The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Reddit, FOMC Meeting, Economics, Sentiment and more stock news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Newsletter Trades – One Transaction for 1 Portfolio

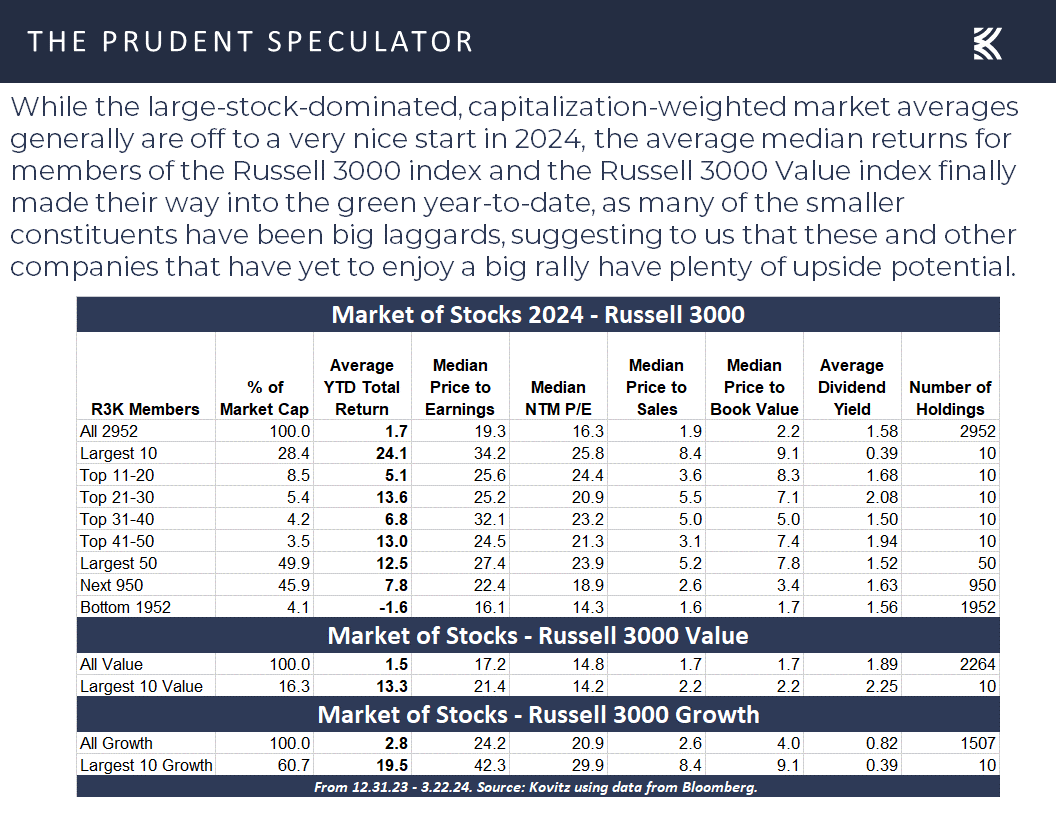

Week in Review – Sizable Rally; Average Stock in the Green YTD

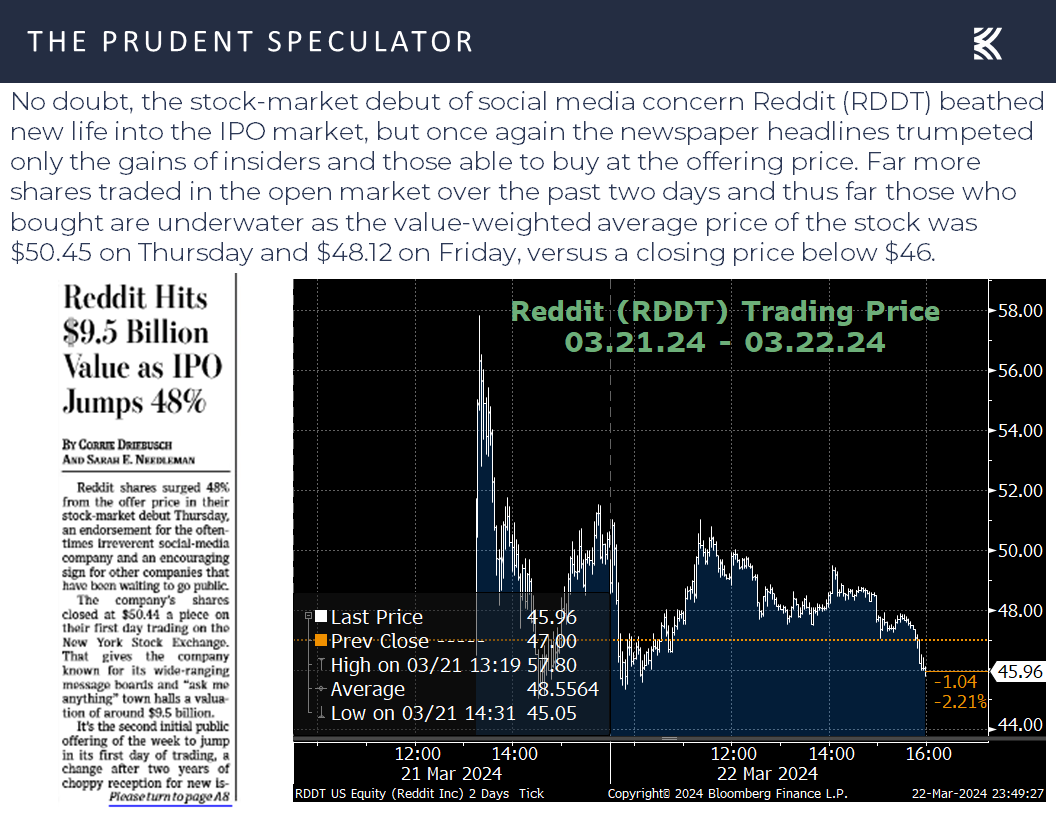

Reddit – Lots of Red for Post-IPO Buyers

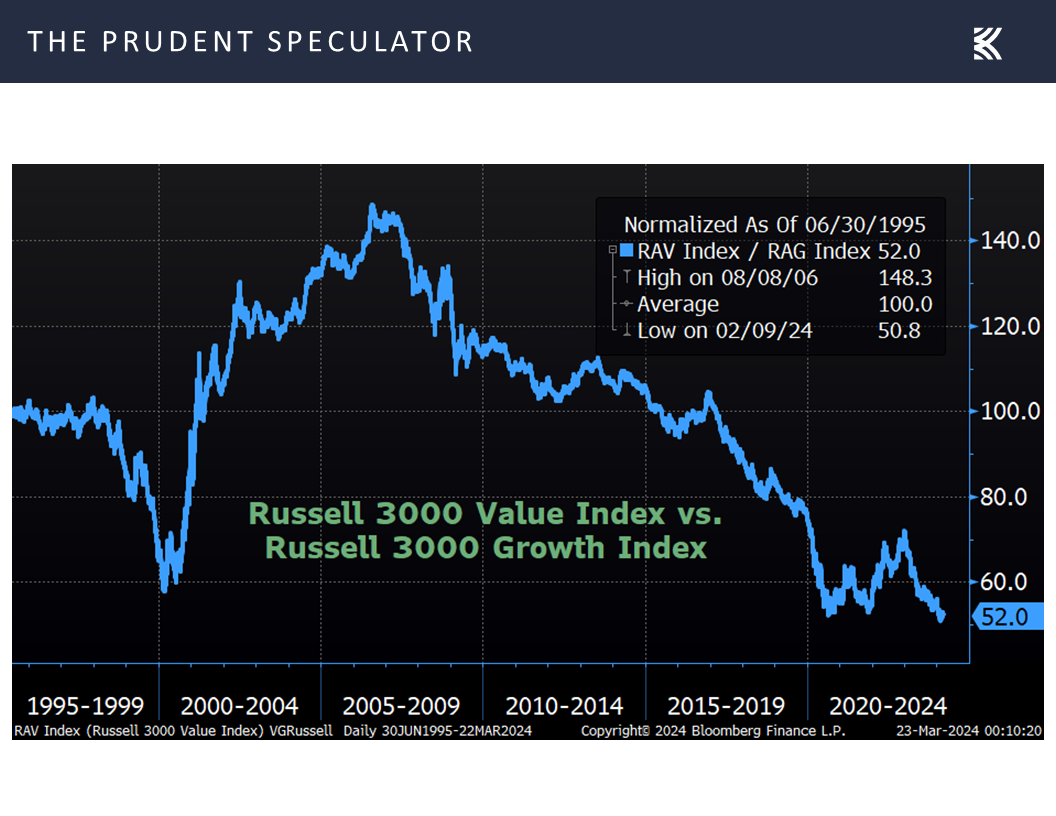

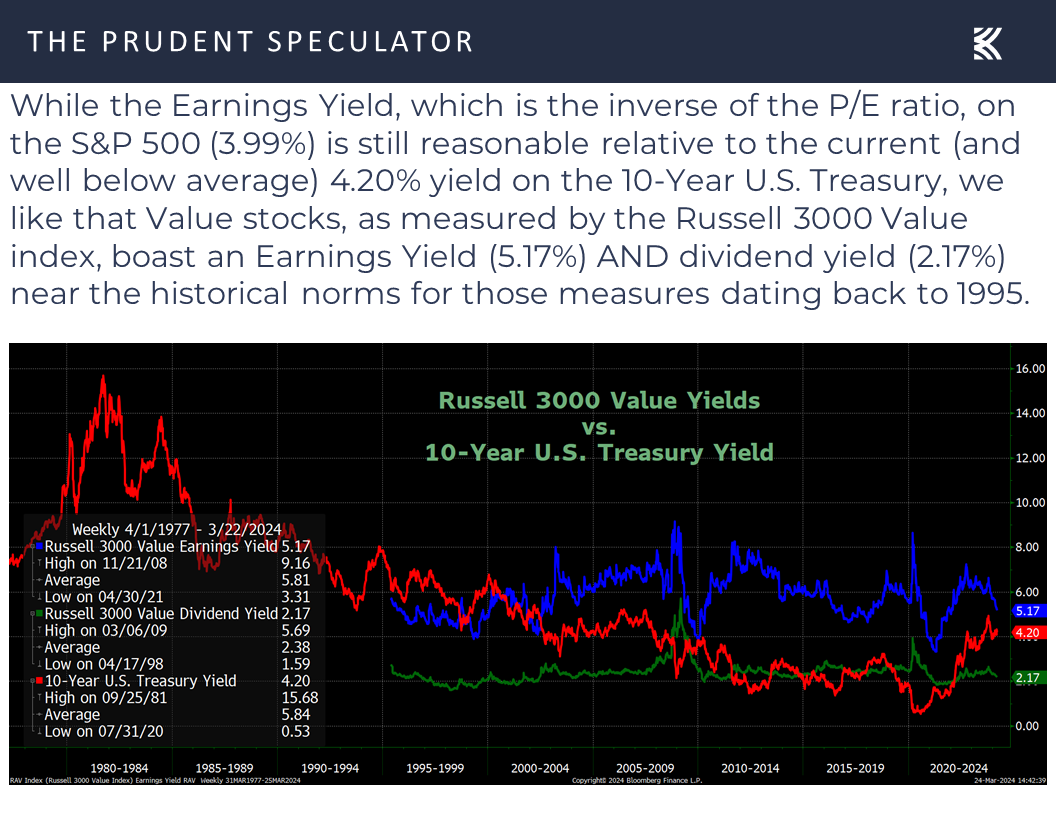

Valuations – Value Stocks Attractively Priced

FOMC Meeting – Soft Landing & Rate Cuts Expected

Econ News – Better-than-Expected Numbers

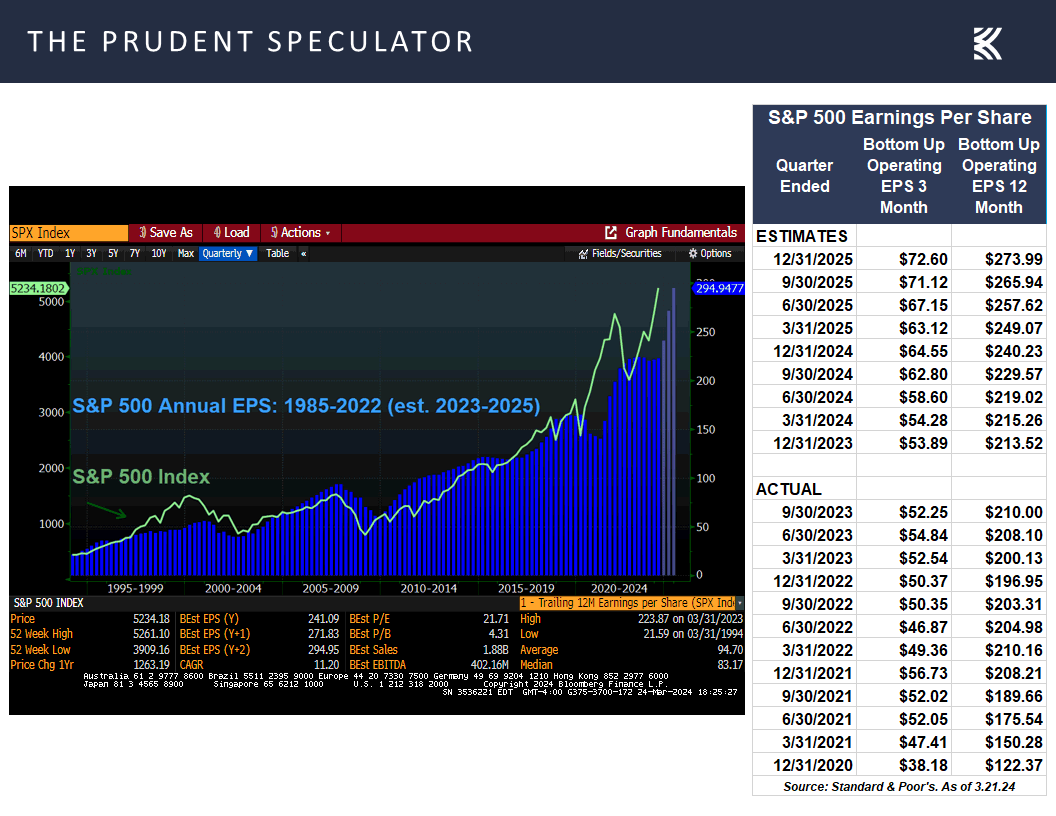

EPS – Solid Growth Projected in ’24 and ’25

Sentiment – Optimism Pulls Back a Bit

Stock News – Updates on AAPL, MU, INTC, JWN, SIEGY, IP, BHE & FDX

Week in Review – Sizable Rally; Average Stock in the Green YTD

Resisting the temptation to complain about Friday’s modest pullback, it was a terrific five days of equity trading for those of us who are long. Indeed, a handsome advance on the week finally moved the average total return for Russell 3000 constituents into the green on the year as the Russell 2000 index has been a laggard with that capitalization-weighted small-cap stock benchmark up just 2.5% thus far in 2024.

Reddit – Lots of Red for Post-IPO Buyers

True, one of your Editor’s biggest pet peeves popped up again last week when the financial press trumpeted the successful IPO of social-media-company Reddit, even as nearly everyone who bought post-IPO, where far more shares have changed hands, was underwater at Friday’s close.

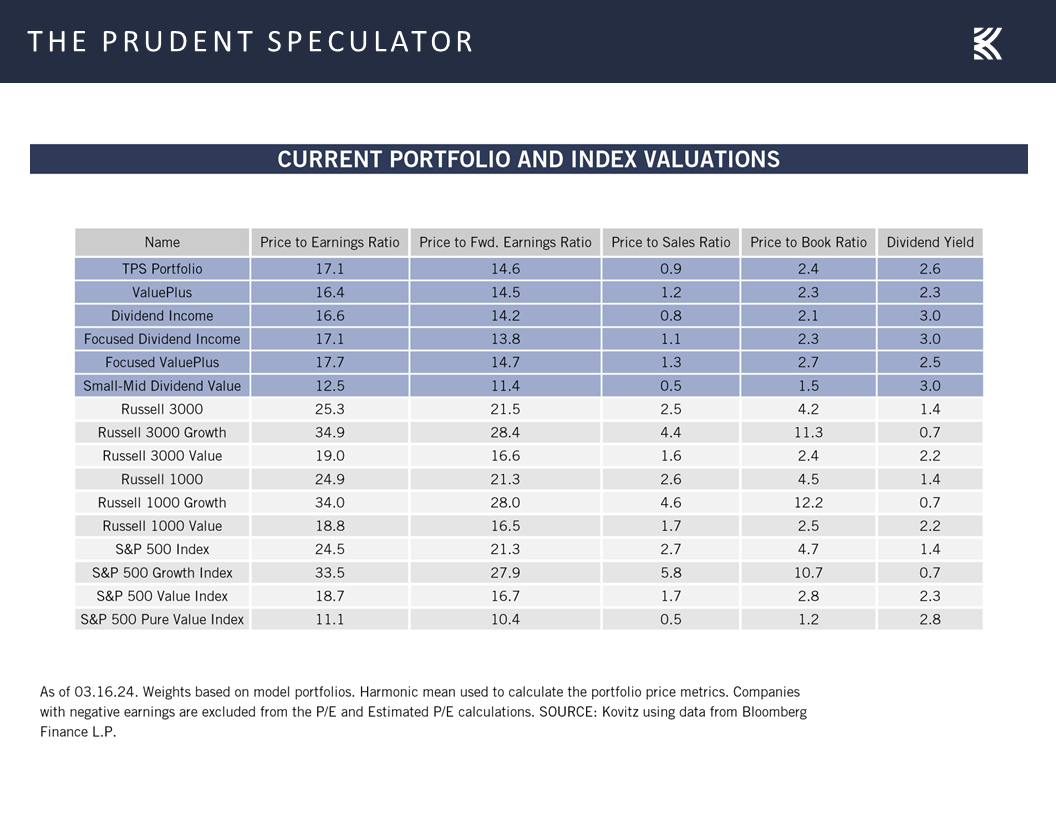

Valuations – Value Stocks Attractively Priced

However, we are not unhappy to see market breadth broadening beyond a handful of mega-cap names, especially as we think many Value stocks, like some of those that we have long championed, are attractively priced relative to Growth stocks

and the benchmark Value index is still inexpensive when considering the current interest rate environment,

…while we remain enthused about the valuation metrics associated with our broadly diversified portfolios of what we believe are undervalued stocks.

FOMC Meeting – Soft Landing & Rate Cuts Expected

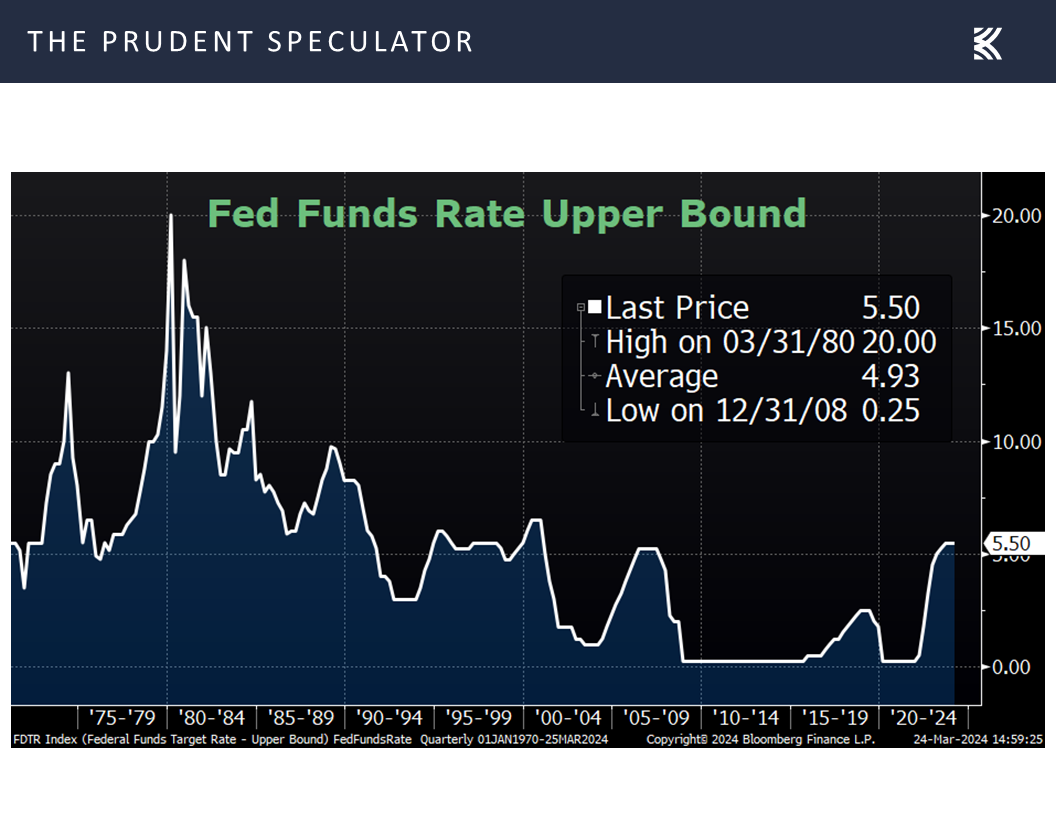

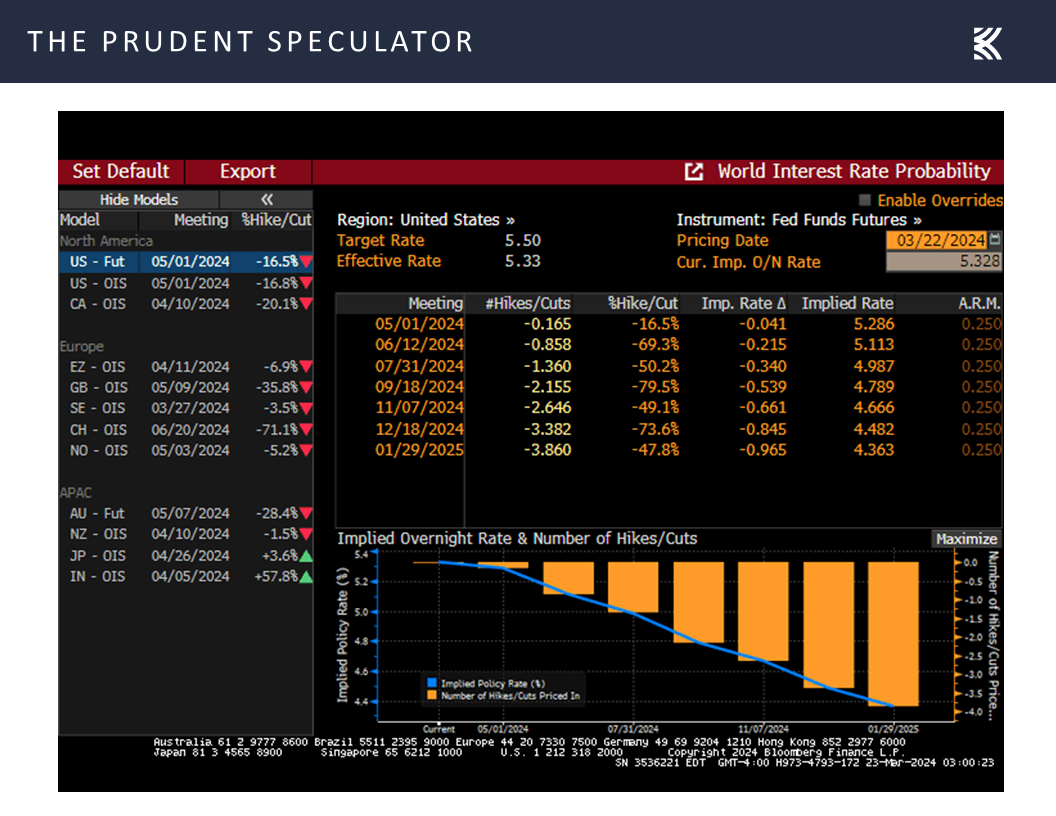

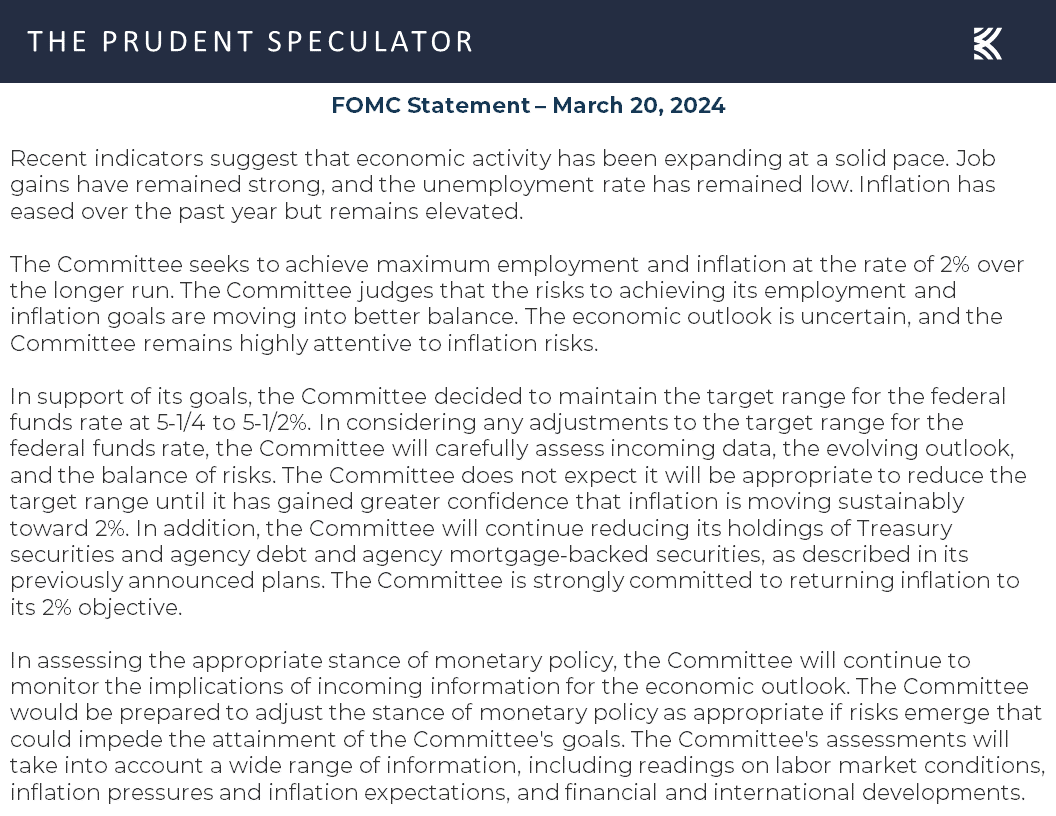

Interestingly, the catalyst for the move higher in stocks last week was the Federal Open Market Committee’s decision to leave its target for the Fed Funds rate unchanged at a range of 5.25% to 5.50%,

with the FOMC Statement indicating, “Inflation has eased over the past year but remains elevated,” and “The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2%.”

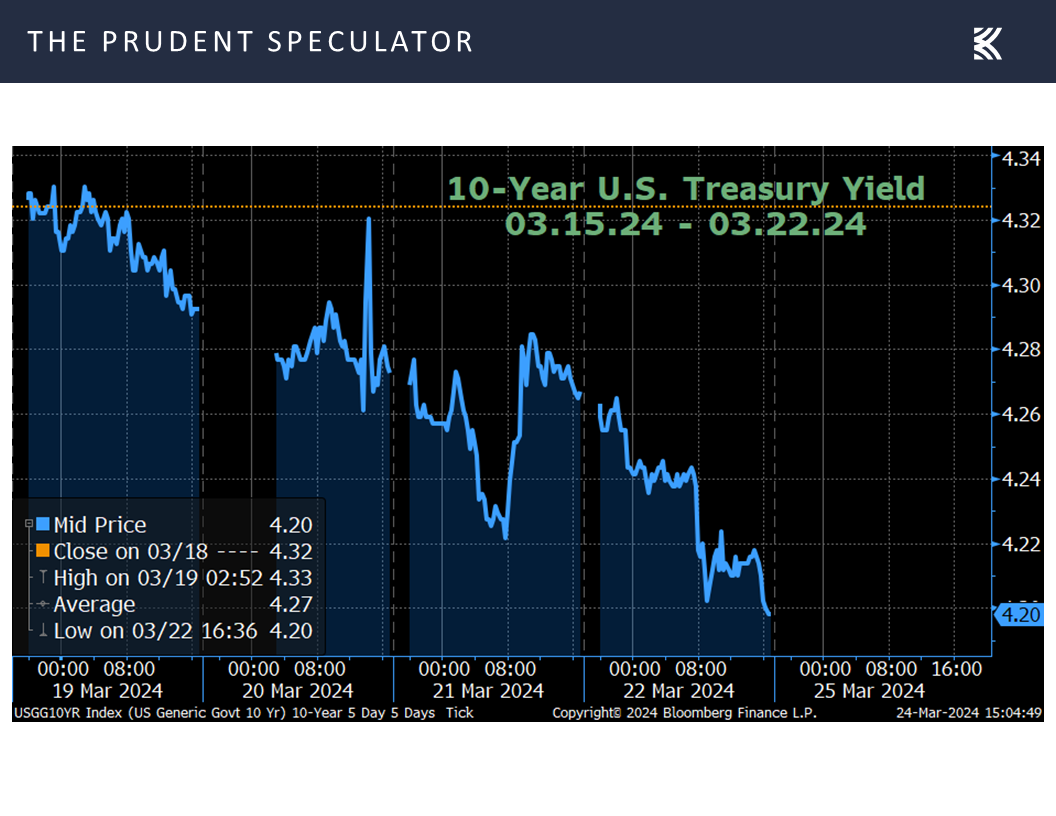

Nonetheless, the bond market liked what it heard, with the 10-Year U.S. Treasury jumping in price and dipping in yield,

and the betting in the futures market continuing to target a year-end Fed Funds rate (4.48%) well below current levels,

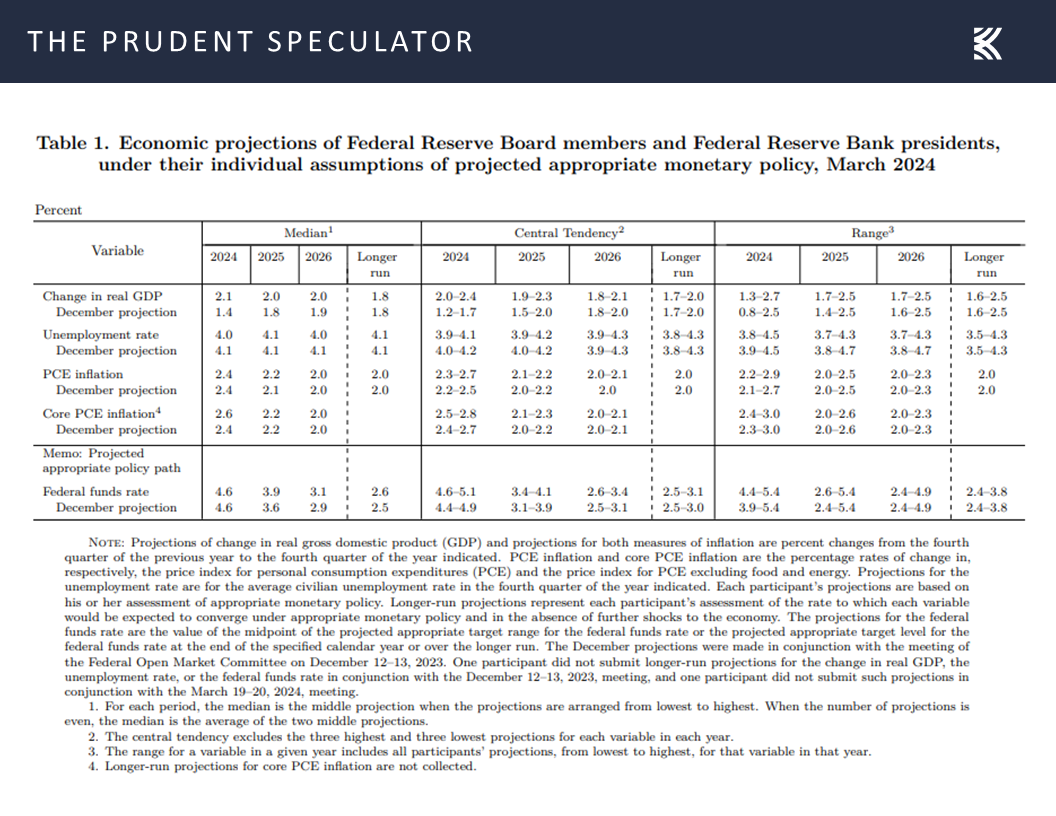

and close to the latest consensus projection of 4.6% offered by Federal Reserve Board members and Federal Reserve Bank presidents.

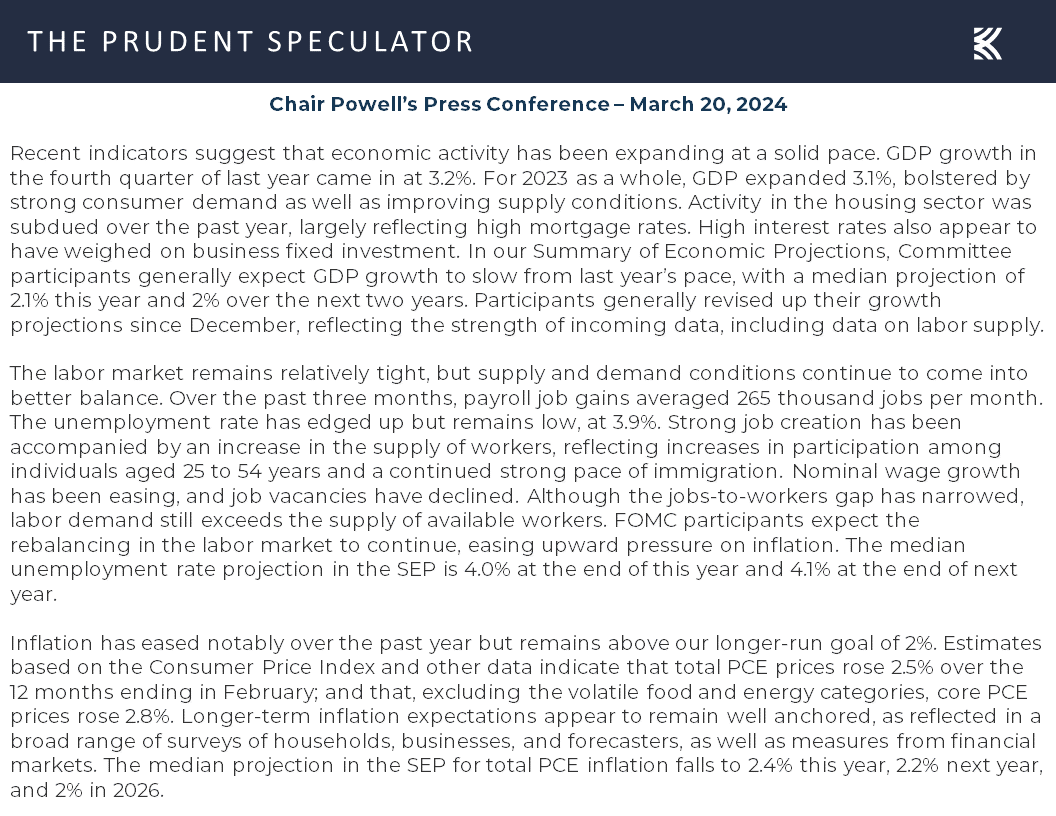

Given that those projections also offered a bump in the 2024 estimate for GDP growth to 2.1%, up from 1.4% three months ago, with modestly higher Core PCE inflation of 2.6%, above the prior forecast 2.4%, traders seemingly remained of the belief that a so-called soft landing is in the cards for the U.S. economy. Fed Chair Jerome H. Powell did nothing to dispel that notion at the Press Conference that followed the decision on interest rates,

Econ News – Better-than-Expected Numbers

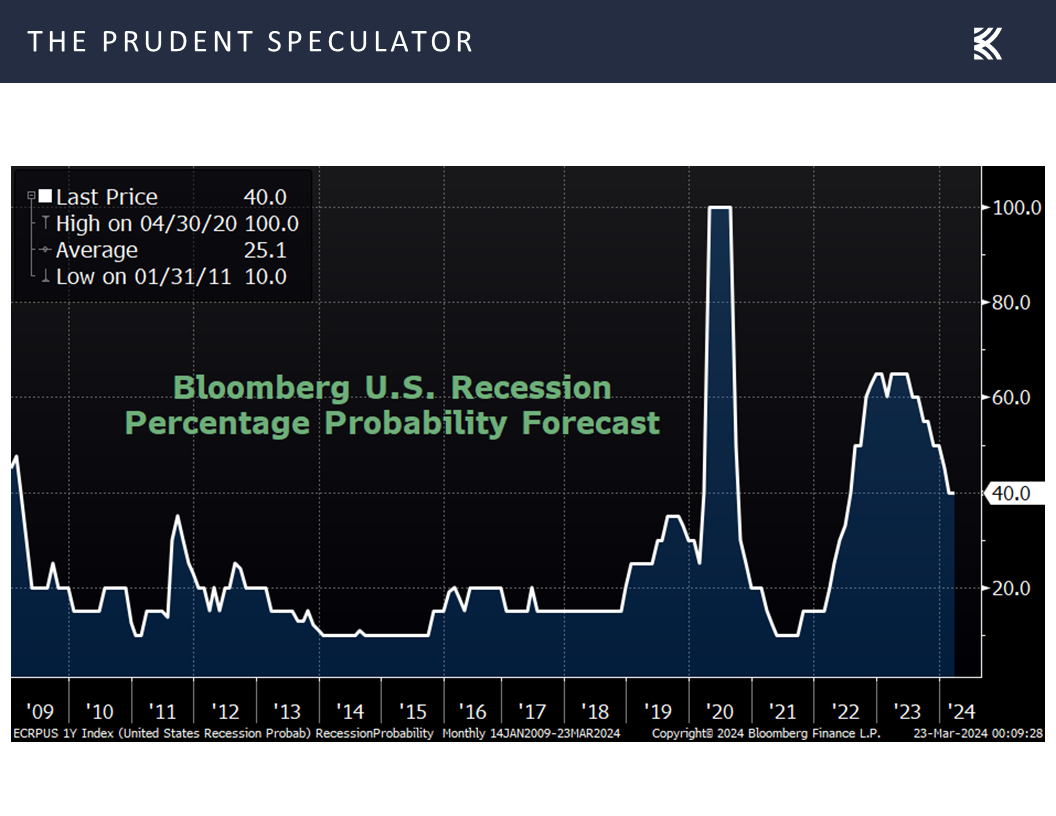

while the latest batch of economic numbers suggested that the current odds of recession, which stand at 40% per tabulations from Bloomberg, might be too high.

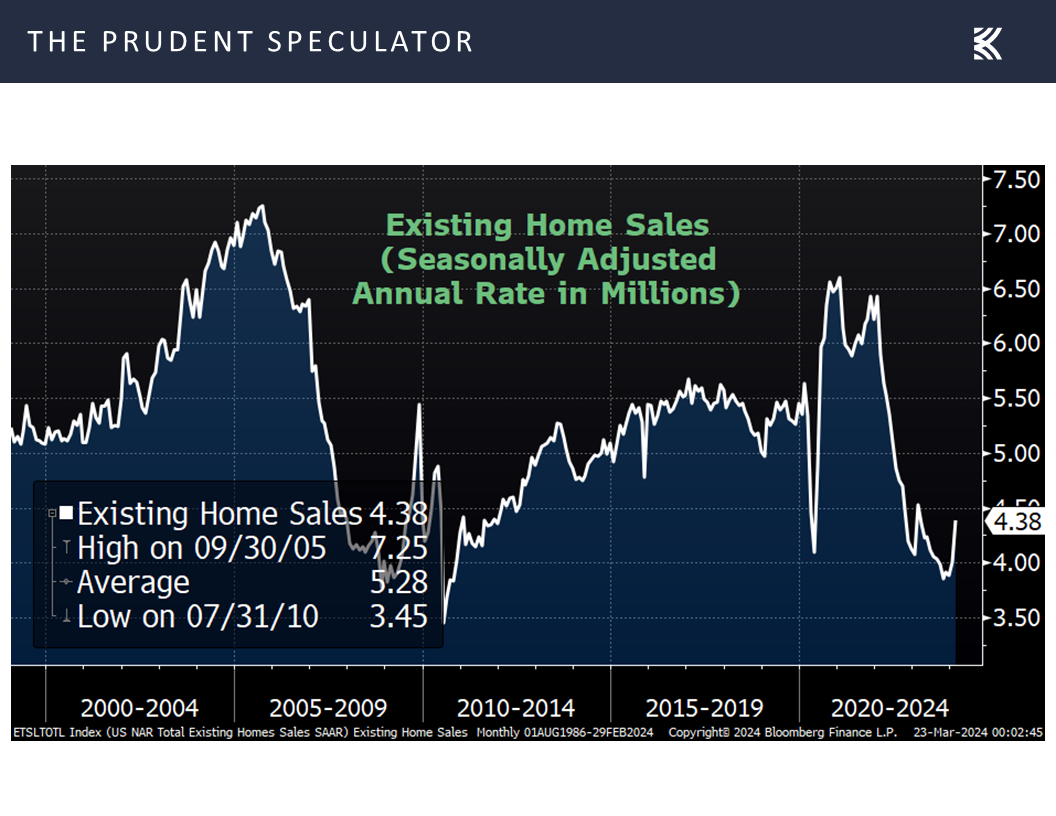

Whether it was existing home sales for February coming in at an annual rate of 1.521 million, vs. 1.374 million the month prior and estimates of 1.440 million,

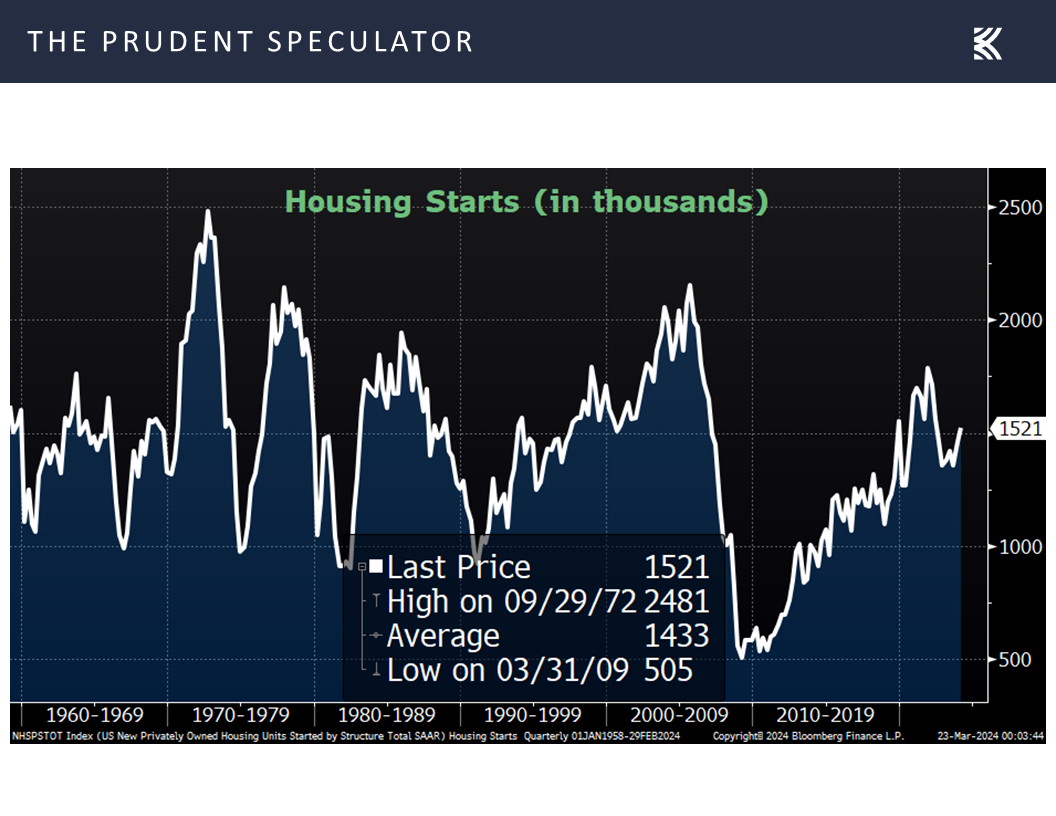

housing starts last month jumping 10.7%, versus estimates of an 8.2% advance,

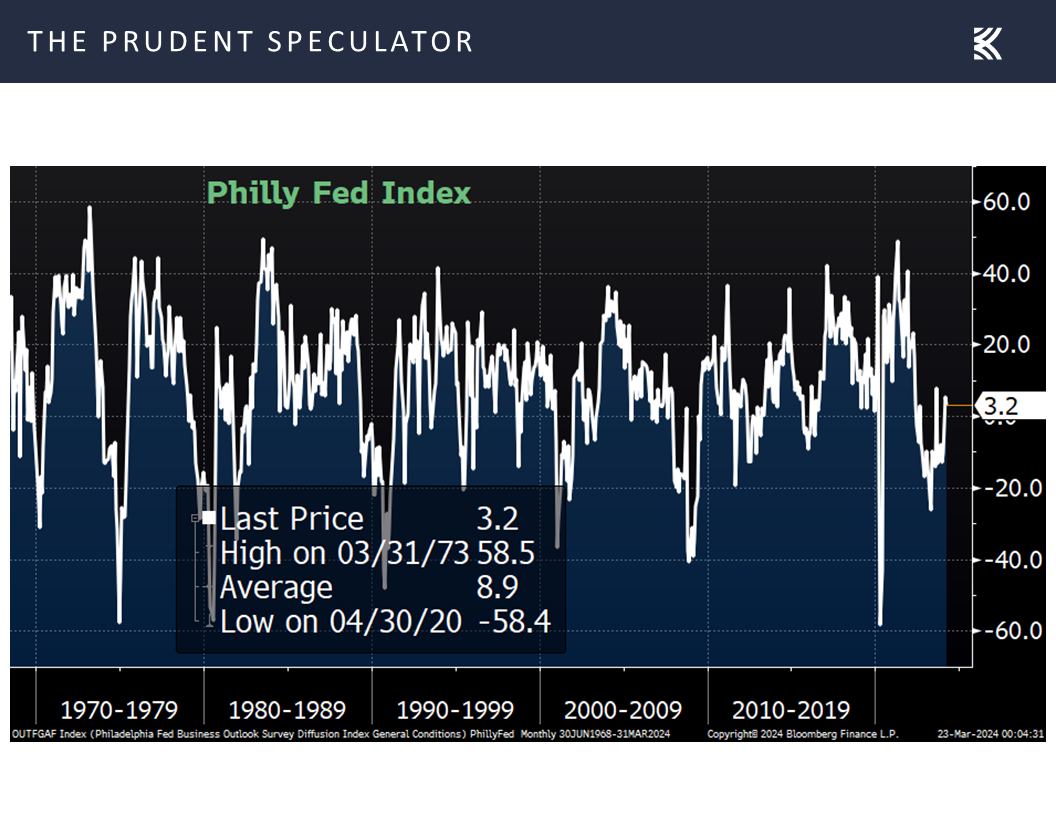

the Philadelphia Fed’s gauge of East Coast manufacturing activity for March coming at in 3.2 vs. a -2.5 estimate,

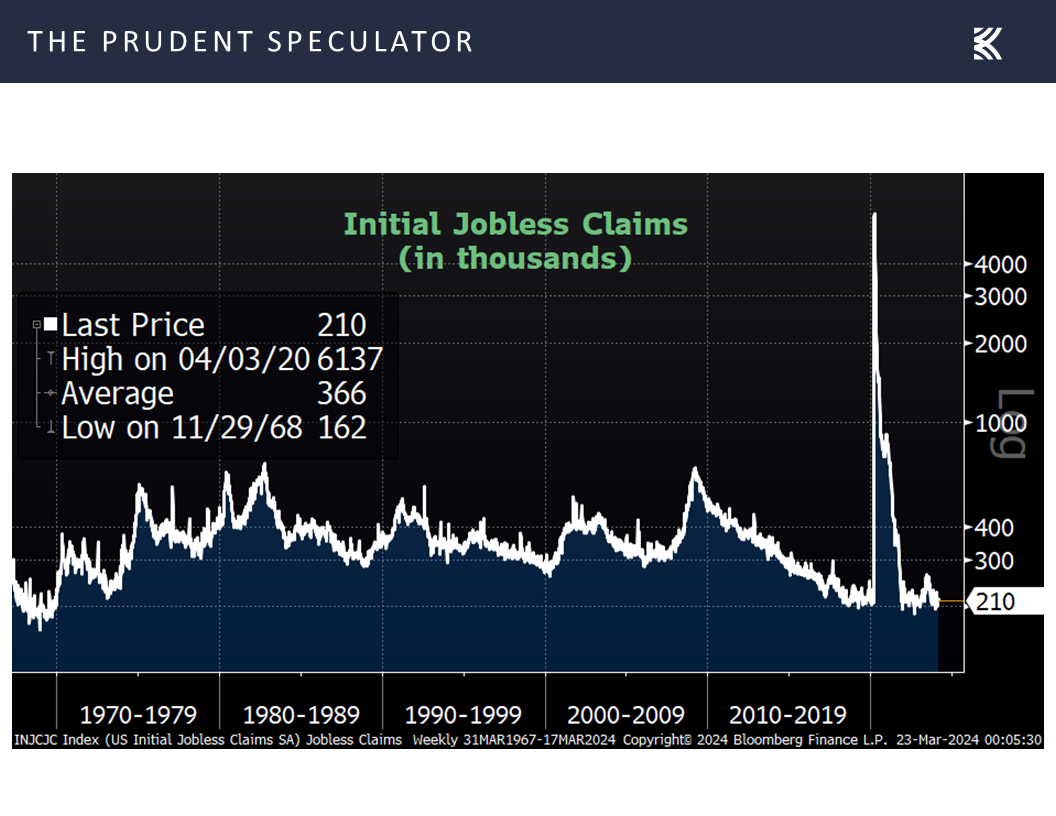

first-time filings for unemployment benefits holding steady in the latest week at 210,000,

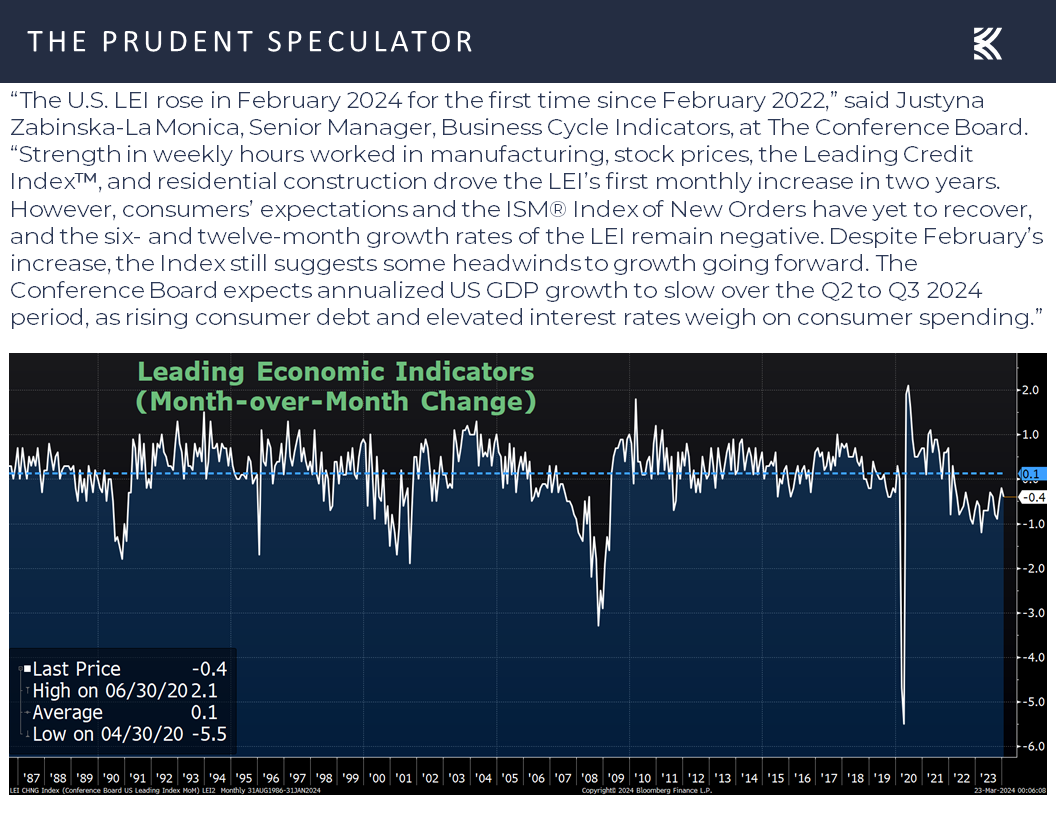

or the Leading Economic Indicators in February topping expectations,

solid U.S. economic growth remains likely,

EPS – Solid Growth Projected in ’24 and ’25

which should support a continued expansion of corporate profits.

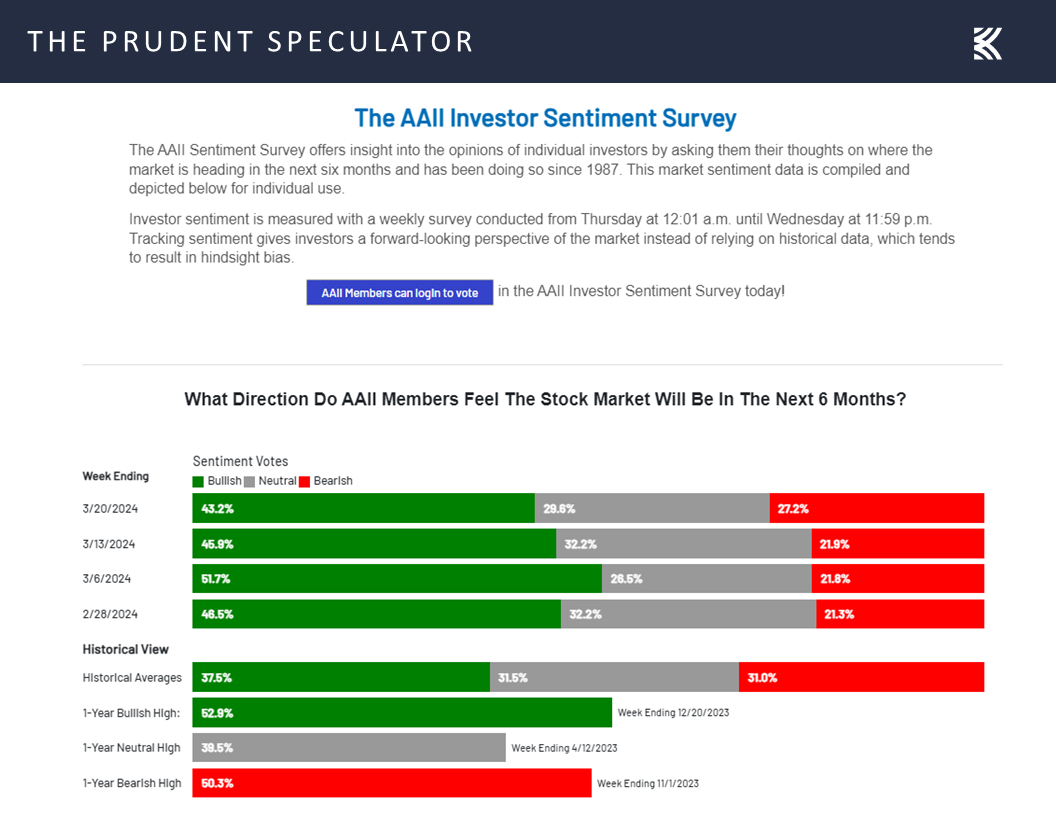

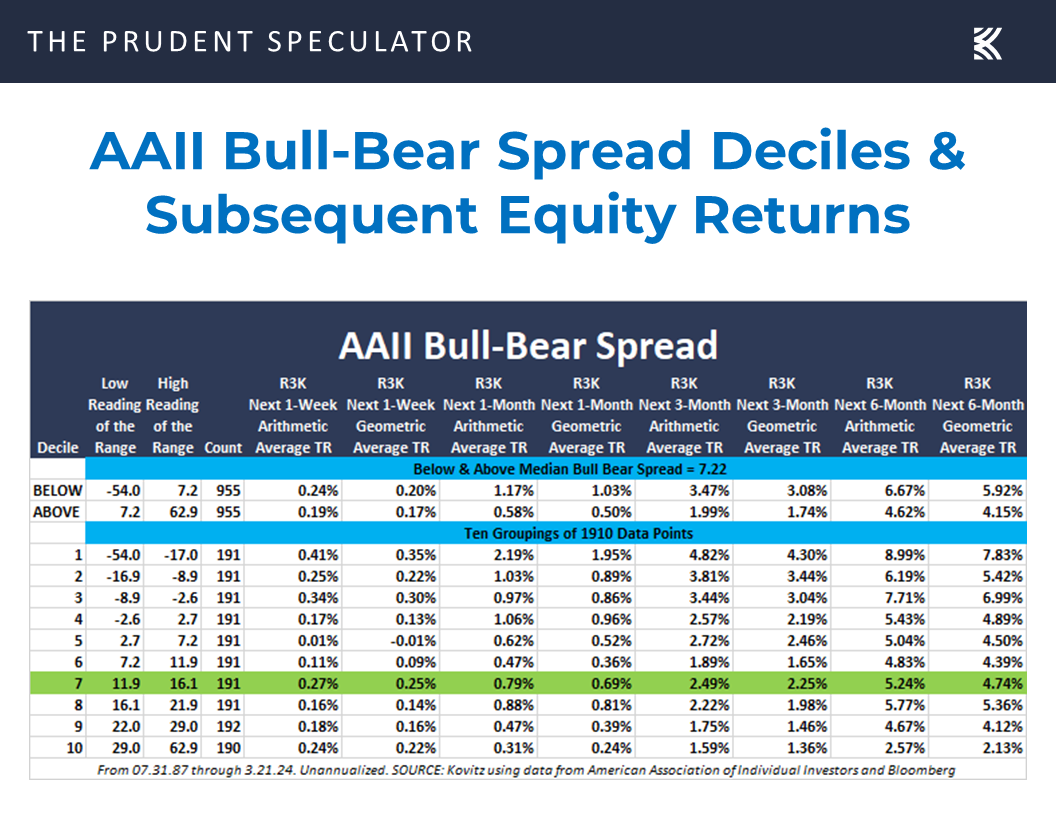

Sentiment – Optimism Pulls Back a Bit

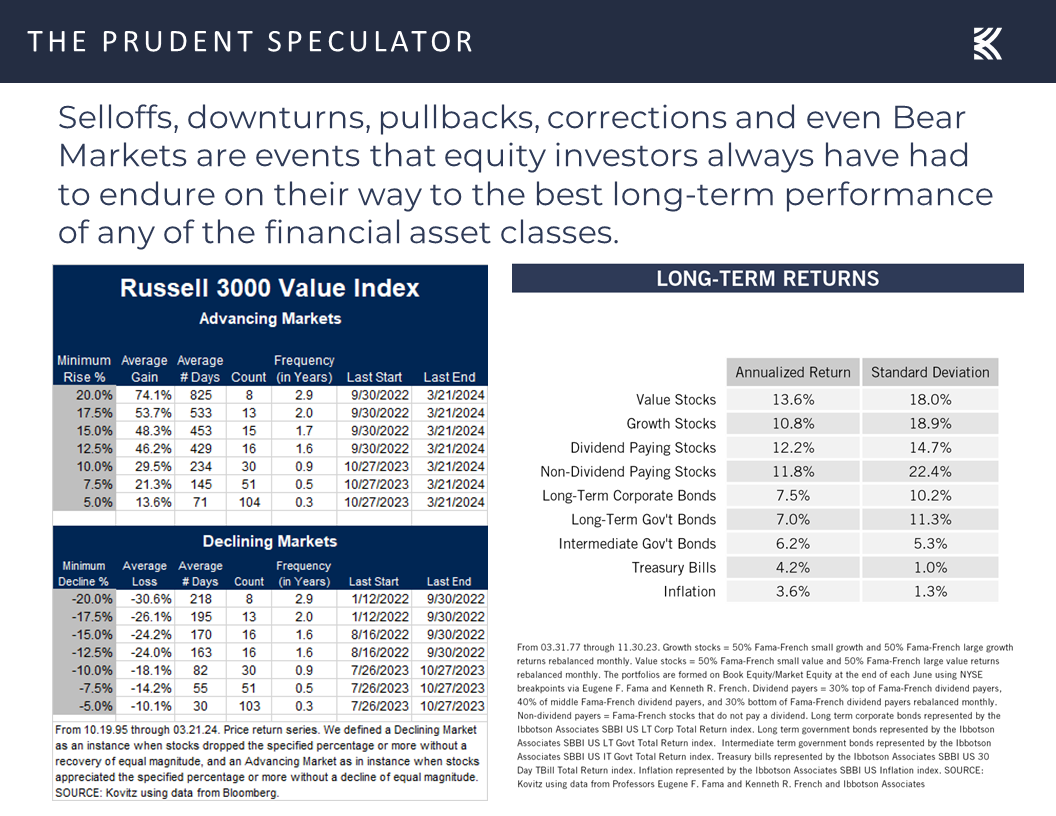

Certainly, we understand that downturns, corrections and even Bear Markets are always part of the investment equation, so we constantly are braced for downside volatility, but we continue to believe that time in the market trumps market timing,

…and we were not unhappy to see enthusiasm for stocks on Main Street pull back a bit last week with the American Association of Individual Investors Sentiment Survey showing a drop of 2.7 percentage points in the number of Bulls and a 5.3 percentage-point rise in the tally of Bears,

even as 37 years of market history supports sticking with stocks no matter the read on this contrarian indicator.

Stock News – Updates on eleven stocks across seven different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Reddit, FOMC Meeting, Sentiment and more Stock News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Reddit, FOMC Meeting, Economics, Sentiment and more stock news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Newsletter Trades – One Transaction for 1 Portfolio

Week in Review – Sizable Rally; Average Stock in the Green YTD

Reddit – Lots of Red for Post-IPO Buyers

Valuations – Value Stocks Attractively Priced

FOMC Meeting – Soft Landing & Rate Cuts Expected

Econ News – Better-than-Expected Numbers

EPS – Solid Growth Projected in ’24 and ’25

Sentiment – Optimism Pulls Back a Bit

Stock News – Updates on AAPL, MU, INTC, JWN, SIEGY, IP, BHE & FDX

Week in Review – Sizable Rally; Average Stock in the Green YTD

Resisting the temptation to complain about Friday’s modest pullback, it was a terrific five days of equity trading for those of us who are long. Indeed, a handsome advance on the week finally moved the average total return for Russell 3000 constituents into the green on the year as the Russell 2000 index has been a laggard with that capitalization-weighted small-cap stock benchmark up just 2.5% thus far in 2024.

Reddit – Lots of Red for Post-IPO Buyers

True, one of your Editor’s biggest pet peeves popped up again last week when the financial press trumpeted the successful IPO of social-media-company Reddit, even as nearly everyone who bought post-IPO, where far more shares have changed hands, was underwater at Friday’s close.

Valuations – Value Stocks Attractively Priced

However, we are not unhappy to see market breadth broadening beyond a handful of mega-cap names, especially as we think many Value stocks, like some of those that we have long championed, are attractively priced relative to Growth stocks

and the benchmark Value index is still inexpensive when considering the current interest rate environment,

…while we remain enthused about the valuation metrics associated with our broadly diversified portfolios of what we believe are undervalued stocks.

FOMC Meeting – Soft Landing & Rate Cuts Expected

Interestingly, the catalyst for the move higher in stocks last week was the Federal Open Market Committee’s decision to leave its target for the Fed Funds rate unchanged at a range of 5.25% to 5.50%,

with the FOMC Statement indicating, “Inflation has eased over the past year but remains elevated,” and “The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2%.”

Nonetheless, the bond market liked what it heard, with the 10-Year U.S. Treasury jumping in price and dipping in yield,

and the betting in the futures market continuing to target a year-end Fed Funds rate (4.48%) well below current levels,

and close to the latest consensus projection of 4.6% offered by Federal Reserve Board members and Federal Reserve Bank presidents.

Given that those projections also offered a bump in the 2024 estimate for GDP growth to 2.1%, up from 1.4% three months ago, with modestly higher Core PCE inflation of 2.6%, above the prior forecast 2.4%, traders seemingly remained of the belief that a so-called soft landing is in the cards for the U.S. economy. Fed Chair Jerome H. Powell did nothing to dispel that notion at the Press Conference that followed the decision on interest rates,

Econ News – Better-than-Expected Numbers

while the latest batch of economic numbers suggested that the current odds of recession, which stand at 40% per tabulations from Bloomberg, might be too high.

Whether it was existing home sales for February coming in at an annual rate of 1.521 million, vs. 1.374 million the month prior and estimates of 1.440 million,

housing starts last month jumping 10.7%, versus estimates of an 8.2% advance,

the Philadelphia Fed’s gauge of East Coast manufacturing activity for March coming at in 3.2 vs. a -2.5 estimate,

first-time filings for unemployment benefits holding steady in the latest week at 210,000,

or the Leading Economic Indicators in February topping expectations,

solid U.S. economic growth remains likely,

EPS – Solid Growth Projected in ’24 and ’25

which should support a continued expansion of corporate profits.

Sentiment – Optimism Pulls Back a Bit

Certainly, we understand that downturns, corrections and even Bear Markets are always part of the investment equation, so we constantly are braced for downside volatility, but we continue to believe that time in the market trumps market timing,

…and we were not unhappy to see enthusiasm for stocks on Main Street pull back a bit last week with the American Association of Individual Investors Sentiment Survey showing a drop of 2.7 percentage points in the number of Bulls and a 5.3 percentage-point rise in the tally of Bears,

even as 37 years of market history supports sticking with stocks no matter the read on this contrarian indicator.

Stock News – Updates on eleven stocks across seven different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.