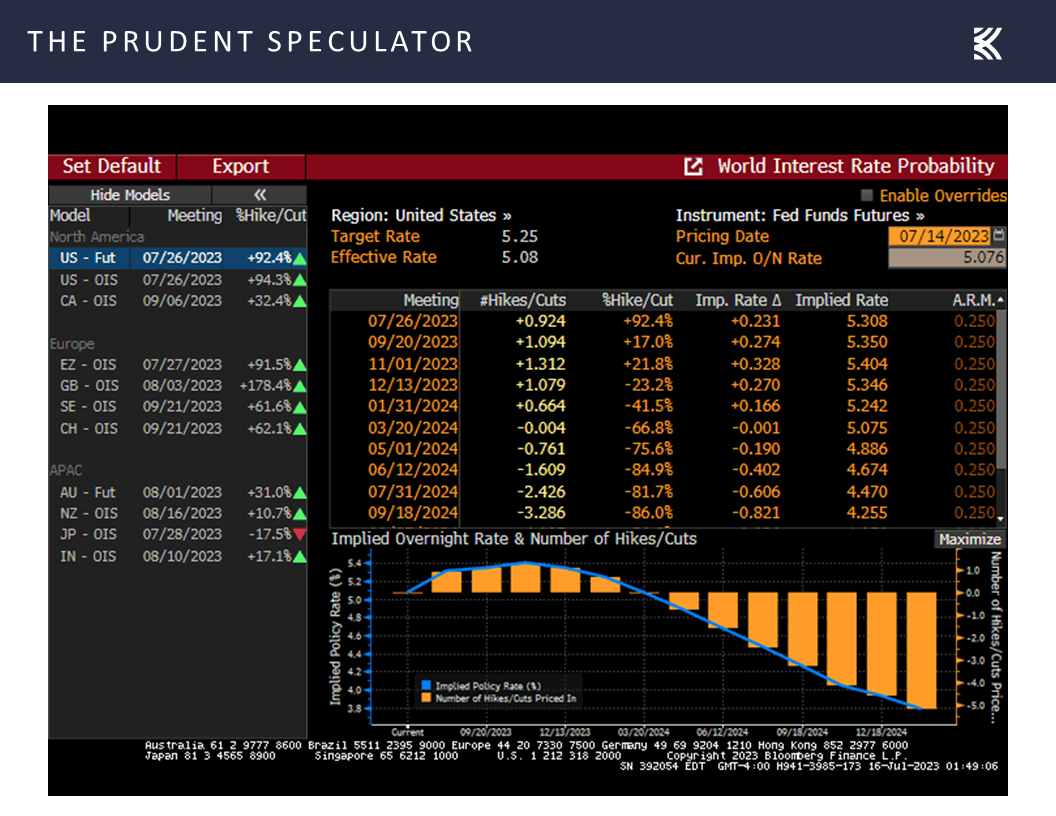

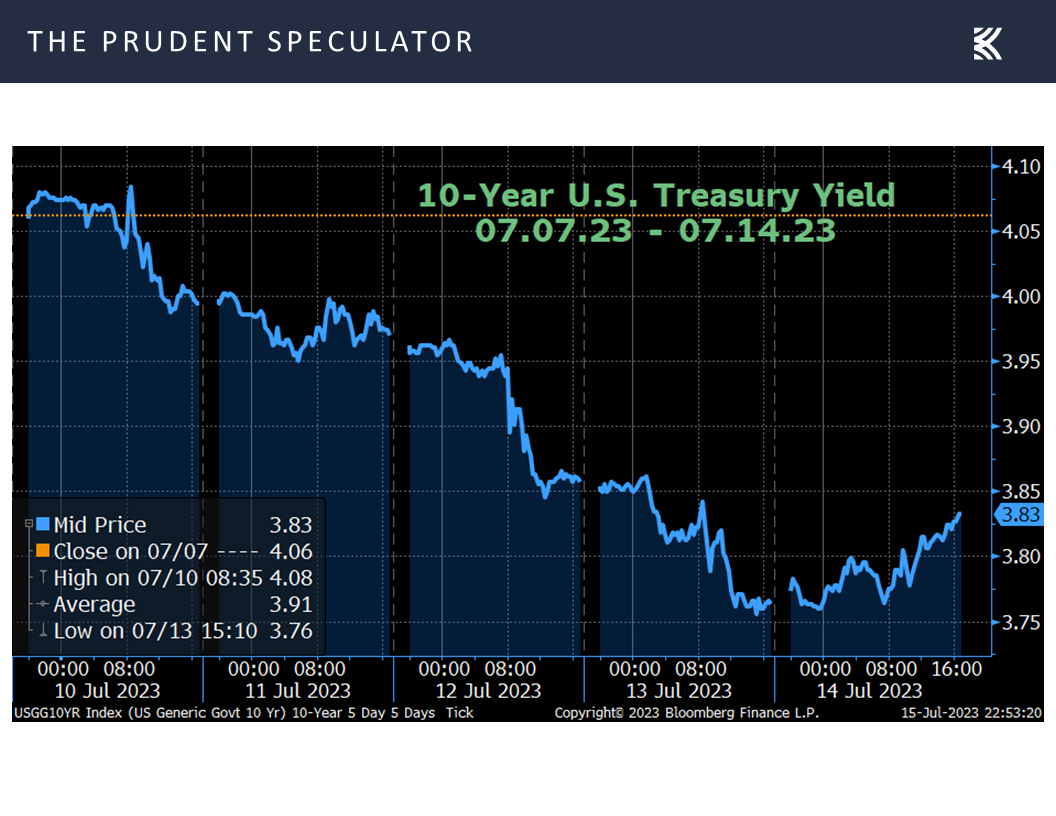

Interest Rates – Big Rally Last Week in the Price of the 10-Year Treasury

Despite the tough talk, market expectations for additional Fed rate hikes this year pulled back in the latest week, with the Fed Funds futures suggesting a 5.35% year-end rate, down from 5.39% a week ago,

and investors gravitating toward U.S. Treasuries, pushing the yield on the benchmark government bond down to 3.83% last week, versus 4.06% at the end of the week prior.

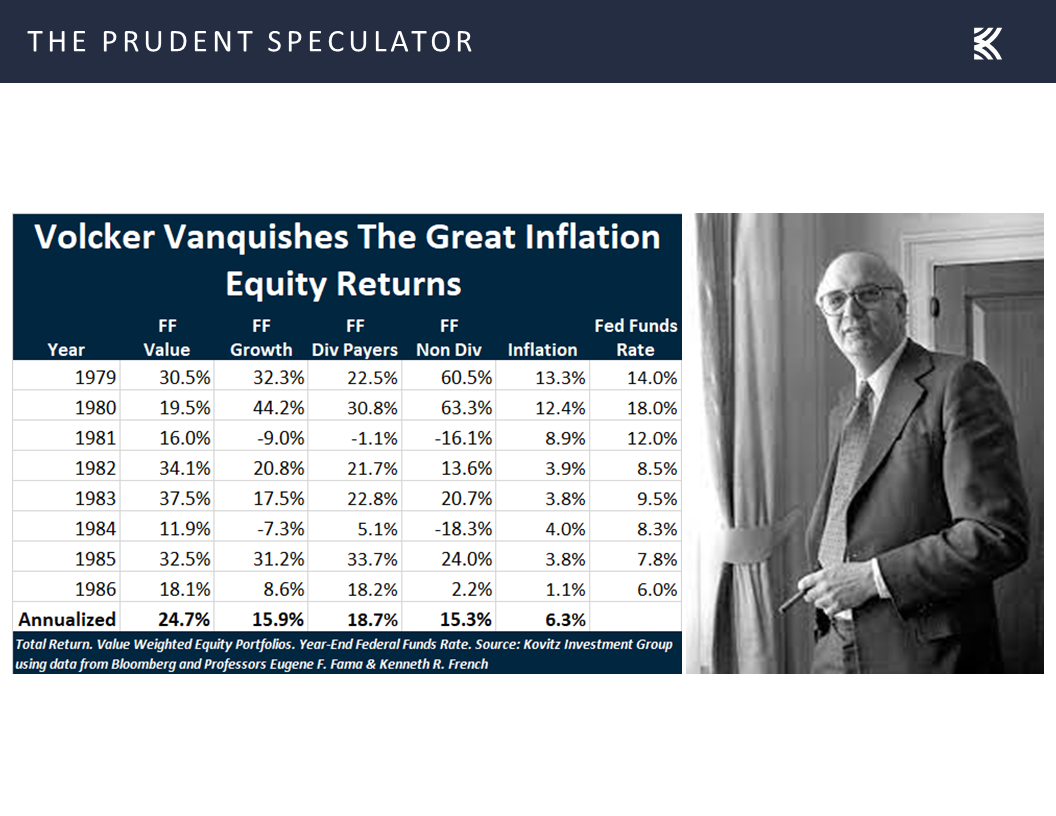

Of course, we continue to lose little sleep over Jerome H. Powell & Co.’s fight against inflation, especially as the last time (the Volcker Years) the Federal Reserve faced a similar battle, Value Stocks and Dividend Payers, like those that we have long favored, enjoyed spectacular returns, despite economic recessions taking place in 1980 and 1981.

Further, even as interest rates are substantially higher today than where they have been in recent years, equity valuations, in general, still compare favorably to fixed income,

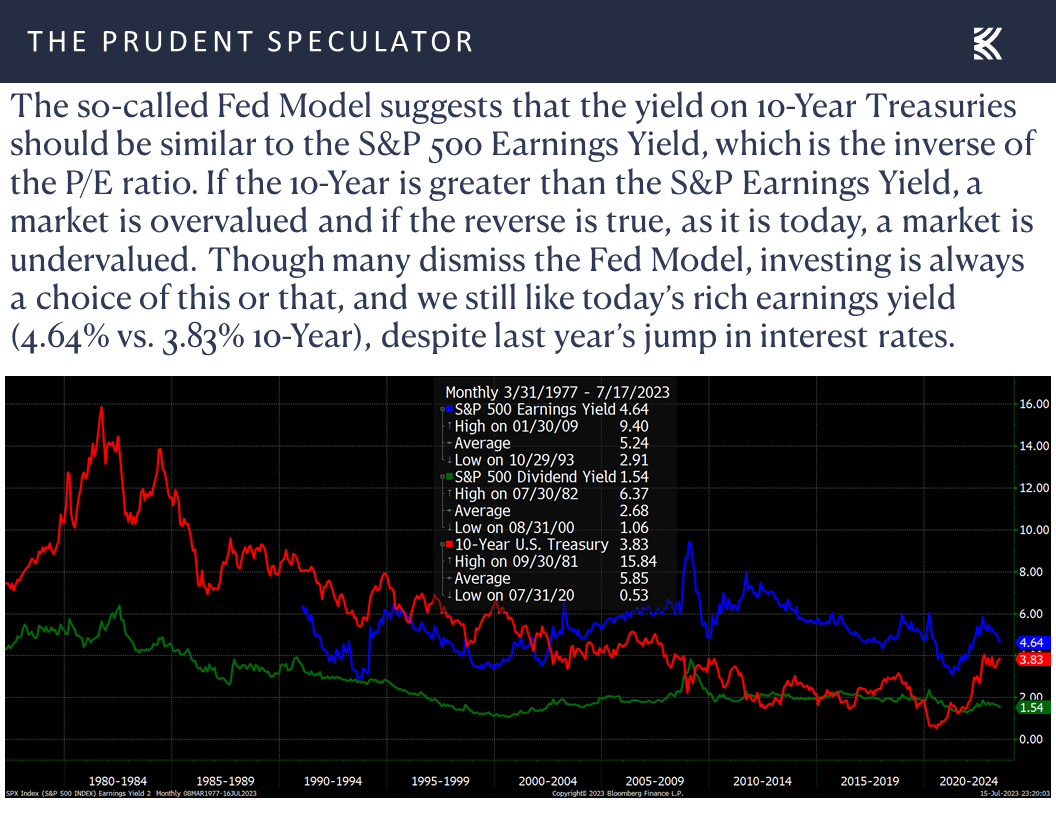

Valuations – Stocks, Especially Value, Remain Reasonably Priced

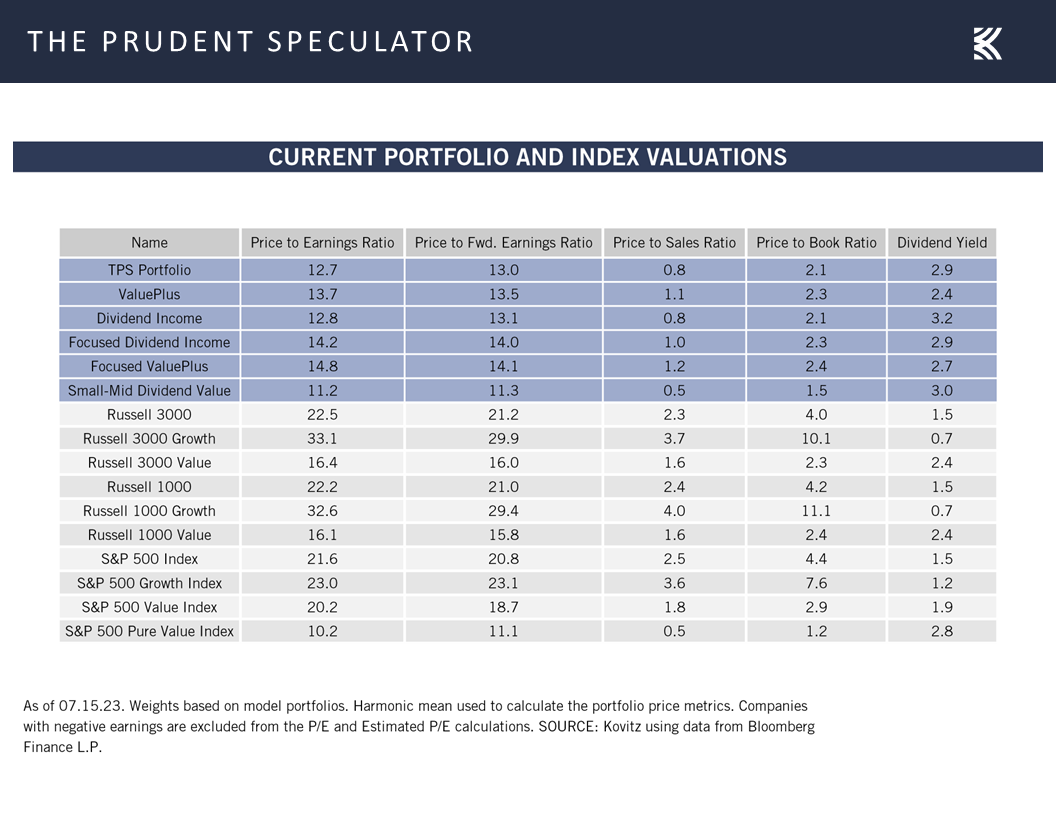

while our broadly diversified portfolios of what we believe to be undervalued stocks continue to boast very attractive valuation metrics,

Dividends – Bond Coupons Usually are Fixed but Dividends Have Risen Over Time

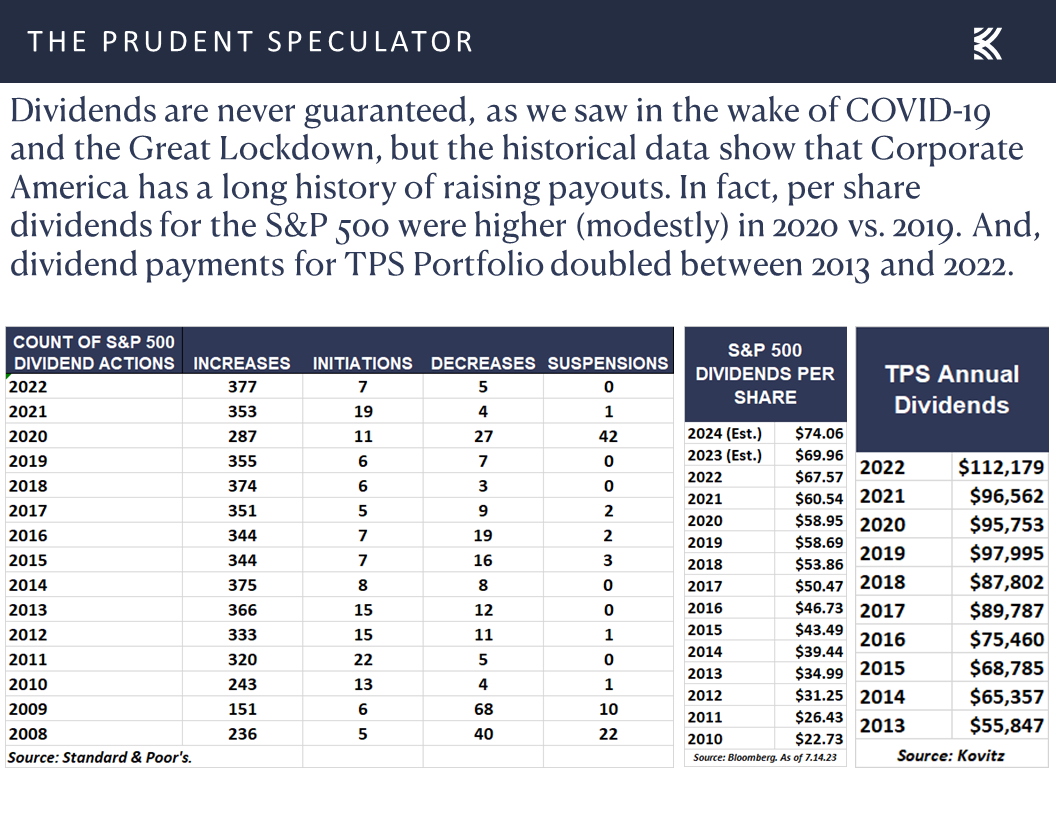

and we can’t forget that while bond coupons are usually fixed, dividend payouts on stocks have grown nicely over time.

Jamie Dimon on the Economy – Resilient with Healthy Consumer Balance Sheets

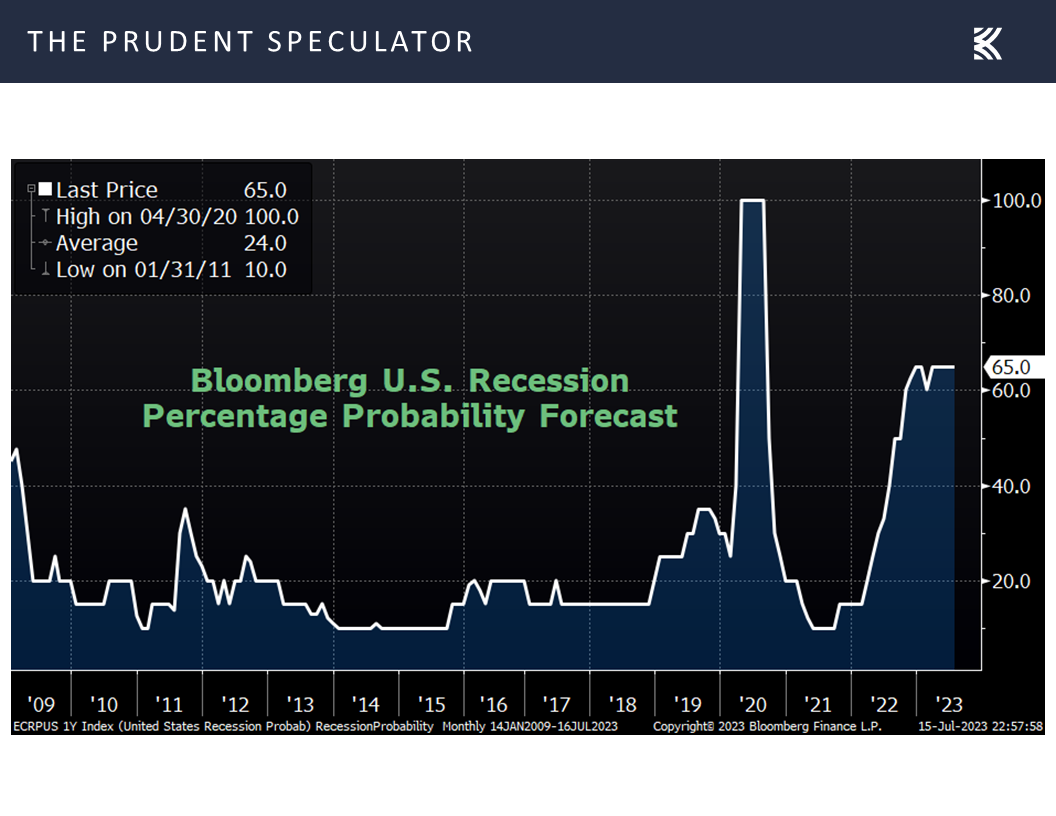

Certainly, we realize that many are worried that the U.S. economy will endure a recession within the next 12 months,

but we note that JPMorgan Chase (JPM – $149.77) Jaime Dimon said on Friday: “The U.S. economy continues to be resilient. Consumer balance sheets remain healthy, and consumers are spending, albeit a little more slowly. Labor markets have softened somewhat, but job growth remains strong. That being said, there are still salient risks in the immediate view—many of which I have written about over the past year. Consumers are slowly using up their cash buffers, core inflation has been stubbornly high (increasing the risk that interest rates go higher, and stay higher for longer), quantitative tightening of this scale has never occurred, fiscal deficits are large, and the war in Ukraine continues, which in addition to the huge humanitarian crisis for Ukrainians, has large potential effects on geopolitics and the global economy. While we cannot predict with any certainty how these factors will play out, we are currently managing the Firm to reliably meet the needs of our customers and clients in all environments.”

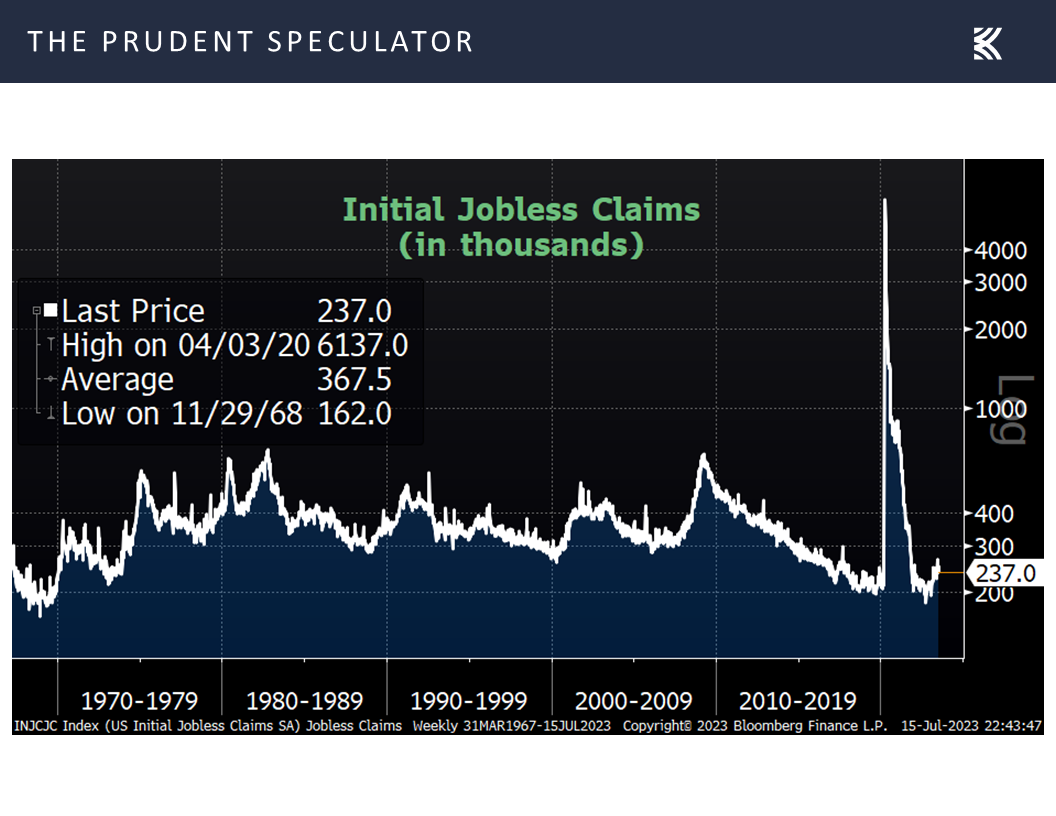

Speaking of jobs, the labor market remains very healthy, with first-time filings for unemployment benefits falling to 237,000 in the latest week,

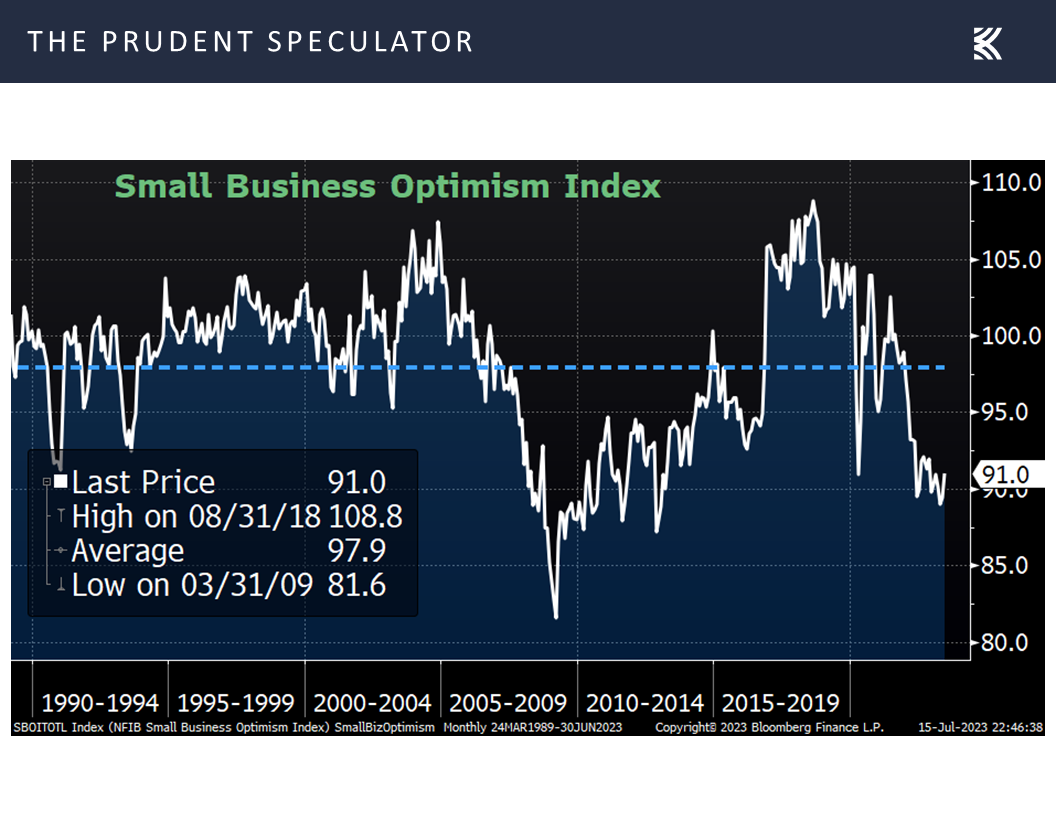

and the decent economic backdrop led to better-than-expected numbers on small-business optimism in June from the National Federation of Independent Business (NFIB),

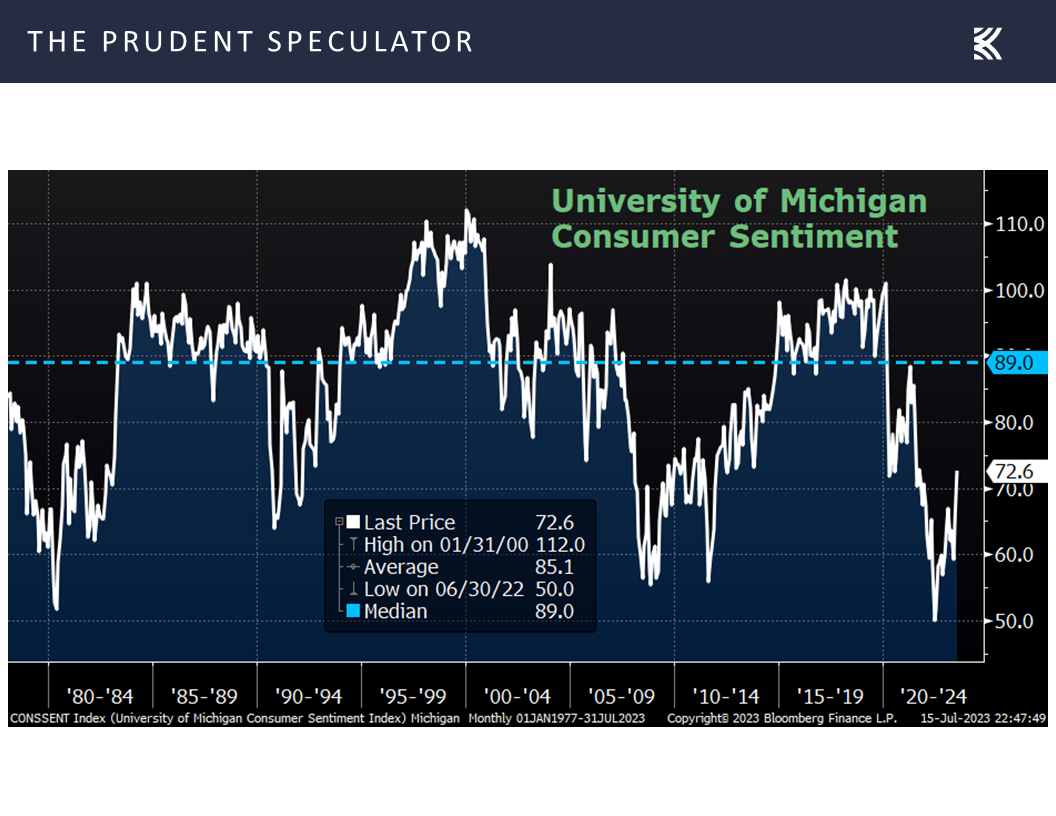

while the first look at consumer sentiment for July from the University of Michigan came in well above forecasts.

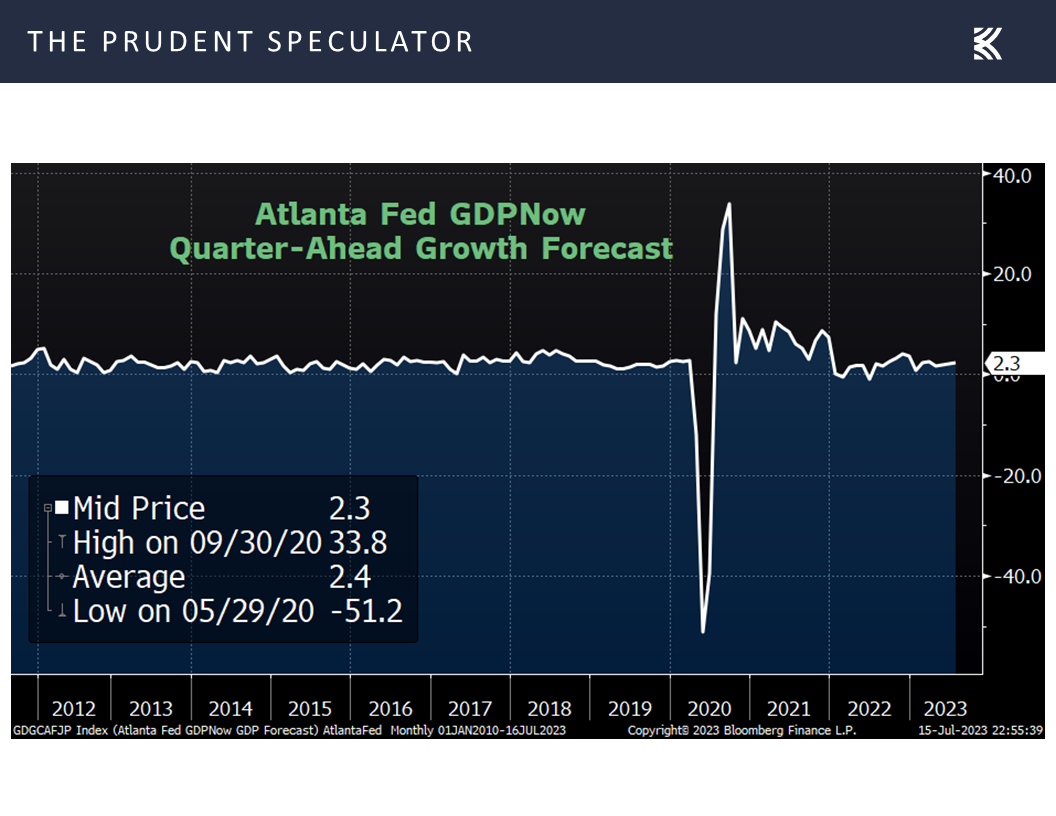

True, both of those Main Street confidence gauges continue to reside at levels well below their historical norms, but the latest estimate for Q2 U.S. GDP growth from the Atlanta Fed rose to 2.3% last week versus 2.1% the week before,

Earnings – Profit Growth Still the Forecast This Year and in 2024

and the current outlook for corporate profit growth from Standard & Poor’s is calling for bottom-up operating EPS for the S&P 500 to rise to $216.05 this year and $242.44 in 2024, versus $196.95 last year.

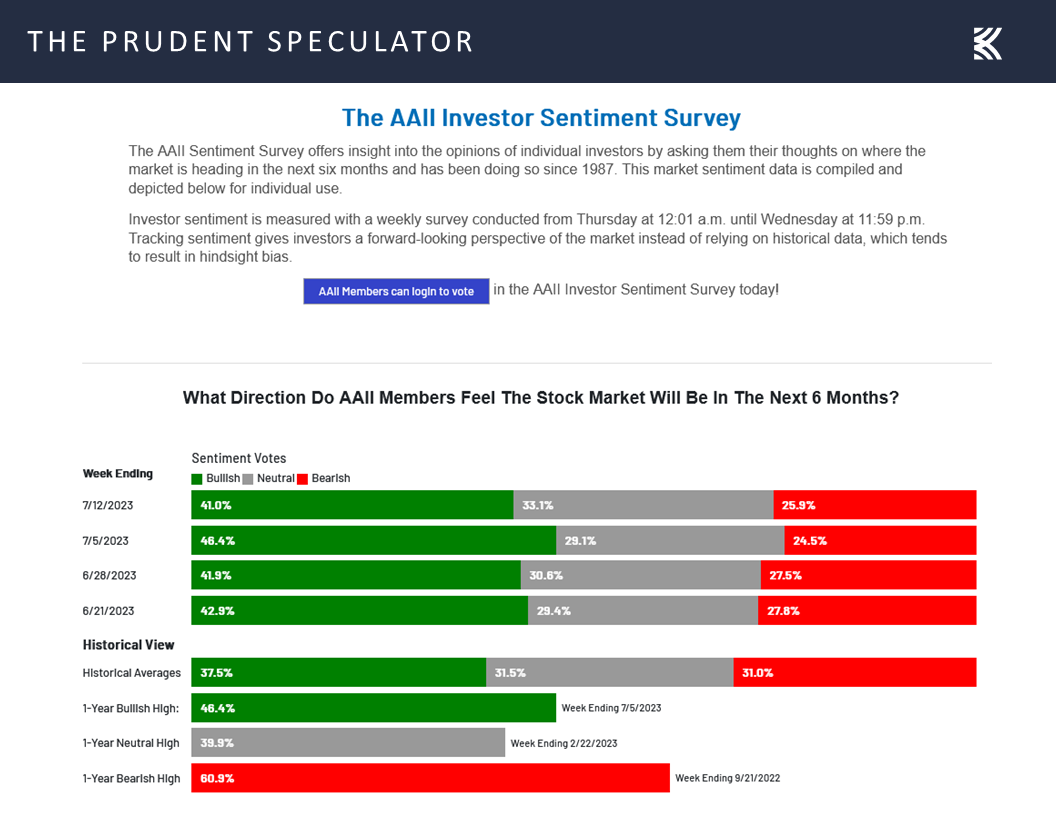

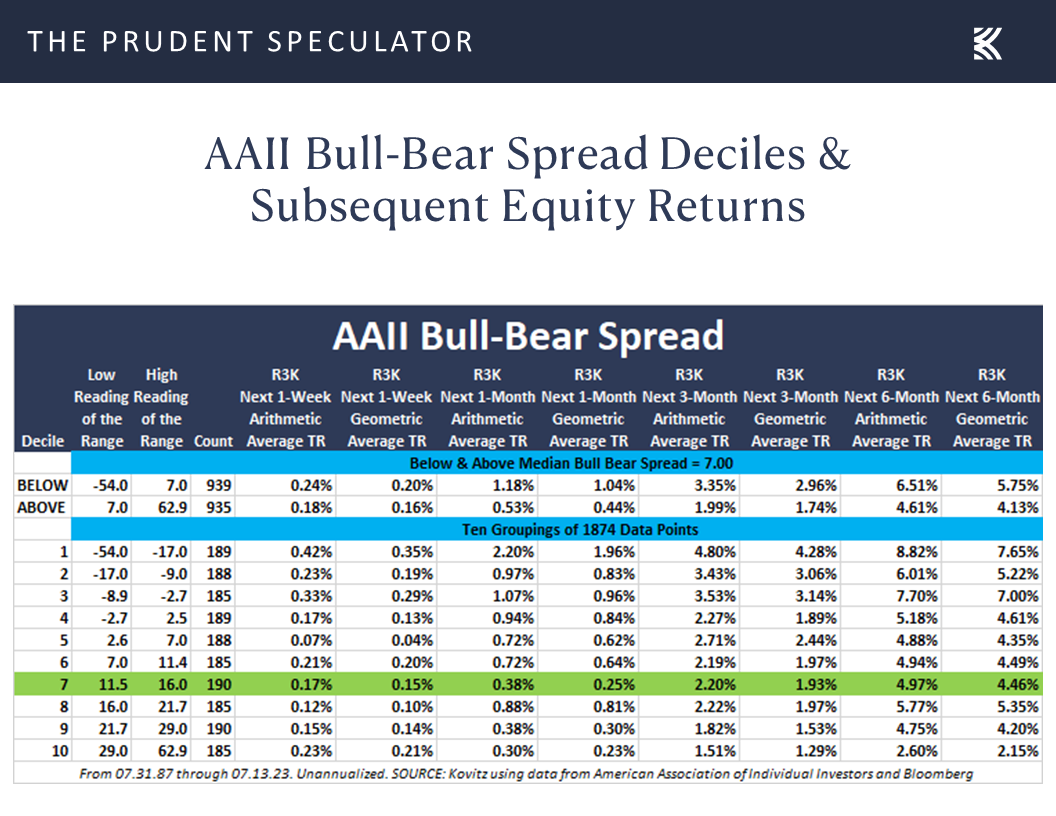

Sentiment – AAII Bullishness is Elevated

It is hard to envision stocks performing poorly if earnings turn out to be anywhere near those projections, so while we might argue that many investors have a bit too much of a bounce in their step, with the number of Bulls in the latest Sentiment Survey from the American Association of Individual Investors topping the Bears by 15.1 percentage points,

we see no reason to alter our faith in the long-term prospects for the equity markets.

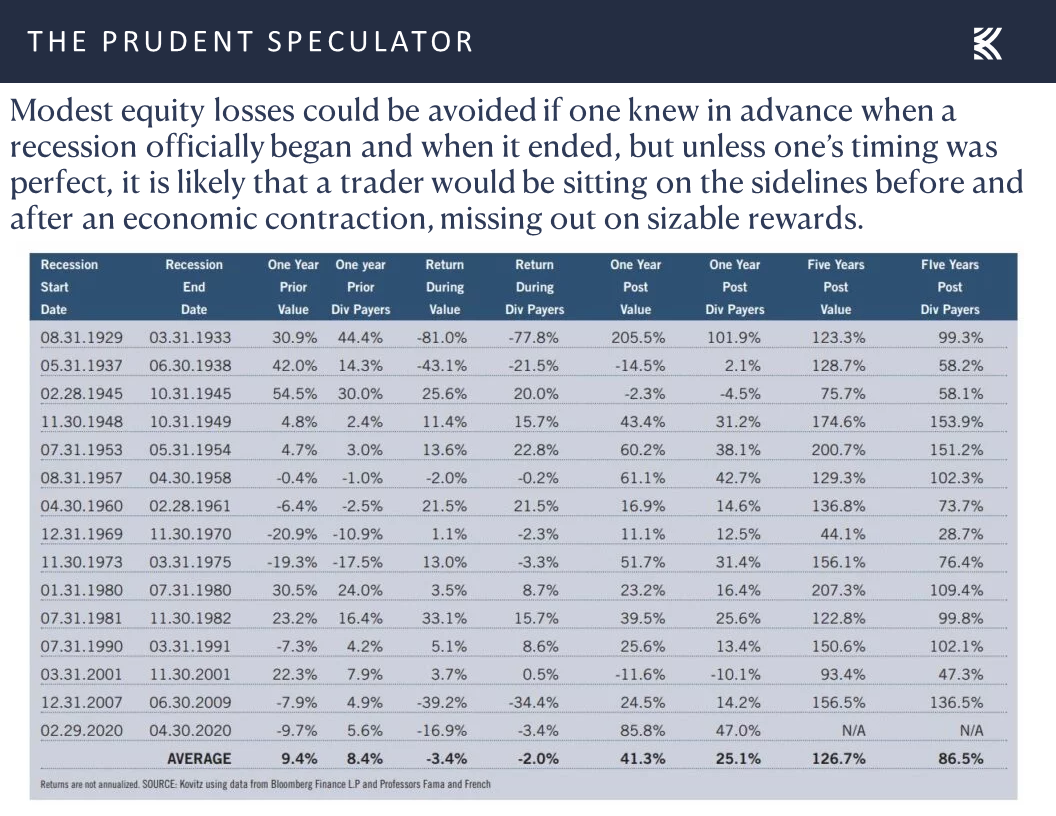

After all, just about any way the historical evidence is sliced and diced,

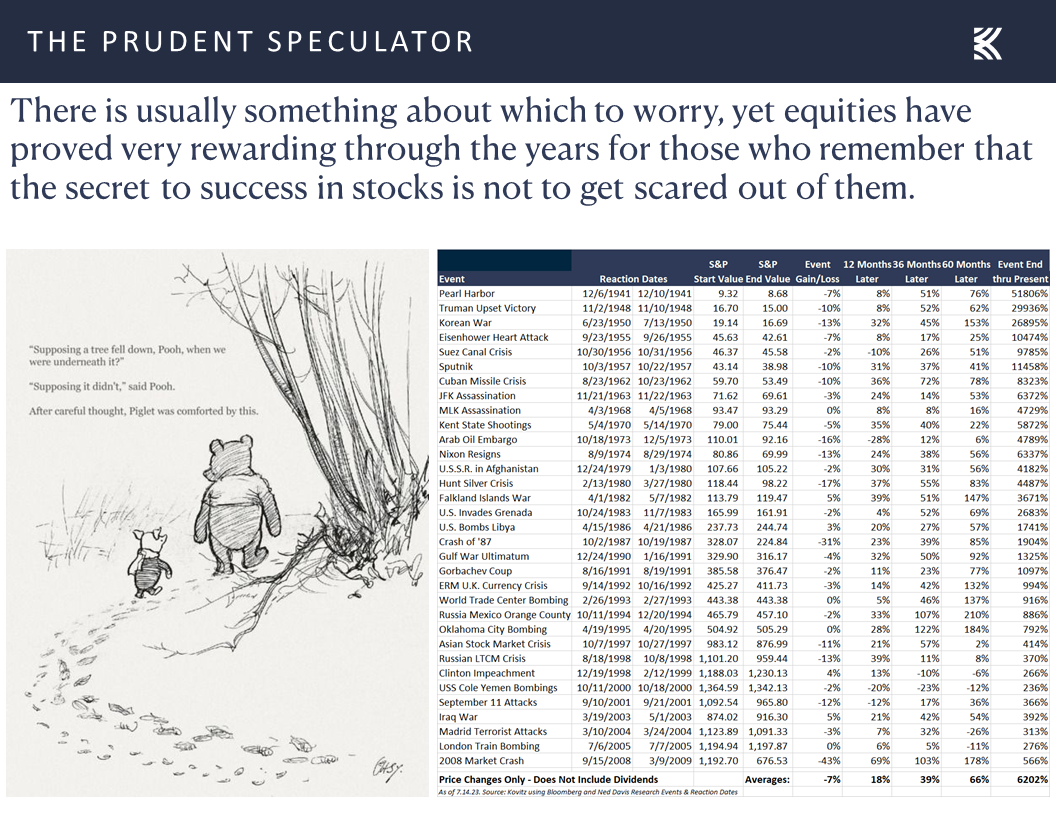

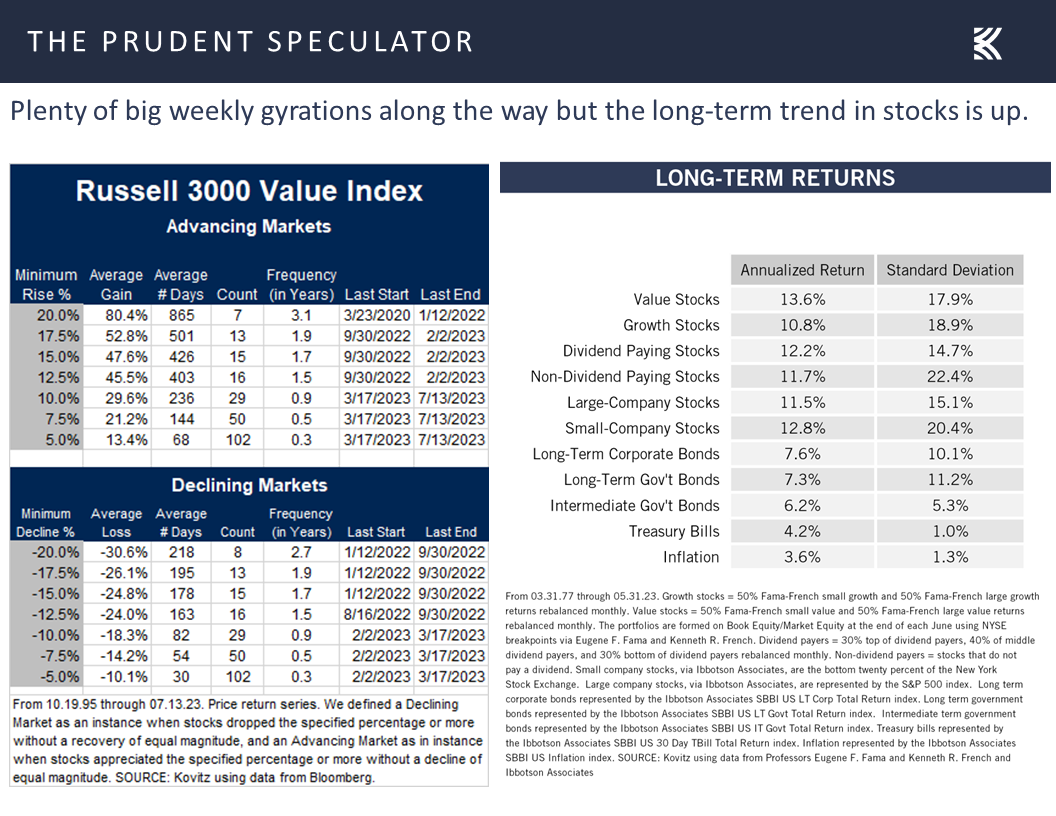

Patience – Stocks Have Proved Very Rewarding Over the Long Term

those who remember that the secret to success in stocks is not to get scared out of them have usually been well rewarded in the fullness of time, despite plenty of disconcerting headlines,

and numerous temporary trips south along the way.

Stock News – Updates on four stocks across three different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Inflation, Interest Rates, Dividends, Earnings and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Inflation, Interest Rates, Dividends, Earnings and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Friday for the Dow – Price-Weighting Can Skew The Index

Managed Care – UnitedHealth Defies Skeptics; Still Liking ELV and CVS

Inflation – CPI & PPI Both Cooler Than Expected

Interest Rates – Big Rally Last Week in the Price of the 10-Year Treasury

Valuations – Stocks, Especially Value, Remain Reasonably Priced

Dividends – Bond Coupons Usually are Fixed but Dividends Have Risen Over Time

Jamie Dimon on the Economy – Resilient with Healthy Consumer Balance Sheets

Earnings – Profit Growth Still the Forecast This Year and in 2024

Sentiment – AAII Bullishness is Elevated

Patience – Stocks Have Proved Very Rewarding Over the Long Term

Stock News – Updates on four stocks across three different sectors

Friday for the Dow – Price-Weighting Can Skew The Index

The trading week ended on a very sour note, given that the average stock in the broad-based Russell 3000 index declined 1.2% on Friday, even as the Dow Jones Industrial Average managed to close higher by 114 points, or 0.3%.

We suspect that many are aware that unlike most other market indexes, the Dow is price-weighted, meaning that the highest-priced stocks like Microsoft (MSFT – $345.24) and Home Depot have a very large impact and lower-priced stocks like Walgreens Boots, Intel (INTC – $33.15), Verizon Communications (VZ – $34.01) and Cisco Systems (CSCO – $50.38) are more or less insignificant in that they combined account for less than 3% of the 30-member benchmark.

Believe it or not, the Dow is calculated by adding up the price of all 30 components and dividing by a divisor, which today is 0.15173. This means that a $1 move up or down in the price of a Dow component translates into a 6.6 point move in the index. Obviously, a big change in a stock with a triple-digit stock price will result in a sizable advance or decline in the Dow, as was the case on Friday when managed care provider UnitedHealth (UNH), the most important Dow constituent, soared more than $32 after announcing better-than-feared Q2 financials.

Managed Care – UnitedHealth Defies Skeptics; Still Liking ELV and CVS

Incredibly, UnitedHealth’s 7.2% price increase accounted for nearly 214-points of the Dow’s 114-point advance on Friday, which means that the other 29 stocks collectively lost 100 Dow points. In fact, 19 of the 30 Dow components finished in the red on the day, providing another reminder that it is a market of stocks and not simply a stock market. We also note that we presently hold 15 Dow members (those in blue in the chart above) in our broadly diversified portfolios.

And speaking of UnitedHealth and its impact on our holdings in the managed care industry, we again witnessed another example of why we always strive to ignore short-term fluctuations in the price of the stocks that we own. A month ago, we penned an update on our managed care providers Elevance Health (ELV – $438.73) and CVS Health (CVS – $71.38) after their stocks were hit hard following a Goldman Sachs investment conference where a UnitedHealth representative highlighted his company’s increasing costs in the Medicare space.

Numerous older adults aged 65 and above covered under Medicare, who had seemingly largely stayed indoors during a long stretch of the pandemic, are getting “more comfortable accessing services for things that they might have pushed off a bit like knees and hips,” UNH management disclosed. Non-urgent surgeries and outpatient services such as heart procedures and knee and hip replacements that had been put off during and after the pandemic were picking up pace.

Short-sighted investors dumped ELV and CVS on that news, even as the former said its medical care trends and costs were in line with expectations, while folks ignored that the latter is broadly diversified across the health care spectrum. Not to everyone’s surprise, UNH reported Q2 financial results that beat both top-and bottom-line expectations, and though margins in its Medicare coverage were squeezed, multiple other parts of the firm were hitting on all cylinders.

UNH CFO John Rex also noted that elevated costs in the Medicare space would continue in Q3, but they were expected to seasonally adjust downwards in Q4. CEO Andrew Witty added during the earnings call, “If I had the choice on a slightly suppressed margin in Q2 or the very significant growth that we’ve taken in, I’ll take the growth all day long, and I’ll take that growth because it’s going to underpin years of growth going forward.” The results and earnings call seemed to ease some overdone investor concerns and sent ELV rebounding by 5.0% and allowed CVS to stay in the green on an otherwise ugly market day on Friday.

While ELV and CVS don’t report their Q2 results until early August, we think emotional reactions to bits of sensationalized news or non-full-context quotes or short-term-focused analyst upgrades and downgrades can be “unhealthy” for long-term oriented investors. We also continue to like that ELV trades at 13.1 times forward adjusted EPS estimates and CVS (which owns Aetna) at 8.3 times, versus UnitedHealth’s 18.3 times. Our Target Prices for ELV and CVS are $620 and $130, respectively.

Inflation – CPI & PPI Both Cooler Than Expected

No doubt, a discussion of Friday’s miserable day of trading ignores the fact that the broad-based rally underway since the end of May resumed last week, with handsome gains across the board for equities over the full five days. The catalyst for the advance was surprisingly good news on inflation,

as the Consumer Price Index (CPI) rose only 0.2% in June, with the year-over-year increase coming in at 3.0%, which is in line with the historical norm going back to the 1920s.

True, the so-called core CPI rate, which excludes volatile food and energy prices, climbed 4.8%, well above the Federal Reserve’s 2.0% target, but this tally slowed from a 5.3% increase in May to a nearly two-year low.

Even more impressive, perhaps, the headline figure for inflation at the wholesale level is now virtually flat, as the Producer Price Index (PPI) rose only 0.1% on a year-over-year basis. The core PPI advanced 2.6% on a year-over-year basis, but this gain was the smallest since March 2021.

To be sure, the Federal Reserve is nowhere near shouting, “Mission Accomplished,” in its fight against inflation. Fed governor Christopher Waller commented on the favorable CPI reading on Thursday, stating, “The recent report warmed my heart, but…I’ve got to make policy with my head. And I can’t do that on one data point.” And Dallas Fed President Lorie Logan, recently said, “I remain very concerned about whether inflation will return to target in a sustainable and timely way.

Interest Rates – Big Rally Last Week in the Price of the 10-Year Treasury

Despite the tough talk, market expectations for additional Fed rate hikes this year pulled back in the latest week, with the Fed Funds futures suggesting a 5.35% year-end rate, down from 5.39% a week ago,

and investors gravitating toward U.S. Treasuries, pushing the yield on the benchmark government bond down to 3.83% last week, versus 4.06% at the end of the week prior.

Of course, we continue to lose little sleep over Jerome H. Powell & Co.’s fight against inflation, especially as the last time (the Volcker Years) the Federal Reserve faced a similar battle, Value Stocks and Dividend Payers, like those that we have long favored, enjoyed spectacular returns, despite economic recessions taking place in 1980 and 1981.

Further, even as interest rates are substantially higher today than where they have been in recent years, equity valuations, in general, still compare favorably to fixed income,

Valuations – Stocks, Especially Value, Remain Reasonably Priced

while our broadly diversified portfolios of what we believe to be undervalued stocks continue to boast very attractive valuation metrics,

Dividends – Bond Coupons Usually are Fixed but Dividends Have Risen Over Time

and we can’t forget that while bond coupons are usually fixed, dividend payouts on stocks have grown nicely over time.

Jamie Dimon on the Economy – Resilient with Healthy Consumer Balance Sheets

Certainly, we realize that many are worried that the U.S. economy will endure a recession within the next 12 months,

but we note that JPMorgan Chase (JPM – $149.77) Jaime Dimon said on Friday: “The U.S. economy continues to be resilient. Consumer balance sheets remain healthy, and consumers are spending, albeit a little more slowly. Labor markets have softened somewhat, but job growth remains strong. That being said, there are still salient risks in the immediate view—many of which I have written about over the past year. Consumers are slowly using up their cash buffers, core inflation has been stubbornly high (increasing the risk that interest rates go higher, and stay higher for longer), quantitative tightening of this scale has never occurred, fiscal deficits are large, and the war in Ukraine continues, which in addition to the huge humanitarian crisis for Ukrainians, has large potential effects on geopolitics and the global economy. While we cannot predict with any certainty how these factors will play out, we are currently managing the Firm to reliably meet the needs of our customers and clients in all environments.”

Speaking of jobs, the labor market remains very healthy, with first-time filings for unemployment benefits falling to 237,000 in the latest week,

and the decent economic backdrop led to better-than-expected numbers on small-business optimism in June from the National Federation of Independent Business (NFIB),

while the first look at consumer sentiment for July from the University of Michigan came in well above forecasts.

True, both of those Main Street confidence gauges continue to reside at levels well below their historical norms, but the latest estimate for Q2 U.S. GDP growth from the Atlanta Fed rose to 2.3% last week versus 2.1% the week before,

Earnings – Profit Growth Still the Forecast This Year and in 2024

and the current outlook for corporate profit growth from Standard & Poor’s is calling for bottom-up operating EPS for the S&P 500 to rise to $216.05 this year and $242.44 in 2024, versus $196.95 last year.

Sentiment – AAII Bullishness is Elevated

It is hard to envision stocks performing poorly if earnings turn out to be anywhere near those projections, so while we might argue that many investors have a bit too much of a bounce in their step, with the number of Bulls in the latest Sentiment Survey from the American Association of Individual Investors topping the Bears by 15.1 percentage points,

we see no reason to alter our faith in the long-term prospects for the equity markets.

After all, just about any way the historical evidence is sliced and diced,

Patience – Stocks Have Proved Very Rewarding Over the Long Term

those who remember that the secret to success in stocks is not to get scared out of them have usually been well rewarded in the fullness of time, despite plenty of disconcerting headlines,

and numerous temporary trips south along the way.

Stock News – Updates on four stocks across three different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.