The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the inflation, interest rates, valuations and more news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – Partial Sale of CAT

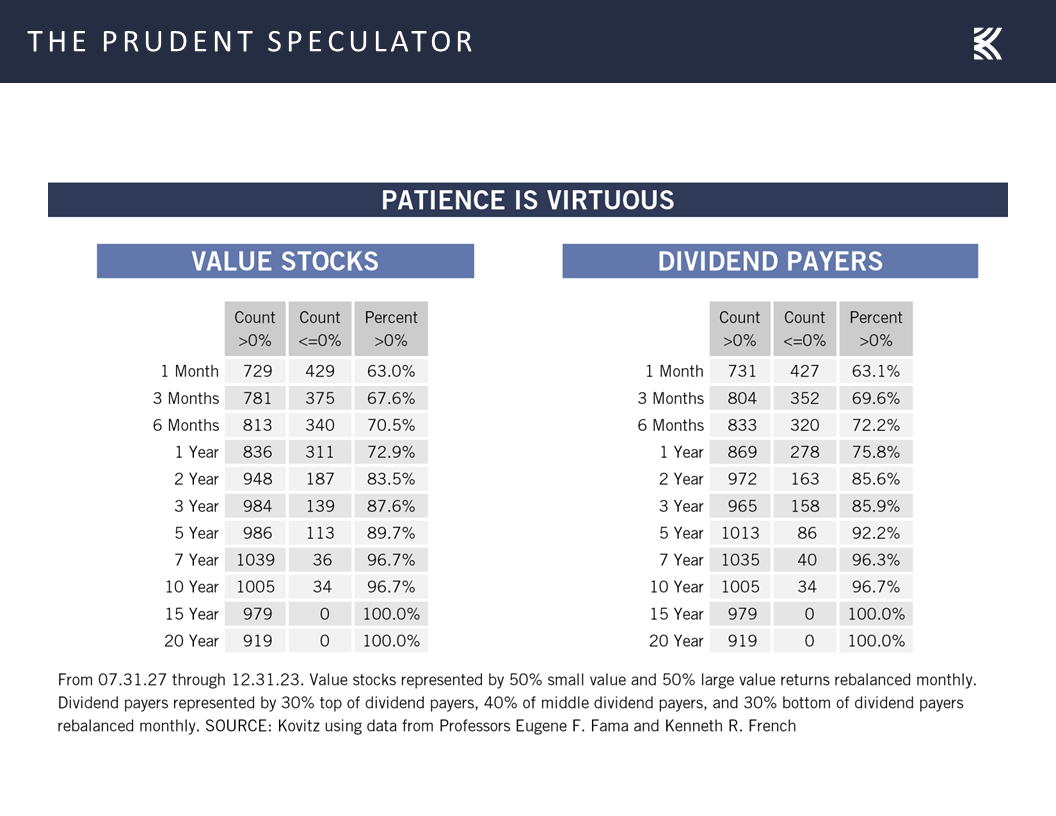

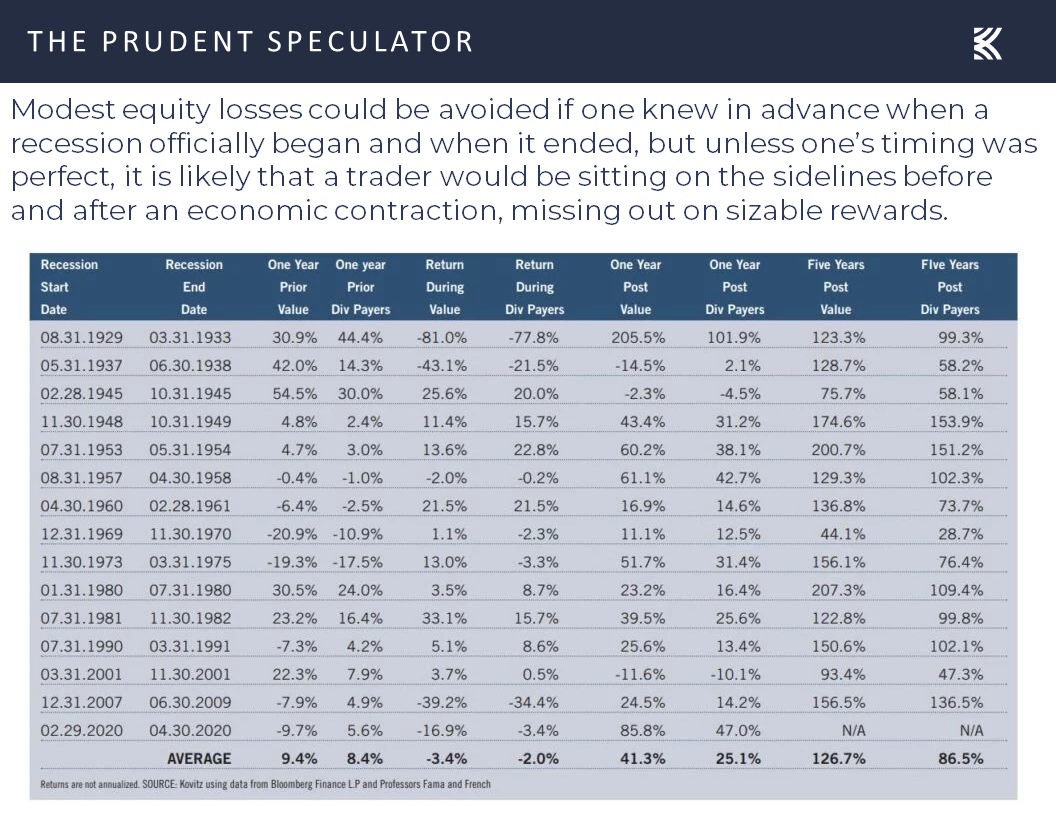

Volatility – The Longer the Hold, the Less the Chance of Loss

Inflation – CPI & PPI Rise; Stocks Haven’t Minded Historically

Interest Rates – Target Rate for Fed Funds & 10-Year Treasury Yield Rise; Stocks are OK

Economy – Mixed Numbers; GDP & Corporate Profits Still Likely to Show Solid Growth

Valuations – Value Stocks Attractively Priced

Sentiment – AAII Still Optimistic

Stock News – Updates on eight stocks across five different sectors

Volatility – The Longer the Hold, the Less the Chance of Loss

Nearly a century of market history illustrates that simply lengthening the measuring stick reduces the odds of loss,

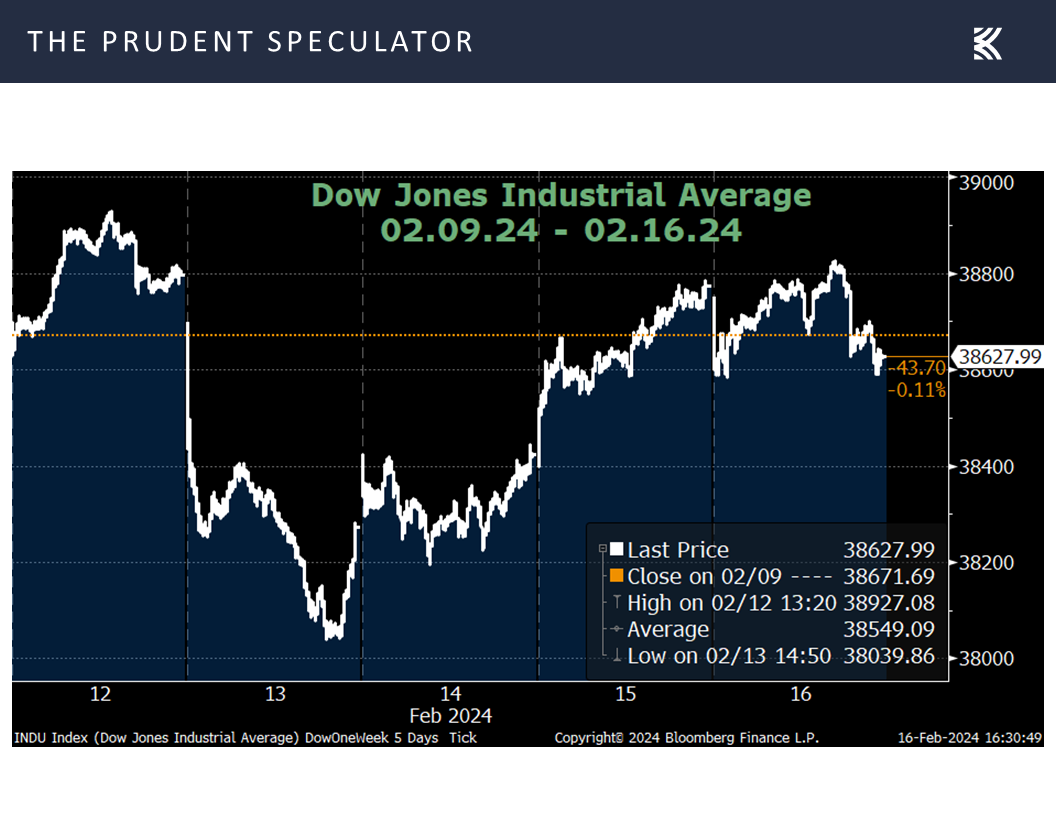

and last week demonstrated that markets can be placid with little in the way of volatility when evaluated on a one-week basis. Indeed, the Dow Jones Industrial Average closed the 5 trading days near where it began,

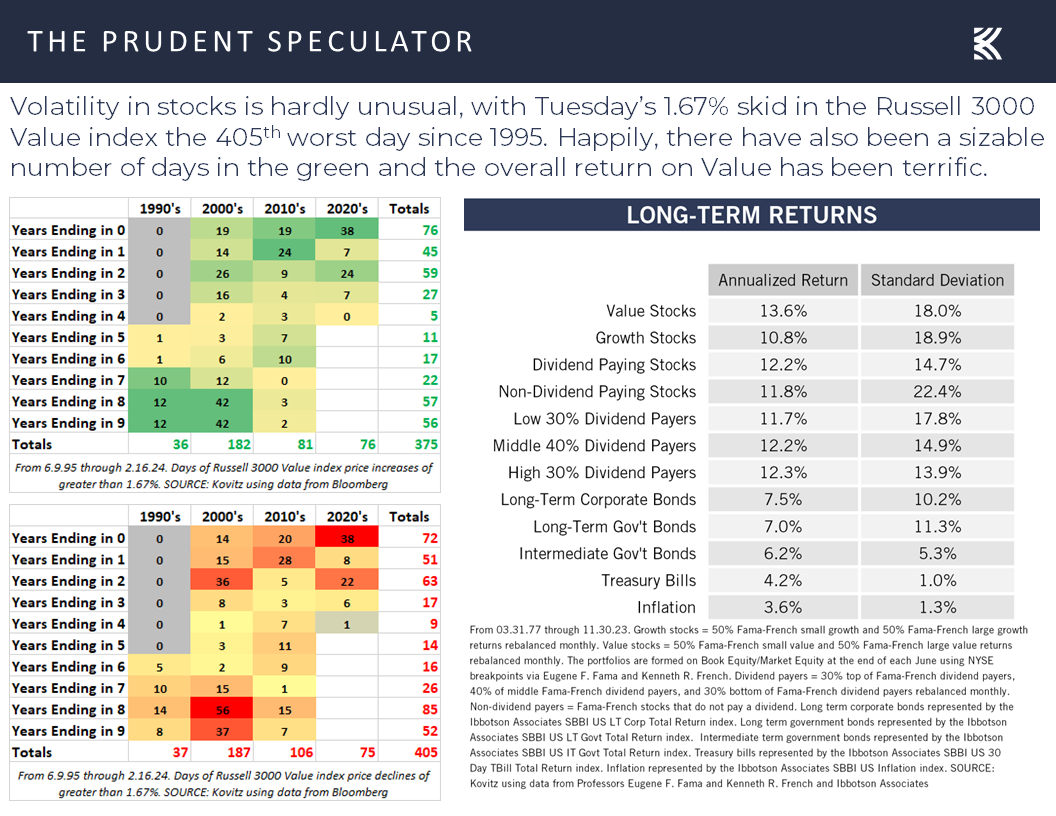

although there was a nasty one-day plunge on Tuesday that was one of the 400 or so worst since the launch of the Russell 3000 Value index in 1995.

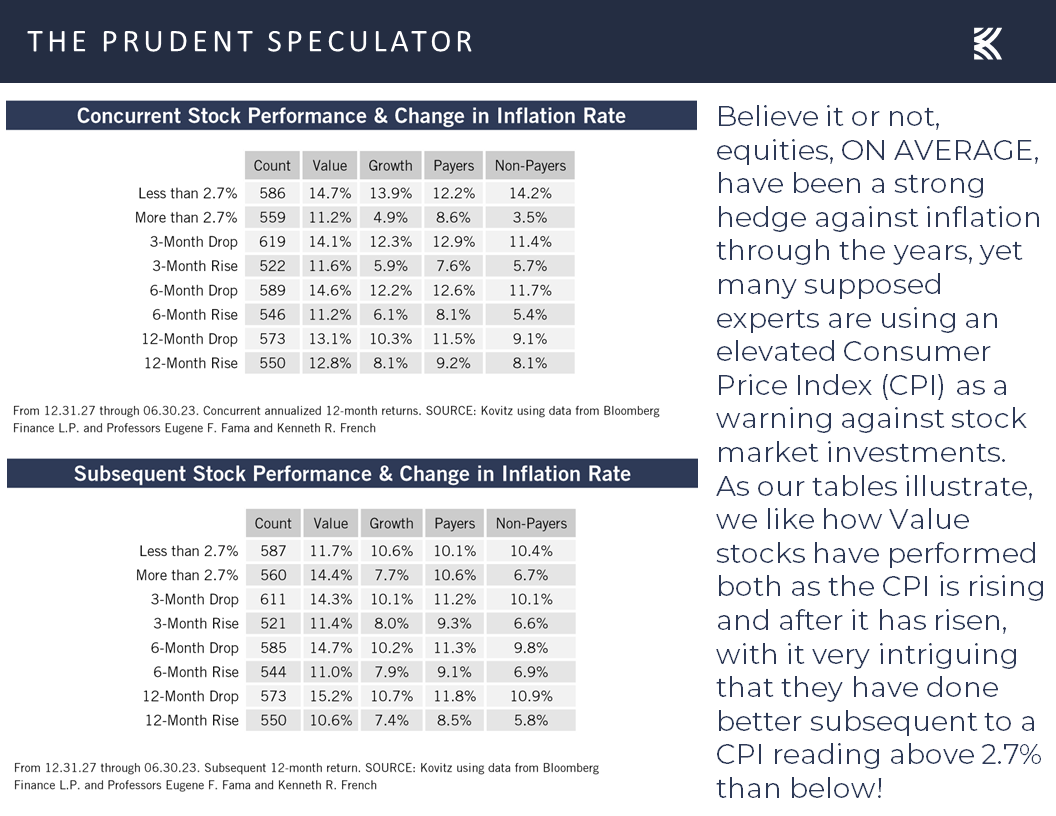

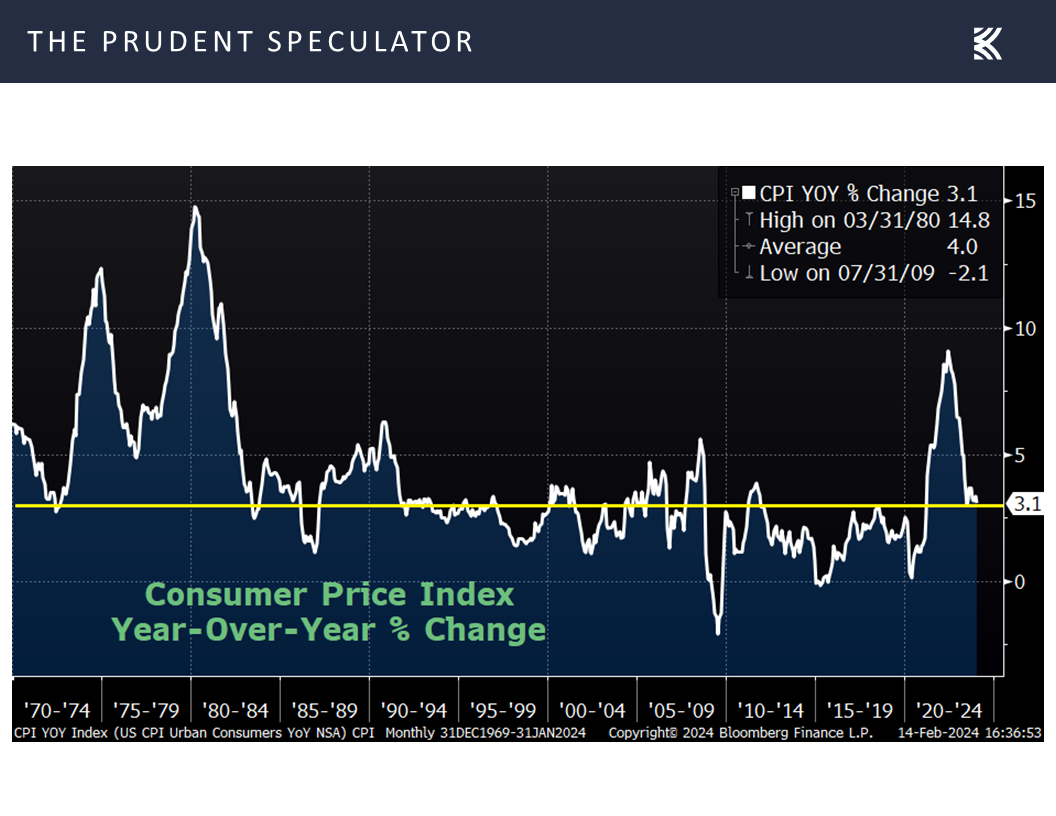

Inflation – CPI & PPI Rise; Stocks Haven’t Minded Historically

Interestingly, despite plenty of evidence that that suggests stocks do not mind a Federal Reserve fight against inflation,

with Value performing fine, on average, whether the Consumer Price Index (CPI) is rising or falling,

traders suffered temporary indigestion when both the full CPI,

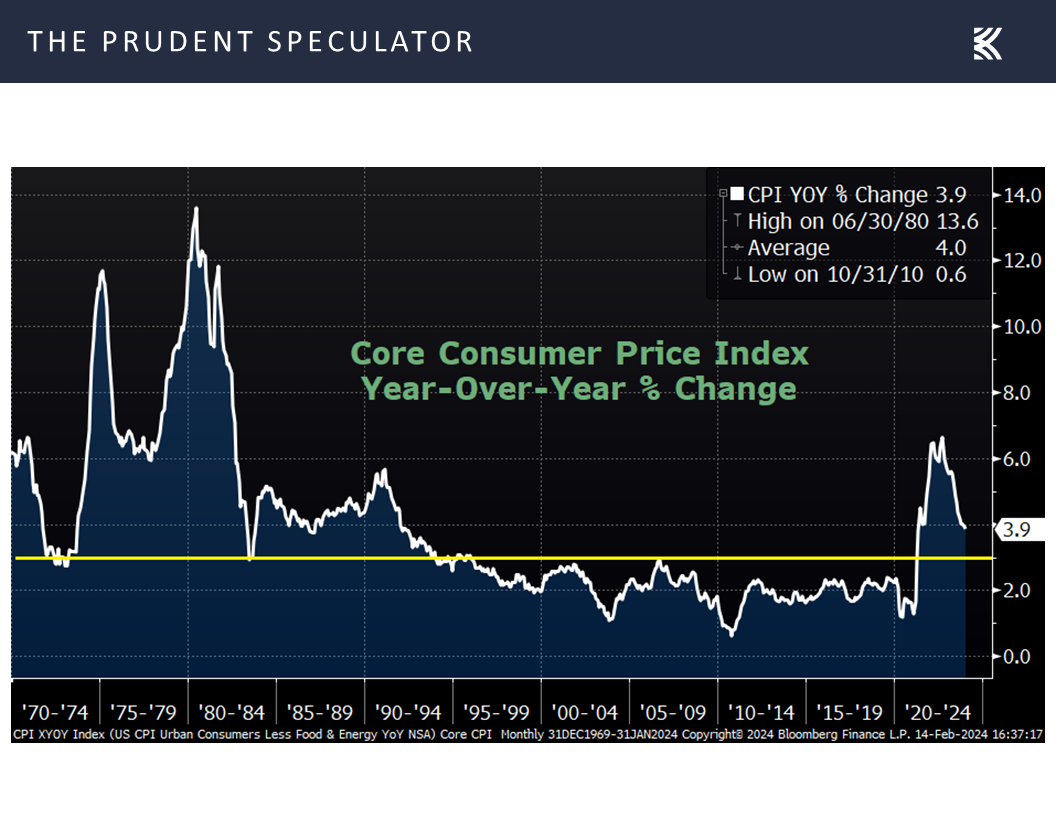

and the core rate (excludes volatile food and energy prices) came in above expectations in January.

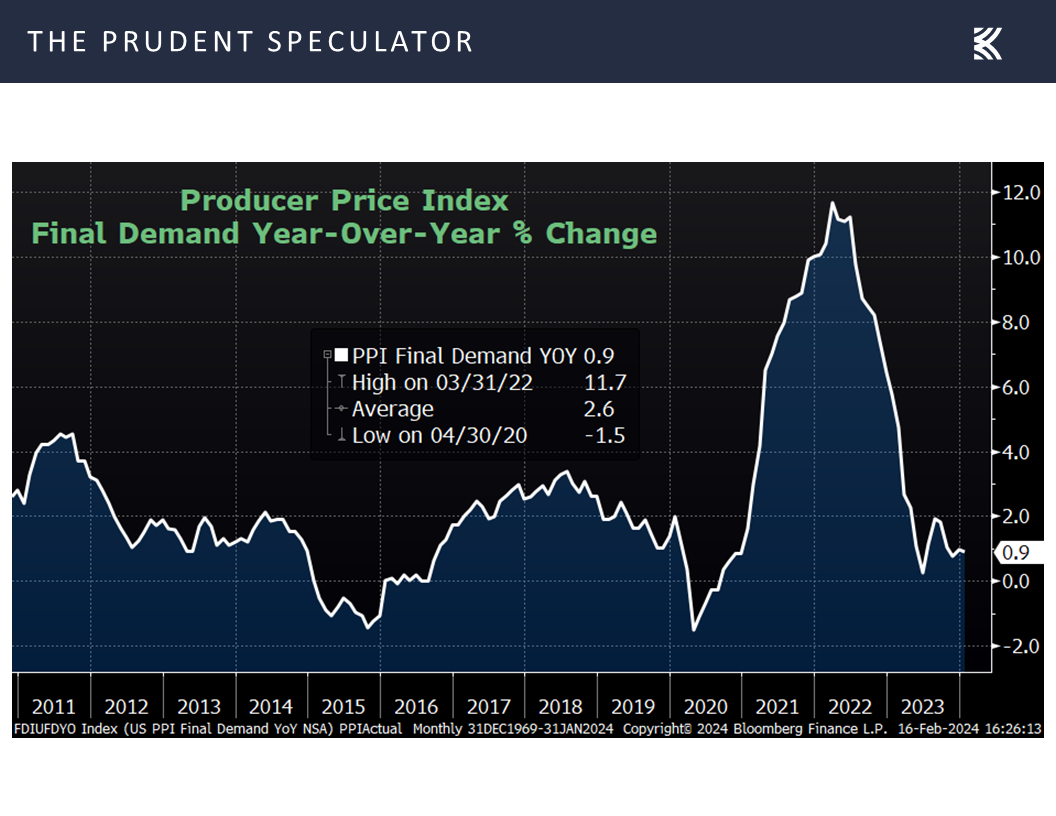

It was a similar story for inflation at the wholesale level as the Producer Price Index for January released on Friday also was hotter than estimated, even as the 0.9% year-over-year advance was well below the long-term average.

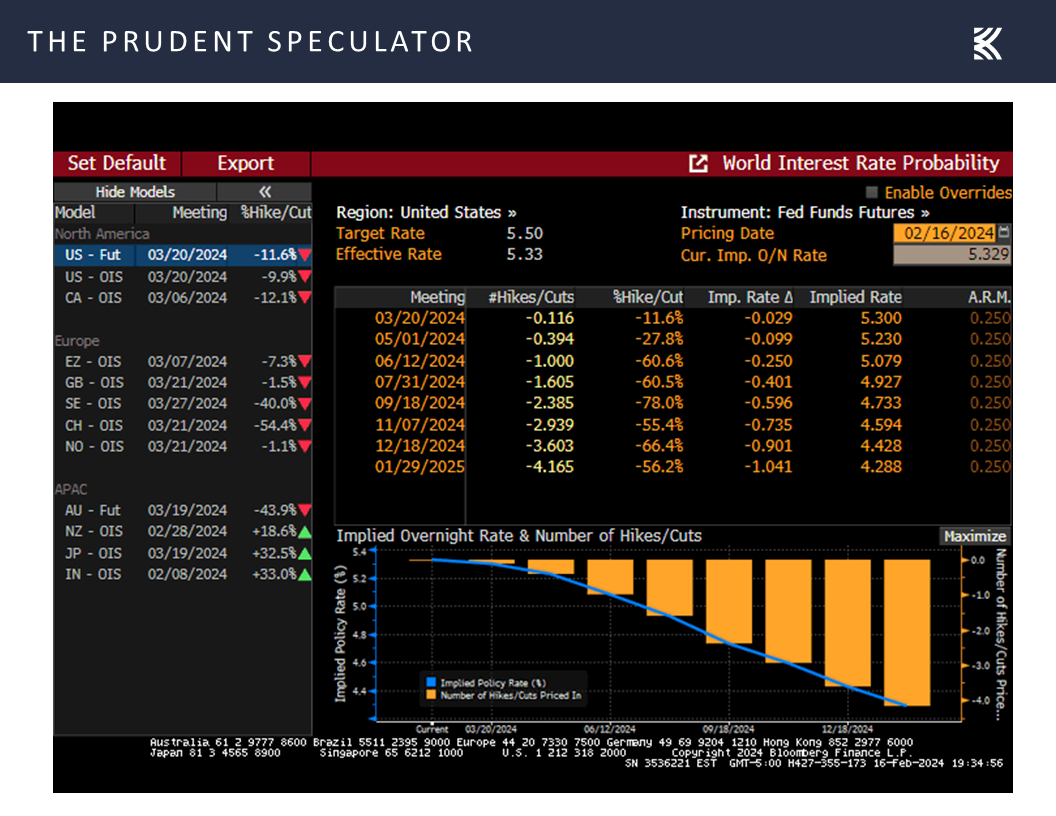

Interest Rates – Target Rate for Fed Funds & 10-Year Treasury Yield Rise; Stocks are OK

Still, bettors in the Fed Funds futures market decided that Jerome H. Powell & Co. would not likely begin to reduce the benchmark lending rate until the June FOMC Meeting versus May the week prior. Further, the odds now suggest that there is likely to be no more than 4 quarter-point rate cuts this year,

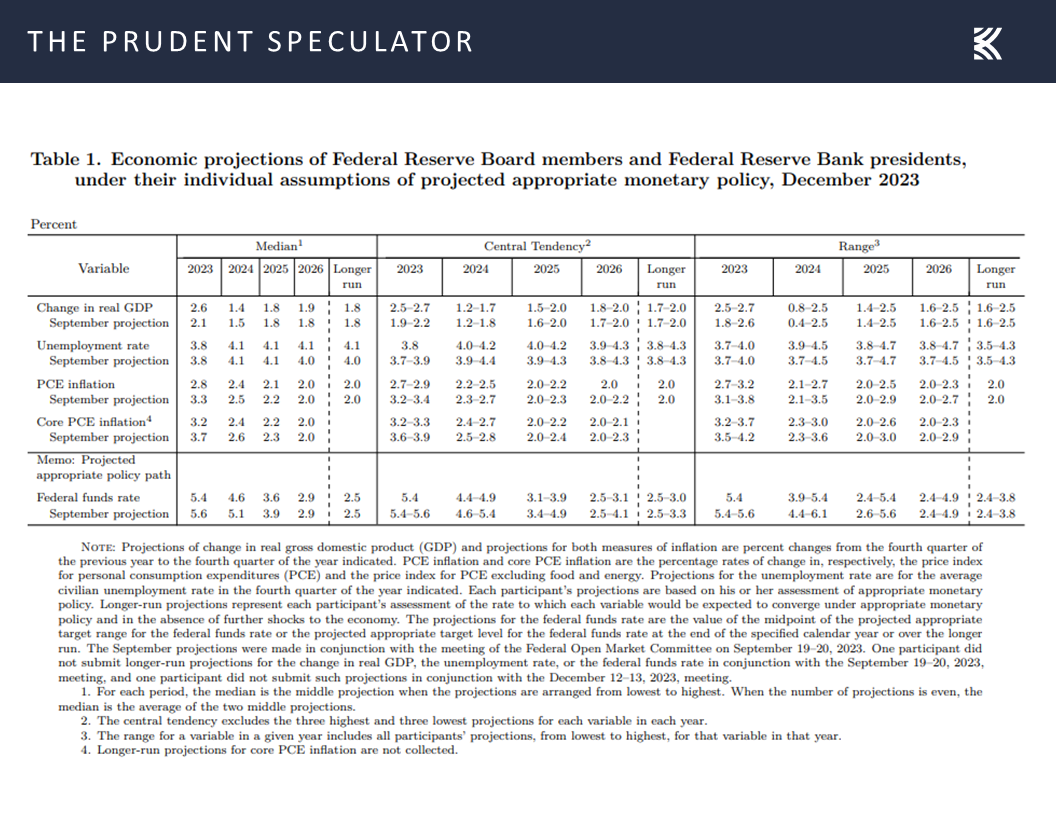

with the current guess of a 4.43% year-end Fed Funds rate now closer to the 4.6% projection the Federal Reserve Board members and Federal Reserve Bank Presidents offered back in December.

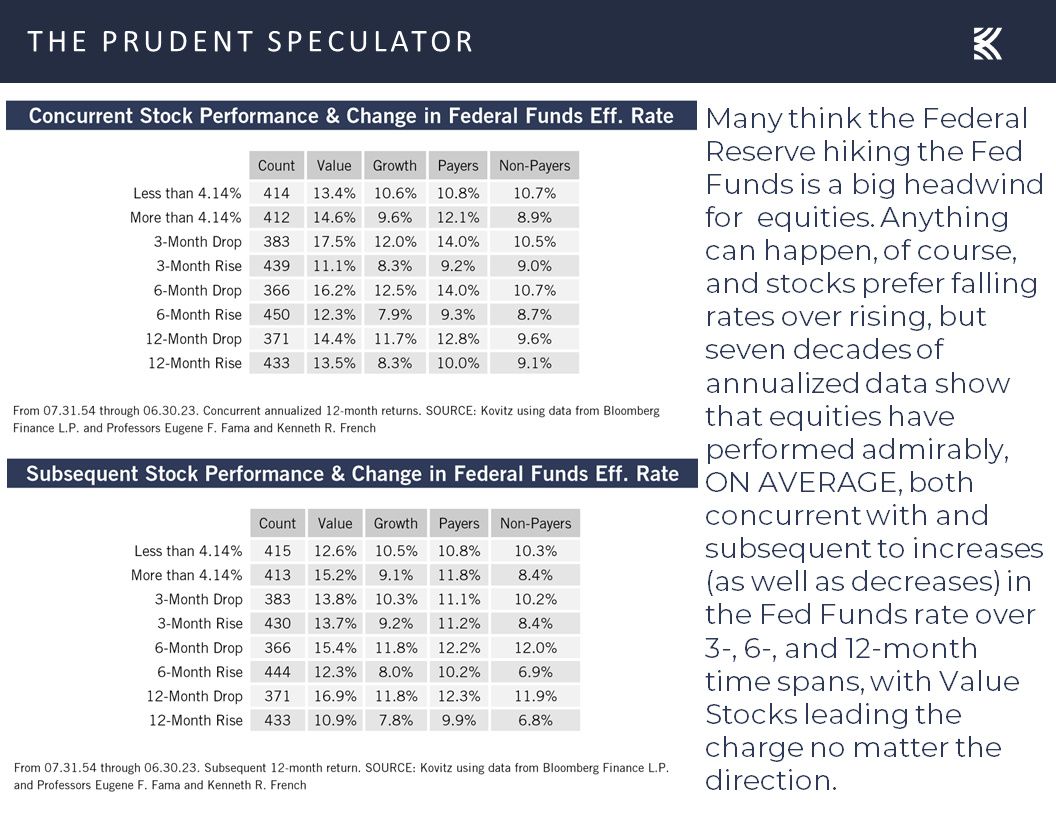

Of course, despite what supposed market gurus and talking heads on financial television might argue, history shows that stocks have performed fine, on average, whether the Fed Funds rate is moving higher or lower,

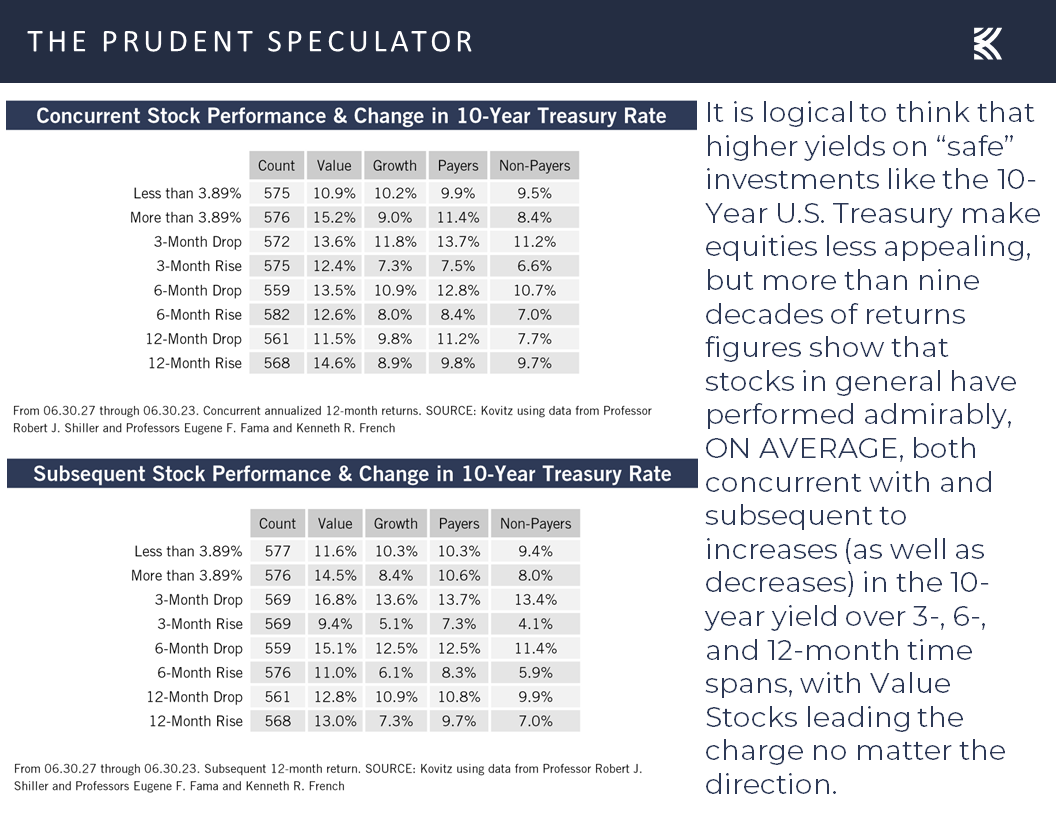

with the long-term evidence similar, on average, whether the benchmark government bond yield is rising or falling.

And for those who might question the 10-Year chart above, we submit additional overwhelming supporting evidence over the last three-and-a-half years,

though we realize that last week’s thinking that the Fed will be less accommodative prompted a jump in the yield on the 10-Year U.S. Treasury to 4.28%, up some 40 basis points from the 3.88% level at which the yield began 2024.

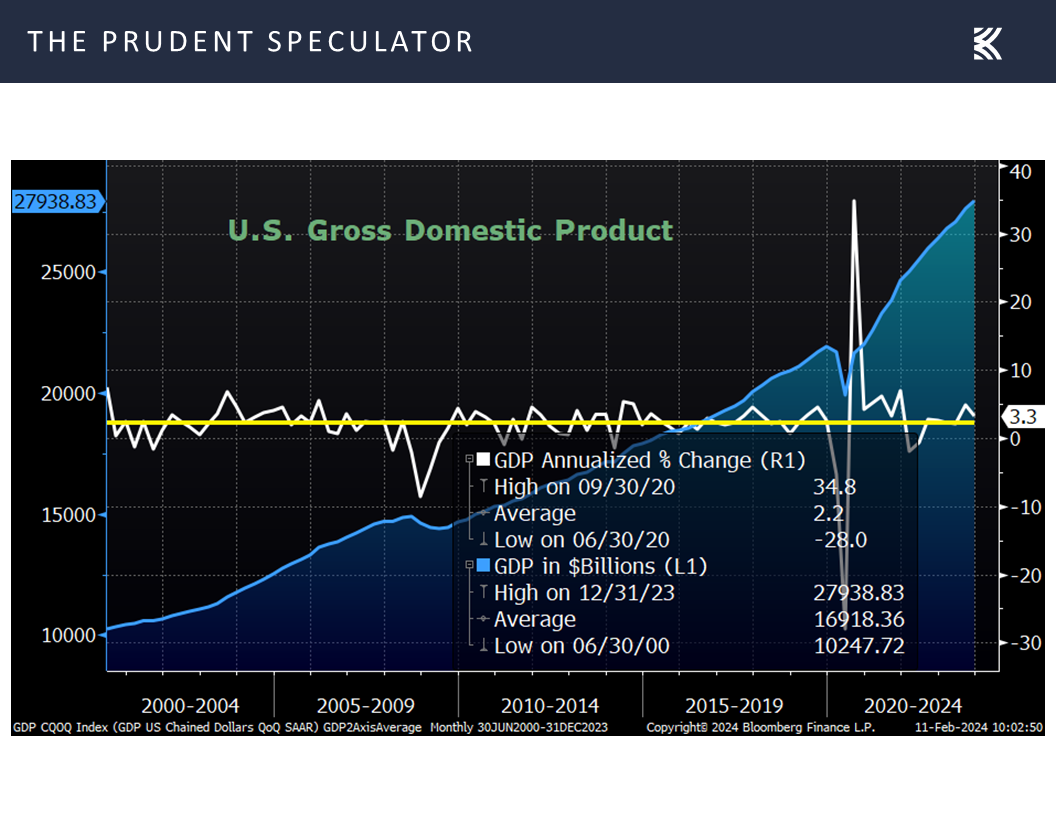

Economy – Mixed Numbers; GDP & Corporate Profits Still Likely to Show Solid Growth

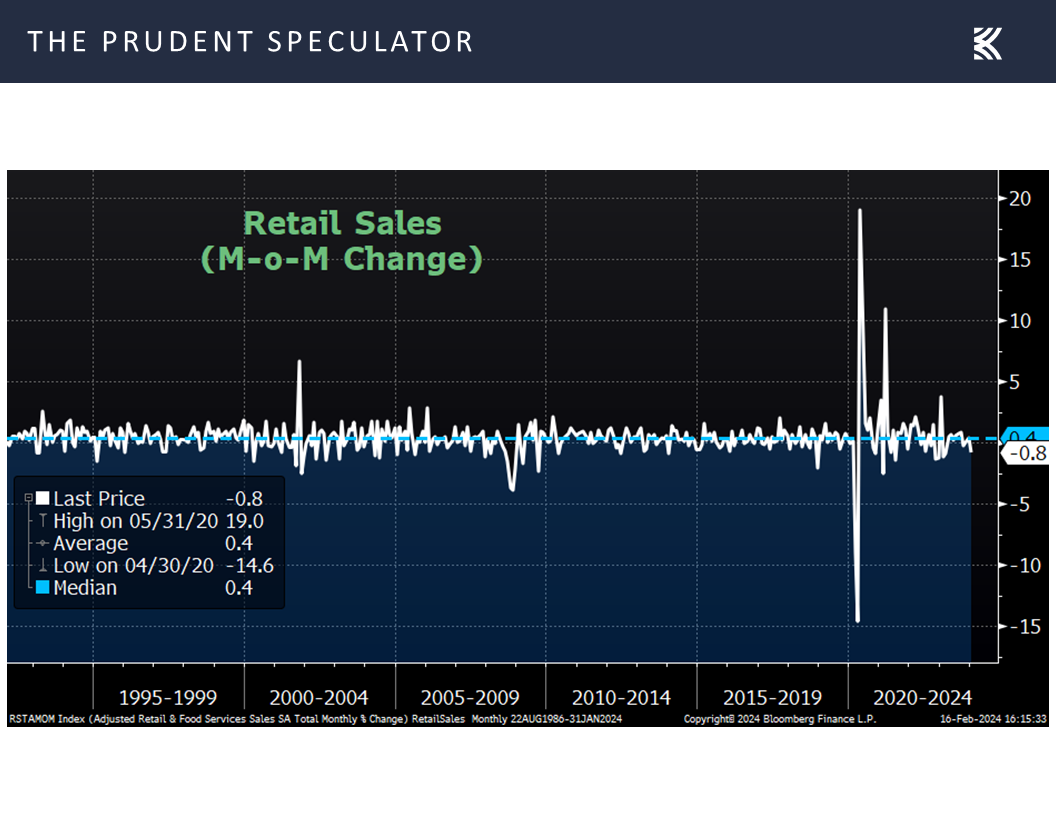

Obviously, interest rates are just one factor influencing stock price gyrations. More important is the health of the U.S. economy, with data mixed last week. While weather deserved some of the blame, retail sales retreated a worse-than-expected 0.8% last month,

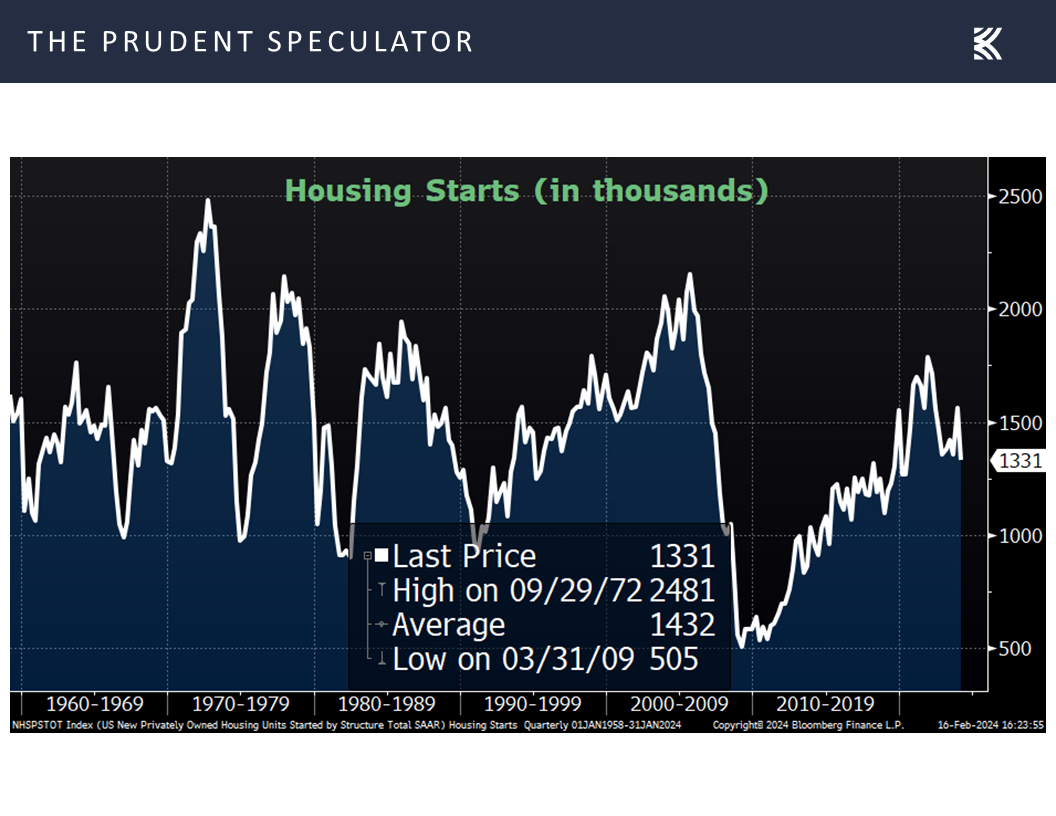

housing starts for January came in below estimates,

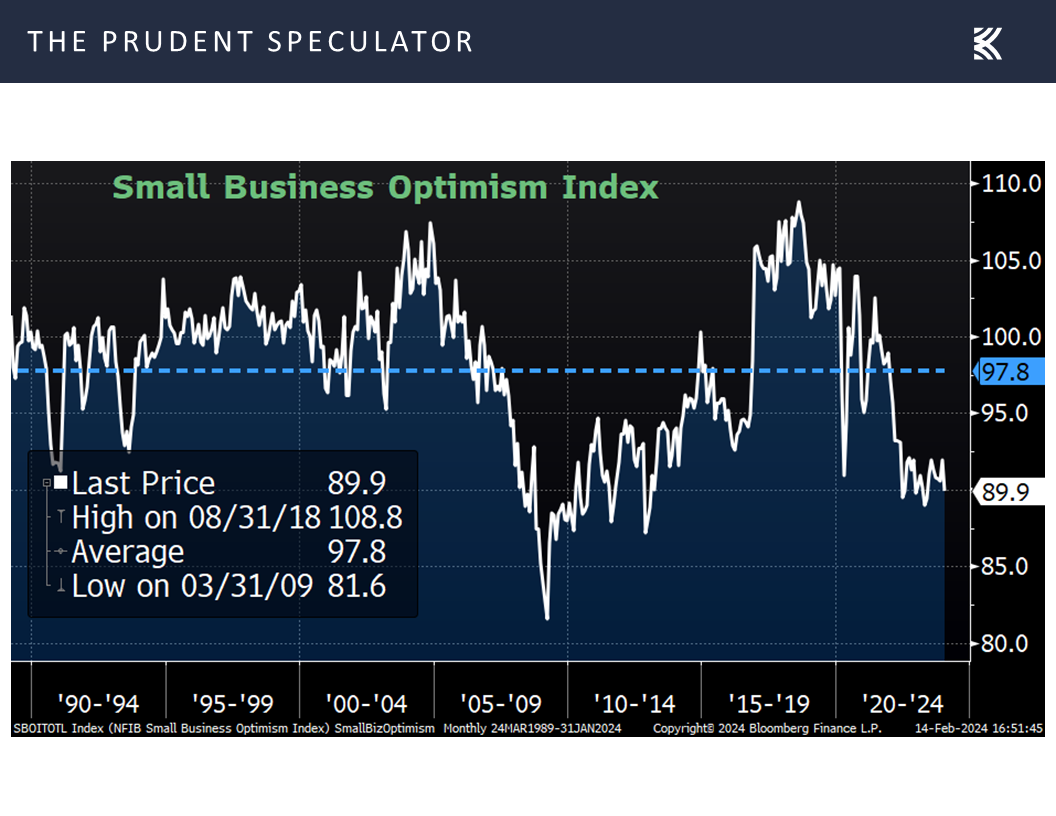

and Small Business Optimism pulled back.

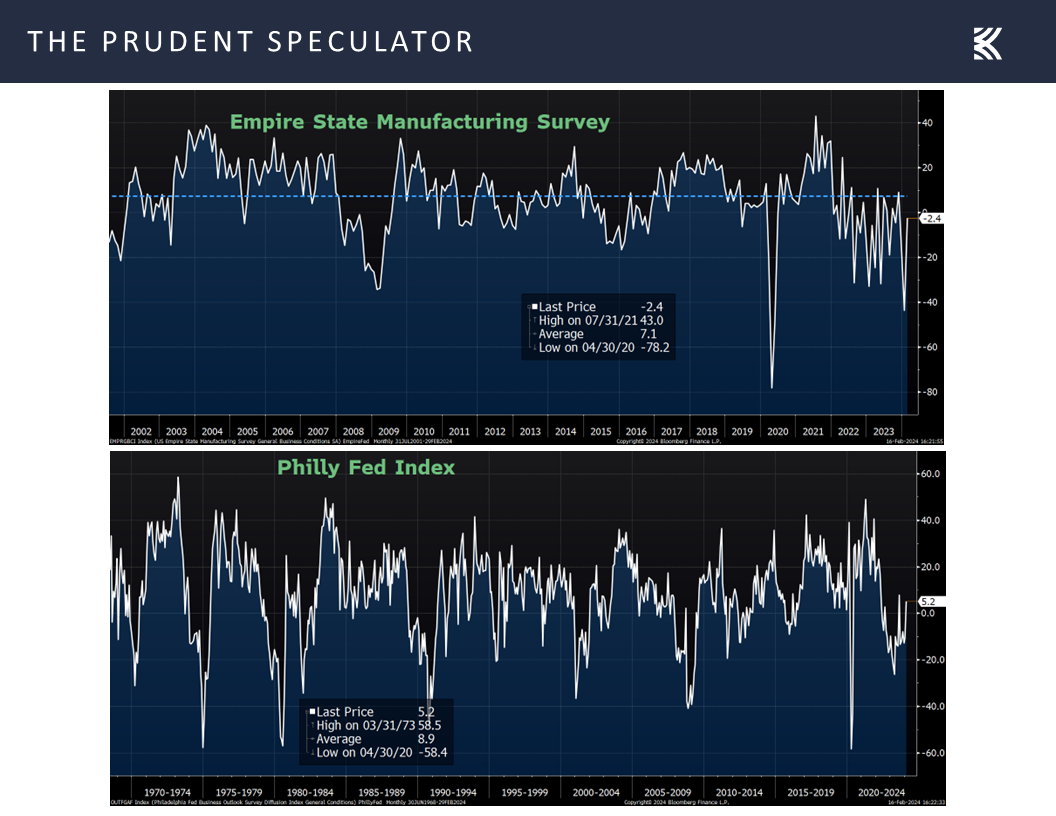

On the other hand, readings on the outlook for East Coast factory activity improved to better-than-estimated tallies for February,

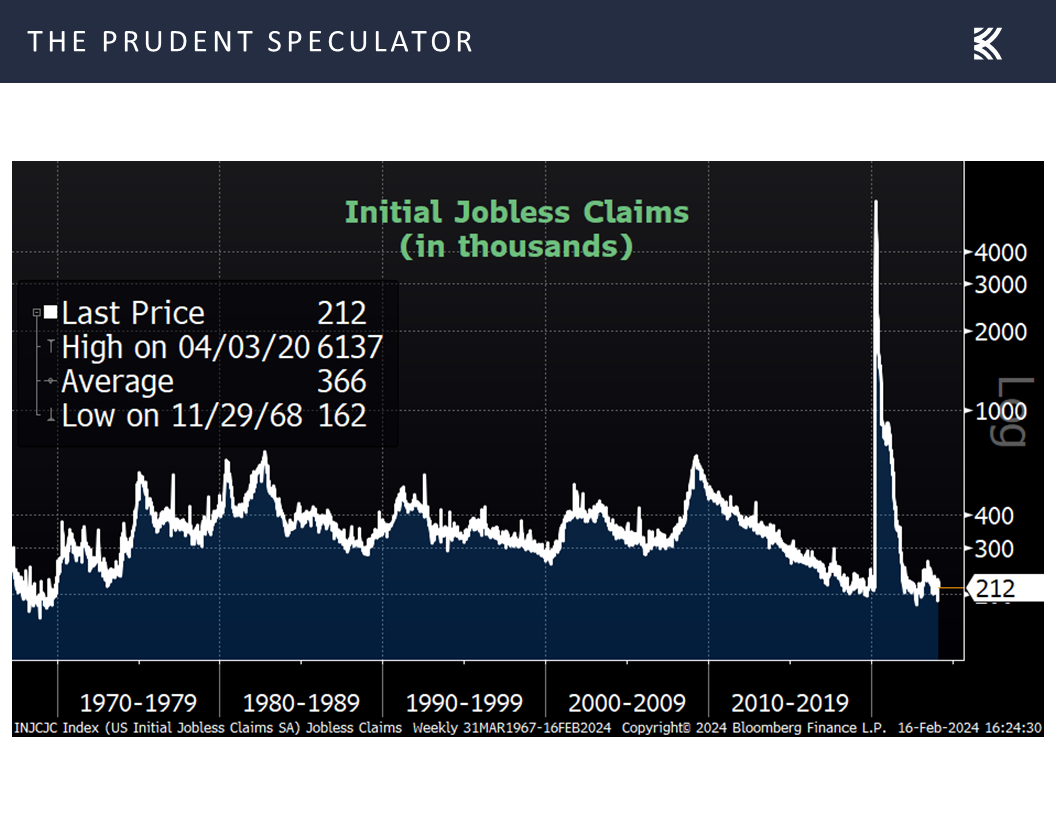

initial filings for unemployment benefits declined in the latest week,

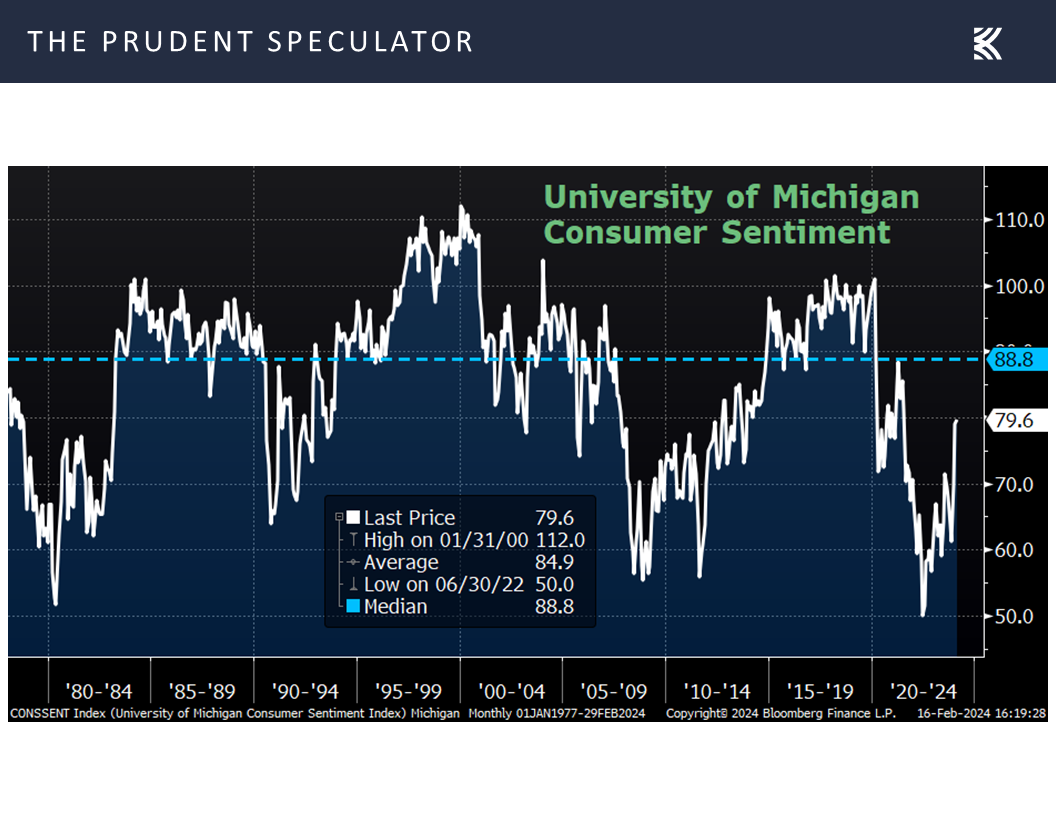

and optimism on Main Street increased this month.

Roll up all the data and the latest forecast from the Atlanta Fed for real (inflation-adjusted) Q1 GDP growth stood at a solid 2.9%,

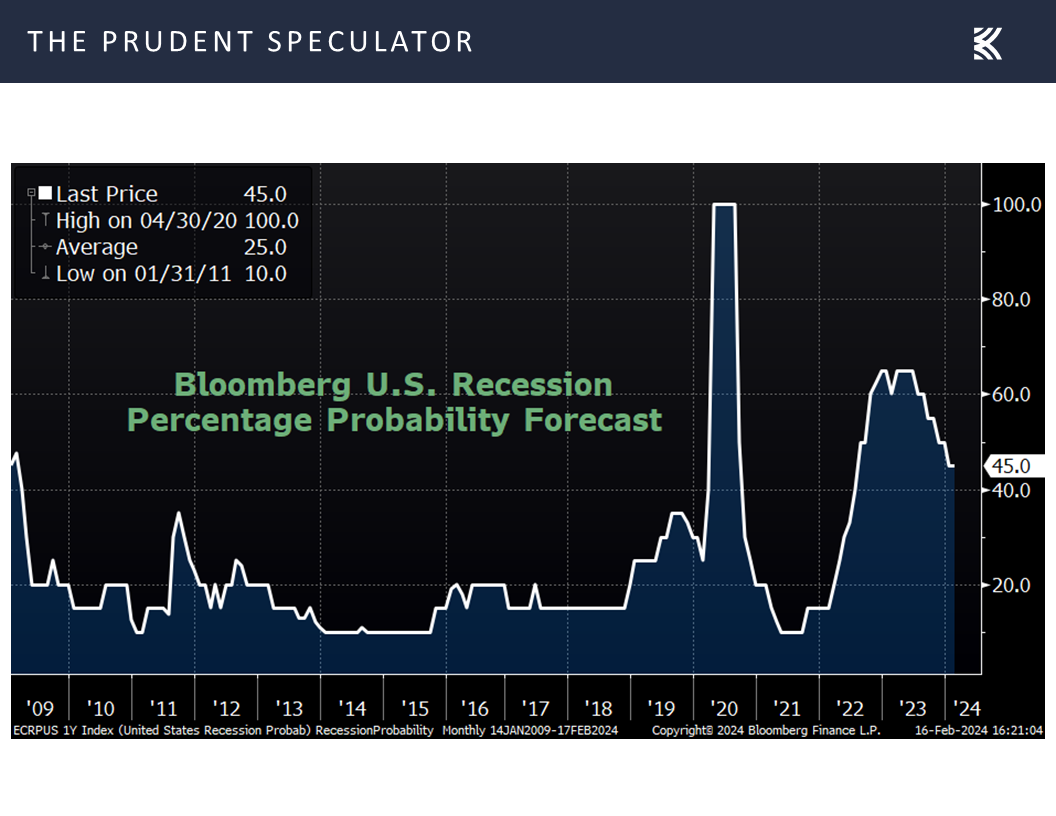

even as the tabulation by Bloomberg of the chance of recession in the next 12 months remained at 45%.

We do not lose sleep fretting about recession as their beginnings and endings are impossible to predict AND the gains on Value stocks coming out of them have been sensational, on average,

while the long-term trend is higher in terms of GDP,

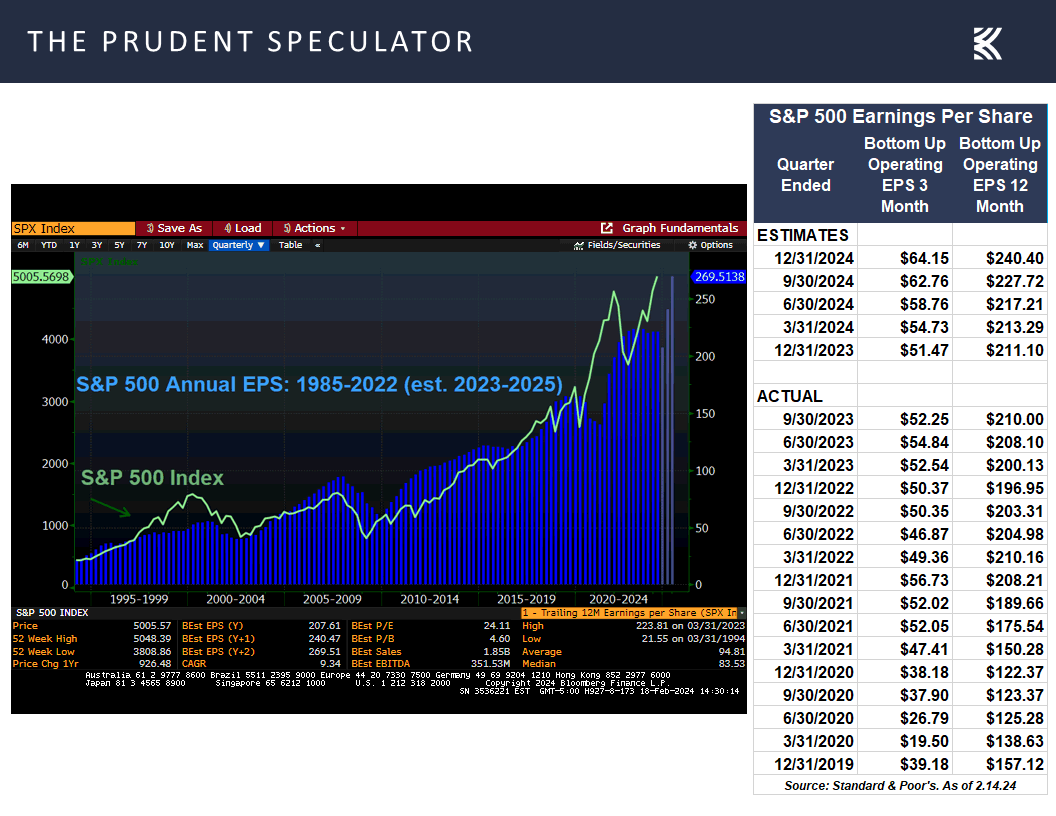

as has been the case for corporate profits, which were solid in Q4 and which are likely to continue to grow this year, just as they have throughout history.

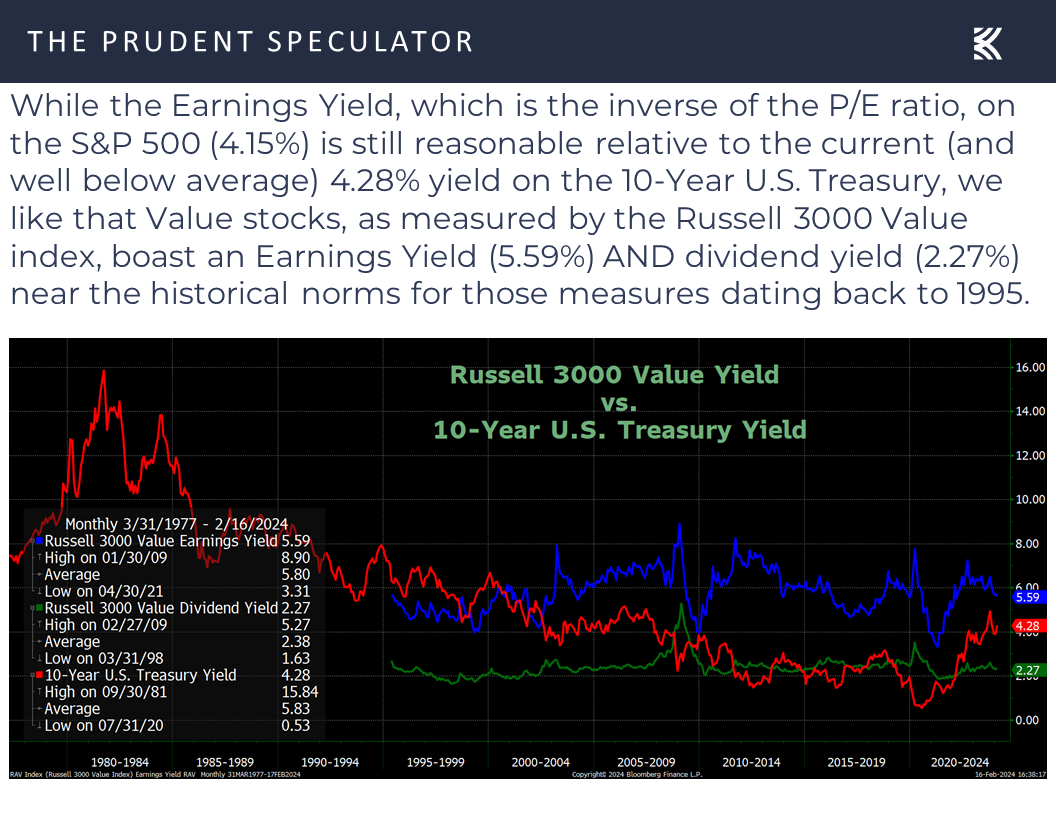

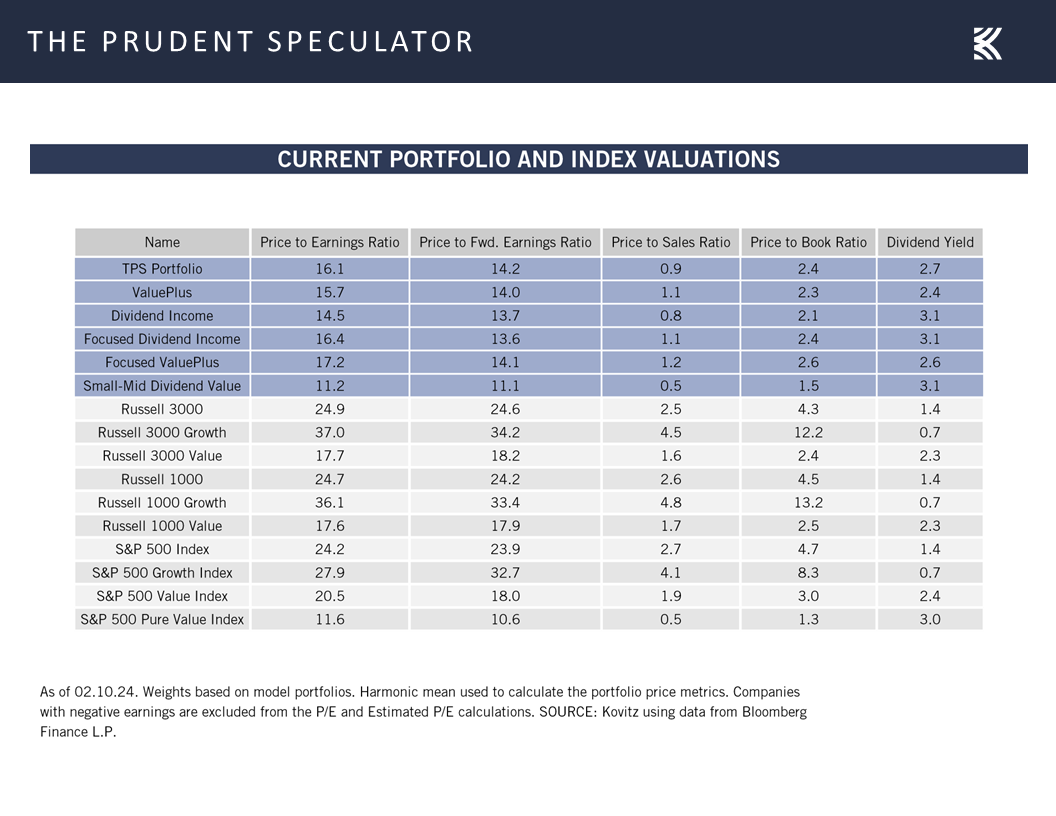

Valuations – Value Stocks Attractively Priced

So, with valuations remaining reasonable for Value stocks in general,

and our broadly diversified portfolios of undervalued stocks in particular,

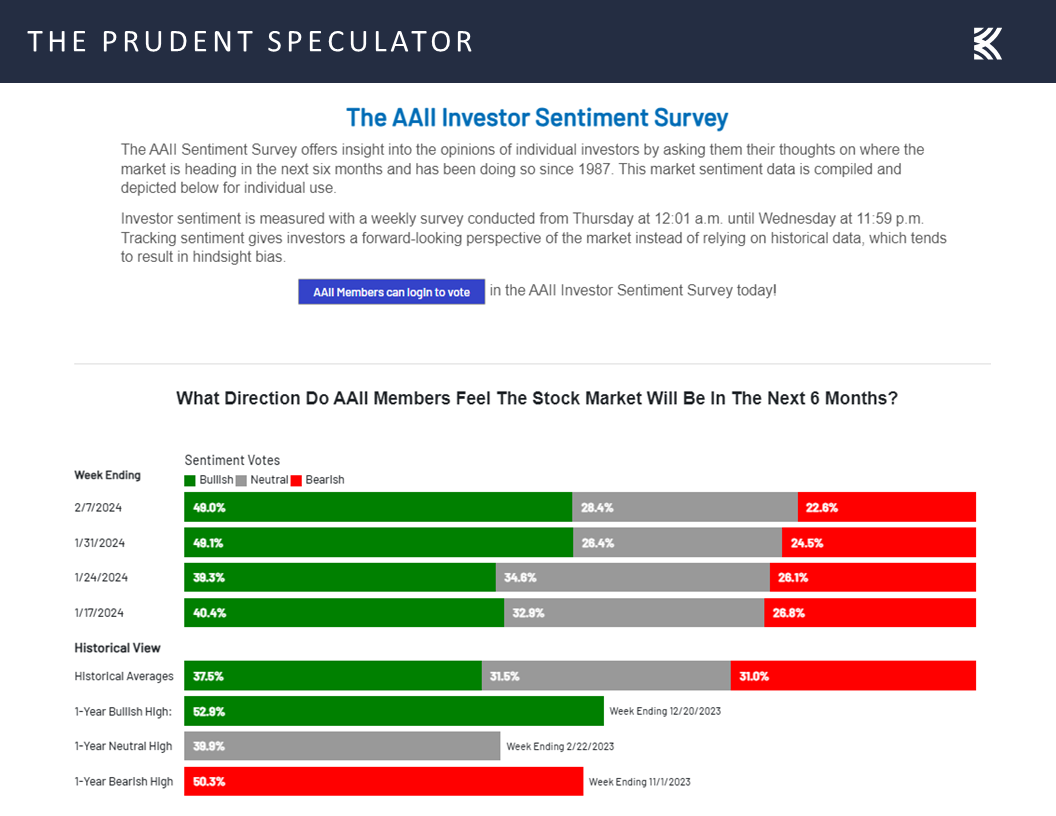

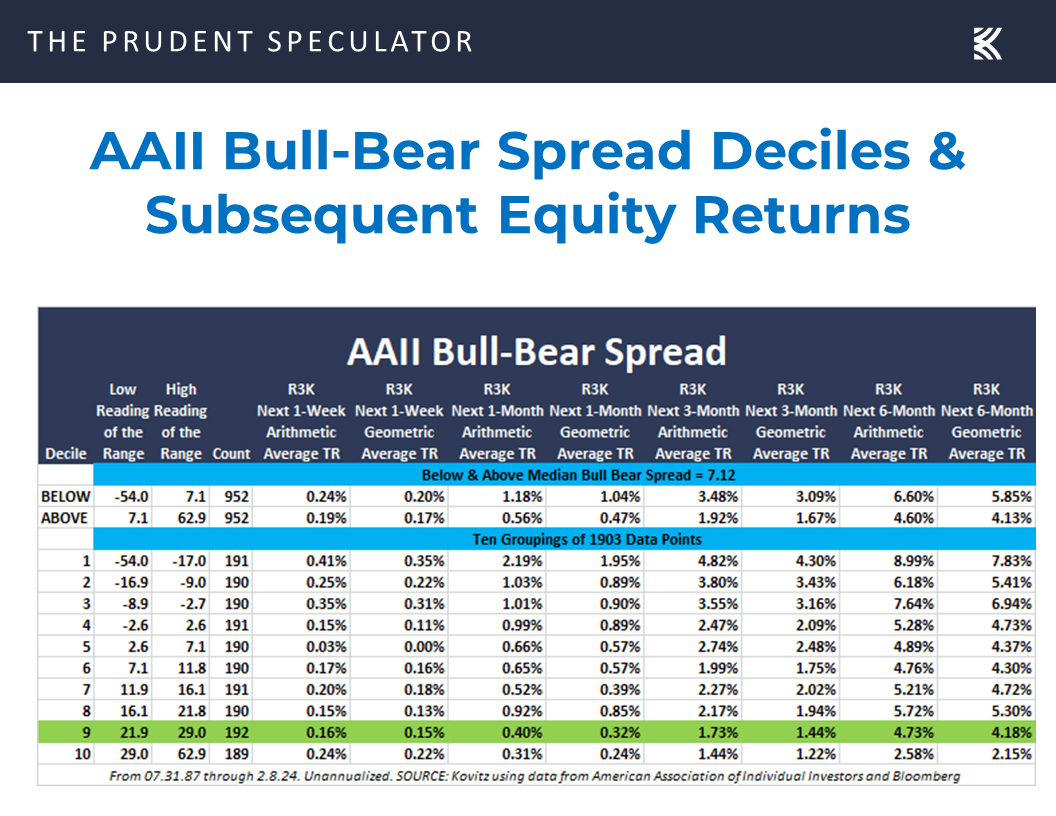

Sentiment – AAII Still Optimistic

we see no reason to alter our long-term enthusiasm, even as we realize that optimism on Main Street is running high

which might suggest that near-term returns for the mega-cap-dominated Russell 3000 index could be modestly lower than normal.

Stock News – Updates on eight stocks across five different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Inflation, Interest Rates, Valuations and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the inflation, interest rates, valuations and more news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – Partial Sale of CAT

Volatility – The Longer the Hold, the Less the Chance of Loss

Inflation – CPI & PPI Rise; Stocks Haven’t Minded Historically

Interest Rates – Target Rate for Fed Funds & 10-Year Treasury Yield Rise; Stocks are OK

Economy – Mixed Numbers; GDP & Corporate Profits Still Likely to Show Solid Growth

Valuations – Value Stocks Attractively Priced

Sentiment – AAII Still Optimistic

Stock News – Updates on eight stocks across five different sectors

Volatility – The Longer the Hold, the Less the Chance of Loss

Nearly a century of market history illustrates that simply lengthening the measuring stick reduces the odds of loss,

and last week demonstrated that markets can be placid with little in the way of volatility when evaluated on a one-week basis. Indeed, the Dow Jones Industrial Average closed the 5 trading days near where it began,

although there was a nasty one-day plunge on Tuesday that was one of the 400 or so worst since the launch of the Russell 3000 Value index in 1995.

Inflation – CPI & PPI Rise; Stocks Haven’t Minded Historically

Interestingly, despite plenty of evidence that that suggests stocks do not mind a Federal Reserve fight against inflation,

with Value performing fine, on average, whether the Consumer Price Index (CPI) is rising or falling,

traders suffered temporary indigestion when both the full CPI,

and the core rate (excludes volatile food and energy prices) came in above expectations in January.

It was a similar story for inflation at the wholesale level as the Producer Price Index for January released on Friday also was hotter than estimated, even as the 0.9% year-over-year advance was well below the long-term average.

Interest Rates – Target Rate for Fed Funds & 10-Year Treasury Yield Rise; Stocks are OK

Still, bettors in the Fed Funds futures market decided that Jerome H. Powell & Co. would not likely begin to reduce the benchmark lending rate until the June FOMC Meeting versus May the week prior. Further, the odds now suggest that there is likely to be no more than 4 quarter-point rate cuts this year,

with the current guess of a 4.43% year-end Fed Funds rate now closer to the 4.6% projection the Federal Reserve Board members and Federal Reserve Bank Presidents offered back in December.

Of course, despite what supposed market gurus and talking heads on financial television might argue, history shows that stocks have performed fine, on average, whether the Fed Funds rate is moving higher or lower,

with the long-term evidence similar, on average, whether the benchmark government bond yield is rising or falling.

And for those who might question the 10-Year chart above, we submit additional overwhelming supporting evidence over the last three-and-a-half years,

though we realize that last week’s thinking that the Fed will be less accommodative prompted a jump in the yield on the 10-Year U.S. Treasury to 4.28%, up some 40 basis points from the 3.88% level at which the yield began 2024.

Economy – Mixed Numbers; GDP & Corporate Profits Still Likely to Show Solid Growth

Obviously, interest rates are just one factor influencing stock price gyrations. More important is the health of the U.S. economy, with data mixed last week. While weather deserved some of the blame, retail sales retreated a worse-than-expected 0.8% last month,

housing starts for January came in below estimates,

and Small Business Optimism pulled back.

On the other hand, readings on the outlook for East Coast factory activity improved to better-than-estimated tallies for February,

initial filings for unemployment benefits declined in the latest week,

and optimism on Main Street increased this month.

Roll up all the data and the latest forecast from the Atlanta Fed for real (inflation-adjusted) Q1 GDP growth stood at a solid 2.9%,

even as the tabulation by Bloomberg of the chance of recession in the next 12 months remained at 45%.

We do not lose sleep fretting about recession as their beginnings and endings are impossible to predict AND the gains on Value stocks coming out of them have been sensational, on average,

while the long-term trend is higher in terms of GDP,

as has been the case for corporate profits, which were solid in Q4 and which are likely to continue to grow this year, just as they have throughout history.

Valuations – Value Stocks Attractively Priced

So, with valuations remaining reasonable for Value stocks in general,

and our broadly diversified portfolios of undervalued stocks in particular,

Sentiment – AAII Still Optimistic

we see no reason to alter our long-term enthusiasm, even as we realize that optimism on Main Street is running high

which might suggest that near-term returns for the mega-cap-dominated Russell 3000 index could be modestly lower than normal.

Stock News – Updates on eight stocks across five different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.