The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss inflation, interest rates, econ data, reasons for optimism and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 5 Sales Across 4 Accounts

Week in Review – Big Advance for Stocks; Value Leads the Way

Inflation – CPI & PPI Lower-than Expected

Interest Rates – Yields Move Lower

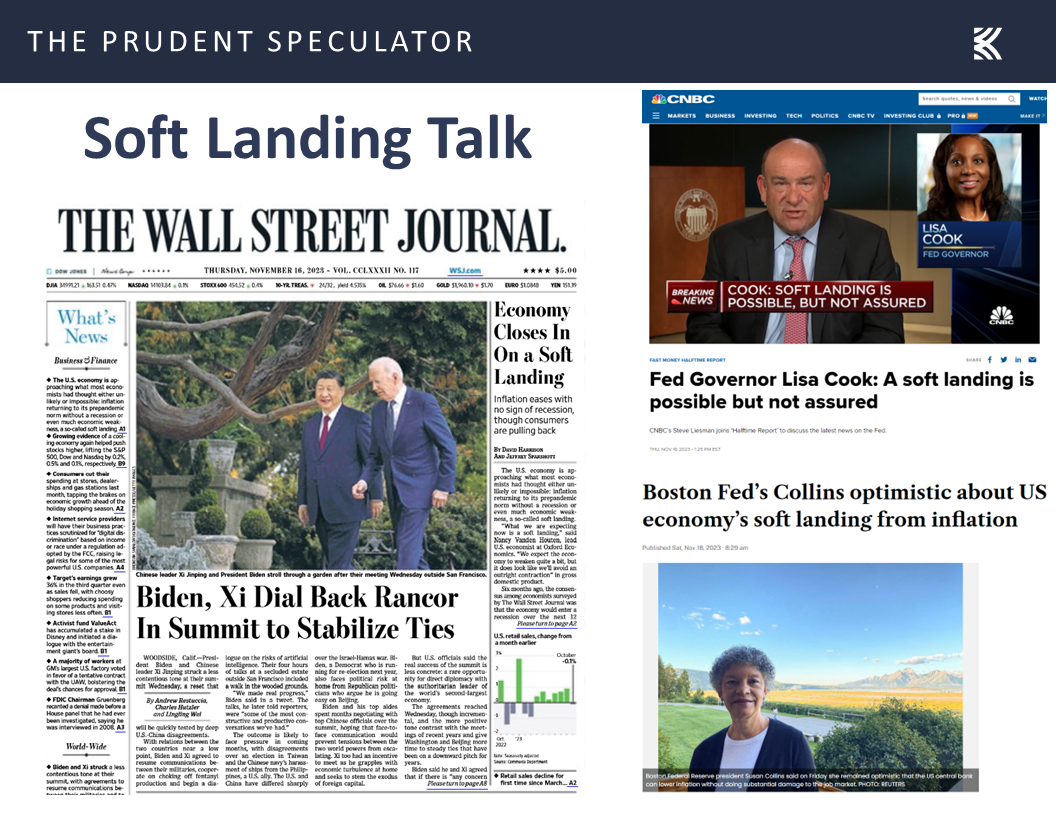

Econ Data – Soft Landing Still Possible

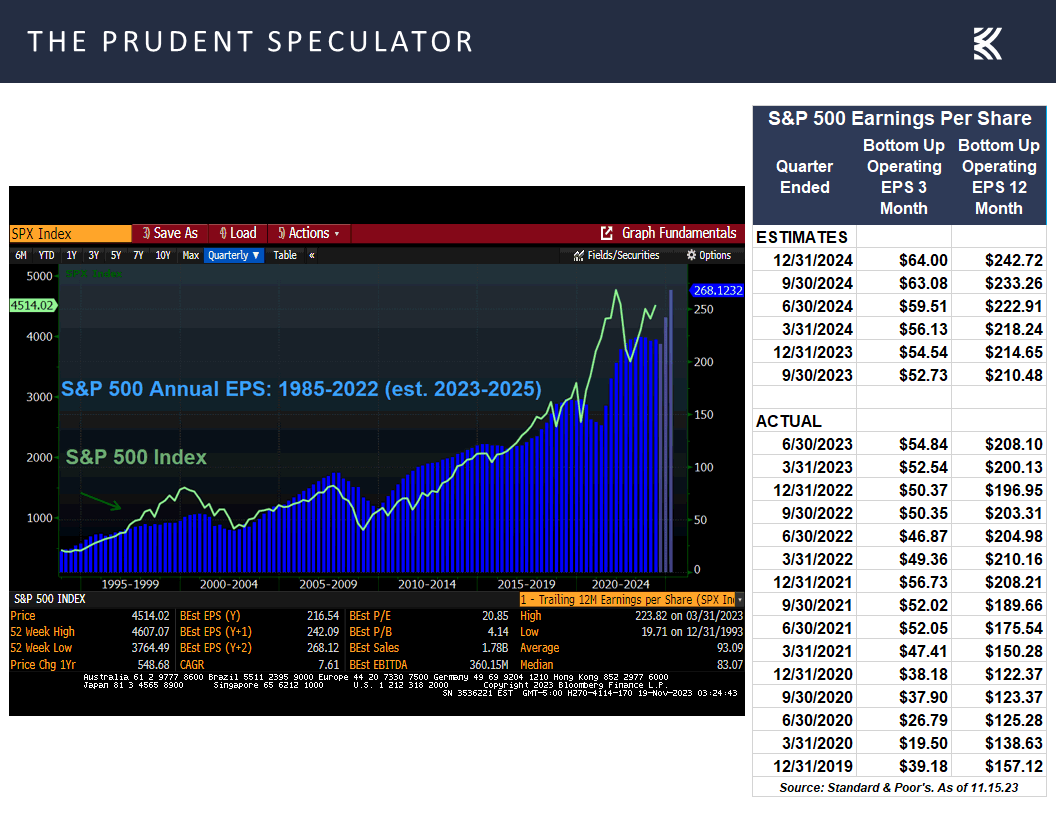

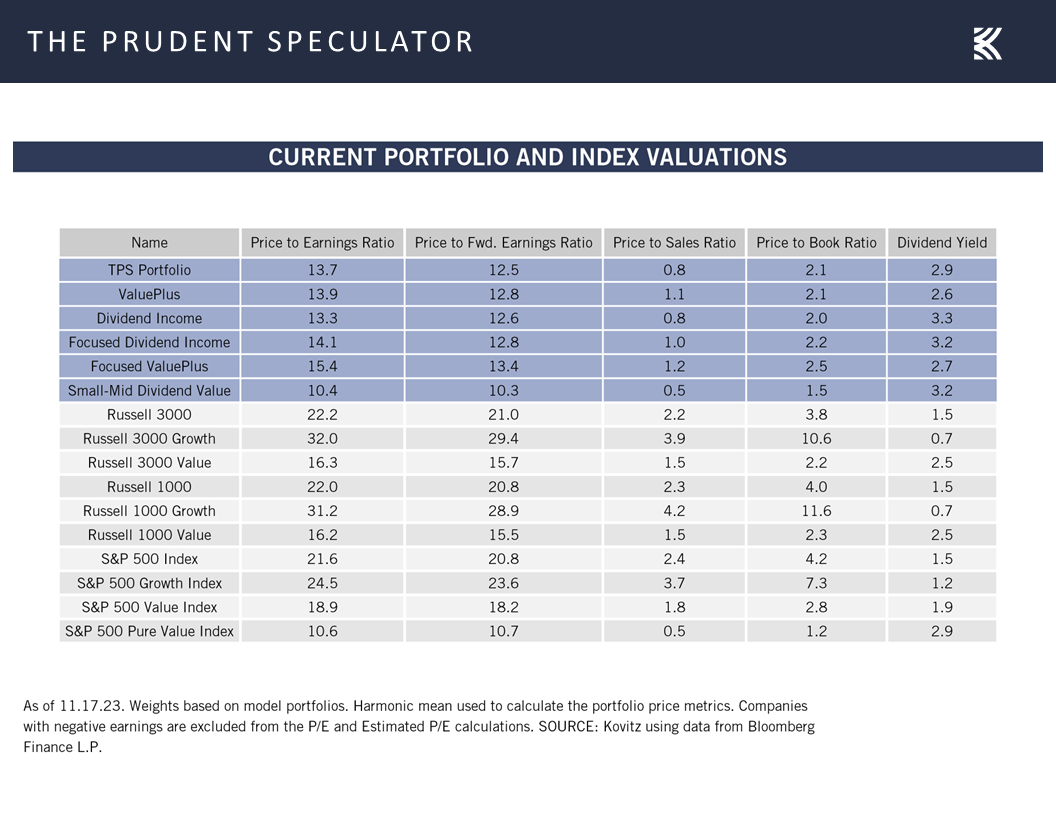

Reasons for Optimism – Earnings Growth, Valuations & Calendar

Stock News – Updates on six stocks across six different sectors

Week in Review – Big Advance for Stocks; Value Leads the Way

The seasonally favorable November – April period for equities,

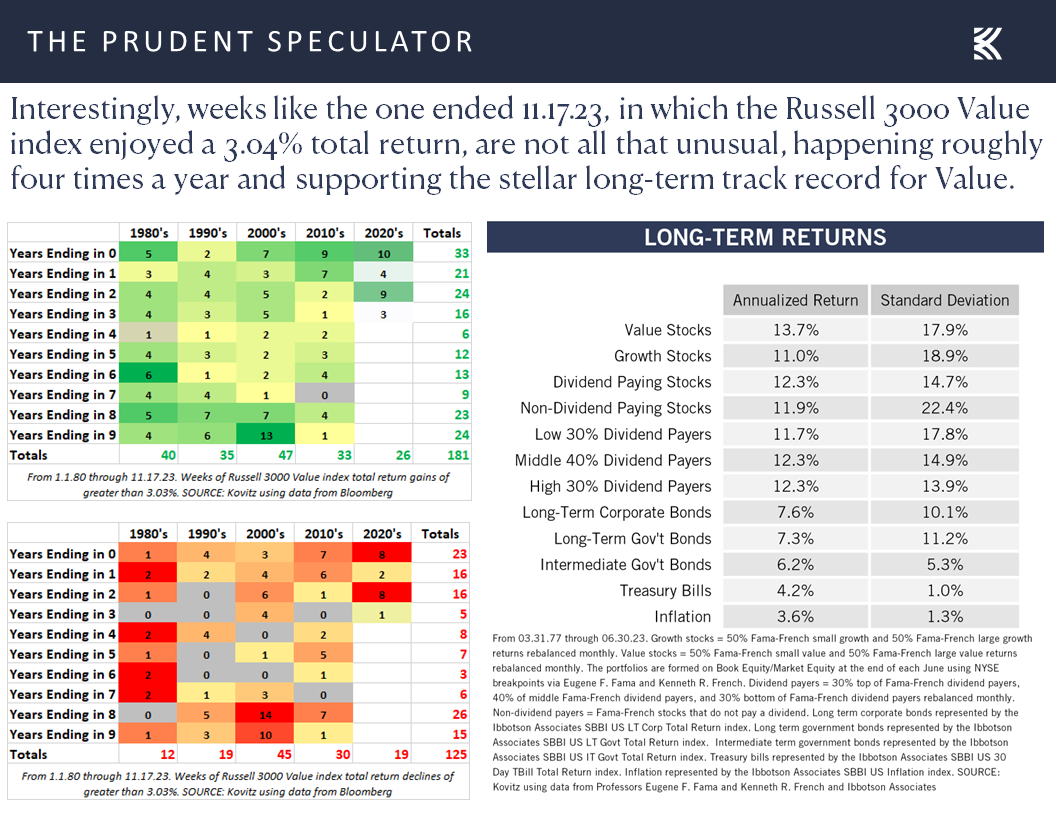

added to its strong start this time around, posting the second terrific week out of the past three. Happily, as with the first week in this span, but definitely not the second, the average stock fared much better than the major market averages and Value showed that it can win a very-short-term returns race in addition to the long-term performance derby.

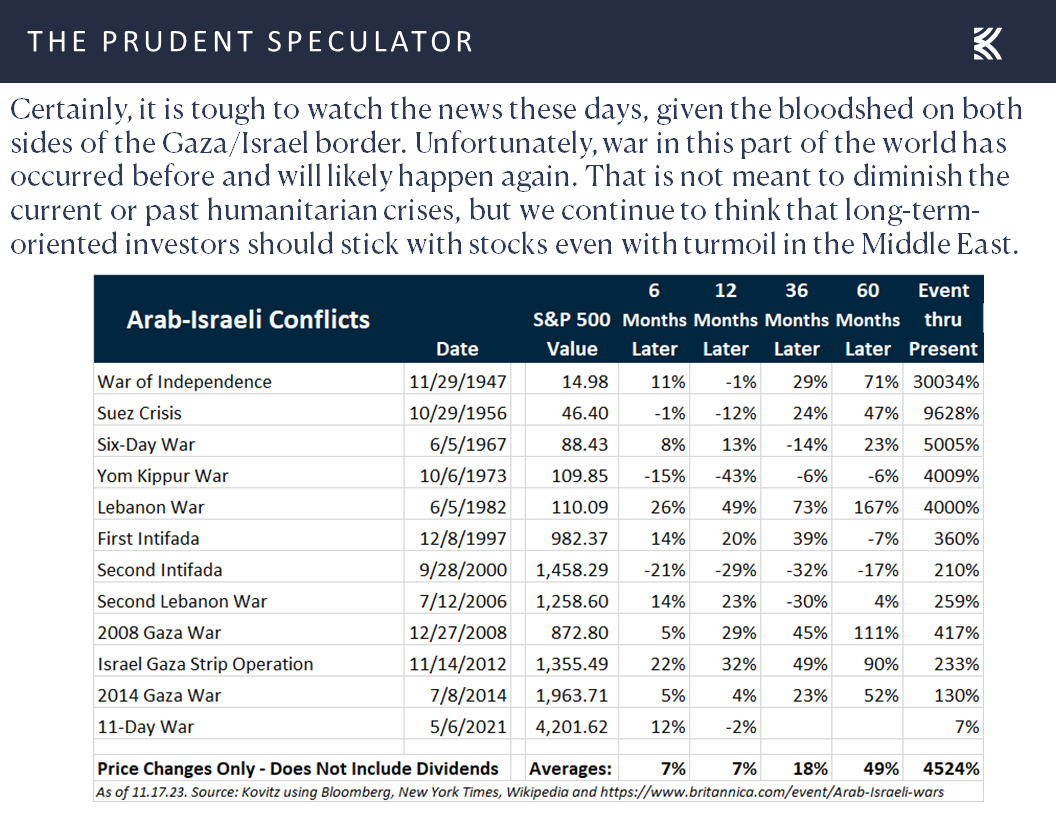

Though some would argue that the Biden-Xi summit talks in the Bay Area were a positive, it was not as if there was much in the way of positive developments on the geopolitical stage, either from the Middle East,

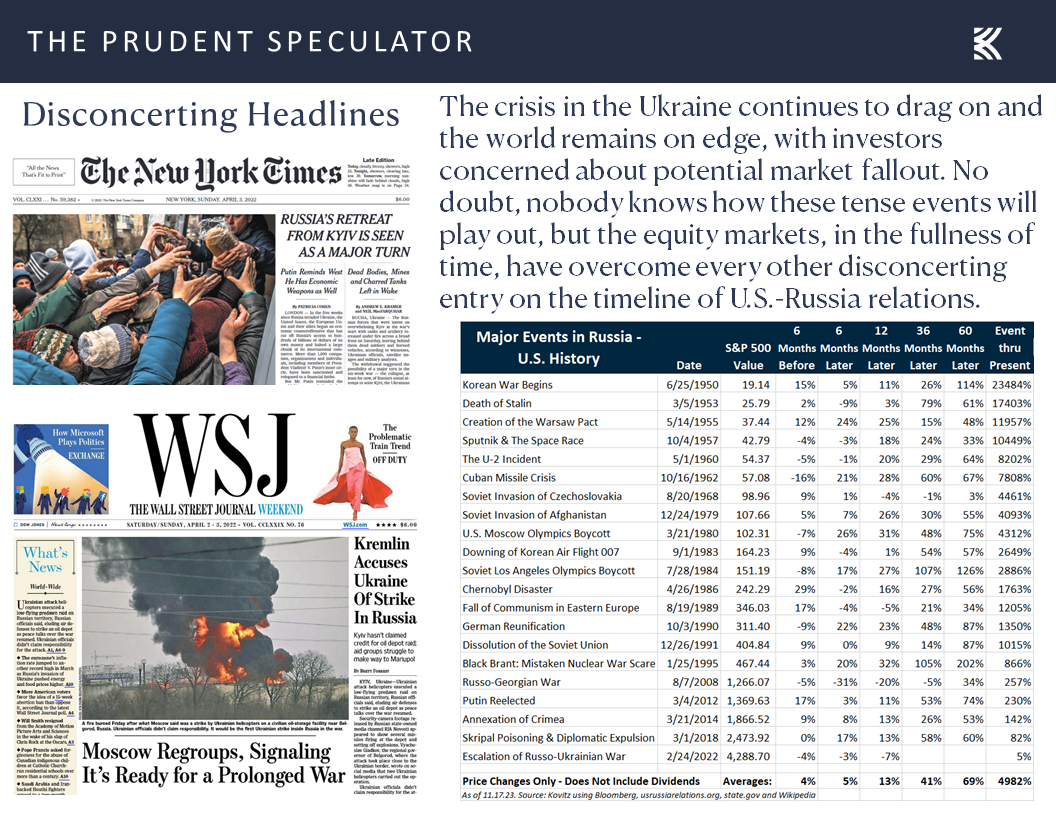

or Ukraine,

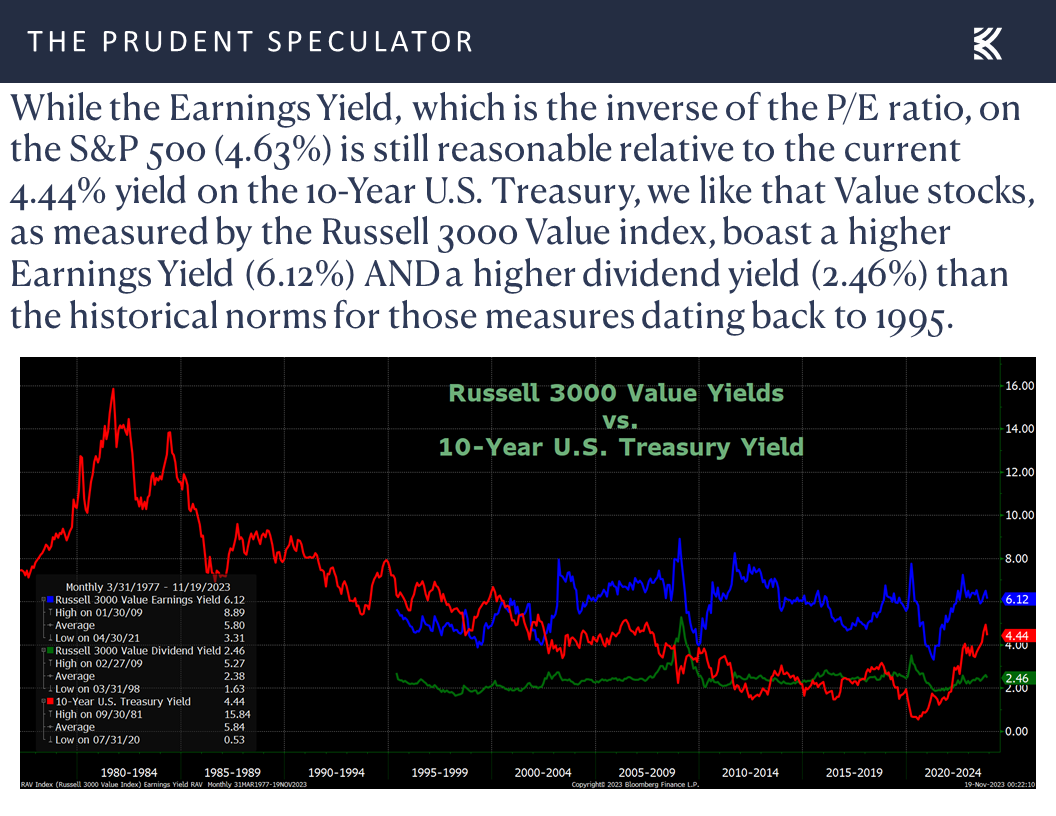

but the catalyst for the equity rally, aside from the fact that most stocks are inexpensively valued,

Inflation – CPI & PPI Lower-than Expected

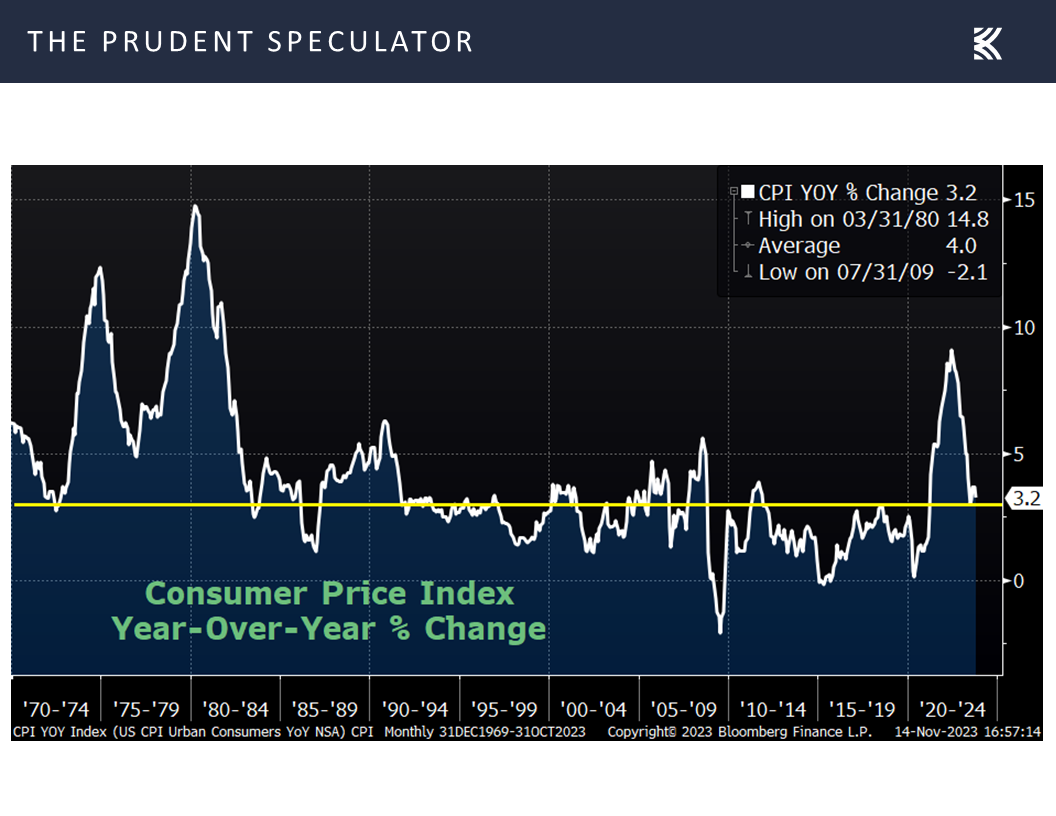

was news that consumer price inflation in October slowed to 3.2%, a slightly lower rate than expected,

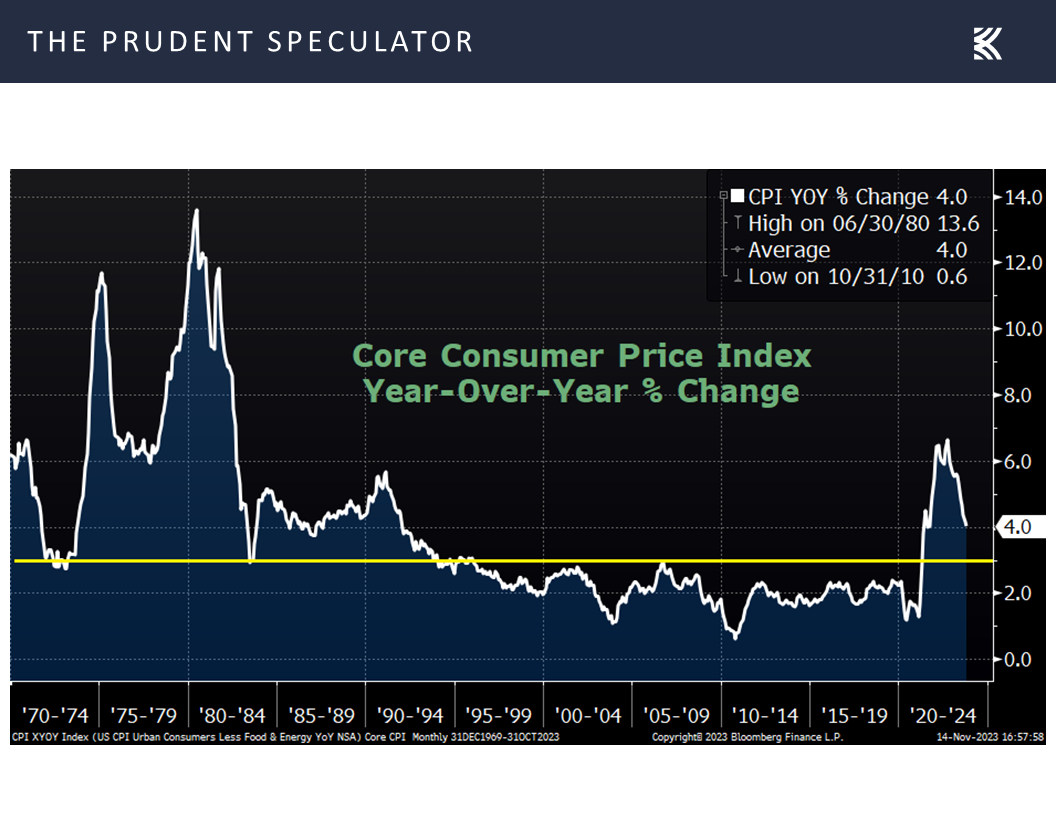

and the core rate (excludes volatile food and energy prices) rose 4.0%, less than forecasts and the lowest year-over-year increase in more than two years.

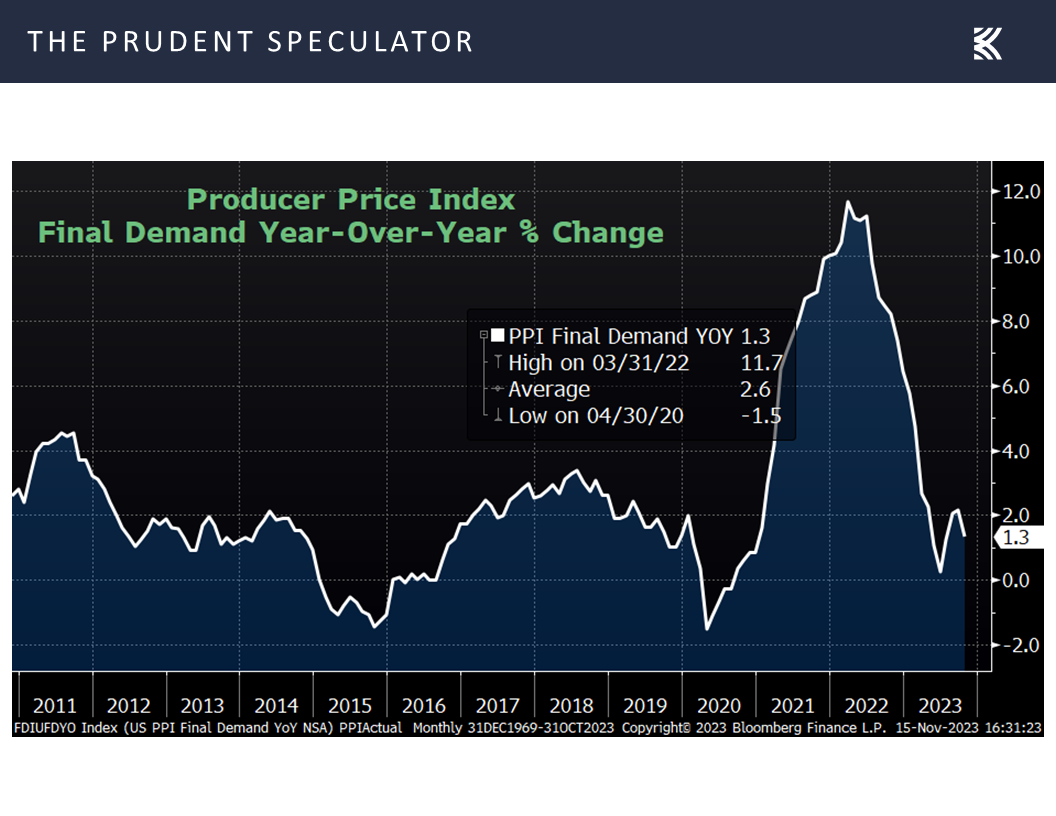

Throw in a big drop in rate of inflation at the producer level,

Interest Rates – Yields Move Lower

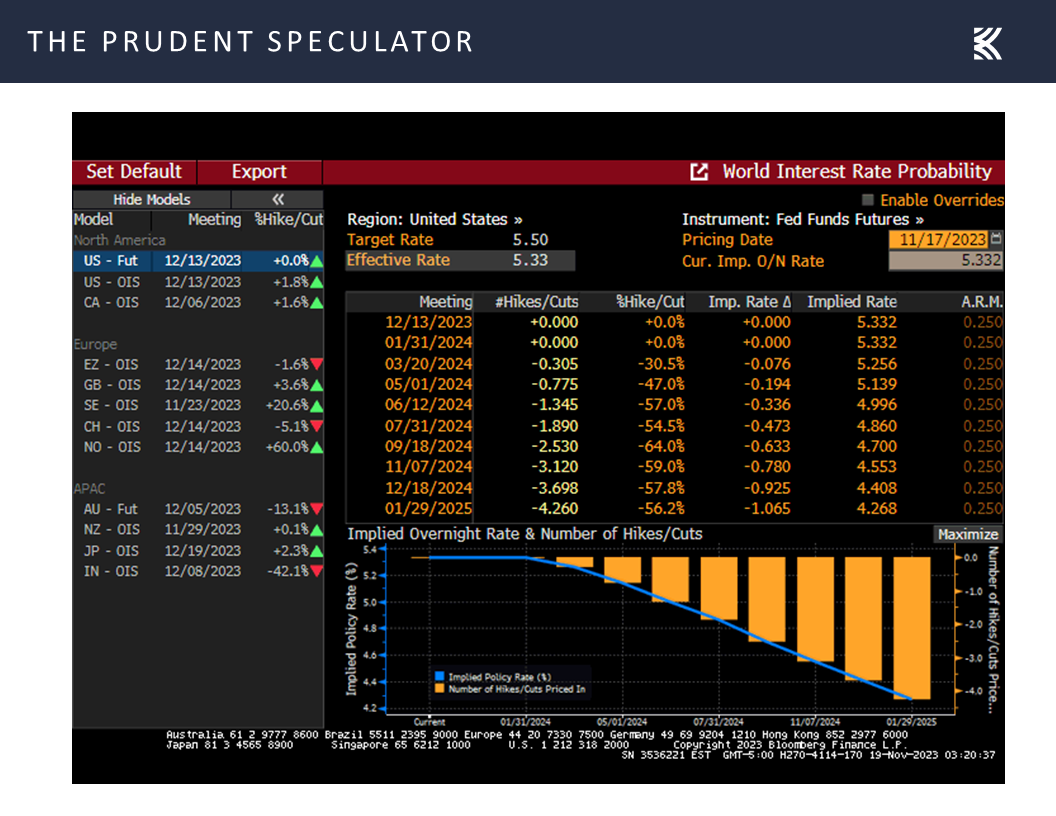

and the probabilities, per the futures market, of easier monetary policy with cuts in the Fed Funds rate increased last week, as the year-end 2024 projection for the benchmark lending rate now stands at 4.41%, down from 4.62% the week prior,

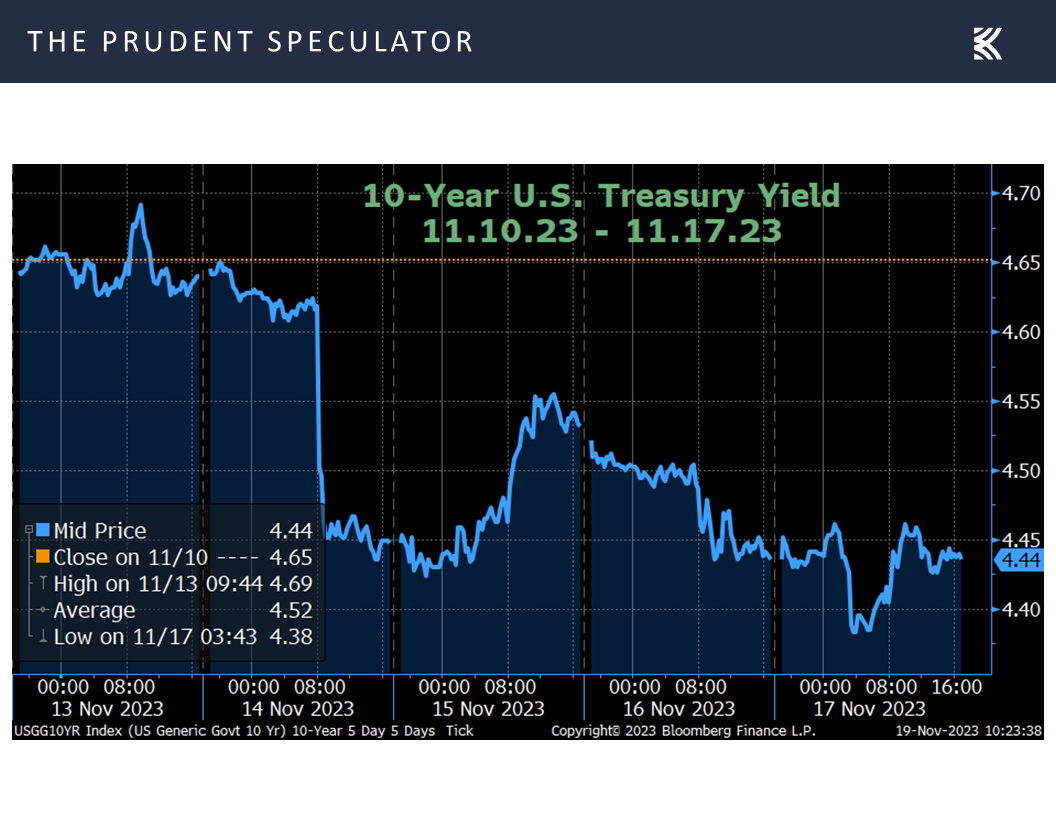

while there was a sizable advance in bond prices, dropping the yield on the 10-Year U.S. Treasury from 4.65% to 4.44%.

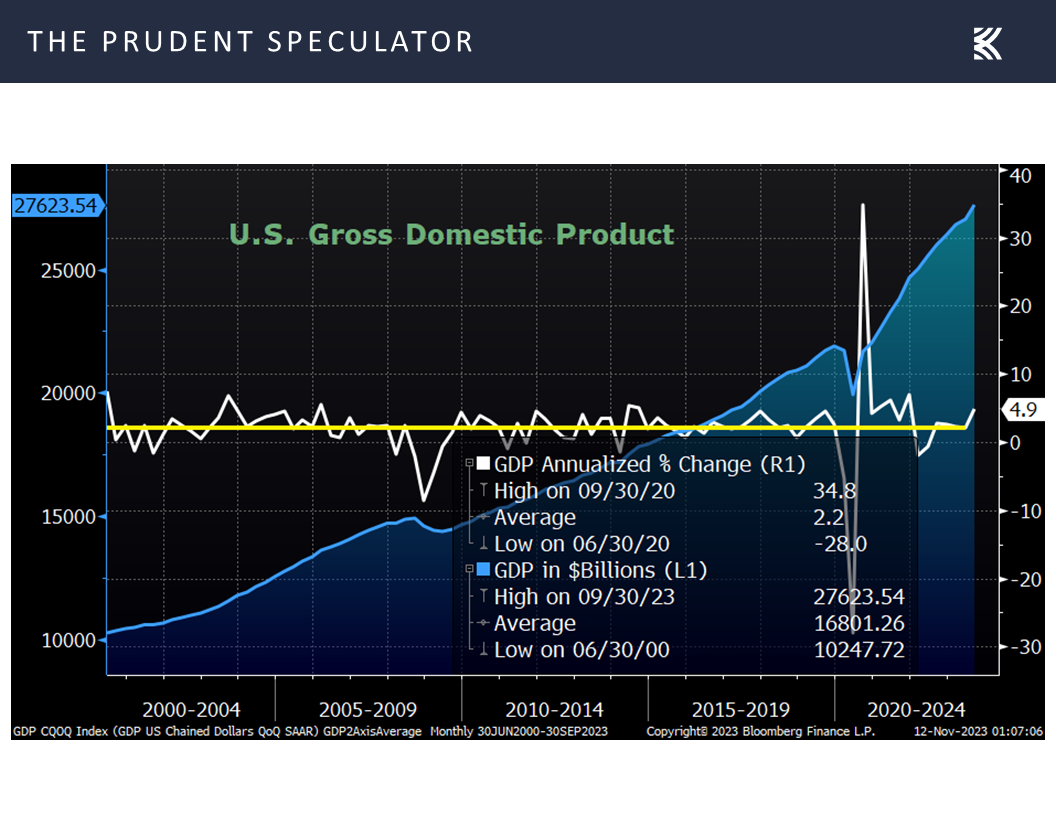

Econ Data – Soft Landing Still Possible

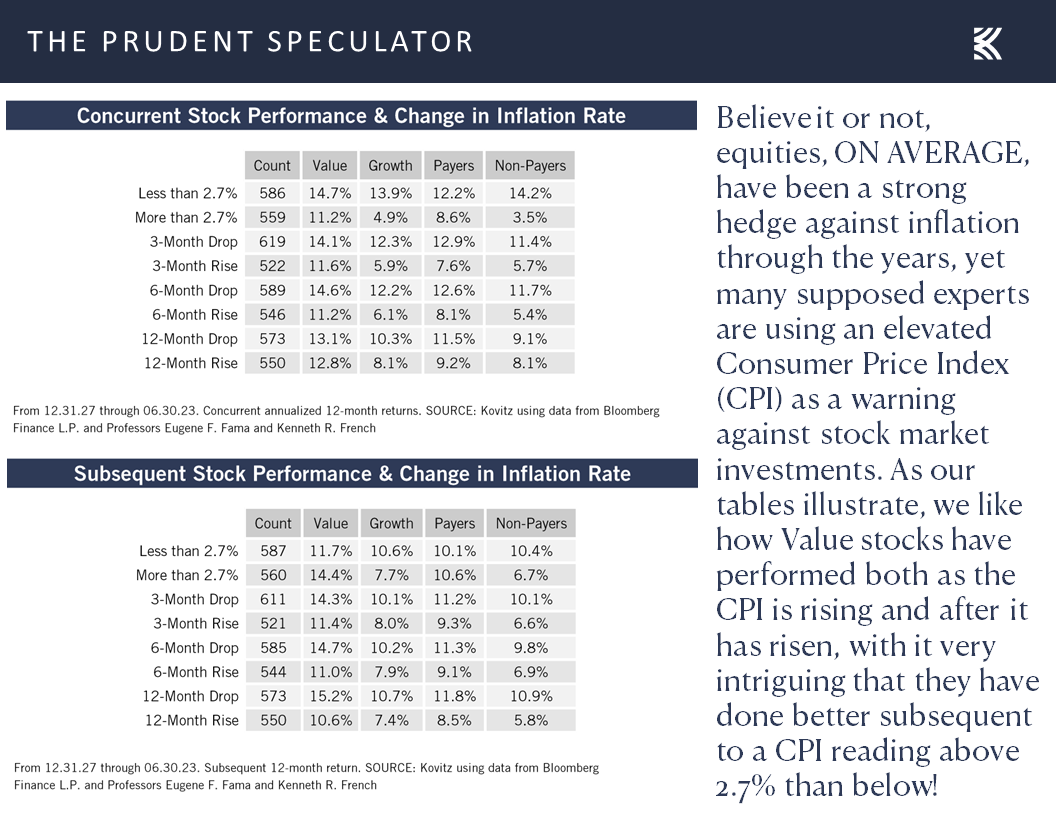

Although history suggests that equities more often than not have been a terrific hedge against inflation,

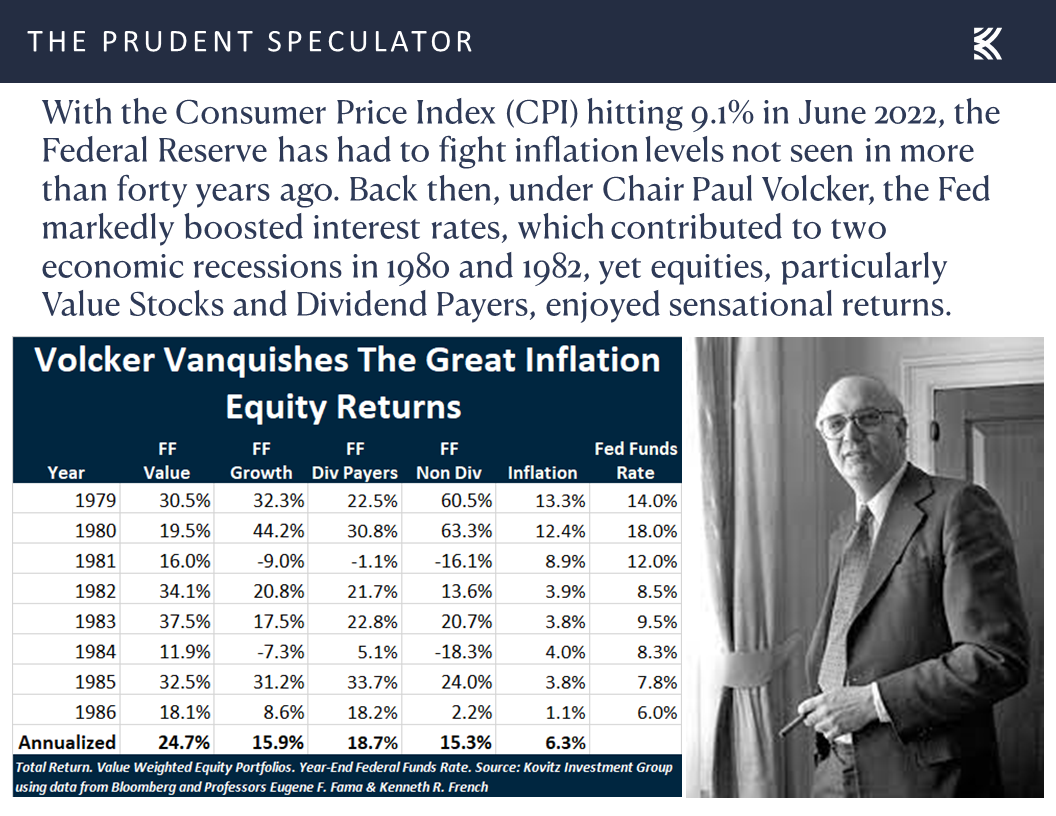

and stocks soared in price in the early 1980s during the last Federal Reserve battle with inflation rates as high as what has been witnessed this cycle,

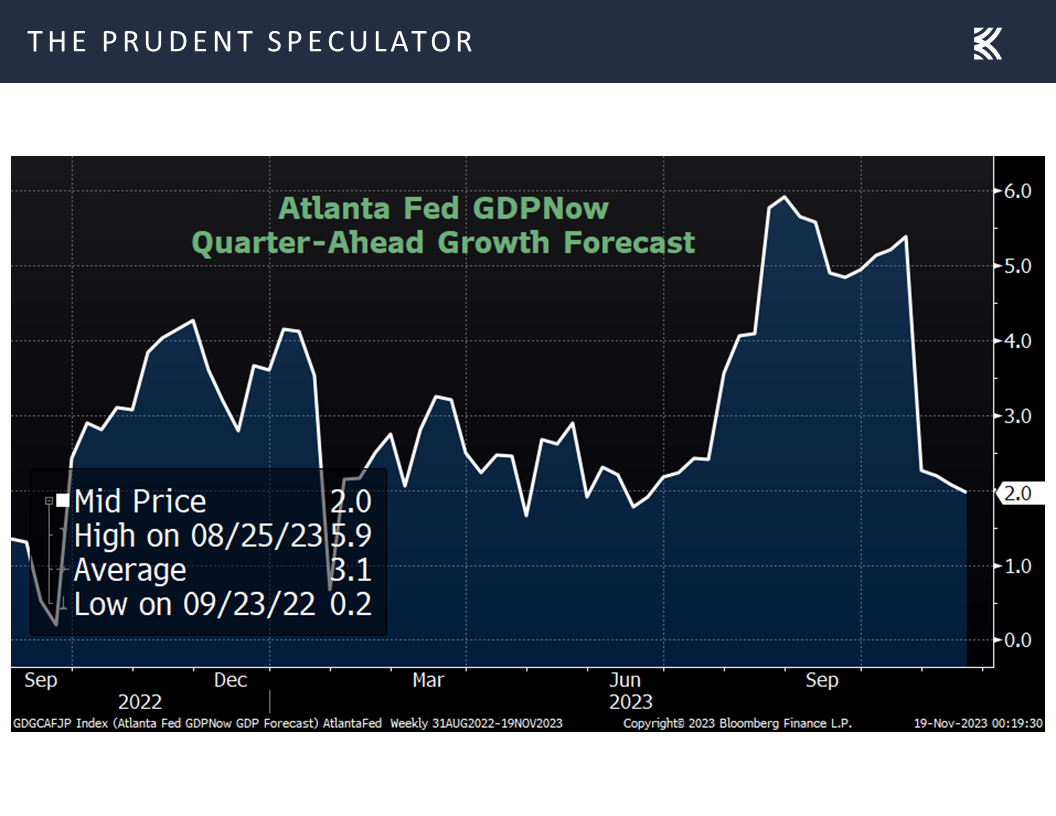

it certainly helps that the economy has held up remarkably well with real (inflation-adjusted) GDP growth coming in at an impressive 4.9% in Q3.

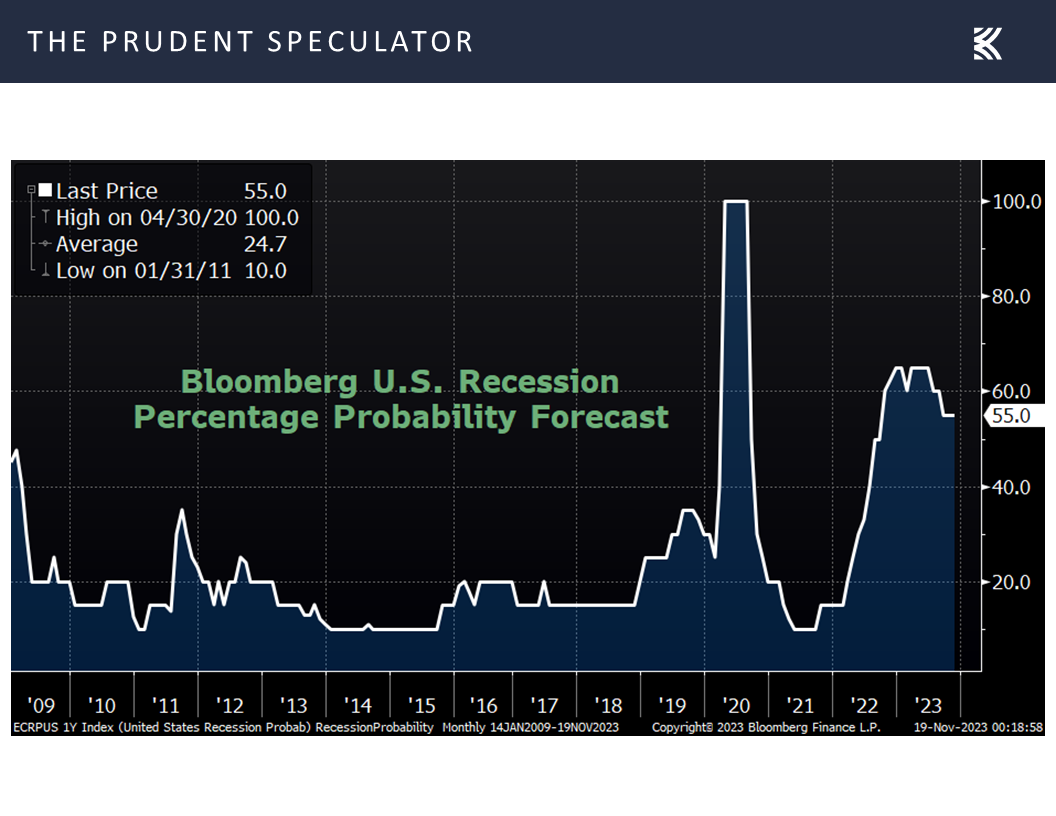

True, many are still of the mind that a recession will hit in the next 12 months,

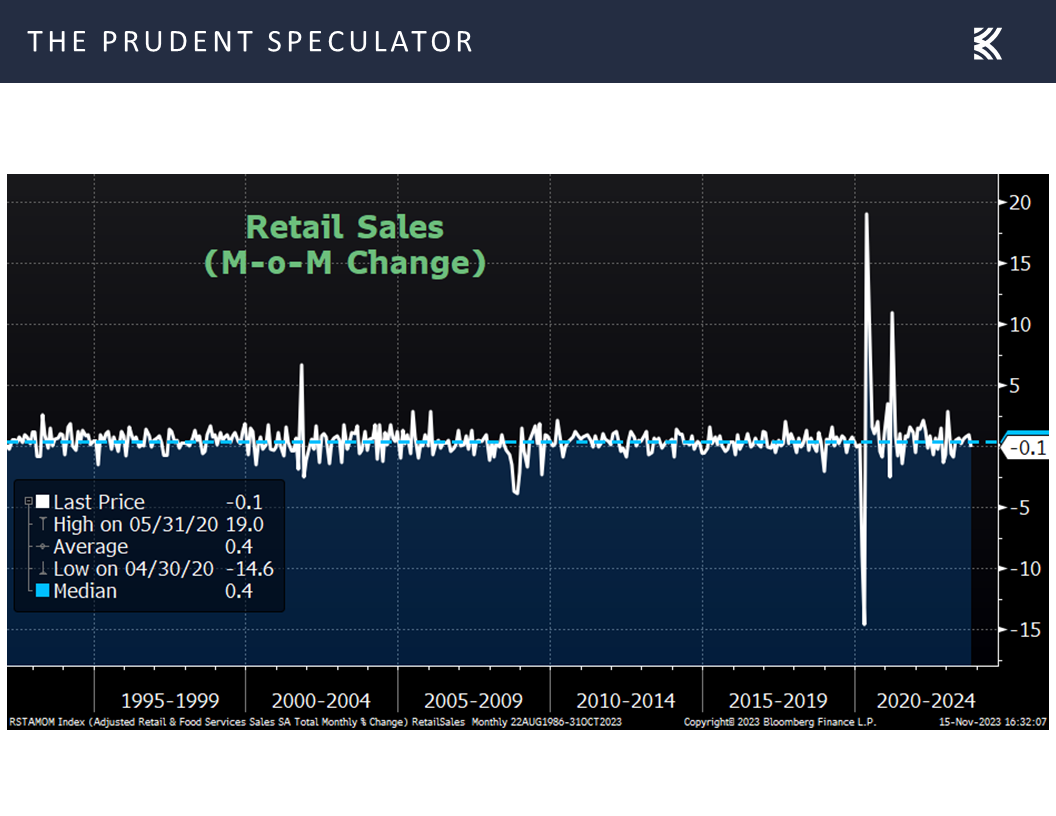

but retail sales have remained healthy, beating projections of a 0.2% dip in October with a 0.1% decrease,

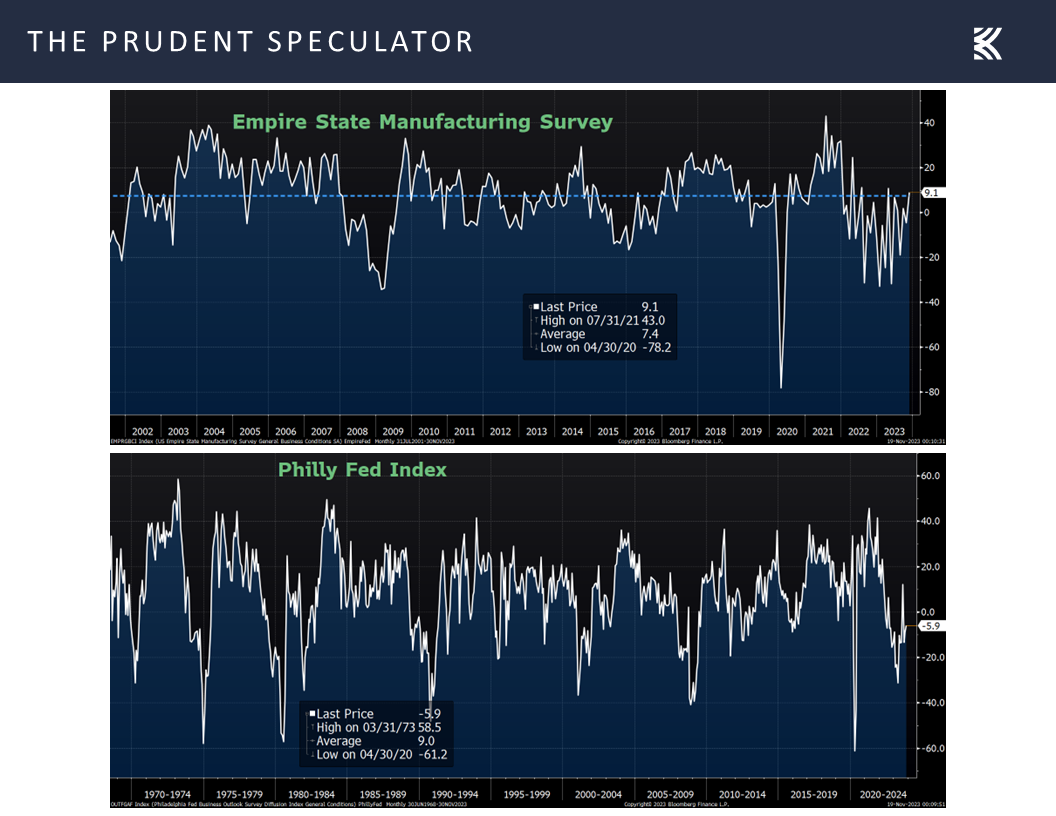

and the latest reads (Empire State and Philly Fed) on the outlook for the East Coast factory sector topped estimates.

Yes, businesses on Main Street are not exactly brimming with confidence,

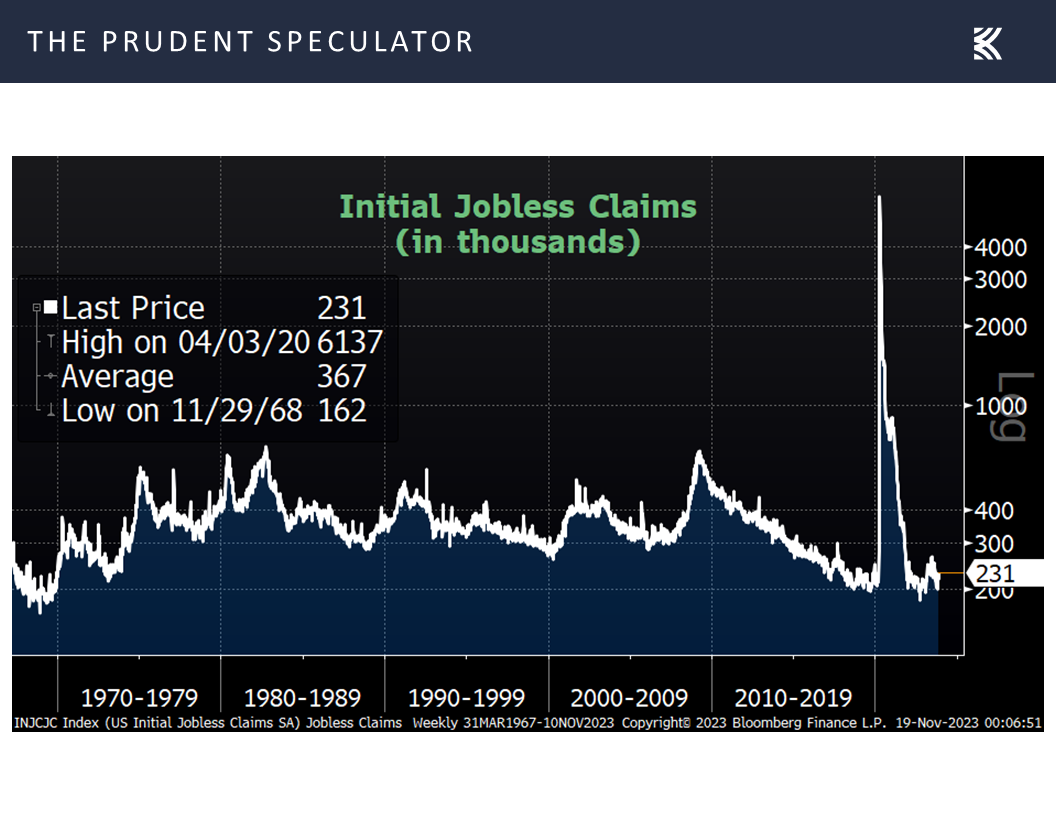

first time filings for unemployment benefits rose in the latest week,

first time filings for unemployment benefits rose in the latest week,

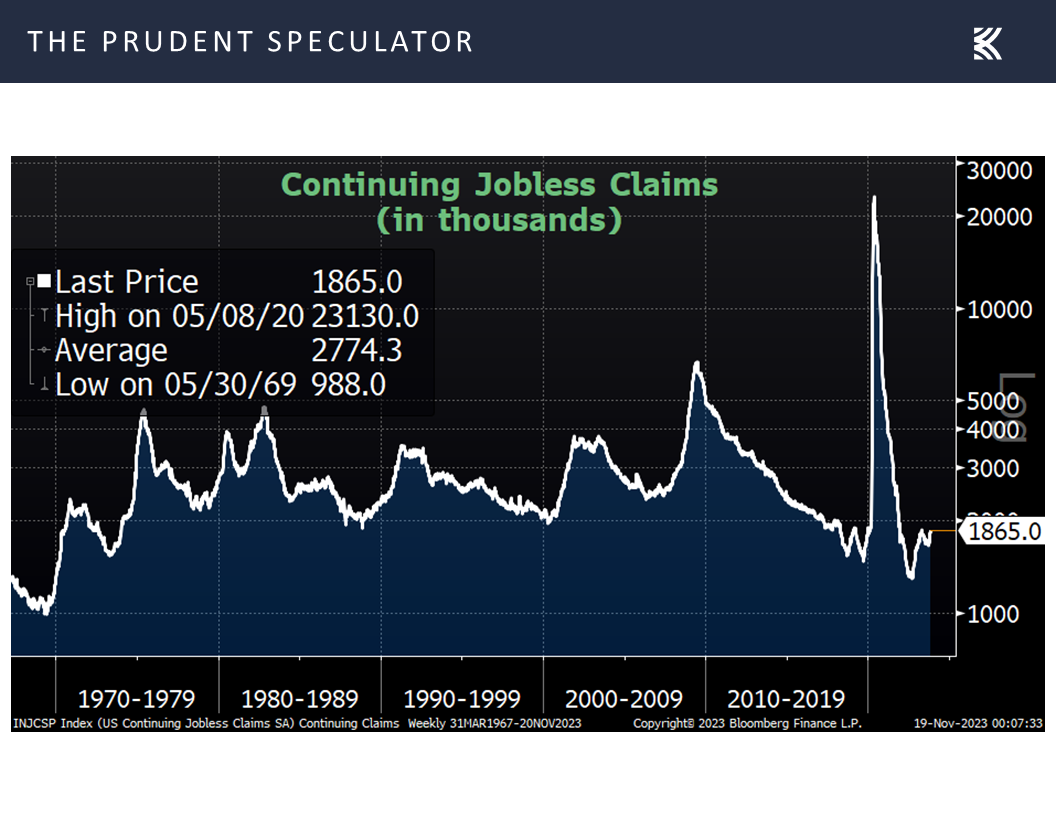

and continuing claims for jobless assistance have been on the rise,

but the outlook for Q4 inflation-adjusted economic growth remains solid,

and talk has increased about a so-called soft-landing for the economy.

Reasons for Optimism – Earnings Growth, Valuations & Calendar

Certainly, it is far too early for the Fed to declare, “Mission Accomplished,” on the inflation front, so we know that there will be more tough talk from Jerome H. Powell & Co. in the weeks and months ahead. Still, it would seem that even if the economy is eventually pushed into a (real) recession, the contraction would be mild, with corporate profits (reported in nominal dollars) likely to continue to grow,

which would only add to the appeal of our broadly diversified portfolios of what we believe to be inexpensively priced and generously yielding stocks.

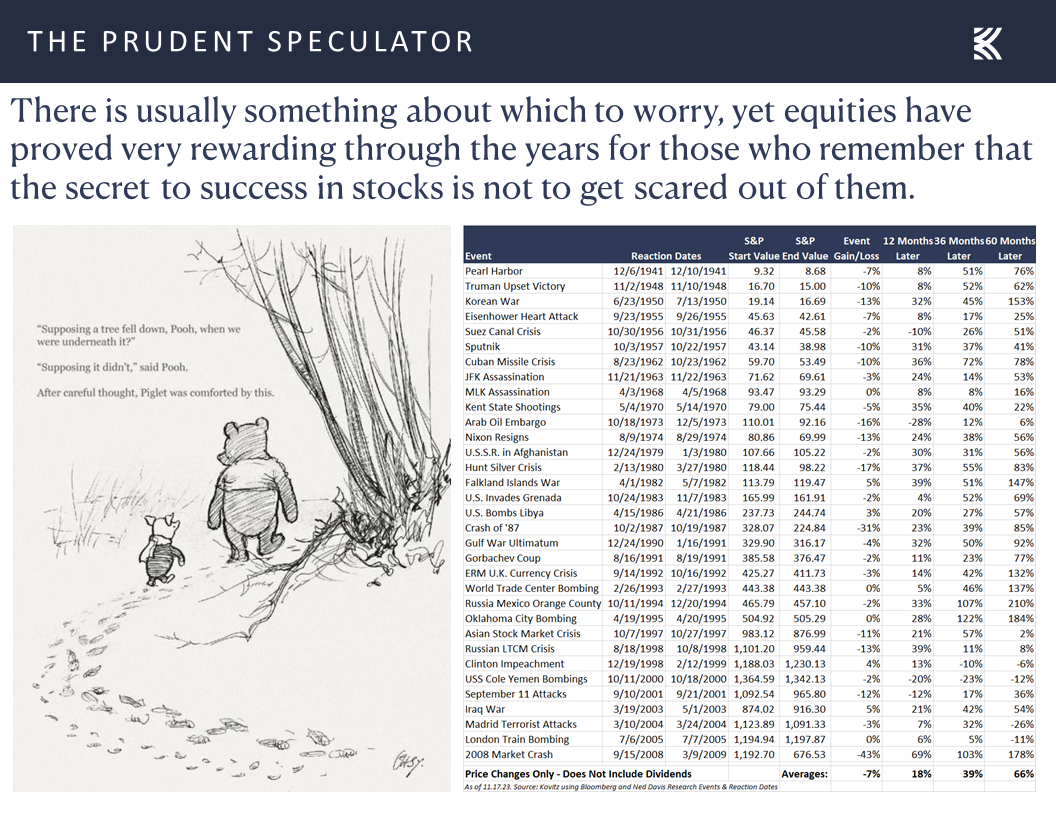

The headlines are disconcerting these days, but such is often the case, yet stocks have overcome plenty of adversity through the years,

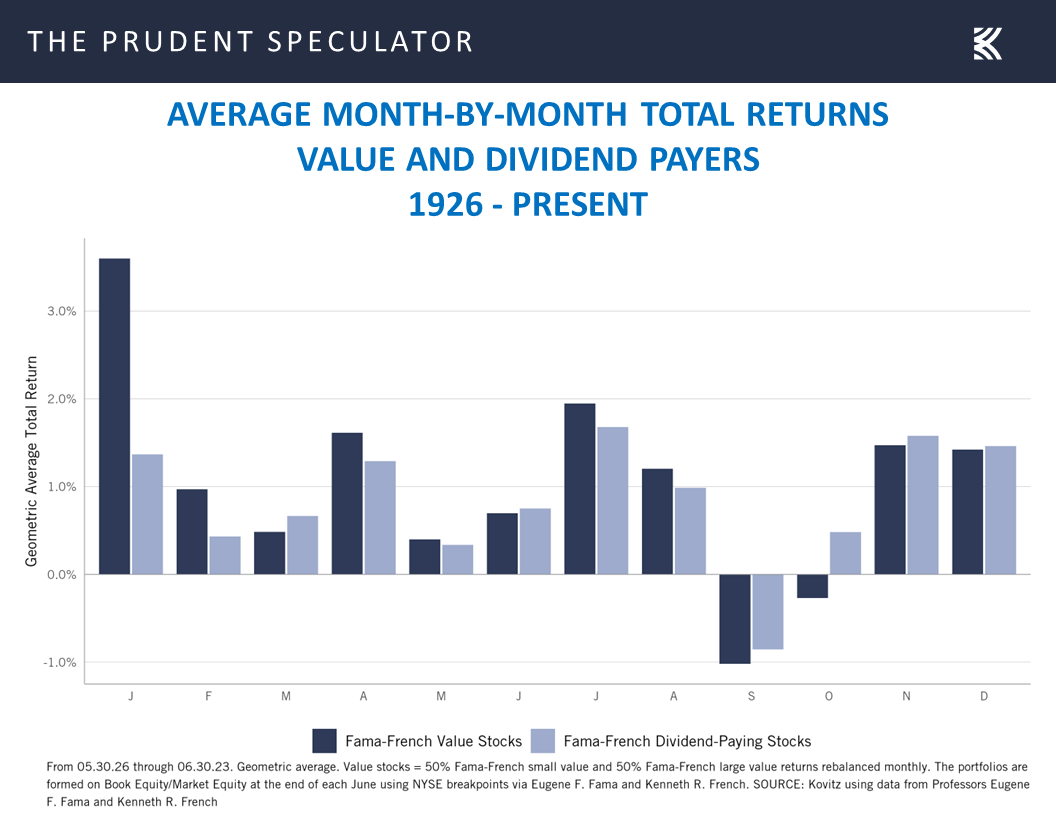

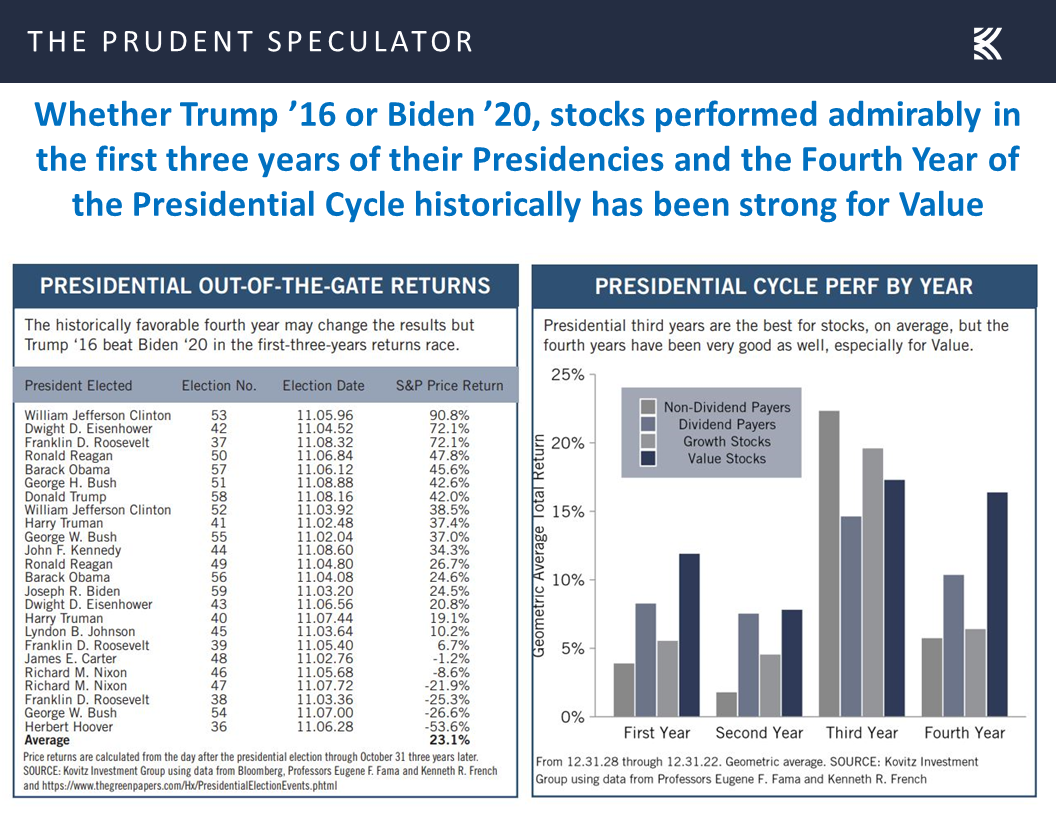

while we like that the current place in the calendar historically has been a tailwind for the kind of equities that we have long championed.

Stock News – Updates on six stocks across six different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Inflation, Interest Rates, Econ Data, Reasons for Optimism and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss inflation, interest rates, econ data, reasons for optimism and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 5 Sales Across 4 Accounts

Week in Review – Big Advance for Stocks; Value Leads the Way

Inflation – CPI & PPI Lower-than Expected

Interest Rates – Yields Move Lower

Econ Data – Soft Landing Still Possible

Reasons for Optimism – Earnings Growth, Valuations & Calendar

Stock News – Updates on six stocks across six different sectors

Week in Review – Big Advance for Stocks; Value Leads the Way

The seasonally favorable November – April period for equities,

added to its strong start this time around, posting the second terrific week out of the past three. Happily, as with the first week in this span, but definitely not the second, the average stock fared much better than the major market averages and Value showed that it can win a very-short-term returns race in addition to the long-term performance derby.

Though some would argue that the Biden-Xi summit talks in the Bay Area were a positive, it was not as if there was much in the way of positive developments on the geopolitical stage, either from the Middle East,

or Ukraine,

but the catalyst for the equity rally, aside from the fact that most stocks are inexpensively valued,

Inflation – CPI & PPI Lower-than Expected

was news that consumer price inflation in October slowed to 3.2%, a slightly lower rate than expected,

and the core rate (excludes volatile food and energy prices) rose 4.0%, less than forecasts and the lowest year-over-year increase in more than two years.

Throw in a big drop in rate of inflation at the producer level,

Interest Rates – Yields Move Lower

and the probabilities, per the futures market, of easier monetary policy with cuts in the Fed Funds rate increased last week, as the year-end 2024 projection for the benchmark lending rate now stands at 4.41%, down from 4.62% the week prior,

while there was a sizable advance in bond prices, dropping the yield on the 10-Year U.S. Treasury from 4.65% to 4.44%.

Econ Data – Soft Landing Still Possible

Although history suggests that equities more often than not have been a terrific hedge against inflation,

and stocks soared in price in the early 1980s during the last Federal Reserve battle with inflation rates as high as what has been witnessed this cycle,

it certainly helps that the economy has held up remarkably well with real (inflation-adjusted) GDP growth coming in at an impressive 4.9% in Q3.

True, many are still of the mind that a recession will hit in the next 12 months,

but retail sales have remained healthy, beating projections of a 0.2% dip in October with a 0.1% decrease,

and the latest reads (Empire State and Philly Fed) on the outlook for the East Coast factory sector topped estimates.

Yes, businesses on Main Street are not exactly brimming with confidence,

and continuing claims for jobless assistance have been on the rise,

but the outlook for Q4 inflation-adjusted economic growth remains solid,

and talk has increased about a so-called soft-landing for the economy.

Reasons for Optimism – Earnings Growth, Valuations & Calendar

Certainly, it is far too early for the Fed to declare, “Mission Accomplished,” on the inflation front, so we know that there will be more tough talk from Jerome H. Powell & Co. in the weeks and months ahead. Still, it would seem that even if the economy is eventually pushed into a (real) recession, the contraction would be mild, with corporate profits (reported in nominal dollars) likely to continue to grow,

which would only add to the appeal of our broadly diversified portfolios of what we believe to be inexpensively priced and generously yielding stocks.

The headlines are disconcerting these days, but such is often the case, yet stocks have overcome plenty of adversity through the years,

while we like that the current place in the calendar historically has been a tailwind for the kind of equities that we have long championed.

Stock News – Updates on six stocks across six different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.